Embed Size (px)

Citation preview

The Payments Maze – Transformation in Enterprise Payments

sqs.com

WHITEPAPER

SQS – the world’s leading specialist in software quality

Authors: Pushpavaneswaran V (Senior Project Manager) Gunasekar M (Functional Consultant) Raajesh R (Lead Business Analyst) Sudarsan U (Lead Business Analyst) Raghunandhanan D (Lead Business Analyst)

SQS India BFSI Limited Published: August 2015

The Payments Maze – Transformation in Enterprise Payments 2

PUSHPAVANESWARAN VSenior Project [email protected]

Pushpavaneswaran, a qualified Chartered Accountant, has been with SQS since 2003. Senior Project Manager in the Cards and Payments practice, his core competencies include domain and test consulting, business analysis, pre-sales, documentation of business requirements and functional specifications, developing strategies for testing, and project management. He has worked with global clients including Morgan Stanley (UK), Citibank (Germany), GE (Indonesia) and Barclays (UK). He has managed the testing of large core banking applications such as Finacle, Flexcube and T24, and payments applications such as Global PayPlus for Emirates Bank, Mashreq Bank, Citibank Barclays Bank and FIS where key activities included the development of strategies for testing, test management, defect management, progress reporting, end-to-end testing, implementation support and managing multiple projects with more than 150 team members.

GUNASEKAR MFunctional [email protected]

Gunasekar Mani holds a bachelor’s degree in Mathematics and has been with SQS since 2005. Functional Consultant in the Cards and Payments practice, his core competencies include domain consulting, business analysis, pre-sales, understanding and documentation of business requirements and functional specifications, and development of strategies for testing. He has worked with global clients including Morgan Stanley (UK), GE (India), Lloyds, Barclays (UK), leading pay-ment processors First Data (EMEA) and s IT Solutions (Austria). He has participated in various large card and payment programmes/ projects as a Subject Matter Expert/Business Analyst, where key activities included analysis of business requirements, business processes, development of strategies for end-to-end testing of payments, and credit/debit card and loans processing across banking and financial software applications.

The Payments Maze – Transformation in Enterprise Payments 3

RAAJESH RLead Business [email protected]

Raajesh Rajamani is a certified PMP professional and holds a bachelor’s degree in Computer Science. With over 11 years of experience in the field of Banking and Financial Services at various levels, he has been with SQS since 2010. Currently a Lead Business Analyst in the Payments practice, his core competencies include business analysis, under-standing and documentation of business requirements and functional specifications and developing strategies for testing. He has worked with global clients including Citibank, AMEX and Barclays, and with regional leaders such as Al-Inma (KSA), Bank Muscat (Oman) and Erste Bank & s IT Solutions (Austria). He has participated in various payments programmes/projects as a Business Analyst, where key activities included analysis of business requirements, business processes, and development of end-to-end testing strategies.

SUDARSAN U Lead Business [email protected]

Sudarsan Uppilikannan holds a master’s degree in Business Adminis-tration. He has over 12 years of experience in the field of Cards & Payments operations and has been with SQS since 2007. Lead Business Analyst in the Cards and Payments practice, his core competencies include business analysis, pre-sales, understanding and documentation of business requirements and functional specifications and developing strategies for testing. He has worked with global clients such as Lloyds Banking Group and Barclays UK, and leading payment processors First Data (EMEA).

The Payments Maze – Transformation in Enterprise Payments 4

RAGHUNANDHANAN DLead Business [email protected]

Raghunandhanan Desikan holds a master’s degree in Computer Science and has over 14 years of experience in the field of Banking and Financial Services at various levels. He has been with SQS since 2011. Currently a Lead Business Analyst in the Payments practice, his core competencies include business analysis, pre-sales, under-standing and documentation of business requirements and functional specifications and developing strategies for testing. He has worked with global clients including Citibank (Indonesia, Singapore, UAE and UK), HSBC (Lebanon, Kuwait and UAE), Barclays (UK), BNP Paribas Fortis (Belgium) and Mashreq Bank (UAE and Bahrain). He has been involved in various payments programmes/projects as a Business Analyst, where key activities included analysis of business require-ments, business processes, and development of end-to-end testing strategies.

The Payments Maze – Transformation in Enterprise Payments 5

Contents

Management summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Introduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Key trends shaping payments industry. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1. Regulatory and external pressures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2. Internal and operational challenges faced by banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Transformation of payment processing & implementation of payment hubs . . . . . . . . . . . . . . . . . . . . . . . 11

Challenges in payments hub implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Challenges & risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Our recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

The Payments Maze – Transformation in Enterprise Payments 6

Management summary

Introduction

Growth in global payments is accompanied by a transformation in the payments infrastructure. The increase in non-cash transactions and technological advances giving rise to newer channels blurs the distinctions between payment types and methods. The payments industry is now at a crucial phase with the incumbent banks being challenged by non-banks providing payment processing services. The regulatory initiatives at various levels, competition among existing and new entrants, and the inherent inefficiencies within the legacy infrastructure are leading the banks down a path of transformation.

Payment hubs are increasingly seen as a solution to the complex problems that hinder the growth of the payments industry. Implementation of payment hubs is an expensive and multi-year initiative which needs to be clearly aligned to the business objectives of the bank initiating such a solution. This white- paper intends to cover the key trends, both external and internal, affecting the payments industry, and various approaches adopted in implementing pay-ment hubs.

Global payments are poised for substantial growth and transformation. 2013 witnessed banks handling $ 410 trillion in non-cash payments, over five times the global GDP. While growth rates and the payments mix (in terms of direct debit, credit transfers, cheques and cards) vary across regions, the overall global non-cash transaction volumes are expected to grow at a compound annual rate of almost 5 % over the next three years. With the continuing growth in the payments industry, the value of non-cash trans-actions is estimated to be around $ 780 trillion by 2023 with a CAGR of 7 %.

On the payments revenue side, Boston Consulting estimated that the payments business generated a revenue of over $1 trillion, amounting to a quarter of all banking revenues globally [1]. This is expected to reach $ 2.1 trillion in 2023, a CAGR of 8 %.

The payments space today is characterised by multiple initiatives at various levels. Over the last few decades, many countries have chosen to modify the settlement procedure employed by their interbank payments system with a view to reducing settlement risks and the potential for adverse system wide implications. Most central banks have opted for the implementation of Real Time Gross Settlement (RTGS) systems.

The World Bank Global Payment System Survey 2010 reported that 116 countries out of 139 (or 83 %) were using at least one RTGS (Real Time Gross Settlement) payments system as of December 2010. Nineteen new RTGS systems were implemented between 2007 and 2010 [2].

The Payments Maze – Transformation in Enterprise Payments 7

In the last five years, SWIFT has worked with a group of seven central banks to design a shared RTGS system back-up service which meets best practices, including tests of affordability, capacity, rapid implementation, minimal impact on users, geographical remoteness and technical diversity. Significant investments have been made by banks in Europe to comply with SEPA rules on credit transfers and direct debits.

The banks and payment service providers are being forced to look again at their payment processing infrastructures in order to maximise revenues, enhance operational efficiency to cut costs, and

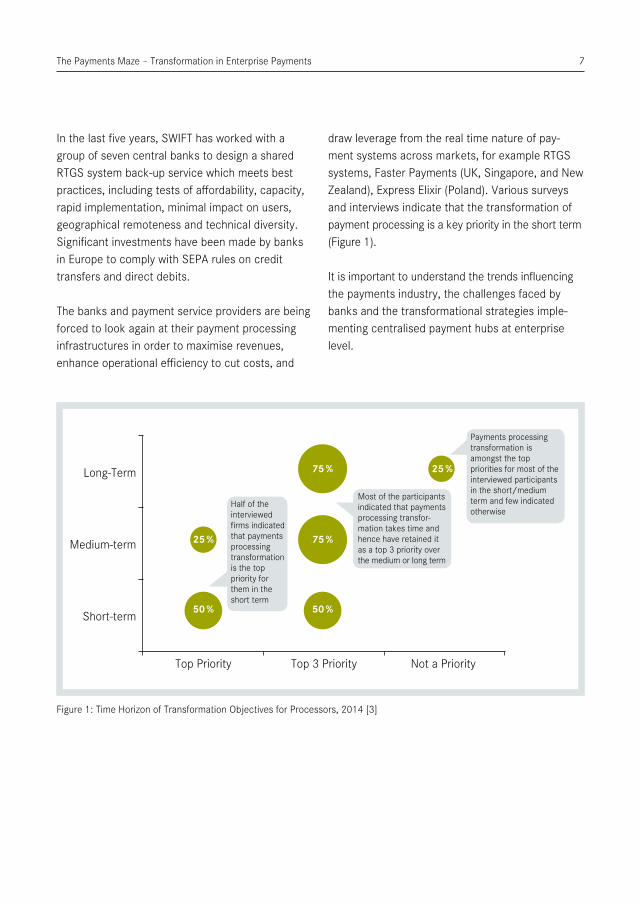

draw leverage from the real time nature of pay-ment systems across markets, for example RTGS systems, Faster Payments (UK, Singapore, and New Zealand), Express Elixir (Poland). Various surveys and interviews indicate that the transformation of payment processing is a key priority in the short term (Figure 1).

It is important to understand the trends influencing the payments industry, the challenges faced by banks and the transformational strategies imple-menting centralised payment hubs at enterprise level.

Figure 1: Time Horizon of Transformation Objectives for Processors, 2014 [3]

Long-Term

Medium-term

Short-term

Top Priority

25 % 75 %

75 % 25 %

50 % 50 %

Top 3 Priority Not a Priority

Half of the interviewed firms indicated that payments processing transformation is the top priority for them in the short term

Most of the participants indicated that payments processing transfor-mation takes time and hence have retained it as a top 3 priority over the medium or long term

Payments processing transformation is amongst the top priorities for most of the interviewed participants in the short/medium term and few indicated otherwise

The Payments Maze – Transformation in Enterprise Payments 8

Key trends shaping payments industry

The key trends shaping the payments landscape include regulatory initiatives and oversight across markets, technological innovations, emerging payment types and channels, entry of new players into the payment processing service, and pricing pressures due to competition. Apart from the chal-lenges related to these external factors, banks and financial institutions are weighed down by the in- efficiencies in their payment processing. Thus, the trends can be broadly classified at two levels:

• Regulatory and external pressures

• Internal and operational challenges faced by banks

1. Regulatory and external pressures

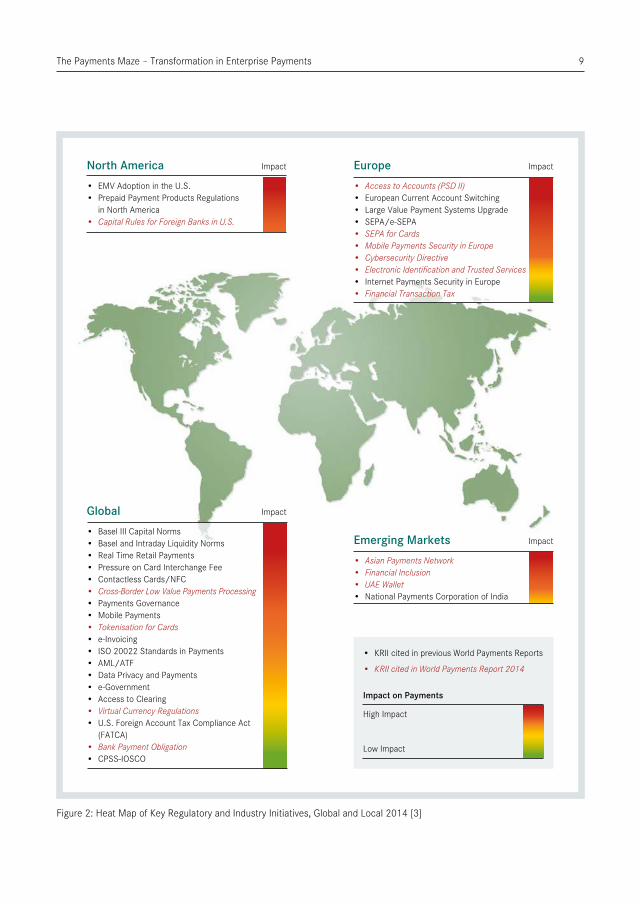

The payments industry now has to grapple with multiple regulatory initiatives at national, regional and global levels. The regulatory initiatives cover Internet payment security, mobile payment security and data privacy. There is an increasing focus on anti-money laundering (AML) and anti-terrorism financing (ATF) regulations involving both domestic and cross-border payments (Figure 2).

Emerging payment types and converging channels (physical, electronic and mobile) add pressure on the banks to provide innovative products and focus on customer experience and consistency across channels. With the new channels, the lines between payment types and methods are becoming blurred,

for example, mobile payment transactions are funded by a variety of means including credit, debit and prepaid cards. And because the vast majority of mobile payments currently flow over card rails, there is increasingly no difference between a mobile payment and a plastic card payment at the point of sale. Mobile wallets bury the details of the cards they contain once the payment credentials have been loaded. Further complicating the environ- ment is the rise of virtual payments. Virtual currencies such as Bitcoin are taxable in Germany.

The entry of non-banking players into payment ser-vice processing has led to innovation and increased competition which further leads to pricing pressure. Examples of non-banking retail players include Boku, Square, iZettle and M-Pesa, while players on the corporate side include Odette, Coface and SWIFT.

Innovation operates as both cause and effect with regard to technological changes and the entry of newer players into payment processing. While retail customers want anytime, anywhere payments using a choice of payment instruments, corporate cus-tomers want improved control, visibility and speed in processing payments. The competition among the incumbent and new players has led to further pricing pressures.

The internal and operational challenges faced by banks in processing payments are explained in the next section.

The Payments Maze – Transformation in Enterprise Payments 9

Figure 2: Heat Map of Key Regulatory and Industry Initiatives, Global and Local 2014 [3]

North America Impact

• EMV Adoption in the U.S.• Prepaid Payment Products Regulations

in North America• CapitalRulesforForeignBanksinU.S.

Europe Impact

• AccesstoAccounts(PSDII)• European Current Account Switching• Large Value Payment Systems Upgrade• SEPA/e-SEPA• SEPAforCards• MobilePaymentsSecurityinEurope• CybersecurityDirective• ElectronicIdentificationandTrustedServices• Internet Payments Security in Europe• FinancialTransactionTax

Impact on Payments

High Impact

Low Impact

• KRII cited in previous World Payments Reports

• KRIIcitedinWorldPaymentsReport2014

Global Impact

• Basel III Capital Norms• Basel and Intraday Liquidity Norms• Real Time Retail Payments• Pressure on Card Interchange Fee• Contactless Cards/NFC• Cross-BorderLowValuePaymentsProcessing• Payments Governance• Mobile Payments• TokenisationforCards• e-Invoicing• ISO 20022 Standards in Payments• AML/ATF• Data Privacy and Payments• e-Government• Access to Clearing• VirtualCurrencyRegulations• U.S. Foreign Account Tax Compliance Act

(FATCA)• BankPaymentObligation• CPSS-IOSCO

Emerging Markets Impact

• AsianPaymentsNetwork• FinancialInclusion• UAEWallet• National Payments Corporation of India

The Payments Maze – Transformation in Enterprise Payments 10

2. Internal and operational challenges faced by banks

The critical challenge faced by banks in processing payments is closely linked to the evolution of the legacy IT infrastructure. The legacy infrastructure is based on siloed implementation (e.g. separate sys-tems for low value payments, high value payments, cross-border payments, corporate payments, card payments, etc.). From an operations perspective, each of the payment types – cheques, ACH payments, domestic and cross-border credit transfers, debit and credit cards – are managed as separate products. It is not uncommon to see a completely separate infrastructure within banks to handle international funds transfers or cross-border payments.

The legacy systems were not built to handle present day volumes, changing regulatory requirements and integration with the newer channels.

Added to the above, banks have undergone signifi-cant mergers and acquisitions, resulting in multiple systems and operational divisions even for the same product. Operations are further complicated with the external pressures related to regulatory compliance, customer-facing channels and servicing activities.

The net effect of all this has resulted in

• Duplication of infrastructures

• Limited capabilities in applying Straight Through Processing (STP)

• Heavy reliance on manual operations

• Inability to support volumes

• Lack of visibility and transparency in processing payments and

• Delayed response to market demands

In turn, this leads to customer dissatisfaction and escalation of costs. According to the Boston Consulting Group, although banks generate 35 % of all revenue through payments, they also incur 40 % of their total costs this way. Many banks are struggling to cope both with external pressures, and with the fact that the legacy infrastructure and its inherent inefficacies in processing payments are inhibiting the growth of business. This is forcing banks to think about their payments operations in terms of profitability and cost management.

The Payments Maze – Transformation in Enterprise Payments 11

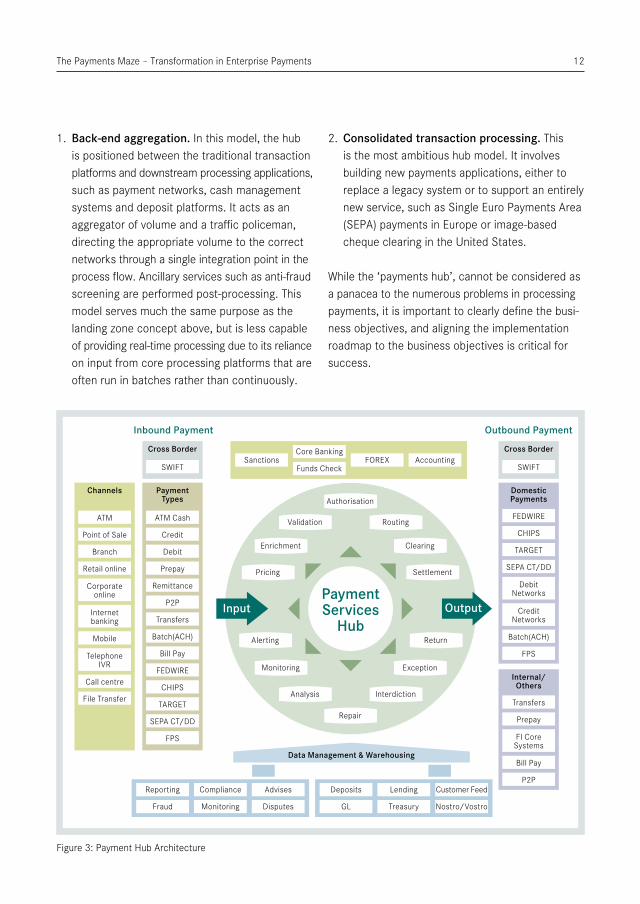

As banks recognise the strategic value of pay-ments, the focus on attaining operational efficiency through the implementation of payment hubs is be-ing seen as the solution. While definitions of what constitutes a ‘Payment Hub’ vary, it can be seen as the infrastructure that ties together the specialised services required to build payments applications, such as data completion, exception handling and settlement. There are also ancillary services, such as anti-fraud screening, risk management and dis-pute resolution. Thus, payment hubs are packaged solutions with pre-built components enabling banks to integrate and orchestrate payment flows from channels and back office systems in a centralised infrastructure.

A Mercator study in 2010 – Payment Hubs: Shrinking the Elephant [4] described the main characteristics of a payment hub as:

1. Highly flexible

2. Agnostic to payment type or form

3. Interactive --capable of normalising and aggregating data

4. Built on an open architecture framework

Figure 3 represents a typical payment hub architecture.

Payment service hubs are expected to become the dominant architecture in the payments industry. During the last 5 years, many large banks have embarked upon implementation of payment hubs in various forms. Payment hub implementations are large, expensive and multi-year projects. There are multiple products offering payment service hub

solutions – FundTech’s Global PayPlus, Clear2Pay (FIS’s) Open Payment Framework, Dovetail Payments Framework, Logica All Payments Solution (LAPS) and Misys’s Payment Manager, to name a few. A Celent study in 2011 noted that over 40 % of all payment service hub implementations, live and on-going, were based at the large financial institutions with assets exceeding $ 100 bn. 72.6 % of all PSH implementations were within Western and Northern Europe, North America and Canada [5]. Furthermore, in a 2014 report it was noted that, ‘there are now nearly three times more live payment services hubs globally. The nine vendors reported growth from 46 live systems in 2010 to an estimated 119 at the end of 2013’ [6]. Many more payment service hub implementations are reported to be underway.

As there are a number of solutions falling under the banner of ‘payments hub’, their implementation strategies vary with the objectives of the bank. The McKinsey June 2010 report indicates three broad categories based on how they fit into the overall payment architecture of the bank [7].

1. Front-end landing zone. Here, the payments hub sits between the front-end channels (e.g., online banking, ATM, treasury management workstation, branches) and the traditional transaction platforms such as the ACH, cheque-processing platforms, wire, etc. This single integration point replaces the multiple interfaces required by the conventional approach. The hub also aggregates data that can be fed into ancillary systems, such as fraud, risk, marketing, reporting, balance and reconcilement, and data analytic applications.

Transformation of payment processing & implementation of payment hubs

The Payments Maze – Transformation in Enterprise Payments 12

1. Back-end aggregation. In this model, the hub is positioned between the traditional transaction platforms and downstream processing applications, such as payment networks, cash management systems and deposit platforms. It acts as an aggregator of volume and a traffic policeman, directing the appropriate volume to the correct networks through a single integration point in the process flow. Ancillary services such as anti-fraud screening are performed post-processing. This model serves much the same purpose as the landing zone concept above, but is less capable of providing real-time processing due to its reliance on input from core processing platforms that are often run in batches rather than continuously.

2. Consolidated transaction processing. This is the most ambitious hub model. It involves building new payments applications, either to replace a legacy system or to support an entirely new service, such as Single Euro Payments Area (SEPA) payments in Europe or image-based cheque clearing in the United States.

While the ‘payments hub’, cannot be considered as a panacea to the numerous problems in processing payments, it is important to clearly define the busi-ness objectives, and aligning the implementation roadmap to the business objectives is critical for success.

Channels

ATM

Point of Sale

Branch

Retail online

Corporate online

Internet banking

Mobile

Telephone IVR

Call centre

File Transfer

Payment Types

ATM Cash

Credit

Debit

Prepay

Remittance

P2P

Transfers

Batch(ACH)

Bill Pay

FEDWIRE

CHIPS

TARGET

SEPA CT/DD

FPS

Domestic Payments

Internal/ Others

FEDWIRE

Cross Border

SWIFT

Cross Border

SWIFT

Sanctions

Funds CheckFOREX Accounting

Core Banking

Monitoring DisputesFraud

Compliance AdvisesReporting

Treasury Nostro/VostroGL

Lending Customer FeedDeposits

Transfers

CHIPS

Prepay

TARGET

FI Core Systems

SEPA CT/DD

Bill Pay

Debit Networks

P2P

Credit Networks

Batch(ACH)

FPS

Outbound PaymentInbound Payment

Authorisation

Validation

Analysis

Enrichment

Monitoring

Pricing

Alerting

Routing

Interdiction

Clearing

Exception

Settlement

Return

Repair

Input OutputPayment Services

Hub

Data Management & Warehousing

Figure 3: Payment Hub Architecture

The Payments Maze – Transformation in Enterprise Payments 13

Challenges in payments hub implementation

The need for transformation in the payments proces-sing infrastructure is acutely felt by institutions as they recognise the inefficiencies in the current systems and processes. However, such transformation exer-cises are fraught with many challenges and risks.

Challenges & risks

• Lack of documentation related to the legacy applications and manual processes

• Identification of redundant processes due to the complexity in the existing operations as a result of past merger and acquisition activities

• Dependency on

◦ Numerous landscape applications (e.g., funds control/core banking, sanctions, AML, forex, accounting, statements, reporting) and impact assessment on the interfaces due to the intended changes

◦ Initiatives involving individual applications – e.g., replacement of/upgrades to banking applications or implementation of AML applications

• Addressing regulatory concerns at various levels – domestic, regional, international

The client was a UK-based global banking group operating in over 50 countries. A few years ago, the bank embarked upon implementing a central- ised payment hub solution based on industry-leading FundTech’s solution, Global PayPlus. In the US, its corporate high value payments (HVP) processing was outsourced to another bank. SQS helped the bank with its in-house testing of the migration of US HVP to the Global PayPlus platform. The migration encompassed numerous landscape applications including sanctions, funds control, FX and accounting for payments involving SWIFT, FEDWIRE and CHIPS schemes. The migration programme spanned 20 months. Extensive testing by SQS involved 14,000+ messages (SWIFT, FEDWIRE & CHIPS). The migration programme went live and the bank currently processes over 30,000 payments a day with a value of US $ 350 billion, without any issue.

SQS has also supported the bank in implement-ing MassPay functionality, involving SEPA Credit Transfer and SEPA Direct Debit, on the Global PayPlus platform. The MassPay programme went live recently after 24 months of testing across multiple phases. Extensive testing by SQS with over 53,000+ XML messages covered all rele-vant message types: ISO 20022 XML messaging standard compliant with EBA – PACS, PAIN & CAMT. MassPay implementation enabled the bank to participate in the SEPA Direct Debit system and is in turn expected to deliver over £35m of benefits in the next 4 years.

SQS’s contribution to the above programmes has been highly appreciated by the bank.

Live Example

The Payments Maze – Transformation in Enterprise Payments 14

Our recommendations

As payment processing is critical at enterprise level, transformational programmes involving the core systems will have to be carefully planned and executed. As many large financial institutions have either successfully implemented or are in the process of implementing payment service hubs, some of the key lessons learnt from such payment infrastructure transformation programmes are given below,

• Avoid a ‘big bang’ approach in implementing payment service hubs – a phase-wise implemen-tation is suggested, considering the payment types, channels and geographies

• Align the implementation programme to busi-ness objectives, for example,

◦ Increased STP rates

◦ Harmonization of payment products

◦ Flexible integration with channels

◦ Compliance with regulatory initiatives like SEPA

• Prioritisation of business objectives and trans-formational activities in tune with objectives

Conclusion

References

As payment hub implementations are ‘large, expensive and multi-year’ initiatives involving all payment types and all aspects of payments pro-cessing, comprehensive testing assumes a greater significance. A crucial factor is the capability of the

testing partner who can bring extensive knowledge of the payments domain, understanding of payment systems, messaging standards, regulatory require-ments and business processes, combined with rigorous testing standards.

[1] The Boston Consulting Group (2014). Global Payments 2014 – Capturing the next level of value.

[2] The World Bank (2011). Payment Systems Worldwide – A Snapshot – Outcomes of the Global Pay-ment Systems Survey 2010.

[3] Capgemini, RBS (2014). World Payments Report 2014.

[4] Mercator Advisory Group (2010). Payment Hubs: Shrinking the Elephant.

[5] Z. Bareisis (2011). Understanding Payment Services Hubs. Celent Webinar

[6] http://www.celent.com/reports/payment-services-hubs-revisited-lessons-learned

[7] McKinsey on Payments (2010). Payment Hubs: Redefining the industry’s infrastructure.

The Payments Maze – Transformation in Enterprise Payments 15

© SQS Software Quality Systems AG, Cologne 2015. All rights, in particular the rights to distribution, duplication, translation, reprint and reproduction by photomechanical or similar means, by photocopy, microfilm or other electronic processes, as well as the storage in data processing systems, even in the form of extracts, are reserved to SQS Software Quality Systems AG.

Irrespective of the care taken in preparing the text, graphics and programming sequences, no responsibility is taken for the correctness of the information in this publication.

All liability of the contributors, the editors, the editorial office or the publisher for any possible inaccuracies and their consequences is expressly excluded.

The common names, trade names, goods descriptions etc. mentioned in this publication may be registered brands or trademarks, even if this is not specifically stated, and as such may be subject to statutory provisions.

SQS Software Quality Systems AGPhone: +49 2203 9154-0 Fax: +49 2203 [email protected] | www.sqs.com