Embed Size (px)

Citation preview

White Paper

Enabling innovation

through paymentsplatform

transformation

Table of content 3 Executive summary

4 Introduction

5 Key market drivers to support payments platform transformation

5 The demand for instant and cross-border payments

6 The compliance burden

7 The pressure on margins

7 The increase in competition

7 The impact of innovative technologies

8 Back-end platforms as enablers of front-end innovation

9 A core concern

9 Unlocking the legacy

9 Payments platform transformation

10 Considering the options

12 Selecting the right partner – and solution

13 Conclusion

Enabling innovation through payments platform transformation2

Navigating these uncharted waters, banks are challenged on their traditional value chain by two driving forces: one is the struggle for banks to retain customer relations through innovative front-end services in an environment where both challenger banks and tech giants are vying for the end-users’ attention; the other is the demand for increased efficiency and scalability as a way of lowering costs of non-differentiating operations in the back-end. Dealing with these forces, banks need a payments solution that:

• is flexible enough to handle different payment types and adapt to future needs

• enables modern open connectivity options for sending, receiving and sharing data (through informed consent) with clients, suppliers, networks, and partners

• delivers 24/7 capabilities as a global and connected world demands systems to be available always

• improves time-to-market for new products and services• supports compliancy with current and future regulations• is scalable for large transaction volumes without a

negative cost impact• enables them to extract valuable analytics from

transactional data• delivers economies of scale through the bundling of

transactions across several parties

However, expenditures for maintaining and upgrading existing IT infrastructure are limiting the resources banks can devote to innovation and investments in new digital technologies – effectively driving the need for banks to pursue alternative options.

To thrive, banks need a clearly defined strategy that focuses either on front-end initiatives or back-end operations for leveraging scale and volume, as maintaining both at par and excelling in one is difficult to achieve on their own. In the first scenario, it would make sense for banks to lower back-end costs and leverage scale through sourcing of payments operations to a third party. In the second scenario, it could make sense for them to become platform players at the back-end themselves and then work with fintechs on front-end innovation. For this second scenario to play out, these banks would need to attract transaction volumes from other banks or third parties to achieve sufficient cost-benefits to be competitive.

In this white paper, we examine how a rapidly changing financial environment is urging banks to rethink their business strategies and back-end operations. We also present a string of key elements and options for banks to consider when driving the necessary change to their payments platforms.

Executive summaryToday, global trends including changing customer demands, new entrants, innovative technologies,

regulatory pressure, higher costs and lower profit margins are driving significant changes to the financial services market. A post-recession economy has tightened regulations and increased

compliance costs for financial institutions, while initiatives like PSD2 have opened up the financial market to innovative competition. In the wake of rapidly evolving customer expectations, new digital standards for financial services are now increasingly being met by a wave of agile fintech companies

which leverage technological advances to enhance customer experiences.

Enabling innovation through payments platform transformation 3

This need is driven by a series of correlated external trends in the financial markets, and indeed society – most of these are motivated by increasing customer expectations as well as by technological advancements. But it is further complicated

by the internal challenges of conservative banking cultures and archaic legacy systems, which are exhausting IT budgets while making it difficult for banks to accommodate modern client needs. In most cases, banks are relying on individual craftsmen

(and women) who can cut, carve and wedge the various components of the legacy systems to fit into others.

Against this backdrop, many banks are still trying to understand how to best adapt to a new digital era of banking. What strategy should they use to address the key challenges of the industry – and where should they begin

the modernization process? Is a new front-end what is needed or should banks consider even more fundamental changes to their back-end operations?

The following chapters present the thought process and options of banks

which aim for long-term success in a new financial reality.

IntroductionFollowing the rational approach to standardization in the old economy, modern banks are facing a similar need to streamline their operations and free up resources to produce quality products

that will help them stand out from their competition.

Enabling innovation through payments platform transformation4

Key market drivers to support payments platform transformation

“I can’t change the direction of the wind,

but I can adjust my sails to always reach my destination.” Jimmy Dean

In an effort to balance short-term growth with long-term strategic transformation, banks grapple with a multitude of challenges, including: complex regulations, margin pressures, increased competition, innovative technologies, and the demand for instant payments and more efficient cross-border payments.

The following section describes the key market drivers that are affecting the financial services industry and banking in particular.

The demand for instant payments and more efficient international payments

The steep rise in demand for real-time, cross-border payments across sectors provide banks with an opportunity to pursue internal payments restructuring.

Instant payments In many European countries, banking and banking services have a history of being very “sector-driven”, with little or no differentiation on standard services like payments. As banks are beginning to realize the value of enhanced payment services like instant payments as part of their “license to operate”, the inability of legacy systems to incorporate new instant payment infrastructures is becoming a significant threat to their survival. And looking ahead, it is becoming increasingly clear how the major trends of today are evolving into de facto standards of tomorrow.

More and more countries around the world have implemented real-time payment schemes, while others are planning to launch them in the near future. Also, regional cross-border real-time systems like the European real-time payment solution, SCT Inst, are expected to gain traction and define the future of payments.

Please state your level of agreement with the following statements about lmmediate payments

2018 2017

Proportion of respondents that agree with the statement

We are developing/interested in new services for consumers based on immediate payments

Payments via immediate payments will improve my customer service

lmmediate payments will drive revenue growth for my organization

We are developing/interested in new services for SMEs based on immediate payments

lmmediate payments will save my organization money

The business case for investing immediate payments is weak

I see no benefits in immediate payments

I have never heard of immediate payments

0% 20% 40% 60% 80% 100%

88% 56%

86%61%

85%53%

79%50%

78%60%

49%39%

16%6%

10%12%

Source: 2018 Ovum Global Payments Insight Survey

Growing adoption and new roadmaps in all regions have increased the interest by retail banks for instant payments

Enabling innovation through payments platform transformation 5

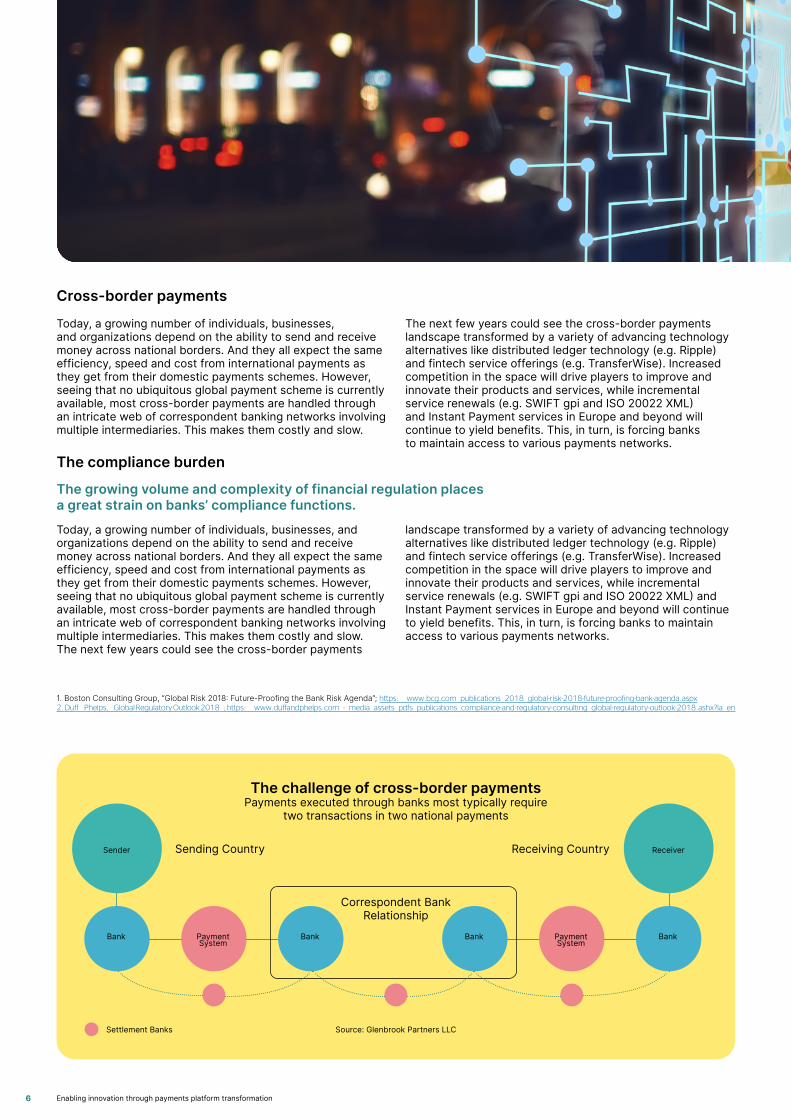

The challenge of cross-border payments Payments executed through banks most typically require

two transactions in two national payments

Sending Country

Correspondent Bank Relationship

Receiving Country Sender

Bank BankPayment System

Receiver

Bank BankPayment System

Source: Glenbrook Partners LLCSettlement Banks

Cross-border payments

Today, a growing number of individuals, businesses, and organizations depend on the ability to send and receive money across national borders. And they all expect the same efficiency, speed and cost from international payments as they get from their domestic payments schemes. However, seeing that no ubiquitous global payment scheme is currently available, most cross-border payments are handled through an intricate web of correspondent banking networks involving multiple intermediaries. This makes them costly and slow.

Today, a growing number of individuals, businesses, and organizations depend on the ability to send and receive money across national borders. And they all expect the same efficiency, speed and cost from international payments as they get from their domestic payments schemes. However, seeing that no ubiquitous global payment scheme is currently available, most cross-border payments are handled through an intricate web of correspondent banking networks involving multiple intermediaries. This makes them costly and slow. The next few years could see the cross-border payments

landscape transformed by a variety of advancing technology alternatives like distributed ledger technology (e.g. Ripple) and fintech service offerings (e.g. TransferWise). Increased competition in the space will drive players to improve and innovate their products and services, while incremental service renewals (e.g. SWIFT gpi and ISO 20022 XML) and Instant Payment services in Europe and beyond will continue to yield benefits. This, in turn, is forcing banks to maintain access to various payments networks.

1. Boston Consulting Group, “Global Risk 2018: Future-Proofing the Bank Risk Agenda”; https://www.bcg.com/publications/2018/global-risk-2018-future-proofing-bank-agenda.aspx 2. Duff / Phelps, /Global Regulatory Outlook 2018/; https://www.duffandphelps.com/-/media/assets/pdfs/publications/compliance-and-regulatory-consulting/global-regulatory-outlook-2018.ashx?la/en

The growing volume and complexity of financial regulation places a great strain on banks’ compliance functions.

The compliance burden

The next few years could see the cross-border payments landscape transformed by a variety of advancing technology alternatives like distributed ledger technology (e.g. Ripple) and fintech service offerings (e.g. TransferWise). Increased competition in the space will drive players to improve and innovate their products and services, while incremental service renewals (e.g. SWIFT gpi and ISO 20022 XML) and Instant Payment services in Europe and beyond will continue to yield benefits. This, in turn, is forcing banks to maintain access to various payments networks.

Enabling innovation through payments platform transformation6

The pressure on margins

The strategic response by banks to the pressure on margins should be increased efficiency of payment processing to reduce costs.

In the past, banks’ intuitive and logical response to margin pressures has been to steer the strategic focus away from low or zero profit margin products like payments and focus on more profitable banking products like lending and investments. Low revenue combined with increasing operational and compliance costs has led to payments getting gradually handed over to card schemes and payment processors to commercialize. For many years, these players have focused on increasing efficiency through scale and thereby driving down costs by increasing the transaction volume. This more infrastructural approach has not been seen by the banks as a direct threat to their core business. But the threat is real, as some of these players are now starting to address the consumer market directly, which potentially puts them in competition with the banks – not for services delivered, but for the consumers’ attention.

The increase in competition

If banks focus on creating an open banking economy, they can better mitigate the threat of disintermediation from new fintech entrants, challenger banks and also the tech giants outrunning them on innovation speed and time-to-market capabilities.

With the introduction of PSD2 in Europe, traditional banks are being pushed to open their data pools and account-based payments capabilities to third-party providers. These companies are typically better at delivering innovative financial solutions at a faster pace because they have the distinct advantage of being unburdened by complex legacy systems and processes. Challenged by conditions of high costs for customer acquisitions, tightened regulations, and the continual threat of becoming irrelevant to customers, banks must decide how best to accelerate innovation and time-to-market capabilities, either through partnerships, acquisitions, or internal initiatives. Most banks choose a combination. Moving from a more competitive perspective, both banks and fintechs are beginning to realize the benefits of collaboration – or co-innovation. To this end, the industry is experiencing a synergetic effect where banks are leveraging the knowledge, technology, and resources of fintech companies to fast-track new innovative products and engage high-demanding customers. Conversely, fintechs are leveraging the banks’ infrastructure, key capabilities, broad client base, and capital. Within this context, it is imperative that banks collaborate with fintechs with differential capabilities that will set them apart in a competitive industry.

Moving from a more competitive perspective, both banks and fintechs are beginning to realize the benefits of collaboration – or co-innovation. To this end, the industry is experiencing a synergetic effect where banks are leveraging the knowledge, technology, and resources of fintech companies to fast-track new innovative products and engage high-demanding customers. Conversely, fintechs are leveraging the banks’ infrastructure, key capabilities, broad client base, and capital. Within this context, it is imperative that banks collaborate with fintechs with differential capabilities that will set them apart in a competitive industry.

The impact of innovative technologies

Huge advances in technology innovation are transforming the very core of financial services, challenging banks to reassess their front- and back-end platform architecture.

To improve efficiency, security standards and reliability of operations while reducing costs significantly, banks are expected to explore the following disruptive technologies such as APIs, machine learning and predictive analysis, robotics and distributed ledger technology. Application Programming Interfaces (APIs) In the continuous quest to enhance customer experiences, open APIs provide banks and fintech companies with the opportunity to leverage complementary strengths and deliver customized services across the banking ecosystem.

Machine learning and predictive analytics As more and more data become accessible through the APIs, more sophisticated tools are needed to analyze and derive value from it. Machine-learning and predictive analytics are becoming key drivers for both customer facing services, as well as for fraud monitoring and analytics.

Robotic Process Automation (RPA) With an increasing amount of data, analytics, services and integrations more advanced process handling is needed to reap the full benefits of the technology and to offer improved Straight Through Processing (STP) as well as automated response to e.g. fraud alerts.

Distributed Ledger Technology (DLT) While still in the early stages of adoption, blockchain technology and distributed ledger systems have demonstrated clear potential for the optimization of processes and operations that involve decentralized networks, such as capital markets, trade finance, cross-border payments, and transaction banking. While the initial expectations from certain groups for total disruption of financial services as we know them did not happen, DLT will surely be a force to be reckoned with going forward.

Enabling innovation through payments platform transformation 7

Back-end platforms as enablers of front-end innovation

“There is no way you can survive in a globalised

internet economy with systems that are built for batch overnight updates – it is ridiculous”

Chris Skinner

In today’s changing payments landscape, banks are subject to many forces affecting their business. There is a fundamental shift in the understanding of the role of a bank from storing, moving and lending money to a more service-driven entity that tailors for individual customers’ needs. This challenges the

traditional value-chain of bank products. Two major forces play different parts of the value chain: 1) the struggle for banks to retain customer relations through the front-end services where both challenger

banks and the tech giants compete for the end-users’ attention and 2) in the back-end where the pressure for increased efficiency leads to demand for scalability and cost reductions.

Across these two factors is a constant pressure on banks to comply with the ever-increasing regulatory requirements presented at both ends of the value chain, as outlined in the previous chapter. And finally, banks are challenged by monolithic and inflexible legacy systems that impede their ability to:• increase scale to reduce costs of operating core systems• leverage the innovation of fintechs through (open) APIs• deliver 24/7 domestic and cross-European (eventually

global) real-time payment processing• perform flexible payment process orchestration• ensure faster time-to-market for new products

In addition, a number of interrelated large-scale movements are transforming payments and are forcing banks to reconsider their strategies and platforms. Some examples:• mature domestic markets turning global and increasingly

competitive• Continued growth in electronic transactions across

channels and borders• a growing number of real-time payment systems going live• the commoditization of payments that makes it difficult

(and even irrelevant) for customers to tell banks apart• the further industrialization of payment processing on a

global scale• substantial costs and capital expenditure allocated to non-

differentiating payment infrastructures

Enabling innovation through payments platform transformation8

A core concern

Against this backdrop, banks are understandably concerned about the growth of their business in a future digital economy. And concerns point to one core issue: the challenge of outdated legacy systems. A significant 71% of respondents surveyed by Finextra in late 2017 agreed or strongly agreed that existing systems are the biggest inhibitor of necessary payments transformations1. A 2018 Accenture survey supports this trend, with two-thirds of bank operations leaders being convinced that customer insights, which could be used to improve future products, enhance services and support innovative initiatives, are not fully utilized due to dated core systems and convoluted processes2.

Unlocking the legacy

Unlike data-driven fintech companies which have organized themselves around customer needs, the challenge for banks in Europe and North America is that legacy infrastructure ties data to product and process silos. This backwards

maneuver is putting a strain on their budgets, and a tier one bank could easily spend up to USD 300 million a year – or around 80% of its IT budget – on existing software that needs constant updates to meet regulatory requirements3. Such disproportionate prioritizing of resources is not only costly, it is also affecting the banks’ ability to innovate at speed and perform necessary data analytics needed for both service development and product innovation.

As most banking services are transactional, the data generation is substantial and continuous. Yet few banks have tapped into the value that the transaction data holds.

The focus has been on core systems to serve mission-critical functions like deposits, accounting, lending, policy administration, and payments processing – which they do in a secure, reliable and resilient way – and hence, banks are not looking to discontinue control over their core systems completely. But to stay competitive and relevant, rather than ‘just compliant’, banks need to find a way to ‘refresh and extend’ these backbone systems so that new digital platforms and technologies can connect to and utilize the immense value in transactional data they possess.

Key characteristics Differentiation,

new revenue streams & deliver excellent

digital services

Race for scale and best price

Key characteristics Commoditization, standardization, industrialization & globalization

War on customer relation

1. Finextra, “Payments transformation: Modernising to stay relevant in the digital age.”; www.finextra.com/finextra-downloads/surveys/documents/ 2. Accenture, “Back-office, it’s time to meet the customers”; www.accenture.com/t20180404T034515Z//w///us-en//acnmedia/PDF-72/Accenture-2018-North-America-Banking-Operations-Survey.pdf/zoom/50 3. www.fnlondon.com/articles/banks-face-spiraling-costs-from-archaic-it-2017091

Enabling innovation through payments platform transformation 9

Payments platform transformation

“It is not the strongest of the species that survives, nor the most intelligent that survives.

It is the one that is most adaptable to change” Charles Darwin

Digital payments –transactions that do not involve physical cash or cards – are on the rise. The total transaction value of digital payments in Europe is expected to show an annual growth rate of

10.5%, resulting in the total amount of more than USD 1 trillion by 20221. Apart from new and exciting opportunities, this growth rate also brings considerable risks to banks. Because if they fail to compete in the digital payments arena, they will surely lose shares to fintech companies. And seeing that banks rely strongly on the continuous relationship and dialogue with customers that can only be maintained

through higher frequency interaction like payments, any reduction in payments interaction is bad news for the banks as it will have a domino effect on the rest of their business.

Considering the options Updating the payments platform is a huge undertaking with considerable implications for the bank’s IT infrastructure, processes, human resources, costs structures and models etc. This is why banks should always take the time to reflect on their current needs and future business requirements before making any definitive decision on the matter. For instance, to what extent are banks looking for a short-term fix (such as middleware software that can translate between existing systems and databases) or a long-term strategic solution that will be able to change with the market? And how are the added functionalities expected to support any technological, business, and strategic visions?

There are a number of different approaches with various pros and cons to consider.

1. Upgrading existing system

This option speaks to those banks that know what they have, and like to stay in full control. The main benefits of this approach are definitely the high degree of familiarity associated with working with the same vendor and the fact that a bank does not need to make any upfront investment in the area of new software and solutions. That being said, bearing in mind the inherent issues of running and maintaining existing legacy systems, this approach might

very well turn out to be costlier in the long run. Additionally, in the process of applying additional functionalities to old systems, it might be difficult to employ the right resources for the job. Developers with an expert understanding of the original system, e.g. Cobol, can be hard to find as many of them have retired and very few in the younger generation of IT developers have learned these (archaic) programming languages.

2. Building in-house

One advantage of a built-in solution is that it enables a bank to remain in full control of every aspect of the development while ensuring that the new system can be integrated with other adjacent in-house solutions. And banks can use most modern technology for this. However, building a custom payment processing system in-house is very costly, and it does not remove any of the present or future maintenance, compliance or improvement costs associated with keeping such a system running and competitive. Furthermore, the proliferation of services means that banks will have a hard time retaining enough people to cover all the skills needed to do everything in-house. Finally, a single bank will not on its own be able to achieve that scale-benefits compared to the volumes that shared solutions can generate.

To combat this threat, banks need to abandon the ‘one-size-fits-all’ solutions and ‘business as usual’ approaches of the past, reassess their business strategy and value chain propositions, and redesign the payment experience to fit modern client demands. This requires a modern and standardized payment processing platform that:• is flexible enough to handle different payment types and

adapt to future needs• enables modern open connectivity options for sending,

receiving and sharing data (through informed consent) with clients, suppliers, networks, and partners

• delivers 24/7 capabilities as a global and connected world demands systems to be available always

• improves time-to-market for new products and services• supports compliancy with current and future regulations• is scalable for large transaction volumes without a

negative cost impact

• enables them to extract valuable analytics from transactional data

• delivers economies of scale through the bundling of transactions across several parties

As legacy systems appear to have reached their limit when it comes to delivering the flexibility and speed needed to keep up with business requirements, and banks assess their traditional front- and back-end platform architecture, they are faced with the question of what to do next. Should they adopt a ‘build-and-adapt’ approach, buy a ready-made solution ‘off-the-shelf’, outsource the solution to an external party, or opt for a combination of the aforementioned options? Whatever approach they choose, in the end, banks definitely need to act to transform their core systems.

1. https://www.statista.com/outlook/296/102/digital-payments/europe

Enabling innovation through payments platform transformation10

3. Buying off-the-shelf

The benefits of buying a solution from a specialist third-party provider are considerable. It will provide the bank with a set of standardized, ready-to-use solutions and effectively reduce the time-to-market for new products and services, while also allowing for shared R&D (Research and Development) and compliance costs with other clients of the solution. Off-the-shelf products, however, entails an upfront investment by means of license costs, and will provide the bank little control over release cycles. While most suppliers do offer bespoke additions to the standard product, banks need to be careful how much they want to adapt a standard system as the benefits mentioned above will not apply to those additions. This, in turn, can lead to increased cost and decreased flexibility. That said – as only few banks decide to replace everything at once, even a standardized system is likely to need bespoke integration to connect to the adjacent (legacy) systems it needs to interact with.

4. Partnering to invent

Banks choose this approach if they feel that there is no appropriate solution available in the market. Partnering with a supplier can provide a bank with an agile and innovative best of breed system that includes scalable benefits. On the other side, partnership management is not a key competence for most banks, and scouting for the right partner can be a time-consuming process. In addition, any invented solution will need to be tried and tested thoroughly, which is also time-consuming.

5. Outsourcing to third party

Choosing outsourcing as an approach will help the bank to develop a more service-oriented banking IT infrastructure. It enables the bank to add new channels and services,

phase out old core systems, and it can support their overall strategies. That said, outsourcing comes with some of the same challenges as off-the-shelf products as it requires a certain degree of streamlining of current processes to fit those of the supplier (and other banks on the same platform). Without a structured assessment of current systems and processes, an outsourcing exercise could easily be limited to the idiomatic “your mess, for less” approach.

When properly utilized, outsourcing back-end systems can help a bank to streamline its business operations significantly. It can deliver a new degree of flexibility to the bank, where the bank is free to pick-and-choose new functions and services it wishes to integrate into the payments platform. In addition, transferring the payments processing functions – or part of them – to a specialized third-party provider will help to minimize the complexity, costs and risk related to non-differentiating operations, as the provider will: • handle the regulatory burden of staying compliant• handle the HR burden of retaining payments experts• make costs lower • make operations more efficient

With most banks offering the same payments services today, outsourcing payments should also provide the bank with a degree of influence on the scope and the scale of the service. In other words, it should be flexible enough to accommodate the need for a bank to add additional functionalities targeted to a specific client base. Outsourcing back-office payments processing will enable banks to free up resources to focus on core competencies and differentiating activities like customer relationships, advisory services, client acquisition, and value-added services. This is the reason why more and more banks are considering outsourcing as a viable strategic solution to their challenges.

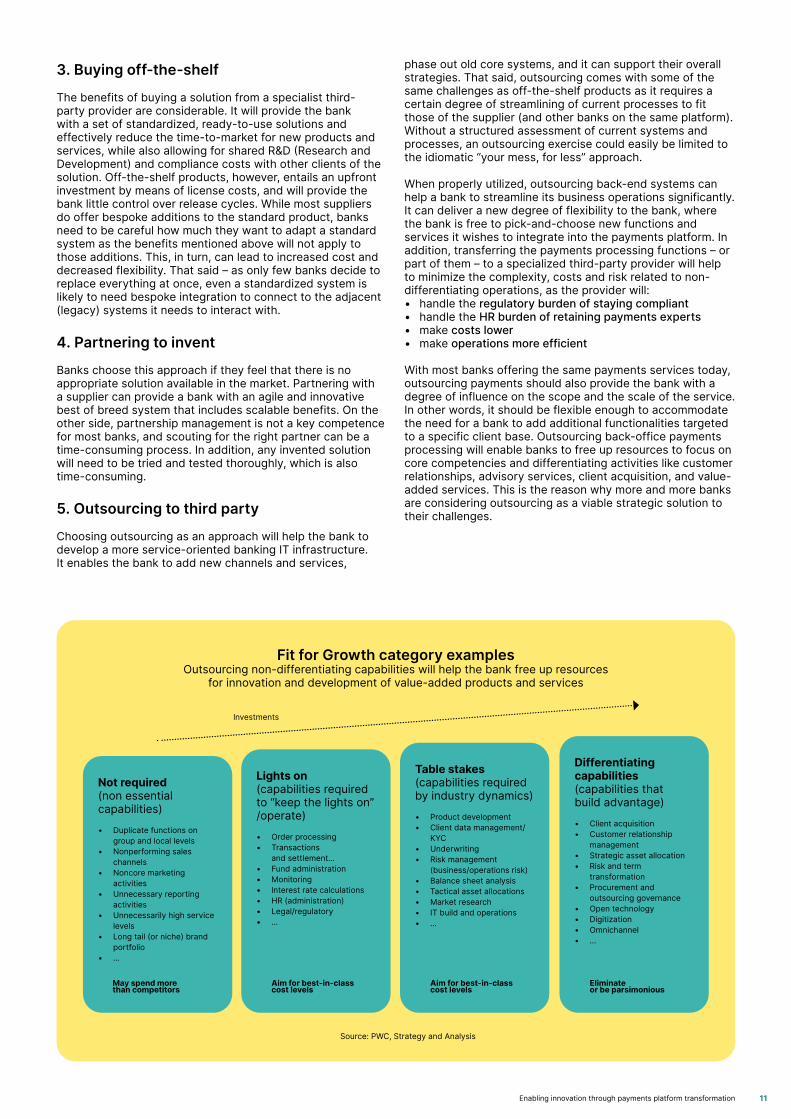

Fit for Growth category examples Outsourcing non-differentiating capabilities will help the bank free up resources

for innovation and development of value-added products and services

lnvestments

Source: PWC, Strategy and Analysis

Differentiating capabilities (capabilities that build advantage)

• Client acquisition• Customer relationship

management• Strategic asset allocation• Risk and term

transformation• Procurement and

outsourcing governance• Open technology• Digitization• Omnichannel• …

Table stakes (capabilities required by industry dynamics)

• Product development• Client data management/

KYC• Underwriting• Risk management

(business/operations risk)• Balance sheet analysis• Tactical asset allocations• Market research• IT build and operations• …

Lights on (capabilities required to “keep the lights on” /operate)

• Order processing• Transactions

and settlement…• Fund administration• Monitoring• lnterest rate calculations• HR (administration)• Legal/regulatory• …

Not required (non essential capabilities)

• Duplicate functions on group and local levels

• Nonperforming sales channels

• Noncore marketing activities

• Unnecessary reporting activities

• Unnecessarily high service levels

• Long tail (or niche) brand portfolio

• …

May spend more than competitors

Aim for best-in-class cost levels

Aim for best-in-class cost levels

Eliminate or be parsimonious

Enabling innovation through payments platform transformation 11

Outsourcing payments processing offers a compelling value proposition for banks as a means of: • lowering TCO on non-differentiating back-end

functionalities through economy of scale• offering 24/7 end-to-end real-time processing of all

payments• managing many different types of transactional

processes at high performance• ensuring full compliance with current and future

regulations and applicable payment schemes • leveraging the provider’s investments in state-of-

the-art technologies and best of breed solutions

In addition to these key qualities, outsourcing helps to enhance efficiency through consolidating and centralizing functions, share costs for compliance and R&D with other customers, and ensure connectivity with all clearing and settlement networks.

It should also be mentioned that every bank considering outsourcing as an option, should always begin by developing a business case to compare their current cost levels with cost levels when outsourcing. This way, banks will get a sense of the possible cost-saving potential of the outsourcing option beforehand.

Selecting the right partner – and solution Core banking functionalities are often referred to as the heart of a bank’s business as they sustain mission-critical operations. As a consequence, entrusting a core function as payment processing to a third-party provider can provoke strong feelings within a bank’s own ranks as well as a sense of losing control of the business. When facing these valid concerns, it is imperative for a bank to understand that outsourcing payments is by no means an ’all or nothing‘ procedure. Third-party providers typically present the bank with a vast selection of operating models to choose from, including ASP (Application Service Provider) solutions and full BPO (Business Process Outsourcing) offerings, which ultimately enables the bank to stay in control by striking a balance between ‘do it yourself ’ and outsourcing. This process is built on firm service level agreements and concludes with customized tools and services that matches the bank’s specific business needs.

In this context, it is paramount for a bank to partner with a provider they trust. This includes partnering with a provider with experience, expertise, integrity, and a long-term commitment to the payments industry. It is also important to take notice of the fact that payment processing outsourcing is often provided as modular solutions, which means that

a bank can choose to be just compliant or it can commit to a holistic end-to-end solutions portfolio. Or anything in-between. A strong partner can increase efficiency in compliance, lower cost and improve operational excellence through consolidation and finally enable differentiation through standardized interfaces to third-parties and value-added APIs for in-house product and service development.

Look before you leap

If banks want to remain relevant in the modern digital era, they need to change and develop along with the times. But change for the sake of change is never the right strategy. Before embarking on any transformative journey, banks should always ask themselves the following question: Are payments a strategic product for the bank? If the answer is yes, then the next question should be: how do we support this strategy best? The bank should assess if it wants to continue investing in payments internally, or if it should treat payments processing as a commodity and make use of the competencies and infrastructures of a specialized third-party provider – thus getting payment processing as a service.

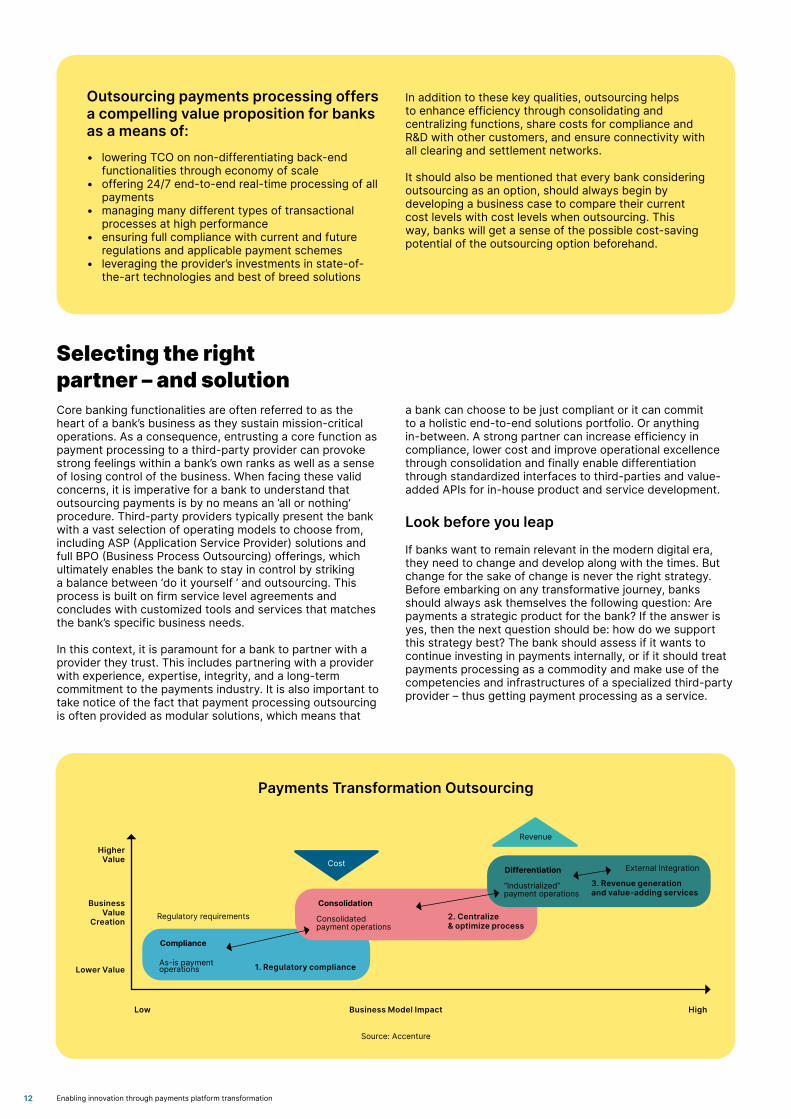

Regulatory requirements

Compliance

As-is payment operations 1. Regulatory compliance

Consolidation

Consolidated payment operations

2. Centralize & optimize process

Differentiation

“Industrialized” payment operations

External Integration

3. Revenue generation and value-adding services

Business Model Impact

Revenue

Cost Higher

Value

Business Value

Creation

Lower Value

Low High

Payments Transformation Outsourcing

Source: Accenture

Enabling innovation through payments platform transformation12

Conclusion

In an attempt to keep up with the competition in a fast-paced digital financial environment, banks are exploring ways to streamline non-differentiating back-end processes and transfer valuable

resources to differentiating front-end developments. However, the attempt is often complicated by expenditures and resources allocated for maintaining monolithic legacy systems which, in effect,

is limiting the banks’ ability to pursue innovation and investments in new digital technologies.

As a direct consequence of these circumstances, banks have started to reassess their business strategies and payment models to determine where to cut costs, reduce risks and improve customer value.

For this purpose, banks are increasingly turning to experienced third-party providers, who are qualified in opening up existing functionalities and data in a controlled and modern manner, delivering fully integrated coverage of the banks’ payment value chain, and who offer a modular step-by-step-approach to payment processing that helps banks of all sizes to address their specific needs.

It is imperative for a bank to understand that outsourcing payments is by no means an ’all or nothing‘ procedure. It’s all about seeking an optimal balance between ‘do it yourself’ and outsourcing.By partnering with a specialized payment service provider, banks ensure they have a stable, scalable and flexible payment environment with multi-channel coverage that is fully compliant and capable of accommodating modern payment requirements like instant payments and fast time-to-market capabilities. In doing this, banks will be able to lower their TCO on non-differentiating back-end functions like payment processing and free up resources to focus on core business strategies and differentiating activities that will help them compete in the new, digitized financial era.

Enabling innovation through payments platform transformation 13

Worldline [Euronext: WLN] is the European leader in the payments and transactional services industry and #4 player worldwide. With its global reach and its commitment to innovation, Worldline is the technology partner of choice for merchants, banks and third-party acquirers as well as public transport operators, government agencies and industrial companies in all sectors. Powered by over 20,000 employees in more than 50 countries, Worldline provides its clients with sustainable, trusted and secure solutions across the payment value chain, fostering their business growth wherever they are. Services offered by Worldline in the areas of Merchant Services; Terminals, Solutions & Services; Financial Services and Mobility & e-Transactional Services include domestic and cross-border commercial acquiring, both in-store and online, highly-secure payment transaction processing, a broad portfolio of payment terminals as well as e-ticketing and digital services in the industrial environment. In 2020 Worldline generated a proforma revenue of 4.8 billion euros.

worldline.com

About Worldline

For further [email protected]

Worldline is a registered trademark of Worldline SA. September 2021© 2021 Worldline.