Embed Size (px)

Citation preview

Eric Ebersole

This report is published for educational purposes only

for the Roland George Investments Program

1

Industry: Packaged Food

Sector: Consumer Goods

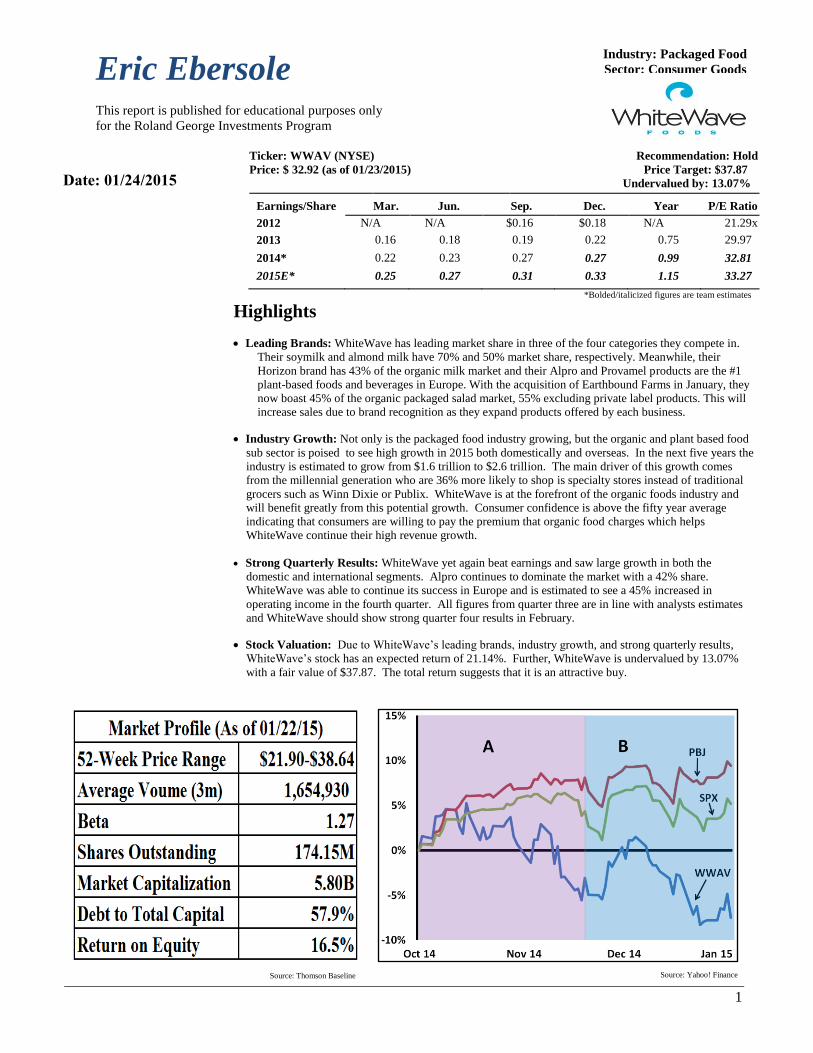

Ticker: WWAV (NYSE) Recommendation: Hold

Price: $ 32.92 (as of 01/23/2015)

Price Target: $37.87

Undervalued by: 13.07%

Earnings/Share Mar. Jun. Sep. Dec. Year P/E Ratio

2012 N/A N/A $0.16 $0.18 N/A

21.29x

2013 0.16 0.18 0.19 0.22 0.75 29.97

2014* 0.22 0.23 0.27 0.27 0.99 32.81

2015E* 0.25 0.27 0.31 0.33 1.15 33.27

*Bolded/italicized figures are team estimates

Highlights

Leading Brands: WhiteWave has leading market share in three of the four categories they compete in.

Their soymilk and almond milk have 70% and 50% market share, respectively. Meanwhile, their

Horizon brand has 43% of the organic milk market and their Alpro and Provamel products are the #1

plant-based foods and beverages in Europe. With the acquisition of Earthbound Farms in January, they

now boast 45% of the organic packaged salad market, 55% excluding private label products. This will

increase sales due to brand recognition as they expand products offered by each business.

Industry Growth: Not only is the packaged food industry growing, but the organic and plant based food

sub sector is poised to see high growth in 2015 both domestically and overseas. In the next five years the

industry is estimated to grow from $1.6 trillion to $2.6 trillion. The main driver of this growth comes

from the millennial generation who are 36% more likely to shop is specialty stores instead of traditional

grocers such as Winn Dixie or Publix. WhiteWave is at the forefront of the organic foods industry and

will benefit greatly from this potential growth. Consumer confidence is above the fifty year average

indicating that consumers are willing to pay the premium that organic food charges which helps

WhiteWave continue their high revenue growth.

Strong Quarterly Results: WhiteWave yet again beat earnings and saw large growth in both the

domestic and international segments. Alpro continues to dominate the market with a 42% share.

WhiteWave was able to continue its success in Europe and is estimated to see a 45% increased in

operating income in the fourth quarter. All figures from quarter three are in line with analysts estimates

and WhiteWave should show strong quarter four results in February.

Stock Valuation: Due to WhiteWave’s leading brands, industry growth, and strong quarterly results,

WhiteWave’s stock has an expected return of 21.14%. Further, WhiteWave is undervalued by 13.07%

with a fair value of $37.87. The total return suggests that it is an attractive buy.

Source: Thomson Baseline

Date: 01/24/2015

Source: Yahoo! Finance

Stetson University Student Research

7/12/201615

2

Business Description

Company: WhiteWave operates in North America and Europe, specializing in plant- based

products, dairy products, coffee creamers and beverages, and fresh and frozen packaged produce.

Their plant-based line include soy, almond, and coconut products sold under through the “Silk”

and “So Delicious Dairy-Free” in North America and the “Alpro” and “Provamel” brands in

Europe. Their coffee creamer and iced coffee brands include International Delight Land O’ Lakes

Half & Half, as well as licensed rights to create creamers for brands such as Dunkin’ Donuts,

Cinnabon, York, and Coldstone Creamery. Their products are sold through grocery retailers and

foodservice distribution channels.

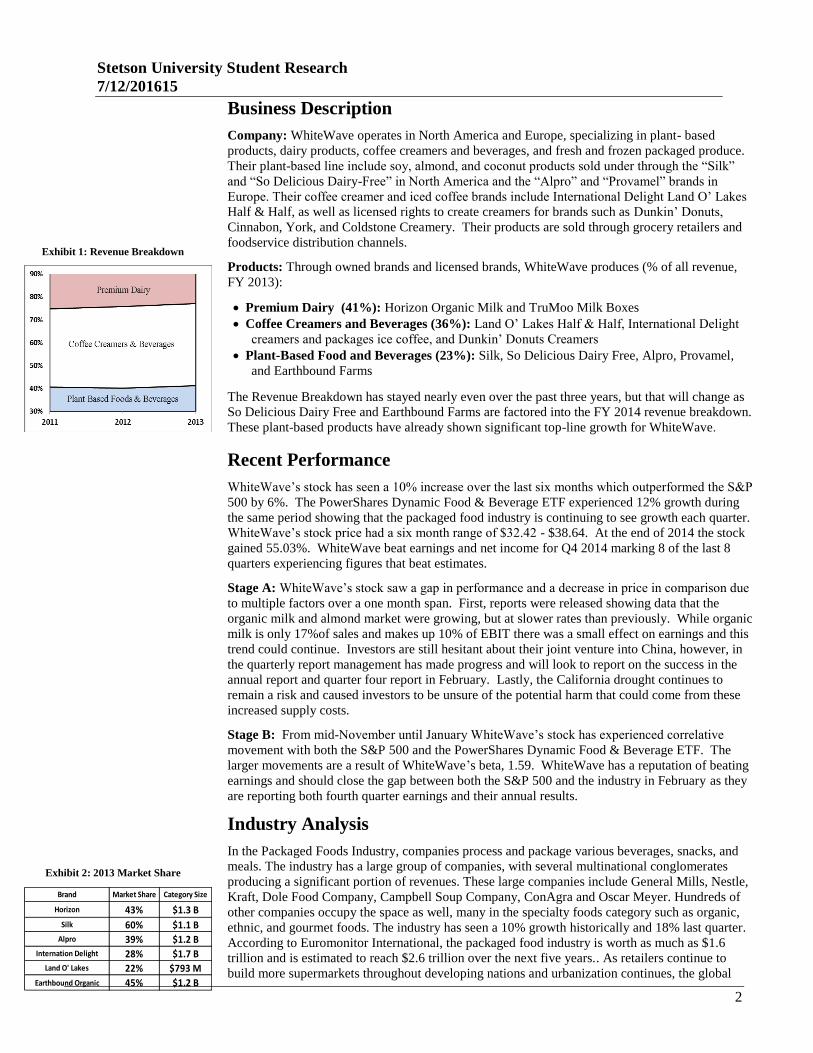

Products: Through owned brands and licensed brands, WhiteWave produces (% of all revenue,

FY 2013):

Premium Dairy (41%): Horizon Organic Milk and TruMoo Milk Boxes

Coffee Creamers and Beverages (36%): Land O’ Lakes Half & Half, International Delight

creamers and packages ice coffee, and Dunkin’ Donuts Creamers

Plant-Based Food and Beverages (23%): Silk, So Delicious Dairy Free, Alpro, Provamel,

and Earthbound Farms

The Revenue Breakdown has stayed nearly even over the past three years, but that will change as

So Delicious Dairy Free and Earthbound Farms are factored into the FY 2014 revenue breakdown.

These plant-based products have already shown significant top-line growth for WhiteWave.

Recent Performance

WhiteWave’s stock has seen a 10% increase over the last six months which outperformed the S&P

500 by 6%. The PowerShares Dynamic Food & Beverage ETF experienced 12% growth during

the same period showing that the packaged food industry is continuing to see growth each quarter.

WhiteWave’s stock price had a six month range of $32.42 - $38.64. At the end of 2014 the stock

gained 55.03%. WhiteWave beat earnings and net income for Q4 2014 marking 8 of the last 8

quarters experiencing figures that beat estimates.

Stage A: WhiteWave’s stock saw a gap in performance and a decrease in price in comparison due

to multiple factors over a one month span. First, reports were released showing data that the

organic milk and almond market were growing, but at slower rates than previously. While organic

milk is only 17%of sales and makes up 10% of EBIT there was a small effect on earnings and this

trend could continue. Investors are still hesitant about their joint venture into China, however, in

the quarterly report management has made progress and will look to report on the success in the

annual report and quarter four report in February. Lastly, the California drought continues to

remain a risk and caused investors to be unsure of the potential harm that could come from these

increased supply costs.

Stage B: From mid-November until January WhiteWave’s stock has experienced correlative

movement with both the S&P 500 and the PowerShares Dynamic Food & Beverage ETF. The

larger movements are a result of WhiteWave’s beta, 1.59. WhiteWave has a reputation of beating

earnings and should close the gap between both the S&P 500 and the industry in February as they

are reporting both fourth quarter earnings and their annual results.

Industry Analysis

In the Packaged Foods Industry, companies process and package various beverages, snacks, and

meals. The industry has a large group of companies, with several multinational conglomerates

producing a significant portion of revenues. These large companies include General Mills, Nestle,

Kraft, Dole Food Company, Campbell Soup Company, ConAgra and Oscar Meyer. Hundreds of

other companies occupy the space as well, many in the specialty foods category such as organic,

ethnic, and gourmet foods. The industry has seen a 10% growth historically and 18% last quarter.

According to Euromonitor International, the packaged food industry is worth as much as $1.6

trillion and is estimated to reach $2.6 trillion over the next five years.. As retailers continue to

build more supermarkets throughout developing nations and urbanization continues, the global

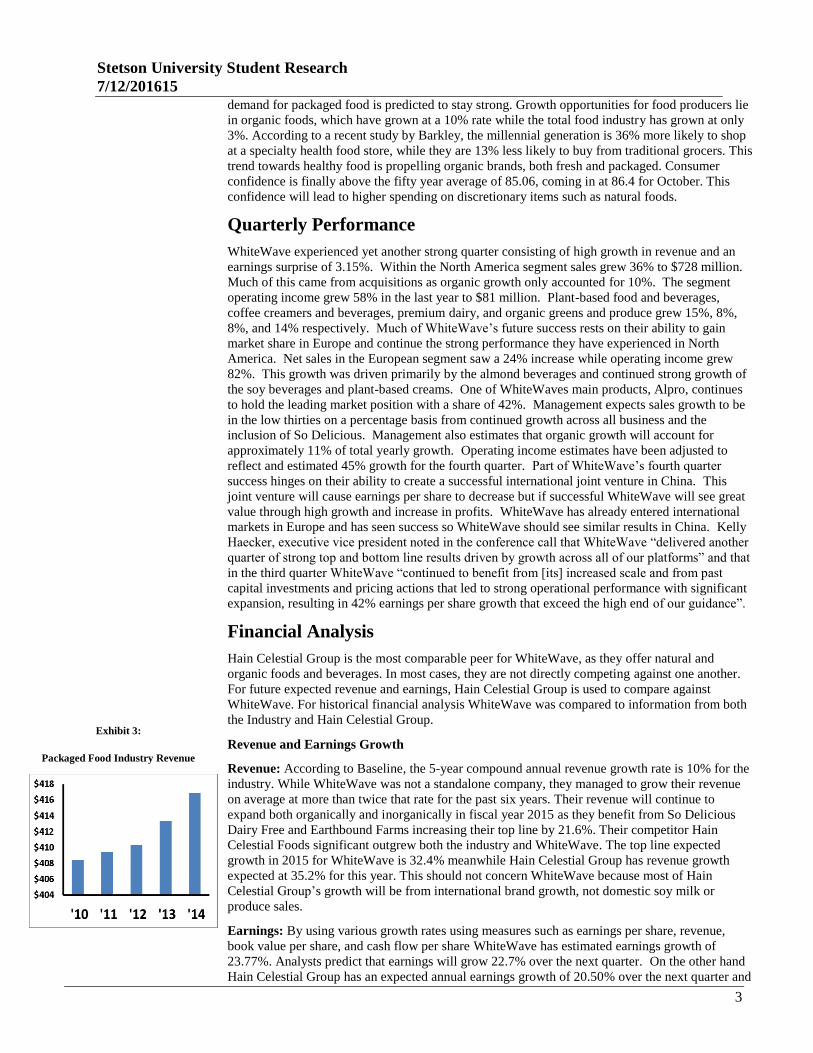

Brand Market Share Category Size

Horizon 43% $1.3 B

Silk 60% $1.1 BAlpro 39% $1.2 B

Internation Delight 28% $1.7 BLand O' Lakes 22% $793 M

Earthbound Organic 45% $1.2 B

Exhibit 1: Revenue Breakdown

Exhibit 2: 2013 Market Share

Stetson University Student Research

7/12/201615

3

demand for packaged food is predicted to stay strong. Growth opportunities for food producers lie

in organic foods, which have grown at a 10% rate while the total food industry has grown at only

3%. According to a recent study by Barkley, the millennial generation is 36% more likely to shop

at a specialty health food store, while they are 13% less likely to buy from traditional grocers. This

trend towards healthy food is propelling organic brands, both fresh and packaged. Consumer

confidence is finally above the fifty year average of 85.06, coming in at 86.4 for October. This

confidence will lead to higher spending on discretionary items such as natural foods.

Quarterly Performance

WhiteWave experienced yet another strong quarter consisting of high growth in revenue and an

earnings surprise of 3.15%. Within the North America segment sales grew 36% to $728 million.

Much of this came from acquisitions as organic growth only accounted for 10%. The segment

operating income grew 58% in the last year to $81 million. Plant-based food and beverages,

coffee creamers and beverages, premium dairy, and organic greens and produce grew 15%, 8%,

8%, and 14% respectively. Much of WhiteWave’s future success rests on their ability to gain

market share in Europe and continue the strong performance they have experienced in North

America. Net sales in the European segment saw a 24% increase while operating income grew

82%. This growth was driven primarily by the almond beverages and continued strong growth of

the soy beverages and plant-based creams. One of WhiteWaves main products, Alpro, continues

to hold the leading market position with a share of 42%. Management expects sales growth to be

in the low thirties on a percentage basis from continued growth across all business and the

inclusion of So Delicious. Management also estimates that organic growth will account for

approximately 11% of total yearly growth. Operating income estimates have been adjusted to

reflect and estimated 45% growth for the fourth quarter. Part of WhiteWave’s fourth quarter

success hinges on their ability to create a successful international joint venture in China. This

joint venture will cause earnings per share to decrease but if successful WhiteWave will see great

value through high growth and increase in profits. WhiteWave has already entered international

markets in Europe and has seen success so WhiteWave should see similar results in China. Kelly

Haecker, executive vice president noted in the conference call that WhiteWave “delivered another

quarter of strong top and bottom line results driven by growth across all of our platforms” and that

in the third quarter WhiteWave “continued to benefit from [its] increased scale and from past

capital investments and pricing actions that led to strong operational performance with significant

expansion, resulting in 42% earnings per share growth that exceed the high end of our guidance”.

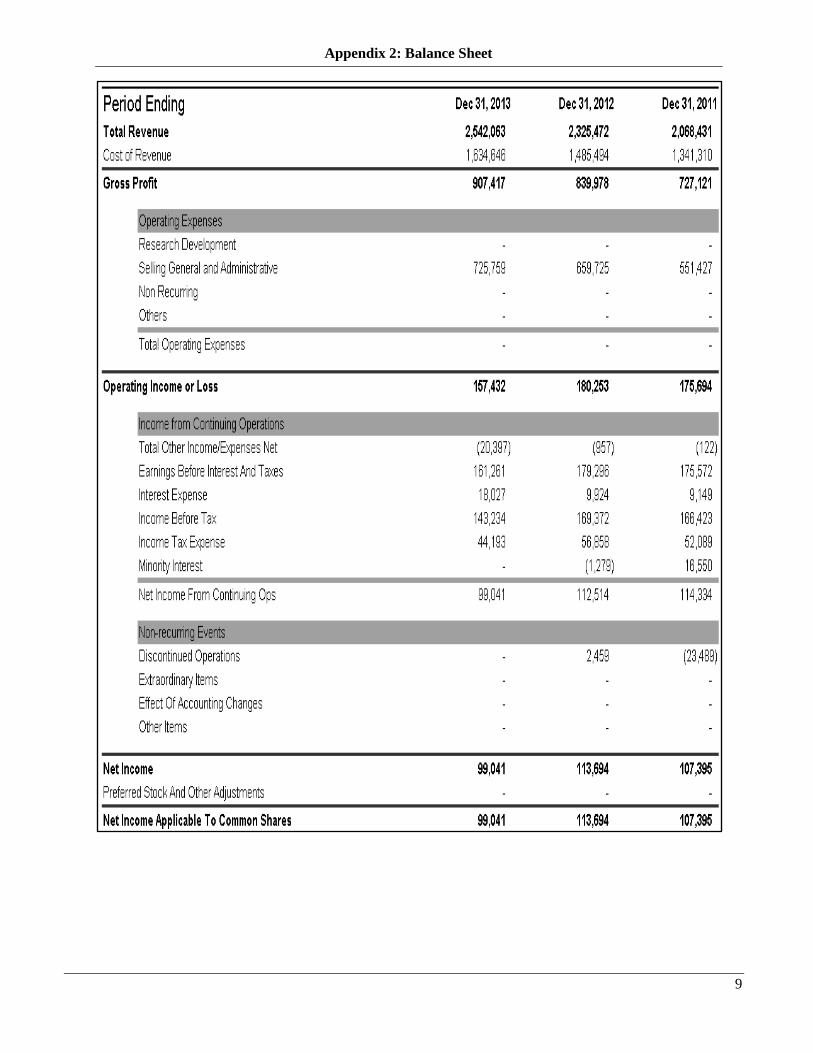

Financial Analysis

Hain Celestial Group is the most comparable peer for WhiteWave, as they offer natural and

organic foods and beverages. In most cases, they are not directly competing against one another.

For future expected revenue and earnings, Hain Celestial Group is used to compare against

WhiteWave. For historical financial analysis WhiteWave was compared to information from both

the Industry and Hain Celestial Group.

Revenue and Earnings Growth

Revenue: According to Baseline, the 5-year compound annual revenue growth rate is 10% for the

industry. While WhiteWave was not a standalone company, they managed to grow their revenue

on average at more than twice that rate for the past six years. Their revenue will continue to

expand both organically and inorganically in fiscal year 2015 as they benefit from So Delicious

Dairy Free and Earthbound Farms increasing their top line by 21.6%. Their competitor Hain

Celestial Foods significant outgrew both the industry and WhiteWave. The top line expected

growth in 2015 for WhiteWave is 32.4% meanwhile Hain Celestial Group has revenue growth

expected at 35.2% for this year. This should not concern WhiteWave because most of Hain

Celestial Group’s growth will be from international brand growth, not domestic soy milk or

produce sales.

Earnings: By using various growth rates using measures such as earnings per share, revenue,

book value per share, and cash flow per share WhiteWave has estimated earnings growth of

23.77%. Analysts predict that earnings will grow 22.7% over the next quarter. On the other hand

Hain Celestial Group has an expected annual earnings growth of 20.50% over the next quarter and

Exhibit 3:

Packaged Food Industry Revenue

Stetson University Student Research

7/12/201615

4

14.10% for the full year. Over the last year WhiteWave had bottom line growth of over 58% while

Hain Celestial’s bottom line decreased.

Profitability

Profit Margin: The average profit margin of WhiteWave over the past six quarters is 4.09%,

whereas the average profit margin of Hain Celestial Group is 5.75%. This is surprising because the

gross margin for WhiteWave is significantly higher than Hain Celestial. The packaged food and

meats industry profit margin is 7.26%, while WhiteWave’s current net profit margin is 3.9%. The

lower profit margins can be attributed to the high interest expenses and SG&A expenses incurred

by WhiteWave as they break away from Dean Foods and develop their businesses. Being a

relatively young company, they have incurred higher expenses for advertising, developing their

supply chain, and building facilities. As the company grows, they expect to reduce their operating

expenses as a percentage of revenue, which will lead the way to higher profit margins. WhiteWave

has also taken losses on several divestures and disposals as their work to focus their business

model. As they mature as a company, WhiteWave should see their operating expenses go down

and they will reap the benefits of the high gross margin for dairy alternatives.

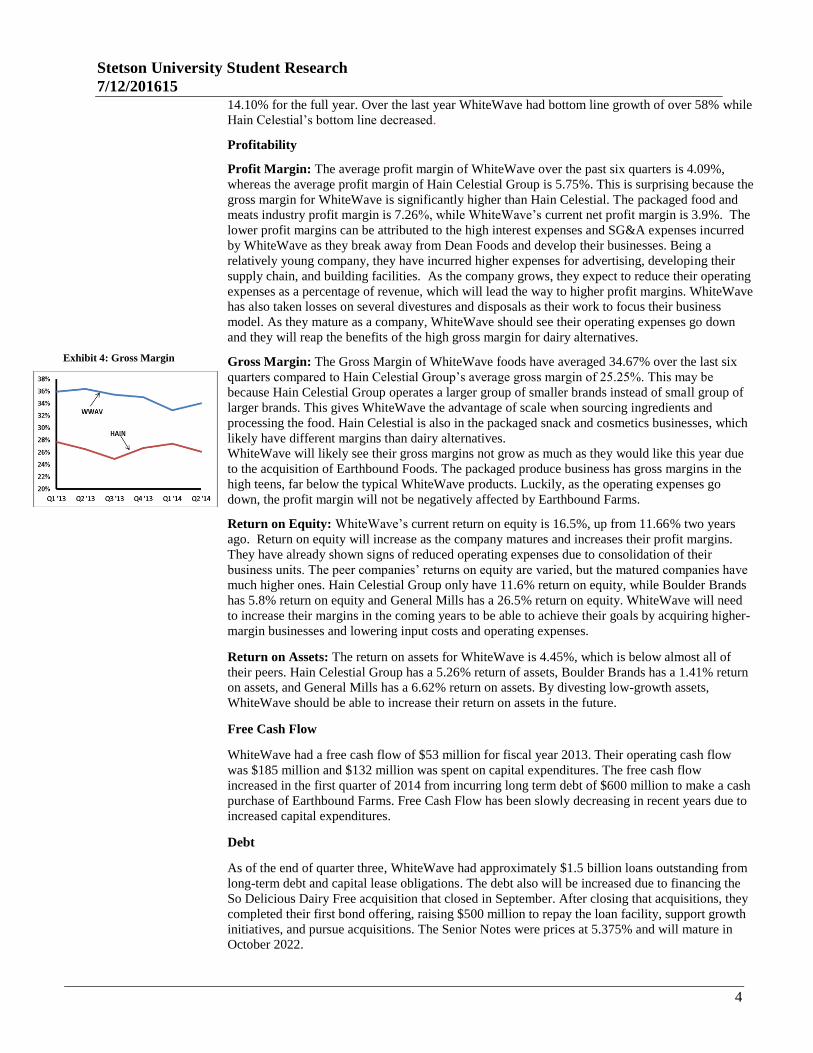

Gross Margin: The Gross Margin of WhiteWave foods have averaged 34.67% over the last six

quarters compared to Hain Celestial Group’s average gross margin of 25.25%. This may be

because Hain Celestial Group operates a larger group of smaller brands instead of small group of

larger brands. This gives WhiteWave the advantage of scale when sourcing ingredients and

processing the food. Hain Celestial is also in the packaged snack and cosmetics businesses, which

likely have different margins than dairy alternatives.

WhiteWave will likely see their gross margins not grow as much as they would like this year due

to the acquisition of Earthbound Foods. The packaged produce business has gross margins in the

high teens, far below the typical WhiteWave products. Luckily, as the operating expenses go

down, the profit margin will not be negatively affected by Earthbound Farms.

Return on Equity: WhiteWave’s current return on equity is 16.5%, up from 11.66% two years

ago. Return on equity will increase as the company matures and increases their profit margins.

They have already shown signs of reduced operating expenses due to consolidation of their

business units. The peer companies’ returns on equity are varied, but the matured companies have

much higher ones. Hain Celestial Group only have 11.6% return on equity, while Boulder Brands

has 5.8% return on equity and General Mills has a 26.5% return on equity. WhiteWave will need

to increase their margins in the coming years to be able to achieve their goals by acquiring higher-

margin businesses and lowering input costs and operating expenses.

Return on Assets: The return on assets for WhiteWave is 4.45%, which is below almost all of

their peers. Hain Celestial Group has a 5.26% return of assets, Boulder Brands has a 1.41% return

on assets, and General Mills has a 6.62% return on assets. By divesting low-growth assets,

WhiteWave should be able to increase their return on assets in the future.

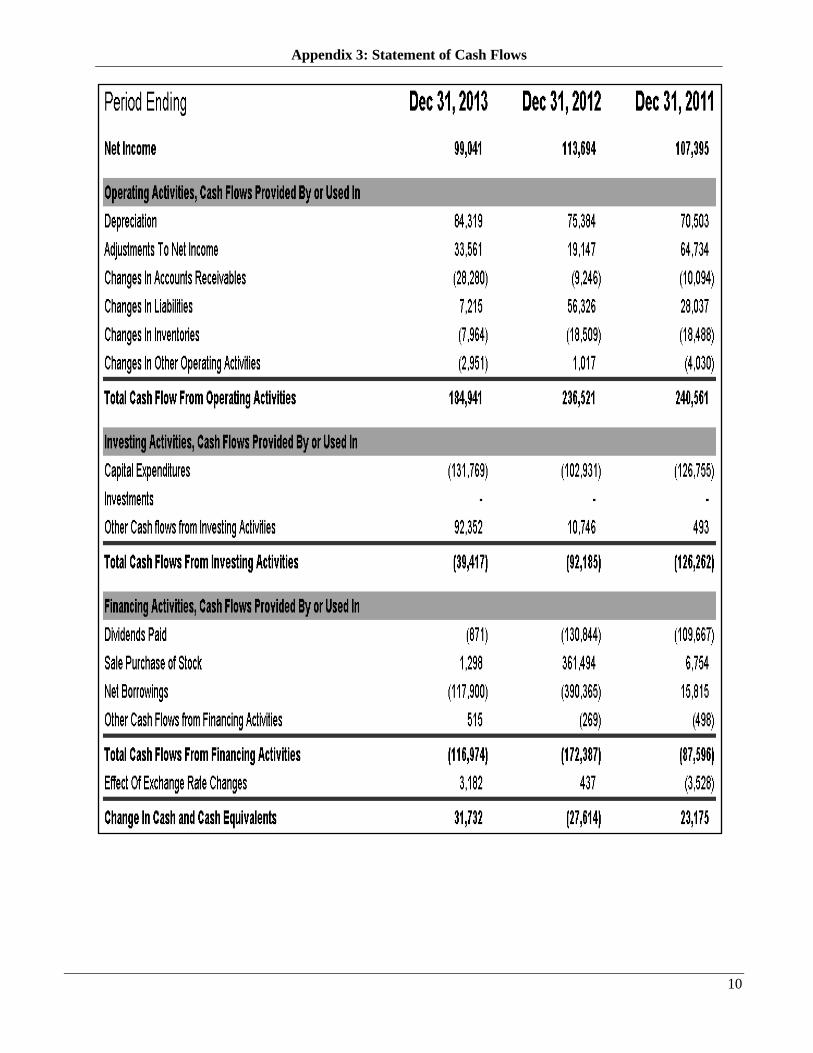

Free Cash Flow

WhiteWave had a free cash flow of $53 million for fiscal year 2013. Their operating cash flow

was $185 million and $132 million was spent on capital expenditures. The free cash flow

increased in the first quarter of 2014 from incurring long term debt of $600 million to make a cash

purchase of Earthbound Farms. Free Cash Flow has been slowly decreasing in recent years due to

increased capital expenditures.

Debt

As of the end of quarter three, WhiteWave had approximately $1.5 billion loans outstanding from

long-term debt and capital lease obligations. The debt also will be increased due to financing the

So Delicious Dairy Free acquisition that closed in September. After closing that acquisitions, they

completed their first bond offering, raising $500 million to repay the loan facility, support growth

initiatives, and pursue acquisitions. The Senior Notes were prices at 5.375% and will mature in

October 2022.

Exhibit 4: Gross Margin

Stetson University Student Research

7/12/201615

5

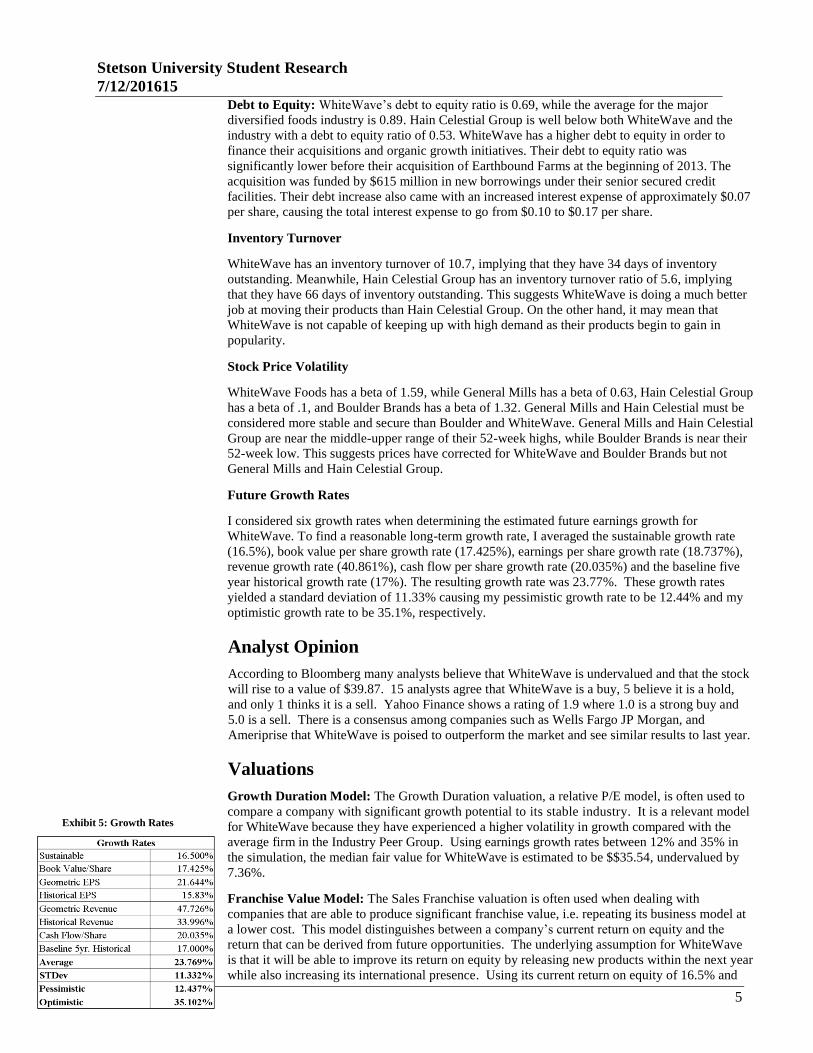

Debt to Equity: WhiteWave’s debt to equity ratio is 0.69, while the average for the major

diversified foods industry is 0.89. Hain Celestial Group is well below both WhiteWave and the

industry with a debt to equity ratio of 0.53. WhiteWave has a higher debt to equity in order to

finance their acquisitions and organic growth initiatives. Their debt to equity ratio was

significantly lower before their acquisition of Earthbound Farms at the beginning of 2013. The

acquisition was funded by $615 million in new borrowings under their senior secured credit

facilities. Their debt increase also came with an increased interest expense of approximately $0.07

per share, causing the total interest expense to go from $0.10 to $0.17 per share.

Inventory Turnover

WhiteWave has an inventory turnover of 10.7, implying that they have 34 days of inventory

outstanding. Meanwhile, Hain Celestial Group has an inventory turnover ratio of 5.6, implying

that they have 66 days of inventory outstanding. This suggests WhiteWave is doing a much better

job at moving their products than Hain Celestial Group. On the other hand, it may mean that

WhiteWave is not capable of keeping up with high demand as their products begin to gain in

popularity.

Stock Price Volatility

WhiteWave Foods has a beta of 1.59, while General Mills has a beta of 0.63, Hain Celestial Group

has a beta of .1, and Boulder Brands has a beta of 1.32. General Mills and Hain Celestial must be

considered more stable and secure than Boulder and WhiteWave. General Mills and Hain Celestial

Group are near the middle-upper range of their 52-week highs, while Boulder Brands is near their

52-week low. This suggests prices have corrected for WhiteWave and Boulder Brands but not

General Mills and Hain Celestial Group.

Future Growth Rates

I considered six growth rates when determining the estimated future earnings growth for

WhiteWave. To find a reasonable long-term growth rate, I averaged the sustainable growth rate

(16.5%), book value per share growth rate (17.425%), earnings per share growth rate (18.737%),

revenue growth rate (40.861%), cash flow per share growth rate (20.035%) and the baseline five

year historical growth rate (17%). The resulting growth rate was 23.77%. These growth rates

yielded a standard deviation of 11.33% causing my pessimistic growth rate to be 12.44% and my

optimistic growth rate to be 35.1%, respectively.

Analyst Opinion

According to Bloomberg many analysts believe that WhiteWave is undervalued and that the stock

will rise to a value of $39.87. 15 analysts agree that WhiteWave is a buy, 5 believe it is a hold,

and only 1 thinks it is a sell. Yahoo Finance shows a rating of 1.9 where 1.0 is a strong buy and

5.0 is a sell. There is a consensus among companies such as Wells Fargo JP Morgan, and

Ameriprise that WhiteWave is poised to outperform the market and see similar results to last year.

Valuations

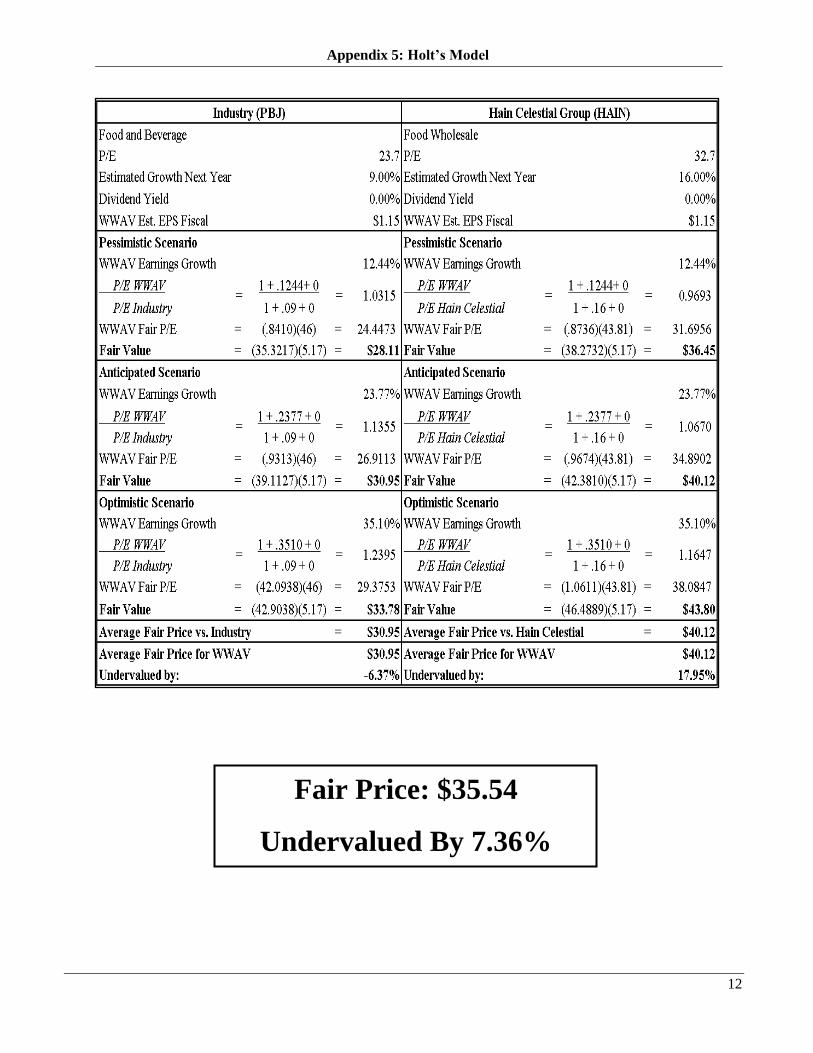

Growth Duration Model: The Growth Duration valuation, a relative P/E model, is often used to

compare a company with significant growth potential to its stable industry. It is a relevant model

for WhiteWave because they have experienced a higher volatility in growth compared with the

average firm in the Industry Peer Group. Using earnings growth rates between 12% and 35% in

the simulation, the median fair value for WhiteWave is estimated to be $$35.54, undervalued by

7.36%.

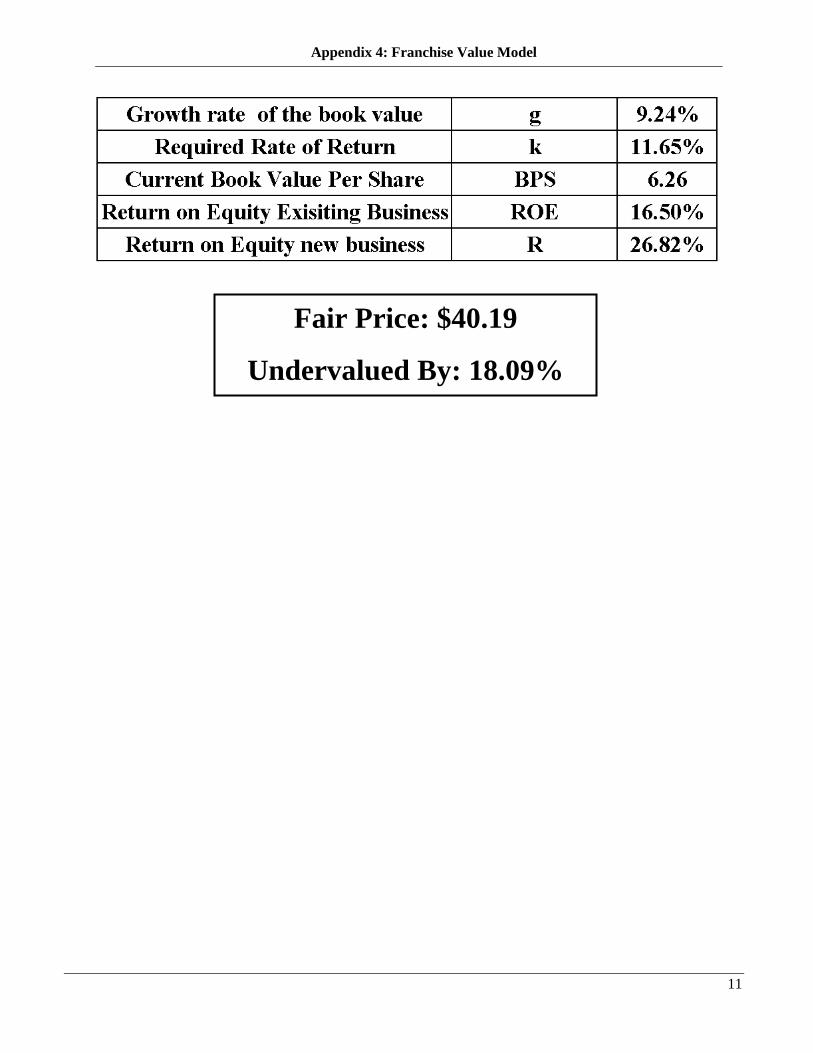

Franchise Value Model: The Sales Franchise valuation is often used when dealing with

companies that are able to produce significant franchise value, i.e. repeating its business model at

a lower cost. This model distinguishes between a company’s current return on equity and the

return that can be derived from future opportunities. The underlying assumption for WhiteWave

is that it will be able to improve its return on equity by releasing new products within the next year

while also increasing its international presence. Using its current return on equity of 16.5% and

Exhibit 5: Growth Rates

Stetson University Student Research

7/12/201615

6

the return on equity of 26.82%, the median fair value for WhiteWave is forecasted to be $40.19,

undervalued by 18.09%.

Average Fair Value: By averaging the valuation models used, the estimated fair value of

WhiteWave is $37.87, meaning it is undervalued by 13.07%.

Stetson University Student Research

7/12/201615

7

Table of Contents

Appendix 1: Income Statement 7

Appendix 2: Balance Sheet 8

Appendix 3: Statement of Cash Flow 9

Appendix 4: Franchise Value Model 10

Appendix 5: Holt’s Model 11

Appendix 6: Sources and Disclosures 12

8

Appendix 1: Income Statement

9

Appendix 2: Balance Sheet

10

Appendix 3: Statement of Cash Flows

11

Fair Price: $40.19

Undervalued By: 18.09%

Appendix 4: Franchise Value Model

12

Fair Price: $35.54

Undervalued By 7.36%

Appendix 5: Holt’s Model

13

Reuters

Baseline

Bloomberg

Morningstar

Yahoo Finance

Google Finance

Company Website

Quarterly Report 2014 Q3

Disclosures:

Ownership and material conflicts of interest: The author, or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author, or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias

the content or publication of this report.

Receipt of compensation: Compensation of the author of this report is not based on investment banking revenue.

Position as a officer or director: The author, or a member of their household, does not serve as an officer, director or advisory board member of the subject company.

Market making: The author does not act as a market maker in the subject company’s securities.

Disclaimer: The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author to

be reliable, but the author does not make any representation or warranty, express or implied, as to its accuracy or completeness. The

information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security.

Appendix 6: Sources