Embed Size (px)

Citation preview

Where are we in the market cycles?16 October 2018

Marine Money |Greek Shipfinance Forum |Athens

Prepared by Angelica Kemene |Head of Market Analysis & Intelligence

Market FundamentalsCycles & Prices & Trends

Ship Earnings in today’s money over three decades

© Optima Shipping Services 2018

0

10000

20000

30000

40000

50000

60000

70000

Jan-90 Jan-95 Jan-00 Jan-05 Jan-10 Jan-15

***Average earnings of bulkers, oil tankers, containers and gas carriers

$’000/Day

$20,320

$27,650

$11,937

The main markets past cycle trough, but

earnings still weak.

Good news on demand side – world industrial

growth peaking; and trade growing fast

Key issues are the development of the world

economic business cycle, China’ s steel,

shipbuilding production, scrapping,

environmental regulations and the dynamics

of releasing the surplus capacity

Not easy to weight up

Sectors: Cycle Position October 2018

% deviation from earnings average 2008-2018

© Optima Shipping Services 2018

Tanker Markets still weak

Bulk carrier & Container rates

improve after the extremely

weak 2016

Source Data: Optima Shipping Services, The Baltic Exchange

-1%

1%

-3%

12%

-106%

-70%

-65%

-37%

35%

-1%

-15%

-1%

-32%

-5%

-38%

-150% -100% -50% 0% 50%

Capesize

Bulker Panamax

Supramax

Handysize

VLCC

Suezmax

Aframax

Clean Products(MR)

Feeder Containership 1700 teu grd

Narrow Beam Containership 4400 teu gls

Intermediate Containership 6800 teu

Neo-Panamax 9000 teu

LNG 145K CBM

LNG 160K CBM

LPG (VLGC)

% change in average earnings from the 2008-2018 average

Bulk carriers much better than 12

months ago, but the Tanker

market deteriorated

The Gas market is well below

trend, however since 2017 rates

are on an upward trend –

positive demand growth through

to 2021

Newbuilding Prices out of the bottom - Bulkers

© Optima Shipping Services 2018

81K DWT Panamax Bulkcarrier NB Prices 61-64K DWT Supramax NB Prices

Newbuilding Prices - Tankers

© Optima Shipping Services 2018

Suezmax Tanker 156-158K DWT Newbuilding Prices Products Tanker 47-51K DWT Newbuilding Prices

Newbuilding Prices - Containers

© Optima Shipping Services 2018

Containers 1700 TEU Newbuilding Prices Containers 8800 TEU Newbuilding Prices

Secondhand Prices: Bulkers

Panamax 76K Bulkcarrier 5 Year Old Secondhand Prices

Handymax 56K 5 Year Old Secondhand Prices

© Optima Shipping Services 2018

Secondhand Prices: Tankers

Suezmax D / H 160K DWT 5 Year Old Secondhand Prices

Products D / H 47K DWT 5 Year Old Secondhand Prices

© Optima Shipping Services 2018

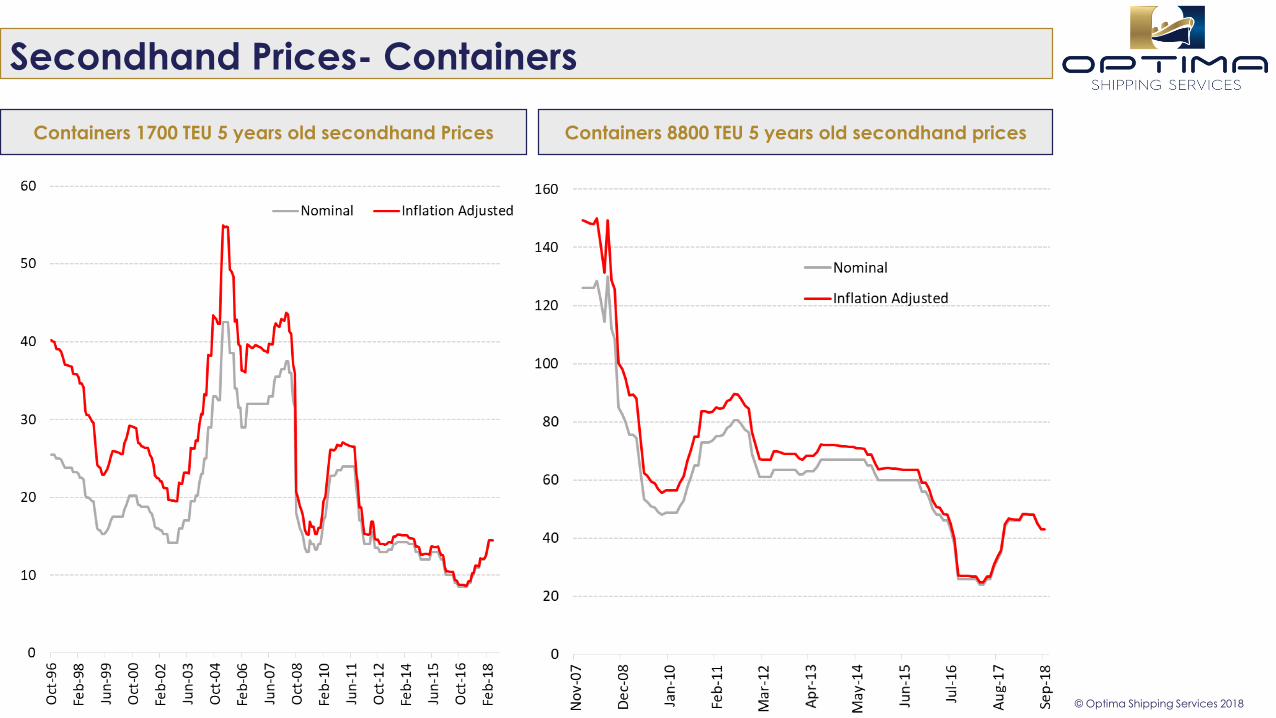

Secondhand Prices- Containers

© Optima Shipping Services 2018

Containers 1700 TEU 5 years old secondhand Prices Containers 8800 TEU 5 years old secondhand prices

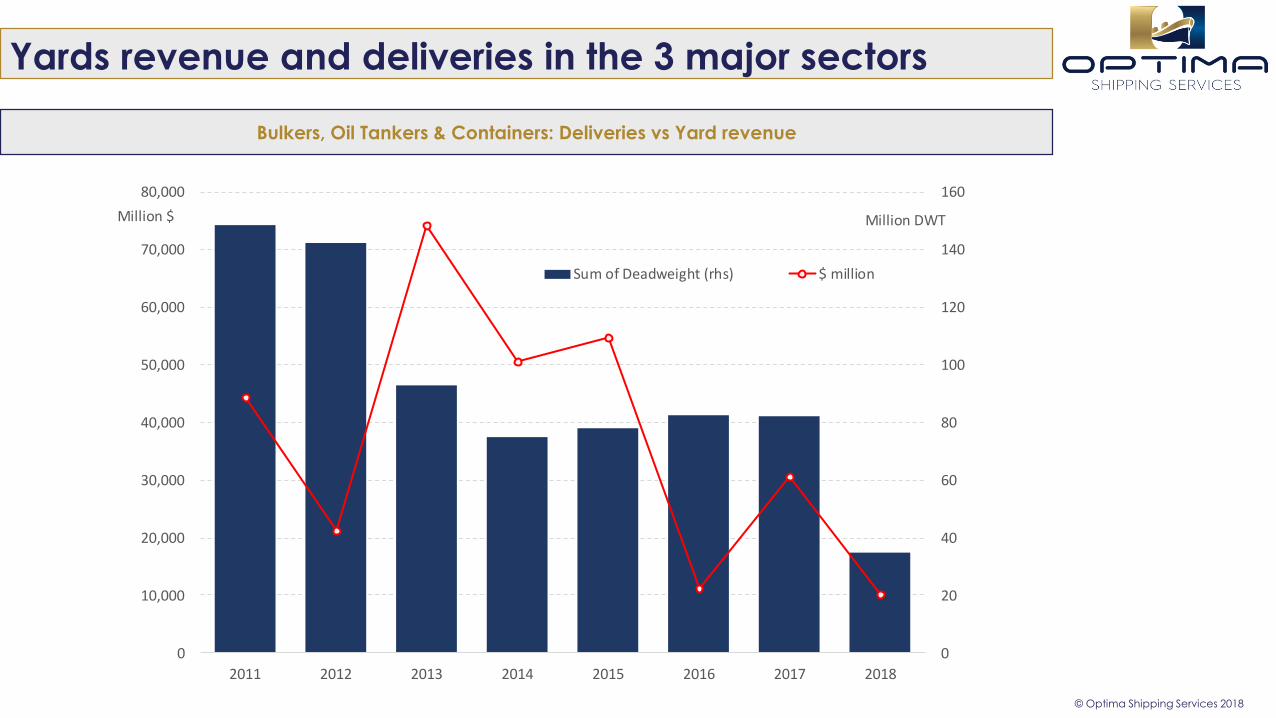

Yards revenue and deliveries in the 3 major sectors

© Optima Shipping Services 2018

Bulkers, Oil Tankers & Containers: Deliveries vs Yard revenue

0

20

40

60

80

100

120

140

160

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2011 2012 2013 2014 2015 2016 2017 2018

Million DWTMillion $

Sum of Deadweight (rhs) $ million

A shift towards Chinese Ship Yards

Major Shipbuilding Countries Current Orderbook %

© Optima Shipping Services 2018

0% 20% 40% 60% 80% 100%

Bulk Carrier

Container

Crude Oil Tanker

Products Tanker

China, People's Republic Of Korea, South Japan Others

For the 3 major sectors there are currently 188active yards – of which 35% is expected todeliver their final order this year, whilst 78% ofthem will deliver their final order until the endof 2019.

In 2007 285 yards received more than 1 order,while in 2017 91 yards received more than 1order – A decrease of 68%.

Inability to secure orders at a profit. Issue: Yard Consolidation China: “Plans on structural reform 2016-2020 in

shipbuilding industry” China’s top 10 state-

owned shipbuilders will be responsible for 70%of the country’s new tonnage by 2020.

Japan follows the trend (capacity cuts &mergers), but S. Korea remains skeptical.

Cost increase: steel prices, labor cost,exchange rates.

The extra cost can be balanced if builderscharge higher.

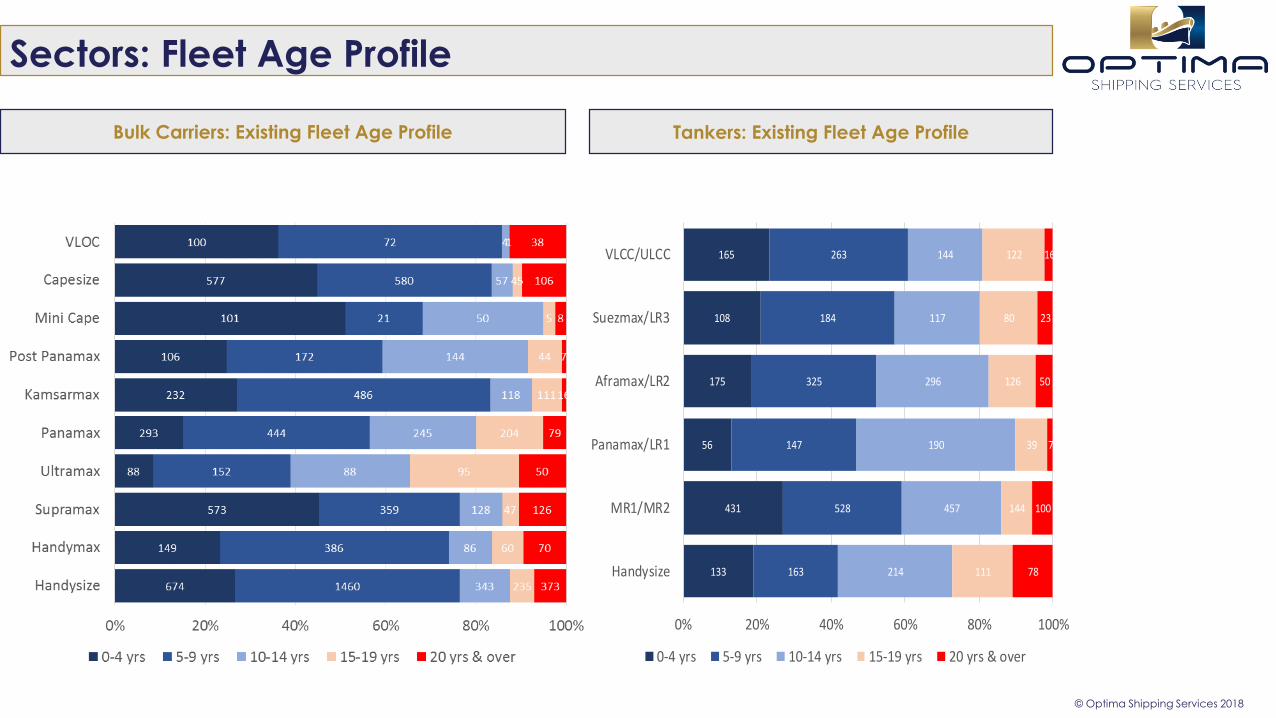

Sectors: Fleet Age Profile

Bulk Carriers: Existing Fleet Age Profile Tankers: Existing Fleet Age Profile

© Optima Shipping Services 2018

133

431

56

175

108

165

163

528

147

325

184

263

214

457

190

296

117

144

111

144

39

126

80

122

78

100

7

50

23

16

0% 20% 40% 60% 80% 100%

Handysize

MR1/MR2

Panamax/LR1

Aframax/LR2

Suezmax/LR3

VLCC/ULCC

0-4 yrs 5-9 yrs 10-14 yrs 15-19 yrs 20 yrs & over

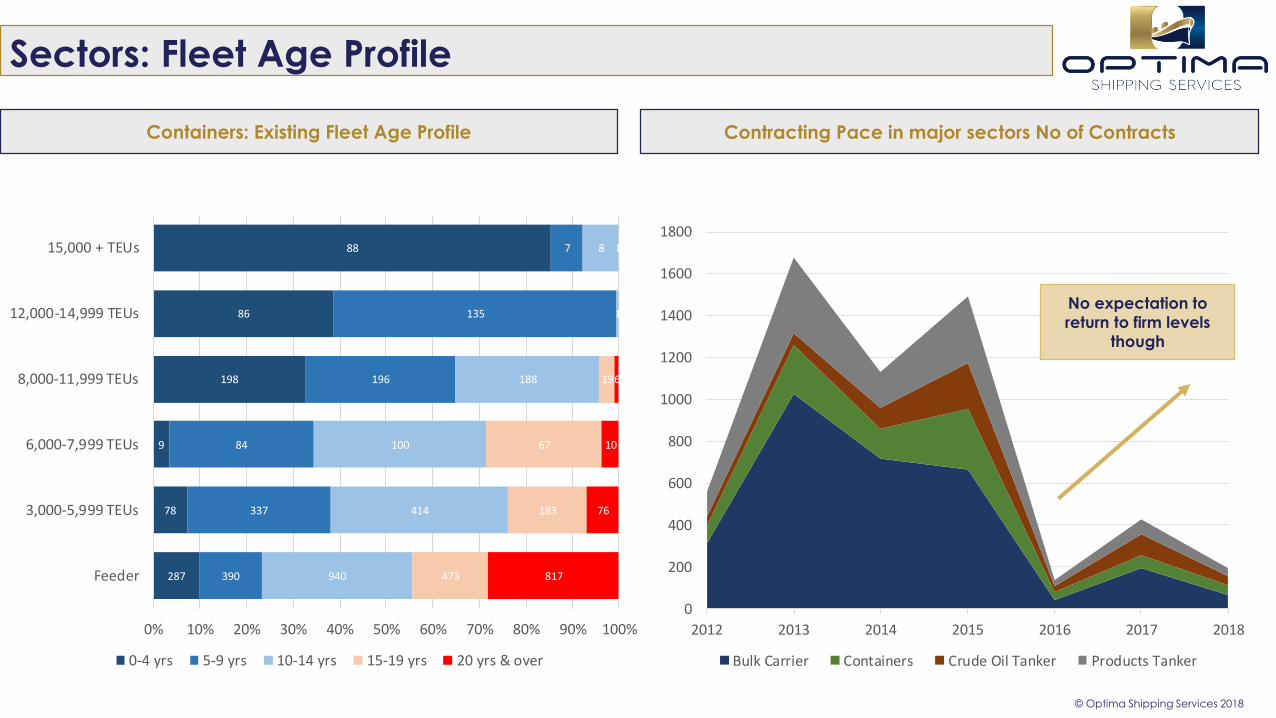

Sectors: Fleet Age Profile

Containers: Existing Fleet Age Profile

© Optima Shipping Services 2018

287

78

9

198

86

88

390

337

84

196

135

7

940

414

100

188

1

8

473

183

67

19

0

0

817

76

10

6

0

0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Feeder

3,000-5,999 TEUs

6,000-7,999 TEUs

8,000-11,999 TEUs

12,000-14,999 TEUs

15,000 + TEUs

0-4 yrs 5-9 yrs 10-14 yrs 15-19 yrs 20 yrs & over

0

200

400

600

800

1000

1200

1400

1600

1800

2012 2013 2014 2015 2016 2017 2018

Bulk Carrier Containers Crude Oil Tanker Products Tanker

Contracting Pace in major sectors No of Contracts

No expectation to

return to firm levels

though

Forward Delivery Schedule No of vessels

© Optima Shipping Services 2018

Bulk Carriers OB:14.5% Capes8.6% Pmax5.5% Supras5.4% Hsize

Oil Tankers OB:15% VLCCs

8.5% Suezmax13.2% Afras

9%Pmax11% LR27% LR1

8% MRs/Handies

Containers OB:20.2% >8K TEU

1.14% 3-7.9K TEU9% Feeders

0

50

100

150

200

250

Cap

esiz

e

Pana

max

BC

Sup

ram

ax

Han

dysi

ze

VLC

C

Suez

max

Afr

amax

Pan

amax

Tan

ker

LR2

LR1

MR

/Han

dy

Post

Pan

amax

Co

ntai

ner

>15,

000

TEU

Neo

Pan

amax

12

-14.

9k T

EU

Neo

Pan

amax

8-1

1.9

TEU

3-7

.9k

TE

U

Feed

er <

3k

TEU

2018 2019 2020 2021 2022

Bulk Carriers Oil Tankers Containers

OrderBook as % of the fleet

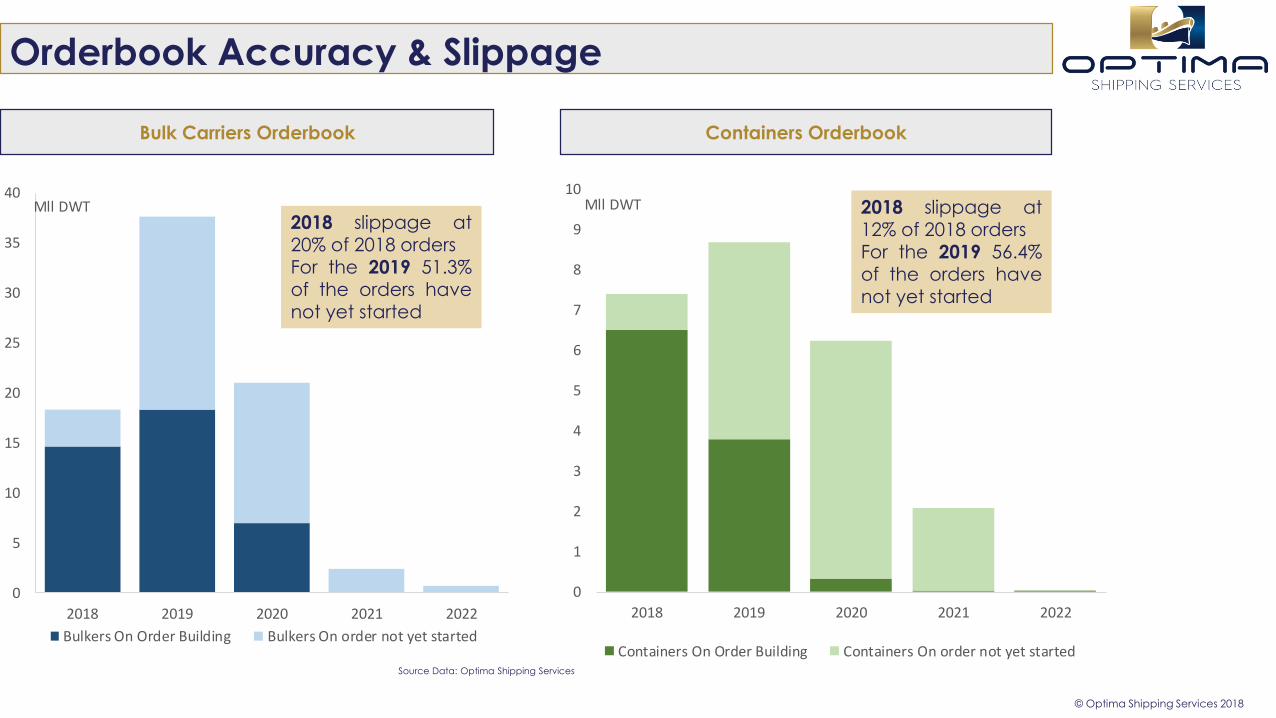

Orderbook Accuracy & Slippage

© Optima Shipping Services 2018

Bulk Carriers Orderbook Containers Orderbook

0

5

10

15

20

25

30

35

40

2018 2019 2020 2021 2022

Mll DWT

Bulkers On Order Building Bulkers On order not yet started

0

1

2

3

4

5

6

7

8

9

10

2018 2019 2020 2021 2022

Mll DWT

Containers On Order Building Containers On order not yet started

2018 slippage at

20% of 2018 ordersFor the 2019 51.3%of the orders havenot yet started

2018 slippage at12% of 2018 ordersFor the 2019 56.4%of the orders havenot yet started

Source Data: Optima Shipping Services

Orderbook Accuracy & Slippage

© Optima Shipping Services 2018

Crude Oil Tankers Orderbook Product Tankers Orderbook

0

5

10

15

20

25

30

2018 2019 2020 2021 2022

Mll DWT

Crude Tankers On order not yetstarted

Crude Tankers On Order Building

0

1

2

3

4

5

6

7

8

9

2018 2019 2020 2021 2022

Mll DWT

Product Tankers On order not yetstarted

Product Tankers On Order Building

2018 slippage at27.3% of 2018 ordersFor the 2019 72.5%of the orders havenot yet started

2018 slippage at 3%of 2018 ordersFor the 2019 51% ofthe orders have notyet started

Source Data: Optima Shipping Services

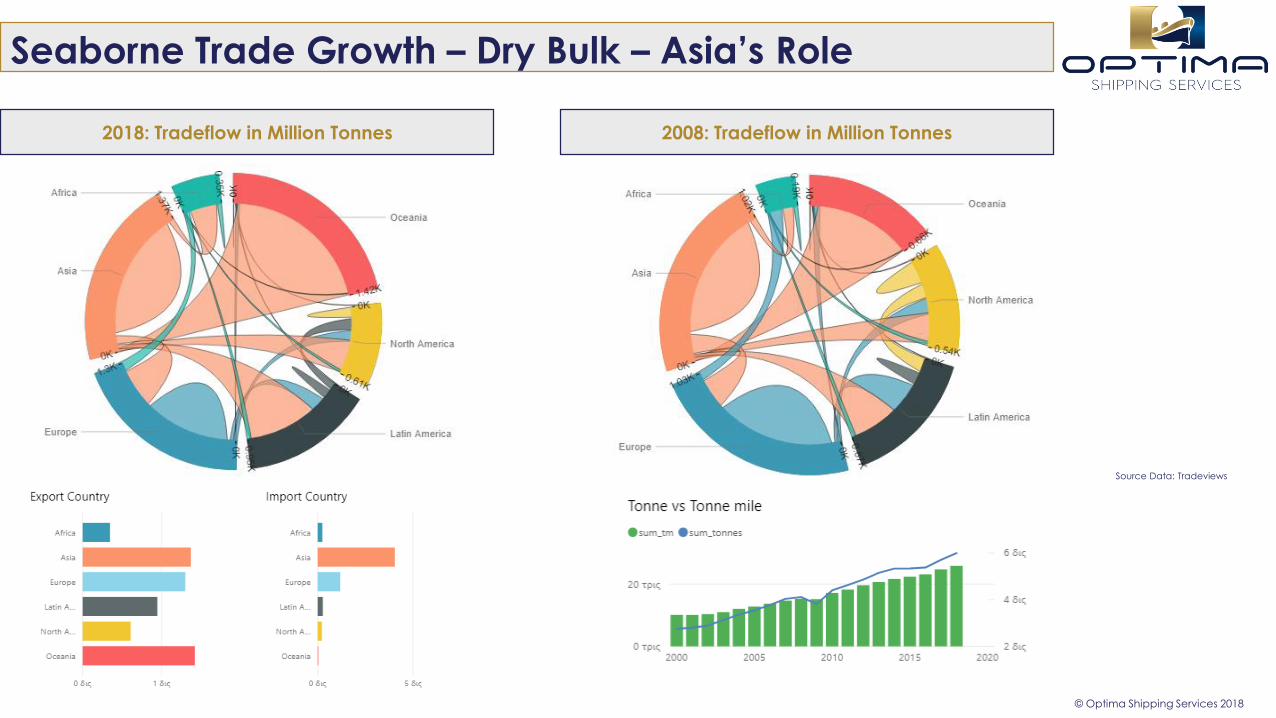

Seaborne Trade Growth – Dry Bulk – Asia’s Role

Source Data: Tradeviews

© Optima Shipping Services 2018

2018: Tradeflow in Million Tonnes 2008: Tradeflow in Million Tonnes

Seaborne Trade Growth – Oil Tankers & Gas – Asia’s Role

Source Data: Tradeviews

© Optima Shipping Services 2018

2018: Tradeflow in Million Tonnes 2008: Tradeflow in Million Tonnes

Seaborne Trade Growth Organization for Economic Cooperation and Development index of industrial production and world indices:

Gross domestic product, merchandise trade and seaborne shipments, 1975–2016(1990 = 100) - UNCTAD

Source Data: Optima Shipping Services

© Optima Shipping Services 2018

The Outlook for the world economy and trade

is expected to improve. Projections for the medium term point to

continued expansion, with volumes growing atan estimated compound annual growth rate of3.2% between 2017-2022.

Volumes are set to expand across allsegments, with containerized trade and majordry bulk commodities trade recording thefastest growth along with LNG.

Investment Opportunities & Risks

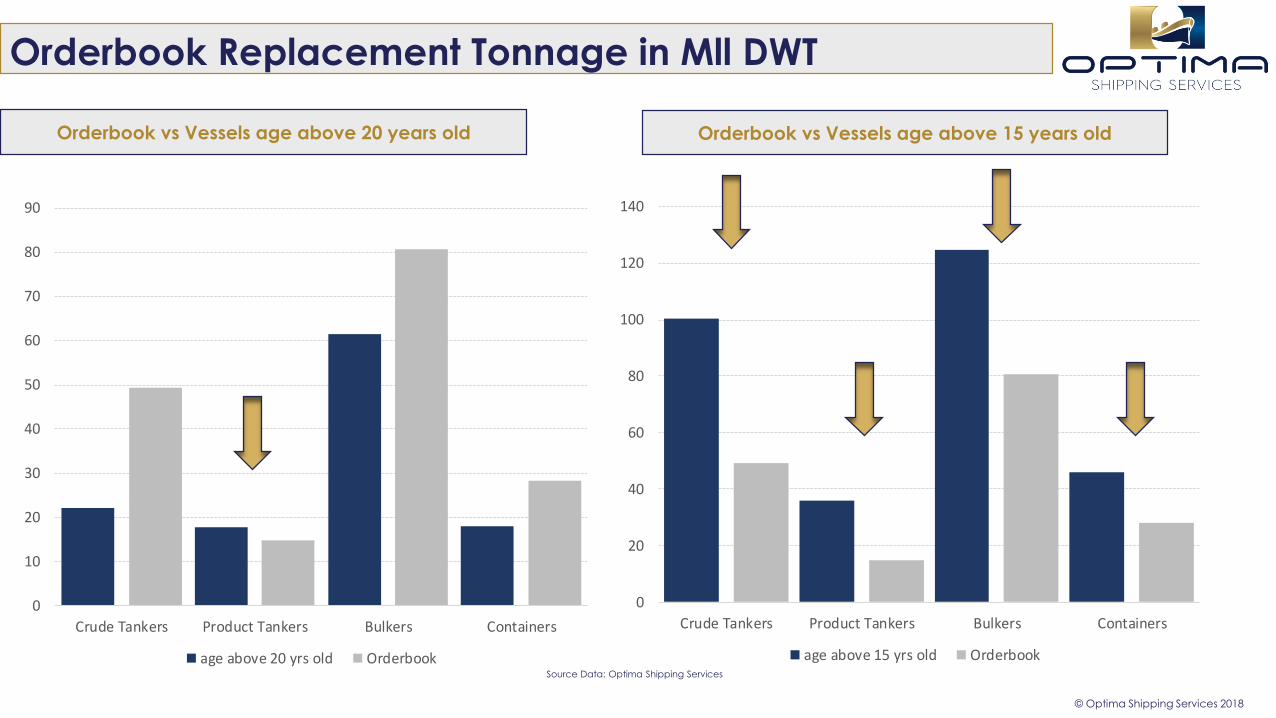

Orderbook Replacement Tonnage in Mll DWT

© Optima Shipping Services 2018

0

10

20

30

40

50

60

70

80

90

Crude Tankers Product Tankers Bulkers Containers

age above 20 yrs old Orderbook

0

20

40

60

80

100

120

140

Crude Tankers Product Tankers Bulkers Containers

age above 15 yrs old Orderbook

Orderbook vs Vessels age above 20 years old Orderbook vs Vessels age above 15 years old

Source Data: Optima Shipping Services

Prospects & Risks

Source Data: Optima Shipping Services

© Optima Shipping Services 2018

Trade still growing: Economic upswing supporting trade in short term and still growth potential in shippingdemand – especially in Asia & developed economies. Trade impacted by Chinese economy and policy(OBOR).

Fleet growth slowing: However, still many ships to hit the water and over 50% bigger, so larger market forservice sector.

Market Cycles: Better looking environment for Bulk Carriers/Containers/ LNG than Oil Tankers. Shipyard Capacity: Shipyard ordering became weak in 2016 and pressured for further consolidation and

capacity reductions. Major change in financial landscape: High interest rates and new entries in shipping investment Environmental regulation change: Regulation accelerating and creating demand for solutions but timing and

technology are pricy. Digitalization, e-commerce and the implementation of the Belt and Road Initiative: The unfolding effects of tech

advances and China’s ambitious reordering of global trade infrastructure will entail important implications forshipping and maritime trade. Potential for a boost in seaborne trade volumes and enhanced efficiency throughdigitalization.

Rising trade barriers: more and more countries adopt protectionist measures and there are many unresolvedmatters regarding several ongoing trade agreements

A trend towards de-globalisation coming out from governments, intensifying protectionist policy approaches. Many factors nowadays have been impacting the shipping industry making it extremely difficult to calculate

risks and plan long term investments. However challenging the markets might be there are still opportunities out there.

THANK YOU !

© Optima Shipping Services 2018

This report has been prepared by Optima Shipbrokers and is addressed to Optima Shipbrokers customers only and is for distribution only under such circumstances as may be permitted by applicable law. This information has no regard to specific investment objectives, financial situation or particular needs of any specific recipient. It is published solely for informational purposes and this information is not, and should not be construed as, an offer or solicitation to sell or buy any product, investment, security or any other financial instrument. Optima Shipbrokers does not make any representation or warranty, express or implied, as to the accuracy, completeness or correctness of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the report. Neither Optima Shipbrokers , nor any of its directors, employees or agents, accepts any liability for any loss or damage, howsoever caused, arising from any reliance on any information or views contained in this report. While this report, and any opinions expressed in it, have been derived from sources believed to be reliable and in good faith they are not to be relied upon as authoritative or taken in substitution for the exercise of your own commercial judgment. Any opinions expressed in this report are subject to change without notice. Optima Shipbrokers is under no obligation to update or keep current the information contained herein. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Optima Shipbrokers accepts no liability whatsoever for the action of third parties in the respect. This information is the intellectual property of Optima Shipbrokers . Optima Shipbrokers logo is the trademark of the company. All rights reserved.

Produced by Optima Shipbrokers Research

10, Ouranou Str166 71Kavouri VouliagmenisGreeceTel: +30 210 8922000

Email: [email protected] www.optimashipbrokers.com

![Kemen gtd v1 [modo de compatibilidad]](https://img.pdfslide.us/doc/110x75/55d56458bb61eb373a8b45a2/kemen-gtd-v1-modo-de-compatibilidad.jpg)