Embed Size (px)

Citation preview

WE’RE MAKINGBETTING ANDGAMING BETTER

Statutory Accounts 2015

Sky Betting & Gaming (‘SB&G’) is an online betting operator, one of the UK’s leading providers of digital betting and gaming services.

CONTENTS

02 | Year in Review04 | Financial Review06 | Consolidated Statement of Comprehensive Income07 | Consolidated Statement of Financial Position08 | Company Statement of Financial Position09 | Consolidated Cash Flow Statement10 | Company Cash Flow Statement11 | Consolidated Statement of Changes in Equity12 | Company Statement of Changes in Equity13 | Notes to the Consolidated Financial Statements32 | Glossary

HIGHLIGHTS 2014/15

Sky Betting & Gaming Statutory Accounts 2015 | 01

2014/15A YEAR TO REMEMBER

£247mSales

+36%Growth

£80mEBITDA

+38%Growth

600Employees

+15%More staff

Today, we bring the excitement of sports betting, casino games, poker and bingo to over 1.5m UK customers.

In the last five years, SB&G have become a major online player in the UK. During that time, the business has delivered an annualised growth in operating profit of over 35%, and a fourfold increase in revenues. We have a strong mobile focus, with over two thirds of our 2014/15 revenue generated via mobile devices.

Formed in 2001, SB&G is led by CEO Richard Flint, headquartered in Leeds and employed approximately 600 people in 2015. We operate five major online products – Sky Bet, Sky Vegas, Sky Casino, Sky Poker and Sky Bingo – as well as leading online betting odds comparison service, Oddschecker.

In a highly regulated market our commitment to creating a safe and responsible gaming environment gives us a strong platform for future growth.

We have developed a close partnership with Sky and, in particular, Sky Sports over the last decade. This gives us credibility and a unique opportunity to co-develop games and promotions that have contributed greatly to our growth.

During 2014/15, SB&G became an independent company, the Sky plc group (‘Sky’) sold its majority share to funds advised and managed by CVC Capital Partners (such funds hereinafter, ‘CVC’), positioning SB&G as a well-funded and ambitious independent company, focusing on home-grown and international expansion, while retaining the rights, strength and support of the Sky brand.

Record revenues, increased customer numbers, and a future as an ambitious independent company. A good 2014/15 for Sky Betting & Gaming.

Sky Betting & Gaming Statutory Accounts 2015 | 02

12

3

5

4

2014/15A YEAR TOREMEMBER

YEAR IN REVIEW

July 2014

Ŷ Super 6 World Cup jackpot winner: an entrant from East London sweats on a goalless draw between Argentina and Switzerland. He is now £100,000 richer

Ŷ Germany beat Argentina in extra-time 1-0 in the World Cup final

Ŷ Sky Bet sponsors Grade 2 Lowther Stakes race at York Ebor Festival

August 2014

Ŷ Sky Casino launches, with live dealer casino table, card and slot games

Ŷ Launch of Premier League season 14/15: Manchester City are defending champions, and Leicester City, Burnley and QPR enter as newly promoted teams

September 2014

Ŷ Launch of multi-tables for poker on mobile and iPad

Ŷ Ryder Cup, Gleneagles, Scotland: Europe retain the Ryder Cup (16 ½ pts to 11 ½ pts), repeating their triumph at Medinah, USA in 2012

November 2014

Ŷ Super 6 winner: £250,000 jackpot landed for the 4th time in 14 months as Burnley grab a surprise 2-1 away win at Stoke

Ŷ Sky Vegas: Sky Vegas Millions is our biggest-ever exclusive £1m cash giveaway promotion

Ŷ Sky Vegas launches ‘Scratch 4’ instant win, an exclusive scratchcard series produced by developer, Core Gaming

October 2014

Ŷ Oddschecker Australia mobile site launched

Ŷ Super 6: one-off Double Jackpot Super 6, £500,000

Sky Betting & Gaming Statutory Accounts 2015 | 03

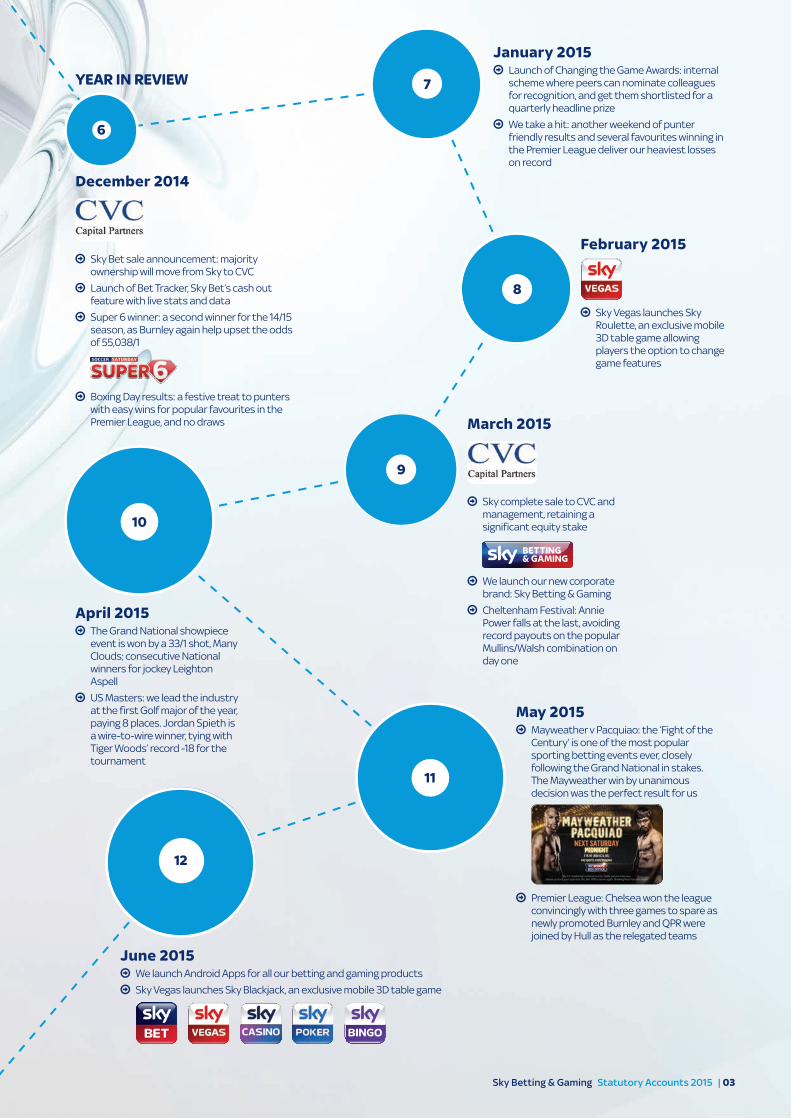

6

7

8

9

10

11

12

December 2014

Ŷ Sky Bet sale announcement: majority ownership will move from Sky to CVC

Ŷ Launch of Bet Tracker, Sky Bet’s cash out feature with live stats and data

Ŷ Super 6 winner: a second winner for the 14/15 season, as Burnley again help upset the odds of 55,038/1

Ŷ Boxing Day results: a festive treat to punters with easy wins for popular favourites in the Premier League, and no draws

January 2015 Ŷ Launch of Changing the Game Awards: internal

scheme where peers can nominate colleagues for recognition, and get them shortlisted for a quarterly headline prize

Ŷ We take a hit: another weekend of punter friendly results and several favourites winning in the Premier League deliver our heaviest losses on record

February 2015

Ŷ Sky Vegas launches Sky Roulette, an exclusive mobile 3D table game allowing players the option to change game features

March 2015

Ŷ Sky complete sale to CVC and management, retaining a significant equity stake

Ŷ We launch our new corporate brand: Sky Betting & Gaming

Ŷ Cheltenham Festival: Annie Power falls at the last, avoiding record payouts on the popular Mullins/Walsh combination on day one

April 2015 Ŷ The Grand National showpiece

event is won by a 33/1 shot, Many Clouds; consecutive National winners for jockey Leighton Aspell

Ŷ US Masters: we lead the industry at the first Golf major of the year, paying 8 places. Jordan Spieth is a wire-to-wire winner, tying with Tiger Woods’ record -18 for the tournament

May 2015 Ŷ Mayweather v Pacquiao: the ‘Fight of the

Century’ is one of the most popular sporting betting events ever, closely following the Grand National in stakes. The Mayweather win by unanimous decision was the perfect result for us

Ŷ Premier League: Chelsea won the league convincingly with three games to spare as newly promoted Burnley and QPR were joined by Hull as the relegated teams

June 2015 Ŷ We launch Android Apps for all our betting and gaming products

Ŷ Sky Vegas launches Sky Blackjack, an exclusive mobile 3D table game

YEAR IN REVIEW

Sky Betting & Gaming Statutory Accounts 2015 | 04

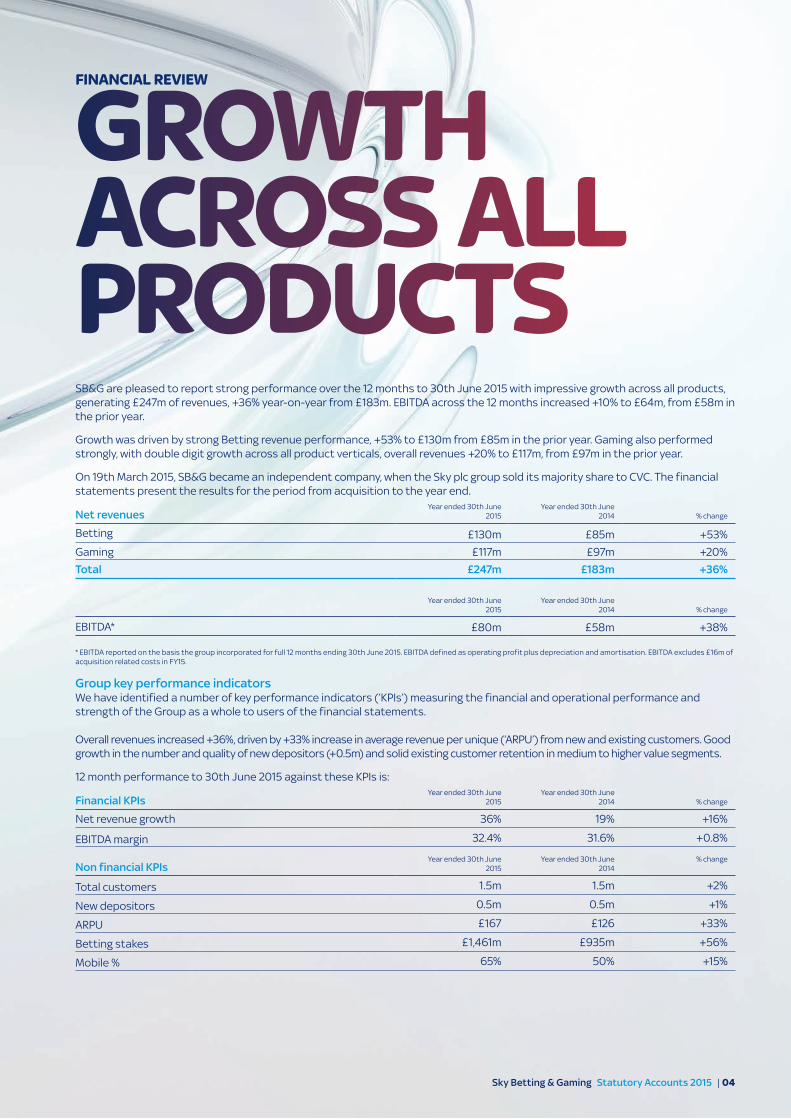

GROWTH ACROSS ALL PRODUCTS

FINANCIAL REVIEW

SB&G are pleased to report strong performance over the 12 months to 30th June 2015 with impressive growth across all products, generating £247m of revenues, +36% year-on-year from £183m. EBITDA across the 12 months increased +10% to £64m, from £58m in the prior year.

Growth was driven by strong Betting revenue performance, +53% to £130m from £85m in the prior year. Gaming also performed strongly, with double digit growth across all product verticals, overall revenues +20% to £117m, from £97m in the prior year.

On 19th March 2015, SB&G became an independent company, when the Sky plc group sold its majority share to CVC. The financial statements present the results for the period from acquisition to the year end.

Net revenuesYear ended 30th June

2015Year ended 30th June

2014 % change

Betting £130m £85m +53%

Gaming £117m £97m +20%

Total £247m £183m +36%

Year ended 30th June 2015

Year ended 30th June 2014 % change

EBITDA* £80m £58m +38%

* EBITDA reported on the basis the group incorporated for full 12 months ending 30th June 2015. EBITDA defined as operating profit plus depreciation and amortisation. EBITDA excludes £16m of acquisition related costs in FY15.

Group key performance indicatorsWe have identified a number of key performance indicators (‘KPIs’) measuring the financial and operational performance and strength of the Group as a whole to users of the financial statements.

Overall revenues increased +36%, driven by +33% increase in average revenue per unique (‘ARPU’) from new and existing customers. Good growth in the number and quality of new depositors (+0.5m) and solid existing customer retention in medium to higher value segments.

12 month performance to 30th June 2015 against these KPIs is:

Financial KPIsYear ended 30th June

2015Year ended 30th June

2014 % change

Net revenue growth 36% 19% +16%

EBITDA margin 32.4% 31.6% +0.8%

Non financial KPIsYear ended 30th June

2015Year ended 30th June

2014% change

Total customers 1.5m 1.5m +2%

New depositors 0.5m 0.5m +1%

ARPU £167 £126 +33%

Betting stakes £1,461m £935m +56%

Mobile % 65% 50% +15%

FINANCIAL REVIEW

Sky Betting & Gaming Statutory Accounts 2015 | 05

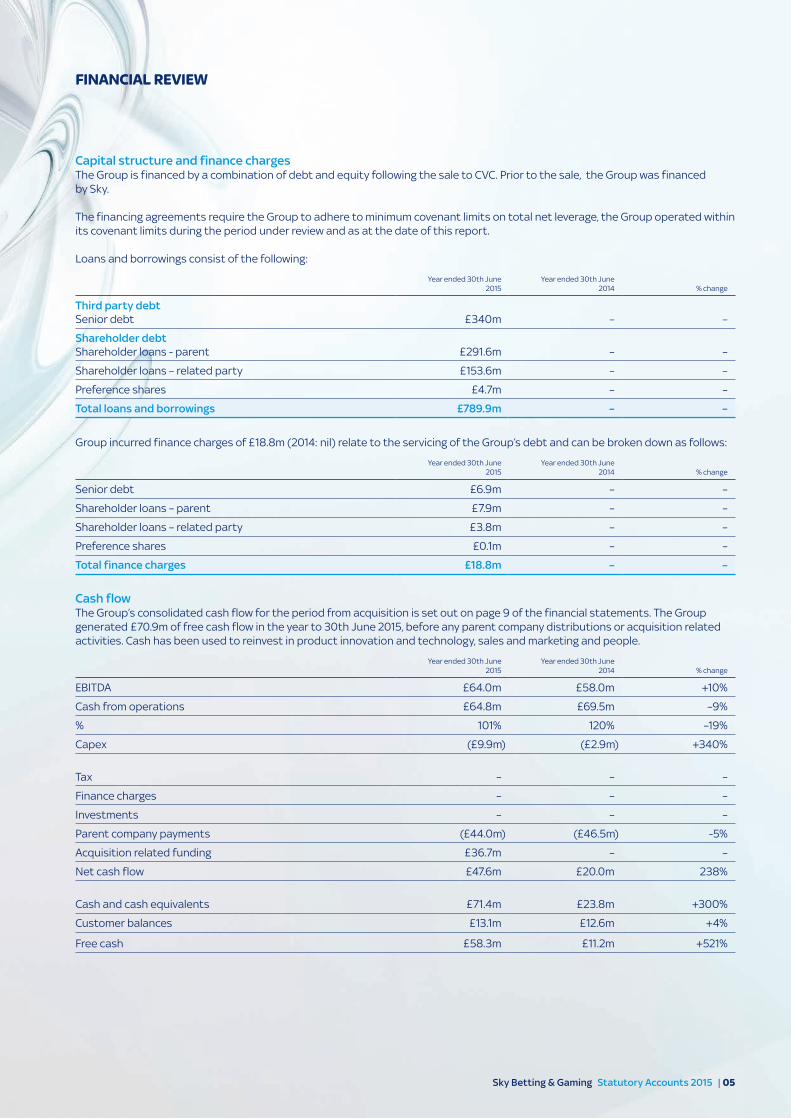

Capital structure and finance chargesThe Group is financed by a combination of debt and equity following the sale to CVC. Prior to the sale, the Group was financed by Sky.

The financing agreements require the Group to adhere to minimum covenant limits on total net leverage, the Group operated within its covenant limits during the period under review and as at the date of this report.

Loans and borrowings consist of the following:

Year ended 30th June 2015

Year ended 30th June 2014 % change

Third party debtSenior debt £340m – –

Shareholder debtShareholder loans - parent £291.6m – –

Shareholder loans – related party £153.6m – –

Preference shares £4.7m – –

Total loans and borrowings £789.9m – –

Group incurred finance charges of £18.8m (2014: nil) relate to the servicing of the Group’s debt and can be broken down as follows:

Year ended 30th June 2015

Year ended 30th June 2014 % change

Senior debt £6.9m – –

Shareholder loans – parent £7.9m – –

Shareholder loans – related party £3.8m – –

Preference shares £0.1m – –

Total finance charges £18.8m – –

Cash flowThe Group’s consolidated cash flow for the period from acquisition is set out on page 9 of the financial statements. The Group generated £70.9m of free cash flow in the year to 30th June 2015, before any parent company distributions or acquisition related activities. Cash has been used to reinvest in product innovation and technology, sales and marketing and people.

Year ended 30th June 2015

Year ended 30th June 2014 % change

EBITDA £64.0m £58.0m +10%

Cash from operations £64.8m £69.5m –9%

% 101% 120% –19%

Capex (£9.9m) (£2.9m) +340%

Tax – – –

Finance charges – – –

Investments – – –

Parent company payments (£44.0m) (£46.5m) -5%

Acquisition related funding £36.7m – –

Net cash flow £47.6m £20.0m 238%

Cash and cash equivalents £71.4m £23.8m +300%

Customer balances £13.1m £12.6m +4%

Free cash £58.3m £11.2m +521%

Sky Betting & Gaming Statutory Accounts 2015 | 06

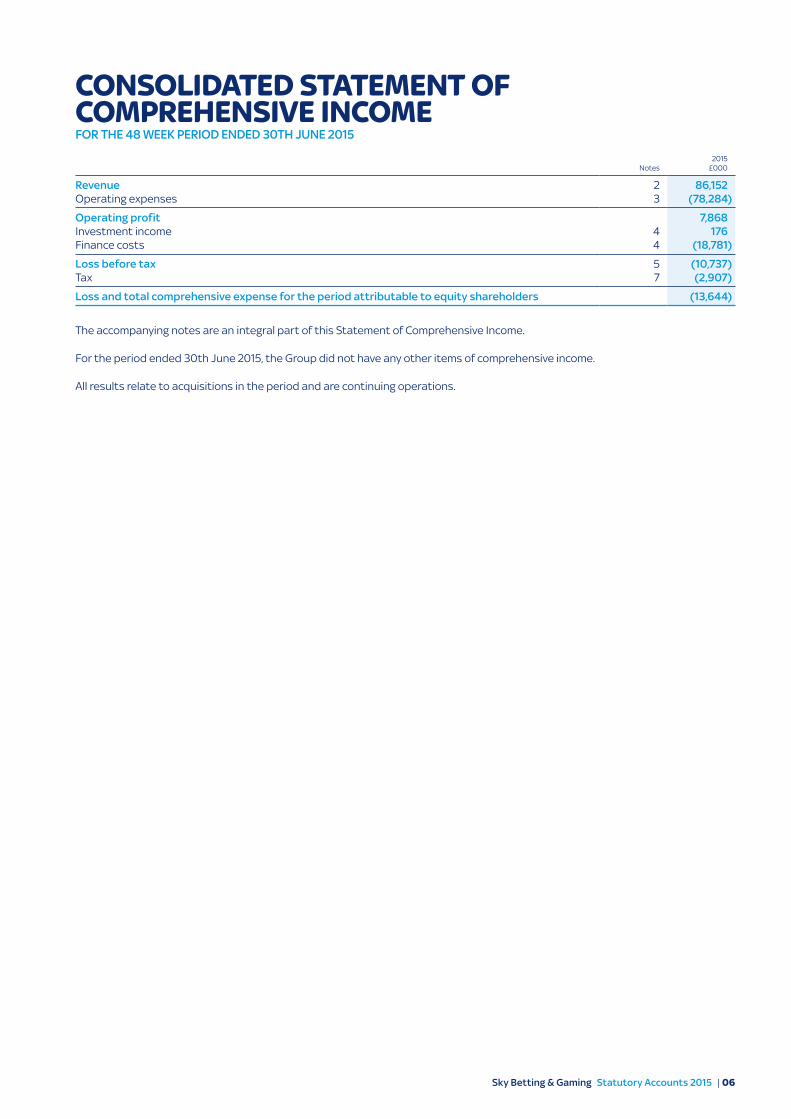

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Notes2015

£000

Revenue 2 86,152Operating expenses 3 (78,284)

Operating profit 7,868Investment income 4 176Finance costs 4 (18,781)

Loss before tax 5 (10,737)Tax 7 (2,907)

Loss and total comprehensive expense for the period attributable to equity shareholders (13,644)

The accompanying notes are an integral part of this Statement of Comprehensive Income.

For the period ended 30th June 2015, the Group did not have any other items of comprehensive income.

All results relate to acquisitions in the period and are continuing operations.

Sky Betting & Gaming Statutory Accounts 2015 | 07

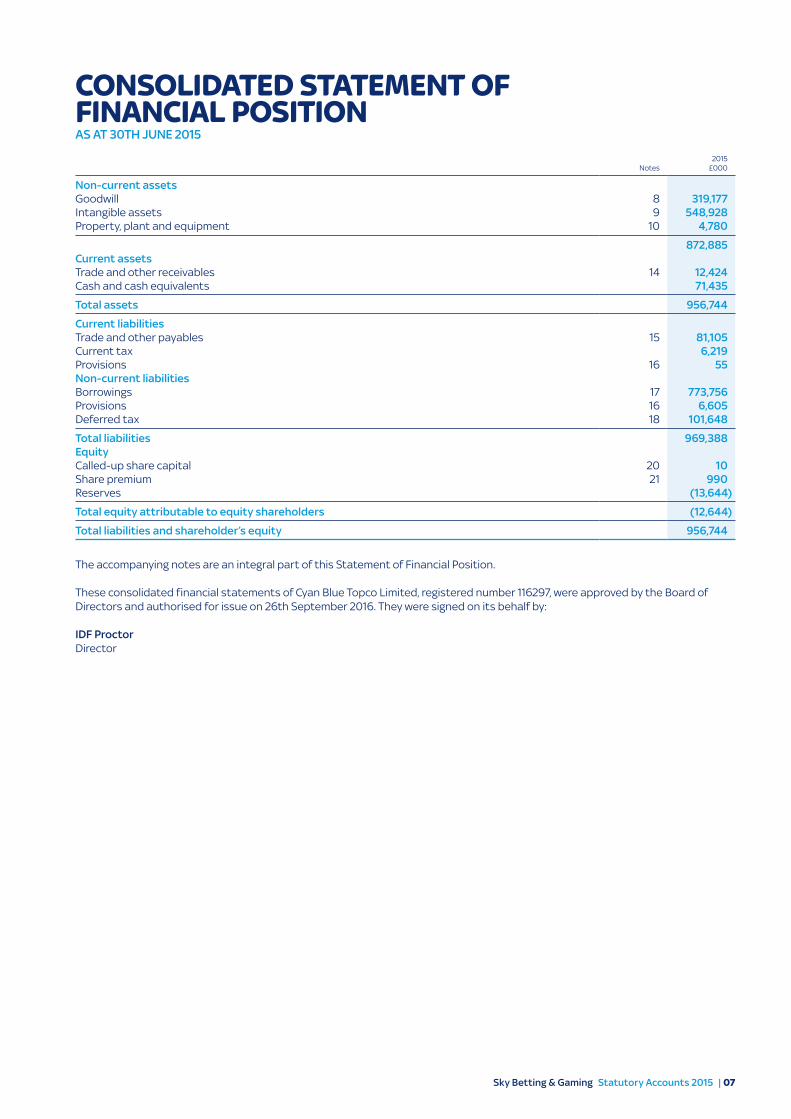

Notes2015

£000

Non-current assetsGoodwill 8 319,177Intangible assets 9 548,928Property, plant and equipment 10 4,780

872,885Current assetsTrade and other receivables 14 12,424Cash and cash equivalents 71,435

Total assets 956,744

Current liabilitiesTrade and other payables 15 81,105Current tax 6,219Provisions 16 55Non-current liabilitiesBorrowings 17 773,756Provisions 16 6,605Deferred tax 18 101,648

Total liabilities 969,388EquityCalled-up share capital 20 10Share premium 21 990Reserves (13,644)

Total equity attributable to equity shareholders (12,644)

Total liabilities and shareholder’s equity 956,744

The accompanying notes are an integral part of this Statement of Financial Position.

These consolidated financial statements of Cyan Blue Topco Limited, registered number 116297, were approved by the Board of Directors and authorised for issue on 26th September 2016. They were signed on its behalf by:

IDF ProctorDirector

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAS AT 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 08

COMPANY STATEMENT OF FINANCIAL POSITIONAS AT 30TH JUNE 2015

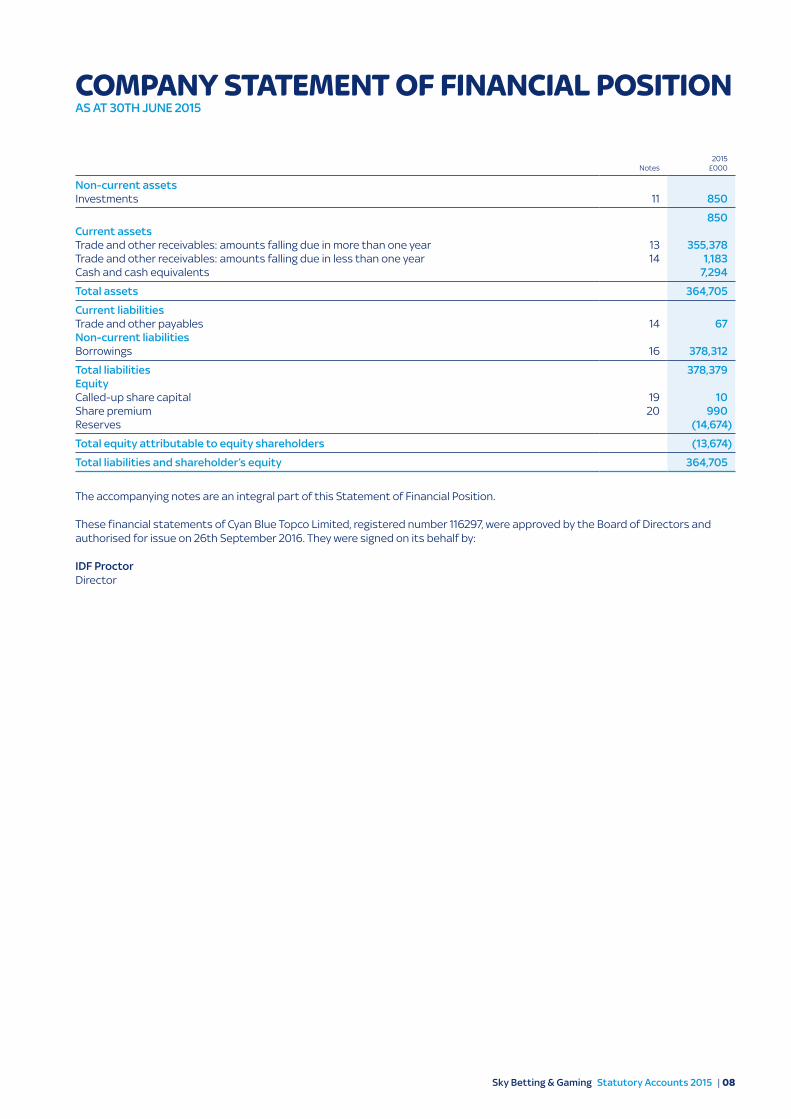

Notes2015

£000

Non-current assetsInvestments 11 850

850Current assetsTrade and other receivables: amounts falling due in more than one year 13 355,378Trade and other receivables: amounts falling due in less than one year 14 1,183Cash and cash equivalents 7,294

Total assets 364,705

Current liabilitiesTrade and other payables 14 67Non-current liabilitiesBorrowings 16 378,312

Total liabilities 378,379EquityCalled-up share capital 19 10Share premium 20 990Reserves (14,674)

Total equity attributable to equity shareholders (13,674)

Total liabilities and shareholder’s equity 364,705

The accompanying notes are an integral part of this Statement of Financial Position.

These financial statements of Cyan Blue Topco Limited, registered number 116297, were approved by the Board of Directors and authorised for issue on 26th September 2016. They were signed on its behalf by:

IDF ProctorDirector

Sky Betting & Gaming Statutory Accounts 2015 | 09

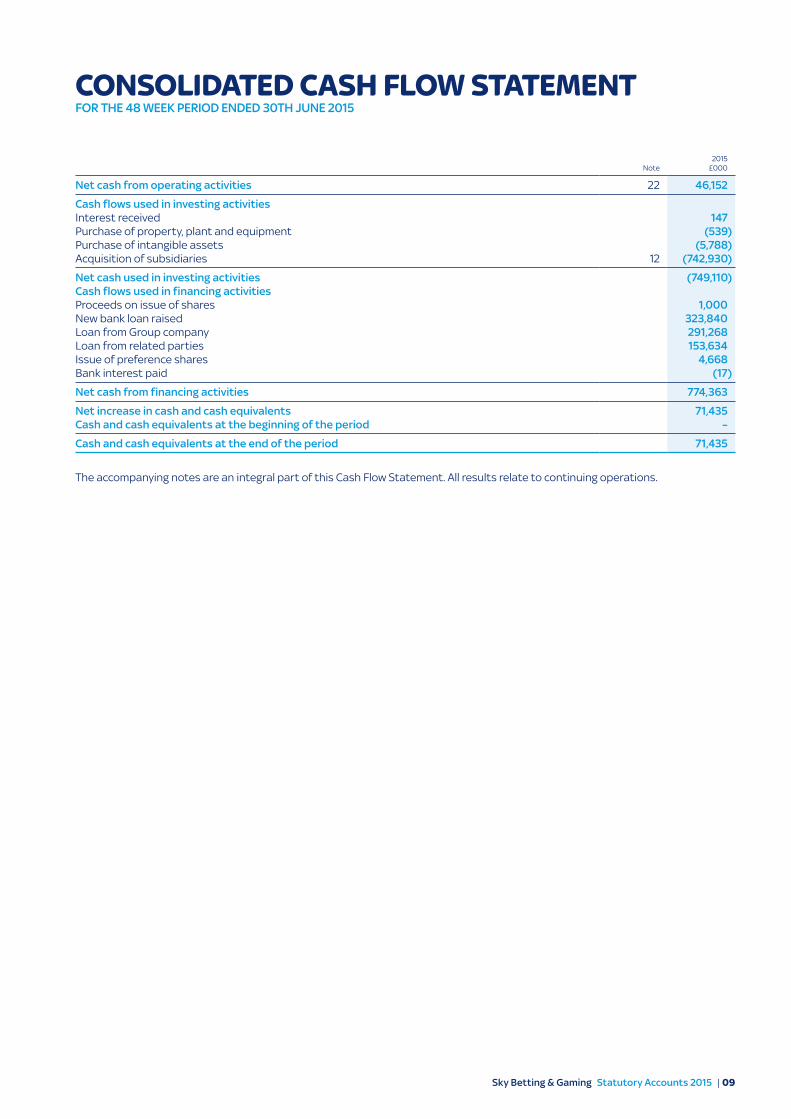

Note2015

£000

Net cash from operating activities 22 46,152

Cash flows used in investing activitiesInterest received 147Purchase of property, plant and equipment (539)Purchase of intangible assets (5,788)Acquisition of subsidiaries 12 (742,930)

Net cash used in investing activities (749,110)Cash flows used in financing activitiesProceeds on issue of shares 1,000New bank loan raised 323,840Loan from Group company 291,268Loan from related parties 153,634Issue of preference shares 4,668Bank interest paid (17)

Net cash from financing activities 774,363

Net increase in cash and cash equivalents 71,435Cash and cash equivalents at the beginning of the period –

Cash and cash equivalents at the end of the period 71,435

The accompanying notes are an integral part of this Cash Flow Statement. All results relate to continuing operations.

CONSOLIDATED CASH FLOW STATEMENTFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 10

COMPANY CASH FLOW STATEMENTFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

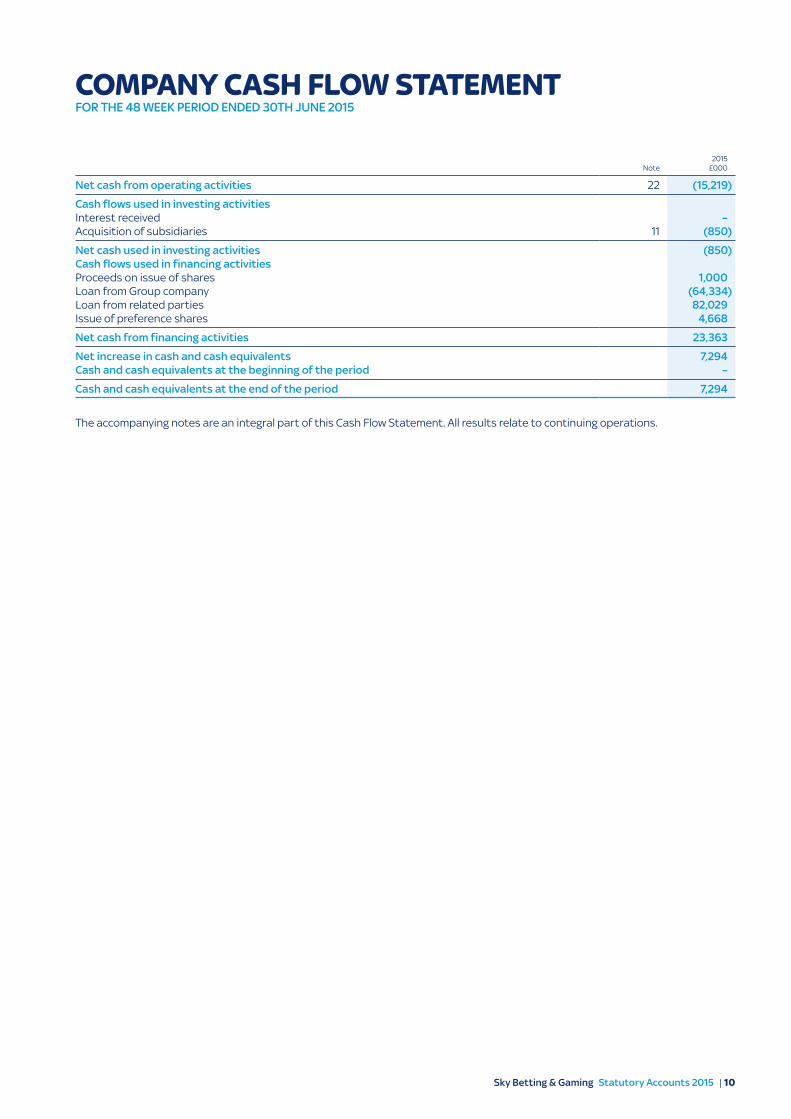

Note2015

£000

Net cash from operating activities 22 (15,219)

Cash flows used in investing activitiesInterest received –Acquisition of subsidiaries 11 (850)

Net cash used in investing activities (850)Cash flows used in financing activitiesProceeds on issue of shares 1,000Loan from Group company (64,334)Loan from related parties 82,029Issue of preference shares 4,668

Net cash from financing activities 23,363

Net increase in cash and cash equivalents 7,294Cash and cash equivalents at the beginning of the period –

Cash and cash equivalents at the end of the period 7,294

The accompanying notes are an integral part of this Cash Flow Statement. All results relate to continuing operations.

Sky Betting & Gaming Statutory Accounts 2015 | 11

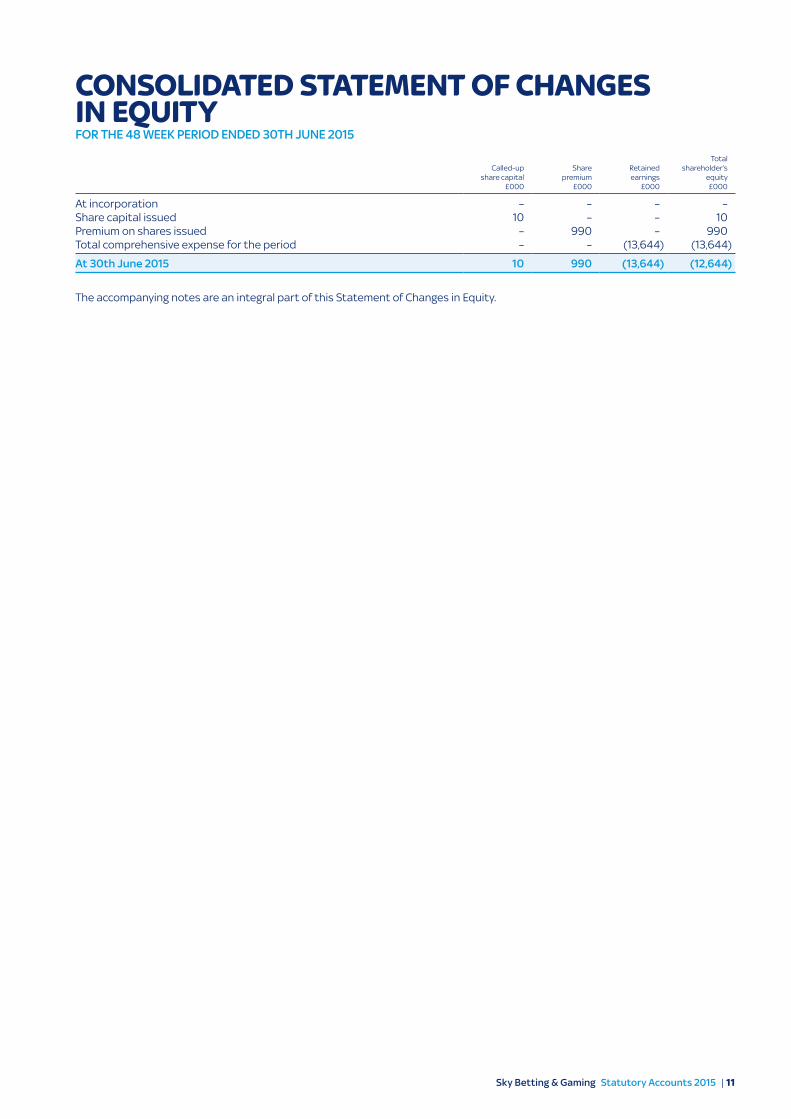

Called-up share capital

£000

Share premium

£000

Retained earnings

£000

Total shareholder’s

equity £000

At incorporation – – – –Share capital issued 10 – – 10Premium on shares issued – 990 – 990Total comprehensive expense for the period – – (13,644) (13,644)

At 30th June 2015 10 990 (13,644) (12,644)

The accompanying notes are an integral part of this Statement of Changes in Equity.

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 12

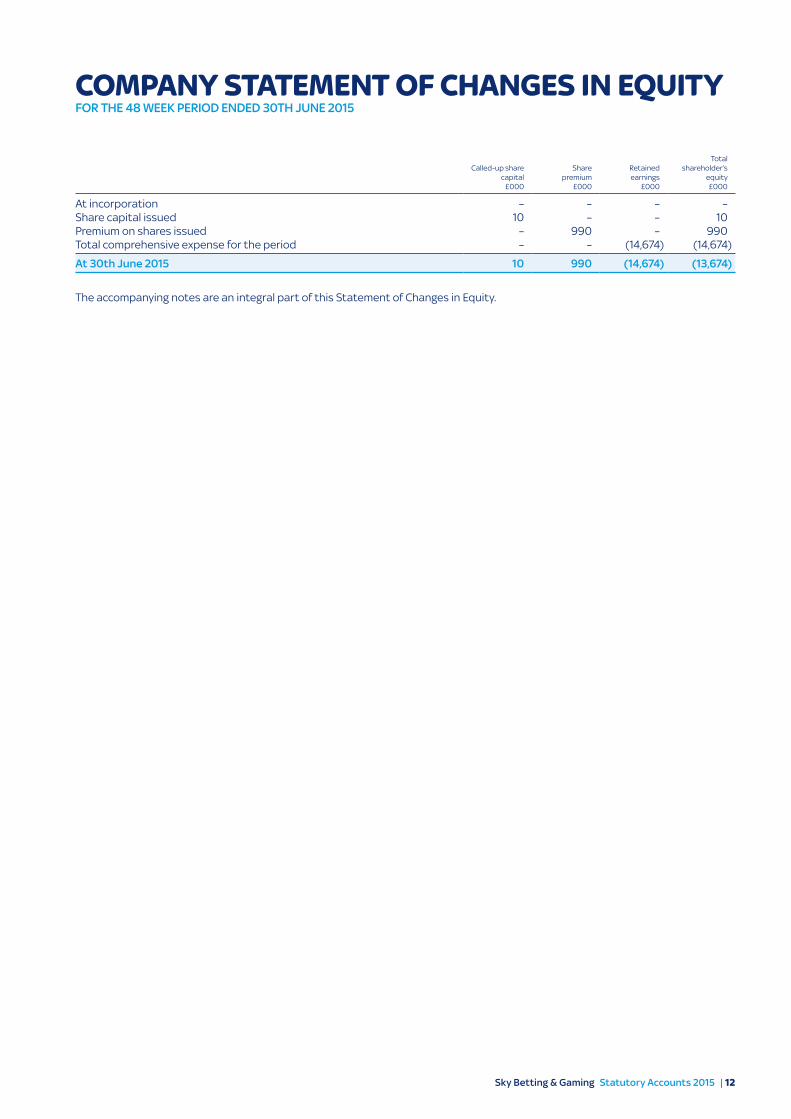

Called-up share capital

£000

Share premium

£000

Retained earnings

£000

Total shareholder’s

equity £000

At incorporation – – – –Share capital issued 10 – – 10Premium on shares issued – 990 – 990Total comprehensive expense for the period – – (14,674) (14,674)

At 30th June 2015 10 990 (14,674) (13,674)

The accompanying notes are an integral part of this Statement of Changes in Equity.

COMPANY STATEMENT OF CHANGES IN EQUITYFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 13

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

1. ACCOUNTING POLICIESGeneral informationCyan Blue Topco Limited (‘the Company’) is a company incorporated on the Island of Jersey under the Companies (Jersey) Law 1991. The principal activities of the Company and its subsidiaries (‘the Group’) and the nature of the Group’s operations are set out in the Product Line-up on pages 4 and 5 of the Annual Review.

These financial statements are presented in pounds sterling because that is the currency of the primary economic environment in which the Group operates.

a) Basis of consolidationThe consolidated financial statements incorporate the financial statements of the Company and entities controlled by the Company (‘the subsidiaries’) made up to 30th June each year. The Group maintains a 52 or 53 week fiscal year ending on the Sunday nearest to 30th June in each year. In fiscal year 2015, this date was 28th June 2015. Since this is within seven days of 30th June each year, the requirements of the Companies Act with regard to the dating of the financial statements are met.

Consolidation of a subsidiary begins when the Company obtains control over the subsidiary and ceases when the Company loses control of the subsidiary. Specifically, the results of subsidiaries acquired or disposed of during the period are included in the Consolidated Statement of Comprehensive Income (‘SCI’) from the date the Company gains control until the date when the Company ceases to control the subsidiary.

Control is achieved when the Company:• has power over the investee;• is exposed, or has rights, to variable returns from its involvement with the investee; and• has the ability to use its power to affect its returns.

All intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between the members of the Group are eliminated on consolidation.

b) Basis of preparationThe financial statements have been prepared in accordance with International Financial Reporting Standards (‘IFRS’) as adopted by the European Union (‘EU’) and the Companies (Jersey) Law 1991. In addition, the Group also complied with IFRS as issued by the International Accounting Standards Board (‘IASB’).

The financial statements have been prepared on a going concern basis and on a historical cost basis, except for the remeasurement to fair value of financial instruments, as described in the accounting policies below. The Group has adopted the new accounting pronouncements which became effective this period; none of which had any significant impact on the Group’s results or financial position.

c) Business combinationsAcquisitions of subsidiaries and businesses are accounted for using the acquisition method. The consideration transferred in a business combination is measured at fair value, which is calculated as the sum of the acquisition date fair values of assets transferred to the Group, liabilities incurred by the Group and the equity interest issued by the Group in exchange for control of the acquiree. Acquisition related costs are recognised in profit or loss as incurred.

At the acquisition date, the identifiable assets acquired and the liabilities assumed are recognised at their fair value, except:• deferred tax assets or liabilities and assets or liabilities related to employee benefit arrangements which are recognised and

measured in accordance with IAS 12 ‘Income Taxes’ and IAS 19 ‘Employee Benefits’ respectively; and• assets (or disposal groups) that are classified as held for sale in accordance with IFRS 5 ‘Non-current Assets Held for Sale and

Discontinued Operations’ are measured in accordance with that Standard.

Goodwill is measured as the excess of the sum of the consideration transferred, the amount of any non-controlling interests in the acquiree, and the fair value of the acquirer’s previously held equity interest in the acquiree (if any) over the net of the acquisition date amounts of the identifiable assets acquired and the liabilities assumed. If, after reassessment, the net of the acquisition date amounts of the identifiable assets acquired and liabilities assumed exceeds the sum of the consideration transferred, the amount of any non-controlling interests in the acquiree and the fair value of the acquirer’s previously held interest in the acquiree (if any), the excess is recognised immediately in the SCI as a bargain purchase gain.

If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the Group reports provisional amounts for the items for which the accounting is incomplete. Those provisional amounts are adjusted during the measurement period, or additional assets or liabilities are recognised, to reflect new information obtained about facts and circumstances that existed as at the acquisition date that, if known, would have affected the amounts recognised on that date.

Sky Betting & Gaming Statutory Accounts 2015 | 14

1. ACCOUNTING POLICIES continued

d) GoodwillGoodwill is initially recognised and measured as set out on the previous page.

Goodwill is not amortised but is reviewed for impairment at least annually. For the purpose of impairment testing, goodwill is allocated to each of the Group’s cash generating units expected to benefit from the synergies of the combination. Cash generating units (‘CGU’s’) to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired. If the recoverable amount of the CGU is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro rata on the basis of the carrying amount of each asset in the unit. An impairment loss recognised for goodwill is not reversed in a subsequent period.

e) LeasesLeases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Rentals payable under operating leases are charged to income on a straight-line basis over the term of the relevant lease except where another more systematic basis is more representative of the time pattern in which economic benefits from the lease asset are consumed. Contingent rentals arising under operating leases are recognised as an expense in the period in which they are incurred.

In the event that lease incentives are received to enter into operating leases, such incentives are recognised as a liability. The aggregate benefit of incentives is recognised as a reduction of rental expense on a straight-line basis over the lease term, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed.

f) Retirement benefit costsPayments to defined contribution retirement benefit schemes are recognised as an expense when employees have rendered services entitling them to the contributions. Payments made to state-managed retirement benefit schemes are dealt with as payments to defined contribution schemes where the Group’s obligations under the schemes are equivalent to those arising in a defined contribution retirement benefit scheme.

g) Intangible assets and property, plant and equipment (‘PPE’)i. Intangible assetsResearch expenditure is recognised in operating expense in the SCI as the expenditure is incurred. An internally-generated intangible asset arising from development (or from the development phase of an internal project) is recognised if, and only if, all of the following conditions have been demonstrated:• The technical feasibility of completing the intangible asset so that it will be available for use or sale.• The intention to complete the intangible asset and use or sell it.• The ability to use or sell the intangible asset.• How the intangible asset will generate probable future economic benefits.• The availability of adequate technical, financial and other resources to complete the development and to use or sell the

intangible asset. • The ability to measure reliably the expenditure attributable to the intangible asset during its development.

The amount initially recognised for internally generated intangible assets is the sum of the expenditure incurred from the date when the intangible asset first meets the recognition criteria listed above. Any other development expenditure is recognised in operating expense as incurred. Subsequent to initial recognition, internally generated intangible assets are reported at cost less accumulated amortisation and accumulated impairment losses, on the same basis as intangible assets that are acquired separately.

Other intangible assets, which are acquired by the Group separately or through a business combination, are stated at cost or fair value, respectively, less accumulated amortisation and impairment losses, other than those that are classified as held for sale, which are stated at the lower of carrying amount and fair value less costs to sell. Intangible assets acquired in a business combination are recognised separately from goodwill.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 15

1. ACCOUNTING POLICIES continued

Amortisation of an intangible asset begins from the start of the month nearest to when the asset is available for use and is charged to the SCI through operating expenses on a straight-line basis over the intangible asset’s estimated useful life unless the asset life is judged to be indefinite. If the useful life is indefinite or the asset is not yet available for use, no amortisation is charged and an impairment test is carried out at least annually. The Group’s intangible assets are amortised in line with accounting policy below:

Internally generated intangible assets 4 yearsCustomer relations 8–16 yearsTechnology 5–10 yearsOther intangible assets 3–25 years

ii. Property, plant and equipmentOwned PPE is stated at cost, net of accumulated depreciation and any impairment losses, (see accounting policy i), other than those items that are classified as held for sale, which are stated at the lower of carrying amount and fair value less costs to sell. When an item of PPE comprises major components having different useful economic lives, the components are accounted for as separate items of PPE.

The cost of PPE is depreciated in operating expense on a straight-line basis over its estimated useful life. Land and assets that are not yet available for use are not depreciated. Principal useful economic lives used for this purpose are:

Equipment, furniture and fixtures 4 years

h) Financial instrumentsFinancial assets and liabilities are initially recognised at fair value plus any directly attributable transaction costs. At each Consolidated Statement of Financial Position (‘SFP’) date, the Group assesses whether there is any objective evidence that any financial asset is impaired. Financial assets and liabilities are recognised on the SFP when the Group becomes a party to the contractual provisions of the financial asset or liability. Financial assets are derecognised from the SFP when the Group’s contractual rights to the cash flows expire or the Group transfers substantially all the risks and rewards of the financial asset. Financial liabilities are derecognised from the SFP when the obligation specified in the contract is discharged, cancelled or expires.

i. Financial assetsAll financial assets are recognised and derecognised on a trade date where the purchase or sale of a financial asset is under a contract whose terms require delivery of the financial asset within the timeframe established by the market concerned, and are initially measured at fair value plus transaction costs, except for those financial assets classified at fair value through profit or loss, which are initially measured at fair value.

Financial assets are classified into the following specified categories: financial assets ‘at fair value through profit or loss’ (‘FVTPL’); ‘held-to-maturity’ investments, ‘available-for-sale’ (‘AFS’); financial assets; and ‘loans and receivables’. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition.

ii. Loans and receivablesTrade and other receivables are non-derivative financial assets with fixed or determinable payments and, where no stated interest rate is applicable, are measured at the original invoice amount, if the effect of discounting is immaterial. Where discounting is material, trade and other receivables are measured at amortised cost using the effective interest method. An allowance account is maintained to reduce the carrying value of trade and other receivables for impairment losses identified from objective evidence, with movements in the allowance account, either from increased impairment losses or reversals of impairment losses, being recognised in the SCI.

iii. Effective interest methodThe effective interest method is a method of calculating the amortised cost of a debt instrument and of allocating interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts (including all fees and points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the debt instrument, or, where appropriate, a shorter period, to the net carrying amount on initial recognition.

iv. Impairment of financial assetsFinancial assets, other than those at FVTPL, are assessed for indicators of impairment at each SFP date. Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investment have been affected.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 16

1. ACCOUNTING POLICIES continued

For certain categories of financial asset, such as trade receivables, assets that are assessed not to be impaired individually are, in addition, assessed for impairment on a collective basis. Objective evidence of impairment for a portfolio of receivables could include the Group’s past experience of collecting payments, an increase in the number of delayed payments in the portfolio past the average credit period of 60 days, as well as observable changes in national or local economic conditions that correlate with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment is the differences between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial asset’s original effective interest rate.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of trade receivables, where the carrying amount is reduced through the use of an allowance account. When a trade receivable is considered uncollectable, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against the allowance account. Changes in the carrying amount of the allowance account are recognised in the SCI.

v. Cash and cash equivalentsCash and cash equivalents include cash in hand, bank accounts, deposits receivable on demand and deposits with maturity dates of three months or less from the date of inception. Bank overdrafts that are repayable on demand and which form an integral part of the Group’s cash management are included as a component of cash and cash equivalents where offset conditions are met.

vi. Financial liabilitiesFinancial liabilities are classified as either financial liabilities ‘at FVTPL’ or ‘other financial liabilities’.

vii. Other financial liabilitiesTrade and other payables are non-derivative financial liabilities and are measured at amortised cost using the effective interest method. Trade and other payables with no stated interest rate are measured at the original invoice amount if the effect of discounting is immaterial.

The effective interest method is a method of calculating the amortised cost of a financial liability and of allocating interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period, to the net carrying amount on initial recognition.

i) ImpairmentAt each SFP date, and in accordance with IAS 36 ‘Impairment of Assets’, the Group reviews the carrying amounts of all its assets excluding financial assets (see accounting policy h) and deferred taxation (see accounting policy l) to determine whether there is any indication that any of those assets have suffered an impairment loss.

An impairment is recognised in the SCI whenever the carrying amount of an asset or its CGU exceeds its recoverable amount. The recoverable amount is the greater of net selling price, defined as the fair value less costs to sell, and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and risks specific to the asset. Where it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the CGU to which to which the asset belongs.

An impairment loss for an individual asset or CGU shall be reversed if there has been a change in estimates used to determine the recoverable amount since the last impairment loss was recognised and is only reversed to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

j) ProvisionsProvisions are recognised when the Group has a probable, present legal or constructive obligation to make a transfer of economic benefits as a result of past events where a reliable estimate is available. The amounts recognised represent the Group’s best estimate of the transfer of benefits that will be required to settle the obligation as of the SFP date. Provisions are discounted if the effect of the time value of money is material using a pre-tax market rate adjusted for risks specific to the liability.

Present obligations arising under onerous contracts are recognised and measured as provisions. An onerous contract is considered to exist where the Group has a contract under which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received under it.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 17

1. ACCOUNTING POLICIES continued

k) Revenue recognitionRevenue, which excludes value added tax, represents the gross inflow of economic benefit from the Group’s operating activities. The Group’s main sources of revenue are recognised as follows:• Betting revenues are recognised in accordance with IAS 18 ‘Revenue’ (‘IAS 18’). All revenues therefore represent income in the

period for betting activities, defined as amounts staked by customers less betting payouts and free bet costs. Ante-post bets (bets staked but not settled) are excluded from revenue and are deferred on the balance sheet in trade and other payables until the event to which they relate has concluded, at which time they are matched with any related payouts. The liability is revalued to fair value at each balance sheet date, in accordance with IAS 39 ‘Financial Instruments Recognition and Measurement’ (‘IAS 39’), with any gain or loss recognised in the SCI.

• Gaming revenues represents net customer losses in the period in respect of the online, mobile telephone and interactive TV gaming, poker and bingo operations. Revenues generated through the principal activities of providing online betting and gaming related information and content to customers are recognised in the period in which the service has been provided.

l) Tax, including deferred taxThe tax expense represents the sum of the tax currently payable and deferred tax. The Group’s liability for current tax is based on taxable profits for the year, and is calculated using tax rates that have been enacted or substantively enacted at the balance sheet date. The tax currently payable is based on taxable profit for the year. Taxable profit differs from net profit as reported in the SCI because it excludes items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible.

Deferred tax assets and liabilities are recognised using the balance sheet liability method, providing for temporary differences between the carrying amounts of assets and liabilities in the SFP and the corresponding tax bases used in the computation of taxable profit. Temporary differences arising from goodwill and the initial recognition of assets or liabilities that affect neither accounting profit nor taxable profit are not provided for. Deferred tax liabilities are recognised for taxable temporary differences arising on investments in subsidiaries and associates, and interests in joint ventures, except where the Group is able to control the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future. The amount of deferred tax provided is based on the expected manner of realisation or settlement of the carrying amount of assets and liabilities, using tax rates that have been enacted or substantively enacted at the SFP date.

The carrying amount of deferred tax assets is reviewed at each SFP date and adjusted to reflect an amount that is probable to be realised based on the weight of all available evidence. Deferred tax is calculated at the rates that are expected to apply in the period when the liability is settled or the asset is realised. Deferred tax assets and liabilities are not discounted. Deferred tax is charged or credited in the SCI, except where it relates to items charged or credited directly to equity, in which case the deferred tax is also included within equity.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the Group intends to settle its current tax assets and liabilities on a net basis.

m) Critical accounting judgements and key sources of estimation uncertaintyCertain accounting policies are considered to be critical to the Group. An accounting policy is considered to be critical if its selection or application materially affects the Group’s financial position or results. The Directors are required to use their judgement in order to select and apply the Group’s critical accounting policies. Below is a summary of the Group’s critical accounting policies and details of the key areas of judgement that are exercised in their application.

Critical accounting policiesi. Revenue recognitionRevenue, which excludes value added tax, represents the gross inflow of economic benefit from the Group’s operating activities. Revenue is measured at the fair value of the consideration received or receivable.

Critical accounting judgementsi. TaxThe Group’s tax charge is the sum of the total current and deferred tax charges. The calculation of the Group’s total tax charge necessarily involves a degree of estimation and judgement in respect of certain items whose tax treatment cannot be finally determined until resolution has been reached with the relevant tax authority or, as appropriate, through the formal legal process.

The amounts recognised in the financial statements in respect of each matter are derived from the Group’s best estimation and judgement, as described above. However, the inherent uncertainty regarding the outcome of these means the eventual resolution could differ from the provision, and, in such an event, the Group would be required to make an adjustment in a subsequent period which could have a material impact on the Group’s profit and or cash position.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 18

1. ACCOUNTING POLICIES continued

ii. Deferred taxationAn estimation of the current tax liability together with an assessment of the temporary differences, which arise as a consequence of different tax and accounting treatments, is required. Assumptions are also made around the extent to which future taxable profits will be available to offset any deferred tax assets carried on the SFP.

iii. ReceivablesJudgement is required in evaluating the likelihood of collection of debt, including intercompany debt. This evaluation requires estimates to be made, including the level of provision to be made for amounts with uncertain recovery profiles.

n) Adoption of new and revised StandardsThe following new and revised Standards and Interpretations have been adopted in the current period. The application of these specific Standards and Interpretations has not had a material effect on the Group.

New and revised Standards on consolidation, joint arrangements, associates and disclosure

In May 2011, a package of five Standards on consolidation, joint arrangements, associates and disclosures was issued comprising IFRS 10 ‘Consolidated Financial Statements’, IFRS 11 ‘Joint Arrangements’, IFRS 12 ‘Disclosure of Interests in Other Entities’, IAS 27 (as revised in 2011) ‘Separate Financial Statements’ and IAS 28 (as revised in 2011) ‘Investments in Associates and Joint Ventures’. Subsequent to the issue of these Standards, amendments to IFRS 10, IFRS 11 and IFRS 12 were issued to clarify certain transitional guidance on the first-time application of the Standards.

In the current period, the Group has applied for the first time IFRS 10, IFRS 11, IFRS 12 and IAS 28 (as revised in 2011) together with the amendments to IFRS 10, IFRS 11 and IFRS 12 regarding the transitional guidance. IAS 27 (as revised in 2011) has also been applied and it deals only with separate financial statements.

None of these Standards has had an impact on the financial statements.

IFRS 13 ‘Fair Value Measurement’ The Group has applied IFRS 13 for the first time in the current period. IFRS 13 establishes a single source of guidance for fair value measurements and disclosures about fair value measurements. The scope of IFRS 13 is broad; the fair value measurement requirements of IFRS 13 apply to both financial instrument items and non-financial instrument items for which other IFRS require or permit fair value measurements and disclosures about fair value measurements, except for share-based payment transactions that are within the scope of IFRS 2 ‘Share-based Payment’, leasing transactions that are within the scope of IAS 17 ‘Leases’, and measurements that have some similarities to fair value but are not fair value (e.g. net realisable value for the purposes of measuring inventories or value in use for impairment assessment purposes).

IFRS 13 defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions. Fair value under IFRS 13 is an exit price regardless of whether that price is directly observable or estimated using another valuation technique. Also, IFRS 13 includes extensive disclosure requirements.

IFRS 13 requires prospective application from 1st January 2013. In addition, specific transitional provisions were given to entities such that they need not apply the disclosure requirements set out in the Standard in comparative information provided for periods before the initial application of the Standard. The application of IFRS 13 has not had any material impact on the amounts recognised in the financial statements.

Amendments to IAS 1 ‘Presentation of Financial Statements’(as part of the Annual Improvements to IFRS 2009/11 Cycle issued in May 2012)

The Annual Improvements to IFRS 2009/11 have made a number of amendments to IFRS. The amendments that are relevant to the Group are the amendments to IAS 1 regarding when a statement of financial position as at the beginning of the preceding period (third statement of financial position) and the related notes are required to be presented. The amendments specify that a third statement of financial position is required when a) an entity applies an accounting policy retrospectively, or makes a retrospective restatement or reclassification of items in its financial statements, and b) the retrospective application, restatement or reclassification has a material effect on the information in the third statement of financial position. The amendments specify that related notes are not required to accompany the third statement of financial position.

This has not resulted in any material adjustments to the financial statements.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 19

1. ACCOUNTING POLICIES continued

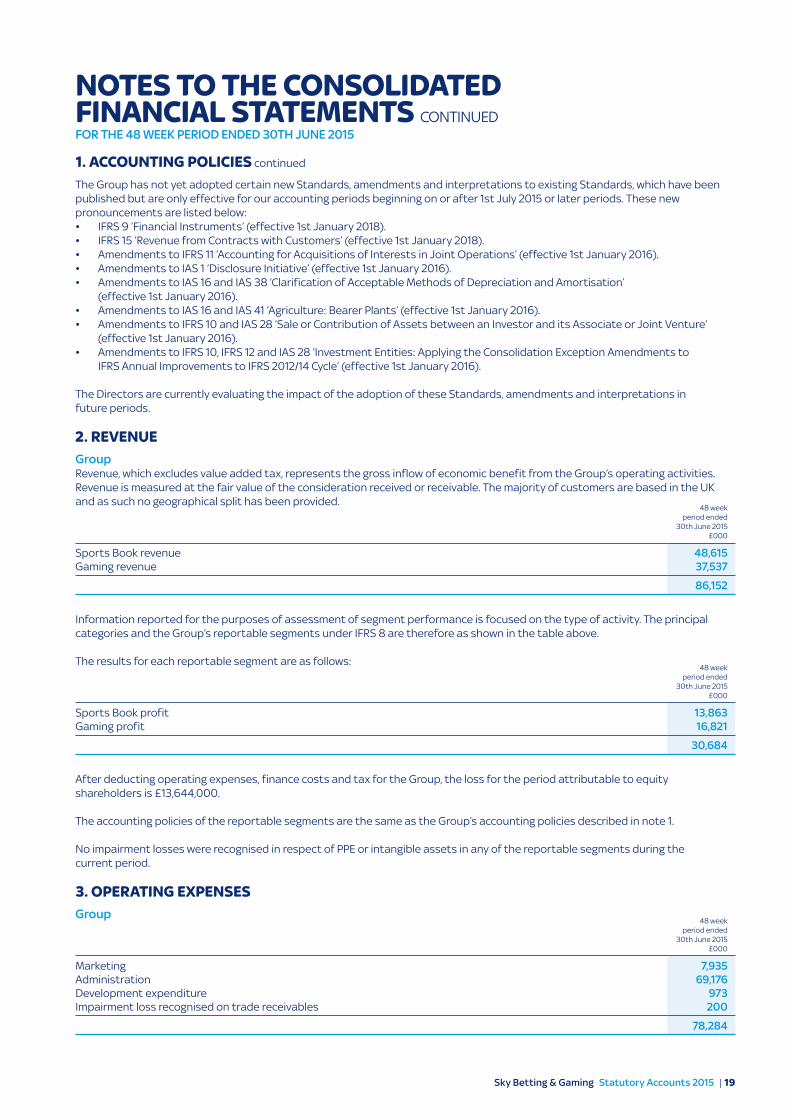

The Group has not yet adopted certain new Standards, amendments and interpretations to existing Standards, which have been published but are only effective for our accounting periods beginning on or after 1st July 2015 or later periods. These new pronouncements are listed below:• IFRS 9 ‘Financial Instruments’ (effective 1st January 2018).• IFRS 15 ‘Revenue from Contracts with Customers’ (effective 1st January 2018).• Amendments to IFRS 11 ‘Accounting for Acquisitions of Interests in Joint Operations’ (effective 1st January 2016).• Amendments to IAS 1 ‘Disclosure Initiative’ (effective 1st January 2016).• Amendments to IAS 16 and IAS 38 ‘Clarification of Acceptable Methods of Depreciation and Amortisation’

(effective 1st January 2016).• Amendments to IAS 16 and IAS 41 ‘Agriculture: Bearer Plants’ (effective 1st January 2016).• Amendments to IFRS 10 and IAS 28 ‘Sale or Contribution of Assets between an Investor and its Associate or Joint Venture’

(effective 1st January 2016).• Amendments to IFRS 10, IFRS 12 and IAS 28 ‘Investment Entities: Applying the Consolidation Exception Amendments to

IFRS Annual Improvements to IFRS 2012/14 Cycle’ (effective 1st January 2016).

The Directors are currently evaluating the impact of the adoption of these Standards, amendments and interpretations in future periods.

2. REVENUEGroupRevenue, which excludes value added tax, represents the gross inflow of economic benefit from the Group’s operating activities. Revenue is measured at the fair value of the consideration received or receivable. The majority of customers are based in the UK and as such no geographical split has been provided.

48 week period ended

30th June 2015 £000

Sports Book revenue 48,615Gaming revenue 37,537

86,152

Information reported for the purposes of assessment of segment performance is focused on the type of activity. The principal categories and the Group’s reportable segments under IFRS 8 are therefore as shown in the table above.

The results for each reportable segment are as follows:48 week

period ended 30th June 2015

£000

Sports Book profit 13,863Gaming profit 16,821

30,684

After deducting operating expenses, finance costs and tax for the Group, the loss for the period attributable to equity shareholders is £13,644,000.

The accounting policies of the reportable segments are the same as the Group’s accounting policies described in note 1.

No impairment losses were recognised in respect of PPE or intangible assets in any of the reportable segments during the current period.

3. OPERATING EXPENSESGroup

48 week period ended

30th June 2015 £000

Marketing 7,935Administration 69,176Development expenditure 973Impairment loss recognised on trade receivables 200

78,284

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 20

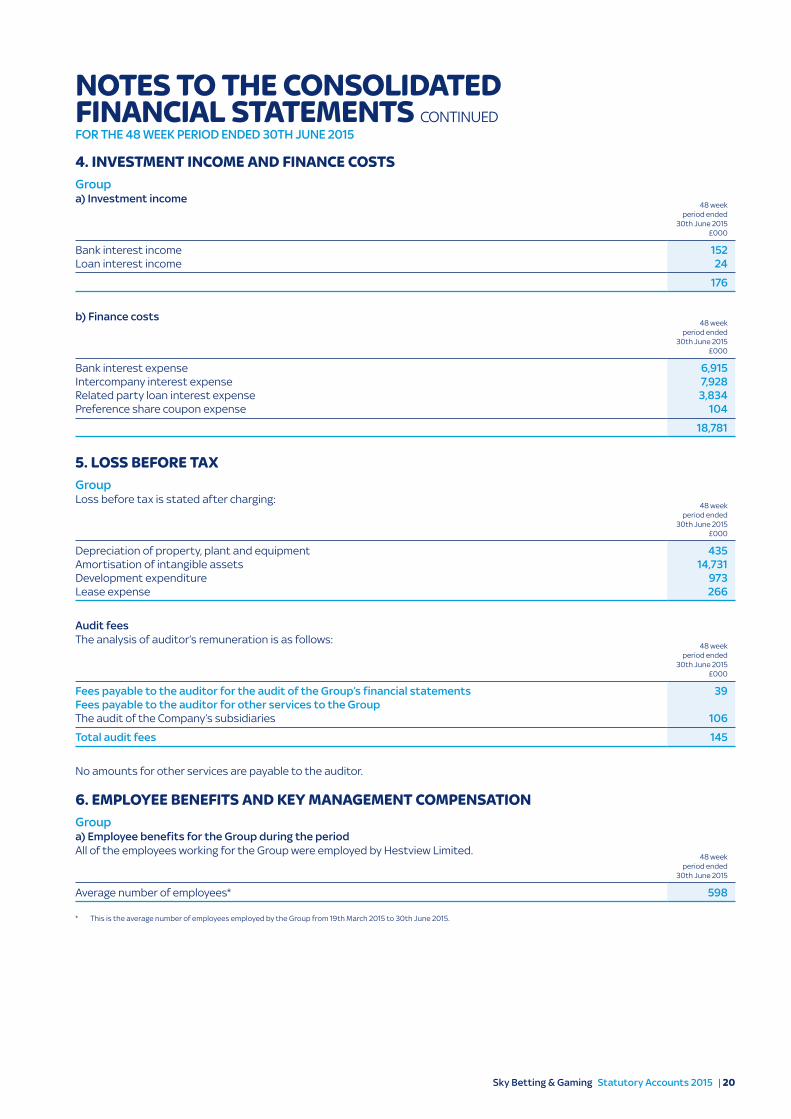

4. INVESTMENT INCOME AND FINANCE COSTSGroupa) Investment income

48 week period ended

30th June 2015 £000

Bank interest income 152Loan interest income 24

176

b) Finance costs48 week

period ended 30th June 2015

£000

Bank interest expense 6,915Intercompany interest expense 7,928Related party loan interest expense 3,834Preference share coupon expense 104

18,781

5. LOSS BEFORE TAXGroupLoss before tax is stated after charging:

48 week period ended

30th June 2015 £000

Depreciation of property, plant and equipment 435Amortisation of intangible assets 14,731Development expenditure 973Lease expense 266

Audit feesThe analysis of auditor’s remuneration is as follows:

48 week period ended

30th June 2015 £000

Fees payable to the auditor for the audit of the Group’s financial statements 39Fees payable to the auditor for other services to the GroupThe audit of the Company’s subsidiaries 106

Total audit fees 145

No amounts for other services are payable to the auditor.

6. EMPLOYEE BENEFITS AND KEY MANAGEMENT COMPENSATIONGroupa) Employee benefits for the Group during the periodAll of the employees working for the Group were employed by Hestview Limited.

48 week period ended

30th June 2015

Average number of employees* 598

* This is the average number of employees employed by the Group from 19th March 2015 to 30th June 2015.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 21

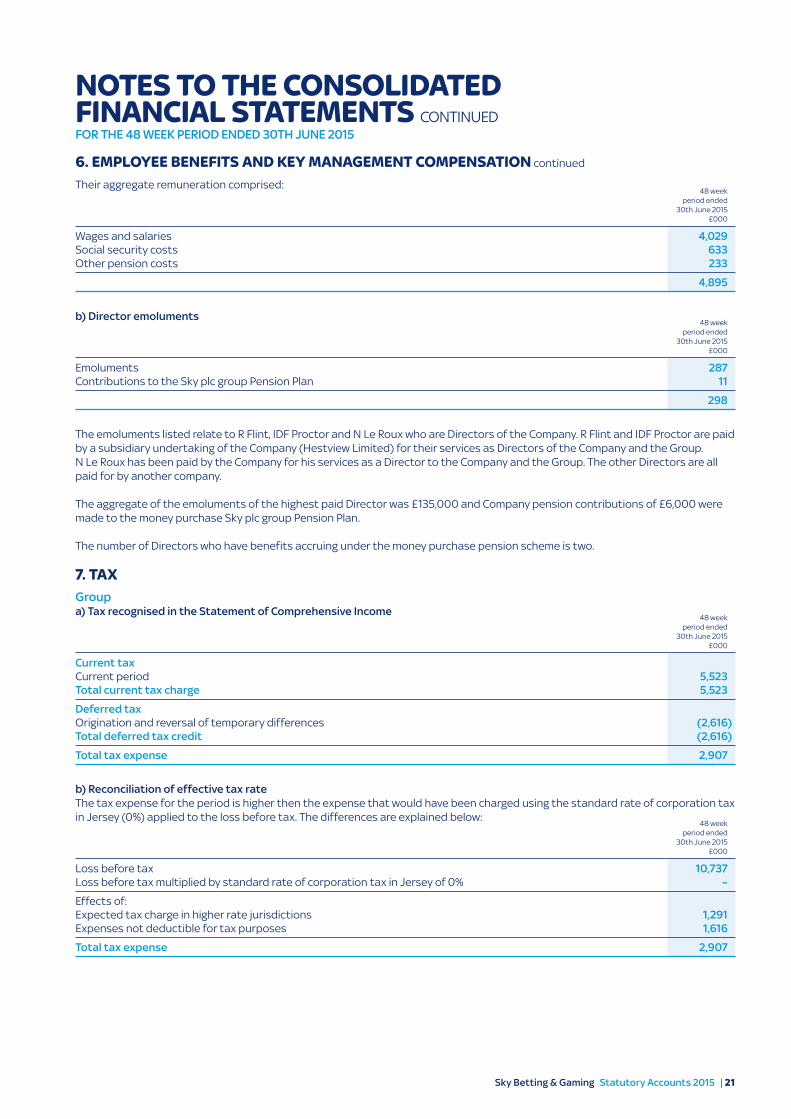

6. EMPLOYEE BENEFITS AND KEY MANAGEMENT COMPENSATION continued

Their aggregate remuneration comprised:48 week

period ended 30th June 2015

£000

Wages and salaries 4,029Social security costs 633Other pension costs 233

4,895

b) Director emoluments48 week

period ended 30th June 2015

£000

Emoluments 287Contributions to the Sky plc group Pension Plan 11

298

The emoluments listed relate to R Flint, IDF Proctor and N Le Roux who are Directors of the Company. R Flint and IDF Proctor are paid by a subsidiary undertaking of the Company (Hestview Limited) for their services as Directors of the Company and the Group. N Le Roux has been paid by the Company for his services as a Director to the Company and the Group. The other Directors are all paid for by another company.

The aggregate of the emoluments of the highest paid Director was £135,000 and Company pension contributions of £6,000 were made to the money purchase Sky plc group Pension Plan.

The number of Directors who have benefits accruing under the money purchase pension scheme is two.

7. TAXGroupa) Tax recognised in the Statement of Comprehensive Income

48 week period ended

30th June 2015 £000

Current taxCurrent period 5,523Total current tax charge 5,523

Deferred taxOrigination and reversal of temporary differences (2,616)Total deferred tax credit (2,616)

Total tax expense 2,907

b) Reconciliation of effective tax rateThe tax expense for the period is higher then the expense that would have been charged using the standard rate of corporation tax in Jersey (0%) applied to the loss before tax. The differences are explained below:

48 week period ended

30th June 2015 £000

Loss before tax 10,737Loss before tax multiplied by standard rate of corporation tax in Jersey of 0% –

Effects of:Expected tax charge in higher rate jurisdictions 1,291Expenses not deductible for tax purposes 1,616

Total tax expense 2,907

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 22

8. GOODWILLGroup

Goodwill £000

Total £000

CostRecognised on acquisition of subsidiaries 319,177 319,177

At 30th June 2015 319,177 319,177

Carrying amounts

At 30th June 2015 319,177 319,177

The goodwill of £319.2m is composed of a number of elements including workforce, future technology and future customers of both SB&G and Oddschecker. None of the goodwill is expected to be deductible for income tax purpose.

Goodwill acquired in a business combination is allocated, at acquisition, to the CGUs or group of units that are expected to benefit from that business combination. Before recognition of impairment losses, the carrying amount of goodwill had been allocated as follows:

£000

Sports Book and Gaming 283,477Oddschecker 35,700

319,177

The Group tests goodwill annually for impairment, or more frequently if there are indications that goodwill might be impaired. No impairment loss was recognised in respect of goodwill during the period.

The recoverable amounts of the CGUs and the group of units are determined from value in use calculations. The key assumptions for the value in use calculations are those regarding the discount rates and growth rates. Management estimates discount rates using pre-tax rates that reflect current market assessments of the time value of money and the risks specific to the CGUs and the group of units. The growth rates are based on industry growth forecasts.

The Group prepares cash flow forecasts derived from the most recent financial budgets approved by management and extrapolates cash flows for the years following the forecast period based on an estimated growth rate.

9. INTANGIBLE ASSETSGroup

Internally-generated intangible

assets £000

Customer relations

£000Technology

£000

Other intangible assets

£000Total

£000

Cost at incorporation – – – – –Acquired on acquisition of subsidiaries 4,347 – – 3,165 7,512Additions 2,913 425,200 36,200 94,479 558,792

At 30th June 2015 7,260 425,200 36,200 97,644 566,304

AmortisationAcquired on acquisition of subsidiaries 1,171 – – 1,474 2,645Amortisation 430 10,006 1,780 2,515 14,731

At 30th June 2015 1,601 10,006 1,780 3,989 17,376

Carrying amounts

At 30th June 2015 5,659 415,194 34,420 93,655 548,928

The Group’s internally-generated intangible assets relate to software development. The Group’s other intangible assets includes external spend on software, software licences, capitalised development costs, and copyright licences.

The estimated future amortisation charge on intangible assets with finite lives for each of the next five years is set out below. It is likely that amortisation will vary from the figures below as the estimate does not include the impact of any future investments, disposals or capital expenditure.

2016 £000

2017 £000

2018 £000

2019 £000

2020 £000

Estimated amortisation charge 49,046 48,503 47,876 47,273 45,688

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 23

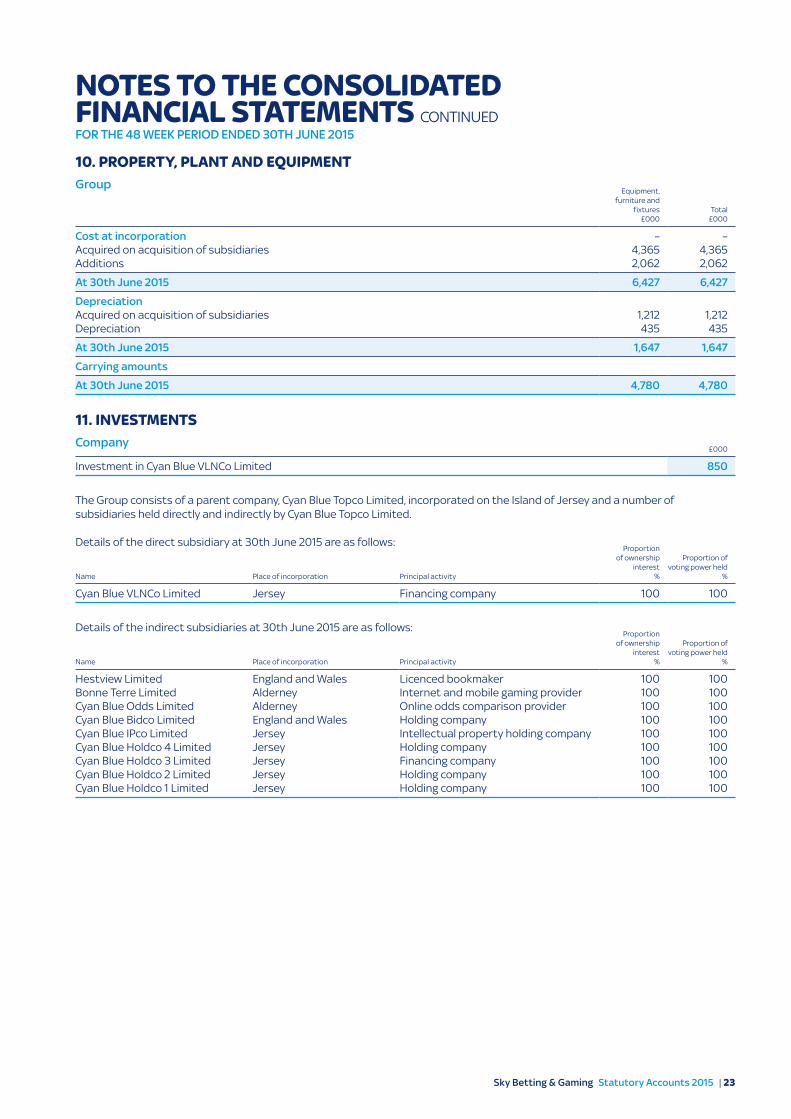

10. PROPERTY, PLANT AND EQUIPMENTGroup

Equipment, furniture and

fixtures £000

Total £000

Cost at incorporation – –Acquired on acquisition of subsidiaries 4,365 4,365Additions 2,062 2,062

At 30th June 2015 6,427 6,427

DepreciationAcquired on acquisition of subsidiaries 1,212 1,212Depreciation 435 435

At 30th June 2015 1,647 1,647

Carrying amounts

At 30th June 2015 4,780 4,780

11. INVESTMENTSCompany

£000

Investment in Cyan Blue VLNCo Limited 850

The Group consists of a parent company, Cyan Blue Topco Limited, incorporated on the Island of Jersey and a number of subsidiaries held directly and indirectly by Cyan Blue Topco Limited.

Details of the direct subsidiary at 30th June 2015 are as follows:

Name Place of incorporation Principal activity

Proportion of ownership

interest %

Proportion of voting power held

%

Cyan Blue VLNCo Limited Jersey Financing company 100 100

Details of the indirect subsidiaries at 30th June 2015 are as follows:

Name Place of incorporation Principal activity

Proportion of ownership

interest %

Proportion of voting power held

%

Hestview Limited England and Wales Licenced bookmaker 100 100Bonne Terre Limited Alderney Internet and mobile gaming provider 100 100Cyan Blue Odds Limited Alderney Online odds comparison provider 100 100Cyan Blue Bidco Limited England and Wales Holding company 100 100Cyan Blue IPco Limited Jersey Intellectual property holding company 100 100Cyan Blue Holdco 4 Limited Jersey Holding company 100 100Cyan Blue Holdco 3 Limited Jersey Financing company 100 100Cyan Blue Holdco 2 Limited Jersey Holding company 100 100Cyan Blue Holdco 1 Limited Jersey Holding company 100 100

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 24

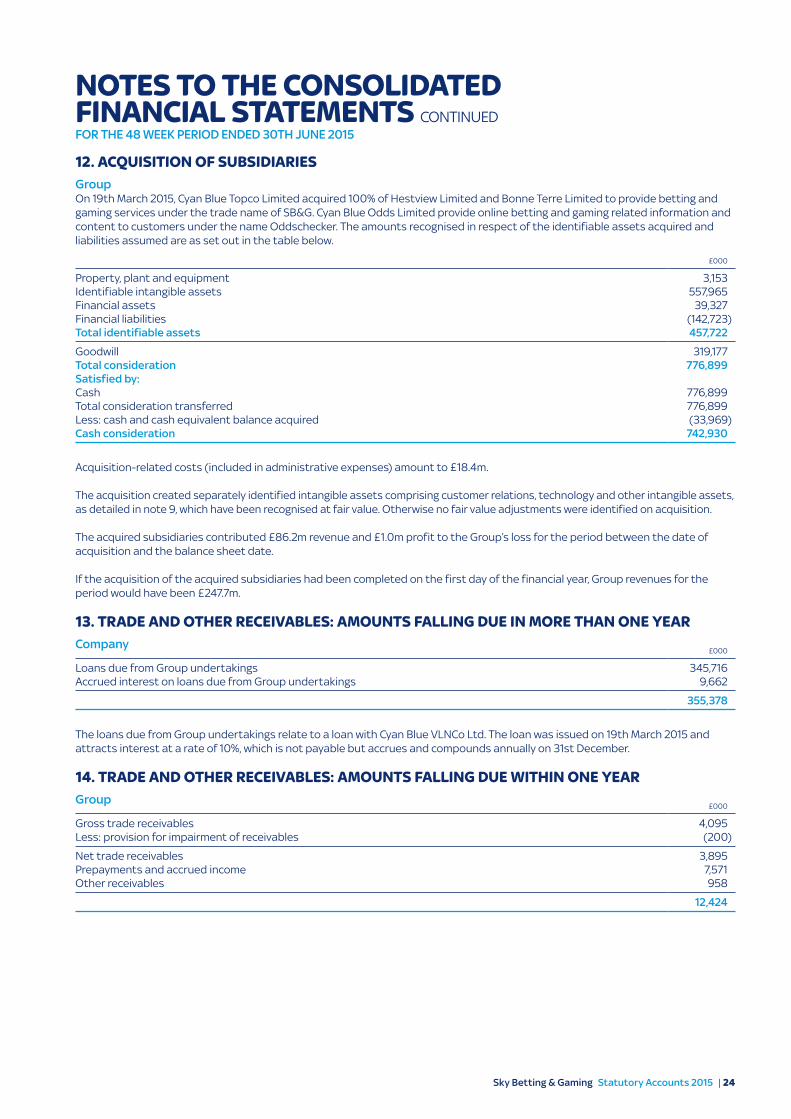

12. ACQUISITION OF SUBSIDIARIESGroupOn 19th March 2015, Cyan Blue Topco Limited acquired 100% of Hestview Limited and Bonne Terre Limited to provide betting and gaming services under the trade name of SB&G. Cyan Blue Odds Limited provide online betting and gaming related information and content to customers under the name Oddschecker. The amounts recognised in respect of the identifiable assets acquired and liabilities assumed are as set out in the table below.

£000

Property, plant and equipment 3,153Identifiable intangible assets 557,965Financial assets 39,327Financial liabilities (142,723)Total identifiable assets 457,722

Goodwill 319,177Total consideration 776,899Satisfied by:Cash 776,899Total consideration transferred 776,899Less: cash and cash equivalent balance acquired (33,969)Cash consideration 742,930

Acquisition-related costs (included in administrative expenses) amount to £18.4m.

The acquisition created separately identified intangible assets comprising customer relations, technology and other intangible assets, as detailed in note 9, which have been recognised at fair value. Otherwise no fair value adjustments were identified on acquisition.

The acquired subsidiaries contributed £86.2m revenue and £1.0m profit to the Group’s loss for the period between the date of acquisition and the balance sheet date.

If the acquisition of the acquired subsidiaries had been completed on the first day of the financial year, Group revenues for the period would have been £247.7m.

13. TRADE AND OTHER RECEIVABLES: AMOUNTS FALLING DUE IN MORE THAN ONE YEARCompany

£000

Loans due from Group undertakings 345,716Accrued interest on loans due from Group undertakings 9,662

355,378

The loans due from Group undertakings relate to a loan with Cyan Blue VLNCo Ltd. The loan was issued on 19th March 2015 and attracts interest at a rate of 10%, which is not payable but accrues and compounds annually on 31st December.

14. TRADE AND OTHER RECEIVABLES: AMOUNTS FALLING DUE WITHIN ONE YEARGroup

£000

Gross trade receivables 4,095Less: provision for impairment of receivables (200)

Net trade receivables 3,895Prepayments and accrued income 7,571Other receivables 958

12,424

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 25

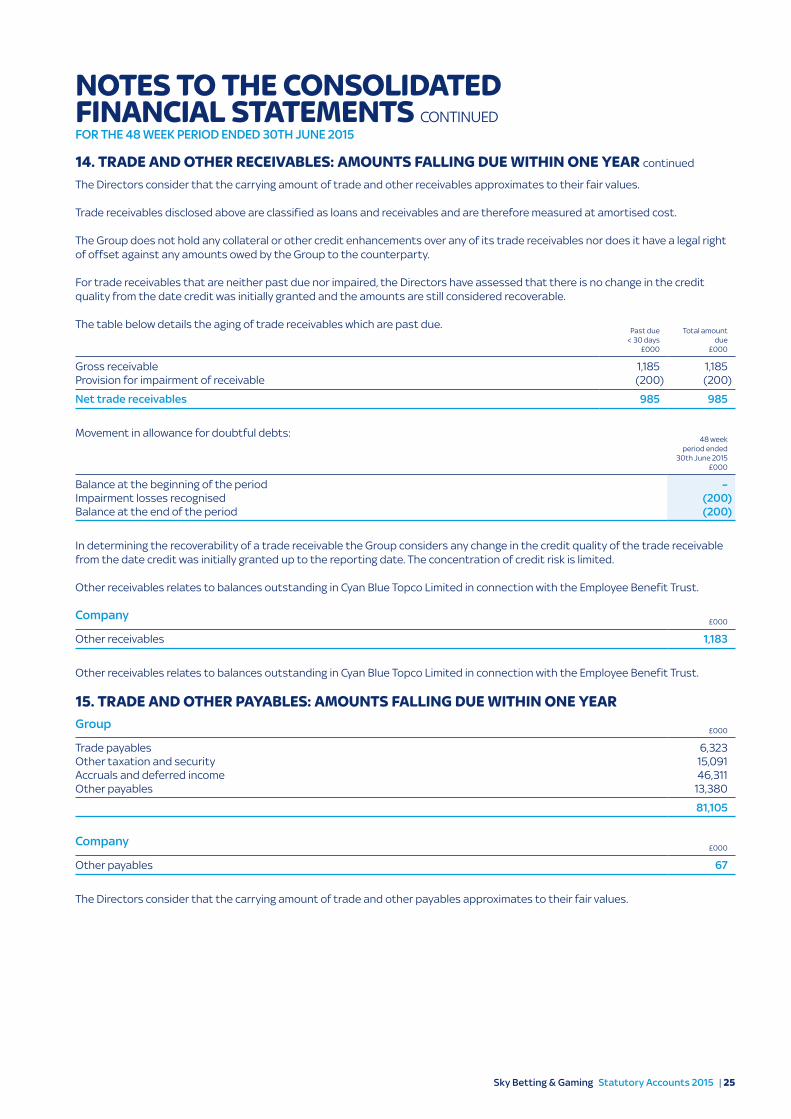

14. TRADE AND OTHER RECEIVABLES: AMOUNTS FALLING DUE WITHIN ONE YEAR continued

The Directors consider that the carrying amount of trade and other receivables approximates to their fair values.

Trade receivables disclosed above are classified as loans and receivables and are therefore measured at amortised cost.

The Group does not hold any collateral or other credit enhancements over any of its trade receivables nor does it have a legal right of offset against any amounts owed by the Group to the counterparty.

For trade receivables that are neither past due nor impaired, the Directors have assessed that there is no change in the credit quality from the date credit was initially granted and the amounts are still considered recoverable.

The table below details the aging of trade receivables which are past due.Past due

< 30 days £000

Total amount due

£000

Gross receivable 1,185 1,185Provision for impairment of receivable (200) (200)

Net trade receivables 985 985

Movement in allowance for doubtful debts:48 week

period ended 30th June 2015

£000

Balance at the beginning of the period –Impairment losses recognised (200)Balance at the end of the period (200)

In determining the recoverability of a trade receivable the Group considers any change in the credit quality of the trade receivable from the date credit was initially granted up to the reporting date. The concentration of credit risk is limited.

Other receivables relates to balances outstanding in Cyan Blue Topco Limited in connection with the Employee Benefit Trust.

Company£000

Other receivables 1,183

Other receivables relates to balances outstanding in Cyan Blue Topco Limited in connection with the Employee Benefit Trust.

15. TRADE AND OTHER PAYABLES: AMOUNTS FALLING DUE WITHIN ONE YEARGroup

£000

Trade payables 6,323Other taxation and security 15,091Accruals and deferred income 46,311Other payables 13,380

81,105

Company£000

Other payables 67

The Directors consider that the carrying amount of trade and other payables approximates to their fair values.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 26

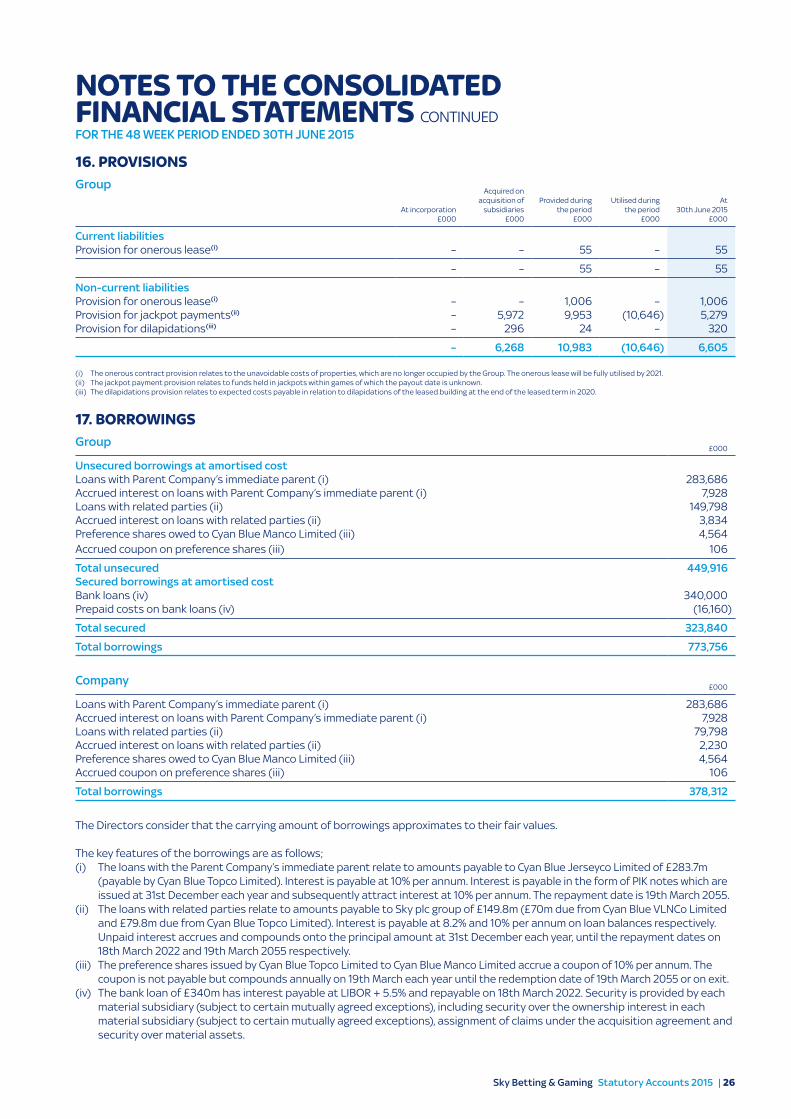

16. PROVISIONSGroup

At incorporation £000

Acquired on acquisition of

subsidiaries £000

Provided during the period

£000

Utilised during the period

£000

At 30th June 2015

£000

Current liabilitiesProvision for onerous lease(i) – – 55 – 55

– – 55 – 55

Non-current liabilitiesProvision for onerous lease(i) – – 1,006 – 1,006Provision for jackpot payments(ii) – 5,972 9,953 (10,646) 5,279Provision for dilapidations(iii) – 296 24 – 320

– 6,268 10,983 (10,646) 6,605

(i) The onerous contract provision relates to the unavoidable costs of properties, which are no longer occupied by the Group. The onerous lease will be fully utilised by 2021.(ii) The jackpot payment provision relates to funds held in jackpots within games of which the payout date is unknown.(iii) The dilapidations provision relates to expected costs payable in relation to dilapidations of the leased building at the end of the leased term in 2020.

17. BORROWINGSGroup

£000

Unsecured borrowings at amortised costLoans with Parent Company’s immediate parent (i) 283,686Accrued interest on loans with Parent Company’s immediate parent (i) 7,928Loans with related parties (ii) 149,798Accrued interest on loans with related parties (ii) 3,834Preference shares owed to Cyan Blue Manco Limited (iii) 4,564Accrued coupon on preference shares (iii) 106

Total unsecured 449,916Secured borrowings at amortised costBank loans (iv) 340,000Prepaid costs on bank loans (iv) (16,160)

Total secured 323,840

Total borrowings 773,756

Company£000

Loans with Parent Company’s immediate parent (i) 283,686Accrued interest on loans with Parent Company’s immediate parent (i) 7,928Loans with related parties (ii) 79,798Accrued interest on loans with related parties (ii) 2,230Preference shares owed to Cyan Blue Manco Limited (iii) 4,564Accrued coupon on preference shares (iii) 106

Total borrowings 378,312

The Directors consider that the carrying amount of borrowings approximates to their fair values.

The key features of the borrowings are as follows;(i) The loans with the Parent Company’s immediate parent relate to amounts payable to Cyan Blue Jerseyco Limited of £283.7m

(payable by Cyan Blue Topco Limited). Interest is payable at 10% per annum. Interest is payable in the form of PIK notes which are issued at 31st December each year and subsequently attract interest at 10% per annum. The repayment date is 19th March 2055.

(ii) The loans with related parties relate to amounts payable to Sky plc group of £149.8m (£70m due from Cyan Blue VLNCo Limited and £79.8m due from Cyan Blue Topco Limited). Interest is payable at 8.2% and 10% per annum on loan balances respectively. Unpaid interest accrues and compounds onto the principal amount at 31st December each year, until the repayment dates on 18th March 2022 and 19th March 2055 respectively.

(iii) The preference shares issued by Cyan Blue Topco Limited to Cyan Blue Manco Limited accrue a coupon of 10% per annum. The coupon is not payable but compounds annually on 19th March each year until the redemption date of 19th March 2055 or on exit.

(iv) The bank loan of £340m has interest payable at LIBOR + 5.5% and repayable on 18th March 2022. Security is provided by each material subsidiary (subject to certain mutually agreed exceptions), including security over the ownership interest in each material subsidiary (subject to certain mutually agreed exceptions), assignment of claims under the acquisition agreement and security over material assets.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 27

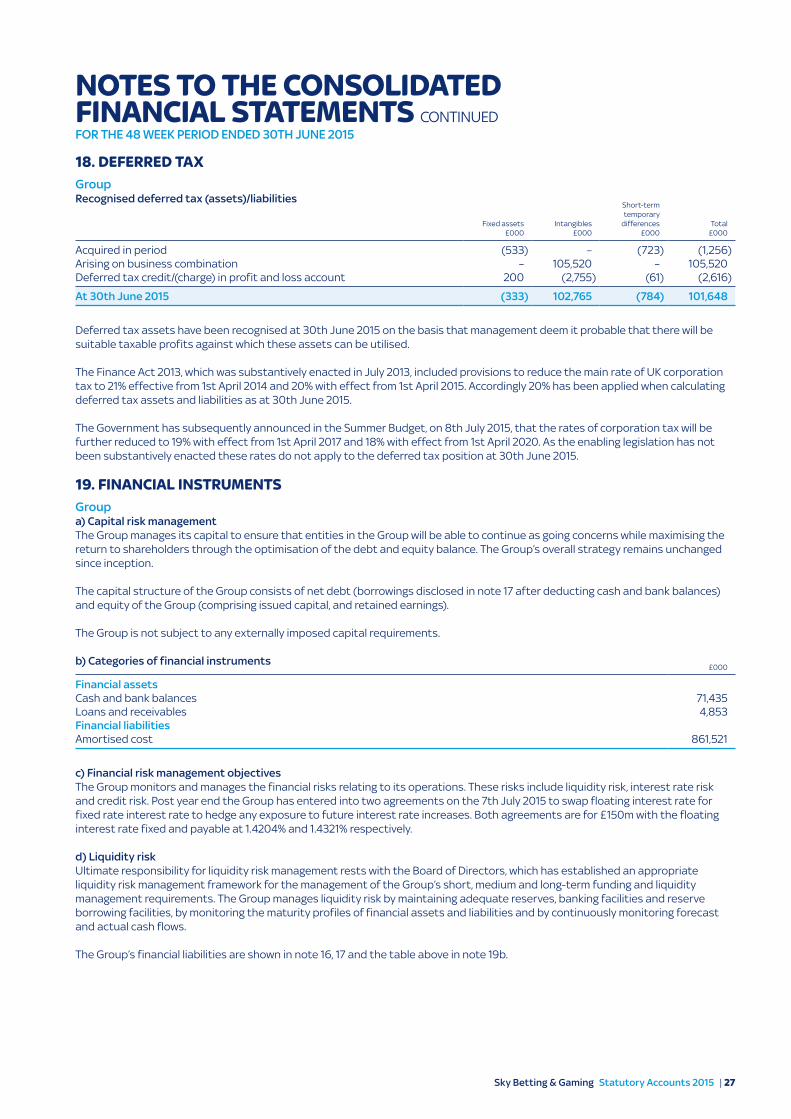

18. DEFERRED TAXGroupRecognised deferred tax (assets)/liabilities

Fixed assets £000

Intangibles £000

Short-term temporary

differences £000

Total £000

Acquired in period (533) – (723) (1,256)Arising on business combination – 105,520 – 105,520Deferred tax credit/(charge) in profit and loss account 200 (2,755) (61) (2,616)

At 30th June 2015 (333) 102,765 (784) 101,648

Deferred tax assets have been recognised at 30th June 2015 on the basis that management deem it probable that there will be suitable taxable profits against which these assets can be utilised.

The Finance Act 2013, which was substantively enacted in July 2013, included provisions to reduce the main rate of UK corporation tax to 21% effective from 1st April 2014 and 20% with effect from 1st April 2015. Accordingly 20% has been applied when calculating deferred tax assets and liabilities as at 30th June 2015.

The Government has subsequently announced in the Summer Budget, on 8th July 2015, that the rates of corporation tax will be further reduced to 19% with effect from 1st April 2017 and 18% with effect from 1st April 2020. As the enabling legislation has not been substantively enacted these rates do not apply to the deferred tax position at 30th June 2015.

19. FINANCIAL INSTRUMENTSGroupa) Capital risk managementThe Group manages its capital to ensure that entities in the Group will be able to continue as going concerns while maximising the return to shareholders through the optimisation of the debt and equity balance. The Group’s overall strategy remains unchanged since inception.

The capital structure of the Group consists of net debt (borrowings disclosed in note 17 after deducting cash and bank balances) and equity of the Group (comprising issued capital, and retained earnings).

The Group is not subject to any externally imposed capital requirements.

b) Categories of financial instruments£000

Financial assetsCash and bank balances 71,435Loans and receivables 4,853Financial liabilitiesAmortised cost 861,521

c) Financial risk management objectivesThe Group monitors and manages the financial risks relating to its operations. These risks include liquidity risk, interest rate risk and credit risk. Post year end the Group has entered into two agreements on the 7th July 2015 to swap floating interest rate for fixed rate interest rate to hedge any exposure to future interest rate increases. Both agreements are for £150m with the floating interest rate fixed and payable at 1.4204% and 1.4321% respectively.

d) Liquidity riskUltimate responsibility for liquidity risk management rests with the Board of Directors, which has established an appropriate liquidity risk management framework for the management of the Group’s short, medium and long-term funding and liquidity management requirements. The Group manages liquidity risk by maintaining adequate reserves, banking facilities and reserve borrowing facilities, by monitoring the maturity profiles of financial assets and liabilities and by continuously monitoring forecast and actual cash flows.

The Group’s financial liabilities are shown in note 16, 17 and the table above in note 19b.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 28

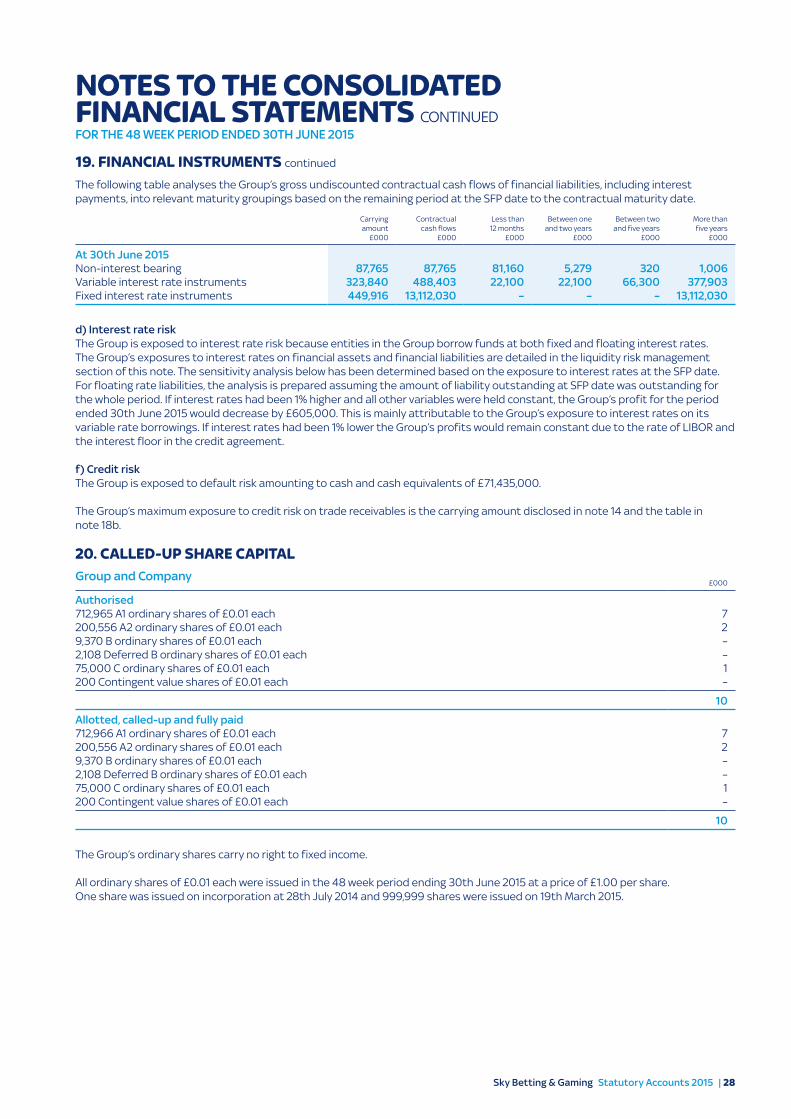

19. FINANCIAL INSTRUMENTS continued

The following table analyses the Group’s gross undiscounted contractual cash flows of financial liabilities, including interest payments, into relevant maturity groupings based on the remaining period at the SFP date to the contractual maturity date.

Carrying amount

£000

Contractual cash flows

£000

Less than 12 months

£000

Between one and two years

£000

Between two and five years

£000

More than five years

£000

At 30th June 2015Non-interest bearing 87,765 87,765 81,160 5,279 320 1,006Variable interest rate instruments 323,840 488,403 22,100 22,100 66,300 377,903Fixed interest rate instruments 449,916 13,112,030 – – – 13,112,030

d) Interest rate riskThe Group is exposed to interest rate risk because entities in the Group borrow funds at both fixed and floating interest rates. The Group’s exposures to interest rates on financial assets and financial liabilities are detailed in the liquidity risk management section of this note. The sensitivity analysis below has been determined based on the exposure to interest rates at the SFP date. For floating rate liabilities, the analysis is prepared assuming the amount of liability outstanding at SFP date was outstanding for the whole period. If interest rates had been 1% higher and all other variables were held constant, the Group’s profit for the period ended 30th June 2015 would decrease by £605,000. This is mainly attributable to the Group’s exposure to interest rates on its variable rate borrowings. If interest rates had been 1% lower the Group’s profits would remain constant due to the rate of LIBOR and the interest floor in the credit agreement.

f) Credit riskThe Group is exposed to default risk amounting to cash and cash equivalents of £71,435,000.

The Group’s maximum exposure to credit risk on trade receivables is the carrying amount disclosed in note 14 and the table in note 18b.

20. CALLED-UP SHARE CAPITALGroup and Company

£000

Authorised712,965 A1 ordinary shares of £0.01 each 7200,556 A2 ordinary shares of £0.01 each 29,370 B ordinary shares of £0.01 each –2,108 Deferred B ordinary shares of £0.01 each –75,000 C ordinary shares of £0.01 each 1200 Contingent value shares of £0.01 each –

10

Allotted, called-up and fully paid712,966 A1 ordinary shares of £0.01 each 7200,556 A2 ordinary shares of £0.01 each 29,370 B ordinary shares of £0.01 each –2,108 Deferred B ordinary shares of £0.01 each –75,000 C ordinary shares of £0.01 each 1200 Contingent value shares of £0.01 each –

10

The Group’s ordinary shares carry no right to fixed income.

All ordinary shares of £0.01 each were issued in the 48 week period ending 30th June 2015 at a price of £1.00 per share. One share was issued on incorporation at 28th July 2014 and 999,999 shares were issued on 19th March 2015.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 29

21. SHARE PREMIUMGroup and Company

£000

Premium arising on issue of equity shares712,966 A1 ordinary shares with premium of £0.99 706200,556 A2 ordinary shares with premium of £0.99 1999,370 B ordinary shares with premium of £0.99 92,108 Deferred B ordinary shares with premium of £0.99 275,000 C ordinary shares with premium of £0.99 74

990

All ordinary shares of £0.01 each were issued in the 48 week period ending 30th June 2015 at a price of £1.00 per share. One share was issued on incorporation at 28th July 2014 and 999,999 shares were issued on the 19th March 2015.

22. NOTES TO THE CASH FLOW STATEMENTGroupReconciliation of profit before taxation to cash generated from operations

48 week period ended

30th June 2015 £000

Loss before taxation (10,737)Depreciation of property, plant and equipment 435Amortisation of intangible assets 14,731Net finance costs 18,605

23,034Increase in trade and other receivables (6,333)Increase in trade and other payables 29,018Increase in provisions 433

Cash generated from operations 46,152

Cash and cash equivalentsCash and cash equivalents comprise cash held by the Group. This amount includes £13.1m of client funds that are matched by liabilities of an equal value. Cash and cash equivalents at the end of the reporting period as shown in the Consolidated Cash Flow Statement (£71.4m) reconciles to the related items in the SFP position.

CompanyReconciliation of profit before taxation to cash generated from operations

48 week period ended

30th June 2015 £000

Loss before taxation (14,674)Net finance costs 571

(14,103)Increase in trade and other receivables (1,183)Increase in trade and other payables 67

Cash generated from operations (15,219)

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 30

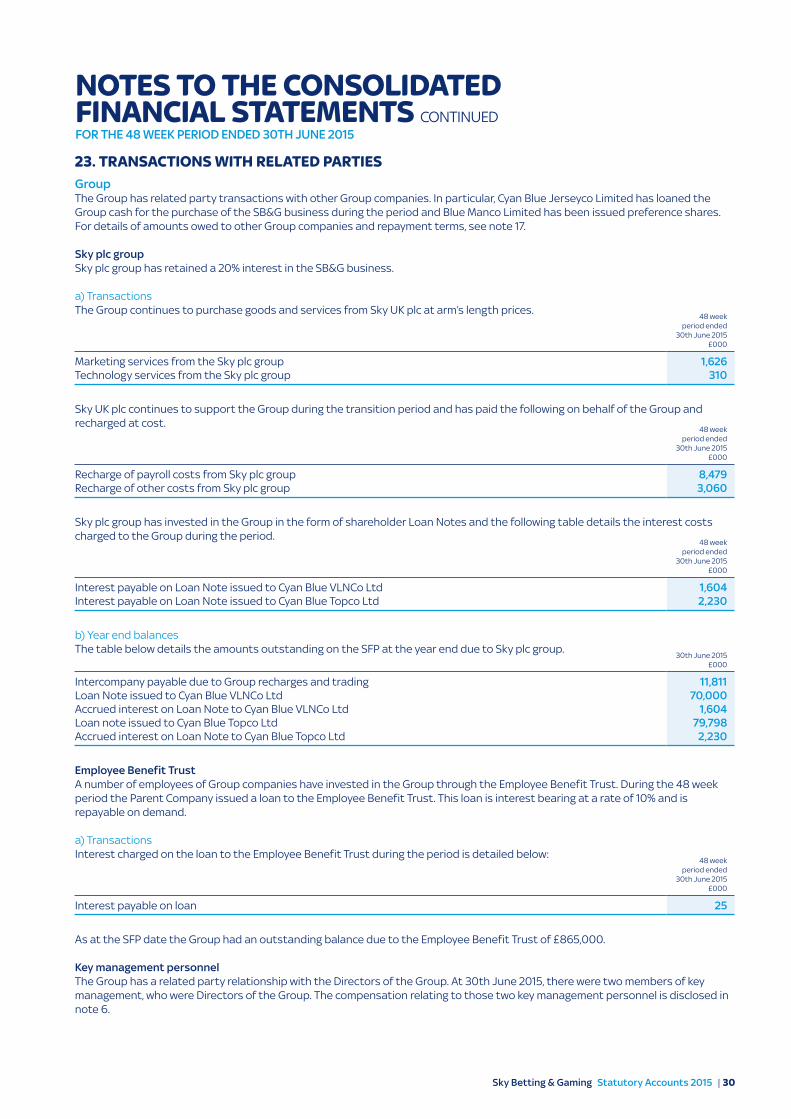

23. TRANSACTIONS WITH RELATED PARTIESGroupThe Group has related party transactions with other Group companies. In particular, Cyan Blue Jerseyco Limited has loaned the Group cash for the purchase of the SB&G business during the period and Blue Manco Limited has been issued preference shares. For details of amounts owed to other Group companies and repayment terms, see note 17.

Sky plc groupSky plc group has retained a 20% interest in the SB&G business.

a) TransactionsThe Group continues to purchase goods and services from Sky UK plc at arm’s length prices.

48 week period ended

30th June 2015 £000

Marketing services from the Sky plc group 1,626Technology services from the Sky plc group 310

Sky UK plc continues to support the Group during the transition period and has paid the following on behalf of the Group and recharged at cost.

48 week period ended

30th June 2015 £000

Recharge of payroll costs from Sky plc group 8,479Recharge of other costs from Sky plc group 3,060

Sky plc group has invested in the Group in the form of shareholder Loan Notes and the following table details the interest costs charged to the Group during the period.

48 week period ended

30th June 2015 £000

Interest payable on Loan Note issued to Cyan Blue VLNCo Ltd 1,604Interest payable on Loan Note issued to Cyan Blue Topco Ltd 2,230

b) Year end balancesThe table below details the amounts outstanding on the SFP at the year end due to Sky plc group.

30th June 2015 £000

Intercompany payable due to Group recharges and trading 11,811Loan Note issued to Cyan Blue VLNCo Ltd 70,000Accrued interest on Loan Note to Cyan Blue VLNCo Ltd 1,604Loan note issued to Cyan Blue Topco Ltd 79,798Accrued interest on Loan Note to Cyan Blue Topco Ltd 2,230

Employee Benefit TrustA number of employees of Group companies have invested in the Group through the Employee Benefit Trust. During the 48 week period the Parent Company issued a loan to the Employee Benefit Trust. This loan is interest bearing at a rate of 10% and is repayable on demand.

a) TransactionsInterest charged on the loan to the Employee Benefit Trust during the period is detailed below:

48 week period ended

30th June 2015 £000

Interest payable on loan 25

As at the SFP date the Group had an outstanding balance due to the Employee Benefit Trust of £865,000.

Key management personnelThe Group has a related party relationship with the Directors of the Group. At 30th June 2015, there were two members of key management, who were Directors of the Group. The compensation relating to those two key management personnel is disclosed in note 6.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS CONTINUEDFOR THE 48 WEEK PERIOD ENDED 30TH JUNE 2015

Sky Betting & Gaming Statutory Accounts 2015 | 31

24. OPERATING LEASE ARRANGEMENTSGroup

48 week period ended

30th June 2015 £000

Lease payments under operating leases recognised as an expense in the period 266

At the balance sheet date, the Group had outstanding commitments for future minimum lease payments under non-cancellable operating leases, which fall due as follows:

£000

Within one year 1,070In second to fifth year inclusive 3,918After five years 226

Operating lease payments represent rentals payable by the Group for certain of its office properties.

25. FINANCIAL COMMITMENTSGroup

£000

Contracted for but not provided for 1,368