Embed Size (px)

Citation preview

ww

w.s

tab

ilit

as.e

u

1

INTRODUCTION, RESULTS AND INTRODUCTION, RESULTS AND EXPERIENCES OF THE EXPERIENCES OF THE

MULTIPORTFOLIO SYSTEM IN THE MULTIPORTFOLIO SYSTEM IN THE HUNGARIAN MANDATORY PENSION HUNGARIAN MANDATORY PENSION

FUNDSFUNDS

27 May 2010, Sinaia

Csaba NagyCsaba Nagy

ChairmanChairmanHungarian Association of Pension FundsHungarian Association of Pension Funds

EFRP CEEC ForumEFRP CEEC Forum

Association of Pension and Health Funds

Contents

Background Drawbacks in competition - Pillar 1 vs Pillar 2 Pressure to improve - Legislative changes in 2008 Implementation of multifunds Accounting unit based approach Post implementation experiences Evaluation of the Hungarian multifund system An alternative approach - „Target date (lifetime) funds” system Conclusions

2

Association of Pension and Health Funds

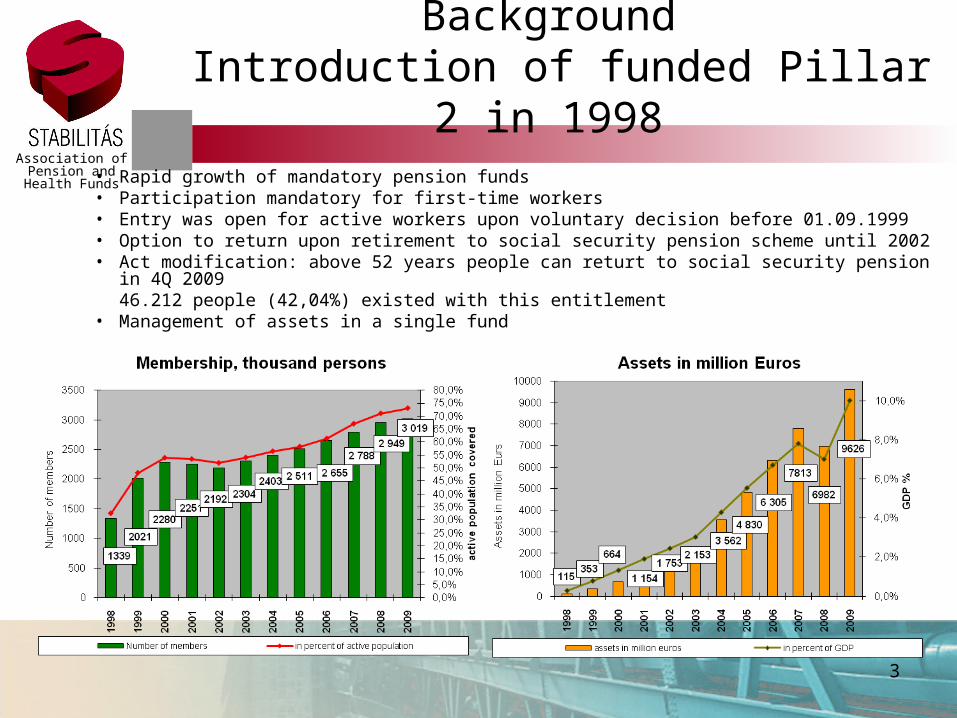

Background Introduction of funded Pillar 2 in 1998

• Rapid growth of mandatory pension funds• Participation mandatory for first-time workers• Entry was open for active workers upon voluntary decision before 01.09.1999• Option to return upon retirement to social security pension scheme until 2002• Act modification: above 52 years people can returt to social security pension in 4Q 2009

46.212 people (42,04%) existed with this entitlement• Management of assets in a single fund

3

Association of Pension and Health Funds

Reasons for underperforming returns

The proportion of the government securities within pension fund’s investments in 2000-2006: ~ 70%

• Relative high government bond’s yields• Frightening effects of the stock exchange crisis 1998 and 2008• Short-term approach (a „wrong year” involves competition drawback at member

recruiting)• Publishing of only 1 year’s yield

4

There is no possibility to take yield advantage of higher risk assets

Association of Pension and Health Funds

Pressure to improve - Legislative changes in 2008

• Introduction of the multiportfolio’s system (from 1 January 2008 it’s an opportunity, from 1 January 2009 it’s compulsory)

• Introduction of the accounting unit based records system (from 1 January 2008 it’s an opportunity, from 1 January 2009 it’s compulsory)

• Restriction of the asset management fee: The annual fee not allowed to exceed the 0.8% of the size of assets.

• Restriction of the operating expenses from 2009: 4.5% of the membership fee incomes can be spent on operating expenses.

• Apart from 1 year’s yield indexes the last 10 years’ indexes must be published.

5

Association of Pension and Health Funds

Implementation of multifunds – administrative requirements

• Funds must create exactly 3 portfolios• Classic (law risk and yield)• Balanced (middle risk and yield)• Growth (high risk and yield)

• A member’s saving can only be in one portfolio at the same time• Member’s decision can be

• an own choice• or „auto-enrolment” which means the acceptance of enrolment based on the time

remaining until retirement age (62 years)• If it’s more than 15 years: Growth portfolio• Between 5-15 years: Balanced portfolio• Less than 5 years: Classic portfolio

• Funds must update the automatic enrolment based on time remaining at the end of every year

• Members can change portfolio any time, but not more than with 6 months’ frequency (fee: 1 ‰, max 2.000 HUF)

6

Association of Pension and Health Funds

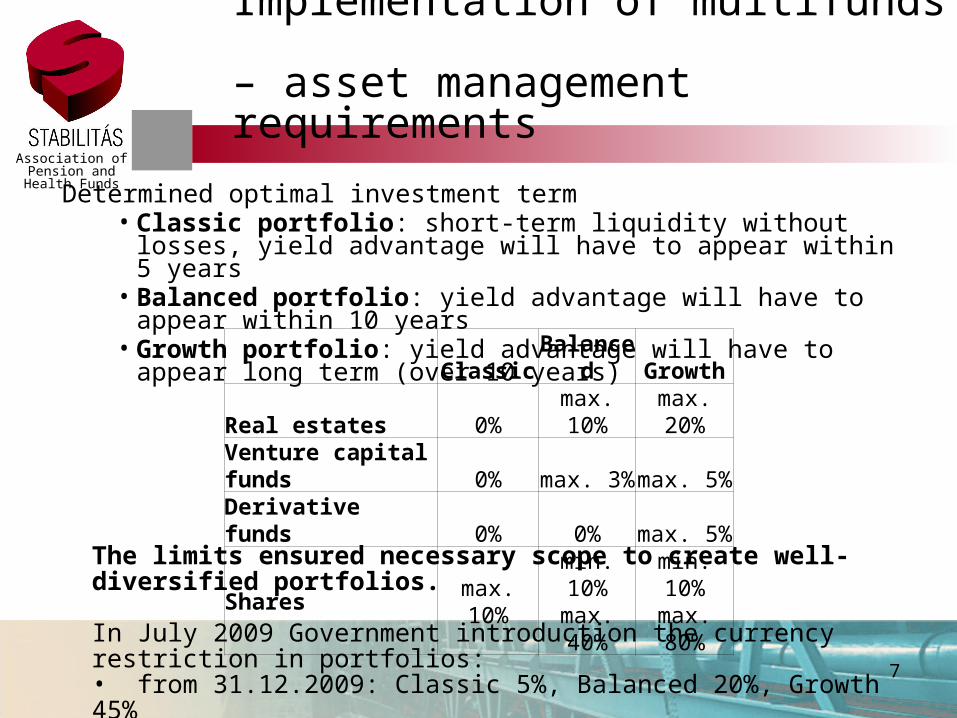

Implementation of multifunds – asset management requirements

7

The limits ensured necessary scope to create well-diversified portfolios.

In July 2009 Government introduction the currency restriction in portfolios:• from 31.12.2009: Classic 5%, Balanced 20%, Growth 45%• from 30.09.2009: Growth 35%

Determined optimal investment term• Classic portfolio: short-term liquidity without losses, yield advantage will have to

appear within 5 years• Balanced portfolio: yield advantage will have to appear within 10 years• Growth portfolio: yield advantage will have to appear long term (over 10 years)

Classic Balanced GrowthReal estates 0% max. 10% max. 20%Venture capital funds 0% max. 3% max. 5%Derivative funds 0% 0% max. 5%

Shares max. 10% min. 10% max. 40%

min. 10% max. 80%

Association of Pension and Health Funds

Accounting unit based approach

• Earlier: Distribution of yields by average stocks of individual accounts every quarter

• Accounting unit based records system• Account keeping in units primarily• Base exchange rate at the time of starting: 1.000000 HUF/unit• Daily calculation and publishing of exchange rates for all portfolios• Every transaction is converted from HUF to units (and in the opposite direction) by daily

exchange rates• Account balance in HUF: account balance in unit x daily unit exchange rate

• The new method is exact, but labour-intensive: it requires close cooperation of fund, asset management company and custodian every day

• The real challenge - system development and operation - was the change to accounting unit based method (less the multiportfolio system)

8

Association of Pension and Health Funds

Implementation statistics

9

Headcount (person)

Distribution

Classic 208 0,03%

Balanced 53 424 7%

Growth 671 097 93%

Together 724 729 100%

Headcount (person)

Distribution

Classic 3 162 4%

Balanced 17 045 22%

Growth 57 879 74%

Together 78 086 100%

Headcount (person)

Distribution

Classic 52 0,1%

Balanced 8 093 10%

Growth 69 941 90%

Together 78 086 100%

Members who didn't choose portfolio (by

age)

Members who chose portfolio (by

own decision)

Members who chose portfolio (by

age)

• 10 from 19 mandatory pension funds started in 2008

• OTP Mandatory Pension Fund’s data(market share by membership: 30%)

• Almost 10% of membership choose individually

• Most of individual decisions reflected the proper classification by age

• Slight overweighting of Classic portfolio

• Portfolios’ distribution of the new entrants in 2009: Classic 12,06%

Balanced 20,13% Growth 67,81%

Association of Pension and Health Funds

Adverse returns geared by multifunds

2008: Unfortunate timing of implementation Due to recession and equity market trends in 2008, pension funds applying multifund system have significantly underperformed the funds with single portfolios.

Private pension-funds lost 20% in 2008.2009: Hungary's private pension-funds generate average yield of over 20% in 2009 OTP Pension Funds generated outstanding yield in 2009 (Growth 33,51%, Balanced 21,72%, Classic 10,11%)

Inflation: 5,60%

10

Standard exchange rate index yields 2008 2009

MAX 2,59% 14,14%BUX -53,34% 73,40%CETOP20 (in HUF) -50,22% 39,98%MSCI Europe -42,39% 30,23%MSCI World -35,70% 30,10%MSCI Emerging Markets -49,25% 78,66%

Association of Pension and Health Funds

Post implementation experiences I.

Fund members’ reactions to the crisis in regard to OTP Mandatory Fund

11

• October 2008: falling of the stock market rates

• February 2009: publishing of the 2008’s yields of pension funds

• End of June 2009: Delivering of the annual statement for members

• 1.882 switching transactions during 2 years (number of members 800 thousand)

• Members don’t show too much interest in their own pension savings.

Association of Pension and Health Funds

Post implementation experiences II.

Recommendations (not too much success) to members regarding the portfolio transfers:

• In case of lack of personal knowledge age based classification

• Choose portfolio for long-term• Don’t realize losses by switching to a

less risky portfolio

12

Fund members’ reactions to the crisis in regard to OTP Mandatory Fund

Classic Balanced 5

Classic Growth 15

Balanced Classic 152

Balanced Growth 41

Growth Classic 679

Growth Balanced 324

1216Total

Distribution of members' switchings by portfolio types in 2009

Association of Pension and Health Funds

Post implementation experiences III.

• Agents capitalize the crisis and „convince” the members of usefulness of switching.

• From the 2nd half of 2009 the rules of switching are more rigorous:• Members must declare they had been informed about fund’s yields and risks of switching• Raising of switching fee

13

Fund members’ reactions to the crisis in regard to switching between funds (all mandatory sector)

Association of Pension and Health Funds

Evaluation of the Hungarian multifund system I.

Positives• Stable and useable model was born in a short time which can and must

develop further.• Possibility to create well-diversified investment portfolios.• In this time - in spite of crisis - retiring members are fortunate with the

new system (proportion of the government securities in „Classic” portfolio more than 90% - in single portfolio system it was only 70%)

Negatives• Funds introduce the multiportfolio system at different times:

• Due to crisis those funds which were faster and more client orientated suffered higher losses in 2008.

• Starting dates of daily exhange rates are different at the funds exchange rates of funds are not comparative directly.

14

Association of Pension and Health Funds

Evaluation of the Hungarian multifund system II.

Need improvement• Duration of portfolios are not optimal for all age-groups

• Duration of the 3 portfolios is not designed to match short-term savings (especially within 2 years before retirement) or the needs of career-starters (over up to 45 years)

• Switching portfolios may lead to losses• The law requires to allocate participants to the matching portfolio as of the end

of the year, regardless of the costs and losses caused by this forced switching.

• Participants are not encouraged to take advantage of diversification• Many of the participants are likely to stick to the portfolio they are allocated to.• Limited opportunities for the individual to allow optimal asset-liability matching.

15

Association of Pension and Health Funds

Multifunds system – an alternative approach I.

„Target date (lifetime) funds” system Intention: To avoid the double traps of taking low risk at young age and high

risk at old age• Creating the portfolios and classifying the members on the basis of age,

also.• But: If the member dosn’t choose individually, will stay in the same

portfolio until retirement.• Portfolios have life-cycle periods and maturity.• Number of portfolios is fixed. If a portfolio runs out, another takes the

place of it, and the new portfolio will be the longest maturity.• In the portfolios - in their duration - proportion of high risk assets

continuously decreases.

16

Association of Pension and Health Funds

„Target date (lifetime) funds” system

Alternative assets

Shares

Government securities

Money Market

Time turn of the asset allocation from working age (around 25 years) to retirement (65 years)

17

Association of Pension and Health Funds

„Target date (lifetime) funds” system - An example from USA

18

Association of Pension and Health Funds

Multifunds system - Conclusions

Key issues• Timing• Education of membership: Financial awareness ( Risk ↔ Yield)• Number of portfolios: Should be optimal for all age-groups• Investment policy: Enough room for diversification

19

ww

w.s

tab

ilit

as.e

u

20

THANK YOU FOR YOUR ATTENTIONTHANK YOU FOR YOUR ATTENTION

www.stabilitas.hu, www.stabilitas.eu

e-mail: [email protected]: [email protected]