Embed Size (px)

Citation preview

RESTRICTED

FILE COPY Report No. AF- 1 Za

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

THE ECONOMY OF ETHIOPIA

Volume I

September 30, 1963

Department of OperationsAfrica

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

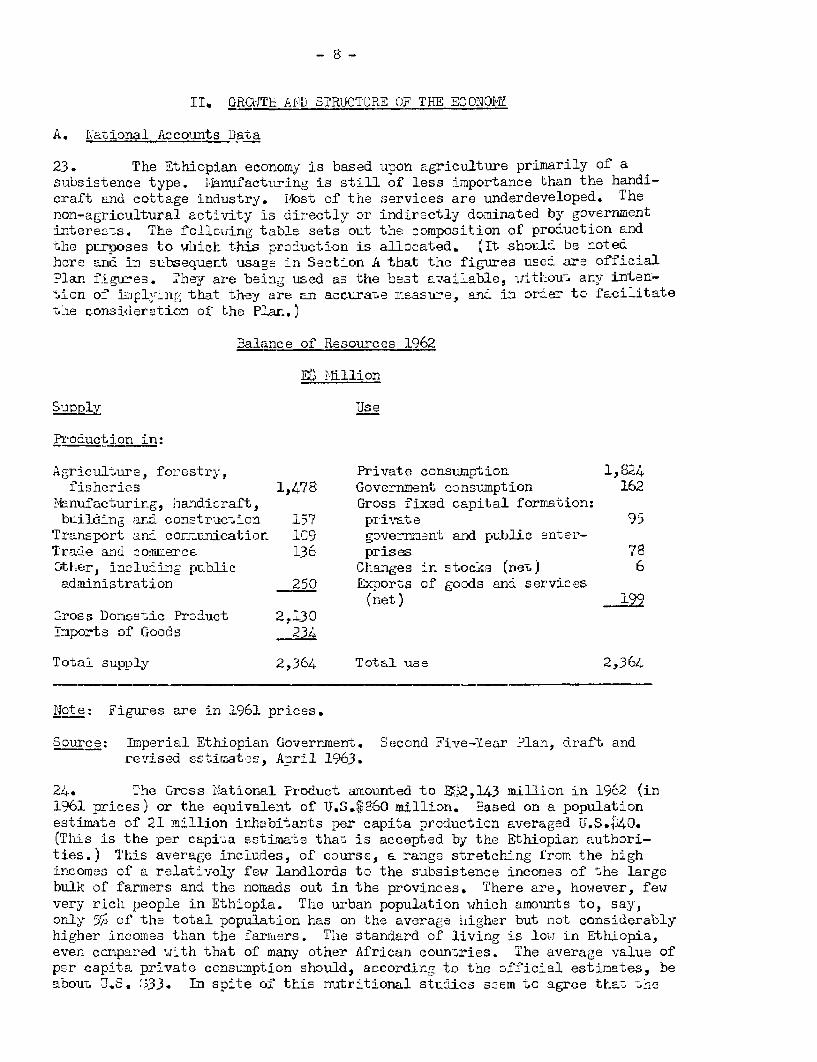

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

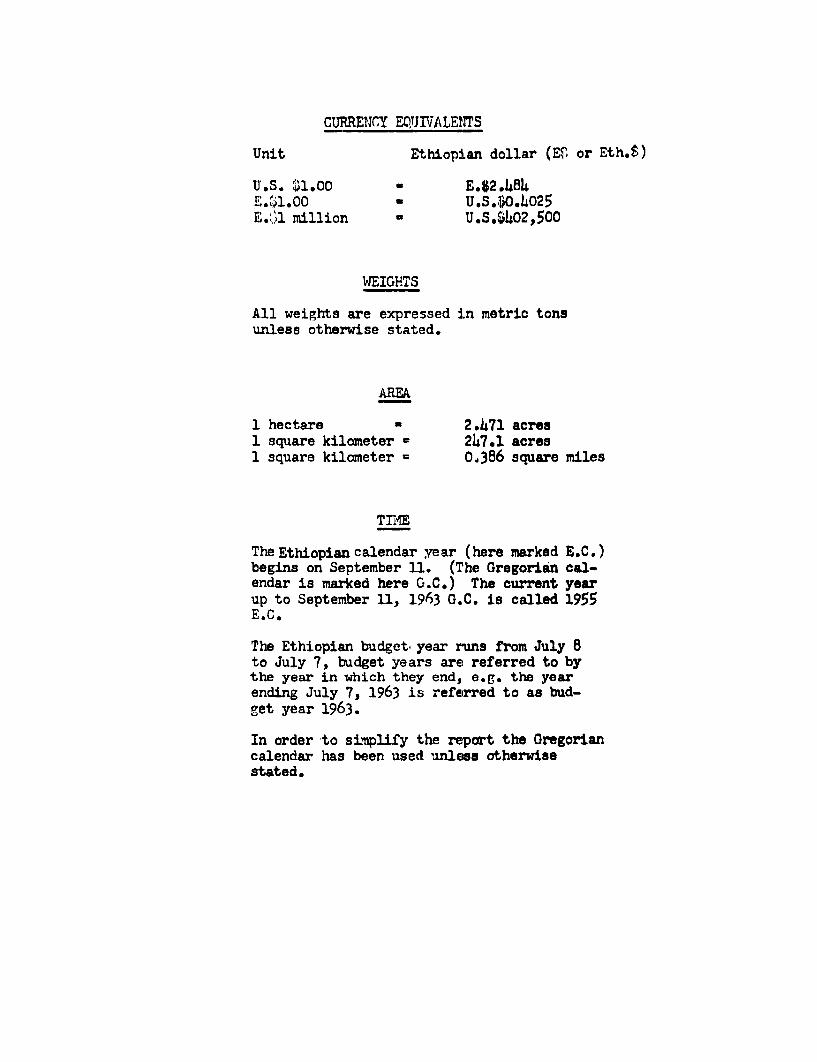

CURRETICY E4UT ALENTS

Unit Ethiopian dollar (Et, or Eth.$)

U.S. $1.00 - E.$2.484E.N'l.00 - U.S.o0.4o25E.4l million a U.S.$402,5O0

WEIGHTS

All weights are expressed in metric tonsunless otherwise stated.

AREA

1 hectare - 2.471 acres1. square kilometer 247.1 acres1 square kilometer 0.386 square miles

TIi_

The Ethiopian calendar year (here marked E.C.)begins on September 11. (The Gregorian cal-endar is marked here G.C.) The current yearup to September 11, 1963 G.C. is called 1955E.C.

The Ethiopian budget year runs from July 8to July 7, budget years are referred to bythe year in which they end, e.g. the yearending July 7, 1963 is referred to as bud-get year 1963.

In order to simplify the report the Gregoriancalendar has been used unless otherwisestated.

TIE ECONOMY OF ETHIOPIA

Table of Contents

Page

BASIC DATA

MAP OF ETHIOPIA

SU1lEARY AND CONCLUSIONS . . . . . . . . . . . . . . . . . . .

I. BACKGROUND FOR DEVELOPMENT . . . . . . . . . . . . . . .

II. GROWTH AND STRLCTURE OF THE ECONOMY . . . . . . . . . .

A. National Accounts Data . . . . .. . .. 8B. Production and Employment by Sectors . . . . . . . . 10

Agriculture . .............. 10Forestry . ... ... ... ... 15Fisheries ...... ... . . . . . . . . . 16Mining . . . . . . . , . . . . . . . . . . . . 16Industry and Handicraft . . . . . . . . . . . 17Building and Construction . . . . . . . . . . . 19

C. Investment Policy . . . . . . . . . . . . . . . . . 19D. Transport and Utilities . . . . . . . . . . . . . . 21E. Education ..... .... .... ... 23F. Public Finances . . . . . . . . . . . . . . . . . . 25G. Money, Credit and the Capital Market . . . . . . . . 31H. Prices and WIages . . . . . . . . . . . . . . . . . 36I. External Finance and Trade . . . . . . . . . . . . . 37

Balance of Payments . . . . . . . . . . . . . . 37Foreign Aid . . . . . . . . . . . . . . . . . 38Foreign Exchange Reserves . . . . . . . . . . . 38External Debt ..... ...... 39Foreign Trade . . . . . . . . . . . . . . . . . 40

J. PLanning . . . . . . . . . . . . . . . . . . . . . 112

III. LONG-TERM PROSPECTS AND CREDITWORTHINESS . . . . . . . . 3

-2-

AD)PENDITOES

1. TRANSPORTATION AND CO,UTNIICATIONS FACILITIES

2. EDUCATIONAL SYSTEM

3 . GOVSRNiNT INVEST?EITS AT ENM OF INDIVIDUALFINANCIAL YEARS

4. iJIAJOR liONETARY INSTITUTIONS AND THEIR FUNCTIONS

5. DEVSELC'Th T`1-,T L3ANK OF ETHIOPIA

6. STATIS,TICAL A?P?ENDIX

BASIC DATA

Area 45jO000 sq. miles

Population estimate 15-21 million (21 million is theofficial estimate)

GNP estimate (1962) U.S. 8 560 million

Per Capita GNP estimate U.S. ki 40

Central Government Budget 1962 (actual) U.S. 4 million Equivalent

Ordinary Revenue 80Expenditure 77

Extra-ordinary or capital expenditure 25of which financed from external sources 17

Balance of Payments 1962

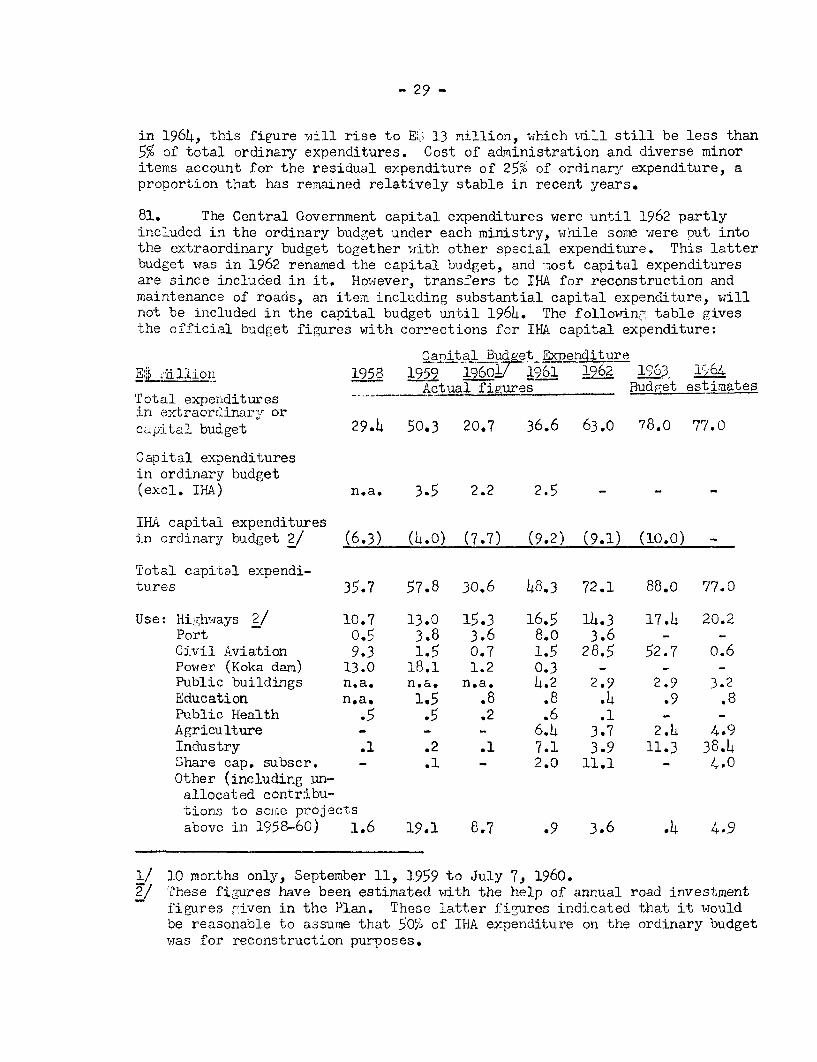

Exports f.o.b. 83

of which coffee 52%hides and skins 12%oilseeds and oilseed

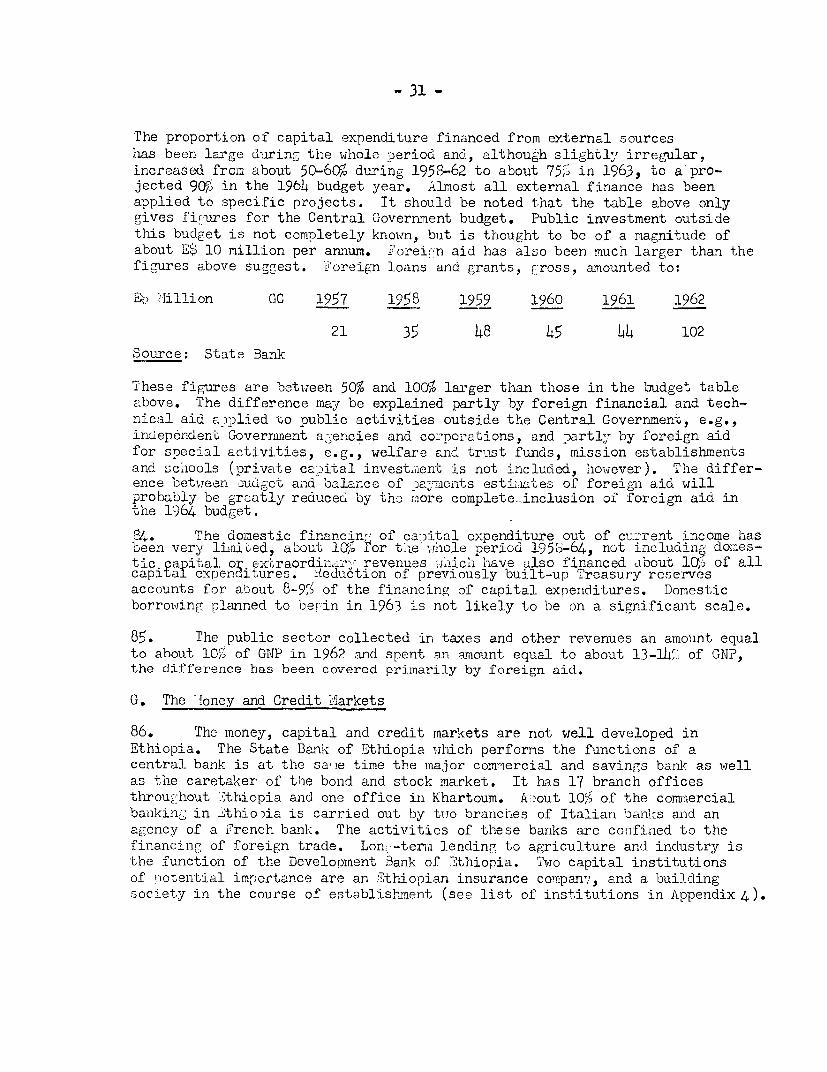

cakes 12%cereals and pulses 3%

Imports c.i.f. 10o

Other current payments, net 9

Capital inflow, net 40

Increase in foreign assets 10

Foreign Exchange Reserves

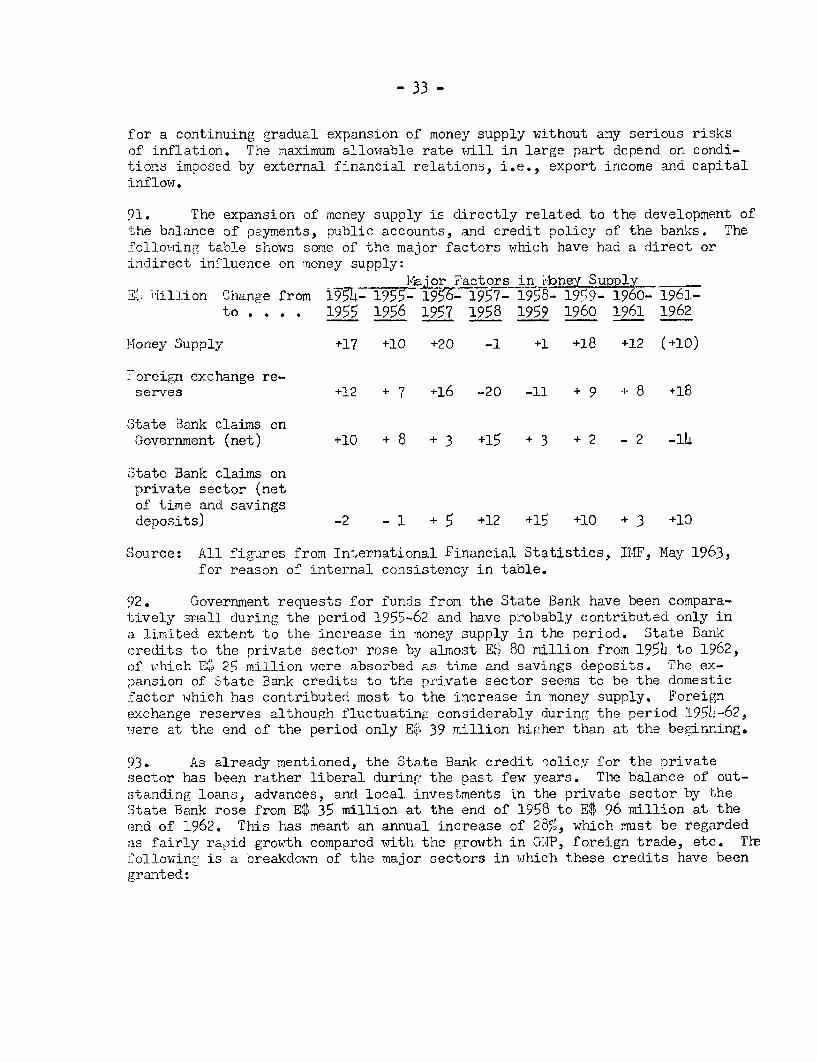

iy 31, 1963 75

Public External Debt

Outstanding December 31, 1962

Net of undisbursed 43.4

Including undisbursed 67.8

Major additions Jan. 1-April 30, 1963 13.5

ETHIOPIAIMAIN ROADS

/ RAILWAY400dBerOl f x . sc

S^bd f jR ," M r,;, 1 3ILOMEITOS 0, to r <@ Endc AdsCoof .. , + \; .t~~~~~0 o _1 29

> > 0! | } M ~~~E K L -,. ' .. '

Ad,

ASSA GONDER Mo, Chew

63 f; SX/orgoro Alu4emolo //

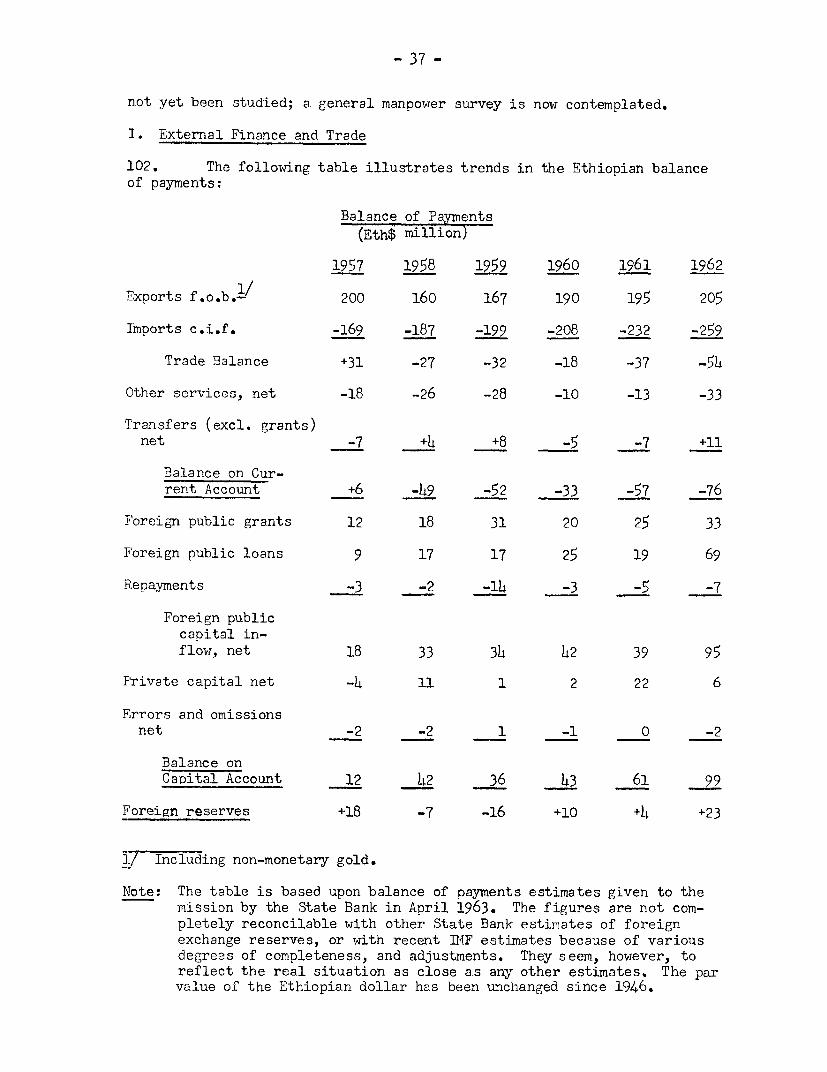

*ebro bor Woldio Sd 0 Aden

D.ngh.e1o 1. a DESSE Bole / .

/ \ < \~~~~on COebroI0 ) /

| Ghimbi*,EKEMPTI AD 5_°2° Jggggog S O M A L IA. Mk 1or0 M ABA

>~~~~~~~~Bro 500,0 SoloLE S,r /o

S.dd. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ -

V.

-~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ N~ ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~-

MAY 1963

THE ECONOIT OF ETIHIOPIA

Summary and Conclusions

1. The geography and topography of Ethiopia, the unique culturalheritage, her historical development and her long independence maintainedover centuries, go a long way towards explaining Ethiopia today, her semi-isolation until recently from the outside world, and her recent appearanceon the world scene as a country seeking development and inviting the helpof external assistance in this task. The basic framework of the governmentderives from the Constitutions of 1931 and 1955. In fact most power reposesin the Emperor. The Council of Ministers, headed by a Prime Minister, isresponsible to the Emperor and not to the Parliament. The administrativestructure of government generally leaves much to be desired with respectto the crucial role it must inevitably play in the country's development.The absence of coordinated collective ministerial activity as well as lackof coordination in and between levels of government has imposed a limita-tion on economic development, and continues to do so. Some of recentdevelopments in public administration hold, however, some promise forimprovemnen-ts, but administrative reorganization remains a pressing problemif growth is to be achieved.

2. The Government has played a large role in the economy in the pastand this tendency remains. It published the c3econd Five-Year Plan during1962. The Planning Office, however, does not occupy a position to enableit to carry enough weight to delineate and follow through on governmentdeveloprment policy as outlined in the Plan. The Second Five-Year Planenvisages a change toward a higher proportion of investments in directlyproductive sectors than in the past as well as a significant increase inthe overall level of investment; it seems quite likely that both of thesetrends will develop, but not to the full extent planned. A major lirnita-tion, on the degree of fulfillment of the Plants objectives will probablyarise from entrepreneurial and private financing stringencies, two elementsassumed to be supplied to a large extent from abroad. An increase in theprivate capital inflow in the near future to the extent required by the Planseems doubtful.

3. The public development effort is not particularly striking as faras public savings and public consumption of a recurrent exoenditure natureare concerned; but seems satisfactory as far as capital expenditure is con-cerned, provided of course that the projected large increase in foreign aidbecomes available. This very availability, however, is likely to be adverselyaffected by the limited domestic resource mobilization effort, which willdiminish the country's capacity to match foreign capital with local resources.

4. The economic potential of Ethiopia has not been fully explored andin any event has not been fully exploited. The fertile soil, the range ofclimate, and the level of rainfall hold out considerable potential forgrowth of agricultural production, including cattle-breeding and animalhusbandry generally, given the right stimulus and support, e.g. land reform,extension services, credit and marketing systems and research. IvMineral

- ii -

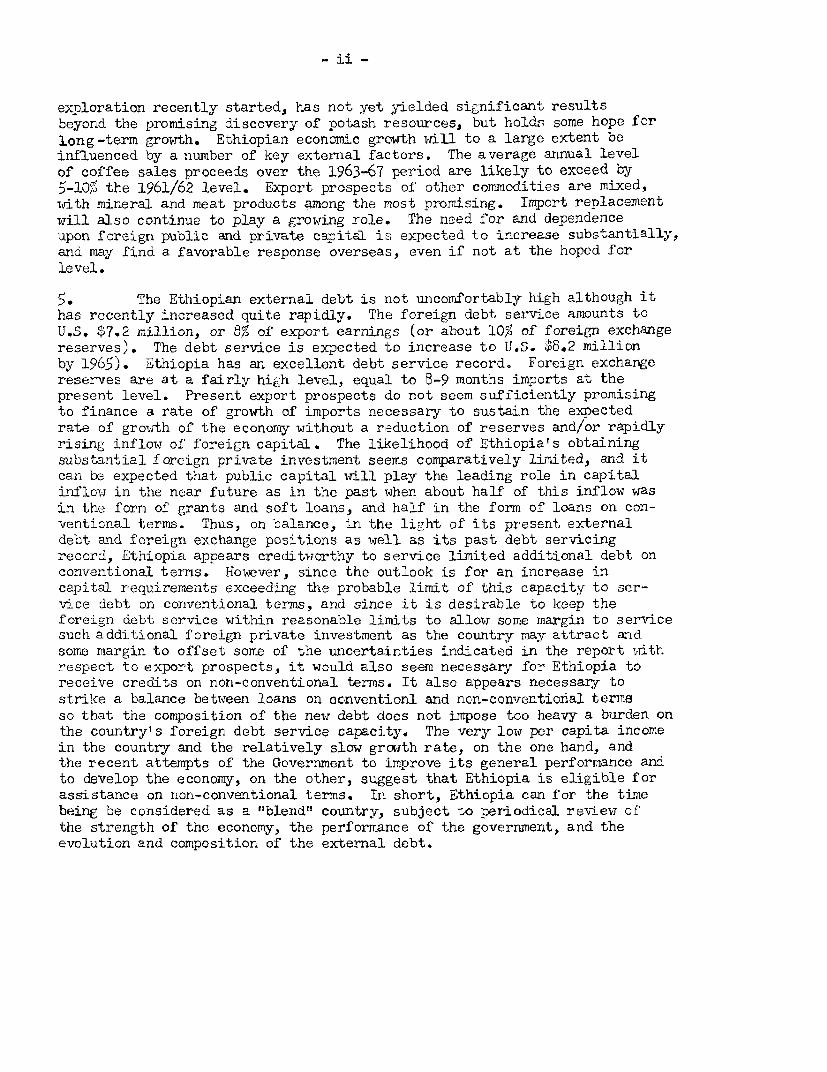

exploration recently started, has not yet yielded significant resultsbeyond the promising discovery of potash resourcesj but holds some hope forlong-term growth. Ethiopian economic growth will to a large extent beinfluenced by a number of key external factors. The average annual levelof coffee sales proceeds over the 1963-67 period are likely to exceed by5-10QZ the 1961/62 level. Export prospects of other commodities are mixed,iwith mineral and meat products among the most promising. Import replacementwill also continue to play a growing role. The need for and dependenceupon foreign public and private capital is, expected to increase substantially,and may find a favorable response overseas, even if not at the hoped forlevel.

5. The Ethiopian external debt is not uncomfortably high although ithas recently increased quite rapidly. The foreign debt service amounts toU.S. $7.2 million, or 8% of export earnings (or about 10% of foreign exchangereserves). The debt service is expected to increase to U.S. $8.2 millionby 1965). Ethiopia has an excellent debt service record0 Foreign exchangereserves are at a fairly high level, equal to 8-9 months imports at thepresent level. Present export prospects do not seem sufficiently promisingto finance a rate of growth of imports necessary to sustain the expectedrate of growth of the economy without a reduction of reserves and/or rapidlyrising inflow of' foreign capital. The likelihood of Ethiopia's obtainingsubstantial foreign private investment seems comparatively limited, and itcan be expected that public capital will play the leading role in capitalinflow in the near future as in the past when about half of this inflow wasin the form of grants and soft loans, and half in the form of loans on con-ventional terms. Thus, on balance, in the light of its present externaldebt and foreign exchange positions as well as its past debt servicingrecord, Ethiopia appears creditworthy to service limited additional debt onconventional terms. Hotever, since the outlook is for an increase incapital requirerments exceeding the probable limit of this capacity to ser-vice debt on conventional terms, and since it is desirable to keep theforeign debt service within reasonable limits to allow some margin to servicesuch additional foreign private investment as the country may attract andsome margin to offset some of the wIcertainties indicated in the report withrespect to export prospects, it would also seem necessary for Ethiopia toreceive credits on non-conventional terms. It also appears necessary tostrike a balance between loans on ocnventionl and ncn-conventicoial termsso that the composition of the new debt does not impose too heavy a burden onthe country's foreign debt service capacity. The very low per capita incomein the country and the relatively slow grc*th rate, on the one hand, andthe recent attempts of the Government to improve its general performance andto develop the economy, on the other, suggest that Ethiopia is eligible forassistance on non-conventional terms. In short, Ethiopia can for the timebeing be considered as a "blend" country, subject to periodical review ofthe strength of the economy, the performance of the government, and theevolution and composition of the external debt.

I. BACKGROUID FOR DEVELOPMfIT

1L. The Empire of Ethiopia occupies the easte;n horn of Africa withS'oialia, and looks across the Red Sea to Saudi Arabia and hden and has forits near neighbors the Sudan and the Northern Frontier District of Kenya.Eor the most part, the principal influences emanating frcm Ethiopia's neigh-bors are Arabic and Moslem. The origin of several of the principal strandsin the Ethiopian population dating back perhaps 2,000 years or more is thoughtto have been in the Arabian peninsula; the official language of the countryAinharic has links with Semitic and Hamitic languages. The principal religionsof the country are also ILddle Eastern in origin. The official religion of-the Established Church of the Empire is a special type of Christianity,based on the doct;rines of Saint Mark, and shares many concepts and practiceswith the small Coptic Church of Egypt. Until recent years there were anunber of organizational and doctrinal links between the two Churches. TheEthiopian Orthodox Church traces its origin back to the fourth century. TheOther major religion in the country is Islam. There are also a number ofanimistic religions of the type found elsewfhere in Africa, practiced bydifferent tribes in various parts of the country. The ruling Solomonicdynasty also traces its origins back to ancient times; in fact it traces itsdescent directly from a union of King Solomon of Jerusalem and the Queen ofSheba of ancient Ethiopia, sometimes referred to as Abyssinia. In light ofthis heritage it has been said "Ethiopia is in Africa, but not of Africa!'.Nevertheless, in recent years Ethiopia has been increasingly active inAfrican affairs and has been taking an increasingly active role in Pan-Africanpolitical affairs (see paragraph 21). Thus in sum Ethiopia today presents aunique synthesis of cultural forces which sharply distinguishes it from anyof its neighbors.

2. In addition to the special cultural synthesis, geographically and

topographically the core of the country is the high plateau which rangesfrom 7,500 feet to 15,000 feet (with the capital Addis Ababa at about 8,500feet) and the low plateau which ranges from 5,000 feet to 7,500 feet. Beyondthese highlands the Ethiopian low lands taper down into the flat desert areasand hot regions of the countries wfhich surround it. The "mountain fortress"which is the heart of Ethiopia has a cool climate, and fertile and reasonablywell-watered lands. The contrast once again between Ethiopia and its neighborsis a sharp one.

3. Historically too Ethiopia stands in contrast with its neighbors.It can trace its origin back 2,000 years or more, during which time, withthe exception of the Italian occupation of 1936-41, it has successfullymaintained its independence. By and large Ethiopia does not have a colonialpast in the sense of most of the African continent. The size, shape andcomposition of the Empire has varied considerably over time; at various timesdifferent local kingdoms coalesced to form the country and only in recenttimes, dating from the reign of i"Jenelik II in the late 19th century (1889-1923),

- 2 -

was the country unified substantially within its present geographical con-figuration (except for Eritrea). In 1952 the formaer Italian colony of

Aitrea was federated by the United 14ations vrth Ethiopia; Ethiopia claimedhistorically that the area, 7with its access to the Red Sea, was part of theEr;pira. Only ten years later, in November 1962, the local legislature ofigcitrea voted to forego its federal status and become constitutionally anintegral part of the unitar3y Ethiopian Empire.

4. Thus, the geography a-nd topography of the country, the uniquecultural heritage, its historical development and its long independence,maintained over the centuries, particularly during the middle and late 19thcentury at a time when the Sudan, Eritrea, Somalia and Kenya all 'becamecolonies, go a ong way towards explaining Ethiopia today, its semi-isolationuntil recently from the outside world, and its recent appearance on the worldscene as a countJry seeking development and inviting the help of exuernalassistance in this task.

5. The constitut.ional development of the country has been slow andalso reflects the special history of the country. The first written consti-tution of the country was prcmulgated in Ju'y 1931 by the Emperor HaileSelassie I on the advent of hi.s accession to the throne. In fact, the briefconstitution of 55 articles for the Jm,Iost part formalized the situation thenextant in the country. Power was totally concentrated in the monarch. Twenty-'ive years later-, in November 1955, the th;peror promulgated the Revised Con-stitution of Ethiopia, lwhich runs to 131 ar-ticles and spells out with moreexactitude tLe distribution of f-unctions and to some extent power, the rightsof the individual and the structure of governnent. Once again, for tae mostpart power is concentrated in the monarch. An attempt is made to spell outwfith more precision the legal succession to the Crown and for the first tiLmeprovision is made for a popularly elected Chamber of Deputies, which shareslimited legislative power with the -Senate, which is appointed by the mperor.

6. The Council of :inisters, headed by a Prime Ministe-, is responsibletlo the Eimperor and not to Parliament. The role of the Council is essentiallyadvisory. Although the concept of joint ministerial responsibility forI"ouncil decisions exists, Practice r4 ouil suggest that irinisters -ake theirlirection from the Emperor and report to him and that the coordinating and:Lttegrating role of the Council is limited. in the last two years there hasbeen an attemLpt to modernize somewhat the government structure through theadoption of a basic civil service statute and the establishment of a centralpersonnel agency. Also under consideration at the present tize is a "projetde loi"l for the organization of a local governmental structure, which, forthe most part, outside of traditional tribal and village institations, onlyexists in rudimentary forrm.

7, There are at t.ie present time 17 mainistries irn addition to the officeof the Prime .intister, 9 or 10 major g,overnment corporations, and, in addition,a variety of boards, bureaux and other special organizations. There is a

- 3 -

considerable duplication of staff in this complex of agencies - e.g., it isnot unusual for a minister or assistant minister to be a member of as manyas 10 or 15 boards of directors of government corporations, boards, bureaux,and other agencies. The tendency towards fragmentation of functions, multiplejobs in the hands of a limited number of individuals, and the nemness andlimited scope of the Civil Service structure all tend to accentuate the lackof cohesion and coordination in the formulation, administration, and executionof government policy, ultimately reflected in the already observed relativelylimited application of tihe principle of collective ministerial responsibility.

3. This absence of coordinated collective ministerial responsibility isreflected not only in the general formulation and administration of governmentpolicy, but also more specifically in the operation of the government'sfinancial system. All too often the national budget is a conglomeration ofindividual ministerial budgets reflecting the exigencies of the moment inone or another field with little if any reference to established general policyor governmental ohjectives. The Second Development Planillustrates this problem in connection with budgeting for the various projectsand programs contemplated in the Plan.

5. In the same way that the central government, where all power in thecountry is concentrated, lacks focus and is weak on coordination so too govern-ment outside of the capital lacks direction and focus. There are now 13provinces plus Eritrea headed by Governor Generals, who are for the most partr-epresentatives of the Emperor, with limited staffs and resources, and wFithlimited capacity for channeling central policy and applying it to the localareas and vice versa for channeling local problems to the attention of thecentral authorities. Beyond the provincial level, the governmental structurebecomes even more tenuous and less certain. There are 6 municipalities in thecountry, headed by mayors appointed by the Zmperor, as well as innumerablehamlets, villages and towms. The latter units have limited contact, directlyor indirectly, writh the central authorities and are essentially governed by-radiiional authorities.

lO Thnus, one of the most serious limitations on the capacity of thegovernment for effective action in all spheres of activity, and particularlyin the sphere of economic development, is the nature of the existing adminis-trative structure and the institutional gaps at the center and between thecenter and the provinces and between the provinces and intermediate and locallevels of government.

11. In addition to the institutional gaps already discussed, there arernany o-ther important ones discussed in various places in the report and onlybriefly mentioned here. In the most important economic sector - agriculture -

there is only a rudimentary extension service, almost a total absence of aneffective agricultural credit system, and no concept of supervised agriculturalcredit, particularly for small and medium-size farmers, a limited agriculturalresearch and experimental system, and the system such as it is is in disputebetween various government authorities, a limited agricultural marketing,ystem, end an almost total lack of an agricultural cooperative system for

- 4 -

marketing or credit or purchasing or buying purposes. In the limitedindustrial sector, on which the new Five-Year Development Plan places somestress, the existing Development Bank of Ethiopia plays a very limited roleindeed. As far as can be ascertained the existing Development Bank apparentlydoes not conceive of itself as a serious source of credit for small or medium-size agricultural enterprises). As a consequence the Five-Year Plan contem-plates the establishment of a new Investment Bank to fulfill these functions.

12. In the economy as a whole, there is a serious lack of savingsinstitutions, and for all practical purposes there is no internal moneymarket. The Government is, however, now experimenting with new issues ofsavings bonds. There is no stock market and the offerings of share com-panies are limrited to a small circle of investors in the capital, many ofthem in one form or another government institutions or government-financedinstitutions.

13. The private sector is limited in scope and in the nurmber of parti-cipants. There are signs, however, of increasing cash-cropping on the partof farmers and some indications that farmers apparently will slift productionof crops in response to prices offered.

14. In addition to the institutional problems already mentioned,there is the major question of land reform, which has been the subject ofconsiderable discussion in the country for some time. There have been twogovernment commissions sitting in the last two years to consider the prob-lem and two FAQ experts have been making a study of the problem at theffovernmentts request. The su-ject is obviously a delicate and complicatedone; it is also extremely difficult to obtain detailed information. Never-theless, it seeas clear that the land-ownership pattern in Ethiopia isprobably -mique for all of Africa. The riajor landowners in the country arethe State itself, the Emperor and the royal family, the Established StateChurch, the clergy, the landed-nobility and in several provinces the moretraditional collective ownership of tribal and sub-tribal organizationsobtains. On much of the land that is not tribally owmed a syJstem of land-lord and tenant relationships exists, involving a type of share-croppingunder which it is reputed that between 25% and 50% of the output goes tothe landlord, varying with the traditional pattern in an area and wJith theservices and supplies pro-vided by the la-ndlord, e.g. seeds and bullocks.In addition certain personal services, on a diminishing scale, apparentlyin some instances are still required to be accorded by tenants to landlords.Tenants are legally free to move, although custom and past prac-tice oftenmilitate against such mobility.

15. :n addition to the landholding system there is the problem of thecollection of land taxes. In addition to the government, the State Churchfrequently has been granted the right to collect land taxes from landlords.For this purpose the Church stands in the role of the government as tax

collector (distinct from its other role as a landlord). In the past too avariety of individuals, frequently soldiers and noblemen who have served theEmpire well, were also granted the right to collect land taxes. This rightof individuals to collect land taxes has been disappearing in recent years.

16. Ever since 1929 there have been a series of decrees and orderspromulgated b; the Emperor in an attempt to clarify, modernize, and to anextent reform the land tenure system and landholding practices. In additionto th1e current studies of the land tenure system itself there are under con-sideration "projets de loi" dealing with landlord-tenant relationships andland tax reform. There is obvious need for a standard land-measurement system.Iarge areas of the country have aoparently never been measured; other areashave been measured with a unit of measurement - a gasha - which is variouslydefined as containing anyrwhere from 40-70 hectares. in addition, many of themeasurements are old and there is little reason to have much confidence intheir accuracy. A new standard measurement used in systematic land surveysand in a program of land registration would not only have the effect of en-larging tax collections and clarifying land-ownership, it would also probablyresult in some redistribution of the land resulting from forfeitures of land-Thich is not now effectively worked or not worked at all. In addition, theabsence of agricultural income from the country's income tax has also becomecl subject of discussion and study.

17. As against the foregoing structural and institutional gaps, Ethiopiastarts with a basically favorable resource endoTAnment. Large parts of thecountry enjoy a temperate climate wJith reasonably good rainfall and reasonablygood soil conditions. There a4so appear to be limited possibilities forirrigation. The range of agriculture possibilities appears extremely broad.The range of agricultural products now successfully cultivated in the countryincludes teff (a local grain much favored by the Ethiopians for producing in-gira, the local equivalent of bread), wheat, barley and other grains, pulses,oil seeds, gardern vegetables, fruit, and the important cash crops, coffee andcattle and other farm animals, with the important by-product of skins and hides.She country is basically self-sufficient in food, and with the operation oftwo sugar-cane plantations by a private Dutch company is now almost self-sufficient in sugar and sugar products. The land/man ratio is oy and largesatisfactory and pressure on the land is still manageable, su(gesting thatorderly landholding and landworking re-organization is still possible.

:18. There has never been a population census in Ethiopia, and estimatesvary from- 15 million to 22 million. The Grovernment for planning purposes hasadopted the number of 21 million. The average annual population increase isthought to be in the neighborhood of 1.5%. A census at an early date plus theestablishment of an appropriate statistical service to record vital statisticsare recognized as important needs for improved planning.

19. In the fields of transportation and communications, discussed indetail in Chapter II and Appendix I , Ethiopia has a long way to go. Bothits economic development and its political, cohesion require opening up andconnecting very large areas of the country with one another and with the

- 6 -

ca-ital, as well as .,ith Ethiopia s outlets to the sea. CorrLrmunications wqithin

2tlbiopia have been developing, particularl-y wi.th the aid of two IJ3D loans.liere too, there is room for further development if the country i-s to be moreclosely Imit together economically and politically.

20. Education, discussed in detail in Chapter II and Apnendci 2, is

another field of major pre-occupation for the Ethiopian Government. Nuch

attention is given to the subject in the Second Development Plan. The hour-glass configuration already emerging in Ethiopia's education, however-, is amnatter of concern. From the point of view of national emphasis there is abulge at the prinmay school level, particularly in the lowest grades, and then

again on a smtaller scale at the university level withn a pinch in the middle,starting at the upper-primary school level, and going through the secondaryschool level, the technical and vocational school level, and the post-,seccndary nor-university technical and vocational level, The prospect of

lthiopia repeating the experience of imany other African countries of producing

large nurbersof partially and fragmentarily educated primary school leavers-aith insufficient education and lack of skills to make an adequate social oreconomic contribution to the society is already apparent. The prospect of

swelling the ranks of displaced young people frcm the rural areas without

sufficient education to make a contribution in the urban centers, and with

just enough education so that their taste for the rural areas as they now

are has been blKunted, is also already discernible. ITuch consideration appears

required wit'h respect to rural educatior. and the role of agricultural and

manual skills training in the curriculunr

21. Turning from the considerations and problems of internal developnnnt

briefly to Ethiopiats emergence on the w,orld scene, the increased activityof Ethiopia in African affairs must be noted. Ethiopia is the site of the

Eacnomic Comm.issicn for Africa and as such has been increasingly draw,xn into

the vortex of Africa-wide economic and political affairs. Ethiopia has been

an active member of tlhe Monrovia Bloc of Aifrican nations. In addition,Ethliopia has been concerned w.ith attempting to reconcile the mo principal

blocs cf African nations - the IM,onrovia and Casablanca Blocs - and as suchhas been active in sponsoring the "'Sumnit Conference", held in Addis Ababalate in May, to which all independent African states wrere invited, other than

the Republic of South Africa and Togo. Ethiopia's relationship with hler near

neighbor, the Somali Republic, has been a strained one involving disputes over

border and grazing rights, primarily in the Haud and Ogaden Region. The claim

of thae Somali Republic to a large part of the Northern Frontier District ofKenya, which has a large population of nomadic Somali cattle raisers, has also

been a subject of contention, with Ethiopia supporting Kenya. Another potential

source of difficulty between the two countries is the Somali Republicts campaignto incorporate Frenchl Somaliland with its important port of Djibouti,, which is

the terminus of the Addis Ababa-Djibouti railway, into a Greater Somali Republic.Ethiopia's relationship with the Sudan appears cordial, w,hereas her relation-

ships w.f;ith Egypt and Saudi Arabia have fluctuated, in some degree as the

relationships of these two countries have with the Somali REepublic. Ethiopia

has also been an active participant in the U.N. operation in the Congo Republic,w-here it 'has provided the largest contingent of African troops in the U.N. force,

- 7 -

approximately 3,000 trcops, as well as at different times a small airforcedetachment of jet planes. Beyond hfrica, Ethiopia h1as boy and large steeredc:lear of all groupings or blocs; however, the Emperor did attend the BelgradeConference of' "non-aligned" states in 1961, at which the African representationc:ame predominantly from the Casablanca Bloc. Ethiopia has centered itsparticipation in extra-African affairs in the U.Ne and its agencies and parti-cipated actively with combat troops in the U.N. force in Korea. She alsojoined with Liberia in raising the question of the status of the League ofNations Mandate over South-West Africa to the then Union of South Africa.idost recently Ethiopia has been engaged in the negotiations of a trade andpay,ments agreement and an econoric assistance agreement with Italy, in whatrnay be an important step towards a rapprochement betwJeen the two countries.Finally, it should be noted that Ethiopia has sought and received foreign aid,economic and military, from a variety of sources, but primarily from theUnited States, and more recently from the Soviet Union, Technical assistanceand 'oreign personnel have been sought and obtained from many European,ountries, partic:ularly from Scandinavian countries, and more recently teachersfrom India and the United States. In fact, as part of its historical develop-ment, Ethiopia has sought to balance the influence of foreign advisers and-technicians by diversifying its sources. On the one hand this prevented any

one foreign country from becoming dominant in any crefield; on the other itcontributed to the lack of focus or coherence already alluded to in overallgovernment policy and action. Over the years down to the present Ethiopiahas hired and pa:id fror from its o-in resources a nuumber of foreign advisersand technicians; others are provided now as grant aid.

22. All' of the foregoing considerations and problems, many of w^.Thichhave been throwJn up by the process of transition from a traditional, non-market, isolated society to a mnore mcdern, market, world-connected society,wshich Ethiopia has emnbarked upon, are the background for and the context in

which the Ethiopian economy will evolve.

-

II. GROWTH ALT' STRUCTURE OF TEE ECON0ILi

A. National Accounts Data

23. The Ethiopian economy is based upon agriculture primarily of asubsistence type. lianufacturing is still of less iaportance than the handi-craft and cottage industry. Most of the services are underdeveloped. Thenon-agricultural activity is directly or indirectly dominated by governmentinterests. The folloiring table sets out the composition of production andthe purposes to which this production is allocated. (It should be notedhere and in subsequent usage in Section A that the figures used are officialPlan figur-es. They are be½nz used as the best available, witLoutr any intent-3 icn o' LnfJino that they are an accurate iTrasure, ant in order to facilitate

e consideration of the Plar-t

Balance of Resources 1962

E$ Million

Su>l3ly 'JUse

Production in:

Agriculture, forestry, Private consumption 1,824fisheries 1,478 Government consumption 162

Manufacturing, landicraft, Gross fixed capital formation:building ar;.a construction 157 private 95

TranEport arid corrunication 1C9 government and public enter-Trarle and co:mterce 136 prises 78otLer, including public Cianges in stocks (net) 6adm.inistration 250 Exports of goods and services

(net) 199.ross Domestic ProDduct 2,2 30saports of Goods 234

Total supply 2,364 Total use 2,364

Note: Figures are in 1961 prices.

Source: Imperial Ethiopian Government. Second Five-Year Plan, draft andrevised estimat s , April 1963.

24. The Gross Yatioral Product amounted to Z?2,143 million in 1962 (in1961 prices) or the equivalent of U.S.$80O million. Based on a populationestimate of 21 million inhabitants per capita production averaged U.S.MO.(TI-ds is the per capit-a estimate that is accepted by the Ethiopian authori-ties.) Th.is average includes, of course, a range stretching from the highincomes of a relatively few landlords to the subsistence incomes of the largebulk of farmers and the nomads out in the provinces. There are, however, fewvery rich people in Ethiopia. The urban population which amounts to, say,

only 5% of the total population has on the average higher but not considerablyhigher incomes th<an the farmuers. Thie standard of living is low in Ethiopia,even compared with that of many other African countries. The average value ofper capita private consumption should, according to the official estimates, beabout U.S. t33. In spote of this nutritional stu-dies seem tc agree that ,he

- 9 -

population, generally speaking, obtains a reasonable calorin intake per headper day and that food stringencies occur only in connection with temporary orregional crop failures. Deficiencies in diet due to lack of other vital in-gredients in food than calories is, however, still a problem, and improvementof the diet balance remains an urgent development need. Housing standardsremain low, despite considerable emphasis on housing in the first Five-YearPlan. Clothing standards have recently improved, as can be seen from the in-crease in purchase of cotton goods, but are still relatively low. Availablepublic health and education services are also very limited.

25. Public consumption is estimated to be E$162 million or 8% of GNP.The definition of public consumPtion is, however, not clear. It is not cer-tain that non-central government activities are included, i.e., those oflocal and regional public authorities. Public investment is computed to havebeen E$78 million in 1962, which included an unspecified but probably smallamount in public enterprises. Total public investment and consumption thusamounted to E$240 million or 11% of GNP.

26. Gross fixed capital formation amounted to E$180 million or about8% of GNP, in 1962, of which half resulted from private investment and halffrom investment by public enterprise and Government. A breakdown of invest-ment in production sectors shows that during the period 1957-1962, 34% oftotal gross fixed investment went into transport and communication, 25% intohousing, 9' into services, etc., and 32% into the productive sectors ofagriculture, mining, power, and manufacturing. The emphasis was thus oninfrastructure during the first Five-Year Plan. This pattern of investmenthas primarily laid the basis for more directly productive investments in thefuture (cf. Section J). 80,b of the investment is said to have been financedby domestic saving and by investment in kind by the rural population, while20% of the financing has been attributed to foreign resources.

27. The growth of the economy in the past is not very well known but of-ficial estimates put the growth rate for the period 1957-62 at 3.4%, and alsooffer as a guess a growth rate of 2 - 2-1/2% for earlier periods. Growth inindividual sectors has been rather uneven. Agricultural production has beenincreasing at a rate below 2% a year, which explains the overall low rate oftotal growth. All other sectors taken together (accounting for only 1/3 oftotal output) have grown well above 7% per year; manufacturing, buildingand construction, public services, and administration have been most expansive,while trade, commerce, and other private services have been growing at lessthan 7% per year. Gross investment for the period 1957-62 shows an increaseof 13% a year, or from E$96 million in 1957 to E$180 million in 1962. This rapidgrowth which was fairly well shared by all major sectors of the economybrought the investment ratio (gross investment as a ratio of GNP) up from5.4, in 1957 to 8.3% in 1962.

28. Development during the past years has been sufficient to raiseper capita income by 1%X to 2% rer year, on the assumption that the populationgrowth rate has been less than 2% ner annum reflects the true situation in thecountry. This per capita increase is not unreasonably low, however, takinginto account that Ethiopia still is in an early stage of development and that

- 10 -

relatively large amounts of investments have been and are being directed toinfrastructure, without a high immediate return. The rate of growth of in-vestment has been satisfactory, due in large part to foreign aid. However,the agricultural sector, which is the principal sector of the economy, hasnot received enough attention in the past, and the growth rate in that sectorhas been disturbingly low. As the problem of raising the grow-ith rate inagriculture is a long-term one, it seems likely that the lack of developmentin the agricultural sector in the past will impose a serious limitation onthe possibilities of raising the growth rate of the economy markedly overthe next five years.

B. Production and Employment by Sectors

Ahriculture

29. Ethiopia has a great range of climates and soils, ranging from thehot and unfertile plains alongside the Red Sea and in the Danakil Depressionto the plains in eastern Ethiopia used primarily for grazing, to the fertileand cultivated savannah in the northern highlands and the intensively culti-vated former woodlands in the high central plateau. The level of rainfallis as varied as the topography of the country. The most cultivated areasseem to enjoy some rainfall all year round, although the country by and largeis dependent for most of its rainfall on the "long-rains" during the monthsof April to September. There are a number of rivers, but only a few carrywater all year round. Special areas such as the Rift Valley are well endowedwith a series of natural lakes. Some irrigation work has been done inEritrea and in the Awash Valley, and further irrigation possibilities in theAhwash Valley are now being studied by a Special Fund team.

30. Agriculture is the largest sector of the economy. It is estimatedthat it contributes 70%0 of the Gross National Product, and that more than90% of the population is directly dependent upon it. Agricultural productsaccount for almost 100% of exports. A large proportion of the agriculturalsector is devoted to subsistence-type production. iM1ost of the land is farmedby peasants in units rarely exceeding 3 hectares. Some of the land is ownedby the individual farmers but the bulk of the cultivated land is operated ona share-cropping basis. A very small fraction'of the cultivated land isfarmed commercially in large units, sometimes by private companies or indi-viduals given concession by the Government, sometimes by experimental statefarms.

31. Land use in Ethiopia:

TvDe of Land Millions of hectares Percentage of total area

Agricultural land cropped 9.5 8.1Coffee forests 0.5 0.4Grazing grounds 33.0 28.0Closed forests 4.0 3.4Open woodland 3.4 2.9Open brush and scrub 22.5 25.0Deserts 37.0 31.0Lakes and rivers 1.1 1.0

Total 118.0 100.0

Source: FAO, Agriculture in Ethiopia, Rome 1961, p.136.

- 11 -

The total area of Ethiopia, including Eritrea, is thus estimated to be about118 million hectares. The area actually under cultivation is between 10 and15 million hectares. Some 50-60 million hectares can be classified as pasture,while only 4 million hectares are forests. The land/man ratio in Ethiopia hasbeen satisfactory and excent for some small pockets of over-population, thedensity in fertile areas is seldom much higher than 25 per square kilometer.This partly explains why such a large area is used for grazing, and whyEthiopian farmers have been able to maintain one of the largest livestockpopulations in Africa.

32. The development of agriculture has been hampered by institutionalfactors as well as by traditional habits and attitudes of the peasantcultivators. As noted in Chapter I (paragraphs l-16 ), the land tenuresystem is among the most important institutional factors inhibiting develop-ment as the system provides little, if any, incentive to the tenant farmer toincrease his production. Any investment made by the tenant farmer belongs tohis landlord, and out of any increment in gross production due to his efforts25-50Cflo must go to the landlord, notwithstanding the fact that the farmer mayhave spent his own funds to induce this increment, for instance, the purchaseof fertilizers. The relationships betweeni the landlord and the tenant arequite often undefined without legal basis, which adds to the insecurity ofthe tenant.

33. The Government has recognized the importance of the land tenureproblem in the second Five-Year Development Plan and has also noted some ofthe more important institutional gaps in the new development plan. However,only in the marketing system have definite organizational steps been taken.The recently established Grain CorDoration is to provide storage facilitieson a substantial scale. The Corporation is expected to be able to offerbetter and more stable prices to producers for their products than they nowreceive from merchants and middlemen, to induce an improvement in the qualityof the produce, and to be able to sell the produce to the consumer cheaperthan the merchants do at present. The Government believes that the Corpora-tion could have a decisive influence on the market without handling more thana part of all grain offered for sale. In order to facilitate marketingcooperatives are now being officially encouraged. The cooperative movement,however, is limited both in number of products handled and areas served, butwith proper guidance and support, may become a useful instrument to facilitatethe modernization of the agricultural sector. A planned National LivestockBoard is to deal with the problems of meat, hides and skin production.Government support of production includes direct assistance to producersthrough agricultural extension workers, veterinary services, etc. Theseservices are now being strengthened somewhat by the improvement and enlarge-ment of existing agricultural schools and veterinary laboratories, partlywith foreign assistance.

34. The development of the agricultural sector has on the whole beenneglected in the past. Expenditures in the budget on agricultural developmenthave never exceeded 5% of total expenditures and more often varied between 1%and 2%. Even more important has been the traditional resistance towardsreforms of an institutional character. There are recent signs, however, of

- 12 -

a modest change in attitude both on the side of the Government, which hasrecognized some of the more glaring problems and has given some preliminaryconsideration to them, and on the side of the local farmers who have shownsome willingness to improve their conditions through community cooperation,taking the form of campaigns for money to build bridges, feeder roads, andschools. W4hether this change in spirit will carry far enough to remove themajor obstacles to agricultural development in an orderly way depends mainlyon whether Government translates its preliminary consideration into concreteactions and the response Government gives to the local initiatives of farmersthrough community development and agricultural extension programs.

35. In terms of volume it is estimated that grains are the most impor-tant crop in Ethiopia. They cover over 80% of the area sowm and are the mainfoodstuff. The actual production figures are not known and estimates varywidely, which is partly explained by the fact that only a part of the crop isactually traded on a market. Total cereal production is thus estimated byFAO and other external sources to be 2.5 - 3.0 million tons while theMinistry of Agriculture in its sectorial plan gives an estimate of 4.9 mil-lion. The estimates for individual crops vary still more. The productionseems by and large to meet the needs of the population. The need for foodimports occurs only intermittently as a result of a temporary or regionalcrop failure. In the past, some grains were exported, but there are nolonger any exportable surpluses. The type and quality of the produce appar-ently does not make the cereals suitable for exports. Teff, an indigenousgrain, accounts for about half of all cereal production and is the basic food

of the farmers. The Government's policy now seems to be, however, to dis-courage the cultivation of teff as a low yielding and high labor-consumingcrop under existing technical conditions, and to substitute the productionof other higher-yielding crops suitable for growing in the different regions.Other major cereal crops are sorghum, barley, corn and wheat. Wheat which is

now the smallest of the crops, with some 150-260 thousand tons produced, is

thought to be the most promising of the grains for expansion of production.

36. Pulses are the second most important food crop, consisting of chick-peas, peas, broad beans, haricot beans and lentils. All of these are grownfor local consumption as well as for exports - export value hovering aroundE$20 million during the past three years, or 10% of total exports. The ex-port value doubled between 1954/5 and 1961/2 although the volume remainedabout the same. Most of present exports are going to Ceylon with smalleramounts going to European countries. Exports are expected to grow. Anotherimportant crop is oilseeds; some 250-350 thousand tons are produced annually.About 20% of the crop is exported, the value varying between E$15 and 20 mil-lion, or about 10% of total exports. This crop is also thought to have apotential for growth in exports. The world market, however, does not looktoo promising for increased exports.

37. A number of other crops are grown commercially. Among the mostimportant is sugar cane, which since 1951 has been produced by a Dutch firmat the Wonji Sugar estates. Production has increased rapidly and shouldcover domestic requirements by the end of 1963. (Import value amounted toabout E$6-7 million before production started.) Cotton is produced on a

- 13 -

small scale almost everywhere in Ethiopia. A few plantations dependent uponirrigation produce cotton for the domestic market, but do not cover more than

part of the domestic demand. Imports now amount to about E$8-9 million a

year or about 5,000 tons. Plans to extend cotton plantations are quite ad-

vanced, and it is expected that Ethiopian domestic production will in a

relatively short time catch up with the increasing demand. Another fibre

producing crop is sisal. which although long produced, has only recently been

adopted as a plantation crop. Contemplated investment and production plans

exceed the expected domestic needs, with a view to entering the presently

favorable world market for sisal. Tobacco production is small but almost

covers the demand of the Ethiopian Tobacco Monopoly; only a small amount

is imported for blending. Recently there was a small export of tobacco to

Eastern Europe. There is a large export of Chat, valued at E$11 million,

to Aden. (Chat is a leaf with certain "narcotic-type" qualities.)

38. Coffee is the most important export commodity of the country.Coffee is a plantation crop, and also grows wild. The actual production isestimated to be between 70 and 140 thousand tons. The higher estimate assu-mes that about 50% of the production is consumed domestically. It seemslikely that the actual production figure lies somewhere between these two

estimates. Coffee exports show the following development:

GC 1954 1955 1956 1957 1958 1959 1960 1961 1962

Exports in thousandsof tons 31.6 42.1 31.5 50.7 39.9 45.2 51.3 56.o 62.5

Exports in E$ million 99.5 90.2 80.1 123.0 84.1 74.6 94.4 93.9 107.2Wholesale price index

for export of coffee 156 104 131 115 100 78 83 84 76

During the last year exports have continued to increase in volume while prices

have continued to decline. The rapid increase in coffee exports starting in

1959/60 is the result of several factors. During the boom years of the mid-1950s when prices for coffee were high large areas were planted which haveonly come into production during the last few years. Further, larger areas

of wild coffee appear to have been harvested in recent years, due to improvedmarketing possibilities and communications, e.g., newly built roads that have

opened up new areas. Finally, some credit for part of the rise in exports

may be due to the National Coffee Board, created in 1957. Its mtain duty is

to give full effect to existing laws and regulations on the cleaning and

grading of coffee for export. It is also charged with suggesting new ways

and means to improve the standard of Ethiopian coffee. Its creation appears

to have led to some improvement in standards and reduction in overseas refu-

sals of coffee shipments. It also may have made Ethiopian coffee prices

somewhat firmer on the international market. However, the Ethiopian Jimna

coffee wias quoted at 31.754 per lb. in July 1963, about 2/ below the compar-

able Brazilian coffee type.

39. The potential for growing coffee in Ethiopia at a low cost is said

to be high and production could increase at a high rate given the right kind

of support and stimulus, in the form of transport and marketing facilities,

- 14 -

agricultural credits, etc. Under the International Coffee Agreement whichcame into force in 1963, Ethiopia has been allocated a basic export quotaof 61,000 tons. The basic quota is approximately the export quota for the1963/64 production year. Thereafter the basic quotas for all countriesare to be adjusted in line with world consumption trends. Ethiopian exportsexceeded 60,000 tons in 1961/62 and the amount available for export isrising. Ethiopia has signed the Agreement and is likely to ratify it beforethe end of 1963. 1/ It would be difficult to envisage Ethiopia remainingout of the Agreement over a long period of time once it becomes fullyoperative, given the present world outlook for coffee sales and prices. Onbalance the average annual level of Ethiopian coffee sales proceeds duringthe 1963-67 period are likely to be 5-10% higher than the 1961/62 level,taking into accoumt a possible small growth in world consumption, the pos-sibility of upgrading of quality, and the general outlook for coffee prices.

40. Ethiopia has an abundance of livestock. The economic benefits ofthis potential wealth have so far been small; up until now domestic andforeign markets for cattle and cattle proclucts have been limited. The totallivestock population was estimated by FAO in 1958 to have the followingcomposition (in millions):

Cattle 24Horses 1Donkeys 4Mules 1Sheep 23Goats 8Camels 1

Total 62

Recent estimates by the Ministry of Agriculture are even slightly higher.The number of goats may actually be considerably underestimated in the tableabove. The total production from these resources has by various sources beene stimated to be E$250-600 million in 1962 or between 10% and 25% of GNP. Themajor part of this value has been accounted for by meat and milk production

for local consumption. The major export products are hides and skins, the

export value of which has varied between E$15 and 30 million.

1/ Ethiopia was initially given a quota of 51,000 tons. Ethiopia claimedthat the production figures used in the computation underlying her quotawere not accurate and it was decided at the August 1963 meeting of theInternational Coffee Organization that a revision was to be made, subjectto a study in the fall 1963. Ethiopia has notified the U.N. of her in-tention to ratify the Agreement given a revised quota of 1,020,000 bags(61,000 tons) in the 1963/6h production year. Under the terms of theAgreement such a notification is sufficient for participation in theAgreement through December 31, 1963.

- 15 -

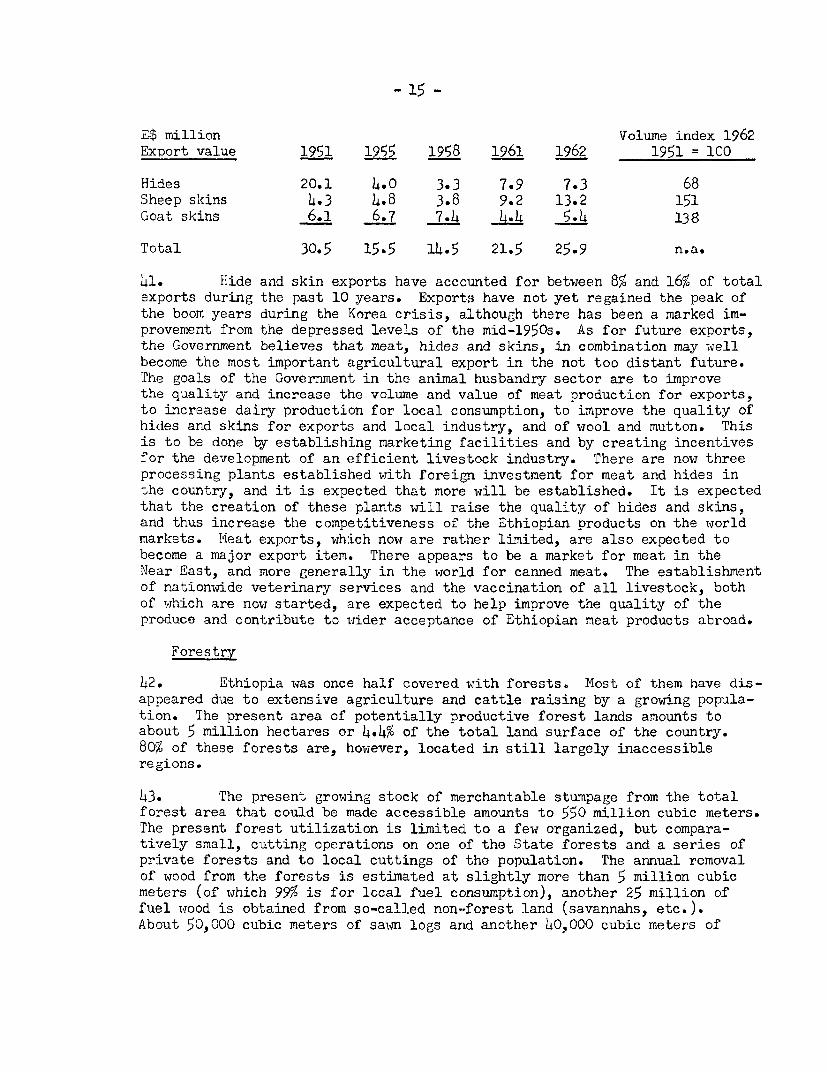

E$ million Volume index 1962ExDort value 1951 1955 1958 1961 1962 1951 = 100

Hides 20.1 4.0 3-3 7.9 7.3 68Sheep skins 4.3 4.8 3.8 9.2 13.2 151Goat skins 6.1 6.7 7. 4. 5. 138

Total 30.5 15.5 14.5 21.5 25.9 n.a.

41. Hide and skin exports have accounted for between 8% and 16% of totalexports during the past 10 years. Exports have not yet regained the peak of

the boom years during the Korea crisis, although there has been a marked im-proverrient from the depressed levels of the mid-1950s. As for future exports,the Government believes that meat, hides and skins, in combination may well

become the most important agricultural export in the not too distant future.The goals of the Government in the animal husbandry sector are to improvethe quality and increase the volume and value of meat production for exports,to increase dairy production for local consumption, to improve the quality ofhides and skins for exports and local industry, and of wool and mutton. Thisis to be done by establishing marketing facilities and by creating incentivesfor the development of an efficient livestock industry. There are now threeprocessing plants established with foreign investment for meat and hides inthe country, and it is expected that more will be established. It is expectedthat the creation of these plants will raise the quality of hides and skins,and thus increase the competitiveness of the Ethiopian products on the worldmarkets. I',eat exports, which now are rather limited, are also expected to

become a major export item. There appears to be a market for meat in theNear East, and more generally in the world for canned meat. The establishment

of nationwide veterinary services and the vaccination of all livestock, bothof which are now started, are expected to help improve the quality of theproduce and contribute to wider acceptance of Ethiopian meat products abroad.

Forestry

42. Ethiopia was once half covered with forests. Most of them have dis-

appeared due to extensive agriculture and cattle raising by a growing popula-tion. The present area of potentially productive forest lands amounts toabout 5 million hectares or 4.4% of the total land surface of the country.80% of these forests are, however, located in still largely inaccessibleregions.

43. The present growing stock of merchantable stumpage from the totalforest area that could be made accessible amounts to 550 million cubic meters.

The present forest utilization is limited to a few organized, but compara-tively small, cutting operations on one of the State forests and a series ofprivate forests and to local cuttings of the population. The annual removalof wood from the forests is estimated at slightly more than 5 million cubicmeters (of which 99% is for local fuel consumption), another 25 million of

fuel wood is obtained from so-called non-forest land (savannahs, etc.).About 50,000 cubic meters of sawn logs and another 40,000 cubic meters of

- 16 -

building poles and industrial wood are produced annually. The eucalyptusplantations, which are of a rather recent origin, supply material for build-ings, fences, and fuel; bamboo is also an important building material incertain districts. There are some imports of timber and wood products, andsome exports of lumber and scented wood.

44. The improved utilization of the forests is expected to be a long-term undertaking. It is believed that the forests have to be transformed toinclude more homogeneous and productive species, a process which at its bestwould change 20% of the area over the next 50 years. Production from virginforests might, however, be stepped up more quickly, and provide a small ex-port supply. Official reforestation policy has recently become explicit,requiring permits for cuttings, providing seedlings from Government forestnurseries for reforestations, and coordinating forest policy with water andsoil conservation policy. As most of the policy measures have only beenadopted recently, the most that can be expected in the near future is thata brakc will be put on the rapid destruction of the Ethiopian forests; andthat over the long run improved forests utilization will be possible.

Fisheries

45. Ethiopia has a coast line of about 760 kilometers at the Red Sea.The sea fishing industry, with a total catch of 209000 - 30,000 tons a year,is based on traditional methods. Most of the fish is caught from shore orclose in to shore; relatively little is known about the prospects formodern fishing units further offshore. It is estimated that 3,000 - 4,000fishermen are employed in fishing during the season. Some development inthis industry appears to be taking place, and some offshore fishing is nowbeing organized. Only a small proportion of the fish is consumed fresh;the major part is dried and ground into fishmeal and is exported. Otherprojects in this general area are contemplated. The shell-fishing industry,which has provided the raw material for buttons etc. has a limited and de-creasing importance, due partly to increased competition from other materials,such as plastics.

Mining

46. In the non-agricultural field there has been very limited develop-ment in Ethiopia, either for the domestic market or for export. The mostpromising potential mineral export now appears to be verified major depositsof potash in the Danakil Depression in northeastern Ethiopia, where anAmerican company expects to come into production in 1964 with an annualproduction starting at 300,000 tons and increasing rapidly to 500,000 tons.The Mobil Oil Company of the U.S. has recently signed an oil exploration andproduction contract for coastal and offshore areas along the northern halfof the Eritrean coast on the Red Sea. A German company has been prospectingfor oil for some time in the Ogaden region of southeastern Ethiopia borderingon Somalia. There are also known to be small deposits of gold and platinumwhich are being worked on a limited scale. For the rest spotty and sporadicexploration activity is going on in the country, some by the government Min-istry of Mines, some under government contract with private companies, and

- 17 -

some under concession to private enterprises. Prospecting is at present beingconcentrated on gold, alluvial platinum, and iron ore.

47. The Government is also at the present time investing in new goldmining equipment in order to raise production. The Government has since 1958been training its own prospectors and has now a staff of 50-60 prospectors.The prospects for finding iron ore of high quality are thought by the Govern-ment to be good. The iron and steel industry, which is included in theSecond Five-Year Development Plan on the basis of an anticipated supply ofdomestic iron ore is, however, premature.

Industry and Handicraft

48. The manufacturing industry in Ethiopia is still of very limited im-portance. The gross value of its production amounted to E$116 million in196 2 and the net value added E$35 million or 1.6% of GNP. Total employ-ment in manufacturing industry was estimated at about 28,000. Ownership andmanagement seem to a large extent to be in the hands of foreigners orEthiopian nationals of foreign descent. The Government has, however, sub-stantial interests in some manufacturing industries, as cement, textile, etc.

49. The handicraft and cottage industry is of more importance than themanufacturing industry. The dividing line is, however, at time somewhatobscure. The net value added was twice as large as that of the manufacturingindustry or E$77 million (gross output E$88 million), and employment wasclose to 200,000. Handicrafts and cottage industry have supplied many needsof the domestic market, in particular certain textile products, footwear,agricultural tools, utensils and other such articles. Building handicraftsand service handicraft have also recently gained some importance.

50. The largest manufacturing industry is the food industry (excludingcoffee and grain cleaning). It accounts for about Lo of total output andemployment. Sugar production (including sugar cane plantations) accounts forabout two-thirds of the food industry. Sugar production capacity was raisedmarkedly by the completion of a second sugar mill in 1962. The small meatpacking and processing industry appears, as already noted, to have the great-est potential for growth. Exports to Israel have recently started, andarrangements for exports to Europe are being negotiated. The potential ofthis industry lies in the availability of livestock, the quality of whichneeds improvement, particularly with regard to health standards, in order tosatisfy export requirements. It has been estimated that given a market, theexport value could be increased over the long run from the present E$2-4 mil-lion to as much as E$80-100 million per year. The Development Plan calls fora sevenfold increase in production. A number of other food industries produ-cing for the domestic market as well as for the export market have been crea-ted recently, as dairies, "tej" factories (tej is a type of beer made fromhoney), tomato canning plants, etc. The official policy is to increase theproportion of processed food products in exports and the Government is nowpromoting the production of coffee powder, edible oils, etc. The importanceallocated to food industry exports in the Development Plan is illustrated bythe fact that 40% of the increase in total exports and 80% of the increase in

- 18 -

manufactured exports during 1962-67 is expected to come from this industry.This requires a sixfold increase in food industry exports from E$10 to E$60million. The actual increase will probably be limited by the marketingprospects for the individual products, and might result in some of the con-templated projects being delayed or shelved.

51. Host other industries produce mainly for the local market. Thetextile industry accounts for roughly one third of outpuit and employment inthe manufacturing industries. The emphasis has been on the extension ofcotton mills during the past five years and the capacity has been and isbeing considerably increased. Investment in textile mills accounts for 50gof all investments made in manufacturing industry during the first Five-YearPlan. As a result, production rose 170%9 between 1957 and 1962. Imports of

finished textiles continue, however, to be the largest import item, and therehave been tendencies of oversupply of certain items. Domestic production hasbeen limited to the cheaper qualities, previously imported from India. Localdemand seems, however, to be rising for better Japanese qualities not yet pro-duced in Ethiopia. Present large domestic consumption of finished textilesmay, given the Government's policy of selective limited protection and asuitable production pattern, allow the industry to expand further. Invest-ments are, however, expected to diminish slightly, and production to growmore slowly than in the past five years. The cotton industry is to a growingextent expected to obtain raw cotton from local plantations now being devel-oped. Raw cotton imports presently amount to E$9 million. The import sub-stitution of textiles and raw fibres (cotton, sisal, wool) may in the longrun have a considerable impact on the balance of payments position.

52. The remaining manufacturing industries are all small (gross outputbelow E$5 million). A number of new industries, however, have been startedor are in the planning stage. The largest of these projects is a petroleumrefinery, now being constructed at the port of Assab, at a cost of E$35 mil-lion, financed mainly by a Russian credit. The refinery is to have aninitial capacity of 500,000 tons. At present, domestic consumption is around20% of that figure; the rest is expected to be sold for ship bunkering. Theprospects for this are not very clear. A small foundry and steel rollingplant with a capacity of up to 18,000 tons has recently been completed closeto Addis Ababa. Local scrap iron is used as raw material. One new cementfactory is under construction in Addis Ababa with a capacity of 70,000 tons(which can be compared with present production of 40,000 tons and imports ofaround 20,000 tons). Other cement factories are under study to be locatedat Bahr Dahr and I'Ilassawa; the latter being expected to produce mainly forexport. Amon; other developments in the manufacturing sector are the plannedconstruction of a canvas and rubbershoe factory, and present negotiations fora paper factory and the enlargement of the wood processing industries.

53. The Development Plan envisages the creation of a chemical industryincluding a paper pulp factory connected with caustic soda, carbon bisulphideand phosphoric acid plants. Pharmaceuticals, plastics, paint and fertilizerplants are also being studied. These projects are still generally in apreliminary stucly stage with the economic justification of many still beingstudied. The financing of such projects as are thought economic is still one

- 19 -

step farther away. Private foreign investment is being sought, and Govern-

rment itself appears to desire significant participation. It is not clearhow many of the projects could be undertaken before 1967. Actual construc-tion activity is likely to lead to an increase in industrial productionduring the next few years. The impact on the economy, however, is likely tobe rather limited from the point of view of employment (an increase at bestof 30,000 employees) and output (at the very best, a trebling of manufactu-ring output, equal to a 3% increase in GNP). But the export production fromthe food industries and the import substitution from the other industriesshould over the long run contribute substantially to an improvement in the

balance of payments situation. However, the investments planned for 1963-

67 in the manufacturing industries will require an amount of imports of

machinery and equipment much larger than the production increase the new

industry will be able to offer for export or import substitution during the

same period.

Buildinil and Construction

54. The building and construction industry is responsible for about 30to 40% of total investments. It had a gross output of approximately E$100million in 1962, of which about 60%o was in infrastructure construction, 30%in housing, and -L0% in industrial and related construction. Another E$15

million of housing were built by farmers for their own use. The production

of the building industry doubled between 1957 and 1962.

55. The Ministry of Public borks is responsible for a large part of

the activity in this sector. Foreign contractors have long played an im-

portant role, especially in the building of more complicated civil enginee-

ring works like the new jet airports,the port of Assab, etc., and in urban

housing. Increasing investments will require a growing capacity in the

building and construction industry. The Government is inclined to try to

"Ethiopianize" the industry by encouraging the establishment of Ethiopian

construction firms. Since 1955, there has been an "Ethio-Swedish" buildingcollege. Initially it supplied building graduates supposed to be suitableto become individual entrepreneurs in the building industry. Now, training

at the institute is primarily directed at producing qualified building

foremen. A material testing and a low-cost housing research department arealso attached to the college.

C. Investment Poliev

56. The Ethiopian Government has decided to promote private investment,foreign and domestic, to carry out the second Five-Year Plan. The Governmentitself undertook major part of all investments during the first five-year

plan (1957-62), primarily in infrastructure. Directly productive investmentsin agriculture, forestry, mining, and industry have in the past been made by

the Government, governmental agencies, and a limited number of foreign com-panies: domestic private entrepreneurs have played a very small role. TheGovernment investment in the productive sector is listed in Appendix 4.There has recently been a shift in emphasis as to what investments are to

- 20 -

have priority, and directly productive investments are now to get more atten-tion than heretofore. The general principle announced by the Emperor in 1961is that of partnership between foreign and domestic interests, private andpublic.

',7. The various means by which the Government wants to promote private-nvestments apply both to domestic and foreign private investors with only afew exceptions. The Ethiopian income tax which varies from 16 per cent to36 per cent allows a lower scale of increase for companies with a paid-upcapital of E$5 million or more. There is a five-year "tax holiday" withrespect to investment in newi industrial, transport, and mining enterprisesmeeting certain specified conditions. Investors can also make furtherspecial agreements with the Ministries concerned regarding certain otherpossible tax advantages.

58. Imports of industrial and agricultural machinery, implements,appliances or parts thereof are exempt from the payment of customs duty,tax or tariff, health and education tax, personal and business tax, ormunicipal tax of any description. Generally the Government policy is toencourage enterprises to use domestic raw materials and goods as far aspracticable, but if adequate justifications exist the Government is nothesitant to forego this requirement in favor of importation of raw materialsand goods required by domestic enterprises. Payments for imports require ex-change licenses which are liberally granted. Export proceeds must be surren-dered.

59. Investors are not promised protection from imports before they have

established themselves. Once in production an investor can apply to a specialinterministerial committee whose function is to protect and encourage domesticenterprises. The committee takes care to assure that there will be competi-tion among local producers even after the protection has been introduced. In

case an industry with a single dominating producer where a price monopolywould be the consequence of protection, there have been special agreements onthe price policy to be followed (as in the case of sugar during a limitedtime of protection) or taxation has been introduced designed to prevent theproducer from benefiting unduly from price increases.

60. Foreign investors usually get permission to remit abroad annuallya fixed percentage of the profit earned, according to the amount of capitalinvested, to enable them to distribute dividends to shareholders and forpayment of other agreed expenses. Foreign residents are permitted to re-patriate their capital gradually. Special agreements are often signedspecifying the percentage of capital or profits which will be allowed tobe remitted abroad.

61. Recently an Investment Guarantee Agreement has been signed withthe United States to assure U.S. private investment against non-businessrisks, such as expropriation and inconvertibility.

- 21 -

62. There are also a number of requirements relating to private invest-ment, which may affect the level of such investment. Foreigners may not ownLand except with the special approval of the Emperor. Thus most of theforeign-run plantations are based on long-term leases. There are a number ofactivities which are dominated by State enterprises, such as banking, airtransport, and tobacco processing and distribution. A new banking law whichis in the offing is expected to allow some increased private banking activityin the future. As indicated, the Government favors participation of domesticcapital in any foreign investment made in Ethiopia. There is, however, nofixed rule about this. In the absence of private local investors, the Govern-inent has shown a desire to participate in industrial undertakings financed byforeigners, which may have the effect of diverting public resources from otherdevelopment projects. The Ministry of Commerce and Industry which issues"industrial licenses" has some power to regulate and supervise the establish-ment of industrial enterprises.

63. There is an official "Ethiopianization policy" which still has more`the form of a recommendation than a regulation. The Government regards theemployment of Ethiopian technicians and trained personnel as important, andacceleration of such employment as urgent. However, where Ethiopians of therequisite qualifications are not available, the employment of non-Ethiopiansof the required technical skill and experience "will be favorably considered"in order to accelerate the economic development of the country and to attractforeign capital.

5S. The attitude toward foreign private investment is somewhat ambivalentin practice. On the one hand there is a campaign to attract foreign capital,with the inducements already noted, while on the other hand there is thetendency of the Government to want to participate directly in investments inthe productive sector, sometimes in a proportion exceeding that of the privateinvestor. However, the major problem of potential foreign investors, who havefound an economically viable project, is the administrative difficulty of ob-taining decisions and receiving permissions from the various Government agen-cies responsible for different aspects of foreign investment. The SecondFive-Year Plan has recognized this problem and has stipulated that coordina-tion shall take place within the Ministry of Commerce and Industry by an"Industrial Promotion Service". The Plan also provides for a number of newinstitutions, such as a new Technical Agency to perform feasibility studies,and an Investment Bank, and for a variety of new economic legislation.

D. Transport and UtilitieslJ

655. In recent years, considerable attention has been given to the impro-vement and expansion of the transportation and communicating facilities.Several road building programs have been undertaken wTith the assistance ofIBRD, IDA, and U.S. credits. The third highway credit, recently extended byIDA, along with existing road building activity should absorb Ethiopia'senergies for the present with respect to main highway construction. Much,however, remnains to be done, particularly with respect to feeder roads ifmonetization of the economy is to continue, if new agricultural areas are tobe brought into production for the market, and if local government is to be

7 See also Appendix 1.

- 22 -

effectively developed and related to central government. There are severalrailroad projects in various states of discussion, which require carefulconsideration before any of them are committed, with particular attention totheir potential role in an integrated transportation grid and with referenceto the alternatives of road and rail transportation in the context of overalleconomic development of the country. In this same connection the variousport facilities directly available to Ethiopia in H'Iassawa and Assab and in-directly available in Djibouti, should be taken into account. All indicationsat present are that there is substantial underutilized capacity at the portof Assab and ilassawa.

66. The Bank loans have also been used to rehabilitate and to expandthe telecommunications facilities during the past ten years, and according tothe present and projected demand, it seems likely that further expansion ofthe existing facilities will be required in the future. Appendix I deals withtransportation and communications facilities in detail.67. The gross production of electric power (including Eritrea), amountedto over 145 million kwh in 1962. Based on an estimated population of 15 - 21million, the per capita production of power is one of the lowest in the world.There are three main producers of power: Ethiopian Electric Light and PowerAuthority (EELPA), an autonomous public entity headquartered in Addis:Societa Electrical dell'Africa Orientale (SEDAO), also a public companyserving the province of Eritrea, and various industrial firms (mostly private).

68. The following table shows the growth of power production from 1957to 1962 and the production targets set for the second plan, from 1963 to 1967;it also indicates the relative importance of the three producers:

Production of Electric Enerzv(in million kwh)