Embed Size (px)

Citation preview

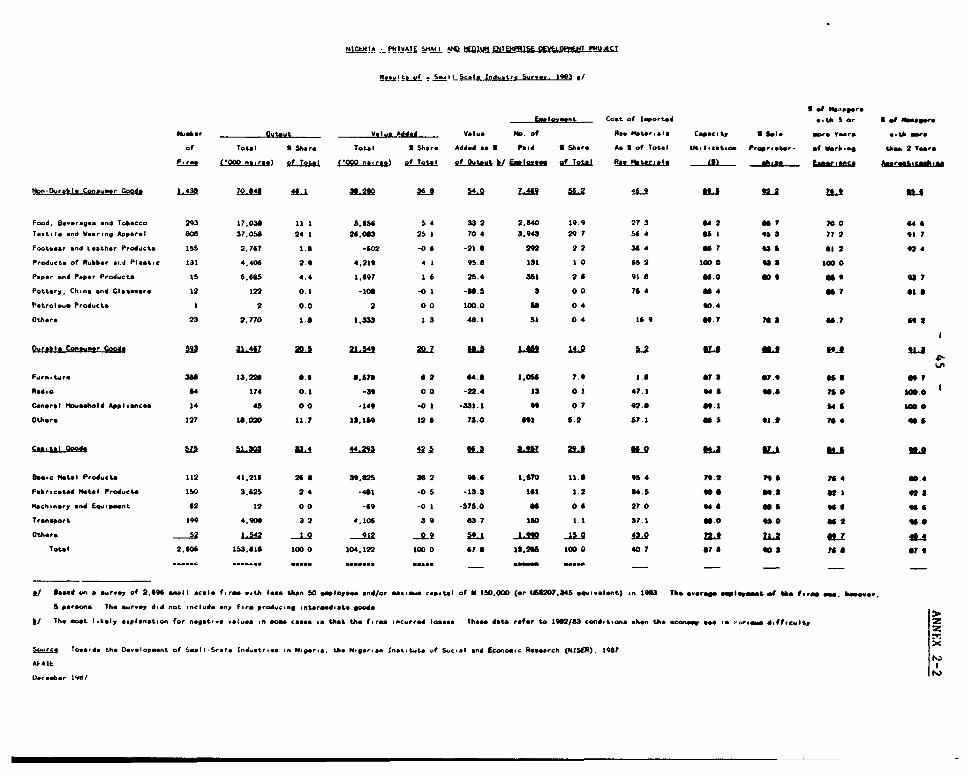

Document of

The World Bank

FOR OFFICIAL USE ONLY

Reprt No. 7114-UNI

STAFF APPRAISAL REPORT

NIGERIA

PRIVATE SMALL AND MEDIUM ENTERPRISE DEVELOPMENT PROJECT

September 23, 1988

Africa Region, Western Africa DepartmentIndustry and Energy Operations Division

This document has a restricted distribution and may be used by recipients only in the performance oft v * , I t- -

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY AND EQUIVALENT UNITS

Currency Unit - Naira (Y)

On September 26, 1986, Nigeria adopted a flexible exchange rate policy andintroduced a second-tier foreign exchange market (SFEH) comprising an auction andinterbank market. On July 2, 1987, SPEH and the official (i.e., first-tier) rateswere merged. All foreign exchange transactions now take place at market-determined exchange rates. The foreign exchange market (FEH) is a combination ofan auction (fortnightly) on the basis of the Dutch system, and a dealer marketwhich operates in response to supply and demand. The FEK rate in the auction ofJuly 7, 1988 was US$1 - N4.47. A rate of US$1 - t14.00 has been used for projectanalysis.

US$1 - M4.00NMl US$0.25

WEIGHTS AND MEASURES

Metric System

GLOSSARY OF ABBREVIATIONS

ASCON - Administrative Staff Collogo of t4ASSI - Nig,-ria Association of Small ScaloNiger! Industriallets

CIRD - Center for Industrial Research and NBCI - Nigerian Bank for Comerce andD-velopment Industry

CUD - Center for Management Development NGO(s) - Non-governmental organization(s)CBN - Central Bank of Nigeria NIDB - Nigorian Industrial DevelopmentCUB - Continental Merchant Bank BankDUBS - Durham University Business School NISER - Nigorian Institute of Social andEDP(s) - Entrepreneurship Development Economic Research

Program(s) NMB - Nigerian Morchant BankELAN - Equipment Leasing Association of ODA - Overseas Development Agency, UK

Nigeria PB(s) - Participating banksFBN - First Bank of Nigeria PCC - Project Coordination ComitteeFEM - Foreign Exchange Market PRODA - Project Development AgencyFGN - Federal Government of Nigeria SFEM - Second-Tier Foreign ExchangeFIIRO - Federal Institute of Industrial Market

Research, Oshodi SME(s) - Small and medium scaleFMI - Federal Ministry of Industries enterprise(s)IBWA - International Bank for West Africa SSE(s) - Small scale enterprise(s)ICON - ICON Merchant Bankers SSID(s)- Sinl! Scale Industry Divisions,IDC(s) - Industrial Development Center(s) State Ministries of Industry andITF - Industrial Training Fund CommerceILO - International Labor Organization WFYP - Work for Yourself ProgramIMB - International Merchant Bank USA - United Bank for AfricaMAN - Manufacturers Association of Nigeria UBN - Union Bank of NigeriaMGA(s) - Mutual guarantee association(s) UNDP - United Nations DevelopmentNAL - NAL Merchant Bank Program

FISCAL YEAR

January 1 to December 31

FM ONVDCUL U Y

NIGERIA

PRIVATE SMALL AND MEDIUM ENTERPRISE DEVELOP ENT PROJECT

TABLE OF CONTENTS

Pane No.

LOAN AND PROJECT SUMMARY ...... .............................. iii

I. INTRODUCTION ............................................. 1

II. THE CETTING ............................................. 1

A. The Economic Environment ........................... 1B. The Manufacturing Sector ..... .................... 3

1. Past Performance .............................. 32. Recent Reforms ................................ 43. Impact of the Industrial Sector Reforms

and Prospects ............................... 6C. The Small and Medium Scale Enterprise (SME) Sector . 7

1. Sectoral Context. 72. Government Policies and Support Programs 83. Prospects and Constraints .11

D. The Financial Sector .11

1. The Institutional Setting .112. Financial Policy Framework .133. Development Constraints .15

E. Government Objectives and the Role of SMEs . .18F. Bank Assistance .19

1. Past Ban!, Involvement .19

2. Bank Role *n the Sector .20

III. THE PROJECT .20

A. Project Rationale and Objectives . .20B. Project Description . .21

1. Line cf Credit Component .222. Pilot Financial Restructuring Component 223. Pilot Mutualist Credit Guarantee Scheme 23

4. Equipment Leasing Component .235. Technical Assistance Component .23

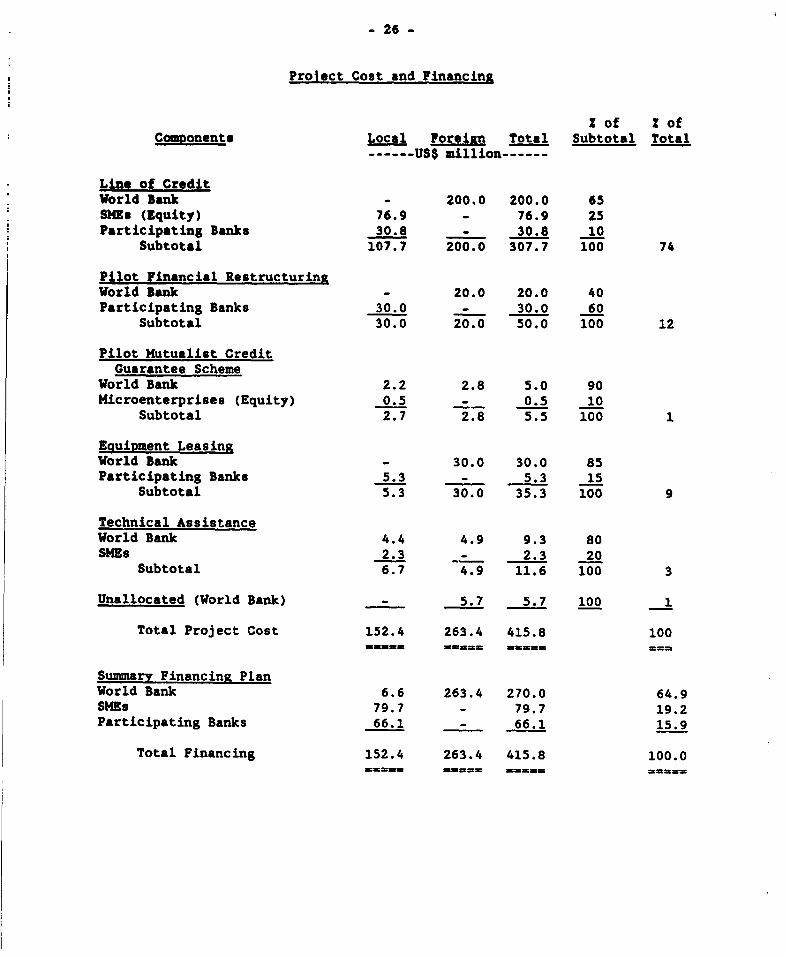

C. Project Cost and Financing Plan . .25

D. Credit Demand .. 25

IV. PRINCIPAL FEATURES OF THE LOAN . .27

A. The Loan and Institutional Arrangements .27

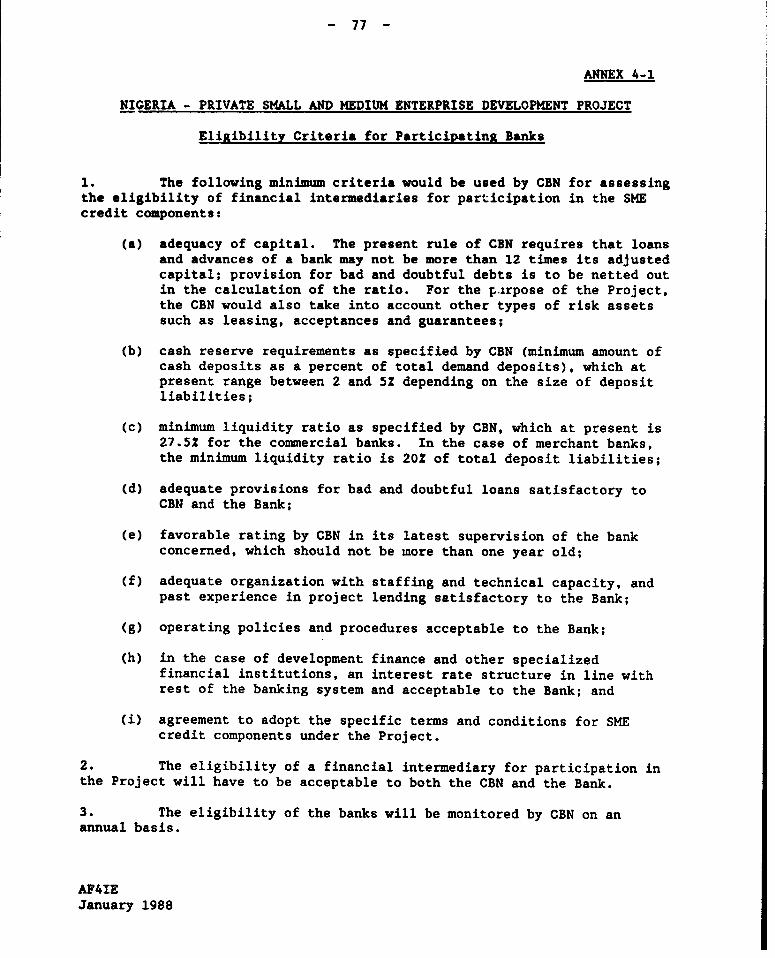

B. Eligible Financial Intermediaries .29

This Report was prepared by Surendra Agarwal (Task Manager), Kaikhosrou

Framji, Willem van Eeghen (Western Africa Department). Tu Dinh and Stephen

Berkman (Africa Technical Department) and N. Gangaram and Leila Webster(Consultants). Eleanor George provided word processing assistance and Iaidu

Hewawasam provided se retarial support in preparation of the Report.

This document has a restricted distribution and may be used by fecipients only in the performanceof their offcial duties. Its contents may no;t otherwise be disclosed without World Banks authorization.

- ii -

Paxe No.

C. Eligible Beneficiaries and Subprojects .... ......... 29D. Subloan Processing and Administration .... .......... 32E. Onlending Terms and Conditions ..... ................ 34F. Project ImplementatioL Arrangements and Schedule ... 35G. Procurement ........................................ 36H. Allocation and Disbursement of Bank Loan .... ....... 37I. Monitoring ......... ................................ 38J. Accounting, Auditing, and Reporting Requirements ... 38

V. PROJECT BENEFITS AND RISKS .............................. 39

VI. AGREEMENTS AND UNDERSTANDINGS REACHED ANDRECOMMENDATIONS ......... ............................. 41

ANNEXES

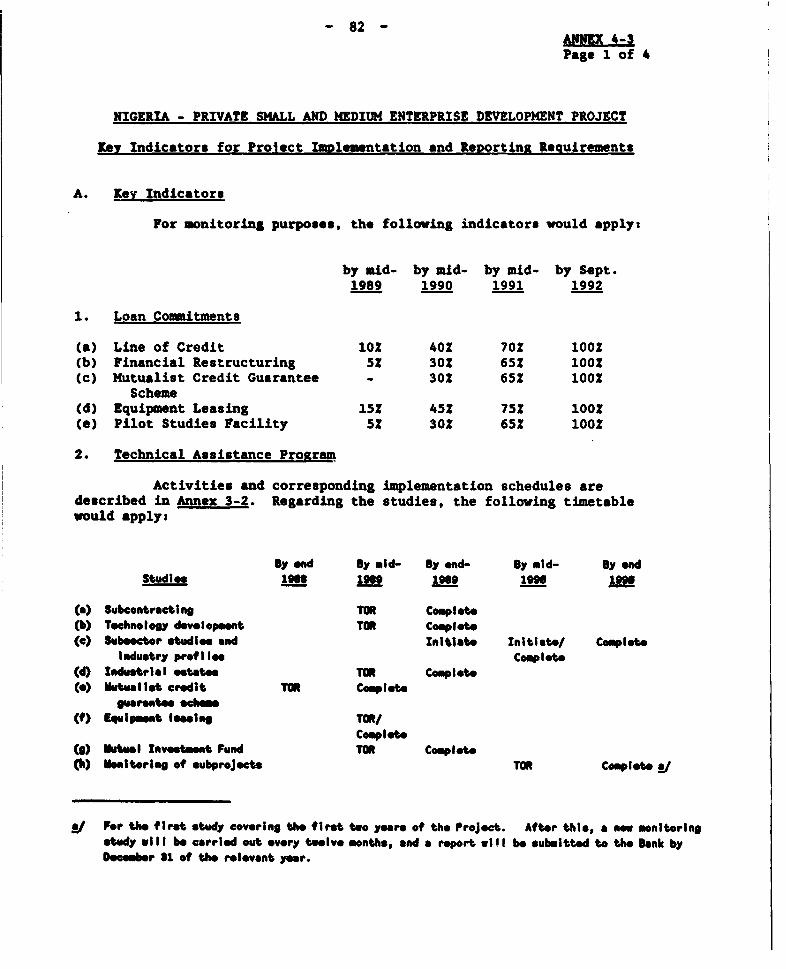

2-1 Index of Manufacturin, Production by Selected Products, 1980-19862-2 Results of a Small Scale Industry Survey, 19832-3 Institutions Providing Investment Promotion, Technical Assistance and

Lxtension Services to SMEs2-4 Industrial Development Centers(IDCs)2-5 Entrepreneurship Development2-6 Equipment Leasing2-7 Monetary Aggregates2-3 Suzmmary Financial Statements of Selected Commercial Banks2-9 Summary Financial Statements of Selected Merchant Banks2-10 Sunmmary Financial Statements of NBCI2-11 Selected Interest Rates2-12 Sectoral Distribution of Credit2-13 Characteristics of Subprojects under the Small- and Medium-Scale

Industry Project (Loan 2376-UNI)

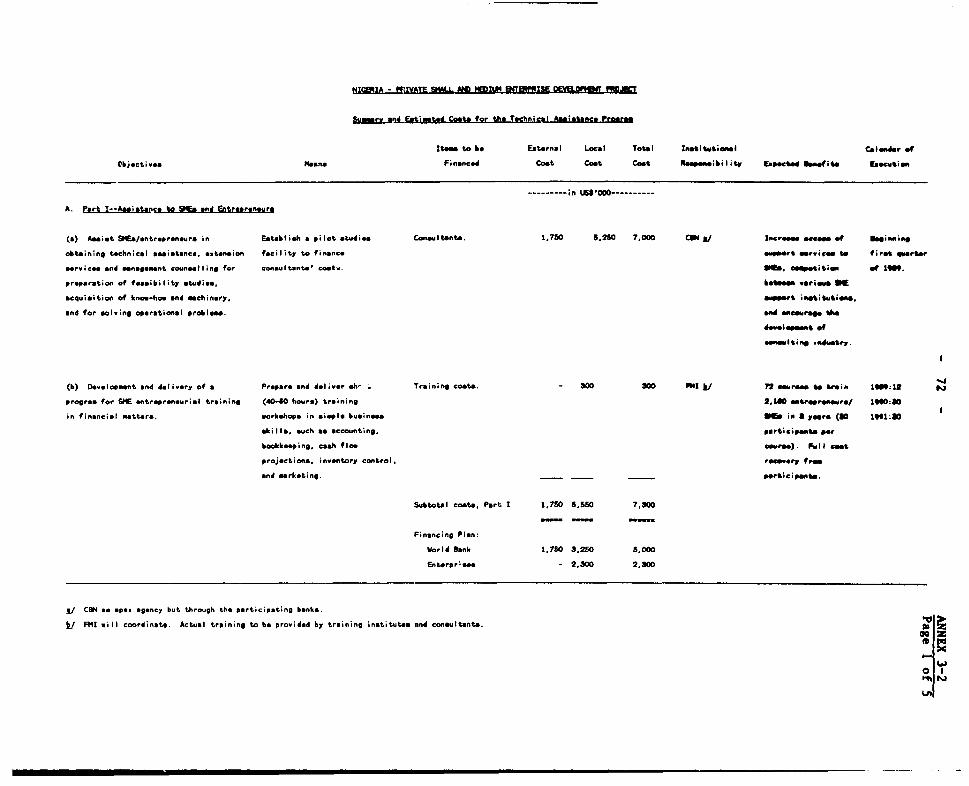

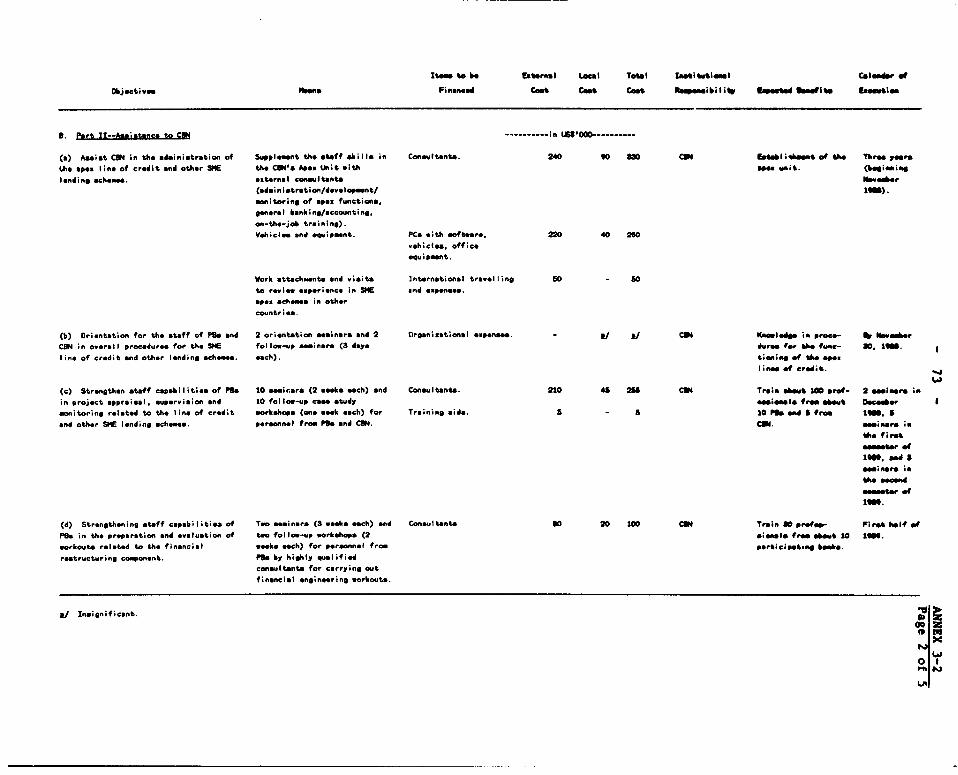

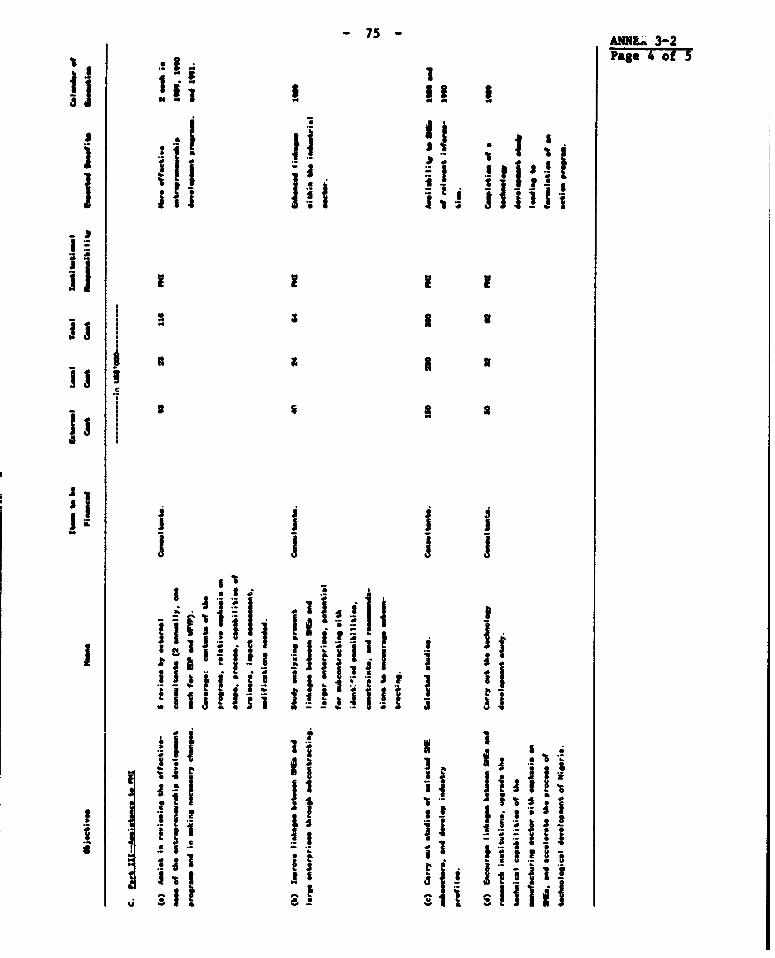

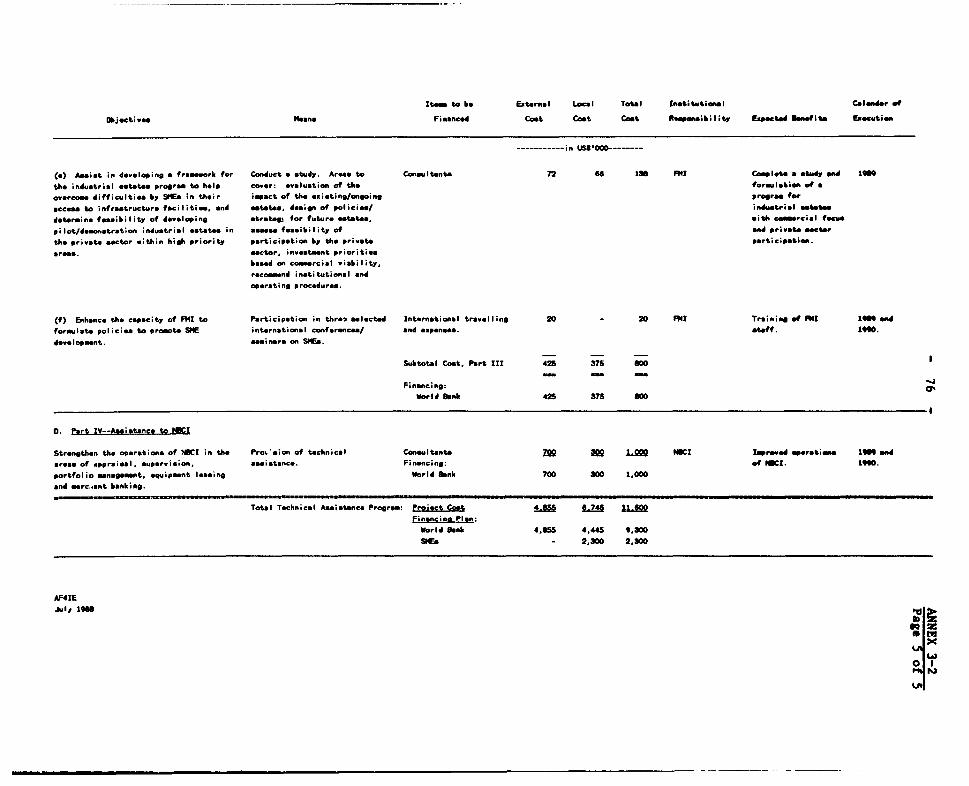

3-1 Pilot Mutualist Credit Guarantee Scheme3-2 Sunmary and Estimated Costs for the Technical Assistance Program

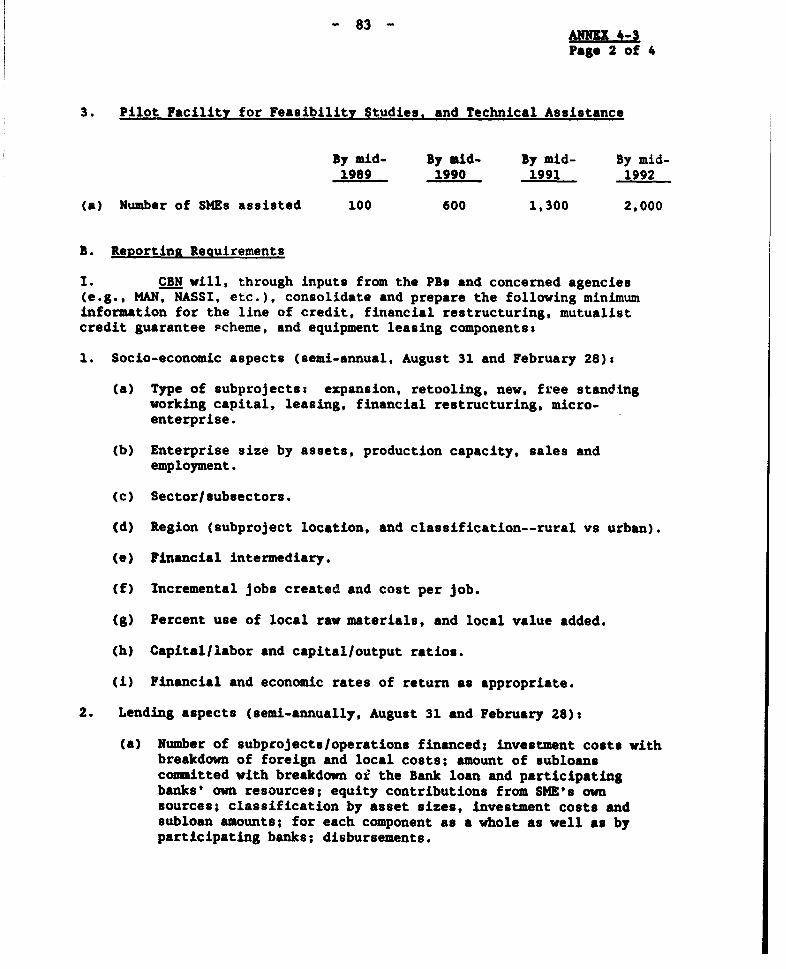

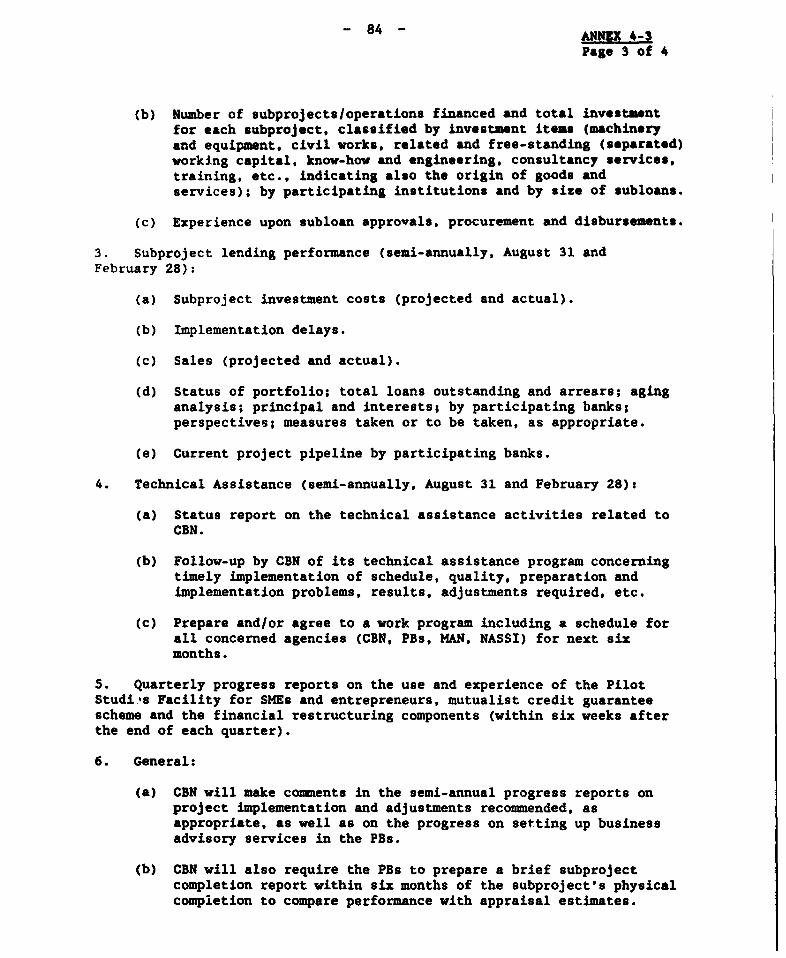

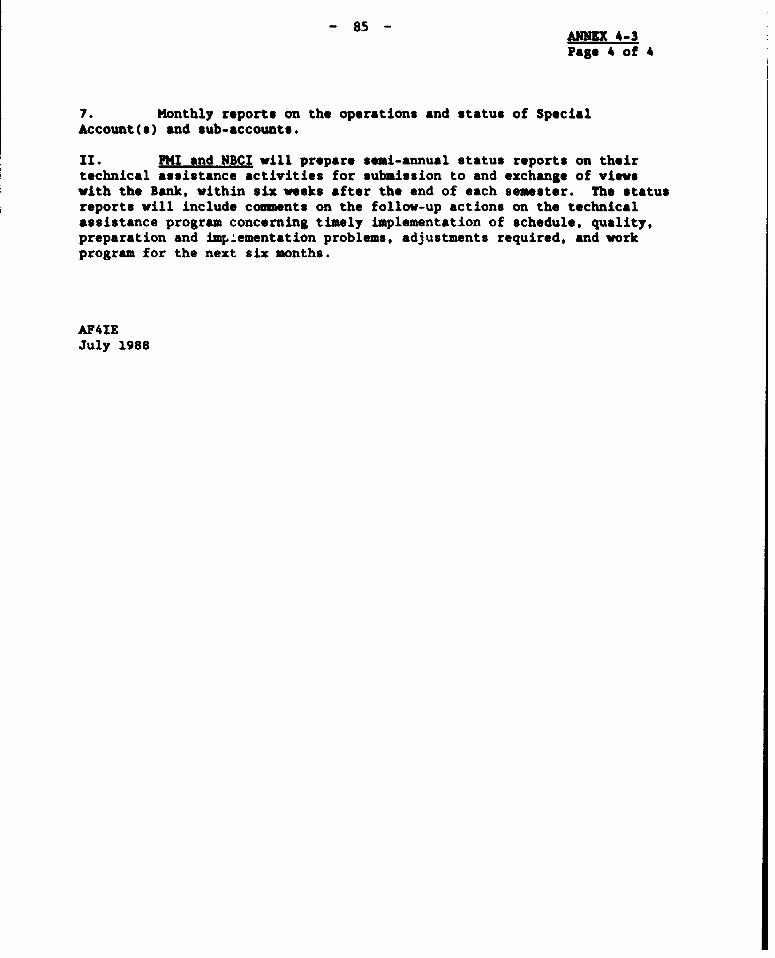

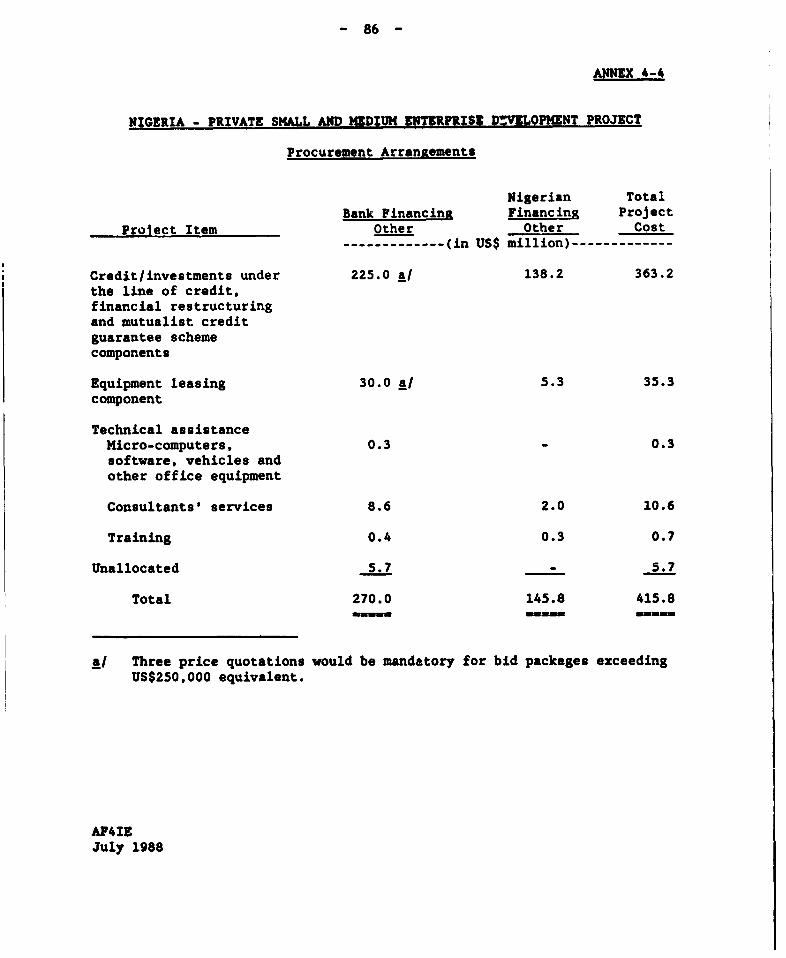

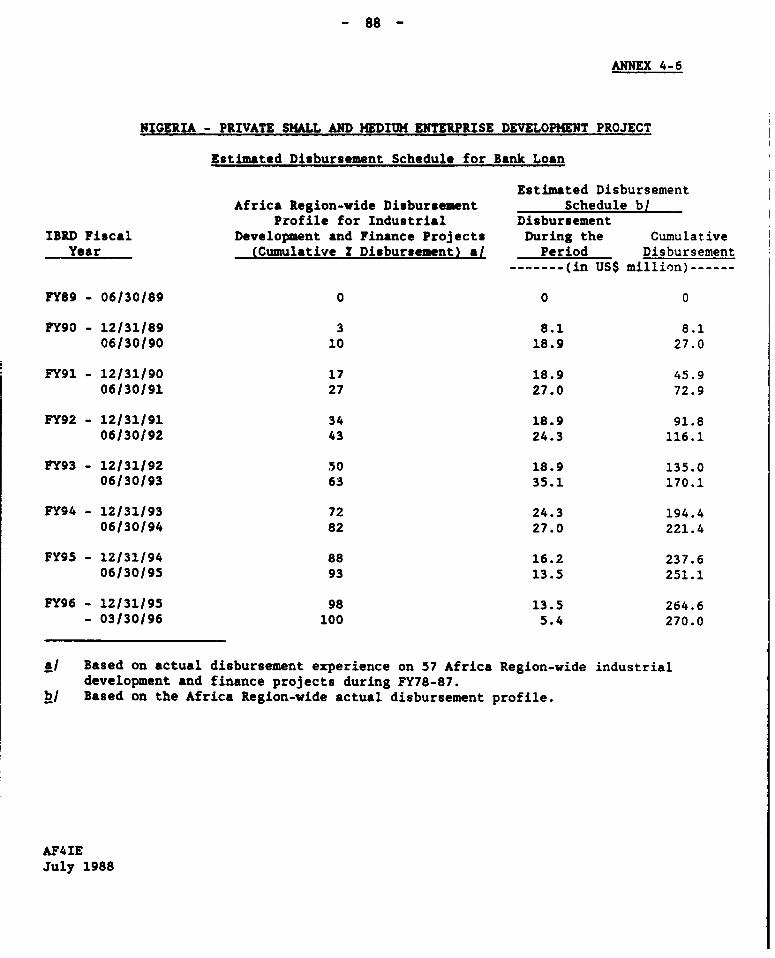

4-1 Eligibility Criteria for Participating Banks4-2 Guidelines for the Financial Restructuring Component4-3 Key Indicators for Project Implementation and Reporting Requirements4-4 Procurement Arrangements4-5 Bank Loan Allocation and Disbursments4-6 Estimated Disbursement Schedule for Bank Loan

6 Selected Documents and Data Available in the Project File

MAP

IBRD No. 20709

- ili -

NIGZRIA

PRIVATE SMALL AND MEDIUY ENTERPRISE DEVELOPMENT PROJECT

Loan and Proiect Summara

Borrower: Federal Republic of Nigeria

Beneficiaries: Central Bank of Nigeria (CBN), participating banks (Pbs),Federal Ministry of Industries (FMl), Nigerian Bank forCommerce and Industry (NBCI), and mall and medium scaleenterprises (SMEs) in the private productive sectors andservice activities.

Amount: US$270 million equivalent

Terms: Twenty years, including a five-year grace period, at theBank's standard variable interest rate.

OnlendingTerms: The Government will: (a) pass on US$268.2 million equivalent

to CBN as follows--US$265.7 million for onlending to SMEsthrough eligible PBs, and US$2.5 millicn for technicalassistance; (b) onlend US$1 million to NBCI forstrengthening its operations at the same terms andconditions as are applicable to the Bank loan; and (c)retain US$0.8 million for technical assistance to PHI. TheCBN would onlend the loan proceeds (US$265.7 million) toeligible PBs in naira terms at a variable rate, equal to theprevailing CBN rediscount rate (currently 12.752 p.a.), anda commitment fee of 0.751, with an amortization schedulereflecting the aggregate subloans made by the PBs. Thefinal onlending rates to beneficiary enterprises would bevariable and determined by the PBs. The CBN would retainabout one percentage point of the spread on the Bank loan tocover its administrative cost and pay the remaining amountto the Government. The foreign exchange risk would be borneby the Government (for a fee implicit in the differentialbetween the onlending rate to the PBs and the interest rateon the Bank loan). Subloans under the line of credit andfinancial restructuring components would have a maturity upto 12 years, including up to a 3-year grace period.Subloans under the mutualist credit guarantee scheme wouldhave a maturity up to 5 years, including up to a one-yeargrace period. The PBs would be allowed to write leasesunder the equipment leasing component for up to 10 years,including up to a 2-year grace period. Subloans under thePilot Stw'dies Facility would have a maturity up to 3 years,including up to a one-year grace period.

ProjectDescription: The principal objective of the Project is to stimulate

productive activity in line with Nigeria's resourceendowments, and generate a sustained supply response inprivate, productive SMEs in the context of the new policy

- iv -

environment and the ongoing adjustment process. The Projectwould, in this way, help in the resumption of growth andefficient employment generation. The Project consists of(a) an apex line of credit to finance fixed assets andworking capital needs of SHEs; (b) a pilot program ofcorporate restructuring of viable SHEs which are currentlyin financial difficulties; tc) a pilot mutualist creditguarantee scheme for microenterprise lending, incollaboration vith selected non-governmental organizations(NGOs); (d) an equipment leasing component to provide analternative and flexible source of long-term financing toSMEs; and (e) an integrated package of technical assistancefor SHEs (Pilot Studies Facility to finance on loan termsthe consultancy costs for feasibility studies and othertechnical assistance), for CBN (strengthening of the SMEApex Unit, training for PBs in project analysis andpreparation of restructuring workouts, implementation designof the mutualist credit guarantee scheme, studies onequipment leasing and the mutual investment funds, andmonitoring the economic and social impact ofsubprojects--tracer studies), for FMI (improvements in theEntrepreneurship Development Programs, studies onsubcontracting, technology development and industrialestates, and training), and for NBCI to strengthen itsoperations in the areas of appraisal, supervision, portfoliomanagement, leasing and merchant banking.

ProiectBenefits andRisks: The integrated package of institutional and financial

measures under the Project would foster a stronger privatesector. The Project would strengthen and improve thecompetitiveness of existing SMEs, and help establish viablenew projects. It would also help generate new employment,maintain employment in existing viable enterprises, and thuspartially alleviate the social cost of the adjustmentprocess, and thereby enhance its sustainability. Theequipment leasing and pilot financial restructuringcomponents, pilot mutualist credit guarantee scheme formicroenterprises, and studies on the establishment of amutual investment fund, and the development of an appro-priate policy and regulatory framework for equipment leasingwould improve the quality and range of financial servicesavailable to the SME sector. The Pilot Studies Facilitywould help SMEs and entrepreneurs obtain consultancyservices of their choice and make the provision oftechnical assistance demand driven, with the involvement ofthe private sector and the banking system. Provision oftechnical assistance to and training for CBN, PBs, FMI andNBCI would enhance their capacity for developing andimplementing SME support programs more effectively.

A major risk of the loan is the possible reluctance of thebanking system to engage in term financing for SMEs,perceived generally as more risky thani traditional

- V -

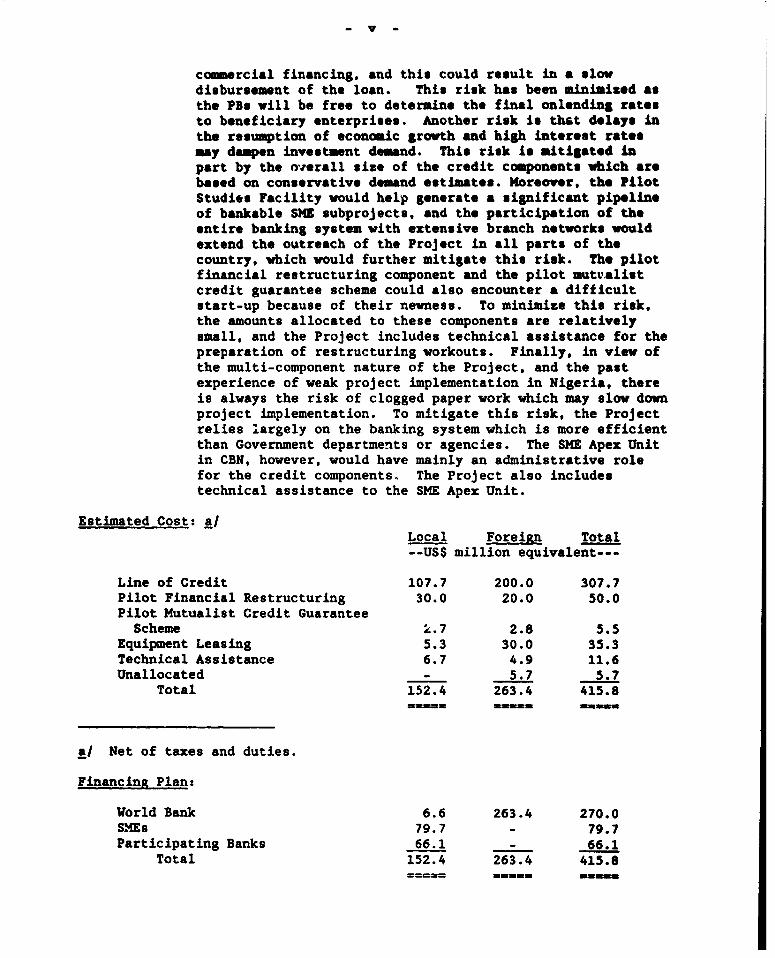

comuercial financing, and this could result in a slowdisbursement of the loan. This risk has been minimized asthe PBs will be free to determine the final onlending ratesto beneficiary enterprises. Another risk is that delays inthe resumption of economic growth and high interest ratesmay dampen investment demand. This risk is mitigated inpart by the overall size of the credit components which arebased on conservative demnd *stimates. Moreoor, thi PilotStudies Facility would help generate a significant pipelineof bankable SHE subprojects, and the participation of theentire banking system with extensive branch networks wouldextend the outreach of the Project in all parts of thecountry, which would further mitigate this risk. The pilotfinancial restructuring component and the pilot mutvalistcredit guarantee scheme could also encounter a difficultstart-up because of their newness. To minimize this risk,the amounts allocated to these components are relativelysmall, and the Project includes technical assistance for thepreparation of restructuring workouts. Finally, in view ofthe multi-component nature of the Project, and the pastexperience of weak project implementation in Nigeria, thereis always the risk of clogged paper work which may slow downproject implementation. To mitigate this risk, the Projectrelies largely on the banking system which is more efficientthan Government departments or agencies. The SME Apex Unitin CBN, however, would have mainly an administrative rolefor the credit components. The Project also includestechnical assistance to the SME Apex Unit.

Estimated Cost: a/Local Foreign Total--USS million equivalent---

Line of Credit 107.7 200.0 307.7Pilot Financial Restructuring 30.0 20.0 50.0Pilot Mutualist Credit GuaranteeScheme 2.7 2.8 5.5

Equipment Leasing 5.3 30.0 35.3Technical Assistance 6.7 4.9 11.6Unallocated - 5.7 5.7

Total 152.4 263.4 415.8

a/ Net of taxes and duties.

Financing Plan:

World Bank 6.6 263.4 270.0SMEs 79.7 - 79.7Participating Banks 66.1 - 66.1

Total 152.4 263.4 415.8

- vi -

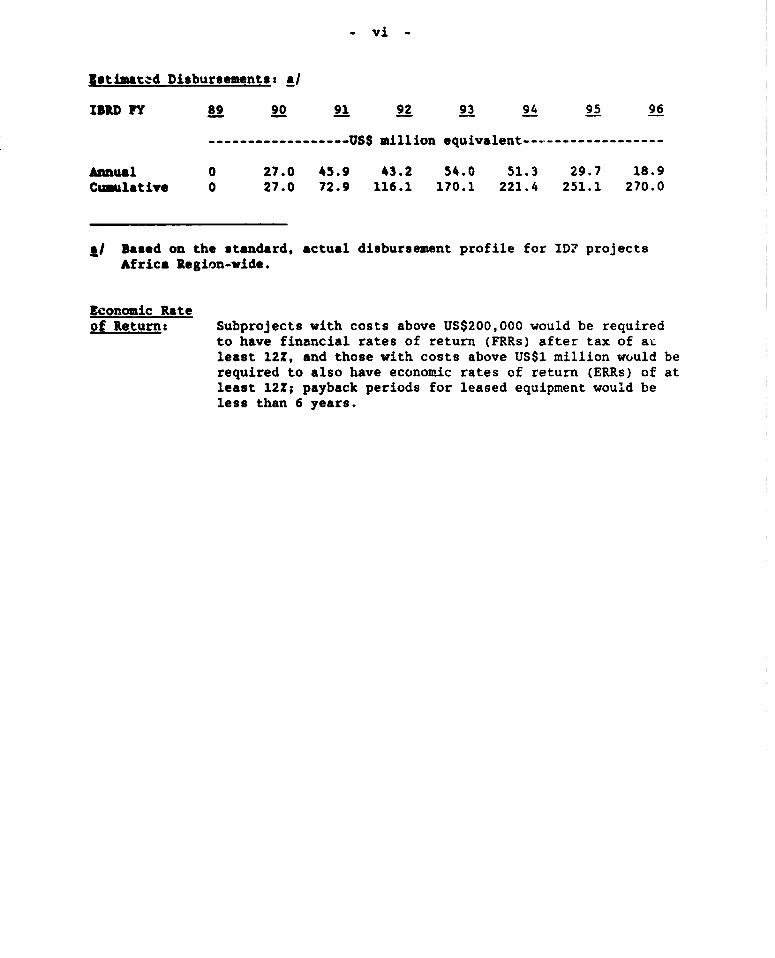

Ystimatzd Disbursements: a/

IBRD FY 89 90 91 92 93 94 95 96

------------------US$ million equivalent-----------------

Annual 0 27.0 45.9 43.2 54.0 51.3 29.7 18.9Cualative 0 27.0 72.9 116.1 170.1 221.4 251.1 270.0

a/ Based on the standard, actual disbursement profile for IDE projectsAfrica Region-wide.

Economic Rateof Return: Subprojects with costs above US$200,000 would be required

to have financial rates of return (FRRs) after tax of atleast 121, and those with costs above US$1 million would berequired to also have economic rates of return (ERRs) of atleast 122; payback periods for leased equipment would beless than 6 years.

NIGERIA

PRIVATE SHALL AND MEDIUH ENTERPRISE DEVELOPMENT PROJECT

I. INTRODUCTION

1.01 The Federal Government of Nigeria (the Government, FGN) hasrequested a Bank loan of US$270 million for a Private Small and MediumEnterprise Development Project (the Project) consisting of an integratedpackage of financial support programs, investment promotion, technicalassistance and extension services for small and medium scale enterprises(SMEs). In July 1986, with the support of a Trade Policy and ExportDevelopment Loan (2758-UNI), the Government launched an ambitious andfar-reaching structural adjustment program to promote economic efficiencyand long-term growth through stabilization policies designed to restorebalance of payments and price stability. The introduction of amarket-determined exchange rate and the liberalization of trade are themost important measures of the Government's adjustment program. TheGovernment has now placed a high priority on developing a nationwideprogram to assist private sector SMEs. The Government believes thatprivate sector SME development is an important vehicle to 3timulateproductive activity and generate a sustained supply response, thusencouraging the resumption of growth and efficient employment generation inline with Nigeria's resource endowments and within the ongoing adjustmentprocess.

1.02 The Project would provide a broad and integrated package offinancial and technical assistance services to productive micro-, small-and medium-size enterprises in the private sector. It includes fivecomponents: (a) credit to SMEs (the Line of Credit Component); (b) supportfor restructuring viable enterprises which are currently in financialdifficulties (the Pilot Financial Restructuring Component); (c) credit tomicroenterprises through selected non-governmental organizations--NGOs (thePilot Mutualist Credit Guarantee Scheme); (d) a leasing program to improveaccess of SMEs to long-term financing (the Equipment Leasing Component);(e) technical assistance program to: improve extension services to SMEsthrough direct involvement of the private sector and the banking system;strengthen credit delivery systems; expand channels of credit; and conductstudies to improve the policy framework for SME development (the TechnicalAssistance Component).

1.03 The Project will require total financing of about US$416 millionequivalent, including US$263.4 million in foreign exchange. The proposedBank loan of US$270 million will cover 65Z of the total financing required(1002 of the total foreign exchange and about 4Z of the local costs).

II. THE SETTING

A. The Economic Environment

2.01 Nigeria, with a population of 103 million, has high potential fordiversified development. The country has considerable mineral wealth;

petroleum accounts for 142 of total GDP and about 90? of exports. It aLaohas vast rese..-7es of natural gas, little of which is being exploited atpresent. The agriculture sector, with cocoa, oil palm, rubber, and cottonas the principal cash crops, employs about three quarters of the laborforce and accounts for 402 of GDP. Agriculture is primarily based onemall-scale farming, and productivity is generally low. The manufacturingsector accounts for about 102 of total GDP and employment. Servicesaccount for ver 25Z of GDP. In terms of many socioeconomic indicators,Nigeria is close to the rest of Sub-Saharan Africa. With the recent dropin oil prices and the subsequent sharp depreciation of the naira since1986, the GNP per capita is expected to be about US$280 in 1988 and US$235in 1989.

2.02 Buoyant oil revenues in the 1970s provided the basis for largeincreases in government expenditures designed to expand infrastructure andnon-oil productive capacity. But, with some important exceptions, e.g.,expansion in transport and educational opportunities, much of the publicspending was on economically inefficient projects. Agriculture exportswere particularly hard hit since the exchange rate was allowed toappreciate substantially. When oil revenucs collapsed in the early 1980Q,the Government responded slowly. Foreign exchange reserves were run downand external payments arrears piled up. When austerity measures were takenbelatedly in 1984, non-oil GDP fell sharply. The inefficiencies that haddeveloped during the period of strong oil revenues multiplied, as importrestrictions and other administrative controls were tightened in an attemptto contain the growing balance of payment crisis.

2.03 On coming to power in August 1985, the new Government declaredits intent to move from mausterity alone to austerity with structuraladjustment. The commitment to reform intensified with the sharp fall inoil export earnings in early 1986. The Government adopted an ambitiousstructural adjustment program covering the period from July 1986 to June1988. The World Bank supported the program (Loan 2758-UNI). The mainfeatures of the new macroeconomic program were: (a) the establishment of amarket-determined exchange rate; (b) the dismantling of the previous systemof import licensing, removal of the majority of import bans, and reductionin tariffs; (c) the removal of ex-factory price controls; (d) a package ofexport incentive measures including simplification of procedures andabolition of the agricultural commodity boards; (e) a tight monetary policyand gradual liberalization of financial markets leading to the abolitioa ofinterest rate ceilings in August 1987; (f) moves to restore equilibrium inpublic finances; and (g) restraints on and rationalization of federalcapital expenditures to generate resources required by the private sectorfor growth. The Government has announced its decision for theprivatization and comercialization of some 135 parastatals, whichconstitute the bulk of the public enterprises of commercial nature, andappointed a technical committee to handle this program. The publicinvestment program and the regulatory environment for private investmentare also currently under review.

2.04 The impact of the structural adjustment program, which has beenin operation for over 18 months, has been to favor exporters over producersof import substitutes with little value added, and to emphasize growth ofdomestic resource-based and intermediate goods industries. However, theprogram has not yet produced the economic growth that had been hoped for.

Preliminary estimates suggest a modest recovery in the urban economy in1987, with manufacturing output rising by 42 in real terms. But despitethese gains, overall GDP is estimated to have fallen by almost 52 in realterms during 1987. Over 502 of GDP derives from crude oil production andagriculture, both of which suffered large declines last year. A key aspectof the austerity period preceding the adjustment program was the rise inunemployment to more than 10T in urban areas. In response to theadjustment program, however, a return migrrtion of workers from urban torural areas has begun to take place as workers take advantage of betterrural employment opportunities. Even so, the unemployment problem hasworsened, as employment needs to rise by 32 pa. simply to keep pace withlabor force growth. The urban and rural unemployment reached 12? and 62 inSeptember 1987, respectively. The Government thus faces a serious problemof unemployment that exceeds 45? among urban-based secondary schoolleavers. The high level of unemployment, together with the populationgrowth rate of 3.3? p.a., is increasing the pressure on the Government toencourage the development of labor-intensive productive activities,including SMEs.

B. The Manufacturing Sector

1. Past Performance

2.05 With buoyant oil revenues and heavy public investments, themanufacturinAg sector grew rapidly at an average rate of about 122 p.a.betveen 1973 and 1982, compared with a growth of 3.7Z p.a. in overall GDP.Share of manufacturing in GDP thus rose from 42 in 1973 to a peak of 10.31in 1982. Between 1982 and 1986, however, real output of the manufacturingsector declined sharply in every year except in 1985. At the end of 1986,its share in GDP was about 9.72. Although data on the relative shares ofcapital versus labor are not available, it is clear that the manufacturingsector has become relatively more capital intensive: while its share inGDP more than doubled, the industrial sector as a whole now employs aboutthe same share of the total labor force as it did in 1973, i.e., about10.8?. Although, the general business environment in Nigeria has alwaysbeen strongly private sector oriented, the Government policies have greatlyinfluenced industrial development. The Government has undertaken, as inother oil economies, most of the country's investment in large basicindustries considered beyond the capacity of the private sector. Theimplementation of the indigenization decrees in the early 1970s led to adivestiture of foreign equity holdings and substantial Nigerian privatecapital were diverted into acquisition of exisa:ing assets. Publicinvestment in manufacturing thus grew more rap. dly than private investment,and the public sector dominated manufacturing investment. This wasfocussed principally on intermediate and capital goods industries--iron andsteel, pulp and paper, petroleum refineries and chemicals, cement, vehicleassembly, and sugar refining--with the aim of stimulating the developmentof a more diversified and integrated industrial base. Most of theseprojects suffered from inadequate project design, high initial projectcosts, cost overruns and excess capacity once completed.

2.06 Private sector decisions on investment and production patternshave been affected by the industrial incentives policies pursued. In the1970s, accelerated inflation and the appreciation of the naira contributedto a significant decline in competitiveness of domestic industry. With the

- 4 -

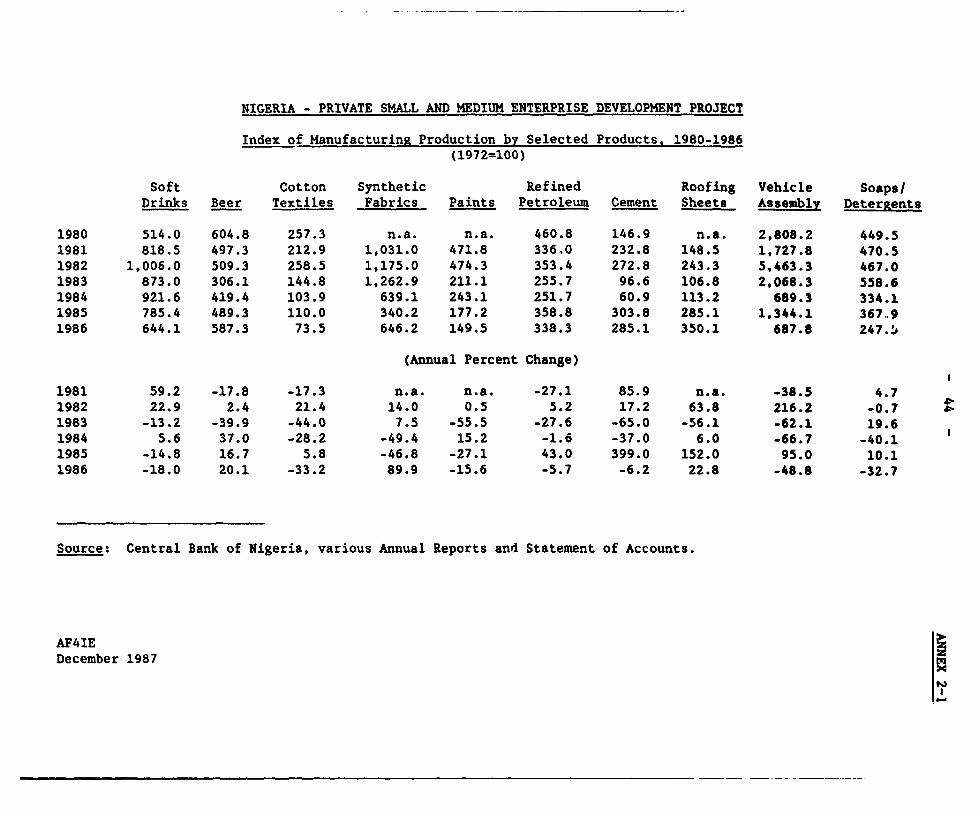

rapid deterioration in the balance of payments situation since 1981,tariffs were increased, quantitative controls were extended to a widerrange of imports, and import licensing and the allocation of foreignexchange were introduced. The protective import regime, used to insulatedomestic industries from foreign competition, encouraged the growth ofimport-based consumer goods and assembly industries with little domesticvalue added. The indastrial sector has suffered badly from the cutbacks inimported raw matbrials and spare parts over the past few years (Annex 2-1).Manufactured exports based on 2gro-processing, about 101 of exports in1970, have all but disappeared. Equally important, industrial productivityand competitiveness have been affected adversely by bottlenecks inindustrial infrastructure and the unavailability of skilled manpower.There have been widespread plant closures, extensive retrenchment of theindustrial workforce, and a substantial overall drop in manufacturingcapacity utilization to an estimated 30-402 and even lower levels incertain major inditstries. Enterprise profitability has, therefore,dropped and many firms are heavily indebted.

2.07 Manufacturing activity is essentially aimed at the domesticmarket, and is mainly concentrated in the large urban centers of Lagos,Kano and Kaduna. Among the wide range of manufactured goods are cottontextiles, soft drinks and beer, refined petroleum products, soap anddetergents, cement, paper products, chemicals and paints, plastic andrubber goods, wood products, metal products, and locally assembled trucksand automobiles. Consumer goods industries dominate the sector with 752 ofthe value added and 702 of the employment. The food, beverages and tobaccosubsector is the largest in terms of value added (32Z) and employment(20Z), followed by textiles and apparel accounting for 152 of the valueadded and 182 of the employment. The intermediate goods industriesaccounted for about 182 of the value added and 23Z of employment in 1984compared with 292 and 242, respectively, in 1971/72. The capital goodsindustries, after a very substantial increase from less than 1Z of thevalue added in 1971/72 to 222 in 1980, now represent a modest 7X of themanufacturlng value added. Most of the decline in capital goods industryis due to poor performance of the heavily import dependent vehicle assemblyplants. The manufacturing sector is estimated to be on average about 552dependent on imported raw materials.

2. Recent Reforms

2.08 Besides the ambitious trade policy reforms adopted in 1986 (para2.03), further reforms in the area of trade policy and to improve theclimate for private investment and rationalize the public investmentprogram are to be supported under the proposed Trade Investment and PolicyLoan.

2.09 Incentive System. The most important step in the adjustmentprogram has been the shift to a market-determined exchange rate. InSeptember 1986, the second-tier foreign exchange market (SFEM) comprisingan auction and interbank market was established. In July 1987, SFEM andthe official (i.e., first-tier) rates were merged, and all foreign exchangetransactions now take place at market-determined exchange rates. Theforeign exchange market (FEM) is a combination of an auction for foreignexchange (fortnightly on the basis of the Dutch auction system), and adealer market which operates in response to supply and demand. The

- 5 -

exchange rate in the auction of July 7, 1988 was N4.47 to the US dollarcompared with N1.6 to the US dollar on September 26, 1986. Foreignexchange is reaching the produc.ive sectors, with industrial raw materialsand capital goods absorbing over 702 of auction funds, compared with some602 of official allocations in the pre-SPEM period. Until recently, theforeign exchange market had been working well. However, in the last fewmonths, downward pressure on the exchange rate has sharply increased thedifferential between the exchange rates on the auction, where there hasbeen a small depreciation, and the interbank market, where the rate hasbeen free to respond to market pressures.

2.10 With the realignment of the exchange rate, the import licensingsystem was abolished, and the majority of import bans were removed. TheGovernment also abolished the 30? import surcharge, and, in October 1986,implemented interim revisions in import duty and excise schedules whichreduced the average trade-weighted tariff rate from 332 to 25Z, with mostrates falling in the range of 10 to 30Z. A comprehensive tariff review toformulate proposals for a more permanent, lower and uniform structure oftariffs and excise duty was completed in December 1987. To avoid imposingundue hardships on existing enterprises from a sudden change in tariffs,and to provide producers and consumers with a longer policy time horizonwithin which to make decisions, the niew tariff schedule is to be phasedover a period of 7 years. The Goverrm.ent has also transferred the dutyassessment and collection functions from the Customs and Excise Departmentto the banking system. The overall tariff structure is a significantimprovement in terms of providing a more certain policy environment withinwhich to make decisions and appropriate signals to investors on efficientresource allocation. Yet, there are significant anomalies in the structureof protection. The Government has established a Tariff Review Board toreview the tariff structure, correct anomalies and improve the structure ofprotection. In conjunction with the exchange rate liberalization,ex-factory price controls on manufactured goods were also abolished inSeptember 1986 to enable producers to operate profitably at import pricesbased on the market-determined exchange rate.

2.11 Export Promotion. Since January 1986, the Government has taken aseries of measures to promote export development. The most powerful newincentive to exporters is the unrestricted access to the foreign exchangemarket for realizing their export earnings and meeting their importrequirements. Non-oil exporters now have 10OZ retention rights. Tofurther encourage non-oil exports, the Government has (a) abolished allexport prohibitions and export licensing requirements; (b) simplifiedexport procedures; (c) abolished six agricultural commodity boards andtheir monopoly export powers; (d) introduced a rediscounting/refinancingfacility for exporters; (e) approved a duty drawback/suspension scheme; and(f) prepared a decree for the reorganization of the Nigerian ExportPromotion Council into an autonomous body with strong private sectorparticipation and strengthened export promotion capabilities.

2.12 Business ReRulations. To improve the business climate forprivate investment, the Government reduced the corporate tax rate from 452to 40? in January 1987, and granted tax free dividends for 3 years oncapital imported between 1987 and 1992. As part of the 1988 budget, theGovernment has exempted investment incomes from dividends, interest androyalties from income taxes beyond the present 15? withholding tax, and

-6-

allowed an additional 5Z initial capital allowance for plant and machineryfor manufacturing and agriculture production. In addition, both existingand new small enterprises with turnover of not more than 3500,000 will nowbe subject to a lower tax rate of 202 for a period of 3 years. Investorswill also benefit from the proposed establishment of the IndustrialDevelopment Coordinating Committee (IDCC) as a one-stop investmentfacilitating and promotional body. In addition, the Nigerian EnterprisePromotion Decree is under review to expand the range of activities in whichforeign ownership is permitted. The overall statement of the Government'spolicy on the role of the private sector will be included in a fBlueprinton Industrial Policy' to be issued shortly.

3. Impact of the Industrial Sector Reforms and Prospects

2.13 Available data suggests some recovery of activity in themanufacturing sector since the start of the adjustment program. Thus,while the index of manufacturing output fell by 52 in volume terms in 1986,estimates point to an increase by about 42 in 1987. At the same time,employment in manufacturing has fallen by about 52 since the opening ofSFEM, reflecting major rationalization exercise in many subsectors.Performance of industry has also been affected by weak aggregate demand dueto the loss in real income in the short-term following the structuraladjustment program. Surveys show that branches of industry with largedomestic value added have benefitted over assembly type of activities whichare heavily import dependent with low value added. Subsectors such astextiles, wood furniture, tanneries, food products, cosmetics and cementseem to be doing well. On the other hand, assembly operations (e.g., motorvehicles) are in trouble due to a combination of lack of demand, escalationof costs due to the sharp devaluation of the naira, and an inability tocompete with imports. Firms now have easier access to foreign exchange forimports of raw materials and spare parts and can plan their operationsproperly. Capacity utilization is, however, down due to lack of effectivedemand, unlike in the past when the supply shortages of raw materials andspare parts kept the capacity utilization low. According to a survey ofthe Manufacturers Association of Nigeria (MAN), there was an increase inaverage capacity utilization from 302 in 1986 to 372 in 1987, with widevariations among the subsectors. Most of the firms in agro-industries,beer, textiles, chemicals, operated at 402 capacity utilization or more,while firms in bakery products, electronics and motor vehicle assemblyoperations operated at levels below 202. Dependence on foreign sourced rawmaterials dropped from 622 in 1986 to 542 in 1987.

2.14 There is now considerable evidence of new interest in exportingas a result of the shift in relative prices through the adjustment in theexchange rate. Besides the increase in the traditional agriculturalexports (cocoa, rubber, palm produce, etc.), interviews with firms suggestthat new potential markets (Europe and ECOWAS countries) are being exploredfor exports of manufactured goods. Exports of items such as cosmetics,plastic shoes, palm kernel cakes, and textiles are already picking up. Inaddition, products such as tires, industrial adhesives, tiles andfiberglass boat shells are being added to the export list.

2.15 Overall, while the recent reforms will help generate new growthopportunities, they will force many enterprises to improve theircompetitiveness through restructuring, including phasing out those

-7-

activities which were kept artificially profitable in the past by anexcessively protective incentive system. Some enterprises are likely toremain unviable and may have to close down. Others vill have to reorienttheir activities through modernization investments, rationalization ofproduction processes, introduction of new technologiee and other reductionsin operating costs (including adjustments in the workforce). Maintenanceof existing assets was neglected in the past because of difficulties inobtaining foreign exchange for imports of spare parts and components.According to the survey by MAN, about two-thirds of the investments byfirms in the first half of 1987 were for plant changes, modifications andreplacements to improve efficiency. In the near term, manufacturing growthis, therefore, dependent to a large extent on the availability of importedraw materials, spare parts and components. Host of the new investments inthe near term are expected to be pursued by smaller, domestic resourcebased enterprises.

2.16 The exchange rate adjustment and accompanying tradeliberalization measures have led to far-reaching changes in the incentivesystem for industry. These, combined with an improved climate for theprivate sector, should help create over the medium- to long-term a bettermanufacturing sector which is consistent with Nigeria's resource endowmentsand comparative advantage. Nigeria's endowment of supply factors (adiversified agricultural and mineral resource base), demand factors (thelarge domestic market with over 100 million peopla), and catalytic factors(a sizeable and dynamic cadre of indigenous entrepreneurs) is favorable tooverall growth. Moreover, more than three-fourths of Nigeria's populationlives in rural areas and its participation and share in the market forexisting goods has been peripheral. Increases in rural incomes under thenew policy reforms should help bring this large segment of the populationinto the market for industrial goods. The policy reforms should emphasizegrowth of domestic resource-based and intermediate goods industries.Subsectors with good potential for growth include food and beveragessubsectors, agro-based non-food industries (textiles, leather products,rubber and rubber products, and wood products), industrial raw materialsand intermediate inputs (glucose and starches from crops, tires and tubesfrom rubber, and paints from petrochemicals), chemicals and buildingmaterials. Considering the sharp decline in manufacturing output over thepast five years and hence a low base, a growth rate approaching 8Z p.a.through 1995 is feasible.

C. The Small and Medium Scale Enterprise (SME) Sector

1. Sectoral Context

2.17 Various definitions of SMEs are used in Nigeria. Since 1985,NBCI has defined small scale enterprises (SSEs) as firms with assets(including working capital but excluding land) not exceeding N750,000 (orabout US$850,000 equivalent at that time). The Nigerian IndustrialDevelopment Bank (NIDB) defines medium scale enterprises as firms withproject costs between NO.75 and N3 million (or US$0.85 and US$3.4 millionin 1985 dollars). Since 1979, the CBN has defined SSEs as enterprises withan annual turnover of less than N500,000. With rapid inflation in theearly 1980s and devaluation of the naira, these definitions are no longerrelevant. For the purpose of the Project, enterprises with fixed assets(excluding land) plus investment under the Project not exceeding N10

million in constant 1988 prices (or US$2.5 million equivalent) will beeligible for financing. Recent statistical data indicating the number ofSMEs and relative importance in each sector are not available. Preliminaryestimates around 1980 placed the number of smaller enterprises employingfever than 10 workers at about 125,000. There are 'ndicaticns that theseSSEs account for about 702 of industrial employment, and 10-152 of themanufacturing output.

2.18 The most recent survey of smaller enterprises was conducted in1984 by the Nigerian Institute of Social and Economic Research (NISER). Itcovered 2,696 firms with a maximum capital of N150,000 (or US$200,000equivalent at that time) and with less than 50 employees (Annex 2-2).Textile and wearing apparel, food and beverages, furniture making, footwearand leather products, rubber and plastic products, basic metal andfabricated metal products for construction industry, and motor vehicle andother repair activities comprise the predominant small enterprises (86Z ofthe total number of SSEs in the sample). In terms of value added andemployment, wearing apparel, food and beverages, furniture, metal productsfor construction industry, and repair activities are the most important,accounting for 802 of the value added and 72Z of the employment in thesample. According to the survey, the average number of employees in a firmwas five, and 902 of firms were sole proprietorships. While about 352 ofthe managers did not attend any school and more than 752 possessed onlyprimary education, about three-fourths of the managers had workingexperience of five or more years, and about 88Z had received more than twoyears apprenticeship. They are also intensive users of domestic rawmaterials which accounted for about 602 of the total cost of materials.

2. Government Policies and Support Programs

2.19 The Government has long recognized the need to foster thedevelopment of small scale industries so as to stimulate employment,mobilize local resources, reduce migration from rural to urban areas, anddisperse industrial enterprises more evenly within the country. Theseobjectives were to be achieved through the provision of special financialan" technical assistance to SSEs. The focal point for all policiesaffecting SSEs is the Small Scale Industries Division (SSID) of the FederalMinistry of Industries (FMI); each State Ministry of Industry and Commercealso has its own SSID. The Industrial Development Centers (IDCs) under FMIand staffed by federal civil servants provide technical and managementassistance to SSEs. There are also a number of other public and privatesector agencies invc'ved in the provision of technical assistance andextension services to SMEs.

2.20 Financial Assistance. A Small Scale Industries Credit Scheme wasestablished by the Federal Goveniment in the mid-1960s. Loan managementcommittees, at the state level consisting of state civil servants,representatives of the IDCs and branch managers of local disbursing banks,were to administer the scheme. Due to political considerations in creditallocation and the lack of budgetary funds, the scheme was unsuccessful andis no longer active. In 1973, the Government established NBCI as aspecialized development bank and has relied exclusively on it to channelfunds to SMEs. During 1982-86, NBCI approved 122 projects with a totalloan amount of N85.1 million with an average loan size of N0.7 million.While NBCI's projects cover all sectors of industry, 362 of the loans in

-9-

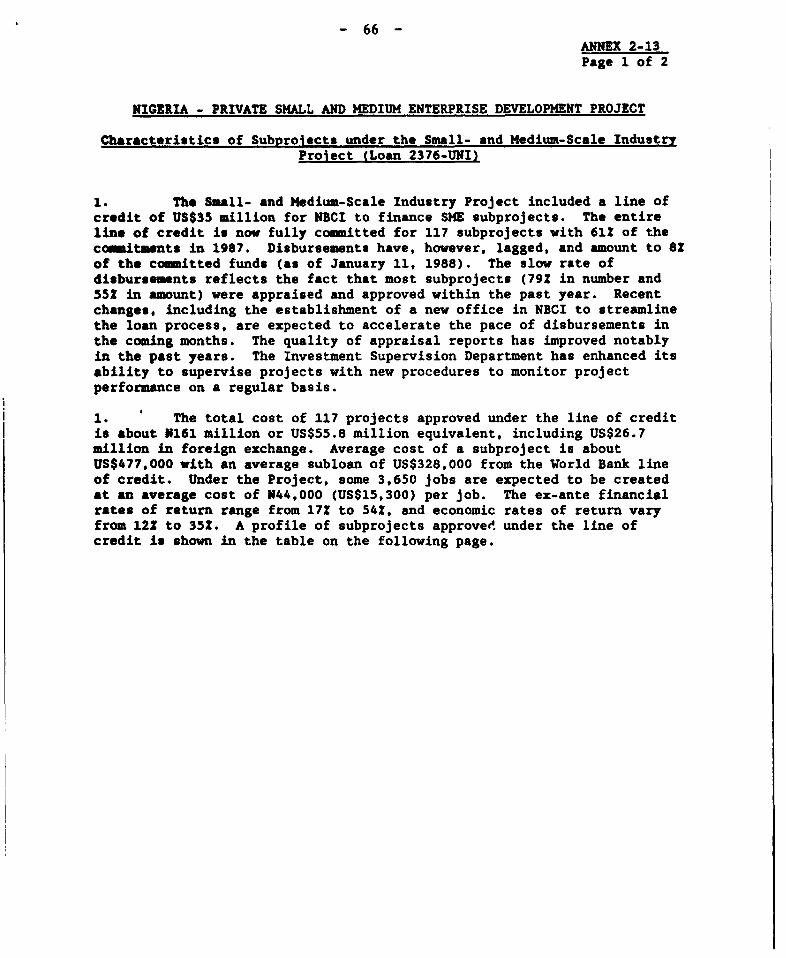

number (and 472 in amount) were for food and beverage industries. NBCIhas also received a line of credit from the Bank under the Small- andMedium-Scale Industry Project--Loan 2376-UNI (paras 2.45 to 2.46). Tochannel resources to SSEs, the CBN requires commercial and merchant banksto direct at least 16Z of their annual loans and advances to smallenterprises (paras 2.32 and 2.33). However, banks have never met thetarget because of the perceived high risk of lending to SSEs. TheGovernment also launched a job creation loan guarantee fund in 1987,administered by the National Directorate of Employment in the FederalMinistry of Employment. Labor and Productivity, for lending to unemployedgraduates for establishing small businesses.

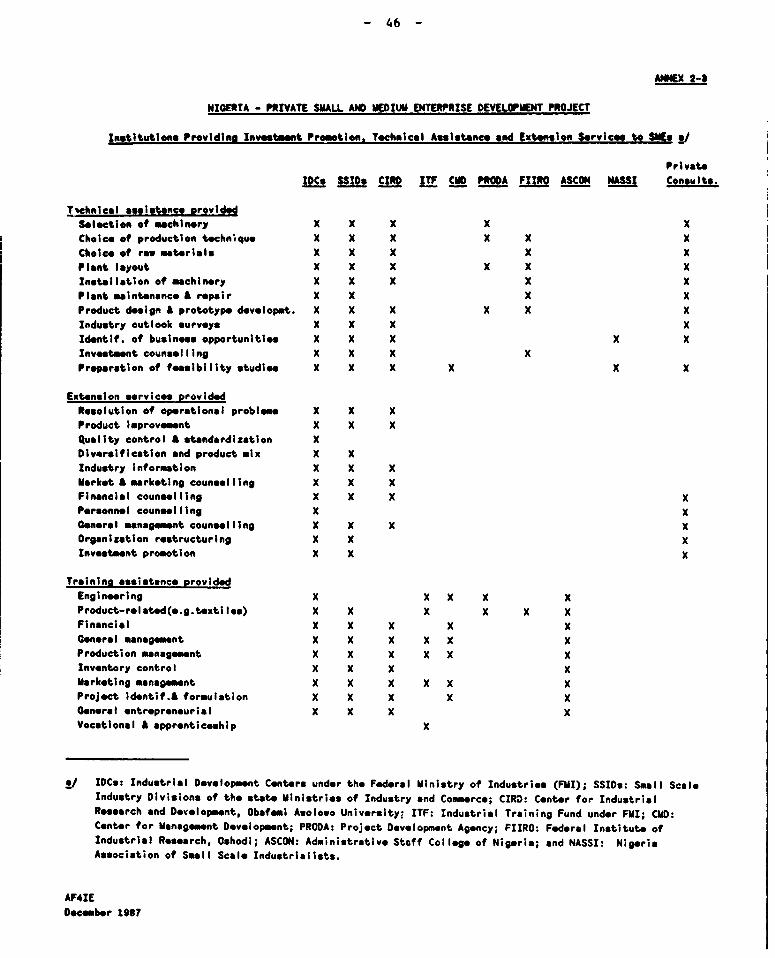

2.21 Extension Services and Technical Assistance. There are a largenumber of both public and private sector agencies involved in providingnon-financial support services to SMEs (Annex 2-3). FMI maintains anetwork of IDCs in various states to provide extension services. FMI isalso responsible for the Industrial Training Fund (ITF), an autonomousagency that collects and disburses a training tax levy on businesses with25 or more employees. ITF maintains a network of area offices to providetraining for the employees of enterprises that participate in the Fund.The SSIDs in some states have also provided limited extension services.Over the years, an increasing number of other government-supportedinstitutions have become actively involved in providing extension services(preparation of feasibility studies, management and technical advisoryservices and training) to the SME sector. These include the AdministrativeStaff College of Nigeria (ASCON), Centre for Management Development (CMD),Center for Industrial Research and Development (CIRD, Obafemi AwolowoUniversity), Federal ID,titute for Industrial Research, Oshodi (FIIRO),Project Development Agency (PRODA) and NISER. There are also variousprivate sector groups and associations such as the Nigerian Association ofSmall Scale Industrialists (NASSI), the Nigerian Council for ManagementDevelopment, the Nigerian Employers Consultative Association, MAN, and theNational Association of Chambers of Commerce, Industry, Mining, andAgriculture, who disseminate information and/or conduct training programson management, product selection, manufacturing, marketing, and othertopics of interest to SMEs. In addition, there are over two hundredprivate firms (mostly located in the Lagos area and other major cities)that provide consulting services to SMEs covering a range of ranagerial,financial, and technical specialties. In sum, there is a sufficient numberof eristing institutions and agencies to provide support to the SME sector.

2.22 The Government's efforts to strengthen extension services to SMEshave been supported by significant external assistance, used mainly forstrengthening IDCs operated by FMI (Annex 2-4). However, IDCs have notperformed satisfactorily because of continued shortages of operating funds,vehicles and training equipment. Under Loan 2376-UN1, a project componentwas included to support and strengthen (a) NBCI through technicalassistance and staff training to improve its project appraisal and lendingoperations; and (b) the delivery of extension services to SMEs throughtraining for staff of FMI, state ministries of Industry and Commerce, IDCs,and other relevant government supported institutions (e.g., ASCON). Whiletechnical assistance to NBCI has been implemented satisfactorily, progressin implementing the extension services subcomponent has been delayed andhas shown mixed results. During project implementation, the technicalassistance component was, therefore, modified to provide equipment for

- 10 _

selected IDCs, and to shift the emphasis in training from courses to workattachments for the IDC staff. About 300 persons have been trainedin-country, and some have received training overseas. including training oftrainers for the Entrepreneurship Development Programs (para 2.24), andwork attachments. Fcllwing long delays, the in-country work attachmentprograms are now being organized. The Government' s objective remains tofully *quip and strengthen IDCs in each state as soon as possible. But inview of the resource constraints and to reduce dependence on public sectorfinancing, there is, however, a need tos (a) concentrate efforts first onthose IDCs which offer the best prospects for success; (b) make IDCs moreautonomous in their day-to-day operations, and allow them to operate assoei-private institutions; and (c) allow them to charge fees for servicesof coomercial nature (e.g., the preparation of feasibility studies). FMIis at present formulating a plan of action for rationalizing the IDCnetwork, and considering the establishment of an umbrella agency foroverall coordination of existing agencies responsible for the delivery ofextension services, and to act as a referral agency for SMEs. The umbrellaagency may also be assigned the responsibility for operations of the IDCnetwork, and the establishment and management of industrial estates.However, it would be desirable to limit functions of the umbrella agency tothe coordination and referral roles only so as to keep it small, avoidduplication and unnecessary use of scarce Government resources.

2.23 It is not proposed to allocate any further technical assistancefunds to support the IDC network under the Project for t)e followingreasonst (a) sufficient funds are available under Loan 2376-UNI forstrengthening the IDC network and training; (b) UNDP has planned additionalassistance for IDCs; and (c) there is a need to increase the role of theprivate sector in the delivery of extension services so as to make theirdelivery demand driven, and enhance competition and efficiency. TheProject, however, includes the establishment of a Pilot Studies Facility tofinance entrepreneurs' costs related to consultants' services of theirchoice for the preparation of feasibility studies and other technicalassistance services. Training to SMEs in simple business skills (e.g.,bookkeeping, accounting and cash flow projections) will also be providedwith full cost recovery features (paras 3.09 and 3.10). The Bank ispreparing an Industrial Manpower Training Project, to be implemented by ITFin FMI, which will focus on increasing the quality and quantity ofon-the-job training with special emphasis on industrial and infrastructuremaintenance skills, and improving the delivery of training services to theindustrial sector.

2.24 Entrepreneurship Development. The Government has placed a highpriority on introducing entrepreneur identification and developmentprograms as an effective means of facilitating the establishment and growthof SSEs. Programs for identification, training, and development ofentrepreneurs can be effective components of a strategy to develop firstgeneration local entrepreneurs and assist them in the establishment ofsmall scale projects. Two separate entrepreneurship development programshave been developed and tested in Nigeria: the EntrepreneurshipDevelopment Program (EDP) based on a model developed by theEntrepreneurship Development Institute of India (EDII), and the Work forYourself Program (WFYP) based on a program developed by the DurhamUniversity Business School (UK) with ILO assistance. The EDP program ispromoted by NBCI, while the WFYP program is under the auspices of FMI in

- 11 -

collaboration with ASCON. Based on experience to date, NBCI and FMI arenow planning to implement their programs in a coordinated mJn'ier on anationwide basis (Annex 2-5). The Project includes assistance for periodicreviews of these programs by experts to assess their overall effectivenessand recomend necessary changes (para 3.12).

2.25 Other Programs. Lack of access to adequate infrastructure (e.g.,pover, roads and water) is a major constraint to the growth of industry inNigeria, particularly SHEs. The Government plans to establish industrialestates in every state under the Fifth Five-Year Plan (1989-1993).However, there is a need to involve the private sector to ensure cost andmanagement efficiencies, to reduce the burden on scarce Governmentresources, and to make the establishment of industrial estates demanddriven. The Project would, therefore, support a study to evaluatealternatives for implementing an industrial estates program on a commercialbasis with private sector participation (para 3.12). Nigeria has longrecognized the importance of technological development forindustrialization. There are a number of universities and specializedresearch agencies such as FIIRO, CIRD and PRODA which can meet thetechnological needs of industry. But SMEs face two main problems: lack ofinformation on the industrial production technologies available, and theneed to build up their technical capacity to assess, choose, acquire, andadapt technological knowledge. The UNDP is providing assistance to FIIROin developing a national industrial information center which would supplyinformation on industrial production technologies, and establish links withindustrial information networks at the national, regional and internationallevels. The Project would support a technology development study toformulate mechanisms for encouraging linkages between SMEs and researchinstitutions, and enhancing technical capabilities of the manufacturingsector in research and development (para 3.12).

3. Prospects and Constraints

2.26 Given the revised macroeconomic policy environment, and theGovernment's interest in SHE development (para 2.41), prospects for SMEgrowth are good. Growth in agriculture would increase the supply ofdomestic raw materials for SMEs such as food processing, raise ruralincome and expand the markets for small industries. Removal of interestrate ceilings will give SMEs better access to institutional credit (para2.31). Realistic exchange rate and an open trade policy favor more use ofdomestic raw materials, and enhance prospects for SMEs which use domesticraw materials more intensively than larger enterprises. Under the neweconomic policies, prospects for subcontracting have also improved aslarger enterprises are now forced to look for their irputs locally.Currently binding constraints for SME development are shortages of equityfunds and term credit on suitable terms, especially for smallerenterprises, and technical assistance (i.e., preparation of feasibilitystudies which meet requirements of banks).

D. The Financial Sector

1. The Institutional Setting

2.27 The financial system of Nigeria consists of (a) CBN; (b) 33commercial banks with 1,407 branches; (c) 15 merchant banks with 31

- 12 -

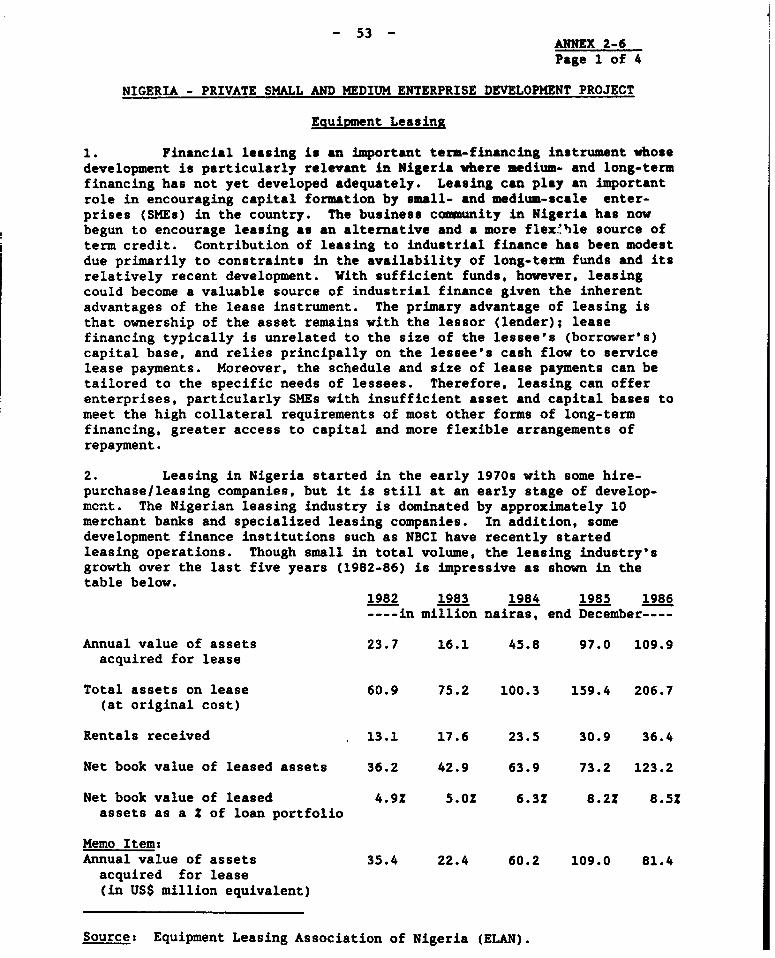

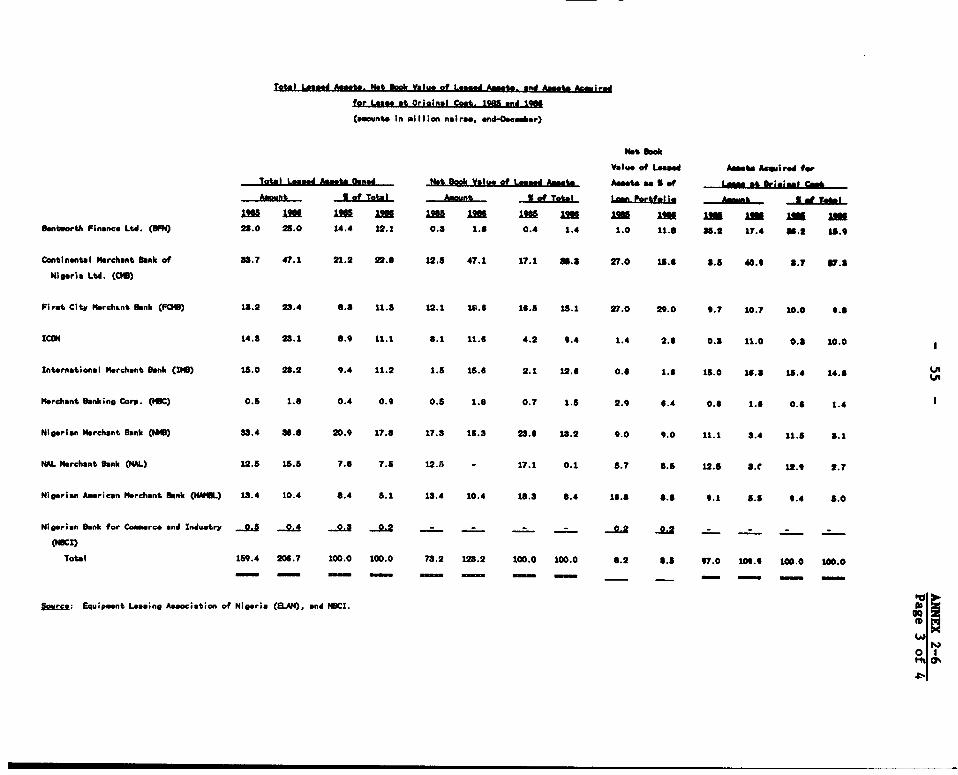

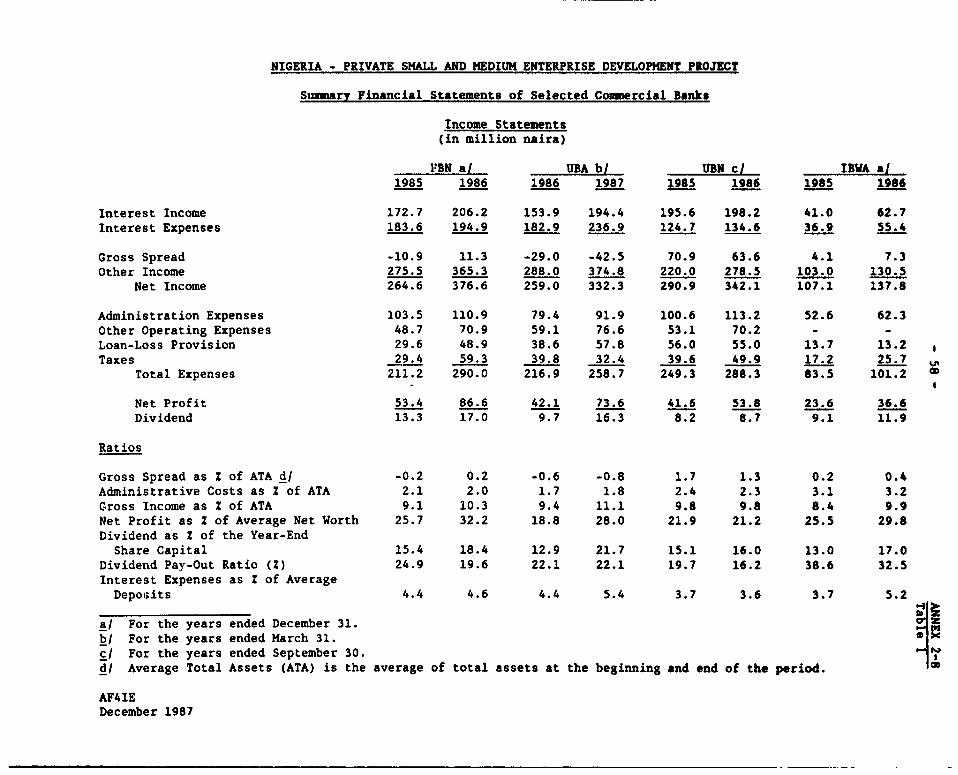

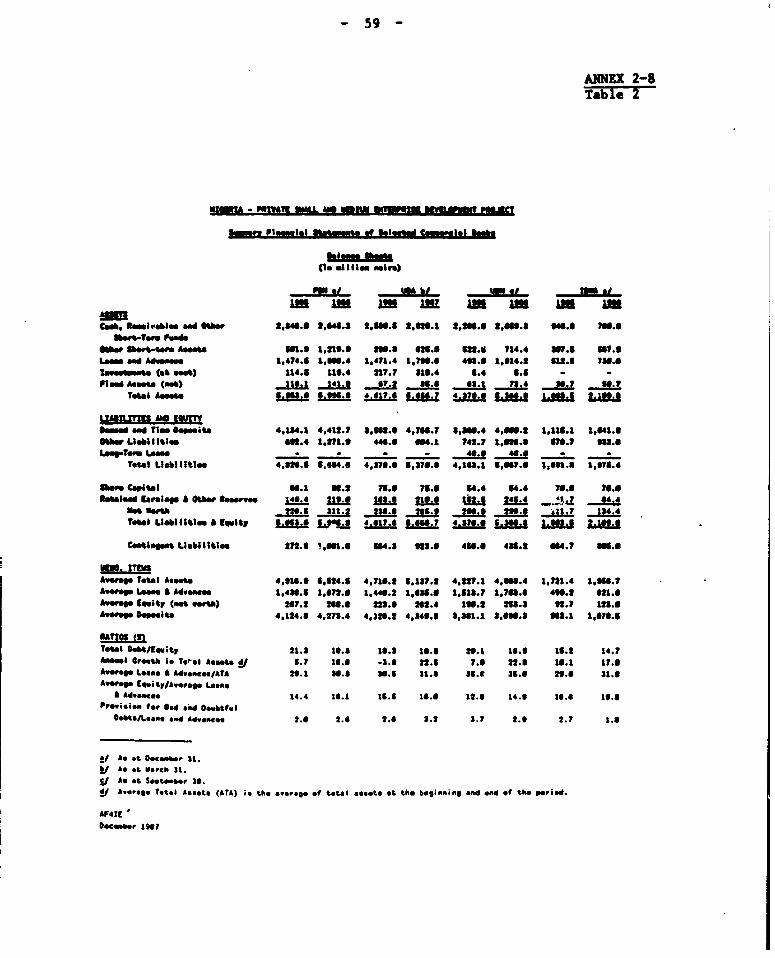

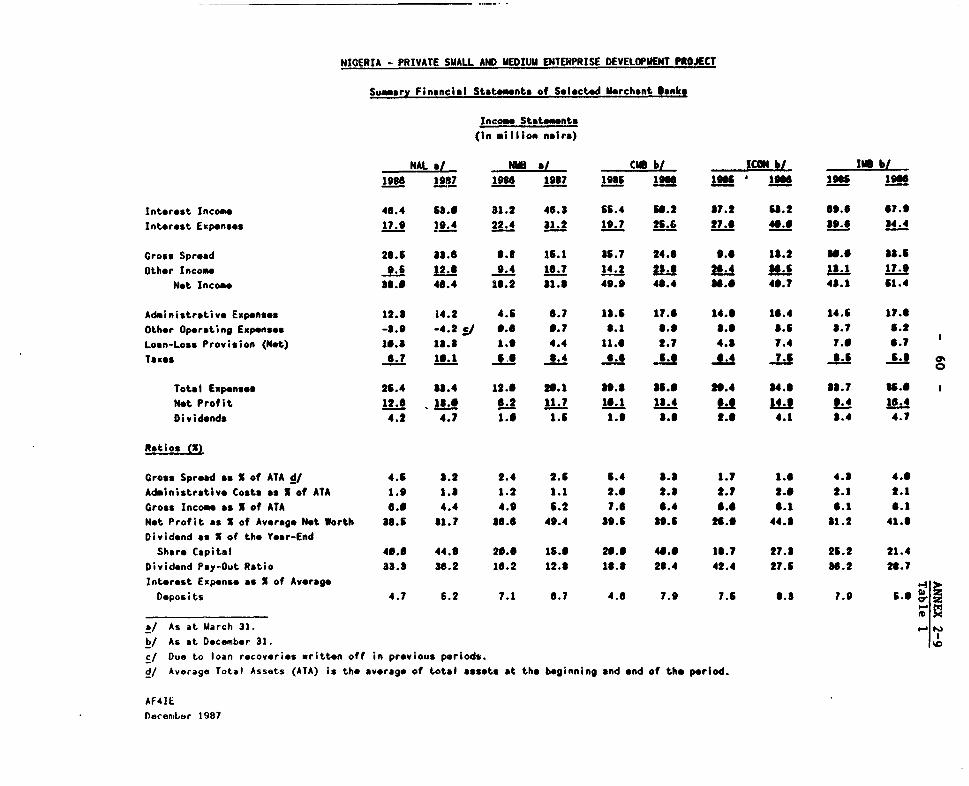

branches; (d) five specialized financial institutions of the FederalGovernment; (e) some twenty regional development finance companies; (f)insurance companies; and (g) the securities market. Under theindigenization decree of 1976, 60Z of the equity of banks must be held bythe Government or private Nigerian interests. Although activities of themerchant banks have grown rapidly in recent years, commercial banks reainthe largest financial intermediaries both in terms of their assets, andnetwork. Their share in the combined assets (148 billion) of thecommercial banks and merchant banks was 82Z in 1986. Among the commercialbanks, 3 banks 1/ account for about 40Z of the assets and the number ofbranches. The number of commercial bank branches in Nigeria has grownrapidly in recent years under the impetus of the CBN's rural bankingprogram which started in 1977. About 445 rural branches were opened duringthe first and second phases of the program (1977-83), and 51 out of theplanned 300 branches have been opened under the third phase (August1985-July 1989). Merchant banks are essentially wholesale banks, servingthe needs of corporate and institutional clients, and are governed byregulations similar to those for commercial banks. They may engage in thesame scope of activities as a commercial bank except for the acceptance ofindividual checking accounts. They also engage in equipment leasingservices which have grown rapidly in recent years (Annex 2-6). Out of the15 merchant banks, five banks 2/ accounted in 1986 for 45Z of the totalassets and 54Z of the total loans and advances by the merchant banks.

2.28 The Government supported specialized financial institutions of theFederal Government include NBCI, NIDB, Nigerian Agricultural andCooperative Bank, Federal Mortgage Bank of Nigeria, and the Federal SavingsBank of Nigeria. Among these, NBCI provides financing (both term loans andequity) for SMEs and also undertakes merchant banking operations; NIDBprovides both term loans and equity financing for relatively largerindustrial projects. Although NBCI and NIDB have thus far been the majorsources of long-term lending to the industrial sector, their combined loansaccounted for only 3.5Z of the total outstanding credit from the commercialand merchant banks at the end of 1986. Under the 1988 budget, theGovernment announced its decision to establish a National EconomicReconstruction Fund to refinance credit to SMEs in manufacturing,agro-allied industries and ancillary service activities on a nationwidebasis through participating commercial and merchants banks. Regulationsfor establishing the fund and its operations are under preparation.

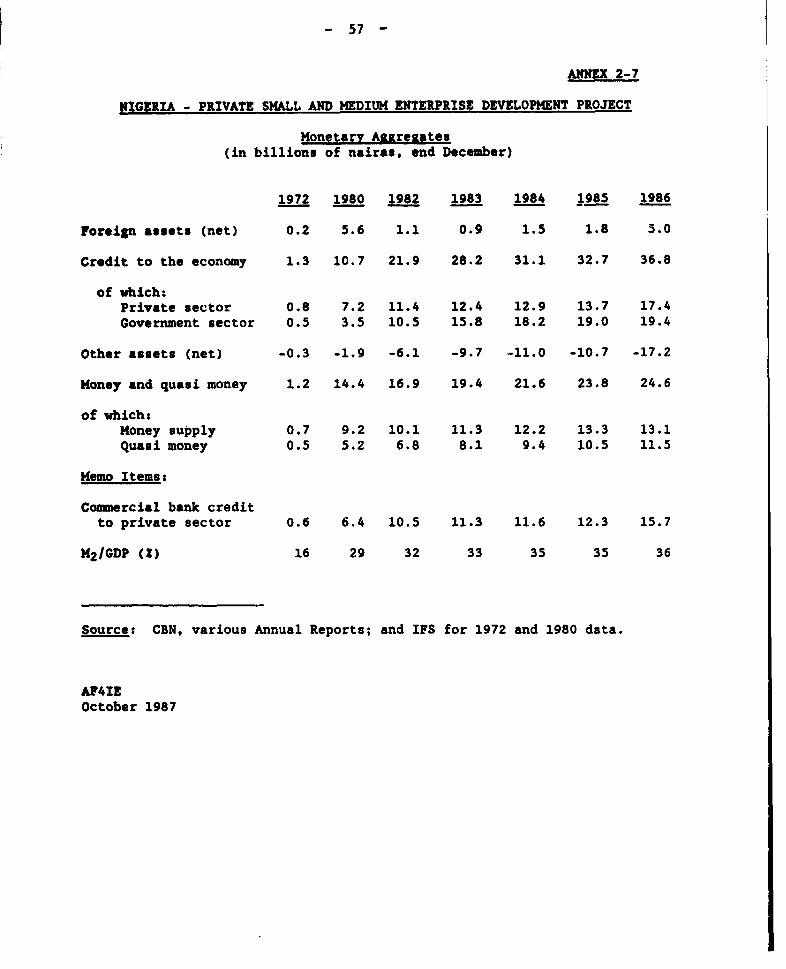

2.29 In terms of the ratio of broad money (M2 ) to GDP, the financialsystem more than doubled from 16Z to 361 between 1972 and 1986 (Annex 2-7).Despite this measure of growth, there has not been a real expansion infinancial intermediation between savers and investors. Much of themonetary growth took place after the increase in oil prices, initially inthe form of an increase in foreign assets and later because of increased

1/ First Bank of Nigeria (FBN), Union Bank of Nigeria (UBN), and UnitedBank for Africa (UBA).

2/ Continental Merchant Bank (CMB), ICON Merchant Bankers (ICON), NALMerchant Bankers (NAL), Nigerian Merchant Bank (NMB), andInternational Merchant Bank (IMB).

- 13 -

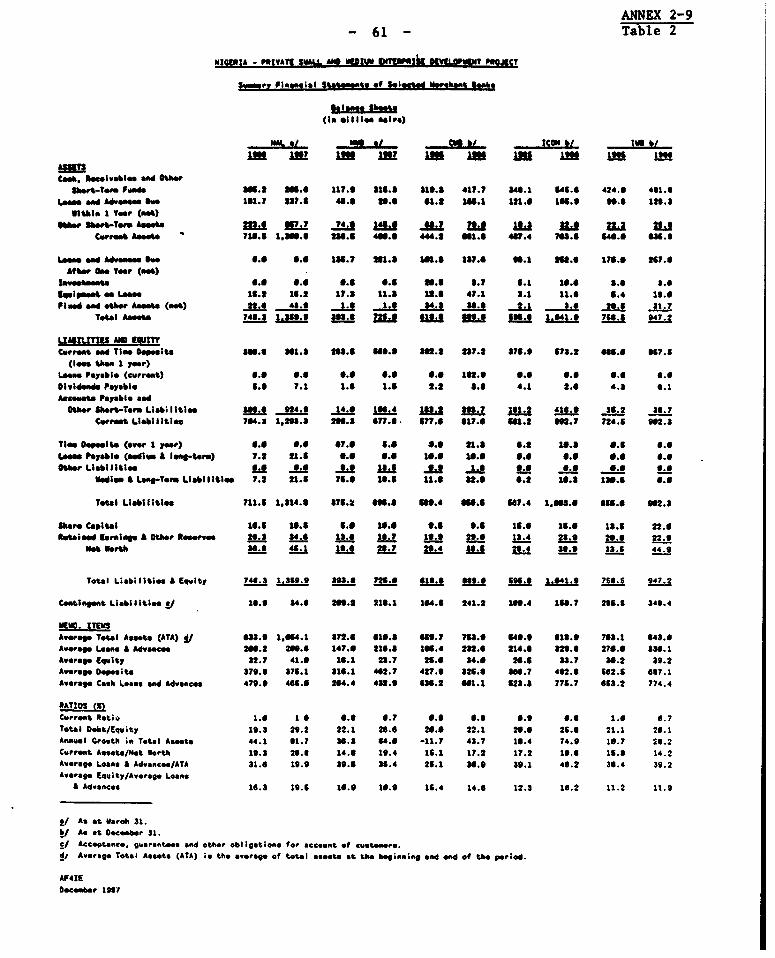

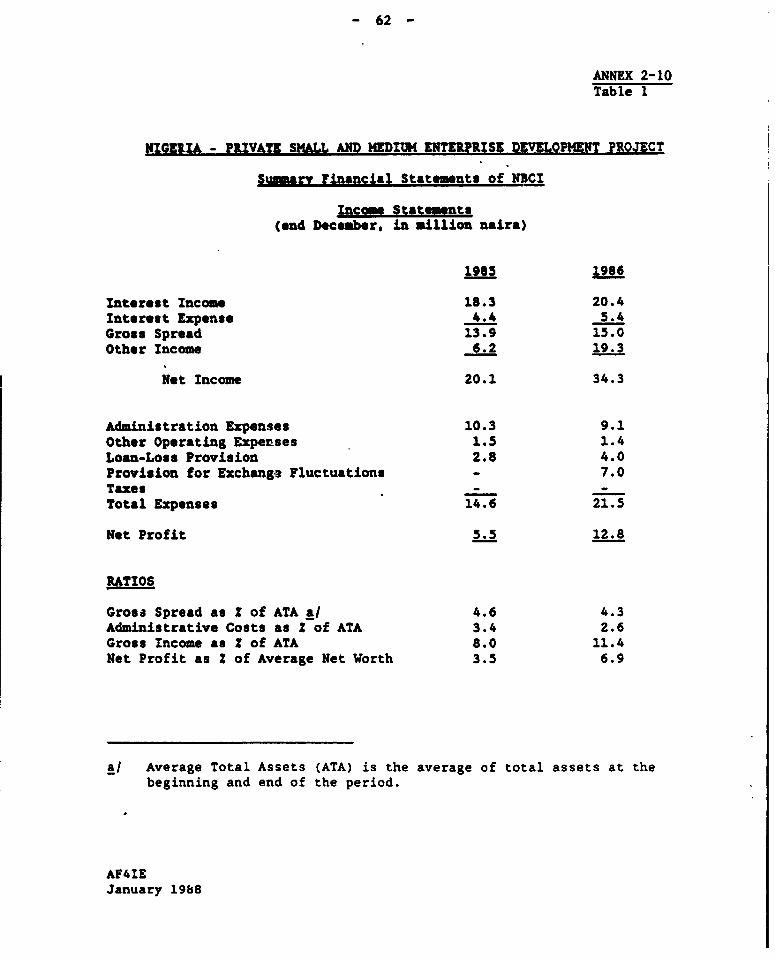

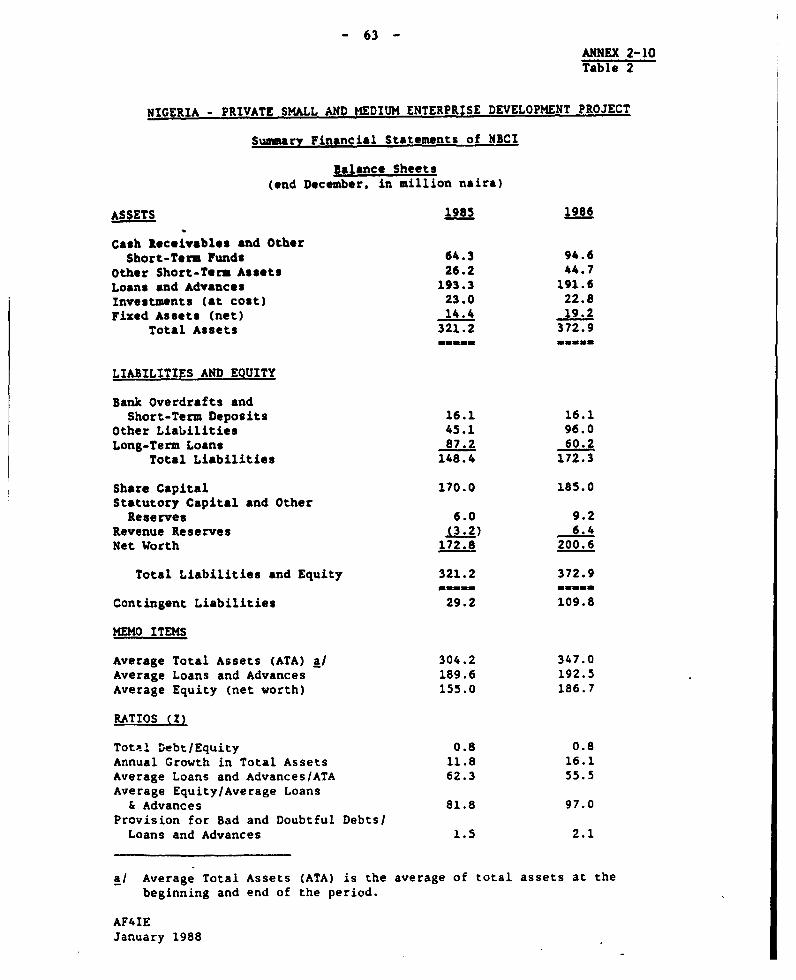

goverinnt borrowing. The array of financial assets available to themajority of savers is still limited to money, defined to include time andsavings deposits The Federal and state governments play a dominant rolein financial intermediation. They borrow actively from the financialsystm, and participate extensively in the ownership of many banks. TheFederal and state governments own most of the indigenous co=mercial banks.The Federal Government also has a controlling interest in the four largestcoamercial banks as well as in the most Important *wrchant banks. Thelargest co=ercial and merchant banks are free of Government interventionexcept for the appointmnts of managing directors, and they operate on acoaercial basis. Suamry financial statements of the four largestco ercial banks, five largest merchant banks 3/ and NBCI are given inAnnexes 2-8. 2-9 and 2-10; all have expressed strong interest in activeparticipation in the Project.

2. Financial Policy Framework

2.30 The Government's financial policies were previously embodied inguidelines for credit allocations to priority sectors and subsidizedinterest rates for these sectors. However, the special low interest ratesmade commercial lending to the priority sectors unprofitable, and thesectoral guidelines for credit allocation have not been generally met withbanks preferring to pay the penalties for shortfalls from these sectoraltargets. With the structural adjustment program, the Government hasadopted a more market-oriented approach and Nigeria is undergoing a rapidliberalization of the financial system. The number of priority sectors forspecial credit allocations has been progressively reduced, with only threepriority sectors remaining, e.g., agriculture, manufacturing and smallscale enterprises. Special interest rates have also been eliminated, andrecently ceilings on all interest rates have been removed. The Governmenthas decided to establish a Nigerian Deposit Insurance Corporation in 1988to protect depositors against bank failures and thereby enhance confidencein the banking system. These are major steps in both the mobilization ofsavings and efficient allocation of financial resources.

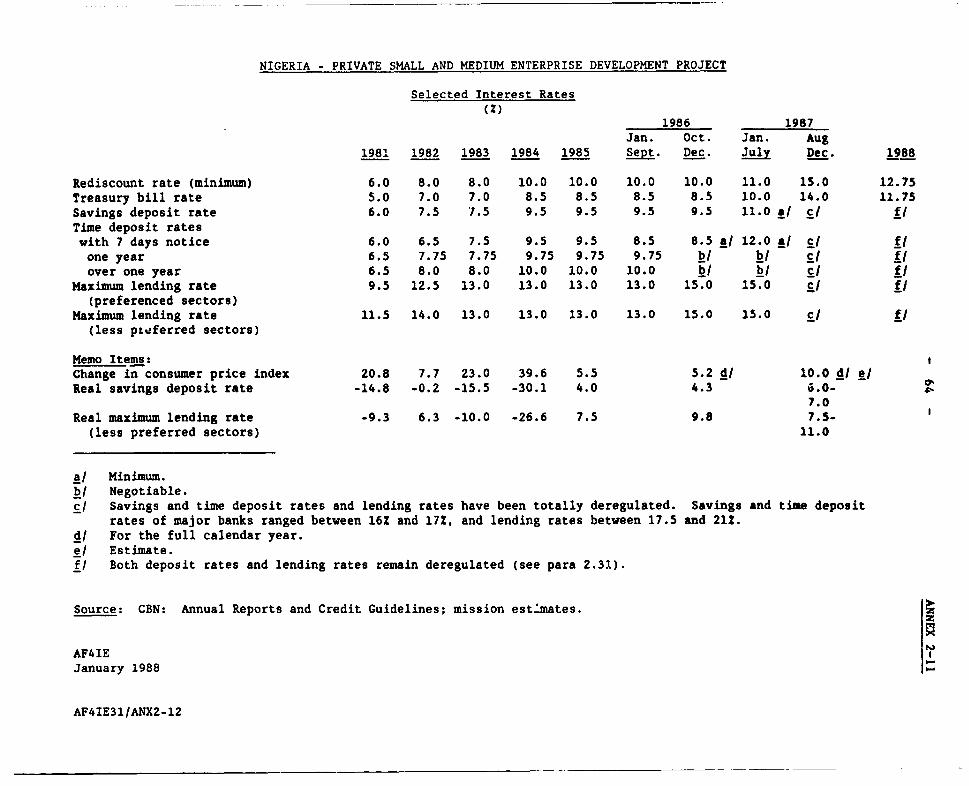

2.31 Interest Rates. The structure and levels of interest rates inthe formal financial system were controlled until recently by CBN throughstrict guidelines issued annually (Annex 2-11). Real interest rates havebeen negative in most years since the first oil boom in 1973/74, and theywere driven sharply lower during 1983 and 1984, as inflation increased inthese years to 23S and 402, respectively. With the marked slowdown ofinflation to 5.5Z in 1985, real interest rates became positive for thefirst time. The negative real interest rates discouraged real savings,discriminated against small and underprivileged borrowers in the allocationof credit, and resulted in a misallocation of resources and the flight ofcapital. The low interest rate policy is likely to have also encouragedthe use of capital intensive technology. In October 1986, CBN began toliberalize the interest rate policy: time deposit rates were allowed to benegotiated between the banks and savers, the maximum lending rate was

3/ Commercial banks: FBN, UBA, UBN, and the International Bank for WestAfrica (IBWA); merchant banks: CMB, ICON, NAL, NMB and IMB.

- 14 -

increased by 2 points to 15, and the differential between preferred andnon-preferred sectors was eliminated. Following these measures and thewithdraval of deposits by CBN from banks related to external paymentarrears to mop up excess liquidity, banks embarked on aggressive campaignsfor deposits, offering competitive and attractive rates to depositors. Thepace of financial policy liberalization increased in 1987. All ceilings onlending and deposit rates were eliminated as of August 1987, and thediscount and treasury bill rates were increased by 4 percentage points from111 to 15? and from 102 to 142, respectively. The discount and treasurybill rates were, however, reduced as of December 29, 1987, by 2.25percentage points to 12.75Z and 11.752, respectively, to stimulate growthof the economy, particularly investment. Savings and time deposit rates ofmajor banks are now about 13-15, and lending rates are about 16-18S. Therate of inflation was less than 102 in 1987, but it is projected to beabout 202 in 1988 reflecting increases for staple food products early inthe year and adjustments in public sector prices as well as the impact ofhigher import prices from the devaluation of the naira. As a result, boththe deposit and lending rates are negative in real terms at this time.Beyond 1988, however, the rate of inflation is forecast to decline to about15? in 1989, and 10? p.a. thereafter. The elimination of ceilings oninterest rates should allow banks to compete for funds more aggressivelyand should allow the market to equate the demand for credit with thesupply.

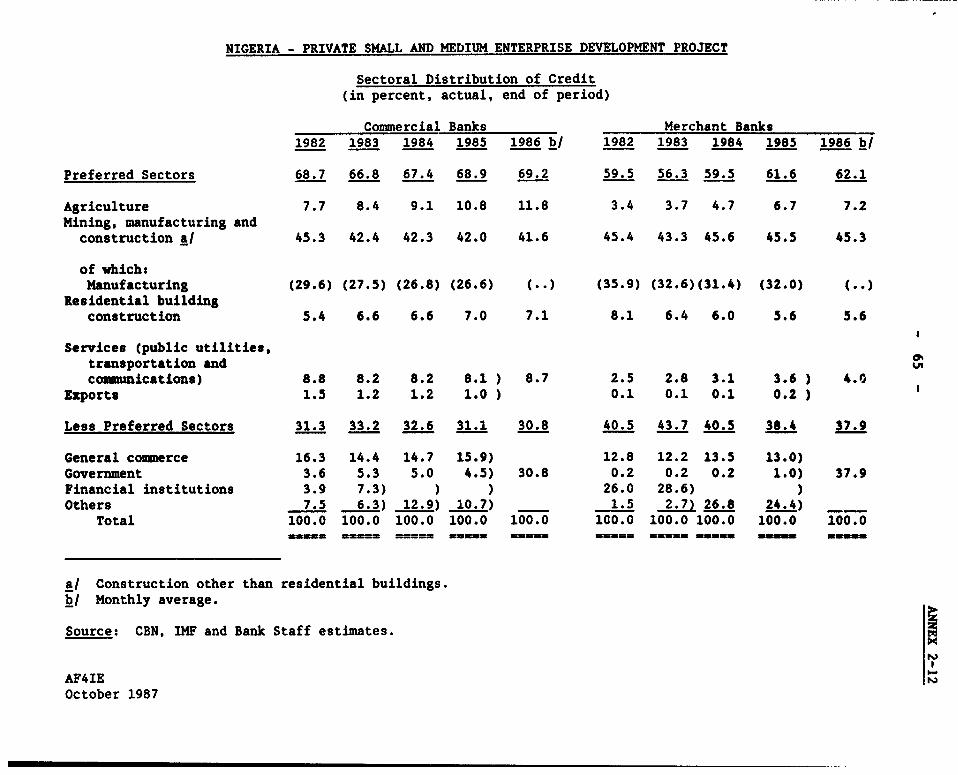

2.32 Credit Policies. The CBN regulates the activities of thecommetcial and merchant banks through annual ceilings on the expansion ofloans and advances, and complex and rigid sectoral credit allocationcriteria which specify minimum shares for preferred sectors. Annual creditceilings have been reduced since 1983 in line with the restrictive monetarypolicy in response to deterioration in the balance of payments andexcessive demand pressures. Penalt.es for noncompliance of ceilings wereraised substantially in August 1987. The ceiling on the growth of banks'credit to the private sector was, however, raised for 1988 from 7.4Z fixedfor the last three quarters of 1987 to 12.5Z so as to stimulate economicgrowth. Until recently, the economy was divided into some 18 sectors/subsectors for the purpose of credit allocation. For example, commercialbanks in 1983 were required to allocate a minimum of 1OZ of their loans andadvances every month to agricultural production, a minimum of 36? tomanufacturing, a maximum of 102 for domestic trade, and so on. Bothcommercial and merchant banks were required to extend 16? of total creditto small scale Nigerian enterprises with turnover not exceeding M500,000.Loans and advances by a rural branch were to be at least 30Z (increased to40? in 1985 and 452 in 1988) of deposits mobilized by it in that area. Inaddition, banks are required to maintain minimum cash and liquidity ratios.The above sectoral guidelines were so complex and rigid that the banks wereunable to comply with the stipulated targets. The actual sectoraldistribution of credit is shown in Annex 2-12. As for loans to small scaleenterprises, the prescribed target of 162 has never been met, though it hasincreased from a low. of 1.6Z in 1980 to 92 and 3.1? in 1986 for commercialand merchant banks, respectively.

2.33 In an effort to allow banks somewhat greater flexibility indetermining composition of their loan portfolios, the number of categorieswas reduced from the previous 18 to only 3 in 1987--agriculture,manufacturing, and small scale enterprises. Furthermore, for the

- 15 -

requirement of extending a minimum of 162 of total credit to SSEs, the sizedefinition of firms was modified for merchant banks in 1988. SSEs formerchant banks are now defined as firms with fixed assets below NZ millionor turnover below N5 million.

3. Development Constraints

2.34 Resource Mobilization. The recent liberalization of interestrates together with the tighter liquidity situation in the banking systemhas led to higher financial savings in naira assets than in the past andfavored a repatriation of capital from abroad. The rural branch bankingpolicy, while succesaful in increasing the number of branch banks, has beenperceived to be costly by the banks. The selection and allocation of sitesfor rural branches to the banks by CBN based on rec.auendation of the stategovernments, and the requirement that a significant share (45X beginning1988) of the deposits generated in each rural branch be relent by the samebranch have meant that the rural branches have not become an integral partof the planning and operations of the banks. There is, therefore, a needto reduce the cost of the branch program by integrating it into the overallbanking system (e.g., allowing the banks to select sites, and relaxing theobligation to lend 45% of each branch deposits in the same area). Therange and type of financial instruments available are also important forincreased savings mobilization. The opportunities available to individualsavers in Nigeria are limited largely tCz savings deposits with commercialbanks and cooperatives. Past policies discouraged the banks to activelyseek deposits. This has been largely corrected by the elimination ofceilings on all interest rates. But the credit expansion targets are setfor each individual bank separately and are not sufficiently marketoriented to encourage banks to attract new savings.

2.35 Lack of Term Financing. The current restructuring of theeconomy is predicated upon the entry of new firms and new investments inareas which have become or are potentially attractive under the newcost-price structure. These private investors will need financing, bothdomestic and external, to expand production. One of the major weaknessesof the Nigerian financial system has been its inability to generate asufficient amount of long-term financing mainly as a result of ceilings oninterest rates. Parastatals have obtained long-term financing from theGovernment through equity participation and direct borrowing, but privatebusinesses have raised little funding through capital markets, relyingmostly on their internal funds and on borrowings from financialinstitutions. However, because of low levels of term financing, this hasmeant for the most part short-term loans and overdrafts. Commercial bankswhich provide about 802 of the formal non-CBN bank credit tend to operateat the short-end of the market; only 122 of their maturities in 1986 werelonger than 3 years and 802 were below 12 months. Part of the explanationlies in the short-term nature of their deposits (602 of their deposits in1986 were demand and savings deposits). The merchant banks, who because oftheir efficiency attract wholesale term deposits from corporate andinstitutional investors (742 of their deposits in 1986 were time deposits),extend about 402 of their loans for over 3 years, and about 202 between oneand three years (1986). However, through continuous roll-overs andrenewals, the banks in effect supply more long-term finance to many oftheir creditworthy customers than their portfolios actually show. Thebanks seem to prefer this type of long-term lending to avoid illiquidity

- 16 _

and the risk of interest rate changes, and to increase their operationalflexibility. With the total deregulation of interest rates, the banksshould now be able to mobilize longer-term deposits by offering higherinterest rates which in turn would provide an appropriate ba:, forlong-term lending.

2.36 The past policy of ceilings on interest rates and complexsectoral credit allocation criteria in practice made financial systembiased in favor of large industrial and coamercial borrowers againstcertain priority sectors, mostly small enterprises and small farmers.Lending to these sectors is associated with relatively higher unit costs ofadministering the small loans and has higher perceived risks, apart fromthe lack of collateral and guarantees. The previous interest rate controlsthus prevented banks from recovering their costs on these loans. NBCI,which is a major source of long-tprm finance to SMIs, represents only 22 ofthe total outstanding credit from commercial banks for productive sectors.There is, therefore, a need to tackle effectively and quickly the seriousproblem of credit availability to SMEs, if the employment and productionpotential of these enterprises made possible by the recent economic reformsis to be realized. While the liberalization of interest rates is a majorstep toward improving the efficiency of the allocation of credit, there isa need to strengthen the legal system for collecting on bad loans, reviewthe collateral base for credit, and promote the development ofnon-governmental mutualist credit guarantee schemes (para 3.06).

2.37 Financial Stability of Banks and Portfolio Management. The mostimportant structural issue facing the banking system is its stability.Manufacturing enterprises have gone through a series of severe shocks andmany firms are in financial distress: (a) prior to recent economicreforms, due to the scarcity of foreign exchange and import license system,many enterprises operated at low levels of capacity utilization since theycould not import adequate raw materials; (b) many heavily import dependentprojects with little value added, which were viable under the previouspolicy regime, are unlikely to be viable under the new price system and mayhave to be closed down; (c) the capacity utilization of many enterprises islow due to the still weak demand and slow economic recovery; and (d) therehave been large foreign exchange losses on long-term loans denominated inforeign currency, and those arising out of the trade arrears. As a result,banks are faced with potentially high arrears in their portfolios. Thereis no uniform policy on the accrual of interest on overdue and doubtfulloans, and it is possible that income is overstated in some banks, asdoubtful debts are rolled aver. According to a recent study, the range ofthe ratio of provisions to loans!and advances in 24 commercial banks was 02to 27Z (9 banks had ratios above 15Z and 5 banks between 10 and 152), andin 12 merchant banks was 02 to 182 (one bank had a ratio of 182, and 4banks had ratios between 5 and 11Z). These wide discrepancies aredisturbing. The CBN has the power to require that additional provisions bemade for doubtful loans and it has disallowed the distribution of dividendsby 9 banks in 1986 that had inadequate provisions. Disallowing dividendsmay not, however, be strong enough a sanction for state owned barks whoseowners (state governments) may not be interested in receiving dividends.The two development banks (NBCI and NIDB) are also facing serious portfolioproblems. As of June 1987, about 602 of NBCI's portfolio was in arrears,and 422 of these arrears were more than 18 months overdue. In the case ofNIDB, while only about 32Z of its portfolio, as of September 1987, was in

- 17 _

arrears, its borrowers are likely to face serious difficulties in servicingtheir increased debt as they bear the foreign exchange risk.

2.38 Control of capital adequacy of the banks is also deficient. TheCBN requires that loans and advances by a bank may not be more than 12times its capital. This rule, however, does not take into account theother types of risk assets such as leasing, acceptances and guarantees.While the high reported profits of the banks in recent years and theprudeece of most banks have reduced the debt to equity ratios of commercialbanks from 44:1 in 1980 to 30:1 in 1986, and of merchant banks from 52:1 in1982 to 44:1 in 1986 (not counting the off-balance sheet items), there arewide variations among the banks. The latest published balance sheets of 9commercial banks showed a range of debt to equity ratio from 20:1 to 44:l,and of 4 merchant banks from 19:1 to 32:1. There is a need to subject thebanks to stronger regulatory pressure to classify their portfoliosproperly, work out their non-performing assets, make up the provisionshortfall, and strengthen their capital base. A strong regulatoryenforcement will also require strengthening of CBN staff in bankingsupervision. Simultaneously, there is a need to put in place a mechanismto assist viable corporate enterprises which are financially distressed inrestructuring their operations to improve profitability.

2.39 Capital Markets. In recent years, merchant banks have becomemajor operators in Nigeria's capital markets offering a wide range offinancial services, including conventional investment banking typeservices. Insurance companies, pension funds and other specialistlong-term institutions are also beginning to play a role in themobilization and deployment of longer-term financial resources. In thepast, however, most financing from institutions has been in the form ofdebt, with only NBCI and NIDB providing a limited supply of equity. Of thetotal combined term investments outstanding for these two institutions atthe end of 1986 of N660 million for example, less than 13Z had been in theform of equity. The pension funds and insurance companies, traditionalproviders of equity finance, are underdeveloped. Nigeria has a young butfairly active stock exchange and a functional Securities and ExchangeCommission. The market capitalization at the end of 1986 was sizeable atabout N7 billion (US$2.1 billion), including N3.2 billion in 57 Governmentstocks and about N3 billion in 9) equities. There has, however, hardlybeen any growth in the number of equities listed (99 in 1986 versus 90 in1980). A second-tier securities exchange set up in April 1986 to inducesmaller Nigerian companies to list on the Stock Exchange has so farattracted only five new issues as of June 1987. The inefficient pricingarrangements in which the Securities and Exchange Commission solelydetermines the pricing of securities, and other administrative arrangementshave also inhibited capital market development. Adequate sources of equityand quasi equity are necessary for the expansion of the small and mediumscale entrepreneurial sector, and for the restructuring of existingenterprises in financial difficulties including mergers, acquisitions andother financial engineering possibilities. The Government has, therefore,decided under the 1988 budget to allow the commercial and merchant banks totake equity position in corporate enterprises, and the CBN is preparingnecessary amendments to the Banking Decree. The equity position by a bankin enterprises is to be limited to lOZ of its paid up capital plus reservesin any one enterprise, and to one-third of its paid up capital plusreserves in all enterprises.

- 18 -

2.40 Further liberalization of the local securities markets,development of a regulatory framework for new financial instruments (e.g.,mutual funds), implementation of the Government's privatization program,and upgrading the technical capability of the Stock Exchange are necessaryto help develop the capital market. A more detailed analysis of the aboveissues is currently underway, and the proposed Financial Sector Policy Loanwill support reforms in the financial sector.

E. Government Obiectives and the Role of SHEs

2.41 Government Obiectives. The Government has assigned a highpriority to industrial development in the growth and diversification of theeconomy away from oil. The medium-term industrial strategy is to reduceimport dependence by accelerating the development and utilization of localtechnology, raw materials, and intermediate inputs through expansion ofprivate sector production and non-oil exports. The Government has alreadyundertaken a far-reaching program of reforms to rationalize the incentivesystem and encourage the private sector (paras 2.08-2.12). Yet, it willtake some time for the recent reforms to work through the system, for theshift and reallocation of resources to take place, and thus forrestructuring of the country's industrial structure. In view of thecontinued austerity and the serious unemployment problem, the Governmentfeels the urgent need to simultaneously combine growth promoting policiesand programs with the ongoing adjustment process. In this context, theGovernment considers private sector SME development as a positive endeavorto stimulate broad-based productive activity, generate a sustained supplyresponse, and to partially mitigate the social cost of adjustment.

2.42 Role of SMEs. Private sector SME development would contribute toNigeria's adjustment Process in several ways. They are complementary toand have significant linkages with the agricultural sector. SMEs promotebroad based agricultural development through the localized adaptation andmanufacture of simple farm equipment which increases productivitv. Theytend to be regionally more evenly distributed than larger industries whichare concentrated in the urban areas. Since SMEs employ generally largenumber of workers, they can become a major source of income, particularlyin small towns and rural areas. With the radical shifts in relative priceswhich have already taken place, SME development should also help establishlinkages with larger industries through subcontracting.

2.43 SMEs, in general, tend to be relatively efficient users ofresources compared with larger enterprises. They are more labor intensive,require less foreign exchange, and are intensive users of domestic rawmaterials. SMEs make the greatest contribution to developing an industrialtradition over time by providing a seed-bed, at the grass-roots level, todevelop entrepreneurial capabilities, management skills, and technologicalinfusion. In addition, they generally have small investment requirements,q-tick paybacks, and more flexibility. SMEs can adapt better and quickly toa changing environment. They also offer a unique opportunity fordeveloping the potential and active participation of women entrepreneurs inproductive activities for the overall economic and social development ofthe country.

2.44 The Government's emphasis on private sector SME development is,therefore, sound and represents an appropriate strategy for pursuing

- 19 -

longer-term growth in the context of the ongoing adjustment process.However, efficient and sustained growth of SMEs will require an integratedpackage of assistance including measures to: (a) foster entrepreneurialcapacity; (b) develop an innovative institutionai support system withactive participation of the private sector for delivery of promotion,technical assistance and extension services; and (c) provide credit inconformity with market mechanisms for financing rehabilitation and workingcapital needs of existing enterprises as well as new investments by SHEM.The proposed Project would assist the Government in these efforts.

F. Bank Assistance

1. Past Bank Involvement