Embed Size (px)

Citation preview

8/6/2019 Welspun Corp Ltd - Q4FY11 Result Update

http://slidepdf.com/reader/full/welspun-corp-ltd-q4fy11-result-update 1/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

NG TERM INVESTMENT CALL

BUY27 May 2011

Company Report | Q4FY11 Result Update

Welspun Corp Ltd (WCL) registered a strong in revenue, higher than

Unicon estimates. EBITDA and PAT however came lower due to a higherthan expected rise in raw material prices and a provision for an out of

court settlement with a foreign customer.

Sales volume of pipes as well as plates increased 31% during the quarter

resulting in a 34% growth in net income. For FY11, sales volumes of pipes

increased 11.5% while plate volumes increased by 25.3%.

EBITDA fell 19% during the quarter with a 754 bps reduction in EBITDA

margin, while it was down 3% for FY11 with a 192bps reduction in

EBITDA margin. WCL made a provision of INR 670 mn during the

quarter and INR 2,007 mn in FY11 for an out of court settlement with aforeign customer to end a long pending litigation. Adjusting for the

provision of INR 670mn, the EBITDA margin was still down 445 bps on

account of a steep rise in raw material expenses.

Interest costs during the quarter increased 51% on account of additional

interest due to consolidation of Saudi facility and Welspun Projects

borrowings. Depreciation costs increased 22% due to capitalization of

Coil Mill, Mandya Plant and Saudi plants. PAT during the quarter fell

29% with a 489 bps reduction in PAT margin, while it was up 4% for

FY11 with a 40bps reduction in margin.

The current Pipe and Plate order book of the Company stands at INR 54

billion (~726K tonnes of Pipes and 32K tonnes of Plates).

Annual Highlights

Welspun acquired ~61% in MSK Projects (Welspun Projects limited).

Welspun also acquired 35% in Leighton, India, subsidiary of

Leighton Australia, a renowned EPC Company globally.

The Group has taken initiative to consolidate all infrastructure

businesses under Welspun Infratech limited, subsidiary of Welspun

Corp Limited.

Outlook & Valuation

WCL’s expansion plan is well on track which provides strong visibility of

future volume and revenue growth. The Coil mill has been commissioned

this year and is in full production. The Saudi Plant was successfully

commissioned in Q4FY11 while the implementation of the L-SAW plant

at Anjar is on schedule, with trial production already started. The facility

is likely to be commissioned by the end of Q1FY12. At the CMP of INR

174, the stock is trading at EV/EBITDA of 4x and 3.4x for FY12 and FY13

respectively. Considering the rising oil prices and strong volume growth

of the company, we remain positive on WCL with a price target of INR225.

ndustry Pipes

CMP (INR) 174Target (INR) 225

Upside / Downside (%) 29

52 week High/Low (INR) 275 / 144

Market Cap (INR Mn) 35,709

3M Avg. Volumes 610,320

EV/EBITDA (FY12e) 6x

Shareholding Pattern (%)

Stock Performance

100

120

140

160

180

200

220

240

260

280

300

May Jul Sep Nov Jan Mar

Welspun Corp Ltd Nifty Performance (%)

1 Month 3 Months 1 YearWCL -11.6 -7.1 -20.2

NIFTY -6.1 3.3 9.5

(INR Mn)

Particulars Actual Estimates

Total Income 21,632 18,690

EBIDTA 2,477 3,680

Reported PAT 1,181 1,755

Source: Bloomberg, Unicon Research

8/6/2019 Welspun Corp Ltd - Q4FY11 Result Update

http://slidepdf.com/reader/full/welspun-corp-ltd-q4fy11-result-update 2/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

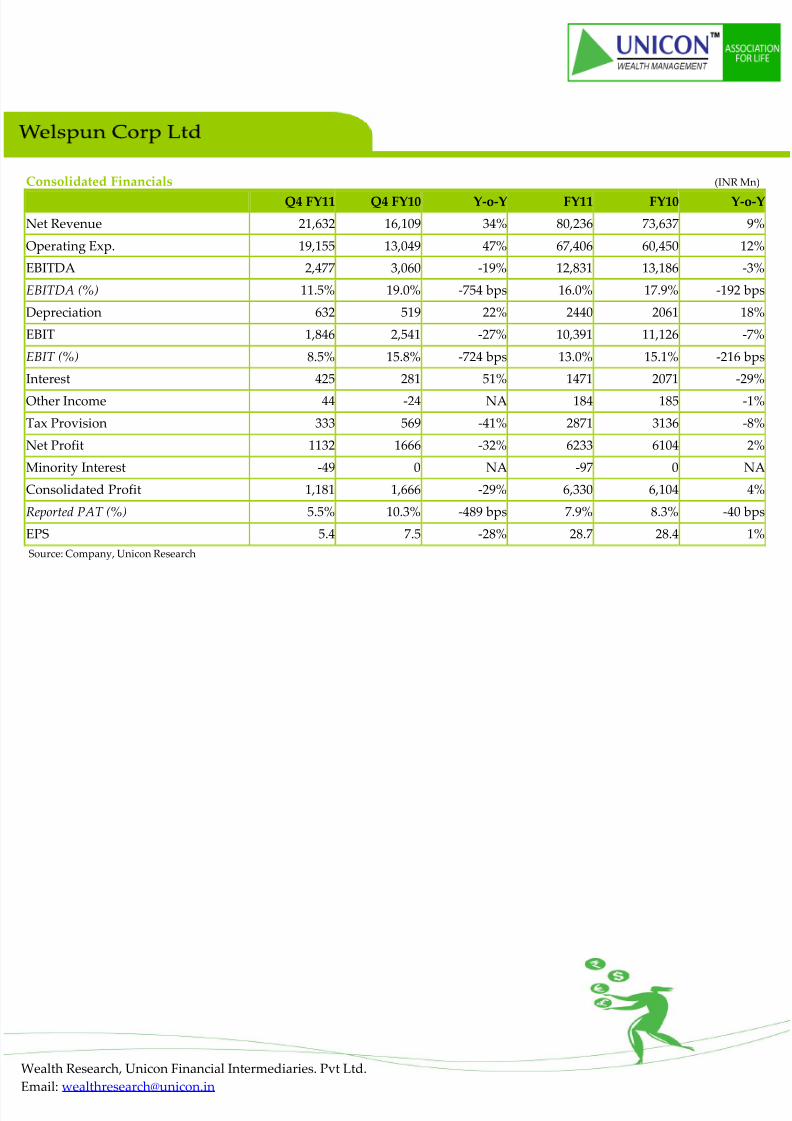

Consolidated Financials (INR Mn)

Q4 FY11 Q4 FY10 Y-o-Y FY11 FY10 Y-o-Y

Net Revenue 21,632 16,109 34% 80,236 73,637 9%

Operating Exp. 19,155 13,049 47% 67,406 60,450 12%

EBITDA 2,477 3,060 -19% 12,831 13,186 -3%

EBITDA (%) 11.5% 19.0% -754 bps 16.0% 17.9% -192 bps

Depreciation 632 519 22% 2440 2061 18%

EBIT 1,846 2,541 -27% 10,391 11,126 -7%

EBIT (%) 8.5% 15.8% -724 bps 13.0% 15.1% -216 bps

Interest 425 281 51% 1471 2071 -29%

Other Income 44 -24 NA 184 185 -1%

Tax Provision 333 569 -41% 2871 3136 -8%

Net Profit 1132 1666 -32% 6233 6104 2%

Minority Interest -49 0 NA -97 0 NA

Consolidated Profit 1,181 1,666 -29% 6,330 6,104 4%

Reported PAT (%) 5.5% 10.3% -489 bps 7.9% 8.3% -40 bps

EPS 5.4 7.5 -28% 28.7 28.4 1%

Source: Company, Unicon Research

8/6/2019 Welspun Corp Ltd - Q4FY11 Result Update

http://slidepdf.com/reader/full/welspun-corp-ltd-q4fy11-result-update 3/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

Unicon Investment Ranking Methodology

Rating Buy Accumulate Hold Reduce Sell

Return Range >= 20% 10% to 20% -10% to 10% -10% to -20% <= -20%

Disclaimer

This document has been issued by Unicon Financial Intermediaries Pvt. Ltd. (“UNICON”) for the information of its customers only. UNICON is governed by

the Securities and Exchange Board of India. This document is not for public distribution and has been furnished to you solely for your information and must

not be reproduced or redistributed to any other person. Persons into whose possession this document may come are required to observe these restrictions. The

information and opinions contained herein have been compiled or arrived at based upon information obtained in good faith from public sources believed to

be reliable. Such information has not been independently verified and no guarantee, representation or warranty, express or implied is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. This document has been produced independently of any

company or companies mentioned herein, and forward looking statements; opinions and expectations contained herein are subject to change without notice.

This document is for information purposes only and is provided on an “as is” basis. Descriptions of any company or companies or their securities mentioned

herein are not intended to be complete and this document is not, and should not be construed as an offer, or solicitation of an offer, to buy or sell or subscribe

to any securities or other financial instruments. We are not soliciting any action based on this document. UNICON, its associate and group companies its

directors or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action

taken on basis of this document, including but not restricted to, fluctuation in the prices of the shares and bonds, reduction in the dividend or income, etc. This

document is not directed to or intended for display, downloading, printing, reproducing or for distribution to or use by any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or would subject UNICON or its associates or group companies to any registration or licensing requirement within such

jurisdiction. If this document is inadvertently sent or has reached any individual in such country, the same may be ignored and brought to the attention of the

sender. This document may not be reproduced, distributed or published for any purpose without prior written approval of UNICON. This document is forthe general information and does not take into account the particular investment objectives, financial situation or needs of any individual customer, and it

does not constitute a personalised recommendation of any particular security or investment strategy. Before acting on any advice or recommendation in this

document, a customer should consider whether i t is suitable given the customer’s particular circumstances and, if necessary, seek professional advice. Certain

transactions, including those involving futures, options, and high yield securities, give rise to substantial risk and are not suitable for all investors. UNICON,

its associates or group companies do not represent or endorse the accuracy or reliability of any of the information or content of the document and reliance

upon it is at your own risk.

UNICON, its associates or group companies, expressly disclaims any and all warranties, express or implied, including without limitation warranties of

merchantability and fitness for a particular purpose with respect to the document and any information in it. UNICON, its associates or group companies, shall

not be liable for any direct, indirect, incidental, punitive or consequential damages of any kind with respect to the document. No part of this publication may

be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise,

without the prior written permission of Unicon Financial Intermediaries Pvt. Ltd.

Address:Wealth Management

Unicon Financial Intermediaries. Pvt. Ltd.

Ground Floor, Jhawar House,

285, Princess Street, Mumbai-400002Ph: 022-4359 1200 / 100

Email: [email protected]

Visit us at www.unicon.in