Embed Size (px)

Citation preview

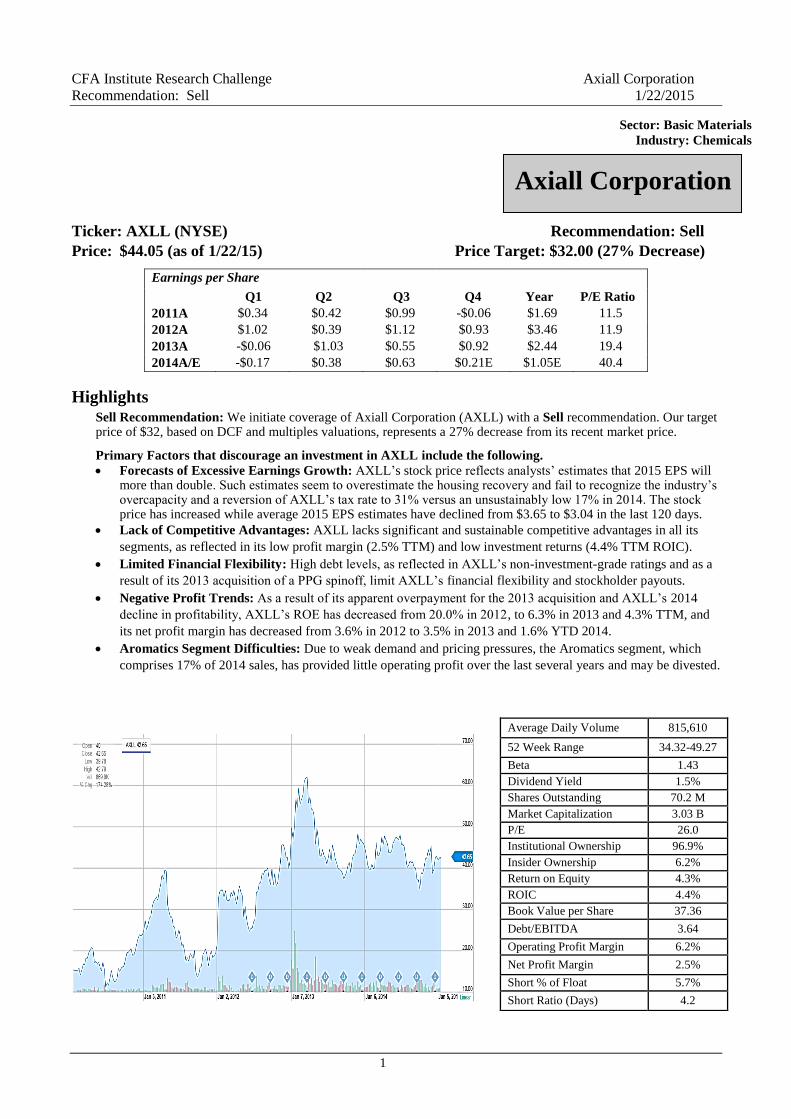

CFA Institute Research Challenge

Southern Classic

Wofford College

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

1

Ticker: AXLL (NYSE) Recommendation: Sell

Price: $44.05 (as of 1/22/15) Price Target: $32.00 (27% Decrease)

Highlights Sell Recommendation: We initiate coverage of Axiall Corporation (AXLL) with a Sell recommendation. Our target price of $32, based on DCF and multiples valuations, represents a 27% decrease from its recent market price.

Primary Factors that discourage an investment in AXLL include the following.

Forecasts of Excessive Earnings Growth: AXLL’s stock price reflects analysts’ estimates that 2015 EPS will more than double. Such estimates seem to overestimate the housing recovery and fail to recognize the industry’s overcapacity and a reversion of AXLL’s tax rate to 31% versus an unsustainably low 17% in 2014. The stock price has increased while average 2015 EPS estimates have declined from $3.65 to $3.04 in the last 120 days.

Lack of Competitive Advantages: AXLL lacks significant and sustainable competitive advantages in all its

segments, as reflected in its low profit margin (2.5% TTM) and low investment returns (4.4% TTM ROIC).

Limited Financial Flexibility: High debt levels, as reflected in AXLL’s non-investment-grade ratings and as a

result of its 2013 acquisition of a PPG spinoff, limit AXLL’s financial flexibility and stockholder payouts.

Negative Profit Trends: As a result of its apparent overpayment for the 2013 acquisition and AXLL’s 2014

decline in profitability, AXLL’s ROE has decreased from 20.0% in 2012, to 6.3% in 2013 and 4.3% TTM, and

its net profit margin has decreased from 3.6% in 2012 to 3.5% in 2013 and 1.6% YTD 2014.

Aromatics Segment Difficulties: Due to weak demand and pricing pressures, the Aromatics segment, which

comprises 17% of 2014 sales, has provided little operating profit over the last several years and may be divested.

Earnings per Share

Q1 Q2 Q3 Q4 Year P/E Ratio

2011A $0.34 $0.42 $0.99 -$0.06 $1.69 11.5

2012A $1.02 $0.39 $1.12 $0.93 $3.46 11.9

2013A -$0.06 $1.03 $0.55 $0.92 $2.44 19.4

2014A/E -$0.17 $0.38 $0.63 $0.21E $1.05E 40.4

Average Daily Volume 815,610

52 Week Range 34.32-49.27

Beta 1.43

Dividend Yield 1.5%

Shares Outstanding 70.2 M

Market Capitalization 3.03 B

P/E 26.0

Institutional Ownership 96.9%

Insider Ownership 6.2%

Return on Equity 4.3%

ROIC 4.4%

Book Value per Share 37.36

Debt/EBITDA 3.64

Operating Profit Margin 6.2%

Net Profit Margin 2.5%

Short % of Float 5.7%

Short Ratio (Days) 4.2

Axiall Corporation

Sector: Basic Materials

Industry: Chemicals

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

2

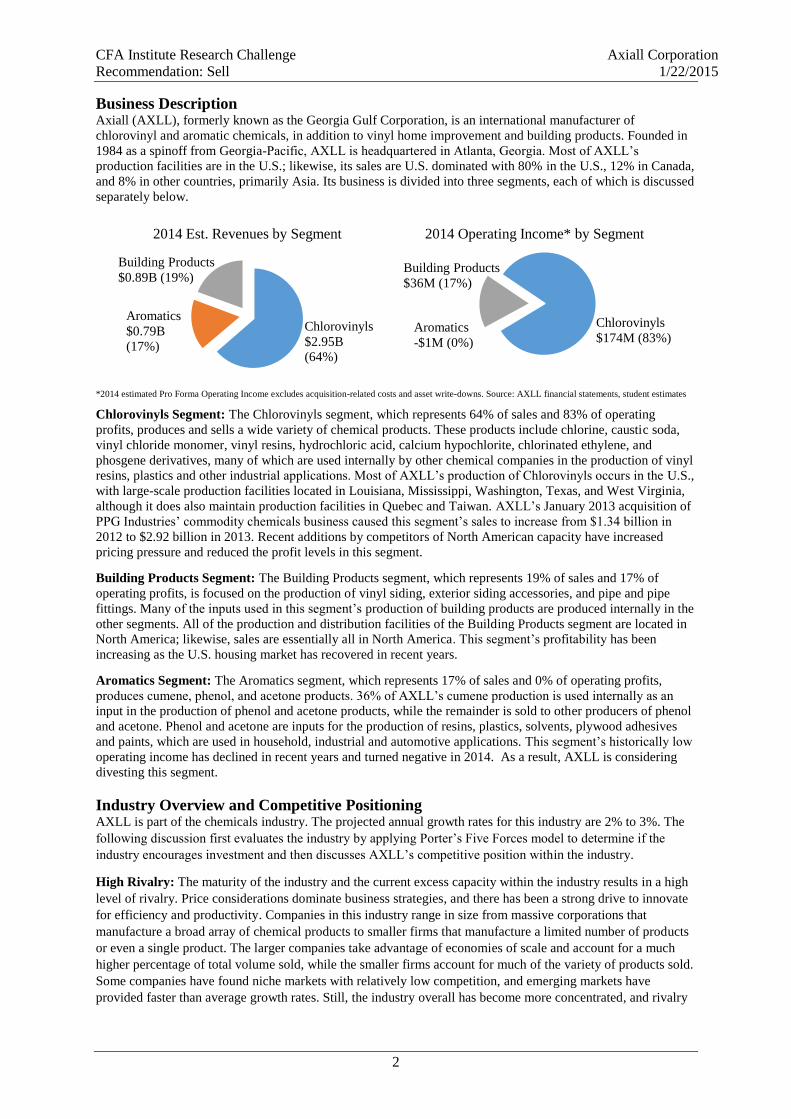

Business Description Axiall (AXLL), formerly known as the Georgia Gulf Corporation, is an international manufacturer of

chlorovinyl and aromatic chemicals, in addition to vinyl home improvement and building products. Founded in

1984 as a spinoff from Georgia-Pacific, AXLL is headquartered in Atlanta, Georgia. Most of AXLL’s

production facilities are in the U.S.; likewise, its sales are U.S. dominated with 80% in the U.S., 12% in Canada,

and 8% in other countries, primarily Asia. Its business is divided into three segments, each of which is discussed

separately below.

*2014 estimated Pro Forma Operating Income excludes acquisition-related costs and asset write-downs. Source: AXLL financial statements, student estimates

Chlorovinyls Segment: The Chlorovinyls segment, which represents 64% of sales and 83% of operating

profits, produces and sells a wide variety of chemical products. These products include chlorine, caustic soda,

vinyl chloride monomer, vinyl resins, hydrochloric acid, calcium hypochlorite, chlorinated ethylene, and

phosgene derivatives, many of which are used internally by other chemical companies in the production of vinyl

resins, plastics and other industrial applications. Most of AXLL’s production of Chlorovinyls occurs in the U.S.,

with large-scale production facilities located in Louisiana, Mississippi, Washington, Texas, and West Virginia,

although it does also maintain production facilities in Quebec and Taiwan. AXLL’s January 2013 acquisition of

PPG Industries’ commodity chemicals business caused this segment’s sales to increase from $1.34 billion in

2012 to $2.92 billion in 2013. Recent additions by competitors of North American capacity have increased

pricing pressure and reduced the profit levels in this segment.

Building Products Segment: The Building Products segment, which represents 19% of sales and 17% of

operating profits, is focused on the production of vinyl siding, exterior siding accessories, and pipe and pipe

fittings. Many of the inputs used in this segment’s production of building products are produced internally in the

other segments. All of the production and distribution facilities of the Building Products segment are located in

North America; likewise, sales are essentially all in North America. This segment’s profitability has been

increasing as the U.S. housing market has recovered in recent years.

Aromatics Segment: The Aromatics segment, which represents 17% of sales and 0% of operating profits,

produces cumene, phenol, and acetone products. 36% of AXLL’s cumene production is used internally as an

input in the production of phenol and acetone products, while the remainder is sold to other producers of phenol

and acetone. Phenol and acetone are inputs for the production of resins, plastics, solvents, plywood adhesives

and paints, which are used in household, industrial and automotive applications. This segment’s historically low

operating income has declined in recent years and turned negative in 2014. As a result, AXLL is considering

divesting this segment.

Industry Overview and Competitive Positioning AXLL is part of the chemicals industry. The projected annual growth rates for this industry are 2% to 3%. The

following discussion first evaluates the industry by applying Porter’s Five Forces model to determine if the

industry encourages investment and then discusses AXLL’s competitive position within the industry.

High Rivalry: The maturity of the industry and the current excess capacity within the industry results in a high

level of rivalry. Price considerations dominate business strategies, and there has been a strong drive to innovate

for efficiency and productivity. Companies in this industry range in size from massive corporations that

manufacture a broad array of chemical products to smaller firms that manufacture a limited number of products

or even a single product. The larger companies take advantage of economies of scale and account for a much

higher percentage of total volume sold, while the smaller firms account for much of the variety of products sold.

Some companies have found niche markets with relatively low competition, and emerging markets have

provided faster than average growth rates. Still, the industry overall has become more concentrated, and rivalry

2014 Est. Revenues by Segment

Chlorovinyls

$2.95B

(64%)

Building Products

$0.89B (19%)

Aromatics

$0.79B

(17%)

2014 Operating Income* by Segment

Building Products

$36M (17%)

Aromatics

-$1M (0%)

Chlorovinyls

$174M (83%)

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

3

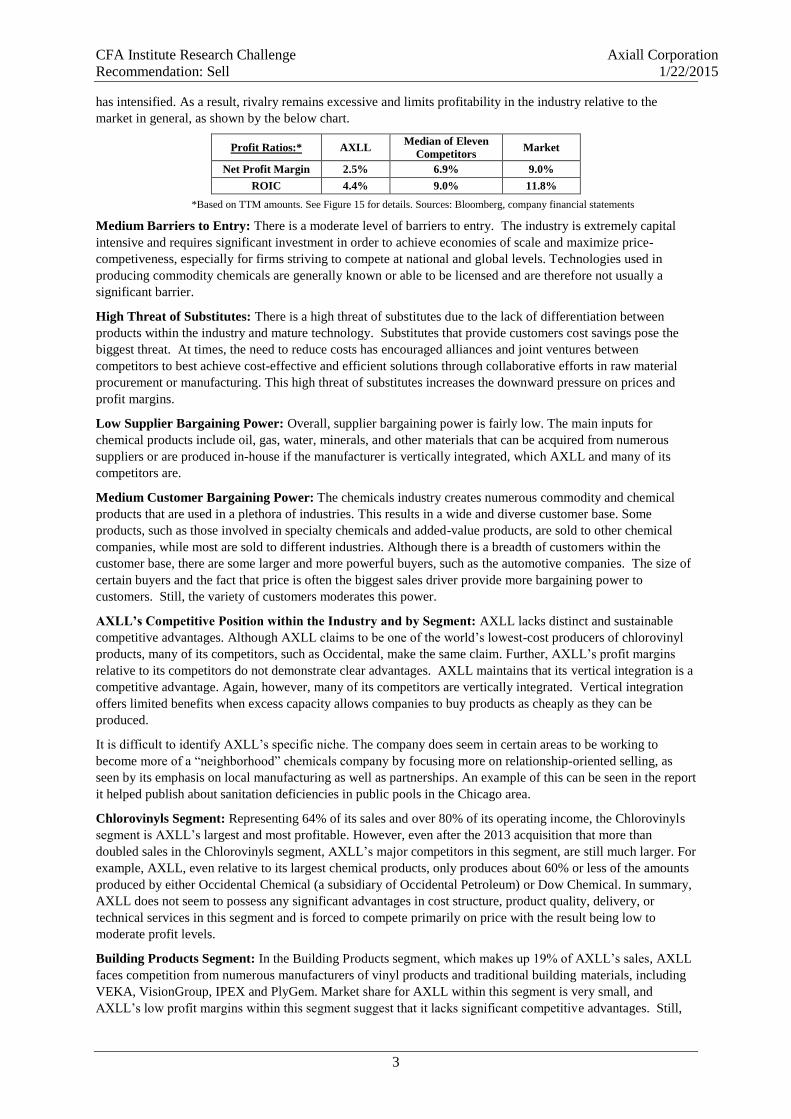

has intensified. As a result, rivalry remains excessive and limits profitability in the industry relative to the

market in general, as shown by the below chart.

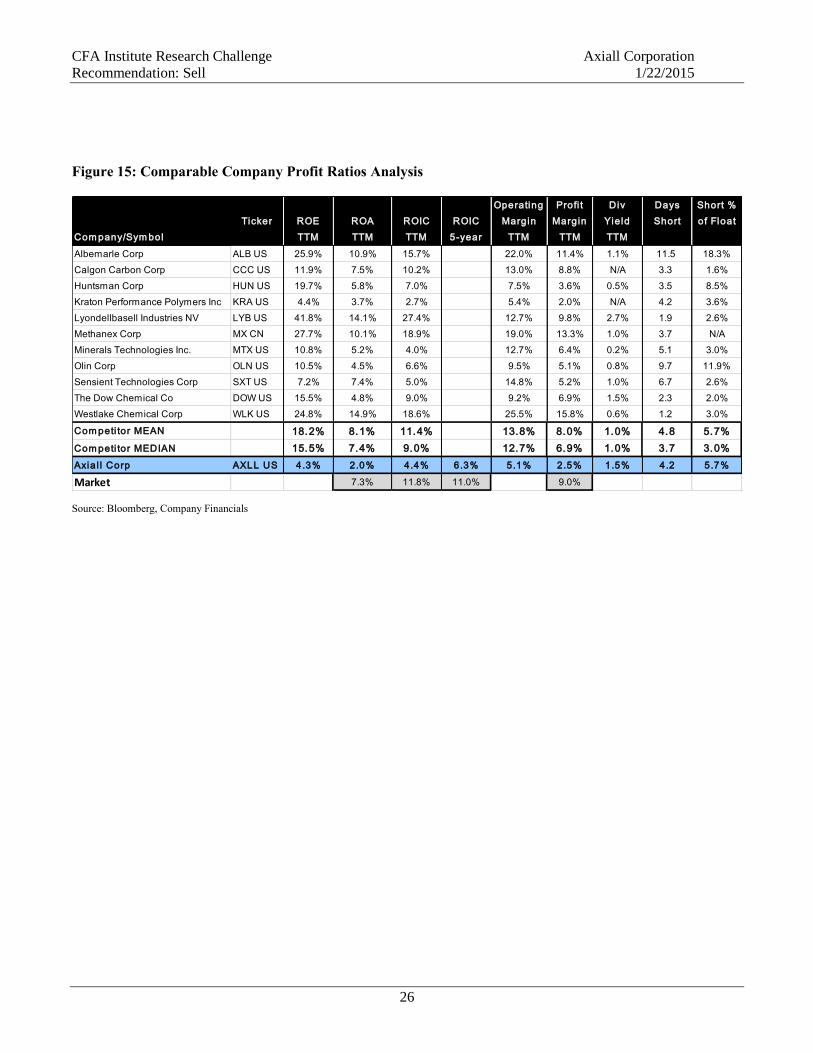

Profit Ratios:* AXLL Median of Eleven

Competitors Market

Net Profit Margin 2.5% 6.9% 9.0%

ROIC 4.4% 9.0% 11.8%

*Based on TTM amounts. See Figure 15 for details. Sources: Bloomberg, company financial statements

Medium Barriers to Entry: There is a moderate level of barriers to entry. The industry is extremely capital

intensive and requires significant investment in order to achieve economies of scale and maximize price-

competiveness, especially for firms striving to compete at national and global levels. Technologies used in

producing commodity chemicals are generally known or able to be licensed and are therefore not usually a

significant barrier.

High Threat of Substitutes: There is a high threat of substitutes due to the lack of differentiation between

products within the industry and mature technology. Substitutes that provide customers cost savings pose the

biggest threat. At times, the need to reduce costs has encouraged alliances and joint ventures between

competitors to best achieve cost-effective and efficient solutions through collaborative efforts in raw material

procurement or manufacturing. This high threat of substitutes increases the downward pressure on prices and

profit margins.

Low Supplier Bargaining Power: Overall, supplier bargaining power is fairly low. The main inputs for

chemical products include oil, gas, water, minerals, and other materials that can be acquired from numerous

suppliers or are produced in-house if the manufacturer is vertically integrated, which AXLL and many of its

competitors are.

Medium Customer Bargaining Power: The chemicals industry creates numerous commodity and chemical

products that are used in a plethora of industries. This results in a wide and diverse customer base. Some

products, such as those involved in specialty chemicals and added-value products, are sold to other chemical

companies, while most are sold to different industries. Although there is a breadth of customers within the

customer base, there are some larger and more powerful buyers, such as the automotive companies. The size of

certain buyers and the fact that price is often the biggest sales driver provide more bargaining power to

customers. Still, the variety of customers moderates this power.

AXLL’s Competitive Position within the Industry and by Segment: AXLL lacks distinct and sustainable

competitive advantages. Although AXLL claims to be one of the world’s lowest-cost producers of chlorovinyl

products, many of its competitors, such as Occidental, make the same claim. Further, AXLL’s profit margins

relative to its competitors do not demonstrate clear advantages. AXLL maintains that its vertical integration is a

competitive advantage. Again, however, many of its competitors are vertically integrated. Vertical integration

offers limited benefits when excess capacity allows companies to buy products as cheaply as they can be

produced.

It is difficult to identify AXLL’s specific niche. The company does seem in certain areas to be working to

become more of a “neighborhood” chemicals company by focusing more on relationship-oriented selling, as

seen by its emphasis on local manufacturing as well as partnerships. An example of this can be seen in the report

it helped publish about sanitation deficiencies in public pools in the Chicago area.

Chlorovinyls Segment: Representing 64% of its sales and over 80% of its operating income, the Chlorovinyls

segment is AXLL’s largest and most profitable. However, even after the 2013 acquisition that more than

doubled sales in the Chlorovinyls segment, AXLL’s major competitors in this segment, are still much larger. For

example, AXLL, even relative to its largest chemical products, only produces about 60% or less of the amounts

produced by either Occidental Chemical (a subsidiary of Occidental Petroleum) or Dow Chemical. In summary,

AXLL does not seem to possess any significant advantages in cost structure, product quality, delivery, or

technical services in this segment and is forced to compete primarily on price with the result being low to

moderate profit levels.

Building Products Segment: In the Building Products segment, which makes up 19% of AXLL’s sales, AXLL

faces competition from numerous manufacturers of vinyl products and traditional building materials, including

VEKA, VisionGroup, IPEX and PlyGem. Market share for AXLL within this segment is very small, and

AXLL’s low profit margins within this segment suggest that it lacks significant competitive advantages. Still,

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

4

AXLL has been attempting to carve out a niche by developing environmentally friendly and sustainable building

products that differentiate AXLL from the competition. For example, this week at the 2015 International

Builders’ Show, AXLL introduced durable and low-maintenance siding products with the look and feel of

wood. However, we anticipate that if demand grows for such products, numerous competitors will develop

comparable competing products.

Aromatics Segment: In the Aromatics segment, which represents 17% of sales, AXLL’s historically low

operating income has declined in recent years and turned negative in 2014, as a result of slack export demand,

increased international industry capacity, and margin pressure caused by rising benzene and propylene prices.

As a result, AXLL is considering divesting this segment. Such ongoing low profit levels and the expressed

desire to divest the segment demonstrate AXLL’s lack of sustainable competitive advantages in this segment.

Overall Summary: The maturity of the industry and the high levels of rivalry and potential substitutes

discourage investment in the chemicals industry. The returns on investment have been historically low for

AXLL and the industry in general. These returns suggest that this industry does not facilitate sustainable

competitive advantages for firms. Along this line, AXLL lacks sustainable competitive advantages in all

segments. There is little reason for customers to prefer AXLL’s products over those of its competitors, unless

AXLL offers lower prices. The present excess capacity within the industry only exasperates these issues. In the

Chlorovinyls segment, significant new capacity has been added in North America by competitors in anticipation

of growth in demand that has not yet materialized. The U.S. housing bubble created excess capacity in the

building products industry; although this excess still lingers, it has lessened as the housing market has

recovered. Finally, AXLL’s U.S. facilities are at a disadvantage relative to transportation costs for the largest

growth opportunities in Pacific Asia, particularly India and China, and the U.S. dollar’s recent strength reduces

the international competitiveness of AXLL’s U.S. facilities.

Investment Summary We are initiating coverage on AXLL with a Sell recommendation and a target price of $32. Various

qualitative and quantitative factors motivate our Sell recommendation.

No Sustainable Competitive Advantages: AXLL lacks sustainable competitive advantages in all of its

segments. Any advantages noted by AXLL, such as vertical integration, are also possessed by various

competitors. AXLL’s below-industry profit levels reflect its lack of competitive advantages.

Current Excess Capacity in the Industry: There have been recent capacity additions by competitors, such as

Dow Chemical and Occidental Chemical, that have caused current industry capacity to be excessive and

margins to decline significantly in 2014. In the Outlook section of its September 2014 10Q (page 56), AXLL

suggests that it may take several years for demand growth to offset this recently added capacity. Economies of

scale in this industry require massive plants and plant construction can take multiple years. Supply and demand

imbalances can easily result when new plants open and forecasted demand growth has not materialized. Excess

industry capacity in both the Chlorovinyls and Aromatics segments is currently suppressing AXLL’s profits.

Low Growth in Industry: Demand for many of AXLL’s products depends significantly on the construction

industry. However, in part due to a lack of income growth, the housing market has plateaued at a new normal,

despite very low mortgage rates. In addition, the prior lax lending standards created an artificially high level of

housing starts that will not be reached in the foreseeable future. Due to higher prior levels of construction, there

is excess capacity in many areas related to housing. We are forecasting that AXLL’s recent low single-digit

levels of organic revenue growth will continue for the foreseeable future.

Overpayment for Eagle Spinco Acquisition: AXLL’s capital structure is burdened by its overpayment for the

January 2013 acquisition of Eagle Spinco, a spinoff of PPG Industries. This acquisition left AXLL with little

additional debt capacity, and its doubling of AXLL’s common shares outstanding has diluted subsequent EPS

amounts. Profit margins of the acquired operations significantly declined in 2014, despite the synergies claimed

by AXLL from the acquisition. As noted in the Financial Analysis section, the price paid for the acquisition is

excessive relative to recent incremental profit levels.

Excessive Earnings Growth Reflected in Current Stock Price: Our target price reflects strong operating

earnings growth of 89% in 2015. Such growth is in the lower quartile of a broad range of analysts’ forecasts.

AXLL’s current stock price, based on our analysis, anticipates that EPS will more than double in 2015 in

comparison to 2014 pro forma levels, despite no significant EPS growth in recent quarters. We believe that the

amount of EPS growth built into the stock price is excessive and may also fail to recognize AXLL’s artificially

low tax rate in 2014.

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

5

$10 $20 $30 $40 $50 $60

DCF

EV/EBITDA

P/E

Value Per Share

Valu

ati

on

Met

hod

Valuation Football Field

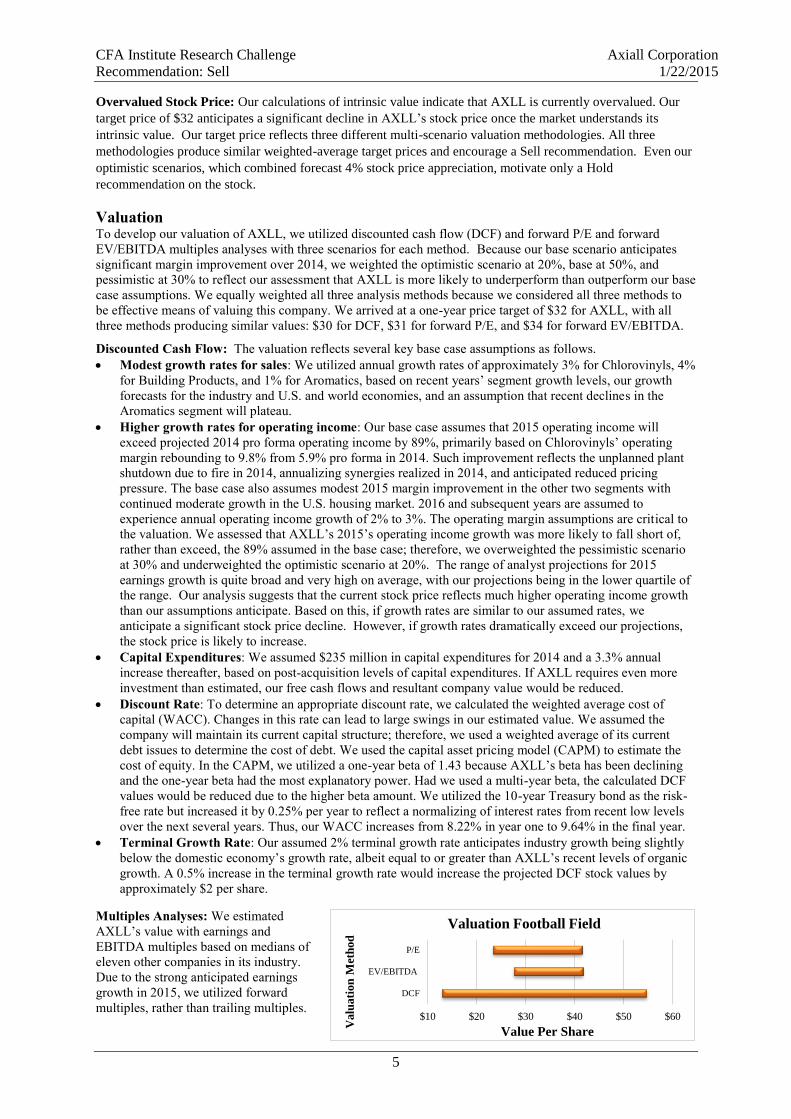

Overvalued Stock Price: Our calculations of intrinsic value indicate that AXLL is currently overvalued. Our

target price of $32 anticipates a significant decline in AXLL’s stock price once the market understands its

intrinsic value. Our target price reflects three different multi-scenario valuation methodologies. All three

methodologies produce similar weighted-average target prices and encourage a Sell recommendation. Even our

optimistic scenarios, which combined forecast 4% stock price appreciation, motivate only a Hold

recommendation on the stock.

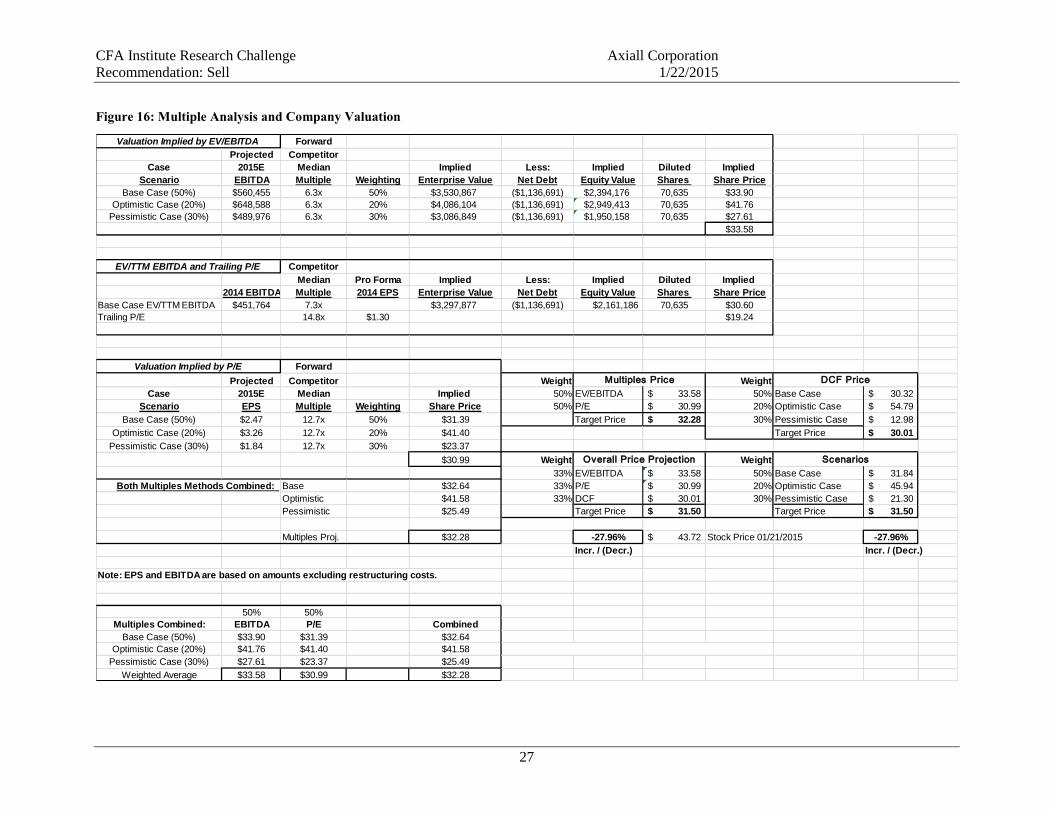

Valuation To develop our valuation of AXLL, we utilized discounted cash flow (DCF) and forward P/E and forward

EV/EBITDA multiples analyses with three scenarios for each method. Because our base scenario anticipates

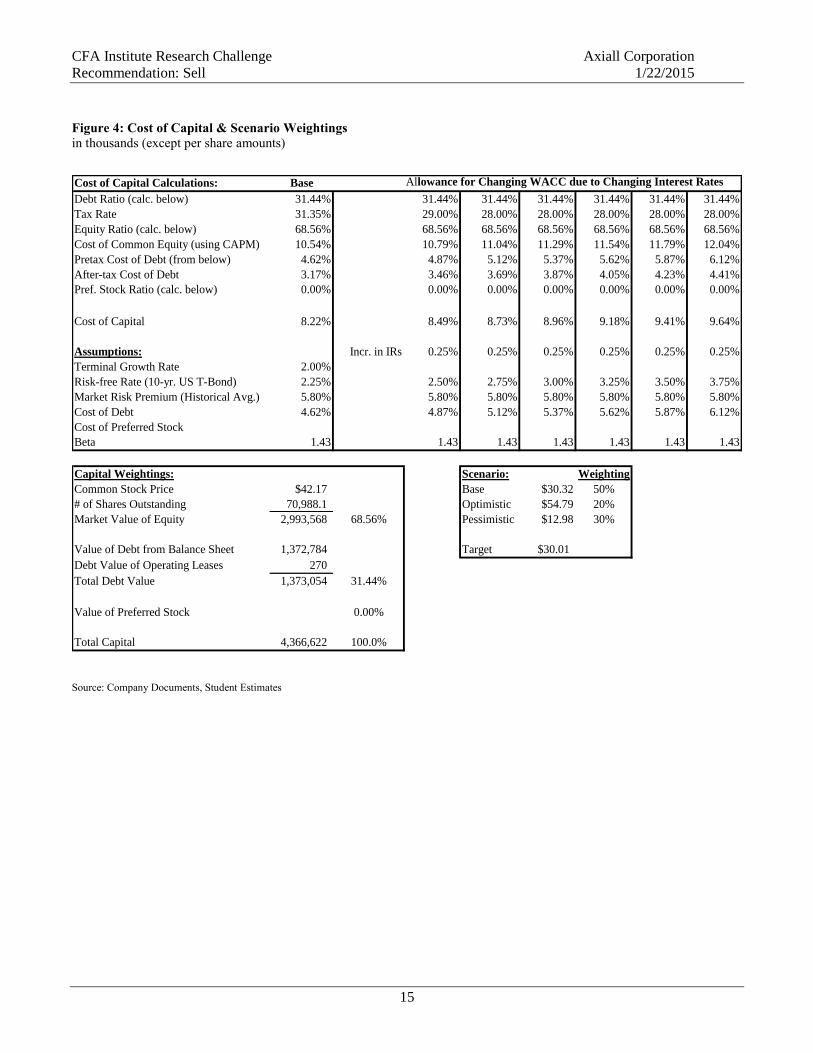

significant margin improvement over 2014, we weighted the optimistic scenario at 20%, base at 50%, and

pessimistic at 30% to reflect our assessment that AXLL is more likely to underperform than outperform our base

case assumptions. We equally weighted all three analysis methods because we considered all three methods to

be effective means of valuing this company. We arrived at a one-year price target of $32 for AXLL, with all

three methods producing similar values: $30 for DCF, $31 for forward P/E, and $34 for forward EV/EBITDA.

Discounted Cash Flow: The valuation reflects several key base case assumptions as follows.

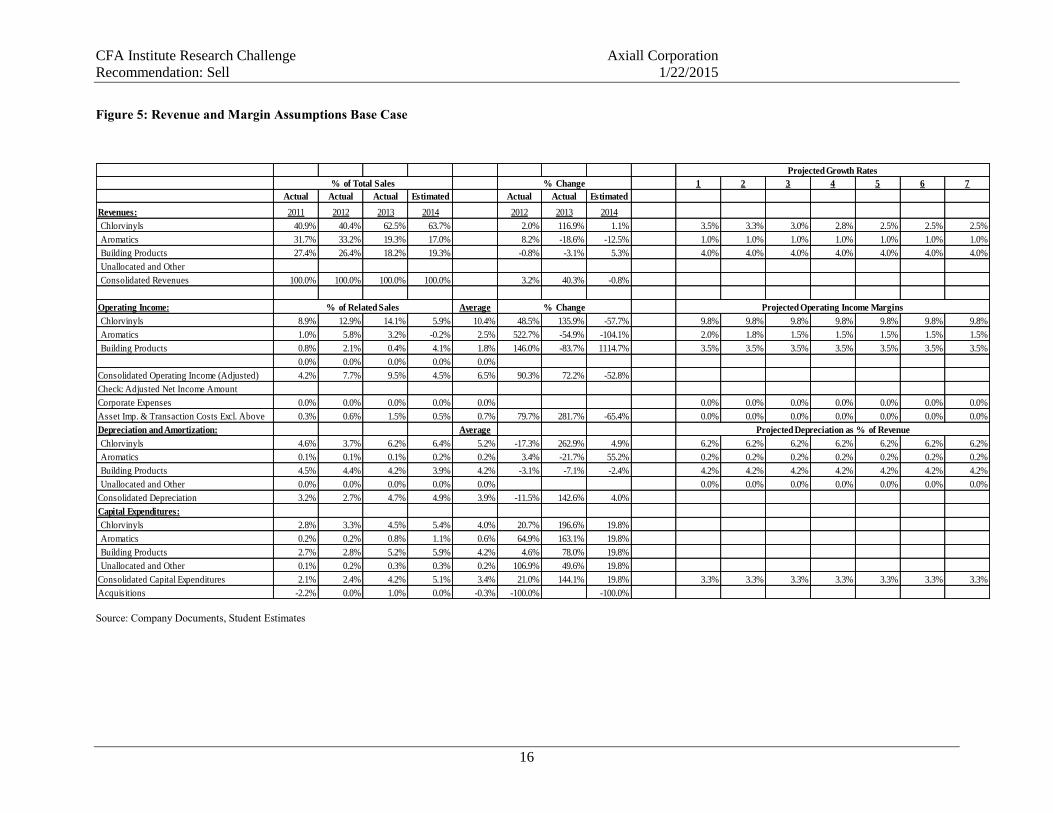

Modest growth rates for sales: We utilized annual growth rates of approximately 3% for Chlorovinyls, 4%

for Building Products, and 1% for Aromatics, based on recent years’ segment growth levels, our growth

forecasts for the industry and U.S. and world economies, and an assumption that recent declines in the

Aromatics segment will plateau.

Higher growth rates for operating income: Our base case assumes that 2015 operating income will

exceed projected 2014 pro forma operating income by 89%, primarily based on Chlorovinyls’ operating

margin rebounding to 9.8% from 5.9% pro forma in 2014. Such improvement reflects the unplanned plant

shutdown due to fire in 2014, annualizing synergies realized in 2014, and anticipated reduced pricing

pressure. The base case also assumes modest 2015 margin improvement in the other two segments with

continued moderate growth in the U.S. housing market. 2016 and subsequent years are assumed to

experience annual operating income growth of 2% to 3%. The operating margin assumptions are critical to

the valuation. We assessed that AXLL’s 2015’s operating income growth was more likely to fall short of,

rather than exceed, the 89% assumed in the base case; therefore, we overweighted the pessimistic scenario

at 30% and underweighted the optimistic scenario at 20%. The range of analyst projections for 2015

earnings growth is quite broad and very high on average, with our projections being in the lower quartile of

the range. Our analysis suggests that the current stock price reflects much higher operating income growth

than our assumptions anticipate. Based on this, if growth rates are similar to our assumed rates, we

anticipate a significant stock price decline. However, if growth rates dramatically exceed our projections,

the stock price is likely to increase.

Capital Expenditures: We assumed $235 million in capital expenditures for 2014 and a 3.3% annual

increase thereafter, based on post-acquisition levels of capital expenditures. If AXLL requires even more

investment than estimated, our free cash flows and resultant company value would be reduced.

Discount Rate: To determine an appropriate discount rate, we calculated the weighted average cost of

capital (WACC). Changes in this rate can lead to large swings in our estimated value. We assumed the

company will maintain its current capital structure; therefore, we used a weighted average of its current

debt issues to determine the cost of debt. We used the capital asset pricing model (CAPM) to estimate the

cost of equity. In the CAPM, we utilized a one-year beta of 1.43 because AXLL’s beta has been declining

and the one-year beta had the most explanatory power. Had we used a multi-year beta, the calculated DCF

values would be reduced due to the higher beta amount. We utilized the 10-year Treasury bond as the risk-

free rate but increased it by 0.25% per year to reflect a normalizing of interest rates from recent low levels

over the next several years. Thus, our WACC increases from 8.22% in year one to 9.64% in the final year.

Terminal Growth Rate: Our assumed 2% terminal growth rate anticipates industry growth being slightly

below the domestic economy’s growth rate, albeit equal to or greater than AXLL’s recent levels of organic

growth. A 0.5% increase in the terminal growth rate would increase the projected DCF stock values by

approximately $2 per share.

Multiples Analyses: We estimated

AXLL’s value with earnings and

EBITDA multiples based on medians of

eleven other companies in its industry.

Due to the strong anticipated earnings

growth in 2015, we utilized forward

multiples, rather than trailing multiples.

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

6

We also calculated values based on trailing multiples, and these supported our overall Sell recommendation

since the values were well below our $32 price target. Our revenue growth and operating income growth

assumptions were the same as those noted above in the DCF section.

We utilized a median forward EBITDA multiple of 6.3x, which was somewhat below the trailing EBITDA

median multiple of 7.3x. We used a median forward P/E multiple of 12.7x, which was somewhat below the

trailing P/E median multiple of 14.8x. Because AXLL lacks any significant sustainable competitive advantages

relative to its competitors, we determined that multiples above the medians could not be justified. We also

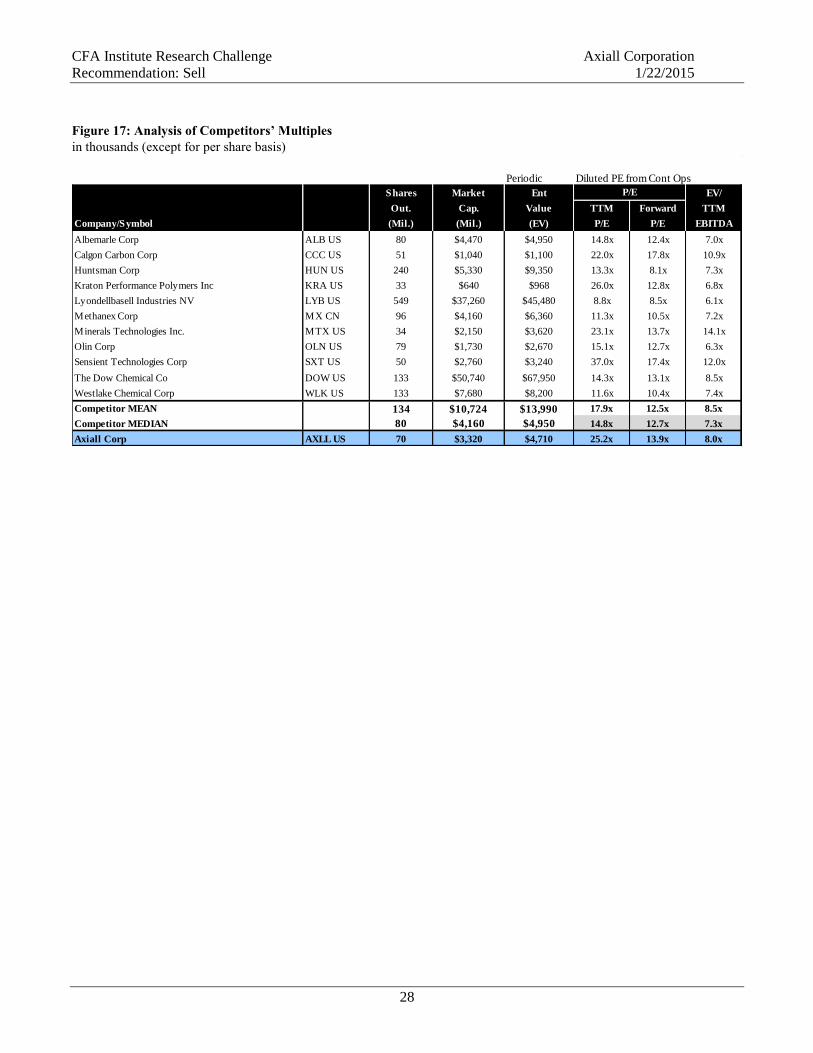

utilized the medians because we could identify no direct competitor with similar market shares and exposures to

AXLL’s three segments. Please refer to Figure 16 for details of the multiples calculations and Figure 17 for the

competitors’ multiples table.

Financial Analysis Prior to analyzing the financial results and financial position of AXLL, we discuss its January 2013 acquisition

of Eagle Spinco, since this acquisition significantly impacts the financial analysis.

Acquisition of Eagle Spinco: On January 28, 2013, Georgia Gulf Corporation acquired substantially all of the

assets and liabilities of Eagle Spinco, a spinoff of PPG Industries’ businesses engaged in the production of

chlorine caustic, soda, and related chemicals. The combined company was renamed Axiall Corporation and

immediately became the third-largest chlor-alkali producer and second-largest vinyl chloride monomer producer

in North America. The acquisition purchase price was approximately $2.8 billion, which was financed through

the assumption of $967 million of debt and the issuance of 35.2 million shares of common stock valued at

approximately $1.8 billion. As a result of the acquisition, AXLL’s shares outstanding essentially doubled to 70

million, while its revenues increased by approximately 40%, virtually all in the Chlorovinyls segment.

In 2012 filings, management anticipated up to $125 million of one-time costs related to the acquisition, of which

$71 million and $25 million were recognized in 2013 and September 2014 YTD, respectively. In the 2012

filings, management predicted $115 million of total annual synergies resulting from the acquisition. In February,

2014, management increased its synergy expectation to $140 million. To date, AXLL has reported $85 million

of realized synergies in 2013 and an additional $70 million in 2014. Management has provided few details of the

realized synergies beyond three categories of synergies: procurement and logistics; operating rate; and general

and administrative reductions. Despite these asserted synergies, the Chlorovinyls segment’s operating income,

which increased from its pre-acquisition level of $174 million in 2012 to $410 million in 2013, is projected to

revert to approximately $174 million in 2014. This level of profits suggests that the Chlorovinyl’s operating

income would be minimal, at less than 1% of sales, without these synergies. Large additional North American

competitor facilities have recently come online and resulted in excess industry capacity, increased price

competition, and significant declines in profit margins.

The primary driver behind the acquisition was the assumption that AXLL would benefit substantially from the

resulting large-scale and consequently low-cost production capabilities, strong export potential, and an

integrated product offering that would leave AXLL positioned to greatly benefit from a housing market

comeback. At the time of the acquisition, AXLL either was unaware of the large competitive plants under

construction or assumed that demand growth would quickly absorb the increased supply. In retrospect, the 2014

declines in the Chlorovinyls segment’s margins indicate that the purchase price paid for Eagle Spinco was

excessive. $444 million of incremental EBITDA is needed justify a $2.8 billion purchase price using a 6.3

forward EBITDA multiple, based on the current median of competitor forward EBITDA multiples. The total of

55%, or $105 million, of the Chlorovinyls segment’s 2014 estimated pro forma operating profits plus $135

million of incremental depreciation and amortization suggests that only $240 million EBITDA (or 54% of the

needed amount) is attributable to Eagle Spinco. Our base case projections for strong growth in 2015 operating

profits still leave us well short of the EBITDA required (67% of the needed amount) to justify the acquisition

price, and even our optimistic case only provides 76% of the needed amount.

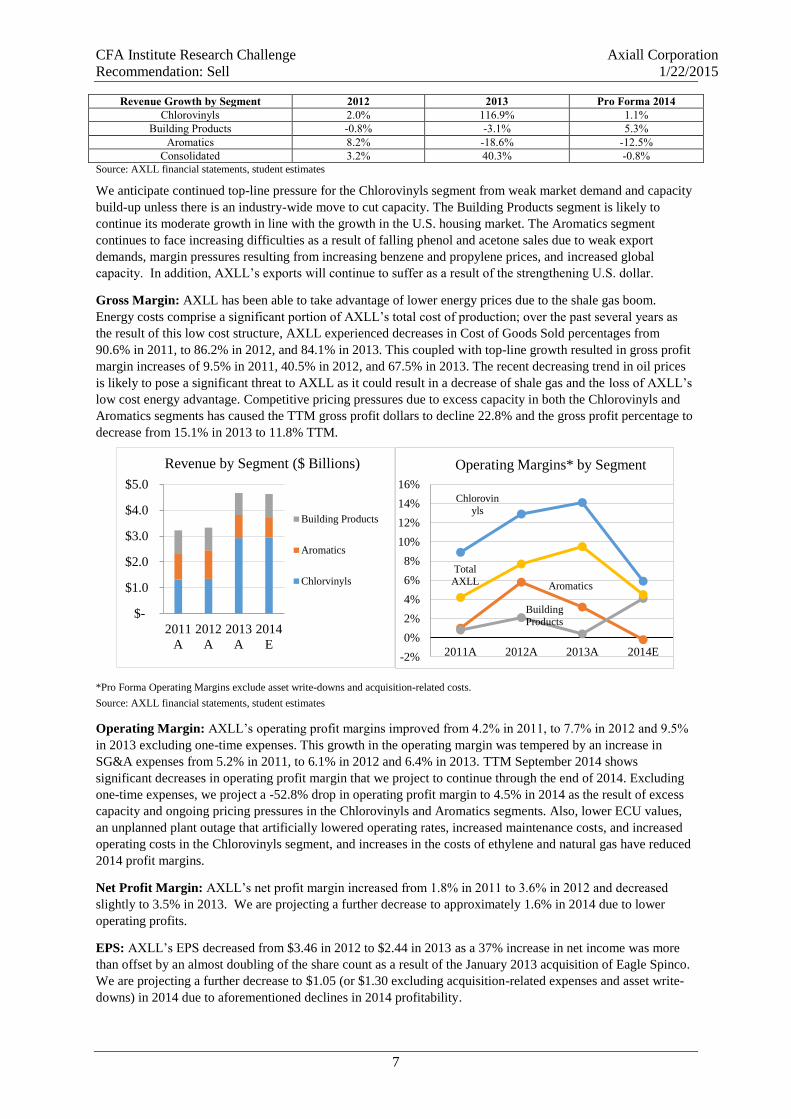

Revenue: AXLL experienced a 40.3% increase in revenue from 2012 to 2013 as a result of the January 2013

acquisition of the PPG spinoff, Eagle Spinco, which roughly doubled the Chlorovinyls segment. As noted in the

chart below, AXLL has experienced low levels of organic growth throughout the last several years. In 2014,

AXLL has experienced low growth in the Chlorovinyls segment due primarily to substantially lower ECU

values driven by recent industry capacity increases and low market demand for caustic. The Building Products

segment experienced moderate growth in both Canadian and U.S. markets, as the U.S. housing market

continued a gradual rebound.

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

7

Revenue Growth by Segment 2012 2013 Pro Forma 2014

Chlorovinyls 2.0% 116.9% 1.1%

Building Products -0.8% -3.1% 5.3%

Aromatics 8.2% -18.6% -12.5%

Consolidated 3.2% 40.3% -0.8%

Source: AXLL financial statements, student estimates

We anticipate continued top-line pressure for the Chlorovinyls segment from weak market demand and capacity

build-up unless there is an industry-wide move to cut capacity. The Building Products segment is likely to

continue its moderate growth in line with the growth in the U.S. housing market. The Aromatics segment

continues to face increasing difficulties as a result of falling phenol and acetone sales due to weak export

demands, margin pressures resulting from increasing benzene and propylene prices, and increased global

capacity. In addition, AXLL’s exports will continue to suffer as a result of the strengthening U.S. dollar.

Gross Margin: AXLL has been able to take advantage of lower energy prices due to the shale gas boom.

Energy costs comprise a significant portion of AXLL’s total cost of production; over the past several years as

the result of this low cost structure, AXLL experienced decreases in Cost of Goods Sold percentages from

90.6% in 2011, to 86.2% in 2012, and 84.1% in 2013. This coupled with top-line growth resulted in gross profit

margin increases of 9.5% in 2011, 40.5% in 2012, and 67.5% in 2013. The recent decreasing trend in oil prices

is likely to pose a significant threat to AXLL as it could result in a decrease of shale gas and the loss of AXLL’s

low cost energy advantage. Competitive pricing pressures due to excess capacity in both the Chlorovinyls and

Aromatics segments has caused the TTM gross profit dollars to decline 22.8% and the gross profit percentage to

decrease from 15.1% in 2013 to 11.8% TTM.

*Pro Forma Operating Margins exclude asset write-downs and acquisition-related costs.

Source: AXLL financial statements, student estimates

Operating Margin: AXLL’s operating profit margins improved from 4.2% in 2011, to 7.7% in 2012 and 9.5%

in 2013 excluding one-time expenses. This growth in the operating margin was tempered by an increase in

SG&A expenses from 5.2% in 2011, to 6.1% in 2012 and 6.4% in 2013. TTM September 2014 shows

significant decreases in operating profit margin that we project to continue through the end of 2014. Excluding

one-time expenses, we project a -52.8% drop in operating profit margin to 4.5% in 2014 as the result of excess

capacity and ongoing pricing pressures in the Chlorovinyls and Aromatics segments. Also, lower ECU values,

an unplanned plant outage that artificially lowered operating rates, increased maintenance costs, and increased

operating costs in the Chlorovinyls segment, and increases in the costs of ethylene and natural gas have reduced

2014 profit margins.

Net Profit Margin: AXLL’s net profit margin increased from 1.8% in 2011 to 3.6% in 2012 and decreased

slightly to 3.5% in 2013. We are projecting a further decrease to approximately 1.6% in 2014 due to lower

operating profits.

EPS: AXLL’s EPS decreased from $3.46 in 2012 to $2.44 in 2013 as a 37% increase in net income was more

than offset by an almost doubling of the share count as a result of the January 2013 acquisition of Eagle Spinco.

We are projecting a further decrease to $1.05 (or $1.30 excluding acquisition-related expenses and asset write-

downs) in 2014 due to aforementioned declines in 2014 profitability.

$-

$1.0

$2.0

$3.0

$4.0

$5.0

2011

A

2012

A

2013

A

2014

E

Revenue by Segment ($ Billions)

Building Products

Aromatics

Chlorvinyls

Chlorovin

yls

Aromatics

Building

Products

Total

AXLL

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2011A 2012A 2013A 2014E

Operating Margins* by Segment

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

8

Tax: In 2012 and 2013, AXLL’s income tax rate averaged 31%. In 2014, one-time accrual adjustments,

including the favorable impacts of changes in uncertain tax positions and of the expiration of statutory time

periods, have resulted in an unsustainably low book tax rate of 17% YTD. We forecast that AXLL’s book tax

rate will revert to 31% in 2015 and subsequently, which will make forecasted growth in EPS more difficult to

achieve. Due to minimal remaining U.S. tax loss carryforwards, we anticipate that future book taxes will

approximate cash taxes.

Cash Flow: Over the past several years, AXLL’s free cash flow and net income have been comparable.

Excluding acquisition-related items, AXLL’s capital expenditures have only slightly exceeded its depreciation.

Also, AXLL’s moderate levels of organic growth have required little incremental net working capital, due to

successful management of inventory and receivables at levels below industry averages.

Balance Sheet and Financing: As of September 2014, AXLL has approximately $1.4 billion in long-term debt

and capitalized lease financings, the bulk of which matures in 2021 and 2023. Moody’s has rated AXLL’s debt

as non-investment grade, with current Moody’s ratings of Ba3 and Ba1, depending on the debt. AXLL’s TIE

ratio of 3.0 and its current non-investment-grade ratings illustrate that AXLL has limited additional debt

capacity. Still, per a recent second amendment and restatement, it was able to increase its asset-based revolving

credit agreement used to fund working capital and operating activities from $500 million to $600 million.

Summary and Management Evaluation: Key conclusions from this financial analysis include the following:

1. The purchase price for Eagle Spinco appears excessive based on recent operating profit results.

2. AXLL’s overall organic growth has been minimal in recent years.

3. Increased costs and pricing pressure due to excess industry capacity have significantly reduced the 2014

profit levels of the Chlorovinyls segment. These factors have offset any reported acquisition synergies

achieved.

4. The Building Products segment has experienced moderate growth and increasing, albeit somewhat low,

operating profit margins. This should continue as the U.S. housing industry experiences moderate growth.

5. Due to weak demand and pricing pressures, the Aromatics segment, which comprises 17% of 2014 sales,

has provided little operating profit contribution to AXLL over the last several years. This may only worsen

going forward as the segment has been shrinking.

6. Anticipated reversion in AXLL’s income tax rate to 31% versus 17% 2014 YTD will reduce growth in EPS.

7. Current debt levels limit AXLL’s financial flexibility going forward.

8. As a result of the 2013 acquisition and the 2014 decline in profitability, AXLL’s investment returns have

declined: ROE from 20.0% in 2012, to 6.3% in 2013 and 4.3% TTM; ROA from 6.7% in 2012, to 2.8% in

2013 and 2.0% TTM; and ROIC from 15.4% in 2012, to 6.5% in 2013 and 4.4% TTM.

Other Considerations Short Positions: AXLL currently has high short positions of 4.2 days and 5.7% of float. 2015 EPS forecasts

have declined and short positions have been steadily rising since the third quarter of 2014, which suggests that

investors are beginning to question the optimistic EPS forecasts upon which AXLL’s current stock price is

based.

Share Repurchases: AXLL does not repurchase shares, nor does it have any plans to do so in the future.

AXLL’s current debt levels will make it difficult for AXLL to engage in significant share repurchases.

Dividends: AXLL’s dividend yield of 1.5% is below average when compared to the market. However, AXLL’s

payout ratio of 38% suggests that its dividend is sustainable. AXLL doubled its quarterly cash dividend in 2013

from $0.08 per share to $0.16 per share. There was no change in the dividend amount in 2014.

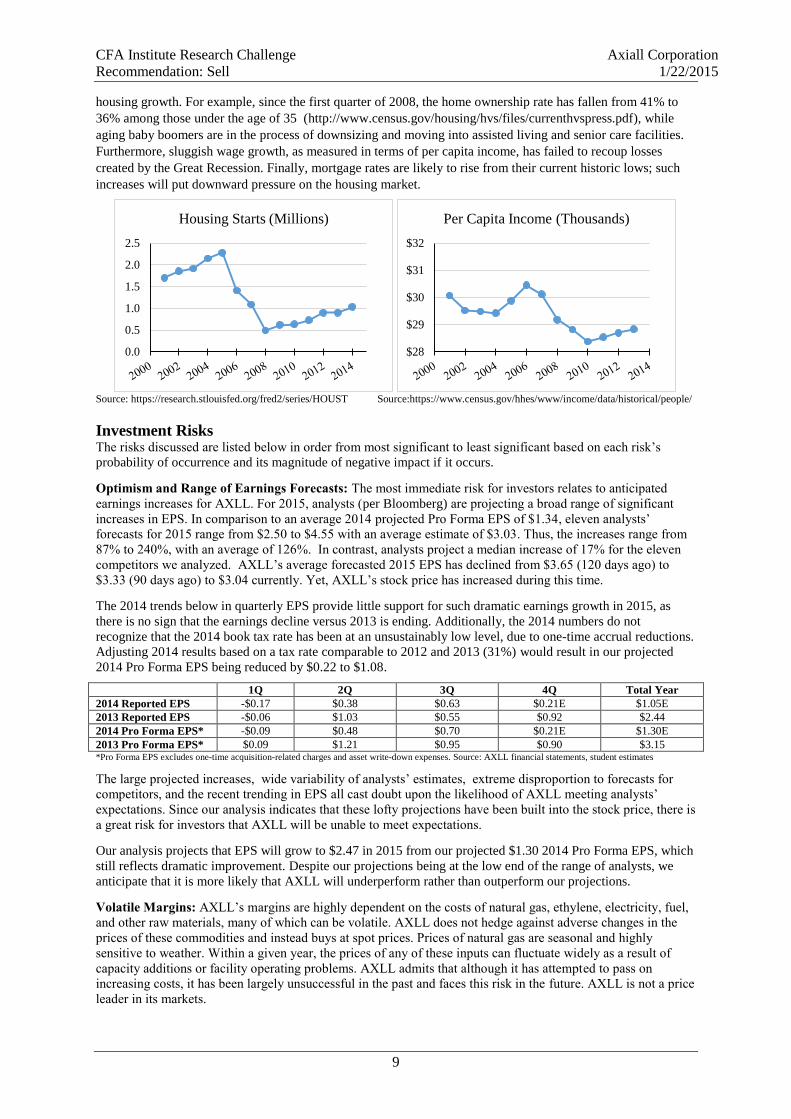

Housing Market Trends: Much of AXLL’s sales and profits are related to the U.S. housing market, either

indirectly in the case of vinyls, resins, paints, and adhesives produced in the Chlorovinyls and Aromatics

segment or directly through its Building Products segment. The burst of the housing bubble caused annual U.S.

housing starts to fall from over 2.2 million in 2005 to 0.5 million in 2008. Subsequently, annual housing starts

have recovered but appear to be plateauing at much lower levels than the bubble amounts. Implicit in many

analysts’ projections for strong earnings growth for AXLL seems to be an anticipated strong rebound in the

housing market to pre-recession levels. In contrast, our forecasts anticipate more tepid growth in housing. We

view recent U.S. housing construction numbers as a new normal that limits AXLL’s growth and profit potential.

This new normal recognizes that the bubble levels were artificially created by lax lending standards and other

factors not likely to be repeated. Current demographic trends and slow wage growth limit the potential for

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

9

housing growth. For example, since the first quarter of 2008, the home ownership rate has fallen from 41% to

36% among those under the age of 35 (http://www.census.gov/housing/hvs/files/currenthvspress.pdf), while

aging baby boomers are in the process of downsizing and moving into assisted living and senior care facilities.

Furthermore, sluggish wage growth, as measured in terms of per capita income, has failed to recoup losses

created by the Great Recession. Finally, mortgage rates are likely to rise from their current historic lows; such

increases will put downward pressure on the housing market.

Source: https://research.stlouisfed.org/fred2/series/HOUST Source:https://www.census.gov/hhes/www/income/data/historical/people/

Investment Risks The risks discussed are listed below in order from most significant to least significant based on each risk’s

probability of occurrence and its magnitude of negative impact if it occurs.

Optimism and Range of Earnings Forecasts: The most immediate risk for investors relates to anticipated

earnings increases for AXLL. For 2015, analysts (per Bloomberg) are projecting a broad range of significant

increases in EPS. In comparison to an average 2014 projected Pro Forma EPS of $1.34, eleven analysts’

forecasts for 2015 range from $2.50 to $4.55 with an average estimate of $3.03. Thus, the increases range from

87% to 240%, with an average of 126%. In contrast, analysts project a median increase of 17% for the eleven

competitors we analyzed. AXLL’s average forecasted 2015 EPS has declined from $3.65 (120 days ago) to

$3.33 (90 days ago) to $3.04 currently. Yet, AXLL’s stock price has increased during this time.

The 2014 trends below in quarterly EPS provide little support for such dramatic earnings growth in 2015, as

there is no sign that the earnings decline versus 2013 is ending. Additionally, the 2014 numbers do not

recognize that the 2014 book tax rate has been at an unsustainably low level, due to one-time accrual reductions.

Adjusting 2014 results based on a tax rate comparable to 2012 and 2013 (31%) would result in our projected

2014 Pro Forma EPS being reduced by $0.22 to $1.08.

1Q 2Q 3Q 4Q Total Year

2014 Reported EPS -$0.17 $0.38 $0.63 $0.21E $1.05E

2013 Reported EPS -$0.06 $1.03 $0.55 $0.92 $2.44

2014 Pro Forma EPS* -$0.09 $0.48 $0.70 $0.21E $1.30E

2013 Pro Forma EPS* $0.09 $1.21 $0.95 $0.90 $3.15 *Pro Forma EPS excludes one-time acquisition-related charges and asset write-down expenses. Source: AXLL financial statements, student estimates

The large projected increases, wide variability of analysts’ estimates, extreme disproportion to forecasts for

competitors, and the recent trending in EPS all cast doubt upon the likelihood of AXLL meeting analysts’

expectations. Since our analysis indicates that these lofty projections have been built into the stock price, there is

a great risk for investors that AXLL will be unable to meet expectations.

Our analysis projects that EPS will grow to $2.47 in 2015 from our projected $1.30 2014 Pro Forma EPS, which

still reflects dramatic improvement. Despite our projections being at the low end of the range of analysts, we

anticipate that it is more likely that AXLL will underperform rather than outperform our projections.

Volatile Margins: AXLL’s margins are highly dependent on the costs of natural gas, ethylene, electricity, fuel,

and other raw materials, many of which can be volatile. AXLL does not hedge against adverse changes in the

prices of these commodities and instead buys at spot prices. Prices of natural gas are seasonal and highly

sensitive to weather. Within a given year, the prices of any of these inputs can fluctuate widely as a result of

capacity additions or facility operating problems. AXLL admits that although it has attempted to pass on

increasing costs, it has been largely unsuccessful in the past and faces this risk in the future. AXLL is not a price

leader in its markets.

0.0

0.5

1.0

1.5

2.0

2.5

Housing Starts (Millions)

$28

$29

$30

$31

$32

Per Capita Income (Thousands)

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

10

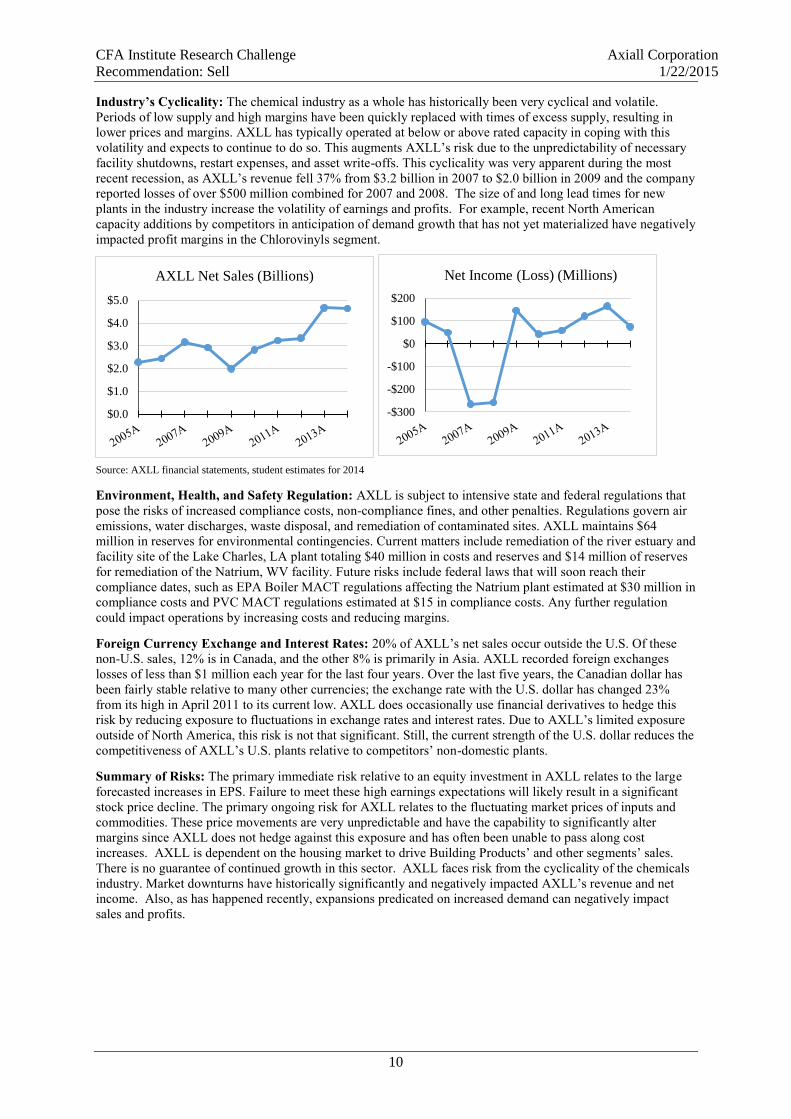

Industry’s Cyclicality: The chemical industry as a whole has historically been very cyclical and volatile.

Periods of low supply and high margins have been quickly replaced with times of excess supply, resulting in

lower prices and margins. AXLL has typically operated at below or above rated capacity in coping with this

volatility and expects to continue to do so. This augments AXLL’s risk due to the unpredictability of necessary

facility shutdowns, restart expenses, and asset write-offs. This cyclicality was very apparent during the most

recent recession, as AXLL’s revenue fell 37% from $3.2 billion in 2007 to $2.0 billion in 2009 and the company

reported losses of over $500 million combined for 2007 and 2008. The size of and long lead times for new

plants in the industry increase the volatility of earnings and profits. For example, recent North American

capacity additions by competitors in anticipation of demand growth that has not yet materialized have negatively

impacted profit margins in the Chlorovinyls segment.

Source: AXLL financial statements, student estimates for 2014

Environment, Health, and Safety Regulation: AXLL is subject to intensive state and federal regulations that

pose the risks of increased compliance costs, non-compliance fines, and other penalties. Regulations govern air

emissions, water discharges, waste disposal, and remediation of contaminated sites. AXLL maintains $64

million in reserves for environmental contingencies. Current matters include remediation of the river estuary and

facility site of the Lake Charles, LA plant totaling $40 million in costs and reserves and $14 million of reserves

for remediation of the Natrium, WV facility. Future risks include federal laws that will soon reach their

compliance dates, such as EPA Boiler MACT regulations affecting the Natrium plant estimated at $30 million in

compliance costs and PVC MACT regulations estimated at $15 in compliance costs. Any further regulation

could impact operations by increasing costs and reducing margins.

Foreign Currency Exchange and Interest Rates: 20% of AXLL’s net sales occur outside the U.S. Of these

non-U.S. sales, 12% is in Canada, and the other 8% is primarily in Asia. AXLL recorded foreign exchanges

losses of less than $1 million each year for the last four years. Over the last five years, the Canadian dollar has

been fairly stable relative to many other currencies; the exchange rate with the U.S. dollar has changed 23%

from its high in April 2011 to its current low. AXLL does occasionally use financial derivatives to hedge this

risk by reducing exposure to fluctuations in exchange rates and interest rates. Due to AXLL’s limited exposure

outside of North America, this risk is not that significant. Still, the current strength of the U.S. dollar reduces the

competitiveness of AXLL’s U.S. plants relative to competitors’ non-domestic plants.

Summary of Risks: The primary immediate risk relative to an equity investment in AXLL relates to the large

forecasted increases in EPS. Failure to meet these high earnings expectations will likely result in a significant

stock price decline. The primary ongoing risk for AXLL relates to the fluctuating market prices of inputs and

commodities. These price movements are very unpredictable and have the capability to significantly alter

margins since AXLL does not hedge against this exposure and has often been unable to pass along cost

increases. AXLL is dependent on the housing market to drive Building Products’ and other segments’ sales.

There is no guarantee of continued growth in this sector. AXLL faces risk from the cyclicality of the chemicals

industry. Market downturns have historically significantly and negatively impacted AXLL’s revenue and net

income. Also, as has happened recently, expansions predicated on increased demand can negatively impact

sales and profits.

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

AXLL Net Sales (Billions)

-$300

-$200

-$100

$0

$100

$200

Net Income (Loss) (Millions)

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

11

Appendix

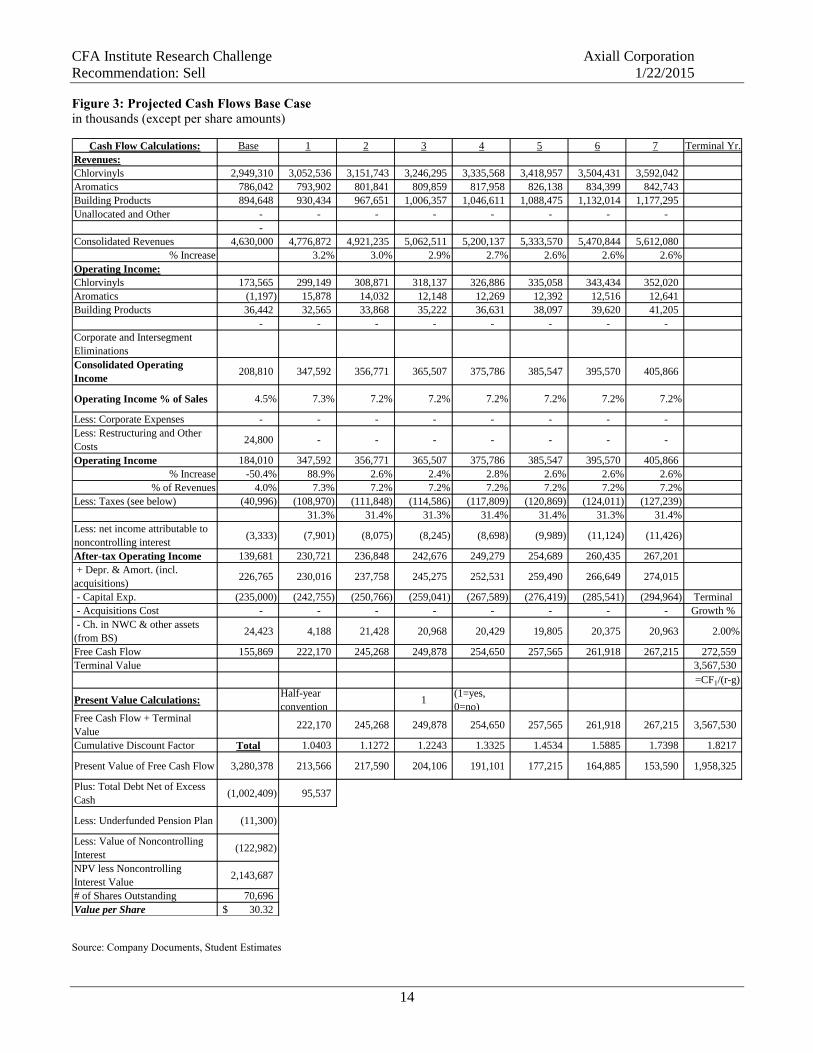

Figure 1: Income Statement Base Case

Figure 2: Balance Sheet Base Case

Figure 3: Projected Cash Flows Base Case

Figure 4: Cost of Capital & Scenario Weightings

Figure 5: Revenue and Margins Assumptions Base Case

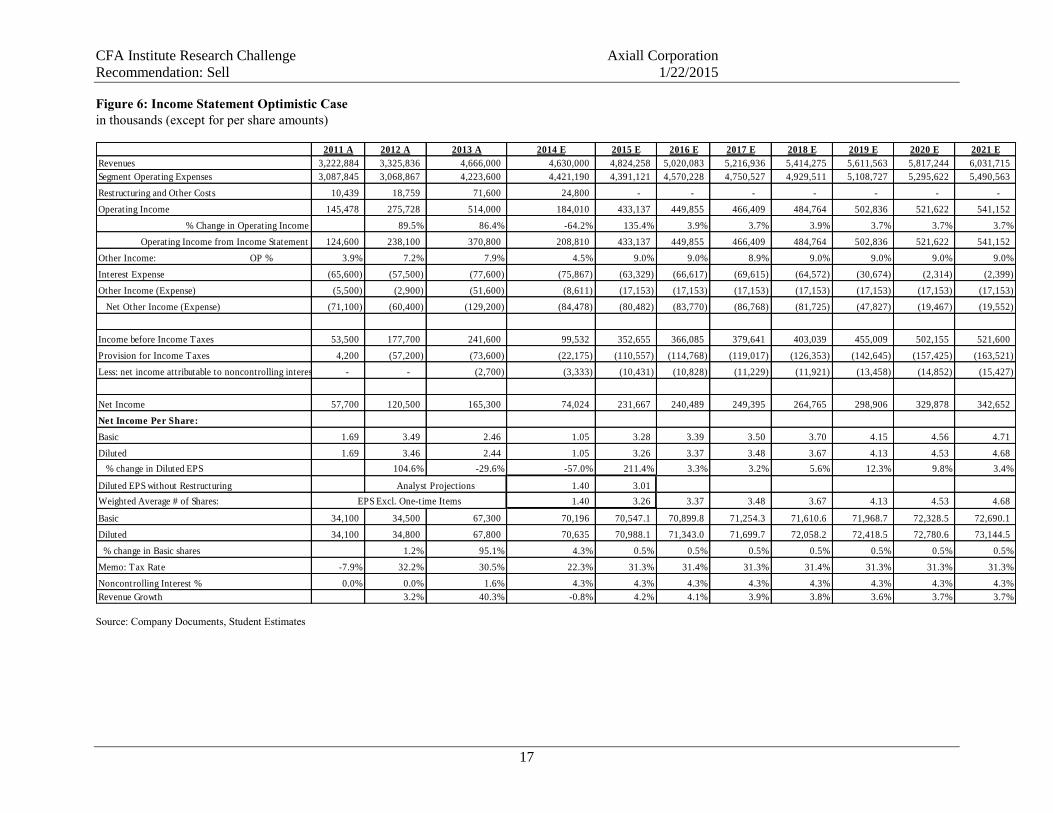

Figure 6: Income Statement Optimistic Case

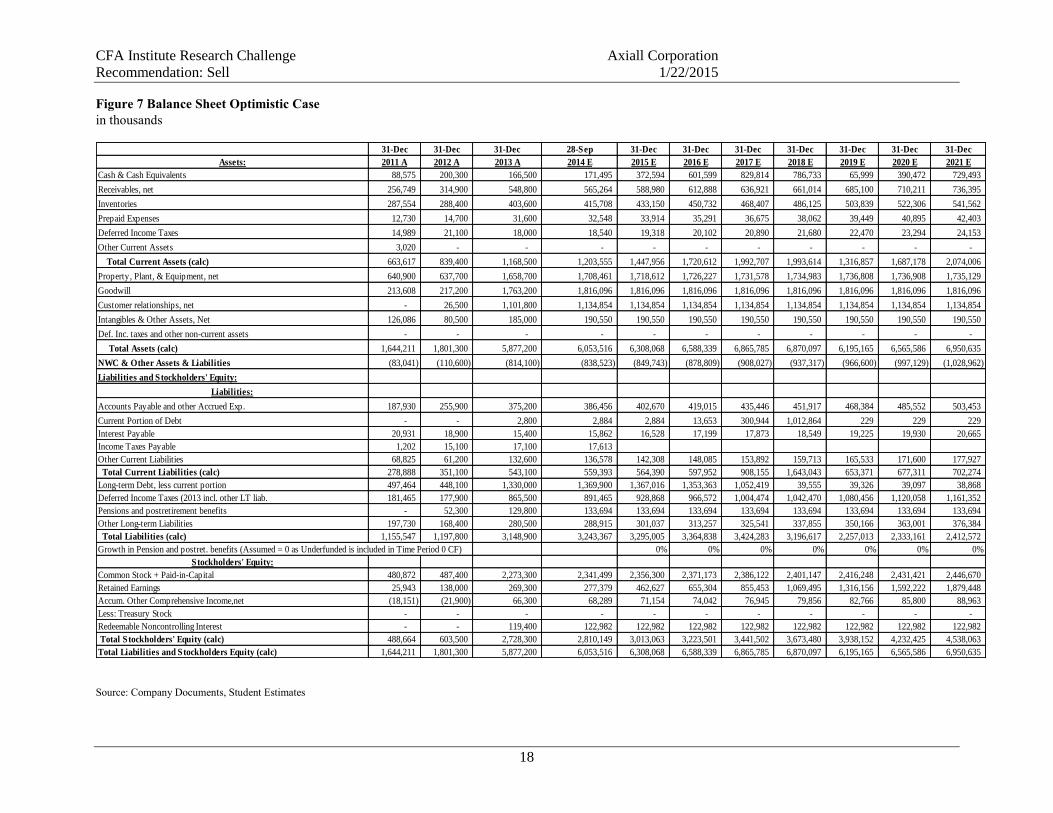

Figure 7: Balance Sheet Optimistic Case

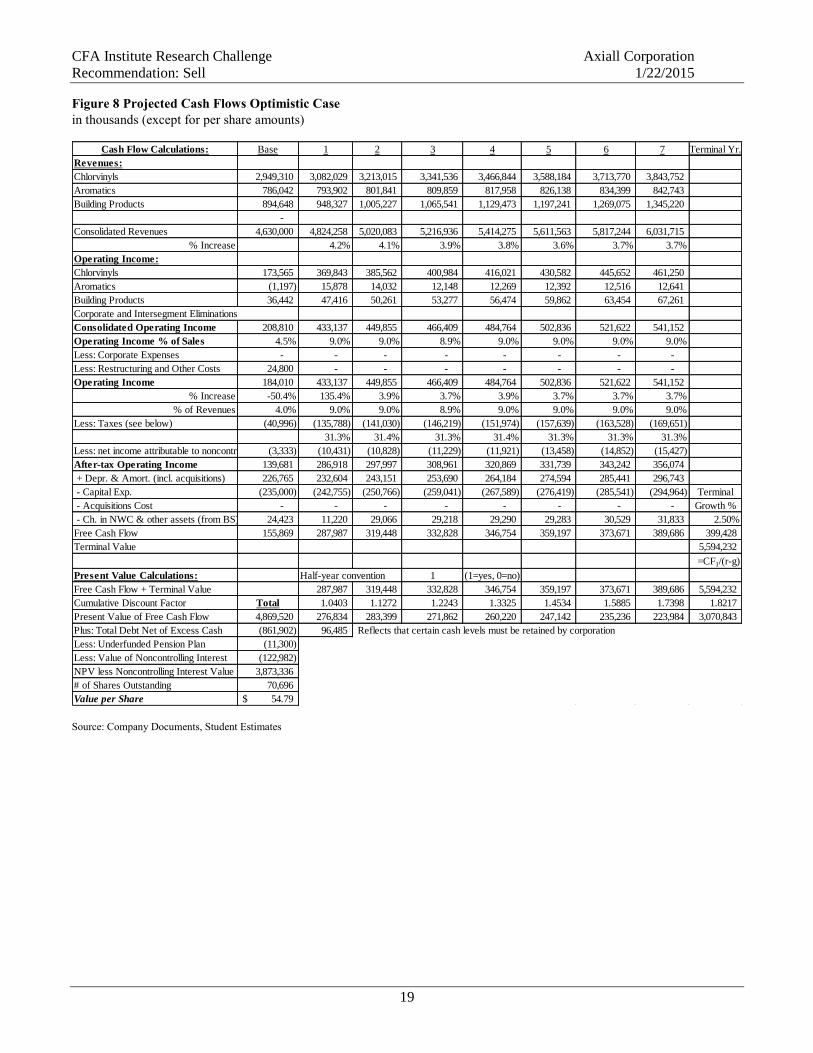

Figure 8: Projected Cash Flows Optimistic Case

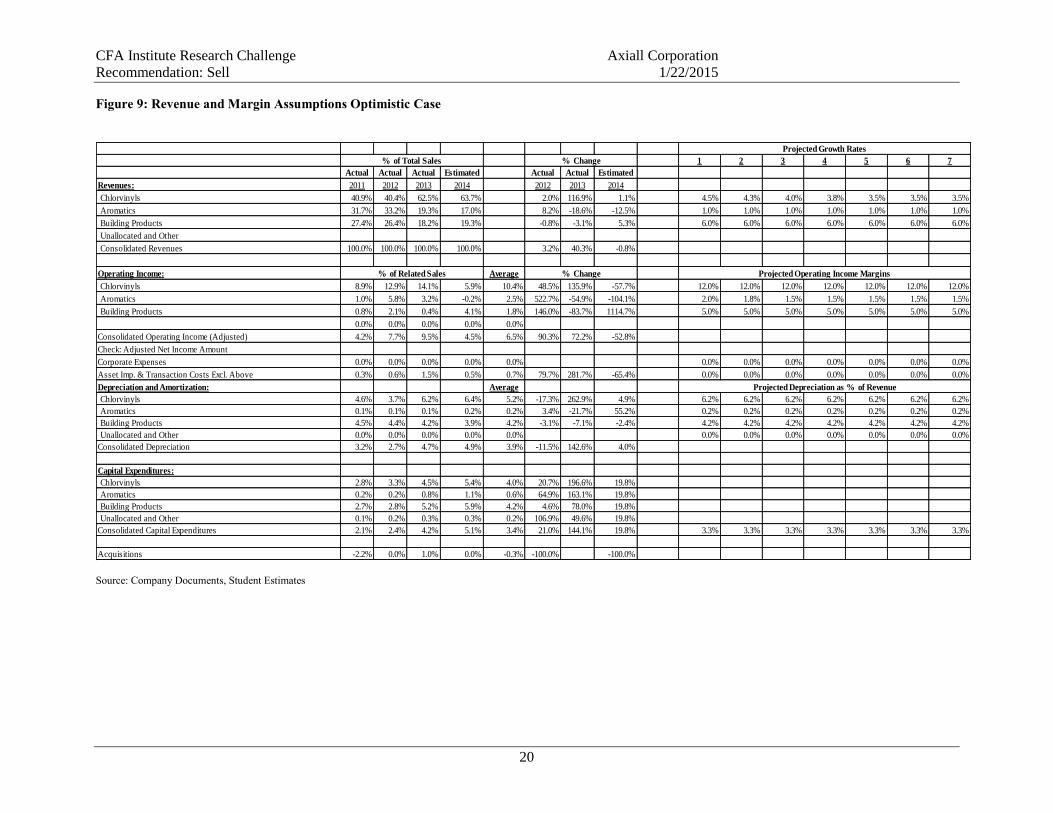

Figure 9: Revenue and Margins Assumptions Optimistic Case

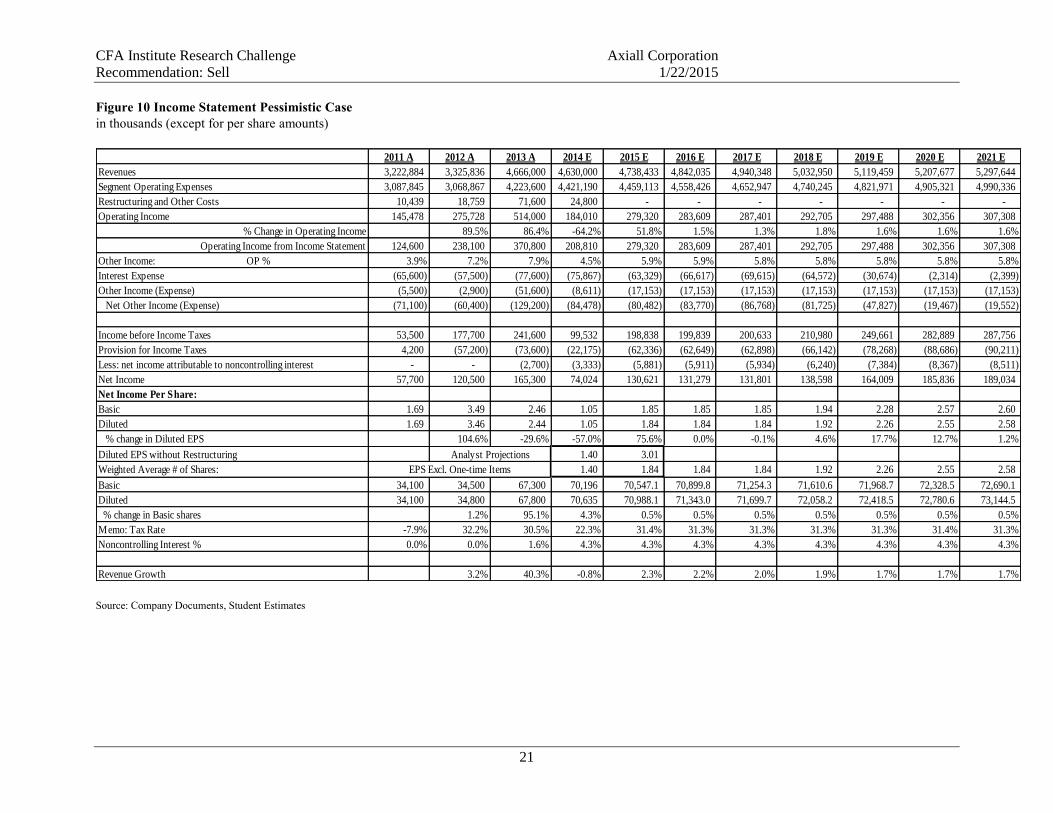

Figure 10: Income Statement Pessimistic Case

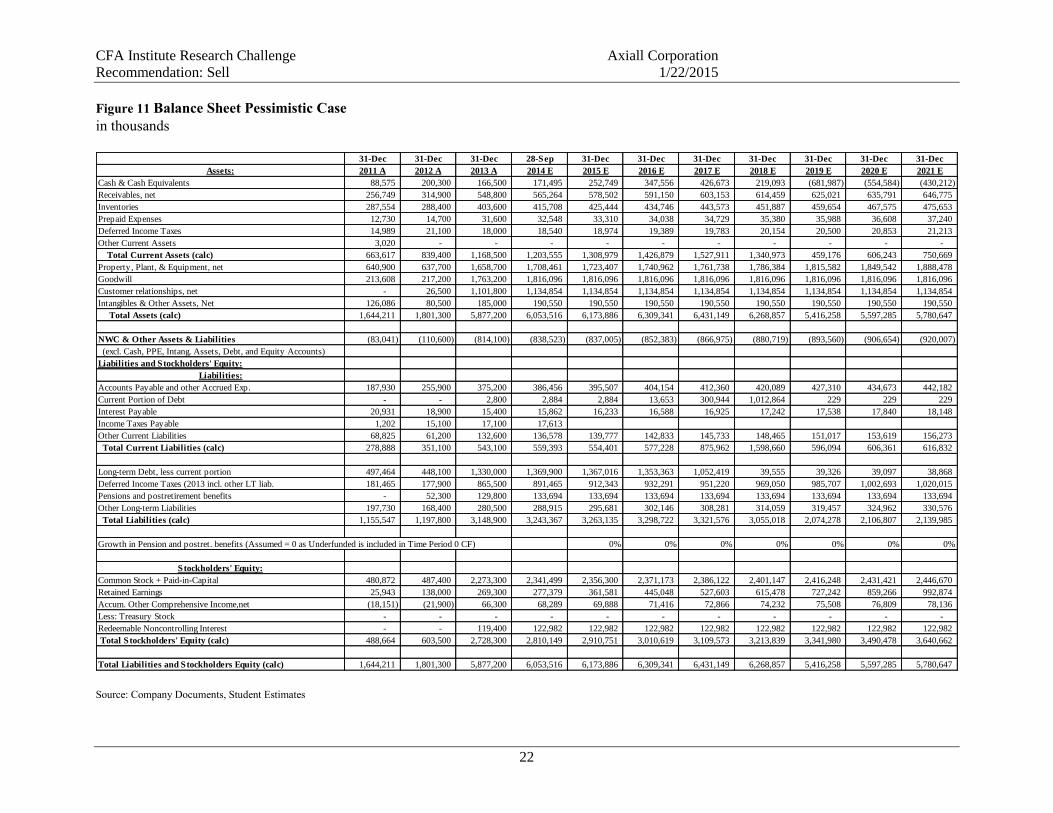

Figure 11: Balance Sheet Pessimistic Case

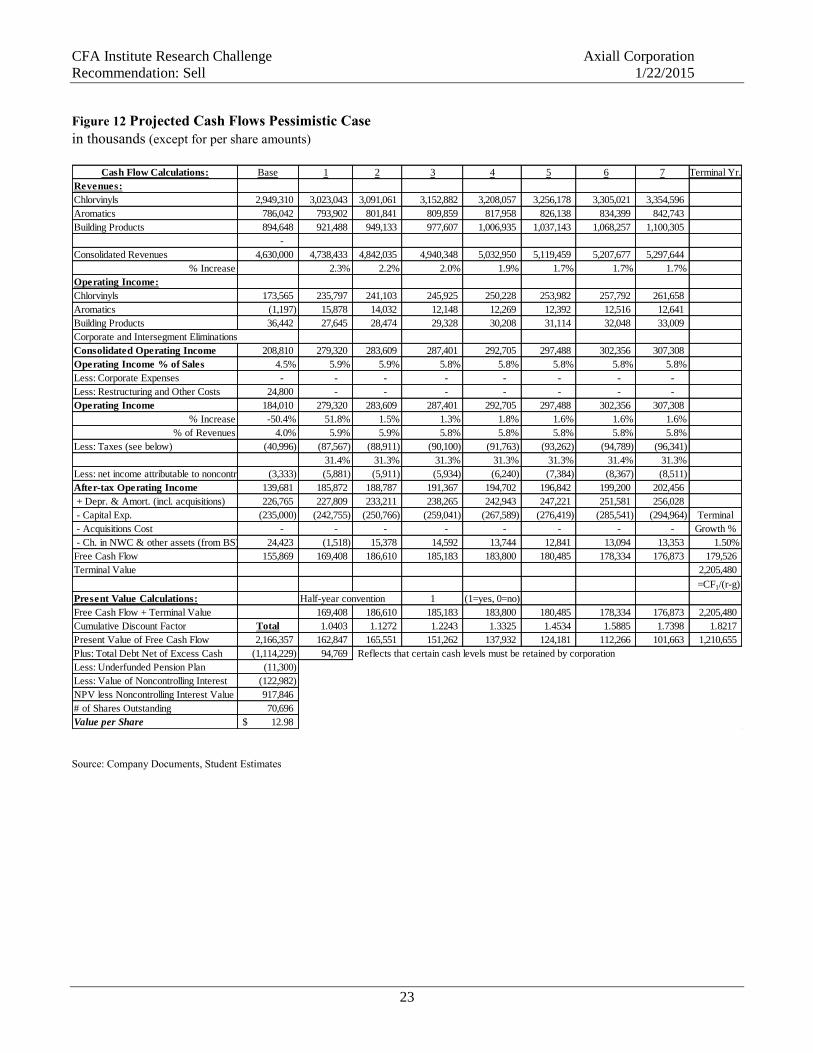

Figure 12: Projected Cash Flows Pessimistic Case

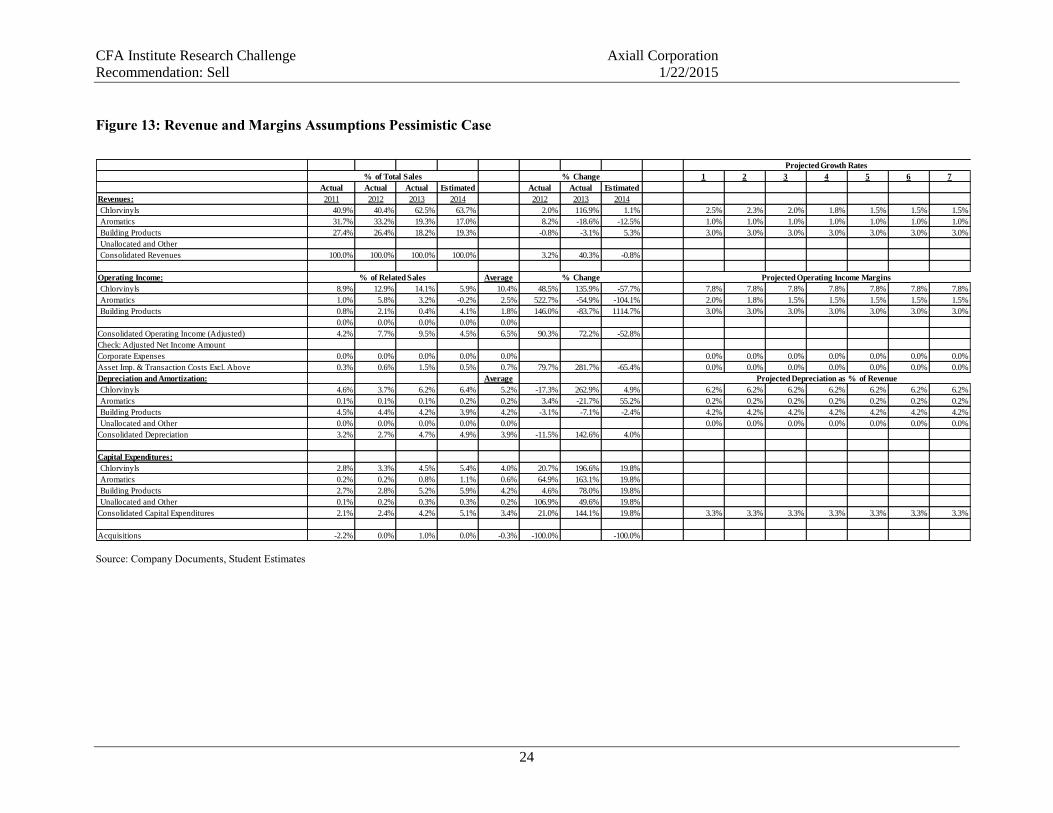

Figure 13: Revenue and Margins Assumptions Pessimistic Case

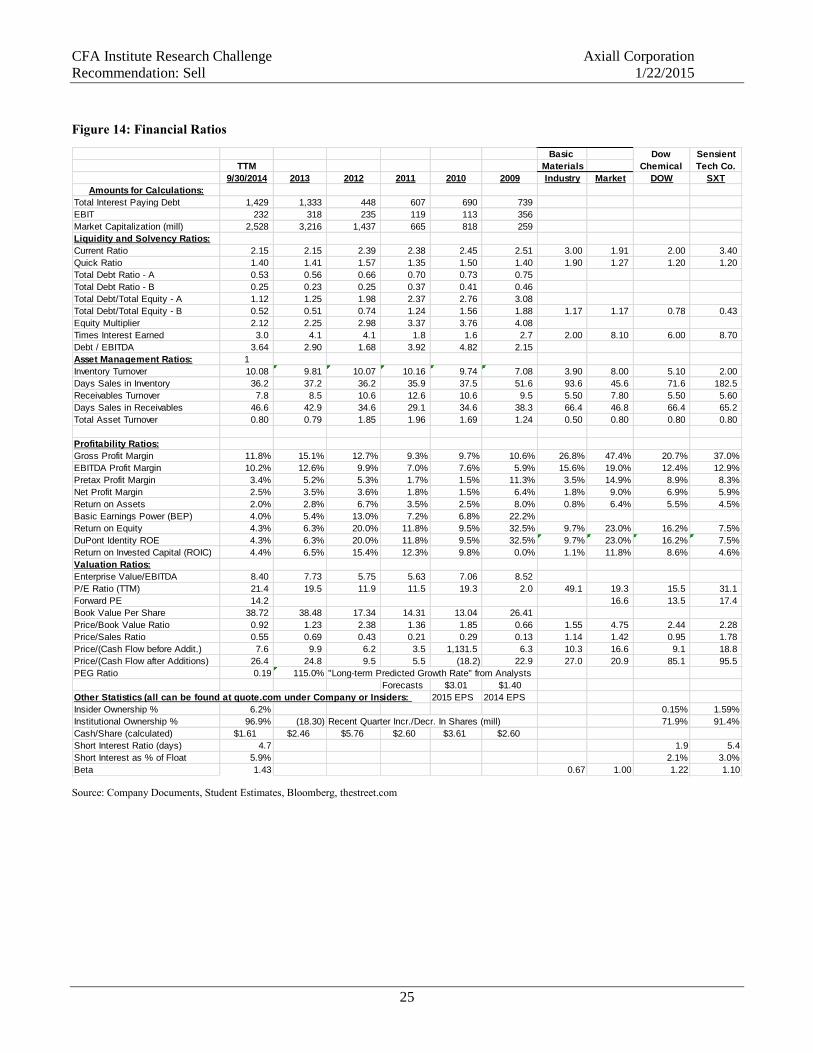

Figure 14: Financial Ratios

Figure 15: Comparable Company Profit Ratios Analysis

Figure 16: Multiples Analysis and Company Valuation

Figure 17: Analysis of Competitors’ Multiples

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

12

Figure 1: Income Statement Base Case

in thousands (except per share amounts)

Source: Company Documents, Student Estimates

2011 A 2012 A 2013 A 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E

Revenues 3,222,884 3,325,836 4,666,000 4,630,000 4,776,872 4,921,235 5,062,511 5,200,137 5,333,570 5,470,844

Segment Operating Expenses 3,087,845 3,068,867 4,223,600 4,421,190 4,429,280 4,564,464 4,697,004 4,824,351 4,948,023 5,075,274

Restructuring and Other Costs 10,439 18,759 71,600 24,800 - - - - - -

Operating Income 145,478 275,728 514,000 184,010 347,592 356,771 365,507 375,786 385,547 395,570

% Change in Operating Income 89.5% 86.4% -64.2% 88.9% 2.6% 2.4% 2.8% 2.6% 2.6%

Operating Income from Income Statement 124,600 238,100 370,800 208,810 347,592 356,771 365,507 375,786 385,547 395,570

Other Income: OP % 3.9% 7.2% 7.9% 4.5% 7.3% 7.2% 7.2% 7.2% 7.2% 7.2%

Interest Expense (65,600) (57,500) (77,600) (75,867) (63,329) (66,617) (69,615) (64,572) (30,674) (2,314)

Other Income (Expense) (5,500) (2,900) (51,600) (8,611) (17,153) (17,153) (17,153) (17,153) (17,153) (17,153)

Net Other Income (Expense) (71,100) (60,400) (129,200) (84,478) (80,482) (83,770) (86,768) (81,725) (47,827) (19,467)

Income before Income Taxes 53,500 177,700 241,600 99,532 267,110 273,001 278,739 294,061 337,720 376,103

Provision for Income Taxes 4,200 (57,200) (73,600) (22,175) (83,739) (85,586) (87,384) (92,188) (105,875) (117,908)

Less: net income attributable to noncontrolling interest - - (2,700) (3,333) (7,901) (8,075) (8,245) (8,698) (9,989) (11,124)

Net Income 57,700 120,500 165,300 74,024 175,470 179,340 183,110 193,175 221,856 247,071

Net Income Per Share:

Basic 1.69 3.49 2.46 1.05 2.49 2.53 2.57 2.70 3.08 3.42

Diluted 1.69 3.46 2.44 1.05 2.47 2.51 2.55 2.68 3.06 3.39

% change in Diluted EPS 104.6% -29.6% -57.0% 135.9% 1.7% 1.6% 5.0% 14.3% 10.8%

Diluted EPS without Restructuring 1.40 3.01

Weighted Average # of Shares: 1.40 2.47 2.51 2.55 2.68 3.06 3.39

Basic 34,100 34,500 67,300 70,196 70,547.1 70,899.8 71,254.3 71,610.6 71,968.7 72,328.5

Diluted 34,100 34,800 67,800 70,635 70,988.1 71,343.0 71,699.7 72,058.2 72,418.5 72,780.6

% change in Basic shares 1.2% 95.1% 4.3% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Memo: Tax Rate -7.9% 32.2% 30.5% 22.3% 31.4% 31.4% 31.3% 31.3% 31.3% 31.3%

Noncontrolling Interest % 0.0% 0.0% 1.6% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3%

Revenue Growth 3.2% 40.3% -0.8% 3.2% 3.0% 2.9% 2.7% 2.6% 2.6%

Analyst Projections

EPS Excl. One-time Items

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

13

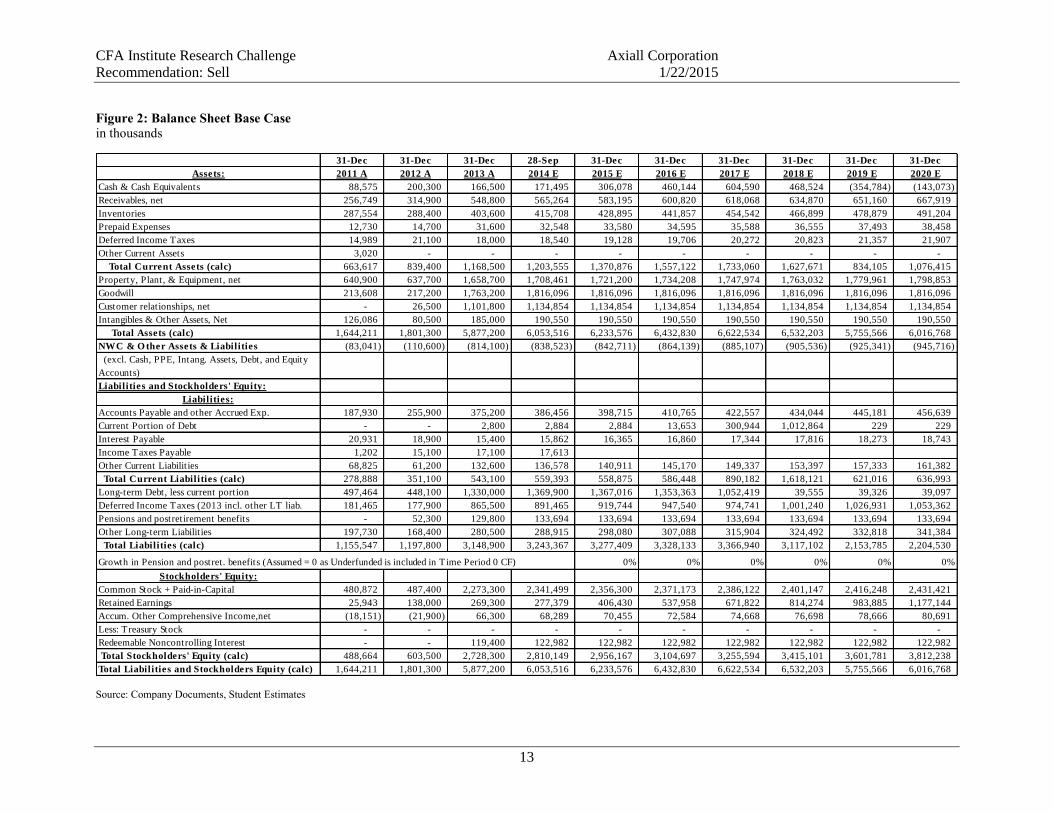

Figure 2: Balance Sheet Base Case

in thousands

Source: Company Documents, Student Estimates

31-Dec 31-Dec 31-Dec 28-Sep 31-Dec 31-Dec 31-Dec 31-Dec 31-Dec 31-Dec

Assets: 2011 A 2012 A 2013 A 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E

Cash & Cash Equivalents 88,575 200,300 166,500 171,495 306,078 460,144 604,590 468,524 (354,784) (143,073)

Receivables, net 256,749 314,900 548,800 565,264 583,195 600,820 618,068 634,870 651,160 667,919

Inventories 287,554 288,400 403,600 415,708 428,895 441,857 454,542 466,899 478,879 491,204

Prepaid Expenses 12,730 14,700 31,600 32,548 33,580 34,595 35,588 36,555 37,493 38,458

Deferred Income Taxes 14,989 21,100 18,000 18,540 19,128 19,706 20,272 20,823 21,357 21,907

Other Current Assets 3,020 - - - - - - - - -

Total Current Assets (calc) 663,617 839,400 1,168,500 1,203,555 1,370,876 1,557,122 1,733,060 1,627,671 834,105 1,076,415

Property, Plant, & Equipment, net 640,900 637,700 1,658,700 1,708,461 1,721,200 1,734,208 1,747,974 1,763,032 1,779,961 1,798,853

Goodwill 213,608 217,200 1,763,200 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096

Customer relationships, net - 26,500 1,101,800 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854

Intangibles & Other Assets, Net 126,086 80,500 185,000 190,550 190,550 190,550 190,550 190,550 190,550 190,550

Total Assets (calc) 1,644,211 1,801,300 5,877,200 6,053,516 6,233,576 6,432,830 6,622,534 6,532,203 5,755,566 6,016,768

NWC & O ther Assets & Liabilities (83,041) (110,600) (814,100) (838,523) (842,711) (864,139) (885,107) (905,536) (925,341) (945,716)

(excl. Cash, PPE, Intang. Assets, Debt, and Equity

Accounts)

Liabilities and Stockholders' Equity:

Liabilities:

Accounts Payable and other Accrued Exp. 187,930 255,900 375,200 386,456 398,715 410,765 422,557 434,044 445,181 456,639

Current Portion of Debt - - 2,800 2,884 2,884 13,653 300,944 1,012,864 229 229

Interest Payable 20,931 18,900 15,400 15,862 16,365 16,860 17,344 17,816 18,273 18,743

Income Taxes Payable 1,202 15,100 17,100 17,613

Other Current Liabilities 68,825 61,200 132,600 136,578 140,911 145,170 149,337 153,397 157,333 161,382

Total Current Liabilities (calc) 278,888 351,100 543,100 559,393 558,875 586,448 890,182 1,618,121 621,016 636,993

Long-term Debt, less current portion 497,464 448,100 1,330,000 1,369,900 1,367,016 1,353,363 1,052,419 39,555 39,326 39,097

Deferred Income Taxes (2013 incl. other LT liab. 181,465 177,900 865,500 891,465 919,744 947,540 974,741 1,001,240 1,026,931 1,053,362

Pensions and postretirement benefits - 52,300 129,800 133,694 133,694 133,694 133,694 133,694 133,694 133,694

Other Long-term Liabilities 197,730 168,400 280,500 288,915 298,080 307,088 315,904 324,492 332,818 341,384

Total Liabilities (calc) 1,155,547 1,197,800 3,148,900 3,243,367 3,277,409 3,328,133 3,366,940 3,117,102 2,153,785 2,204,530

0% 0% 0% 0% 0% 0%

Stockholders' Equity:

Common Stock + Paid-in-Capital 480,872 487,400 2,273,300 2,341,499 2,356,300 2,371,173 2,386,122 2,401,147 2,416,248 2,431,421

Retained Earnings 25,943 138,000 269,300 277,379 406,430 537,958 671,822 814,274 983,885 1,177,144

Accum. Other Comprehensive Income,net (18,151) (21,900) 66,300 68,289 70,455 72,584 74,668 76,698 78,666 80,691

Less: Treasury Stock - - - - - - - - - -

Redeemable Noncontrolling Interest - - 119,400 122,982 122,982 122,982 122,982 122,982 122,982 122,982

Total Stockholders' Equity (calc) 488,664 603,500 2,728,300 2,810,149 2,956,167 3,104,697 3,255,594 3,415,101 3,601,781 3,812,238

Total Liabilities and Stockholders Equity (calc) 1,644,211 1,801,300 5,877,200 6,053,516 6,233,576 6,432,830 6,622,534 6,532,203 5,755,566 6,016,768

Growth in Pension and postret. benefits (Assumed = 0 as Underfunded is included in T ime Period 0 CF)

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

14

Figure 3: Projected Cash Flows Base Case

in thousands (except per share amounts)

Source: Company Documents, Student Estimates

Cash Flow Calculations: Base 1 2 3 4 5 6 7 Terminal Yr.

Revenues:

Chlorvinyls 2,949,310 3,052,536 3,151,743 3,246,295 3,335,568 3,418,957 3,504,431 3,592,042

Aromatics 786,042 793,902 801,841 809,859 817,958 826,138 834,399 842,743

Building Products 894,648 930,434 967,651 1,006,357 1,046,611 1,088,475 1,132,014 1,177,295

Unallocated and Other - - - - - - - -

-

Consolidated Revenues 4,630,000 4,776,872 4,921,235 5,062,511 5,200,137 5,333,570 5,470,844 5,612,080

% Increase 3.2% 3.0% 2.9% 2.7% 2.6% 2.6% 2.6%

Operating Income:

Chlorvinyls 173,565 299,149 308,871 318,137 326,886 335,058 343,434 352,020

Aromatics (1,197) 15,878 14,032 12,148 12,269 12,392 12,516 12,641

Building Products 36,442 32,565 33,868 35,222 36,631 38,097 39,620 41,205

- - - - - - - -

Corporate and Intersegment

Eliminations

Consolidated Operating

Income208,810 347,592 356,771 365,507 375,786 385,547 395,570 405,866

Operating Income % of Sales 4.5% 7.3% 7.2% 7.2% 7.2% 7.2% 7.2% 7.2%

Less: Corporate Expenses - - - - - - - -

Less: Restructuring and Other

Costs24,800 - - - - - - -

Operating Income 184,010 347,592 356,771 365,507 375,786 385,547 395,570 405,866

% Increase -50.4% 88.9% 2.6% 2.4% 2.8% 2.6% 2.6% 2.6%

% of Revenues 4.0% 7.3% 7.2% 7.2% 7.2% 7.2% 7.2% 7.2%

Less: Taxes (see below) (40,996) (108,970) (111,848) (114,586) (117,809) (120,869) (124,011) (127,239)

31.3% 31.4% 31.3% 31.4% 31.4% 31.3% 31.4%

Less: net income attributable to

noncontrolling interest(3,333) (7,901) (8,075) (8,245) (8,698) (9,989) (11,124) (11,426)

After-tax Operating Income 139,681 230,721 236,848 242,676 249,279 254,689 260,435 267,201

+ Depr. & Amort. (incl.

acquisitions)226,765 230,016 237,758 245,275 252,531 259,490 266,649 274,015

- Capital Exp. (235,000) (242,755) (250,766) (259,041) (267,589) (276,419) (285,541) (294,964) Terminal

- Acquisitions Cost - - - - - - - - Growth %

- Ch. in NWC & other assets

(from BS)24,423 4,188 21,428 20,968 20,429 19,805 20,375 20,963 2.00%

Free Cash Flow 155,869 222,170 245,268 249,878 254,650 257,565 261,918 267,215 272,559

Terminal Value 3,567,530

=CF1/(r-g)

Present Value Calculations:Half-year

convention1

(1=yes,

0=no)Free Cash Flow + Terminal

Value222,170 245,268 249,878 254,650 257,565 261,918 267,215 3,567,530

Cumulative Discount Factor Total 1.0403 1.1272 1.2243 1.3325 1.4534 1.5885 1.7398 1.8217

Present Value of Free Cash Flow 3,280,378 213,566 217,590 204,106 191,101 177,215 164,885 153,590 1,958,325

Plus: Total Debt Net of Excess

Cash(1,002,409) 95,537

Less: Underfunded Pension Plan (11,300)

Less: Value of Noncontrolling

Interest(122,982)

NPV less Noncontrolling

Interest Value2,143,687

# of Shares Outstanding 70,696

Value per Share 30.32$

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

15

Figure 4: Cost of Capital & Scenario Weightings

in thousands (except per share amounts)

Source: Company Documents, Student Estimates

Cost of Capital Calculations: Base Allowance for Changing WACC due to Changing Interest Rates

Debt Ratio (calc. below) 31.44% 31.44% 31.44% 31.44% 31.44% 31.44% 31.44%

Tax Rate 31.35% 29.00% 28.00% 28.00% 28.00% 28.00% 28.00%

Equity Ratio (calc. below) 68.56% 68.56% 68.56% 68.56% 68.56% 68.56% 68.56%

Cost of Common Equity (using CAPM) 10.54% 10.79% 11.04% 11.29% 11.54% 11.79% 12.04%

Pretax Cost of Debt (from below) 4.62% 4.87% 5.12% 5.37% 5.62% 5.87% 6.12%

After-tax Cost of Debt 3.17% 3.46% 3.69% 3.87% 4.05% 4.23% 4.41%

Pref. Stock Ratio (calc. below) 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Cost of Capital 8.22% 8.49% 8.73% 8.96% 9.18% 9.41% 9.64%

Assumptions: Incr. in IRs 0.25% 0.25% 0.25% 0.25% 0.25% 0.25%

Terminal Growth Rate 2.00%

Risk-free Rate (10-yr. US T-Bond) 2.25% 2.50% 2.75% 3.00% 3.25% 3.50% 3.75%

Market Risk Premium (Historical Avg.) 5.80% 5.80% 5.80% 5.80% 5.80% 5.80% 5.80%

Cost of Debt 4.62% 4.87% 5.12% 5.37% 5.62% 5.87% 6.12%

Cost of Preferred Stock

Beta 1.43 1.43 1.43 1.43 1.43 1.43 1.43

Capital Weightings: Scenario: Weighting

Common Stock Price $42.17 Base $30.32 50%

# of Shares Outstanding 70,988.1 Optimistic $54.79 20%

Market Value of Equity 2,993,568 68.56% Pessimistic $12.98 30%

Value of Debt from Balance Sheet 1,372,784 Target $30.01

Debt Value of Operating Leases 270

Total Debt Value 1,373,054 31.44%

Value of Preferred Stock 0.00%

Total Capital 4,366,622 100.0%

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

16

Figure 5: Revenue and Margin Assumptions Base Case

Source: Company Documents, Student Estimates

1 2 3 4 5 6 7

Actual Actual Actual Estimated Actual Actual Estimated

Revenues: 2011 2012 2013 2014 2012 2013 2014

Chlorvinyls 40.9% 40.4% 62.5% 63.7% 2.0% 116.9% 1.1% 3.5% 3.3% 3.0% 2.8% 2.5% 2.5% 2.5%

Aromatics 31.7% 33.2% 19.3% 17.0% 8.2% -18.6% -12.5% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Building Products 27.4% 26.4% 18.2% 19.3% -0.8% -3.1% 5.3% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0%

Unallocated and Other

Consolidated Revenues 100.0% 100.0% 100.0% 100.0% 3.2% 40.3% -0.8%

Operating Income: Average

Chlorvinyls 8.9% 12.9% 14.1% 5.9% 10.4% 48.5% 135.9% -57.7% 9.8% 9.8% 9.8% 9.8% 9.8% 9.8% 9.8%

Aromatics 1.0% 5.8% 3.2% -0.2% 2.5% 522.7% -54.9% -104.1% 2.0% 1.8% 1.5% 1.5% 1.5% 1.5% 1.5%

Building Products 0.8% 2.1% 0.4% 4.1% 1.8% 146.0% -83.7% 1114.7% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5% 3.5%

0.0% 0.0% 0.0% 0.0% 0.0%

Consolidated Operating Income (Adjusted) 4.2% 7.7% 9.5% 4.5% 6.5% 90.3% 72.2% -52.8%

Check: Adjusted Net Income Amount

Corporate Expenses 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Asset Imp. & Transaction Costs Excl. Above 0.3% 0.6% 1.5% 0.5% 0.7% 79.7% 281.7% -65.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Depreciation and Amortization: Average

Chlorvinyls 4.6% 3.7% 6.2% 6.4% 5.2% -17.3% 262.9% 4.9% 6.2% 6.2% 6.2% 6.2% 6.2% 6.2% 6.2%

Aromatics 0.1% 0.1% 0.1% 0.2% 0.2% 3.4% -21.7% 55.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2%

Building Products 4.5% 4.4% 4.2% 3.9% 4.2% -3.1% -7.1% -2.4% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2%

Unallocated and Other 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Consolidated Depreciation 3.2% 2.7% 4.7% 4.9% 3.9% -11.5% 142.6% 4.0%

Capital Expenditures:

Chlorvinyls 2.8% 3.3% 4.5% 5.4% 4.0% 20.7% 196.6% 19.8%

Aromatics 0.2% 0.2% 0.8% 1.1% 0.6% 64.9% 163.1% 19.8%

Building Products 2.7% 2.8% 5.2% 5.9% 4.2% 4.6% 78.0% 19.8%

Unallocated and Other 0.1% 0.2% 0.3% 0.3% 0.2% 106.9% 49.6% 19.8%

Consolidated Capital Expenditures 2.1% 2.4% 4.2% 5.1% 3.4% 21.0% 144.1% 19.8% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3%

Acquisitions -2.2% 0.0% 1.0% 0.0% -0.3% -100.0% -100.0%

Projected Growth Rates

Projected Operating Income Margins

Projected Depreciation as % of Revenue

% of Total Sales

% of Related Sales % Change

% Change

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

17

Figure 6: Income Statement Optimistic Case

in thousands (except for per share amounts)

Source: Company Documents, Student Estimates

2011 A 2012 A 2013 A 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E 2021 E

Revenues 3,222,884 3,325,836 4,666,000 4,630,000 4,824,258 5,020,083 5,216,936 5,414,275 5,611,563 5,817,244 6,031,715

Segment Operating Expenses 3,087,845 3,068,867 4,223,600 4,421,190 4,391,121 4,570,228 4,750,527 4,929,511 5,108,727 5,295,622 5,490,563

Restructuring and Other Costs 10,439 18,759 71,600 24,800 - - - - - - -

Operating Income 145,478 275,728 514,000 184,010 433,137 449,855 466,409 484,764 502,836 521,622 541,152

% Change in Operating Income 89.5% 86.4% -64.2% 135.4% 3.9% 3.7% 3.9% 3.7% 3.7% 3.7%

Operating Income from Income Statement 124,600 238,100 370,800 208,810 433,137 449,855 466,409 484,764 502,836 521,622 541,152

Other Income: OP % 3.9% 7.2% 7.9% 4.5% 9.0% 9.0% 8.9% 9.0% 9.0% 9.0% 9.0%

Interest Expense (65,600) (57,500) (77,600) (75,867) (63,329) (66,617) (69,615) (64,572) (30,674) (2,314) (2,399)

Other Income (Expense) (5,500) (2,900) (51,600) (8,611) (17,153) (17,153) (17,153) (17,153) (17,153) (17,153) (17,153)

Net Other Income (Expense) (71,100) (60,400) (129,200) (84,478) (80,482) (83,770) (86,768) (81,725) (47,827) (19,467) (19,552)

Income before Income Taxes 53,500 177,700 241,600 99,532 352,655 366,085 379,641 403,039 455,009 502,155 521,600

Provision for Income Taxes 4,200 (57,200) (73,600) (22,175) (110,557) (114,768) (119,017) (126,353) (142,645) (157,425) (163,521)

Less: net income attributable to noncontrolling interest - - (2,700) (3,333) (10,431) (10,828) (11,229) (11,921) (13,458) (14,852) (15,427)

Net Income 57,700 120,500 165,300 74,024 231,667 240,489 249,395 264,765 298,906 329,878 342,652

Net Income Per Share:

Basic 1.69 3.49 2.46 1.05 3.28 3.39 3.50 3.70 4.15 4.56 4.71

Diluted 1.69 3.46 2.44 1.05 3.26 3.37 3.48 3.67 4.13 4.53 4.68

% change in Diluted EPS 104.6% -29.6% -57.0% 211.4% 3.3% 3.2% 5.6% 12.3% 9.8% 3.4%

Diluted EPS without Restructuring 1.40 3.01

Weighted Average # of Shares: 1.40 3.26 3.37 3.48 3.67 4.13 4.53 4.68

Basic 34,100 34,500 67,300 70,196 70,547.1 70,899.8 71,254.3 71,610.6 71,968.7 72,328.5 72,690.1

Diluted 34,100 34,800 67,800 70,635 70,988.1 71,343.0 71,699.7 72,058.2 72,418.5 72,780.6 73,144.5

% change in Basic shares 1.2% 95.1% 4.3% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Memo: Tax Rate -7.9% 32.2% 30.5% 22.3% 31.3% 31.4% 31.3% 31.4% 31.3% 31.3% 31.3%

Noncontrolling Interest % 0.0% 0.0% 1.6% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3%

Revenue Growth 3.2% 40.3% -0.8% 4.2% 4.1% 3.9% 3.8% 3.6% 3.7% 3.7%

Analyst Projections

EPS Excl. One-time Items

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

18

Figure 7 Balance Sheet Optimistic Case

in thousands

Source: Company Documents, Student Estimates

31-Dec 31-Dec 31-Dec 28-Sep 31-Dec 31-Dec 31-Dec 31-Dec 31-Dec 31-Dec 31-Dec

Assets: 2011 A 2012 A 2013 A 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E 2021 E

Cash & Cash Equivalents 88,575 200,300 166,500 171,495 372,594 601,599 829,814 786,733 65,999 390,472 729,493

Receivables, net 256,749 314,900 548,800 565,264 588,980 612,888 636,921 661,014 685,100 710,211 736,395

Inventories 287,554 288,400 403,600 415,708 433,150 450,732 468,407 486,125 503,839 522,306 541,562

Prepaid Expenses 12,730 14,700 31,600 32,548 33,914 35,291 36,675 38,062 39,449 40,895 42,403

Deferred Income Taxes 14,989 21,100 18,000 18,540 19,318 20,102 20,890 21,680 22,470 23,294 24,153

Other Current Assets 3,020 - - - - - - - - - -

Total Current Assets (calc) 663,617 839,400 1,168,500 1,203,555 1,447,956 1,720,612 1,992,707 1,993,614 1,316,857 1,687,178 2,074,006

Property, Plant, & Equipment, net 640,900 637,700 1,658,700 1,708,461 1,718,612 1,726,227 1,731,578 1,734,983 1,736,808 1,736,908 1,735,129

Goodwill 213,608 217,200 1,763,200 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096 1,816,096

Customer relationships, net - 26,500 1,101,800 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854 1,134,854

Intangibles & Other Assets, Net 126,086 80,500 185,000 190,550 190,550 190,550 190,550 190,550 190,550 190,550 190,550

Def. Inc. taxes and other non-current assets - - - - - - - - - - -

Total Assets (calc) 1,644,211 1,801,300 5,877,200 6,053,516 6,308,068 6,588,339 6,865,785 6,870,097 6,195,165 6,565,586 6,950,635

NWC & Other Assets & Liabilities (83,041) (110,600) (814,100) (838,523) (849,743) (878,809) (908,027) (937,317) (966,600) (997,129) (1,028,962)

Liabilities and Stockholders' Equity:

Liabilities:

Accounts Payable and other Accrued Exp. 187,930 255,900 375,200 386,456 402,670 419,015 435,446 451,917 468,384 485,552 503,453

Current Portion of Debt - - 2,800 2,884 2,884 13,653 300,944 1,012,864 229 229 229

Interest Payable 20,931 18,900 15,400 15,862 16,528 17,199 17,873 18,549 19,225 19,930 20,665

Income Taxes Payable 1,202 15,100 17,100 17,613

Other Current Liabilities 68,825 61,200 132,600 136,578 142,308 148,085 153,892 159,713 165,533 171,600 177,927

Total Current Liabilities (calc) 278,888 351,100 543,100 559,393 564,390 597,952 908,155 1,643,043 653,371 677,311 702,274

Long-term Debt, less current portion 497,464 448,100 1,330,000 1,369,900 1,367,016 1,353,363 1,052,419 39,555 39,326 39,097 38,868

Deferred Income Taxes (2013 incl. other LT liab. 181,465 177,900 865,500 891,465 928,868 966,572 1,004,474 1,042,470 1,080,456 1,120,058 1,161,352

Pensions and postretirement benefits - 52,300 129,800 133,694 133,694 133,694 133,694 133,694 133,694 133,694 133,694

Other Long-term Liabilities 197,730 168,400 280,500 288,915 301,037 313,257 325,541 337,855 350,166 363,001 376,384

Total Liabilities (calc) 1,155,547 1,197,800 3,148,900 3,243,367 3,295,005 3,364,838 3,424,283 3,196,617 2,257,013 2,333,161 2,412,572

Growth in Pension and postret. benefits (Assumed = 0 as Underfunded is included in Time Period 0 CF) 0% 0% 0% 0% 0% 0% 0%

Stockholders' Equity:

Common Stock + Paid-in-Capital 480,872 487,400 2,273,300 2,341,499 2,356,300 2,371,173 2,386,122 2,401,147 2,416,248 2,431,421 2,446,670

Retained Earnings 25,943 138,000 269,300 277,379 462,627 655,304 855,453 1,069,495 1,316,156 1,592,222 1,879,448

Accum. Other Comprehensive Income,net (18,151) (21,900) 66,300 68,289 71,154 74,042 76,945 79,856 82,766 85,800 88,963

Less: Treasury Stock - - - - - - - - - - -

Redeemable Noncontrolling Interest - - 119,400 122,982 122,982 122,982 122,982 122,982 122,982 122,982 122,982

Total Stockholders' Equity (calc) 488,664 603,500 2,728,300 2,810,149 3,013,063 3,223,501 3,441,502 3,673,480 3,938,152 4,232,425 4,538,063

Total Liabilities and Stockholders Equity (calc) 1,644,211 1,801,300 5,877,200 6,053,516 6,308,068 6,588,339 6,865,785 6,870,097 6,195,165 6,565,586 6,950,635

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

19

Figure 8 Projected Cash Flows Optimistic Case

in thousands (except for per share amounts)

Source: Company Documents, Student Estimates

Cash Flow Calculations: Base 1 2 3 4 5 6 7 Terminal Yr.

Revenues:

Chlorvinyls 2,949,310 3,082,029 3,213,015 3,341,536 3,466,844 3,588,184 3,713,770 3,843,752

Aromatics 786,042 793,902 801,841 809,859 817,958 826,138 834,399 842,743

Building Products 894,648 948,327 1,005,227 1,065,541 1,129,473 1,197,241 1,269,075 1,345,220

-

Consolidated Revenues 4,630,000 4,824,258 5,020,083 5,216,936 5,414,275 5,611,563 5,817,244 6,031,715

% Increase 4.2% 4.1% 3.9% 3.8% 3.6% 3.7% 3.7%

Operating Income:

Chlorvinyls 173,565 369,843 385,562 400,984 416,021 430,582 445,652 461,250

Aromatics (1,197) 15,878 14,032 12,148 12,269 12,392 12,516 12,641

Building Products 36,442 47,416 50,261 53,277 56,474 59,862 63,454 67,261

Corporate and Intersegment Eliminations

Consolidated Operating Income 208,810 433,137 449,855 466,409 484,764 502,836 521,622 541,152

Operating Income % of Sales 4.5% 9.0% 9.0% 8.9% 9.0% 9.0% 9.0% 9.0%

Less: Corporate Expenses - - - - - - - -

Less: Restructuring and Other Costs 24,800 - - - - - - -

Operating Income 184,010 433,137 449,855 466,409 484,764 502,836 521,622 541,152

% Increase -50.4% 135.4% 3.9% 3.7% 3.9% 3.7% 3.7% 3.7%

% of Revenues 4.0% 9.0% 9.0% 8.9% 9.0% 9.0% 9.0% 9.0%

Less: Taxes (see below) (40,996) (135,788) (141,030) (146,219) (151,974) (157,639) (163,528) (169,651)

31.3% 31.4% 31.3% 31.4% 31.3% 31.3% 31.3%

Less: net income attributable to noncontrolling interest(3,333) (10,431) (10,828) (11,229) (11,921) (13,458) (14,852) (15,427)

After-tax Operating Income 139,681 286,918 297,997 308,961 320,869 331,739 343,242 356,074

+ Depr. & Amort. (incl. acquisitions) 226,765 232,604 243,151 253,690 264,184 274,594 285,441 296,743

- Capital Exp. (235,000) (242,755) (250,766) (259,041) (267,589) (276,419) (285,541) (294,964) Terminal

- Acquisitions Cost - - - - - - - - Growth %

- Ch. in NWC & other assets (from BS) 24,423 11,220 29,066 29,218 29,290 29,283 30,529 31,833 2.50%

Free Cash Flow 155,869 287,987 319,448 332,828 346,754 359,197 373,671 389,686 399,428

Terminal Value 5,594,232

=CF1/(r-g)

Present Value Calculations: Half-year convention 1 (1=yes, 0=no)

Free Cash Flow + Terminal Value 287,987 319,448 332,828 346,754 359,197 373,671 389,686 5,594,232

Cumulative Discount Factor Total 1.0403 1.1272 1.2243 1.3325 1.4534 1.5885 1.7398 1.8217

Present Value of Free Cash Flow 4,869,520 276,834 283,399 271,862 260,220 247,142 235,236 223,984 3,070,843

Plus: Total Debt Net of Excess Cash (861,902) 96,485

Less: Underfunded Pension Plan (11,300)

Less: Value of Noncontrolling Interest (122,982)

NPV less Noncontrolling Interest Value 3,873,336

# of Shares Outstanding 70,696

Value per Share 54.79$

Reflects that certain cash levels must be retained by corporation

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

20

Figure 9: Revenue and Margin Assumptions Optimistic Case

Source: Company Documents, Student Estimates

1 2 3 4 5 6 7

Actual Actual Actual Estimated Actual Actual Estimated

Revenues: 2011 2012 2013 2014 2012 2013 2014

Chlorvinyls 40.9% 40.4% 62.5% 63.7% 2.0% 116.9% 1.1% 4.5% 4.3% 4.0% 3.8% 3.5% 3.5% 3.5%

Aromatics 31.7% 33.2% 19.3% 17.0% 8.2% -18.6% -12.5% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

Building Products 27.4% 26.4% 18.2% 19.3% -0.8% -3.1% 5.3% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0%

Unallocated and Other

Consolidated Revenues 100.0% 100.0% 100.0% 100.0% 3.2% 40.3% -0.8%

Operating Income: Average

Chlorvinyls 8.9% 12.9% 14.1% 5.9% 10.4% 48.5% 135.9% -57.7% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0% 12.0%

Aromatics 1.0% 5.8% 3.2% -0.2% 2.5% 522.7% -54.9% -104.1% 2.0% 1.8% 1.5% 1.5% 1.5% 1.5% 1.5%

Building Products 0.8% 2.1% 0.4% 4.1% 1.8% 146.0% -83.7% 1114.7% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0%

0.0% 0.0% 0.0% 0.0% 0.0%

Consolidated Operating Income (Adjusted) 4.2% 7.7% 9.5% 4.5% 6.5% 90.3% 72.2% -52.8%

Check: Adjusted Net Income Amount

Corporate Expenses 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Asset Imp. & Transaction Costs Excl. Above 0.3% 0.6% 1.5% 0.5% 0.7% 79.7% 281.7% -65.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Depreciation and Amortization: Average

Chlorvinyls 4.6% 3.7% 6.2% 6.4% 5.2% -17.3% 262.9% 4.9% 6.2% 6.2% 6.2% 6.2% 6.2% 6.2% 6.2%

Aromatics 0.1% 0.1% 0.1% 0.2% 0.2% 3.4% -21.7% 55.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2%

Building Products 4.5% 4.4% 4.2% 3.9% 4.2% -3.1% -7.1% -2.4% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2% 4.2%

Unallocated and Other 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Consolidated Depreciation 3.2% 2.7% 4.7% 4.9% 3.9% -11.5% 142.6% 4.0%

Capital Expenditures:

Chlorvinyls 2.8% 3.3% 4.5% 5.4% 4.0% 20.7% 196.6% 19.8%

Aromatics 0.2% 0.2% 0.8% 1.1% 0.6% 64.9% 163.1% 19.8%

Building Products 2.7% 2.8% 5.2% 5.9% 4.2% 4.6% 78.0% 19.8%

Unallocated and Other 0.1% 0.2% 0.3% 0.3% 0.2% 106.9% 49.6% 19.8%

Consolidated Capital Expenditures 2.1% 2.4% 4.2% 5.1% 3.4% 21.0% 144.1% 19.8% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3%

Acquisitions -2.2% 0.0% 1.0% 0.0% -0.3% -100.0% -100.0%

Projected Operating Income Margins

Projected Depreciation as % of Revenue

% of Total Sales

% of Related Sales % Change

% Change

Projected Growth Rates

CFA Institute Research Challenge Axiall Corporation

Recommendation: Sell 1/22/2015

21

Figure 10 Income Statement Pessimistic Case

in thousands (except for per share amounts)

Source: Company Documents, Student Estimates

2011 A 2012 A 2013 A 2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E 2021 E

Revenues 3,222,884 3,325,836 4,666,000 4,630,000 4,738,433 4,842,035 4,940,348 5,032,950 5,119,459 5,207,677 5,297,644

Segment Operating Expenses 3,087,845 3,068,867 4,223,600 4,421,190 4,459,113 4,558,426 4,652,947 4,740,245 4,821,971 4,905,321 4,990,336

Restructuring and Other Costs 10,439 18,759 71,600 24,800 - - - - - - -

Operating Income 145,478 275,728 514,000 184,010 279,320 283,609 287,401 292,705 297,488 302,356 307,308

% Change in Operating Income 89.5% 86.4% -64.2% 51.8% 1.5% 1.3% 1.8% 1.6% 1.6% 1.6%

Operating Income from Income Statement 124,600 238,100 370,800 208,810 279,320 283,609 287,401 292,705 297,488 302,356 307,308

Other Income: OP % 3.9% 7.2% 7.9% 4.5% 5.9% 5.9% 5.8% 5.8% 5.8% 5.8% 5.8%

Interest Expense (65,600) (57,500) (77,600) (75,867) (63,329) (66,617) (69,615) (64,572) (30,674) (2,314) (2,399)

Other Income (Expense) (5,500) (2,900) (51,600) (8,611) (17,153) (17,153) (17,153) (17,153) (17,153) (17,153) (17,153)

Net Other Income (Expense) (71,100) (60,400) (129,200) (84,478) (80,482) (83,770) (86,768) (81,725) (47,827) (19,467) (19,552)

Income before Income Taxes 53,500 177,700 241,600 99,532 198,838 199,839 200,633 210,980 249,661 282,889 287,756

Provision for Income Taxes 4,200 (57,200) (73,600) (22,175) (62,336) (62,649) (62,898) (66,142) (78,268) (88,686) (90,211)

Less: net income attributable to noncontrolling interest - - (2,700) (3,333) (5,881) (5,911) (5,934) (6,240) (7,384) (8,367) (8,511)

Net Income 57,700 120,500 165,300 74,024 130,621 131,279 131,801 138,598 164,009 185,836 189,034

Net Income Per Share:

Basic 1.69 3.49 2.46 1.05 1.85 1.85 1.85 1.94 2.28 2.57 2.60

Diluted 1.69 3.46 2.44 1.05 1.84 1.84 1.84 1.92 2.26 2.55 2.58

% change in Diluted EPS 104.6% -29.6% -57.0% 75.6% 0.0% -0.1% 4.6% 17.7% 12.7% 1.2%

Diluted EPS without Restructuring 1.40 3.01

Weighted Average # of Shares: 1.40 1.84 1.84 1.84 1.92 2.26 2.55 2.58

Basic 34,100 34,500 67,300 70,196 70,547.1 70,899.8 71,254.3 71,610.6 71,968.7 72,328.5 72,690.1

Diluted 34,100 34,800 67,800 70,635 70,988.1 71,343.0 71,699.7 72,058.2 72,418.5 72,780.6 73,144.5

% change in Basic shares 1.2% 95.1% 4.3% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

Memo: Tax Rate -7.9% 32.2% 30.5% 22.3% 31.4% 31.3% 31.3% 31.3% 31.3% 31.4% 31.3%

Noncontrolling Interest % 0.0% 0.0% 1.6% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3% 4.3%