Embed Size (px)

Citation preview

Docnut of

T he World Bank

FORK OWKI1AL USE ONLY

* ~~~~~~~~~~~~~~~~~~~~Repot N. 7073-IND

STAFF APPRAISAL REPORT

INDONESIA

ACCOUNTANCY DEVELOPMENT PROJECT

April 8, 1988

Country Department VAsia Regional Office

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

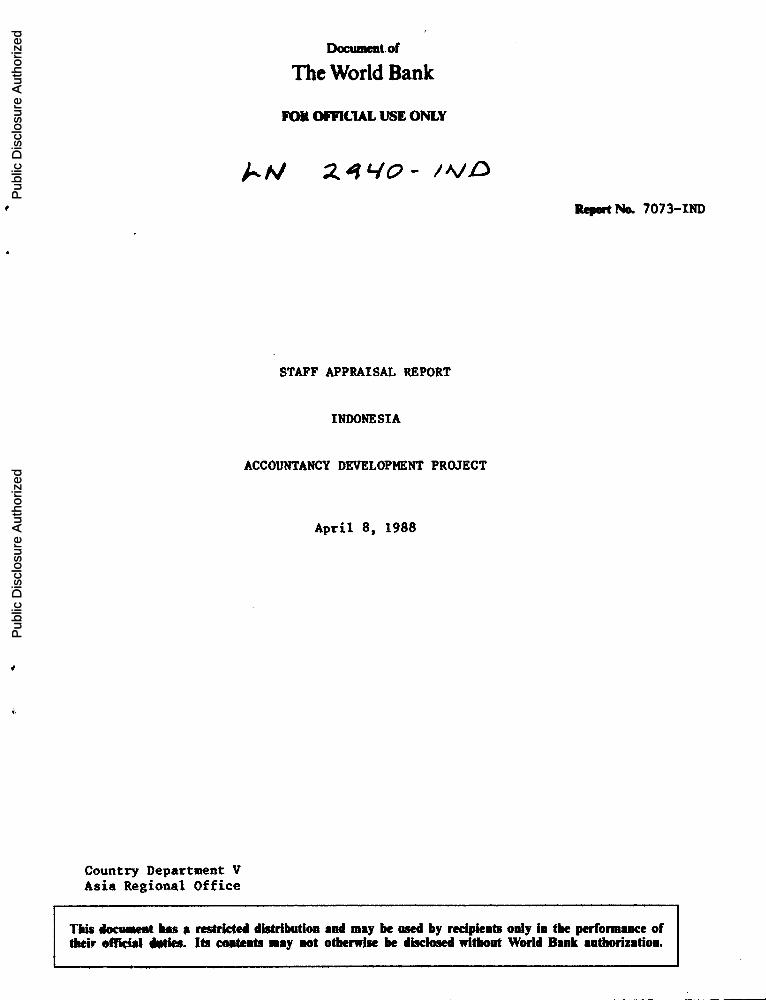

CURRENCY EQUIVALENTS(as-of February 1988)

Currency Unit - Indonesian Rupiah (Rp)US$1.00 - Rp 1,650Rp 1 million US$606

FISCAL YEAR

April 1 - March 31

ACADEMIC YEAR

July 1 - June 30

PRINCIPAL ABBREVIATIONS AND ACRONYMS USED

ADC - Accountancy Development CenterBAPEPAM - Capital Market Executive AgencyBAPPENAS - National Development Planning AgencyBPK - Supreme Audit BoardBPKP - Financial and Development Supervisory BoardCAAD - Coordinating Agency for Accountancy JevelopmentCAPA - Confederation of Asian and Pacific AccountantsDGHE - MOEC Directorate General of Higher EducationDIKHAS - MOEC Directorate of Community EducationIAI - Indonesian Institute of AccountantsICB - International Competitive BiddingIFAC - International Federation of AccountantsKKN - Regional State Cash OfficeKPN - Regional State Treasury OfficeMOEC - Ministry of Education and CultureMOF - Ministry of FinancePAN - Annual Budget Realization ReportPIU - Project Implementation UnitPKG - Pemantapan Kerja Guru (In-service and on-service teacher

training program)REPELITA - National Five-Year Development Plan (Repelita IV, 1984-89)SGV - Sycip, Gorres, Velayo & Co (Consulting Company)SMA - Upper Secondary General SchoolsSMEA - Upper Secondary Commercial SchoolsSOE - Statement of ExpenditureSTAN - Sekolah Tingi Akuntansi Negara (State School of Government

Accounting)UGM - University of Gadjah MadaUI - University of IndonesiaUSU - University of North Sumatra

FOR OFFICIAL USE ONLIINDONESIA

ACCOUNTANCY DEVELOPMENT PROJECT

Table of Contents

Page No.

LOAN AND PROJECT SUMMARY ................... ......... *... iii

I. ACCOUNTANCY DEVELOPMENT: ISSUES AND STRATEGY .................. 1

Introduction o.o.o..*9. .................................. 1

Issues* ... ... .................................. 2

Government Accounting and Auditing .......................... 2

Private-Sector Accounting and Auditing...................... 5

Capital Market. ..................................... 6

Accountancy Manpower Supply and Demand........................ 7

Accountancy Education and Training Programs.... .............. 8

Accountancy Development Strategy ..... 11

Government Strategy............................ *. ..........*. 11

Bank Strategy,,*.oo*o...................................... 13

II. THE PROJECT ...........9 . ...... 15

Project Objectives ........... 9999s999e......................... 15

Project Decito ....................................15

Accounting Practice....9999999999 *............. 16

Accounting Edcto ....................................21

Project Management, Monitoring and Evaluation.................. 25

III. PROJECT IMPLEMENTATION .................... 27

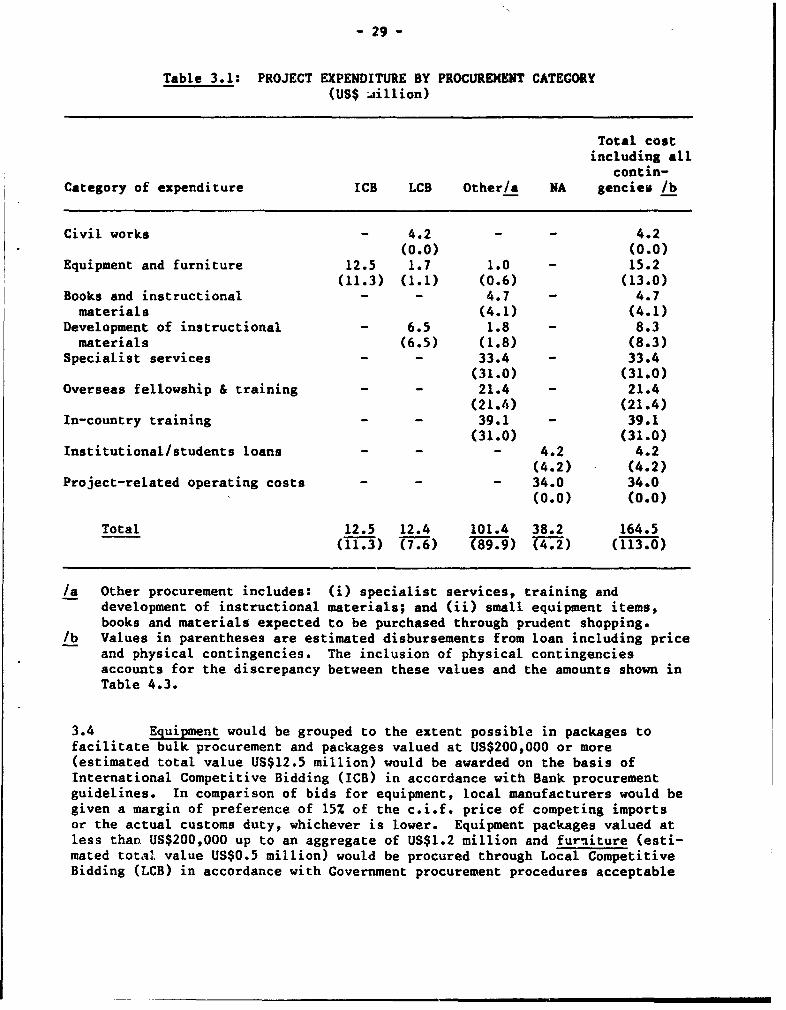

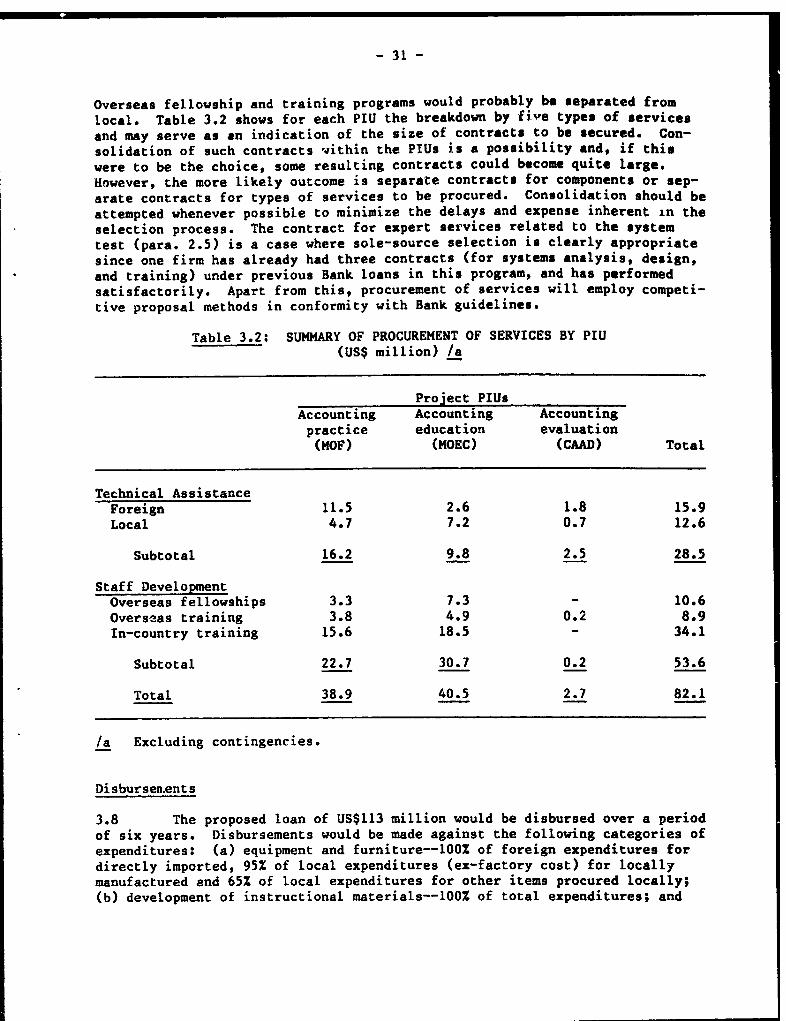

Implementation ............ - ~~~27Procurement .............................................. 99........9 28

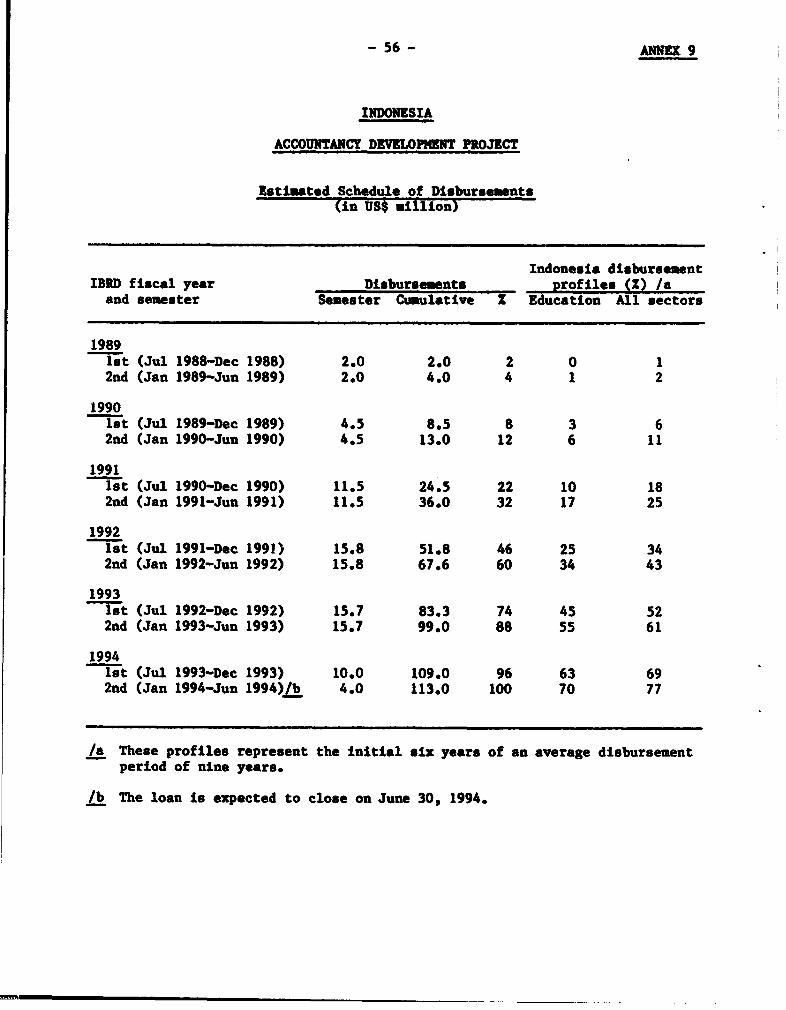

Disbursements ...... ................................. 31

Project Accounts, Audits and Reporting........................ 32

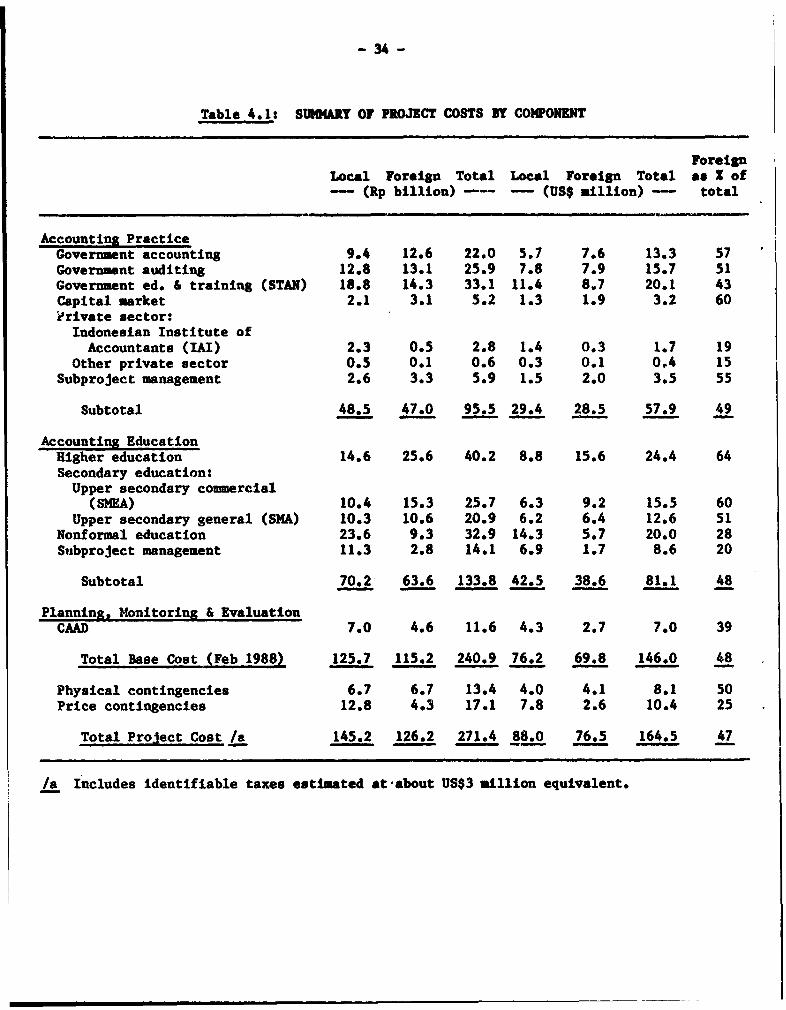

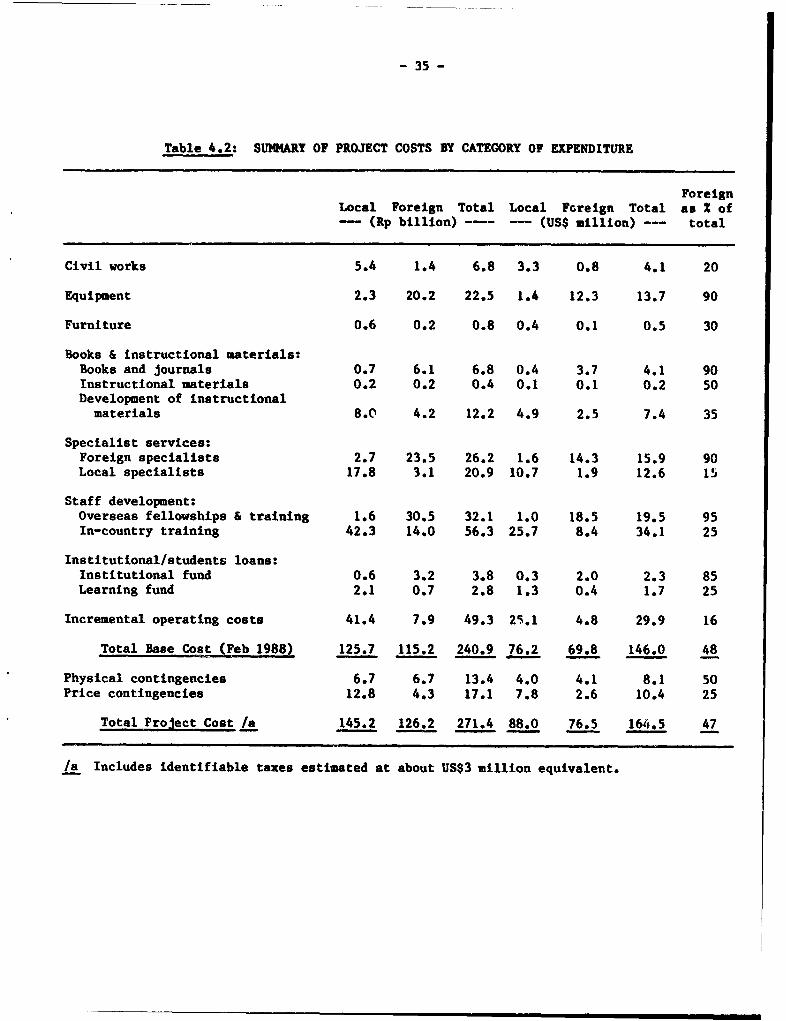

IV. PROJECT COSTS AND FINANCING ................ 33

Cost Estimates ... ................................. 33

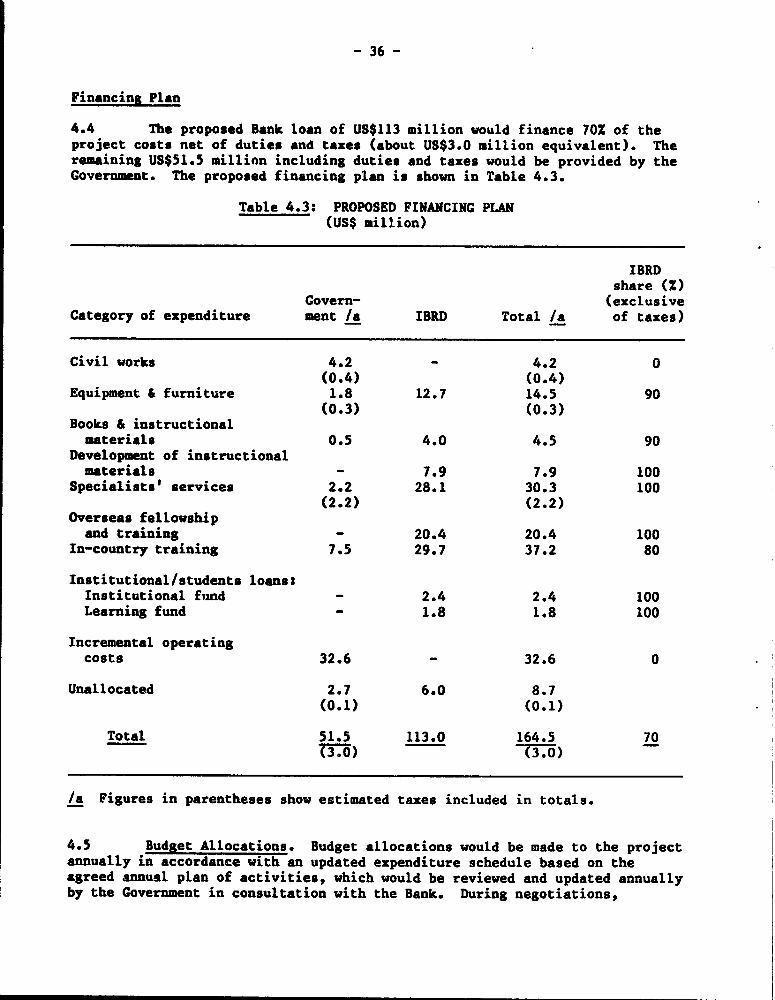

Financing Plan ....... 3....................................... 36

V.BNFTS, IS................................... 37

VI. AGREEMENTS REACHED AND RECOMMENDATION.....o ..............o.o.. 37

This report is based on the findings of an appraisal mission to Indonesia in

October 1987. Mission members included F. Farner (mission leader), M.

Mertaugh (economist), K. Thomas (financial analyst), C. Escudero (lawyer),

M. Masuda (operations assistant) and R. Osterlund (consultant).

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

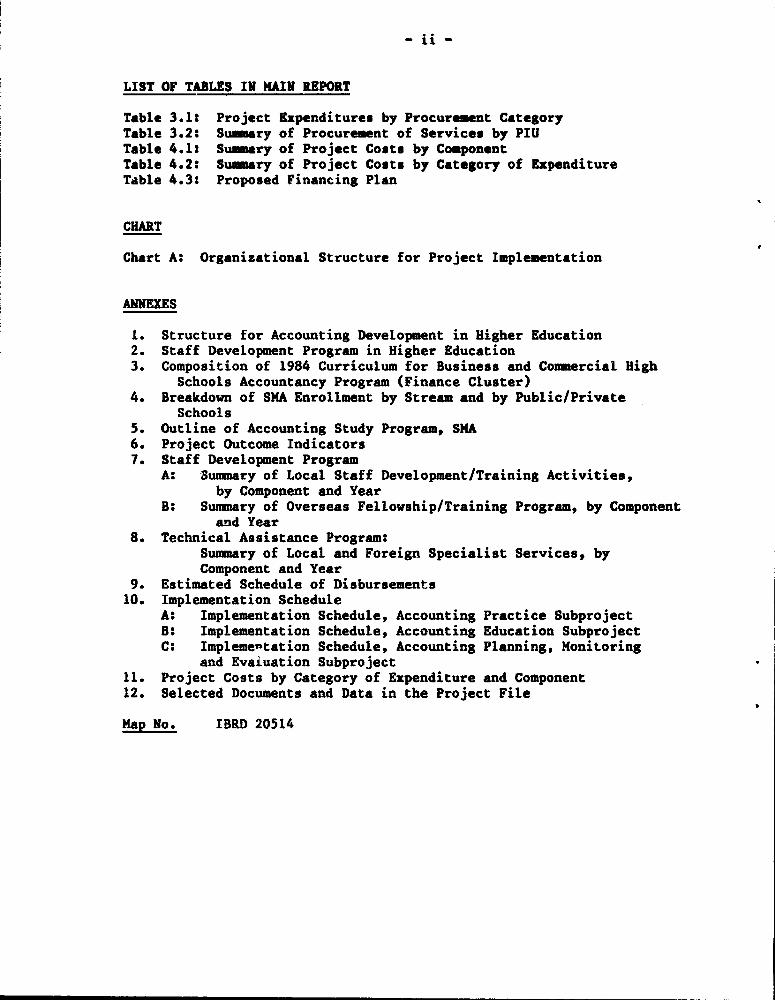

LIST OF TABLES IN MAIN REPORT

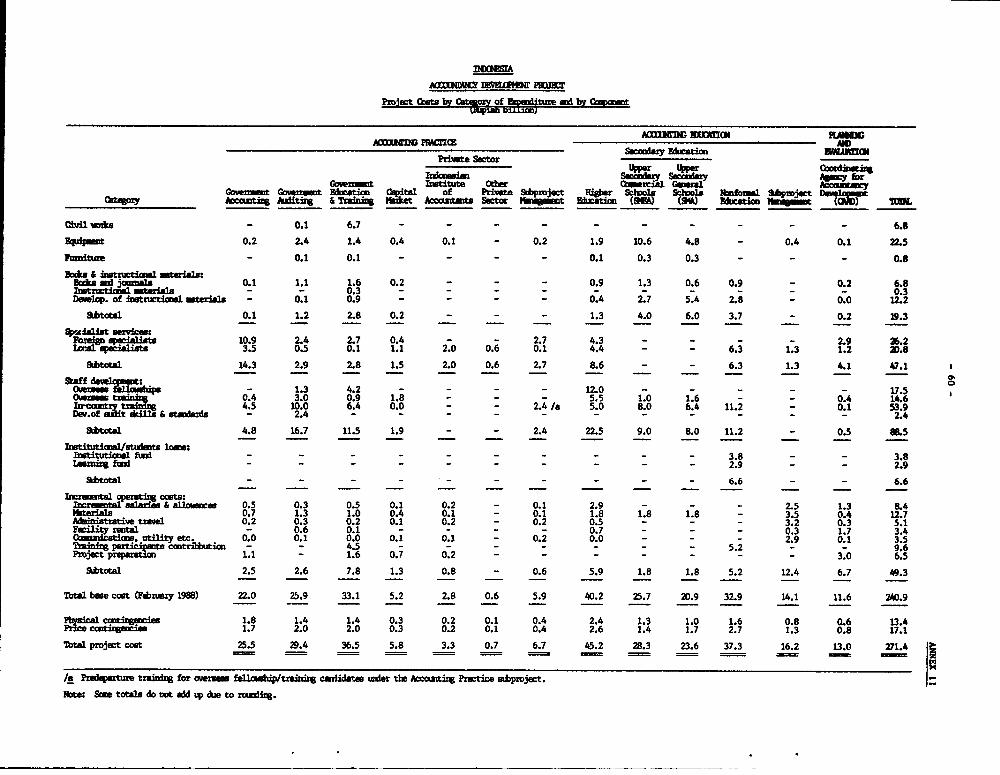

Table 3.1: Project Expenditures by Procurement CategoryTable 3.2: Sumary of Procurement of Services by PIUTable 4.1: Summary of Project Costs by ComponentTable 4.2: Summary of Project Costs by Category of ExpenditureTable 4.3: Proposed Financing Plan

CHART

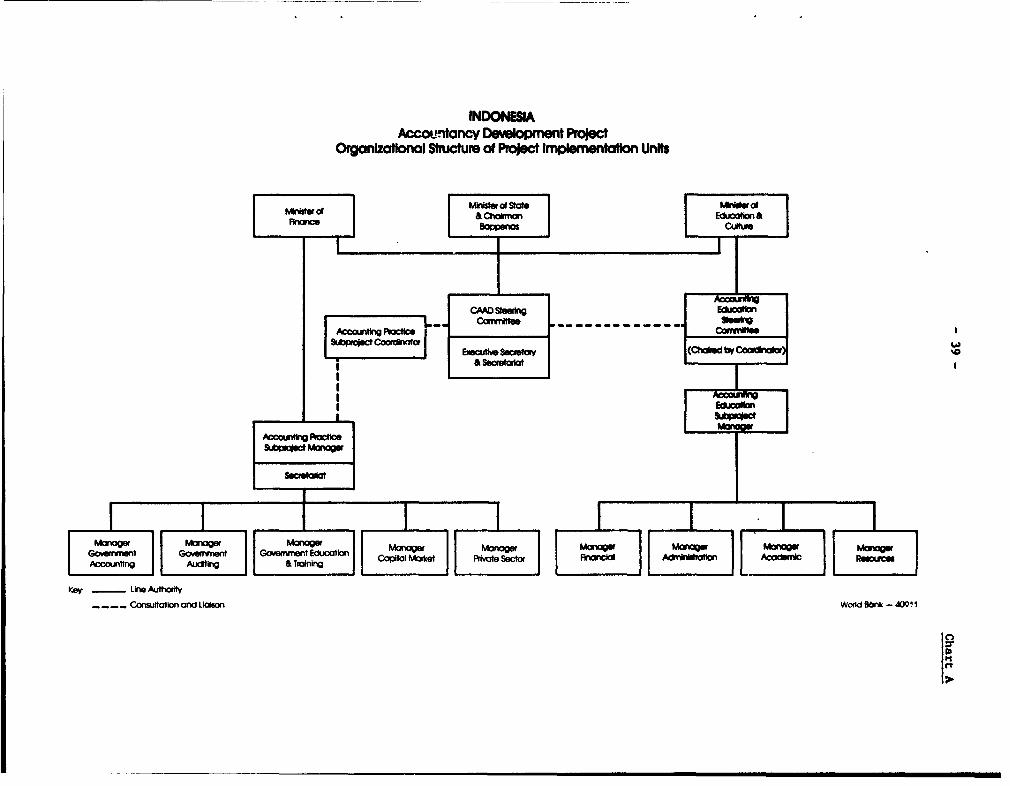

Chart A: Organizational Structure for Project Implementation

ANNEXES

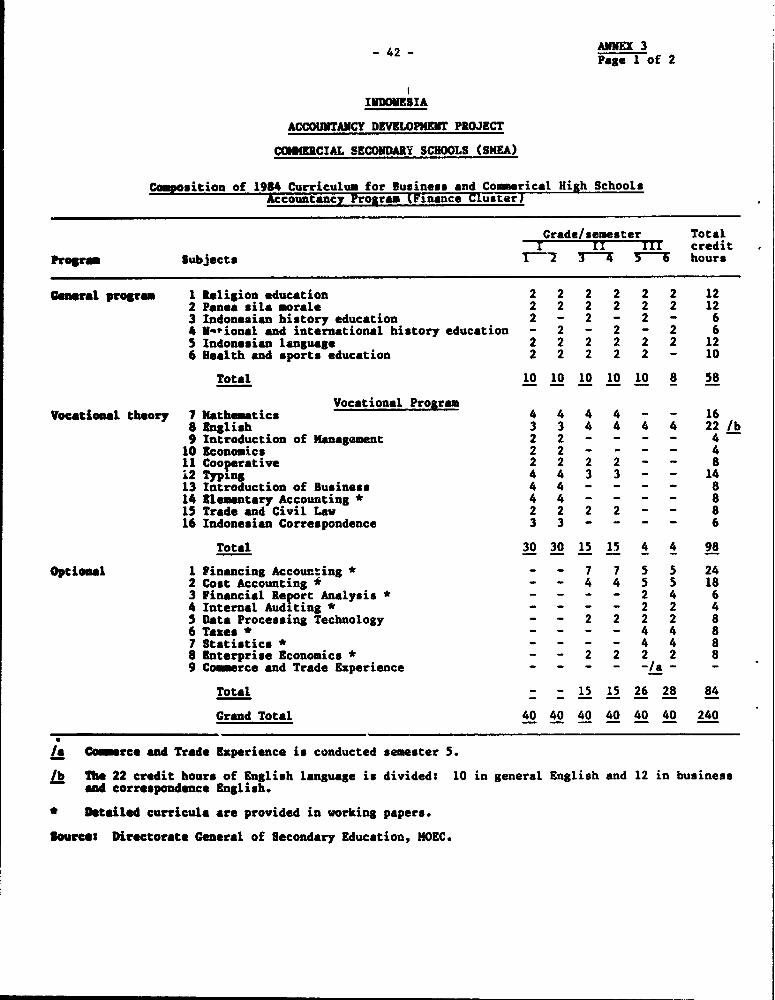

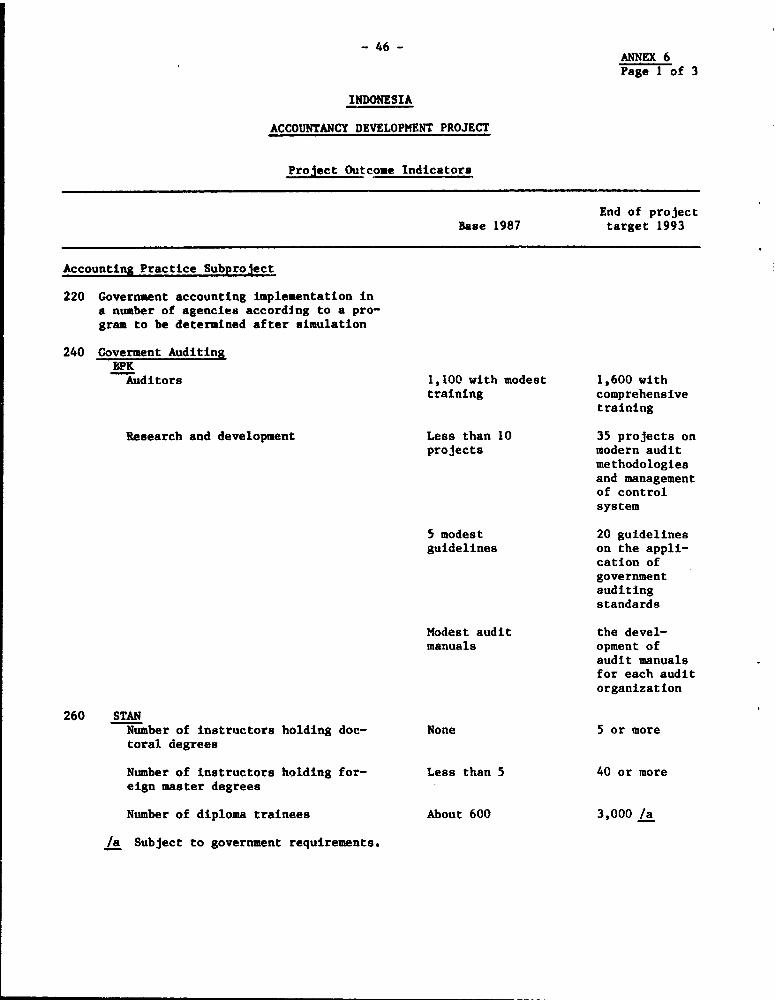

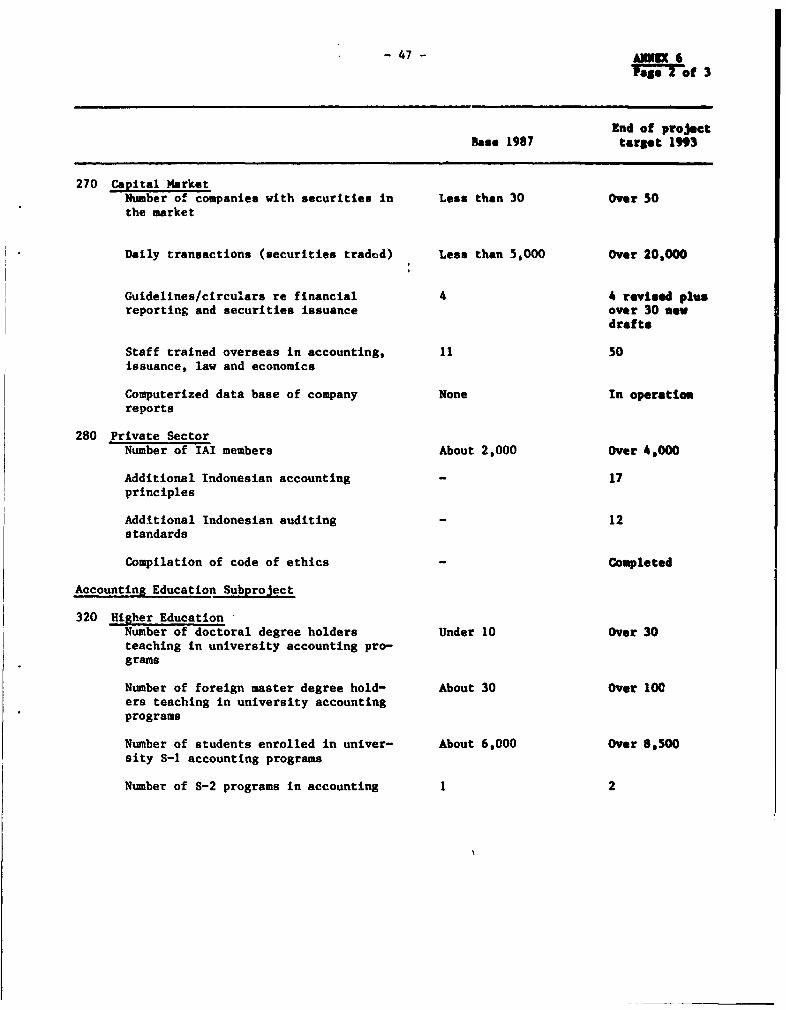

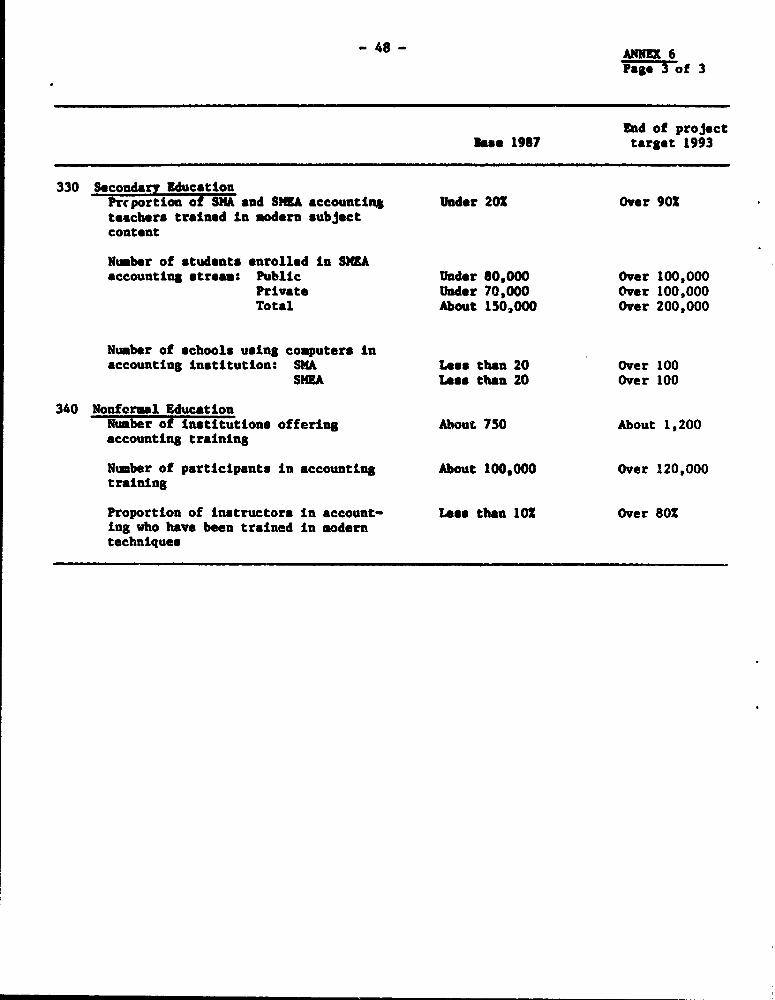

1. Structure for Accounting Development in Higher Education2. Staff Development Program in Higher Education3. Composition of 1984 Curriculum for Business and Commercial High

Schools Accountancy Program (Finance Cluster)4. Breakdown of SMA Enrollment by Stream and by Public/Private

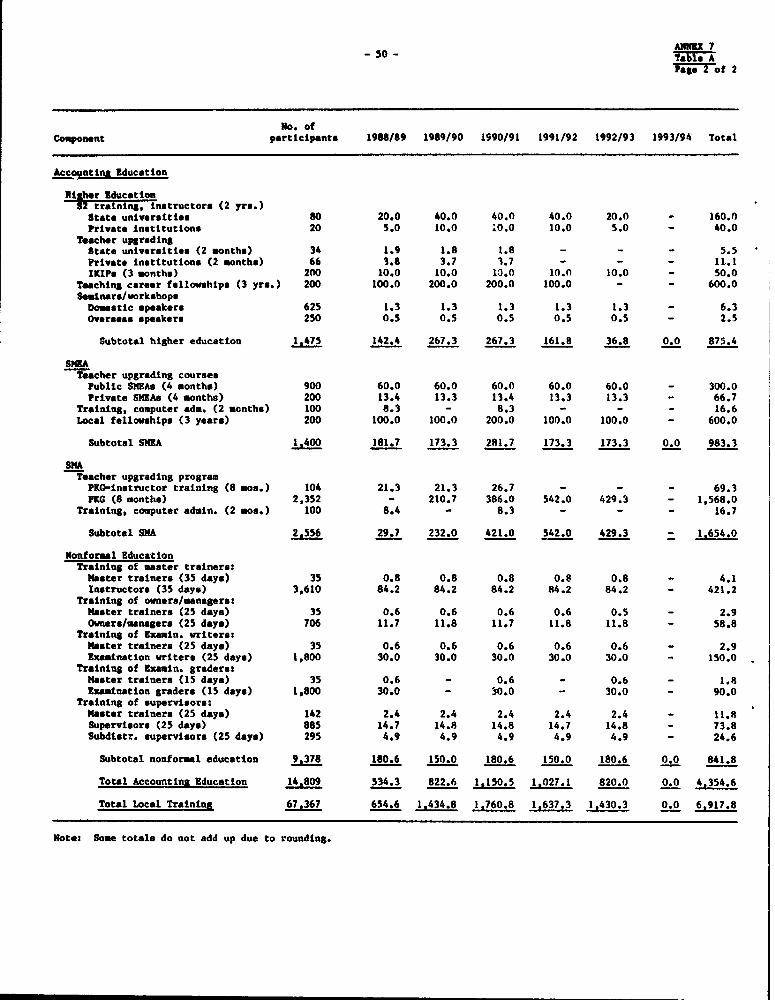

Schools5. Outline of Accounting Study Program, SMA6. Project Outcome Indicators7. Staff Development Program

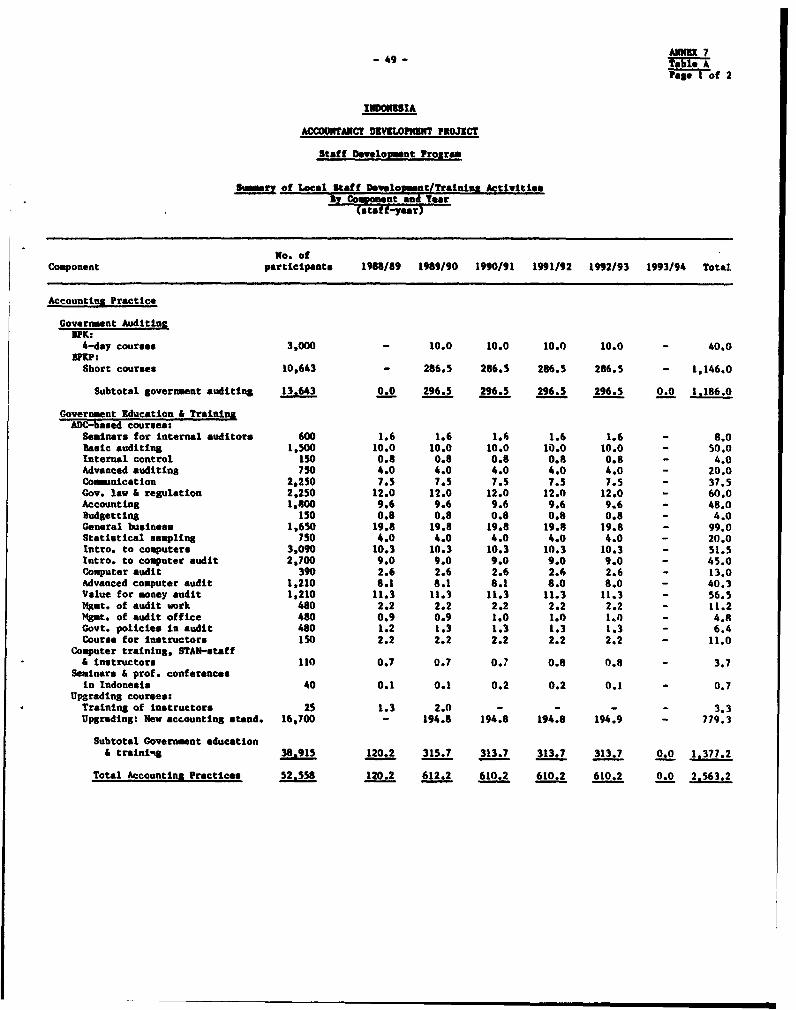

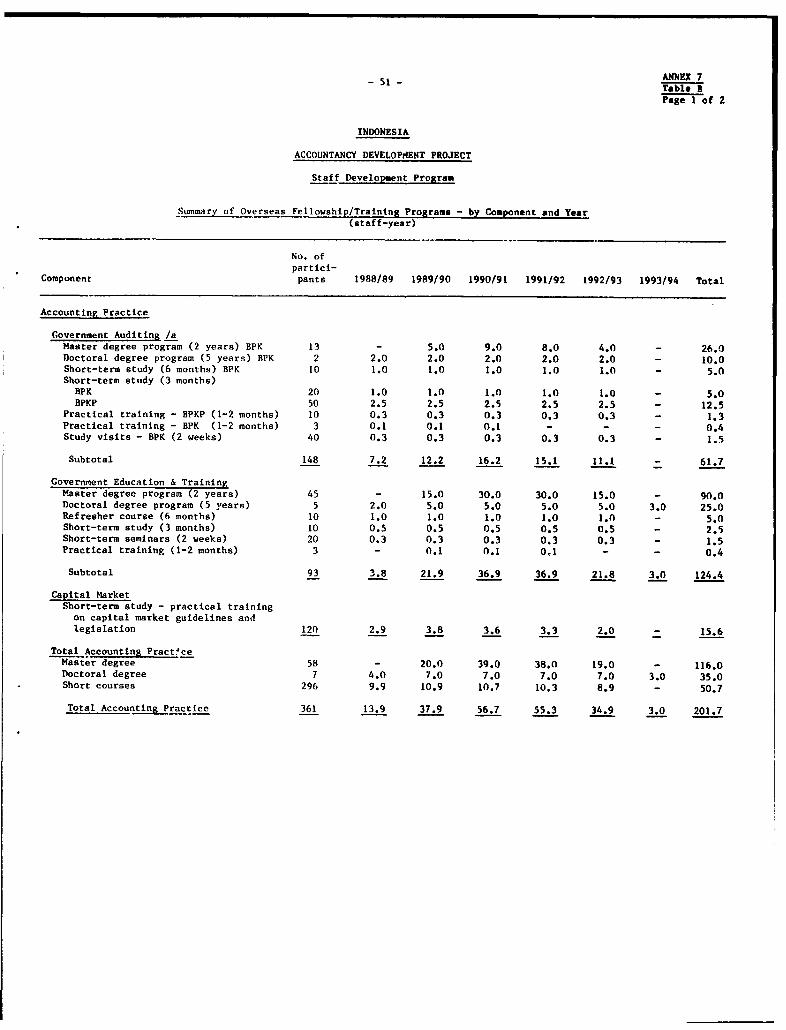

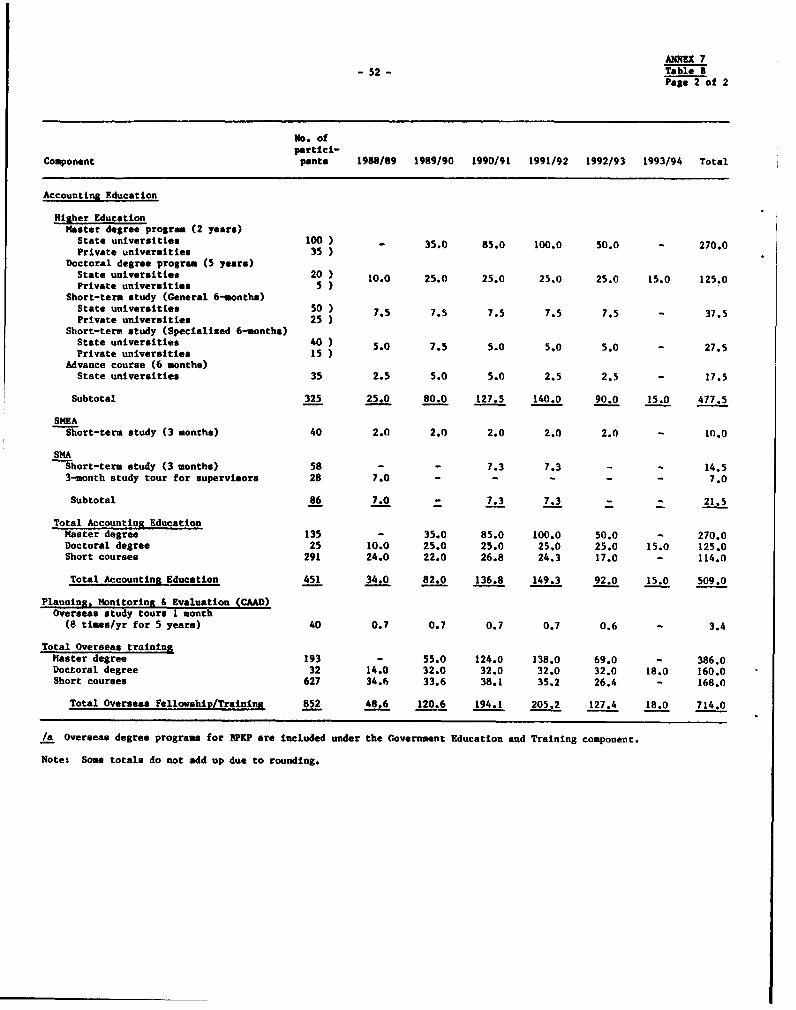

A: Sutimmary of Local Staff Development/Training Activities,by Component and Year

B: Summary of Overseas Fellowship/Training Program, by Componentand Year

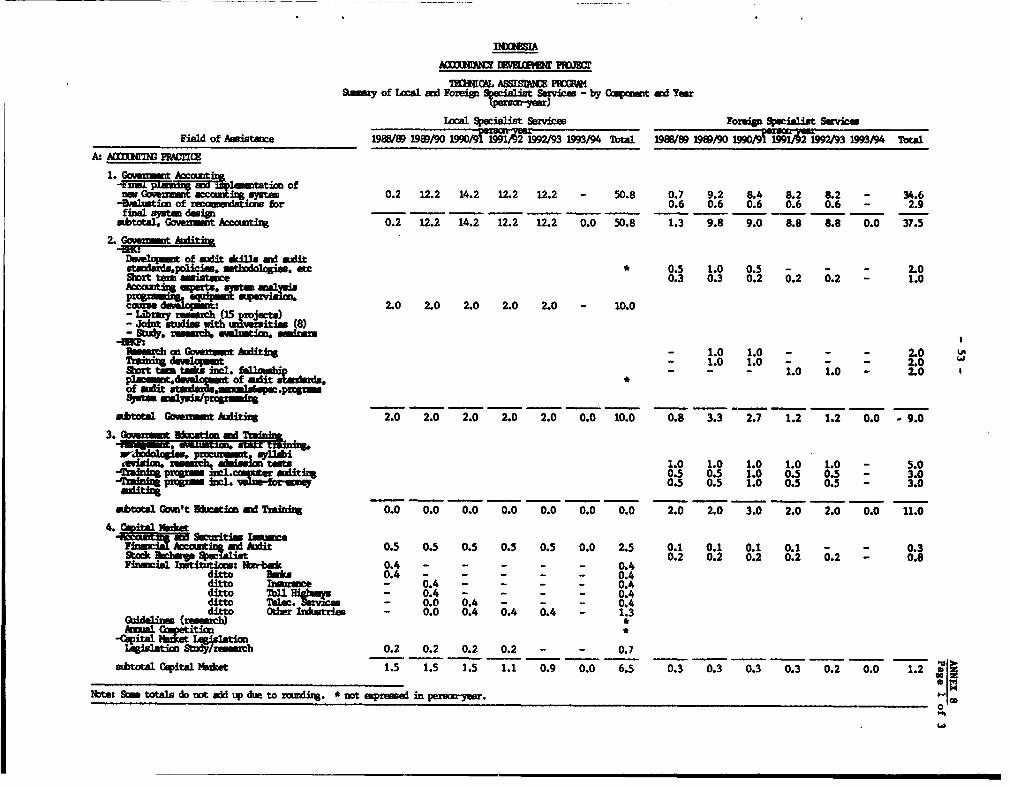

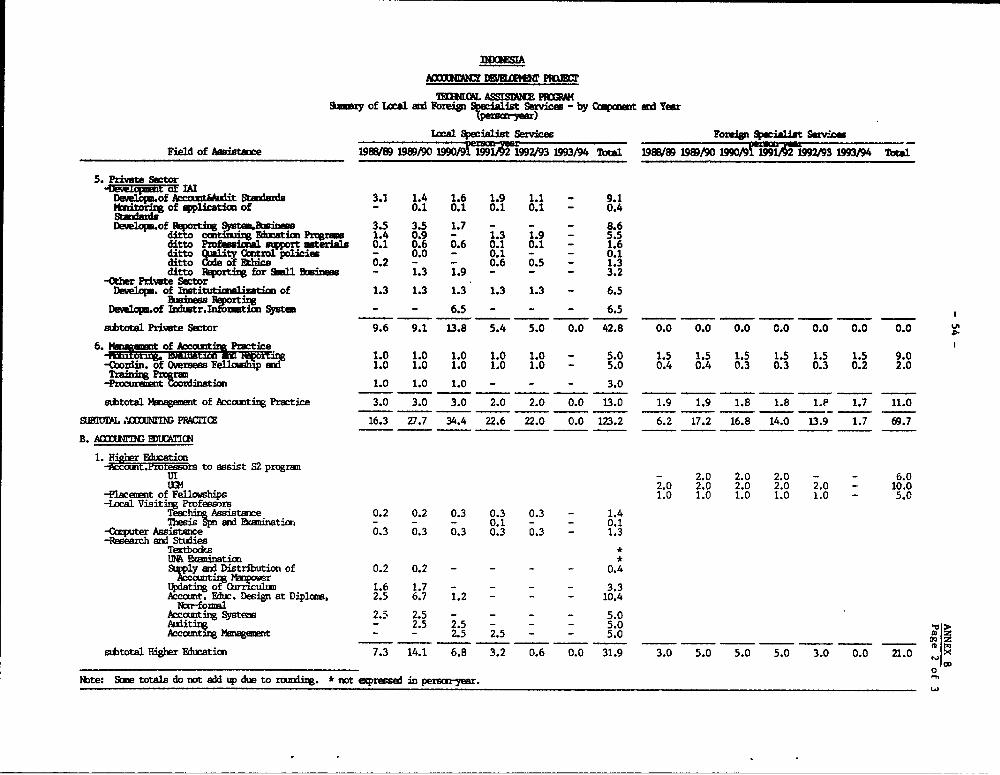

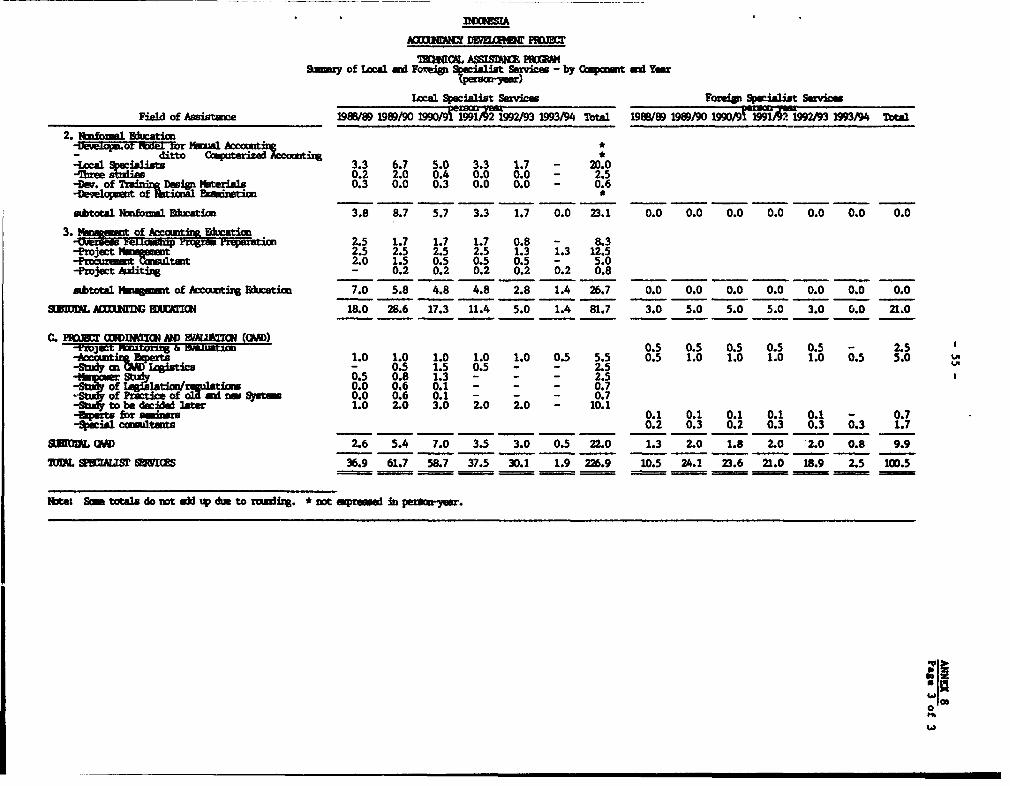

8. Technical Assistance Program:Summary of Local and Foreign Specialist Services, byComponent and Year

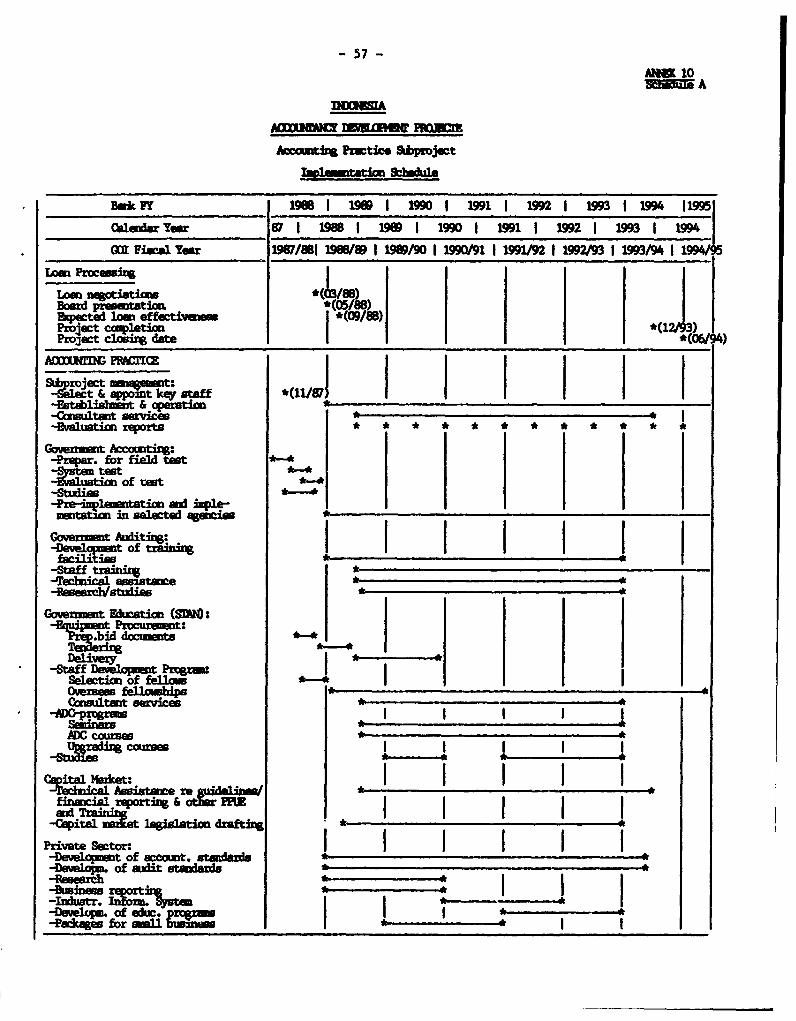

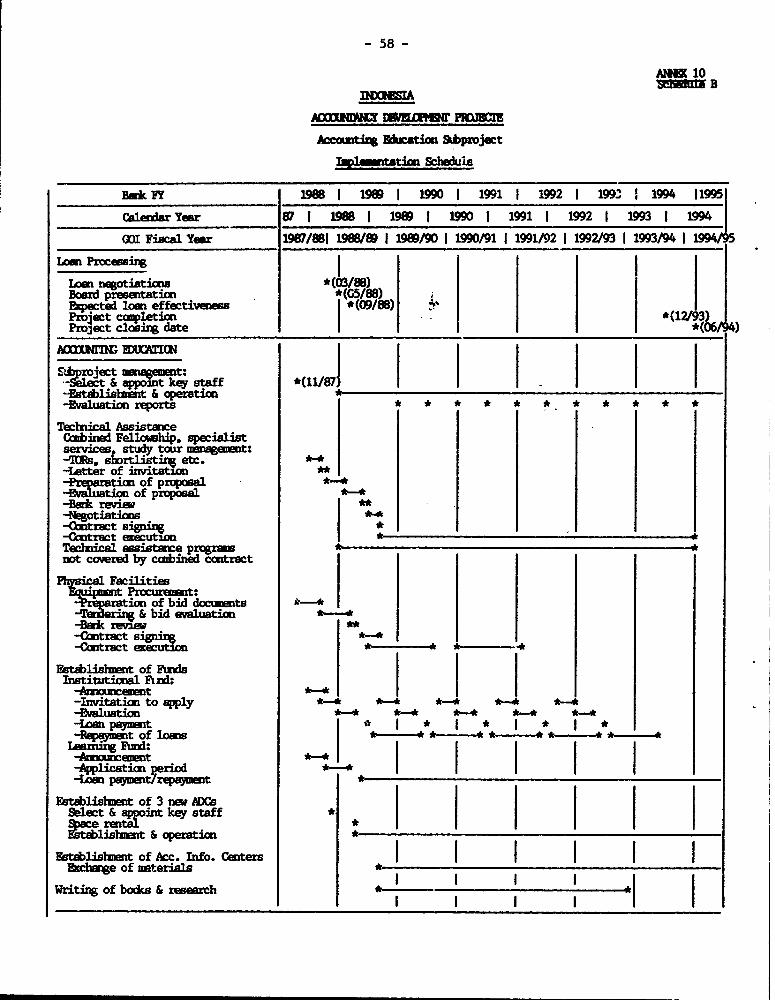

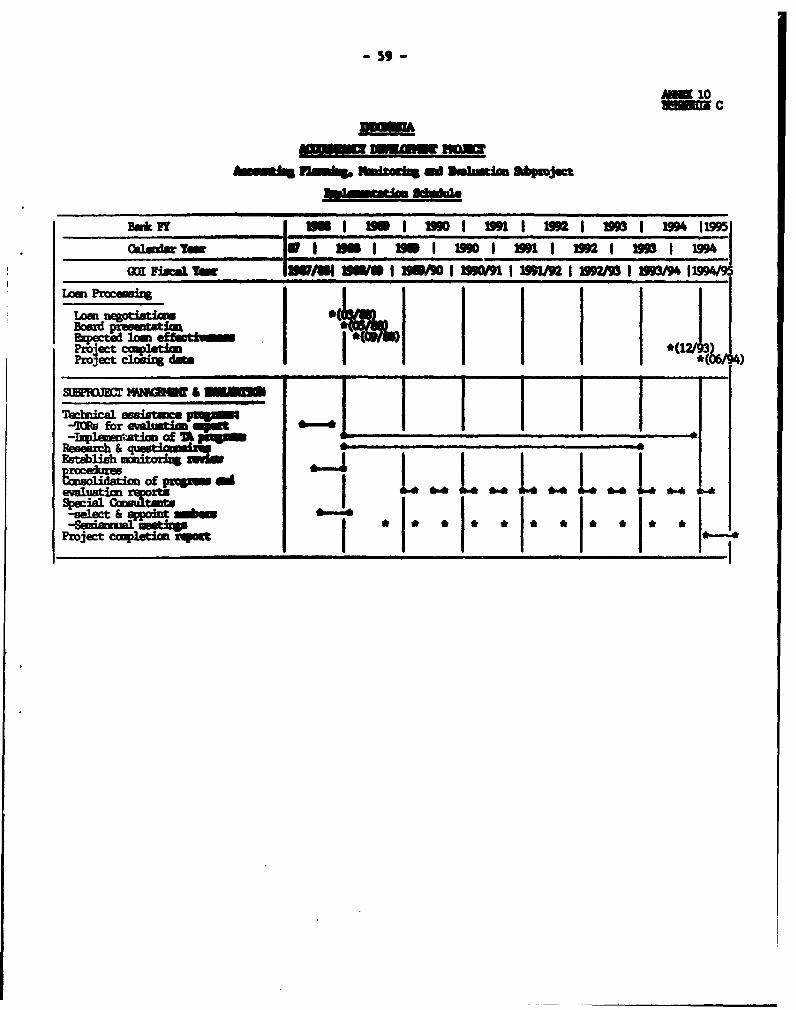

9. Estimated Schedule of Disbursements10. Implementation Schedule

A: Implementation Schedule, Accounting Practice SubprojectB: Implementation Schedule, Accounting Education SubprojectC: Implementation Schedule, Accounting Planning, Monitoring

and Evaiuation Subproject11. Project Costs by Category of Expenditure and Component12. Selected Documents and Data in the Project File

Map No. IBRD 20514

- iii -

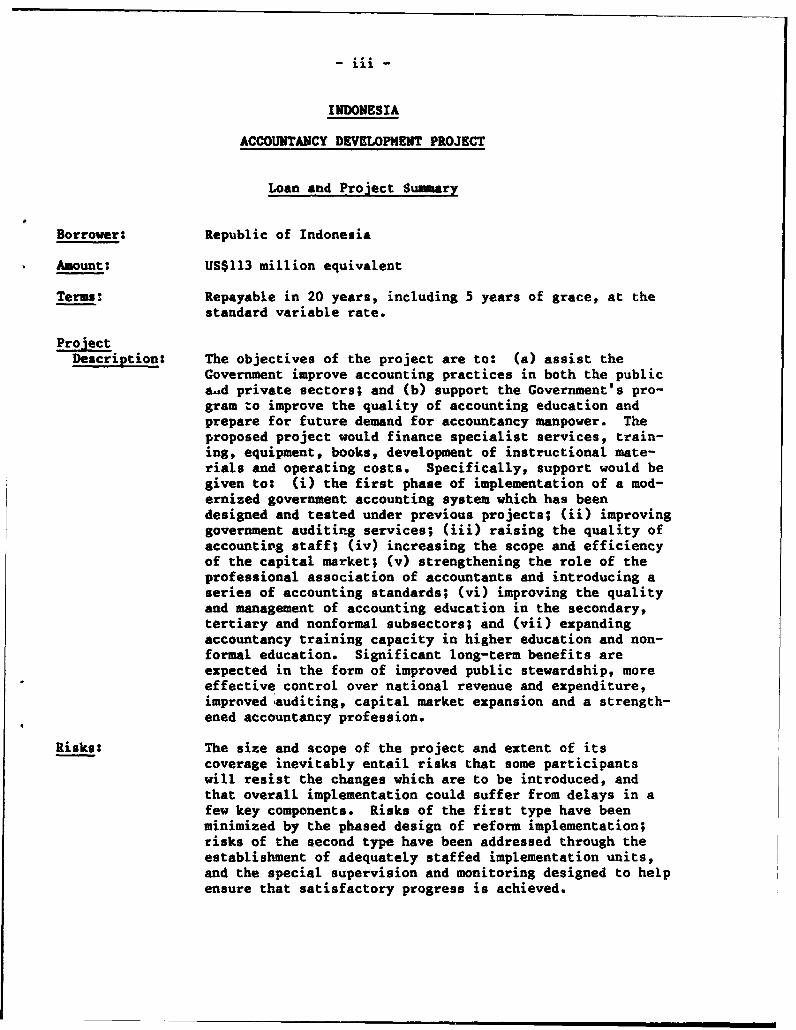

INDONESIA

ACCOUNTANCY DEVELOPMENT PROJECT

Loan and Project Summary

Borrower: Republic of Indonesia

Amount: US$113 million equivalent

Terms: Repayable in 20 years, including 5 years of grace, at the

standard variable rate.

ProjectDescription: The objectives of the project are to: (a) assist the

Government improve accounting practices in both the public

a.d private sectors; and (b) support the Government's pro-

gram to improve the quality of accounting education and

prepare for future demand for accountancy manpower. The

proposed project would finance specialist services, train-

ing, equipment, books, development of instructional mate-

rials and operating costs. Specifically, support would be

given to: (i) the first phase of implementation of a mod-

ernized government accounting system which has been

designed and tested under previous projects; (ii) improving

government auditing services; (iii) raising the quality of

accounting staff; (iv) increasing the scope and efficiency

of the capital market; (v) strengthening the role of the

professional association of accountants and introducing a

series of accounting standards; (vi) improving the quality

and management of accounting education in the secondary,

tertiary and nonformal subsectors; and (vii) expanding

accountancy training capacity in higher education and non-

formal education. Significant long-term benefits are

expected in the form of improved public stewardship, more

effective control over national revenue and expenditure,improved-auditing, capital market expansion and a strength-

ened accountancy profession.

Risks: The size and scope of the project and extent of its

coverage inevitably entail risks that some participants

will resist the changes which are to be introduced, and

that overall implementation could suffer from delays in a

few key components. Risks of the first type have been

minimized by the phased design of reform implementation;

risks of the second type have been addressed through the

establishment of adequately staffed implementation units,

and the special supervision and monitoring designed to help

ensure that satisfactory progress is achieved.

- iv -

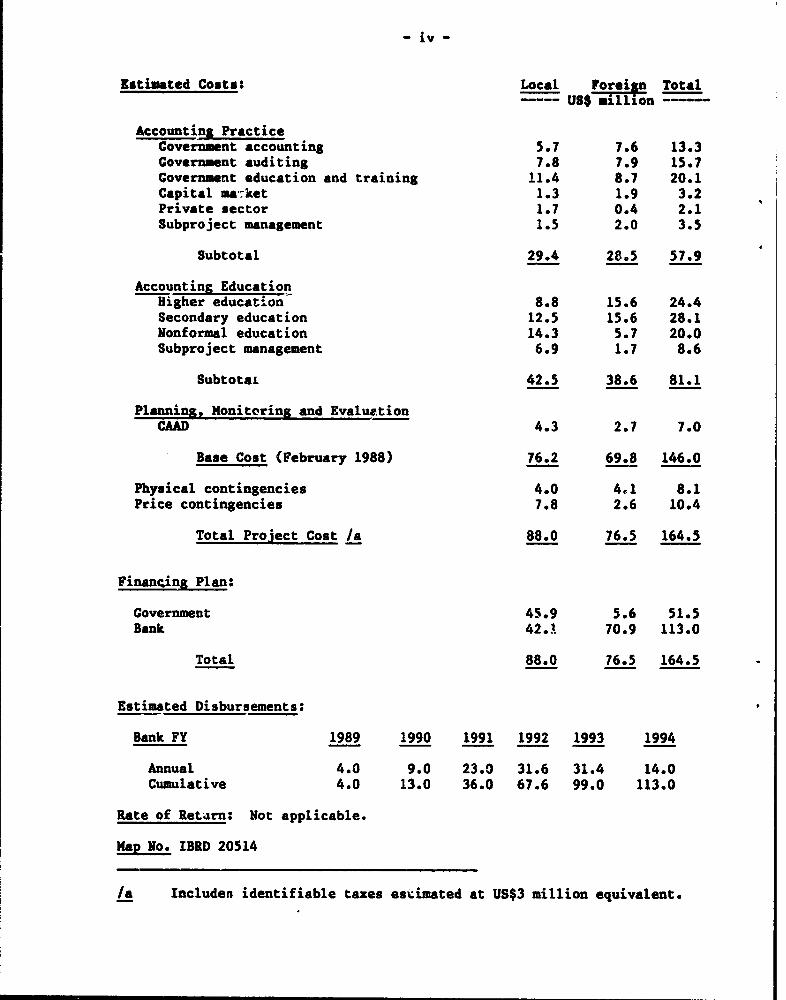

Estimated Costs: Local Forei n Total…-…-UuS$ million --

Accounting PracticeCovernment accounting 5.7 7.6 13.3Government auditing 7.8 7.9 15.7Government education and training 11.4 8.7 20.1Capital ma-:et 1.3 1.9 3.2Private sector 1.7 0.4 2.1Subproject management 1.5 2.0 3.5

Subtotal 29.4 28.5 57.9

Accounting EducationHigher education 8.8 15.6 24.4Secondary education 12.5 15.6 28.1Nonformal education 14.3 5.7 20.0Subproject management 6.9 1.7 8.6

SubtotaL 42.5 38.6 81.1

Planning, Monitoring and EvaluationCAAD 4.3 2.7 7.0

Base Cost (February 1988) 76.2 69.8 146.0

Physical contingencies 4.0 4l 8.1Price contingencies 7.8 2.6 10.4

Total Project Cost /a 88.0 76.5 164.5

Financing Plan:

Government 45.9 5.6 51.5Bank 42.1 70.9 113.0

Total 88.0 76.5 164.5

Estimated Disbursements:

Bank FY 1989 1990 1991 1992 1993 1994

Annual 4.0 9.0 23.0 31.6 31.4 14.0Cumulative 4.0 13.0 36.0 67.6 99.0 113.0

Rate of Retarn: Not applicable.

Map No. IBRD 20514

/a Includen identifiable taxes estimated at US$3 million equivalent.

I. ACCOUNTANCY DEVELOPMENT: ISSUES AND STRATEGY

Introduction

1.1 Archaic accounting practices limit the effectiveness and efficiency

of accounting and auditing activities throughout the public and private

sectors in Indonesia. To some extent, this situation reflects the deficien-

cies of inherited accounting conventiono. More fundamentally, it results from

the scarcity of professional and technical staff who are adequately trained in

modern methods of accountancy.

1.2 The most conspicuous problem occurs in the public sector. Deficien-

cies in government accounting hamper public administration in two key

respects: they compromise public stewardship by limiting the Government's

ability to ensure that public funds are used for their intended purposes; and

they obstruct budget p.Lanning by not providing accurate and timely information

on public resource availability and cost of program options. Improvements in

government accounting practices and parallel efforts in staff training in

Indonesia are urgently needed to close the serious gaps in timeliness and

accuracy of existing government accounts. One indication of the problem is

the long delay--currently two years--between the time that central government

expenditures are made and the time those expenditures are reported to Parlia-

ment. Another is the existence of major and irreconcilable differences

between different data series on the same transactions, resulting from

fragmented accounting systems and from the absence of a uniform chart of

accounts.

1.3 Further deficiencies in government accountancy arise from short-

comings of the budget process, including excessively short-term and fragmented

budget allocations, incomplete coverage of public enterprise transactions, and

blurring of distinctions between capital and revenue items._/ Improvements in

the timeliness, completeness, and accuracy of government accounts would

contribute both to better planning of public expenditures and to improved

implementation of investments and routine government activities.

1.4 The scarcity of competent government accountants and auditors also

limits the scope for improving tax audits as a means of increasing revenues

through better compliance with corporate and personal income and value added

taxes. There is major potential for improved yield under existing tax codes:

Filing ratios are estimated at 55Z for the corporate income tax, 85t f52

personal income taxes, and 39Z for the value added tax on enterprises.-

Planned improvements in government auditing are expected to lead to better tax

1/ For a fuller description of these issues, see Indonesia, Public Invest-

ment in Repelita IV, World Bank Report Number 5849-IND (December 27,

1985 ), paras. 1.39-1.41.

2/ Indonesia, Strategy for Economic Recovery, World Bank Report No.

6694-IND, May 5, 1987.

-2-

compliance, but significant improvements in compliance with corporate incometaxes and value added taxes will also require the introduction of consistentaccounting standards and the enforcement of statutory audits. This in turnimplies an expanded role for the professionrl association of accountants indevelopment oi accounting standards, certification of accountancv skills, andprovision of auditing services.

1.5 The private sector is also hampered by a shortage of professionaland technical staff with up-to-date skills in accountancy. Managementaccounting as a tool of managerial efficiency is virtually nonexistent.Financial disclosure requirements for private firms are very limited.

1.6 Development of improved and uniform reporting on enterprise perfor-mance is a prerequisite to the further expansion of the nascent market forprivate securities. Under Repelita. IV, the Governnent aims to increase theshare of private savings in total domestic savings. The goal of expandedprivate sector savings is more likely to be met if the stock market can bemade to assume a more active role in capital mobilization. Currently, theshares of only 24 companiZs are listed on the Jakarta stock exchange. As aprerequisite for improved investor confidence in the private securitiesmarket, appropriate standards for reporting the financial performance ofenterprises need to be developed and put into practice. More generally, astudy of the existing market's operation needs to be carried out with a viewto identifying appropriate changes to invigorate the market as a source ofinvestment capital.

1.7 This chapter presents issues relating to accountancy development infive broad areas: (a) government accounting and auditing, (b) private-sectoraccounting, (c) capital market, (d) accountancy manpower supply and demand,and (e) accountancy education. For topical areas (a) and (e), issues arepresented in the context of a description of the structure of implementing andtraining entities. Because of the importance of accountancy education to anyresolution of current problems in accountancy, this topic is treated in gre.t-est detail. The chapter concludes with a description of the Government'sstrategy and the Bank's strategy for accountancy development.

Issues

1.8 Government Accounting and Auditing. An array of accounting andauditing activities are carried out in the public sector to enable the Govern-ment to comply with constitutional and legal requirements governing collectionand use of public fumds. All government departments and agencies maintainaccounts of their receipt and use of funds, accounts which are routinelyaudited by their internal audit staff under the supervision of each depart-ment's or agency's Inspector General. External audits of government depart-ments' and agencies' accounts are carried out by the Supreme Audit Board(BPK), which reports directly tv, Parliament. BPK emplo-s about 1,700 staff,including about 1,100 professional audit staff, but of whom only 42 are regis-tered accountants. A parallel audit agency for the executive branch of Gov-ernment, the Financial and Development Supervisory Board (BPKP), functions asthe Government's internal auditor. Created initially as a Ministry of Finance(MOF) Directorate General, BPKP in 1983 was separated from the MOF and made an

I~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~_________

-3-

independent agency reporting directly to the President. BPKP has a mandate to

conduct both financial compliance audits and value-for-money (or cost/benefit)

audits of all government accounts. In practice, BPKP audits consist predomi-

nantly of financial compliance audits, which overlap somewhat with the exter-

nal audits conducted by BPK. In view of the separate lines of respansibility

of the two audit agencies, improved efficiency of government audit operations

will require informal cooperation between the two agencies. BPKP also func-

tions as the external auditor for 220 public enterprises, as well as for Bank-

group projects. BPKP currently employs about 6,000 auditors in its Jakarta

headquarters and its 27 regional offices.

1.9 Central control of government expenditures is vested in the Ministry

of Finance's Directorate General for Budgetary Affairs. The Directorate

General for Budgetary Affairs is responsible for ensuring that cumulative

expenditures of government departments and agencies under each budget category

are consistent with budget allocations in the annual budget law. Through its

Regional State Treasury Offices (KPN), it reviews payment requests, certifies

their conformity with budget allocations, and issues payment authorization.

Payment is made by the MOF's Regional State Cash Offices (KKN), which are

under the Directorate General for Budgetary Affairs.

1.10 The MOF's State Financial Accounting Center is responsible for main-

taining consolidated accounts of all central government expenditures and reve-

nues and for reporting them to Parliament in the form of the Annual Budget

Realization Report (PAN). It does so on the basis of reports generated by

various offices within MOF (in particular, offices within the Directorates

General of Budget and Taxes), and supplemented by analyses provided by

accounting offices in the other ministries.

1.11 In addition to central government ministries and agencies, public-

sector accounting functions are carried out by other le.els of government, and

by public enterprises. There are four levels of government below the central

government: (a) provinces (27 in number), (b) regencies and municipalities

(294), (c) subdistricts (3,500), and (d) villages (58,000). All have their

own budgets, most can levy taxes and charges; and most have their own secre-

tariats, including ac:ounting staff. There is a complex flow of budgetary

transfers within this government hierarchy--typically, from top to bottom.

And there is an equally complex flow of accounting and auditing information in

the reverse direction, principally for the purpose of documenting and justify-

ing budget authorization and paymewnts. At least 400,000 civil seyants are

employed in regional government administration at various levels._ It is

logical to presume that about half this number is engaged in accounting func-

tions of some description, but no firm statistics are available.

3/ Indonesia Management Development, World Bank Report No. 4965-IND (May 20,

1985), p. II, 65.

-4-

1.12 There are over 220 public enterprises at the national level, ad amuch larger number of small enterprises managed by regional governments._Together, they constitute an important part of the productive sector, account-ing for about 25% of national fixed capital formation and a roughly similarshare of national value added. The total number of managerias,and supervisorystaff in the public enterprises has been estimated at 96,00C.-_ The number ofclerical staff who perform some accounting functions is undoubtedly muchlarger.

1.13 Government accounting practices in Indonesia h&ve changed littlesince the 1864 Dutch Financial Administration Act on which they are based.Although an Indonesian translation of the Act was eventually prepared andminor changes were introduced when this became the Financial AdministrationAct of 1968, government accounting practices have failed to keep pace with theincreasing size and complexity of the Government's financial transactionssince Independence. They have also fallen behind the private sector, wheremore modern accounting practices are being adopted. Moreover, governmentaccounting practices have not developed beyond their historical role ofmeasuring compliance with mandated budget allocations (a role which is in anyevent only incompletely discharged because of system deficiencies and delays).In particular, they have not evolved to reflect the newer functions ofaccounting as an instrument of performance efficiency and effectiveness,widely adopted elsewhere both in public administration and in the privatesector.

1.14 The most conspicuous deficiencies of existing government accountingpractices are the following:

(a) Single-Entry Accounts. Revenue and expenditure accounts are main-tained as a simple listing of revenue and expenditure entries,without the double-entry system of offsetting debits and creditswhich is conventional practice in modern accounting systems, andwhich allows some verification of the accuracy and completeness ofaccounting records, and hence of information derived from them.

(b) Incompatible Reporting Systems. The State Financial AccountingCenter in MOF is responsible for preparing consolidated reports ofall central government revenues and expenditures, and reporting themto Parliament in the PAN. The reports from which the PAN isprepared are incompatible in a number of respects: for example,(i) they ao not share a common chart of accounts; (ii) they do notall recognize revenue and expenditure items at the same point in thetransaction cycle; and (iii) some items (in particular, taxrevenues) are classified as to type on the basis of analysesreported by one source applied to totals rLported by another,without any reconciliation being possible between the two. The PAN

4/ Ibid, p. II, 73.

5/ Ibid, p. II, 79.

-5-

report therefare lacks a consistent basis and contains, at best, a

number of significant approximations.

(c) Delayed Reporting. The shortage of qualified accounting staff and

bottlenecks in recording, transmitting and consolidating accounts

lead to unaccaptably long delays in reporting to Parliament on

actual government expenditures. The PAN has typically reached

Parliament two to three years after the close of the fiscal year inquestion. These delays seriously compromise the nation's control of

its financial affairs.

(d) Classification of Accounts. Classifications of government accounts

are designed exclusively for monitoring and reporting of actual cen-

tral government revenues and expenditures. They are not designed

for analysis of the cost effectiveness of programs or program compo-

nents, or to provide adequate information to control expenditures on

development projects. Agency accounts are thus not as useful as

they could be to guide the decisions of directors general and other

managers of agency programs and projects.

(e) Asset Accounting. Because the budget does not adequately

distinguish capital from revenue items, and because the recording of

fixed asset inventories is not the responsibility of accounting

offices, such inventories cannot be reconciled to the financial

accounts and may accordingly be unreliable in both physical and

value terms.

1.15 Private-Sector Accounting and Auditing The private sector com-

prises Indonesian public and private companies (including about 300 public

accounting firms), cooperatives, partnership. and sole traders. The quality

of accounting in the private sector varies widely, tending to be better in

those companies which have foreign investors or are listed on the local stock

exchange (which imposes certain reporting standards-para. 1.18); but in

general the development of accounting has fallen behind that of other skills

required in industry and commerce. Accounting systems frequently do not pro-

vide adequate financial control, and few accountants and managers are trained

to produce or use accounting information as a management tool.

1.16 To some extent this situation can be attributed to a general absence

in Indonesian law of regulations of the type which in other countries fre-

quently enforce the maintenance of basic standards of accounting. The

Indonesian Companies' Act and Commercial Code are anachronisms dating back to

colonial times and are silent on accounting matters; there are no statutory

reporting requirements for companies; and there are no audit requirements

(apart from listed companies). The tax law does require companies to file a

profit-and-loss account and balance sheet along with their tax computation,

but the level of compliance is low (para. 1.4).

1.17 A second factor which in other countries frequently contributes to

the maintenance of accounting standards is the presence of a strong profess-

ional body of accountants. In Indonesia, the professional body--the

Indonesian Institute of Accountants (IAI)--is relatively young and has not yet

6

developed the stature to comaand wide respect among businessmen and otherpotential users of accounting and auditing services. Of the 5,0O0 registeredaccountants in Indonesia, 3,500 are nominally mmbers of IAI but only about1,000 are paid-up. The Institute's only full-time staff is a small secre-tariat; all the officers contribute their services part-time. In thesecircumstances the Institute's capacity to lead the profession--let alonepromote it in the eyes of the public--is clearly limited. A basic statementof accounting principles has been issued, a program of continuing professionaleducation for members has been initiated, and relations are maintained withinternational organizations such as the International Federation of Accoun-tants (IFAC) and the Confederation of Asia and Pacific Accountants (CAPA).But the IAI lacks a body of detailed accounting and auditing standards toguide the profession and a code of ethics and disciplinary processes toregulate it.

1.18 Capital Market. The Indonesian capital market was established inits present form in 1977. It operates under the overall authority of theMinister of Finance and comprises three principal institutions: a CapitalMarket Policy Council, a Capital Market Executive Agency and an investmenttrust, PT. Danareksa. The Policy Council formulates guidelines and policyalternatives for the operation of the Capital Market and the management of PT.Danareksa. The Capital Market Executive Agency (BAPEPAM) controls and managesthe Capital Market in accordance with the policy outlined by the Government,and is directly responsible to the Minister of Finance. The agency has threemain functions. It evaluates whether companies which sell their gharesthrough the Capital Market have met all listing requirements and are sound andwell managed; it operates the stock exchange; and it monitors the progress ofcompanies which are listed on the stock exchange. Members of the exchangeinclude state and private banks, financial institutions and brokerage firms.Listed companies are required to submit to BAPEPAM their financial Fta&teents(profit and loss, balance sheet, and statement of changes in financialposition) and the audit report of a Registered Accountant thereon, and suchother reports as BAPEPAM may from time to time require. In recent year* thebusiness of the exchange has been declining. New issues (stocks and bonds)amounted to only Rp 50 billion in 1986 compared to Rp 144 billion in 1984; thevolume of shares traded fell to 1.4 million from a peak of 5 million in 1982;and the number of listed companies has remained static at 24 for three years.

1.19 It is clear that measures to revitalize the market are nowrequired. These measures would have three main objectives:

(a) to broaden investor familiarity with, and interest in, the market;

(b) to offer a wider range of investment vehicles, including possiblymutual funds and further investment trusts; and

(c) to strengthen confidence in the market by consolidating the associa-ted legislation (some of which is out of date), and codifying theregulations concerning company listing, stock issuance, reportingand related matters and tightening their enforcement.

1.20 Accountancy Manpower Supply and Demand. There is a large unmet

demand for professional accountants. There are currently only about 5,000

registered accountants working in Indonesia, out of a total nonagricultural

labor force of 25 million. Of these, about 3,000 work for Government (chiefly

as auditors for BPKP, SPK and the larger government enterprises), 1,600 workfor private industry, and 400 work for public accounting iirms. This propor-

tion of professional accountants in the labor force (0.02X) is small by compa-

rison with other countries in the region, and extremely small by comparison

with the industrialized countries. The scarcity of professional accountants

is largely attributable to the limited capacity of existing accountancy pro-

grams (para. 1.27). The large unmet demand for accountants resultg in a

sizable salary premium for registered accountants. A 1982 survey -/ of 680

medium and large enterprises, carried out under the First Polytechnic Project,

reports more than a six-fold earnings differential between registered accoun-

tants and accounting staff with secondary-level training. This differential

is almost twice as large as the average ,,rnings differential between masters-

level graduates and secondary graduates.-

1.21 A large proportion of accountancy manpower at subprofessional levels

also neeas upgrading of technical qualifications. Over a third of the 300,000

bookkeepers and cashiers in the labor force have received no formal schooling

in accountancy. Of the 250,000 managers and proprietors working in industry

and service-sector activities, fewer than 10Z have any training in accounting

techniques.

1.22 Small-scale industries are planned under Repelita IV and Repelita V

to provide an important source of private-sector industrial growth. If these

enterprises are to play the dynamic role envisaged for them, it will be reces-

sary to provide more of their managers with training in basic accountancy

practices. These skills will also improve the capacity of small enterprises

to comply with the recently enacted reporting requirements for corporate and

personal income taxes (para. 1.4).

1.23 Although accountancy is traditionally a male-dominated profession,

women are well represented in accountancy employment in Indonesia. Women cur-

rently comprise 20 to 302 of the members of IAI, the professional association,

and female membership has grown more rapidly than male membership during the

past two years. The proportion of female accountants in many professione.l

jobs has remained at a level somewhat lower than this largely because of self

selection ef job applicants. The proportion of females in the professional

audit staff of the central government audit agencies (152 in BPKP and 191 in

BPK), for example, results from the scarcity of past female applicants, which

6/ Reported in "Final Report: Study on Demand of Accounting Manpower in

Indonesia," prepared by the Management Institute of the Faculty of

Economics, the University of Indonesia; November, 1983.

7/ As reported in Chapter 2 ("Economic and Financial Analysis") of the 1986

Education and Human Resources Sector Review carried out by the MOEC and

USAID.

in turn reflects the reluctance of qualified women and their families toaccept the travel and other work requirements of the job of state auditor.There is evidence, however, that the traditional reluctance of wom. to acceptsuch jobs is decreasing. A recent article in BPK's staff journal - exploresthe reasons which discourage women from taking jobs as state auditors, andconcludes that they are likely to be less of a deterrent to female job appli-cants in the future. Indeed, the proportion of women aong the state auditorsrecruited during the past year is above the average proportion of female stateauditors.

1.24 Available evidence suggests that female participation in accountingemployment at the sub-professional level is higher than at the professionallevel. The 1985 intercensal survey reports that 232 of urban employment inthe finance, real estate, insurance and business services sector is female.Moreover, fully 80% of SMEA enrollments and a similar proportion of graduatesare female. This very high percentage implies that female employment as P.

proportion of total accountancy employment at the sub-professional level islikely to increase in the future.

1.25 Accountancy Education and Training Programs. Prior to Independencein 1945 and to the nationalization of Dutch enterprises in 1957, most account-ing practices in government and in the private sector followed Dutch account-ing conventions. Because most senior positions involving accounting were heldby expatriate staff, in-country accountancy training was initially limited tobookkeeping courses offered in trade and comerce institutions. These lower-level training programs have evolved into two main categories of accountancyinstruction: the accountancy courses offered in the Hinistry of Education andCulture's (MOEC) general secondary schools (SMAs) and secondary commercialschools (SMEAs), and the nonformal courses in accountancy administered byvarious goverrment and private agencies, often through short-term, in-servicetraining.

1.26 Higher-level training in accountancy was introduced in 1952, whenthe University of Indonesia's Faculty of Economics began to offer accountancycourses at the bachelor's level. By the time the first graduates of this newprogram graduated (1954), legislation was introduced which enabled mastersdegree graduates of accredited university accountancy programs to be certifiedby the MOF to practice as professional accountants (Registered Accountants) inIndonesia. Currently, there are 8 public universities with accredited pro-grams in accountancy. Graduatea of accountancy programs in private universi-ties and non-accredited public universities may be certified as RegisteredAccountants only by passing a rigorous, two-stage State Accountancy Examina-tion, jointly administered by MOF and MOEC.

1.27 In order to help meet the growing demand for qualified accountantsin government service, new legislation was enacted in 1961 to require that allqualified applicants for professional certification as accountants must

8/ "Joys and Tribulations of a Female Auditor of the State Audit Bureau(BPK)," available in the project file.

-9-

complete at least three years of government service before certification would

be granted. This measure, however, proved insufficient to meet government

needs, and in 1975 the MOEC approved the establishment by the MOF of its own

accountancy training institute, the State School of Government Accounting

(STAN). The STAN pre-service accountancy courses are offered at two levels:

a three-year adjunct accountant course (called the Diploma III level), and a

five-year accountant course (called the Diploma IV level), which also requires

a thesis and working experience as an adjunct accountant. Diploma IV

graduates are eligible for certification by MOF as Registered Accountants.

STAN trains about 400 graduates per year in its pre-service diploma III and

diploma IV programs of accountancy, all of whom are required to serve at least

15 years in government employment. In addition, STAN offers an extensive

program of in-service training for government accountants and auditors--

usually in the form of two-week training courses on specific topics of

accounting or auditing practice.

1.28 There are currently a total of 85 universities, institutes, and

academies which offer post-secondary courses of accountancy, but there are

important differences among these programs in terms of their size and quality.

The vast majority of Registered Accountants in Indonesia are graduates of STAN

and the eight state universities with accredited accountancy programs.

Together, these programs graduate about 420 students per year at the regis-

tered accountant level. By 1978, private institutes had trained over 2,500

students of accounting at the bachelors level. However, by 1987 only 90

master's level graduates had registered for the certification exam, and of

these only 24 had passed. In part, this weak performance by the private

institutes of accountancy, and more generally, by the non-accredited accoun-

tancy programs reflects the difference in certification requirements for

graduates of non-accredited accountancy programs--who must pass the profes-

sional certification exam--versus graduates of accredited programs--who are

not required to take the exam. But, more basically, it reflects the weakness

of their programs and staff: A general problem with accountancy training

programs of all kinds is the shortage of qualified teaching staff and teaching

materials for the new methods of accountancy which are now widely adopted in

the private sector and which are about to be introduced in the public sector.

1.29 This problem results from the dualism which has characterized

accountancy training programs for most of the past three decades. Following

the nationalization of Dutch companies in 1957, private-sector companies

progressively replaced the former, inherited accounting practices with more

modern accounting practices--particularly, of North American origin. At the

same time, government accounting has continued to follow the earlier prac-

tices. There had thus been a need for accountancy training at all levels to

provide instruction in both the old and new systems of accounting. As the

Government has progressively become committed to modernization of government

accountancy and as the private sector's adoption of new accounting practices

has become widespread, however, the need for maintaining a dual system of

accountancy education no longer exists. Recognizing this fact, the MOEC moved

early in the 1980's to prepare new curricula for accountancy education at all

levels. These curricula are now complete and in operation, but their effec-

tiveness is impaired by teachers' unfamiliarity with the new techniques and

with the lack of suitable Indonesian language textbooks, teachers' manuals,

and other teaching materials.

- 10 -

1.30 Accounting education at the secondary level is included in two ofthe upper secondary (grades 10-12) education programs: Upper SecondaryCommercial Schools (SMEAs) and Upper Secondary General Schools (SMAs). Ofthese, the SMEAs offer the more extensive training in accountancy. The SMEAsalso constitute by far the largest vocational school system in Indonesia,covering about one-third of all students enrolled in the more than 25 differ-ent types of vocational programs. There are currently about 1,200 SMEAs, ofwhich 300 are public and 900 are private. Although more numerous, the privateSMEAs tend to be much smaller than the public SMEAs: Total enrollments in theprivate SMEAs are 250,000, versus about 200,000 in the public SMEAs. The cur-ricula are the same in the public and the private SHEAs. Both provide three-year specializations in administration, accounting, business and commerce,cooperatives and tourism. Each of these specializations contains a set ofaccounting courses ranging from basic tourism-related accounting in thetourism specialization to more advanced financial and cost accounting, audit-ing, finance and taxation in the accounting program. (An outline of theaccounting curriculum is included in Annex 3.) About 30X of SMEA students areenrolled in the accounting specialization. Annual graduates from this stream(from both public and private SMEAs) number about 40,000 per year. Most ofthese graduates enter the workforce as accounting technicians. About one-third of the 2,500 teachers of accountancy in the public and private SMEAsreceived upgrading training in accountancy under the First Polytechnic Project(paras. 1.33 and 1.39).

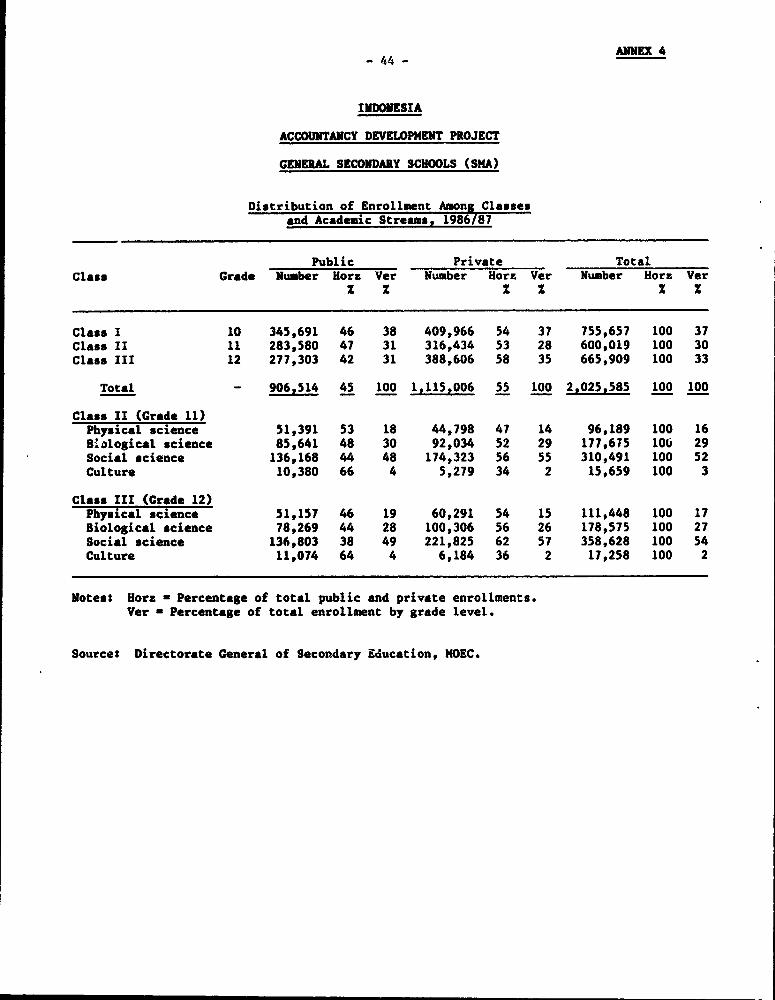

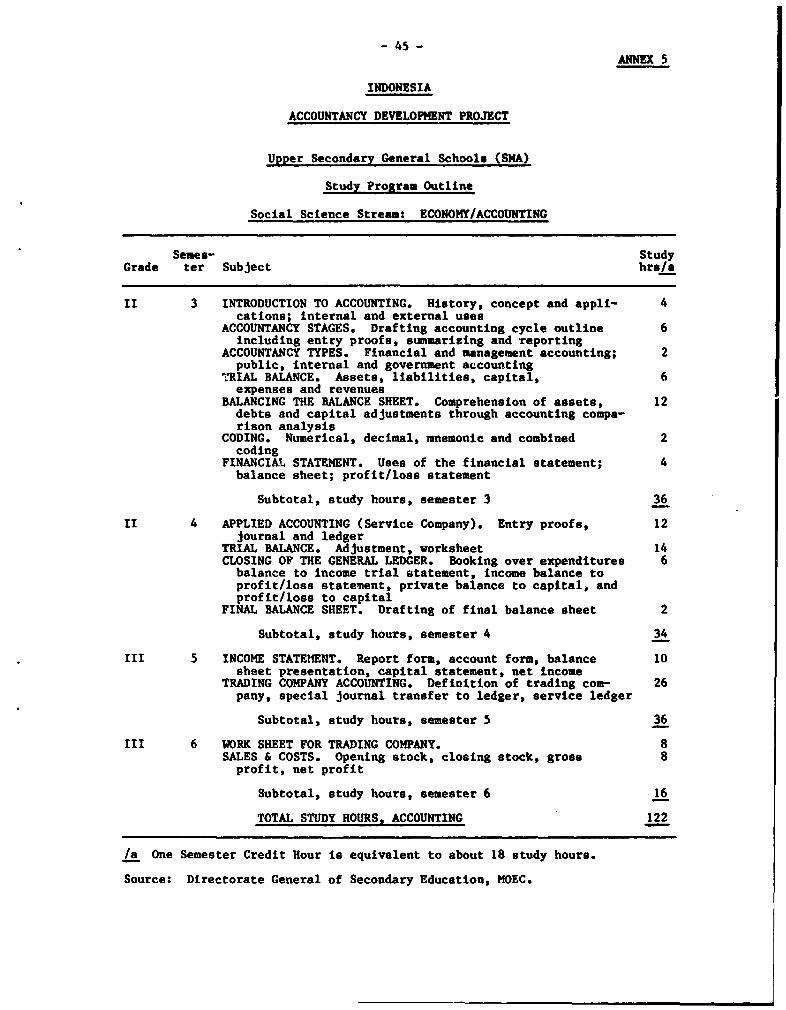

1.31 A less intensive program of basic accounting training is offered inupper secondary general schools (SMAs). Currently, the SMAs consist of asingle, 3-year academic stream with 4 options: physical science, biologicalscience, social science and culture. Two hours a week of instruction in basicaccounting is taught in the second and third year of the social sciencestream, which enrolls the majority (55%) of SMA students. Since over half ofSMA students choose the social science stream, approximately one third of the2.2 million SMA students in 1986 received this basic accounting training inabout 1,400 public and 4,500 private SMAs (Annex 4). Of about 140,000 SMAteachers, approximately 2,500 are teachers of accounting. Most of theseaccounting teachers have been trained in outdated bookkeeping procedures, anda limited upgrading program conducted by the Accountancy Development Centers(ADCs) has not proved adequate as a basis for improving the quality ofinstruction.

1.32 Under the authority of the MOEC's Directorate General for NonformalEducation, Youth and Sports, nonformal education programs are conducted inmore than 13,400 (mainly private) institutions in Indonesia, with a total ofabout 1.4 million students enrolled in 1986. Two different types of nonfoirmaleducation programs are offered under this system. The largest is a generaleducation program with main emphasis on literacy courses. The other is anoccupational program designed to foster specific employable skills. Studentscompleting the program are eligible to take an examination certifying comple-tion of training equivalent to upper secondary vocational schooling (grade12). The largest of the nonformal programs is in bookkeeping and accounting.Courses in these subjects are offered by 752 institutions at 4 differentlevels of training, ranging from 156 lessons of basic accounting to 459lessons of more advanced accounting. In 1986, these courses enrolled a total

- 11 -

of about 100,000 students, of whom 59Z took the secondary-level equivalency

examination in accounting. Surveys undertaken by the Directorate General

indicate that the popularity of the accounting specialization among the

students taking the nonformal occupational courses reflects the successful

record of job placement of former graduates, particularly in small and medium-

sized enterprises. Until recently, the former Dutch-based system of account-

ing was the preferred method of instruction, and only very few of the 750 full

time and 2,900 part-time instructors are trained in modern accounting. By

1993, the total number of accounting instructors is expected to reach 3,600

employed at about 1,200 institutions. Beginning in 1988, the national exami-

nation will test only modern accounting, which will add to the severe need for

revision of the programs and retraining of the teachers.

Accountancy Development Strategy

1.33 Government Strategy. The Government's awareness of the issues

described above and its concern about their consequences has grown progres-

sively over the past decade. Under the recently completed Polytechnic Project

(Cr. 869-IND 1979), it established ADCs at three leading state universities

and at STAN. It also expanded enrollments at the secondary level and in non-

formal education. The Government now recognizes that there are limits to how

effectively it can address the recognized accountancy deficiencies through

such training expansion alone. More basic changes are clearly called for--

particularly in government accounting practices. If such changes are

eventually to be made, there is merit in deciding on those changes sooner

rather than later so that ongoing training programs can prepare for them.

Moreover, efforts to modernize accountancy now are timely in that they would

complement the Government's ongoing macroeconamic adjustment program, which,

among its major goals, emphasizes economic efficiency.

1.34 Also under the Polytechnic Project, MOF commissioned an exsensive

study of needs for modernization in government accounting practices._ That

study developed a detailed program of proposed meaures to modernize government

accountancy. After MOF's evaluation of the study and consultation with the

other ministries involved (as well as with the Bank), the Government has made

the decision to incorporate the preposed changes into its systev of central

government accounts and to reflect those changes in its various accountancy

training programs.

9/ The full findings of the study, which occupy more than 20 volumes, are

summarized in an October 1984 consultant's report entitled "Study on

Government Accounting and Auditing Modernization in Indonesia: Major

Findings on the Existing Budgeting, Accounting, and Reporting Systems."

The sumary report is available in the project file.

- 12 -

1.35 The most important changes to be introduced in 8, the modernizedsystem of central government accounts are the following:_

(a) Double-Entry Accounts. To improve accuracy and completeness ofgovernment accounts (para. 1.14(a)], all revenue and expenditureaccounts are to be kept on a double-entry basis, with offsettingdebits and credits.

(b) Consolidation of Central Accounting. To improve the timeliness,accuracy, consistency and completeness of reports on overall govern-ment revenues and expenditures (para. 1.14(b)], responsiblAity formaintaining government-wide accounts of revenues and expenditures isto be fully centralized within the State Financial Accounting Centerof the MOF. The main immediate effect of this measure will be tointegrate into the MOF's consolj4qted accounts the formerly separateaccounts of Bagian Anggaran 16 and the Central State TreasurySystem. At the same time, the MOF State Financial Accounting Centeris to be given responsibility for introducing and maintainingaccountancy standards throughout the Government.

(c) Improved Agency Accounting. To provide better support to agencyprogram and project managers, the responsibility for maintainingbasic agency accounts is to be decentralized. Expenditures will beclassified in agency accounts by program/project and category ofexpenditure--introducing detail on program-level components which isnot generally available under current classifications of agencyaccounts. At the same time, controls are to be applied by theagencies in extracting and reporting information for the consoli-dated budget report; this will strengthen financial control of theaccuracy and completeness of reports on government revenues andexpenditures.

(d) Introduction of Balance-Sheet Accounting. To support enhancedaccountability for state investments, the notion of governmentequity [para. 1.14(e)] is to be introduced into government accountsby distinguishing capital items in government revenue and

10/ The objectives, rationale, and thrust of the modernization program weredescribed in a September 1986 presentation by the Minister of Finance,Mr. Radius Prowiro, to the International Financial Management Conferencein Washington, D.C. The presentation is reproduced as "Reforming Finan-cial Management in Government: The Indonesian Agenda," in InternationalJournal of Government Auditing, January 1987 (available in the projectfile).

11/ "Bagian Anggaran 16" designates the special fund managed by the Ministerof Finance, which is not for the exclusive use of any specific depart-ment, and which includes the budget allocated for such items as pensionpayments, subsidies to locail governments, investments in stateenterprises, and amortization of foreign loans.

- 13 -

expenditure accounts, and carrying them in separate asset andliability accounts.

(e) Uniform Chart of Accounts. To assure consistency of recording andreporting, a uniform chart of accounts (or schedule of budgetheadings) [para. 1.14(b)(i)] is to be developed and introduced.

1.36 This program of changes to modernize government accountancy is vast.

It would eventually affect the work of hundreds of thousands of civil ser-vants, and for some of them it would mean a fundamental change in how theyconceive their work. The Government is aware of the ambitiousness of theprogram. To minimize the inevitable disruption involved and to preclude the(unacceptable) risk of a lapse in coverage by either the old system or the new

system of accounts, the Government has decided to implement the changes inti-ally on a pilot basis in selected directorates general of four ministries,with subsequent, progressive extension to other directorates general and then

to other ministries. The existing system of accounts would be maintained and

would run in parallel with the new system in each directorate general untilstaff training had been completed and the new system had been successfullypiloted. At that point, the changeover to the new system would occur. Imple-

mentation of the government accounting modernization, then, would progress in

stepwise fashion across the various units of central government. Followingsuccessful implementation at this level, it is envisioned that similarimprovements in accounting practices would be adodpted by public enterprisesand by lower levels of Government. In preparation for implementation of the

accountancy modernization program, the Government established in 1985 aninterministerial Coordinating Agency for Accountancy Development (CAAD), whichincludes representation from the IAI. Support for this activity was providedunder the Second Polytechnic Project (Ln. 2290-IND, 1984). CAAD's objectives

are to develop new accounting standards for the public and private sectors, to

coordinate implementation of those standards, and to ensure that trainingprograms are consistent with them.

1.37 In addition to the modernization of government accountancy, the

Government's strategy for accountancy development includes a number of comple-mentary actions to strengthen accountancy training at all levels, to expand

the role of the professional association of accountants, and to promote the

development of a private securities market. Although the Government expectsto continue to expand accountancy training capacity, its current trainingefforts will focus on improving the qualifications of existing accountingmanpower. This qualitative emphasis in the Government's accountancy develop-ment strategy is appropriate in view if the urgency of existing needs.

1.38 Bank Strategy. The Bank Group has been engaged in a dialogue with

the Government on needs in accountancy development since the preparation of

the 1979 Polytechnic Project. The accountancy component of that projectincluded a study of government accounting practices and proposed changes which

are the basis of the Government's current accountancy modernization program.The Bank worked closely with the Government in reviewing the specificproposals which emerged from the study, and advised the Government on the

creation of CAAD as a key element to assure successful implementation of theprogram. The Bank fully endorses the Government's accountancy modernization

- 14 -

program, as well as its plan for phased implementation of the program(para. 1.36). It views these efforts as an appropriate response to the majorissues described above (paras. 1.8-1.32), and as a timely complement to theGovernment's ongoing macroeconomic adjustment efforts. The proposed Accoun-tancy Deylopment Project would support the initial implementation of theprogram.-

1.39 In addition to supporting the development of the current accountancymodernization program, the 1979 Polytechnic Project also financed theestablishment of three new ADCs within the faculties of economics of theUniversity of Indonesia (UI) University of Gajah Mada (UGM), and theUniversity of North Sumatra (USU) as well as a new ADC at STAN, the MOF'straining institute. Together, these centers have trained more than 5,000accountants and accounting teachers to date (December 1987). The PolytechnicProject was the first Bank-group education project in Indonesia to providesupport for specialized programs of accountancy training. The project closedin June 1985, and is being followed up under the Second Polytechnic Project(Ln. 2290-IND, 1984). This ongoing project includes support for the creationof 770 training places in accounting under a new commercial stream which isbeing introduced in the national polytechnic system.

1.40 In addition to the two polytechnic projects, the Bank Group hassupported a total of 17 education and training projects in Indonesia, amount-ing to total commitments of US$948 million, net of cancellations. Most ofthese projects have been or are being implemented by MOEC. The implementationexperience with those projects indicates the importance of as simple anadministrative structure as possible and the early appointment of full-timestaff to manage implementation units. The design of the current projectreflects these concerns: Managers of all project units have been designated,including the key staff of the accounting practice (MOF) component who arealready at work. Moreover, two consolidated PIUs will manage implementationin the various departments of the two ministries involved (para. 2.38)--asignificant innovation in light of past experience in the MOEC.

1.41 A question of concern in past Bank-sponsored projects in all sectorsis the timeliness of submission of project audit reports. The Bank hasaddressed the problem of late audit reports on a project-by-project basisthrough several actions, including financing assistance for preparing finan-cial statements and special supervision efforts by Bank staff with PIU and

12/ Prior Bank Group experience with support of system-wide accountancyreform is limited to two recent projects in Madagascar (Credits 1155-MAGand 1661-MAG), whose implementation has been generally satisfactory. Theaccountancy modernization program whose implementation the proposed loanwould support differs from the Madagascar operations in that: (a) itinvolves a more extensive set of changes in accountancy practices; (b) itincludes more complementary actions--including training, capital marketdevelopment, and strengthening the professional association ofaccountants; and (c) it was preceded by much more intensive preparations--including development of detailed plans for phased implementation.

- 15 -

audit agency staff. These efforts, which have led to improved audit perfor-mance, vill continue. In the meantime, the proposed project, by supportingactions to strengthen BPKP and ministry staff capabilities in accountancy andauditing, is expected to contribute to further improvements in governmentaudit performance in the mediun term.

II. THE PROJECT

Project Objectives

2.1 The objectives of the proposed project are:

(a) to improve accounting practices: (i) in the public sector, bysupporting the introduction of modernized government accountingpractices, initially in MOF and three other agencies, and eventuallyin all agencies; and (ii) in the private sector by supporting thedevelopment of technical standards and a code of ethics for theaccountancy profession; and

(b) to support the Government's program to raise the quality ofaccounting faculty and teaching staff, and to prepare for futureexpansion of accountancy education and training.

2.2 The project has a number of secondary objectives, each of which isaligned with one of the main objectives. Of the secondary objectives, themost important are: (a) developing the quality of government auditingagencies and government auditors; (b) strengthening the organization of theprofession of accountancy; (c) increasing the scope and efficiency of thecapital market; (d) increasing the supply of qualified accountingprofessionals; and (e) improving the management of accounting education.

2.3 A single project can only be viewed as a small part of a reform asfar-reaching as that outlined in para. 1.35. The entire process may well callfor successive projects involving further policy, structural and proceduralchanges over the next two decades. To give continuity of direction to thisprocess, the project provides for the guidance of special consultants ofeminence in the international profession of accountancy to be available to theGovernment (para. 2.40).

Project Description

2.4 Project components have been designed and grouped into two subproj-ects: Accounting Practice and Accounting Education. This grouping reflectsthe division of primary responsibility for project implementation within theGovernment of Indonesia, between MOF on the one hand and MOEC on the other(para. 2.38). Linking these two subprojects is a third (CAAD), which isconcerned with the administrative and logistical arrangements for maintainingcoordination between various project activities, and for planning anddesigning future stages of accounting development.

- 16 -

Accounting Practice

(US$57.9 million excluding contingencies)

2.5 Government Accounting Modernization (US$13.3 million, net ofcontingencies. In this component of the Accounting Practice subproject, astart would be made in implementing the modernized government accountingsystem which has been designed with the help of consultants (SGV-Utomo) fundedunder the Polytechnic Project (Cr. 869-IND) and the Polytechnic II Project(Ln. 2290-IND). The main changes to be introduced under the modernized systemare described in para. 1.35, above. The principal improvements to be effectedby this system are in control (through the introduction of double-entry book-keeping), consistency (by the establishment of a uniform chart of accounts andconsolidation of central accounting), and utility (by extending the financialreporting system to balance-sheet items as well as revenue and expenditureitems, and by introducing a functional classification of expenditures). Thenew government accountancy program involves four main accounting subsystems:

(a) the Central Accounting System for MOF. This system provides MOFwith the capability to produce reports of budget realization andstatements of assets, liabilities and fund equity in an accurate andtimely manner and without dependence on the prior completion ofreports by the agencies;

(b) the Central State Treasury Accounting System. This system willprovide MOF for the first time with centralized accounting for thewhole of government's cash resources;

(c) the Agency Accounting System. This system will provide agencymanagement with better information to monitor and control budgetimplementation, and in particular offers the capability to generateinformation at the program and project level; and

(d) the "Bagian Anggaran 16" System, which provides an accounting systemto cover the diverse activities of this set of budgets. (Seefootnote 11.)

2.6 A system test of the modernized government accountancy program (alsofunded under the Polytechnic II Project) was carried out in parallel with thepresent system during the period December 1987 through March 1988, followingwhich finxal refinements are being made to the system design and detailedimplementation plans are being drawn up. It is intended that implementationshould begin as soon as possible after the conclusion of the system test sothat that momentum will be maintained and the expertise of the staff trainedin the new system will not be lost. Implementation will begin in MOF and inthe agencies selected for the system test, which include certain directorates-general in the Ministries of Public Works, Trade and Social Affairs. Eachsucceeding year, implementation will begin in a further four agencies. Imple-mentation in each agency is expected to take 4-5 years to be fully effec-tive. The major tasks involved, and funded in this component of the project,are the preparation of the books and forms required, development of systemsoperation manuals, and training the staff in the new procedures. Consultants,

- 17 -

to be appointed at the conclusion of the system test, will undertake most of

the technical work under the direction of the Accounting Practice PIU

(para. 2.38). STA1 will be extensively involved in the training program; its

instructors will first be fully briefed on the new system, and will then

participate in training succeeding groups of staff as implementation

proceeds. Implementation of the new government accounting system requires the

authority of Instructions from the Minister of Finance. The implementation of

the modernized government accounting system will also involve organizational

changes in both the MOF and other agencies. The main features of these

changes have already been determined and comprise:

(a) the consolidation of central government accounting operations under

a Central Accounting Office;

(b) the consolidation of treasury operations under a Central State

Treasury and their separation from accounting; and

(c) the decentralization of agencies' basic bookkeeping.

Following the system test, the details of the revised organizational

arrangements will be finalized for implementation along with the new system.

At the same time, the extent of feasible and desirable computerization of the

new system will be evaluated; however, the system has been designed for, and

would be introduced with, lOOZ manual operation.

2.7 Assurances were obtained at negotiations that, on the basis of the

results of the systems test, the Government would prepare and submit to the

Bank for comment by December 31, 1988, a detailed program for implementation

of government accountancy modernization, including the organizational arrange-

ments and government Instructions necessary for implementaion. Following

consultation with the Bank, the Government would subsequently implement the

program in a manner satiefactory to the Bank.

2.8 The completion of implementation throughout all government agencies

will clearly require a time span much longer than that of the proposed proj-

ect. However, at the end of the first phase implementation covered by the

project, the groundwork will have been laid for a smooth extension of the

modernized accounting system. The Central Accounting Office will be directing

the installation and development of the system; the Central State Treasury

will be managing the Government's cash; key systems of budgetary and financial

reporting will be in place in MOF; and a number of other agencies will have

begun to use the new systems. The participating staff of these agencies will

constitute a core of trained and experienced staff for the succeeding phases

of implementation. It is intended that the State budget should be compiled on

the basis of the new chart of accounts for the year 1990/91, and that the

consolidated budget realization reports for that year and subsequent years

should be produced by MOF using the new system.

2.9 Government Auditing (US$15.7 million, net of contingencies). This

component is directed to improving the efficiency and effectiveness of the

overall government audit function. Improved efficiency implies less time

spent on the audit by both auditor and client, without loas of quality;

- 18 -

improved effectiveness calls for sharpening the focus of the audit process onvalue-for-money aspects such as reduction of waste, saving of cost, improvedmanagement of resources and more effective reporting. To this end, the big-gest part of this component (US$5.5 million excluding contingencies) comprisesin-country training for audit staff of BPK and BPKP; for this purpose BPKPwill also cater to the needs of Inspectorate-General and other central andregional audit agency staff. Almost 100 courses will be prepared anddelivered by BPK, BPKP and STAN lecturers; it is estimated that about 75Z ofthe agencies' 23,000 auditors will be reached. The courses will cover thedesign and conduct of audits in general and for -ific situations, as wellas modern tBchniques of auditing for both accountaoility and value-for-money.

2.10 Besides training at the staff level, this component also includes:

(a) for BPK and BPKP senior staff, attendance at short courses overseas;and

(b) for BPK, 13 masters and 2 doctoral programs overseas, and attendanceby selected senior staff at seminars and conferences sponeared bythe International and Asian Organizations of Supreme Audit Institu-tions (INTOSAI and ASOSAI).

Funding will be included in this component for the provision of specialistservices, enhanced training facilities and equipment in BPK and BPKP premises,including computers, visual aids, library equipment and textbooks.

2.11 Government Education and Training (US$20.1 million, net of contin-gencies). The project would provide assistance for the following fouractivities being undertaken by STAN:

(a) the provision of equipment, books, and materials for STAN's newsuburban Jakarta campus now being readied for full scaleoperation;

(b) the regular STAN preservice accountancy diploma programs (Dip. IIIand Dip. IV);

(c) the ongoing inservice educational programs for internal auditors ingovernment and state corporations and for government auditors in BPKand BPKP, managed by the ADC located in STAN. These c yses wouldbe expanded to cover about 21,000 course participants - during thefive-year period, as compared with a total of about 3,350 courseparticipants from 1980 through November 1986; in preparation forthis training, 154 instructors (64 from STAN, 60 from BPKP, and 30from BPK) would be trained for a period of 22 days; and

13/ The figure covers approximately 3,250 employees, most of whom wouldparticipate in several courses.

- 19 -

(d) a planned comprehensive inservice training program for government

accountants and auditors covering the new government accountingpractices. During the project period, this program would cover

about half of an estimated 36,000 accounting personnel Icentral,regional and local government offices needing training._

Regarding the diploma programs, the component would emphasize quality improve-

ment through procurement of teaching and administration equipment, personnel

development programs, technical assistance, revision of syllabi, production

and procurement of teaching materials, books and journals, and three research

activities covering needs assessment. The quality of the programs mentioned

under (b) and (c) would also benefit from the input of equipment, staff devel-

opment activities, technical assistance, library materials, and the research

activities mentioned above.

2.12 The procurement of equipment would provide STAN with computers

including peripherals and furniture for teaching, administration and library,

audiovisual teaching equipment and reproduction facilities. The staff devel-

opment programs would include a series of 60 seminars, short domestic courses

(1,100 staff-days in total), short overseas courses and study visits (about 95

staff-months) and fellowships for overseas advanced degrees (115 staff-years

covering 45 fellowships for master's-degree programs, including 15 fellowships

for BPKP, and 5 fellows for doctorate programs). Upon completion of overseas

studies, the graduates would return to teach and supervise other teachers at

the STA ,which at present employs only 10 full-time teachers out of a total

of 155, Foreign technical assistance would total about 11 person-years,

including 5 person-years of general assistance within management and educa-

tional development activities, and 6 person-years of more specialized assist-

ance in syllabus and course revision within computer auditing and value-for-

money auditing. Local experts would be employed in the field of development,

management and administration of computer systems. Implementation of programs

would be carried out within a framework of the minimum curriculum prescribed

by MOEC.

2.13 Capital Markets (US$3.2 million, net of contingencies). This compo-

nent will assist the Capital Market Executive Agency (BAPEPAM) and the Stock-

brokers' Association in arresting the declining volume of business on the

exchange, and in promoting the capital market as an effective instrument of

resource mobilization. The services of a specialist advisor (about 10 consul-

tant person-months) would be retained to examine the present structure and

operations of the market and advise on legislative and administrative measures

necessary to secure a high level of confidence in the integrity and efficiency

of the exchange on the part of investors (including potential foreign inves-

tors), and to broaden its utility to Indonesian companies as a source of

finance. The specialist advisor would also monitor the implementation of

14/ The figures are exclusive of information sessions for management and

users.

15/ The long-term target is 45 full-time teachers.

- 20 -

specific subcomponents designed to: (a) consolidate and clarify the law andregulations governing the conduct of the capital markets; and (b) establishreporting standards for prospectuses and annual reports of listed companies.The project provides the technical assistance required by BAPEPAM's own staffto research and complete these tasks. Finally, the project provides for staffof BAPEPAN (and of PT Danareksa and of the Money and Securities Traders' Asso-ciation members where appropriate) to be trained by foreign experts in modernstock exchange practices.

2.14 Private Sector (US$2.1 million, net of contingencies). This compo-nent is designed principally to assist the Indonesian Institute of Accountants(IAI) in its evolution towards leadership of the accountancy profession inIndonesia. Apart from a small secretariat, the IAI is dependent on the part-time service of its officers. This component will provide technical assis-tance (about 150 consultant person-months) to support the ongoing efforts ofvarious committees of IAI to: (a) formulate and promulgate a number ofaccounting and auditing standards; (b) develop a program of continuing profes-sional education for accounting practitioners; and (c) establish a code ofethics and a quality control mechanism for accountants in public practice. Tohelp establish the IAI as a source of assistance to the business community,packages will be developed to meet the needs of small businesses for account-ing, costing, banking and taxation systems.

2.15 The accounting standards [para. 2.14(a)J will form the basis formore consistent financial reporting by private sector businesses, and will beharmonized to the extent possible with International Accounting Standards. Ameans of enforcing compliance with these standards is clearly desirable, andfor the time being this can be found in the Indonesian tax law. By article28(4) of the General Provisions and Procedure on Taxes (1983), the Minister ofFinance is empowered to issue regulations as to the accounts to be filed bycompanies for tax purposes.

2.16 In the longer term, the Government is considering strengthening theregulation of companies and improving the statistical base on industrialactivities in Indonesia by instituting some form of companies' registry andrequiring certain information to be reported to the registry on a regularbasis by all Indonesian companies. A feasibility study for this purpose isincluded in the private sector component of the project. This will includethe review of similar arrangements in other countries, and the development ofspecifications for the information systems necessary to support statutoryreporting.

2.17 As with government accounting modernization (para. 2.8), the devel-opment and strengthening of accountancy standards and practices in the privatesector clearly requires a timeframe longer than that of the proposed project.The project is designed to provide a sound basis for future development byestablishing certain fundamental accounting principles for all financialreporting, and a mechanism for their enforcement; by preparing for the intro-duction of more systematic business reporting and monitoring; and by assistingIAI to equip itself to direct the practice of accountancy in Indonesia withthe authority and independence required of a professional institution.

- 21 -

2.18 Subproject Management (US$3.5 million, net of contingencies). This

component includes various activities to facilitate implementation of the five

components under the Accounting Practice subproject. Activities include

(a) coordination of overseas degree and nondegree fellowship programs includ-

ing selection of fellows, arrangements for pre-departure training, placement

and reintegration of the fellows upon completion of the programs; (b) coordi-

nation of procurement of equipment and technical assistance, including prep-

aration of bidding documents, tendering, evaluation, contract administration;

(c) financial management and administration including preparation of annual

plans of activities and budget, maintenance of subproject accounts and loan

disbursement accounts; and (d) monitoring, evaluation and reporting. To

support these activities, the project would provide for specialist services

(13 local consultant person-years and 11 foreign consultant person-years), and

related equipment and incremental operating cost!

Accounting Education

(US$81.1 million excluding contingencies)

2.19 This subproject would assist the Government to improve the quality

of accounting manpower by the provision of assistance to accounting education

in the following subsectors of public and private education: (a) Higher Edu-

cation, (b) Upper Secondary Commercial Education, (c) Upper Secondary General

Education, and (d) Nonformal (Adult) Education. The assistance would include

technical assistance, personnel development, procurement of teaching equipment

and materials, research, establishment of capacity for teacher training and

long-term development of accounting education, fellowships to train accounting

teachers and loan programs for institutions and students in nonformal educa-

tion. The improved quality of the training programs would eventually permit

expansion of accountancy enrollments.

2.20 Accounting Education in Higher Education (US$24.4 million, net of

contingencies). Assistance to accountancy education in the higher education

subsector will emphasize efforts to improve quality rather than to expand

undergraduate capacity, but a limited enrollment increase will result from a

general system expansion. The structure for accountancy development in higher

education comprises 18 institutions arrayed in three groups (Annex 1). A

cascade approach will be employed with more mature universities assisting less

developed institutions. The top group comprises three institutions, UGM, UI,

and USU. They are classed as "assisting" universities because they are

expected to provide staff and curriculum development programs for the

others. These q7tain three of the four existing Accountancy DevelopmentCenters (ADCs).- The only ex.sting S-2 (master's degree) program is located

at UGH and the proposed second S-2 program is to be established at UI. A

second group of three universities, Padjadjarah, Airlangga and Brawijaya,

comprises the next level. These will be the location of the three new ADCs to

be launched under the project. They will also assist less-mature universities

of level three.

16/ The remaining existing ADC is located at STAN (para. 2.11).

- 22 -

2.21 Since the quality of higher education is dependent upon facultyperformance more than any other factor, an extensive p:agram of staff develop-ment is the cornerstone of this subcomponent. Overall 725 individuals will beprovided various forms of education and training ranging from the doctorateabroad to two-month local nondegree upgrading courses (Annex 2). In order toincrease the future supply of potential faculty in accounting, 100 local fel-lowships will be made available to outstanding undergraduate students. Fel-lows will be selected on the basis of thei' performance in their first orsecond year of study and their financial support will continue for the remain-der of their university period, about 3 years in most cases. A bondingarrangement will be used which will assure a reasonable period of universityteaching after graduation. Efforts will be made to have fellows serve in thenewly developed accountancy departments. Expatriate and local specialistswill be employed in the higher education program. Expatriate professors willbe engaged to teach in and render advice to the accountancy departments of UIand UGM where graduate level instruction is planned. Local consultants willbe used in the university affiliation program (para. 2.20). Local computermanagers will be engaged to serve in the 18 universities which will receivecomputers under the project (para 2.23).