Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-7286-ZA

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL DEVELOPMENT ASSOCIATION

TO THE

EXECUTIVE DIRECTORS

ON A PROPOSED CREDIT

IN THE AMOUNT EQUIVALENT TO SDR 122.7 MILLION

TO THE

REPUBLIC OF ZAMBIA

FOR A

PUBLIC SECTOR REFORM AND EXPORT PROMOTION CREDIT

December 30, 1998

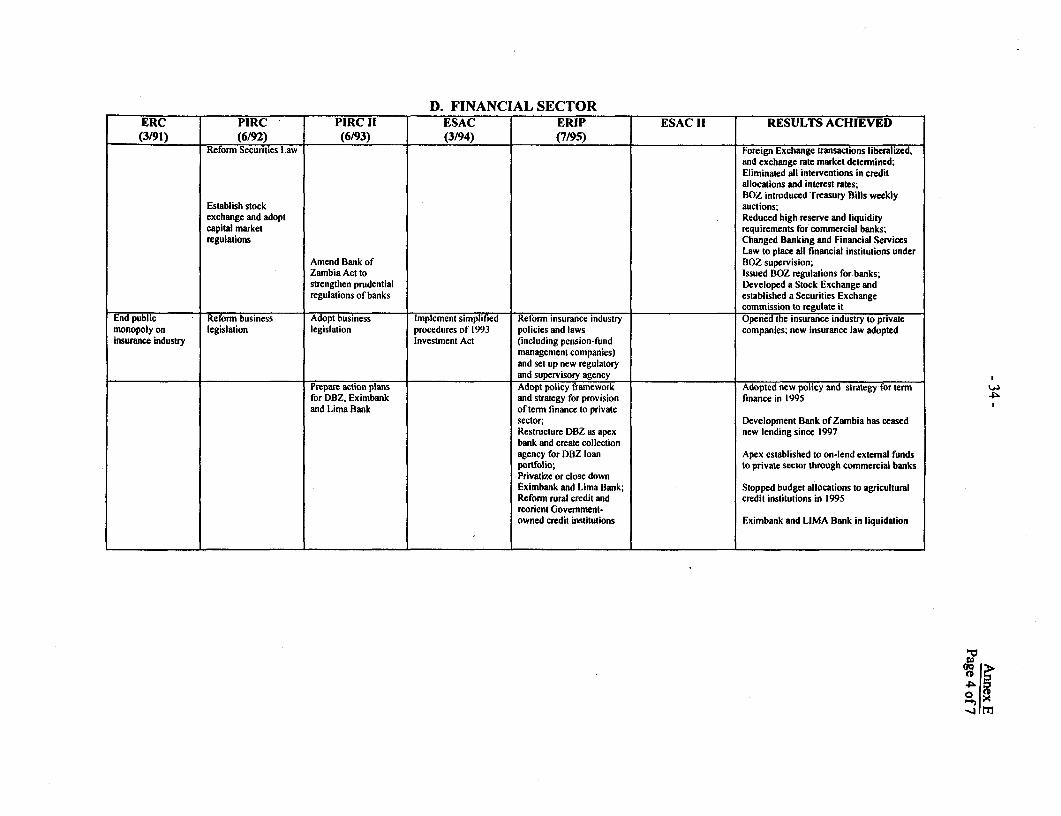

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

Pub

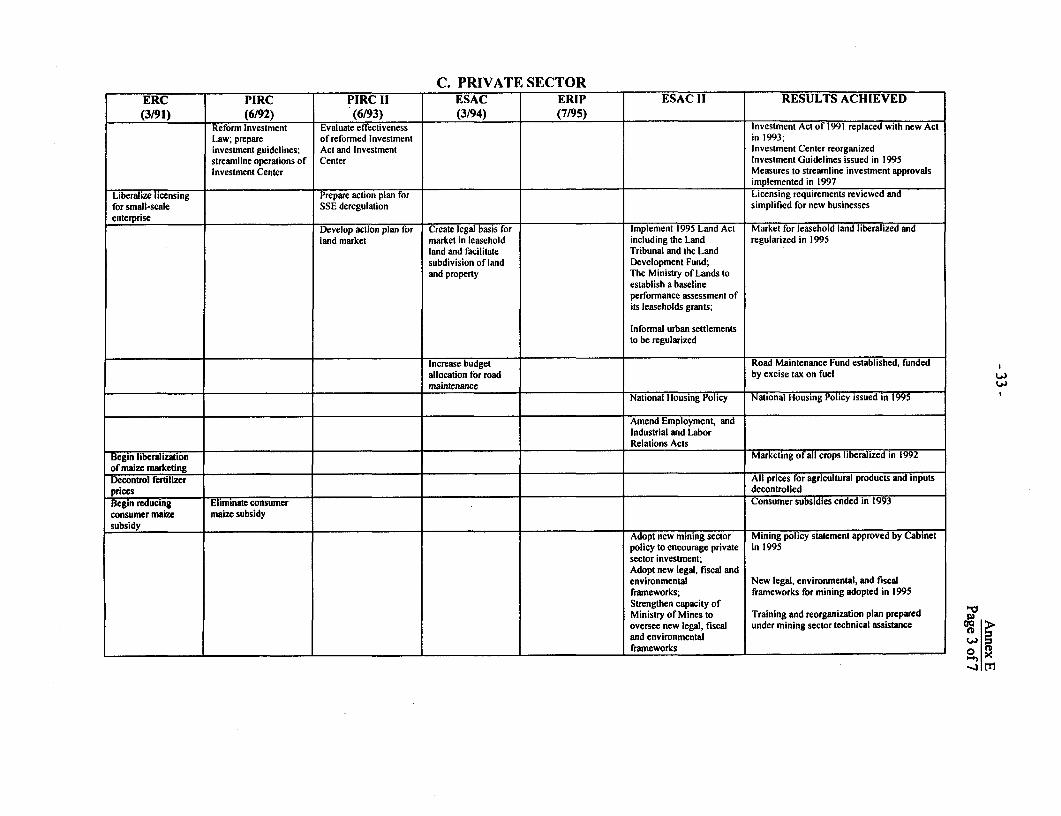

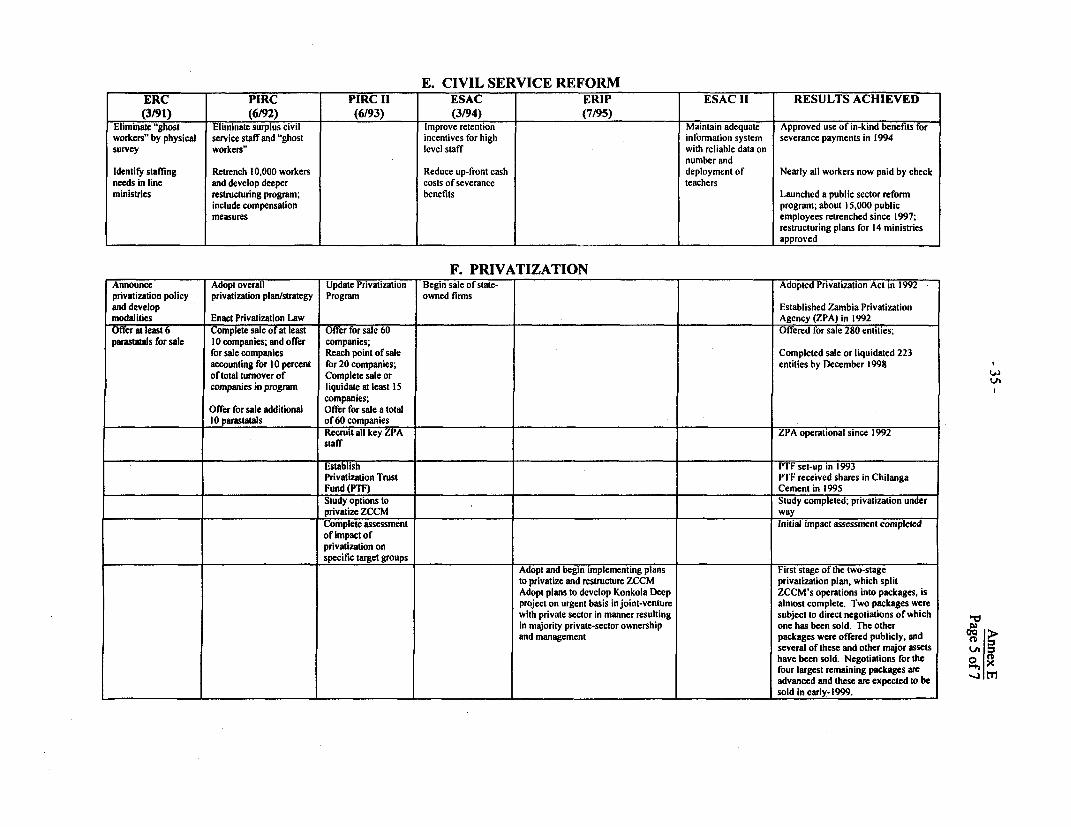

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

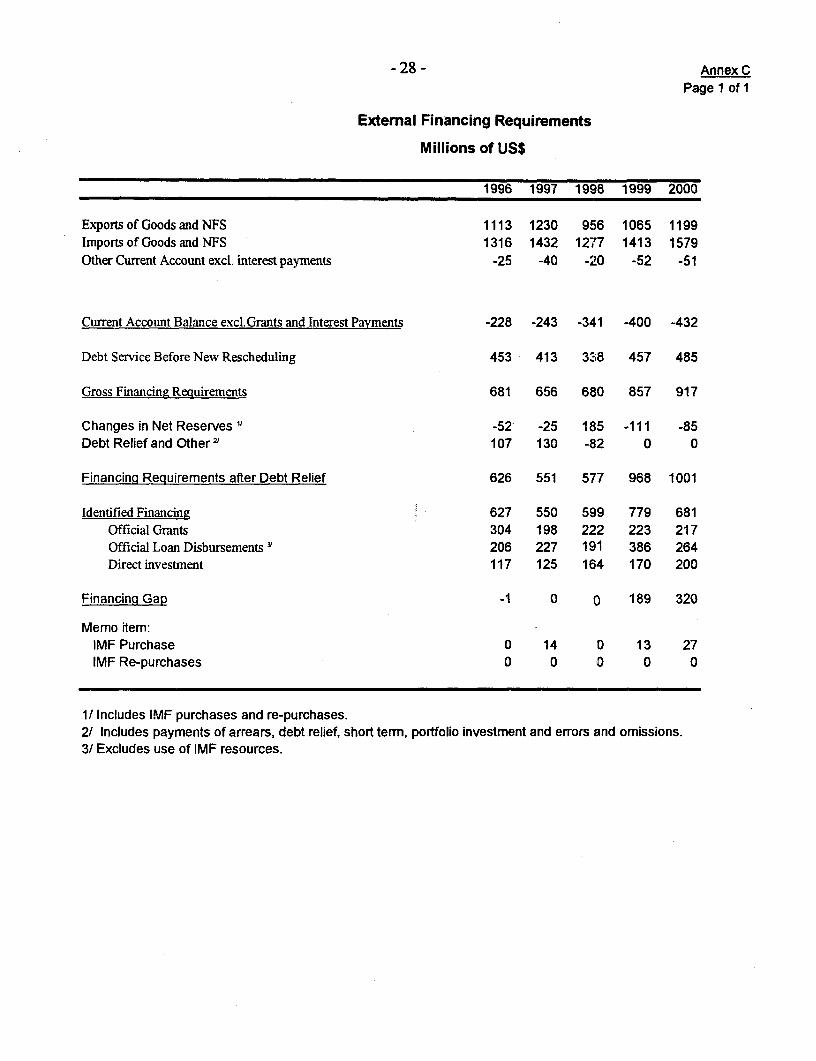

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

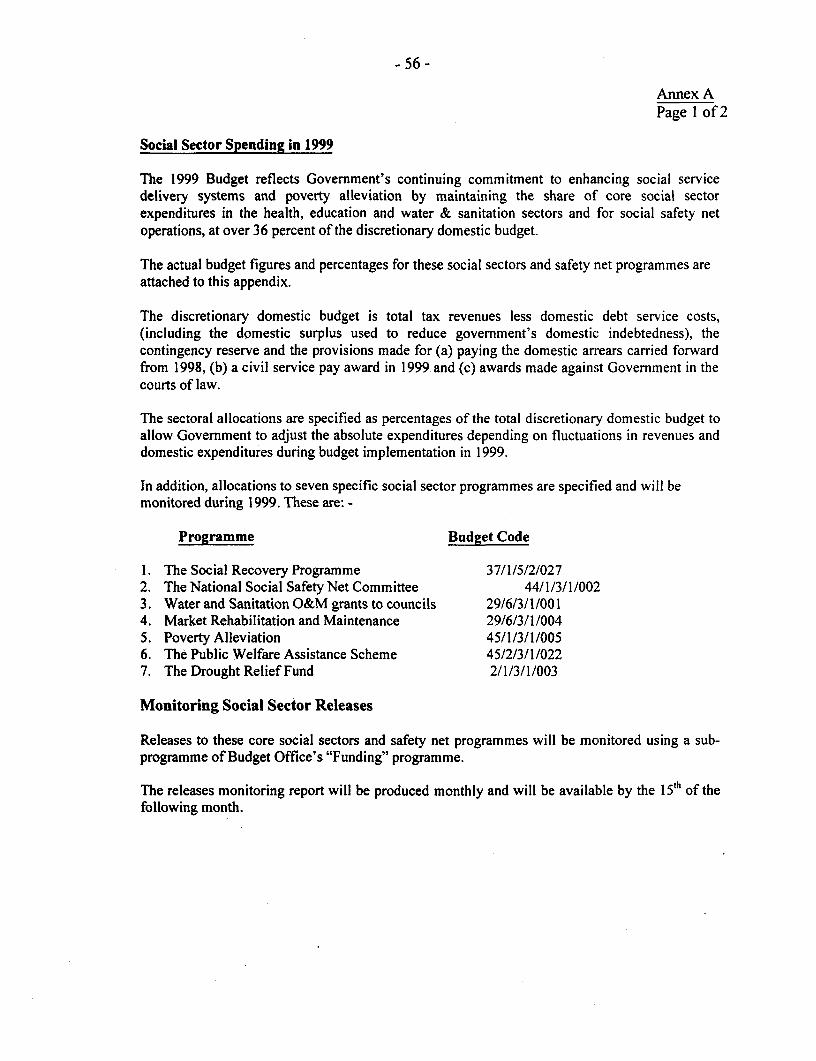

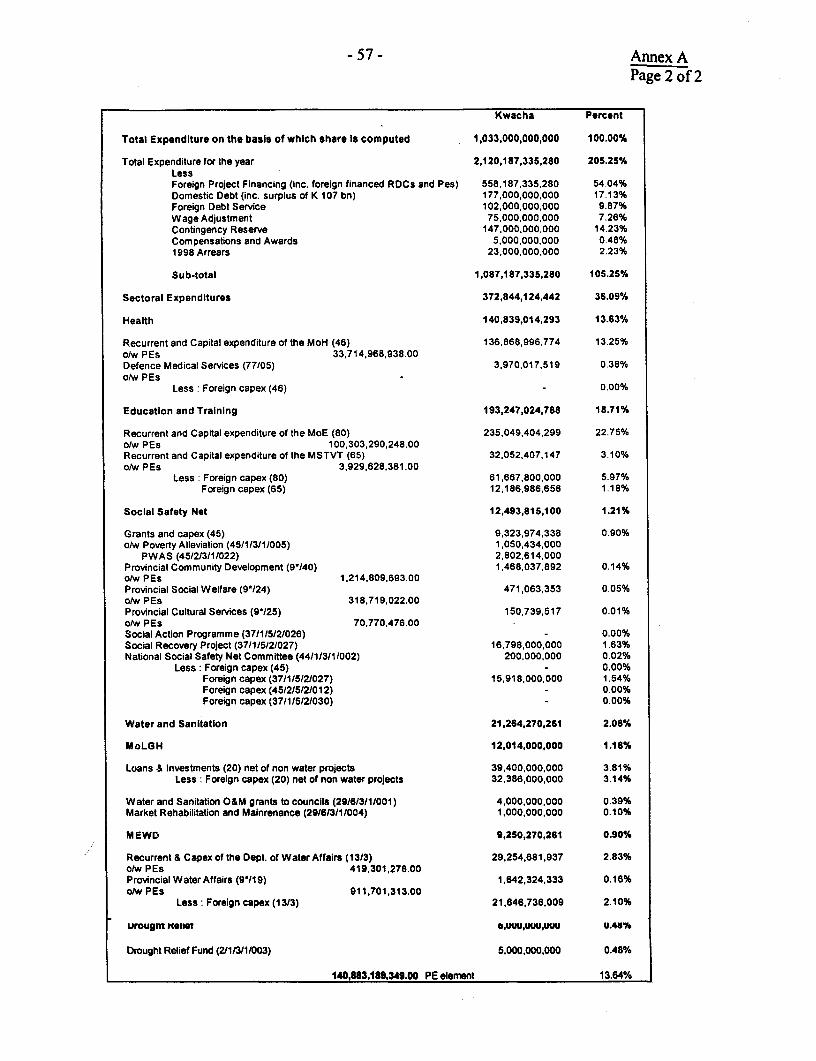

iscl

osur

e A

utho

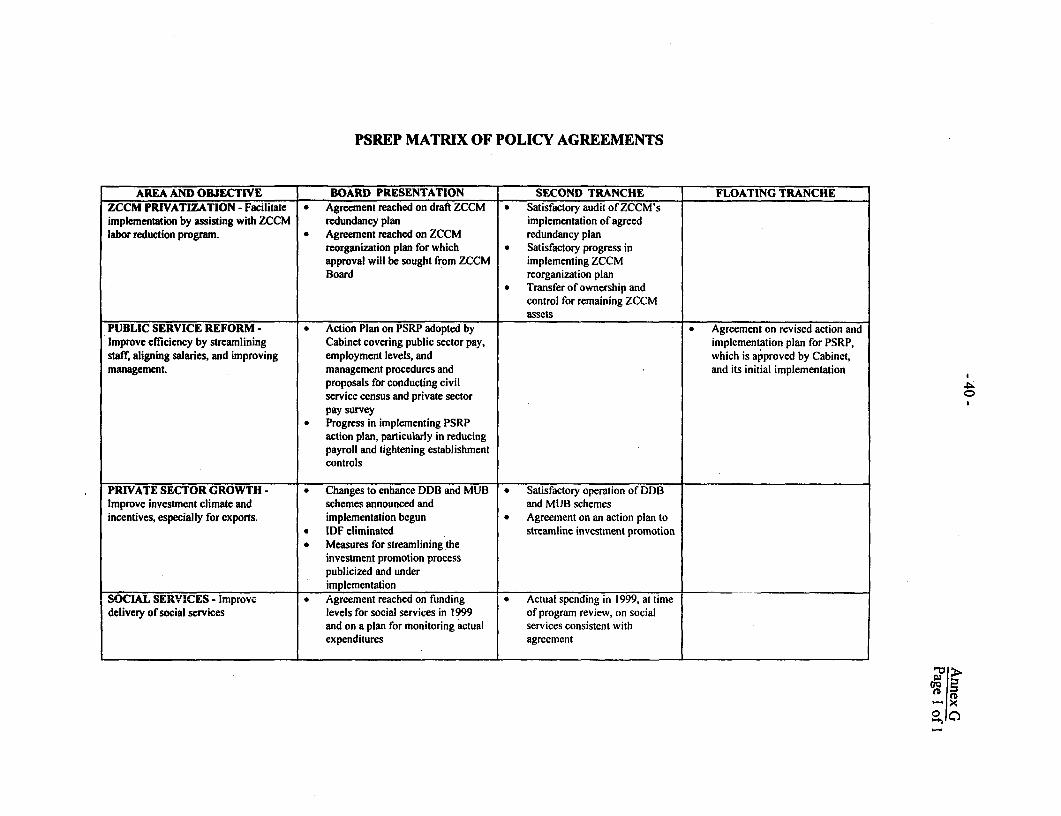

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit: Zambia Kwacha (K)US$ 1=2,33 7.95

FISCAL YEARJanuary 1 to December 31

ABBREVIATIONS AND ACRONYMSAAC Anglo-American CorporationBOZ Bank of ZambiaBW Bonded WarehouseCOMESA Common Market for Eastern and Southern AfricaCPI Consumer Price InflationDDB Duty DrawbackERC Economic Recovery CreditERIPTA Economic Recovery and Investment Promotion Technical Assistance CreditESAC Economic and Social Adjustment CreditESAF Enhanced Structural Adjustment FacilityHIPC Highly Indebted Poor CountriesIDA International Development AssociationIDF Import Declaration FeeIMF International Monetary FundMCDSS Ministry of Community Development and Social ServicesMMD Movement for Multiparty DemocracyMOU Memorandum of UnderstandingMUB Manufacturing-under-EBondNFNC National Food and Nutrition CommissionNGO Non-Governmental OrganizationPER Public Expenditure ReviewPFP Policy Framework PaperPIRC Privatization and Industrial Reform CreditsPSRP Public Sector Reform ProgramPWAS Public Welfare Assistance SchemeSAF Structural Adjustment FacilitySIP Sector Investment ProgramSPA Special Program of AssistanceUNDP United Nations Development ProgramZCCM Zambia Consolidated Copper MinesZPA Zambia Privatization Agency

Vice President: Callisto E. MadavoCountry Director: Phyllis PomerantzSector Manager: Ataman AksoyTask Team Leader: Sudhir Shetty

FOR OFFICIAL USE ONLYZAMBL4

PUBLIC SECTOR REFORMAND EXPORTPROMOTION CREDIT

Table of Contents

L. THE ECONOMY ...................................... 1

A. BACKGROUND ..................................... IB. RECENT DEVELOPMENTS AND PROSPECTS ..................................... 2

II. ZAMBIA'SADJUSTMENT PROGRAM ..................................... 4

A. MACROECONOMIC MANAGEMENT ..................................... 5B. PRIVATIZITIONANDPARASTATALMANAGEMENT ..................................... 6C. IMPROVINGPUBLICSERVICES ..................................... 8D. FOSTERING PRIVATESECTOR GROWTH ..................................... 9E. MEDIUM TERMPROSPECTSAND FINANCING PLAN ...................................... I.I

IM. THE PROPOSED CREDIT .................................. 11

A. SUPPORTING ZCCM PRIVATIZATION ............................ 12B. PUBLIC SERVICE REFORM ............................ 13C. INVESTMENTAND EXPORT PROMOTION .......................................... 1... 14D. SOCIAL SERVICES ............................... 15E. POVERTYIMPACT .............................. I 6F. ENVIRONMENTAL IMPACT ............................... 17G. SPECIFIC AGREEMENTS ............................... 17H. IMPLEMENTA TiON ARRANGEMENTS ............................ .. 18. IMPLEMENTA TION ASSISTANCE .............................. 1 8

J. COFINANCING .............................. 1 9K. PROGRAM BENEFITS ANDRISKS ..............................R. 19

IV. BANKOPERATIONS .............................. 19

V. COLLABORATION WITH IMF .............................. 21

VI. RECOMMENDA TION .............................. 22

A .NNEXES .............................. 23

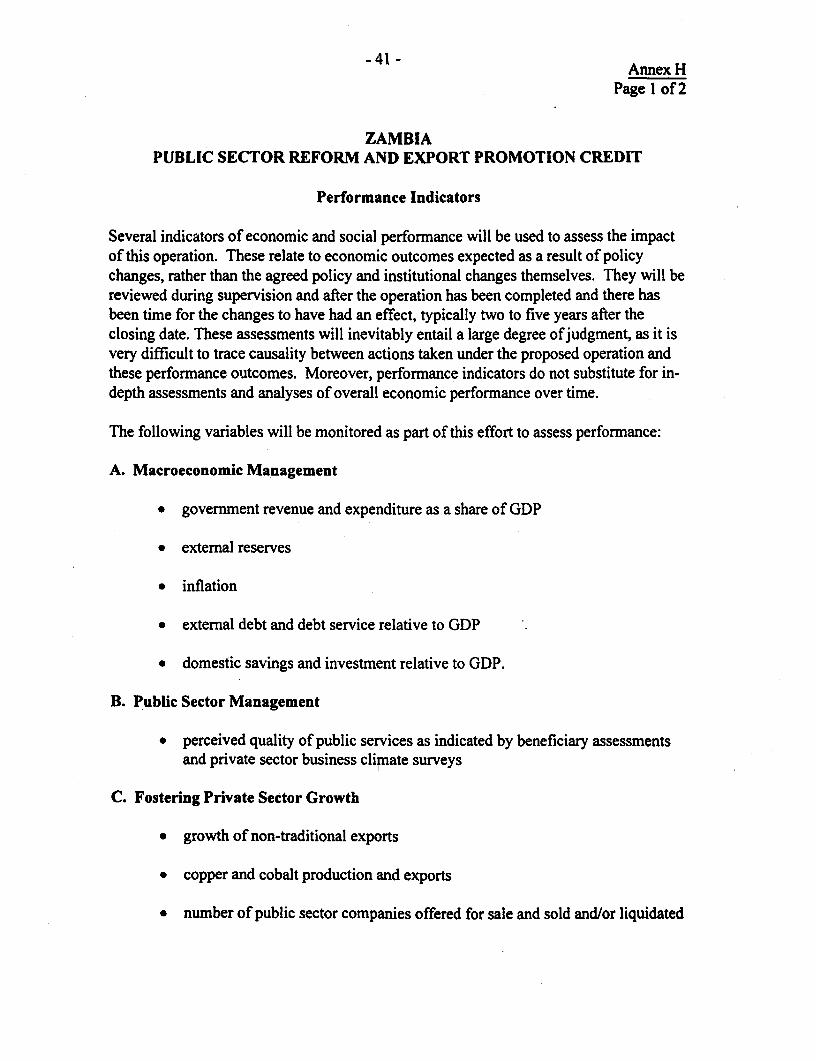

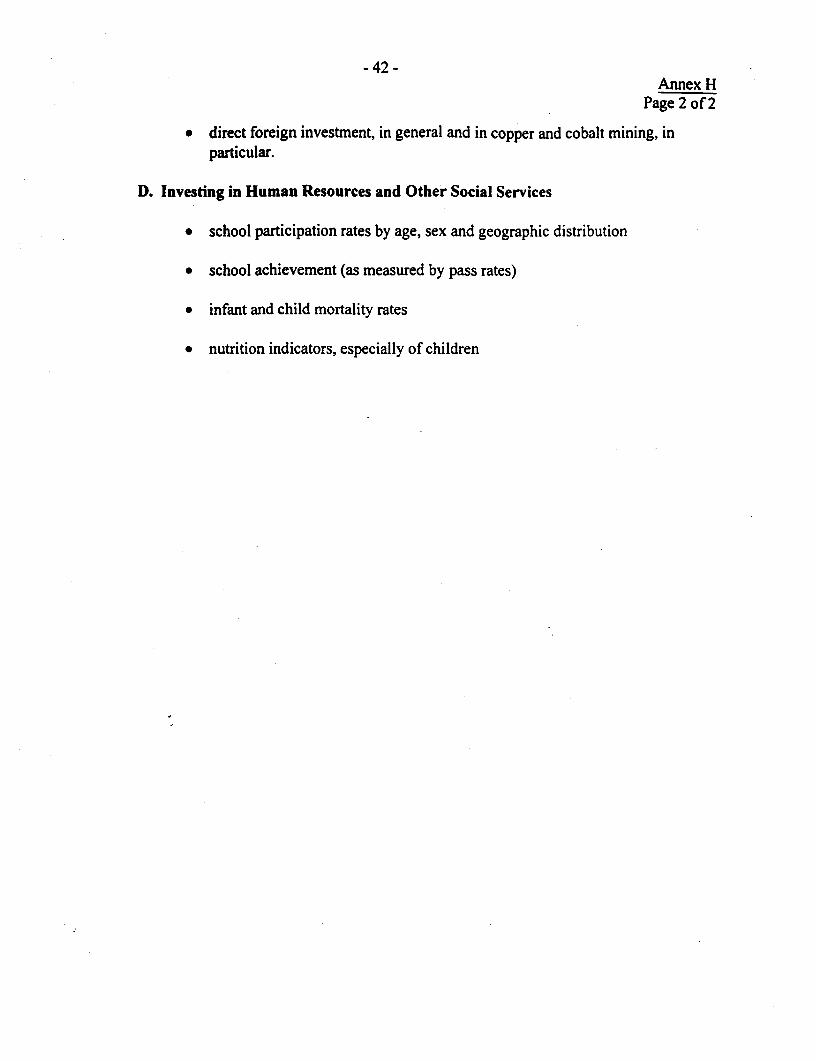

A. SOCIAL INDICATORS OF DEVELOPMENTB. KEY ECONOMIC INDICATORSC. EXTERNAL FINANCING REQUIREMENTSD. STATUS OF BANK GROUP OPERATIONSE. EVOLUTION OF POLICY REFORM AGREEMENTSF. ZAMBIA AT A GLANCEG. MATRIX OF POLICY AGREEMENTSH. PERFORMANCE INDICATORS1. LETrER OF DEVELOPMENT POLICY

This operation was prepared by a team consisting of Sudhir Shetty (Principal Economist and TaskManager, AFTM I); Emile Sawaya (Principal Private Sector Specialist, AFTPI); Charles Husband (SeniorFinancial Analyst, EMTIE); Harry Gamett (Senior Public Management Specialist, AFT12); John Todd(Principal Economist, SRMSG); Hinh Dinh (Principal Economist, AFTM I), Aberra Zerabruk (SeniorCounsel, LEGAF); Said Al-Habsy (Senior Counsel, LEGAF), Steve Gaginis (Disbursement Officer,LOAAF), Ligia Murphy (Senior Task Team Assistant, AFTM 1) and Kendall Schaefer (Research Analyst,AFTMI)

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

ZAMBIA

PUBLIC SECTOR REFORM AND EXPORT PROMOTION CREDIT

SUMMARY

Borrower: Republic of Zambia

Executing Agency: Ministry of Finance

Amount and Terms: SDR 122.7 million (US$170 million equivalent) on standardIDA terms with 40 years maturity.

Description: The proposed adjustment Credit would support Zambia'seconomic reform program, which aims at reducing thewidespread poverty by promoting broadly-shared, privatesector-led growth and improving the delivery of vital socialservices. In particular, the proposed Credit would supportmeasures that would: (a) facilitate completion of theprivatization of the copper parastatal, ZCCM, by assisting in itslabor reduction program; (b) improve the performance of thepublic service by reforming pay and employment practices andimproving management controls; (c) promote privateinvestment, particularly in export-oriented activity, byimproving access to imported inputs and streamlininginvestment approvals and, (d) strengthen the delivery of socialservices by monitoring budget allocations to key socialexpenditure categories and supporting key policy reforms.

Benefits: The main benefits of this Credit will be faster economicgrowth, employment creation, and poverty reduction arisingfrom a more efficient and effective public sector (ZCCMprivatization and public service reforms), a more competitiveprivate sector and fewer barriers to investment (ZCCMprivatization and trade and investment reforms), mitigation ofthe adverse impacts of ZCCM privatization (support to itslabor reduction program), and more effective social servicedelivery and safety net provisions (monitoring of budgetallocations and social service policy reforms). These changeswould benefit all groups in the population, including thepoorest. They would also provide the basis for sustainingmacroeconomic stability and the expansion and diversificationof exports. Consequently, Zambia's prospects for sustainablemedium-term growth would be enhanced.

- ii -

Risks: There are two broad categories of risk. First, it is possible thatthe Government's reform program could falter due to policyreversal, the impact of major external shocks, or a continuingshortfall in external donor support due to either economic orgovernance related concerns. The commitment of theGovernment to economic reforms has been steadfast even inthe face of adverse external conditions, including the recentcollapse in copper prices. Completion of the privatization ofZCCM, and efforts to expand non-mining exports would alsohelp withstand the effects of adverse external shocks. TheGovernment has committed to continuing the dialogue withdonors on governance-related issues, and developments in thisarea will be closely monitored. The second set of risks relateto the reforms supported by this Credit. The risk that the saleof the remaining core ZCCM assets could be delayed beyondmid-1999 is mitigated by the detailed agreemnents that havebeen reached. And, the risk that the agenda and timetable forpublic service reforms could pose political problems ismitigated by the Government's continuing consultations withall major stakeholders during program formulation andimplementation as well as its reliance on continued supportfrom the Bank and other external partners.

Disbursement: The proposed Credit will be disbursed through the Bank ofZambia. Disbursement will be in three tranches. The firsttranche (US$65 million) will be released at effectiveness. Thefloating tranche (US$40 million) will be released when thespecific conditions related to public service reform aresatisfied. The second tranche (US$65 million) will bedisbursed when the specific conditions associated with itsrelease are met, which is expected to be around May 1999.

Project ID Number: ZM-PA-35641

INTERNATIONAL DEVELOPMENTASSOCIA TIONREPORTAND RECOMMENDATION OF THE PRESIDENT

TO THE EXECUTIVE DIRECTORSONA PROPOSED

PUBLIC SECTOR REFORMAND EXPORTPROMOTION CREDITTO THE REPUBLIC OF ZAMBIA

1. I submit for your approval the following report and recommendation on aproposed development credit to the Republic of Zambia for SDR 122.7 million (US$170million equivalent) in support of its economic reform program. The Credit would be onstandard IDA terms, with an amortization period of 40 years, including a grace period of10 years.

2. The proposed Public Sector Reform Export Promotion Credit (PSREP) would bethe seventh structural adjustment credit to Zambia since the clearance of its arrears to theBank in March 1991. Zambia continues to face very large external financing needs dueto its high debt service requirements and the steep decline in the price of its principalexport--copper. In recognition of this need and of the accomplishments of Zambia'seconomic reform program, the international community provided exceptional levels ofbalance of payments support between 1991 and 1997. The objective of this Credit is tocontinue IDA's support of Zambia's program of economic reform, which aims to reducethe widespread poverty in Zambia through measures aimed at promoting broadly-shared,private sector-led growth and improving the delivery of vital social services. Inparticular, the proposed Credit would support measures to: (a) facilitate completion ofthe privatization of the copper parastatal, ZCCM, by assisting in its labor reductionprogram; (b) improve the performance of the public service by reforming pay andemployment practices and strengthening management controls; (c) promote privateinvestment, particularly in export-oriented activity, by improving access to importedinputs and streamlining the investment approval process; and (d) strengthen the deliveryof social services by monitoring budget allocations to key social expenditure categoriesand supporting the implementation of selected policy reforms.

I. THE ECONOMY

A. BACKGROUND

3. From Independence in 1964 through the 1980s, Zambia relied on a developmentstrategy that emphasized central planning, public ownership, and foreign borrowing. Theeconomy's performance was also adversely affected throughout this period by the heavydependence on copper, despite its falling real price and declining production as a result ofinsufficient investment. Zambia undertook several partial economic reform programsduring the 1980s, but these had little lasting effect (except to increase the national debt).When elections were called in late- 1991, Zambia was suffering from a large external debtoverhang (over US$7 billion), an inefficient and highly protected parastatal sector that

- 2 -

dominated the economy, continued dependence on copper, steadily declining per capitaincome (half its 1975 level), and an unwillingness on the part of its government to holdthe course on difficult but necessary policy reforms. The election of the opposition party,the Movement for Multiparty Democracy (MMD), was seen as an overwhelmingendorsement of its economic reform program. Its objectives were to restore internal andexternal balance, to reduce public sector involvement in business activity, and to focusgovernment efforts on establishing the enabling environment for the private sector and onproviding the necessary infrastructure and social services.

4. Zambia's overall economic policy performance has been good since the reformprogram was initiated in 1991. In particular, the pace of liberalization and decontrol hasbeen impressive. Prices were decontrolled and subsidies eliminated; the exchange rateand interest rates are now market determined; quantitative restrictions on imports havebeen eliminated; and, import tariffs have been reduced and their structure simplified.Parastatal monopolies have ended, crop marketing has been liberalized, and an ambitiousprivatization program has made impressive progress. Not everything has gone smoothly,however. It took several years for the high rates of inflation to be brought down, andmacroeconomic stability, including consistently low inflation rates, is still to be fullyachieved. Structural reforms also remain incomplete, particularly where institutionalchanges are required, as with public service reform. And, the investment and outputresponse to these reforms has been muted by high real interest rates, continueddeterioration in the performance of the copper mines, a series of droughts, and aidshortfalls. Although growth resumed in 1996 and 1997, the delay in privatizing thecopper mines, the fall in world copper prices, and the continued suspension of bilateralbalance of payments support have tested the Government's commitment to the reformprogram and its ability to keep the program on track in 1998. Despite these challenges,understandings have been reached at the staff level with the IMF on a policy program tobe supported by a three-year ESAF arrangement for 1999-2001.

B. RECENTDEVELOPMENTS AND PROSPECTS

5. The Government's economic reform program has remained on course since thesecond half of 1996 despite much lower external assistance than anticipated. Bilateraldonors initially suspended balance of payments assistance in June 1996, largely inresponse to concerns about the proposed conduct of presidential elections later that year.This hiatus extended into 1997 and 1998 in response to continued concerns aboutpolitical governance. In 1998, multilateral balance of payments support was also held updue to the delays in privatizing ZCCM. Consequently, external program support, whichwas only US$141 million in 1996 (less than half the original estimate), was even lower in1997 (US$120 million), and was negligible in 1998.

6. Despite the drop in external assistance, economic performance was encouragingin 1997, and by the end of the year, it looked like Zambia was well placed to movebeyond stabilization to deepening the structural reforms needed to accelerate growth.Although GDP growth slowed to 3.5 percent (from 6.5 percent in 1996), due to a poormaize harvest and a fall in metals production, it was the first time since 1989 that GDP

- 3 -

had grown in consecutive years. Non-metal exports continued their impressive growth --about 30 percent in 1997 and over 25 percent p.a. since 1994. And, inflation continued todecline, with the twelve-month CPI inflation rate falling from 35 percent at end-1996 toless than 19 percent at end- 1997. The tight fiscal and monetary policy stance that wasmaintained during much of 1997 contributed to this reduction in inflation. The overallcentral government deficit (on a cash basis) was reduced to about 1.9 percent of GDP(from 2.5 percent of GDP in 1996), while a domestic budget surplus (on a cash basis, andexcluding grants, external interest payments and foreign-financed capital expenditures) ofabout 1.2 percent of GDP was registered. Tight financial policies also helped curbimports, and despite the fall in copper prices in the second half of 1997, the trade deficitfell. But, the current account deficit widened to 5.5 percent of GDP (from 3.6 percent in1996) due to a fall in net transfers and a deterioration in the services account.

7. However, a combination of adverse shocks -- internal and external -- has slowedthe economy and worsened external and internal imbalances during the past year. Copperprices have fallen by almost 25 percent since mid-1997, while ZCCM's operational andfinancial problems and the delay in completing its privatization have reduced copperproduction and exports. This decline in the copper mining sector has hurt other sectors ofthe economy, and combined with the weather-related decline in maize production, GDPis estimated to have contracted in 1998 by about 2 percent. The fall in foreign exchangeearnings from copper exports (of over 27 percent) has been exacerbated by the fall innon-traditional exports. Combined with the lack of balance of payments support, thesefactors have resulted in the Kwacha depreciating in nominal terms by over 50 percent in1998, while official foreign exchange reserves fell from about 2 months of imports atend- 1 997 to less than 2 weeks of imports by end-November 1998. The current accountdeficit (after transfers) worsened to over 9 percent of GDP. Meanwhile, average annualinflation rose to almost 30 percent by end-November 1998. Although efforts were madeto maintain a tight fiscal stance in 1998, the lack of balance of payment support meantthat the domestic fiscal balance and the overall central government deficit deteriorated in1998. The decline in confidence in the Kwacha since late- 1997 has been reflected in therapid growth of foreign currency deposits as a share of broad money while the easing ofmonetary policy in late-1997 also led to an expansion of credit growth.

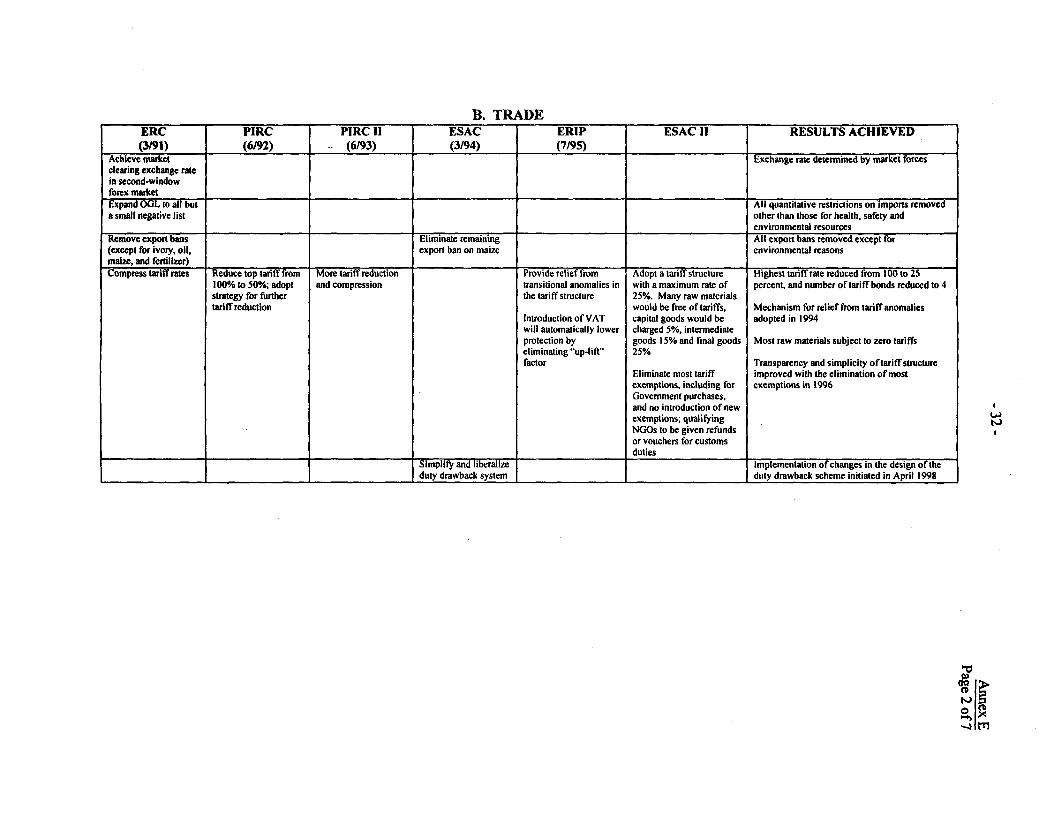

8. Progress on structural reform has been most substantial in recent years onprivatization and trade policy. By December 1998, almost 80 percent of the 280 non-mining public enterprises slated for divestiture had been privatized or liquidated. Theprivatization of the publicly-owned copper company, ZCCM, suffered a setback in mid-1998 when an international consortium withdrew from negotiations on the sale of thelargest asset package, but this process has moved ahead with an agreement in Decemberto sell these assets to other buyers. With the trade policy reforms since 1995, includingthe elimination of the 5 percent Import Declaration Fee in July 1998, Zambia now has atrade regime that is one of the most outward oriented in the sub-region.

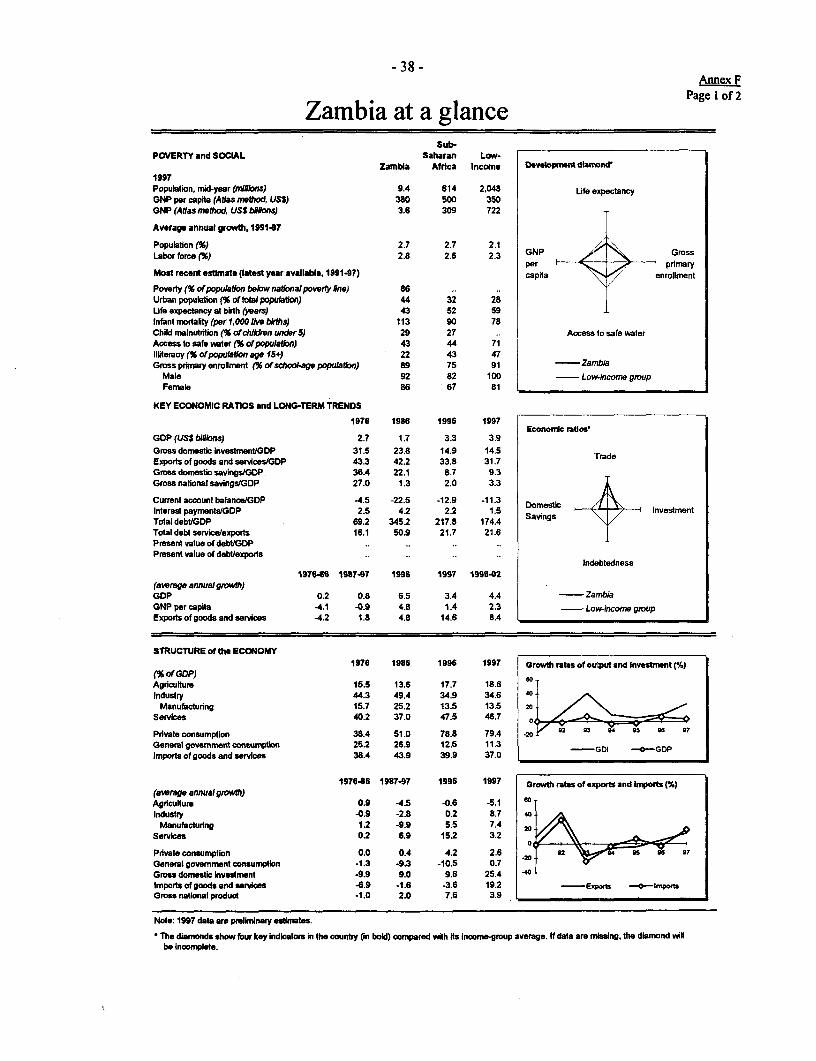

9. The incidence of poverty in Zambia remains high, reflecting the collapse of thecopper industry and the residual effects of the economic mismanagement of the 1970sand 1980s. In 1991, about 70 percent of all Zambians were living in poverty with 58percent of the population lacking sufficient income even to meet basic nutritional needs.

-4 -

Recent data show a slight decrease in poverty. After increasing to about 74 percent in1993, poverty incidence fell to about 69 percent in 1996 with decreases in rural and urbanpoverty between 1991 and 1996. The depth and severity of poverty also declined duringthis period. Rural poverty still remains more widespread and more severe than urbanpoverty. Most social indicators mirror the high incidence of poverty. Infant mortality,adult illiteracy and malnutrition all remain extremely high and the prevalence ofHIV/AIDS has exacerbated the situation.

10. Zambia's medium-term prospects have to be assessed in light of its resources aswell as the policy challenges that remain. Its advantages include ample arable land andrainfall, abundant raw materials, and a liberalized policy environment. Acceleratinggrowth will require policies aimed at ensuring macroeconomic stabilization, completingthe privatization process, especially of ZCCM, improving infrastructure, and enhancingthe quality and coverage of public services. However, even with a supportive policyenvironment and consistent donor support, the legacies of over two decades of economicmismanagement and the current unfavorable external environment mean that GDP isprojected to grow at only about 4.5 percent per year in 1999-2001. Sustained economicgrowth and poverty reduction will come about only with steady policies and consistentaction over a number of years combined with accelerated debt relief.

HI. ZAMBIA 'SADJUSTMENTPROGRAM

11. Zambia's economic reform program aims to achieve a significant and sustainedimprovement in the living standards of the population through broadly-shared, privatesector-led growth. Attaining this goal, in turn, will depend on achieving and maintaininga stable macroeconomic environment, improving the climate for private investmentthrough liberalizing markets, privatizing commercial enterprises, investing in humancapital and physical infrastructure, and making progress toward long-term externalviability.

12. Zambia has successfully implemented many aspects of its reform program,particularly in the areas of liberalization and privatization. The emphasis has now shiftedfrom instituting "stroke of the pen" policy measures to undertaking the more complicatedagenda of institutional strengthening and program implementation. On macroeconomicmanagement, the focus is shifting to improving budgetary management, enhancingmonetary control, and strengthening the financial system, building on support fromprevious IDA adjustment operations. Many sectoral reforms are being supported byinvestment projects as described in Section IV below, and in several key sectors these arealso being supported under sector investment programs (SIPs). SIPs are underimplementation for the health, agriculture and roads sectors, a Power SectorRehabilitation Prograrn will begin implementation shortly, and a SIP is under preparationfor basic education.

13. The current reform program builds on these accomplishments. The status of theeconomic reform program, along with future actions, is summarized below under four

- 5 -

general headings: macroeconomic management; privatization and parastatalmanagement; improving public services; and, fostering private sector growth.

A. MACROECONOMICMANAGEMENT

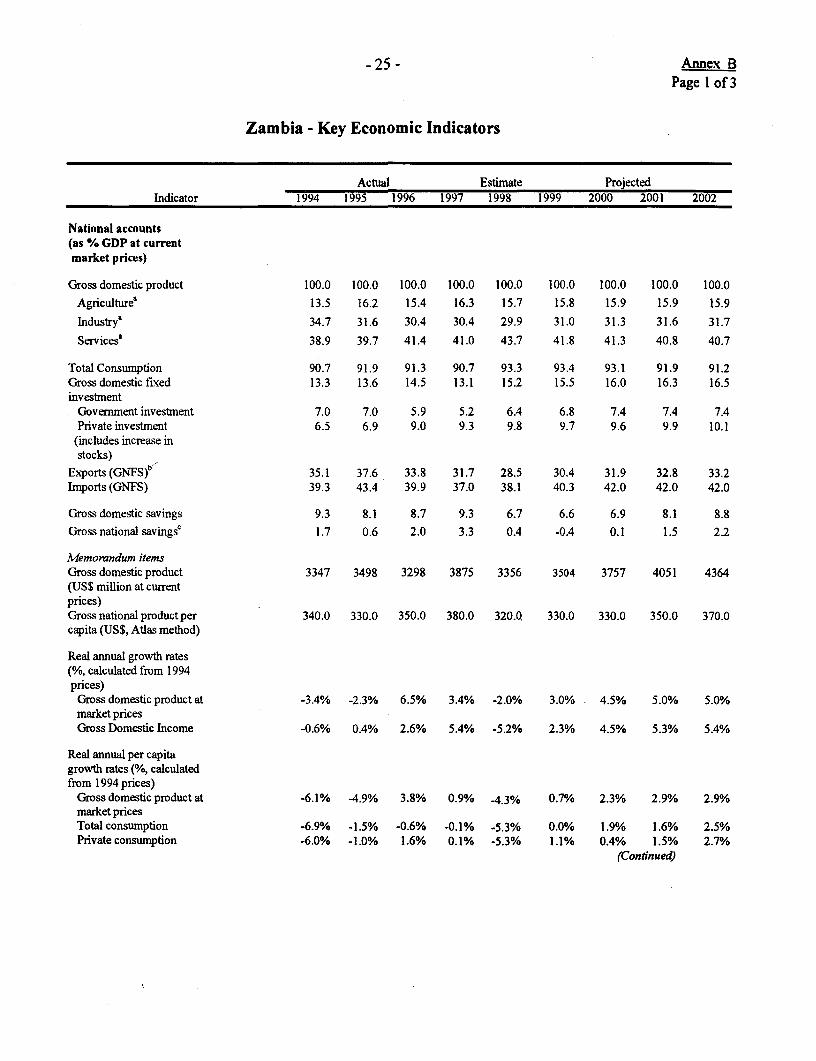

14. The domestic fiscal balance has improved steadily from a deficit of 4.2 percentof GDP in 1993 to a surplus of about 0.6 percent of GDP in 1998'. In the same period,the overall (cash) deficit of the central government, excluding grants, has fallen from 13.6percent of GDP to about 9 percent of GDP. While this improvement is commendable,particularly in the light of the difficult circumstances in 1998, several aspects of fiscaladjustment still need to be addressed. Tax revenues have fallen from 19.8 percent ofGDP in 1994 to 17 percent in 1998 and a number of tax exemptions, which were grantedin 1998 but later revoked, further threatened the revenue base. The significantcompression in non-wage expenditures, particularly domestically-financed publicinvestment, since 1994 points to the need to reduce the size of the public sector andcontain the wage bill. Finally, fiscal management performance has fluctuated widelyduring the adjustment period, prolonging the time taken to reduce inflation.

15. The Governnent's fiscal targets for 1999-2001 are to maintain a domestic budgetsurplus of, on average, about 1.3 percent of GDP and to reduce the overall deficit tobelow 1 percent of GDP (including grants) by 2001, from almost 4 percent in 1998.Strengthening tax administration and public expenditure management will be key toachieving these objectives and to strengthening overall fiscal management. Taxadministration will need to improve to increase effective tax yields, particularly withrespect to income and corporate taxes. The public expenditure management system willneed to be strengthened by improving the linkages between the cash budget andcommitted expenditures, thereby avoiding the build-up of new domestic arrears.

16. On revenue, the challenge over the medium term is to continue the restructuringof the tax system while increasing its ratio to GDP. The government will build on theprogress recently made in restructuring the tax system, which will involve a further shiftof the incidence of taxation toward consumption and away from international trade.Given the limited scope to raise tax rates further, the bulk of revenue improvements willneed to be found in the strengthening of tax administration and elimination ofexemptions.

17. To be sustainable, reductions in expenditures will need to be accompanied byrestructuring to safeguard priority spending on social sectors and infrastructureinvestments. A specific area where budgetary savings need to be achieved is in thepublic service wage bill. The reduction in the size of the public service (even with someincreases in wage levels) will allow the government to reduce the wage bill to about 25percent of total domestic non-interest expenditures in 2001 from about 38 percent in1996-98. In addition, the reduction in the stock of domestic debt and declining interest

Defined as the difference between revenues, excluding grants, and expenditures, excluding externalinterest and foreign-financed capital.

- 6 -

rates will lead to a drop in interest payments of about 0.75 percentage points of GDPbetween 1998 and 2001. Both of these will create room for the needed increases indomestically-financed public investment and social expenditures. Public investment isprojected to increase to 7.4 percent of GDP by 2001 (from 6.1 percent in 1998) in thecontext of a medium-term public investment program.

18. Following the setbacks in restoring macroeconomic stability in 1998, the keyobjectives for monetary policy will be to assist in regaining control over inflation andrebuilding external reserves. To this end, the monetary policy stance will be tightened in1999 by controlling the growth of net domestic assets of the banking system. To allowsufficient growth in private-sector credit, the increase in the government's claims on thebanking system will be regulated. The Bank of Zambia also intends to intensify its use ofopen market operations while maintaining positive real interest rates on Treasury bills.

19. Reflecting growing concerns over the financial weakness of the commercialbanking sector, the priority in the financial sector will be strengthening prudentialoversight of the banking system. Several banks have closed in recent years, while othershave failed to meet the increased minimum capital requirements. Decisive actions to dealwith the weak institutions and to strengthen banking supervision in the Bank of Zambiawill be required to ensure that the banking sector can support the projected increase inprivate sector economic activity.

20. With import restrictions reduced and foreign exchange controls removed (withsupport from previous adjustment operations), the focus in the external sector is shiftingto establishing a viable long-term balance of payments position. This requiresdeveloping the capacity to withstand external shocks due to adverse weather and fallingcopper prices, as well as reducing Zambia's dependence on copper receipts and donorassistance by strengthening non-metal exports. Building external reserves will be a keyelement of this strategy along with the maintenance of a market-determined exchangerate. Bank of Zambia operations in the exchange market will be aimed at achieving thedesired accumulation of reserves and smoothing short-term fluctuations in the exchangerate. Reserves will not be used to defend the exchange rate if it appears out of line withmarket fundamentals and the longer-term goal of external viability, but policies will beadjusted if exchange rate developments jeopardize the inflation objective or reduce theprofitability of the tradable goods sector.

B. PRIVATIZATIONAND PARASTA TAL MANAGEMENT

21. The privatization program is well advanced in Zambia. At the outset of theprogram, the government enacted a sound legal framework and established a semi-autonomous privatization agency, the Zambia Privatization Agency (ZPA). Significantprogress has been made in implementing the privatization program, which started in 1993with a list of 138 companies to be privatized, and has increased in late 1998 to a portfolioof about 280 entities. Of these, 223 entities have been privatized or liquidated. Theprogram will now focus on completing the sale of the remaining assets of ZambiaConsolidated Copper Mining Ltd. (ZCCM), the copper mining parastatal, privatization of

- 7 -

the utilities, and on increasing private sector involvement in the provision ofinfrastructure services.

22. By far the single most important privatization transaction that has been attemptedso far is that of ZCCM. When the current government came to power in 1991, ZCCMwas facing deep-rooted operational, managerial and financial problems, includingundermaintained plant and equipment; aging technology; declining identified ore reserves(despite an abundant resource base); low productivity; declining profitability; excessivedebt; conflicting commercial and social objectives; and surplus labor. The company'slabor complement was about 57,000, and the annual productivity level was 6.8 tons ofcopper per employee, low by world standards. The management appointed by the newGovernment attempted to improve ZCCM's performance, but failed, and in 1995, theGovernment decided to privatize ZCCM in order to mobilize the capital, technology andmanagement needed to restore the company and the copper mining sector to financial andoperational health.

23. To accomplish this, the Government and the minority shareholders (mainly AngloAmerican Corporation - AAC), on the recommendation of the international investmentbankers (financed under IDA's Economic Recovery and Investment Promotion TechnicalAssistance Credit (ERIPTA), approved in FY96), adopted a two-stage Privatization Planfor ZCCM. During the first stage, ZCCM would dispose of majority interests in itsmining assets by unbundling the latter and offering them for sale to qualified privateinvestors. In the second stage after the disposal of these packages, the residual ZCCMwould become an investment holding company that would collect outstandingreceivables, settle all outstanding liabilities, oversee the Government's minority interestin the privatized companies, and implement a program to reduce the residual labor forcefrom about 7,400 people (eighteen percent of ZCCM's current labor force) to about 30 bymid-1999. Subsequently, the Government's shares in "ZCCM Investment Holding"would be sold through public flotations to the Zambian public and other investors.

24. The first stage of this plan is well under way. The company's operations havebeen split into packages. Two of the packages (Konkola North Mine Development areaand Konkola Deep Mining Project) were subject to direct negotiations with majorinternational mining companies. Bids were called for the other packages by end-February 1997, and the investor response was favorable. Konkola North was sold to aSouth African mining company, and due diligence work and negotiations for KonkolaDeep was undertaken by AAC under the provisions of a Memorandum of Understanding(MOU) with ZCCM/Government. Several of the publicly offered packages and othermajor assets have been sold (LuanshyalBaluba Mine, Kansanshi Mine, the PowerDivision, Chibuluma Mine, Chambishi acid and cobalt plants, and the Precious MetalsPlant). Negotiations for the sale of the other major packages are at an advanced stage andMemoranda of Understanding have been signed with two prospective buyers. TheGovernment currently is aiming to transfer the remaining assets currently undernegotiation by the end of the first quarter of 1999. In the transactions concluded so far,the new owners have undertaken to take over the existing labor force and to honor allexisting terms and conditions of service. Any labor reduction programs will thereafter beimplemented at their discretion and cost. The investors negotiating for the remaining

- 8 -

assets are reluctant to take over all the workers. Thus, the remaining employees, alongwith commercial obligations and short term loans not assumed by the new owners andresidual assets, will remain with "ZCCM Investment Holding."

25. The cost of the residual labor force redundancy program is now estimated atUS$65 million. The amount per person appears to be high because the compensationbeing paid is a terminal benefit, which is tantamount to a lump-sum pension that ispayable to all departing employees, including retirees, and because a large proportion ofthe workers being retrenched are long-time ZCCM employees. The costs of thisredundancy program go well beyond the financial capability of"ZCCM InvestmentHolding" in the short- to medium-term. However, a successful labor reduction programwould help ensure the completion of ZCCM's privatization and enhance productivity inthe sector, while reducing the scope for potential distress and social up]heaval on theCopperbelt during the transitional period. In an effort to minimize the costs of severanceand to encourage preference for continued employment in the privatized operations,ZCCM will: (a) actively promote the skills and services which are found in theCorporate Head Office, the Operations Center and the remaining core assets to the newowners prior to transfer of assets; (b) market the self-contained functions, such asResearch and Development, Industrial Relations, and Central Winding and MaterialsTesting; (c) sell company-owned houses to employees; and, (d) enforce thereimbursement to ZCCM of severance benefits by those who are subsequently re-employed in existing operations by the new owners.

C. IMPROVINGPUBLICSERVICES

26. The effectiveness of public services in Zambia has declined significantly over thepast 10 years. The basic problems are similar to those faced in many other countries.First, there are too many employees relative to current requirements; second, personnelcosts take too great a percentage of limited resources (almost 30 percent of domesticrevenues), thereby crowding out expenditure on essential supplies and capital spending.Third, salary scales have been compressed, resulting in wages at senior levels too low toattract and retain good quality staff. Finally, management and organizational proceduresare outmoded so that the existing manpower is not used efficiently, and the public servicehas become generally unresponsive to the country's development needs.

27. In 1993, the Government launched a Public Service Reform Program (PSRP)with a view to improving the quality of public services. Some progress has been made inrestructuring ministries to relate their organization more closely to their functions, to hiveoff non-core functions, and to identify surplus positions. Although new plans have beenapproved for most ministries and departments and some staff appointed to the newpositions, implementation continues to be hampered by the high cost of involuntaryretrenchment of surplus civil servants.

28. A revised PSRP was adopted in September 1997, which aimed at substantiallyreducing non-military public service employment, decompressing public-sector salarieswhile simplifying pay scales and consolidating allowances, introducing new personnelpolicies and procedures, including actuarially sound pension arrangements, strengthening

- 9-

the system for controlling the public payroll, and developing improved performancemanagement systems. The program would institute a full census of civil servants toidentify "ghost workers", use a combination of voluntary and involuntary separationpackages for those tenured civil servants identified as surplus, and implementstrengthened procedures for personnel management and a new program of performance-based management. Some of the savings from reducing the wage bill by cutting publicemployment would be allocated over the ensuing three years to decompress salary levelswith larger increases at the higher and middle levels. Donor contributions are expected tomeet a substantial share of costs of retrenchment.

29. Improved delivery of public services also involves reforms at the sectoral level indelivery mechanisms. In the health sector, those reforms are supported by a SectorInvestment Program (SIP) involving multiple donors, and center around decentralizationof decision-making and responsibility for service delivery to levels of government closerto those being served. For a number of years now, funding for health services has beenallocated as block grants to the district level. Similar systems are being developed inbasic education. These reforms are expected to increase efficiency and responsiveness tobeneficiary needs.

30. Of particular importance in the social sectors, reforms are currently underway inthe areas of nutrition and public welfare. Over the past year, an extensive study of theNational Food and Nutrition Council (NFNC) was undertaken, and the Government hasdeveloped an agenda for reform including redirecting the functions of NFNC to be moreof a catalyst than a service provider, and providing it with adequate resources. ThePublic Welfare Assistance Scheme (PWAS) is intended to help the poorest of the poordeal with short-term disasters, to pay for health and school fees, and to assist thechronically poor, such as widows, orphans, the aged and the handicapped. In the past, ithas suffered from design weaknesses, limited administrative capacity and low budgetallocations. The Governrnent has recently revamped the scheme, devising new eligibilitycriteria and developing new operational guidelines. The Ministry of CommunityDevelopment and Social Services (MCDSS) has developed a pilot scheme to test therevamped PWAS and will launch the new scheme over four years. An eligibility criteriamatrix has been developed, and implementation guidelines have been developed and fieldtested. Critical to the success of this revised program will be adequate funding. AboutK. 2.8 billion has been budgeted in 1999 for welfare transfer payments. A NationalPoverty Reduction Unit has also been established in MCDSS to coordinate theimplementation of the Govermment's Poverty Reduction Plan.

D. FOSTERING PRIVATE SECTOR GROWTH

31. Zambia's trade and investment policies have undergone substantial reform sincethe adoption of an outward-looking and market-oriented growth strategy in 1991. Thesereforms have helped to improve the climate for private investment and to enhance theattractiveness of export-oriented production. Decontrol of prices, elimination ofsubsidies, privatization of public enterprises, and removal of restrictions on private-sectoractivity have all contributed to improving the business environment. The availability offoreign exchange at the market-determined exchange rate, the elimination of quantitative

- 10-

import restrictions, and rationalization of the tariff structure with consolidation of tariffbands and reductions in nominal tariffs have been of particular importance in reducingthe anti-export bias of the trade regime. Meanwhile, until late-1997, tariff revenues weremaintained by limiting the availability of tariff exemptions to clearly identified groups orproducts while extending tariff coverage to most government imports.

32. Tariff reforms since 1996 have enhanced the attractiveness of export production.Nominal tariffs were lowered, particularly for raw materials and capital goods, and thenegative protection faced by many domestic businesses using imported raw materials wasreduced or eliminated. The maximum tariff rate was reduced from over 100 percent in1994 to 30 percent in 1997 (including the 5 percent Import Declaration Fee) while theaverage import-weighted tariff rate fell from 20.6 percent in 1994 to 11.4 percent in1996, and the standard deviation fell from 12.6 percent to 9.9 percent over the sameperiod. The process of lowering tariffs continued in 1998 with the elimination in July ofthe Import Declaration Fee (IDF), which had been assessed since late-1995 at 5 percentof the import value as a temporary measure to compensate for the revenue losses due tothe first round of tariff reductions. While these tariff reductions have clearly increasedthe profitability of export production, as reflected in the rapid growth of non-metalexports (27 percent per year in value terms between 1994 and 1997), it is difficult to bemore precise about the exact contribution of these changes to export production since thechanges are recent and precise data on cost structures and effective protection rates arenot available.2

33. In order to sustain the response of exports and private investment, continuedmacroeconomic stability, strengthening of the financial sector, and improvements inphysical infrastructure will be essential in the medium term. Complementary policy andinstitutional reforms are also needed in two main areas. First, to ensure that exportershave access to their imported inputs at world prices, the existing schemes--the dutydrawback (DDB) scheme, which refunds import duties to eligible exporters, and themanufacturing-under-bond (MUB) scheme, which exempts designated exporters fromimport duties--need to be improved. Despite past attempts to improve their functioning,both schemes have continued to suffer from implementation problems, and neitherscheme has had a perceptible impact on the profitability of export production. Theproblems with the DDB have been that the availability of funding for the provision ofduty refunds is inadequate and unreliable, while the procedures and documentation forclaiming refunds are time-consuming and cumbersome. The MUB had suffered from notbeing focused on exporters because it was not distinguished clearly from the BondedWarehouse (BW) scheme, which is available to all importers.

34. Second, the institutional basis for export and investment promotion needs to bestrengthened by streamlining the investment approval process, including that related toland acquisition, and reducing the number of often-overlapping consultative private andpublic sector institutions. At the same time, wide-ranging investment incentives in theform of fiscal exemptions need to be avoided.

2 The fall in non-metal exports in 1998 is likely to be an aberration on account of the recession and theaccumulation of arrears to businesses throughout the country by ZCCM.

- 11 -

E. MEDIUM TERMPROSPECTSAND FINANCING PLAN

35. Among the most challenging aspects of Zambia's economic reform program is toestablish a viable and self-reliant balance of payments that is compatible with Zambiameeting its external obligations and achieving steady economic growth. This isparticularly difficult because of the weakening of copper prices with little expectation ofsignificant recovery in the medium term. At the same time, Zambia's external debt ofalmost twice its GDP (nearly half of which is multilateral) implies that substantial debtservice payments will be required even with successful negotiations with creditors. Thus,even with success in expanding non-metal exports and limiting the growth in the demandfor imports, even modest levels of economic growth will mean an increase in the currentaccount deficit during the coming decade. Zambia is a severely indebted low incomecountry and, therefore, eligible to benefit from the HIPC initiative. Once a new ESAFarrangement is agreed with the IMF and the necessary technical work is completedduring 1999, Zambia's case could be reviewed by the Bank and Fund Boards, providedoverall program performance continues to be satisfactory.

36. With the suspension of bilateral balance of payments assistance in June 1996, alarger share of Zambia's financing needs in 1996 and 1997 was met from foreign directinvestment and private capital flows, including privatization proceeds. Balance ofpayments support in 1997 was about $120 million, mostly in the form of IDA Credits.External financing requirements for 1998 were discussed at the Consultative GroupMeeting in May 1998. Although about US$235 million was pledged as program support,it did not materialize due to delays in completing ZCCM privatization. In 1999, theexternal financing requirement (excluding foreign-financed capital expenditure) isestimated at about US$640 million. Of this amount, about US$190 million is expected tocome from multilateral sources (including IDA), about US$360 million is expected totake the form of private capital inflows and new Paris Club debt relief, with theremainder coming from bilateral donors. It is expected that the next Consultative GroupMeeting will be scheduled for the first half of 1999, following IMF approval of a newthree-year ESAF.

III. THE PROPOSED CREDIT

37. The proposed Credit would be the seventh adjustment operation for Zambia in thepast eight years. Zambia's economic reform program is well advanced, and the emphasisis now on consolidating past reforms and improving their implementation. The centraltheme of the proposed operation is on improving the performance of the public sector indelivering key social services and in supporting private sector activity. To this end, itexplicitly supports important actions in four critical areas of Zambia's adjustmentprogram described above-ZCCM privatization, public service reform, export andinvestment promotion, and investment in social sectors. These areas are consistent withthe priorities of the Bank program in Zambia as described in the most recent CountryAssistance Strategy reviewed by the Bank Board in July 1996. Many of the actions to besupported under the proposed operation will be complemented by specific activities beingimplemented under ongoing or new investment operations. Technical assistance and

- 12 -

other activities relating to the privatization of ZCCM have received ongoing support fromthe Mining TA and ERIPTA Credits. Public service reforms already being supported bythe Financial and Legal Management Upgrading Project will be built upon in a proposedfollow-up operation to build public sector capacity. To support the private sector, theEnterprise Development Credit provides credit and matching grants for projectdevelopment, while the ongoing Agriculture Sector Investment Project provides a RuralInvestment Fund. Complementary infrastructure is being funded under multi-donor roadsand power programs. Improved delivery of social services is being supported under theHealth SIP and the Social Recovery Project and will be supported by a Basic EducationSIP under preparation.

A. SUPPORTING ZCCM PRI VA TIZA TION

38. The assistance under the Credit aims to facilitate the completion of theprivatization of ZCCM and improve the productivity of the copper industry by reducingthe labor component of overheads and centralized technical services, and by mitigatingthe social cost of adjustment. The ZCCM redundancy program will be completed byabout June 1999. Government funds for this purpose will be lent to ZCCM oncommercial terms. The estimated cost of the program is US$65 million, net of theobligations assumed by the new owners in respect of divisional personnel. Of the totalcost, US$58 million would be for payments to departing workers and US$7 million forretraining and outplacement assistance programs, comprising financial counseling, jobsearch seminars, and skills bridging programs. The Government and ZCCM will agree toa redundancy plan acceptable to IDA based on a draft plan that was agreed atnegotiations, which includes mechanisms for identifying those who would receivepayments and the terms of those payments. A loan agreement will be signed between theGovernment and ZCCM for onlending the proceeds of the Credit to cover the costs of theredundancy program. An audit without qualification by an independent auditor thatcertifies that ZCCM has implemented the redundancy plan as agreed with IDA would bea condition for release of the Second Tranche.

39. As ZCCM sells more of its mining/core and non-core assets, it will be left with aportfolio of assets that consists mainly of investments in mining companies for which theorganizational structure of a mining concern, such as ZCCM's current organization, is notsuitable. The residual ZCCM will be a company that has different objectives andfunctions, and will have significantly different organizational and staffing requirements.Specifically, it will have to emphasize the monitoring of investments and follow-up onthe commitments of the buyers of its assets under the development and other agreements.It will also need far fewer staff (about 30) whose qualifications are by and large differentfrom those employed by ZCCM, the mining company. The change in the objectives,functions, and organizational structure will require ZCCM to revise its Articles ofAssociation, shareholder agreements, administrative rules, and terms and conditions ofservice. During Negotiations, IDA agreed with Government and ZCCM: (a) on a"ZCCM Reorganization Plan,"; and (b) that ZCCM will seek the approval of the agreed"ZCCM Reorganization Plan" by the ZCCM Board of Directors. A certified copy of theBoard's approval resolution will be provided to IDA, and satisfactory progress in

- 13 -

implementing this Plan is a condition for release of the Second Tranche. The transfer tothe new owners of ownership and control of the remaining core ZCCM assets for whichMOUs and/or sales agreements have been reached and decisions concerning the futurestatus of any major ZCCM assets that are unsold will also be conditions for release of theSecond Tranche.

B. PUBLIC SER vICE REFORM

40. To achieve sustainable improvements in the performance of the public service, thegovernment recognizes that it must address the key issues of overstaffing, low andcompressed pay scales, and inadequate management controls. In September 1997,therefore, it adopted a revised PSRP to address these problems decisively andcomprehensively by aiming to: reduce nonmilitary public employment substantially byend-1999; decompress public sector salaries to bring pay levels and structures more inline with those in the private sector while simplifying pay scales and consolidatingallowances; introduce new personnel policies, procedures, and practices, includingactuarially sound pension arrangements, as the basis for a new employment contractbetween the government and the public service; strengthen the systems for controlling thepublic payroll; and, develop improved performance management systems.

41. Since the adoption of the revised PSRP, some progress has been made towardsthese goals. A detailed action and implementation plan for the program was prepared andapproved by the Cabinet in April 1998. A full-time Director General was appointed inearly-1998 to oversee the implementation of the program, in consultation with a SteeringCommittee of senior officials from various ministries. To ensure enforcement of tighterestablishment controls, a hiring freeze was instituted in August 1997. Initial reductionsin the public payroll have been made in 1998 with the retrenchment of over 15,500classified employees (who are not eligible for the separation packages under the PensionsAct), of whom about 12,300 have been paid their terminal benefits, averaging about K.4.5 million each. The terminal benefits for the remaining 3200 will be paid by early-1999. Staffing reviews have been initiated for the ministries that account for the bulk ofcivil service employment.

42. However, the original phasing of the program, as spelt out in the action plan thatwas finalized in April 1998 has been modified. These changes in the implementation andphasing of actions on PSRP reflect the deterioration in the economic situation during1998 as well as delays in moving ahead in some areas due, in part, to unclear delineationof responsibilities and inadequate coordination among the key agencies responsible foraction. Specifically, the pace of retrenchment of pensionable civil servants will now beconsiderably slower than was originally envisioned, while the implementation ofimproved management controls with regard to the payroll, establishment controls,performance management, and the ministerial staffing reviews and restructurings will becompleted later than was anticipated in the action plan. The pace of retrenchingpensionable civil servants has been slowed because of a poor response to the voluntaryseverance package announced in February 1998, in part, due to the worsening economicsituation.

- 14 -

43. To agree on the details of this rephasing of actions on PSRP, managementarrangements for the program will be finalized and implemented in early-l 999.Following this, a revised action and implementation plan for PSRP will be prepared, andwill include clearly-assigned responsibilities for time-bound actions and targets in areassuch as retrenchments, pay and pension policies, establishment and payroll controls,ministerial restructuring, performance monitoring, and the mitigation of the social impactof retrenchments. It is expected that this action plan will be finalized and approved byCabinet so that its implementation begins by June 1999. An important issue to beaddressed in revising the action plan is the evaluation of various options for retrenchingpensionable civil servants in an affordable manner. As the condition for release of thefloating Tranche, the Government will agree with IDA on this action and implementationplan for PSRP and begin its implementation.

44. Since successful public service reform is a long-tern process, the action plan forPSRP will necessarily stretch beyond the implementation period of this operation.Continued support from the Bank and other donors to the implementation of the actionplan will likely be provided under the framework of an Adaptable Program Credit aimedat building public sector capacity, which is currently under preparation. The IDA Creditwould finance retrenchments as needed, depending on support from other donors, as wellas the necessary technical assistance to implement the reforms in such areas as publicservice pay and employment, and performance management frameworks.

C. INVESTMENTAND EXPORTPROMOTION

45. The reforms supported under this Credit relating to export promotion would buildon the trade and tax measures implemented since 1991, and would aim at accelerating thesupply response by: (i) ensuring that exporters have access to their imported inputs atworld prices by improving the workings of the DDB and MUB schemes, therebycompensating for the residual anti-export bias of the tariff regime; (ii) reducing tariffsfurther; and (iii) improving the institutional basis for investment and export promotion.

46. Making the DDB and MUB schemes work better remains important because,despite the recent reduction in tariffs, the average rate on intermediate inputs is still over9 percent, while less than a tenth of the value of intermediate goods imports now receiveexemptions, compared to 43 percent of the value of capital goods imports. Hence, tariffson intermediate inputs continue to have an appreciable impact on production costs formany promising export products. To address the problems with the working of the DDBand MUB schemes, changes aim at providing exporters with access to duty-free inputsquickly and transparently while ensuring that they can be administered and controlledeasily by the Zambia Revenue Authority. Therefore, the funding mechanism for theDDB has been revamped to ensure adequate and timely financing for refunds, and thenecessary documentation and procedures will be simplified. In particular, the duty refundmechanism, including procedures for verifying exports, builds on that already in place forVAT refunds. The MUB has been redefined so that it focuses directly on exporters andthe provision of duty-free imports to them has been linked to the revamped DDB scheme.

- 15-

47. As a condition of Board Presentation, several changes in the design andfunctioning of the DDB and MUB schemes were announced and their implementationbegun in April 1998. These changes included: (a) for the DDB, introducing proceduresfor computing the duty drawback based on coefficients that link duty paid to exportvalues; adopting the standard export documentation currently used for VAT refunds;improving the mechanism for funding duty drawbacks; and, drawing up a code ofconduct for applying procedures, which includes tracking the elapsed time for payment ofduty refunds; and (b) for the MUB, streamlining procedures and documentation along thelines for the DDB. As a condition of Second Tranche release, it would be verified thatboth schemes are being implemented satisfactorily, in terms of agreed criteria includingthe timeliness of processing of duty refunds and the implementation of simplifiedprocessing and documentation for the schemes.

48. In facilitating and supporting private investment, the process of investmentapprovals needs to be clarified and streamlined. With the reduction of fiscal incentives asa tool of investment promotion, the role of the Investment Center is now that of afacilitator, especially for foreign investors. However, the investment approval processstill involves the need to deal with multiple agencies, and can be both confusing andtime-consuming. Streamlining the investment approval process by clarifying the role andauthority of the Investment Center is, therefore, a priority. Some measures forstreamlining the investment approval process have been implemented, includingbroadening the composition of the Committee that considers Investment Certificateapplications and establishment of an independent consultancy company, which hasprivate-sector representation on its Board, to provide services to potential investors.Additional actions are being considered by the Government to streamline the investmentpromotion process. These proposals would be included in an action plan to beimplemented beyond the period of this Credit; and on which the Government will agreewith IDA as a condition of Second Tranche release.

D. SOCIAL SERVICES

49. Although some progress has been made in recent years, the delivery of socialservices in Zambia continues to be constrained by inadequate policies, shrinking financialresources and poor institutional mechanisms. Under this Credit, budget allocations to thesocial sectors would be agreed and monitored. In addition, two administrative reformswould be included. Improving nutritional status is a cross-sectoral issue that could bringsignificant benefits to a large share of the Zambia population at a relatively small cost.Under the previous ESAC II operation, a study of the Government's efforts to addressnutritional problems and especially the role of the National Food and NutritionCommission was carried out and some policy recommendations adopted. Applying theresults of that study and developing in more detail the policies and institutionalframework to deal effectively with nutrition issues will be a focus of the government'sefforts. Specifically, the Letter of Development Policy reflects the Government'scommitment to begin implementation of these policies during the period covered by thisCredit. The second area is to improve the effectiveness of the safety net so as to assistthe poor by mitigating the transition costs of adjustment. The Public Welfare Assistance

- 16-

Scheme (PWAS) is the Government's main vehicle for meeting the needs of the poorest,but its effectiveness has been limited in the past. PWAS has been reformed andstrengthened, and implementation of these reforms and the provision of adequatesufficient funding for the revamped program will be supported by this Credit.Specifically, the Letter of Development Policy includes the Government's commitmentto initiate implementation of the revamped PWAS during the PSREP period.

50. Under agreements reached in previous adjustment operations, the share of thediscretionary budget going to the social sectors has increased from 28 percent in 1993 to33.7 percent in 1995 and 34.6 percent in 1996. In 1997 and 1998, over 36 percent wasallocated to these budget categories although agreement on this figure was not acondition under an IDA Credit. Under this Credit, the Government will again maintain aminimum percentage (about 36 percent) of the total discretionary budget (i.e. excludingdebt service, donor funded development expenditures, and other statutorily requiredexpenditures) for allocations to and expenditures in the agreed social sector categories inthe 1999 Budget.

51. In previous operations, there has also been agreement on a subset of items thatwould be specifically protected from budget cuts. These items, which totaled 6 percentof the budget in ESAC II, were felt to be the highest priority in achieving sector goals andthe most sensitive to expenditure shortfalls. Under this Credit, there is an agreement,reflected in the Letter of Development Policy on protecting the budgeted amounts for keynon-personnel spending components in health, education, and public welfare, includingthe level of transfers to the Public Welfare Assistance Scheme. However, for simplicityof monitoring, only a few key categories would be monitored. The budget shares and themechanisms for monitoring actual expenditures have been agreed as a condition of BoardPresentation. Satisfactory implementation of the agreement on social sector spending asreflected in actual disbursements at the time of program review in 1999 would be acondition of Second Tranche release.

E. POVERTYIMPACT

52. The proposed Credit will improve the economic prospects of the poor in Zambiaby supporting the Government's efforts to stay the course on policy reforms, thusincreasing the prospects for sustainable economic growth and increased investment inZambia's human resources. Economic growth should expand real income andemployment opportunities. Further improvements in the trade regime should expandopportunities for non-mining exports, which analysis has shown to be more labor-intensive than the import substitution industrialization efforts of the 1970s. Of particularimportance to the poor will be the efforts to maintain social spending. The long-termefforts to eradicate poverty can only be successful if the Government is able to increasethe investment in Zambia's human resources for all population groups. This should alsobe strengthened by specific commitments supported under this Credit to improve budgetallocations to the social services and to strengthen the administrative arrangements in theareas of nutrition and public welfare. Of possible concern in terms of its short-termimpact on incomes will be the thousands of redundancies contemplated in both the publicservice and ZCCM. Severance benefits averaging several years of pay are to be paid to

- 17-

these employees, but it will also be necessary to offer services and training to ease thetransition to the private sector, and careful follow-up monitoring will be needed toidentify and remedy any significant problems that these redundancies might create.

F. ENVIRONMENTAL IMPACT

53. Addressing the issues related to the environment has been a vital part of Zambia'seconomic reform program. The Government was one of the first to complete a NationalEnvironmental Action Plan, and an IDA-supported Environmental Support Program iscurrently being implemented to strengthen the institutions that carry out Zambia'senvironmental program and to increase the cooperation between the public and privatesectors in this critical area. In addition, the Government has recently issued revisedenvironmental regulations for the mining sector, and a new environmental department inthe Ministry of Mines has been established. These should ensure that future mininginvestment take place with due regard to environmental considerations. The proposedCredit does not have an environmental focus, but it should have an overall positive effectby strengthening the capacity of the public sector to enforce environmental legislation.

G. SPECIFICAGREEMENTS

54. The specific conditions for release of the Second Tranche and the floatingTranche are summarized below. The maintenance of a satisfactory macroeconomicenvironment will be necessary to release both tranches.

55. The proposed specific conditions for Second Tranche Release are:

(a) Satisfactory audit of ZCCM's implementation of agreed redundancy plan;

(b) Satisfactory progress in implementing the ZCCM reorganization plan;

(c) Transfer of ownership and control of remaining core ZCCM assets forwhich memoranda of understanding and/or sales agreements have beenreached;

(d) Satisfactory operation of revamped DDB and MUB schemes;

(e) Agreement with IDA on an action plan to streamline investmentpromotion; and,

(f) Actual spending in the first quarter of 1999 consistent with agreed socialspending targets.

56. The proposed specific condition for release of the floating tranche is:

(a) Agreement with IDA on a revised action and implementation plan forPSRP, which is approved by Cabinet, and its initial implementation interms of arrangements for managing the program, strengthening

- 18-

management controls, and restructuring ministries (including thenecessary retrenchments).

H. IMPLEMENTATIONARRANGEMENTS

57. The proposed Credit of US$170 million will assist Zarnbia in meeting its externalfinancing requirements in 1999 and will facilitate the retrenchment of redundantemployees of ZCCM to enable its privatization and conversion to efficient operation.The Credit will be disbursed through the Bank of Zambia with US$65 million available ateffectiveness, US$40 million tied to a floating Tranche with a specific condition relatingonly to the public service reform program, and the remaining US$65 million tied to thesecond tranche with specific conditions in the three other areas, namely, ZCCMprivatization, export and investment promotion, and social services. Simplifieddisbursement procedures under adjustment credits will apply. The Borrower will open anaccount in the Central Bank. Upon IDA notification of tranche release for each tranche,proceeds of the Credit will be deposited by IDA in this account at the request of theBorrower. If after deposits in this account, the proceeds of the Credit are used forineligible purposes (to finance items imported from non-member countries, or goods orservices in the standard negative list), IDA will require the borrower to either (a) returnthat amount to the account for use for eligible purposes; or (b) refund the amount directlyto IDA, in which case IDA will cancel an equivalent undisbursed amount of the Credit.Although routine audit of the account will not be required, IDA reserves the right torequire it. As has been the case with previous adjustment operations, the Ministry ofFinance will be responsible for the overall implementation and monitoring of reformssupported by the PSREP Credit. This will involve continuing the monitoring andimplementation unit already established, and revising its terms of reference accordingly.

I. IMPLEMENTA TIONASSISTANCE

58. Administrative capacity remains a constraint on the Government's ability toachieve the objectives of its economic recovery program. The Bank has been assistingthe Government's efforts to upgrade this capacity while recognizing that the direction ofthis program must remain firmly in Zambian hands. Several IDA-assisted projects aredirected primarily at capacity building, including the Financial and Legal ManagementUpgrading Project (which includes administrative strengthening of public procurement),the Privatization and Industrial Reform Technical Assistance Project, the recently-completed Transport Engineering Project and the Economic Recovery and InvestmentPromotion Technical Assistance Project. All investment projects have major componentsaddressing capacity issues, particularly the sector investment operations in health,agriculture and roads (and under preparation in basic education). Use has also been madeof the Institutional Development Fund in building capacity in advance of projectinvestments. Considerable technical assistance is being provided in the public sectormanagement area by other donors and by the UNDP, and a possible follow-up capacitybuilding operation by the Bank is under consideration.

- 19 -

J. COFINANCING

59. At this stage, the African Development Bank has expressed an interest in parallelcofinancing. Indications are that bilateral donors will make their own arrangements forproviding balance of payments support.

K. PROGRAMBENEFITSAND RISKS

60. The primary benefit of this Credit will be the advancement of policy reforms inthe critical areas of ZCCM privatization, public service reform, export and investmentpromotion, and social service delivery. These reforms should help sustainmacroeconomic stability, accelerate economic growth and increase employment whileimproving the delivery of social services. The measures related to ZCCM privatizationand investment promotion should enhance the prospects for medium-term growth whilethe protection of social sector expenditures should increase Zambia's prospects forsustainable growth in the longer term.

61. There are two broad categories of risk. The first is that the Government's reformprogram as a whole could falter. This could result from major policy reversals and/or theimpact of major external shocks, including a continuing shortfall in external donorsupport because of either economic or governance-related concerns. The commitment ofthis Government to economic reform has remained steadfast in the past seven years.Many of the measures supported under this Credit and previous adjustment operationshave strengthened the capacity of the Zambian economy to withstand external shocks,including the collapse in copper prices during the past year. Dialogue with donors ongovernance-related issues, pledged by the Government at the last Consultative GroupMeeting, continues to be needed and is of high priority. The second source of risk forthis Credit concerns the possibility that the specific reforms supported under it are notundertaken. While it is possible that the sale of the remaining core ZCCM assets couldbe delayed beyond 1999, this risk is mitigated by the detailed agreements that have beenreached between the Government, ZCCM and the prospective buyers for the purchase ofthe bulk of these assets. On public service reform, there is a risk that the agenda andtimetable for reforms could pose political problems. To mitigate this risk, theGovernment will continue consultations with all major stakeholders during theformulation of its action plan and implementation of the program, and rely on continuedsupport from the Bank and other external partners.

IV. BANK OPERA4TIONS

62. The Bank's 1994 Poverty Assessment prepared with significant donor andGovernment involvement, provides a focus for Zambia's development objectives andframes the priorities of the Bank's assistance strategy for Zambia. The Bank is pursuinga three-pronged strategy to assist the Government in implementing an action plan forreducing poverty in Zambia: creating a stable macroeconomic enviromnent favorable togrowth; promoting private sector development and greater public sector efficiency; and,targeting assistance to poor and vulnerable groups. Under the first prong of this strategy,

- 20 -

Zambia has achieved some notable successes, and on balance, seems to have emergedfrom the most difficult first stages of its economic transition. Yet Zambia's high debtburden and limited prospects for copper exports in the short term mean that continuedreform and balance of payments support will be needed for the next decade if economicgrowth is to be achieved. Under the second prong, past reforms have resulted in theeconomy being now among the most open and private-sector oriented in Africa. IDA issupporting activities through specific investment projects and sector investmentoperations (SIPs) to improve the efficiency of service delivery as well as helping toincrease the private sector's role in the economy through continued support for theprivatization program and through new initiatives aimed at providing enterprises with theinformation, technology, and term finance to adapt to the new business environment. Inaddition, IDA is assisting the Government to arrest environmental deterioration and toput in place an effective environmental management system in Zambia.

63. To help target assistance to poor and vulnerable groups (the third prong of thestrategy), stabilization and budget reform measures supported by IDA adjustment lendinginclude protection of core social expenditures. Similarly, the Bank's investment lendingemphasizes supporting community-based development initiatives, integrating growth andpoverty reducing activities better within sectors, improving the delivery of services to thepoor, and linking poverty reducing activities across sectors.

64. The Bank's program in Zambia includes adjustment lending, investment lending,economic and sector work, and aid coordination. Bank adjustment operations each yearhave been aimed at strengthening macroeconomic stabilization and market liberalization,supporting privatization and parastatal reform, reducing structural constraints on thedelivery of social services, strengthening the social safety net, and promoting publicsector reform. In addition, IDA is supporting thirteen investment operations inagriculture, health, roads, power, urban water and sanitation, environmental protection,private sector development and social recovery, and in technical assistance in mining, thepetroleum sector, privatization and financial and legal reforn. The Bank is now shiftingits investment lending towards SIPs, whose aim is to increase public efficiency byavoiding the overlap, inconsistency, and administrative overload associated with a largenumber of separate donor-funded projects within each sector. As umbrella operations inwhich the Government takes the lead, SIPs are expected to promote dynamic growth bothbroadly, through improving the efficiency of service delivery within the sector, and in atargeted way, by financing pilot projects with a more immediate impact on the poor.They also provide long-terrn capacity building within the sector. SIPs have beenapproved in health (1994), agriculture (1995), roads and power (1998). Future IDAinvestment operations will consist predominantly of similar operations in basic educationand vocational education, a public sector capacity building project and a small number ofnarrowly targeted operations to achieve needed short-term gains. Preparation of a newCAS, involving a series of consultations with the Government and other stakeholders, isunderway and will be presented to the Executive Directors early in FY00.

65. The Bank's economic and sector work will include broader studies to providesome of the analytical underpinning for the economic reforms. Recent examples of suchwork are the Policy Framework Papers (PFPs), the Public Expenditure Reviews (PERs),

- 21 -

the Growth Prospects paper, and a Fiscal Management Review. In addition, the PovertyAssessment has provided additional insights into the extent and determinants of povertyin Zambia, explored the impact of the reform program on the poor, and recommendedfurther reformns and targeted investment programs. As Zambia is one of the most heavilyindebted of the low income countries, considerable attention will continue to be paid toanalyzing the country's prospects for further debt relief, and Zambia is one of thecountries highlighted in the joint Bank-Fund study on Debt Sustainability for HeavilyIndebted Poor Countries. Further work on Zambia's eligibility for HIPC will take placein 1999. Aid coordination will continue to figure prominently in the Bank's strategy.This includes: supporting the aid coordination that takes place in Lusaka under theleadership of the Government; chairing the Consultative Group; providing countryconsultations on Zambia in Special Program of Assistance for Africa (SPA) meetings;and, maintaining frequent informal contacts with Zambia's principal bilateral partners.

V. COLLABORATION WITH IMF

66. The programs of the Bank and Fund in Zambia have been closely coordinatedsince assistance to Zambia resumed in 1991. Balance of payments needs are jointlyagreed among the Bank, the Fund, and the Government as part of the PFP andConsultative Group processes. Bank proposals on trade, taxation, spending allocations,privatization, public service reform and related structural policy benchmarks arecoordinated with the Fund's fiscal targets, while the Fund's macroeconomic benchmarksare developed in close consultation with the Bank. The Fourth Policy Framework Paperwas approved by the Bank and Fund Boards in December 1995, and a new PFP for 1999-2001 is being finalized. Zambia successfully completed its Rights AccumulationProgram in December 1995, and the Fund Board approved a three year SAF/ESAFprogram, the mid-term review of which was concluded in February 1997. An IMF teamhas reached understandings with the Government on a policy program for 1999,including the macroeconomic framework, to be supported by a three-year ESAFarrangement. These understandings are reflected in the draft PFP.

- 22 -

VI. RECOMMENDATION

67. I am satisfied that the proposed Credit would comply with the Articles ofAgreement of the Association, and I recommend that the Executive Directors approve it.

James D. WolfensohnPresidentby: Sven Sandstrom

Washington, D.C.December 30, 1998

Attachments

-23 -

ANNEXES

A. SOCIAL INDICATORS OF DEVELOPMENT

B. KEY ECONOMIC INDICATORS

C. EXTERNAL FINANCING REQUIREMENTS

D. STATUS OF BANK GROUP OPERATIONS

E. EVOLUTION OF POLICY REFORM AGREEMENTS

F. ZAMBIA AT A GLANCE

G. MATRIX OF POLICY AGREEMENTS

H. PERFORMANCE INDICATORS

1. LETTER OF DEVELOPMENT POLICY

- 24 - Annex APage I of I

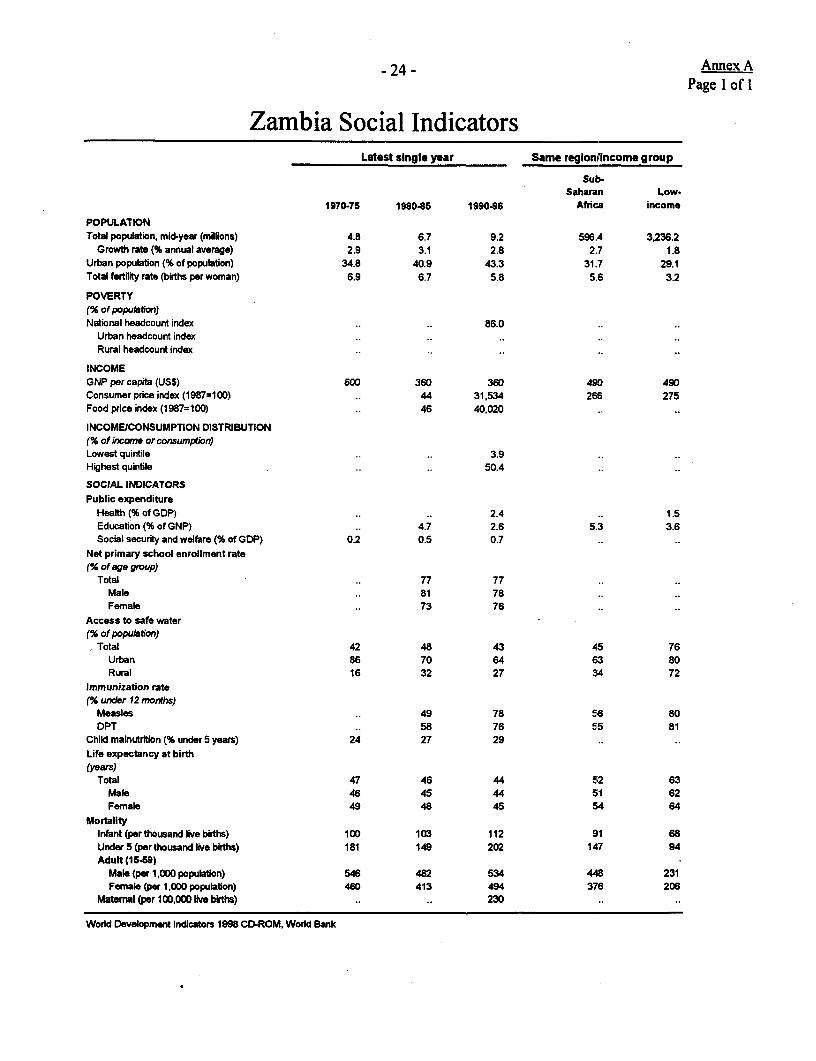

Zambia Social IndicatorsLatest single year Same reglonflncome group

Sub-Saharan Low-

1970-75 1980-85 1990-96 Aftica income

POPULATIONTotal poptiation, mid-year (milions) 4.8 6.7 9.2 596.4 3,236.2

Growth rate (% annual average) 2.9 3.1 2.8 2.7 1.8Urban population (% of population) 34.8 40.9 43.3 31.7 29.1Total fertility rate (births per woman) 6.9 6.7 5.8 5.6 3.2

POVERTY(% of population)National headcount index 86.0

Urban headcount indexRural headcount index

INCOMEGNP per capita (US$) 600 360 360 490 490Consumer price index (1987=100) 44 31,534 266 275Food price index (1987=100) 46 40,020

INCOMEICONSUMPTION DISTRIBUTION(% of income or consumption)Lowest quintile 3.9Highest quinble 50.4

SOCIAL INDICATORSPublic expenditure

Heafth (% of GDP) 2.4 1.5Education (% of GNP) 4.7 2.6 5.3 3.6Social security and welfare (% of GDP) 0.2 0.5 0.7