Embed Size (px)

Citation preview

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 9078

PROJECT COMPLETION REPORT

MADAGASCAR

MADAGASCAR ACCOUNTING AND AUDIT ORGANIZATION

AND TRAINING PROJECT

CREDIT 1155-MAG

Africa Country Department IIIPopulation and Human Resources Division

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

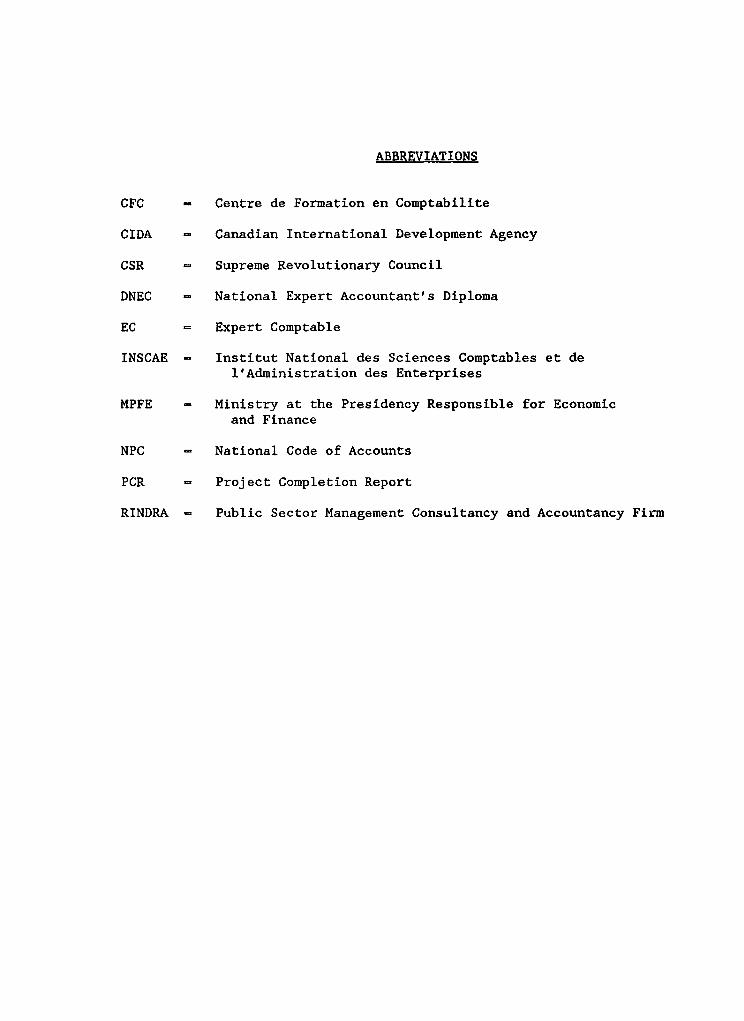

ABBREVIATIONS

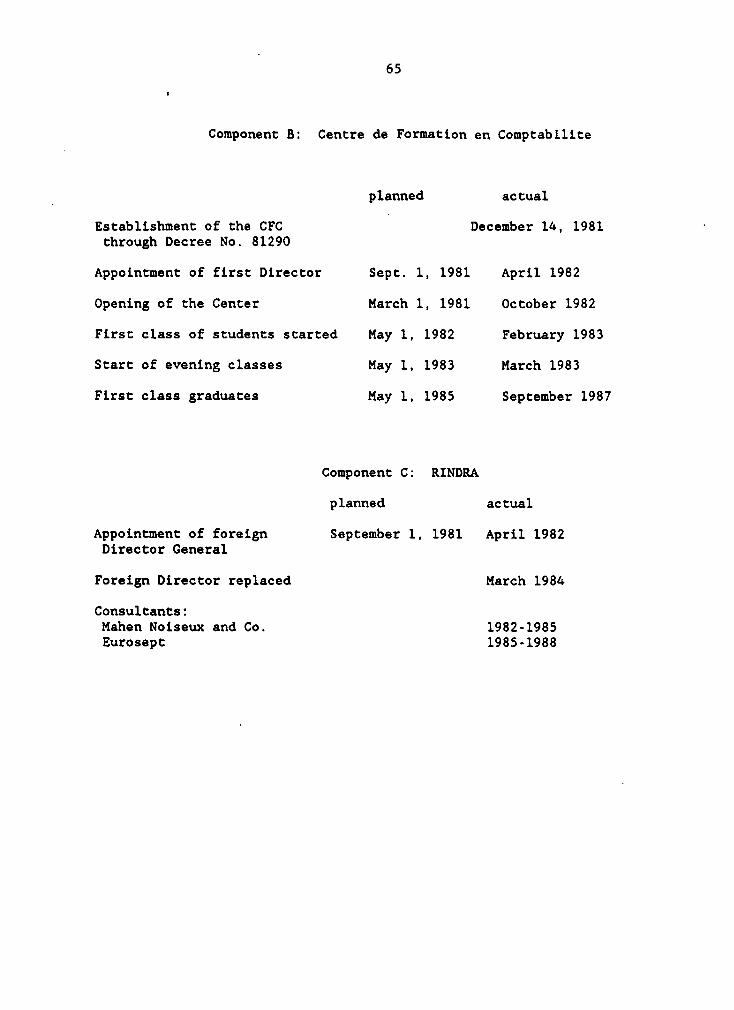

CFC - Centre de Formation en Comptabilite

CIDA - Canadian International Development Agency

CSR - Supreme Revolutionary Council

DNEC - National Expert Accountant's Diploma

EC c Expert Comptable

INSCAE - Institut National des Sciences Comptables et del'Administration des Enterprises

MPFE - Ministry at the Presidency Responsible for Economicand Finance

NPC = National Code of Accounts

PCR = Project Completion Report

RINDRA - Public Sector Management Consultancy and Accountancy Firm

you omcizL US ONLYTHE WORLD BANKWashington. D.C. 20433

U.S.A.

office d Dnvcgvr.C.gaiOptatmt bvakaatnm

October 12, 1990

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on Madagascar -Madagascar Accounting and Audit Organizationand Training Proiect (Credit 1155-MAG)

Attached, for information, is a copy of a report entitled "ProjectCompletion Report on Madagascar - Madagascar Accounting and Audit Organizationand Training Project (Credit 1155-MAG)" prepared by the Africa Regional Officewith Part II of the report contributed by the Borrower. No audit of thisproject has been made by the Operations Evaluation Department at this time.

Attachment '

Thui document has a restricted distribution and may be used by recipients only in the performaneof their offlcal dutis Its contents may not otherwie be disclosed without Word ank authorintion.

FOR OFFICIAL USE ONLY

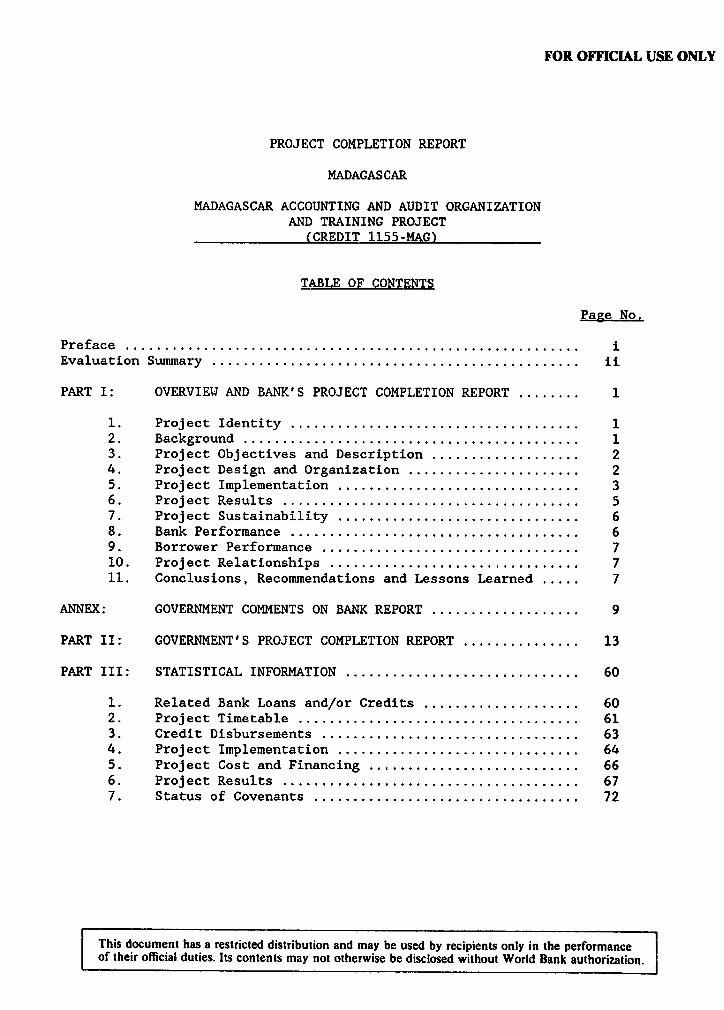

PROJECT COMPLETION REPORT

MADAGASCAR

MADAGASCAR ACCOUNTING AND AUDIT ORGANIZATIONAND TRAINING PROJECT

(CREDIT 1155-MAG)

TABLE OF CONTENTS

Page No.

Preface ................. iEvaluation Summary ................. ii

PART I: OVERVIEW AND BANK'S PROJECT COMPLETION REPORT .... .... 1

1. Project Identity ..................................... 12. Background ........... ................................ 13. Project Objectives and Description ................... 24. Project Design and Organization ...................... 25. Project Implementation ............................... 36. Project Results ...................................... 57. Project Sustainability ............................... 68. Bank Performance ..................................... 69. Borrower Performance ................................. 710. Project Relationships. 711. Conclusions, Recommendations and Lessons Learned 7

ANNEX: GOVERNMENT COMMENTS ON BANK REPORT. 9

PART II: GOVERNMENT'S PROJECT COMPLETION REPORT .... ........... 13

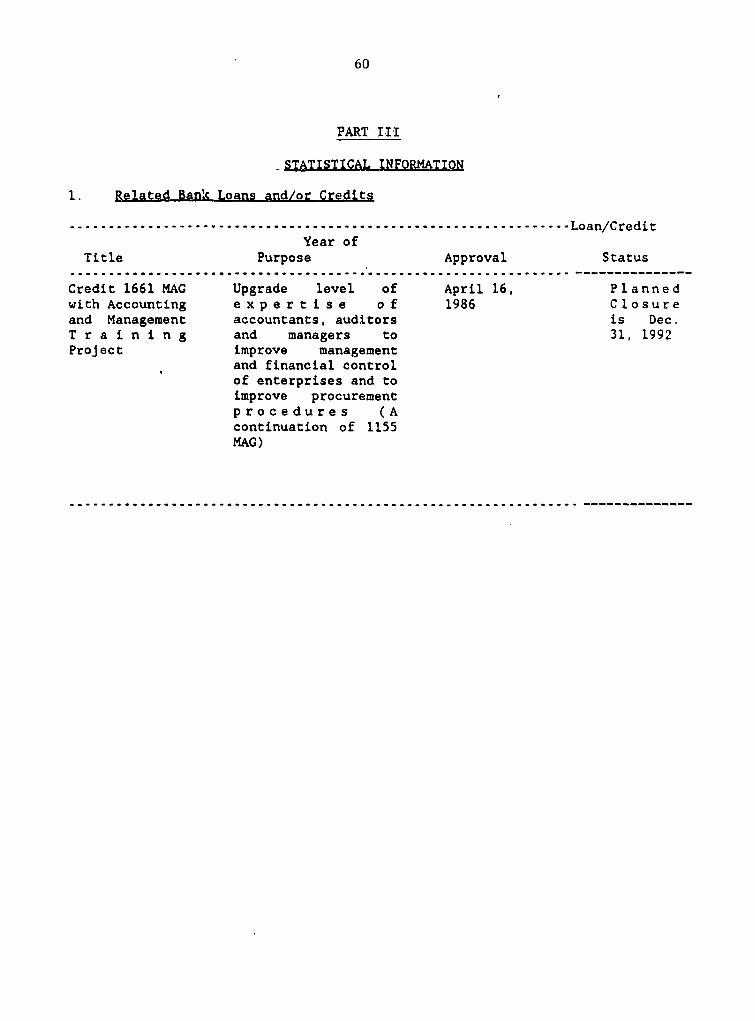

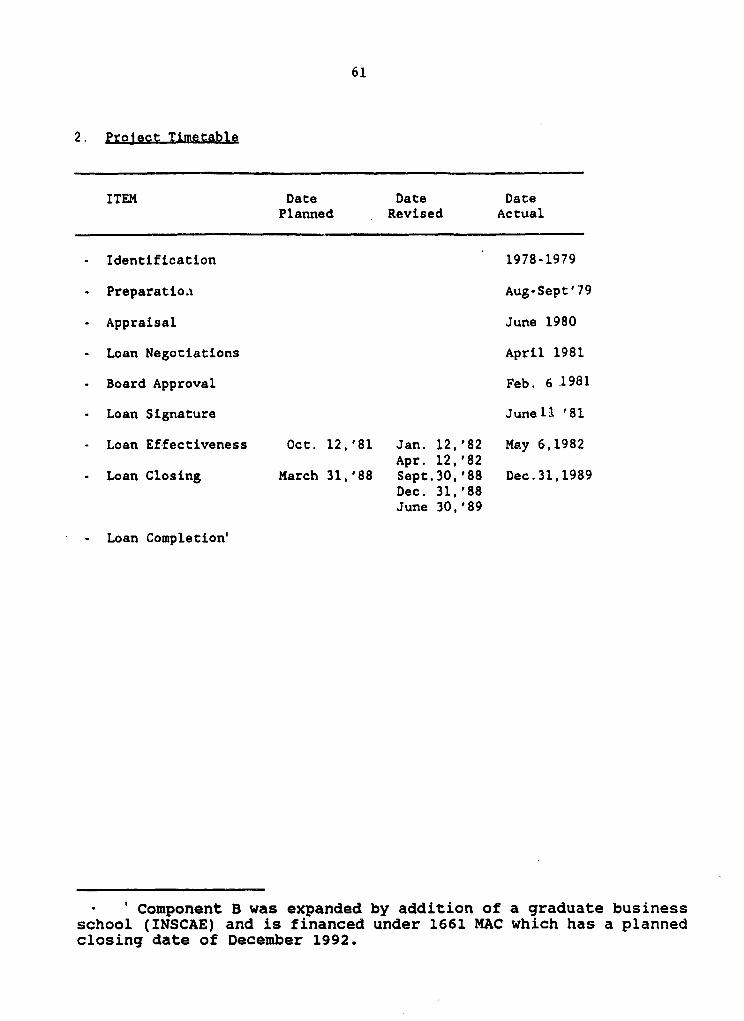

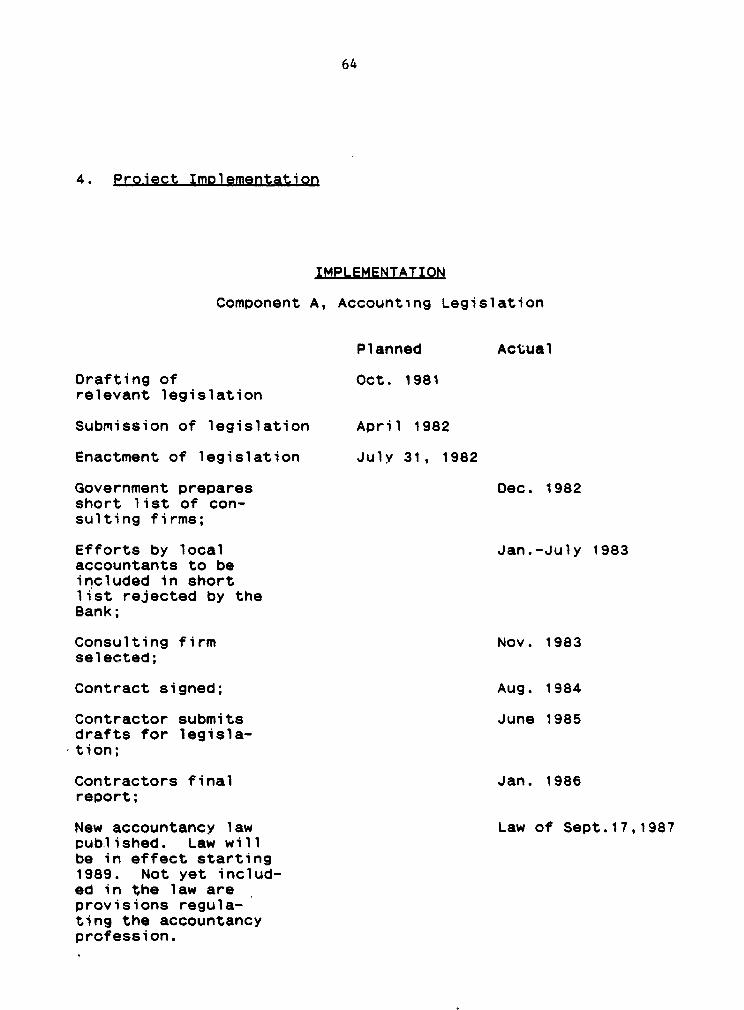

PART III: STATISTICAL INFORMATION .............................. 60

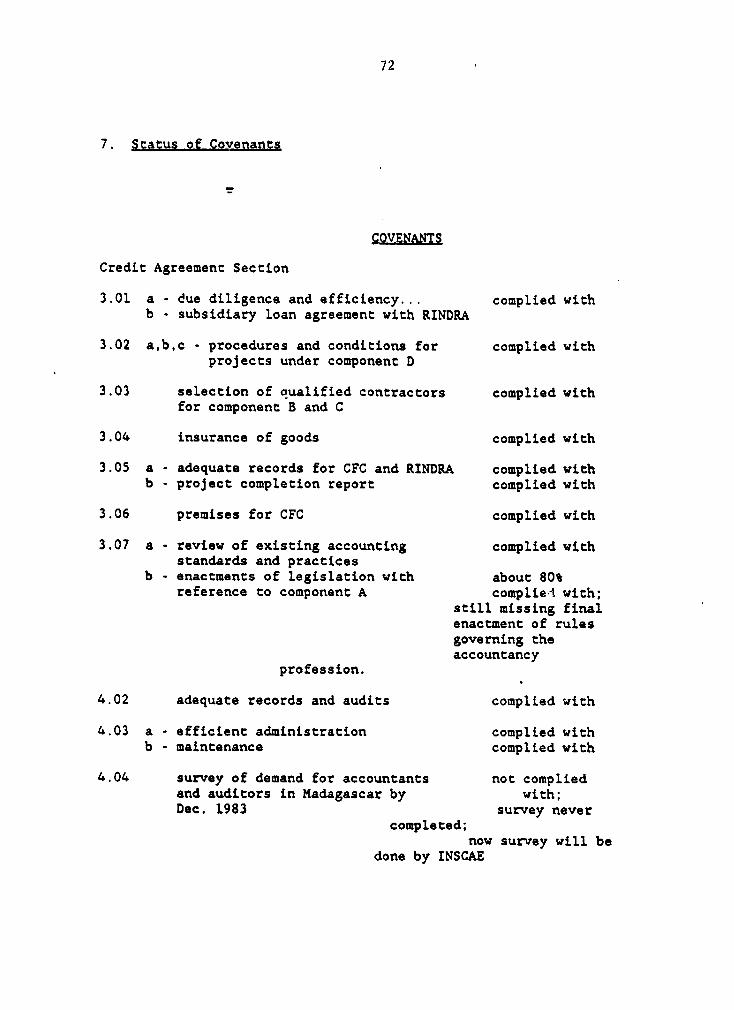

1. Related Bank Loans and/or Credits ....... ............. 602. Project Timetable ................................... 613. Credit Disbursements ................................. 634. Project Implementation ............................... 645. Project Cost and Financing ............ ............... 666. Project Results ................................... 677. Status of Covenants .................................. 72

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

i

PROJECT COMPLETION REPORT

MADAGASCAR

MADAGASCAR ACCOUNTING AND AUDIT ORGANIZATION AND TRAINING PROJECT

CREDIT 1155 - HAG

PREFACE

This is the Project Completion Report (PCR) for the MadagascarAccounting and Audit Organization and Training Project, for which Credit inthe amount of SDR 9,400,000 was approved on June 11, 1981. The Credit wasclosed on November 10, 1989, one year and six months behind schedule. As ofthat date there was an outstanding balance of SDR 9261 i.e. less than 0.1%of the Credit, which was cancelled.

The PCR was prepared by AF3PH (Preface, Basic Data Sheet, EvaluationSummary, Part I Overview and Bank's Report, and Part III Statistical Annex)and the Borrower (Part II - Government's Project Completion Report).

Preparation of this PCR started during the Bank's last supervisionmission in 1989 and is based inter alia, on the Staff Appraisal Report; theDevelopment Credit Agreement; supervision reports; correspondence betweenthe Bank and the Borrower; internal Bank memoranda; and on an extensivecase study prepared by the Bank's Operations Evaluation Department 1/ aspart of a broader study of technical assistance projects in Africa.

The Borrower was provided a copy of the Bank's contribution to thePCR to comment on. The Government provided some comments which wereprimarily explanatory in nature. There was no significant difference ofopinion between the Government and the Bank. A translation of theGovernment's letter as well as the original letter in French is provided atthe end of the Part I.

1/ Madagascar: Evaluation du Prolet Organisation et Formation en Comptablit6 et Revision(Cr6dit 1156), Operations Evaluation Department, The World Bank

ii

PROJECT COMPLETION REYORT

MADAGASCAR

!4ADAGASCAR ACCOUNTING AND AUD:T ORGANIZATIOS AND TRAINING PROJECT

CRBDXT 1155 - MAG

EVALUATION SUOMYRY

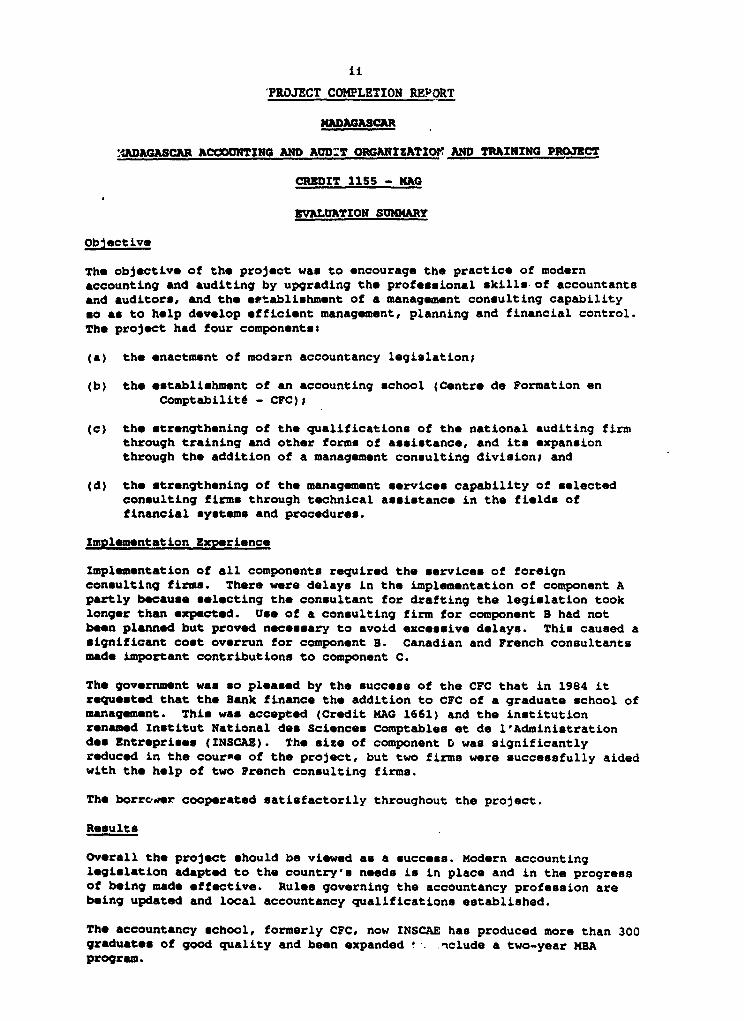

Obiective

The objective of the project was to encourage the practice of modernaccounting and auditing by upgrading the professional skills of accountantsand auditors, and the *etablishment of a management consulting capabilityso as to help develop officient management, planning and financial control.The project had four componentst

(a) the enactment of modarn accountancy legislation;

(b) the establishment of an accounting school (Centre de Formation enComptabilit6 - CFC);

(c) the strengthening of the qualifications of the national auditing firmthrough training and other forms of assistance, and its expansionthrough the addition of a management consulting division; and

(d) the strengthening of the management services capability of selectedconsulting firms through technical assistance in the fields offinancial systems and procedures.

Implementation Experience

Implmentation of all components required the services of foreignconsulting firms. There were delays in the implementatLon of component Apartly because solecting the consultant for drafting the legislation tooklonger than expected. Use of a consulting firm for component B had notbeen planned but proved necessary to avoid excessive delays. This caused asignificant cost overrun for component B. Canadian and French consultantsmade important contributions to component C.

The government was so pleased by the success of the CFC that in 1984 itrequested that the Bank finance the addition to CFC of a graduate school ofmanagment. This was accepted (Credit MAO 1661) and the institutionrenamed Institut National des Sciences Comptables et de l'Administrationdes Entrepriess (INSCAE). Tho size of component n was significantlyreduced in the course of the project, but two firms were successfully aidedwith the help of two French consulting firms.

The borrcoer cooperated satisfactorily throughout the project.

Results

Overall the project should be viewed as a success. Modern accountinglegislation adapted to the country's needs is in place and in the progressof being made effective. Rules governing the accountancy profession arebeing updated and local accountancy qualifications established.

The accountancy school, formerly CFC, now INSCAE has produced more than 300graduates of good quality and been expanded - nclude a two-year MBAprogram.

iii

The national accounting firm RINDRA has greatly benefitee from thetechnical assistance received and is widely recognized for the quality ofits auditing and consulting services. RINDRh operations would beprofitable if it were not for the interest on the on-lending by thegovernment of the proceeds of the Credit on terms that proved to be tooonerous, and the amortization of the technical resistance received. RINDRAwas expected to buy expertise at world market prices and sell the acquiredexpertise at the depressed prices paid for such services in theunderdeveloped market of a poor country.

The unexpectedly higher cost of component B required a reallocation offunds among components resulting in a significant reduction of fundsavailable for component D. Two private consulting firms, however, didreceive specialized technical assistance that enhanced their competence.

Sustainability

The accountancy legislation is in place and effective as of Januar 1,1989. Some provisions concerning the accounting profession are still inthe process of being enacted.

INSCAE's (CFC) operating costs are still largely financed through Credit(MAG 1661) but government support will increase annually. When HAG 1661 isclosed, INSCAE is expected to be fully supported by government funds andits own revenues.

RINDRA's financial position is hopeless unless its debt to the governmentis drastically reduced. The debt may be converted to equity allowingRINDRA to become a private sector firm with a significant government stakein it if it is to continue as a financially viable accounting firm.

Findings and Lessons Learned

The political difficulties of introducing an accountancy law without thefull cooperation of the existing accounting profession had not beenforeseen. The profession, although very small, had significant politicalinfluence. The start up costs of the CFC far exceeded the originalestimates because the problems of procuring needed technical assistance hadbeen underestimated. The on lending arrangements for RINDRA proved toocostly; it was impossible for the firm to absorb the full costs of foreigntechnical assistance and remain competitive in local markets.

Both the Borrower and the Bank view the project as a success with somecaveats. The major unresolved problem was that while the accountancy codewas changed commercial law has not been changed tc conform to the new code.This issue has been taken up under Credit-1661 the follow on Credit to1155.

PART I

MADAGASCAR

ACCOUNTING AND AUDIT ORGANIZATION

AND TRAINING PROJECT

CREDIT NUMBER 1155 MAG

OVERVIEW AND BANK'S PROJECT COMPLETION REPORT

1. Project Identity

Name Accounting and Audit Organizationand Training Project

Credit Number 1155 MAG

RVP Unit AF3PH

Country Madagascar

Sector Education

2. Background

2.01 Immediately after independence in 1960, Madagascar's governmentencouraged investments in commerce and industry. As a result, value aidedin the industrial sector increased from 5% of GNP in 1960 to about 17% in1977.

2.02 The change in government in 1972 resulted in major policy changes,and many French managers and, technicians had left by 1975, when majorforeign-owned enterprises were nationalized. Top management and accountingpositions were then filled by people with inadequate experience. In theyears that followed, many public enterprises suffered from weak financialmanagement and were either unable to produce reliable financial statementsor prepared financial statements only after excessive delays.

2.03 Although an accounting profession had been established by law in1962, the profession had only 36 members, some with obviously inadequatequalifications, and no new admissions since 1971. Neither the universitynor any other institution offered any professional level of training inaccounting. Accounting at the University was not oriented to aprofessional qualification.

2.04 In the late '70s, the government took measures to ensure greatercontrol over the newly nationalized industries and established a nationalaudit company, RINDRA, in 1979. RINDRA was to provide audit servicesmainly to government owned and controlled companies.

2

2.05 In 1976, the government requested Bank assistan-e to financetechnical assistance to RINDRA by the international accounting fir.n. Sincethis assistance was to be financed retroactively and the fees involvedviewed excessive, the Bank initially declined. The Bank did, however,approve a subsequently submitted comprehensive accountancy project which

aimed at reforming accounting related laws, establishing a professionalschool of accountancy, strengthening the effectiveness of RINDRA andupgjrading the expertise of Malagasy management consulting firms. Theproject was appraised on May 11, 1981.

3. Project Objectives and DGscription

3.01 The long run objective of the project was to assist in theimprovement of business management through more effective accounting inboth nationalized and private sectors. The project had the following fourcomponents?

(a) A review of the existing accounting requirements for varioustypes of enterprises and of the professional standards requiredfrom accountants and auditors, and the preparation andimplementation of appropriate requirements in this respect,including proposals for legislation which, inter alia, wouldrequire enterprises in Madagascar to prepare audited accounts inaccordance with specified standards and classification ofaccounts under a national accounting code.

(b) Establishment and operation of an accounting training center(Centre de Formation en Comptabilitd) in Antananarivo, staffingthereof and the provision of training books and other coursematerials, supplies, services and equipment required for itsoperation.

(c) Strengthening of RINDRA's audit activities through the provisionof training and other assistance to its staff. To finan-7e theseservices, the government was to on lend to RINDRA USS 3.7million of the loan proceeds at 12% p.a. to be repaid in tenyears. The borrower would bear the exchange risk.

(d) Strengthening of the management services capability of selectedmanagement consulting firms through the provision of trainingand other services in the fields of financial systems andprocedures under sub-projects to be approved by the Association,and a feasibility study for the establishment of a publicmanagement consulting firm.

4. Project DesiLgn and Organization

4.01 The project was well-designed and apparently well-understood by allparties concerned. It was innovative in trying to create the prerequisitesfor the effective use of accounting as a planning and control tool bybusiness management and the government. In this context, it addressedsimultaneously the legislative, educational and professional dimension ofthe accounting function. It was also innovative in the sense that the

3

Anglo-Saxon concept of an audit was to be introduced in a society thathitherto was not acquainted with modern accounting and auditing.

4.02 The original project design was sound but unrealistic with regard tothe technical assistance cost estimates of component B; staffing the CFCproved much costlier than anticipated. The assumption that the entireMalagasy teaching staff could be trained locally was wrong. Extensiveoverseas training was necessary to assure an adequately qualified teachingstaff. Originally, the CFC was to hire its foreign Director General andteaching staff individually. When this proved impossible, a consultingfirm was retained to recruit both the CFC's director and its foreignfaculty.

4.03 The recurrent cost per student originally estimated at USS 2000.00will be below that amount when the school no longer needs foreign teachers.Expectations with regard to RINDRA's ability to reimburse the loan advancedby the government to finance its technical assistance were totallyunrealistic. Project planners were also too optimistic with regard to thetime required to pass a comprehensive accountancy legislation (includingrequired changes in the commercial law code).

4.04 With the exception of the shortcomings mentioned, the project'sconception and design were sound and contributed to its success.

4.05 In 1983, the government requested and the Bank agreed to extend theassistance to RINDRA to include the creation of a management consulting armwhich was to be operated as a division of RINDRA. This expansion of RINDRAreplaced the originally planned feasibility study lor the establishment ofa public consulting firm (Omega).

4.06 In 1985, the Bank co-financed with the Canadian bilateral aid agency,CIDA (or ACDI to use its French acronym), at the government's request, afeasibility study concerning the expansion of CFC into a graduate school ofmanagement through the addition of a two-year MBA program. Thismodification of the project, which involved changing the name of the CFCinto INSCAE (Institut National des Sciences Comptables et del'Administration d'Entreprises) was approved. With some delay, thenecessary legislation was passed and the two-year MBA program started in1988. INSCAE will be financed mainly under Credit 1661-MAG; there will besignificant cc-financing by ACDI and France.

5. Project Implementation

5.01 Critical variances in project implementation

5.02 Component A (Accounting Legislation): the Bank rightfully consideredtimely implementation of the legislation as a prerequisite for the successof components B and C. Serious delays were experienced because it took twoyears to identify and hire the consulting firm which was to prepare theproposals for the accounting legislation. The local accounting profession,concerned that new laws may threaten its status, exerted considerableinfluence to modify and delay the legislation. Although most of therequired legislation was enacted at the project completion date, importantparts were still missing. These include provisions regulating accees to the

4

profession and the precise definition of the "cursus" leading to thequalification as Expert Comptable (EC). The performance of the Frenchconsulting firm was satisfactory. The Borrower submiitted a detailed PCR,which, makes, among others, the following statements: 'It is regrettablethat the credit did not provide any funds for the dissemination of the"Plan Compteble" '. It does mention the many efforts (not financed by thecredit) by INSCAE, RINDRA and other accounting firms to disseminate thelaw. It was because of those efforts that the Bank did not consider this tobe a priority.

5.03 Component 3 (CFC-INSCAE): the cost of operating the CFC during thefirst three years (S 3.3 rnillion; exceeded the original estimates of theCFC for six years ($ 1.6 million). It had been planned that the newlyappointed Director General of the CFC would hire individual accountingteachers without the help of an overseas coordinating institution. Thisproved to be impossible. To assure the timely start of the project, itbecame necessary to engage a Canadian consulting firm to recruit the CFC'sdirector and the foreign teaching staff. The firm also assisted inarranging overseas training for future Malagasy teaching staff. Theinitial "Canadian" orientation of CFC's program was criticized by somelocal accountants. It occasionally caused some friction between Frenchoriented and Anglo-Saxon (Quebecois) trained teachers. These problemspractically disappeared with the requirements of the new accountinglegislation were incorporated in the CFCs curriculum. None of the schoolsfirst graduates experienced any serious difficulties because of this socalled "Canadian' orientation. At the beginning, the consulting firm'sperformance was very good, but its refus-l to cooperate with potentialfuture co-financiers and a newly appointed, Bank approved, French Dean ofStudies, necessitated the termination of all ties with that firm.

5.04 Component C (RINDRA): RINDRA's foreign Director General, appointedunder the Credit, proved ineffective and controversial. He was replaced bya Malagasy director who turned out to be dynamic and efficient.Performance of the original consulting firm was satisfactory, while that ofthe second firm was generally appraised aa excellent. The expectation thatRINDRA would be able to reimburse the loan advanced by the governmentturned out to be unrealistic. To expect RINDRA to acquire its neededadditional skills at world market prices and then to sell them at similarprices on a market that, at least initially has little appreciation forsuch services, proved to be too optimistic. Although RINDRA is able togenerate positive operating cash flows, paying interest and reimbursingthis debt far exceeds its present and future capabilities. The decision tofina'.:e RINDRA's technical assistance through a loan was allegedly based ona f recast of RINDRA's earnings potential made around 1980. This forecastmisjudged the market for auditing and consulting services in a developingcountry. In the early phases of development such a market is minimal. Asit gradually develops it commands prices that are in tune with price levelof its undeveloped environment, hence far below the world market level.

5.05 The delay of component A could have been reduced somewhat had it beenmade clearer from the start that a firm %ith international experience wasneeded. As _.t was, the three firms, essentially making up the Malagasyaccounting profession, who wanted the contract for themselves, used theirsignificant political influence to get on the short list and to influence

5

the choice of firms. This led to protracted delays. It would have beendifficult to foresee these problems during project preparation.

5.06 The cost overrun for component B could have been reduced (but notavoided) if the absence of anyone to manage the initial establishment ofCFC, and the problems of availability and cost of accounting teachers hadbeer correctly assessed. Ideally, a contract with a university should havebeen sought for the organization and management of the school. TheassumptLon that RINDRA would be sufficiently profitable to repay the loanshould have never been made.

5.07 The appraisal report d'd not identify the risk of delaying theproject's completion by the delay of component A. The other risks, nameyLthe timely appointments of foreign directors for the CFC and RINDRA,mentioned in the appraisal report were of no consequence.

5.08 Under component D only two sub-projects were successfully completed.Originally, this component also provided for a feasibility study for theestabl.shment of a public consulting firm. The Borrower's Projectcompletion report states (p. 40) that the conditions for this assistancewere not stated clearly and never adequately publicized. This allegedlyexplains the delay in submitting projects for approval. Only two projectswere submitted. Both were approved. The first submiss!.on was on November17, 1983.

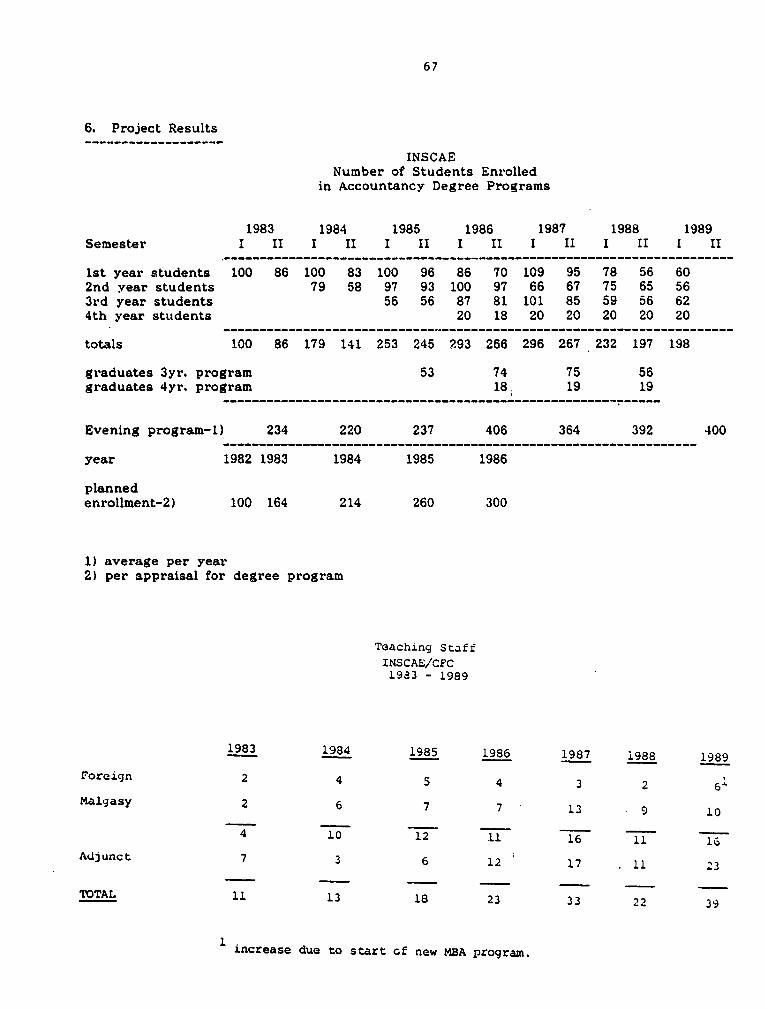

6. Project results

6.01 Component A: A modern accountancy law adapted to Madagascar's needswas passed in 1987 (Plan comptable). Still to be enacted are relatedchanges in the Commercial Law Code, important provisions regulating accessto the profession, and the "cursus" leading to the qualification" expertcomptable".

6.02 The project's most successful component was the establishment andstaffing of the CFC, latter renamed INSCAE. The school started operationsin 1983 and currently graduates approximately 50 to 60 students from itsthree-year accountancy program and another 20 from its four-yearprofessional accountancy program. Its fully tuition-financed eveningschool has an enrollment of approximately 400 per year. Graduates have nodifficulty in finding appropriate employment. The project also providedthat RINDRA prepare a study estimating Madagascar's demand for accountants.The study, started in 1983 but never completed, was to serve as a guidelinefor the future expansion of INSCAE's accounting programs. It will now becarried out by INSCAE.

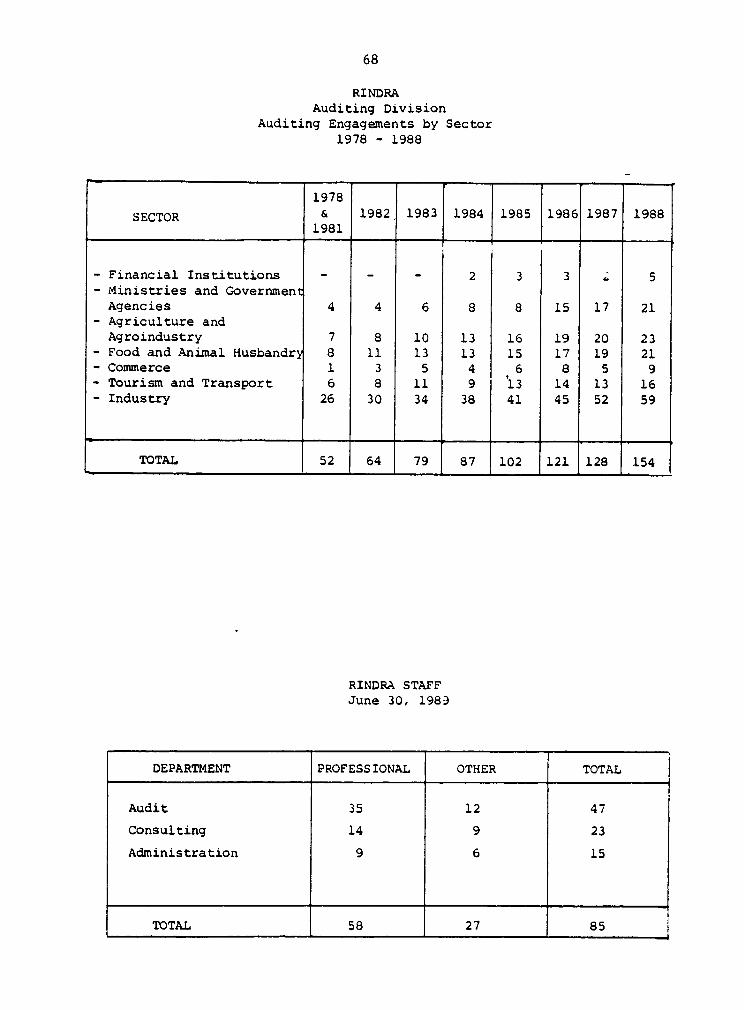

6.03 component C: The technical assistance to RINDRA, despite some initialproblems with an expatriate director, must be judged successful. RINDRA isnow fully under Malagasy management. The auditing division presently has astaff of thirty-five qualified accountants who are organized along thelines of modern accounting firms with solid programs of internal trainingand quality control. RINDRA has as its clients some of Madagascar sbiggest companies and is well known for the quality of its audit work.

6

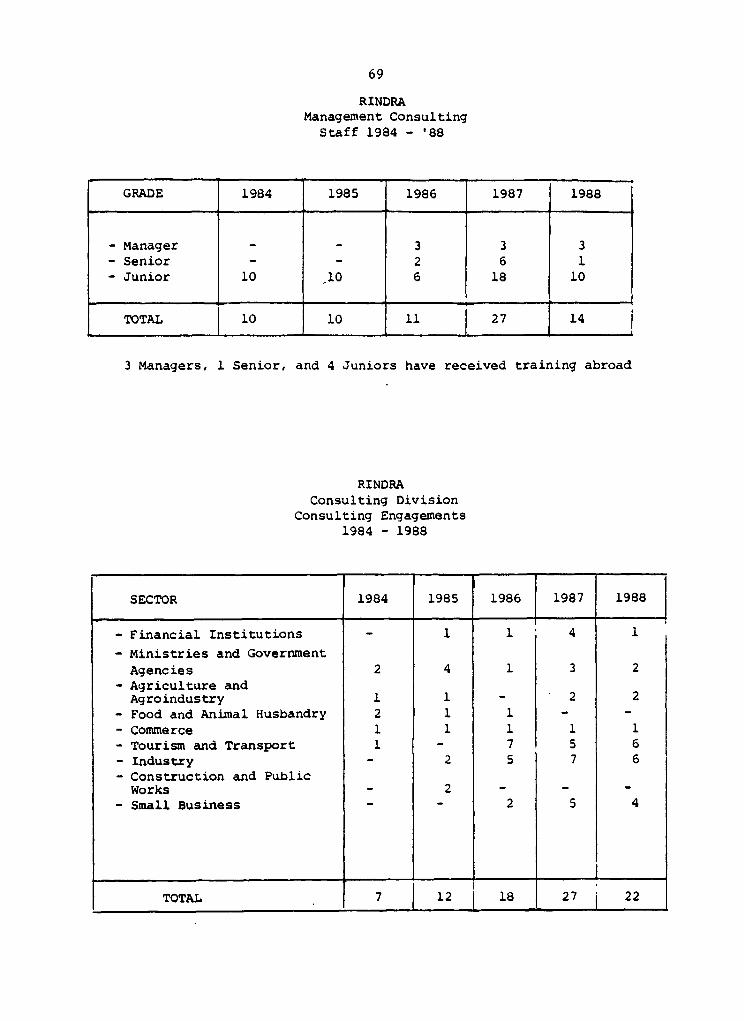

6.04 The consulting division of RINDRA now employs 20 professionals,enjoys a good reputation and is now apparently operating at a profit beforedebt service. Because of its debt to the government, RINDRA will befinancially viable only if this debt is drastically reduced or annulled.

6.05 The new accountancy law requires that accounting firms be fullyindependent. This precludes government ownership and control of anaccounting firm. If RINDRA is to continue to function as an auditing firm,it must be reorganized as a private firm. Present plans call for theprivatization of RINDRA and the reduction or annulment of its debt; thegovernment will retain cnly a small minority interest in RINDRA's equity.

6.06 Component D (Technical Assistance to Malagasy Management Consultingfirms): the two main private accounting and consulting firms, Fivoaranaand Ramaholimihaso, received some effective technical assistance fromFrench accounting and consulting firms that improved the quality of theirservices in the area of computerized systems.

7. Project Sustainability

7.01 A modern accounting legislation is in place, although some detailsconcerning the regulation of the accounting profession are yet to beenacted. Both INSCAE and RINDRA have been instrumental in disseminatingthe new law through courses and seminars. The legislation has beencarefully analyzed and modified to adequately meet the requirements of theMalagasy economy. It became effective on January 1st, 1989.

7.02 The accountancy training project should be viewed as a success.INSCAE turns out wwll-trained accounting graduates. All find employment atsalaries significantly higher than those of university graduates. Foreigntrained Malagasy teachers constitute about 80% of its teaching staff, andin the foreseeable future the program will no longer depend on expatriateteachers. Currently most of INSCAE operating costs are still financed bythe Bank (Credit 1661-MAG). It is planned that the Government ofMadagascar will finance an annually increasing share of these operatingexpenses. INSCAE is able to generate revenues from both the public and theprivate sector through its continuing education seminars and consulting.This revenue plus the tuition paid by students will never amount to morethan 30% percentage of its annual budget. A study in 1987 required underthe Credit agreement showed that many students would have difficulty inpaying more than they do and recommended against increasing tuition feesfor full-time students.

7.03 RINDRA's future success as an auditing and consulting firm dependsonly on its successful privatization and the reorganization of itsfinancial structure. There are indications that both problems will beresolved in the foreseeable future.

8. Bank Performance

8.01 Bank Performances The Bank's Performance was satisfactory. Itcontributed to the project's success by strongly insisting that deadlinesbe observed and covenants respected (not always successfully).Overestimating RINDRA's financial viability and underestimating the cost of

7

initially staffing the CFC were the only important planning errors.Supervision missions of the project were carried out about twice a year byEAPED staff, from 1985 on with the assistance of an accounting specialistconsultant. Supervision of the project was adequate.

8.02 There were three crises that had to be faced by the Bank: (1) when itturned out that the initial staffing of the CFC would require the servicesof a consulting firm, Bank staff decided quickly and correctly that theresulting higher cost outweighed the alternative of delaying the project;(2) when RINDRA's ineffective Director General was replaced by a Malagasynational, the Bank re'uctantly agreed to what turned out to be a sounddecision; and (3) when the initially excellent work of the CFC's firstcon'ulting firm deteriorated to the point where the continued success ofthe project was threatened, the government was correctly permttted to cutall ties with that firm.

9. Borrower Performance

9.01 The Government consistently showed a strong commitment to theproject. It fully supported the concept of creating the CFC as a "grande4cole", separate from the university; it provided adequate premises for theschool and gave full support to the politically difficult enactment of theaccounting legislation. It seems willing to restructure RINDRA as aprivate firm to assure its continued functioning as an effective accountingand consulting firm.

10. Pro4ect Relationships

10.01 Government-Bank relationships were satisfactory throughout theproject. Through the initial engagement of a Canadian consulting firm, itwas possible to interest Canada's foreign aid (ACDI) program in theproject. ACDI is now making a significant contribution to INSCAE'sprograms. The Bank was also successful in enlisting FAC assistance forfinancing of some highly qualified French teichers for INSCAE.

11. Conclusions, Recommendations and Lessons Learned

11.01 The Borrower's report makes the following recommendations:(a) Early creation of the "Conseil Supdrieur en Comptabilit4" todeal with some remaining legal problems, and new issues in accountingand auditing.(b) The early enact.,ient of the rules concerning the accountingprofession.(4) Implementation of #2 will enable INSCAE to fulfill its originalmission of training future "experts comptables".(d) The government should prepare a strategy to modify INSCAE'sobjectives and to assure its financial viability.(e) The financial reorganization of RINDRA by converting its de'-it toequity capital and changing its legal status into a partnership.(f) Another technical assistance contract to strengthen theconsulting division of RINDRA.

11.02Bank's comments on above recommendations:- Recommendations " a" and " b" are reportedly in the process ofbeing implemented.- Regarding recommendation " c", INSCAE is fully qualified and hasthe capacity to teach any preparatory "cursus" for the "expertisecomptable" once such "cursus" is defined.- As to recommendations "d" and "e", INSCAE is presently preparirng along range strategy which will be discussed and analyzed with thegovernment, the Bank and the co-financters. The reorganization ofRINDRA and the change of its legal status are currently beingnegotiated by RINDRA staff and the government. Final and successfulconclusion of these negotLations is expected by mid-1990.- With regard to "f", RINDRA is presently the beneficiary of an ACDIfinanced technical assIstance program for its management consultingdivision.

11.03The political difficulties of introducing an accountancy law withoutthe full cooperation of the existing accounting profession had not beenforeseen. The profession, although very small, had significant politicalinfluence. The start up costs of the CFC far exceeded the originalestimates because the problems of procuring needed technical assistance hadbeen underestimated. The on lending arrangements for RINDRA proved toocostly; it was impossible for the firm to absorb the full costs of foreigntechnical assistance and remain competitive in local markets.

11.04Both the Borrower and the Bank view the project as a success withsome caveats. The major unresolved problem was that while the accountancycode was changed commercial law has not been changed to conform to the newcode. This issue has been taken up under Credit-1661 the follow on Creditto 1155. There are no significant differences in the findings andconclusions of the Bank and those reported by the borrower.

9ANNEX

DEMOCRATIC REPUBLIC OF MADAGASCAR,Antananarivo, 7th September, 1990

Ministry of Finance and Budget

GOVERNMENT COMMENTS ON BANK REPORT

OFFICE OF THE MINISTER

The Resident Representative,The World Bank

RE: Government of R.D.M.'s commentaries about the report of Post evaluationof credit 1155-MAG.

Dear Sir,

Please find hereafter the Government of R.D.M.'s commentaries aboutthe report of Post evaluation of credit 1155-MAG:

a) General view

In general, the report is an accurate reflection ofthe project's history.

b) Political problems encountered in the introduction ofthe new 1987 Malagasy accounting plan

Three years passed between the time when the FrenchConsulting Firm started its activities and thepublication day of the new accounting plan. Webelieve that the difficulties met during .his periodof time were not due political reasons, but rather,the mair. reason for the publication delay of the newaccounting plan were technical problems.

The draft accounting plan prepared by the Consultantfirm was the subject of two seminars organized by thefirm at the Hilton Hotel, during which every detail of540-page draft report was analyzed. The seminarparticipants included accounting professionals,accounting teachers in addition to key representativesof the Public and private sectors concerned withaccounting issues. Other technical meetings followedthose seminars before the document was finalized.

For your information, the 1957 French plan revisionofficially started in 1971 and a waiting period ofmore than 11 years was necessary before the new Frenchaccounting plan was definitely established.

10

c) Concern of the Accounting Profession Regarding itsStatus

The accounting profession did not have any reason tofear that its status would be Jeopardized by the newdispositions which concerned strictly technicalmatters. Indeed, such a change in the statusaccounting profession only happen in the context of anew law governing the profession which is currentlygoverned by regulation no.62.104.

d) Political problems in the new Accountinz Planpromulgation

The new Accounting Plan promulgation decree, wasconsidered in the Council of Ministers. The discussionwas fairly straightforward as all Ministers gave theiragreement.

e) RINDRA File

The miscellaneous points raised as well as therecommendations stated in the report are presentlybeing considered in the context of a global settlementof the RINDRA issue.

Yours sincerely,

Leon RAJAOBELINA

Minister

t11 ~ '-"-b '07 SEP IMMINISYtrk 090 PINANCES

JT aU SUDGEKT

Li MANINY Monsieur LE REPRESENTANT RESIDENT DELA BANQUE IlONDIALE

- ANTANANRIVO -

N- WBC /SG/DPC

0 B J t : Comntairts du ouvernhmnt de la R.O.M. sur la rapportde Post &valuation du cr6it 1155-MM.

Monsieur Lt Reprisentant.

Ja1 1 mhonmur da vous faire connaitre quo le rapportdu post Ivaluation du cridit 1155-NM applle do la part du Gouvernem_ntde la R.D.M. Its comentaires ci-apris

*) Vue globale.

Dans l'ansOle l rapport reflte correctawnt lavie du proJet.

b) Problus golitiq rencontrhes dans 1'introductIondu nouveau pian comptab a m lpace 1557.Entre Is ammut Io le consultant frgacis Audit etsysthms a commnei ses travoux et Io Jour de laparution du nouveau plan coptable 11 seat GcoulQenviron 3 ans.Nous esti* ns quo les difflcultAs rencontries aucours do cette pr1ode n'avalent *bsolumentu sa un carac-

Le principal facteur qul a reterd# la purtlion dunouveau plan ccsptable est essentiellmnt dtordretochnique.En effet, le projet de plan co qtabe pipar# parla cabinet framaips Audit et syst s a felt I obJetdo doux shinaires animis per leurs autaurs I PlHotelHilton et *u cours desquels ont At& examins chequepage d'un volum do 540 pages.

--.I ~ ~ -4o-,

Re~v~ lZ49+.

~~~~~~~~d

12 t1sif 3

Les participants l ces sb"inaires ftaient desprefessionnels de I& ceaptabilit#, des prefesseurs de l'Ense1-gnement Supiriour en gestien. des personnal1tds du secteurpublic concern6es per la co.ptabilitf (Pr6sident de la Chambredes Coptes, Directeur G6neral de l'inspection Gn#ra1ede l'Etat etc....) ainsi quo des op6ratours 6cononiques.

Ces siminaires ont 6t0 suivis d'autres rOunionstechniques avant de parmnir au docu ent final.

A titre dlinforsation. on notere que la rivisiondu plan frangals de 1957 a comnenc6 officieTlemnt en 1971et 11 a fallu une piriode de gestation de plus de 11 ansavant que le nouveau plan comptable franqais alt pris saforum dffinitive.

c) Inquiftude de la profession comptabe qjuant I son statut.La profession comptable n'avait aucune ruison

de votr son statut mnac6 p.r les nouvel;s Gispositlonsqu1 sont d'ordre puruumnt technique.

Un changsmut Iventuel du statut de la professioncomptable ne peut en effet intervenir que dans le cadred'une nouvelle 101 organisait la profession coWtable laquellemSt rZile actuell_emnt par l'ordonnace 62.104

d) Difficult# politi quo dans_la promulgation du nouveau Plam(mtab1 0.

La pramlgatlon de nouveau plan comptable quisest faite par d6cret pris en 'Conseil des Ministres i ttris facile pu1sque tous les Minist6res ont accordi lourvisa lors de la camunication tournante y afffirente.

0) Dossier RINDRAtis divers points soulev6s dans le rapport ainsi

quo los recoamandtions qul y sont foruulles sont actuell emntexainmis dans le cadre d'un rgli_nt global de la situationde RINDRA.

VeWuilez nsiour Le Reprisentant, l'assurancede ma haute consid

~~~~~~~~~~~~~~~~~~~~~~~~~~~I

13

PART II

GOVERNMENT'S PROJECT COMPLETION REPORT 5/

1. SUMMARY AND CONTEXT AND OBJECTIVE OF STUDY

CONTEXT AND OBJECTIVE OF MISSION

1.01 In accordance with the provisions of Section 3.05.b of DevelopmentCredit Agreement 1155-MAG, the Government of Madagascar is to provide theWorld Bank, by six months following the closing of the credit or at anylater date agreed with the World Bank, with a complete and detailed reportaddressing the following topics:

- execution of and initial operations under the Project;- costs of the Project and advantages deriving or expected to be

derived therefrom;- execution of obligations incumbent on the Government of

Madagascar and the World Bank, respectively;- achievement of the objectives of the credit.

1.02 The purpose of our mission is to draft the completion report for theAccountancy and Auditing Organization and Training Project financed byCredit 1155-MAG on behalf of the Government of Madagascar.

METHODOLOGY

1.03 The mission was carried out in the three following stages:

- Survey of documentation (appraisal report, contracts, variouscorrespondence, etc.);

3 Analysis of the documentation;- Discussions with various leaders who participated in project

development, execution and monitoring.

STRUCTURE OF REPORT

1.04 This report addresses in turn:- summary and background;- the description of the project;- conduct of the project;- results and problems;- conclusions and recommendations

HISTORICAL OVERVIEW

1.05 The chronological starting point for this project was the idea ofestablishing a National Auditing Corporation in June 1978. Taking intoaccount the suggestions of tht accounting profession and bearing in mind

5/ The borrower's report was prepared in French by Malogasy Consultants, Fiovarans andRINDRA, on behalf of the Government who submitted it to the Bonk. It was translated by theBank. The original French version is available from Africs Files. Copies of tho Frenchversion are being supplied to the Operations Evaluation Department. This report was preparedfor the Government and the World Bank Is not rosponsible for the opinions expressed ;n thereport.

14

that the interventions of the National Auditing CorporatLon would beeffective only if enterprises have the capacity and the legal obligation tosubmit their financial statements in a form which can be audited, in January1990 the World Bank defined a "national accountancy project" which not onlyincluded auditing, but also covered the organization of the profession, thedefinition of a national accounting framework, the training of accountants,and enhancement of the intervention capacity of private accountancy firms.

1.05 The accountancy and auditing organization and training project, aproject to assist the accounting profession, thus included the followingfour components:

- Component A: Study of accounting standards and legislation- Component B: Creation and operation of an Accountancy Training

Center- Component C: Strengthening of the activities of RINDRA

Socialist Enterprise- Component D: Support of private management consulting firms.

OVERVIEW OF THE CREDIT AGREEMENT

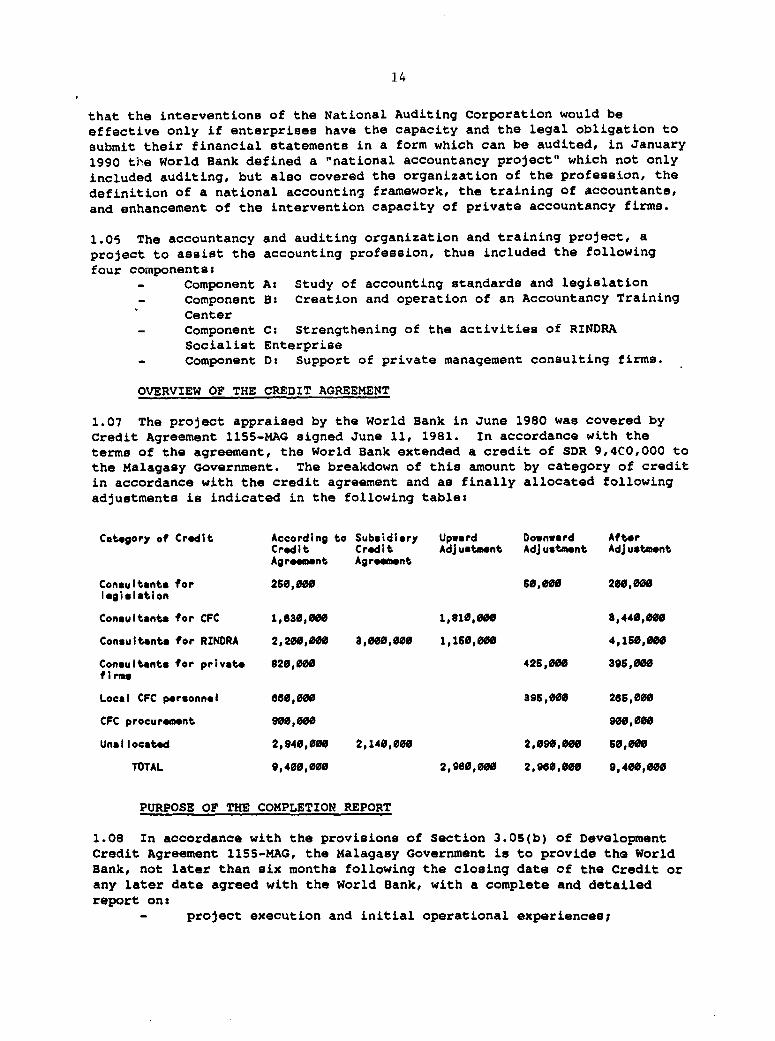

1.07 The project appraised by the World Bank in June 1980 was covered byCredit Agreement 1155-MAG signed June 11, 1981. In accordance with theterms of the agreement, the World Bank extended a credit of SDR 9,4CO,000 tothe Malagasy Government. The breakdown of this amount by category of creditin accordance with the credit agreement and as finally allocated followingadjustments is indicated in the following table:

Category of Credit According to Subsidiary Upward Downward AfterCredit Credit Adjustment Adjustment AdjustmentAgreement Agreement

Consultants for 260,000 50,000 200,00legislation

Consultants for CFC 1,630,000 1,810,000 3,440,000

Consultants for RINDRA 2,200,000 3,600,000 1,160,000 4,160,0MO

Consultants for private 820,000 426,000 396,000fIrms

Local CFC personnel 680,600 395,0ao 286,000

CFC procurement 900,0i0 900,000

Unallocated 2,940,000 2,140,060 2,090,000 s6,o00

TOTAL 9,400,606 2,980,000 2,986,006 9,400,000

PURPOSE OF THE COMPLETION REPORT

1.08 In accordance with the provisions of Section 3.05(b) of DevelopmentCredit Agreement 1155-MAG, the Malagasy Government is to provide the WorldBank, not later than six months following the closing date of the Credit orany later date agreed with the World Bank, with a complete and detailedreport on:

- project execution and initial operational experiences;

15

project costs and the gains derived from it or expected to bederived from It;

- performance by the Malagasy Government and the World Bank of theobligations incumbent on each of them, respectively;

- accomplishment of the objectives of the credit.Our mission iL to draw up the completion report for the Accountancy andFinancial Auditing Organization and Training Project under Credit 1155-MAGon behalf of the Malagasy Government.

2. GENERAL INTRODUCTION

2.01 Preparation of the project effectively waS spread over a three-yearperiod from June 1978 to June 1981. The first 20 months were devoted to thepre-identification phase. The project, exclusively for technical assistanceof a new kind for the World Bank, was not within the purview of any of itscustomary divisions, which produced a good deal of hesitancy.

2.02 The date on which the credit took effect, scheduled to be October 12,1981, subsequently was postponed until May 6, 1982. The process of hiringof the Directors-General of CFC (Accountancy Training Center] and RINDRA,who were intended to be expatriates and whose appointment constituted one ofthe Bank's conditions for the entry into force of the credit, took nearly ayear. The closing date for the credit, initially scheduled for March 30,1989, was thus moved back to June 30, 1989.

CONDUCT OF THE PROJECT

Component A: Accounting Standards and Legislation

2.03 The component devoted to "accounting standards and legislation" hadthe following aims:

examination of the regulations applicable to the various typesof enterprises as regards accounting and of the professionalstandards to which accountants and auditors must adhere.

- drafting and implementation of appropriate regulations,including draft laws which would require, inter alia, thatMalagasy enterprises establish accounts which are audited inaccordance with specific standards and with a national plan ofaccounts.

2.04 This component, considered to be a priority, was the one in which thegreatest delay was experienced. The Bank had scheduled the introduction ofnew legal provisions on accounting legislation for July 1982, while theconsulting firm which was to assist the Government in this work was notformally announced until January 29, 1985, i.e., two and a half years later.This delay is basically attributable to:

- rather long delays in:+ preparation of the short list of consultancies;+ final drafting of the terms of reference;+ international call for bids;+ fine-tuning of the contract between the Government and the

consultancy;

16

- problems of relationships between the Order, theGovernment and the Banks in effect, the Order argued foran expansion of the project as well as for its intensiveinvolvement in project execution. For this reason, thePresident of the Order participated in the negotiations inApril 1981.

2.05 These factors were compounded by the fact that the foreign expertsselected for the study were unfamiliar with prevailing conditions inMadagascar, which led to lengthy discussions and numerous revisions duringthe course of conducting the study, and even required members of the firmMalagasy accounting profession (order, INSCAE, RINDRA) to participateactively and decisively in completing the study for Component A: criticalanalysis, formulation of recommendations, final drafting of the regulatoryprovisions and the annotated guide.

2.06 The 1987 code of accounts (PCG 87) constitutes the most palpableachievement of the project, as company law has yet to be affected. Theproject, however, provided for no financing for dissemination of the newcode of accounts, and the request for World Bank financing made first by theConsultants and later by the Malagasy Government, has yet to be acted upon.Initial dissemination work has been begun anyway by local accountingconsultancies and the INSCAE; several enterprises have already submittedtheir latest financial statements (1988) in accordance with the new code ofaccounts, whose effective date has been postponed until January 1, 1990. Asregards the accounting profession, specific proposals have been submitted tothe authorities to bolster the Ordre des Experts Comptables et ComptablesAgr44s [Order of Expert Accountants and Authorized Accountants] under thetransitional provisions and to create structures that will be called upon todefine the training course to be routinely offered for purposes of obtainingthe National Diploma of Expertise in Accounting.

2.07 Our principal recommendations relate mainly to the following points:- Creation as soon as possible of the Supreme Accountancy Council

for resolving existing problems (sectoral codes of accounts,practical modalities for implementing certain accountingprinciples, etc.);

- Publication of the legal and regulatory provisions governing theaccounting profession: training using the course for expertaccountants and organization of access to the profession underthe transitional provisions;

- Evaluation of the training needs relating to the 1987 generalcode of accounts and its dissemination, so as to define thesteps to be taken.

Component B: Creation and operation of an Accountancy Training Center

2.08 This component concerns:- creation of the Accountancy Training Center (CFC) in

Antananarivo;- hiring of the staff needed by the Center;- furnishing of training manuals and other educational materials,

supplies, services, and equipment necessary for its operation.

17

2.09 The operation of the Accountancy Training Center (CFC) began inFebruary 1983, itself some 10 months behind schedule, owing in particular to

the delay in hiring the Director-General and to the considerable workinvolved in rehabilitating the three stories made available to the Center inthe "House of Products." Moreover, because of an inadequate projectappraisal, the credit planned to cover 6 years was exhausted in 3 years,

making necessary:- on the one hand, an adjustment in the initial credit by drawing

against the non-earmarked funds and against the funds intendedfor Component D; and

- on the other hand, the preparation of a second project in the

amount of $13.1 million to continue the teaching of accounting,but under a new name: The National Institute for AccountingSciences and Business Management (INSCAE), established inSeptember 1986 and now financed by the new Credit 1661-MAG.

2.10 This being so, CFC endeavored to maintain the category of "grande

4cole" and provide complete or partial training to nearly 300 high quality

accountants (number not including that of students in evening courses)before it was transformed into the INSCAE, which thus benefitted from itsrolling start.

2.11 However, this pertaxns to Credit 1155-MAG, and does not cover the

study on the current INSCAE (functioning and effectiveness of the ExecutiveBoard, degree of effectiveness of the Pedagogical Council, etc.), which is

part of Credit 1661-MAG. Such a study is, moreover, envisaged by the

management of the INSCAE.

2.12 Inter alia, it is necessary to study the ultimate coverage of

CFC-INSCAE costs under the General State Budget. In addition, themanagement of the INSCAE currently wish to know:

the status of the INSCAE as regards the other institutions fortraining accountants both in Madagascar and abroad;whether the structure and organization of the INSCAE are adaptedto its activities;

- whether its activities relate to the needs of the market both inqualitative and quantitative terms.

2.13 Accordingly, a study covering the three following components isenvisaged:

- pedagogical audit;- management audit; and- market study.

Component Cs Activities of RINDRA Socialist Enterprise

2.14 The reinforcement of RINDRA's activities involves training of its

supervisors and the supervision of its work by an outside consultancy.

After two or three years of indirection initially, RINDRA now has a soliemastery of the audit function (a staff of 35 in the division), initial

18

experience in management counselling (a staff of 14 in the division), asound internal organization, and a reputation for professionalism.

2.15 However, the long period of external technical assistance has provenextremely costly, making RINDRA's financial position unsustainable, all themore so as the terms for on-lending the credit ultimately proved to be tooharsh. Indeed, given the burden of its debt to the Treasury (SDR 4.15 mil-lion over 10 years at 12 percent), the company is virtually at the point ofceasing payments. During the course of our mission, It was not possible toproduce any document testifying to the anticipated capabilities of RINDRA tosupport financing on this large a scale. In addition, it bears noting thatRINDRA's status as a socialist enterprise is not such as to ensure thestability of its senior staff.

2.16 As regards the study on needs for accountants in Madagascar providedfor under the Credit Agreement, this was to be dealt with by the formerexpatriate Director-General of RINDRA, but ialtimately was not completed. Inthis connection, however, the INSCAE, at the request of its Board ofDirectors, intends to conduct a market study in order to determine bothquantitative and qualit"cive accounting requirements with a view toadjusting class sizes provide teacher training at the INSCAE.

2.17 It would be advisable to revise the status of RINDRA so as to make itlegally independent and to enable its higher ranking staff to have access topartnership. Moreover, a financial restructuring of RINDRA is mandatory soas to enable it to develop sufficient positive rolling capital and asufficient gross self-financing margin.

Comsonent Ds Support for Private Management Consultancies

2.18 This component enables the firms concerned to use the credit tofinance support in financial and accounting organization from an outsideconsultancy firm.

2.19 As regards the component on enhancing the capacity of the privateconsultancies, 52 percent of the small amount of credit provided for had tobe allocated to other needs, which made it possible to carry out on y twoexternal assistance operations. This external assistance, however, didstrengthen the capabilities of two private firms as regards managementconsulting services and bank auditing.

2.20 It must be acknowledged that project 1155-MAG is a success, thisbecause the project made it possible for:

- the country to have a more modern code of accounts that isadapted to its needs;

- the accounting profession to clarify the problems relatlng toaccounting regulations, ongoing training of accountants and theorganization of access to the profession, under the transitionalregulations;

- CFC to provide partial or complete training to almost 300acco ntants (excluding evening courses) before its activitieswere ta .an over by the INSCAE;

- RINDRA to become a highly capable accountancy firm; and

19

- two private firms to take advantage of external assistance tostrengthen their capacities in management consulting.

2.21 However, the project has the two following major weaknesses, which arestrictly financial in nature:

_ the initial loan allccation for a six-year period to CFC wasexhausted in only three years; and

- the financial structure of RINDRA is unsustainable owing to theterms for on-lending.

BASIC DATA ON THE PROJECT

PROJECT: Project for Accountancy and Auditing Organization and Training inMadagascar (1155-MAG)

Component A

Examination of the regulations applied to the various types ofenterprises as regards accountancy and of the professional standards towhich accountants and auditors must aspire; development and implementationof appropriate regulations, including draft laws which would require interalia that the Malagasy enterprises draw up accounts which would be auditedin accordance with specific standards and would establish a nationalaccounting code.

Component B

Creation of an accountancy training center in Antananarivo; hirirn ofthe necessary staff for said center; and provision of the training manualsand other educational tools, supplies, services and equipment necessary forits operation.

Component C

Enhancement of the activities of RINDRA.

Component D

Strengthening of the capacity of domestic management consultancyfirms.

Borrower

Government of Madagascar.

Executing Agencies

As originally planned:

- Ministry of Economy and Commerce, as regards the consultancyservices for purposes of helping develop accounting mechanismsand methods and preparing legislative measures.

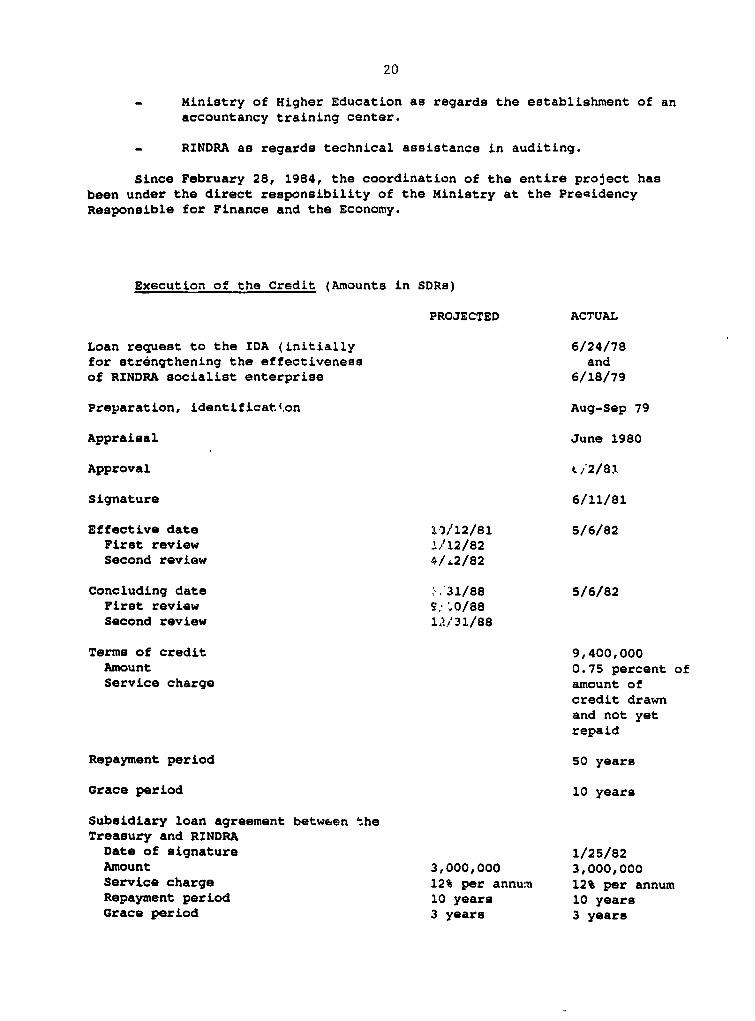

20

Ministry of Higher Education as regards the establishment of anaccountancy training center.

RINDRA as regards technical assistance in auditing.

Since February 28, 1984, the coordination of the entire project hasbeen under the direct responsibility of the Ministry at the PresidencyResponsible for Finance and the Economy.

Execution of the Credit (Amounts in SDRs)

PROJECTED ACTUAL

Loan request to the IDA (initially 6/24/78for strengthening the effectiveness andof RINDRA socialist enterprise 6/18/79

Preparation, identificat4 .on Aug-Sep 79

Appraisal June 1980

Approval C/2/81

Signature 6/11/81

Effective date /l12/81 5/6/82First review J/12/82Second review 4/42/82

Concluding date .. 31/88 5/6/82First review S.:;.0/a8Second review 1.! 31/88

Terms of credit 9,400,000Amount 0.75 percent ofService charge amount of

credit drawnand not yetrepaid

Repayment perLod 50 years

Grace period 10 years

Subsidiary loan agreement between theTreasury and RINDRA

Date of signature 1/25/82Amount 3,000,000 3,000,000Service charge 12% per annumn 12% per annumRepayment period 10 years 10 yearsGrace period 3 years 3 years

21

Codicil to the subsidiary loanagreement between the Public Treasuryand RENDRADate of signature 7/18/86Additional amount 1,150,000Credit increased to: 4,150,000Service charge 12% per annumRepayment period 6 yearsGrace period 2 yearsPenalty interest (on all amounts 3.5% per annumdue and paid at a date afterthe due date)

Financial status of credit as atMarch 31, 1989Amount 9,400,000 9,400,000Amount released 9,359,809Balance 40,190.83

22

3. HISTORY OF PROJECT

ENTERPRISE MANAGEMENT ASSISTANCE PROJECT

3.01 In 1978, the Mlnistry of Economy and Commerce designed an enterprisemanagement assistance project in cooperation with two major internationalfirms. There were three components to this project:

- creation of a National Auditing Corporation;- creation of a Management Consulting Company;- creation of a National Center for Management Training.

3.02 The Commission of the European Communities had previously shown greatintereHt in the establishment of the National Center for ManagementTraininlg, an'd the Government of Madagaecar sought the cooperation of theWorld Bank for support of the first two project components. The requestwent unanswered.

TECHNICAL ASSISTANCE PROJECT FOR STRENGTHENING THE EFFECTIVENESS OFRINDRA

3.03 After the establishment of RINDRA socialist enterprise on April 7,1979, efforts were concentrated within this auditing firm. In June 1979, acredit of $2,300,000 was requested from the World Bank to finance technicalassistance from the consulting firm for purposes of enhancing RINDRA'seffectiveness, it being intended to provide retroactive coverage of fees,which were regarded as too high. This second request was not approved bythe World Bank, which did, however, consider the issue at length beforereaching its final decision.

NATIONAL ACCOUNTANCY PROJECT

3.04 Taking into account the suggestions of the profession and the factthat RINDRA's activities would be effective only if the enterprises wereboth able and legally required to provide their financial statements in anauditable form, in January 1980 the Bank defined a "national accountancyproject" including, to be sure, auditing, but also the organization of theprofession, the definition of a national accounting framework, the trainingof accountants, and the enhancement ef the intervention capacity uf privatefirms. This intearated project was appraised by the Bank in June 1980 andwas covered by Credit Agreement 1155-MAG signed on June 11, 1981.

3.05 A modest project entaillng assistance to a National AuditingCorporation thus led three years later to a project for assistance to theentire profession at a total cost of $14.2 million. Preparation of theproject was somewhat time consuming. This project, focused solely ontechnical assistance, was of a new type for the World Bank, and did not fallwithin the purview of any of its divisions. This resulted in a good dea.. ofhesitation. The World Bank finally took advantage of a number of missionsto Madagascar by an expert from the Energy and Water Division and entrustedhim with the project appraisal.

PRINCIPAL CHARACTERISTICS OF THE PROJECT

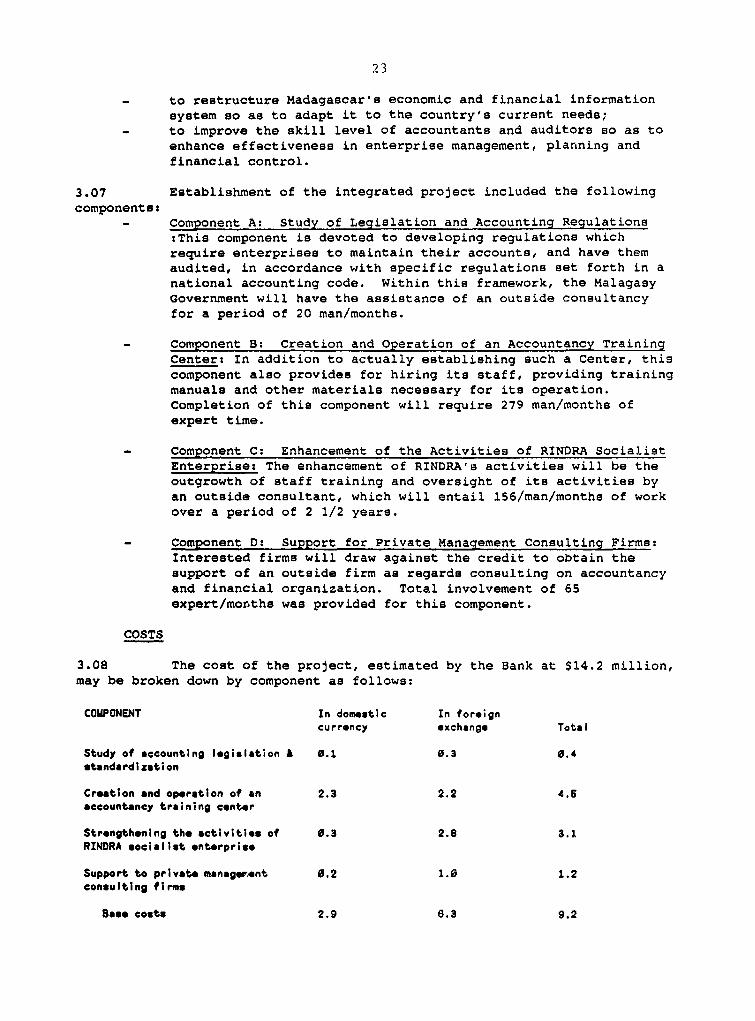

3.06 The objectives of the project were:

23

- to restructure Madagascar's economic and financial informationsystem so as to adapt it to the country's current needs;

- to improve the skill level of accountants and auditors so as toenhance effectiveness in enterprise management, planning andfinancial control.

3.07 Establishment of the integrated project included the followingcomponents:

- Component A: Study of Legislatlon and Accounting Regulations:This component is devoted to developing regulations whichrequire enterprises to maintain their accounts, and have themaudited, in accordance with specific regulations set forth in anational accounting code. Within this framework, the MalagasyGovernment will have the assistance of an outside consultancyfor a period of 20 man/months.

- Component B: Creation and Operation of an Accountancy TrainingCenter: In addition to actually establishing such a Center, thiscomponent also provides for hiring its staff, providing trainingmanuals and other materials necessary for its operation.Completion of this component will require 279 man/months ofexpert time.

- Component C: Enhancement of the Activities of RINDRA SocialistEnterprise: The enhancement of RINDRA's activities will be theoutgrowth of staff training and oversight of its activities byan outside consultant, which will entail 156/man/months of workover a period of 2 1/2 years.

- Component D: Support for Private Management Consulting Firms:Interested firms will draw against the credit to obtain thesupport of an outside firm as regards consulting on accountancyand financial organization. Total involvement of 65expert/months was provided for this component.

COSTS

3.08 The cost of the project, estimated by the Bank at $14.2 million,may be broken down by component as follows:

COMPONENT In domestic In foreigncurrency exchange Total

Study of accounting legislation A 0.1 0.3 0.4standardization

Creation and operation of an 2.3 2.2 4.6accountancy training center

Strengthening the activities of 0.3 2.8 3.1RINDRA socialist enterprise

Support to private management 0.2 1.0 1.2consulting firms

Base costs 2.9 f.3 9.2

24

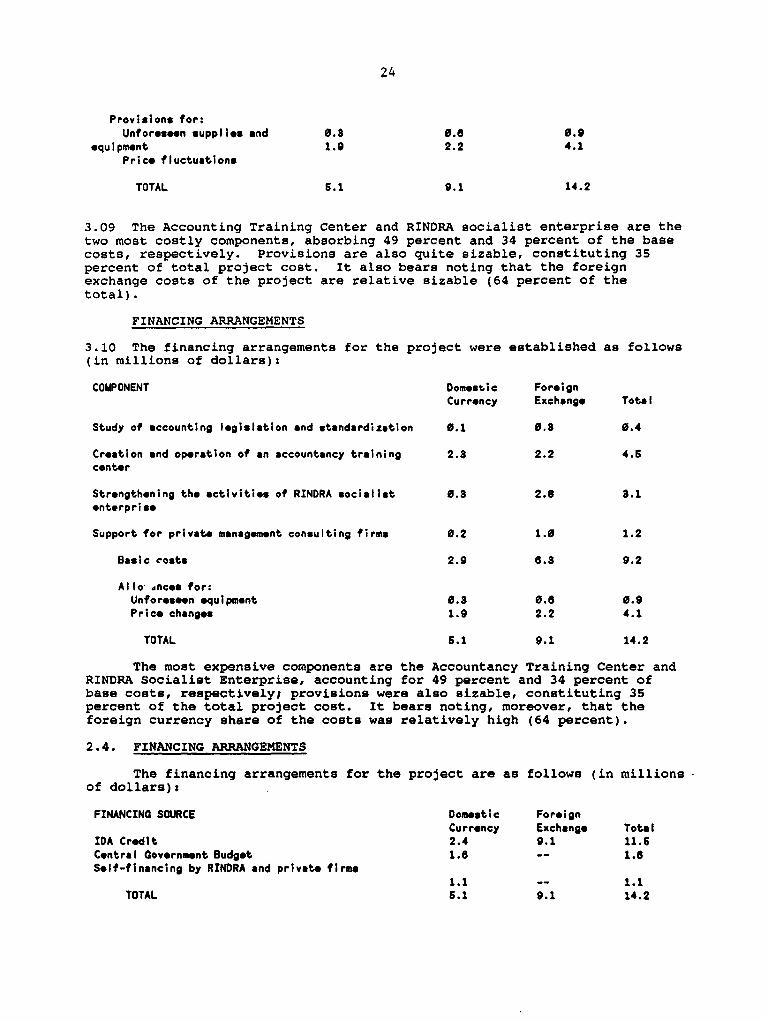

Provisions for:Unforeseen supplies and 0.3 0.6 0.9

equipment 1.9 2.2 4.1Prico fluctuations

TOTAL 5.1 9.1 14.2

3.09 The Accounting Training Center and RINDRA socialist enterprise are thetwo most costly components, absorbing 49 percent and 34 percent of the basecosts, respectively. Provisions are also quite sizable, constituting 35percent of total project cost. It also bears noting that the foreignexchange costs of the project are relative sizable (64 percent of thetotal).

FINANCING ARRANGEMENTS

3.10 The financing arrangements for the project were established as follows(in millions of dollars):

COMPONENT Domestic ForeignCurrency Exchange Total

Study of accounting legislation and standardization 0.1 0.8 0.4

Creation and operation of an accountancy training 2.3 2.2 4.5center

Strengthening the activities of RINDRA socialist 0.8 2.8 3.1enterprise

Support for private management consulting firms 0.2 1.0 1.2

Basic costs 2.9 8.3 9.2

Allo 1nces for:Unforeseon equipment 0.3 0.6 0.9Price changes 1.9 2.2 4.1

TOTAL 6.1 9.1 14.2

The most expensive components are the Accountancy Training Center andRINDRA Socialist Enterprise, accounting for 49 percent and 34 percent ofbase costs, respectively; provisions were also sizable, constituting 35percent of the total project cost. It bears noting, moreover, that theforeign currency share of the costs was relatively high (64 percent).

2.4. FINANCING ARRANGEMENTS

The financing arrangements for the project are as follows (in millionsof dollars):

FrNANCING SOURCE Domestic ForeignCurrency Exchange Total

IDA Credit 2.4 9.1 11.6Central Government Budget 1.6 -- 1.6Self-financing by RINDRA and private firms

1.1 -- 1.1TOTAL 5.1 9.1 14.2

25

3.11 The Bank thus provided financing for 81 percent of the total projectcost. Due to antlcipated contributLons from RINDRA and from private firms,the Central Government's participation is relatively small.

3.12 In a departure from its customary practices, the Bank agreed tofinance costs in local currency representing the equivalent of $2.4 million,corresponding to 95 percent of the costs payable ln local currency of thoconsultants and of the local purchases of CFC as well as 60 percent CFC'spersonnel costs.

3.13 The IDA credit torms were established in accordance with theConvontion of June 11, 1981 as follows

Amount SDR 9,400,000

Service charge 0.75 percent of the amount of the credit drawn andnot yet repaid

Repayment period 50 yearsGrace period 10 years.

3.14 The amount of the credLt may be broken down as follows (amounts inSDRs)

Consultants for legislation 250,000Consultants for CFC 1,630,000Consultants for RINDRA 2,200,000Consultants for prlvate firms 820,000Local personnel--CYC 660,000CFC purchases 900,000Unallocated 2,940,000

TOTAL 9,400,000

3.15 In accordance with Article 3 of the credlt agreement, the borrowerwill on-lend to RINDRA the equivalent of SDR 3 million within the frameworkof a subsidiary loan agreement. This agreement, signed between the PublicTreasury and RINDRA on January 25, 1982, sets the loan terms as follows:

Service charge 12 percent per annumRepayment perlod 10 yearsGrace perlod 3 years

The terms of the subsidiary loan agreement are thus "harsher" than the termsof the maln loant RINDRA wlll not, however, be responsLble for coverlngexchange rliks.

DISBURSEMENT SCHEDULE

3.16 The dLibursement schedule for the IDA credlt established in globalterms by the World Bank are lndlcated in the followLng table (Ln milllons ofdollars):

1982 198 1964 19s 1986 1967 1966

Per fIscal yer 1. 2 2.0 2.8 2.2 2.0 1.5 6.5

Cumulative 1.2 8.2 5.6 7.7 9.7 11.2 11.5

Use of the credit would opan a period of seven years.

26

3.17 Given the increasing need noted in moat enterprisee, particularly thepublic enterprises, for assistance in the areas of organization andmanagement, the Malagasy Government decided to setup up the management unitprovided for when negotiating the accountancy and auditing organization andtraining project within an existing enterprise, in this case RINDRAsociallst enterprlse. The creatLon of a Management Consulting Departmentwithin RINDRA in March 1985 resulted in a further need for technicalassitance, which was to result in an additional assistance contract withthe original Consulting fLrm in March 1985.

3.18 In order to enable RINDRA to extend its activities in the area ofcomputerized auditing and the auditing of banks and insurance companies, onthe one hand, and, on the other hand, to bolster its internal management, asecond assistance contract was signed in April 1985 with a French firm.

3.19 The credit allocated to the Accountancy Training Center, scheduled tobe spread over six years, was fully utilized in three years. It was used toflnanced unforeseen expenditure at the appraisal level (teacher trainingabroad, recourse to consultants for purposes of hirLng technicalassistants). The increase in the value of the dollar via-&-vie the SDR alsoreduced the dollar value of the credit.

3.20 In view of RINDRA's new requirements and those of the AccountancyTraining Center, an adjustment in the credit proved necessary. Thereallocation process, carried out in April 1986, was as follows (amounts InSDRs):

Category of Credit According to Subsidiary Upward Downward AfterCredit Credit Adjustment Adjustment AdjustmentAgreement Agreement

Consultants for 250,000 s6,0O0 200,060legislation

Consultants for CFC 1,680,000 1,8X0,00 ,440,000

Consultants for RINDRA 2,200,000 8,000,600 1,150,000 4,160,000

Consultante for privete 820,060 426,000 895,000f I rmo

Local CFC personnol 880,060 896,000 266,000

CFC procurement P00,0me 900,000

Unallocated 2,940,000 2,140,000 2,090,000 50,000

TOTAL 9,400,000 2,998,000 2,966,000 9,400,000

3.21 The new requirements of RINDRA and the Accountancy TrainLng Centerwere largely financed by drawing on the non-earmarked funds and on the fundsintended for Component D.

3.22 In order to ensure continuity for CFC activities, in 1985 theGovernment found it necessary to prepare a new project. CFC, whoseactivities had extended into the area of management training, assumed a newnames "Institut National des Sciences Comptables et d'Administrationd'Entreprises (National Institute for Accountancy and Business Management](INSCAE). For operational purposes, the INSCAE received a new credit fromthe World Bank (Credit 1661-MAG) in April 1986. This situation complicatesthe appraisal of Component B of Credit 1155-MAG, which concerns CFC only;

27

the World Bank (Credit 1661-MAG) in April 1986. This situation complicatesthe appraisal of Component B of Credit 1155-MAG, which concerns CFC only;the performance of CFC thus cannot be assessed except in light of what hasbeen accomplished by the INSCAE.

Successive Delays in Effective Dates and Closing Dates

3.23 The effective date of the credit, scheduled for October 12, 1981, waspostponed twice (January 12 and April 12, 1982) before finally coming intoforce on May 6, 1982. The Bank's conditions for the credit taking effectwere as follows:

- appointment of a Director of CFC and a Director of RINDRA, madeofficial by decree;

- the draft contract of the Director of RINDRA had to be submittedto him;

- the subsidiary loan agreement needed to be signed.

3.24 The hiring of the Directors-General of CFC and RINDRA, who accordingto plans were to be expatriates, took almost a year, which explains thesuccessive delays in the effective date.

3.25 The closing date for the credit was scheduled to be March 1988. Atthe request of the Government of Madagascar, the Wor'2d Bank agreed to rollthe date back, first to September 30, 1988, subsequently to December 31,1988, and finally to June 30, 1989.

Financial Status of the Credit

3.26 As yet, there has been no financial audit on the use of Credit 1155-MAG. The information provided to us by the Ministry of Finance indicatesthe following status as of March 31, 1989 (amounts in SDRs):

COMPONENT Domestic ForeignCurrency Exchange Total

Study of accounting legislation and standardization 0.1 0.3 0.4

Creation and operation of an accountancy training 2.3 2.2 4.6center

Strengthening the activities of RINDOA socialist 0.3 2.8 3.1enterpris-

Support for private management consulting firms 0.2 1.0 1.2

Basic costs 2.9 6.3 9.2

Allowances for:Unfor-seen *quipment 0.3 0.6 0.9Price changes 1.9 2.2 4.1

TOTAL 6.1 9.1 14.2

3.27 During June 1984, the Bank authorized RINDRA to finance $125,000 inequipment from Category 3. As of March 31, 1989, almost all of the credit(99.6 percent) had been exhausted.

28

4. COMPONENT A: ACCOUNTING LEGISLATION AND STANDARDIZATION

CONTEXT AND OBJECTIVES

4.01 There are few accounting experts in Madagascar, and they are extremelyscarce in enterprises whose accounts are audited; financial information isunreliable and is presented in a different way by each iniividualenterprise. In 1981, when the project began, the overall status of theaccounting profession had scarcely changed from that of 1970, for lack ofany training in accountancy and owing to the fact that the prevailinglegislation set forth no standards for the format or auditing of financialstatements. The only official regulations applicable to financialstatements that were effectively adhered to were those of the TaxDirectorate, which required that companies with a turnover in excess ofFMG 30 million (or over $150,000) submit statements which documented theirtax returns in accordance with a given code of accounts; this accountingcode, however, was limited to providing a breakdown of the accountingheadings to be posted to the books, but did not govern the annual financialstatements themselves.

4.02 The decree of February 7, 1969 had, to be sure, introduced and adaptedthe French code of accounts of 1947 (revised in 1957) to Madagascar, but nodirectives could be enforced. Moreover, the 1867 law on corporationsstipulated only that financial statements had to be submitted toshareholders after review by an auditor, whose qualifications were notspecified. The law does not indicate the proper content of the financialstatements or the extend to which they had to be verified by the auditors,with the result that this auditing process is often rudimentary. The 1925law on limited liability companies is just as lacking in specificity.

4.03 The objectives of the "Accounting Legislation and Standardization"component are thus to:

- enable enterprises to obtain, in a timely manner, reliable andinformative financial statements which allow for effectivecontrol and planning of management;

- facilitate, through the uniform format of accountinginformation, the preparation of sectoral, regional, and nationalstatistics which are of value at the various planning levels;

- develop the accounting profession by creating a demand forindividuals with the skills required to draw up, analyze,interpret and audit the financial statements prepared inaccordance with the lawful professional standards.

AGREED REFORMS

4.04 The new legislative measures envisaged should require that:- organizations functioning as companies maintain books of

accounts, and prepare and publish in due time financialstatements that are consistent with a new and more restrictiveaccounting code;

- these financial statements be audited by authorized independentauditors, who shall certify that they correctly provide afaithful and honest image of the company's financial position,it being understood that this annual auditing requirement shall

29

be applied gradually, beginning with the major companies in thepublic sector;

- the persons authorized to act as auditors have the minimumqualifications required;

- the order of professional accountants and auditors defineaccounting and auditing standards, keep them up to date, proposeamendments to them as necessary, and investigate any violationsthereof.

The preparation of legislation measures should also entail review ofcommercial law provisions (company law, criminal law, taxation, etc.).

IMPLEMENTATION SCHEDULE

4.05 With the help of consultants, the Malagasy Government will carry outthis portion of the project in accordance with the following timetable:

- December 1, 1981: establishment of a committee entrusted withdrafting the proposed legislation on:

- existing laws;- organization of accountancy and auditing;- organization of the accounting profession;- April 30, 1982: submission of the new legislative proposals to

the Government and the Bank;- July 31, 1982: passage of the legislation.

4.06 This component of the project has always been considered to be highpriority. Its contents have an impact on a significant proportion of allthe other components.

IMPLEMENTATION

Hiring of a consulting firm to assist the Government

4.07 In June 1981, the Ministry of Economy and Commerce drew up a shortlist of consulting firms to be approached. At the end of this cycle, inAugust 1982, one firm was ranked first. However, no contract was signedafter the relevant negotiations. At the request of the Order ofAccountants and Authorized Accountants, which sought to be involved in theproject, the procedure was repeated. A new short list of consultants wasthen scheduled to be prepared by November 1982; as earlier, the list wascomposed solely of foreign firms. A request by the Malagasy Government toinclude local firms was submitted to the Bank in July 1983, but was refusedfor the following reasons:

- the call for bids had already been issued in April 1983, andfive of the six firms consulted had already replied;

- the Bank felt that the Order had neither the experience nor thenecessary skills to undertake by itself the study of therelevant legislation and the accounting code, and, as both judgeand defendant, would lack the required independence.

4.08 After reviewing the bids in February 1984, a firm was selected thoughit was not the one ranked first following the first round. The contractwas drawn up in May 1984 and signed in December of the same year. The

30

mission of the selected consulting firm was to cover a 12-month periodbeginning on the date of notification (January 28, 1985).

4.9 Thus, more than three years had passed between the drawing up of thefirst short list and the starting of work. Apart from the fact that theinternational call for bids took almost a year (their were two calls made),the delay in starting up the "Accounting Legislation and Standardization"component may also be explained by the problems of relations between theOrder, the Government, and the Bank. In particular, the Order wasextremely wary of the Government's "statist" options, which, in thesocialist-oriented spirit of the times, had created RINDRA, and of theBank, which was singing the praises of Anglo-Saxon styles of auditing andhad a tendency to resort exclusively to Canadian consultants and teachers.The atmosphere relaxed thanks to the selection of a French firm for thestudy of legislation.

4.10 The consultants contract provided for a workload of 15 man/months(less than initially projected) to deal with the following objectives:

- critical analysis of the situation as regards:- accounting standardization;- accounting legislation;- the teaching of accountancy;- proposals for new legal provisions regarding:- the new code of accounts;- the dissemination and teaching of the new accounting

system.

The contract provided for the involvement of a Malagasy legal specialistfor 2 man/months.

4.11 The consulting firm submitted its reports with their analyses andproposals on accounting legislation, accounting standardization, and theteaching of accountancy in June 1985; the reports setting forth formalrecommendations were submitted on January 15, 1986. The proposals,initially looked upon favorably by the parties concerned, were modifiedconsiderably, with the result that the consultants were unable to submitits final report until March 5, 1987. As of March 31, 1989, the"Accounting Legislation and Standardization" component cost SDR 195,902.