Embed Size (px)

Citation preview

www.cme-mec.ca

Roadmap to RecoveryInnovation, Investment, & Growth

Durham Economic Prosperity ConferenceNovember 5th, 2010

www.cme-mec.ca

Moving Forward Together

Strengths Weaknesses

Opportunities Threats

www.cme-mec.ca

Strengths• Regional

– Skilled labour– Airport with Canada Customs & Deep-water port (Canadian Port Authority)– Strong agricultural base & abundant land– 3 state-of-the-art educational & research institutions – World-class medical facility– Nuclear power– State-of the-art auto manufacturing & abundant production capacity– Quality of life, recreation, green space, nature, extensive waterfront

• Provincial– Proximity to customers, suppliers, world-class innovation infrastructure– Strong federal and provincial support for innovation and next generation technologies

• National– Competitively low business tax rates– Comparatively low levels of government debt– Comparatively strong financial sector

www.cme-mec.ca

Weaknesses• Regional

– Road system– Job creation does not keep pace with population growth– Loss of industrial base

• Provincial– Uncertain, slow, costly, and at times impractical regulatory system– Reliable access to cost competitive energy?– Lack of a clear transportation plan– Lack of clear economic development objectives– Weak connections between innovation infrastructure & business needs

• National– Lack of a clear long-term economic/industrial strategy– Partisanship trumps policy– Highly leveraged consumer sector– Manufacturing and exporting sector highly integrated with the United States

www.cme-mec.ca

Threats• A Sustainable Recovery?– Global financial and currency risks– Unwinding stimulus

• Obstacles to Recovery– Strong and volatile Canadian dollar– Weak cash flow = limited availability and higher cost of business financing– Overcapacity in many industrial markets, corporate consolidation & loss of product mandates– Unfair trading practices, protective restrictions in export markets (Buy American) & aggressive

use of investment incentives in the United States– Increasing mandatory overheads – fees, taxes & regulatory compliance costs– Thickening border – security, customs, regulations, fees, administration

• Game Changers – Changing customer requirements & expectations– Shift in market power & economic growth to emerging economies (China, Asia, Latin America)– Corporate restructuring & supply chain reorganization– An aging population – Skill shortages, increased demand for health care & retirement income

with fewer people working & investing– Energy constraints & environmental priorities

www.cme-mec.ca

Opportunities• Challenges = New Business Opportunities

– Changing customer requirements & expectations– Shift in market power & economic growth to emerging economies (China, Asia, Latin America)– New procurement & supply chain requirements = auto, energy, infrastructure, aerospace– An aging population = Productivity, products, services– Energy opportunities = energy efficiency, new processes, nuclear & alternative energy, oil sands

– technologies, services, and manufacturing supply chain– Environmental priorities = clean technologies & services

• Technology Priorities– Energy – Smart grid, energy efficiency– Manufacturing – Auto, agri-food, aerospace, automation, design & engineering, resource

processing– Environment – Clean technologies & services– Health care – Medical technologies & services

• New business opportunities in Ontario, across Canada, North America, and around the world.

www.cme-mec.ca

Critical Questions

• Is manufacturing disappearing?• What are the growth sectors?• What do businesses/industries need to do to

succeed and grow?• What can Durham Region do to promote

economic growth, generate high paying jobs, and sustain a high quality community?

www.cme-mec.ca

Manufacturing in Canada• Companies that produce things = A $540 billion business ($650 billion in 2008)

– 13% of Canada’s GDP (16% in 2005)– 10% of workforce = 1.75 million Canadians (2.4 million in 2005)

• A highly diversified sector • Manufacturing accounts for two-thirds of Canada’s exports• Highly integrated with the US market

– Approximately 50% of Canadian production is exported into or through the United States

– About 40% of manufacturing inputs are imported from the United States• 75% of business sector R&D• 85% of new product commercialization • Canada’s leader in GHG emission reduction (10% reduction since 1990)• The business of manufacturing = A $1.6 trillion business

– Every dollar of output in manufacturing drives $3.25 of total economic activity

www.cme-mec.ca

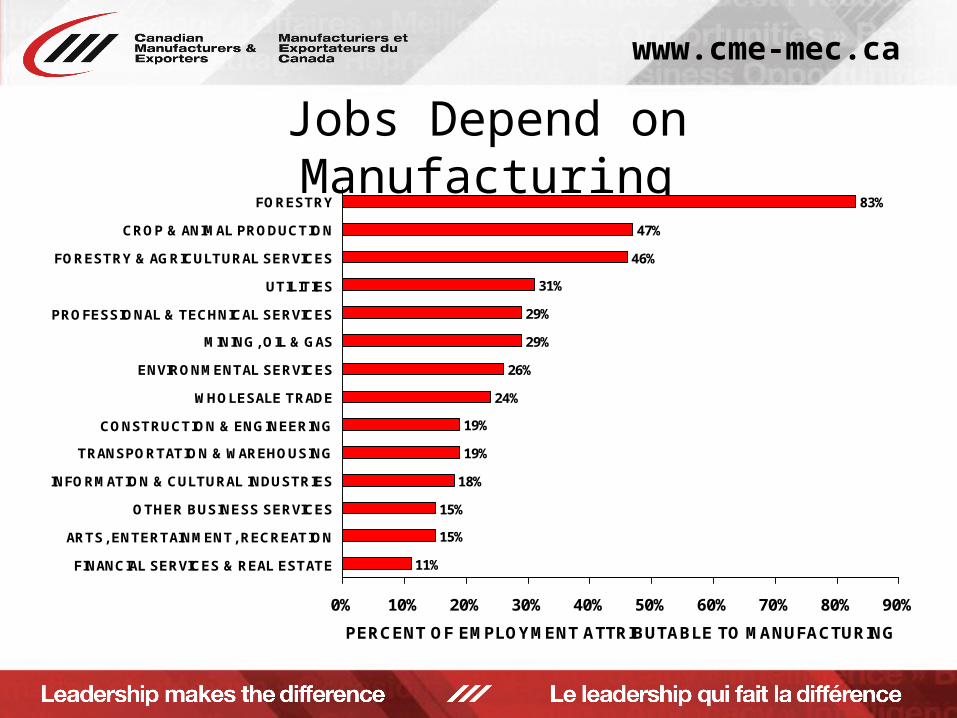

Jobs Depend on Manufacturing83%

47%

46%

31%

29%

29%

26%

24%

19%

19%

18%

15%

15%

11%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

FORESTRY

CROP & ANIMAL PRODUCTION

FORESTRY & AGRICULTURAL SERVICES

UTILITIES

PROFESSIONAL & TECHNICAL SERVICES

MINING, OIL & GAS

ENVIRONMENTAL SERVICES

WHOLESALE TRADE

CONSTRUCTION & ENGINEERING

TRANSPORTATION & WAREHOUSING

INFORMATION & CULTURAL INDUSTRIES

OTHER BUSINESS SERVICES

ARTS, ENTERTAINMENT, RECREATION

FINANCIAL SERVICES & REAL ESTATE

PERCENT OF EMPLOYMENT ATTRIBUTABLE TO MANUFACTURING

www.cme-mec.ca

Manufacturers’ New Orders & Sales

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 201130

35

40

45

50

55

60

Sales New Orders

Billi

ons

of D

olla

rs p

er M

onth

www.cme-mec.ca

Canada’s Merchandise Trade

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 201020

25

30

35

40

45

Total Exports Exports to USA Total Imports

Billi

ons o

f Dol

lars

per

Mon

th

www.cme-mec.ca

Manufacturing Sales(August 2009 – August 2010)

Canada BC Alta Sask Man Ont Que NB NS PEI NL-15

-10

-5

0

5

10

15

10.38.4

13.2

4.3

-3.6

12.7

8.9

6.3

12.3

-9.5-8.0

Year

-ove

r-Yea

r Per

cent

Cha

nge

www.cme-mec.ca

Manufacturing Sales by Sector(August 2009 – August 2010)

Food Products

Beverage & Tobacco Products

Textile Mills

Textile Products

Clothing

Leather Products

Wood Products

Paper

Printing

Petroleum Products

Chemicals

TOTAL MANUFACTURING

-10 -5 0 5 10 15 20 25 30

3.6

3.9

5.6

15.2

16.4

1.2

5.4

13.0

1.7

4.5

8.1

10.3

1.9

0.3

4.0

21.0

25.0

-0.8

-4.3

10.8

-2.3

14.6

4.2

12.7

Ontario

Canada

Year-over-Year Percent Change

www.cme-mec.ca

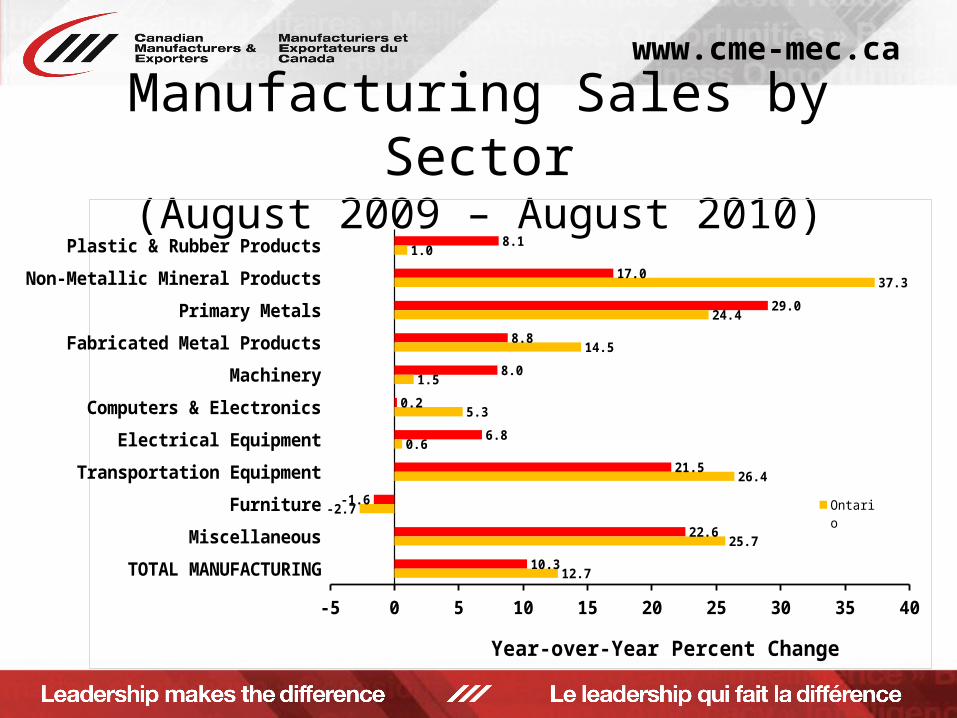

Manufacturing Sales by Sector(August 2009 – August 2010)

Plastic & Rubber Products

Non-Metallic Mineral Products

Primary Metals

Fabricated Metal Products

Machinery

Computers & Electronics

Electrical Equipment

Transportation Equipment

Furniture

Miscellaneous

TOTAL MANUFACTURING

-5 0 5 10 15 20 25 30 35 40

8.1

17.0

29.0

8.8

8.0

0.2

6.8

21.5

-1.6

22.6

10.3

1.0

37.3

24.4

14.5

1.5

5.3

0.6

26.4

-2.7

25.7

12.7

Ontario

Canada

Year-over-Year Percent Change

www.cme-mec.ca

Business as Usual is not an Option• Leadership – New strategies & effective implementation

– Become an integral part of customer/supplier success– Focus on solutions, not products

• New market development – Finding new customers in new supply chains

• Innovation – New & improved solutions, products, services, production and business processes

• Logistics & Supply Chain solutions – Agile, just-when-needed solutions

• Cash Flow – Cash management & financing• LEAN cost reduction – Focus on what customers value & eliminate

waste in business & production processes• Achieving results through people – skills and workforce capabilities

www.cme-mec.ca

Innovation Strategies for Manufacturing• Innovation is a business strategy – and ultimately an investment decision• Drivers of Change

– Challenges = Global competition & commoditization, structural changes– Opportunities = New markets, customers, structural changes

• Objective = Differentiate products as customer solutions• What Manufacturers Need To Do

– Identify problems to solve for customers– Develop & design specialized solutions for customers– New and improved products, services, technologies, services– Work with partners = researchers, suppliers, customers, integrators, services

• Resources = Productive Assets– Knowledge (R&D, Intellectual Property, Knowledge from Extended Networks)– People (Competencies, Techniques, Leadership & Work Practices)– Technology (Materials, Machinery, Equipment, Software)– Money

www.cme-mec.ca

Cash Flow Drives Investment in Research & Development

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009-10

-5

0

5

10

15

20

25

Business Spending on R&D After-Tax Cash Flow

Year

-ove

r-Ye

ar P

erce

nt C

hang

e

www.cme-mec.ca

Cash Flow Drives Investment in New Machinery & Equipment

1980 1985 1990 1995 2000 2005 2010-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

40

Corporate After-Tax Cash Flow Business Investment in Machinery & Equipment

Year

-ove

r-Ye

ar P

erce

nt C

hang

e

www.cme-mec.ca

Technology Investment as a Share of Cash Flow

19791980

19811982

19831984

19851986

19871988

19891990

19911992

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20090

5

10

15

20

25

30

35

40

45

Machinery & Equipment Investment in Current Dollars Machinery & Equipment Investment Adjusted for Price Changes

Perc

ent

of A

fter

-Tax

Cas

h Fl

ow

www.cme-mec.ca

Policy OptionsImpact of Policy

Measure on Cash Flow Examples of Policy Measures

Impacts of 1% Change in Cash Flow on Innovation

Investments resulting from Policy Measures

Increase in Before-Tax Profits

- Harmonization of provincial sales taxes with the GST- Elimination of duties on imported technologies, goods, and services- Reduction in regulatory compliance costs- Subsidies tied to business investment

+ 0.36%

Reduction of Effective Tax Rate on Profits

- Reduction in corporate income tax rate- Elimination of capital taxes + 0.11%

Increase in Capital Cost Allowance - Accelerated depreciation rates + 0.64%

Refundable investment Tax Credit

- Scientific Research & Development Tax Credit- Refundable Investment Tax Credit

+ 3.20%

www.cme-mec.ca

Public Policy Priorities• A manufacturing strategy to boost productivity & growth• Encourage productive investments

– Follow though on commitments to lower corporate income tax rates– Make 2-year write-off for M&E investments permanent– Make SR&ED refundable and improve eligibility requirements– Introduce a training tax credit creditable against EI premiums– Introduce a tax credit for regulatory compliance

• Help businesses find new customers and identify new opportunities to participate in technology development initiatives around the world

• Support the development, commercialization, and adoption of new and improved products and processes

• Strengthen technology transfer to business• Maintain an innovative workforce – math, science, engineering, technical

and workplace competencies, transitional training• Improve the availability of financing for innovation and business growth• Improve the business infrastructure – logistics, Lean regulation

www.cme-mec.ca

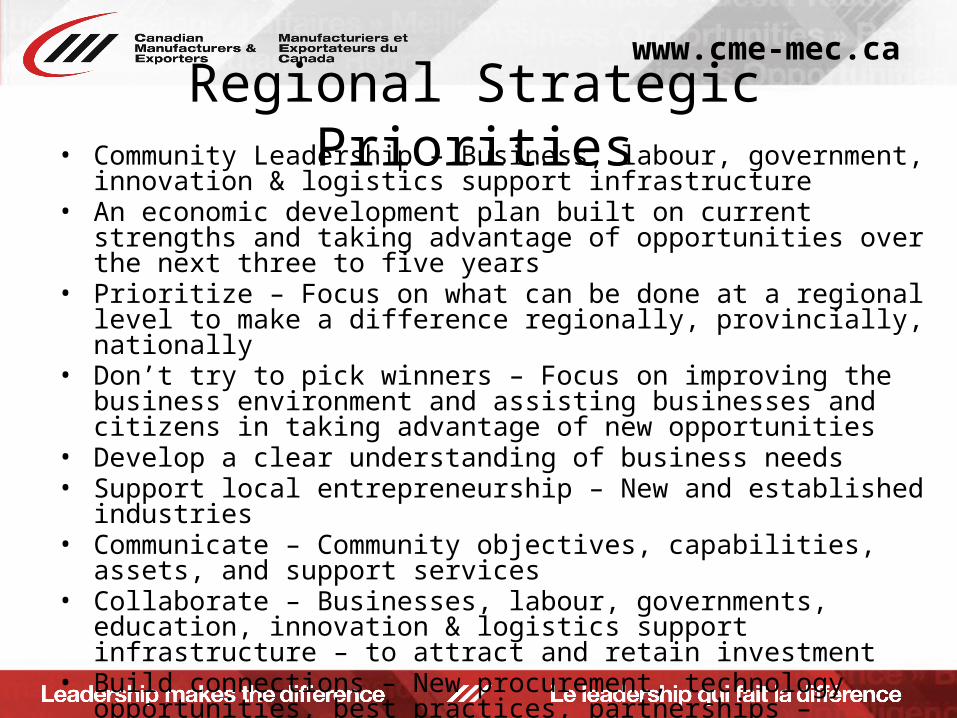

Regional Strategic Priorities• Community Leadership – Business, labour, government, innovation &

logistics support infrastructure• An economic development plan built on current strengths and taking

advantage of opportunities over the next three to five years• Prioritize – Focus on what can be done at a regional level to make a

difference regionally, provincially, nationally• Don’t try to pick winners – Focus on improving the business environment

and assisting businesses and citizens in taking advantage of new opportunities

• Develop a clear understanding of business needs• Support local entrepreneurship – New and established industries• Communicate – Community objectives, capabilities, assets, and support

services• Collaborate – Businesses, labour, governments, education, innovation &

logistics support infrastructure – to attract and retain investment• Build connections – New procurement, technology opportunities, best

practices, partnerships – regional, provincial, national, global• Establish benchmarks and measure progress