Embed Size (px)

Citation preview

XBRL In the Classroom

The Time is Now

Presented by Neal Hannon

What is the business problem ?

Is XBRL right for the classroom today ?

The crux of the problem is to develop a comprehensive system that is

• All inclusive and • Transparent to the user

YES IF

XBRL will soon become a dominant method of handling business reporting

Other areas of business are also moving to XML enabled information.

The Case for XML and XBRL

XML - a computer markup language that is extensible (flexible XML - a computer markup language that is extensible (flexible … can be added to)… can be added to)

XML is actually a bare-bones set of syntax rules to markup XML is actually a bare-bones set of syntax rules to markup any kind of text and dataany kind of text and data

XML is used to supply the structure of the text or dataXML is used to supply the structure of the text or data XML is used to tell both a human & computer software XML is used to tell both a human & computer software

what the text or data is … not how to display itwhat the text or data is … not how to display it

XML has become the fastest growing technology for information transportation and exchange the world of computing has ever seen.

Business Integrator Magazine says that nearly nine out of every ten enterprises claim that XML will be and important technology for their IT strategies over the next year

The Case for XBRL

The purpose of XBRL is “to enhance the flow of financial information through the creation of a globally useful language in which to describe financial facts and concepts.” David vun Kannon

XBRL is uniquely positioned to Provide mobility and transportability

to financial and business facts.

Students in AIS, Advanced Accounting,Auditing, Consolidations,

Mergers, Tax, Not-for-Profit will all be affected by XBRL

The Case for XBRL

I would like to see you take your XBRL project a step further, providing

account classifications for companies in common industries. In short, I challenge you

to turn all of this data into meaningful information for investors

Arthur Levitt, Former chair, SEC

The Case for XBRL

Students will need to collect, interpret andreport data in many different XML dialects

XBRL provides a bridge not only to financial statements, but to all business reporting.

XBRL Business Uses

The internal use of XBRL is just Beginning to be explored, broughton by XBRL for General Ledger in

public beta. New XBRL releases are compliant with the latest version

of W3C’s XML Schema

Internal Uses include:Account analysisBalanced Scorecard

Automated exception reporting

Wireless, PDACell Phone

XBRL Business Uses

External Uses include:SEC FilingsIRS and State Tax Filing

Annual Reports Creditor Reports

Wireless, PDACell Phone

Externally, XBRL focuses on theproduction of GAAP financial statements for the business financial reporting supply chain. The externalfocus of XBRL is evident by theheavy participation in XBRL.org bythe AICPA and Big 5 Accountingfirms

XBRL International

International Accounting Standards and Major Countries arechanging the way Accounting is conducted world-wide

Hot spots of development include Australia, Singapore, Germany, Japan, followed by Canada, the Netherlands, Spain, South Africa,Hong Kong, Great Britain, and theScandinavian countries.

Stig Enevoldsen

(Chairman IASC) September 1998

“The fact is that we not only speak different accounting languages but

also give different interpretations of the same events and transactions……

“I believe that the best way forward in accounting is to converge towards one

single world-wide accounting language.”

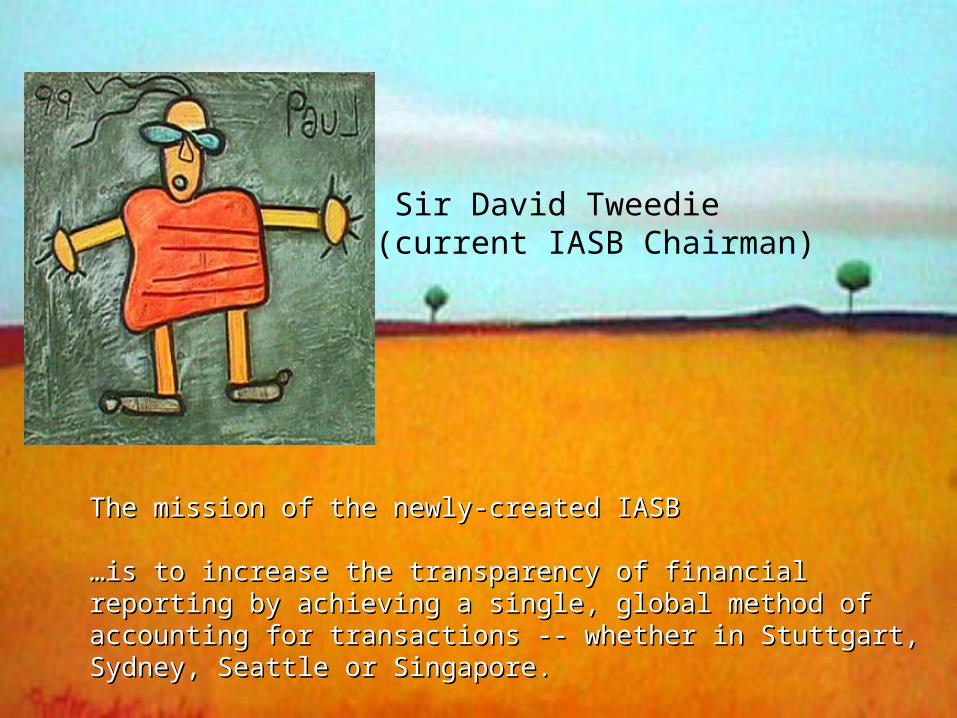

Sir David Tweedie (current IASB Chairman)

The mission of the newly-created IASB The mission of the newly-created IASB

……isis to increase the transparency of financial reporting byto increase the transparency of financial reporting by achieving a achieving a single, global method of accounting for transactions -- whether in single, global method of accounting for transactions -- whether in Stuttgart, Sydney, Seattle or Singapore.Stuttgart, Sydney, Seattle or Singapore.

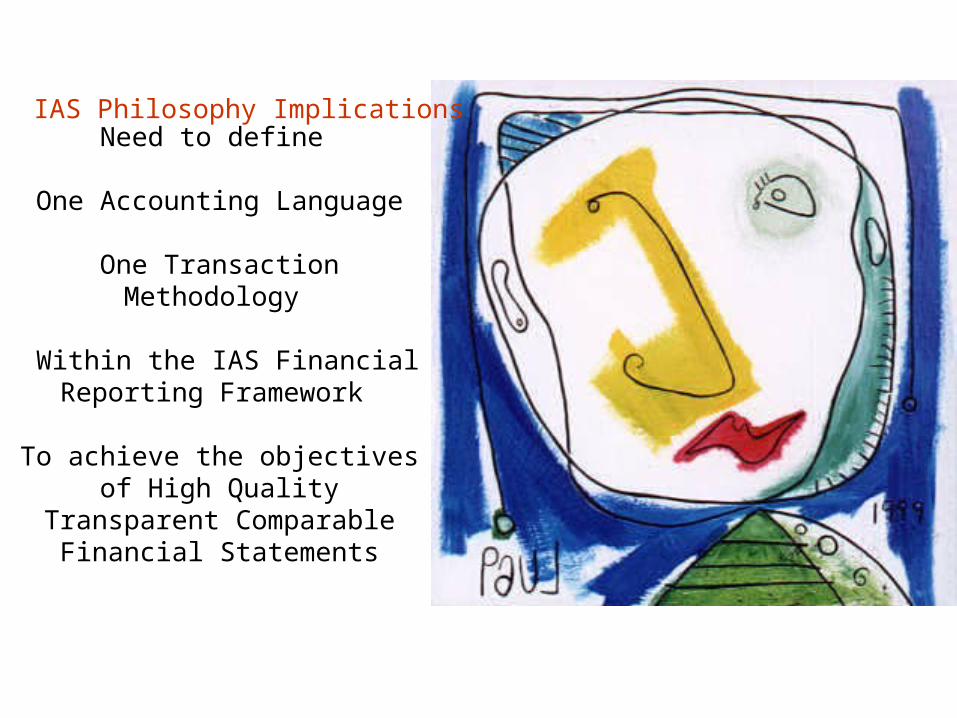

Need to define

One Accounting Language

One Transaction Methodology

Within the IAS Financial Reporting Framework

To achieve the objectives of High Quality Transparent Comparable

Financial Statements

IAS Philosophy Implications

Getting consensus / agreement

Managing Change

Implementation

Within Organizations

Between Organizations

Between Countries

Politics is a Problem

XBRL IAS can play a large part especially via the Big 5

Challenge of Change

The Vision

To produce

High quality, Transparent, Comparable,General Purpose Financial Reporting

to

International Accounting StandardsUsing one accounting languageOne transaction methodology

Which are useful for making economic decisions.

The Vision for XBRL is no different!

Just do it

Electronically

in a binary environment

With the Seamless Transfer

Of Financial Information

In a known state

Without

Human Intervention

Accounting

Specification & Design

One accounting language One transaction methodology

One presentation methodology

to define all the facts required

on an inclusive exclude basis

for a binary environment for the seamless transfer of Financial Information in a known state

without Human Intervention

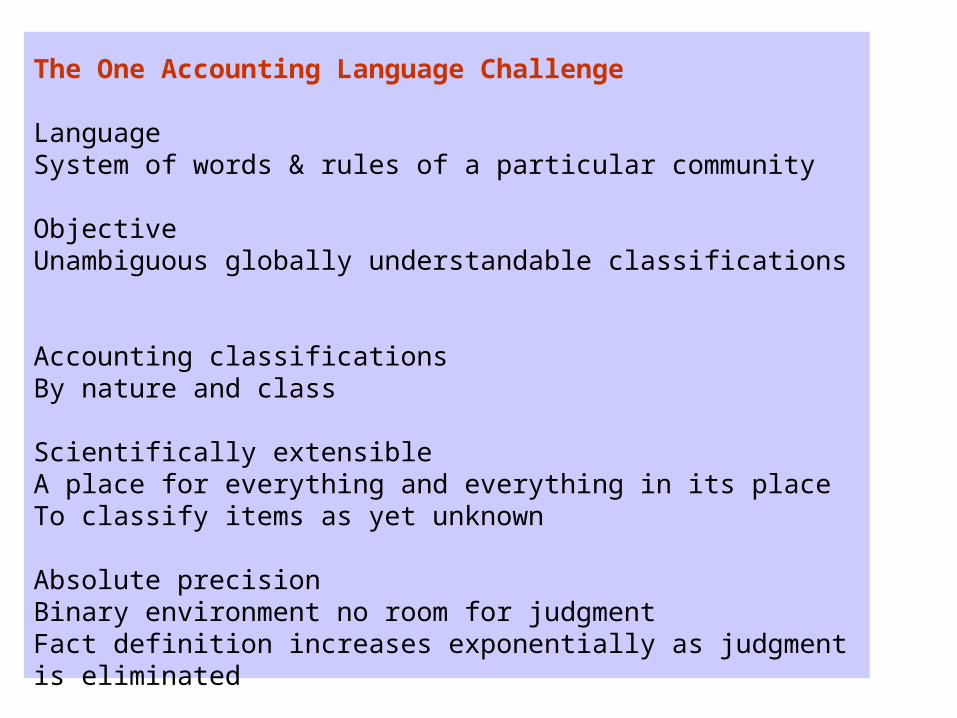

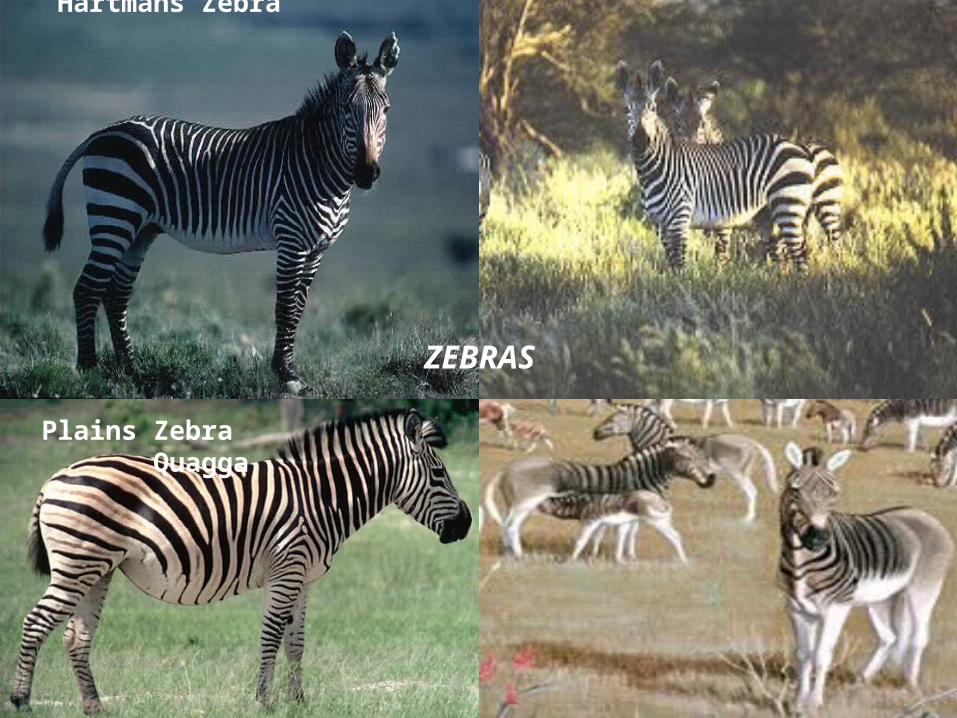

The One Accounting Language Challenge

Language System of words & rules of a particular community

ObjectiveUnambiguous globally understandable classifications

Accounting classificationsBy nature and class

Scientifically extensibleA place for everything and everything in its placeTo classify items as yet unknown

Absolute precisionBinary environment no room for judgmentFact definition increases exponentially as judgment is eliminated

Mountain Zebra Hartmans Zebra

ZEBRAS

Plains Zebra Quagga

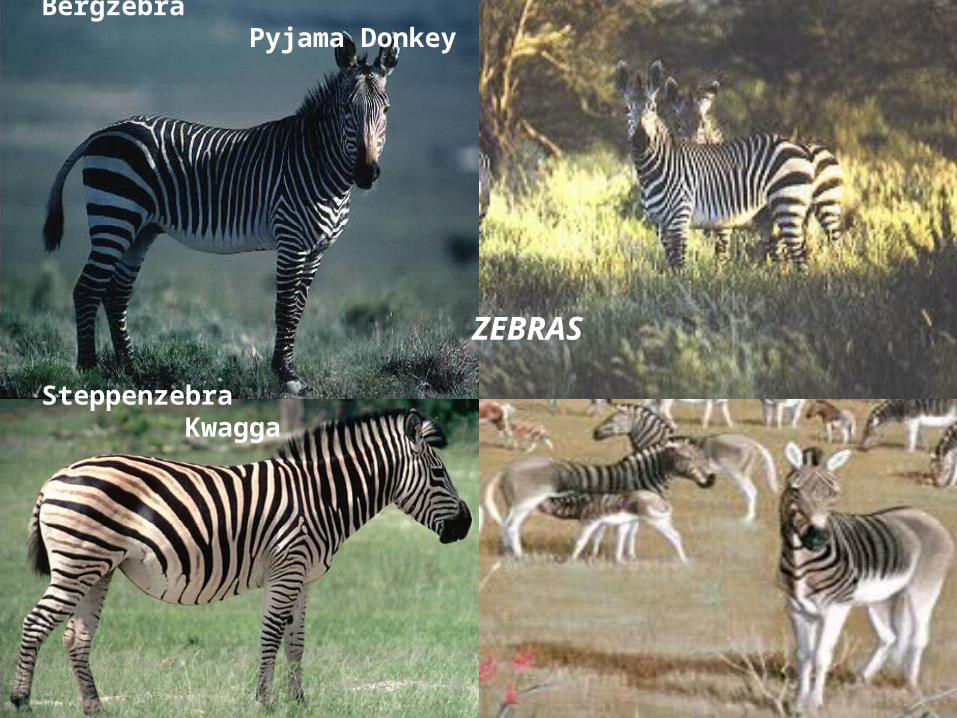

Bergzebra Pyjama Donkey

ZEBRAS

Steppenzebra Kwagga

Zebra

(Equus Zebra Zebra) (Equus Zebra Hartmannae )

(Equus Quagga) (Equus Quagga Quagga)

Grevy’s Zebra

(Equus Grevyi )

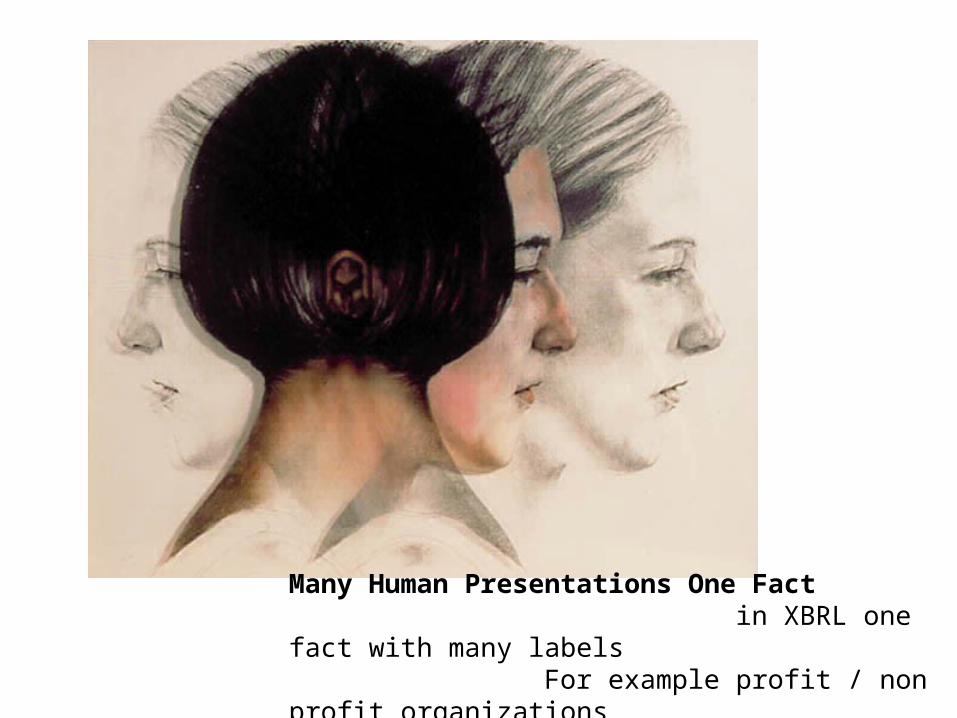

Many Human Presentations One Fact in XBRL one fact with many labels For example profit / non profit organizations

One Accounting Language Lessons Learned

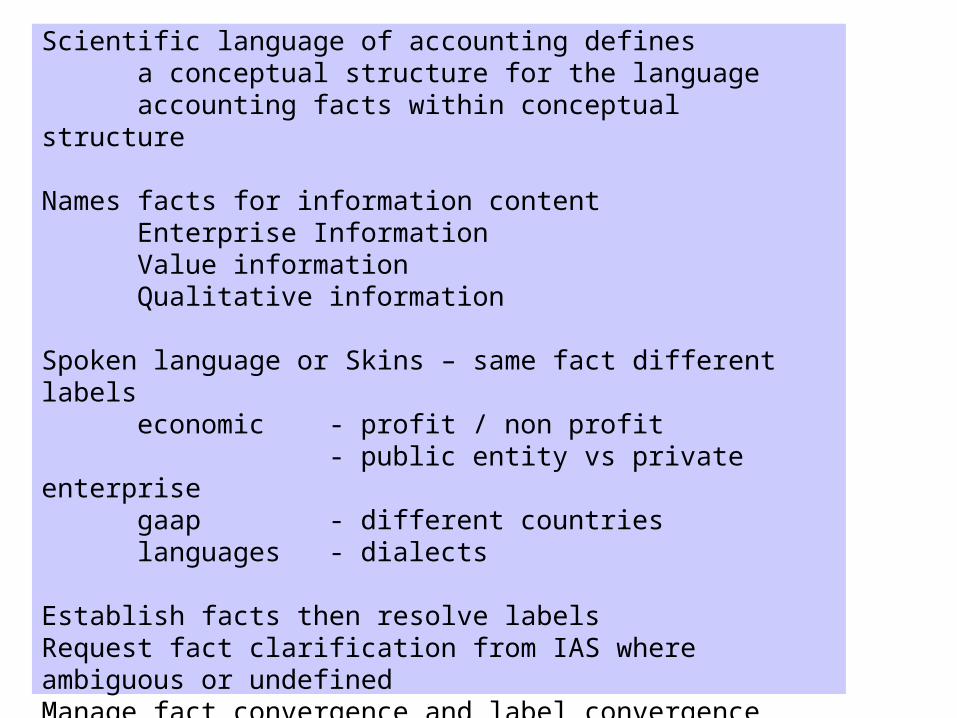

Scientific language of accounting definesa conceptual structure for the language accounting facts within conceptual structure

Names facts for information contentEnterprise InformationValue informationQualitative information

Spoken language or Skins – same fact different labelseconomic - profit / non profit

- public entity vs private enterprisegaap - different countrieslanguages - dialects

Establish facts then resolve labelsRequest fact clarification from IAS where ambiguous or undefinedManage fact convergence and label convergence separately

One Transaction Methodology Lessons Learned

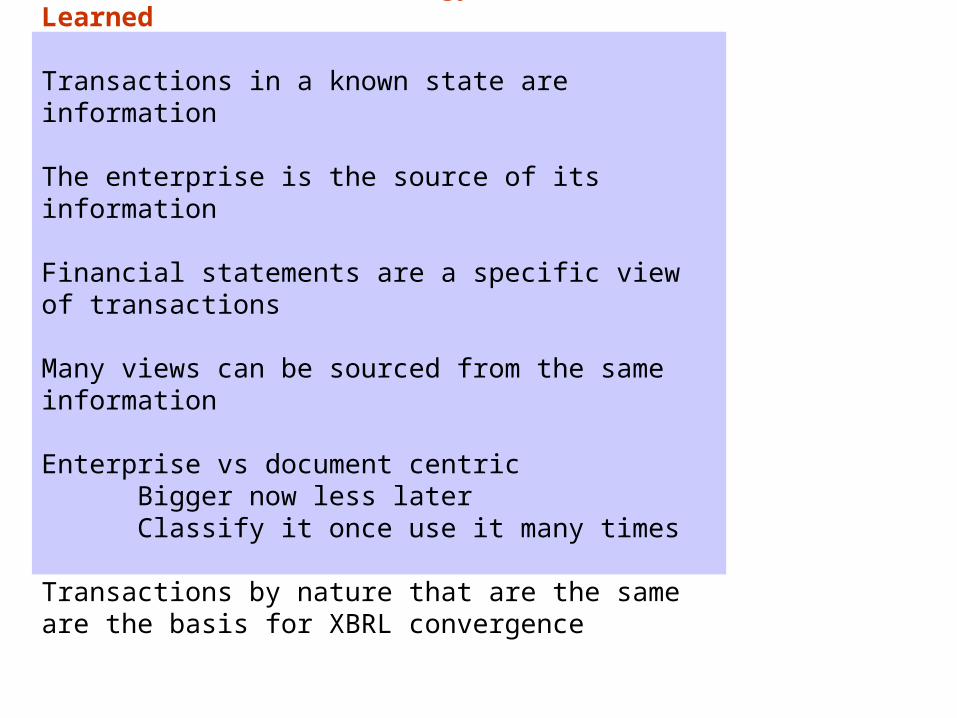

Transactions in a known state are information

The enterprise is the source of its information

Financial statements are a specific view of transactions

Many views can be sourced from the same information

Enterprise vs document centricBigger now less laterClassify it once use it many times

Transactions by nature that are the same are the basis for XBRL convergence

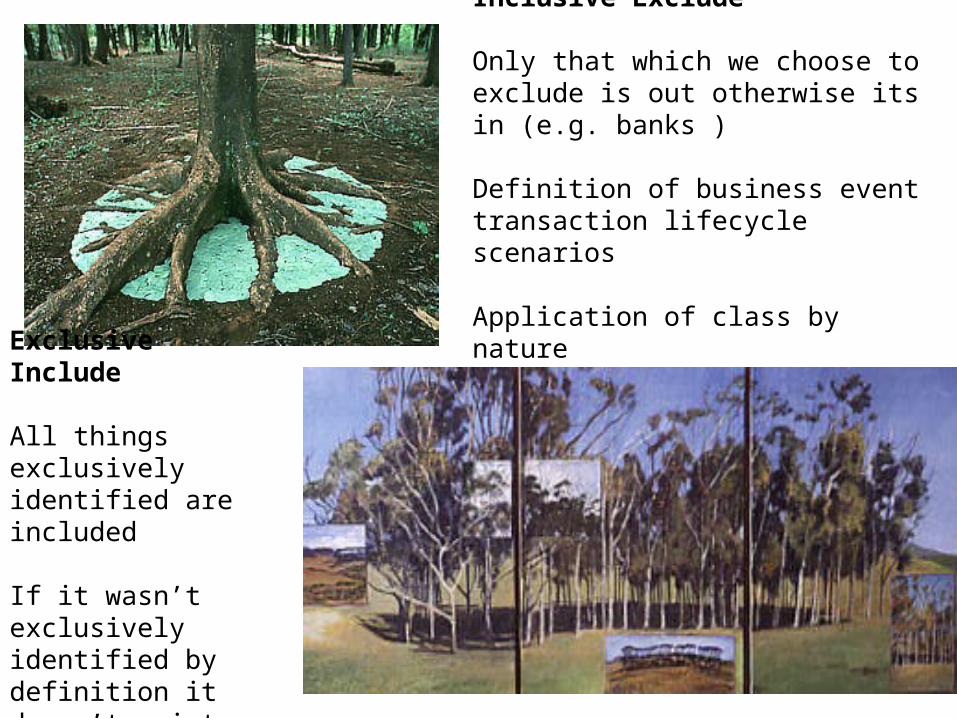

Exclusive Include

All things exclusively identified are included

If it wasn’t exclusively identified by definition it doesn’t exist

Inclusive Exclude

Only that which we choose to exclude is out otherwise its in (e.g. banks )

Definition of business event transaction lifecycle scenarios

Application of class by nature

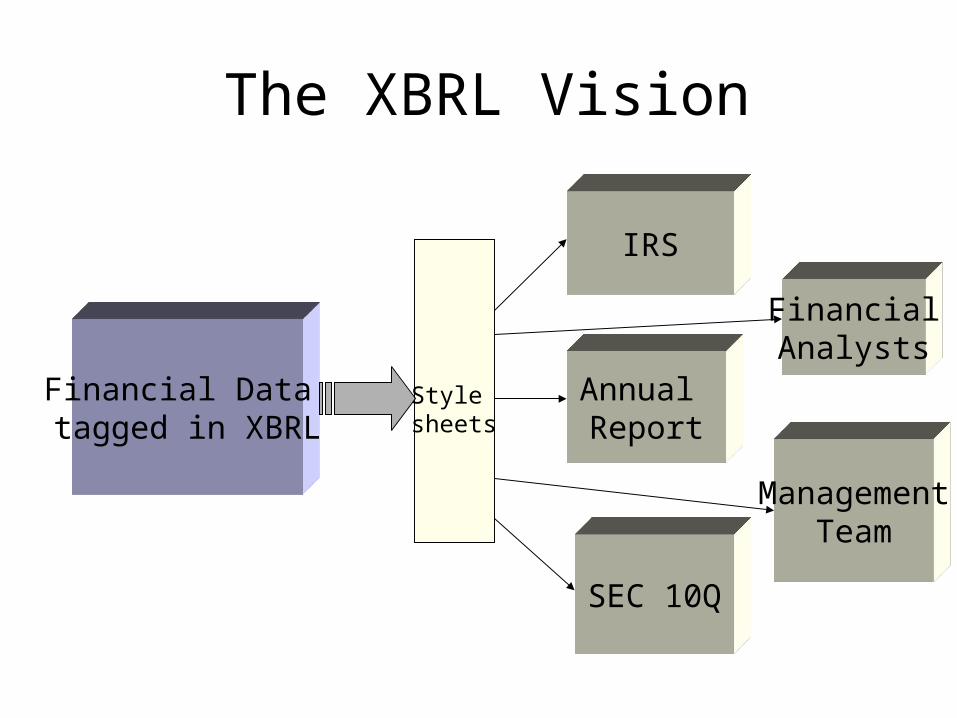

The XBRL Vision

Financial Data tagged in XBRL

IRS

Annual Report

SEC 10Q

FinancialAnalysts

ManagementTeam

Style sheets

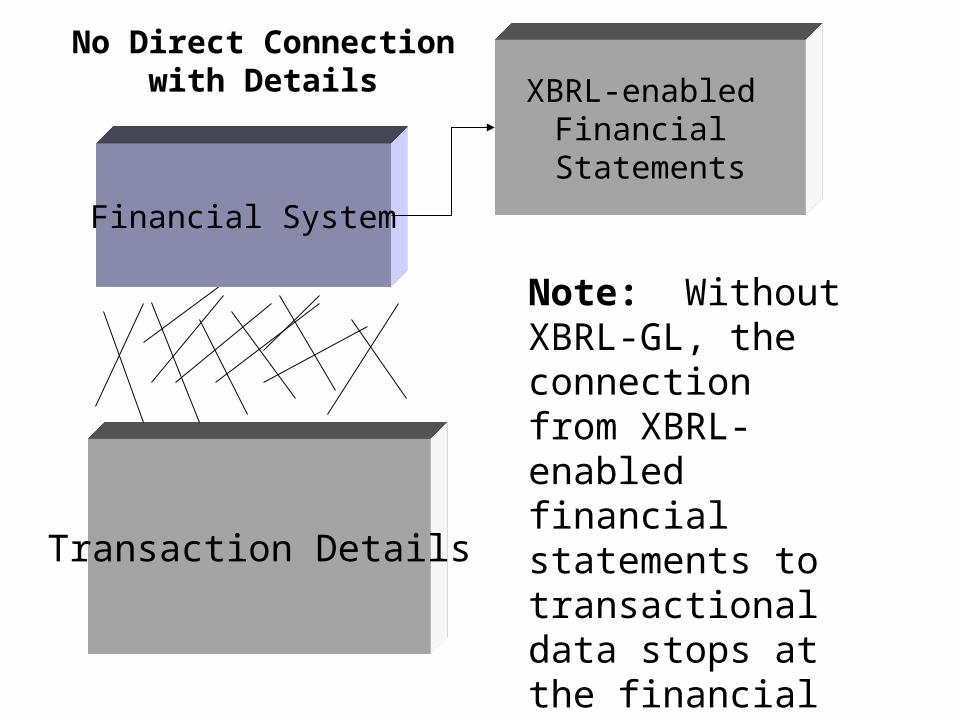

Transaction Details

Financial System

No Direct Connectionwith Details XBRL-enabled

Financial Statements

Note: Without XBRL-GL, the connection from XBRL-enabled financial statements to transactional data stops at the financial system

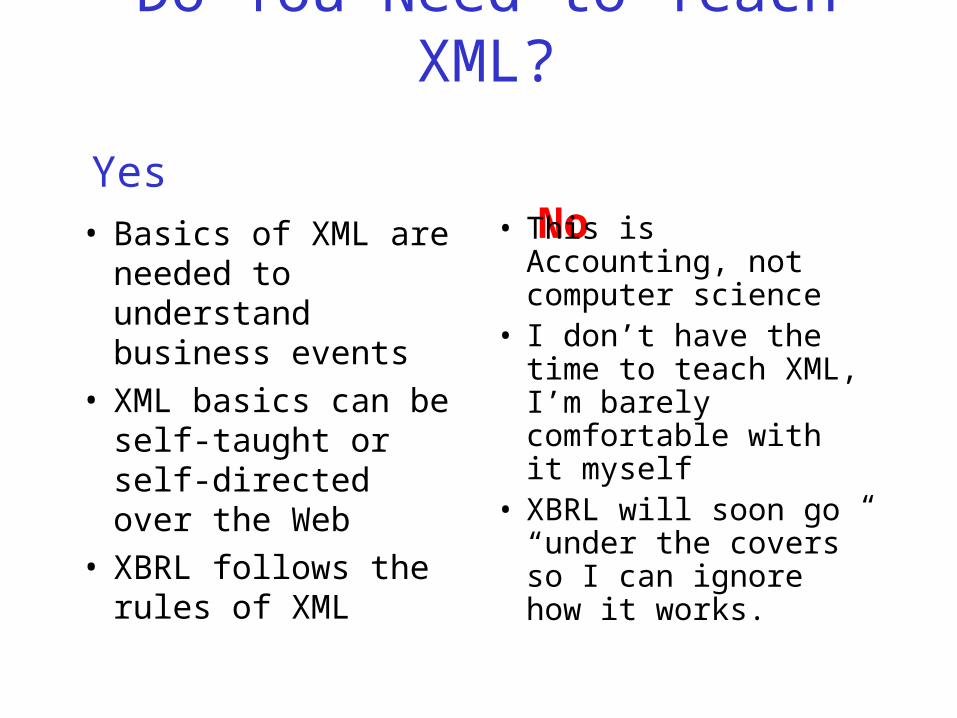

Do You Need to Teach XML?

Yes No

• Basics of XML are needed to understand business events

• XML basics can be self-taught or self-directed over the Web

• XBRL follows the rules of XML

• This is Accounting, not computer science

• I don’t have the time to teach XML, I’m barely comfortable with it myself

• XBRL will soon go “under the covers” so I can ignore how it works.

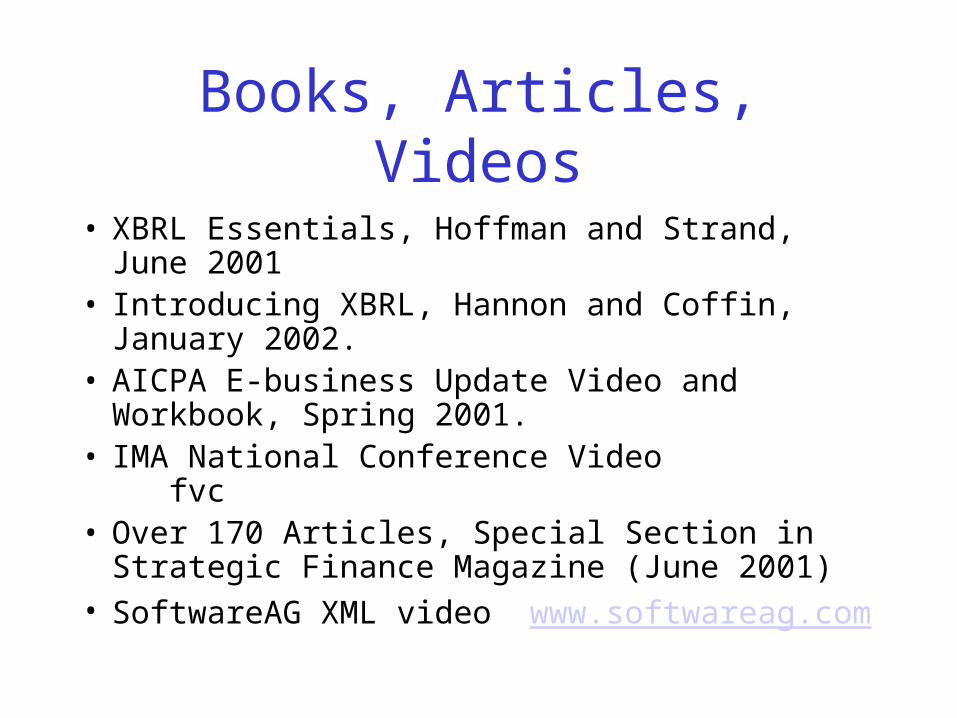

Books, Articles, Videos

• XBRL Essentials, Hoffman and Strand, June 2001• Introducing XBRL, Hannon and Coffin, January

2002.• AICPA E-business Update Video and Workbook,

Spring 2001.• IMA National Conference Video fvc• Over 170 Articles, Special Section in Strategic

Finance Magazine (June 2001)• SoftwareAG XML video www.softwareag.com

XBRL Tools

• Taxonomy Builders– Required to map a financial fact to XBRL

• See xbrl.org/tools.htm for details

• XML Validators– XML Spy 3.5