Embed Size (px)

Citation preview

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No: 28532 EC

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$20 MLLION

TO THE

REPUBLIC OF ECUADOR

FOR A

INSTITUTIONAL REFORM PROJECT

May 26,2004

Poverty Reduction and Economic Management Sector Management Unit Bolivia, Ecuador, Peru and Venezuela Country Management Unit Latin America and the Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. I t s contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

REPUBLIC OF ECUADOR

ALCA

APL BCE

CAE

CAS CAF cccc

CFAA CGE

CLD

CNC

COMEXI

CONAM

CONAREM

COSUDE

DIGMER

DO EU FCCGL

FEIREP

FM FMA FMR FTA GDP GOE GTZ

HR HRM

FISCAL YEAR January 1-December 3 1

CURRENCY EQUIVALENTS (Since January 2000)

Currency Unit = US dollar

WEIGHTS AND MEASURES Metric System

SELECTED ABBREVIATIONS AND ACRONYMS

Free Trade Agreement of the Americas (Acuerdo de Libre Comercio pura /us AmCricas) Adaptable Program Loan Central Bank of Ecuador (Bunco Central del Ecuador) Ecuadorian Customs Corporation (Corporucidn Aduaneru Ecuutoriunu) Country Assistance Strategy Colporacidn Andina de Foment0 Commission of Civic Control for Corruption (Comisidn de Control Civic0 de la Corrupcidn) Country Financial and Fiduciary Analysis Comptroller General Office (Contrulonh General del Estudo) Latin American Corporation for Development (Corporucidn Latino Americana pura el Desurrollo) National Competitiveness Council (Consejo Nucional de Competividud) Foreign Trade and Investment Council (Consejo de Comercio Exterior e Inversiones) National Council for State Modernization (Consejo Nucionul de Modemizucidn del Estudo) National Commission of Remunerations (Consejo Nacionul de Remuneruciones) Swiss Agency for Development and Cooperation (Agenciu Suizu pura el Desarrollo y la Cooperacidn- Cooperation Suisse du Dkeloppement) General Directorate of the Merchant Marine and Coasts - Guayaquil Port Authority (Direccidn General de lu Marina Mercante) Development Objective European Union Fiscal Consolidation and Competitive Growth Loan I, I1 Fund for Stabilization, Investment, and Public Debt Reduction (Fondo de Estubilizacidn, Inversidn Social y Productiva y Reduccidn del Endeudamiento Pu'blico) Financial Management Financial Management Assessment Financial Monitoring Report Free Trade Agreement Gross Domestic Product Govemment of Ecuador German Technical Cooperation - Gesellschaft fur Technische Zusammenarbeit Human Resources Human Resources Management

IADB IBRD

ICB ICR IESS

IRSISRI

IRP ISDS IT LAC LOAFYC

M&E MDAs MDGs MEF

MOSTA

NCB NFPS NGO OP OSCIDI

PAD PCN PCU PER PERHD

PetroEcuador PETS PDO PID PCU QCBS RO RVP SA SALT0 SBA SBD

Inter- American Development Bank Intemational Bank for Reconstruction and Development International Competitive Bidding Implementation Completion Report Ecuadorian Institute for Social Security (Institufo Ecuutoriuno de Seguridud SociuL) Internal Revenue Services (Servicio de Rentus Intemus) Institutional Reform Project Integrated Safeguards Data Sheet Information Technology Latin America and the Caribbean Financial Administration Legislation (Ley Orgrinicu de Administrucidn Financieru y Control) Monitoring and Evaluation Ministries, departments, agencies Millennium Development Goals Ministry of Economy and Finance (Ministerio de Economiu y Finunzas) Modernization of the State Technical Assistance Loan National Competitive Bidding Non-Financial Public Sector Non-govemmental organization Operational Policy National Office for Institutional Development (Oficinu de Servicio Civil y Desurrollo Institucionul) Project Appraisal Document Project Concept Note Project Coordination Unit Public Expenditure Review Program for Economic Restructuring and Human Development State-owned Petroleum Company Public Expenditure Tracking Surveys Project Development Objectives Project Information Document Project Coordination Unit Quality and cost-based selection Official Register (Registro Oficial) Regional Vice-presidency Special Account Structural Adjustment Liberalization Task Order Stand-By Arrangement Standard Bidding Documents

FOR OF'FICLAL USE ONLY

SENDA National Secretary for Administrative Development (Secretanh Nacional de Desarrollo Administrativo) National Technical Secretariat for Human Resource Development and Remuneration (Secretaria Nacional Ticnica de Desarrollo de Recursos Humanos y Remuneraciones del Sector Publico) Integrated Debt Management System (Sistema de Gestidn y Administracidn de Deuda)

System (Sistema Integrado de Gestidn Financiera) National Information System o f Institutional Development, Human Resources and Public Sector Remunerations (Sistema Integrado de Administracidn de Recursos Humanos)

SENRES

SIGADE

SIGEF Integrated Government Financial Management

SIGRH

SOEs TAL TE

TG

T I

TR TTL URHIs USAID

VAT WBI WTO

Statement of Expenditures Technical Assistance Loan Special Account (Cuenta Transitoria de Recursos Exremos) Local Counterpart Account (Cuenta Transitoria de Recursos del Gobiemo) Transparency International Chapter of Ecuador, Civic Participation Payment Account Task Team Leader Human Resources Administrative Units United States Agency for International Development Value-added tax World Bank Institute World Trade Organization

Vice President: David de Ferranti Country Director: Marcelo Giugale

Sector Director: Ernesto May Sector Manager: Ronald Myers

Edgardo Mosqueira Kathrin A. Plangemann Task Team Leaders:

This operation was prepared by a World Bank team composed of Messrs./Mmes. E. Mosqueira, K. Plangemann, J. Frank, C. Machicado, J. Rinne, E. Simon, S. Alborta-Hudson (LCSPS); M. Andrade, N. Brune, G. Durand, E. Fanta, C. Olle, B. Merino, J. Salazar, G. Shepherd, A. del Villar, (Consultants, LCSPS); J. Lopez-Calix (LCSPE), P. Larreamendy (LCCEC), R. Senderowitsch (LCSPR), F. Braun (Consultant, LCSPR), W. Reuben (LCSEO), A. Silva-Leander (SDV), F. Altimari, E. Brito (LEGLA), X. Morel (LOAG3); P. M c Kenzie (LCOAA), A. Jimenez (Consultant, LCOAA), K. Alfaro, M. Osorio (LCOPR), G. Reid (ECSPE), F. Recanatini (WBIGG), M. Zold (Consultant, INT). Peer Reviewers: Y. Matsuda (LCSPS), E. Campos (PRMPS), R. Pinto (AFTPR).

This team was led by MessrsIMmes. Edgardo Mosqueira and Kathrin A. Plangemann (LCSPS, Task Managers), and worked under the general guidance o f Messrs. Marcelo Giugale (Director, LCC6C), Vicente Fretes-Cibils (Lead Economist and Sector Leader, LCC6C), Ernesto May (Director, LCSPR), Ronald Myers (Sector Manager, LCSPS), and McDonald Benjamin (Country Manager, LCCEC).

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. I t s contents may n o t be otherwise disclosed without W o r l d Bank authorization.

ECUADOR EC Institutional Reform

CONTENTS

Page A . STRATEGIC CONTEXT AND RATIONALE .................................................................. 6

COUNTRY AND SECTOR ISSUES .............................................................................................. 6 RATIONALE FOR BANK INVOLVEMENT .................................................................................. 9 HIGHER LEVEL OBJECTIVES TO WHICH THE PROJECT CONTRIBUTES ...................................... 9

B . PROJECT DESCRIPTION ................................................................................................ 10 LENDING INSTRUMENT ........................................................................................................ 10 PROJECT DEVELOPMENT OBJECTIVE AND KEY INDICATORS ................................................. 10 PROJECT COMPONENTS ....................................................................................................... 11 LESSONS LEARNED AND REFLECTED IN THE PROJECT DESIGN ............................................. 16 ALTERNATIVES CONSIDERED AND REASONS FOR REJECTION ............................................... 16

C . IMPLEMENTATION. ........................................................................................................ 17 1 . PARTNERSHIP ARRANGEMENTS ........................................................................................... 17 2 . INS~TIONAL AND IMPLEMENTATION ARRANGEMENTS ................................................... 17 3 . MONITORING AND EVALUATION OF OUTCOMES/RESULTS ................................................... 18 4 . S U S T A I N A ~ ~ ~ ~ Y ................................................................................................................. 18 5 . CRITICAL RISKS AND POSSIBLE CONTROVERSIAL ASPECTS .................................................. 18 6 . LOAN~REDIT CONDITIONS AND COVENANTS ...................................................................... 19

APPRAISAL SUMMARY .................................................................................................. 20 1 . ECONOMIC AND FINANCIAL ANALYSES ............................................................................... 20 2 . TECHNICAL ......................................................................................................................... 20 3 . FIDUCIARY .......................................................................................................................... 20 4 . SOCIAL ............................................................................................................................... 21 5 . ENVIRONMENT .................................................................................................................... 21 6 . SAFEGUARD POLICIES ......................................................................................................... 21 7 . POLICY EXCEPTIONS AND READINESS ................................................................................ 22

ANNEX 1: COUNTRY AND SECTOR OR PROGRAM BACKGROUND ......................... 23

ANNEX 2: MAJOR RELATED PROJECTS FINANCED BY THE BANK AND/OR OTHER AGENCIES ................................................................................................................... 28 ANNEX 3: RESULTS FRAMEWORK AND MONITORING ............................................... 31 ANNEX 4: DETAILED PROJECT DESCRIPTION .............................................................. 43

ANNEX 5: PROJECT COSTS ................................................................................................... 51 ANNEX 6: IMPLEMENTATION ARRANGEMENTS .......................................................... 52

ANNEX 7: FINANCIAL MANAGEMENT AND DISBURSEMENT ARRANGEMENTS53 ANNEX 8: PROCUREMENT ARRANGEMENTS ................................................................. 57

1 . 2 . 3 .

1 . 2 . 3 . 4 . 5 .

D .

4

ANNEX 9. ECONOMIC AND FINANCIAL ANALYSIS ...................................................... 67 ANNEX 10: SAFEGUARD POLICY ISSUES .......................................................................... 70 ANNEX 11: PROJECT PREPARATION AND SUPERVISION ........................................... 71 ANNEX 12: DOCUMENTS IN THE PROJECT FILE ........................................................... 72 ANNEX 13: STATEMENT OF LOANS AND CREDITS ....................................................... 73 ANNEX 14: COUNTRY AT A GLANCE ................................................................................. 74 ANNEX 15: MULTISTAKEHOLDER CONSULTATIONS ................................................. 76

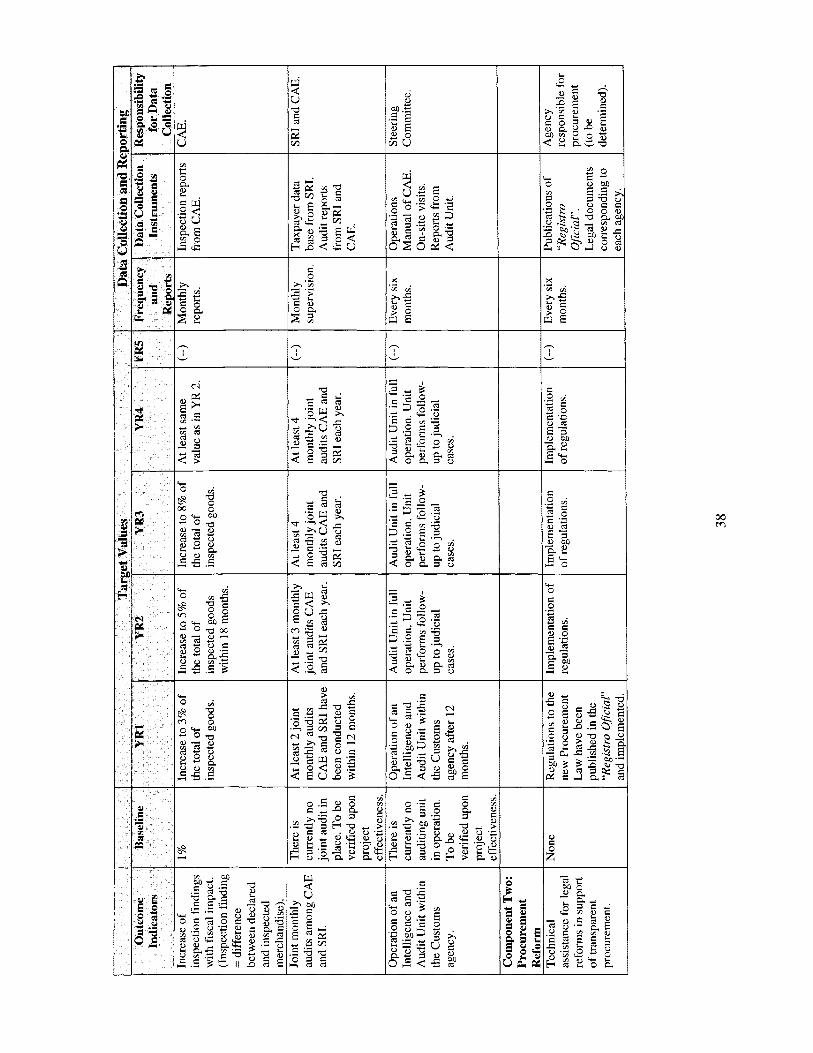

Figures: Figure 1. The Government’s Public Sector Reform Strategy Figure 2. Tax and Non-Tax Revenue o f Central Government (% GDP) and Important Tax Reform Efforts, 1964-2002 Figure 3. Government Effectiveness (LAC, 2000-2001)

Tables: Table 1. Project Development Objective and K e y Indicators Table 2. Criteria for Selection o f Components Table 3. Risks and Mitigation Measures Table 4. Progress in the Government’s Program supported by the FCCGL-I in 2003 Table 5. Governance indicators for Ecuador (World Bank Institute, WBI) Table 6: Related Wor ld Bank Projects Table 7. Projects and Programs o f Other Donors in the Area o f State Reform Table 8. Implementation Arrangements per Component Table 9. Project Structure

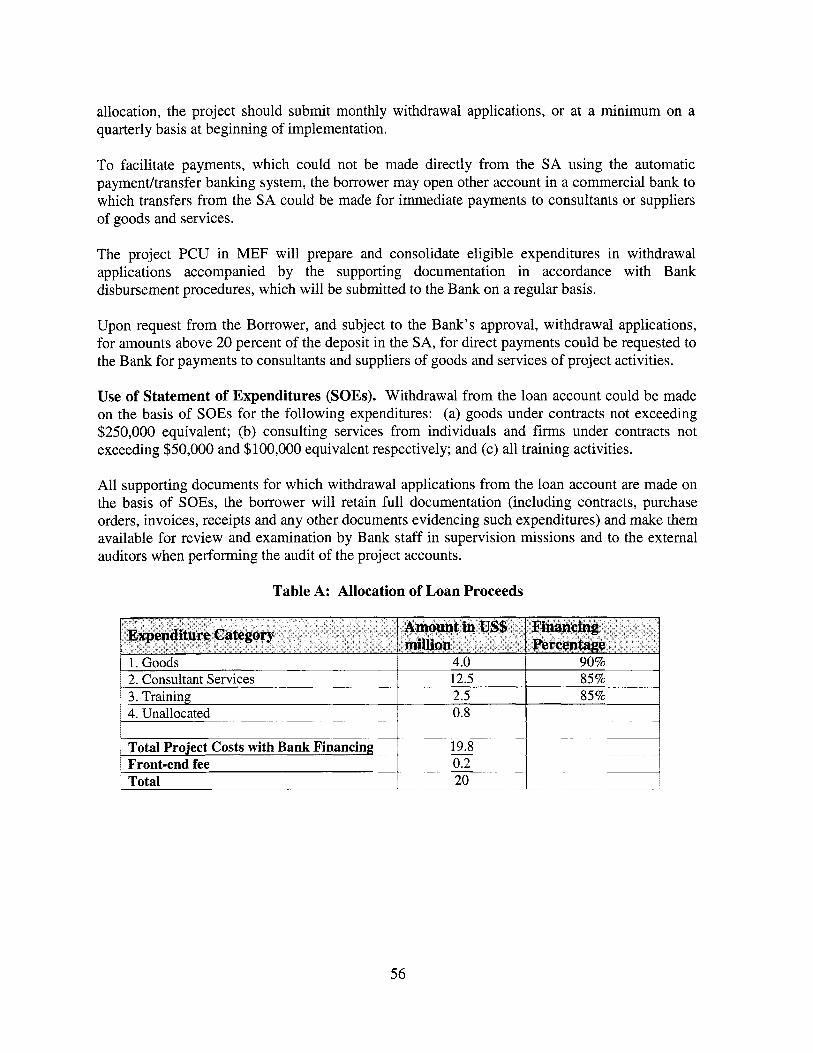

Procurement Tables: Table A: Allocation o f Proceeds

Boxes: Box 1. The Program for Economic Restructuring and Human Development (PEHRD)

5

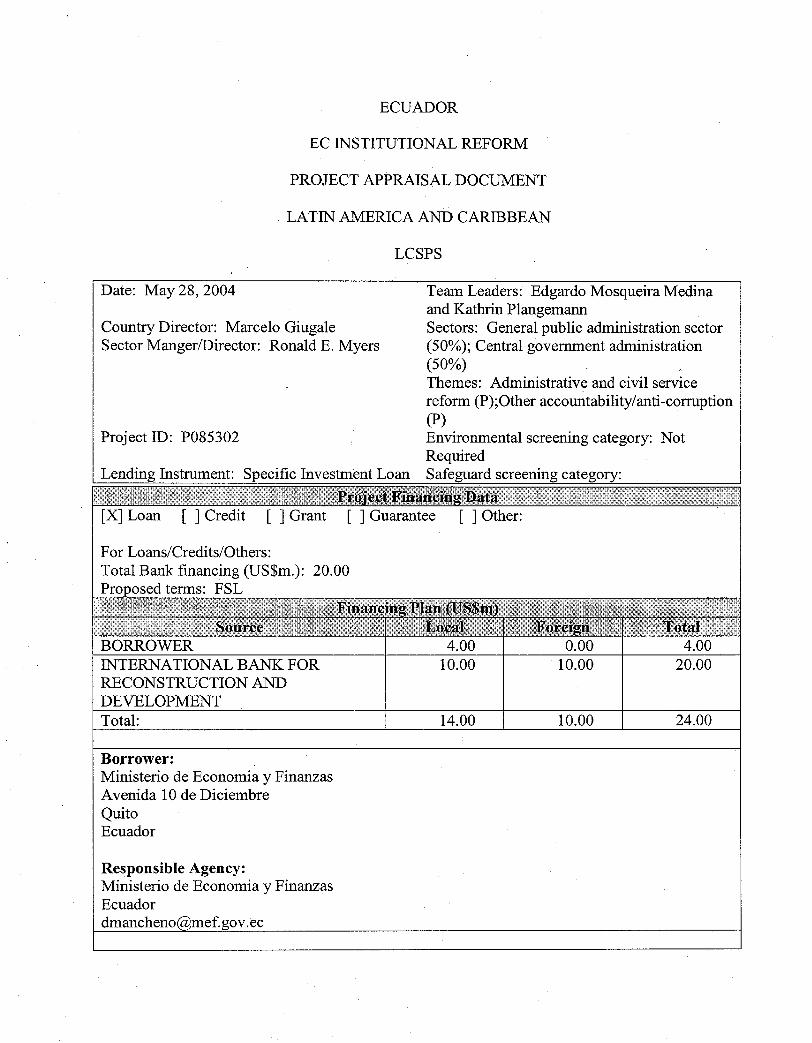

ECUADOR

EC INSTITUTIONAL REFORM

PROJECT APPRAISAL DOCUMENT

LATIN AMERICA AND CARIBBEAN

LCSPS

Date: May 28,2004 Team Leaders: Edgardo Mosqueira Medina

Country Director: Marcel0 Giugale Sectors: General public administration sector Sector Mangermirector: Ronald E. Myers (50%); Central government administration

(50%) Themes: Administrative and civil service reform (P);Other accountability/anti-corruption (P)

and Kathrin Plangemann

Project ID: P085302 Environmental screening category: Not Required

[X] Loan [ ] Credit [ ] Grant [ ] Guarantee [ ] Other:

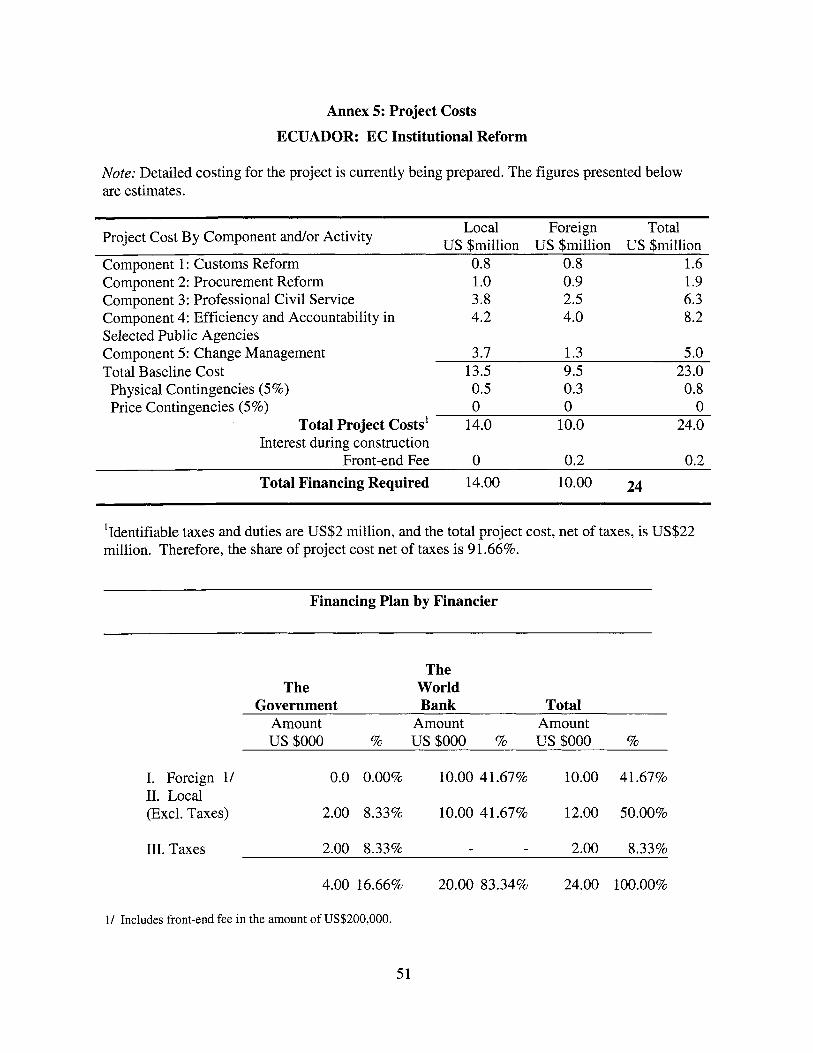

For Loans/Credits/Others: Total Bank financing (US$m.): 20.00

BORROWER 4.00 0.00 4.00 INTERNATIONAL BANK FOR 10.00 10.00 20.00 RECONSTRUCTION AND DEVELOPMENT Total: 14.00 10.00 24.00

Borrower: Ministerio de Economia y Finanzas Avenida 10 de Diciembre Quito Ecuador

Responsible Agency: Ministerio de Economia y Finanzas Ecuador [email protected]

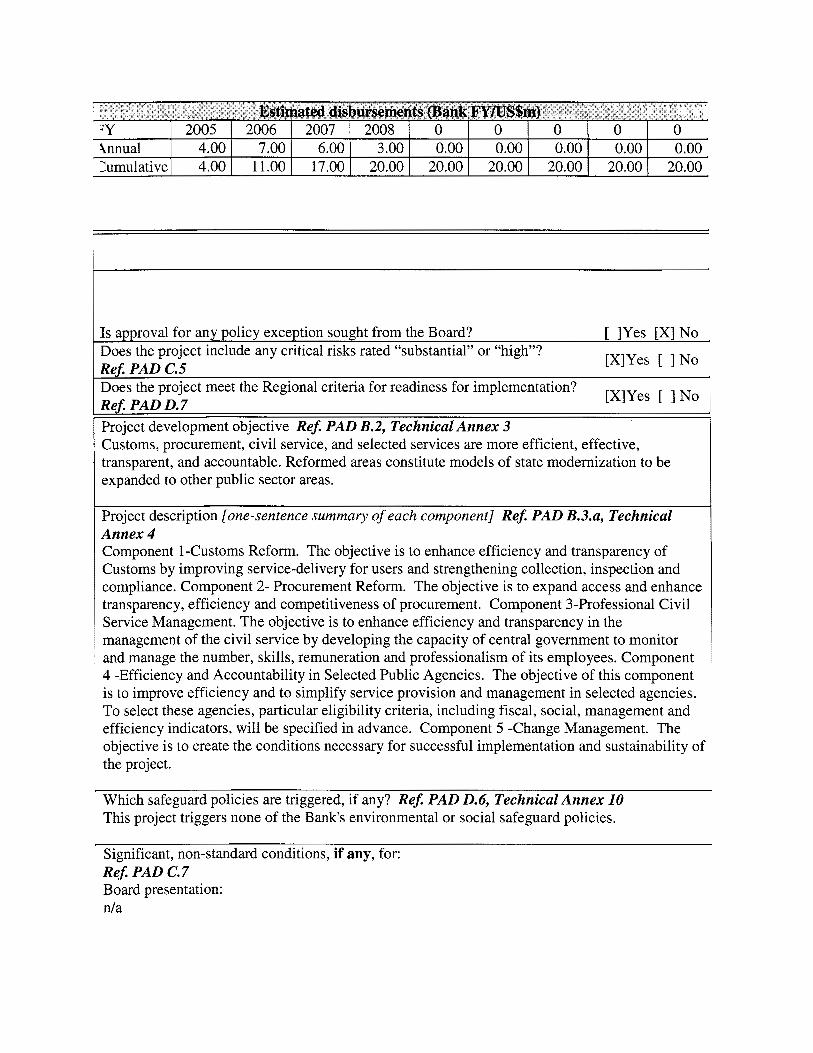

Estimated disbursements (Bank FY/US$m) ;Y 4nnual hmulative

2005 2006 2007 2008 0 0 0 0 0 4.00 7.00 6.00 3.00 0.00 0.00 0.00 0.00 0.00 4.00 11.00 17.00 20.00 20.00 20.00 20.00 20.00 20.00

I s approval for any policy exception sought from the Board? Does the project include any critical r isks rated “substantial” or “high”? Ref. PAD C.5 Does the project meet the Regional criteria for readiness for implementation? Ref. PAD 0.7

[ ]Yes [XINO

[XIYes [ ] N o

[XIYes [ ]No u

Project development objective Ref. PAD B.2, Technical Annex 3 Customs, procurement, c iv i l service, and selected services are more efficient, effective, transparent, and accountable. Reformed areas constitute models of state modernization to be expanded to other public sector areas.

Project description [one-sentence summary of each component] Ref. PAD B.3.a, Technical Annex 4 Component 1-Customs Reform. The objective i s to enhance efficiency and transparency o f Customs by improving service-delivery for users and strengthening collection, inspection and compliance. Component 2- Procurement Reform. The objective i s to expand access and enhance transparency, efficiency and competitiveness of procurement. Component 3-Professional Civ i l Service Management. The objective i s to enhance efficiency and transparency in the management of the civil service by developing the capacity o f central government to monitor and manage the number, skills, remuneration and professionalism o f i t s employees. Component 4 -Efficiency and Accountability in Selected Public Agencies. The objective o f this component i s to improve efficiency and to simplify service provision and management in selected agencies. To select these agencies, particular eligibility criteria, including fiscal, social, management and efficiency indicators, w i l l be specified in advance. Component 5 -Change Management. The objective i s to create the conditions necessary for successful implementation and sustainability o f the project.

Which safeguard policies are triggered, if any? Ref. PAD 0.6, Technical Annex 10 This project triggers none of the Bank’s environmental or social safeguard policies.

Significant, non-standard conditions, if any, for: Ref. PAD C.7 Board presentation: n/a

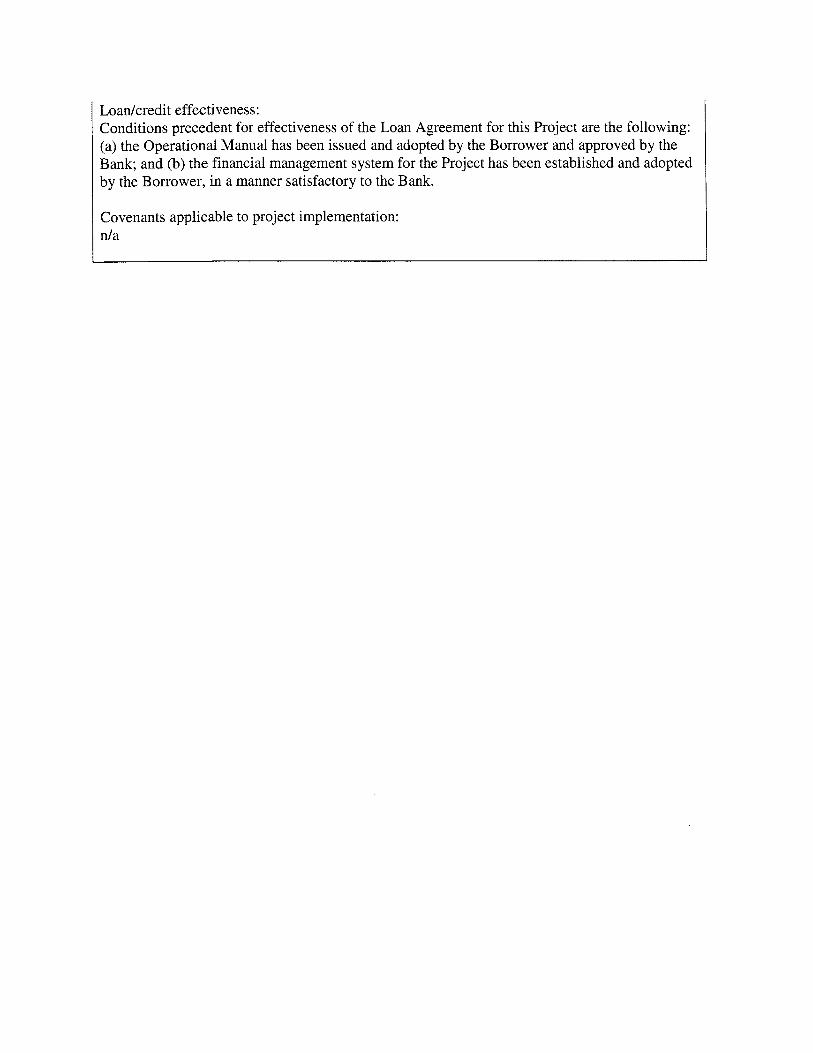

Loadcredit effectiveness: Conditions precedent for effectiveness o f the Loan Agreement for this Project are the following: (a) the Operational Manual has been issued and adopted b y the Borrower and approved by the Bank; and (b) the financial management system for the Project has been established and adopted by the Borrower, in a manner satisfactory to- the Bank.

Covenants applicable to project implementation: d a

A. STRATEGIC CONTEXT AND RATIONALE

1. Country and sector issues

Ecuador i s s t i l l recovering from one of the most serious economic crises in i t s history. Following the Asian crisis, a steep fall in oi l prices, and the negative impact of El Niiio, from 1997 onwards the country had serious problems balancing revenue and expenditures. In 1999, the fiscal deficit reached 6.7 percent o f GDP. Nearly half the banking sector, which in previous years had lent imprudently, collapsed. The severity o f the fiscal crisis, high inflation, a debt default in 1998, and the devaluation of the domestic currency, led the government to officially dollarize in January 2000. The social impact o f the crisis was considerable: unemployment rose from 10 to 15 percent and half a million people emigrated to find jobs abroad. The poverty rate increased by 7 percent in just the first two years o f the crisis (1998-99). Particularly severe was the impact on urban poverty, with the number of poor increasing from 1.1 mill ion to 3.5 million. Frequently changing governments and a high turn-over o f key ministers illustrate the corresponding political instability in the country.

Since 2000, however, Ecuador has achieved important progress in stabilizing the economy by restoring .price stability, growth, and confidence in the financial system. In 2003, growth reached 3 percent and inflation declined from 9.4 percent in 2002 to 6.1 percent. The NFPS primary surplus increased from 4.5 percent of GDP in 2002 to about 5 percent in 2003. As a result, the fiscal surplus doubled to about 2 percent of GDP. Real salary levels and unemployment rates are now back to 1998 levels.

Ecuador i s now at a critical juncture, facing crucial challenges and choices.’ I t can capitalize on the progress achieved in previous years and further commit itself to fiscal discipline, state reform, greater efficiency and transparency in public management, and improved service delivery. Or it can return to fiscal profligacy and speculate that international o i l prices wi l l remain high enough to avoid a new economic crisis.

The GutiCrrez Administration, which took office in January 2003, has committed itself to further economic, political, and governance reforms in the Program for Economic Restructuring and Human Development (PERHD; Annex 1). Under i t s economic pillar, the PERHD seeks to improve fiscal discipline, stimulate production and commerce, improve basic infrastructure, strengthen financial markets, and create more flexible and competitive labor markets. The social pillar pursues reforms in education, health, and social assistance to fight poverty more effectively. Finally, the governance pillar aims at combating corruption, improving public service delivery and transparency, and increasing overall security. The reform agenda i s supported by a Stand-By Arrangement (SBA) with the IMF.

’ See the analysis in the background policy notes prepared as part o f the preparation of this project: “Foundations for Institutional Reform in Ecuador,” Washington, D.C., May 2004.

6

Public sector reform and service improvement wi l l be key to overcoming the challenges highlighted in the PERHD. State capture, rent-seeking, weak accountability and transparency have adversely affected growth and poverty outcomes. The government loses an estimated one-third of i t s tax income through corruption, although recent reforms indicate the situation i s improving. Companies report having to pay an additional 15 percent o f total contract cost to win public bids. Low transparency also works as a regressive tax on the most poor and vulnerable which are often most seriously affected by corruption and poor service delivery. Households report paying bribes to public officials for selected public services in 41 percent of cases.2

A civil service marked by inefficiencies and a lack of transparency i s not only a burden for fiscal accounts, but also limits the capacity o f government to improve the coverage and quality o f public services. Dollarization imposes new constraints as fiscal policy i s the only means for steering the economy, underscoring the need to balance revenue and expenditures. If Ecuador wants to achieve economic growth, sustain dollarization, be competitive in the global economy, and reach the MDGs, it has to improve the efficiency and transparency o f public management and the quality of service delivery.

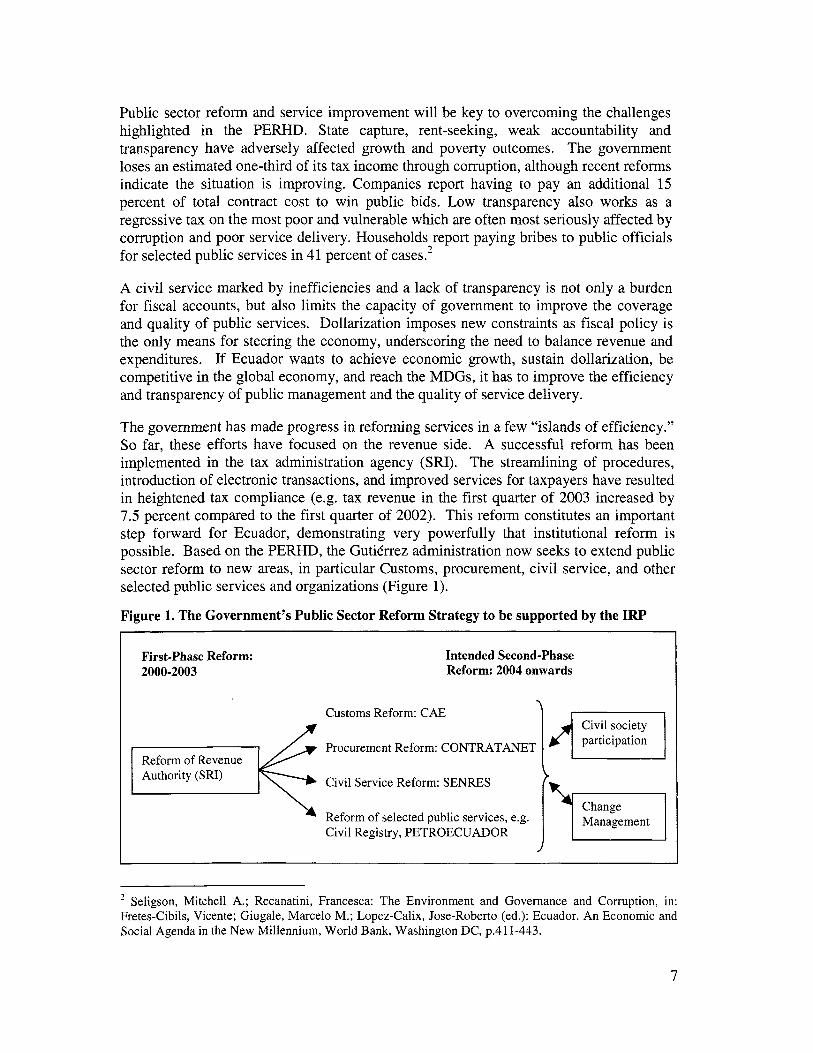

The government has made progress in reforming services in a few “islands o f efficiency.” So far, these efforts have focused on the revenue side. A successful reform has been implemented in the tax administration agency (SRI). The streamlining of procedures, introduction of electronic transactions, and improved services for taxpayers have resulted in heightened tax compliance (e.g. tax revenue in the first quarter of 2003 increased by 7.5 percent compared to the first quarter of 2002). This reform constitutes an important step forward for Ecuador, demonstrating very powerfully that institutional reform i s possible. Based on the PERHD, the Gutikrrez administration now seeks to extend public sector reform to new areas, in particular Customs, procurement, civil service, and other selected public services and organizations (Figure 1).

Figure 1. The Government’s Public Sector Reform Strategy to be supported by the IRP

First-Phase Reform: 2 0 0 0 - 2 0 0 3

Intended Second-Phase Reform: 2004 onwards

Customs Reform: CAE

Procurement Reform: CONTRATANET

Civi l Service Reform: SENRES

Reform o f selected public services, e.g. Civ i l Registry, PETROECUADOR

participation

Management

Authority (SRI)

Seligson, Mitchell A.; Recanatini, Francesca: The Environment and Governance and Corruption, in: Fretes-Cibils, Vicente; Giugale, Marcel0 M.; Lopez-Calix, Jose-Roberto (ed.): Ecuador. An Economic and Social Agenda i n the New Millennium, World Bank, Washington DC, p.411-443.

The reform o f the Ecuadorian Customs Administration (CAE) has a central role in this strategy. The CAE has designed a draft Modernization Plan that includes strengthening the role o f the SRI on the CAE board, greater access to crosscheck import bills and CAE taxpayer information, stiffer penalties for the understatement o f imports, and improved border controls (see Annex 4). These combined efforts w i l l ensure improved service- delivery for Customs clients, in particular for small and medium-sized enterprises that lose resources due to delays in Customs clearance and the payment of bribes. Customs reform wi l l not only reduce fiscal losses ‘due to inefficiencies and corruption, but also facilitate trade integration and competitiveness-a pre-condition to conclude the Free Trade Agreements (FTA) with the United States, MERCOSUR and the EU in 2005.

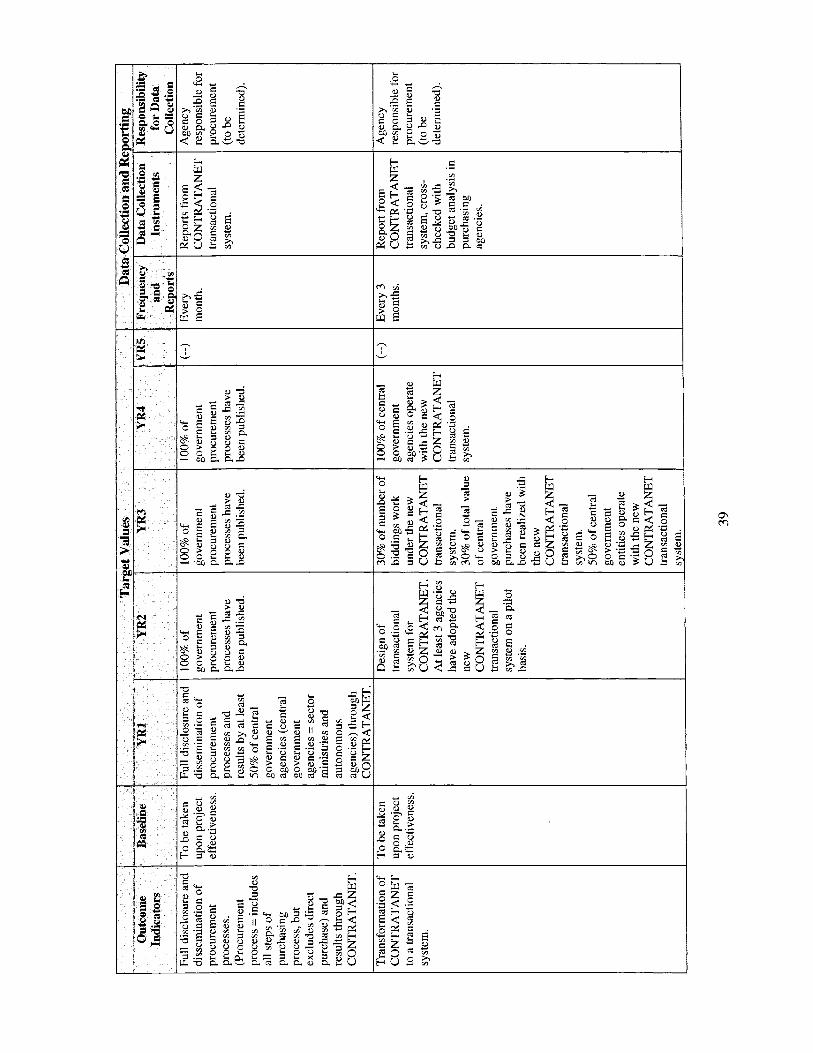

Another important area of service delivery improvement i s to create a transparent and efficient procurement system, where corruption now leads to a loss of public resources. In 2003, an Executive Decree made the use of the electronic procurement system CONTRATANET mandatory for all public agencies. Developed under the leadership o f the Anti-Corruption Commission (CCCC) - a constitutionally mandated organization composed of c iv i l society representatives - all public institutions now have to publish electronically their procurement offers and the documents underlying the procurement process. Once CONTRATANET i s transformed into a transactional system, bidding documents w i l l be published, and bidders and their offers wi l l be registered. The new draft Procurement Law and the recently passed Law on Access to Information wi l l also help eliminate exemptions and loopholes, and define clear standards and reference prices. The state o i l company Petroecuador, which accounts for 70 percent o f government purchases, has been selected as a pilot entity to introduce the new transactional system.

Personnel management reform i s another key component of the reform agenda. In 2003, Congress approved a Civ i l Service and Salary Unification Law. The National Technical Secretariat for Human Resources Development and Remuneration in the Public Sector (SENRES) and the Human Resources Administrative Units (URHIs) in each government agency are responsible for implementing the new law. Management reforms wi l l help the government to regain control over the wage bill, and contribute to a more effective, efficient, professional and accountable civil service.

The government has also committed to reforming selected services that have a broad- based impact on citizens, such as the civil registry, small business registration, the authorizations provided by the national agency for food and drug administration (Registro Suniturio) and selected social programs. More efficient and transparent service-delivery would not only reduce transaction costs, but also barriers to market entry, particularly for small and medium-sized businesses, leading to greater competition.

While the benefits of state reform are evident, the government’s strategy faces serious challenges. Efficiency-enhancing reform threatens the interests o f those who have a stake in the status quo. Whereas the “losers” of the intended reforms often are a concentrated group, the “winners” - such as general citizens and taxpayers - are dispersed and therefore difficult to mobilize. State reform needs to produce some quick and visible results to demonstrate the feasibility and benefits o f reform. I t requires

8

strategic decision-making, careful sequencing and a close engagement with stakeholders through change management. I t also demands political leadership, commitment and ownership to design, implement, and sustain reform.

2. Rationale for Bank involvement

Bank involvement i s tailored to respond closely both to government requests to support key reforms and to the Bank’s country assistance strategy expressed in the CAS. In particular, three factors have generated a positive momentum for reform and the Bank’s involvement in Ecuador. First, following the SRI reforms, demand i s growing to tackle the expenditure and efficiency side of the public sector, particularly in procurement and civ i l service management. Second, there i s an important shift in the incentive framework facing policy makers. Trade, global competition and dollarization send signals to authorities to reform the public sector and achieve transparency and efficiency, rather than relying mainly on oi l income. Finally, the Ministry o f Economy and Finance -under stronger and more stable leadership than in previous governments - i s committed to state reform, primarily for efficiency and fiscal reasons, helping build strong ownership.

The Bank i s seizing the momentum for reform and w i l l support the government in i t s reform efforts. The close policy dialogue across al l major development areas has been reflected in the CAS, the Ecuador Policy Notes and the expanding lending portfolio, particularly the two Programmatic Loans related to this project. This gives the Bank not only a strong role as a “knowledge bank” in Ecuador, but also the role of a catalyst for further reforms, especially in politically sensitive and complex areas. The Bank can leverage support from other donors, such as U S AID, and w i l l coordinate implementation closely with other agencies such as the IADB (refer to Annex 2). The Bank can also share knowledge and experiences from other countries and foster a debate on new and innovative ways of designing and implementing institutional reforms. Finally, the Bank’s previous involvement in institutional reforms in Ecuador includes important lessons learned from an earlier institutional reform project, MOSTA, carried out from 1996-2000.

3. Higher level objectives to which the project contributes

The higher level objective of the operation i s to contribute to greater transparency, efficiency and accountability by helping to improve public revenue, expenditure management capacity and service delivery. The proposed project supports the Government in the implementation of the PERHD (Annex l), which seeks to fight corruption and improve public service delivery and transparency in Customs, procurement, civil service, and selected services.

The proposed project also supports the objectives o f the 2003 Ecuador CAS. I t i s consistent with the third pillar of the CAS aimed at strengthening governance and helping officials build an accountable and efficient government that provides services accessible to all Ecuadorians. Likewise, i t contributes to i t s f i rst pillar, which aims at consolidating the macroeconomic framework to lay the foundation for sustainable growth and poverty reduction. In addition, i t builds on the CFAA and CPAR recommendations, which have

9

shown that the lack of transparency and efficiency are key obstacles to achieving social and economic development.

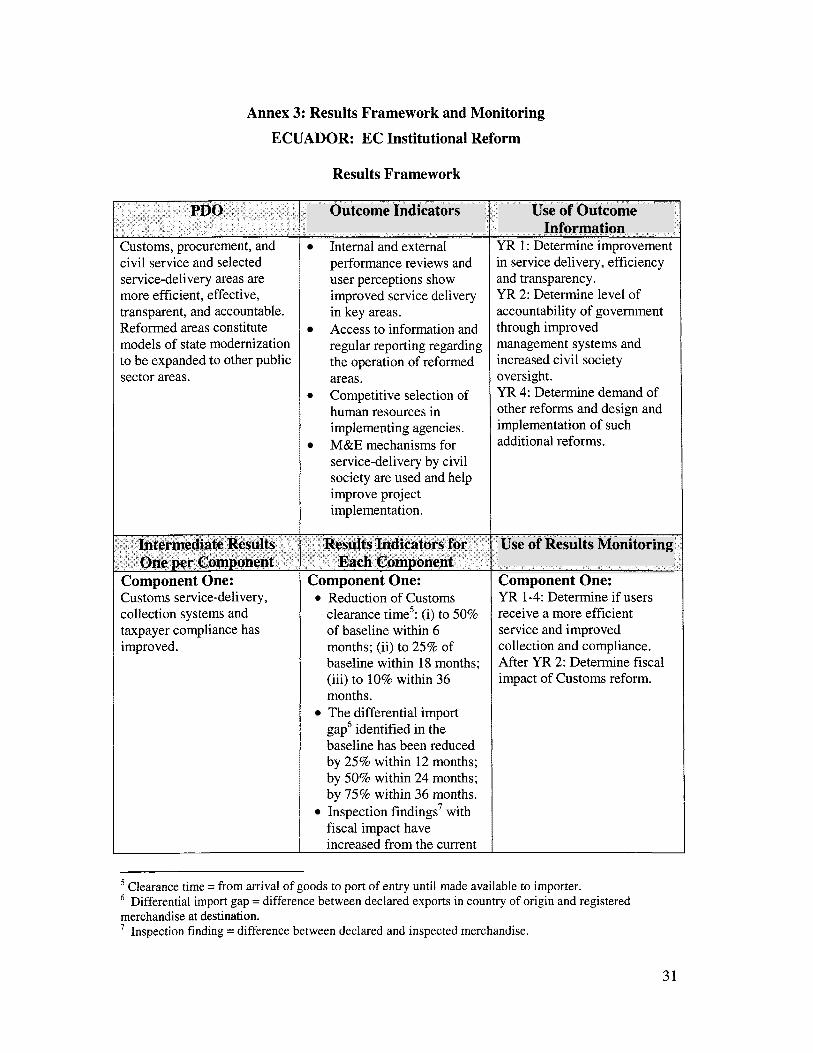

Project Development Objective

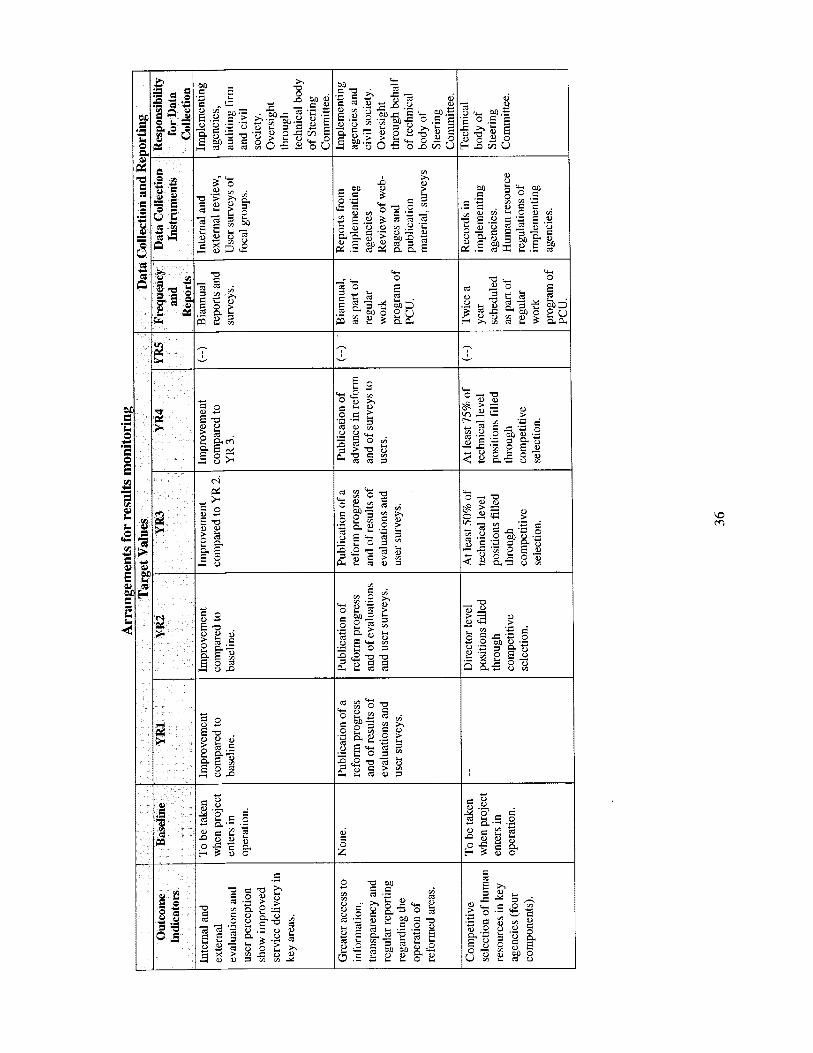

Key Indicators

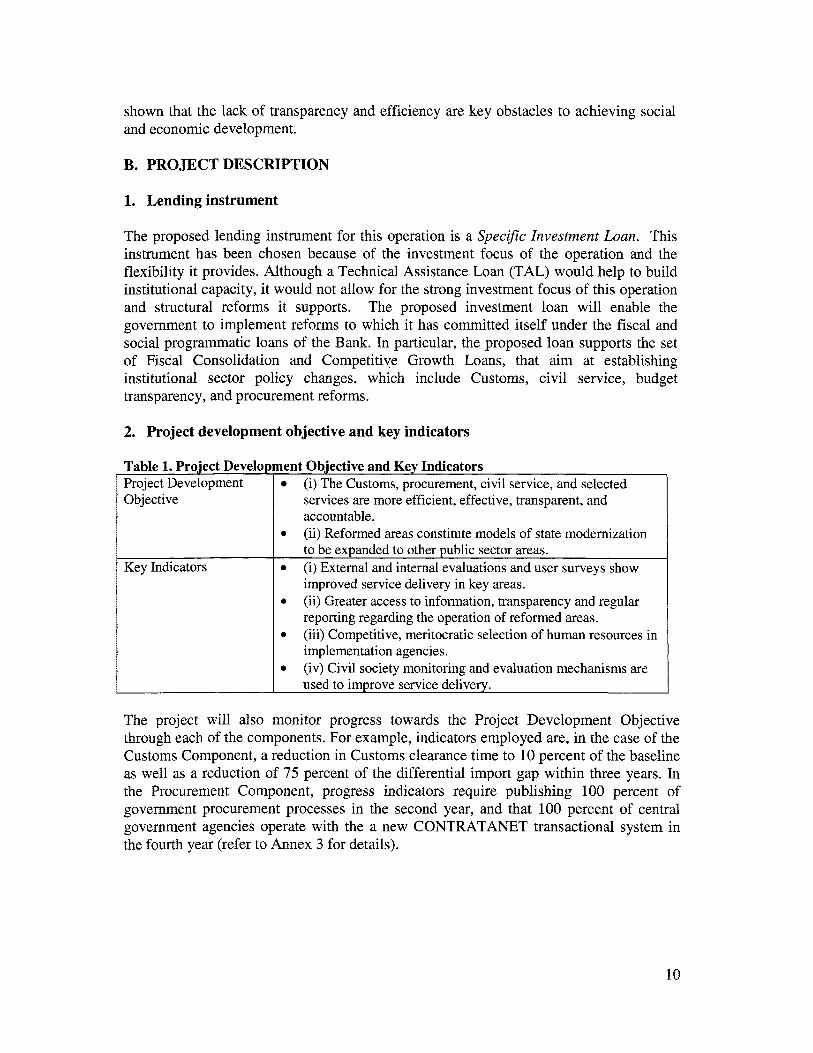

B. PROJECT DESCRIPTION

(i) The Customs, procurement, civi l service, and selected services are more efficient, effective, transparent, and accountable. (ii) Reformed areas constitute models o f state modernization to be expanded to other public sector areas. (i) External and internal evaluations and user surveys show improved service delivery in key areas. (ii) Greater access to information, transparency and regular reporting regarding the operation o f reformed areas. (iii) Competitive, meritocratic selection o f human resources in implementation agencies. (iv) Civ i l society monitoring and evaluation mechanisms are used to improve service delivery.

0

0

0

0

0

1. Lending instrument

The proposed lending instrument for this operation i s a Specific Investment Loan. This instrument has been chosen because of the investment focus o f the operation and the flexibility i t provides. Although a Technical Assistance Loan (TAL) would help to build institutional capacity, i t would not allow for the strong investment focus o f this operation and structural reforms i t supports. The proposed investment loan w i l l enable the government to implement reforms to which it has committed itself under the fiscal and social programmatic loans of the Bank. In particular, the proposed loan supports the set of Fiscal Consolidation and Competitive Growth Loans, that aim at establishing institutional sector policy changes, which include Customs, civil service, budget transparency, and procurement reforms.

2. Project development objective and key indicators

The project wi l l also monitor progress towards the Project Development Objective through each of the components. For example, indicators employed are, in the case of the Customs Component, a reduction in Customs clearance time to 10 percent of the baseline as well as a reduction of 75 percent of the differential import gap within three years. In the Procurement Component, progress indicators require publishing 100 percent o f government procurement processes in the second year, and that 100 percent of central government agencies operate with the a new CONTRATANET transactional system in the fourth year (refer to Annex 3 for details).

10

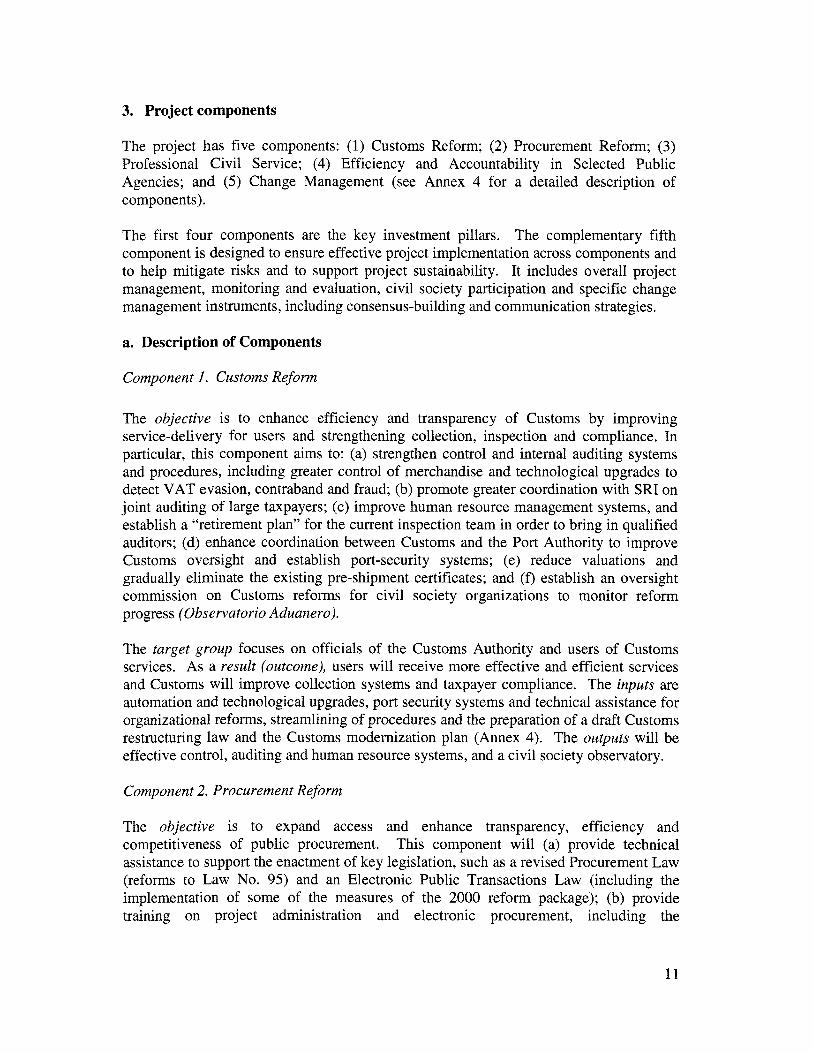

3. Project components

The project has five components: (1) Customs Reform; (2) Procurement Reform; (3) Professional Civ i l Service; (4) Efficiency and Accountability in Selected Public Agencies; and (5) Change Management (see Annex 4 for a detailed description o f components).

The first four components are the key investment pillars. The complementary fifth component i s designed to ensure effective project implementation across components and to help mitigate risks and to support project sustainability. I t includes overall project management, monitoring and evaluation, civil society participation and specific change management instruments, including consensus-building and communication strategies.

a. Description of Components

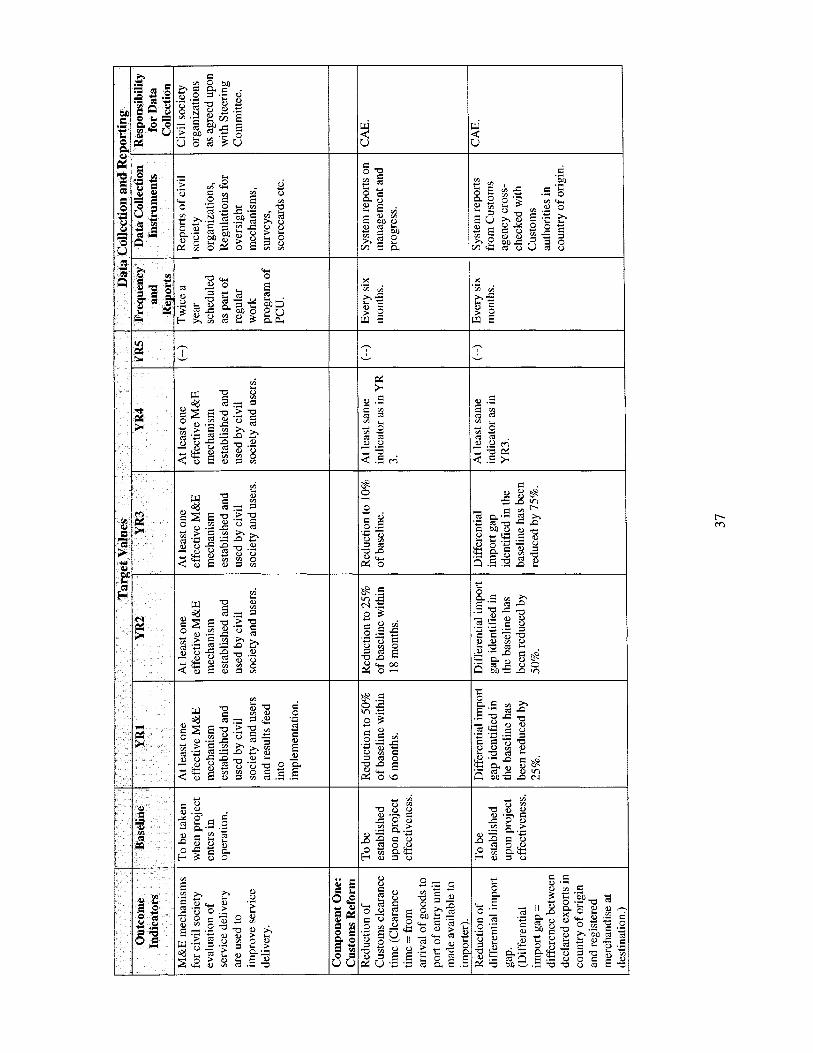

Component 1. Customs Reform

The objective i s to enhance efficiency and transparency of Customs by improving service-delivery for users and strengthening collection, inspection and compliance. In particular, this component aims to: (a) strengthen control and internal auditing systems and procedures, including greater control of merchandise and technological upgrades to detect VAT evasion, contraband and fraud; (b) promote greater coordination with SRI on joint auditing of large taxpayers; (c) improve human resource management systems, and establish a “retirement plan” for the current inspection team in order to bring in qualified auditors; (d) enhance coordination between Customs and the Port Authority to improve Customs oversight and establish port-security systems; (e) reduce valuations and gradually eliminate the existing pre-shipment certificates; and (f) establish an oversight commission on Customs reforms for c iv i l society organizations to monitor reform progress (Obsewatorio Aduanero).

The target group focuses on officials of the Customs Authority and users of Customs services. As a result (outcome), users w i l l receive more effective and efficient services and Customs w i l l improve collection systems and taxpayer compliance. The inputs are automation and technological upgrades, port security systems and technical assistance for organizational reforms, streamlining of procedures and the preparation o f a draft Customs restructuring law and the Customs modernization plan (Annex 4). The outputs wi l l be effective control, auditing and human resource systems, and a c iv i l society observatory.

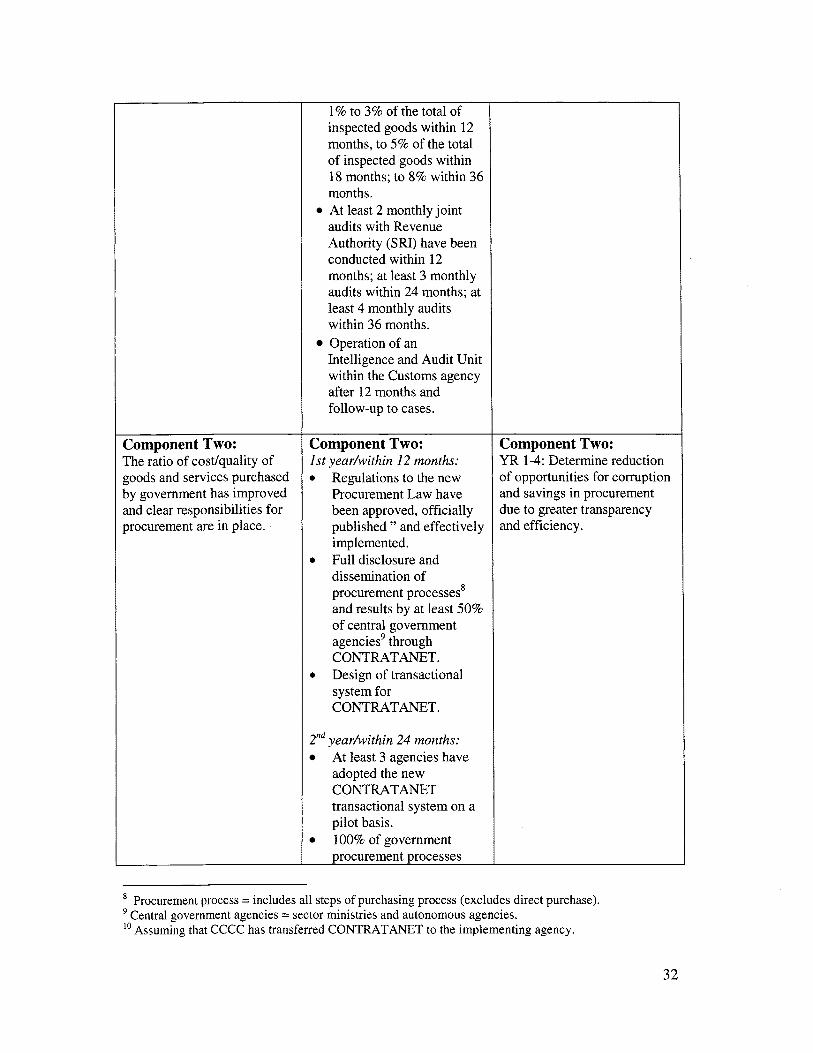

Component 2. Procurement Reform

The objective i s to expand access and enhance transparency, efficiency and competitiveness of public procurement. This component w i l l (a) provide technical assistance to support the enactment o f key legislation, such as a revised Procurement Law (reforms to Law No. 95) and an Electronic Public Transactions Law (including the implementation of some of the measures o f the 2000 reform package); (b) provide training on project administration and electronic procurement, including the

11

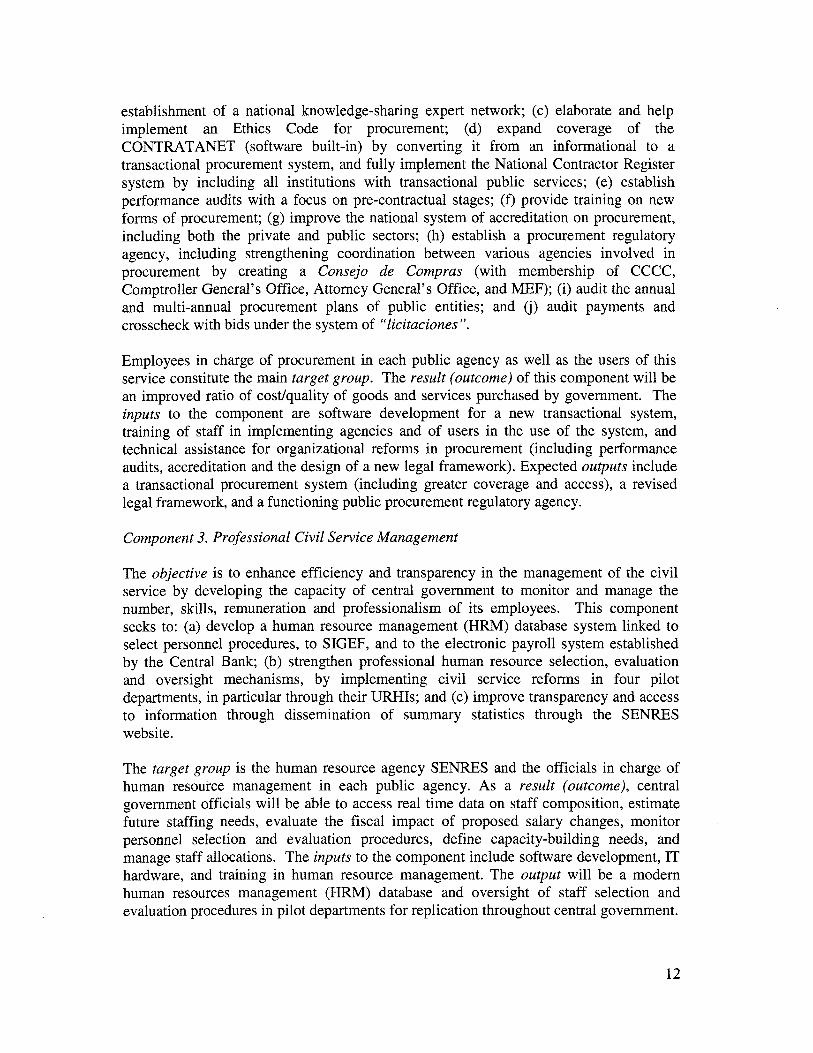

establishment of a national knowledge-sharing expert network; (c) elaborate and help implement an Ethics Code for procurement; (d) expand coverage of the CONTRATANET (software built-in) by converting it from an informational to a transactional procurement system, and fully implement the National Contractor Register system by including all institutions with transactional public services; (e) establish performance audits with a focus on pre-contractual stages; (f) provide training on new forms of procurement; (8) improve the national system o f accreditation on procurement, including both the private and public sectors; (h) establish a procurement regulatory agency, including strengthening coordination between various agencies involved in procurement by creating a Consejo de Compras (with membership of CCCC, Comptroller General’s Office, Attorney General’s Office, and MEF); (i) audit the annual and multi-annual procurement plans of public entities; and (i) audit payments and crosscheck with bids under the system of “licitaciones ”.

Employees in charge of procurement in each public agency as well as the users of this service constitute the main target group. The result (outcome) of this component wi l l be an improved ratio of cost/quality of goods and services purchased by government. The inputs to the component are software development for a new transactional system, training o f staff in implementing agencies and of users in the use of the system, and technical assistance for organizational reforms in procurement (including performance audits, accreditation and the design of a new legal framework). Expected outputs include a transactional procurement system (including greater coverage and access), a revised legal framework, and a functioning public procurement regulatory agency.

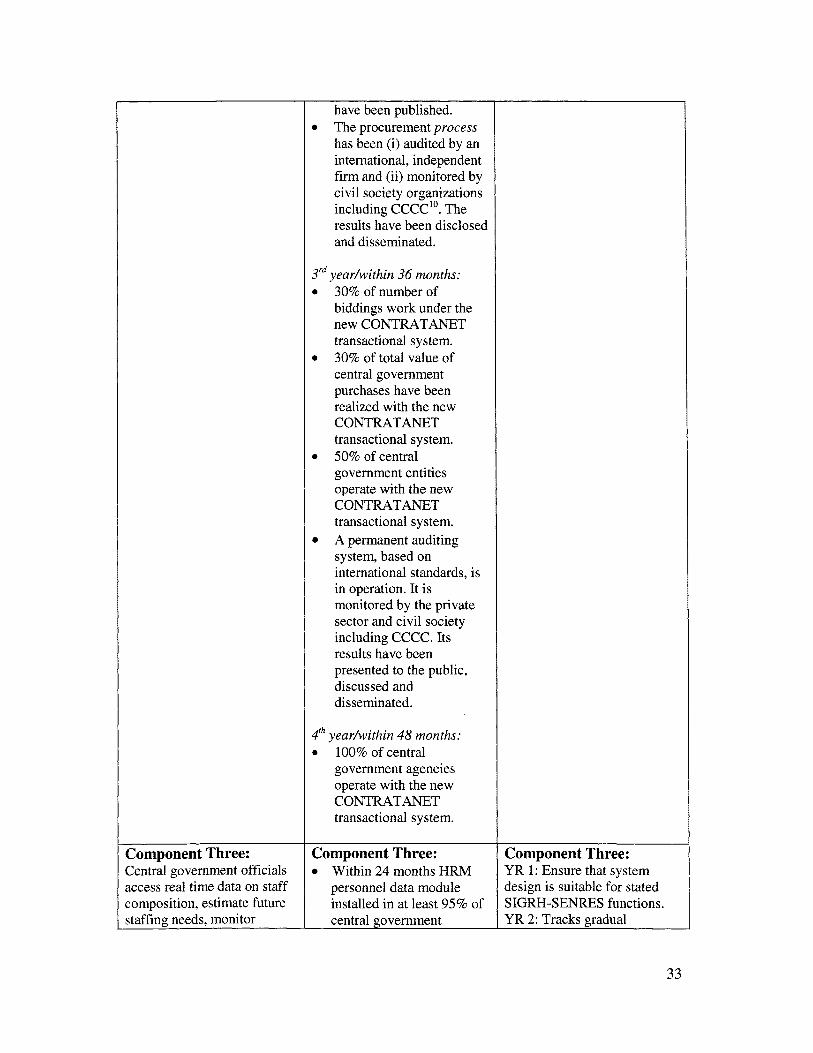

Component 3. Professional Civil Service Management

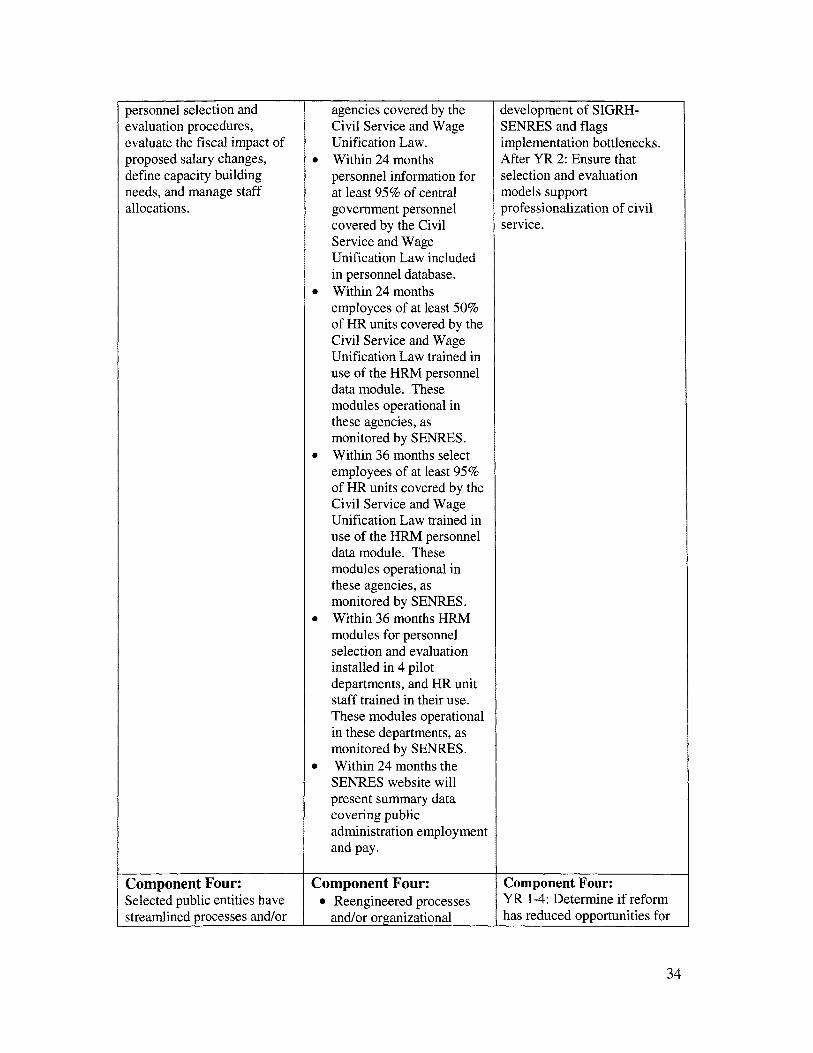

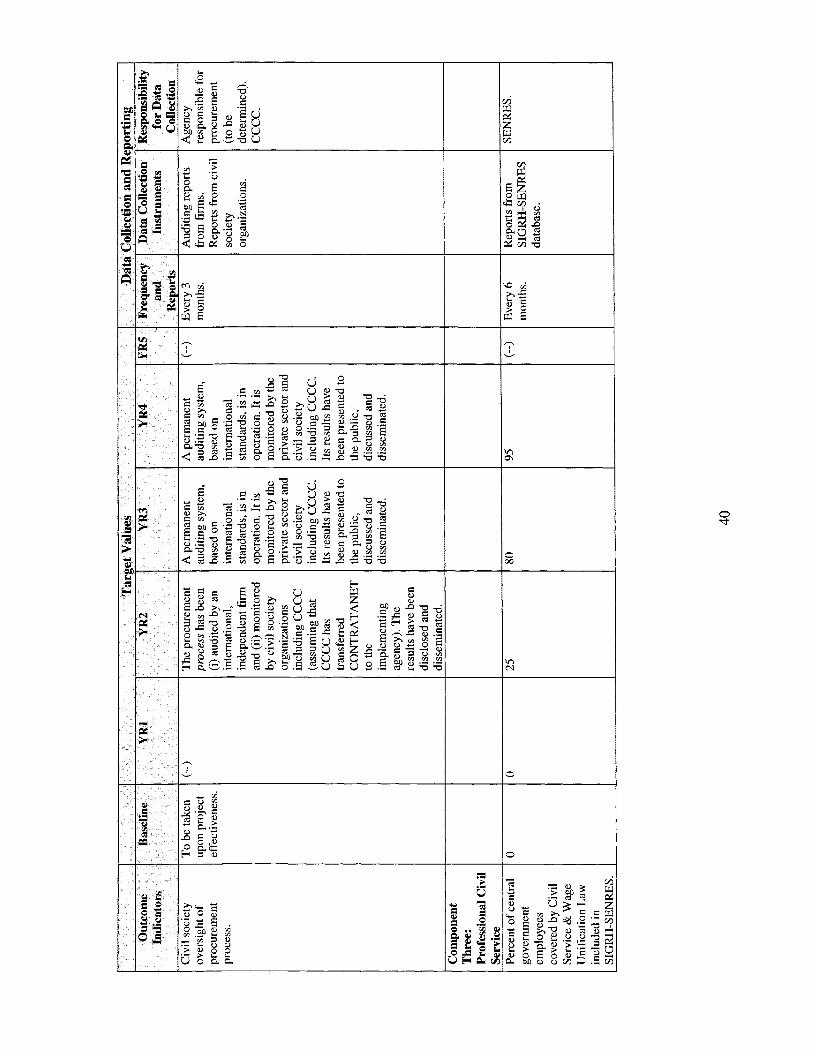

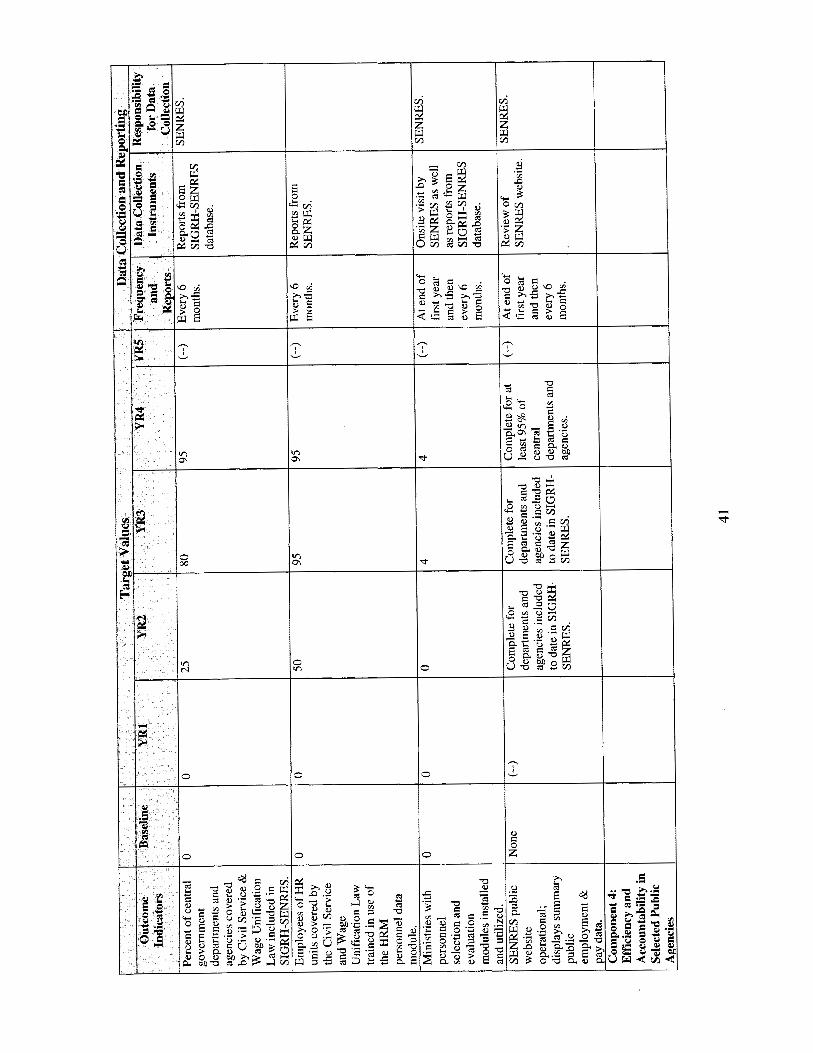

The objective i s to enhance efficiency and transparency in the management of the c iv i l service by developing the capacity of central government to monitor and manage the number, skills, remuneration and professionalism of i t s employees. This component seeks to: (a) develop a human resource management (HRM) database system linked to select personnel procedures, to SIGEF, and to the electronic payroll system established by the Central Bank; (b) strengthen professional human resource selection, evaluation and oversight mechanisms, by implementing c iv i l service reforms in four pilot departments, in particular through their URHIs; and (c) improve transparency and access to information through dissemination of summary statistics through the SENRES websi te.

The target group i s the human resource agency SENRES and the officials in charge o f human resource management in each public agency. As a result (outcome), central government officials w i l l be able to access real time data on staff composition, estimate future staffing needs, evaluate the fiscal impact o f proposed salary changes, monitor personnel selection and evaluation procedures, define capacity-building needs, and manage staff allocations. The inputs to the component include software development, IT hardware, and training in human resource management. The output wi l l be a modern human resources management (HRM) database and oversight o f staff selection and evaluation procedures in pilot departments for replication throughout central government.

12

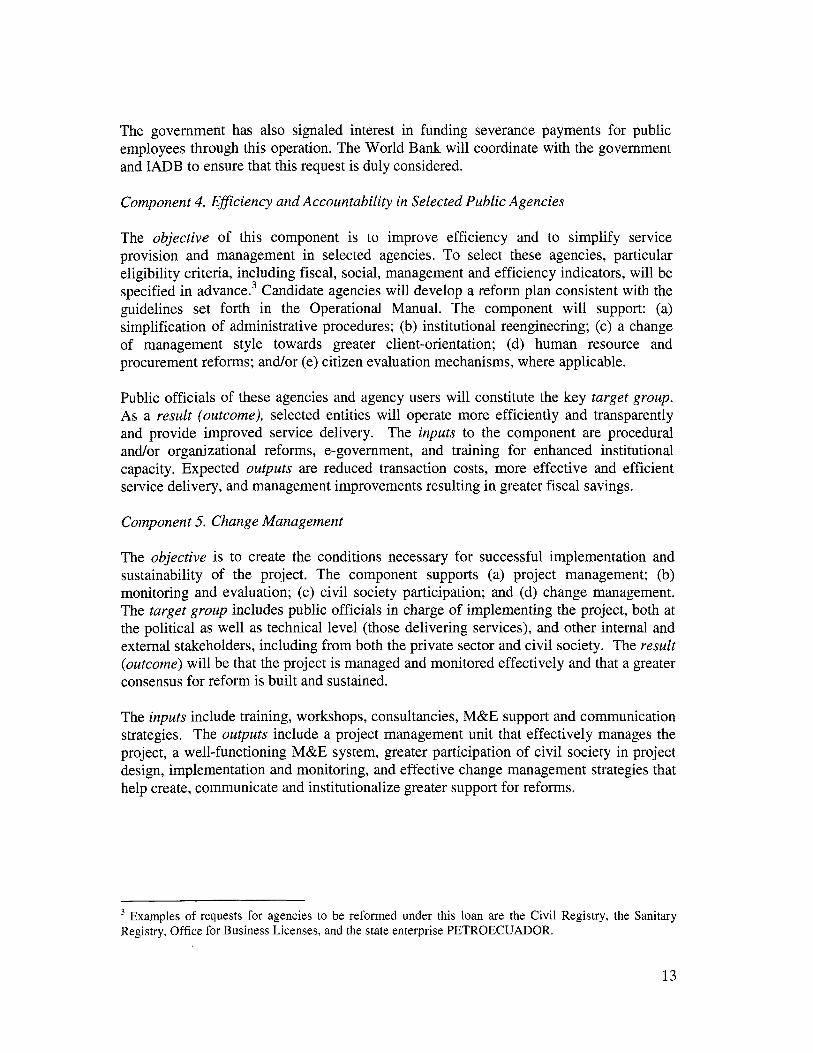

The government has also signaled interest in funding severance payments for public employees through this operation. The World Bank wi l l coordinate with the government and IADB to ensure that this request i s duly considered.

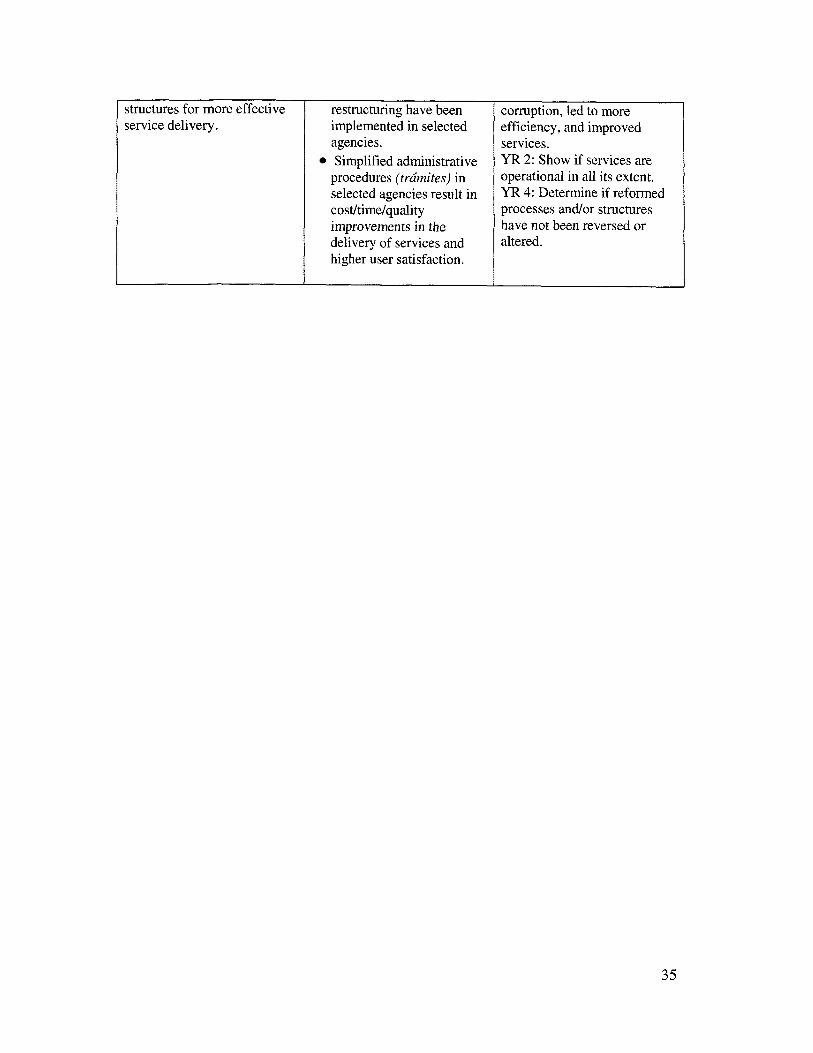

Component 4. EfSiciency and Accountability in Selected Public Agencies

The objective of this component i s to improve efficiency and to simplify service provision and management in selected agencies. To select these agencies, particular eligibility criteria, including fiscal, social, management and efficiency indicators, wi l l be specified in ad~ance.~ Candidate agencies wi l l develop a reform plan consistent with the guidelines set forth in the Operational Manual. The component w i l l support: (a) simplification of administrative procedures; (b) institutional reengineering; (c) a change of management style towards greater client-orientation; (d) human resource and procurement reforms; and/or (e) citizen evaluation mechanisms, where applicable.

Public officials of these agencies and agency users w i l l constitute the key target group. As a result (outcome), selected entities wi l l operate more efficiently and transparently and provide improved service delivery. The inputs to the component are procedural and/or organizational reforms, e-government, and training for enhanced institutional capacity. Expected outputs are reduced transaction costs, more effective and efficient service delivery, and management improvements resulting in greater fiscal savings.

Component 5. Change Management

The objective i s to create the conditions necessary for successful implementation and sustainability of the project. The component supports (a) project management; (b) monitoring and evaluation; (c) civil society participation; and (d) change management. The target group includes public officials in charge of implementing the project, both at the political as well as technical level (those delivering services), and other internal and external stakeholders, including from both the private sector and civil society. The result (outcome) wi l l be that the project i s managed and monitored effectively and that a greater consensus for reform i s built and sustained.

The inputs include training, workshops, consultancies, M&E support and communication strategies. The outputs include a project management unit that effectively manages the project, a well-functioning M&E system, greater participation o f civil society in project design, implementation and monitoring, and effective change management strategies that help create, communicate and institutionalize greater support for reforms.

Examples of requests for agencies to be reformed under this loan are the Civil Registry, the Sanitary Registry, Office for Business Licenses, and the state enterprise PETROECUADOR.

13

b. Selection of Components: Strategy

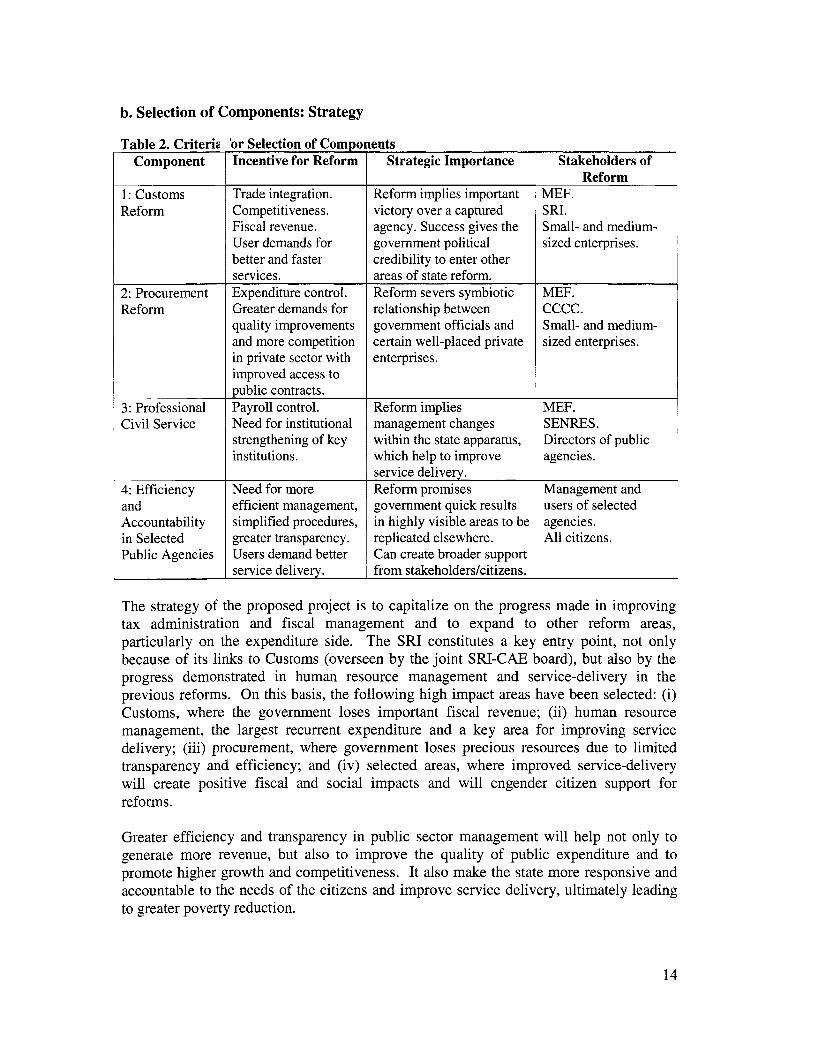

Table 2. Criteria Component

1: Customs Reform

2: Procurement Reform

~

3: Professional Civi l Service

4: Efficiency and Accountability in Selected Public Agencies

or Selection of Compo Incentive for Reform

Trade integration. Competitiveness. Fiscal revenue. User demands for better and faster services. Expenditure control. Greater demands for quality improvements and more competition in private sector with improved access to mb l ic contracts. Payroll control. Need for institutional strengthening of key institutions.

Need for more efficient management, simplified procedures, greater transparency. Users demand better service delivery.

ents Strategic Importance

Reform implies important victory over a captured agency. Success gives the government political credibility to enter other areas of state reform. Reform severs symbiotic relationship between government officials and certain well-placed private enterprises.

Reform implies management changes within the state apparatus, which help to improve service delivery. Reform promises government quick results in highly visible areas to be replicated elsewhere. Can create broader support from stakeholderskitLzens.

Stakeholders of Reform

MEF. SRI. Small- and medium- sized enterprises.

MEF. cccc. Small- and medium- sized enterprises.

MEF. SENRES. Directors of public agencies.

Management and users o f selected agencies. All citizens.

The strategy of the proposed project i s to capitalize o n the progress made in improving tax administration and fiscal management and to expand to other re form areas, particularly on the expenditure side. The S R I constitutes a key entry point, not only because of i t s l inks to Customs (overseen by the jo in t SRI-CAE board), but also by the progress demonstrated in human resource management and service-delivery in the previous reforms. On this basis, the following high impact areas have been selected: (i) Customs, where the government loses important f iscal revenue; (ii) human resource management, the largest recurrent expenditure and a key area fo r improv ing service delivery; (iii) procurement, where government loses precious resources due to l imi ted transparency and efficiency; and (iv) selected areas, where improved service-delivery wi l l create positive fiscal and social impacts and wil l engender cit izen support for reforms.

Greater efficiency and transparency in publ ic sector management wi l l help not on ly to generate more revenue, but also to improve the quality of publ ic expenditure and to promote higher growth and competitiveness. I t also make the state more responsive and accountable to the needs of the citizens and improve service delivery, ult imately leading to greater poverty reduction.

14

The strategy of the project reflects the fact that state reform requires strong champions. The idea i s to create winners of reform - efficiency and transparency champions - that have an interest in maintaining the changes promoted. The operation takes into account the fact that the private sector (particularly small-and medium sized enterprises) and specific public agencies such as the Anti-Corruption Commission (CCCC) and MEF are key players with an interest in transparency and efficiency reforms. Once these stakeholders obey the new rules o f the game, they w i l l raise the cost for those players who have incentives to break the new rules. The involvement of civil society i s intended to create and expand pressure for reform implementation. B y creating civil society oversight committees and monitoring tools (such as citizen scorecards in procurement and selected service-delivery), and by promoting the use o f participatory Public Expenditure Tracking Surveys (PETS), users and citizens at large w i l l have formal means to increase their leverage over policymakers and hold them accountable for the results produced.

State reform also requires sufficient capacity and demand for change. Civ i l service reform wi l l improve this capacity within the public administration. Both internal and external change thus need to work in coordinated fashion to ensure that incentives are mutually reinforcing. This requires a careful sequencing o f reforms, based upon an incremental strategy, starting in a few high impact reform areas and then expanding to other areas on the basis of visible reform progress. The goal i s to create sustainable reform and, through institutional strengthening and change management, help government achieve the intended second-level o f reform - one that not only focuses on raising more revenue, but also on a more effective deployment o f expenditures.

Given the expected high level of vested interests and potential opposition, the operation i s applying innovative reform management tools to build greater consensus and buy-in for the proposed reforms through a strong emphasis on change management (Component 5). On the basis o f a diagnostics o f the status quo, obstacles and the creation of a sense of urgency, this component w i l l help engage key different stakeholders to develop a shared vision of reforms. I t w i l l also build greater consensus and communicate the benefits and progress of reforms to institutionalize reforms, ultimately helping create greater sustainability o f on-going and increase demand for additional reforms.

c. Sector Issues

The operation tackles the principal problems o f inefficient provision o f services and the loss of fiscal revenue due to inefficiencies and corruption. In Customs, procurement, and select public services efficiency w i l l be promoted through the streamlining of procedures and organizational reengineering. This w i l l create savings in service delivery and reduce opportunities for corruption. This i s complemented by the use o f electronic instruments and procedures (HRM database, E-government, E-services) that reduce the possibility for individuals to alter or evade the rules of the game, thus raising the cost of corruption.

At the same time, the reforms w i l l create and enhance competition and thereby reduce rent-seeking opportunities that originate in lack o f transparency. B y broadening access to services, in particular with regards to procurement, small and medium-sized enterprises

15

wi l l benefit from their participation in doing business with the state. Customs reform i s also intended to achieve more trade and competitiveness in the domestic arena. The resulting competition w i l l create incentives to adhere to clearly defined rules o f the game.

Lessons learned In-depth analytical work i s needed to ensure high quality and relevance o f project design.

The operation w i l l also heighten taxpayer compliance by promoting stronger enforcement and closing loop-holes. In the Customs component, for instance, joint audits by SRI and CAE wi l l make tax evasion more difficult for companies. In procurement, bidders can only qualify if they have paid all taxes that are due. The creation o f social accountability mechanisms such as civil society oversight committees, public expenditure tracking surveys (PETS), management contracts and citizen scorecards w i l l help give greater voice to civil society and increase demand for reforms.

Application in project preparation Extensive policy notes have been prepared parallel to project preparation.

4. Lessons learned and reflected in the project design

In a high-risk environment, i t i s necessary to design and implement a strong strategy to reduce risks and to build project sustainability.

The project pioneers change management in Ecuador through a strategy o f stakeholder engagement to reduce resistance, risks and enhance sustainability of reforms.

I reform in the executive and judiciary.

~~

Broad-based reforms are often too ambitious and need to The project focuses on key agencies instead of broader be better targeted.

Institutional reforms, especially in an environment marked by strong state capture, need to be tackled incrementally.

Improving the supply side o f reforms through institutional strengthening in selected reform agencies should be supplemented by increasing demand for reforms through by engaging civil society and other stakeholders.

~ ~~~

The operation i s built on a sequencing strategy that i s based on achieving and expanding visible early results.

The project has a highly participatory approach in each of i t s components and as part o f project management, , including different M&E and oversight mechanisms and a

, targeted approach to private sector engagement.

To optimize project design and draw on lessons learned, the team has invested in extensive analytical work undertaken parallel to project preparation: background notes on “Foundations for Institutional Reform in Ecuador.” For each component - Customs, Procurement, Civ i l Service - a detailed analysis was prepared b y team members and external experts, which highlight the opportunities and constraints o f reform. This was complemented by papers on the broader conditions o f state reform, anti-corruption strategies, the role of civil society, and the lessons o f past state reforms in Ecuador (including the MOSTA and SIGEF projects).

5. Alternatives considered and reasons for rejection

In the course o f preparing the project several alternative approaches were considered. One alternative was a project with a strong anti-corruption focus. The team decided not to opt for this alternative because o f the limited opportunities for tangible results and the expected resistance to implement reforms. A second alternative consisted of a broader

16

public sector reform, including the Comptroller General's Office, but impacts would have been limited due to a lack of focus and the proposed incremental approach would have significantly raised implementation challenges. A third alternative would have been a project focusing exclusively on Customs or civil service reforms. However, such an approach would have been too narrow to create necessary reform synergies and would not have generated the same demand for additional, broad-based reforms.

C. IMPLEMENTATION

1. Partnership arrangements

In preparation for this operation, the Bank has engaged in a close dialogue on institutional reforms with other donors and civil society, including the participants o f the "Mesa de Gobernabilidad". As a result o f this donor coordination, specific partnership arrangements w i l l be created to support the proposed project. USAID wi l l work in close cooperation with the Bank and w i l l support the Plan for Customs Cooperation. The Bank and the IADB wi l l coordinate closely their work on civil service reforms. The Bank w i l l also cooperate with COSUDE (which financed the f i rs t stage o f the CONTRATANET) in procurement reforms. Other partners include the CAF, GTZ and the EU. The close cooperation with other donors wi l l help to provide broad and strong support to key reforms and w i l l reinforce and the Bank's reform program through greater efficiencies and synergies, as explicitly requested by the MEF and CAE (see Annex 6).

The Bank also has been active in seeking involvement of civil society in project preparation, and has carefully assessed the strengths and weaknesses of civil society in Ecuador. Project design has benefited from regular meetings with civil society organizations and two major civil society consultations (see Annex 15).

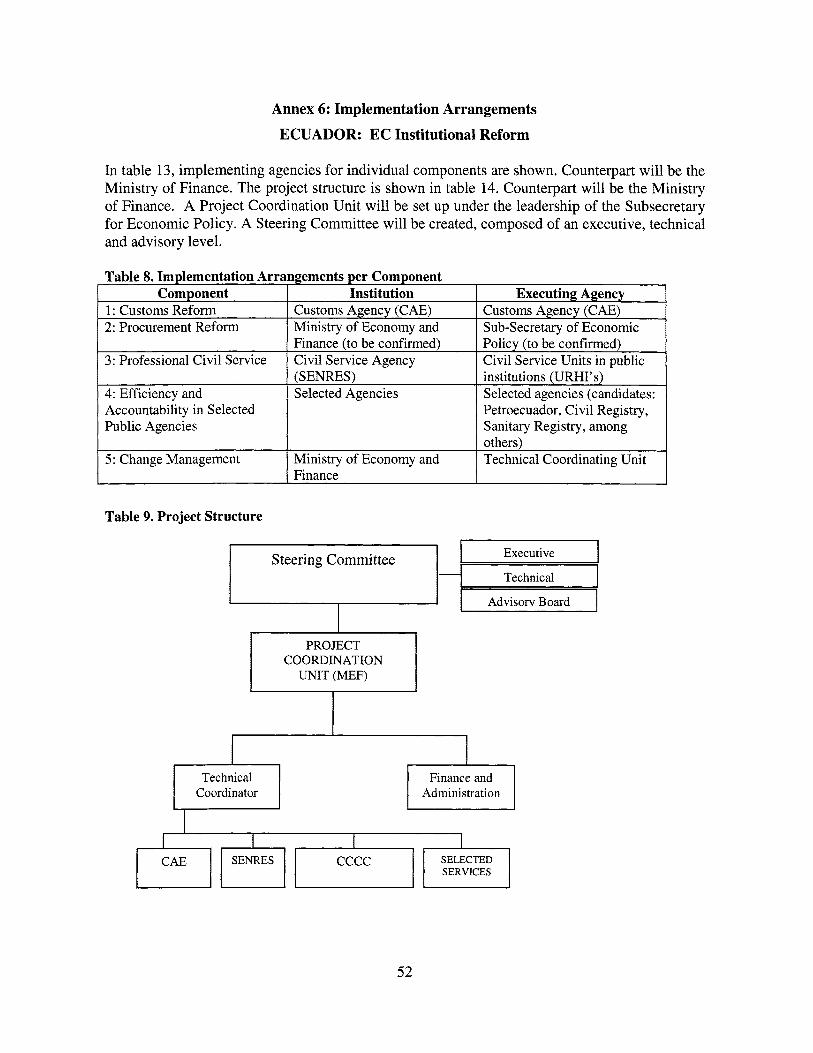

2. Institutional and implementation arrangements

A Project Coordination Unit (PCU) w i l l be set up within the Ministry of Economy and Finance (MEF), under the leadership of the Subsecretary of Political Economy. I t s organization and functions w i l l be detailed in an Operational Manual, satisfactory to the Bank. The PCU wi l l coordinate the activities o f the implementing agencies, which w i l l sign an implementation agreement with the MEF, satisfactory to the Bank.

A Steering Committee wi l l be constituted to oversee project implementation. Under the leadership o f the Minister of Economy and Finance the Steering Committee w i l l be composed o f the heads of the CAE, SENRES and CCCC and w i l l provide strategic leadership to guide project implementation. The Steering Committee w i l l be supported by a Technical Body, composed o f coordinators in each implementing agency, to oversee and direct project implementation in each component. In addition, an Advisory Board to the Steering Committee w i l l include national and international experts on the specific components, including representatives from civ i l society, to provide technical advice and support to the implementing agencies.

17

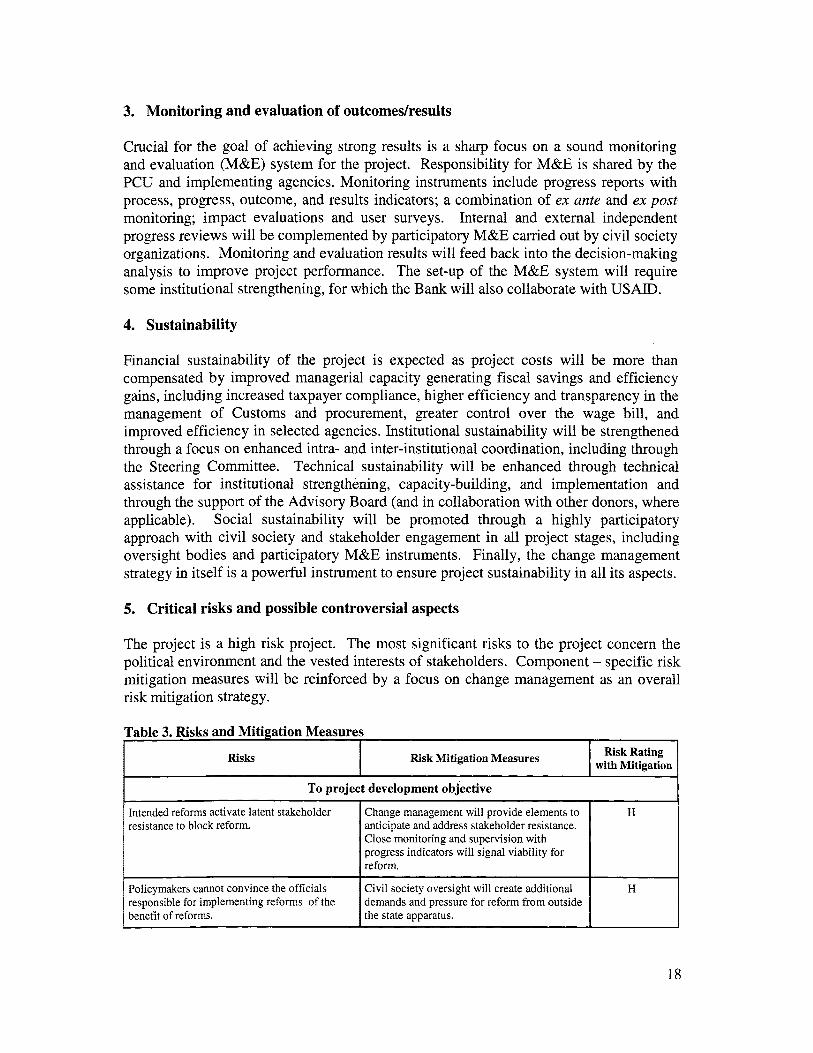

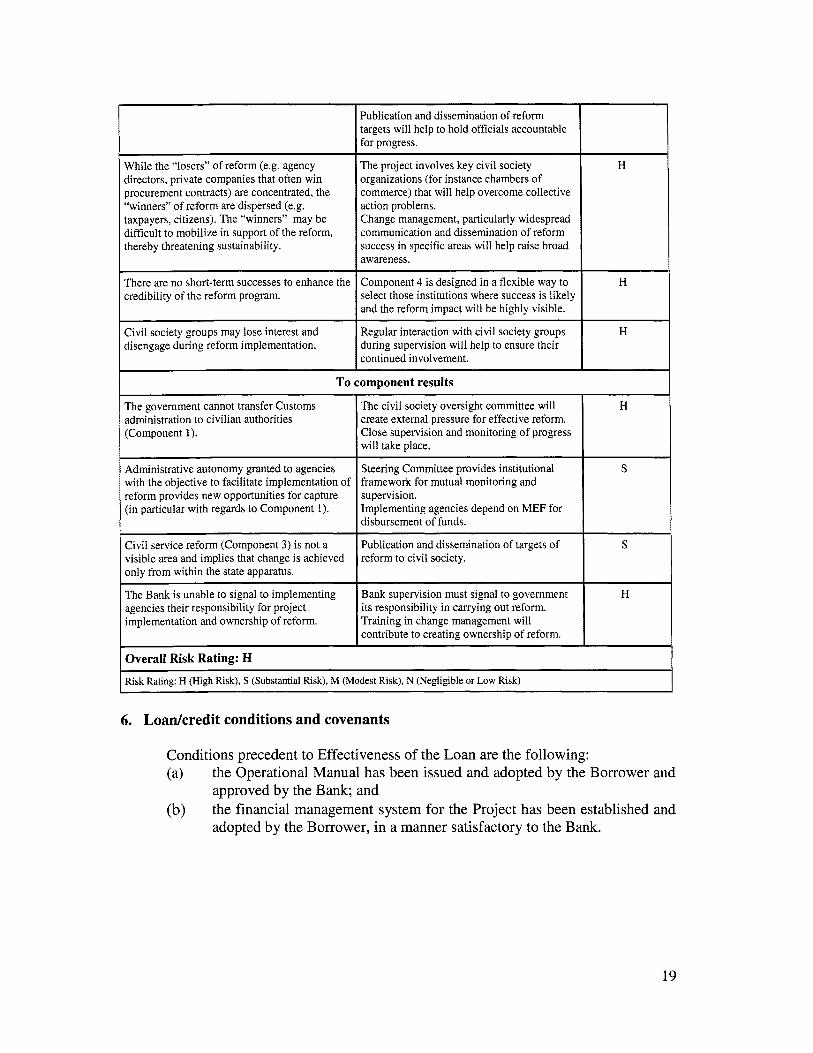

3. Monitoring and evaluation of outcomeshesults

Risk Mitigation Measures R i S k S

Crucial for the goal of achieving strong results i s a sharp focus on a sound monitoring and evaluation (M&E) system for the project. Responsibility for M&E i s shared by the PCU and implementing agencies. Monitoring instruments include progress reports with process, progress, outcome, and results indicators; a combination of ex ante and ex post monitoring; impact evaluations and user surveys. Internal and external independent progress reviews w i l l be complemented by participatory M&E carried out by civil society organizations. Monitoring and evaluation results wi l l feed back into the decision-making analysis to improve project performance. The set-up of the M&E system wi l l require some institutional strengthening, for which the Bank w i l l also collaborate with U S AID.

Risk Rating with Mitigation

4. Sustainability

Intended reforms activate latent stakeholder resistance to block reform.

Financial sustainability of the project i s expected as project costs w i l l be more than compensated by improved managerial capacity generating fiscal savings and efficiency gains, including increased taxpayer compliance, higher efficiency and transparency in the management o f Customs and procurement, greater control over the wage bill, and improved efficiency in selected agencies. Institutional sustainability w i l l be strengthened through a focus on enhanced intra- and inter-institutional coordination, including through the Steering Committee. Technical sustainability w i l l be enhanced through technical assistance for institutional strengthening, capacity-building, and implementation and through the support of the Advisory Board (and in collaboration with other donors, where applicable). Social sustainability wi l l be promoted through a highly participatory approach with civil society and stakeholder engagement in al l project stages, including oversight bodies and participatory M&E instruments. Finally, the change management strategy in itself i s a powerful instrument to ensure project sustainability in all i t s aspects.

Change management will provide elements to H anticipate and address stakeholder resistance. Close monitoring and supervision with progress indicators will signal viability for reform.

5. Critical risks and possible controversial aspects

Policymakers cannot convince the officials responsible for implementing reforms o f the benefit of reforms.

The project i s a high risk project. The most significant risks to the project concern the political environment and the vested interests o f stakeholders. Component - specific risk mitigation measures w i l l be reinforced b y a focus on change management as an overall risk mitigation strategy.

Civil society oversight will create additional demands and pressure for reform from outside the state apparatus.

To project development objective 1

H

Publication and dissemination of reform targets will help to hold officials accountable for progress.

While the “losers” of reform (e.g. agency directors, private companies that often win procurement contracts) are concentrated, the “winners” of reform are dispersed (e.g. taxpayers, citizens). The “winners” may be difficult to mobilize in support of the reform, thereby threatening sustainability.

The project involves key civil society organizations (for instance chambers of commerce) that will help overcome collective action problems. Change management, particularly widespread communication and dissemination o f reform success in specific areas will help raise broad awareness.

H

~~

There are no short-term successes to enhance the credibility of the reform program.

Civil society groups may lose interest and disengage during reform implementation.

Component 4 i s designed in a flexible way to select those institutions where success i s likely

during supervision will help to ensure their continued involvement.

To

The government cannot transfer Customs administration to civilian authorities (Component 1).

:omponent results

The civil society oversight committee will create external pressure for effective reform. Close supervision and monitoring of progress will take place.

Administrative autonomy granted to agencies with the objective to facilitate implementation of reform provides new opportunities for capture (in particular with regards to Component 1).

Steering Committee provides institutional framework for mutual monitoring and supervision. Implementing agencies depend on MEF for disbursement of funds.

Civil service reform (Component 3) i s not a visible area and implies that change i s achieved only from within the state apparatus.

The Bank i s unable to signal to implementing agencies their responsibility for project implementation and ownership of reform.

Publication and dissemination of targets of reform to civil society.

~~ ~

Bank supervision must signal to government its responsibility in carrying out reform. Training in change management will contribute to creating ownership of reform.

Overall Risk Rating: H

H

S

S

H

Risk Rating: H (High Risk), S (Substantial Risk), M (Modest Risk), N (Negligible or Low Risk)

6. Loadcredit conditions and covenants

Conditions precedent to Effectiveness o f the Loan are the following: (a)

(b)

the Operational Manual has been issued and adopted by the Borrower and approved by the Bank; and the financial management system for the Project has been established and adopted by the Borrower, in a manner satisfactory to the Bank.

19

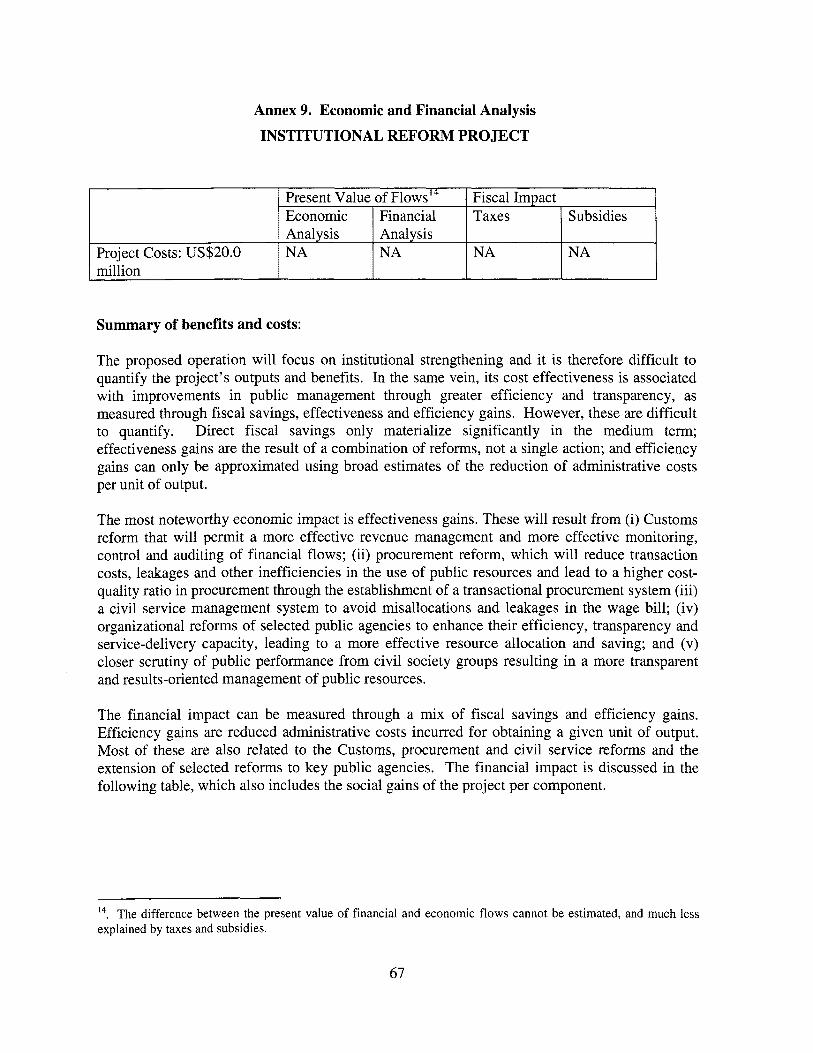

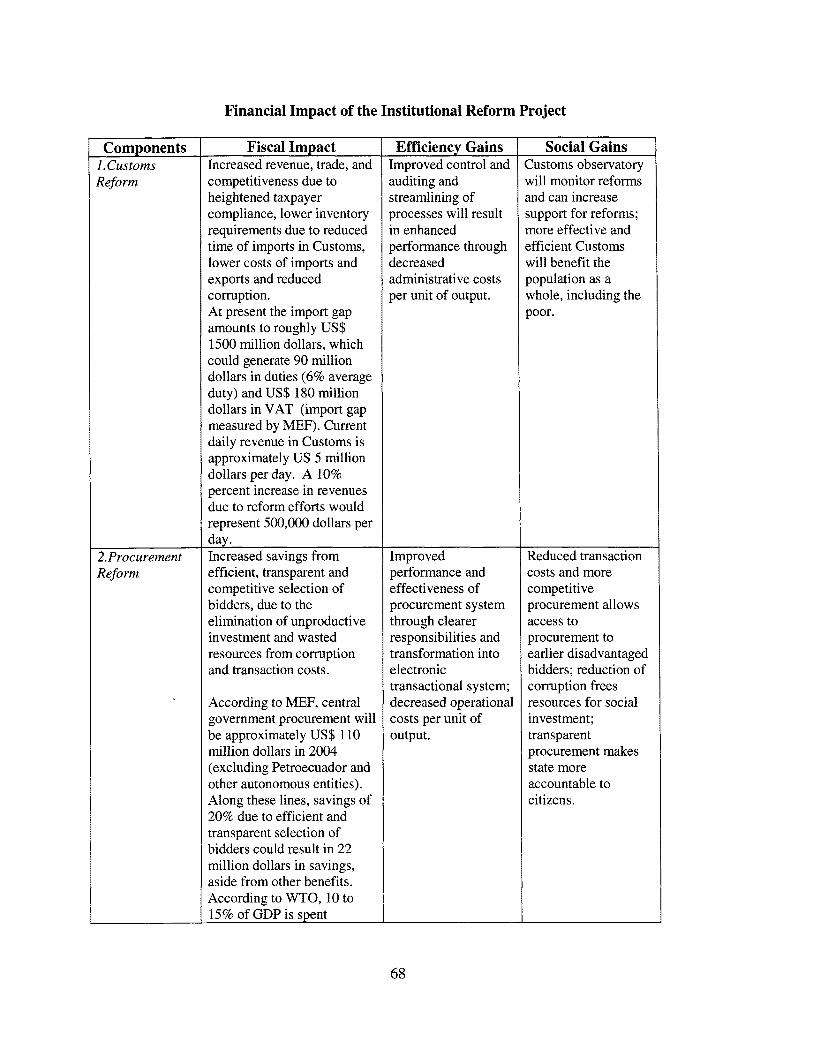

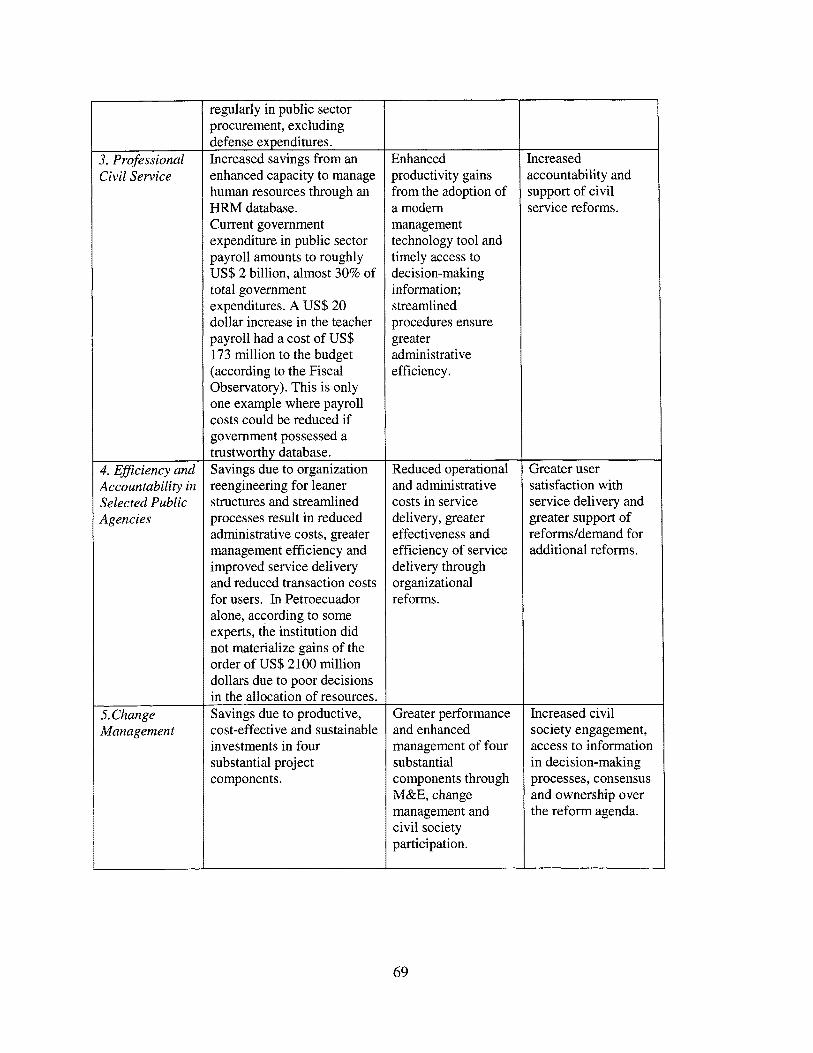

D. APPRAISAL SUMMARY

1. Economic and financial analyses

The proposed project i s considered cost-effective. The economic impact w i l l be realized largely through effectiveness gains. The project’s financial impact i s considered sustainable, as the project costs should be more than compensated by improved managerial capacity reflected in fiscal savings and efficiency gains. Quantitative estimates of the fiscal savings, effectiveness and efficiency gains w i l l be elaborated during appraisal. (See Annex 9)

2. Technical

The technical analysis i s based on prior in-depth analytical work, including notes on different aspects of public sector reform (refer to Annex 12 for details). The selected approach reflects international experience and best practices in public sector management, including an analysis of risks and risk mitigation. International references for the operation include: for Customs, Bolivia, Chile, Mexico, and Peru; for procurement, Chile and Mexico; for civil service reform, Bolivia, and Brazil; and for selected services, Argentina, Mexico and Peru. Experts from these countries who have been involved in these reforms w i l l advise implementing agencies regularly. Project design wi l l also benefit from technical assistance and institutional strengthening, change management mechanisms, and close monitoring and supervision.

3. Fiduciary

A Financial Management Assessment (FMA) o f the Sub-secretaria de Politica Econdmica and Sub-secretaria Administrativa of the Ministry of Economy and Finance (MEF) was performed to evaluate the proposed financial management arrangements and the Project Coordination Unit’s capacity to provide the Bank with accurate, reliable and timely information regarding resources and expenditures. The joint assessment (performed on site from March 29 to April 1, 2004) with the Procurement Capacity Assessment was conducted in accordance with OP/BP 10.02 and the Guidelines for Assessment of Financial Management Arrangements in World Bank Financed Projects. As a result of the assessment, a consolidated time-bound Financial Management (FM) and Procurement Action plan has been proposed.

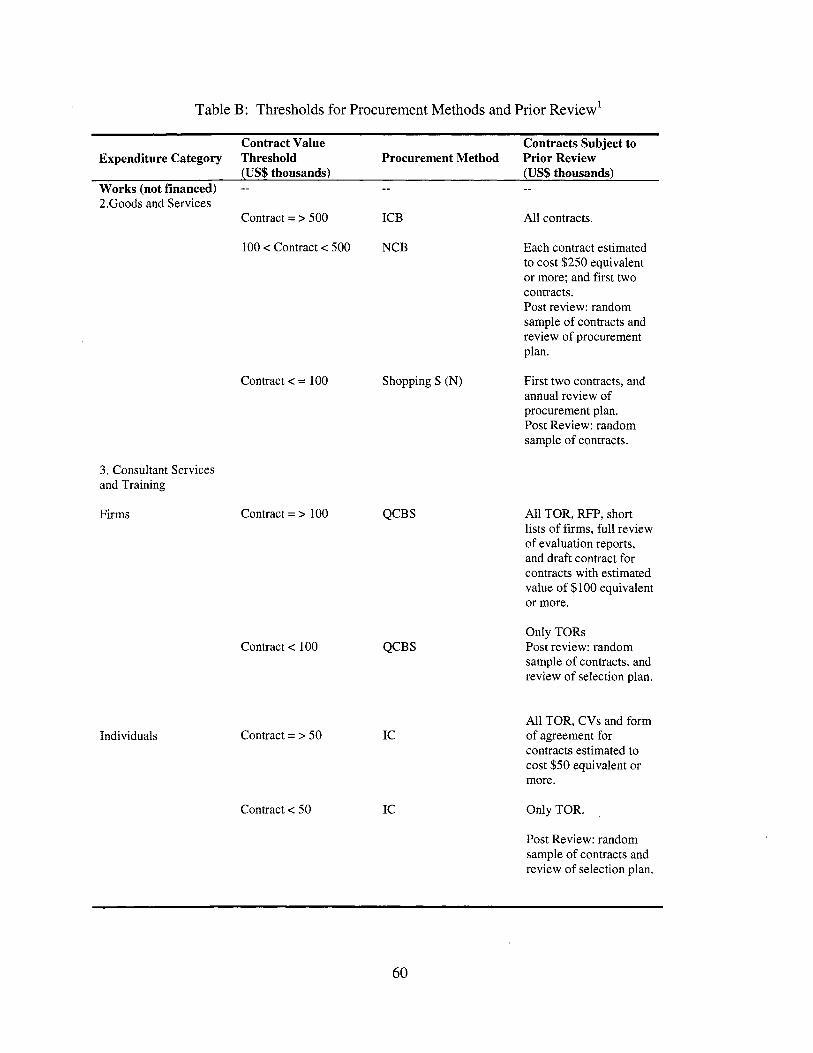

Procurement wi l l be carried out in accordance with World Bank guidelines and the provisions stipulated in the Loan Agreement. The proposed thresholds for prior review are based on the procurement capacity assessment o f the PCU and summarized in Table B, Annex 8. The PCU wi l l be in charge of preparing all bidding documents, carrying out bid openings, shopping procedures, and selecting and contracting consultant services for all contracts above and below prior review threshold. The technical staff of the PCU wi l l be responsible for the quality o f technical documents and products delivered by consultants, or physical inputs financed under the project.

20

The Operational Manual for the project wi l l specify the duties and responsibilities of al l the institutions involved in the implementation of the project. I t w i l l also include the procurement procedures, the Standard Bidding Documents to be used for each procurement method, and model contract for goods procured on the basis of three quotations or shopping.

Disbursements wi l l be transaction based (Le., against Statements of expenditure (SOEs), full documentation, direct payments or special commitments). Deposits into the Special Account and replenishments up to the authorized allocation set out in the legal agreement wi l l be made on the basis o f applications for withdrawals prepared by the PCU in MEF and accompanied by the supporting documentation in accordance with Bank disbursement procedures.

4. Social

The project w i l l produce positive social impacts by generating greater efficiency in the utilization of public resources. There i s no direct negative social impact to be expected from implementation of Component 4, Professional Civ i l Service. However, the HFW database w i l l enable the government to reduce the negative impact o f an indiscriminate personnel reduction, should government decide to reduce public employment.

5. Environment

Given the project objective to strengthen the management capacity of the government and to improve public service delivery in Customs, procurement, civil service and select public services, the project w i l l not affect the existing environmental framework. N o environmental study or analysis w i l l be required and none o f the environmental or social safeguard policies wi l l be triggered. The Project i s rated as Category “C”.

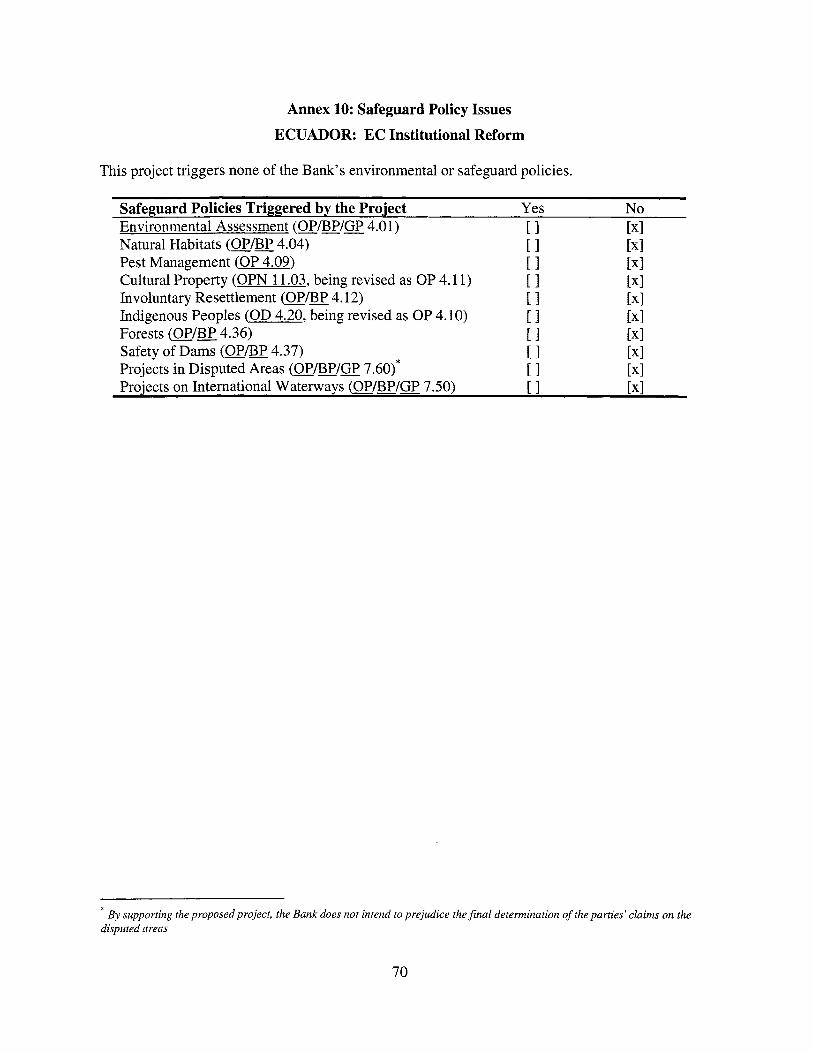

6. Safeguard policies

This project triggers none of the Bank’s environmental or social safeguard policies.

Safeguard Policies Triggered by the Project Yes No Environmental Assessment (OP/BP/GP 4.01) Natural Habitats (OP/BP 4.04) Pest Management (OP 4.09) Cultural Property (OPN 1 1.03, being revised as OP 4.1 1) Involuntary Resettlement (OP/BP 4.12) Indigenous Peoples (OD 4.20, being revised as OP 4.10) Forests (OP/BP 4.36) Safety of Dams (OP/BP 4.37) Projects in Disputed Areas (OP/BP/GP 7.60)* Projects on International Waterways (OP/BP/GP 7.50)

* By supporting the proposedproject, the Bank does not intend to prejudice the final determination of the parties‘ claims on the disputed areas

21

7. Policy Exceptions and Readiness None.

22

Annex 1: Country and Sector or Program Background

ECUADOR: EC Institutional Reform

In recent years Ecuador has tried to remake itself, both economically and politically. The country has changed - and i s s t i l l changing - but these changes have not been able to reduce the key constraints on social and economic development posed by a weak state and inefficient services. Although attempts at state reform are numerous, their outcome and impact have been fairly limited at best.

The reasons for this under-performance are embedded in the political, economic and social structure of Ecuador. Since the early 1970s buoyant revenue from o i l has allowed most governments to live with inefficiencies. O i l income impeded policy makers from recognizing underlying economic and fiscal constraints. After 1979, this dilemma became more complex: democratization provided groups access to arenas where policy was debated and enacted - Congress, the Executive, Judiciary - and they seized this opportunity to gain access to o i l rents. With l i t t le incentive to tax, but with a strong need to serve their clientele, all governments contributed to state growth by expanding public employment and investment. Efficiency concerns were not given priority.

After 1990, some incentives to reform the state emerged. The percentage of o i l in total government revenue declined, heightening distributional pressures. More openness and regional integration have created more competition and incentives for efficiency. In 1995, the National Modernization Council (CONAM) was founded and in the following years it launched several ambitious reform programs that focused mainly on privatization. But so far, the outcomes of these reform programs are limited. Although there were some incentives to improve services, those with a stake in maintaining inefficiencies have outmaneuvered those with a genuine interest in making the public sector more effective.

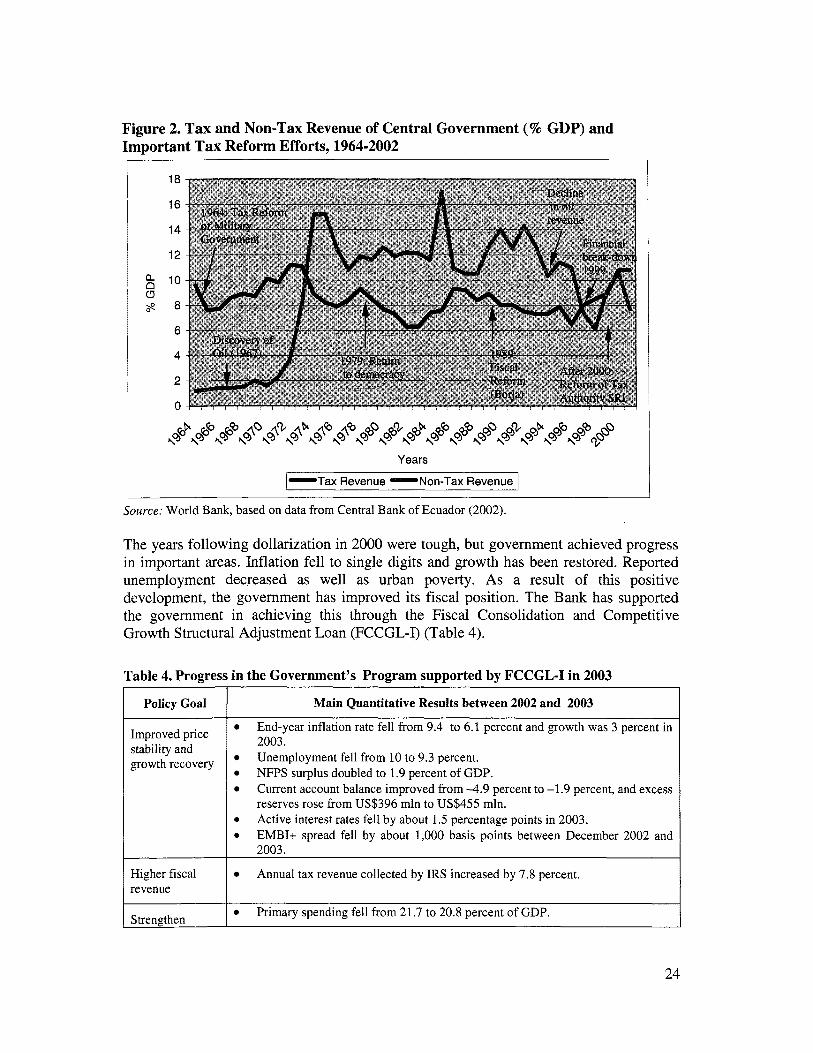

The financial and economic crisis of 1999 represents a sharp break with this past. With the international price of o i l plummeting to 7 USD per barrel, the weather phenomenon El NiAo devastating crops in coastal lowlands, and the collapse of private banks, there was no other opportunity for government than to reform the state. The dollarization regime adopted in January 2000 as a response to this crisis provided a significant budget constraint: fiscal policy remained as the only tool for economic policy. Whereas before currency devaluations were a comfortable means to disguise inefficiencies, now revenue needed to be raised from voters and taxpayers. For the f i rs t time, policy makers had a real incentive to tax. The Revenue Authority (SRI) was given the managerial autonomy to simplify procedures, impose sanctions, and serve their clients. As a result, tax revenue increased significantly when measured as a percentage o f GDP. For f irst time in more than 30 years, the share of tax revenue was higher than non-tax revenue (mainly oil) (Figure 2). Citizens now have a powerful argument to hold politicians accountable for their actions. This i s a key entry point for state reform.

23

Figure 2. Tax and Non-Tax Revenue of Central Government (% GDP) and Important Tax Reform Efforts, 1964-2002

18

16

14

12

10

8

6

4

2

0

Years

1-Tax Revenue -Nan-Tax Revenue 1 Source: World Bank, based on data from Central Bank of Ecuador (2002).

The years following dollarization in 2000 were tough, but government achieved progress in important areas. Inflation fell to single digits and growth has been restored. Reported unemployment decreased as well as urban poverty. As a result o f this positive development, the government has improved i ts fiscal position. The Bank has supported the government in achieving this through the Fiscal Consolidation and Competitive Growth Structural Adjustment Loan (FCCGL-I) (Table 4).

Table 4. Progress in the Government’s Program supported by FCCGL-I in 2003

Policy Goal

Improved price stability and growth recovery

Higher fiscal revenue

Strengthen

Main Quantitative Results between 2002 and 2003

0

0

End-year inflation rate fel l from 9.4 to 6.1 percent and growth was 3 percent i n 2003. Unemployment fel l from 10 to 9.3 percent. NFPS surplus doubled to 1.9 percent o f GDP. Current account balance improved from -4.9 percent to -1.9 percent, and excess reserves rose from US$396 mln to US$4SS mln. Active interest rates fel l by about 1 .S percentage points in 2003. EMBI+ spread fel l by about 1,000 basis points between December 2002 and 2003.

Annual tax revenue collected by IRS increased by 7.8 percent.

Primary spending fel l from 21.7 to 20.8 percent o f GDP.

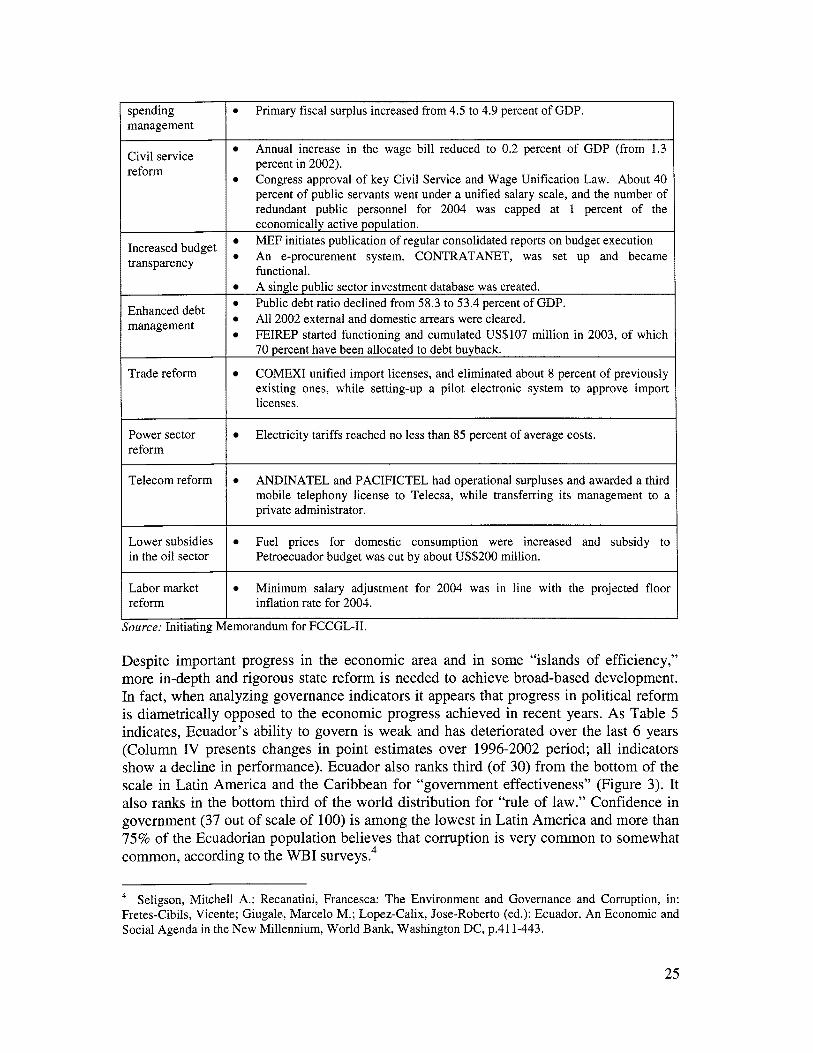

24

spending management

Civil service reform

0 Primary fiscal surplus increased from 4.5 to 4.9 percent of GDP.

Increased budget transparency

Lower subsidies in the oil sector

Labor market reform

Annual increase in the wage bil l reduced to 0.2 percent of GDP (from 1.3 percent in 2002). Congress approval of key Civil Service and Wage Unification Law. About 40 percent of public servants went under a unified salary scale, and the number of redundant public personnel for 2004 was capped at 1 percent of the economically active population. MEF initiates publication of regular consolidated reports on budget execution An e-procurement system, CONTRATANET, was set up and became functional.

Fuel prices for domestic consumption were increased and subsidy to Petroecuador budget was cut by about US$200 million.

Minimum salary adjustment for 2004 was in line with the projected floor inflation rate for 2004.

A single public sector investment database was created. Public debt ratio declined from 58.3 to 53.4 percent of GDP. Al l 2002 external and domestic arrears were cleared. FEIREP started functioning and cumulated US$107 million i n 2003, of which

Enhanced debt management

70 percent have been allocated to debt buyback. I

Trade reform COMEXI unified import licenses, and eliminated about 8 percent of previously existing ones, while setting-up a pilot electronic system to approve import licenses.

Power sector reform

Electricity tariffs reached no less than 85 percent of average costs.

Telecom reform ANDINATEL and PACIFICTEL had operational surpluses and awarded a third mobile telephony license to Telecsa, while transferring i t s management to a private administrator.

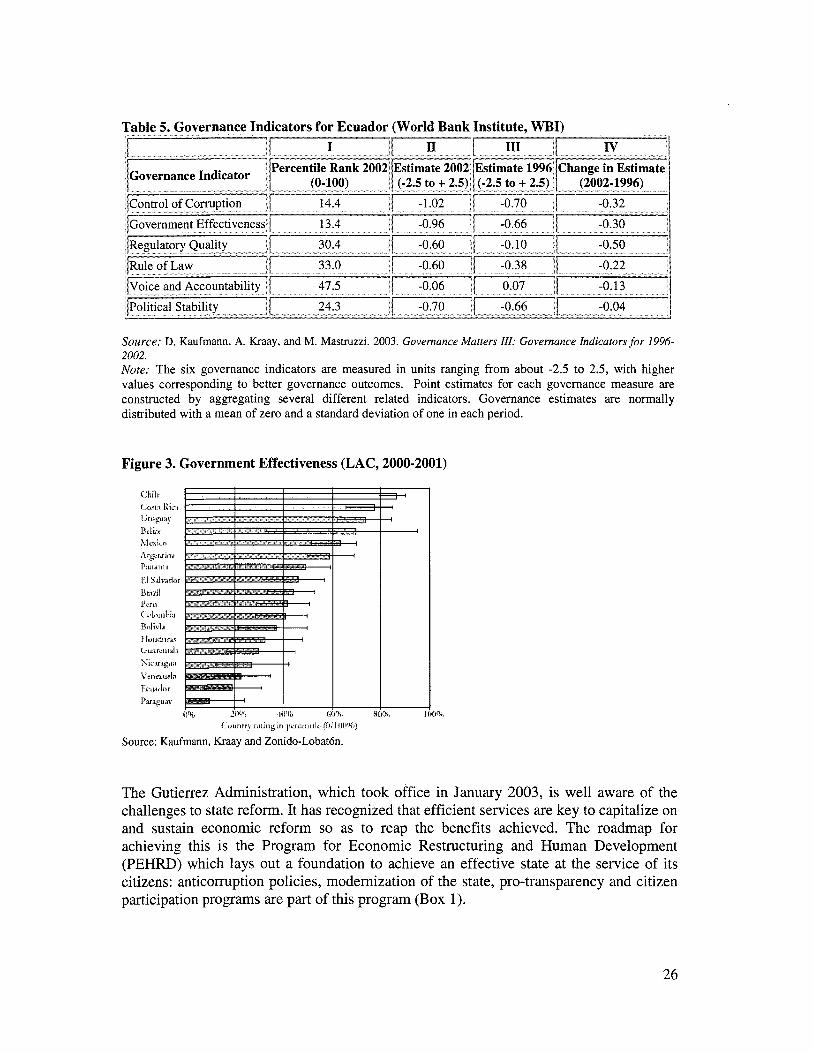

Despite important progress in the economic area and in some “islands of efficiency,” more in-depth and rigorous state reform i s needed to achieve broad-based development. In fact, when analyzing governance indicators i t appears that progress in political reform i s diametrically opposed to the economic progress achieved in recent years. As Table 5 indicates, Ecuador’s ability to govern i s weak and has deteriorated over the last 6 years (Column I V presents changes in point estimates over 1996-2002 period; all indicators show a decline in performance). Ecuador also ranks third (of 30) from the bottom of the scale in Latin America and the Caribbean for “government effectiveness” (Figure 3). I t also ranks in the bottom third of the world distribution for “rule of law.” Confidence in government (37 out of scale of 100) i s among the lowest in Latin America and more than 75% of the Ecuadorian population believes that corruption i s very common to somewhat common, according to the WBI survey^.^

Seligson, Mitchell A.; Recanatini, Francesca: The Environment and Governance and Corruption, in: Fretes-Cibils, Vicente; Giugale, Marcel0 M.; Lopez-Calix, Jose-Roberto (ed.): Ecuador. An Economic and Social Agenda in the New Millennium, World Bank, Washington DC, p.411-443.

25

Table 5. Governance Indicators for Ecuador (World Bank Institute, WBI) I Iv I

Source: D. Kaufmann, A. Kraay, and M. Mastmzzi. 2003. Govemance Matters III: Govemance Indicators for I996- 2002. Note: The six governance indicators are measured in units ranging from about -2.5 to 2.5, with higher values corresponding to better governance outcomes. Point estimates for each governance measure are constructed by aggregating several different related indicators. Governance estimates are normally distributed with a mean o f zero and a standard deviation o f one in each period.

Figure 3. Government Effectiveness (LAC, 2000-2001)

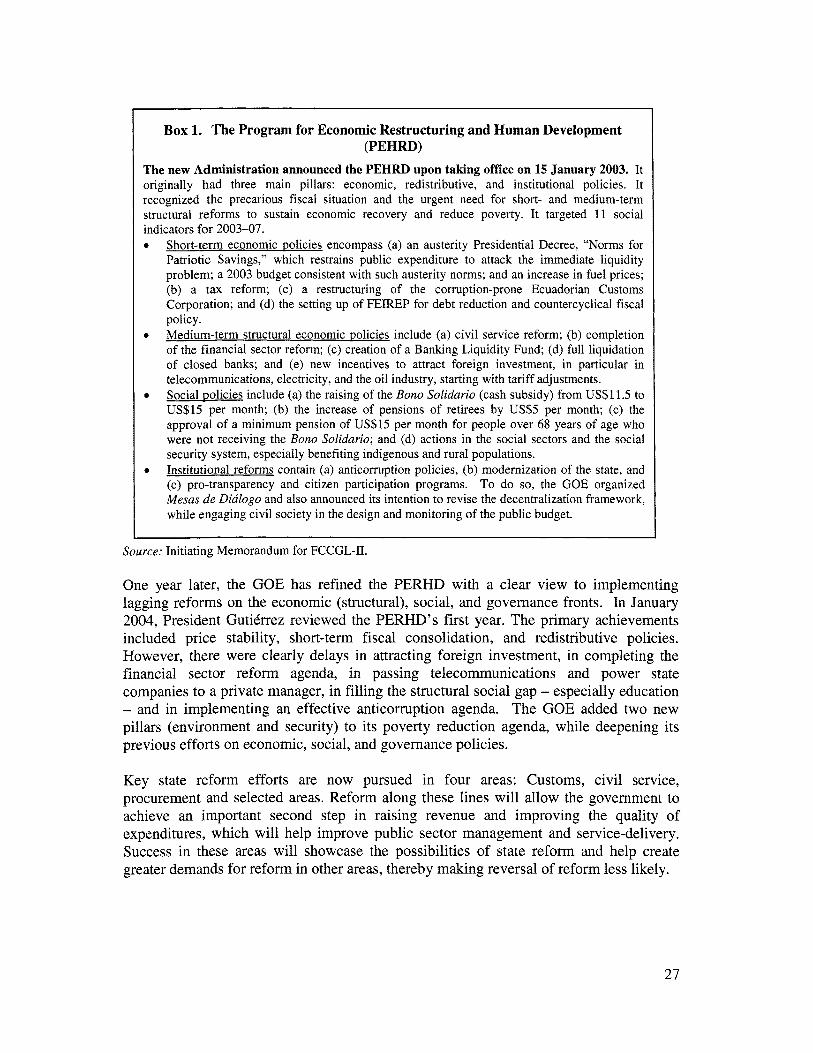

The Gutierrez Administration, which took office in January 2003, is wel l aware o f the challenges to state reform. I t has recognized that efficient services are key to capitalize on and sustain economic reform so as to reap the benefits achieved. The roadmap for achieving this i s the Program for Economic Restructuring and Human Development (PEHRD) which lays out a foundation to achieve an effective state at the service o f i t s citizens: anticorruption policies, modernization o f the state, pro-transparency and citizen participation programs are part o f this program (Box 1).

26

Box 1. The Program for Economic Restructuring and Human Development (PEHRD)

The new Administration announced the PEHRD upon taking office on 15 January 2003. I t originally had three main pillars: economic, redistributive, and institutional policies. I t recognized the precarious fiscal situation and the urgent need for short- and medium-term structural reforms to sustain economic recovery and reduce poverty. I t targeted 11 social indicators for 2003-07.

Short-term economic policies encompass (a) an austerity Presidential Decree, “Norms for Patriotic Savings,” which restrains public expenditure to attack the immediate liquidity problem; a 2003 budget consistent with such austerity norms; and an increase in fuel prices; (b) a tax reform; (c) a restructuring o f the corruption-prone Ecuadorian Customs Corporation; and (d) the setting up o f FEIREP for debt reduction and countercyclical fiscal policy. Medium-term structural economic policies include (a) c iv i l service reform; (b) completion of the financial sector reform; (c) creation o f a Banking Liquidity Fund; (d) full liquidation of closed banks; and (e) new incentives to attract foreign investment, in particular in telecommunications, electricity, and the o i l industry, starting with tariff adjustments. Social policies include (a) the raising o f the Bono Solidario (cash subsidy) from US$11.5 to US$15 per month; (b) the increase o f pensions o f retirees by US$5 per month; (c) the approval o f a minimum pension o f US$15 per month for people over 68 years o f age who were not receiving the Bono Solidario; and (d) actions in the social sectors and the social security system, especially benefiting indigenous and rural populations. Institutional reforms contain (a) anticorruption policies, (b) modernization of the state, and (c) pro-transparency and citizen participation programs. To do so, the GOE organized Mesas de Didlogo and also announced i ts intention to revise the decentralization framework, while engaging civi l society in the design and monitoring o f the public budget.

Source: Initiating Memorandum for FCCGL-11.

One year later, the GOE has refined the PERHD with a clear view to implementing lagging reforms on the economic (structural), social, and governance fronts. In January 2004, President GutiCrrez reviewed the PERHD’s f i rs t year. The primary achievements included price stability, short-term fiscal consolidation, and redistributive policies. However, there were clearly delays in attracting foreign investment, in completing the financial sector reform agenda, in passing telecommunications and power state companies to a private manager, in fill ing the structural social gap - especially education - and in implementing an effective anticorruption agenda. The GOE added two new pillars (environment and security) to i t s poverty reduction agenda, while deepening i t s previous efforts on economic, social, and governance policies.

Key state reform efforts are now pursued in four areas: Customs, c iv i l service, procurement and selected areas. Reform along these lines w i l l allow the government to achieve an important second step in raising revenue and improving the quality of expenditures, which w i l l help improve public sector management and service-delivery. Success in these areas w i l l showcase the possibilities o f state reform and help create greater demands for reform in other areas, thereby making reversal of reform less likely.

27

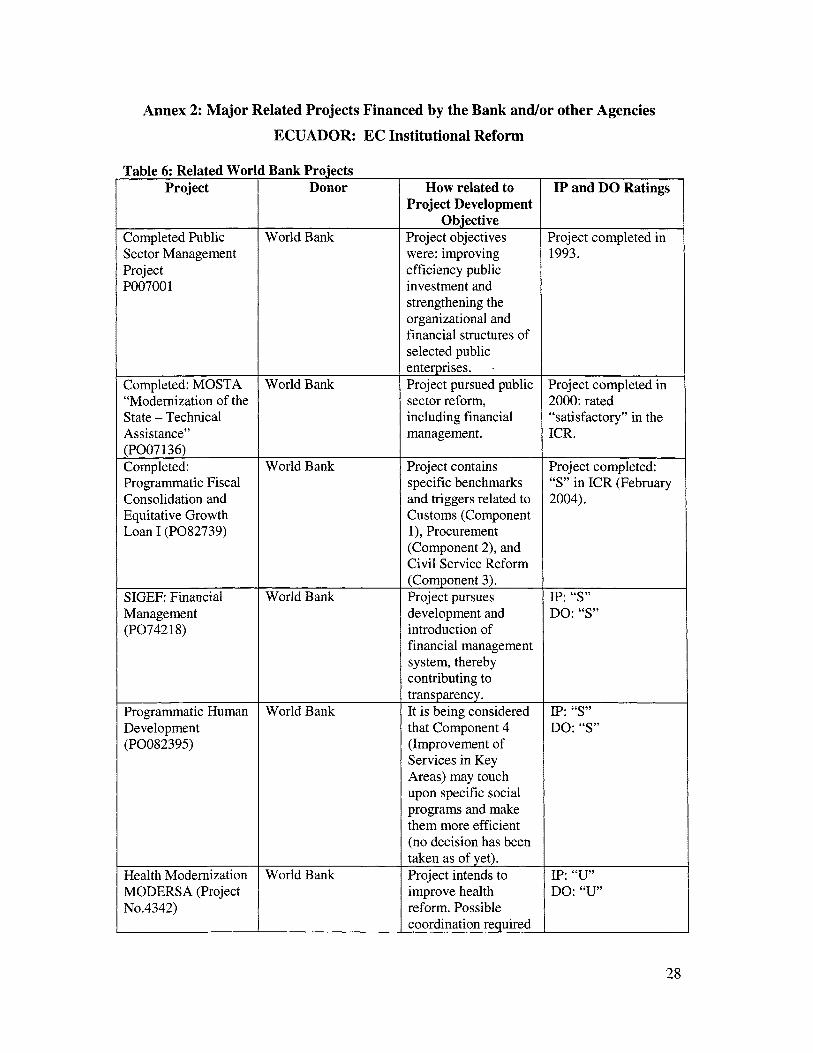

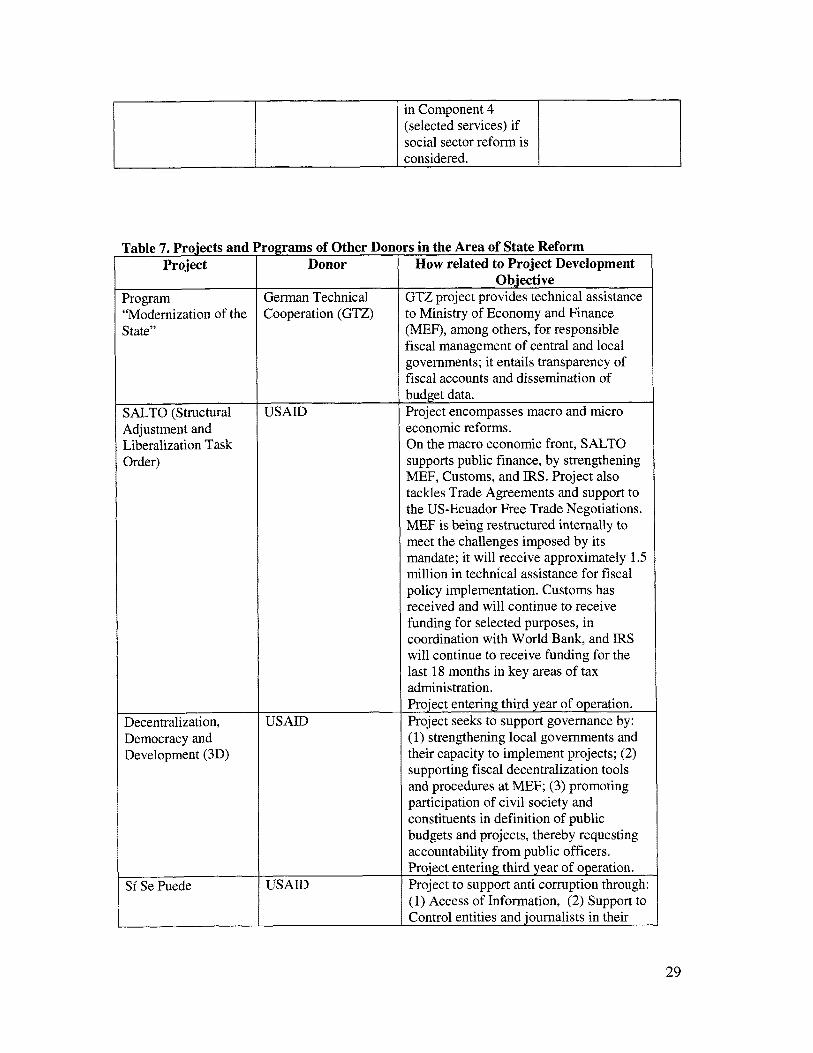

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies ECUADOR: EC Institutional Reform

Table 6: Related Wor Project

Completed Public Sector Management Project PO0700 1

Completed: MOSTA “Modernization o f the State - Technical Assistance” (PO07 136) Completed: Programmatic Fiscal Consolidation and Equitative Growth Loan I (P082739)

SIGEF: Financial Management (P074218)

Programmatic Human Development (P0082395)

Health Modernization MODERSA (Project No.4342)

I Bank Projects Donor

World Bank

World Bank

World Bank

World Bank

World Bank

World Bank

How related to Project Development

Objective Project objectives were: improving efficiency public investment and strengthening the organizational and financial structures o f selected public enterprises. Project pursued public sector reform, including financial management.