Embed Size (px)

Citation preview

www.infinisource.net www.infinisource.comwww.infinisource.com

Copyright © 2011 All rights reserved.

www.infinisource.net www.infinisource.comwww.infinisource.com

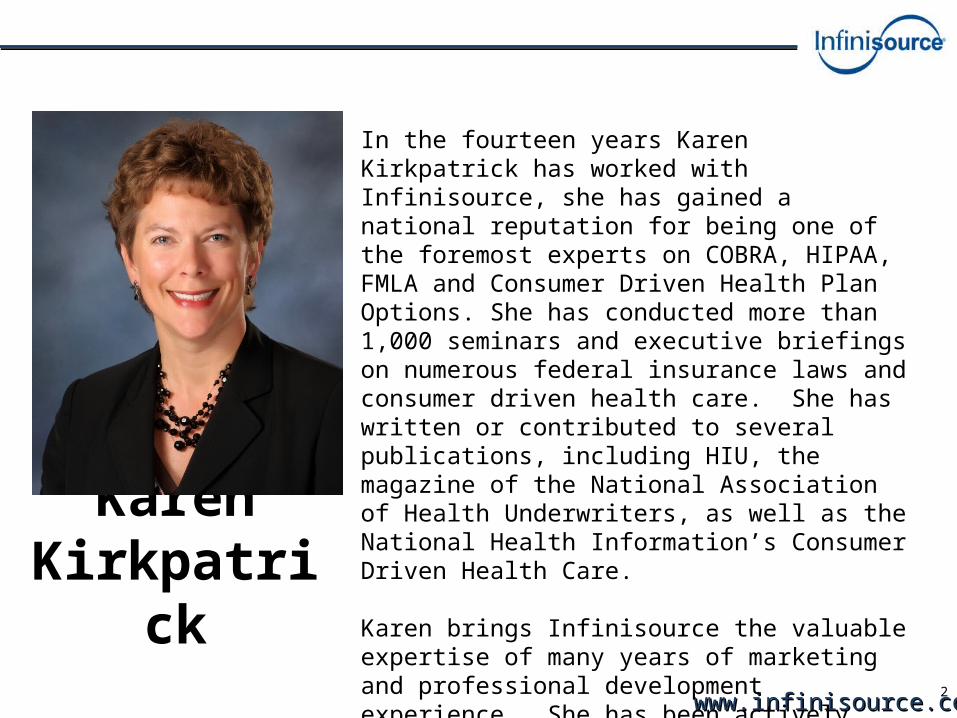

In the fourteen years Karen Kirkpatrick has worked with Infinisource, she has gained a national reputation for being one of the foremost experts on COBRA, HIPAA, FMLA and Consumer Driven Health Plan Options. She has conducted more than 1,000 seminars and executive briefings on numerous federal insurance laws and consumer driven health care. She has written or contributed to several publications, including HIU, the magazine of the National Association of Health Underwriters, as well as the National Health Information’s Consumer Driven Health Care. Karen brings Infinisource the valuable expertise of many years of marketing and professional development experience. She has been actively involved with Toastmasters International, which helps individuals become more effective speakers, leaders and listeners.

Karen Kirkpatrick

2

www.infinisource.net www.infinisource.comwww.infinisource.com

Introduction to Exchanges

www.infinisource.net www.infinisource.comwww.infinisource.com

Intro Letter to States• “states have the opportunity to play a major role in the creation and

operation of the Health Insurance Exchanges -new competitive insurance marketplaces where millions of Americans and small businesses will be able to purchase affordable coverage. Exchanges will give these consumers and employers similar health insurance options as are available to Members of Congress. As we look ahead to the establishment of the Exchanges and other reforms, it is essential that we work closely with states every step of the way.”-Kathleen Sebelius to the states

www.infinisource.net www.infinisource.comwww.infinisource.com

What is an Exchange?• An Exchange is a mechanism for organizing the health insurance

marketplace to help consumers and small businesses shop for coverage in a way that permits easy comparison of available plan options based on price, benefits and services, and quality. By pooling people together, reducing transaction costs, and increasing transparency, Exchanges create more efficient and competitive markets for individuals and small employers.

www.infinisource.net www.infinisource.comwww.infinisource.com

Governance and Models

• Governance– Public agency model– Public non-profit model– Quasi-governmental model

• Models– Clearinghouses– Active purchasers– Market organizers

www.infinisource.net www.infinisource.comwww.infinisource.com

Multi-State Plans Within Exchanges

• The Director of the Office of Personnel Management (referred to in this section as the ‘Director’) shall enter into contracts with health insurance issuers (which may include a group of health insurance issuers affiliated either by common ownership and control or by the common use of a nationally licensed service mark), without regard to section 5 of title 41, United States Code, or other statutes requiring competitive bidding, to offer at least 2 multi-State qualified health plans (one must be non-profit) through each Exchange in each State. Such plans shall provide individual, or in the case of small employers, group coverage.

www.infinisource.net www.infinisource.comwww.infinisource.com

Multi-State Plan Criteria

• Uniform in each state• Qualified Health Plans (QHP) for bronze, silver, gold

and catastrophic plans• Meets rating requirements• Offered in all states that have adopted adjusted

community rating prior to 3/23/10

www.infinisource.net www.infinisource.comwww.infinisource.com

Co-ops Within Exchanges

• A non-profit entity in which the same people who own the company are insured by the company. Cooperatives can be formed at a national, state or local level, and can include doctors, hospitals and businesses as member-owners.

www.infinisource.net www.infinisource.comwww.infinisource.com

States Responsibilities

• Each state must establish an individual and a small business exchange

• Small Business Health Options Program (SHOP) exchanges are established to assist small employers– Up to 2016: <50– Post 2016: 1-100

www.infinisource.net www.infinisource.comwww.infinisource.com

States Responsibilities

• States may operate multiple exchanges within the state• States may jointly form regional exchanges• A federal exchange will be established for states that choose

not to do it themselves• Exchanges must be operational for open enrollment by July

2013

www.infinisource.net www.infinisource.comwww.infinisource.com

Exchange Principles & Priorities

• Establishing a state-based exchange• Promoting efficiency• Avoiding adverse selection• Streamlined access and continuity of care• Public outreach and stakeholder involvement• Financial accountability

www.infinisource.net www.infinisource.comwww.infinisource.com

Exchange Core Functions

• Certification, recertification and decertification of plans• Operation of a toll-free hotline• Maintenance of a website for providing information on plans to

current and prospective enrollees• Assignment of a price and quality rating to plans• Presentation of plan benefit options in a standardized format• Provision of information on Medicaid and CHIP eligibility and

determination of eligibility for individuals in these programs

www.infinisource.net www.infinisource.comwww.infinisource.com

Functions Continued• Provision of an electronic calculator to determine the actual cost of

coverage taking into account eligibility for premium tax credits and cost sharing reductions

• Certification of individuals exempt from the individual responsibility requirement

• Provision of information on certain individuals identified in Section 1311 (d)(4)(I) to the Treasury Department and to employers

• Establishment of a Navigator program that provides grants to entities assisting consumers as described in Section 1311(i)

www.infinisource.net www.infinisource.comwww.infinisource.com

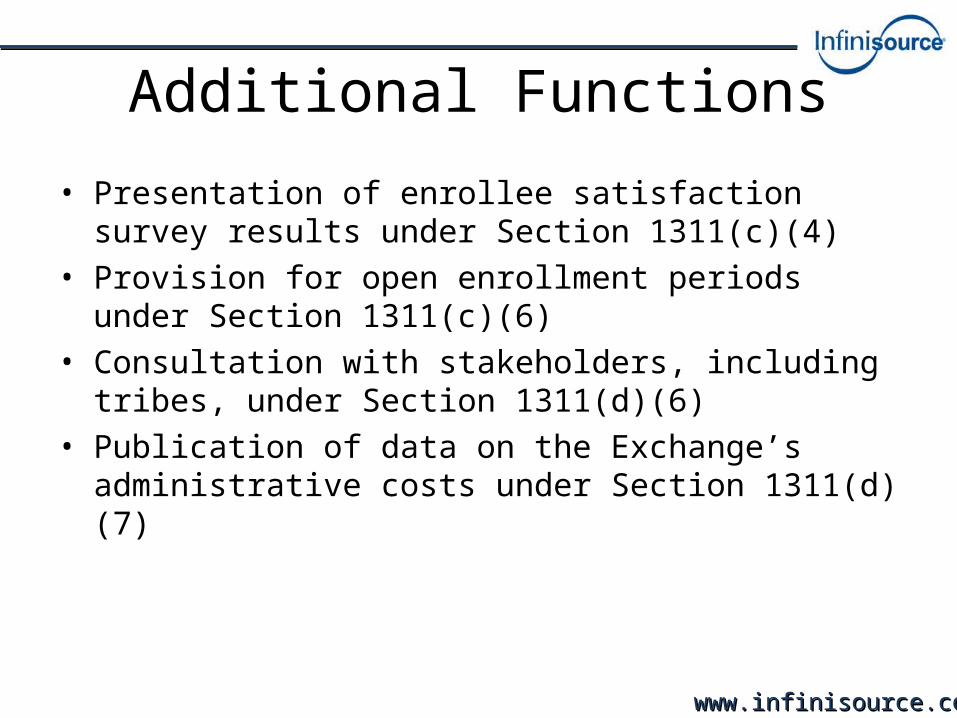

Additional Functions

• Presentation of enrollee satisfaction survey results under Section 1311(c)(4)

• Provision for open enrollment periods under Section 1311(c)(6)

• Consultation with stakeholders, including tribes, under Section 1311(d)(6)

• Publication of data on the Exchange’s administrative costs under Section 1311(d)(7)

www.infinisource.net www.infinisource.comwww.infinisource.com

Oversight Responsibilities

• In order for insurers to be certified as Qualified Health Plans, they must:– Marketing– Network adequacy– Accreditation for performance measures– Quality improvement and reporting– Uniform enrollment procedures

www.infinisource.net www.infinisource.comwww.infinisource.com

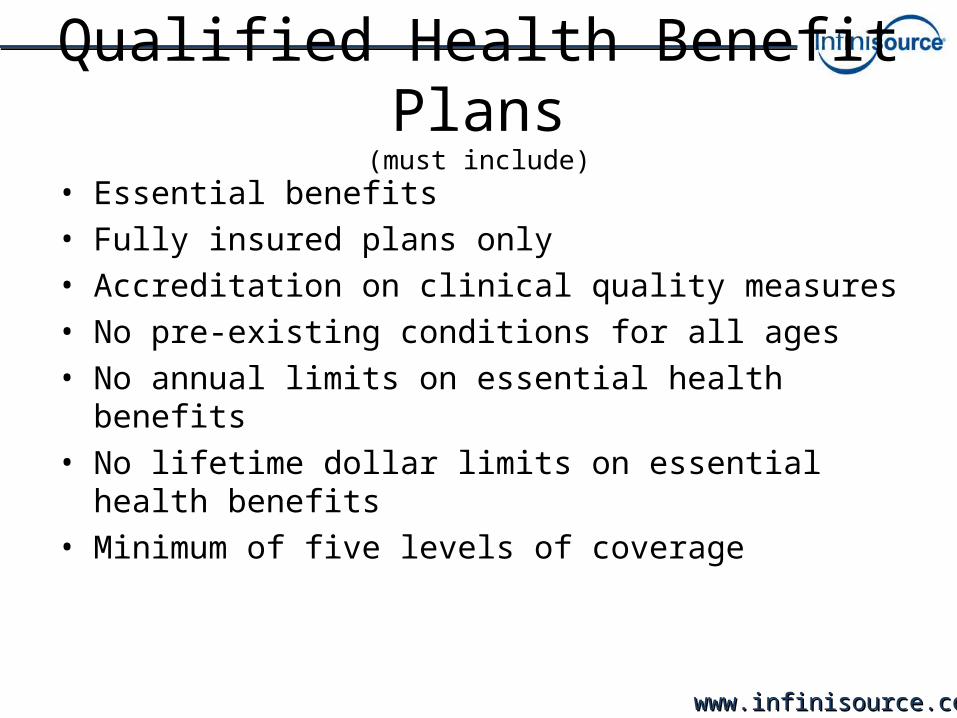

Qualified Health Benefit Plans(must include)

• Essential benefits• Fully insured plans only• Accreditation on clinical quality measures• No pre-existing conditions for all ages• No annual limits on essential health benefits• No lifetime dollar limits on essential health benefits• Minimum of five levels of coverage

www.infinisource.net www.infinisource.comwww.infinisource.com

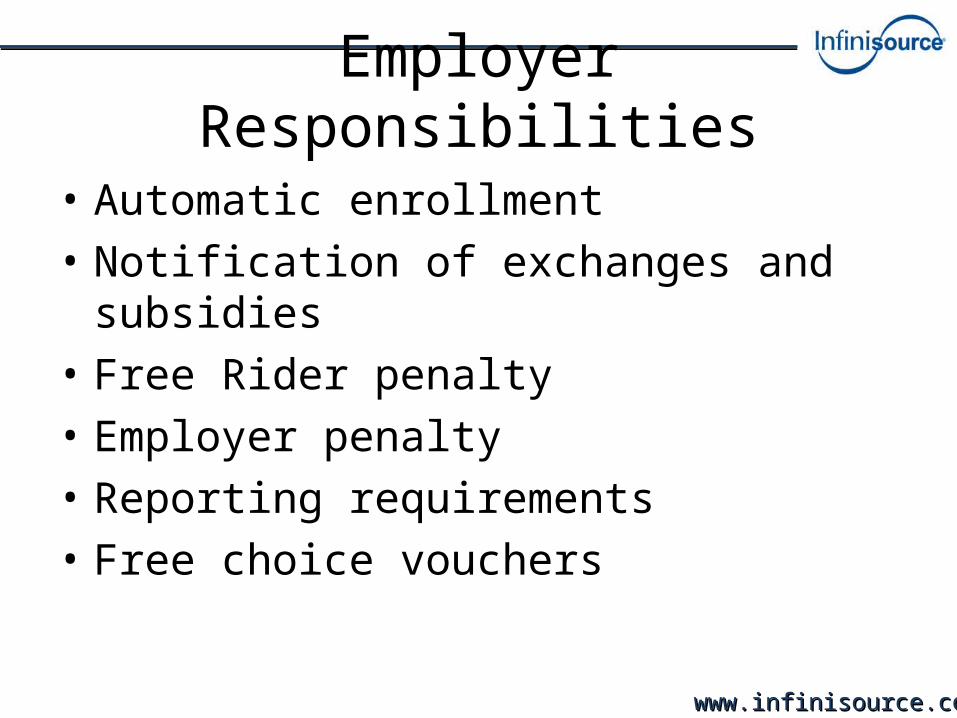

Employer Responsibilities

• Automatic enrollment• Notification of exchanges and subsidies• Free Rider penalty• Employer penalty• Reporting requirements• Free choice vouchers

www.infinisource.net www.infinisource.comwww.infinisource.com

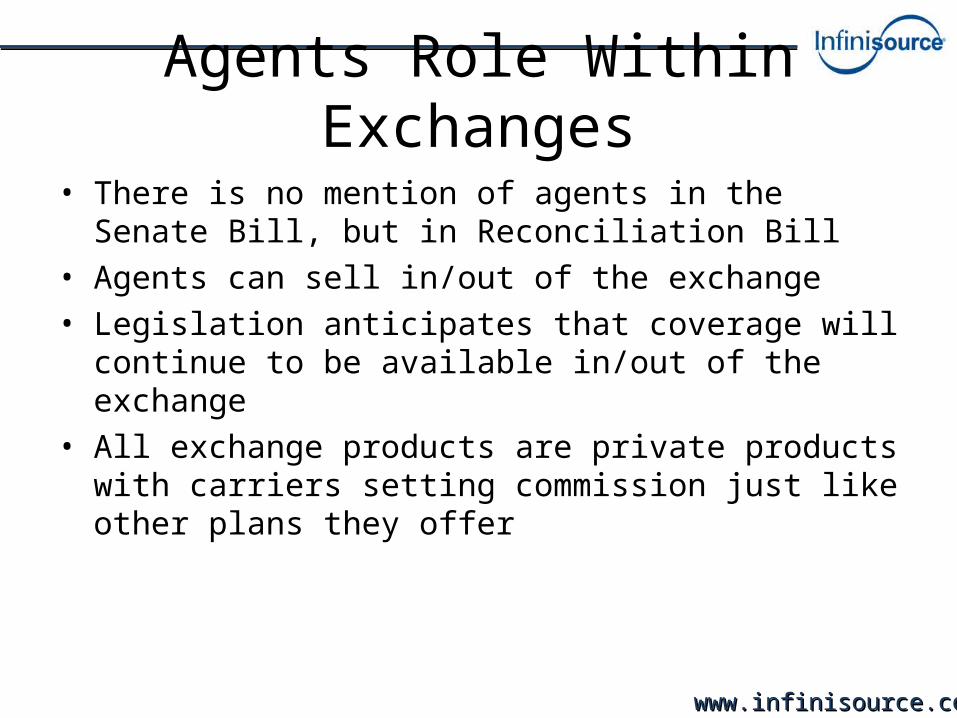

Agents Role Within Exchanges

• There is no mention of agents in the Senate Bill, but in Reconciliation Bill

• Agents can sell in/out of the exchange• Legislation anticipates that coverage will continue to be

available in/out of the exchange• All exchange products are private products with carriers

setting commission just like other plans they offer

www.infinisource.net www.infinisource.comwww.infinisource.com

Written Plan Requirements

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:Plan Documents

• Required elements– “a written instrument”– Identification of named fiduciary– Description of how responsibilities are

allocated– Funding policy– Basis for making payments– Procedure for amending plan

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:Plan Documents (cont.)

• Optional elements– More than one fiduciary capacity (e.g., trustee

and administrator)– Fiduciary may employ others to fulfill its plan

duties – Fiduciary may appoint plan asset manager – Incorporate SPD by reference

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs

• Basic questions – Who must provide?

• Plan administrators– To whom must it be provided?

• Covered employees– How may it be provided?

• In a manner “reasonably calculated to ensure receipt” • For example, first-class mail, hand-delivery, and electronic

distribution, if the employees have access to computers in the workplace and can print a copy easily.

• Provide non-English assistance

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs (cont.)

• Basic questions– When must it be provided?

• Within 90 days of enrollment• Within 120 days of plan formation• Every five years if changes made to SPD

information or plan is amended

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs (cont.)

• Content requirements– Plan name, employer’s name and address– Plan sponsor’s EIN and plan number – Indication of plan year– Plan type (e.g., health FSA, group health plan)– Identification of how plan is administered

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs (cont.)

• Content requirements– Plan administrator’s and trustee’s name,

address and phone– Designated legal agent’s name, address and

statement that process may be served on plan administrator/trustee

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs (cont.)

• Content requirements– Special statement for union plans– Eligibility statement, benefit summary and

QMCSO information– Participant ineligibility/termination

www.infinisource.net www.infinisource.comwww.infinisource.com

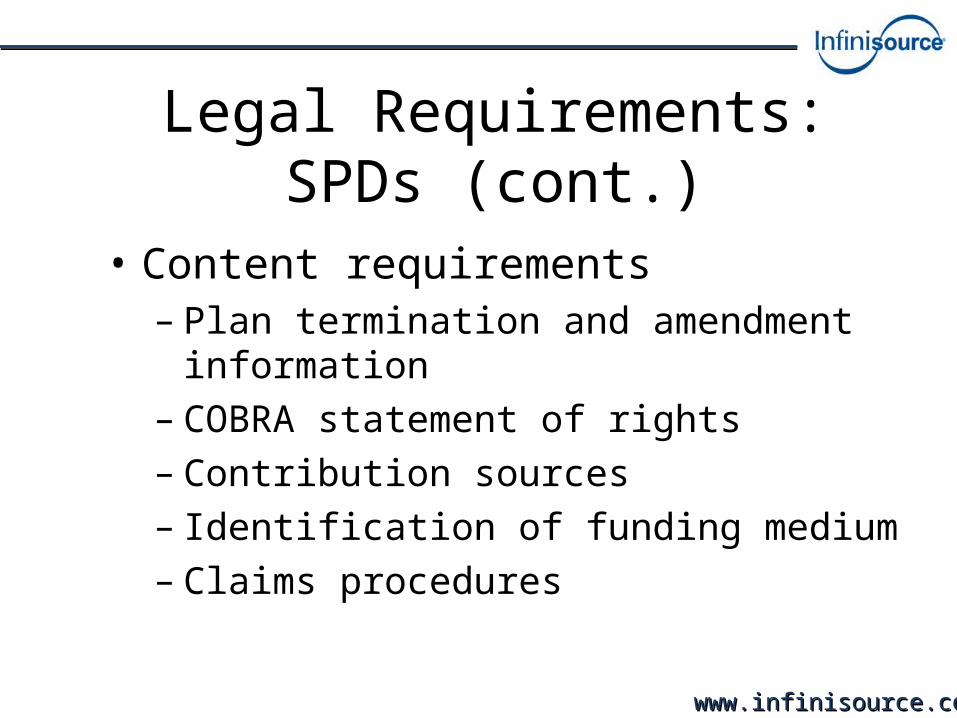

Legal Requirements:SPDs (cont.)

• Content requirements – Plan termination and amendment information– COBRA statement of rights– Contribution sources– Identification of funding medium– Claims procedures

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:SPDs (cont.)

• Content requirements – ERISA rights statement– Statement related to newborn children– Other required notices

• HIPAA portability• Other ERISA mandates

www.infinisource.net www.infinisource.comwww.infinisource.com

Legal Requirements:

• Summary of Material Modifications (SMM)– For material modifications or SPD changes– Must provide within 210 days of plan year end (or

within 60 days of change if material benefit reduction)– “… written in a manner calculated to be understood by

the average plan participant …”– Includes changes to rates, premiums, contributions,

copayments

www.infinisource.net www.infinisource.comwww.infinisource.com

Summary of Benefits and Coverage

• PUR: To provide a “four-page” summary of benefits for plan comparison purposes

• AGE: EBSA, CMS, IRS• WHO: Participants• DEL: With enrollment materials• TIM: March 23, 2012, then 30 days before plan year or

60 days before material modification and upon request• PEN: Up to $1,000 for each failure and $100 daily IRS

excise tax

March 23, 2012 start date is likely to be delayed

www.infinisource.net www.infinisource.comwww.infinisource.com

W-2 Reporting Requirements

www.infinisource.net www.infinisource.comwww.infinisource.com

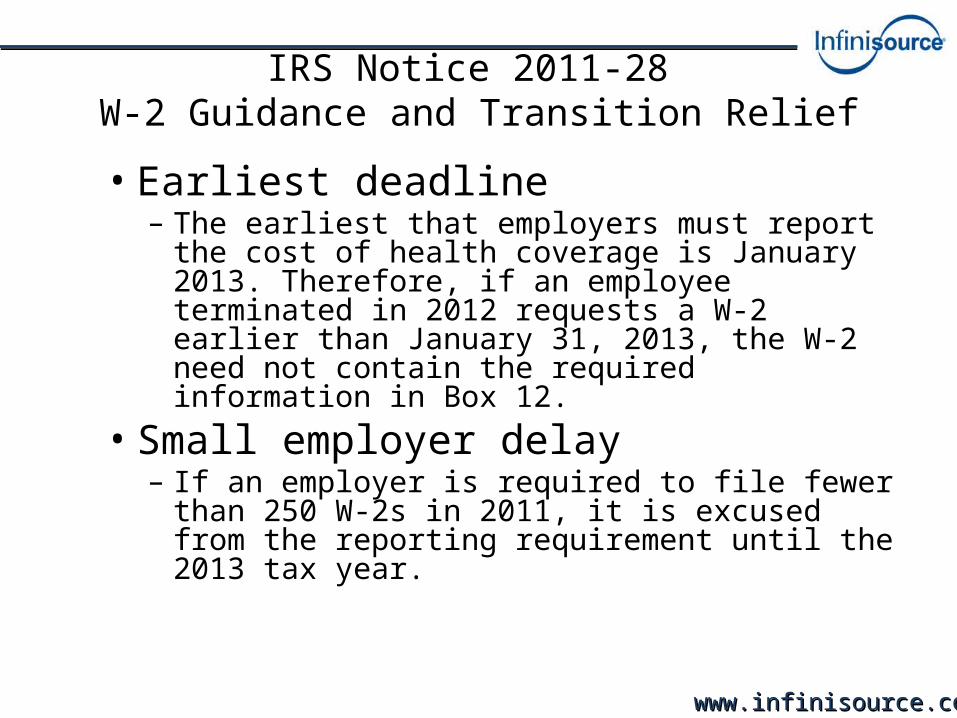

IRS Notice 2011-28 W-2 Guidance and Transition Relief

• Earliest deadline– The earliest that employers must report the cost of

health coverage is January 2013. Therefore, if an employee terminated in 2012 requests a W-2 earlier than January 31, 2013, the W-2 need not contain the required information in Box 12.

• Small employer delay– If an employer is required to file fewer than 250

W-2s in 2011, it is excused from the reporting requirement until the 2013 tax year.

www.infinisource.net www.infinisource.comwww.infinisource.com

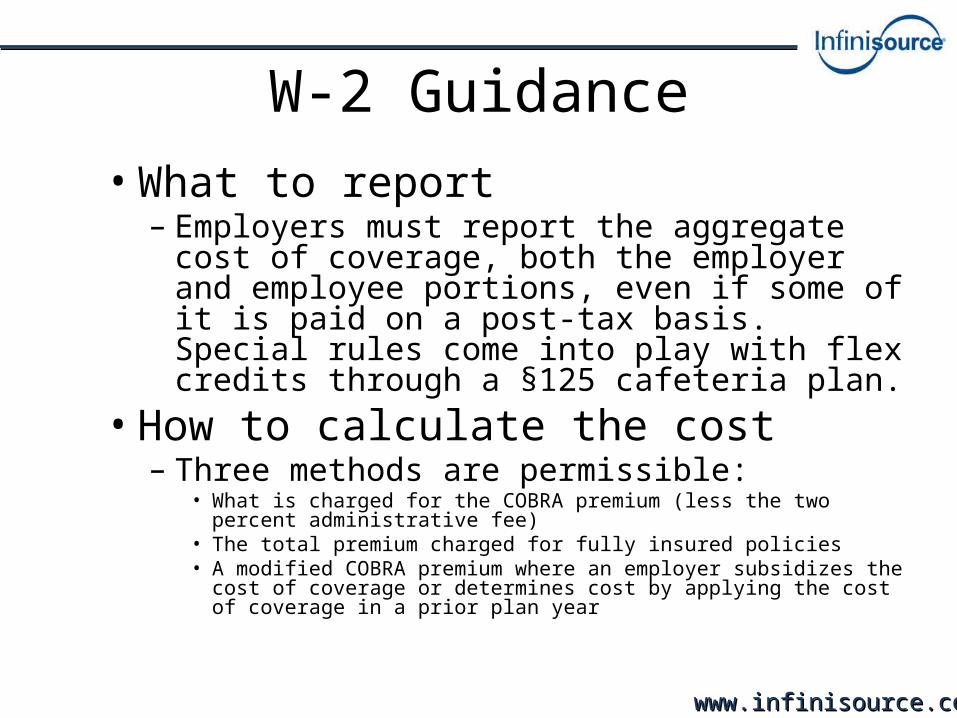

W-2 Guidance• What to report

– Employers must report the aggregate cost of coverage, both the employer and employee portions, even if some of it is paid on a post-tax basis. Special rules come into play with flex credits through a §125 cafeteria plan.

• How to calculate the cost– Three methods are permissible:

• What is charged for the COBRA premium (less the two percent administrative fee)

• The total premium charged for fully insured policies • A modified COBRA premium where an employer subsidizes the cost of

coverage or determines cost by applying the cost of coverage in a prior plan year

www.infinisource.net www.infinisource.comwww.infinisource.com

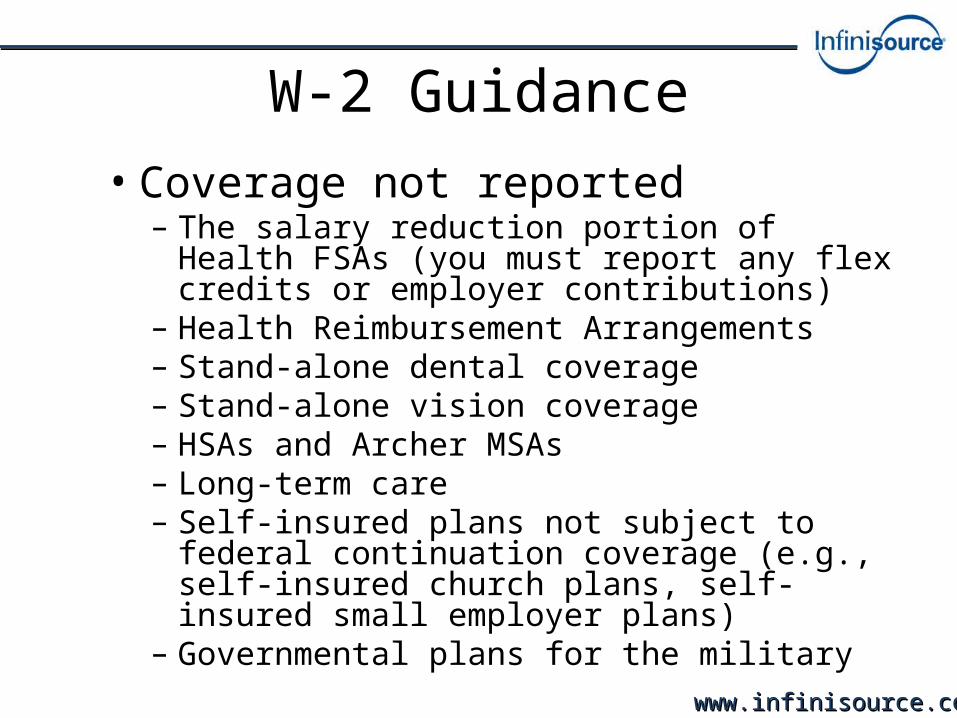

W-2 Guidance• Coverage not reported

– The salary reduction portion of Health FSAs (you must report any flex credits or employer contributions)

– Health Reimbursement Arrangements – Stand-alone dental coverage – Stand-alone vision coverage – HSAs and Archer MSAs – Long-term care – Self-insured plans not subject to federal

continuation coverage (e.g., self-insured church plans, self-insured small employer plans)

– Governmental plans for the military

www.infinisource.net www.infinisource.comwww.infinisource.com

Medicare Secondary Payer (MSP)

www.infinisource.net www.infinisource.comwww.infinisource.com

MSP Topics

• COBRA events• Lawsuit regarding employer advice• MSP and HRAs

www.infinisource.net www.infinisource.comwww.infinisource.com

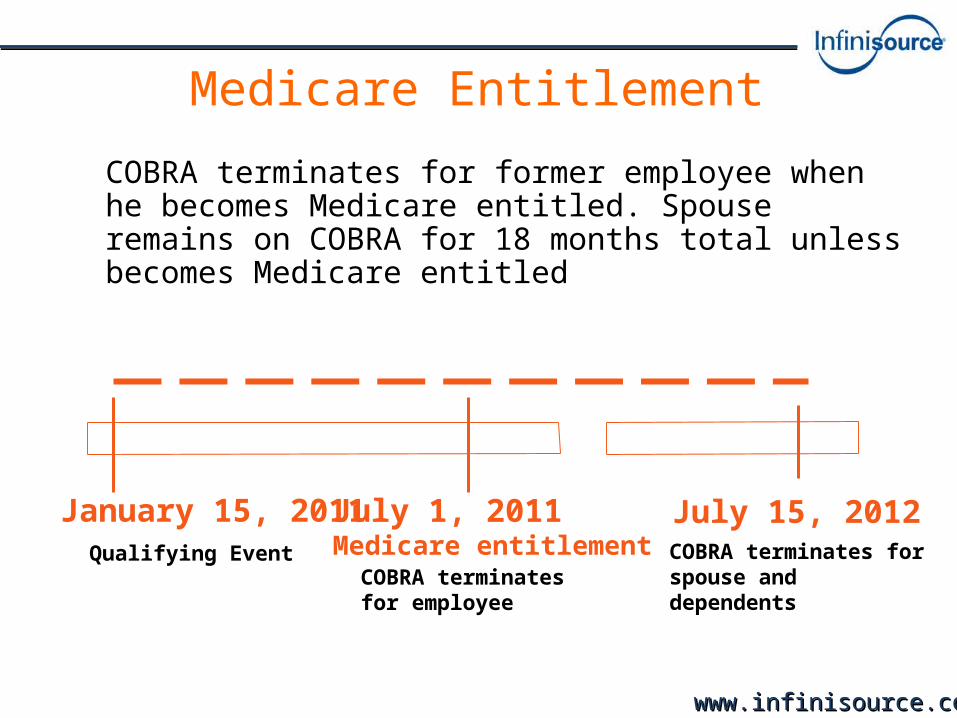

Medicare Entitlement

COBRA terminates for former employee when he becomes Medicare entitled. Spouse remains on COBRA for 18 months total unless becomes Medicare entitled

July 1, 2011Medicare entitlementQualifying Event

January 15, 2011 July 15, 2012

COBRA terminates for employee

COBRA terminates for spouse and dependents

www.infinisource.net www.infinisource.comwww.infinisource.com

Medicare Entitlement

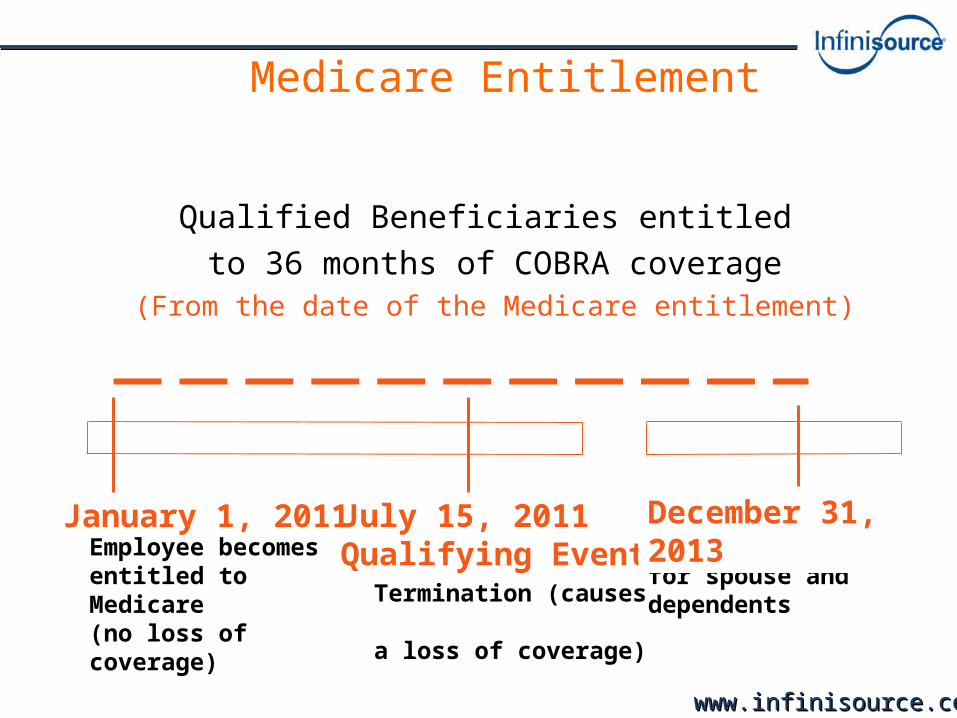

Qualified Beneficiaries entitled to 36 months of COBRA coverage

(From the date of the Medicare entitlement)

July 15, 2011Qualifying EventEmployee becomes

entitled to Medicare(no loss of coverage)

January 1, 2011

Termination (causes a loss of coverage)

COBRA terminates for spouse and dependents

December 31, 2013

www.infinisource.net www.infinisource.comwww.infinisource.com

Why Offer an FSA?

www.infinisource.net www.infinisource.comwww.infinisource.com

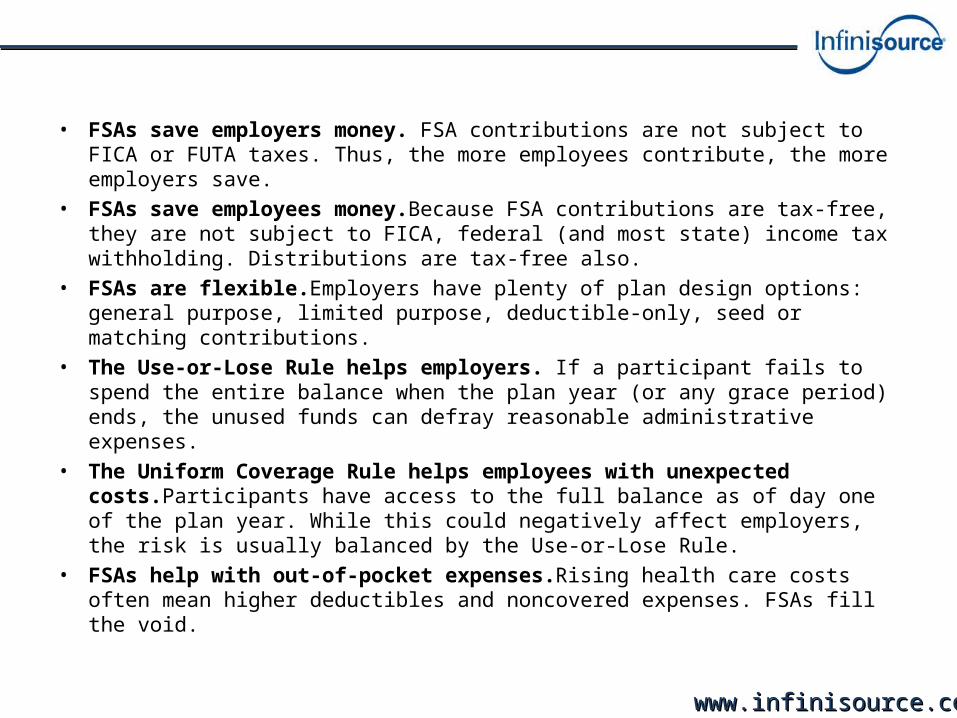

• FSAs save employers money. FSA contributions are not subject to FICA or FUTA taxes. Thus, the more employees contribute, the more employers save.

• FSAs save employees money.Because FSA contributions are tax-free, they are not subject to FICA, federal (and most state) income tax withholding. Distributions are tax-free also.

• FSAs are flexible.Employers have plenty of plan design options: general purpose, limited purpose, deductible-only, seed or matching contributions.

• The Use-or-Lose Rule helps employers. If a participant fails to spend the entire balance when the plan year (or any grace period) ends, the unused funds can defray reasonable administrative expenses.

• The Uniform Coverage Rule helps employees with unexpected costs.Participants have access to the full balance as of day one of the plan year. While this could negatively affect employers, the risk is usually balanced by the Use-or-Lose Rule.

• FSAs help with out-of-pocket expenses.Rising health care costs often mean higher deductibles and noncovered expenses. FSAs fill the void.

www.infinisource.net www.infinisource.comwww.infinisource.com

• Health FSAs are not always subject to COBRA.Generally, an overspent Health FSA is not subject to COBRA. Health FSA COBRA coverage only lasts through the end of the current plan year.

• Health FSAs can cover adult children.Because of the Affordable Care Act (ACA), participants can cover their adult children on a Health FSA until the year in which the children turn age 27.

• You can save on orthodontia.Typically, an orthodontist provides a discount if payment is up front, instead of month to month. Health FSAs may now reimburse orthodontia expenses when paid, instead of when they are incurred.

• Dependent care expenses are a no-brainer.Dependent care expenses are usually a fixed cost that easily exceeds the $5,000 FSA limit in a year, even for just one child. Tax-free reimbursement makes a lot of sense.

• Debit cards make it even easier.Debit card auto-substantiation rates are usually over 90 percent, virtually eliminating the hassle of keeping receipts and waiting for reimbursement.

www.infinisource.net www.infinisource.comwww.infinisource.com

How to Survive an Audit

www.infinisource.net www.infinisource.comwww.infinisource.com

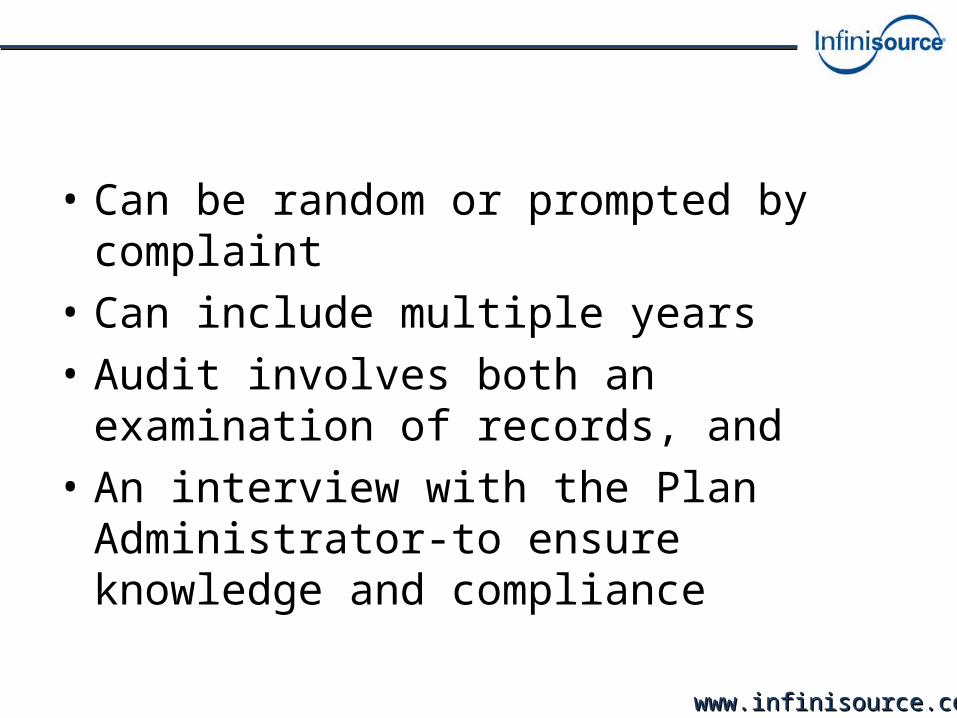

• Can be random or prompted by complaint• Can include multiple years• Audit involves both an examination of records,

and• An interview with the Plan Administrator-to

ensure knowledge and compliance

www.infinisource.net www.infinisource.comwww.infinisource.com

• Signed plan documents including all amendments in use since *date*

• Signed Annual Report Form 5500’s and schedules since *date*

• All Summary Plan Descriptions since *date*• All health insurance contracts and policies including all

amendments and riders covering the Plan since *date*• Copies of all employee enrollment applications in use since

*date*

www.infinisource.net www.infinisource.comwww.infinisource.com

• All written agreements between the Plan and Insurance issuer whereby certificates of creditable coverage (Certs) are issued by a separate issuer

• To the extent there is no agreement between the Plan and Issuer to provide Certs for individuals who have lost coverage under the Plan or have requested Certs, provide a list or log of issued Certs

• Written procedures provided to individuals to request and receive Certs

www.infinisource.net www.infinisource.comwww.infinisource.com

• A copy of the Plan’s General Notice of Preexisting Condition issued to enrollees and a copy of the Individual Notice of determination of any preexisting condition exclusion period that applies to the individual and notification of creditable coverage applied to the preexisting condition exclusion period including lists or logs of issued notices

www.infinisource.net www.infinisource.comwww.infinisource.com

• Notices of Special Enrollment Rights including lists and logs of issued notices

• The plan’s Newborn’s Act notice (this should appear in the plan’s SPD), including lists or logs of notices an administrator may keep of issued notices

• Notices provided as required by the Women’s Health and Cancer Rights Act, including lists or logs of issued notices

www.infinisource.net www.infinisource.comwww.infinisource.com

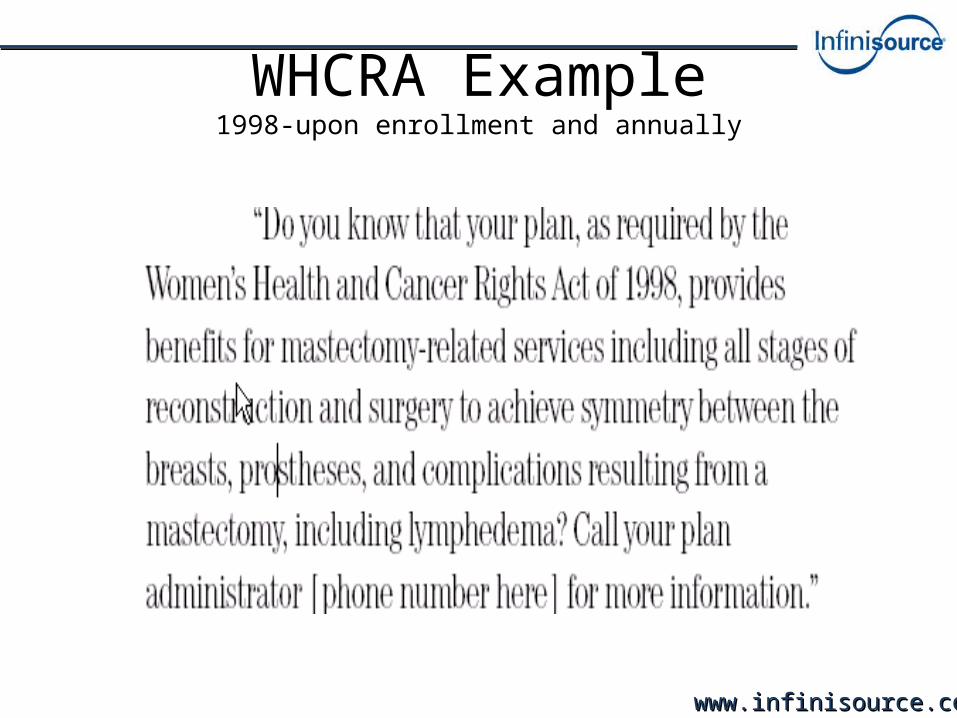

WHCRA Example1998-upon enrollment and annually

www.infinisource.net www.infinisource.comwww.infinisource.com

• Health insurance billing invoices, premium schedules, employee and employer contribution schedules, and/or payroll records of withholding for benefits

• Materials describing any wellness programs or disease management programs offered by the plan. If the program offers a reward based on the individual’s ability to meet a standard related to a health factor, the plan should also include its wellness program disclosure statement regarding the availability of a “reasonable alternative”

www.infinisource.net www.infinisource.comwww.infinisource.com

• Notices provided to participants and beneficiaries explaining their rights to continuation of coverage as required by COBRA of 1985, including a list or log of notices issued

• Employee census reports provided to the health insurance providers

www.infinisource.net www.infinisource.comwww.infinisource.com

• All correspondence between the Plan and the health insurance providers

• Any Service Provider Contracts in existence since *date*, including, (Investment Manager Agreements, Insurance Contract Agreements, TPA Agreements, Actuary Agreements, Accounting Agreements and Legal Agreements).

www.infinisource.net www.infinisource.comwww.infinisource.com

• “The examiner will need copies of the items marked with a * (which were most items in the audit letter). Additional records may be requested following review of the above.”

www.infinisource.net www.infinisource.comwww.infinisource.com

Be Prepared

• Conduct compliance reviews for COBRA• Ensure manuals, policies and procedures are

written and adhered to• Form 8928 compliance• Relationship between payroll and benefits

www.infinisource.net www.infinisource.comwww.infinisource.com

• Thank you for attending today! If you have any questions, please direct them to:

Alex Lara, 800-300-3838 or [email protected]