Embed Size (px)

Citation preview

1

Worthington Industries

The Troops

John Barret

Zack Leggett

Shane Nowak

Aaron Burt

Brant Fuller

2

Table of Contents

Executive Summary ……………………………………………………………………………………. 8

Business and Industry Analysis …………………………………………………………………….. 15

Company Overview ……………………………………………………………………………. 15

Industry Overview ……………………………………………………………………………. 15

Five Forces Model ……………………………………………………………………………………….. 18

Rivalry Amongst existing Firms …………………………………………………………… 19

Industry Growth ……………………………………………………………………… 20

Concentration of Competitors …………………………………………………… 21

Level of Differentiation and Switching Costs ………………………………. 22

Learning /Scale of Economy and Ratio of Fixed to Variable Cost ….. 23

Excess Capacity and Exit Barriers ……………………………………………… 24

Conclusion ……………………………………………………………………………… 24

Threat of New Entrants ……………………………………………………………………… 25

Economies of Scale …………………………………………………………………. 25

First Mover Advantage …………………………………………………………….. 26

Access to Channels of Distribution and Relationships …………………... 26

Legal Barriers ………………………………………………………………………….. 27

Conclusion ……………………………………………………………………………… 27

Threat of Substitute Products ………………………………………………………………28

Relative Price and Performance ………………………………………………… 28

Customer’s Willingness to Switch ………………………………………………. 29

Conclusion ………………………………………………………………………………. 30

3

Bargaining Power of Customers ………………………………………………………….. 30

Price Sensitivity ……………………………………………………………………….. 31

Relative Bargaining Power ………………………………………………………… 31

Conclusion ……………………………………………………………………………….32

Bargaining of Suppliers ……………………………………………………………………….32

Price Sensitivity ………………………………………………………………………..32

Relative Bargaining Power ………………………………………………………… 33

Conclusion ………………………………………………………………………………. 33

Key Success Factors …………………………………………………………………………………….. 34

Cost Leadership ………………………………………………………………………………… 35

Economies of Scale ………………………………………………………………….. 35

Cost Control ……………………………………………………………………………. 35

Reduced Transportation Costs …………………………………………………… 36

Differentiation …………………………………………………………………………………… 37

Research and Development ………………………………………………………. 37

Firms Competitive Advantage ……………………………………………………. 39

Cost Leadership ………………………………………………………………………..39

Economies of Scale ………………………………………………………………….. 39

Cost Control ……………………………………………………………………………. 40

Differentiation ……………………………………………………………….………… 41

Research and Development ………………………………………………………. 41

Conclusion ………………………………………………………………………………. 42

Key Accounting Policies ……………………………………………………………………………….. 43

Operating Leases ………………………………………………………………………………. 43

4

Pension Plans …………………………………………………………………………………… 44

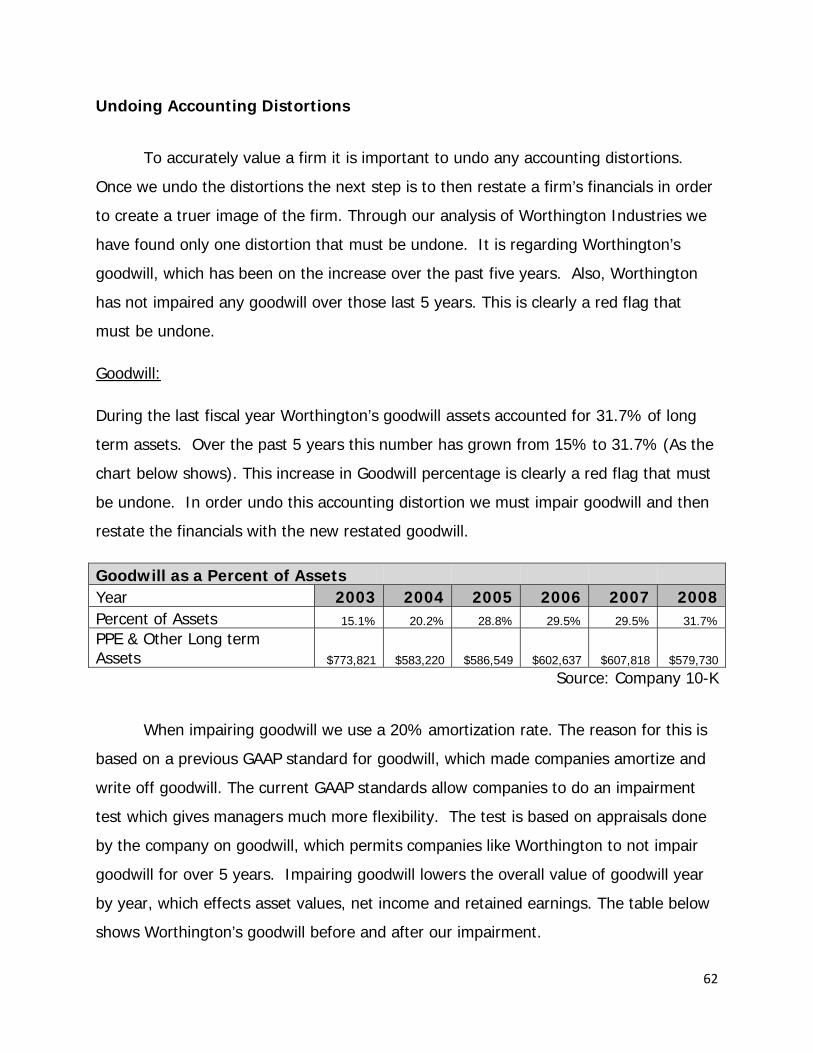

Reporting Goodwill …………………………………………………………………………….. 44

Foreign Currency Risk ……………………………………………………………………….. 46

Evaluating Accounting Strategies ………………………………………………………………….. 46

Level of Disclosure …………………………………………………………………………….. 46

Aggressiveness of Accounting Policies …………………………………………………. 47

Pension Plans …………………………………………………………………………..47

Operating Leases …………………………………………………………………….. 48

Goodwill ………………………………………………………………………………….. 48

Evaluating the Quality of Disclosure ………………………….……………………………………49

Qualitative Analysis ……………………………………….……………………………………49

Pension Plans …………………………………….…………………………………….49

Goodwill ………………………………………….………………….…………………… 49

Operating Leases …………………………………………………………………….. 50

Currency Risk …………………………………………………………………………..50

Quantitative Analysis …………………………………………………………………………. 51

Revenue and Expense Diagnostics……………………………………………… 51

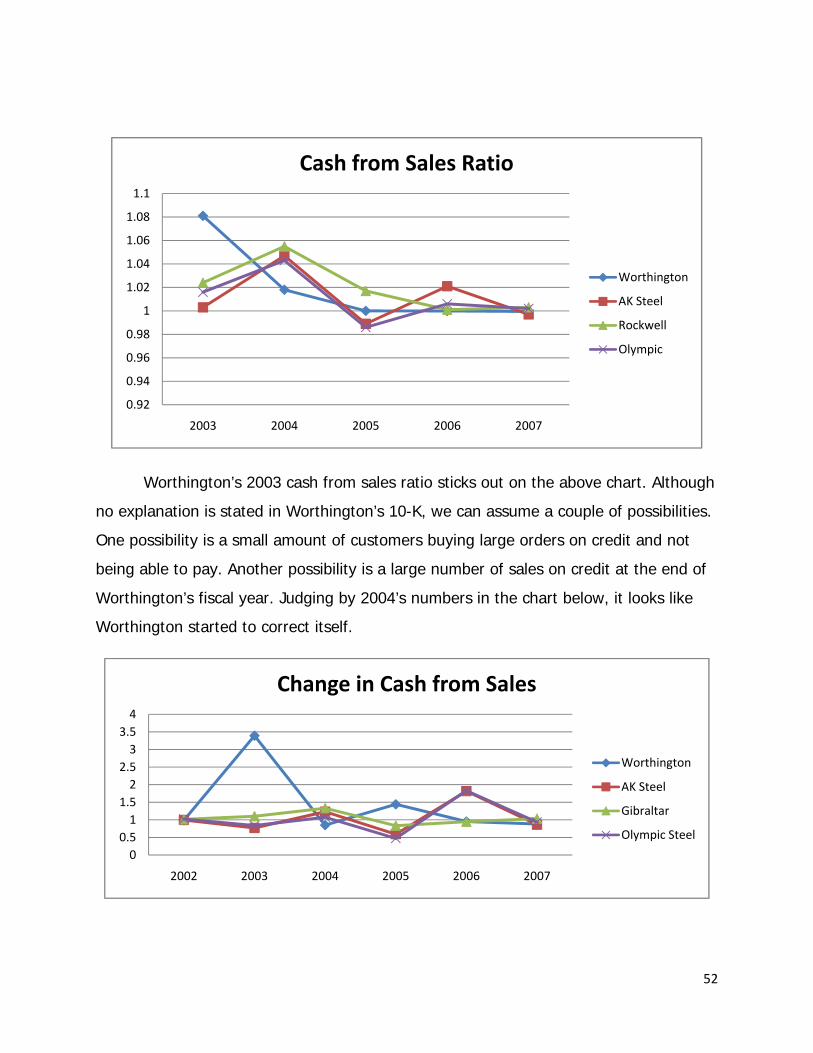

Cash from Sales Ratio……………………………………………………… 51

Accounts Receivable Ratio……………………………………………….. 53

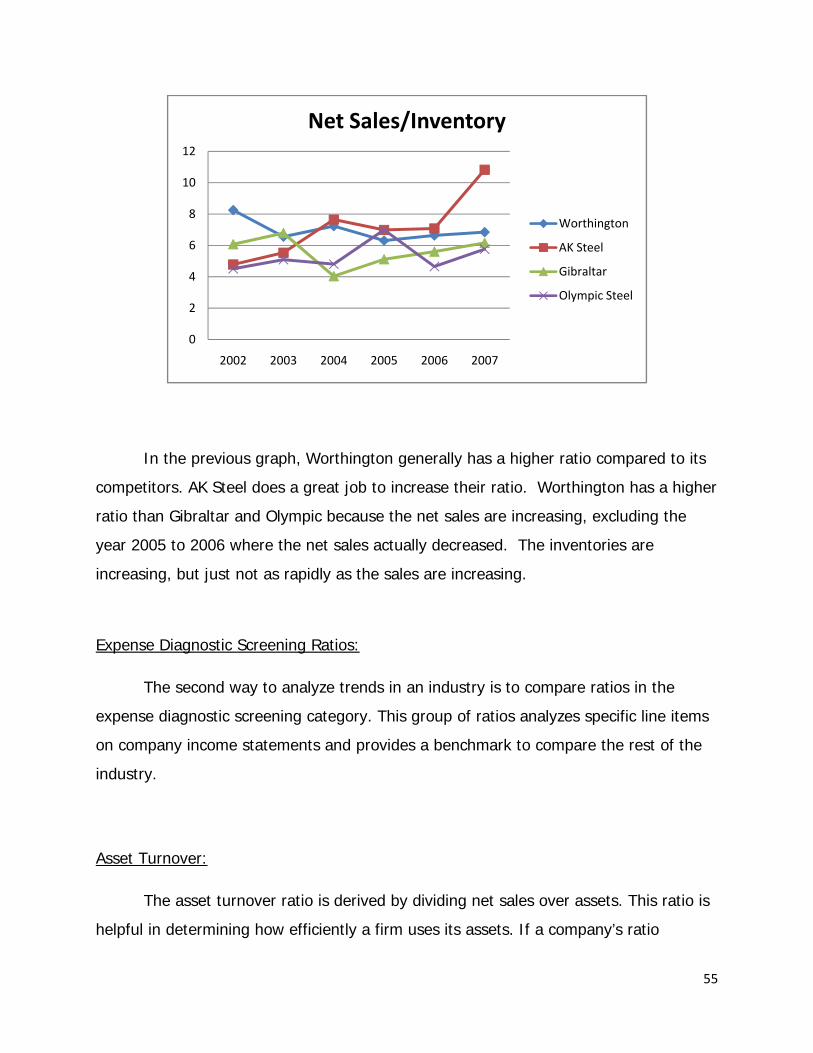

Nets Sales/ Inventory……………………………………………………… 54

Expense Diagnostic Ratios………………………………………………………….55

Asset Turnover………………………………………………………………..55

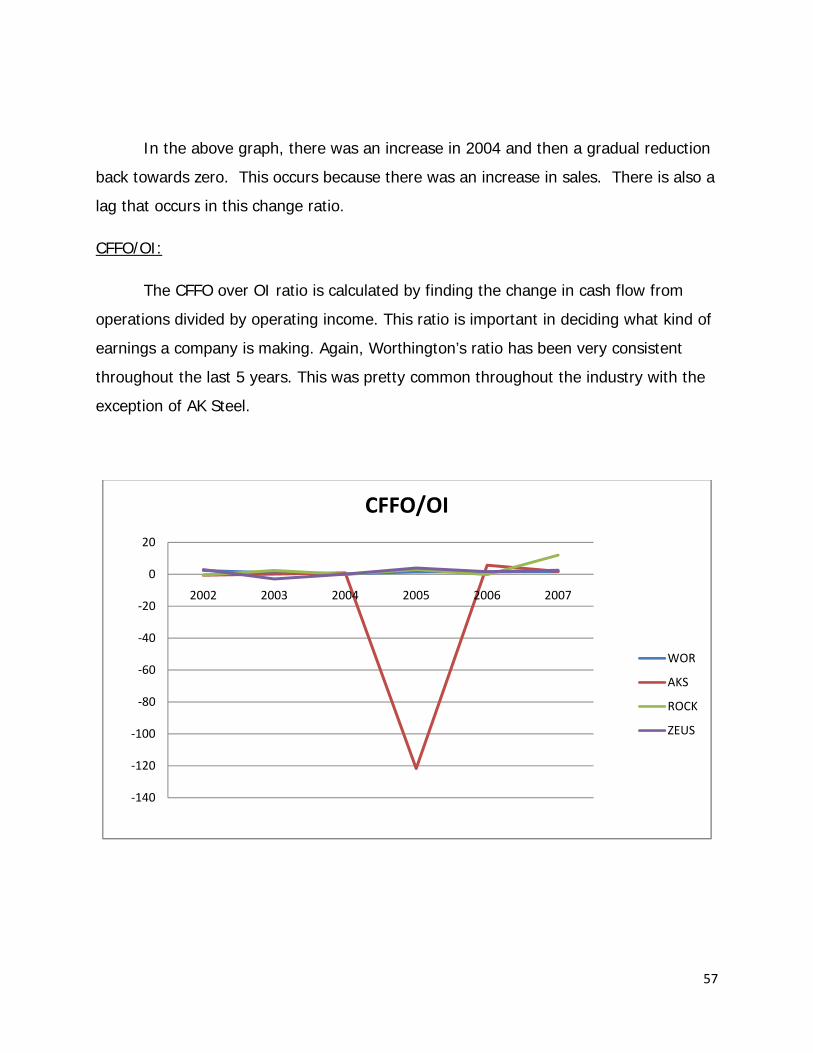

CFFO/ OI……………………………………………………………………….. 57

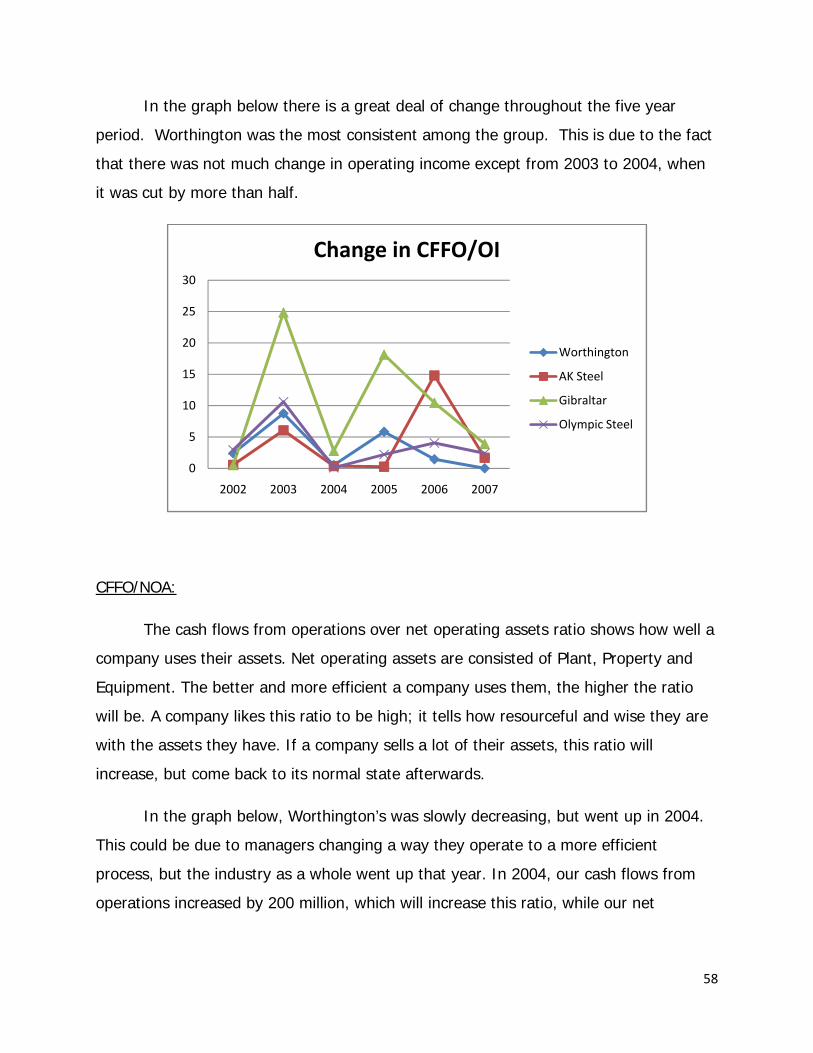

CFFO/ NOA…………………………………………………………………….. 58

5

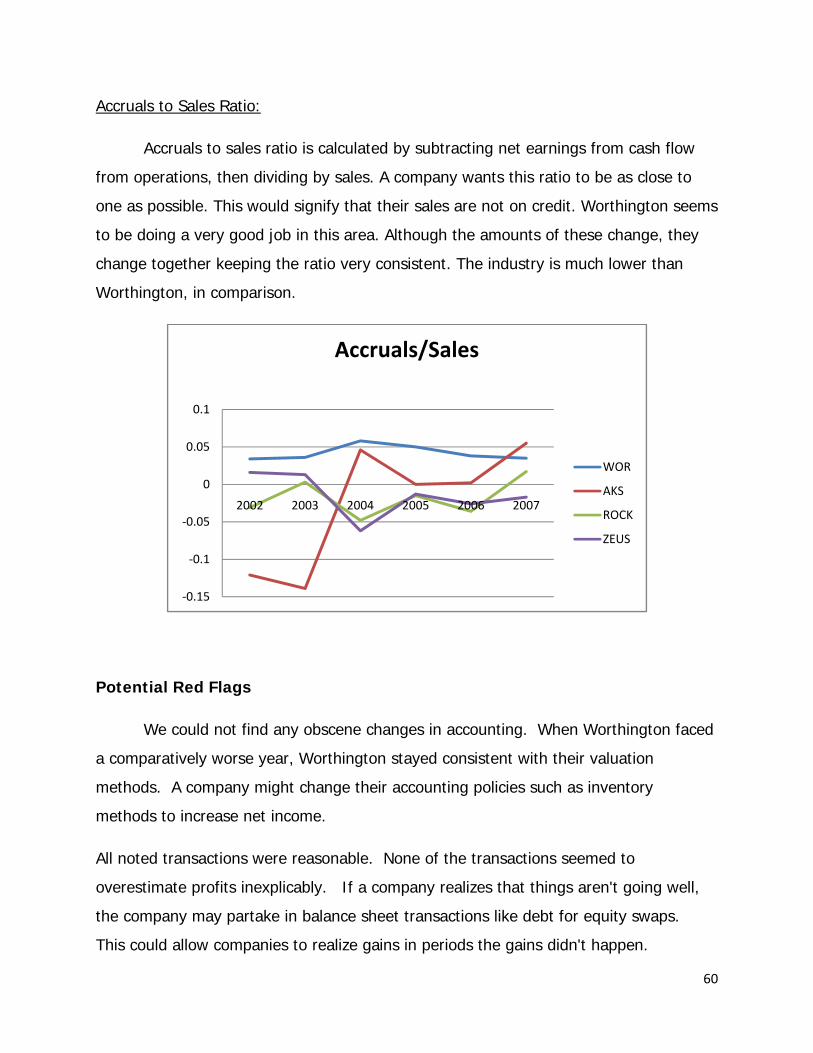

Accruals to Sales Ratio…………………………………………………….. 60

Potential Red Flags……………………………………………………………………………… 60

Undo Accounting Distortions………………………………………………………………… 62

Financial Analysis…………………………………………………………………………………………. 65

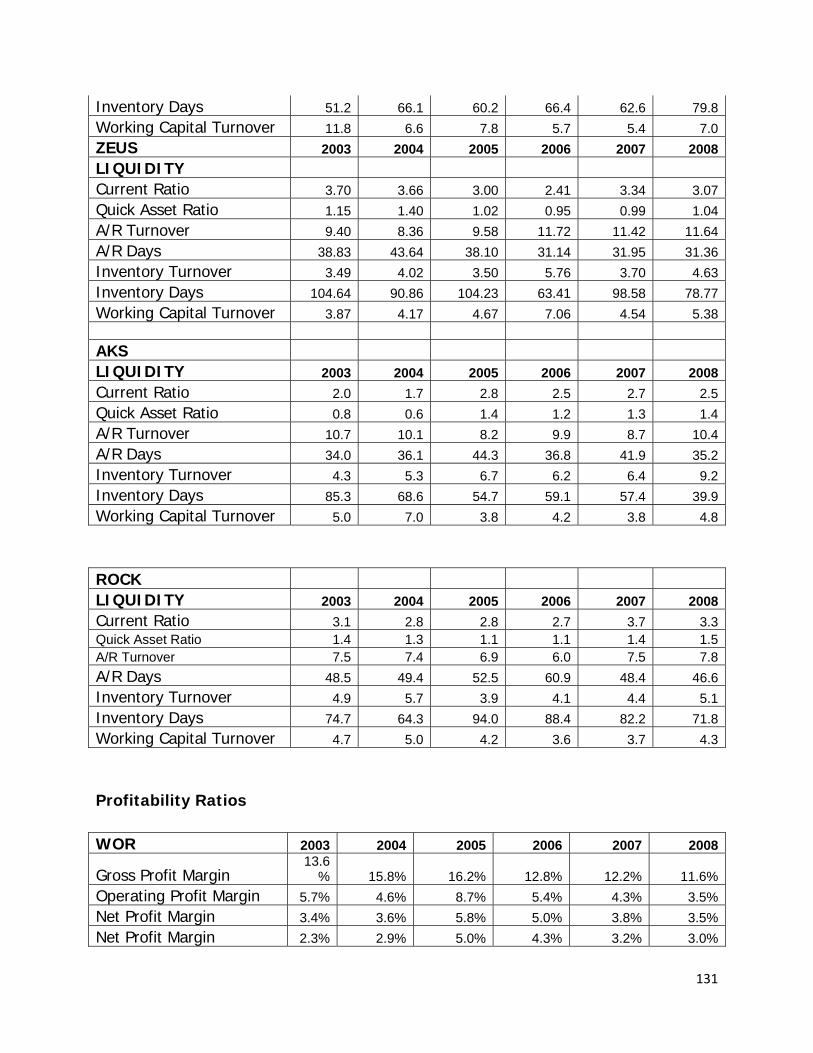

Liquidity Analysis………………………………………………………………………………… 65

Current Ratio……………………………………………………………………………. 66

Quick Assets Ratio……………………………………………………………………. 67

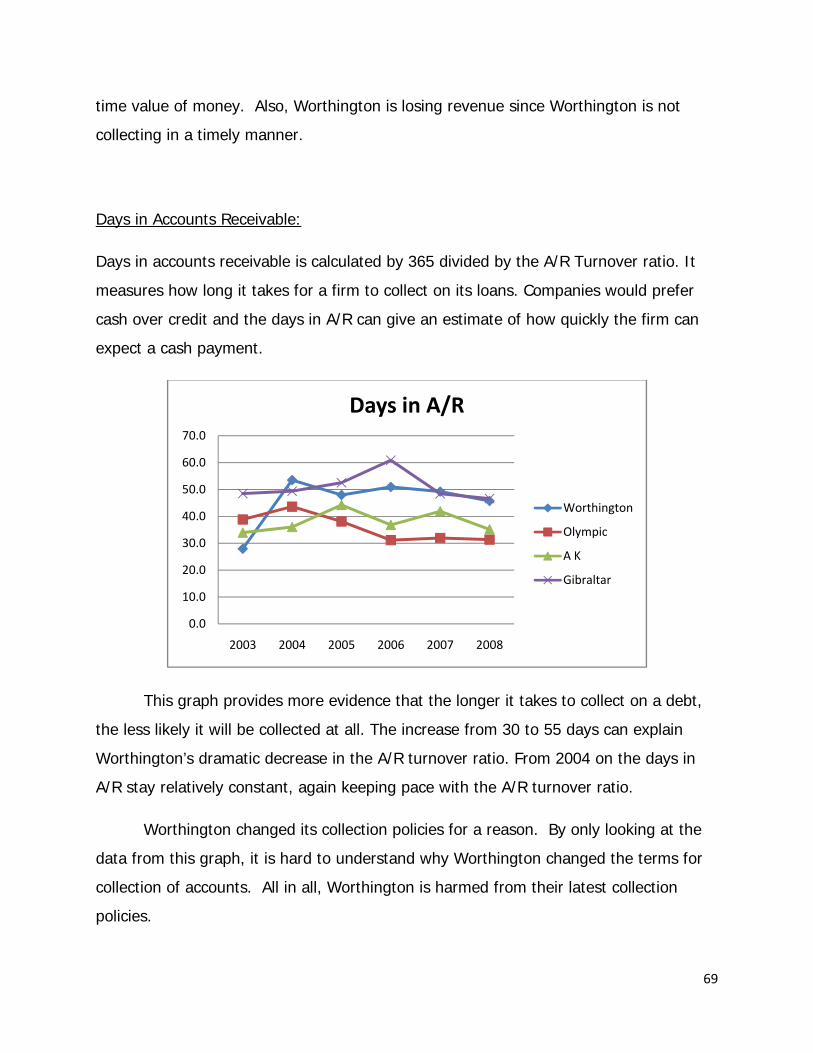

Accounts Receivable Turnover Ratio…………………………………………… 68

Days in Accounts Receivable……………………………………………………… 69

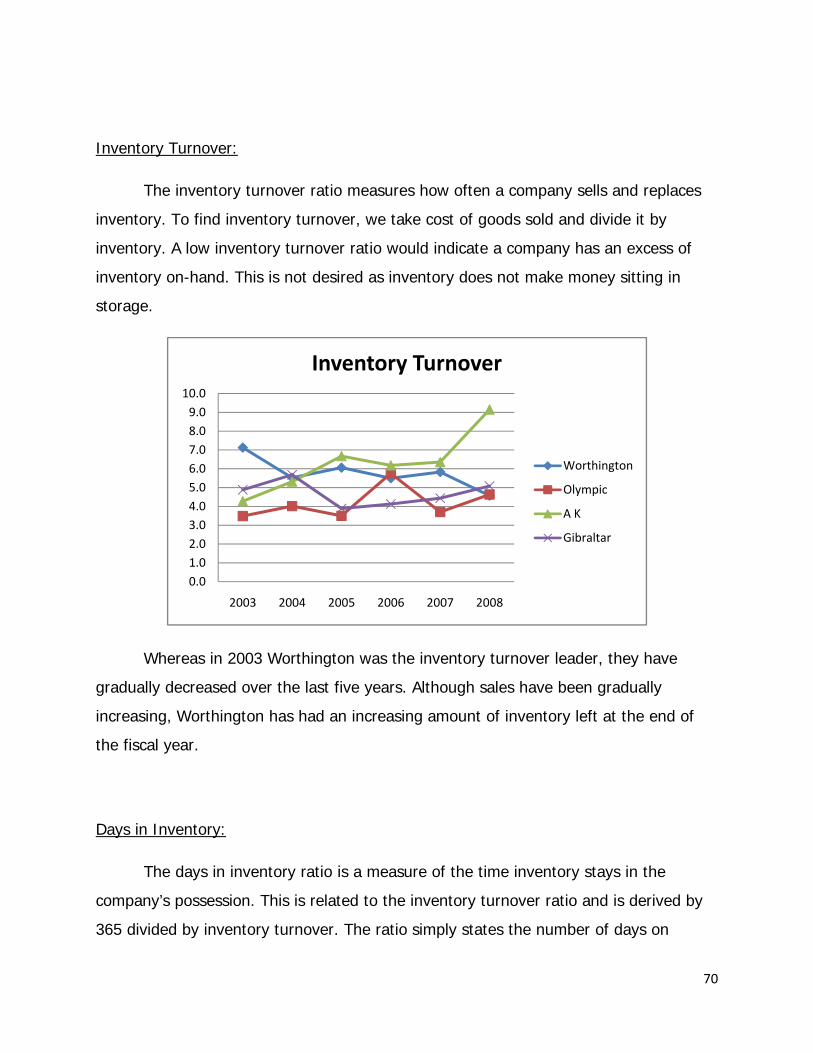

Inventory Turnover…………………………………………………………………… 70

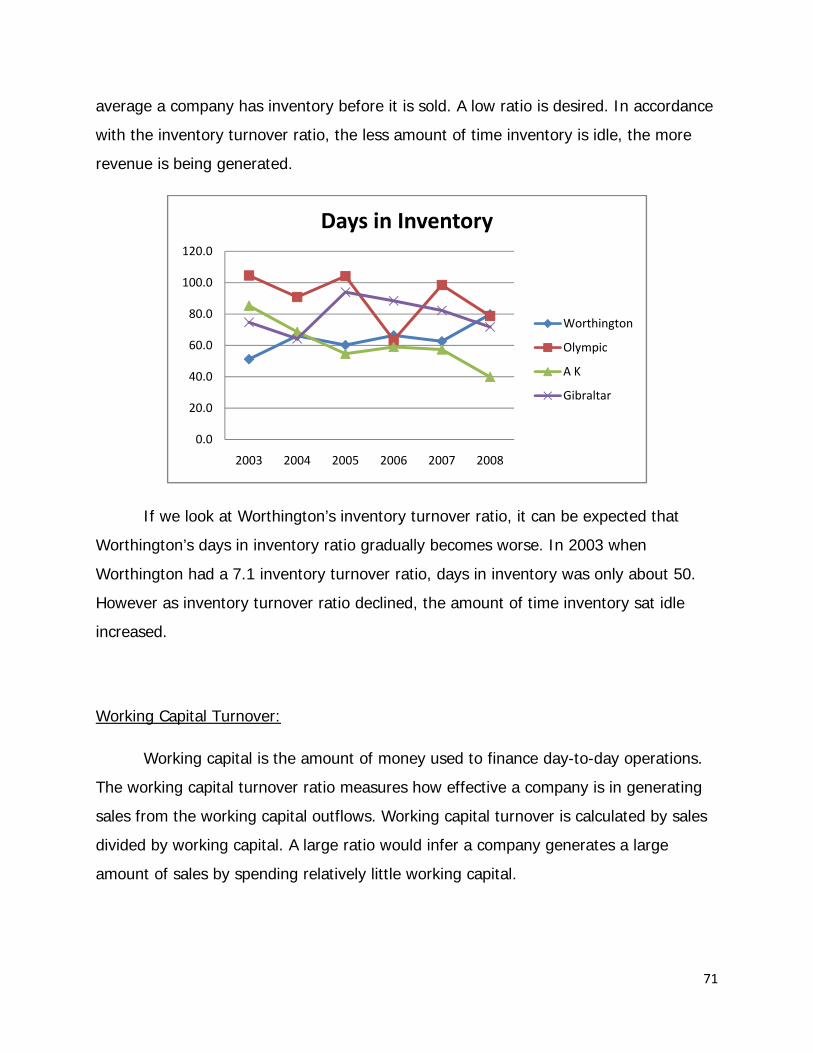

Days in Inventory……………………………………………………………………… 70

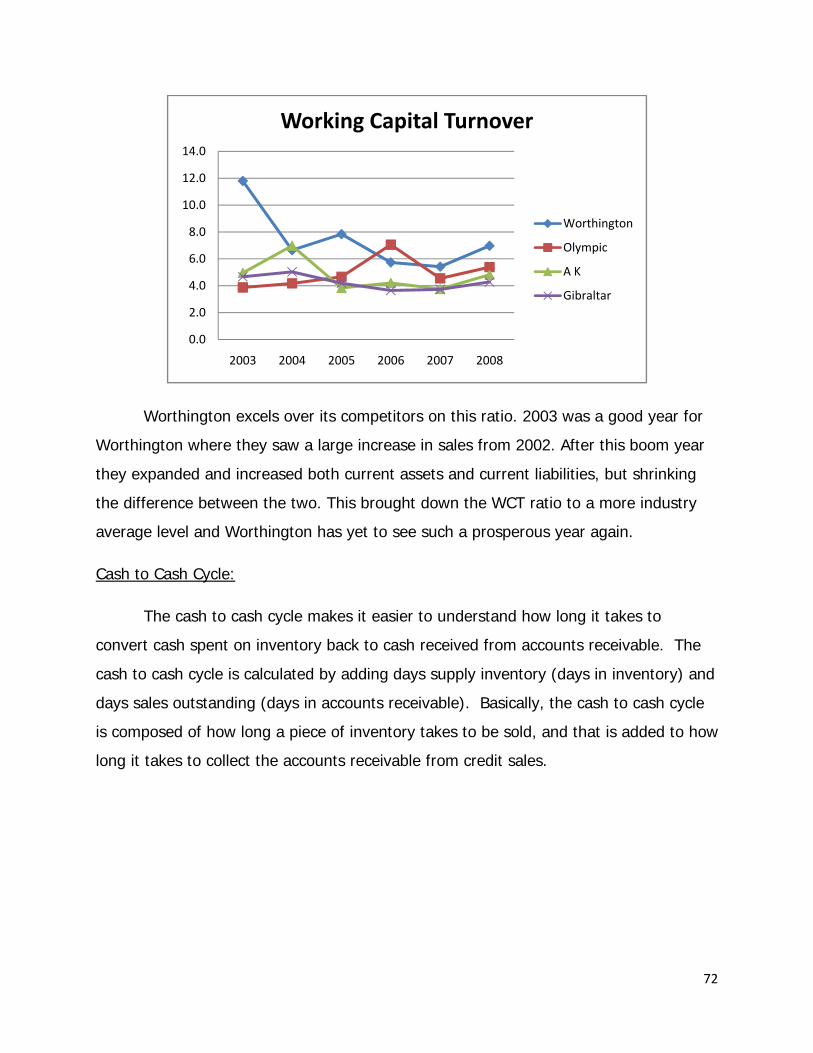

Working Capital Turnover………………………………………………………….. 71

Cash to Cash Cycle……………………………………………………………………. 72

Conclusion……………………………………………………………………………….. 73

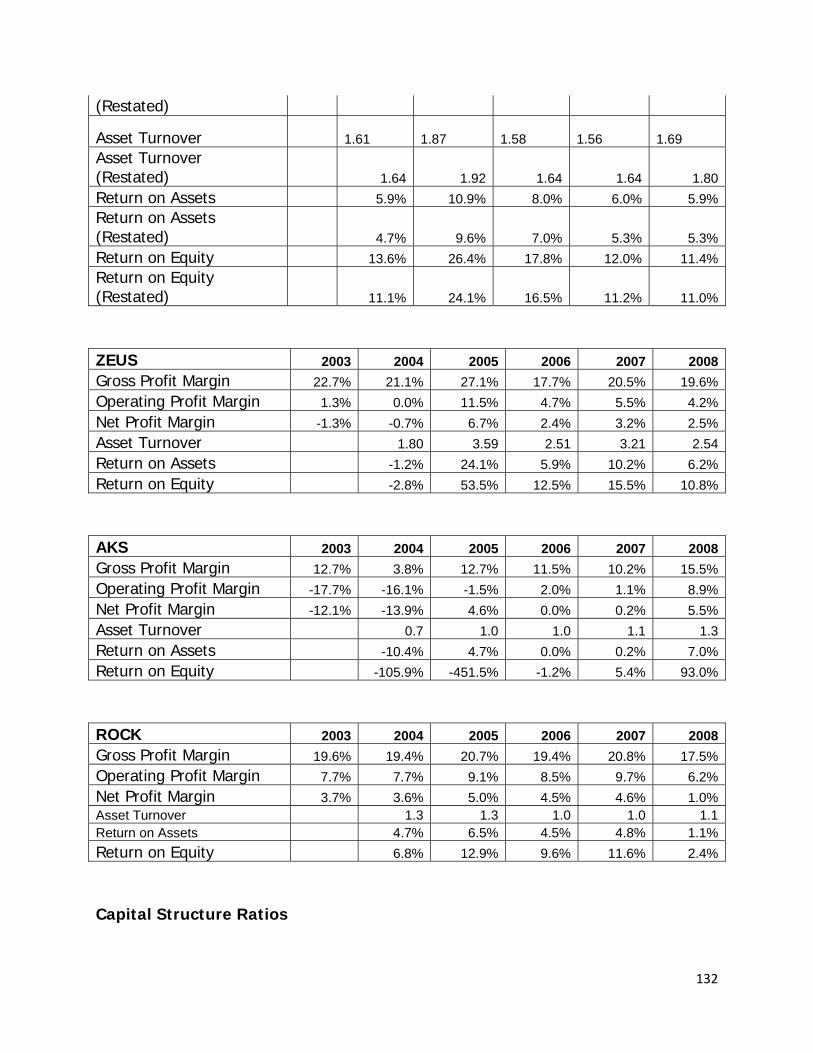

Profitability Ratio Analysis…………………………………………………………………… 74

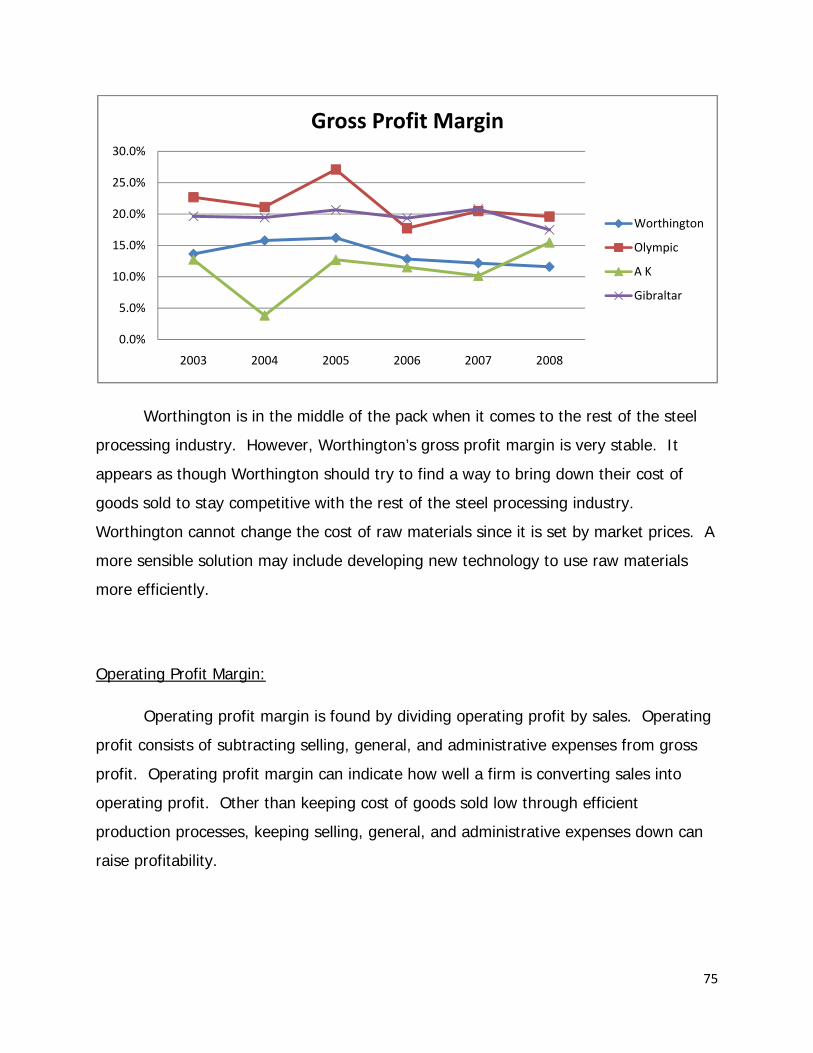

Gross Profit Margin…………………………………………………………………… 74

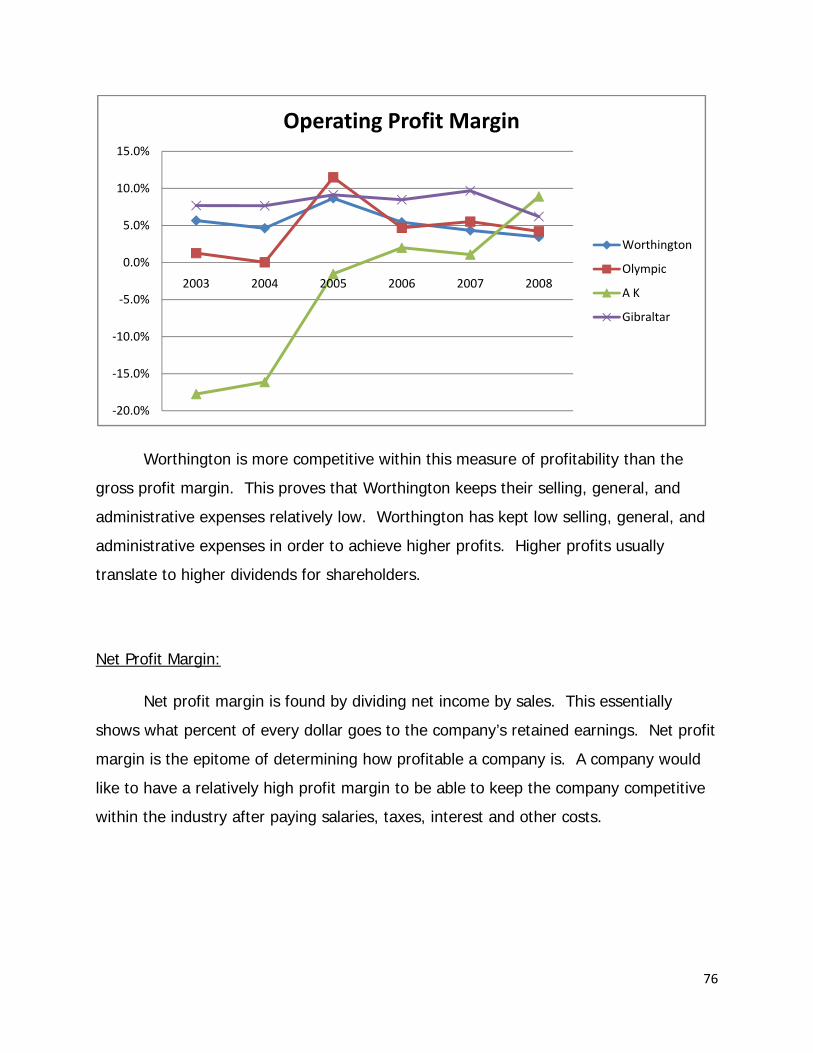

Operating Profit Margin……………………………………………………………… 75

Net Profit Margin……………………………………………………………………….76

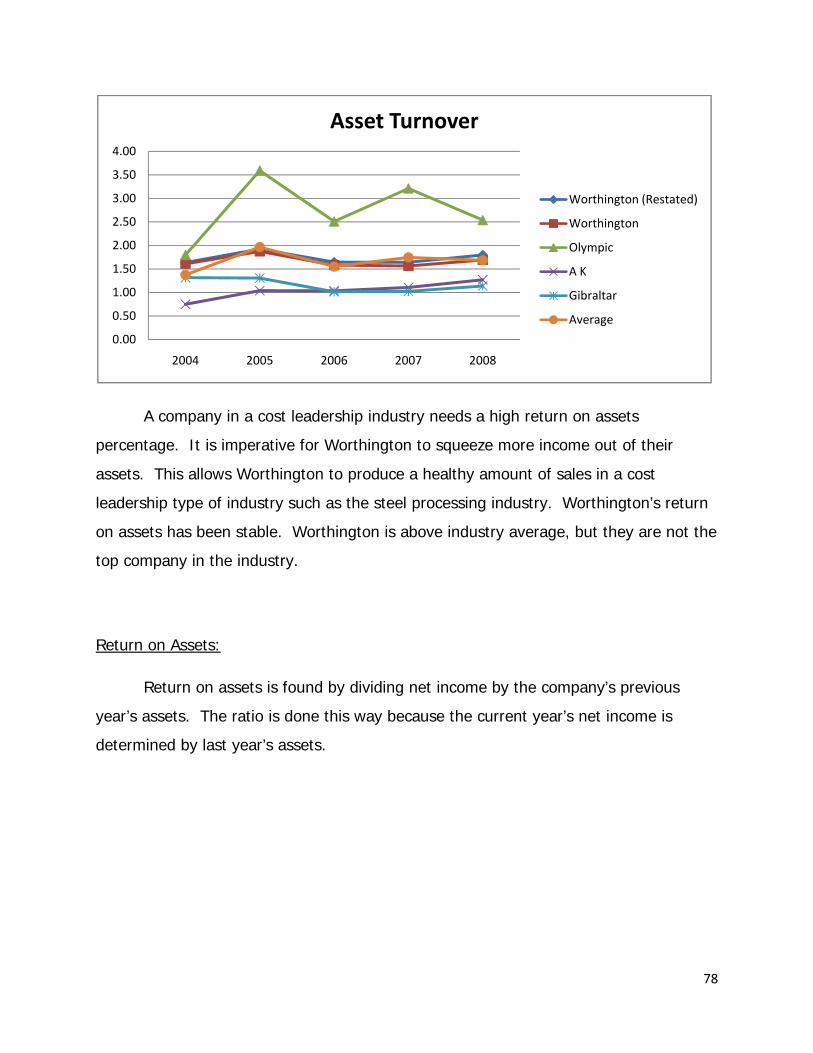

Asset Turnover…………………………………………………………………………. 77

Return on Asset………………………………………………………………………… 78

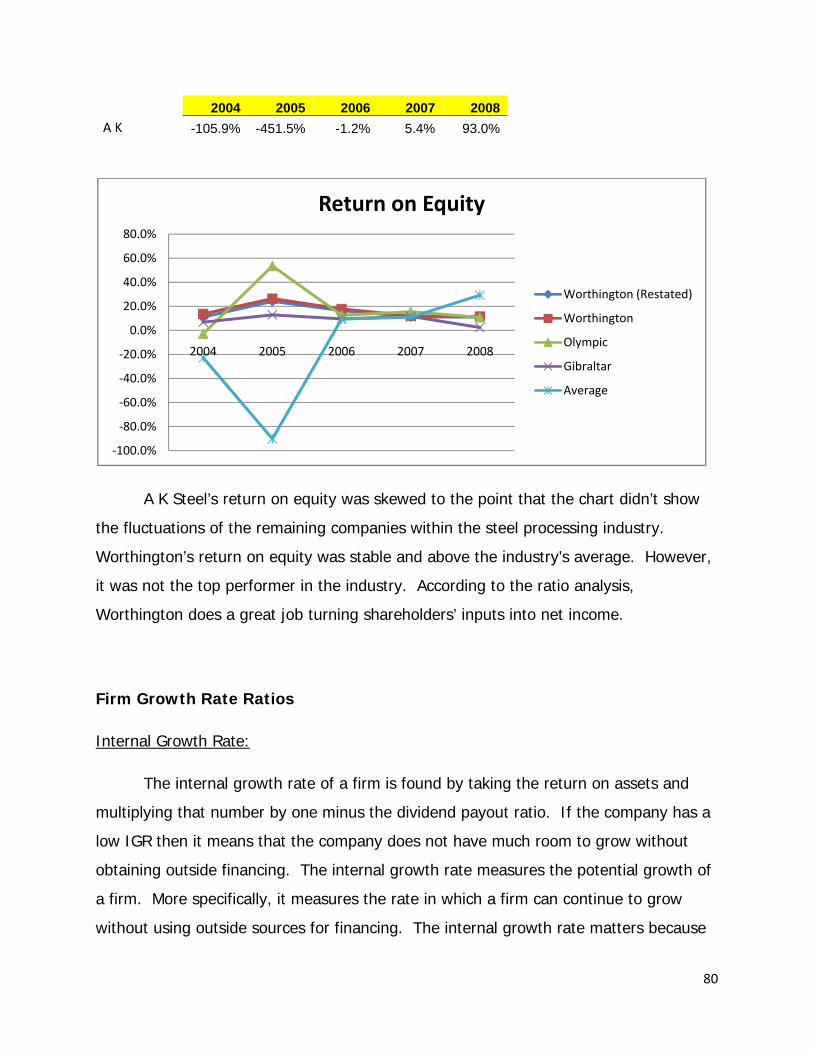

Return on Equity……………………………………………………………………… 79

Firms Growth Rate Ratios……………………………………………………………………. 80

Internal Growth Rate………………………………………………………………… 80

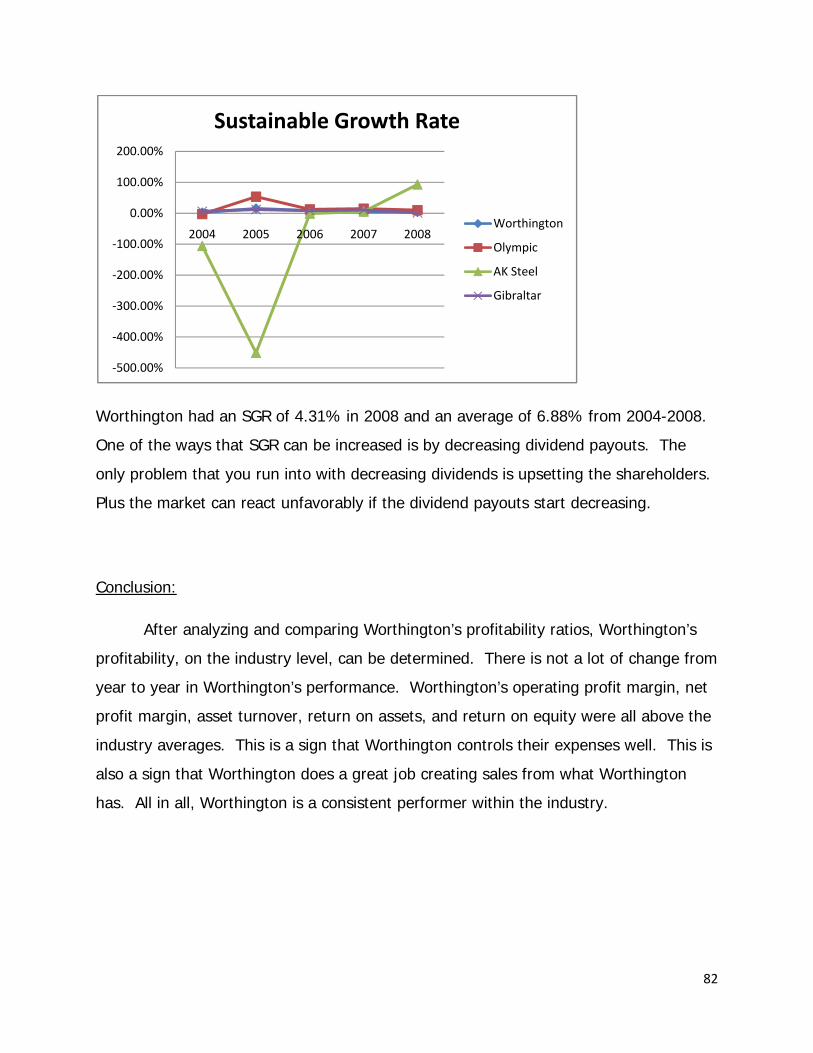

Sustainable Growth Rate……………………………………………………………. 81

6

Conclusion……………………………………………………………………………….. 82

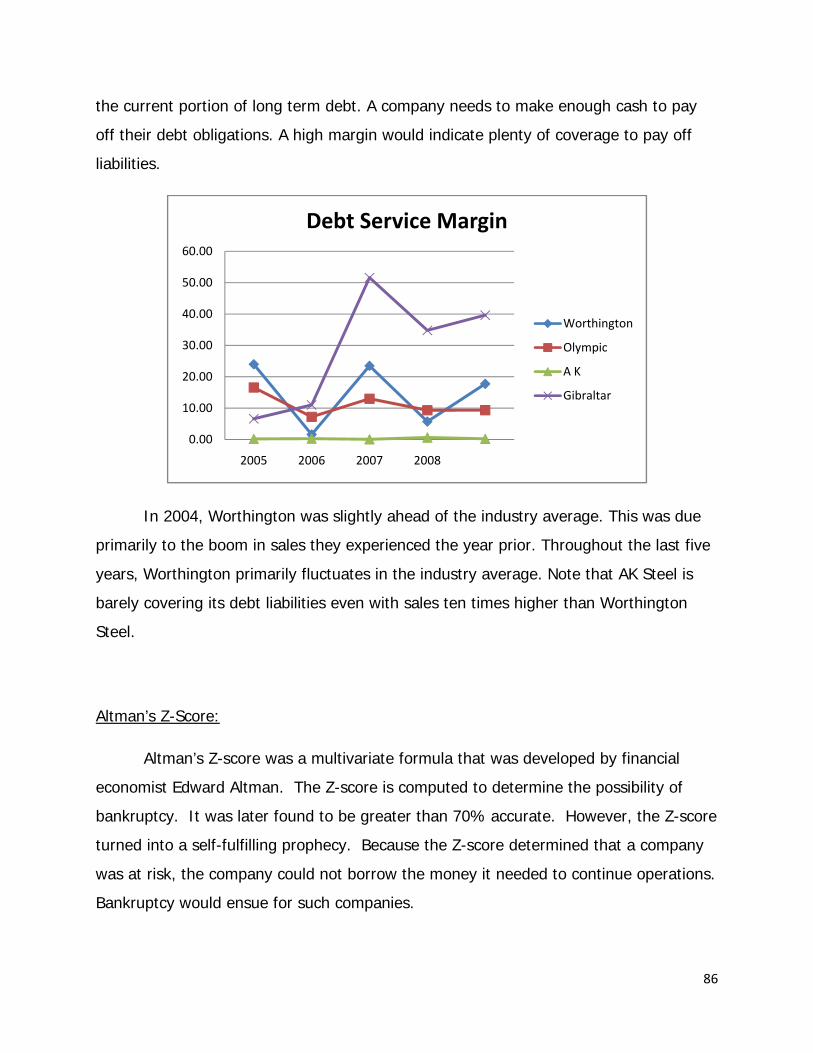

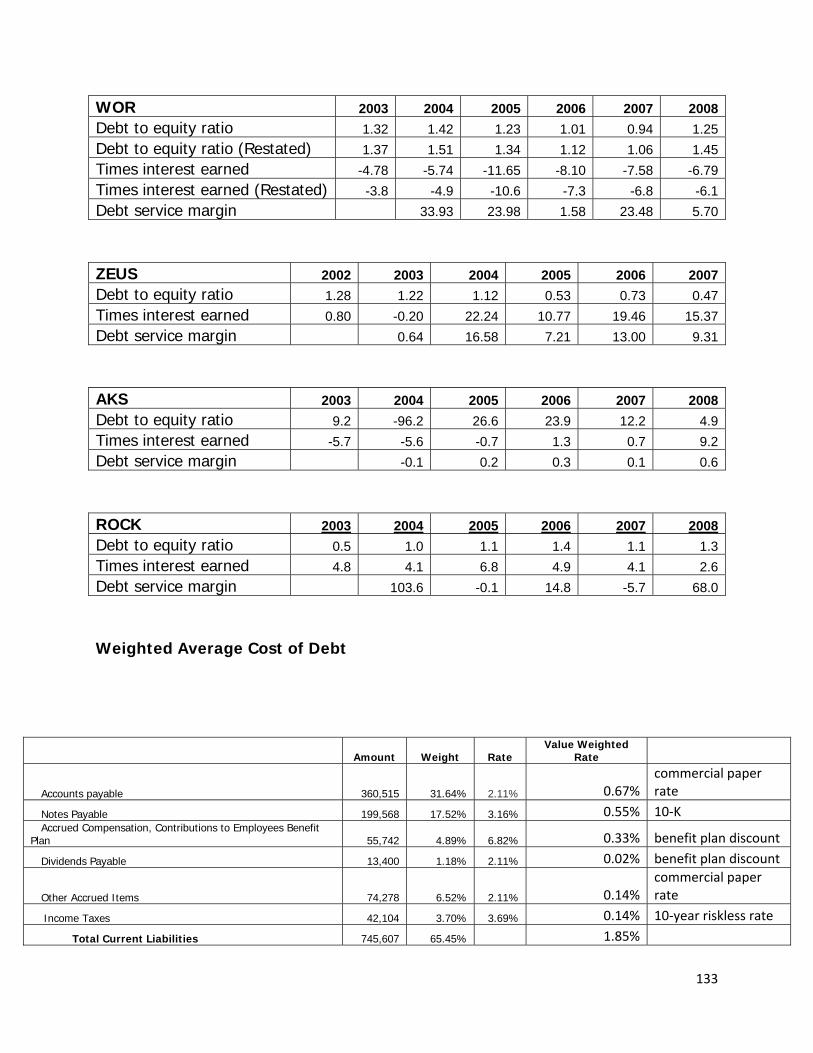

Capital Structure Ratios………………………………………………………………………. 83

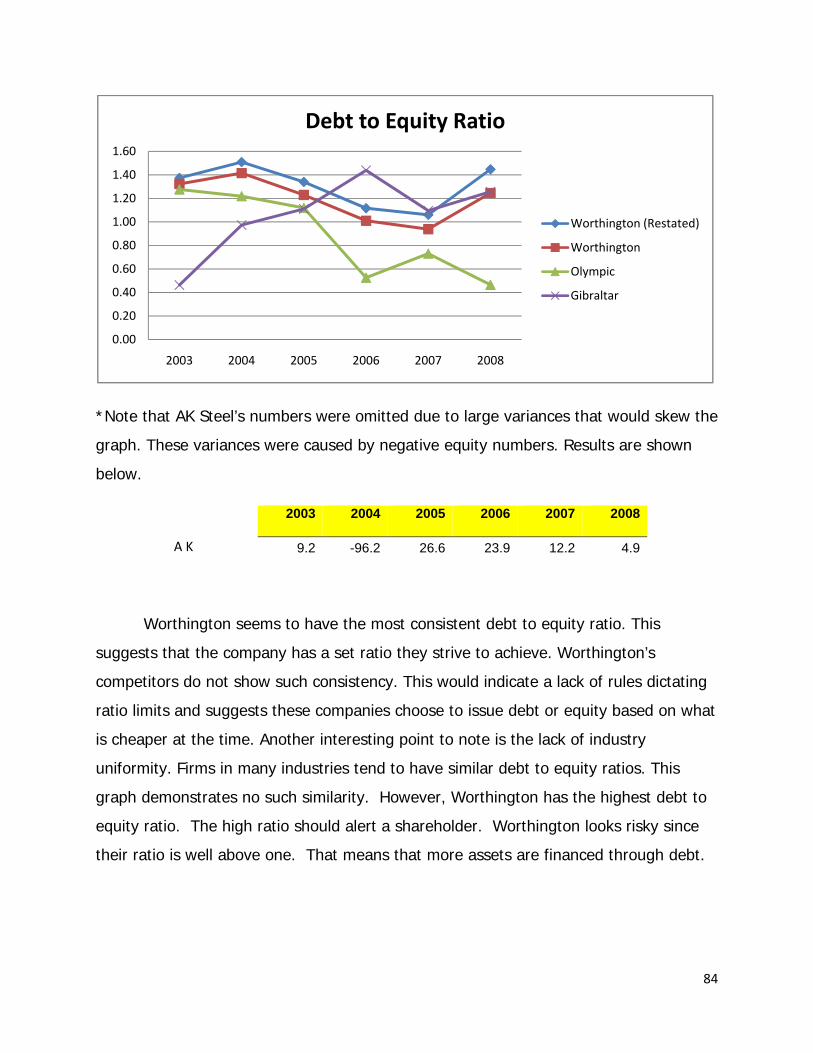

Debt-to-Equity Ratio…………………………………………………………………. 83

Times Interest Earned………………………………………………………………. 85

Debt Service Margin………………………………………………………………….. 85

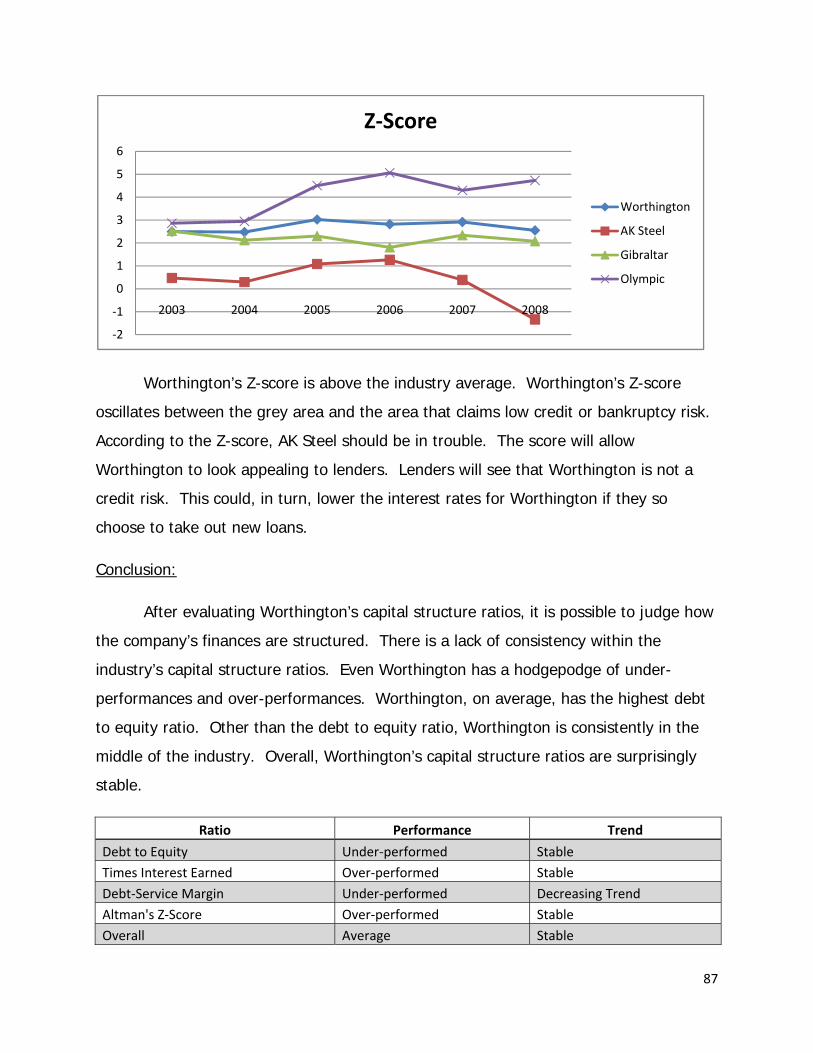

Altman’s Z-Score………………………………………………………………………. 86

Conclusion………………………………………………………………………………..87

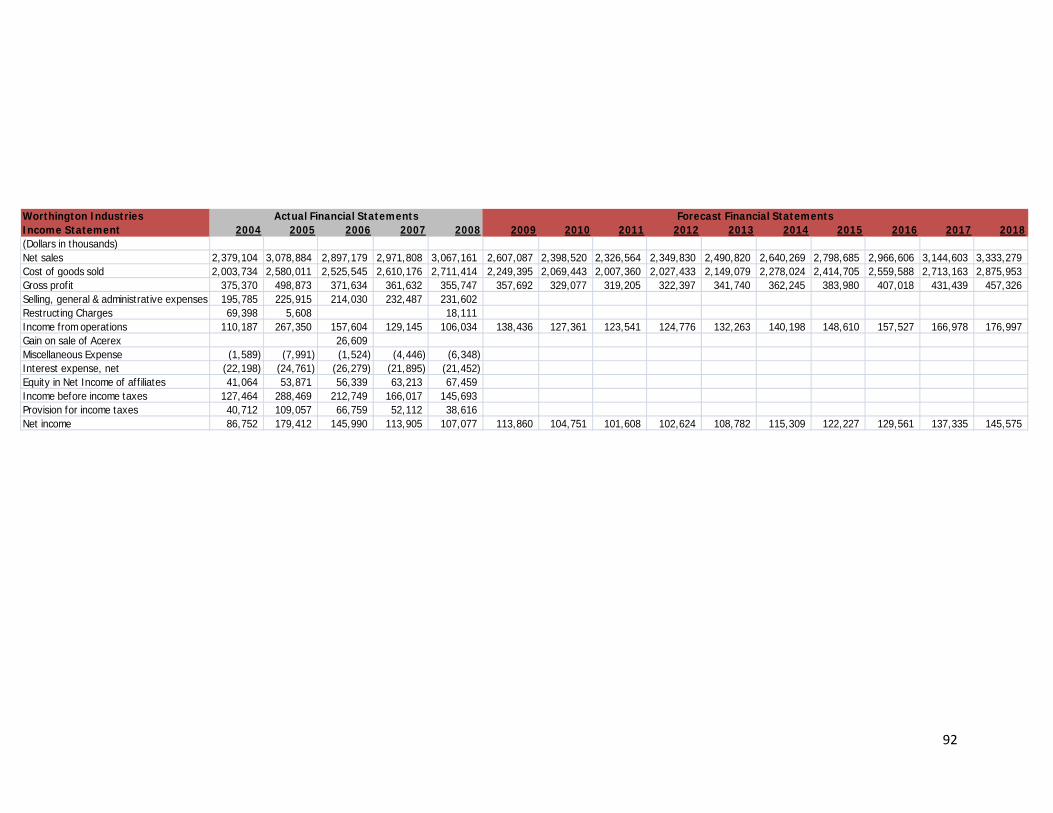

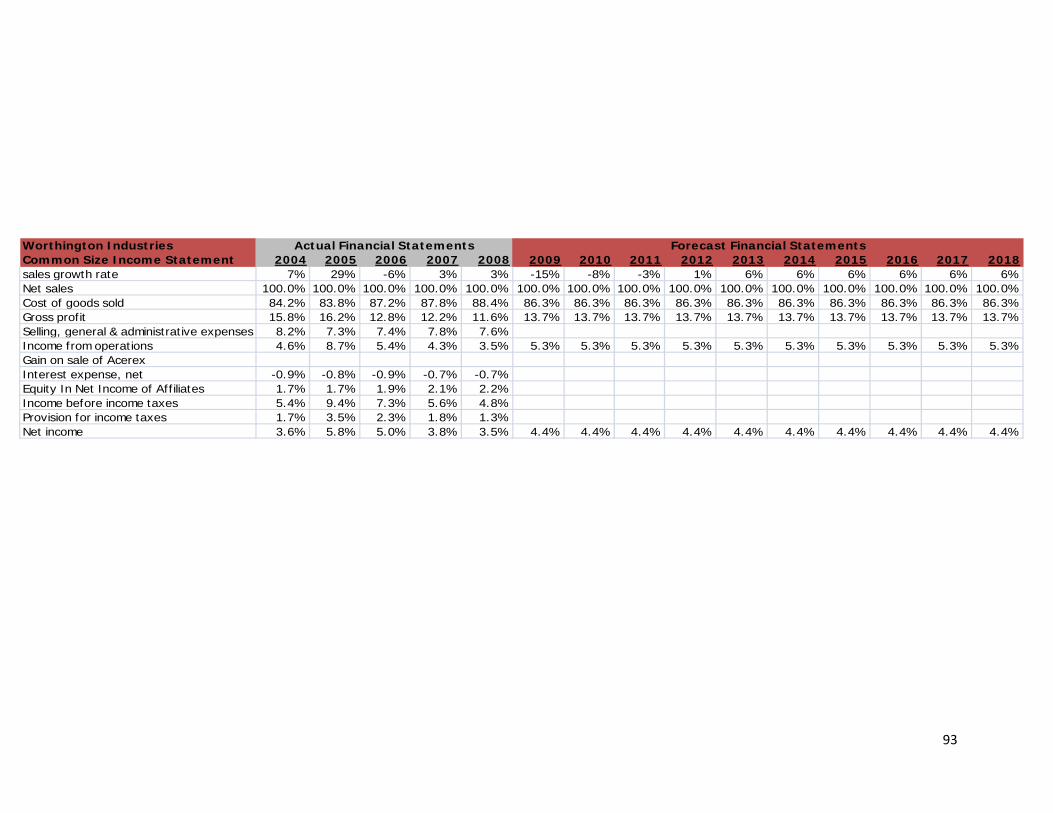

Forecasting………………………………………………………………………………………………….. 88

Year 1 Income Forecast………………………………………………………………………. 90

Income Statement………………………………………………………………………………. 90

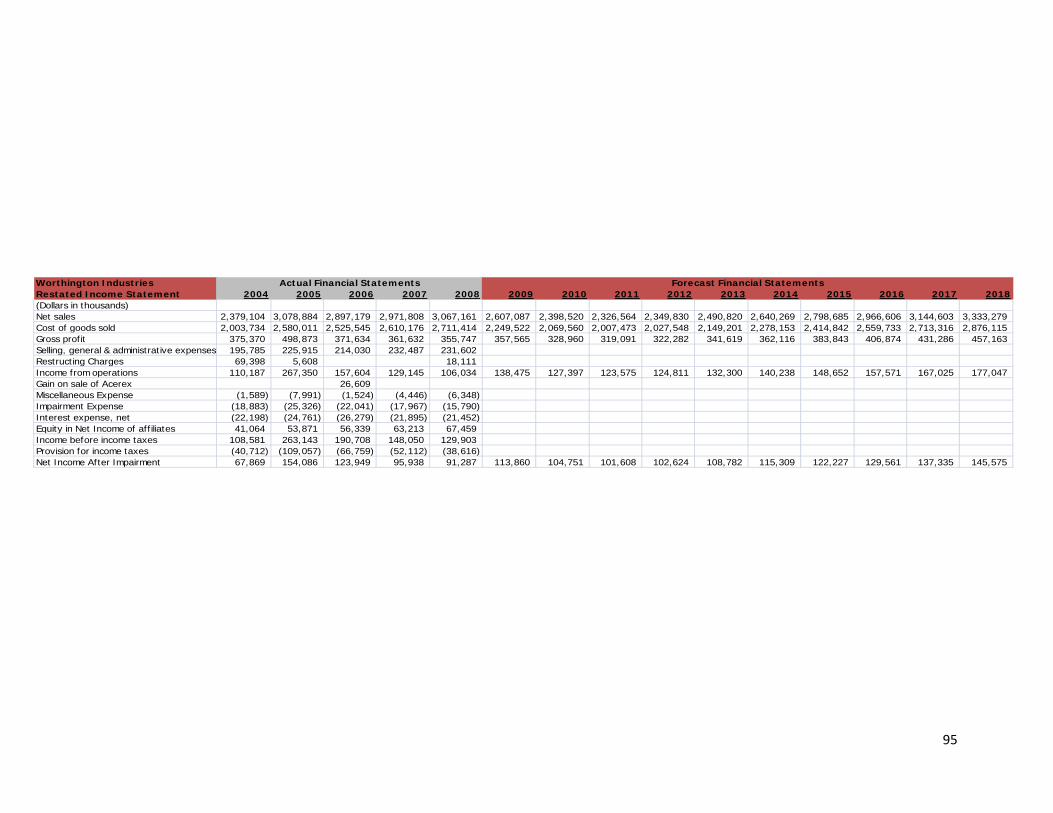

Income Statement (Revised) ………………………………………………………………. 94

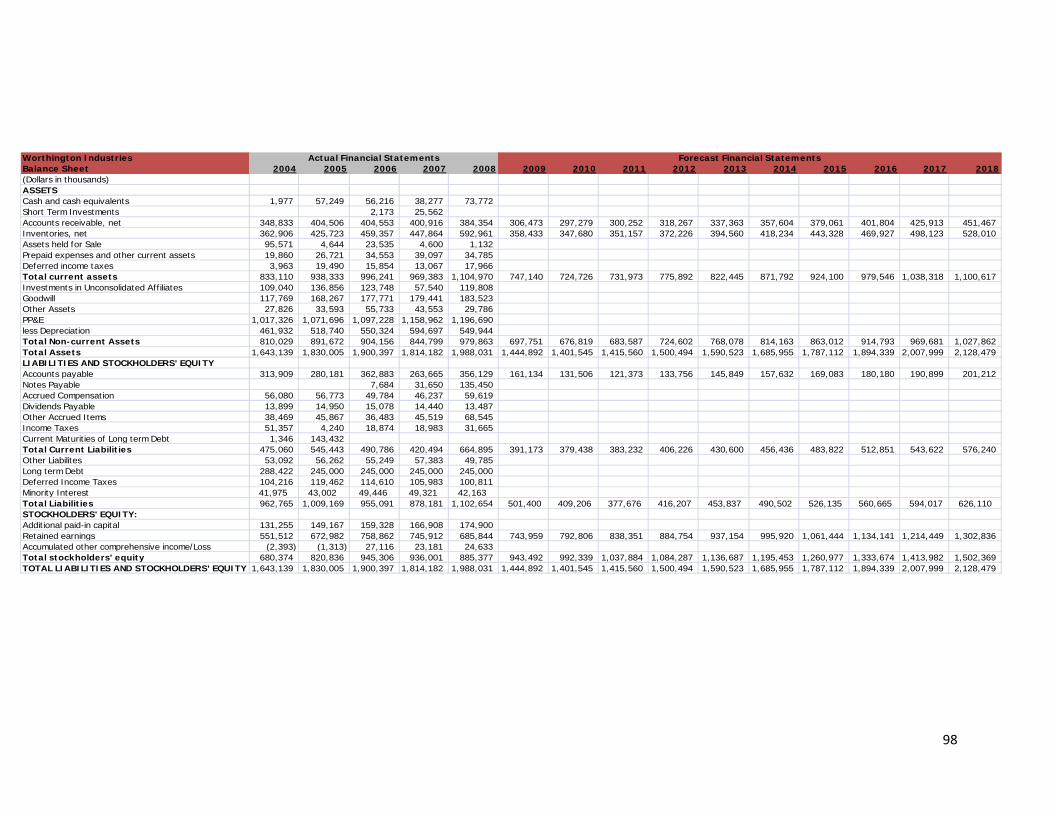

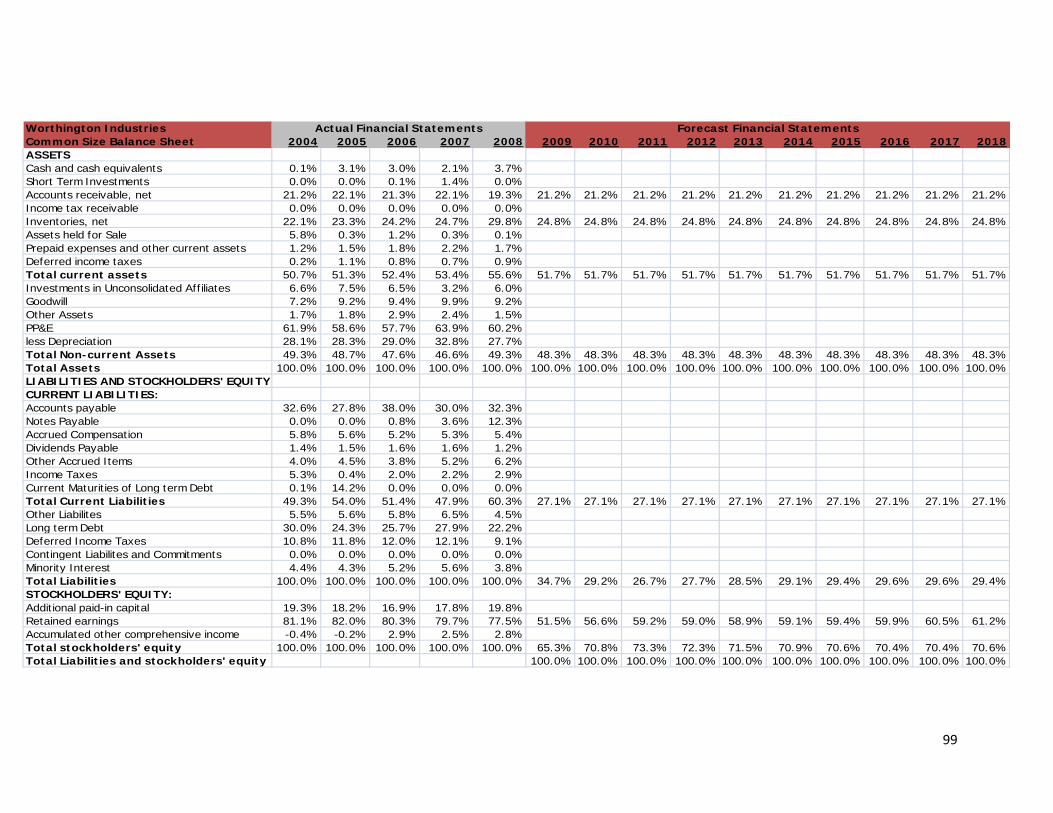

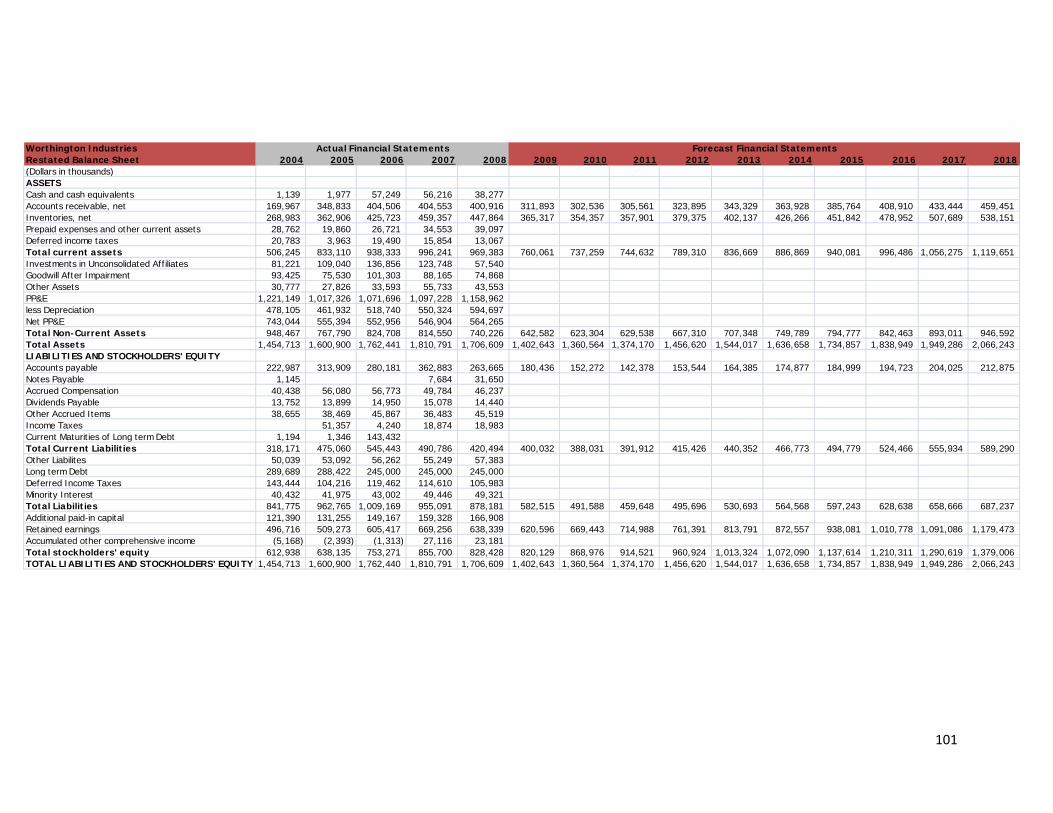

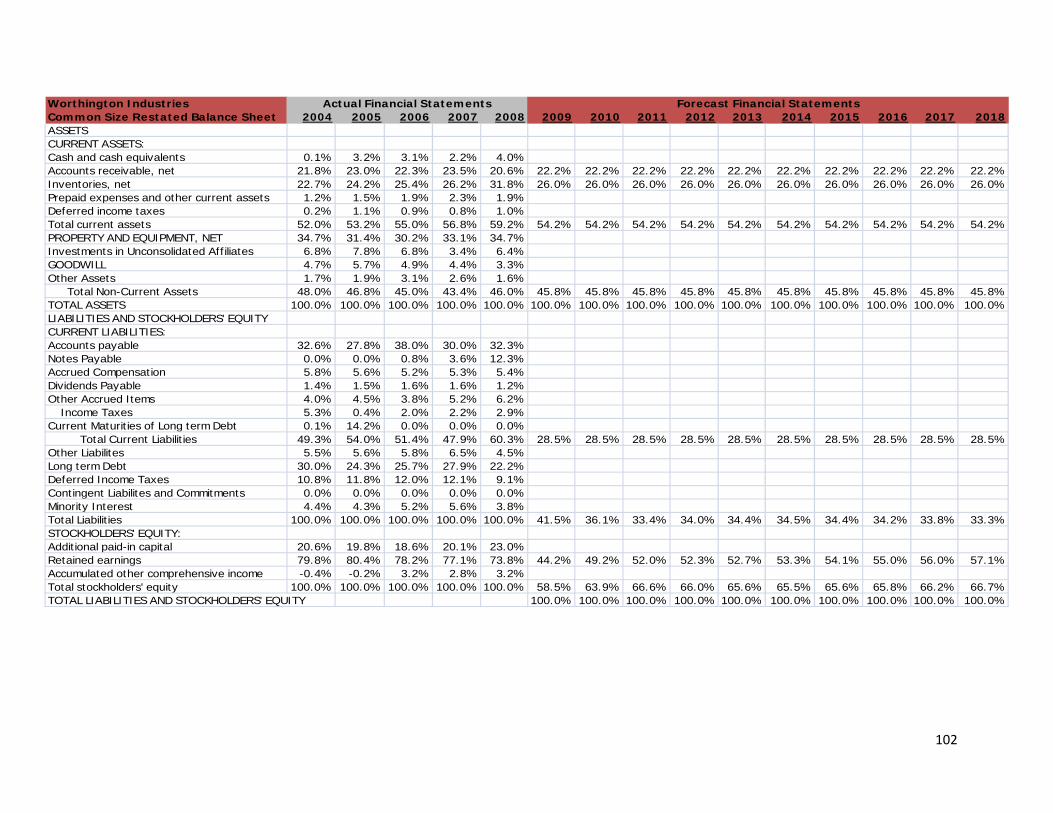

Balance Sheet……………………………………………………………………………………..97

Balance sheet (Revised)……………………………………………………………………… 100

Statement of Cash Flows…………………………………………………………………….. 103

Cost of Financing…………………………………………………………………………………………. 105

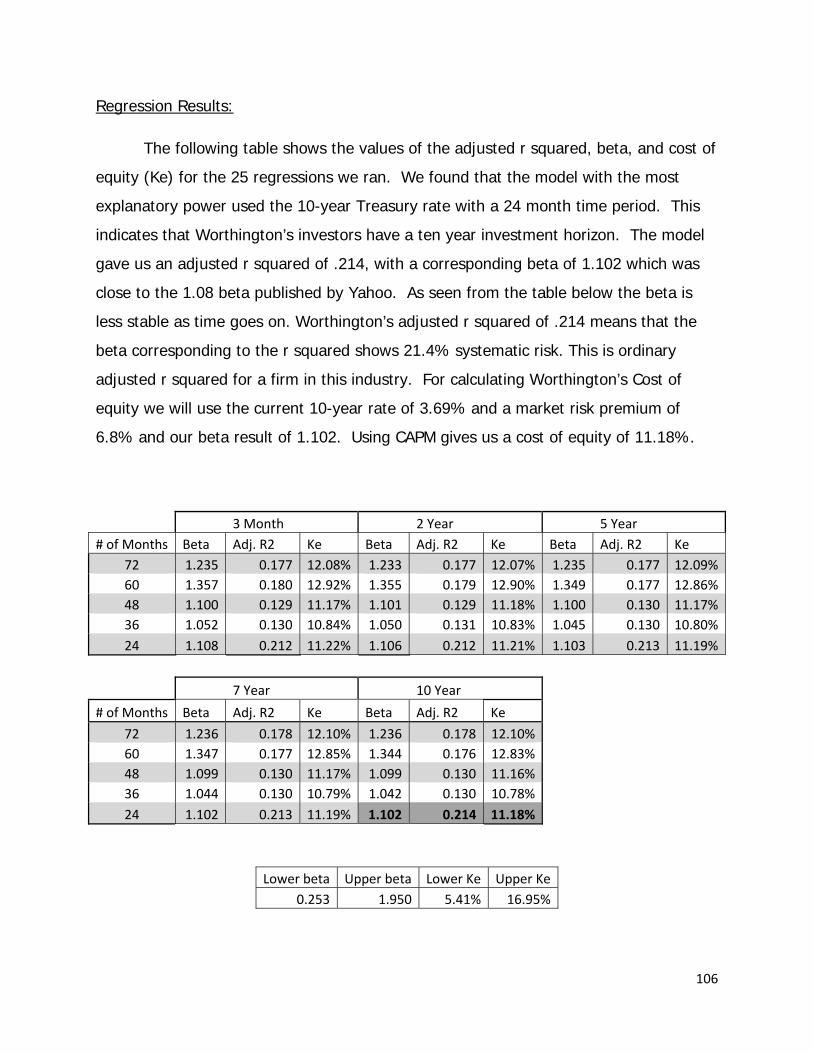

Cost of Equity (Ke)……………………………………………………………………………… 105

Estimating Beta………………………………………………………………………………….. 105

Regression Results……………………………………………………………………………… 106

Backdoor Method……………………………………………………………………………….. 107

Cost of Debt (Kd)……………………………………………………………………………….. 108

Weighted Average Cost of Capital (WACC)……………………………………………. 109

Valuation Analysis………………………………………………………………………………………… 110

Method of Comparables………………………………………………………………………. 110

Price/ Earnings Trailing……………………………………………………………… 111

7

Price/ Earnings Forecasting………………………………………………………… 112

Price/ Book………………………………………………………………………………. 112

Price Earnings Growth (P.E.G.)…………………………………………………… 113

Price/ EBITDA…………………………………………………………………………… 114

Enterprise Value/ EBITDA………………………………………………………….. 114

Price to Free Cash Flows……………………………………………………………. 115

Dividends/ Price………………………………………………………………………… 116

Conclusion……………………………………………………………………………….. 116

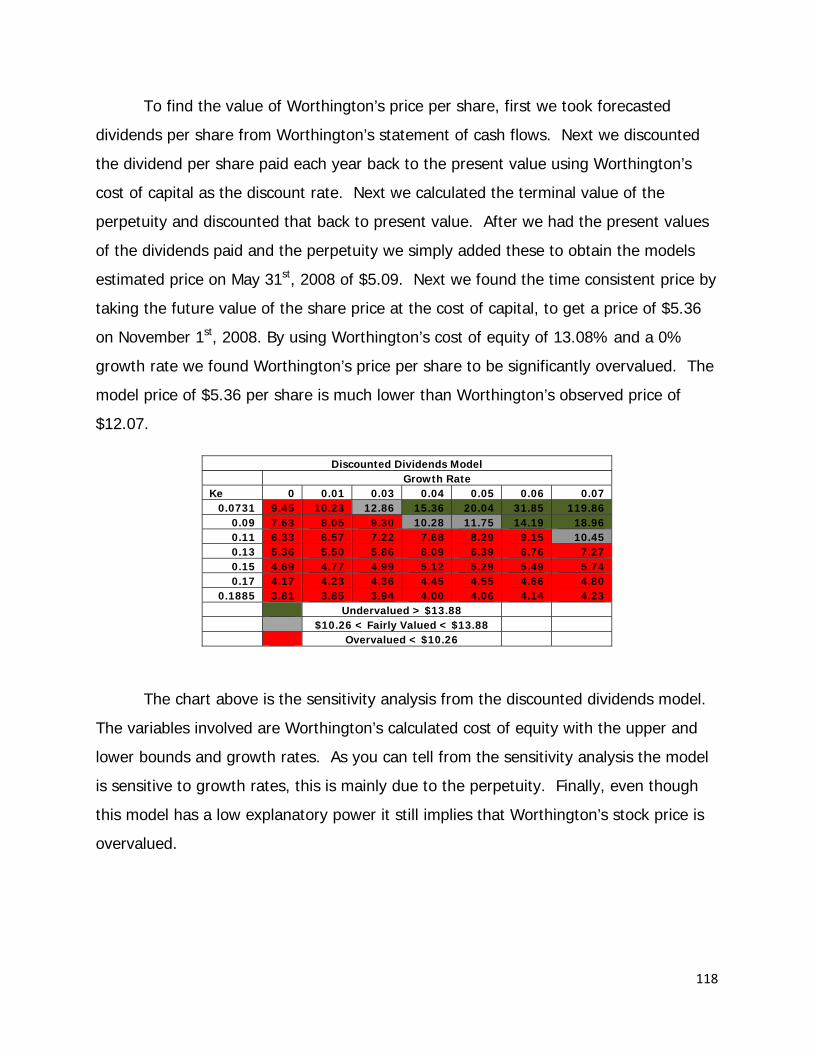

Intrinsic Value Models…………………………………………………………………………. 117

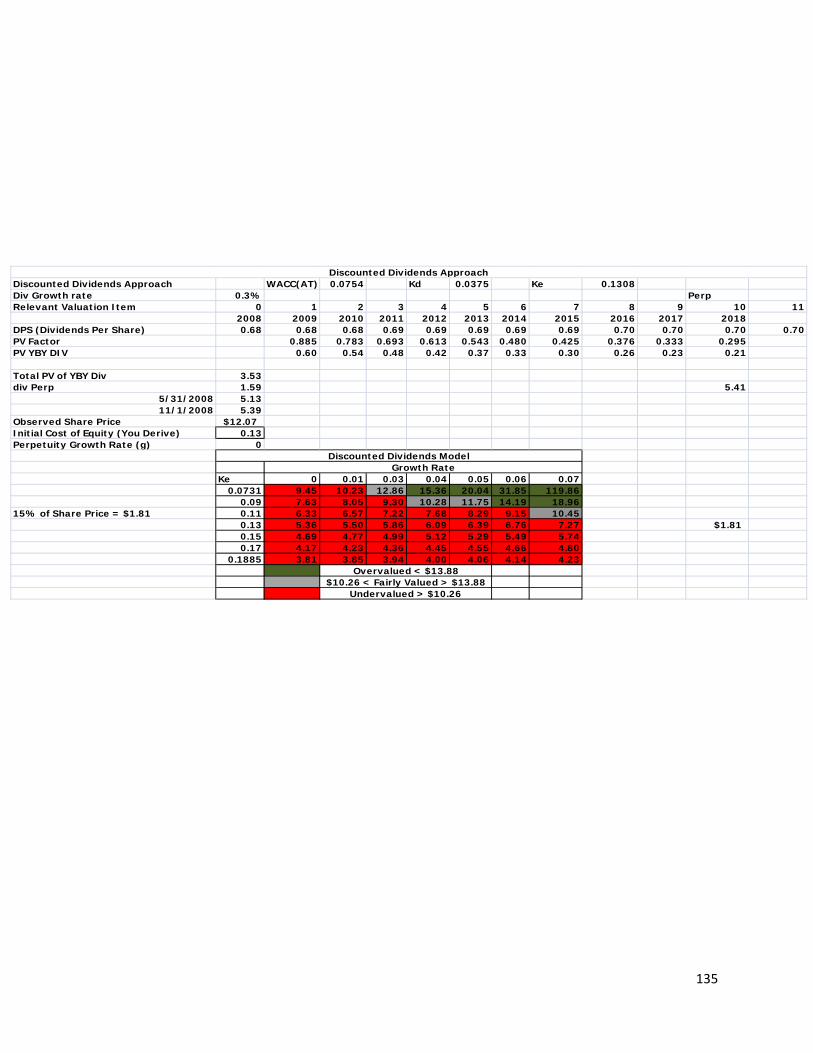

Discounted Dividends Model……………………………………………………….117

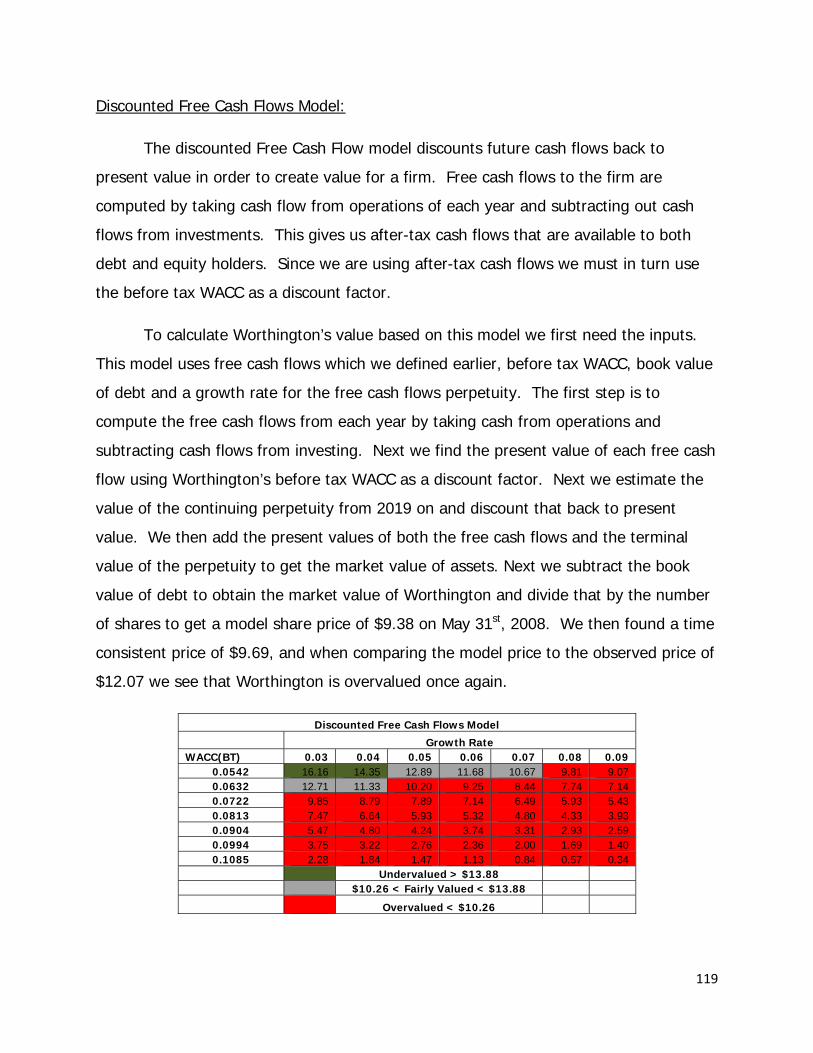

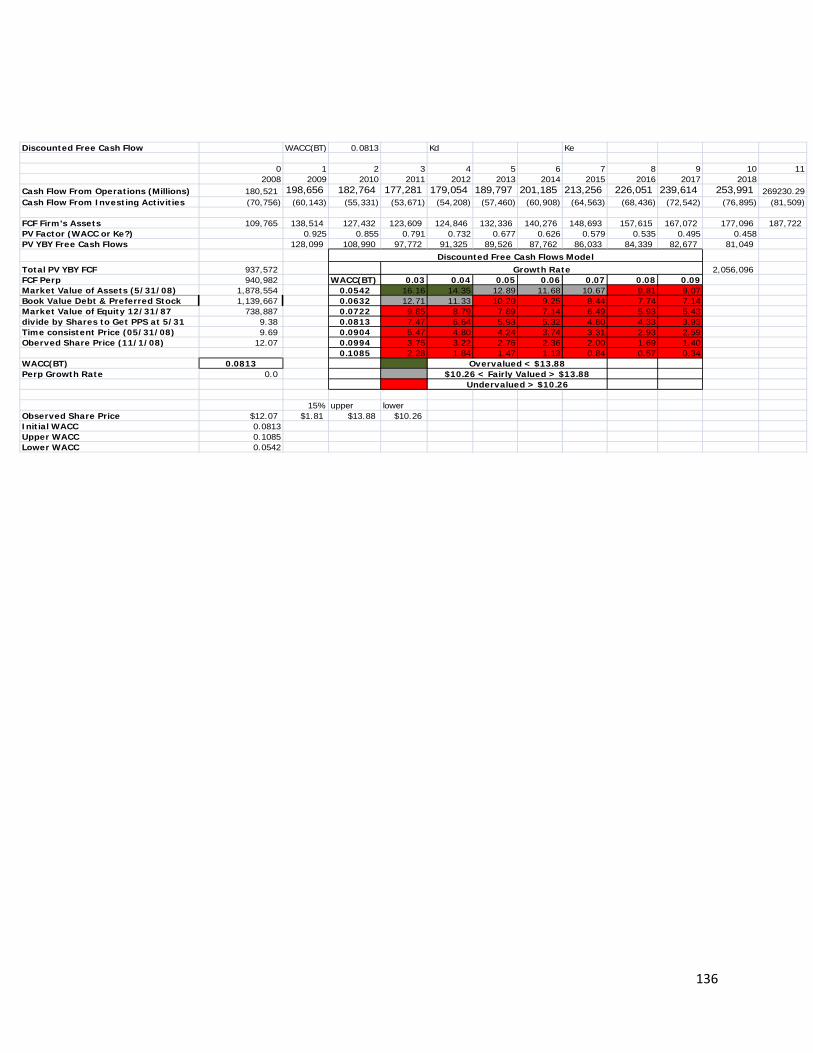

Discounted Free Cash Flows Model…………………………………………….. 119

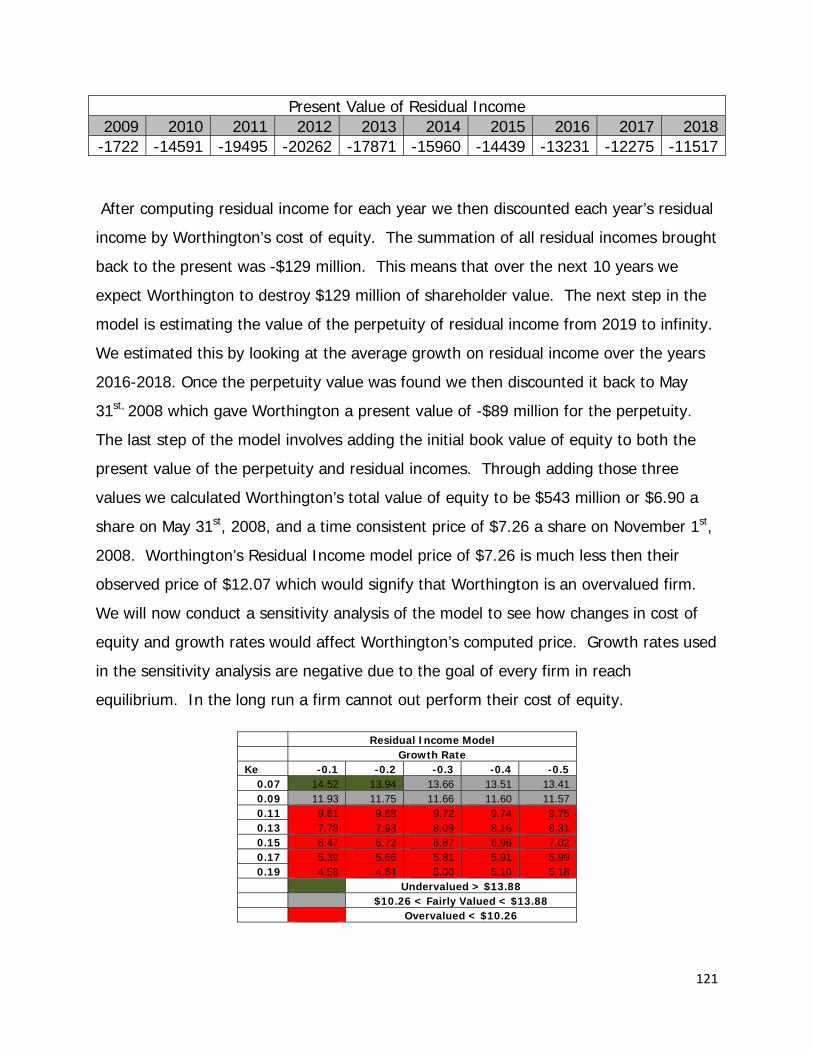

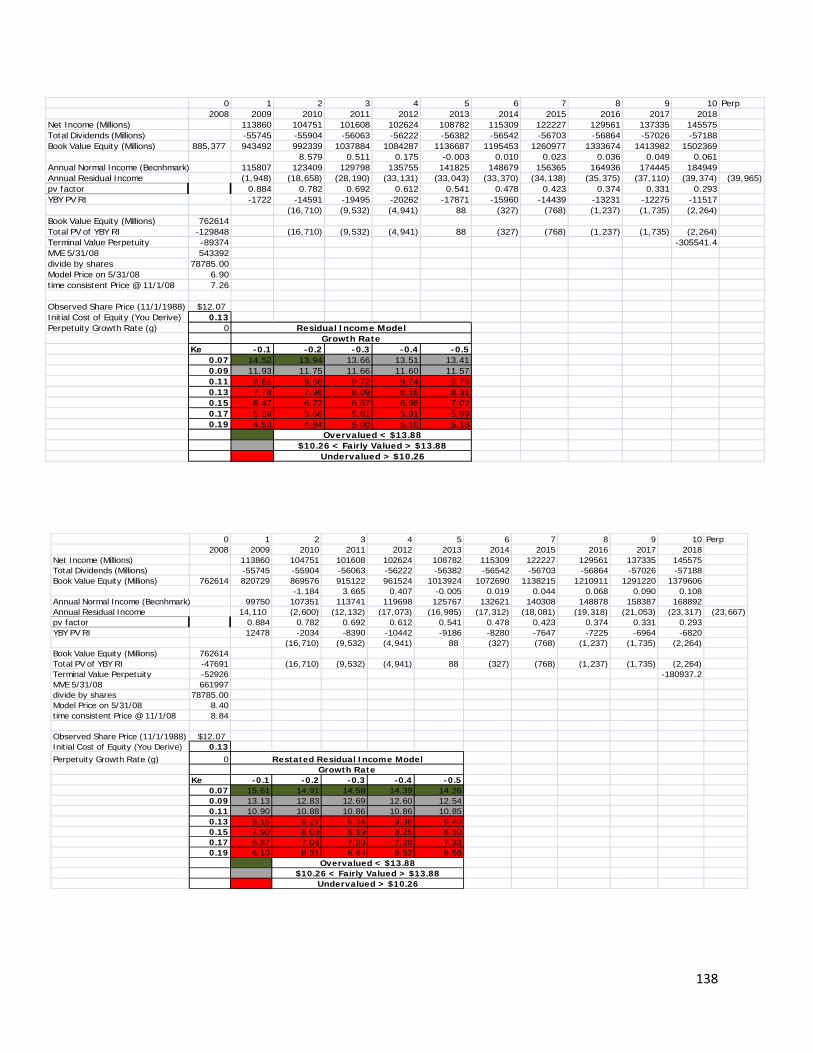

Residual Income Model……………………………………………………………… 120

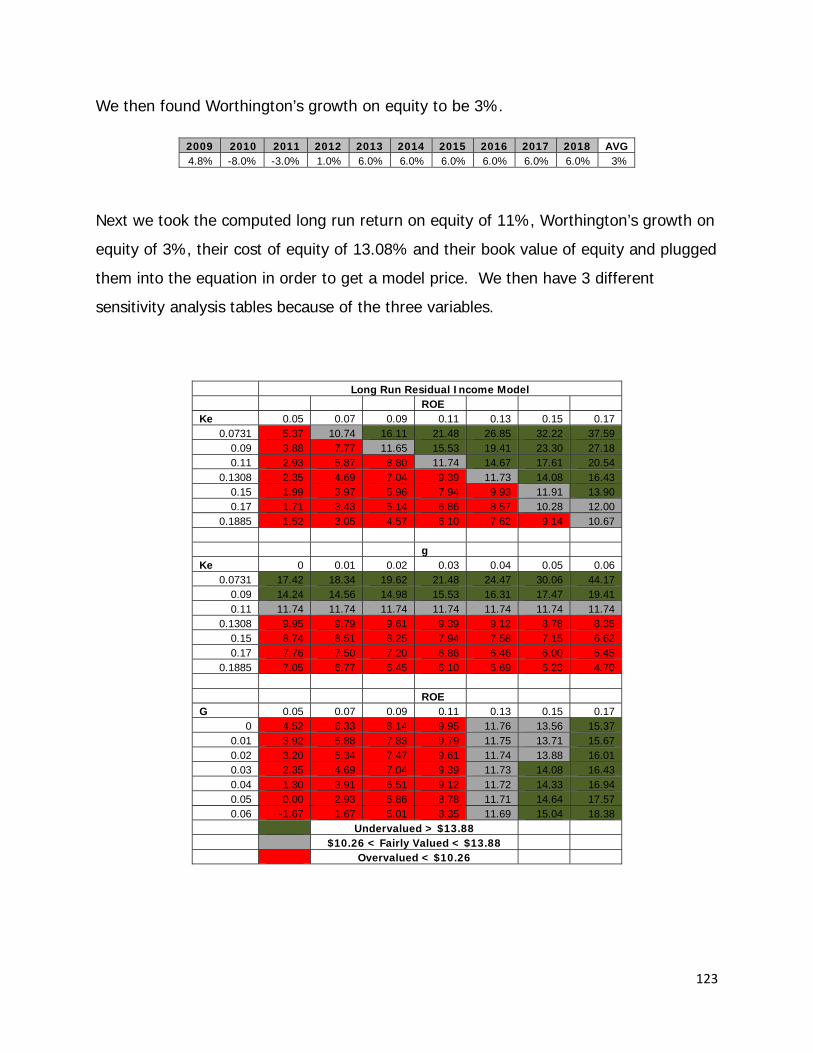

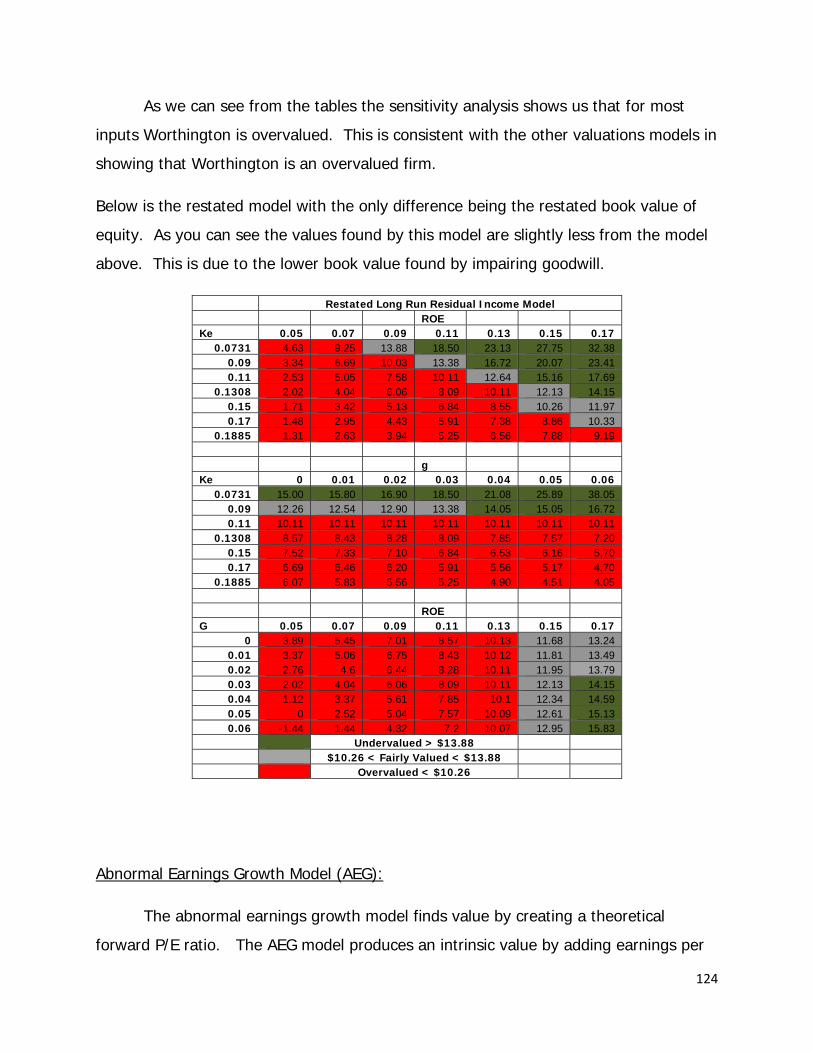

Long Run Residual Income Model………………………………………………. 122

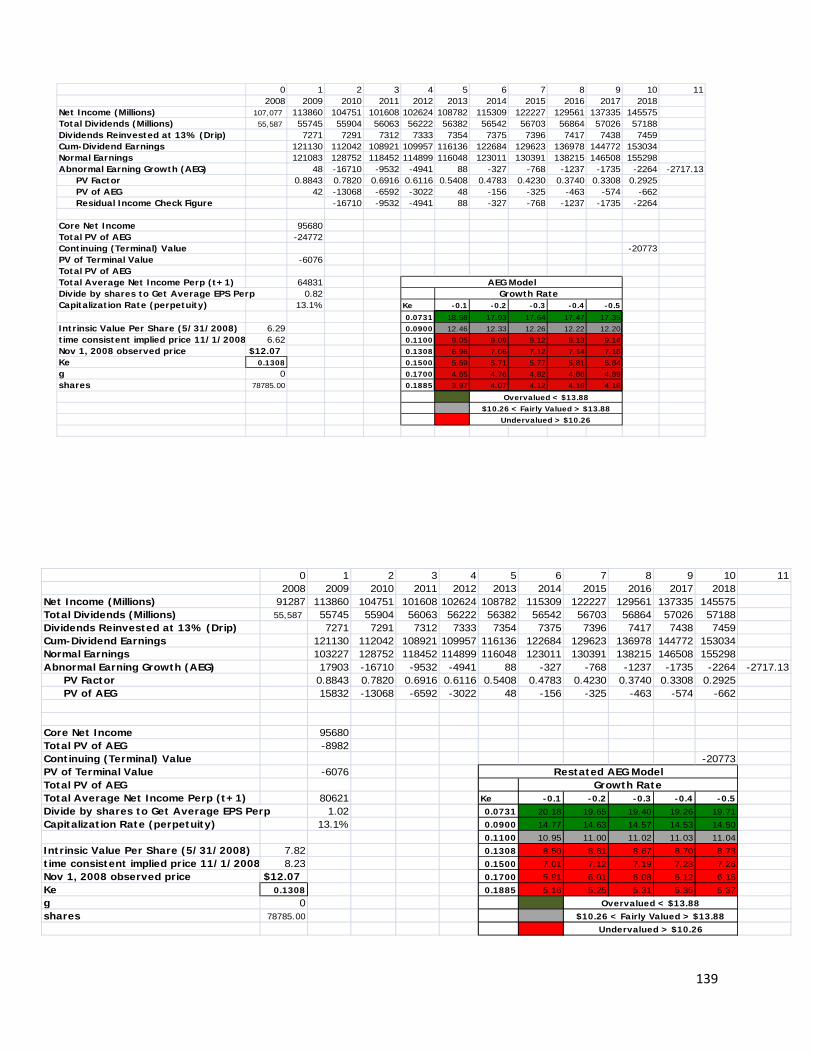

Abnormal Earnings Growth Model……………………………………………… 124

Analyst Recommendation………………………………………………………………………………. 127

Appendices………………………………………………………………………………………………….. 129

References…………………………………………………………………………………………………… 140

8

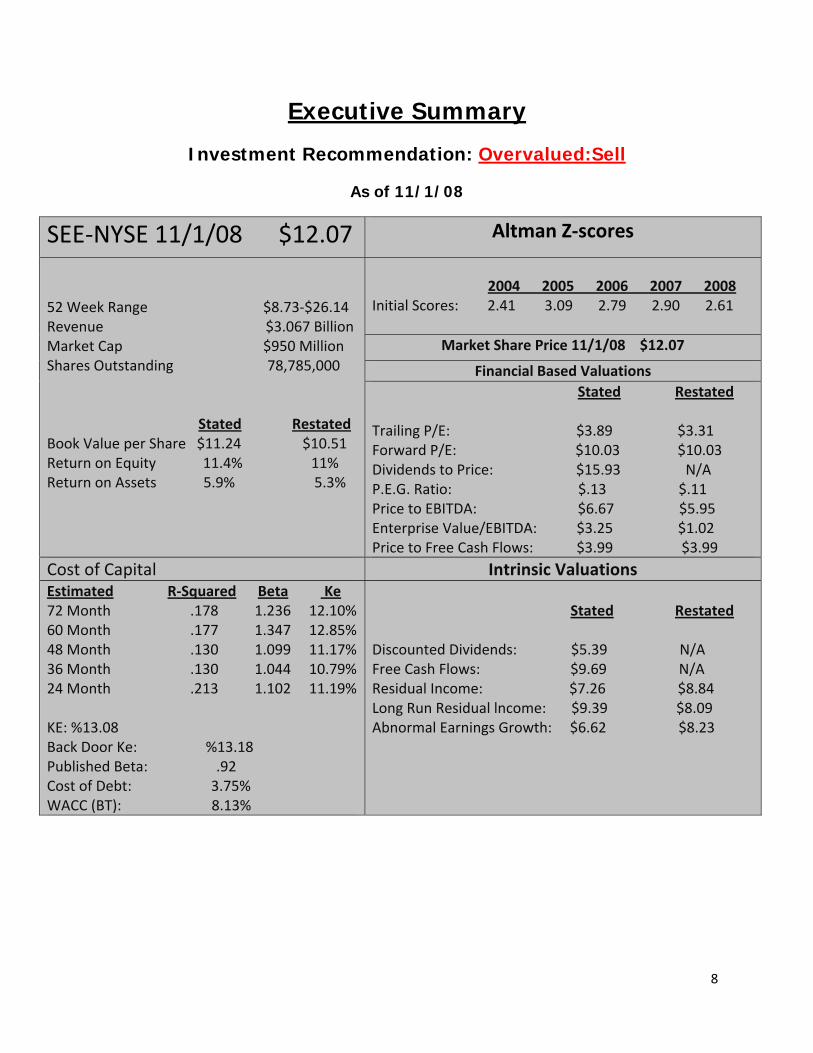

Executive Summary

Investment Recommendation: Overvalued:Sell

As of 11/1/08

SEE‐NYSE 11/1/08 $12.07 Altman Z‐scores

52 Week Range $8.73‐$26.14 Revenue $3.067 Billion Market Cap $950 Million Shares Outstanding 78,785,000 Stated Restated Book Value per Share $11.24 $10.51 Return on Equity 11.4% 11% Return on Assets 5.9% 5.3%

2004 2005 2006 2007 2008 Initial Scores: 2.41 3.09 2.79 2.90 2.61

Market Share Price 11/1/08 $12.07

Financial Based Valuations Stated Restated Trailing P/E: $3.89 $3.31 Forward P/E: $10.03 $10.03 Dividends to Price: $15.93 N/A P.E.G. Ratio: $.13 $.11 Price to EBITDA: $6.67 $5.95 Enterprise Value/EBITDA: $3.25 $1.02 Price to Free Cash Flows: $3.99 $3.99

Cost of Capital Intrinsic Valuations Estimated R‐Squared Beta Ke 72 Month .178 1.236 12.10%60 Month .177 1.347 12.85% 48 Month .130 1.099 11.17% 36 Month .130 1.044 10.79%24 Month .213 1.102 11.19% KE: %13.08 Back Door Ke: %13.18 Published Beta: .92 Cost of Debt: 3.75% WACC (BT): 8.13%

Stated Restated Discounted Dividends: $5.39 N/A Free Cash Flows: $9.69 N/A Residual Income: $7.26 $8.84 Long Run Residual lncome: $9.39 $8.09 Abnormal Earnings Growth: $6.62 $8.23

9

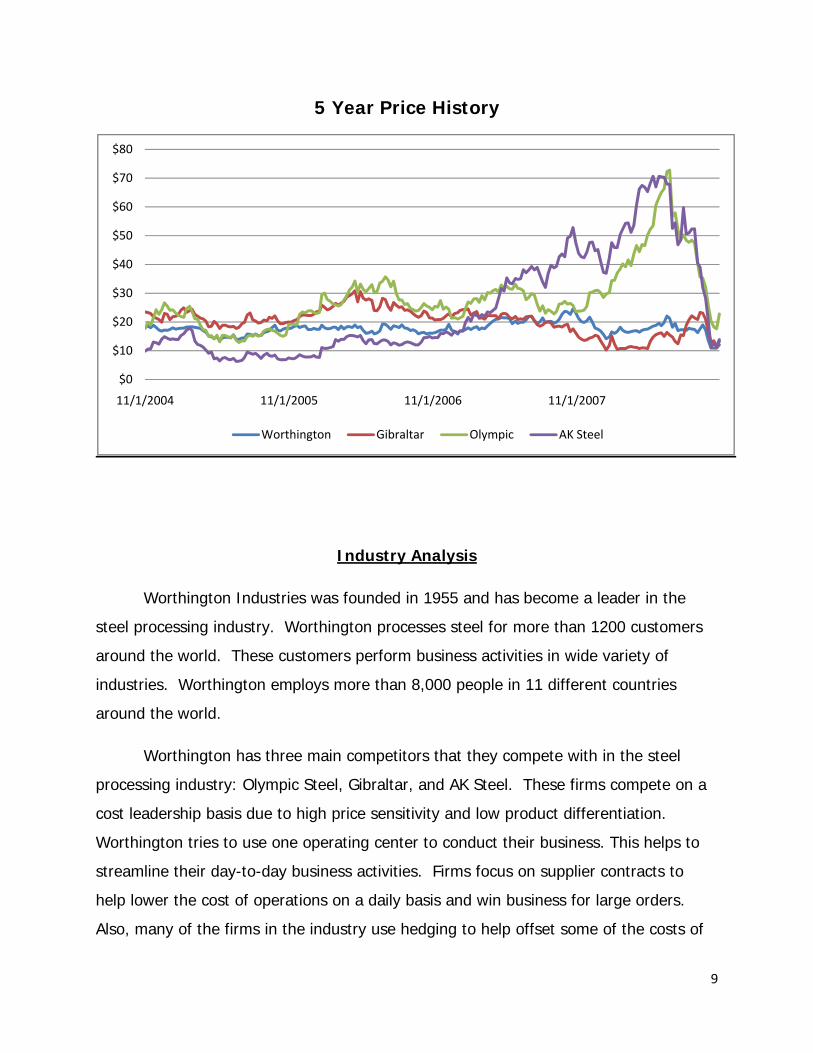

5 Year Price History

Industry Analysis

Worthington Industries was founded in 1955 and has become a leader in the

steel processing industry. Worthington processes steel for more than 1200 customers

around the world. These customers perform business activities in wide variety of

industries. Worthington employs more than 8,000 people in 11 different countries

around the world.

Worthington has three main competitors that they compete with in the steel

processing industry: Olympic Steel, Gibraltar, and AK Steel. These firms compete on a

cost leadership basis due to high price sensitivity and low product differentiation.

Worthington tries to use one operating center to conduct their business. This helps to

streamline their day-to-day business activities. Firms focus on supplier contracts to

help lower the cost of operations on a daily basis and win business for large orders.

Also, many of the firms in the industry use hedging to help offset some of the costs of

$0

$10

$20

$30

$40

$50

$60

$70

$80

11/1/2004 11/1/2005 11/1/2006 11/1/2007

Worthington Gibraltar Olympic AK Steel

10

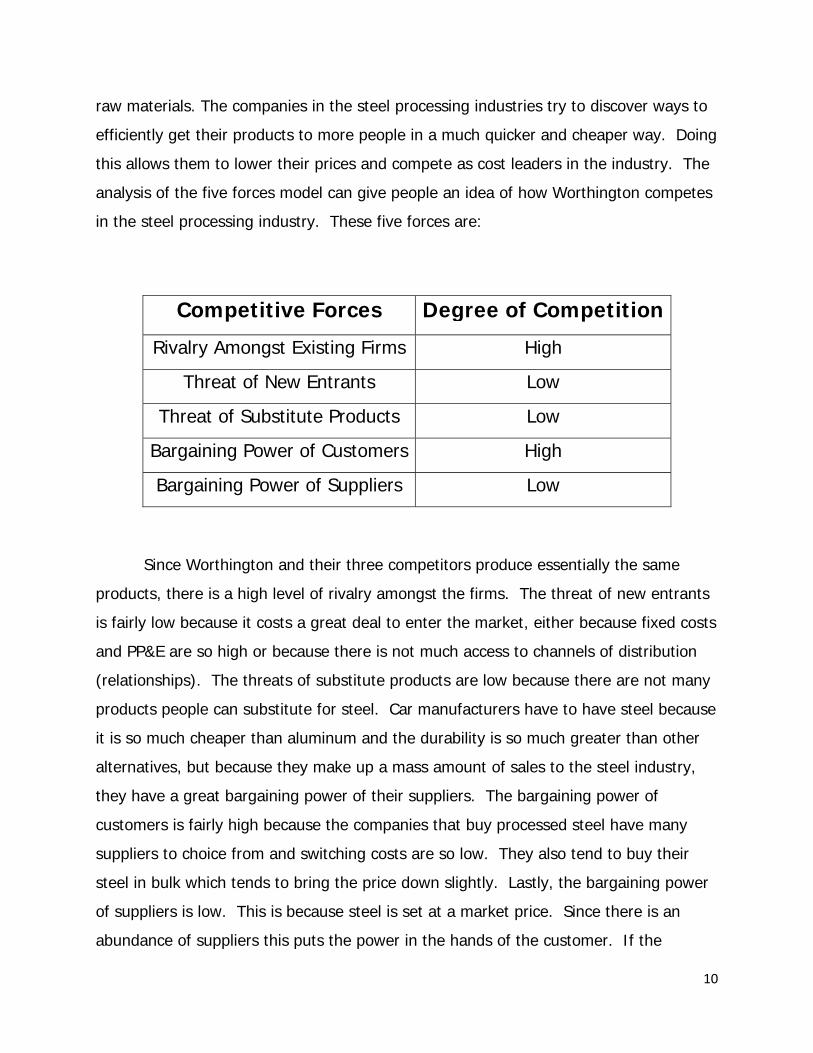

raw materials. The companies in the steel processing industries try to discover ways to

efficiently get their products to more people in a much quicker and cheaper way. Doing

this allows them to lower their prices and compete as cost leaders in the industry. The

analysis of the five forces model can give people an idea of how Worthington competes

in the steel processing industry. These five forces are:

Competitive Forces Degree of Competition

Rivalry Amongst Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products Low

Bargaining Power of Customers High

Bargaining Power of Suppliers Low

Since Worthington and their three competitors produce essentially the same

products, there is a high level of rivalry amongst the firms. The threat of new entrants

is fairly low because it costs a great deal to enter the market, either because fixed costs

and PP&E are so high or because there is not much access to channels of distribution

(relationships). The threats of substitute products are low because there are not many

products people can substitute for steel. Car manufacturers have to have steel because

it is so much cheaper than aluminum and the durability is so much greater than other

alternatives, but because they make up a mass amount of sales to the steel industry,

they have a great bargaining power of their suppliers. The bargaining power of

customers is fairly high because the companies that buy processed steel have many

suppliers to choice from and switching costs are so low. They also tend to buy their

steel in bulk which tends to bring the price down slightly. Lastly, the bargaining power

of suppliers is low. This is because steel is set at a market price. Since there is an

abundance of suppliers this puts the power in the hands of the customer. If the

11

suppliers try to raise prices the firms will be tempted to go somewhere else to buy their

processed steel.

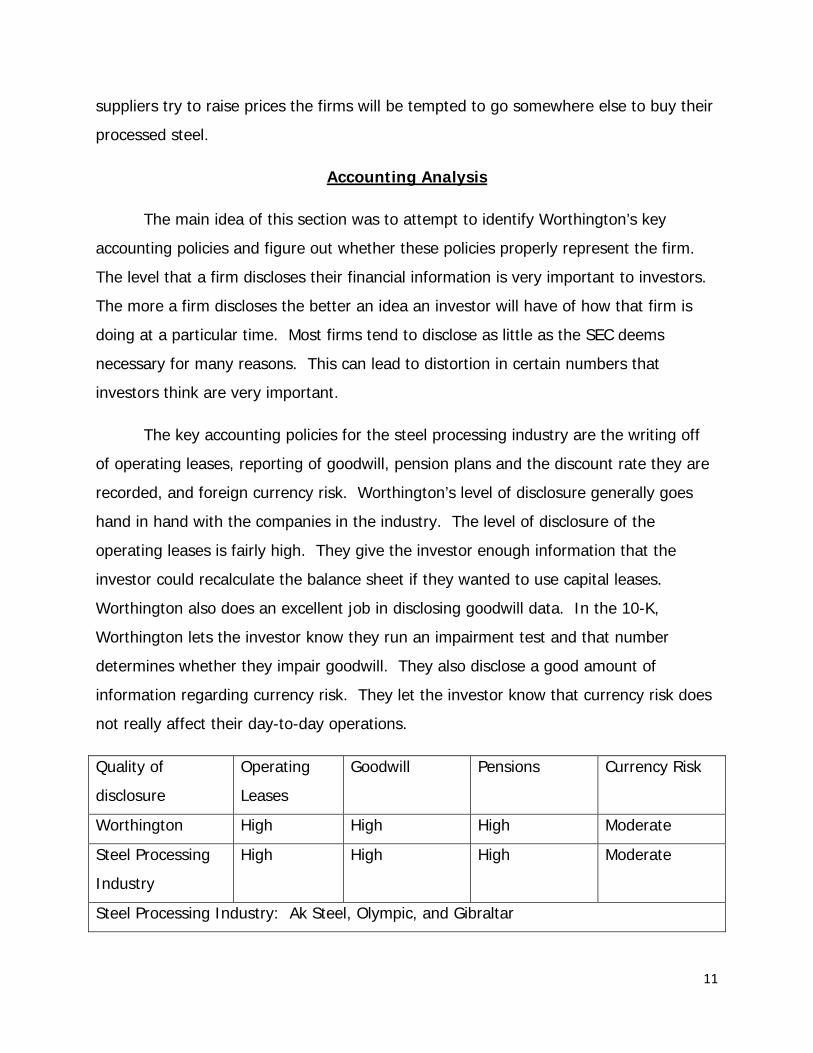

Accounting Analysis

The main idea of this section was to attempt to identify Worthington’s key

accounting policies and figure out whether these policies properly represent the firm.

The level that a firm discloses their financial information is very important to investors.

The more a firm discloses the better an idea an investor will have of how that firm is

doing at a particular time. Most firms tend to disclose as little as the SEC deems

necessary for many reasons. This can lead to distortion in certain numbers that

investors think are very important.

The key accounting policies for the steel processing industry are the writing off

of operating leases, reporting of goodwill, pension plans and the discount rate they are

recorded, and foreign currency risk. Worthington’s level of disclosure generally goes

hand in hand with the companies in the industry. The level of disclosure of the

operating leases is fairly high. They give the investor enough information that the

investor could recalculate the balance sheet if they wanted to use capital leases.

Worthington also does an excellent job in disclosing goodwill data. In the 10-K,

Worthington lets the investor know they run an impairment test and that number

determines whether they impair goodwill. They also disclose a good amount of

information regarding currency risk. They let the investor know that currency risk does

not really affect their day-to-day operations.

Quality of

disclosure

Operating

Leases

Goodwill Pensions Currency Risk

Worthington High High High Moderate

Steel Processing

Industry

High High High Moderate

Steel Processing Industry: Ak Steel, Olympic, and Gibraltar

12

Worthington does an excellent job of letting the investor know what kind of

leases they use and the amounts they are for. They also let the investor know about

the foreign currency acquisitions and how they affect their business. As far as goodwill

goes, Worthington does not impair any goodwill. This causes the assets to be

overstated, which causes the owners equity of the firm to be overstated. This could

lead investors to believe that Worthington is making more money than they really

make. Throughout this report we adjusted the balance sheet and income statement to

represent what would have happened had the goodwill actually been impaired.

Generally speaking, Worthington lets the investor know where they stand financially

speaking. The 10-K report was very concise and has an appropriate amount of

information regarding financial figures.

Financial Analysis, Cost of Capital Estimation, and Forecasting

The first step of performing financial analysis is through the use of ratios. These ratios

can be categorized in three groups: liquidity, profitability, and capital structure. By

using these ratios we can compare Worthington’s performance to its competitor over

time. Liquidity ratios measure how well a company is able to take care of, or pay, their

liabilities. Banks or other types of lenders are interested in these ratios. Liquidity ratios

give a good idea how probable a firm can pay back liabilities, like a loan. Worthington

liquidity ratios, overall, tend to line up with the rest of the industry. Worthington’s

liquidity ratios were stable, on the whole. Profitability ratios indicate how well a firm

translates things, such as assets or equity, into profit. Profitability ratios also compute

how well a firm manages their expenses. Worthington’s profitability ratios were able to

out-perform the industry average on a consistent basis. Capital structure ratios are

ratios that can indicate possible problems and risks. The capital structure ratios,

however, do not use performance measures to judge the possible problems or risks.

Capital structure ratios measure things like how a company finances assets. A company

can finance through borrowing money from lenders or through selling new stock to

13

shareholders. Worthington’s capital structure ratios, similar to the liquidity ratios, were

close to the industry average.

Finding the cost of capital was necessary to value the firm because we needed

proper discount and growth rates related to the firm. We found Worthington’s cost of

equity, cost of debt and their weighted average cost of capital. To find Worthington’s

cost of equity we used regression analysis to determine a beta. From the regressions

we then chose the beta that gave us the most explanatory power of the firms

systematic risk, which is shown by the adjusted R squared from each regression. We

then found Worthington’s cost of equity bay using the capital asset pricing model.

Inputs in this model include the risk free rate, Worthington’s beta of 1.102 and the

market risk premium. For the risk free rate we used the 10-year U.S. Treasury Bill rate

and for the market risk premium we took an average of S&P 500 returns. After using

the capital asset pricing model we computed Worthington’s cost of equity to be

11.18%. But then we had to adjust the risk due to the market size of the firm which

increased Worthington’s cost of equity to 13.08%. Next we found Worthington’s cost of

debt by taking the weighted average of all interest rates of all the firms debt. We

calculated Worthington’s cost of debt to be 3.75%. Now that we have Worthington’s

cost of equity and cost of debt we were able to compute a weighted average cost of

capital both before tax and after tax.

Forecasting Worthington’s financial statement proved to be the most important

part of the financial analysis because valuations are based upon it. We started by

forecasting total sales by estimated growth rates. These growth rates were estimated

on conclusions draw form historical trends and the recent recession. Once we had total

sales forecasted we then used Worthington’s liquidity and profitability ratios to properly

link and forecasted all financial statements. As an example we used Worthington’s

average 5 year asset turnover to link forecasted sales to total assets. Also, the

accuracy of forecasts of the income and balance sheet should be better than the

statement of cash flows. Because cash flows of a firm are erratic and extremely difficult

to predict.

14

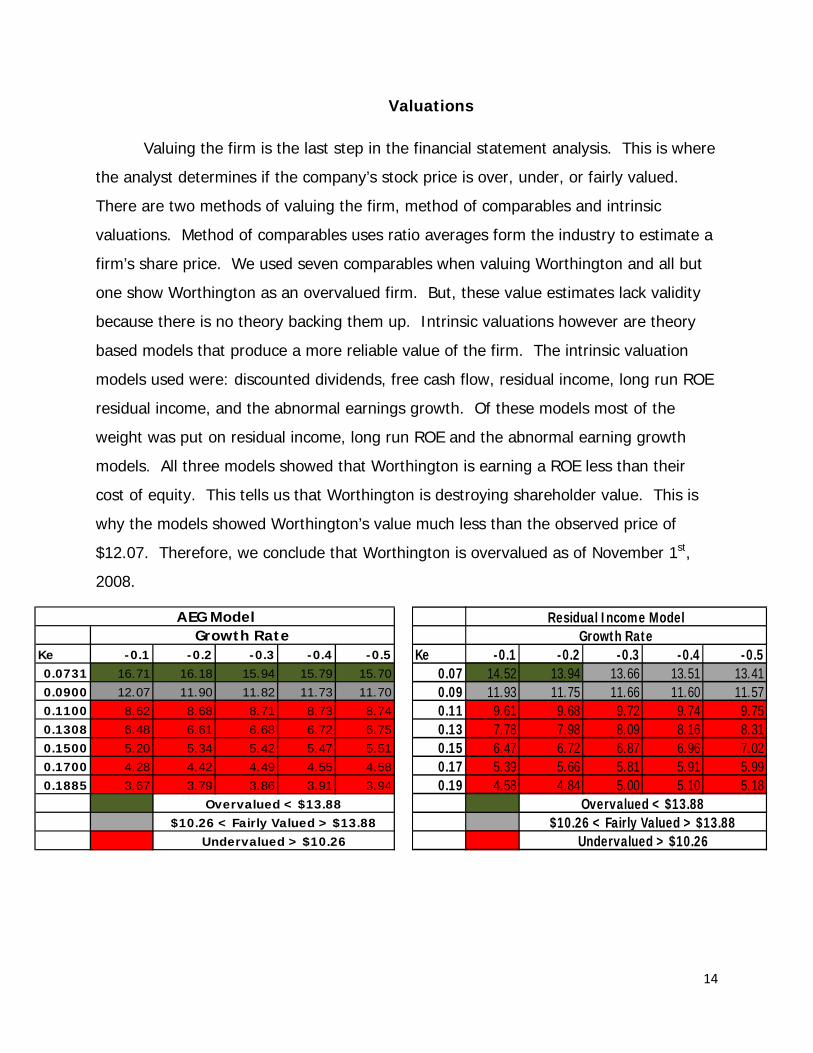

Valuations

Valuing the firm is the last step in the financial statement analysis. This is where

the analyst determines if the company’s stock price is over, under, or fairly valued.

There are two methods of valuing the firm, method of comparables and intrinsic

valuations. Method of comparables uses ratio averages form the industry to estimate a

firm’s share price. We used seven comparables when valuing Worthington and all but

one show Worthington as an overvalued firm. But, these value estimates lack validity

because there is no theory backing them up. Intrinsic valuations however are theory

based models that produce a more reliable value of the firm. The intrinsic valuation

models used were: discounted dividends, free cash flow, residual income, long run ROE

residual income, and the abnormal earnings growth. Of these models most of the

weight was put on residual income, long run ROE and the abnormal earning growth

models. All three models showed that Worthington is earning a ROE less than their

cost of equity. This tells us that Worthington is destroying shareholder value. This is

why the models showed Worthington’s value much less than the observed price of

$12.07. Therefore, we conclude that Worthington is overvalued as of November 1st,

2008.

Ke -0.1 -0.2 -0.3 -0.4 -0.50.0731 16.71 16.18 15.94 15.79 15.700.0900 12.07 11.90 11.82 11.73 11.700.1100 8.62 8.68 8.71 8.73 8.740.1308 6.48 6.61 6.68 6.72 6.750.1500 5.20 5.34 5.42 5.47 5.510.1700 4.28 4.42 4.49 4.55 4.580.1885 3.67 3.79 3.86 3.91 3.94

Overvalued < $13.88$10.26 < Fairly Valued > $13.88

Undervalued > $10.26

Growth RateAEG Model

Ke -0.1 -0.2 -0.3 -0.4 -0.50.07 14.52 13.94 13.66 13.51 13.410.09 11.93 11.75 11.66 11.60 11.570.11 9.61 9.68 9.72 9.74 9.750.13 7.78 7.98 8.09 8.16 8.310.15 6.47 6.72 6.87 6.96 7.020.17 5.39 5.66 5.81 5.91 5.990.19 4.58 4.84 5.00 5.10 5.18

Overvalued < $13.88$10.26 < Fairly Valued > $13.88

Undervalued > $10.26

Growth RateResidual Income Model

15

Overview

Worthington Industries was started and founded in 1955 with its headquarters in

Columbus, Ohio. Since then, they have grown to a corporation with a net market

capital of 1.32 billion dollars. Worthington process’ steel for more than 1200 customers

in various industries across the globe. Their customers include industries in areas such

as agriculture, lawn & garden, hardware, aviation, automotive, office furniture, and

others. Worthington creates many different kinds and shapes of metal. Some of these

include cold rolling, slitting, pickling, primacoat, dry-coating, and others. Fortune

Magazine placed them in the “Top 100 companies to work for in America” in 2006,

2002, 1998, 1997. Its number one priority is to make the shareholders money while

increasing the value of their investments.

They make different metals parts for many different industries. The biggest of

these industries is the automobile industry. A large proportion of Worthington’s sales

are to the “Big 3” here in the United States. Worthington makes many different parts

for them such as frames to bolts.

Worthington operates in three segments: steel processing, metal framing, and

cylinders. The steel processing unit consists of finished steel products primarily used in

automobile manufacturing. The metal framing segment consists of steel framing used in

construction. Worthington’s third segment, cylinders, is a small niche segment

consisting of made-to-order pressure cylinders.

A few of the direct competitors of Worthington are AK Steel, Gibraltar, Nucor,

and Olympic Steel Incorporation. There are different competitors for different areas. In

the steel framing segment, Gibraltar is the biggest competitor. In the steel processing

segment, AK Steel and Olympic Steel are their biggest competitors.

Worthington tries to incorporate all of their operating activities in one location

which makes it easier to communicate within the company. This also reduces freight

cost for its customers. (www.worthingtonsteel.com)

16

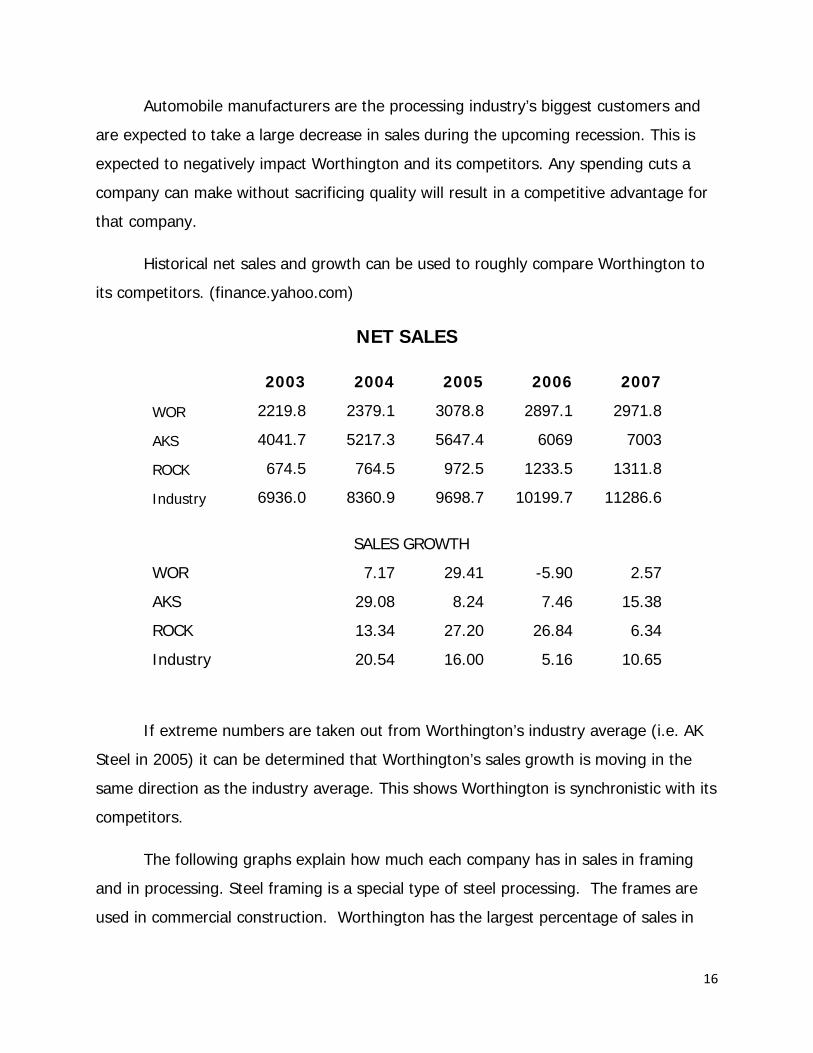

Automobile manufacturers are the processing industry’s biggest customers and

are expected to take a large decrease in sales during the upcoming recession. This is

expected to negatively impact Worthington and its competitors. Any spending cuts a

company can make without sacrificing quality will result in a competitive advantage for

that company.

Historical net sales and growth can be used to roughly compare Worthington to

its competitors. (finance.yahoo.com)

NET SALES

2003 2004 2005 2006 2007

WOR 2219.8 2379.1 3078.8 2897.1 2971.8

AKS 4041.7 5217.3 5647.4 6069 7003

ROCK 674.5 764.5 972.5 1233.5 1311.8

Industry 6936.0 8360.9 9698.7 10199.7 11286.6

SALES GROWTH

WOR 7.17 29.41 -5.90 2.57

AKS 29.08 8.24 7.46 15.38

ROCK 13.34 27.20 26.84 6.34

Industry 20.54 16.00 5.16 10.65

If extreme numbers are taken out from Worthington’s industry average (i.e. AK

Steel in 2005) it can be determined that Worthington’s sales growth is moving in the

same direction as the industry average. This shows Worthington is synchronistic with its

competitors.

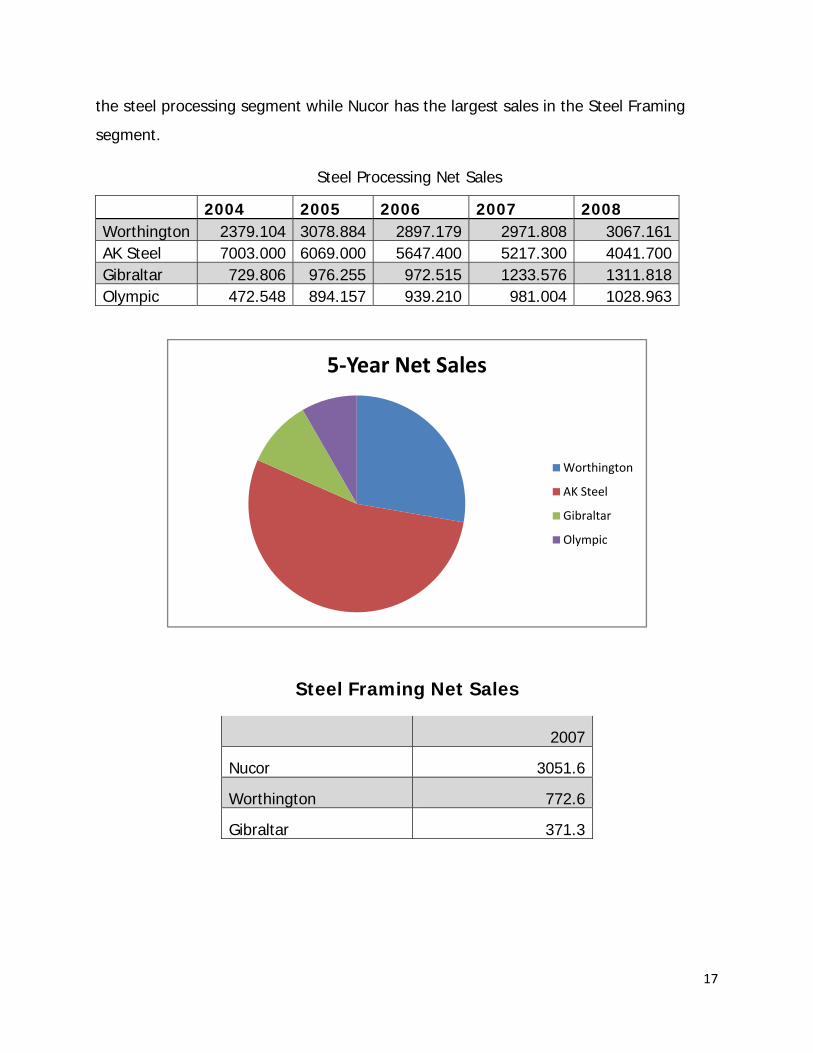

The following graphs explain how much each company has in sales in framing

and in processing. Steel framing is a special type of steel processing. The frames are

used in commercial construction. Worthington has the largest percentage of sales in

17

the steel processing segment while Nucor has the largest sales in the Steel Framing

segment.

Steel Processing Net Sales

2004 2005 2006 2007 2008 Worthington 2379.104 3078.884 2897.179 2971.808 3067.161AK Steel 7003.000 6069.000 5647.400 5217.300 4041.700Gibraltar 729.806 976.255 972.515 1233.576 1311.818Olympic 472.548 894.157 939.210 981.004 1028.963

Steel Framing Net Sales

2007

Nucor 3051.6

Worthington 772.6

Gibraltar 371.3

5‐Year Net Sales

Worthington

AK Steel

Gibraltar

Olympic

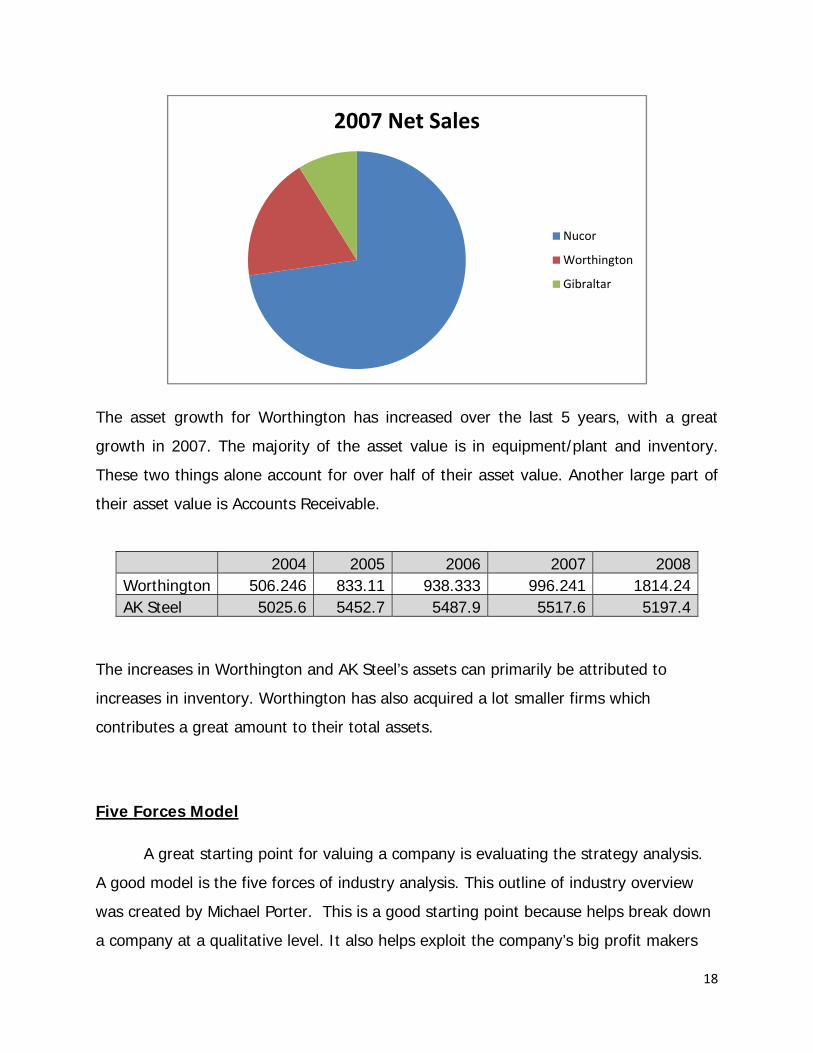

18

The asset growth for Worthington has increased over the last 5 years, with a great

growth in 2007. The majority of the asset value is in equipment/plant and inventory.

These two things alone account for over half of their asset value. Another large part of

their asset value is Accounts Receivable.

2004 2005 2006 2007 2008Worthington 506.246 833.11 938.333 996.241 1814.24AK Steel 5025.6 5452.7 5487.9 5517.6 5197.4

The increases in Worthington and AK Steel’s assets can primarily be attributed to

increases in inventory. Worthington has also acquired a lot smaller firms which

contributes a great amount to their total assets.

Five Forces Model

A great starting point for valuing a company is evaluating the strategy analysis.

A good model is the five forces of industry analysis. This outline of industry overview

was created by Michael Porter. This is a good starting point because helps break down

a company at a qualitative level. It also helps exploit the company’s big profit makers

2007 Net Sales

Nucor

Worthington

Gibraltar

19

and the big risk takers of the company. The five areas in this type of analysis are:

rivalry among existing firms, threat of new entrants, threat of substitute products,

bargaining power of buyer, and bargaining power of suppliers. The first three areas

involve the potential sources of competition in an industry (Palepu and Healy 2-20).

The last two areas discussed focus on how profits are affected by the industries

bargaining power with its customers and suppliers. Individually the five forces may not

provide much detail for the business. When viewed as a whole, the five forces model

can be very helpful when trying to determine what drives the profit in a firm’s industry.

Competitive Forces Degree of CompetitionRivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products Low

Bargaining Power of Customers High

Bargaining Power of Suppliers Low

The threat of existing firms is considerably higher than others because of the low steel

processing industry concentration. The bargaining power of suppliers is low because

costs and prices have been cut already quite a bit. The bargaining power is high also.

When there is not a big difference in products from one firm to another, it is much

easier for customers to shop from one to another. Therefore, companies must keep

their prices low to compete with existing firms.

Rivalry Among Existing Firms

If an industry is highly competitive, as the steel processing industry proves to be,

cost leadership tends to be the most common used. Competition in the steel processing

industry is intense to the point that firms in the industry drive the prices downward

closer to marginal costs to get the business of customers. There are many factors that

20

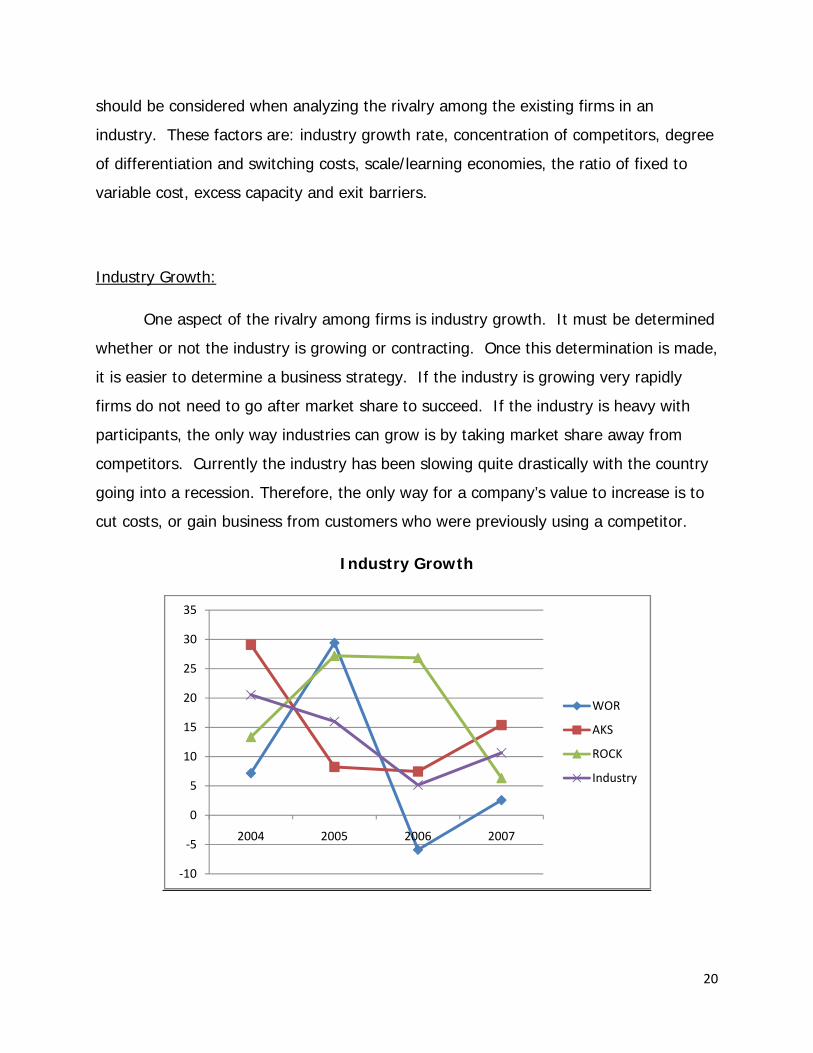

should be considered when analyzing the rivalry among the existing firms in an

industry. These factors are: industry growth rate, concentration of competitors, degree

of differentiation and switching costs, scale/learning economies, the ratio of fixed to

variable cost, excess capacity and exit barriers.

Industry Growth:

One aspect of the rivalry among firms is industry growth. It must be determined

whether or not the industry is growing or contracting. Once this determination is made,

it is easier to determine a business strategy. If the industry is growing very rapidly

firms do not need to go after market share to succeed. If the industry is heavy with

participants, the only way industries can grow is by taking market share away from

competitors. Currently the industry has been slowing quite drastically with the country

going into a recession. Therefore, the only way for a company’s value to increase is to

cut costs, or gain business from customers who were previously using a competitor.

Industry Growth

‐10

‐5

0

5

10

15

20

25

30

35

2004 2005 2006 2007

WOR

AKS

ROCK

Industry

21

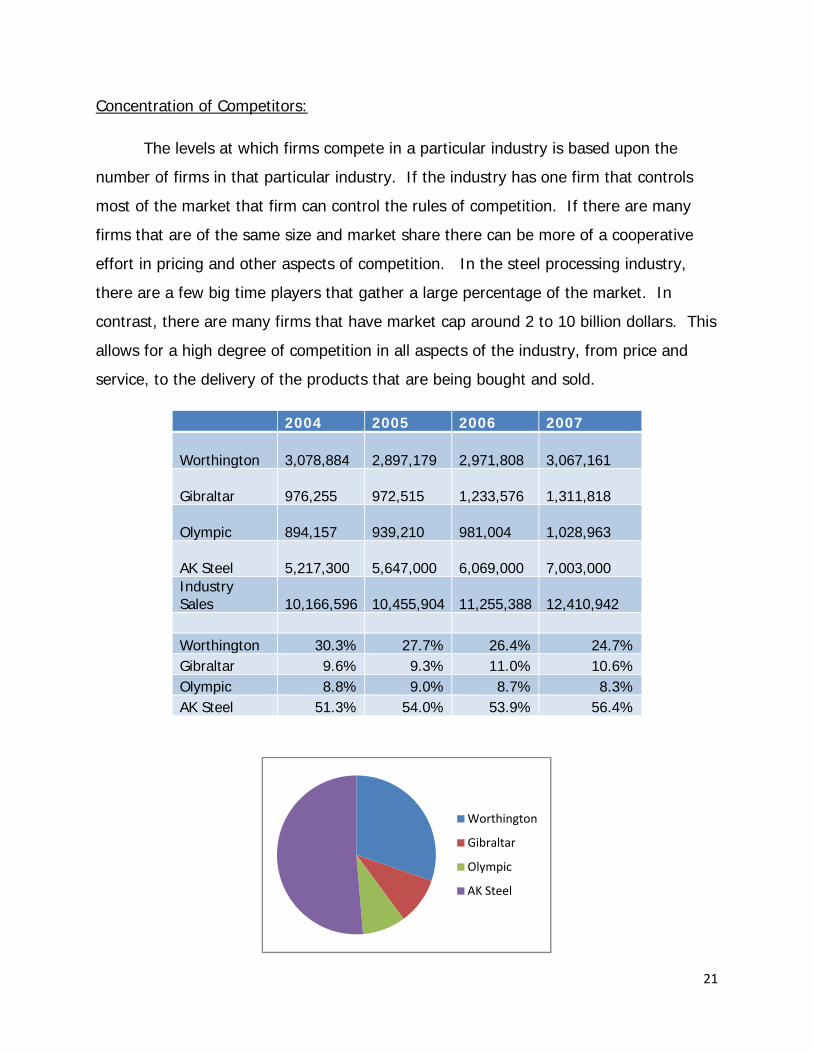

Concentration of Competitors:

The levels at which firms compete in a particular industry is based upon the

number of firms in that particular industry. If the industry has one firm that controls

most of the market that firm can control the rules of competition. If there are many

firms that are of the same size and market share there can be more of a cooperative

effort in pricing and other aspects of competition. In the steel processing industry,

there are a few big time players that gather a large percentage of the market. In

contrast, there are many firms that have market cap around 2 to 10 billion dollars. This

allows for a high degree of competition in all aspects of the industry, from price and

service, to the delivery of the products that are being bought and sold.

2004 2005 2006 2007

Worthington 3,078,884

2,897,179

2,971,808

3,067,161

Gibraltar 976,255

972,515

1,233,576

1,311,818

Olympic 894,157

939,210

981,004

1,028,963

AK Steel 5,217,300

5,647,000

6,069,000

7,003,000

Industry Sales

10,166,596

10,455,904

11,255,388

12,410,942

Worthington 30.3% 27.7% 26.4% 24.7% Gibraltar 9.6% 9.3% 11.0% 10.6% Olympic 8.8% 9.0% 8.7% 8.3% AK Steel 51.3% 54.0% 53.9% 56.4%

Worthington

Gibraltar

Olympic

AK Steel

22

As the graphs above shows, the percent of Worthington’s sells in comparison to

the industry has been dropping at a fairly constant rate in the last 4 years, while AK

Steel’s and Olympic Steel’s stay pretty constant and Gibraltar’s goes up than back

down, but still finishing higher than they did in 2004. Although it appears that AK Steel

holds the largest proportion, AK Steel has considerably more segments than the rest of

the firms in the steel processing industry. Worthington holds a smaller proportion than

AK Steel but much larger than the other two firms of Olympic and Gibraltar. This

proves that the steel processing industry concentration is low.

Level of Differentiation:

One of the ways that firms can avoid direct competition depends on how the

firms can differentiate their products and services. If there is low product

differentiation in the industry, firms will tend to compete on price. A higher level of

differentiation allows a firm to set a higher price. Although there are many ways to

manufacture and produce steel products, the finished goods are mostly identical.

Therefore, because the mass amount of the products produced from each firm at

identical, the competition comes back to price and a firm’s ability to control its cost to

be able to reduce the cost.

Switching Cost:

Another risk a company has to watch is their customers’ switching costs. If a

customer of the firm can easily change from one steel processing company to the next,

it wouldn’t take much for the customer to start dealing with a competitor. Within the

steel processing industry, switching costs are low. According to both companies’ 10-Ks,

Worthington and AK Steel process steel for the “Big Three” in the United States

automotive industry. If one of the “Big Three” are dissatisfied with AK Steel, there

wouldn’t be much of a drop off or penalty to switch to Worthington and vice-versa.

23

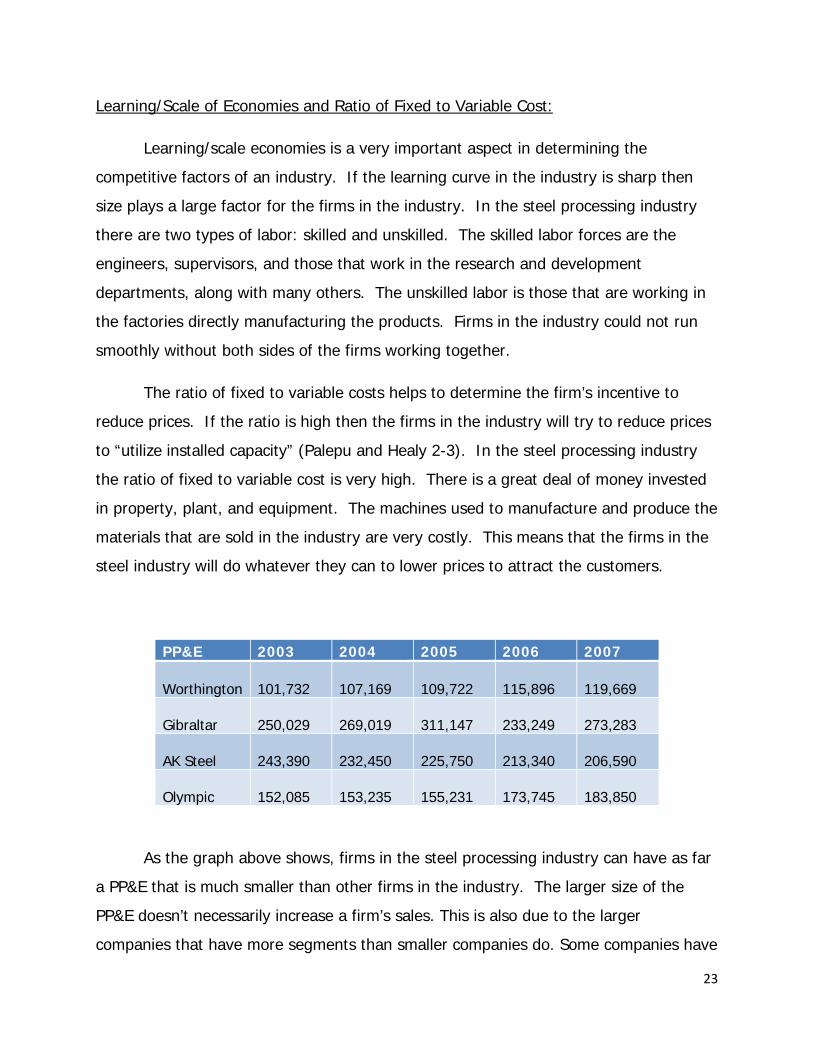

Learning/Scale of Economies and Ratio of Fixed to Variable Cost:

Learning/scale economies is a very important aspect in determining the

competitive factors of an industry. If the learning curve in the industry is sharp then

size plays a large factor for the firms in the industry. In the steel processing industry

there are two types of labor: skilled and unskilled. The skilled labor forces are the

engineers, supervisors, and those that work in the research and development

departments, along with many others. The unskilled labor is those that are working in

the factories directly manufacturing the products. Firms in the industry could not run

smoothly without both sides of the firms working together.

The ratio of fixed to variable costs helps to determine the firm’s incentive to

reduce prices. If the ratio is high then the firms in the industry will try to reduce prices

to “utilize installed capacity” (Palepu and Healy 2-3). In the steel processing industry

the ratio of fixed to variable cost is very high. There is a great deal of money invested

in property, plant, and equipment. The machines used to manufacture and produce the

materials that are sold in the industry are very costly. This means that the firms in the

steel industry will do whatever they can to lower prices to attract the customers.

PP&E 2003 2004 2005 2006 2007

Worthington 101,732

107,169

109,722

115,896

119,669

Gibraltar 250,029

269,019

311,147

233,249

273,283

AK Steel 243,390

232,450

225,750

213,340

206,590

Olympic 152,085

153,235

155,231

173,745

183,850

As the graph above shows, firms in the steel processing industry can have as far

a PP&E that is much smaller than other firms in the industry. The larger size of the

PP&E doesn’t necessarily increase a firm’s sales. This is also due to the larger

companies that have more segments than smaller companies do. Some companies have

24

more specific fields than their competitors. The PP&E does make up a mass amount of

every company’s assets. Worthington’s PP&E has been growing over the years just as

Olympics’, while their competitors have been declining.

Excess Capacity:

Excess capacity in an industry has to do with supply and demand. If supply

exceeds demand there will be a strong incentive for firms to lower cost to increase

sales. In the steel processing industry, most of the firms base their production on the

customer orders. In most cases, excess capacity is not an issue. Most of the firms in

the steel processing industry have a number of operations centers that are used for

customers to receive their products in a timely manner. This strategy keeps inventories

down and allows the steel companies to only produce what the customers need. This,

in turn, keeps the excess capacity to a minimum. The problem of excess capacity can

be increased a great deal if the barriers to exit are high. Exit barriers are extremely

high in the industry. The highly specialized equipment that is needed for production

makes for low resale value. In addition, the factory employees are unionized and have

pension plans that must be taken into account.

Exit Barriers:

Exit Barriers are very costly, especially in the steel industry because the PP&E are

so expensive and specific. Not many people need steel processing plants. Therefore, it

is very hard to sell any of the PP&E. So, companies will do everything they can to

prevent this from happening, making competition that much steeper.

Conclusion:

Because rivalry among the companies is very high, it is important to get a clear

picture of what is taking place in the industry. Starting with the analysis of the industry

growth, concentration and balance of the competitors, degree of differentiation,

switching costs, scale/learning economies, excess capacity and exit barriers, one can

get a good idea of where a firm needs to be and which pricing strategy should be used.

25

Also, because the steel industry is so competitive, expensive to for new entries, and

specialized, this industry is high cost competitive.

Threat of New Entrants

The second competitive force is the threat of new entrants. The threat of new

entrants to a market exists for every firm. If an industry is making abnormal amounts of

profits, this make is a prime candidate for new entrants. This competitive force plays a

large part in the pricing structure of existing firms within the market. There are several

factors that should be taken into account. These factors are: economies of scale, first

mover advantage, access to channels of distribution and relationships, and legal

barriers. All of these factors play a part in determining the profitability of a firm as new

firms enter the already existing market. But, because of the competitiveness of the

industry, and the costs to start, makes it very tough for new entrants.

Economies of Scale:

The first factor to consider when discussing the threat of new entrants is

economies of scale. The term ‘economies of scale’ refers to how much the cost per unit

decreases as a firm increases output. When large economies of scale exist, new firms

may have to choose between investing in large capacity, or entering with a lower

capacity than desired. These choices may be very critical. If a firm does not have the

proper capacity they may not have enough resources to compete with existing firms.

This will put new entrants in the market at a major disadvantage.

For the steel processing industry, the high economies of scale is a major

deterrent for new firms into this market. The high initial start up cost and the technical

nature of the production systems used to produce steel are two factors that lead to the

high level of economies of scale. Furthermore, companies would need a large amount

26

of capital to be able to compete on the same level as the firms that already exist in the

rather large steel processing market.

First Mover Advantage:

The first mover advantage is established when a company moves into a market

and establishes rights that are exclusive to one firm. First movers are able to obtain

contracts or other agreements with suppliers that are difficult to obtain otherwise. First

movers would have an advantage due to lower raw materials costs, and better

negotiate contracts.

In the steel processing industry, which is a fairly homogeneous field among the

industry, the first mover advantage has a low deterrent level on firms that may want to

join the market. The industry standards are the same for all firms in the industry. All

firms also have to abide by the same environmental standards. In addition, suppliers

provide the same raw materials to most companies and the price they pay is generally

based on the quantity ordered.

Access to Channels of Distribution and Relationships

This is a factor that hinders many new firms from entering a particular market,

especially in an industry that has been around for long time and relationships have

been going on for decades. Once relationships are formed and channels of distribution

are established, the cost of developing new channels can be rather high. Some existing

companies have relationships with particular suppliers that go back a long time. With

these relationships comes a sense of trust that money may not be able to surpass.

For example in 1995, Worthington made an agreement with North Star steel

company who is a supplier, to build the biggest plant they have adjacent with North

Star. An agreement like this basically locks up Worthington’s relationship with North

27

Star since they are adjacent with them. It will be highly expensive for any other steel

company to come take the business away from Worthington. And because North Star is

the thirteenth largest steel producer in the world, this is a very important relationship

for Worthington, so Worthington will do just about whatever it takes to keep this

relationship. (http://findarticles.com/p/articles/mi_m0EIN/is_/ai_16934172)

In the steel processing industry, a lack of a relationship within the channels of

distribution leads to a lower bargaining power. Most firms get most raw materials from

a limited number of suppliers. This helps to develop good relationships with a particular

supplier. The better relationship with suppliers, the better price steel processing

companies are likely to receive. These actions may deter new firms from being able to

acquire the same goods for the same price.

Legal Barriers

The last factor to consider is the legal barriers that must be overcome. In many

research-intensive industries, the price of patents and copyrights alone are enough to

deter new firms from entering the market. Licensing agreements are also legal barriers

firms must overcome before they can consider entering a market. Most companies

require a legal department to help with the daily operations that are required to keep a

firms head above water.

For instance, in Worthington’s 2008 10-k, they have trademark and patent costs

of only $11,364, which is very small in comparison to the rest of the costs in the

company.

Conclusion

In conclusion, the threat of new entrants into the steel processing market is very

low. The majority of firms in this market have been around for a large amount of

28

years, with relationships that have been around for a long time. Because of this, for a

new entry to be able to take business away from another is very expensive and

unlikely. Between the required high economies of scale, the extreme high costs of

PP&E to get started, the access to channels of distribution and relationships, one can

conclude it will be difficult for a new firm to enter the steel processing industry.

Threat of Substitute Product

Firms in an industry should be aware of the possible substitute products. If the firms in

the steel processing industry are not prepared for the substitute products, they will be

out of the loop. The substitute products for the steel processing industry include

aluminum, wood, and heavy-duty plastic.

Relative Price and Performance

Aluminum is one type of substitute product for steel. When a car manufacturer wants

to make the car lighter like in high performance sports cars, aluminum would be a

sensible choice. What has to be taken into consideration for the substitution, however,

is the price of aluminum relative to steel.

(http://xnet3.uss.com/auto/steelvsal/cost.htm)

29

In the graph above, it shows the price of steel in comparison to aluminum, in which

steel is almost 3 times cheaper than aluminum, and twice as strong. Because of this, it

will be very tough for aluminum to be able to replace steel has alternative, especially in

the automobile industry which is a large percentage of Worthington’s sales.

Steel, however, is the pricier alternative in the construction business. Most residential

builders opt to use wood for framing. Wood is much cheaper, but it is not as strong.

But for large buildings, steel is used because of its strength and price.

Customer’s willingness to switch

Not all customers’ wants are alike. A large amount of our customers are the “Big

3” automobile industry and construction. A low-end car manufacturer might not be

willing to put forth twice the amount of money in order to make their cars weigh less.

A higher-end sports car manufacturer that doesn’t want to use carbon-fiber would be

more likely to forgo the price penalty in order to improve car performance.

30

A single story residential building can use a weaker material than steel, such as

wood. On the other hand, a multi-story skyscraper could not stand if it were framed

with wood. A commercial builder would opt to pay the premium for the steel in order

to provide the needed strength to accomplish the build. Commercial builders use steel

framing to build the much bigger structures and need steel to do so rather than wood.

Conclusion

The customers in the steel industry have already chosen steel. The only

possibility customers that would leave steel for a different material would be for either a

rise in steel price, a decrease in the price of aluminum, or an increase in a lower quality

substitute’s attributes. And the price of aluminum is so much more than steel, one can

pretty confident that this will not happen anytime soon. Also, with car safety ratings

becoming so important, and the weakness of aluminum, steel for the automobile is the

only product they can use that can accomplish what they need.

Bargaining Power of Customers

Customers can have a leg up on their suppliers if the customer can switch

between companies without a loss in profit. And with the competitiveness of the steel

industry, there is a fair threat of this. But as we stated before, relationships are very

important and are respected from both the customers and suppliers. Also, because the

products of steel from one company to another are so similar, and prices are so evenly

matched, switching to another supplier is not that common. Price sensitivity plays the

main role in a customer to switch to another supplier.

31

Price Sensitivity

The abundance of companies in the steel industry makes a competitive market.

The competitive market leads to competitive pricing. The customers, especially in

construction, buy large volumes of steel framing. The steel companies are eager to do

business with the high volume orders from the customers. The steel companies are

more apt to lower prices to stay competitive to earn business. And anything a company

can do to help lock up long term contracts, they will do. And going back to

relationships, most customers will give their supplier first hand when comes to renewing

contracts, but again this puts the pressure back on the supplier to keep their prices low

so they can renew their business.

Relative Bargaining Power

Companies buying processed steel have many options. There are plenty of steel

companies for them to choose from. This puts the bargaining power in the customer’s

hands. If a customer is dissatisfied with the quality or the price of the steel good, the

customer can change suppliers. The high volume in an order looks attractive to the

supplier. The customer wants a discount for the volume and the supplier is willing to

cooperate. Therefore, customers will make large orders so they can drive down the

price. Every company in the steel processing industry will lower their prices to compete

and try to get the business of the customer.

In addition, switching costs, which is the costs that would occur of switching

suppliers, is relatively low. This plays in favor of the customer to be able to bargain and

shop for cheaper prices. So suppliers must do everything they can to keep or earn the

business of suppliers.

32

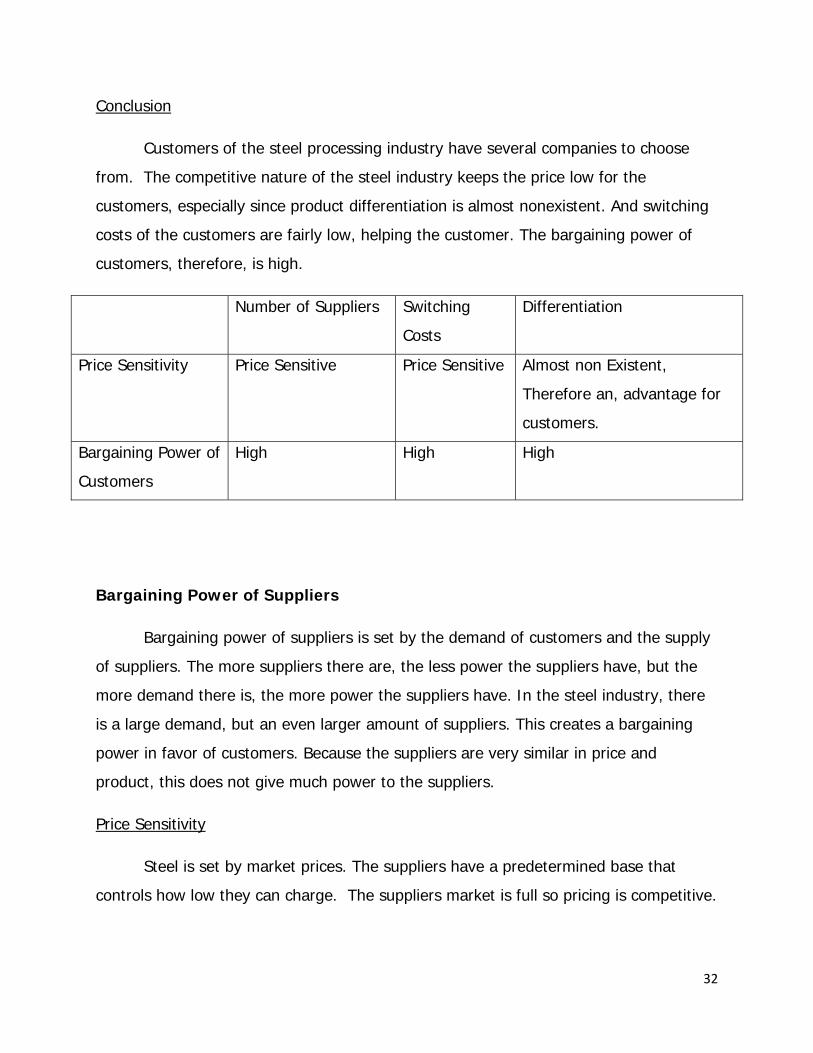

Conclusion

Customers of the steel processing industry have several companies to choose

from. The competitive nature of the steel industry keeps the price low for the

customers, especially since product differentiation is almost nonexistent. And switching

costs of the customers are fairly low, helping the customer. The bargaining power of

customers, therefore, is high.

Number of Suppliers Switching

Costs

Differentiation

Price Sensitivity Price Sensitive Price Sensitive Almost non Existent,

Therefore an, advantage for

customers.

Bargaining Power of

Customers

High High High

Bargaining Power of Suppliers

Bargaining power of suppliers is set by the demand of customers and the supply

of suppliers. The more suppliers there are, the less power the suppliers have, but the

more demand there is, the more power the suppliers have. In the steel industry, there

is a large demand, but an even larger amount of suppliers. This creates a bargaining

power in favor of customers. Because the suppliers are very similar in price and

product, this does not give much power to the suppliers.

Price Sensitivity

Steel is set by market prices. The suppliers have a predetermined base that

controls how low they can charge. The suppliers market is full so pricing is competitive.

33

Also, because switching costs are so low, and suppliers will bring down their prices to

renew contracts and win new business, it increases price sensitivity.

Steel processing companies cannot simply shop the market for lower cost

alternative materials. It is impossible to produce steel framing from heavy-duty plastic.

The suppliers understand this, but it is evened out through competitive pricing amongst

competing suppliers.

Relative Bargaining Power

Bargaining power depend on the cost of each company to not do business with

the other. Because switching costs are very low, this favors the customer. The customer

can change to another supplier and not lose much at all, but could get a better price

which would help them in the long run. Because the amount of suppliers in the

industry, shopping around for prices is something customers do after every contract.

For instance, the automobile industry has a large amount of bargaining power over the

steel industry because of the large orders, with a large number of suppliers to choose

from. In this, the auto industry can drive the prices down.

“Steelmakers are suspending and renegotiating contracts with their raw-material

suppliers as they grapple with the sudden drop in demand for everything from cars and

appliances to bridges and buildings.”

(http://online.wsj.com/article/SB122697117526435811.html)

Conclusion

Bargaining power in the steel industry is in favor the customer. This conclusion is

drawn from a few key factors. The large amount of suppliers compared to the demand

gives the customer the advantage to shop around and drive the prices down. Also,

34

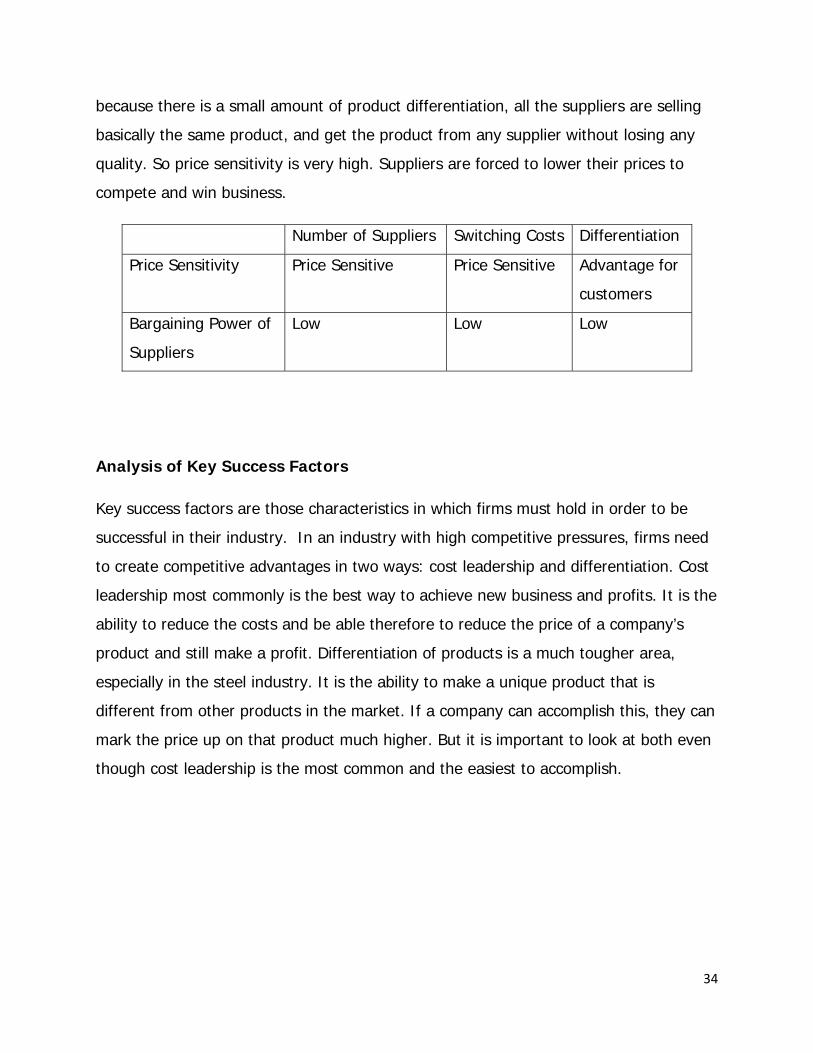

because there is a small amount of product differentiation, all the suppliers are selling

basically the same product, and get the product from any supplier without losing any

quality. So price sensitivity is very high. Suppliers are forced to lower their prices to

compete and win business.

Number of Suppliers Switching Costs Differentiation

Price Sensitivity Price Sensitive Price Sensitive Advantage for

customers

Bargaining Power of

Suppliers

Low Low Low

Analysis of Key Success Factors

Key success factors are those characteristics in which firms must hold in order to be

successful in their industry. In an industry with high competitive pressures, firms need

to create competitive advantages in two ways: cost leadership and differentiation. Cost

leadership most commonly is the best way to achieve new business and profits. It is the

ability to reduce the costs and be able therefore to reduce the price of a company’s

product and still make a profit. Differentiation of products is a much tougher area,

especially in the steel industry. It is the ability to make a unique product that is

different from other products in the market. If a company can accomplish this, they can

mark the price up on that product much higher. But it is important to look at both even

though cost leadership is the most common and the easiest to accomplish.

35

Cost Leadership

In a highly competitive industry, like the steel industry, firms must compete on price in

order to be successful. To be profitable, firms must be able to increase profit margins

by controlling and minimizing their costs. In order for the industry to be successful,

employing cost leadership strategies is vital. A company must be very efficient and

continually looking for new ways to be able to do the same thing in a cheaper manner

to reduce costs. This means finding a way to make the same product with less material,

or a new shape that is more efficient. This is the primary focus of steel companies.

They run on very tight budgets and stiff cost control. One can reduce costs a number of

different ways, such as economies of scale, cost control, recycling material,

transportation costs, and more efficient product design.

Economies of Scale:

The use of economies of scale refers to the lowering of average costs per unit due to

a larger production capacity. Firms that have the resources to produce with larger

economies to scale will have the advantage in this industry. With lower production

costs, larger firms can offer their products at a lower price than their smaller

competitors. The bigger a firm is, the more they can make at a lower costs, every single

product is not as important as it would be to a firm that makes half of what the bigger

firm produces. So the bigger a company gets, the more advantage they have over a

smaller company. More costs come with a larger company, but can produce more,

supply more, and win more business by lowering their prices.

Cost Control:

Cost control is the most important part of the steel industry. The steel processing

industry is highly competitive on price as well as the quality of their products. To be

profitable, firms need to cut costs as much as they can. The ability to manage and

reduce costs is required for any firm to stay competitive in this industry. By centralizing

36

organizational chores, which help in the managing and maintaining of inventory

efficiently, a firm can have a huge advantage over their competitors. Firms who are

able to control these factors will be able to lower their average cost per unit and in turn

increase their margins. Firms who are inefficient and cannot control costs will have a

hard time surviving in this industry.

Another big part of cost control is trying to be as resourceful in making every individual

product. If a company can reduce the amount of products that are produced that are

not quite right, variable costs, this can lower costs, because of the extra expense of

having to go back and redo a product that costs have occurred on.

Brand advertising in the industry is a minor expense and does not help sell any more

than one would sell if not advertised as heavily. By eliminating the amount of marketing

and advertising costs, this can help be able to lower the price of the product without

losing profits.

Reduced Transportation Costs:

Being able to reduce transportation costs can help drastically. If fuel prices are $3.00

like this previous summer, having suppliers and customers very close is very important.

Like stated earlier, Worthington built a plant that was adjacent to their supplier. This

will reduce costs drastically. Not having hardly any costs at all, rather than driving

trucks to transport many tons of steel from one location to another. This is not playing

as huge a roll currently with fuel prices dropping by 50%, but if energy prices spike

again, this will become very important once again. Worthington is not the only

company. According Wall Street Journal, in July, oil was selling for $145 a barrel, but in

early December was closing for as low as $46.96 a barrel.

( http://online.wsj.com/article/SB122822915071272421.html) This is a unexpected

lowering in transportation costs. In Gibraltar’s 2007 10-K, they state that “Increases in

energy and freight prices will increase our operating costs, and we may be unable to

pass all

37

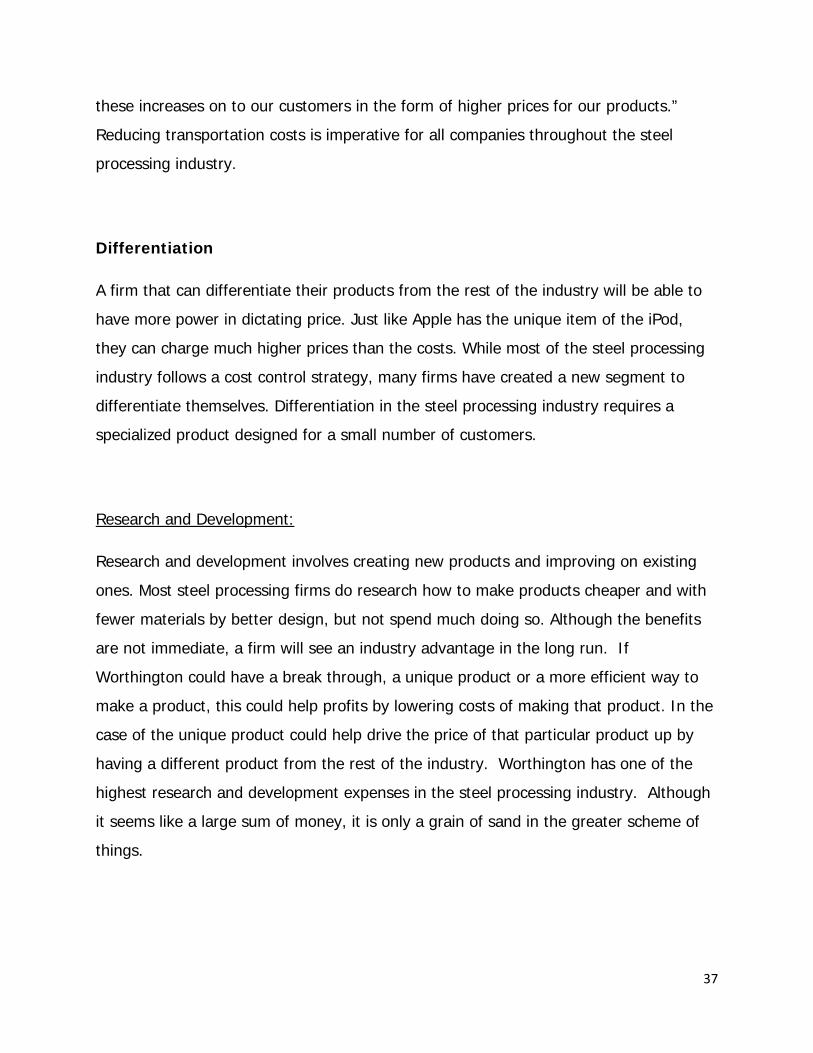

these increases on to our customers in the form of higher prices for our products.”

Reducing transportation costs is imperative for all companies throughout the steel

processing industry.

Differentiation

A firm that can differentiate their products from the rest of the industry will be able to

have more power in dictating price. Just like Apple has the unique item of the iPod,

they can charge much higher prices than the costs. While most of the steel processing

industry follows a cost control strategy, many firms have created a new segment to

differentiate themselves. Differentiation in the steel processing industry requires a

specialized product designed for a small number of customers.

Research and Development:

Research and development involves creating new products and improving on existing

ones. Most steel processing firms do research how to make products cheaper and with

fewer materials by better design, but not spend much doing so. Although the benefits

are not immediate, a firm will see an industry advantage in the long run. If

Worthington could have a break through, a unique product or a more efficient way to

make a product, this could help profits by lowering costs of making that product. In the

case of the unique product could help drive the price of that particular product up by

having a different product from the rest of the industry. Worthington has one of the

highest research and development expenses in the steel processing industry. Although

it seems like a large sum of money, it is only a grain of sand in the greater scheme of

things.

38

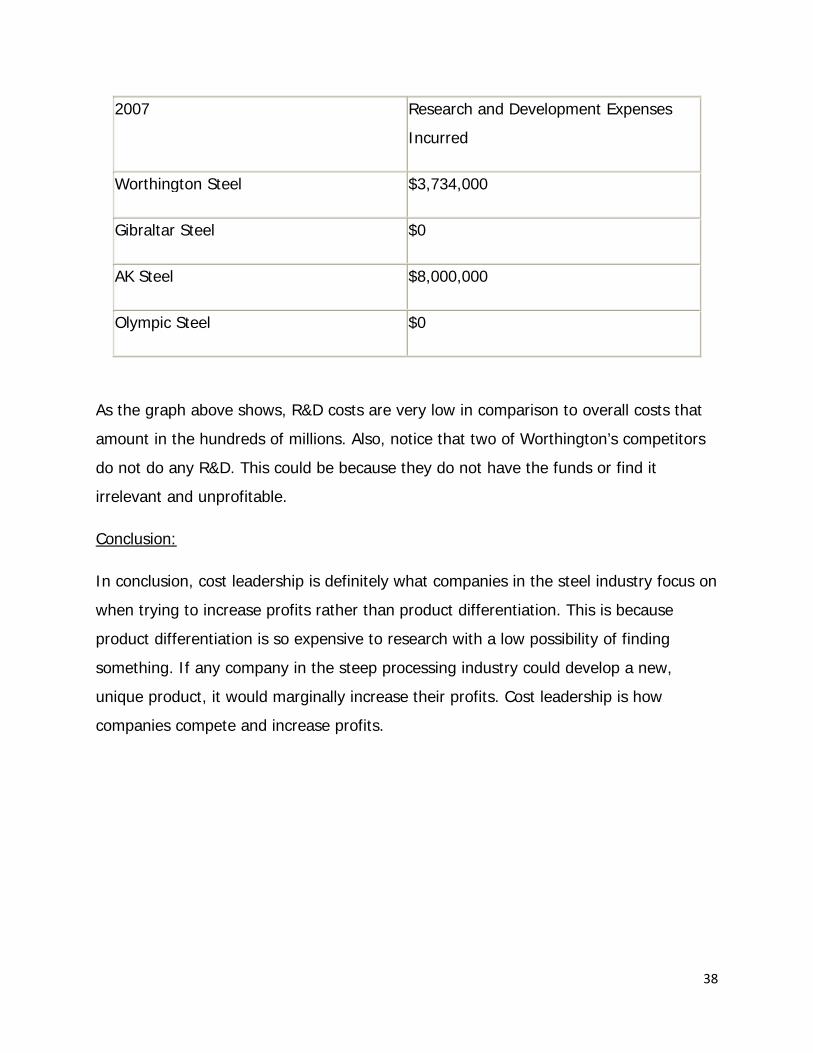

2007 Research and Development Expenses

Incurred

Worthington Steel $3,734,000

Gibraltar Steel $0

AK Steel $8,000,000

Olympic Steel $0

As the graph above shows, R&D costs are very low in comparison to overall costs that

amount in the hundreds of millions. Also, notice that two of Worthington’s competitors

do not do any R&D. This could be because they do not have the funds or find it

irrelevant and unprofitable.

Conclusion:

In conclusion, cost leadership is definitely what companies in the steel industry focus on

when trying to increase profits rather than product differentiation. This is because

product differentiation is so expensive to research with a low possibility of finding

something. If any company in the steep processing industry could develop a new,

unique product, it would marginally increase their profits. Cost leadership is how

companies compete and increase profits.

39

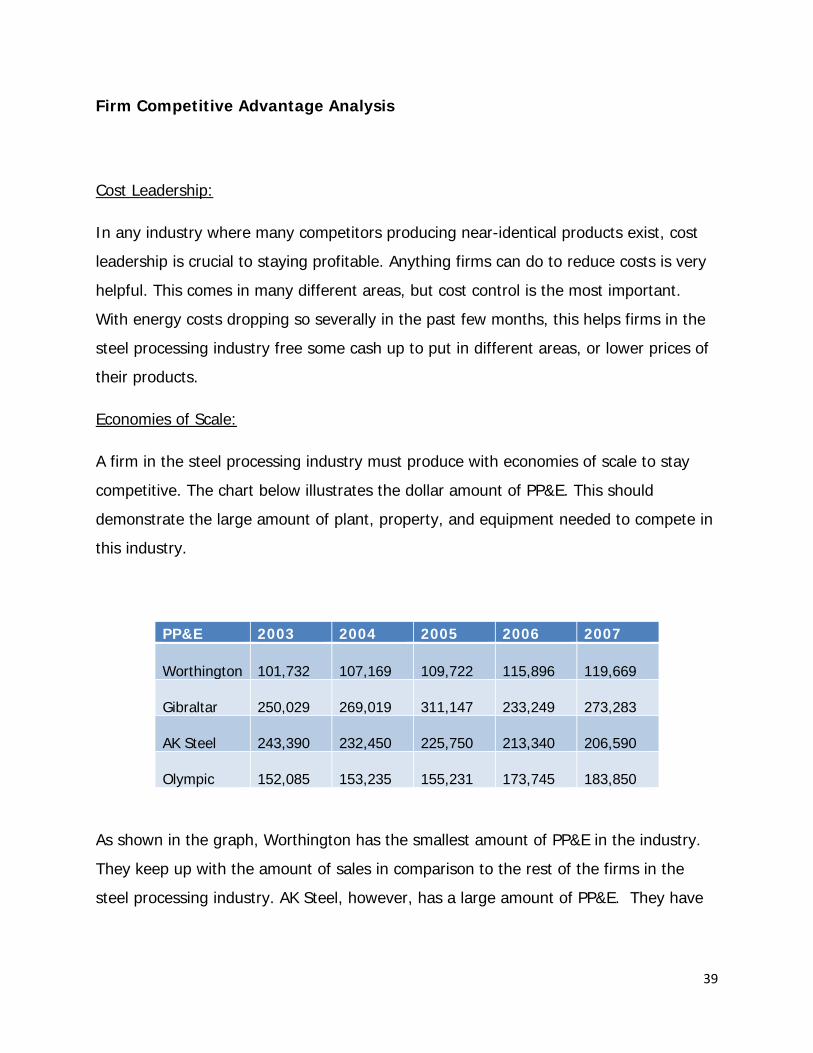

Firm Competitive Advantage Analysis

Cost Leadership:

In any industry where many competitors producing near-identical products exist, cost

leadership is crucial to staying profitable. Anything firms can do to reduce costs is very

helpful. This comes in many different areas, but cost control is the most important.

With energy costs dropping so severally in the past few months, this helps firms in the

steel processing industry free some cash up to put in different areas, or lower prices of

their products.

Economies of Scale:

A firm in the steel processing industry must produce with economies of scale to stay

competitive. The chart below illustrates the dollar amount of PP&E. This should

demonstrate the large amount of plant, property, and equipment needed to compete in

this industry.

PP&E 2003 2004 2005 2006 2007

Worthington 101,732

107,169

109,722

115,896

119,669

Gibraltar 250,029

269,019

311,147

233,249

273,283

AK Steel 243,390

232,450

225,750

213,340

206,590

Olympic 152,085

153,235

155,231

173,745

183,850

As shown in the graph, Worthington has the smallest amount of PP&E in the industry.

They keep up with the amount of sales in comparison to the rest of the firms in the

steel processing industry. AK Steel, however, has a large amount of PP&E. They have

40

had trouble in the past translating PP&E into profit. AK Steel’s large facilities can not

influence how well a company manages their expenses.

Cost Control:

Since the steel processing industry cannot dictate prices, the firms in the industry must

control their costs to make a profit. Looking to cut costs, Worthington shut down five

insignificant metal framing plants while increasing product price. This resulted in an

increased gross margin from 12.7% to 15.1%. “Across the company, we have been

focused on cutting costs, expanding our market reach through new products and

services and steering through a volatile and demanding steel pricing environment,” said

Chairman and Chief Executive John P. McConnell.(WSJ Online Jun 26, 2008). Steel used

by these firms is purchased in large quantities at regular intervals from both domestic

and foreign producers in the open market. Worthington uses multi-year contracts to

limit the impact of pricing fluctuations. By purchasing materials through multi-year

contracts Worthington is able to receive discounts which helps lower the costs of

materials. AK Steel also uses multi-year contracts as stated in their 2007 10-K. AK

Steel claims that, “To the extent that multi-year contracts are available in the

marketplace, the Company has secured adequate sources of supply to satisfy other key

raw materials needs for the next three to five years.”

Reduced Transportation Costs:

If fuel prices are high, firms would be wise to decrease transportation expense.

Worthington accommodates for this by negotiating multi-year contracts for both

incoming and outgoing products. Worthington also reduces transportation expenses by

shipping to other regional facilities when available. But if fuel prices are unexpectedly

low like currently, then transportation costs are not high, because Worthington has

expected them to be much higher than now. Gibraltar is also finding ways to reduce

freight costs. It is crucial to be able to reduce variable costs in a cost leadership

41

industry. In Gibraltar’s 2007 10-K, Gibraltar even believes that, “During periods of

higher freight and energy costs, we may not be able to recover our operating cost

increases through price increases without reducing demand for our products.”

Transportation is an industry-wide factor.

Differentiation

In an effort to maintain profitability, some steel processing firms have created a new

segment to differentiate themselves. Worthington has created a steel cylinder segment

that focuses on making specialty products based on exact customer specifications.

Worthington’s gross margin for its pressure cylinder segment was 24.5%, compared to

only 10.1% for steel processing. As a result of having a slightly different product than

normal does help Worthington drastically in profits. Gibraltar is developing patents in

order to gain a competitive advantage through a small type of differentiation. Gibraltar

is trying to put their name on the roof vent world. Gibraltar’s 2007 10-K states that,

“While not material, we do believe one of our patents related to a roof vent sold in our

Building Products segment, scheduled to expire in November 2009, gives us a

competitive advantage with regard to that product.”

Research and Development:

Research and development is a way for companies to develop new products or improve

on existing ones. Most R&D conducted in the steel industry involves improving on

existing products. The chart below illustrates how much research and development

expenses were incurred by the different firms in the steel processing industry.

42

2007 Research and Development Expenses

Incurred

Worthington Steel $3,734,000

Gibraltar Steel $0

AK Steel $8,000,000

Olympic Steel $0

Note that only one of Worthington’s competitors conducts research. The other two

companies are smaller and may not have the resources to spend on research.

Worthington and AK Steel differentiate themselves as companies who invest in research

and development. They are appealing companies because of the possibility of

developing a new product or developing new cost-reducing technology. They do not

spend much on R&D in comparison. If a break through occurs, even if just a minor

design change of a product, it can lead to large amounts of cost reduction. That, in

turn, leads to higher profits.

Conclusion:

In summary, the industry follows a cost leadership strategy. As long as these

companies continue with their current cost control practices, they will remain

competitive in the steel processing industry. In companies that have unique segments,

such as Worthington’s cylinders segment, their biggest threat is the threat of new

entrants. With no domestic competitors in these markets, any steel processing rivals

could add a competitor’s unique segment to their companies. This would cause a

43

reduction in profits of these segments because customers could gain bargaining power

over the steel processing firms.

Key Accounting Policies

A company utilizes its key success factors to maintain profitability. They choose

certain accounting policies to emphasize these factors on paper. Even with GAAP

(Generally Accepted Accounting Principles), firms still have flexibility to distort figures

for their benefit. Since Worthington’s key success factor is cost leadership, we can

discern the accounting policies they use to emphasize this.

Operating Leases:

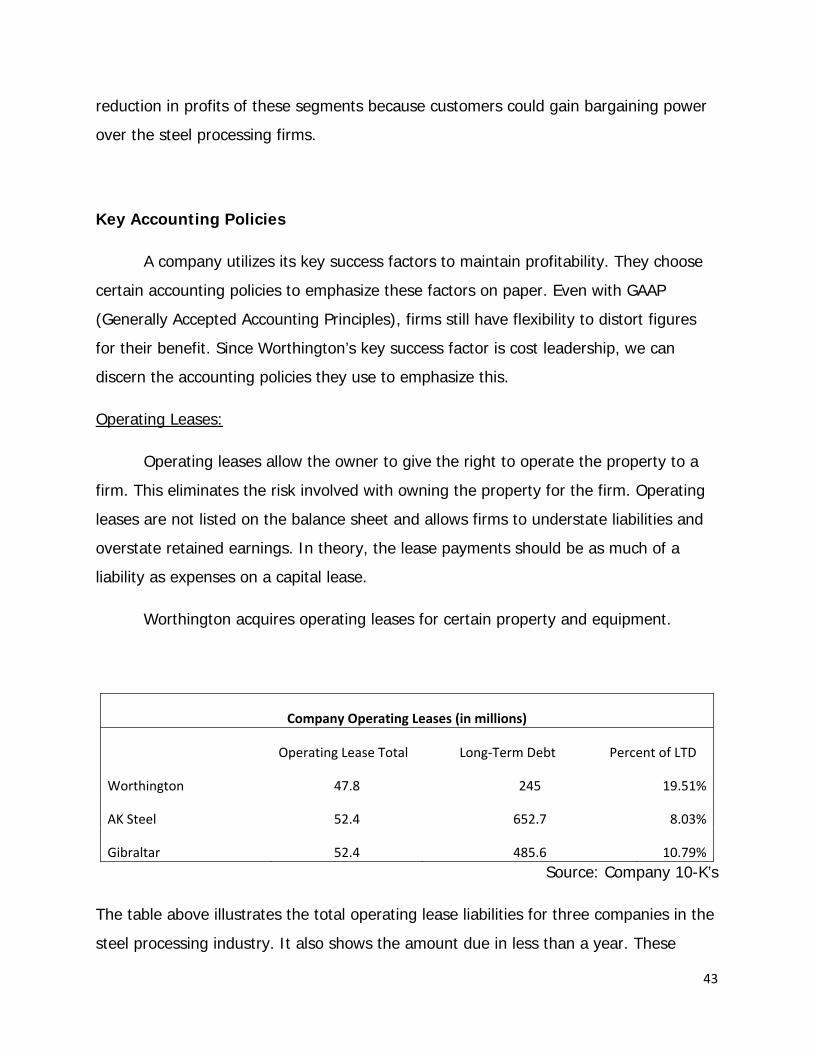

Operating leases allow the owner to give the right to operate the property to a

firm. This eliminates the risk involved with owning the property for the firm. Operating

leases are not listed on the balance sheet and allows firms to understate liabilities and

overstate retained earnings. In theory, the lease payments should be as much of a

liability as expenses on a capital lease.

Worthington acquires operating leases for certain property and equipment.

Company Operating Leases (in millions)

Operating Lease Total Long‐Term Debt Percent of LTD

Worthington 47.8 245 19.51%

AK Steel 52.4 652.7 8.03%

Gibraltar 52.4 485.6 10.79%Source: Company 10-K’s

The table above illustrates the total operating lease liabilities for three companies in the

steel processing industry. It also shows the amount due in less than a year. These

44

numbers would understate liabilities on the balance sheet for all three companies, while

overstating retained earnings. Steel processing firms are cost leaders and would view

this accounting policy as beneficial.

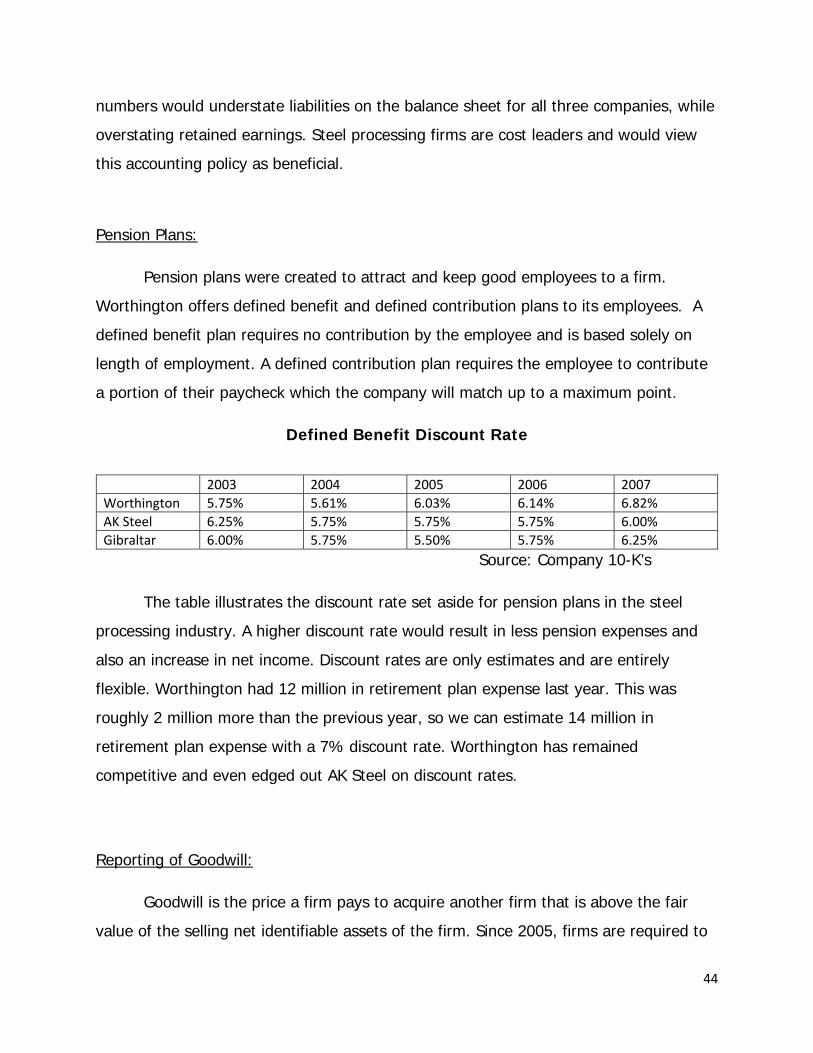

Pension Plans:

Pension plans were created to attract and keep good employees to a firm.

Worthington offers defined benefit and defined contribution plans to its employees. A

defined benefit plan requires no contribution by the employee and is based solely on

length of employment. A defined contribution plan requires the employee to contribute

a portion of their paycheck which the company will match up to a maximum point.

Defined Benefit Discount Rate

Source: Company 10-K’s

The table illustrates the discount rate set aside for pension plans in the steel

processing industry. A higher discount rate would result in less pension expenses and

also an increase in net income. Discount rates are only estimates and are entirely

flexible. Worthington had 12 million in retirement plan expense last year. This was

roughly 2 million more than the previous year, so we can estimate 14 million in

retirement plan expense with a 7% discount rate. Worthington has remained

competitive and even edged out AK Steel on discount rates.

Reporting of Goodwill:

Goodwill is the price a firm pays to acquire another firm that is above the fair

value of the selling net identifiable assets of the firm. Since 2005, firms are required to

2003 2004 2005 2006 2007 Worthington 5.75% 5.61% 6.03% 6.14% 6.82% AK Steel 6.25% 5.75% 5.75% 5.75% 6.00% Gibraltar 6.00% 5.75% 5.50% 5.75% 6.25%

45

perform a goodwill impairment check annually (FASB 142). This voids any flexibility

companies used to have regarding goodwill write-offs. Worthington had 182 million in

goodwill in 2008. The impairment test was used and no amount could be deducted.

However, in future years the value of Worthington’s goodwill may decrease and write-

offs will decrease retained earnings. This key accounting policy is used to prevent

rapidly inflating retained earnings in highly profitable years.

Source: Company 10-K’s

Goodwill as a Percentage of PP&E and Other Assets (in millions)

Goodwill Other Assets & PPE Percentage Worthington 182 733 24.83 AK Steel 37 2770.6 1.35 Gibraltar 453 287.9 157.35 Olympic 6 96.1 6.24

As the chart demonstrates, Worthington is near the 24% mark and AK Steel and

Olympic are fairly close to the same percentage. We can assume that Gibraltar has

recently expanded and acquired a large amount of goodwill. A high percentage of

goodwill is not necessarily detrimental, although investors must take into account its

effect on owner’s equity.

We amortized goodwill over a five year period and included the amount of

additional goodwill gained each year. According to FASB statement 142, companies are

not allowed to amortize goodwill on the balance sheet. However, companies amortize

goodwill on internal statements in order to get a more accurate net income number.

The increase in Worthington’s goodwill was due primarily to changes in foreign

exchange rates.

46

Foreign Currency Risk:

There is an additional risk when buying or selling in other countries. The foreign

currency values change every moment, resulting in an ever-changing cost of goods

sold. Under GAAP, little flexibility is allowed to manipulate foreign exchange rates.

However, Worthington imposes forward contracts to minimize exposure of both

favorable and unfavorable exchange rates. Because of these contracts, Worthington

believes a 10% change in the dollar value would not materially affect profitability. Also,

because of the assumption that rates change uniformly, this may overstate the impact

of foreign exchange rates on assets and liabilities. Foreign sales account for 9% of total

sales (see 10-K).

Evaluating Accounting Strategy

A firm’s accounting strategy can generally be broken down into two parts. The

first thing one must assess is the level of disclosure in the company’s financial reports.

The second step in evaluating the accounting strategy is to determine if the company is

conservative or aggressive in its accounting policies.

Level of Disclosure:

Worthington exhibits a medium to high level of disclosure. We determine the

amount of disclosure by looking at the company’s 10-K report and comparing the report

with our competitor’s 10-K reports. Worthington operates in three segments and

provides specific data regarding those segments. This makes it easier for an investor to

discern what segment of the company is contributing to the overall data. Most firms in

the steel processing industry operate in more than one segment. These firms also

report on these segments individually, leading us to believe that segment reporting

differentiation is recommended in this industry. Also, the SEC requires all companies to

47

disclose certain financial statements, as well as various other documents so that the

public can be as informed as possible.

A look into Worthington’s 10-K will also show that they segment their customers

into three categories: automotive, construction, and other. Another comparison to other

firms in the steel processing industry will show that a large number of firms also divide

their customers into a percentage of sales. In the 10-K Worthington discloses a large

amount of information regarding the sales breakdown of many aspects of the industries

they are involved in compared to the lack of information disclosed about research and

development

An item that prevents us from giving a high rating of disclosure is Worthington’s

disclosure of R&D. A search of Worthington’s 10-K will reveal a single line regarding

R&D. While they follow GAAP standards by reporting the amount expensed, the single

statement is towards the end of the 10-K and not itemized on the balance sheet. A

comparison to AK Steel will show the same approach in R&D reporting. This may echo

the low emphasis these cost-leadership firms put on R&D.

Aggressiveness of Accounting Policies:

The second step of evaluating an accounting strategy is to determine the level of

aggressiveness of their accounting policies. As Worthington is a cost leadership

company, it is no surprise that they are highly aggressive in their reporting methods.

Pension Plans:

Pension plans can represent a large expense to a company. Worthington

estimates future pension plan liability using a discount rate. A higher discount rate

would result in lower pension plan expense and a higher net income. Worthington is

48

continuously increasing discount rate for their pension plans. Worthington is also more

aggressive than its competitors in estimating pension plan expense.

Operating Leases:

Operating leases allow a firm to reduce the amount of liabilities on the books.

This is especially favorable for cost leadership companies to reduce costs shown on the

books. Although in theory the liability of a capital versus an operating lease is equal,

choosing to use an operating lease is inherently aggressive. We have compared the

present value of the firm’s operating lease payments to the total long term debt and

have determined that if the company had used capital leases it would not have a

material effect on retained earnings.

2009 2010 2011 2012 2013 2013+ TotalLease Payments $10,753 $9,804 $8,016 $6,349 $6,022 $6,903 $47,847Discount Rate 6.82% 1.0682 1.1411 1.2189 1.3020 1.3908 1.4856Present Value $10,066 $8,592 $6,577 $4,876 $4,330 $4,646 $39,088Total Long Term Debt $294,785 Operating Lease Percentage 13.26%

Goodwill:

Goodwill is the additional amount paid over book value to acquire another firm.

It makes up a significant amount of assets for Worthington. Goodwill is subject to an

early impairment test that compares fair value to book value. If book value is deemed

to be greater than fair value, impairment is used. This process requires a high degree of

estimation and allows Worthington to aggressively overvalue assets. There is cause for

concern since Worthington has not impaired goodwill over the last five years. Since we

49

are not impairing goodwill Worthington is overstating assets and net income. Also, by

overstating net income they are overstating retained earnings and shareholders’ equity.

Evaluating Quality of Disclosure

Qualitative Analysis:

A company’s 10-K is only as good as the quality of information it contains. A

financial report masked in obscurity but meets minimum GAAP requirements should be

looked at with a keen eye.

Pension Plans:

Worthington does a good job on disclosing pension plan data. A look at their

10-K will show a chart of pension plan expenses as well as a summary of how they

calculated their data. They disclose the discount rates used to determine the net

periodic pension cost. They even go so far as to disclose the amount invested in debt

and equity securities and forecast future pension payments.

The steel processing industry generally discloses the same amount of pension

plan data. Gibraltar goes as far as disclosing other retirement plan data while Olympic

Steel does a very poor job.

Goodwill:

Worthington does an excellent job of disclosing goodwill data. They explain how

they arrived at their numbers and identified the impairment test they used as the

present value technique. After the test for impairment was performed they decided

that the goodwill amount did not need to be impaired. They also give readers the extra

benefit of dividing their goodwill into the three segments they operate in.

50

Worthington’s competitors do not meet the quality standards on this subject.

While most made an adequate attempt, Olympic Steel simply states the amount of

goodwill on their balance sheet.

Operating Leases: