Embed Size (px)

Citation preview

page 1

WSTA Annual Wine Report

May 2016

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Contents

Champagne and Sparkling, p.14

Foreword, p.4 Wine duty in the UK, p.6

Consumer polling, p.7 Still wine overview, p.8

White, p.10 Red, p.12

Import and export, p.18

Fortified and others, p.16

page 3

About

About us

The WSTA represents over 300 companies producing, importing, exporting, transporting and selling wines and spirits in the United Kingdom.

We campaign for a vibrant and sustainable wine and spirit industry, helping to build a future in which alcohol is produced, sold and enjoyed responsibly.

Methodology

This publication aims to build upon the wine-based information and data in the WSTA Quarterly Market Reports. The most up-to-date data possible has been used and, though the end dates are not consistent across the report, the data is exactly accurate to its source. For example, where the market data for the on and off trade is dated to December 2015 and January 2016 respectively, UK export data is for the entire year of 2015. Premiumisation and other parts of the publication uses IWSR projection data for 2015. All insights and analysis written by WSTA.

Special thanks to:

For more information on data providers and publications they produce for the drinks industry, please contact [email protected].

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Foreword

Welcome to the inaugural edition of the WSTA’s Wine Report. We have brought together data from various sources to give you a broad overview of the market in the UK, which remains one of the world’s most important and diverse markets for wine businesses and consumers alike.

The industry in the UK has faced tough trading conditions for a number of years, particularly due to the tightening of consumer spending. As a mature market there is little room to grow and these factors have led to a slow, consistent decline in volume sales and a rise in consolidation of businesses in the trade.

However, there have been some positive changes for the industry recently. Following the WSTA’s campaigning the alcohol duty escalator was scrapped, ending year on year inflation busting duty rises. In the past two years wine duty has risen at its lowest rates for 13 years helping to save the industry millions in tax liabilities.

The Government is also starting to understand the importance of our work. In February 2016 we hosted the first English wine round table including WSTA members and the Secretary of State for Environment, Food and Rural Affairs, Liz Truss MP. More recently the WSTA also met the Prime Minister to discuss the industry’s capacity to contribute to growing UK exports.

PM invites WSTA to No10 to discuss EU and exports- 23rd March 2016

page 5

Foreword

“It was an incredible honour to be invited to Number 10 and sit at the Cabinet table with the Prime Minister and the Environment Secretary. We were able to share with them our aspirations, experiences of exporting and how with their help we would like to see the industry grow.”

- Tamara Roberts, CEO of Ridgeview, March 2016

Secretary of State (DEFRA) Liz Truss MP visits Bolney Wine Estate- 26th October 2015

Inaugural English Wine Round table, hosted by WSTA- 2nd March 2016

The wine industry faces many imminent challenges; campaigning for a more supportive tax regime, more interaction with government and exploring export opportunities to name just a few. The round table and meeting with the Prime Minister are just the beginning and the WSTA will be working hard to achieve these aims for the benefit of the entire industry.

These are interesting times for the industry and we would like to thank our data providers for helping us to bring together this report. I hope that you find it of interest.

Miles BealeChief Executive

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

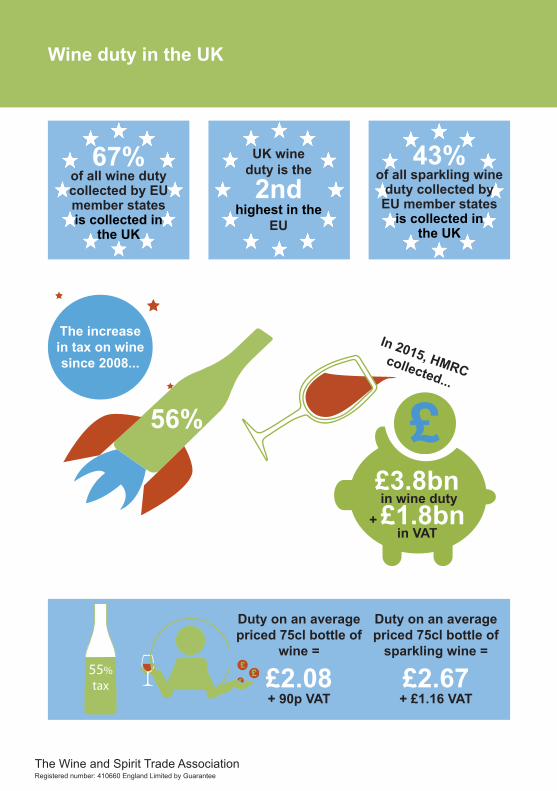

Wine duty in the UK

UK wine duty is the

2nd highest in the

EU

In 2015, HMRC collected...

£3.8bn in wine duty

+ £1.8bn in VAT

Duty on an average priced 75cl bottle of

wine =

£2.08+ 90p VAT

55%tax

Duty on an average priced 75cl bottle of

sparkling wine =

£2.67+ £1.16 VAT

43% of all sparkling wine

duty collected by EU member states

is collected in the UK

67% of all wine duty collected by EU member states is collected in

the UK

56%

The increase in tax on wine since 2008...

page 7

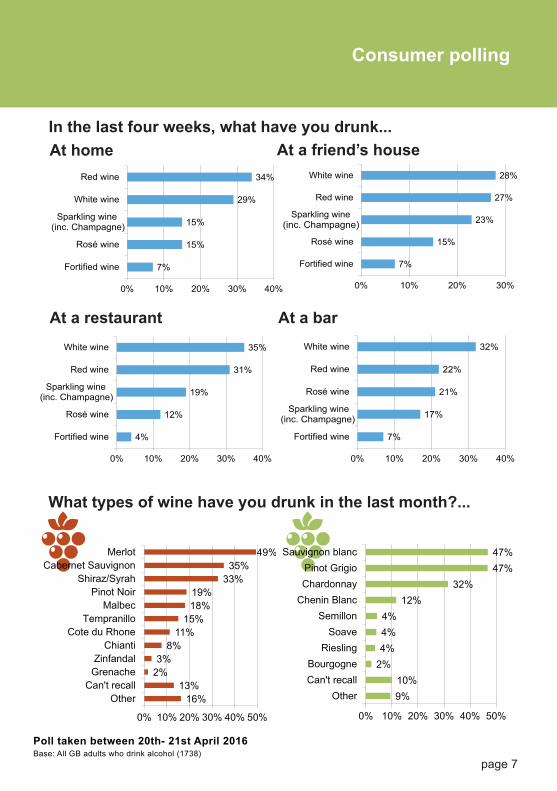

Consumer polling

Base: All GB adults who drink alcohol (1738) Poll taken between 20th- 21st April 2016

What types of wine have you drunk in the last month?...

16%13%

2%3%

8%11%

15%18%19%

33%35%

49%

0% 10% 20% 30% 40% 50%

OtherCan't recall

GrenacheZinfandal

ChiantiCote du Rhone

TempranilloMalbec

Pinot NoirShiraz/Syrah

Cabernet SauvignonMerlot

9%10%

2%4%4%4%

12%32%

47%47%

0% 10% 20% 30% 40% 50%

OtherCan't recallBourgogne

RieslingSoave

SemillonChenin BlancChardonnayPinot Grigio

Sauvignon blanc

In the last four weeks, what have you drunk...

7%

15%

15%

29%

34%

0% 10% 20% 30% 40%

Fortified wine

Rosé wine

Sparkling wine(inc. Champagne)

White wine

Red wine

At home

7%

15%

23%

27%

28%

0% 10% 20% 30%

Fortified wine

Rosé wine

Sparkling wine(inc. Champagne)

Red wine

White wine

At a friend’s house

7%

17%

21%

22%

32%

0% 10% 20% 30% 40%

Fortified wine

Sparkling wine(inc. Champagne)

Rosé wine

Red wine

White wine

At a bar

4%

12%

19%

31%

35%

0% 10% 20% 30% 40%

Fortified wine

Rosé wine

Sparkling wine(inc. Champagne)

Red wine

White wine

At a restaurant

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

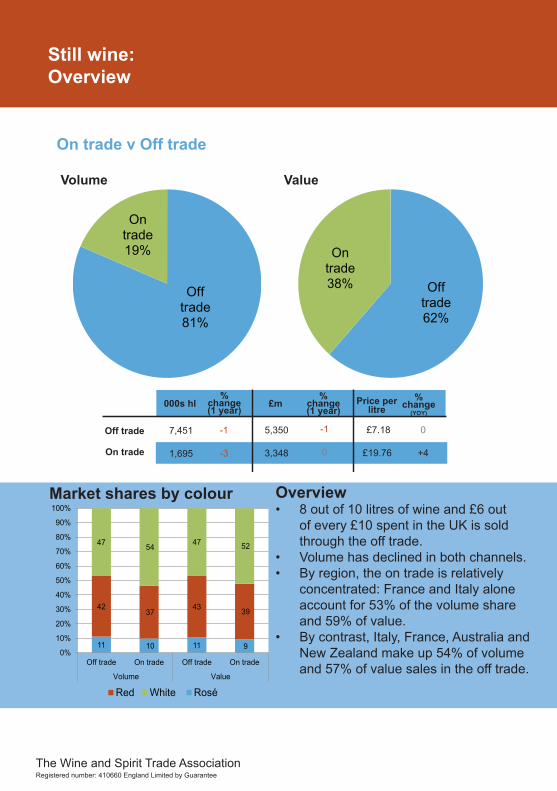

Still wine:Overview

11 10 11 9

4237

43 39

47 54 47 52

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Off trade On trade Off trade On trade

Volume Value

Red White Rosé

Market shares by colour

Off trade81%

On trade19%

Off trade62%

On trade38%

On trade v Off trade

% change (1 year)

% change (1 year)

£m000s hl % change

(YOY)

Price per litre

7,451

1,695

-1

-3

£7.18

£19.76

5,350

3,348

Off trade

On trade

-1

0

0

+4

Overview• 8 out of 10 litres of wine and £6 out

of every £10 spent in the UK is sold through the off trade.

• Volume has declined in both channels.• By region, the on trade is relatively

concentrated: France and Italy alone account for 53% of the volume share and 59% of value.

• By contrast, Italy, France, Australia and New Zealand make up 54% of volume and 57% of value sales in the off trade.

Volume Value

page 9

3%

8%

9%

28%

1%

25%

6%

11%

3%6%

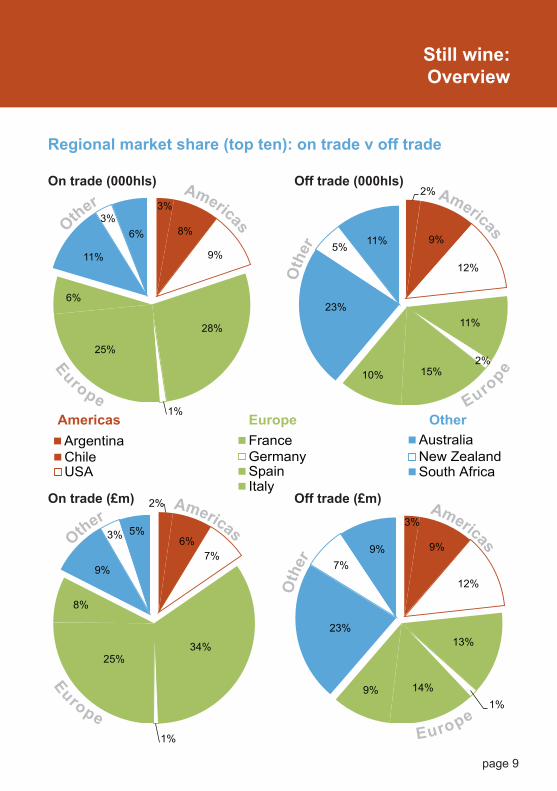

Still wine:Overview

Regional market share (top ten): on trade v off trade

2%

9%

12%

11%

2%15%10%

23%

5% 11%

On trade (000hls) Off trade (000hls)

2%

6%7%

34%

1%

25%

8%

9%

3% 5%3%

9%

12%

13%

1%14%9%

23%

7%9%

ArgentinaChileUSA

FranceGermany

ItalySpain

AustraliaNew ZealandSouth Africa

Americas Europe Other

On trade (£m) Off trade (£m)

Oth

er

Americas

Other

Americas

O

ther Americas

Oth

er

Americas

Europe

EuropeEurope

Euro

pe

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

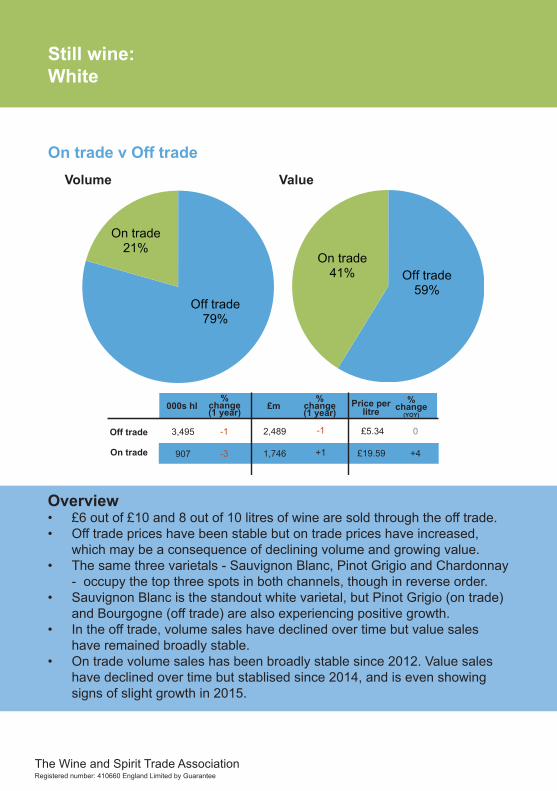

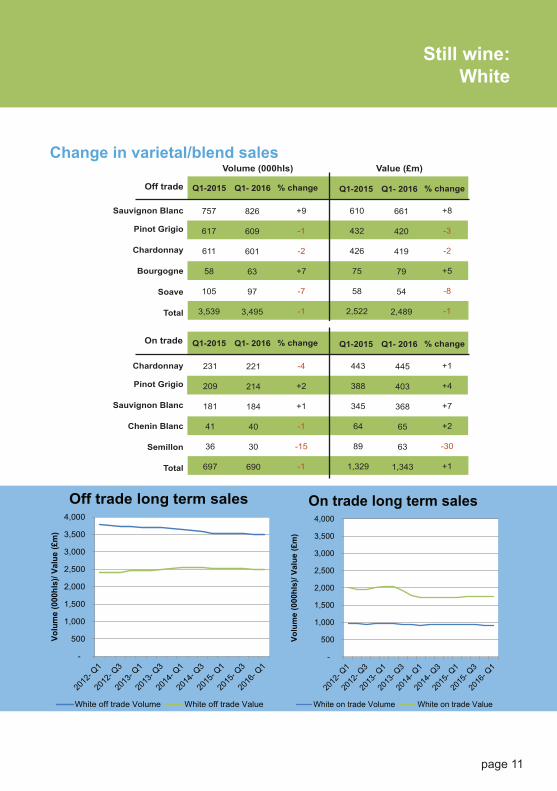

Still wine: White

% change (1 year)

% change (1 year)

£m000s hl % change

(YOY)

Price per litre

3,495

907

-1

-3

£5.34

£19.59

2,489

1,746

Off trade

On trade

-1

+1

0

+4

Value (£m)

Off trade59%

On trade41%

Overview• £6 out of £10 and 8 out of 10 litres of wine are sold through the off trade. • Off trade prices have been stable but on trade prices have increased,

which may be a consequence of declining volume and growing value.• The same three varietals - Sauvignon Blanc, Pinot Grigio and Chardonnay

- occupy the top three spots in both channels, though in reverse order.• Sauvignon Blanc is the standout white varietal, but Pinot Grigio (on trade)

and Bourgogne (off trade) are also experiencing positive growth.• In the off trade, volume sales have declined over time but value sales

have remained broadly stable.• On trade volume sales has been broadly stable since 2012. Value sales

have declined over time but stablised since 2014, and is even showing signs of slight growth in 2015.

On trade v Off tradeVolume Value

Off trade79%

On trade21%

page 11

Still wine: White

white

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Volu

me

(000

hls)

/ Val

ue (£

m)

On trade long term sales

White on trade Volume White on trade Value

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Volu

me

(000

hls)

/ Val

ue (£

m)

Off trade long term sales

White off trade Volume White off trade Value

Q1- 2016Q1-2015

Volume (000hls)

Sauvignon Blanc

Pinot Grigio

Chardonnay

Bourgogne

Soave

Total

Value (£m)

% change Q1- 2016Q1-2015 % change

+9

-1

-2

+7

-7

-1

610

432

426

75

58

2,522

661

420

419

79

54

2,489

+8

-3

-2

+5

-8

-1

757

617

611

58

105

3,539

826

609

601

63

97

3,495

Off trade

Change in varietal/blend sales

Q1- 2016Q1-2015

Chardonnay

Pinot Grigio

Sauvignon Blanc

Chenin Blanc

Semillon

Total

% change Q1- 2016Q1-2015 % change

-4

+2

+1

-1

-15

-1

443

388

345

64

89

1,329

445

403

368

65

63

1,343

+1

+4

+7

+2

-30

+1

231

209

181

41

36

697

221

214

184

40

30

690

On trade

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Still wine: Red

% change (1 year)

% change (1 year)

£m000s hl % change

(YOY)

Price per litre

3,123

620

-1

-4

£5.51

£20.81

2,295

1,290

Off trade

On trade

0

+1

+1

+5

On trade17%

Off trade83%

On trade36%

Off trade64%

Overview• The off trade dominance is more pronounced in red wine than in white,

occupying more of the market share in both volume (+4%) and value (+5%) sales.

• As with much of the category,prices have increased in the last year, especially in the on trade.

• The top two spots are occupiued by the same two varietals, Merlot and Shiraz, in both the on and off trade.

• The on trade is a very concentrated market by country of origin (see p.9) but also by red varietal/blend. Merlot dominates the on trade, occupying a 46% volume share of the top five varietals (in the off trade Merlot has 15% of the market share). Given its market share, Merlot may be a key indicator of red’s overall decline.

On trade v Off tradeVolume Value

page 13

Still wine:Red

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

Volu

me

(000

hls)

/ Val

ue (£

m)

On trade long term sales

Red on trade Volume Red on trade Value

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Volu

me

(000

hls)

/ Val

ue (£

m)

Off trade long term sales

Red off trade Volume Red off trade Value

Change in varietal/blend sales

Q1- 2016Q1-2015

Volume (000hls)

Merlot

Shiraz

Tempranillo

Cabernet Sauvignon

Rhone

Total

Value (£m)

% change Q1- 2016Q1-2015 % change

+9

+9

+2

-2

0

-1

292

266

204

184

115

2,522

315

290

213

179

119

2,489

+8

+9

+5

-3

+4

-1

416

381

242

250

126

3,142

454

414

248

245

126

3,123

Off trade

Q1- 2016Q1-2015

Merlot

Shiraz

Cabernet Sauvignon

Zinfandel

Pinot Noir

Total

% change Q1- 2016Q1-2015 % change

-3

-9

-10

-6

+3

-5

462

129

140

110

107

947

452

123

129

106

114

924

-2

-5

-8

-4

+7

-2

228

77

73

62

52

492

221

70

66

58

54

469

On trade

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

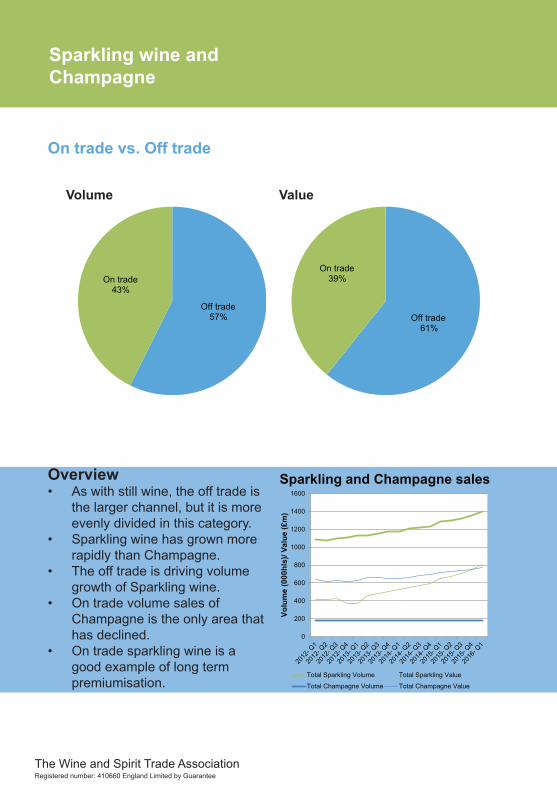

Sparkling wine andChampagne

Overview• As with still wine, the off trade is

the larger channel, but it is more evenly divided in this category.

• Sparkling wine has grown more rapidly than Champagne.

• The off trade is driving volume growth of Sparkling wine.

• On trade volume sales of Champagne is the only area that has declined.

• On trade sparkling wine is a good example of long term premiumisation.

Off trade61%

On trade39%

On trade vs. Off trade

0

200

400

600

800

1000

1200

1400

1600

Volu

me

(000

hls)

/ Val

ue (£

m)

Sparkling and Champagne sales

Total Sparkling Volume Total Sparkling Value

Total Champagne Volume Total Champagne Value

Off trade57%

On trade43%

Volume Value

page 15

Sparkling wine andChampagne

-

100

200

300

400

500

600

700

800

900

Vlou

me

(000

hls)

/ Val

ue (£

m)

Sparkling wine sales

Off trade Volume Off trade Value

On trade Volume On trade Value

-

50

100

150

200

250

300

350

400

450

500

Volu

me

(000

hls)

/ Val

ue (£

m)

Champagne sales

Off trade Volume Off trade Value

On trade Volume On trade Value

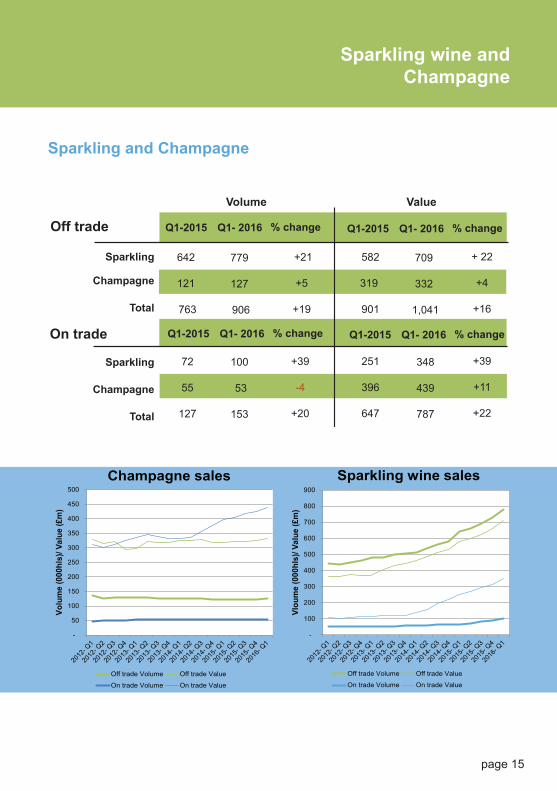

Q1- 2016Q1-2015

Volume

Sparkling

Champagne

Total

On trade

Sparkling

Champagne

Total

Value

% change Q1- 2016Q1-2015 % change

+21

+5

+19

+39

-4

+20

582

319

901

251

396

647

709

332

1,041

348

439

787

+ 22

+4

+16

+39

+11

+22

642

121

763

72

55

127

779

127

906

100

53

153

Off trade

Q1- 2016Q1-2015 % change Q1- 2016Q1-2015 % change

Sparkling and Champagne

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

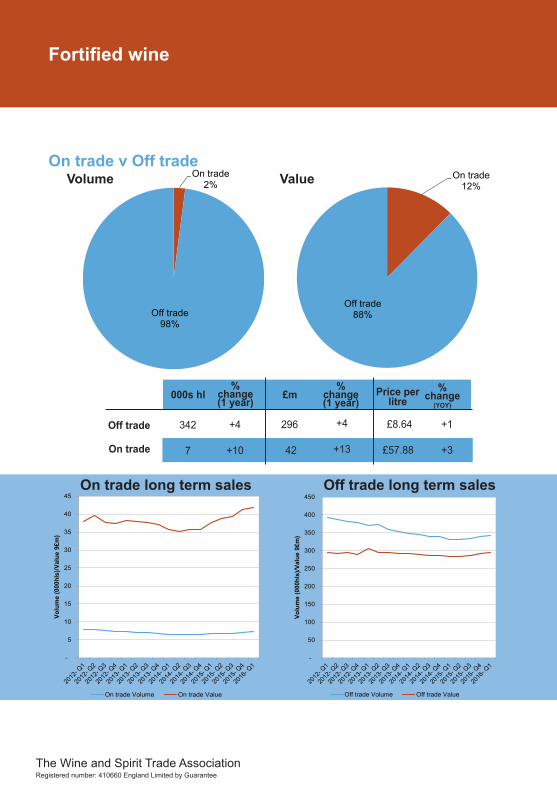

On trade2%

Off trade98%

Fortified wine

On trade12%

Off trade88%

On trade v Off tradeVolume Value

-

50

100

150

200

250

300

350

400

450

Volu

me

(000

hls)

/Val

ue 9

£m)

Off trade Volume Off trade Value

-

5

10

15

20

25

30

35

40

45

Volu

me

(000

hls)

/Val

ue 9

£m)

On trade Volume On trade Value

On trade long term sales Off trade long term sales

% change (1 year)

% change (1 year)

£m000s hl % change

(YOY)

Price per litre

342

7

+4

+10

£8.64

£57.88

296

42

Off trade

On trade

+4

+13

+1

+3

page 17

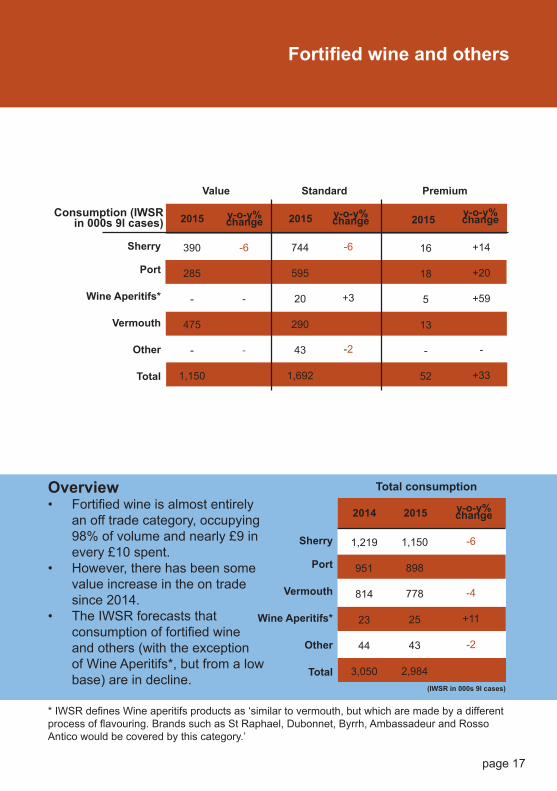

Fortified wine and others

2014

Sherry

Port

Vermouth

Wine Aperitifs*

Other

Total

2015

1,150

898

778

25

43

2,984

-6

-6

-4

+11

-2

-5

1,219

951

814

23

44

3,050

Total consumption

y-o-y% change

(IWSR in 000s 9l cases)

Value

2015

Sherry

Port

Wine Aperitifs*

Vermouth

Other

Total

y-o-y% change 2015 2015

Standard Premium

-6

-5

-

-5

-

-5

744

595

20

290

43

1,692

16

18

5

13

-

52

+14

+20

+59

-68

-

+33

-6

-6

+3

-5

-2

-6

390

285

-

475

-

1,150

Consumption (IWSR in 000s 9l cases)

y-o-y% changey-o-y% change

Overview• Fortified wine is almost entirely

an off trade category, occupying 98% of volume and nearly £9 in every £10 spent.

• However, there has been some value increase in the on trade since 2014.

• The IWSR forecasts that consumption of fortified wine and others (with the exception of Wine Aperitifs*, but from a low base) are in decline.

* IWSR defines Wine aperitifs products as ‘similar to vermouth, but which are made by a different process of flavouring. Brands such as St Raphael, Dubonnet, Byrrh, Ambassadeur and Rosso Antico would be covered by this category.’

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Import and Export:Overview

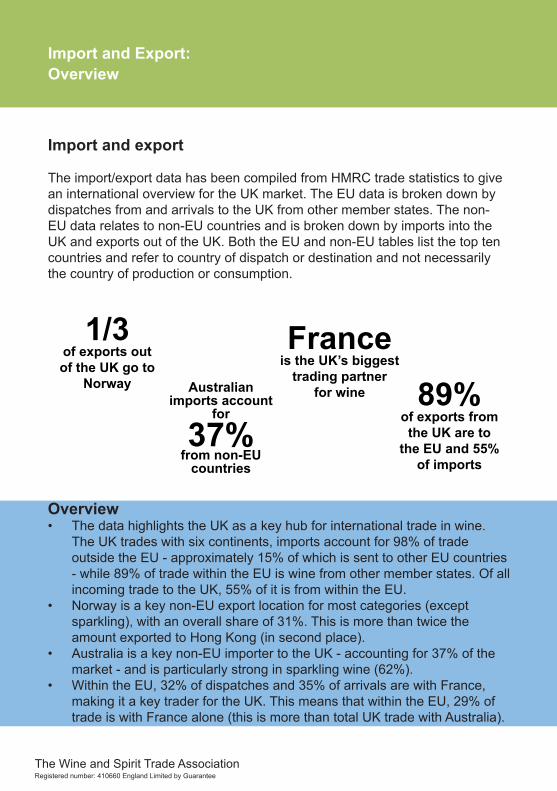

Import and export

The import/export data has been compiled from HMRC trade statistics to give an international overview for the UK market. The EU data is broken down by dispatches from and arrivals to the UK from other member states. The non-EU data relates to non-EU countries and is broken down by imports into the UK and exports out of the UK. Both the EU and non-EU tables list the top ten countries and refer to country of dispatch or destination and not necessarily the country of production or consumption.

Overview• The data highlights the UK as a key hub for international trade in wine.

The UK trades with six continents, imports account for 98% of trade outside the EU - approximately 15% of which is sent to other EU countries - while 89% of trade within the EU is wine from other member states. Of all incoming trade to the UK, 55% of it is from within the EU.

• Norway is a key non-EU export location for most categories (except sparkling), with an overall share of 31%. This is more than twice the amount exported to Hong Kong (in second place).

• Australia is a key non-EU importer to the UK - accounting for 37% of the market - and is particularly strong in sparkling wine (62%).

• Within the EU, 32% of dispatches and 35% of arrivals are with France, making it a key trader for the UK. This means that within the EU, 29% of trade is with France alone (this is more than total UK trade with Australia).

France is the UK’s biggest

trading partner for wine 89%

of exports from the UK are to

the EU and 55% of imports

Australian imports account

for

37%from non-EU

countries

1/3 of exports out of the UK go to

Norway

page 19

Import and Export:All wine

Market Market Share (%)

31

14

8

6

6

4

4

2

2

2

Norway

Hong Kong

Switzerland

USA

Australia

UAE

China

Japan

Singapore

South Africa

1

2

3

4

5

6

7

8

9

10

Non-EU exports from UK in 2015

Total

3,384

1,564

878

650

619

430

396

266

252

228

10,928

Net Mass (000kgs) Market Market

Share (%)

37

17

16

16

9

4

0.1

0.1

0.1

0.04

Australia

USA

Chile

South Africa

New Zealand

Argentina

Canada

Moldova

Lebanon

Israel

1

2

3

4

5

6

7

8

9

10

Non-EU imports to UK in 2015

Total

245,798

109,013

107,959

105,395

59,318

27,313

941

535

428

260

658,196

Net Mass (000kgs)

Market Market Share (%)

32

18

11

10

7

5

4

2

2

2

France

Netherlands

Denmark

Ireland

Sweden

Spain

Germany

Finland

Belgium

Czech Republic

1

2

3

4

5

6

7

8

9

10

Dispatches to EU in 2015

£

Total

30,876

16,984

10,427

9,925

6,618

4,617

4,149

2,348

2,224

1,768

95,270

Net Mass (000kgs) Market Market

Share (%)

38

29

20

8

3

1

0.4

0.4

0.3

0.3

Italy

France

Spain

Germany

Portugal

Hungary

Bulgaria

Romania

Belgium

Netherlands

1

2

3

4

5

6

7

8

9

10

Arrivals from EU in 2015Net Mass (000kgs)

Total

303,709

225,825

154,618

67,072

20,476

5,206

3,205

3,011

2,104

2,070

790,170

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Import and Export:

Market Market Share (%)

30

8

7

7

7

6

4

4

3

3

Norway

Hong Kong

Switzerland

UAE

USA

Australia

New Zealand

Iceland

China

South Korea

1

2

3

4

5

6

7

8

9

10

Non-EU exports from UK in 2015

Total

830

226

199

195

189

162

108

98

73

73

2,810

Net Mass (000kgs) Market Market

Share (%)

35

18

17

17

11

2

0.2

0.1

0.02

0.02

Australia

New Zealand

South Africa

Chile

USA

Argentina

Canada

Moldova

Israel

India

1

2

3

4

5

6

7

8

9

10

Non-EU imports to UK in 2015

Total

107,738

54,266

53,152

52,263

32,752

4,608

739

362

70

55

306,351

Net Mass (000kgs)

Market Market Share (%)

47

15

9

7

4

4

3

2

2

2

France

Netherlands

Ireland

Denmark

Spain

Sweden

Germany

Belgium

Finland

Czech Republic

1

2

3

4

5

6

7

8

9

10

Dispatches to EU in 2015

£

Total

22,917

7,473

4,264

3,387

2,155

2,089

1,493

1,187

932

829

48,911

Net Mass (000kgs) Market Market

Share (%)

46

24

14

13

1

1

1

0.5

0.3

0.2

Italy

France

Germany

Spain

Hungary

Romania

Portugal

Belgium

Bulgaria

Netherlands

1

2

3

4

5

6

7

8

9

10

Arrivals from EU in 2015Net Mass (000kgs)

Total

125,752

65,756

37,509

36,486

3,032

1,825

1,817

1,372

745

429

275,953

White wine

page 21

Import and Export:

Market Market Share (%)

35

17

9

5

4

4

3

2

2

2

Norway

Hong Kong

Switzerland

Australia

USA

China

UAE

South Africa

Japan

Canada

1

2

3

4

5

6

7

8

9

10

Non-EU exports from UK in 2015

Total

2,524

1,207

659

390

309

305

198

163

153

152

7,227

Net Mass (000kgs) Market Market

Share (%)

39

22

16

15

7

1

0.1

0.1

0.1

0.05

Australia

USA

Chile

South Africa

Argentina

New Zealand

Lebanon

Canada

Israel

Moldova

1

2

3

4

5

6

7

8

9

10

Non-EU imports to UK in 2015

Total

135,327

76,002

55,587

51,565

22,668

4,586

375

198

188

173

347,368

Net Mass (000kgs)

Market Market Share (%)

21

17

15

11

10

6

5

3

2

2

Netherlands

France

Denmark

Ireland

Sweden

Germany

Spain

Finland

Belgium

Czech Republic

1

2

3

4

5

6

7

8

9

10

Dispatches to EU in 2015

Total

9,447

7,581

6,906

5,026

4,472

2,625

2,380

1,416

985

828

44,580

Net Mass (000kgs) Market Market

Share (%)

37

28

24

7

1

1

1

0.4

0.3

0.2

France

Italy

Spain

Germany

Portugal

Bulgaria

Hungary

Netherlands

Romania

Belgium

1

2

3

4

5

6

7

8

9

10

Arrivals from EU in 2015

Total

130,880

97,949

82,954

24,299

4,716

2,461

2,069

1,322

1,183

577

349,903

Net Mass (000kgs)

Red wine

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

Import and Export:Sparkling

Market Market Share (%)

Net Mass (000kgs)

18

15

11

7

6

4

4

3

3

3

USA

Hong Kong

Singapore

Australia

Japan

South Korea

Uae

South Africa

Brazil

Egypt

1

2

3

4

5

6

7

8

9

10

Non-EU exports from UK in 2015

Total

148

126

90

62

47

36

33

29

22

22

833

Market Market Share (%)

62

15

11

6

2

1

1

1

0.4

0.3

Australia

South Africa

New Zealand

USA

Chile

UAE

Switzerland

Argentina

Brazil

Hong Kong

1

2

3

4

5

6

7

8

9

10

Non-EU imports to UK in 2015

Total

2,733

677

465

257

108

48

40

36

17

11

4,416

Net Mass (000kgs)

Market Market Share (%)

37

19

8

7

5

4

4

4

3

2

Irish Republic

France

Italy

Denmark

Spain

Sweden

Belgium

Portugal

Czech Republic

Netherlands

1

2

3

4

5

6

7

8

9

10

Dispatches to EU in 2015

£

Total

506

260

104

97

73

57

51

50

43

31

1,355

Net Mass (000kgs) Market Market

Share (%)

56

21

20

3

0.2

0.1

0.1

0.04

0.02

0.02

Italy

France

Spain

Germany

Netherlands

Belgium

Hungary

Lithuania

Irish Republic

Portugal

1

2

3

4

5

6

7

8

9

10

Arrivals from EU in 2015

Total

79,749

29,092

28,026

4,102

307

156

105

58

28

25

141,695

Net Mass (000kgs)

page 23

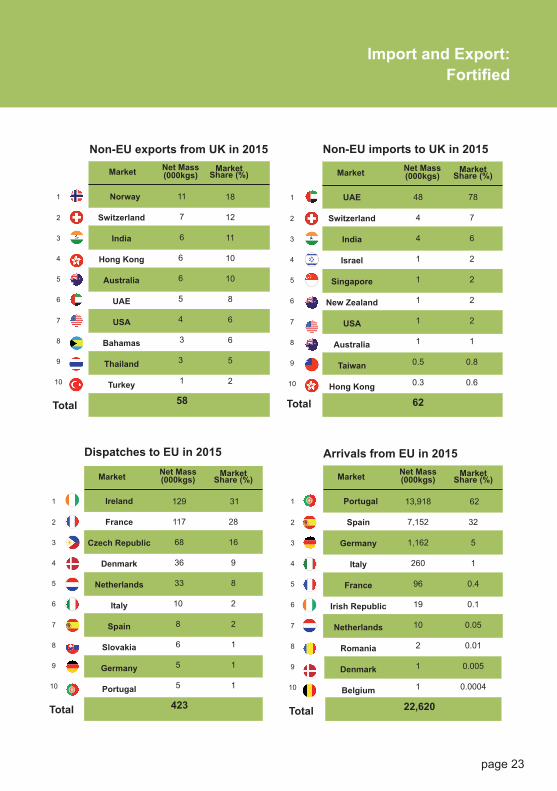

Import and Export:

Market Market Share (%)

18

12

11

10

10

8

6

6

5

2

Norway

Switzerland

India

Hong Kong

Australia

UAE

USA

Bahamas

Thailand

Turkey

1

2

3

4

5

6

7

8

9

10

Non-EU exports from UK in 2015

Total

11

7

6

6

6

5

4

3

3

1

58

Net Mass (000kgs) Market Market

Share (%)

78

7

6

2

2

2

2

1

0.8

0.6

UAE

Switzerland

India

Israel

Singapore

New Zealand

USA

Australia

Taiwan

Hong Kong

1

2

3

4

5

6

7

8

9

10

Non-EU imports to UK in 2015

Total

48

4

4

1

1

1

1

1

0.5

0.3

62

Net Mass (000kgs)

Market Market Share (%)

31

28

16

9

8

2

2

1

1

1

Ireland

France

Czech Republic

Denmark

Netherlands

Italy

Spain

Slovakia

Germany

Portugal

1

2

3

4

5

6

7

8

9

10

Dispatches to EU in 2015

£

Total

129

117

68

36

33

10

8

6

5

5

423

Net Mass (000kgs) Market Market

Share (%)

62

32

5

1

0.4

0.1

0.05

0.01

0.005

0.0004

Portugal

Spain

Germany

Italy

France

Irish Republic

Netherlands

Romania

Denmark

Belgium

1

2

3

4

5

6

7

8

9

10

Arrivals from EU in 2015

Total

13,918

7,152

1,162

260

96

19

10

2

1

1

22,620

Net Mass (000kgs)

Fortified

The Wine and Spirit Trade AssociationRegistered number: 410660 England Limited by Guarantee

www.wsta.co.uk

@wstauk

+44 (0)20 7089 3877