Embed Size (px)

Citation preview

1

Making Super Fast Broadband a Reality for UK plc

Chris Smedley, Chief Executive Geo

Networkshop Plenary

2

What is Super Fast Broadband?

Next Generation Access (NGA) is defined by Ofcom as:

“Broadband services that are capable of delivering sustained bandwidths significantly in excess of those currently available using existing local access infrastructures or technologies.”

Opposite ends of the next generation broadband spectrum:

• Digital Britain looking to set the USO bar at “up to” 2Mbps

• South Korea setting a goal of a 1Gbps USO by 2012

3

What does super fast broadband look like to the man in the street?

It is a bit like going back in time to the era of the horse and cart and asking people to visualise a car

We need to paint a picture that is compelling and easily understood ….. this can be a significant challenge

4

6

How Big is the Challenge?

The cost of delivering NGA in the UK:

• FTTC estimated at £5 billion

• FTTH estimated at £30 billion

2

7

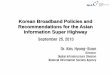

Options for Delivering Super Fast Broadband

Option 1: Private sector cherry pick the market and public sector fund the gaps

Option 2: Public/Private partnership to make strategic investment in next generation networks

In reality, UK plc will require both options to compete effectively on a global stage

8

Public investment requires proof of market failure

• The UK, along with other developed economies, has just spent the last two decades deregulating the telecoms market to stimulate market forces

• It is unlikely that the Government wants to see the public sector pile in and build/ run networks, distorting competition and undermining investment

• It is therefore especially important, in the ICT sector, to prove beyond doubt, that substantial market failure exists

9

Market Failure Conditions

Unfortunately the yard stick for measuring market failure is not yet clearly defined

However as a rule of thumb…… • Monopoly supply • Limited or lacking in services • High prices • Timing of resolution (eg BT or VM rollout) unacceptable (impatience is not always a strong argument however) • Benchmark other regions/countries

10

Making the Case for Public Intervention

• State objectives in economic and social improvement terms • Demonstrate (and quantify) how ICT strategy contributes • Economic impact is a powerful argument:

• Innovation, productivity and enterprise effects • Best measured as GVA uplift • Helping close the regional (and local) GDP gap • Combat impacts of the recession

• Quantify the specific contribution of NGA • Relative comparisons - significant and growing economic

disadvantage

11

The Super Fast Broadband Partnership Challenge

Proof of market failure to attract EU/UK public sector funding

Proof of demand to to attract private sector partnership

Shared Risk and Reward Profile

12

A Blueprint for Super Fast Broadband Partnerships

• Agreed cost and ROI profiles over life time of the deal

• Shared risk and reward • Long term investment

15 to 20 years with exit options

• SPV model • Supply partners • Agile resource

3

13

A Working Model for Next Generation Networks

14

FibreSpeed: the Network • Geo won a competitive

tender to build and operate a 320km network Manchester to Anglesey

• Funded by EU, WAG & Geo

• Initial cost £30m over 15 years

• Build completed in 15 months: now live

• Code powers • Wireless access • An essential

infrastructure for Next Gen Broadband services

15

FibreSpeed: The Business

• Open access network • High speed data

services • Includes “passive”

network components • Service provider

channel model • First sales closed;

healthy sales pipeline • Brings infrastructure

competition to North Wales

• Pricing benchmarked to SE England

• 14 business parks

End-User End-User End-User

16

Digital Britain: Geo’s View on Priorities • Low cost, high quality core network infrastructure is now available to all major

broadband players and is a competitive market

• Current pressing challenge is to do the same for the “middle mile” – backhaul from BT’s network to the core: • An economic bottleneck getting worse due to impact of video downloads & streaming • Access to BT duct (Metronode to Core) would quickly deliver lower prices & faster speeds • Transparent and stable BT pricing and a certain regulatory regime essential for investment

• In less populated areas, public intervention is needed in the middle mile (eg FibreSpeed)

• Next Generation Access will happen but competition is essential • LLU’s success is due to it being a passive infrastructure remedy • The same is needed in an NGA world from the exchange to(wards) the home • Duct access remedy is key (BT & Local Authority access – “Duct Atlas”) • And unlike LLU, no BT products to be allowed before this solution is available to all • An Industry Working Group recommended to Ofcom to resolve practicalities

17

Optical Fibre & Alternative Duct Systems

• Geo’s National network is mostly located adjacent to the gas network • Very secure and suitable for large core networks

• Geo’s London network is based in Thames Water’s Central London sewer system • Ideal for business use due to security and size, BUT • Other town or suburban sewer systems much smaller –

frequently cut into by sewer company • Gaps filled with high risk build techniques such as slot

trenching • Often non-existent in rural areas

• Detailed procedures, and an excellent commercial and working relationship required with utility owner

• Realism required: • Alternative ducts not the answer on their own • Existing, purpose-built infrastructure owned by BT & Virgin

Media • Local Authority Duct Atlas

18

The Public Sector’s Role • Economic Stimulus • Broadband is a key economic driver: optical fibre is the 21st century equivalent of roads and

railways • New networks in poor, rural and/or remote areas of Britain will not be built by the market • FibreSpeed is the model for a publicly funded “open access” network • The FibreSpeed model could be mobilised into other regions of the UK in 9-12 months • It is critical that this model be deployed whenever public money is put to work in this way • Don’t just reduce an existing telco’s capex budget

• Other Government & Regulatory Initiatives • Reform business rates on optical fibre – a disincentive to NGA investment • Ensure recommendations by Caio Review on initiatives to lower cost of NGA build out are

developed through industry working groups • Ensure that common standards and open procurement processes are used for all public

investment in optical fibre

• A major opportunity exists today for Government to invest in critical national infrastructure

4