Embed Size (px)

Citation preview

1

WELCOME TO:

ALL ABOUT FUNDINGFOUNDERS, FAMILY & FRIENDS,

GOVERNMENTS, BANKS, ANGELS & VCs

May 20, 2009 6:30pm – 9:30pm

Speakers: Roger Killen & Tanner Philp

2

MY OBJECTIVES

To help you raise up to $2m of Seed and Startup capital:• preparations • sources• amounts• sequence

3

PROCESS

• PowerPoint slides• Q&A• Post seminar access:

– [email protected]– (604) 408-0888

• Break between speakers

4

BECOME A WORTHY

INVESTMENT OPPORTUNITY

© 2009 Waterford Executive Services Ltd. All rights reserved. 5

The right market

The right startup people

The right fit

The right skills

The right product

The right exit

strategy

The right legal

structure

The right infra-

structure

Day 1: Build Day 1: Build an SME that is an SME that is a Home Run in a Home Run in the makingthe making

© 2009 Waterford Executive Services Ltd. All rights reserved. 6

SME AT END OF Q2• Skilled Founder(s)• Strong market• Strong product/service• Defined Exit Strategy• Credible Startup people:

– Board– Advisory Councils– Professional Advisors

• Correct legal structure• Robust Infrastructure

• Discipline • Confidence • Attitude

© 2009 Waterford Executive Services Ltd. All rights reserved. 7

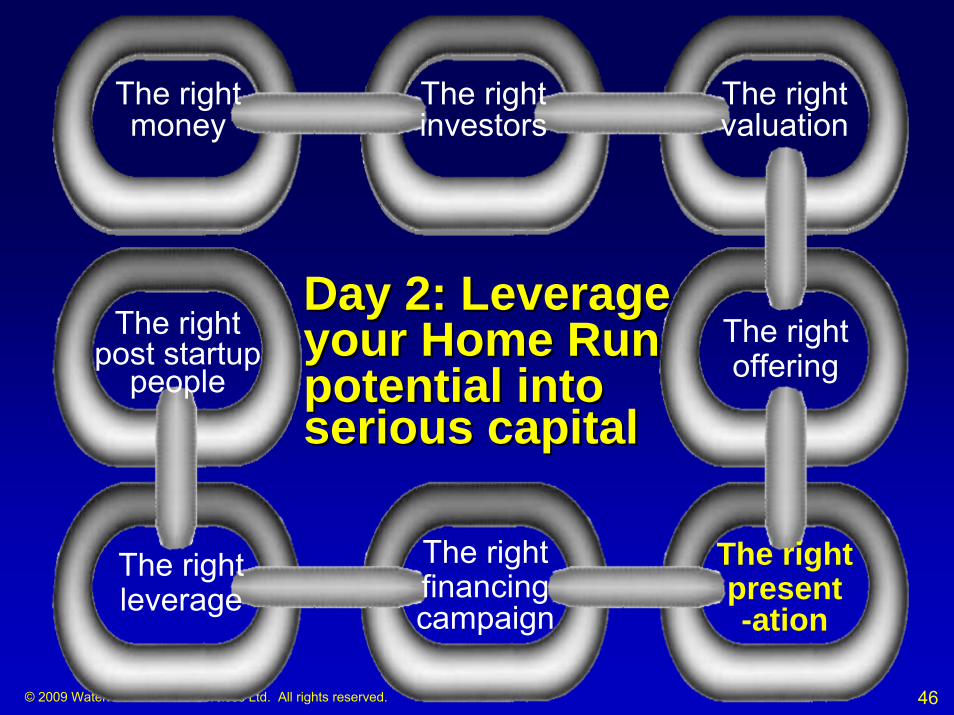

The right money

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

The right offering

The right valuation

The right financing campaign

The right present-

ation

The right investors

The right post startup

people

The right leverage

© 2009 Waterford Executive Services Ltd. All rights reserved. 8

The right

money

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

The right offering

The right valuation

The right financing campaign

The right present-

ation

The right investors

The right post startup

people

The right leverage

© 2009 Waterford Executive Services Ltd. All rights reserved. 9

TYPES OF MONEY• EQUITY - ownership interest in a

business; there is no requirement to repay

• DEBT - a legal obligation to repay the capital advanced, generally monthly and with interest

© 2009 Waterford Executive Services Ltd. All rights reserved. 10

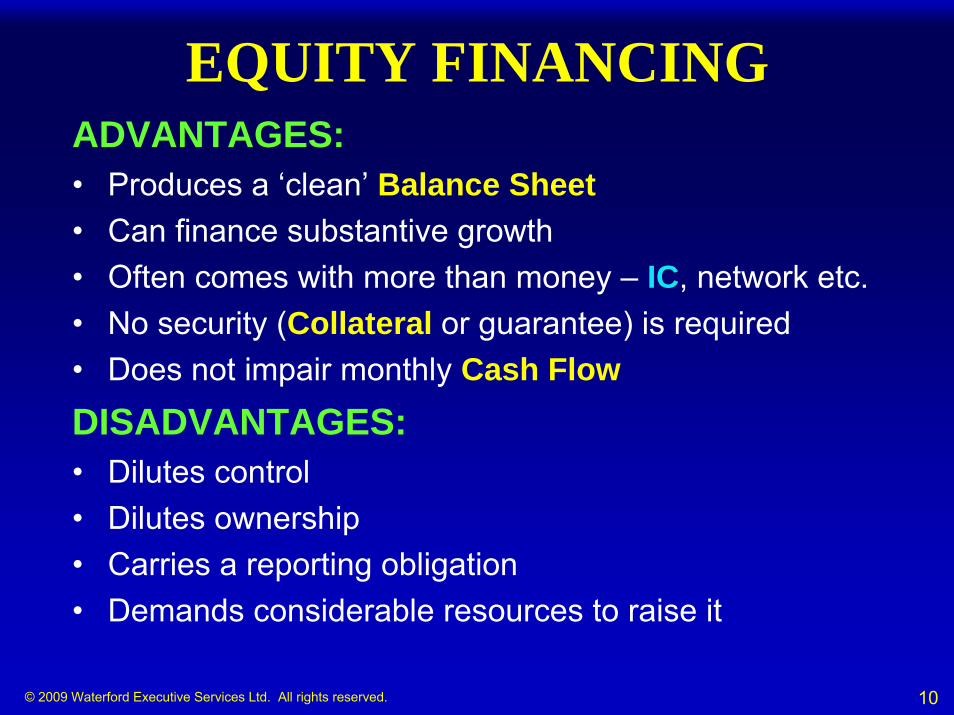

EQUITY FINANCING

DISADVANTAGES:• Dilutes control• Dilutes ownership• Carries a reporting obligation • Demands considerable resources to raise it

ADVANTAGES:• Produces a ‘clean’ Balance Sheet• Can finance substantive growth• Often comes with more than money – IC, network etc.• No security (Collateral or guarantee) is required• Does not impair monthly Cash Flow

© 2009 Waterford Executive Services Ltd. All rights reserved. 11

INVESTOR CENTRED BUSINESS– POST FINANCING OWNERSHIP

Employees10%

Key hires10%

Seed Stage Investors

10%

Directors5%

Angels10%

Founders10%

Venture Capitalists

30%

Others15%

© 2009 Waterford Executive Services Ltd. All rights reserved. 12

DEBT FINANCING

DISADVANTAGES:• Increases risk:

– transfers power to the lender– reduces monthly Cash Flow– ignores business cycle fluctuations

• ‘Dirties’ a Balance Sheet• Requires security: Collateral, personal guarantee, co-signer• You generally only get money• Cannot finance substantive growth• Carries a reporting obligation

ADVANTAGES:• Minimizes dilution• For wealthy Founders, Debt is relatively quick and easy to secure• Relatively inexpensive

Major turnoffs toSeasoned Investors

© 2009 Waterford Executive Services Ltd. All rights reserved. 13

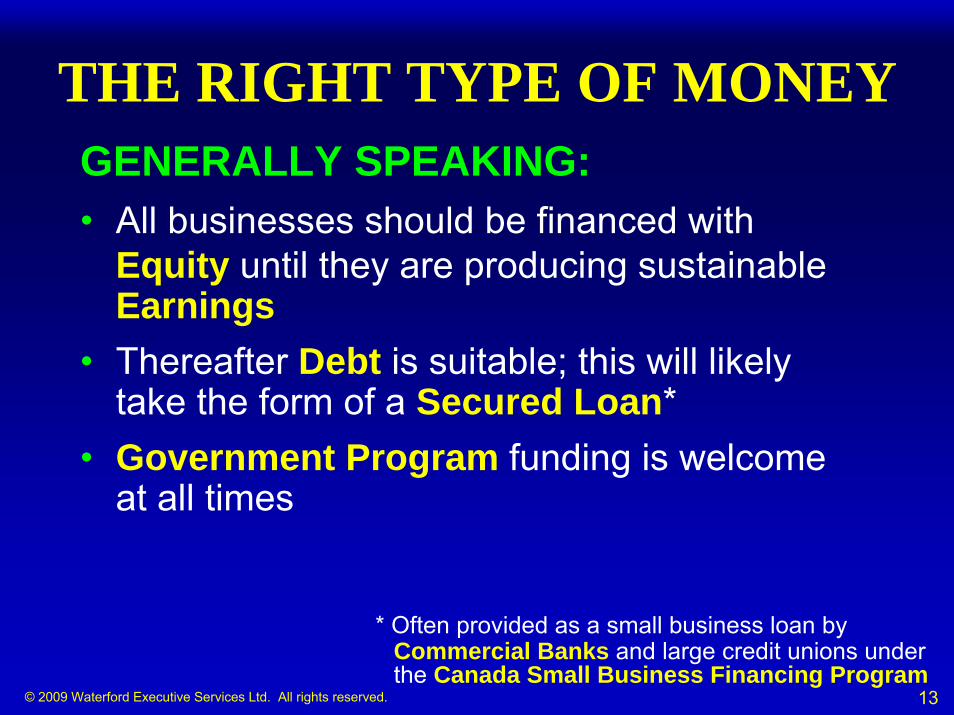

THE RIGHT TYPE OF MONEY

* Often provided as a small business loan by Commercial Banks and large credit unions under the Canada Small Business Financing Program

GENERALLY SPEAKING:• All businesses should be financed with

Equity until they are producing sustainable Earnings

• Thereafter Debt is suitable; this will likely take the form of a Secured Loan*

• Government Program funding is welcome at all times

© 2009 Waterford Executive Services Ltd. All rights reserved. 14

AMOUNT(S) OF MONEYCONSIDERATIONS:• Financial Model is source• Understand your Burn Rate and its drivers• Runway Length should be >6 months• Raise Capital in several Financing Rounds • Need for cash trumps avoidance of Dilution

© 2009 Waterford Executive Services Ltd. All rights reserved. 15

BUSINESS FAILURE CAUSES

Failure by undercapitalization:in growing an Investor CentredBusiness, one of the highest priorities is the need for Capital.When Founders avoid raising Capital because they fear Dilution they risk running out of cash

“You can’t change the world if you’re dead, and when you’re out of money you’re dead.” Guy Kawasaki in ‘The Art of the Start’

© 2009 Waterford Executive Services Ltd. All rights reserved. 16

The right

investors

The right offering

The right valuation

The right financing campaign

The right present-ation

The right money

The right post startup

people

The right leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 17

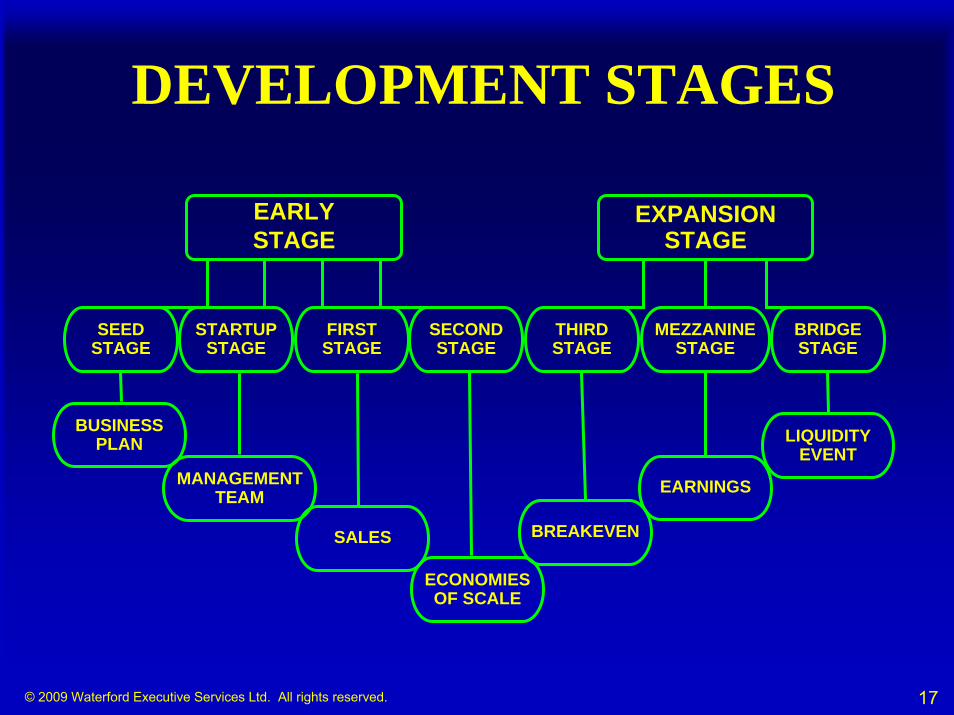

DEVELOPMENT STAGES

EARLYSTAGE

EXPANSION STAGE

SEED STAGE

STARTUPSTAGE

FIRST STAGE

SECOND STAGE

THIRD STAGE

MEZZANINE STAGE

BRIDGE STAGE

BUSINESS PLAN

MANAGEMENT TEAM

SALES

ECONOMIES OF SCALE

BREAKEVEN

EARNINGS

LIQUIDITY EVENT

© 2009 Waterford Executive Services Ltd. All rights reserved. 18

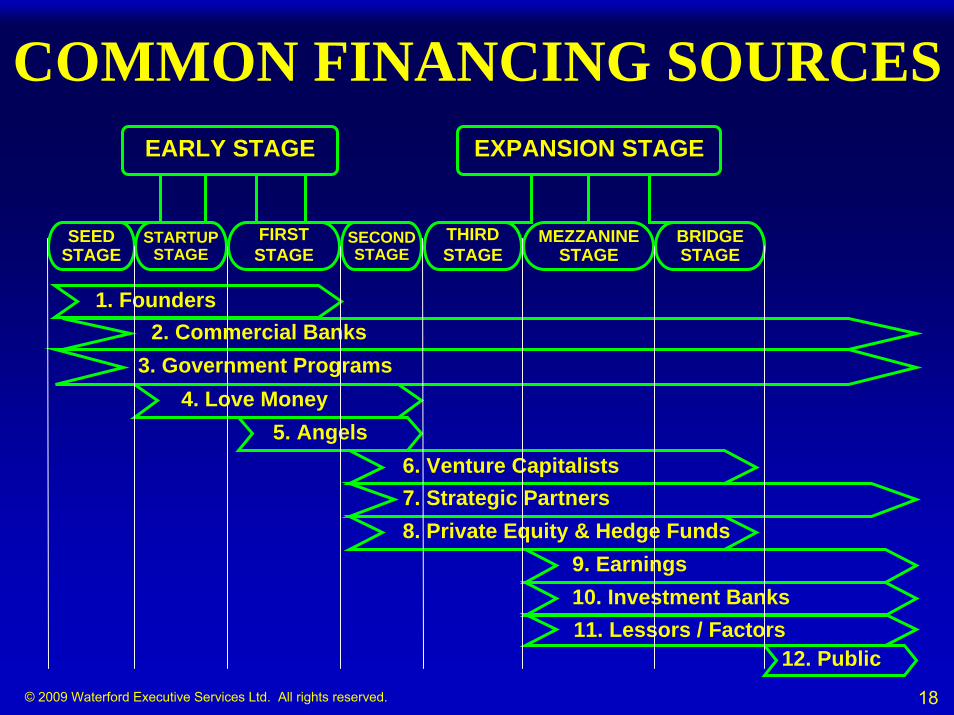

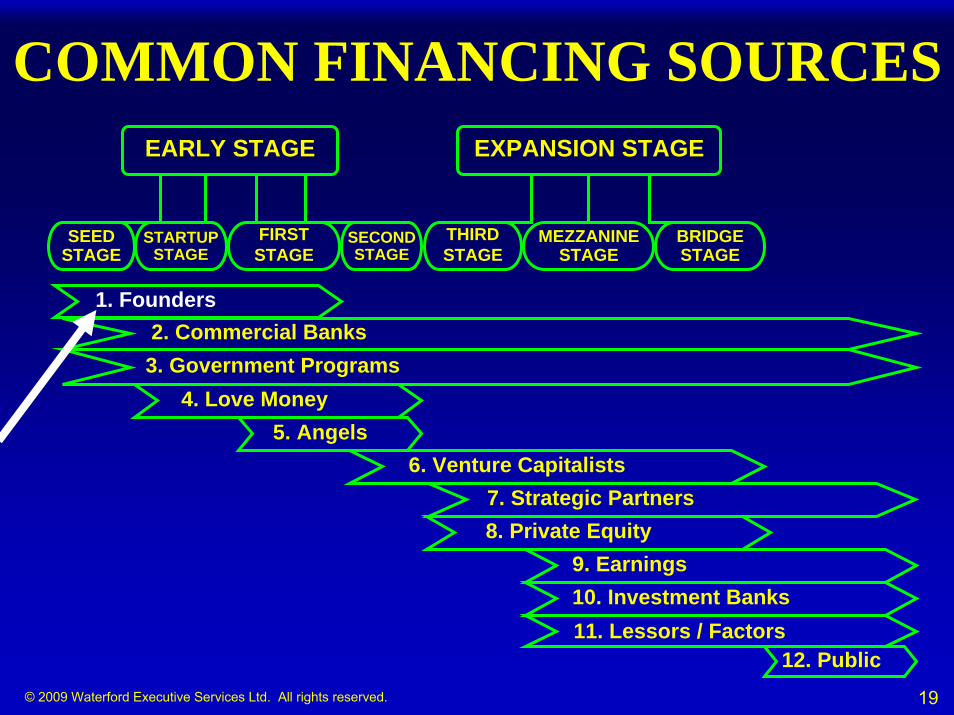

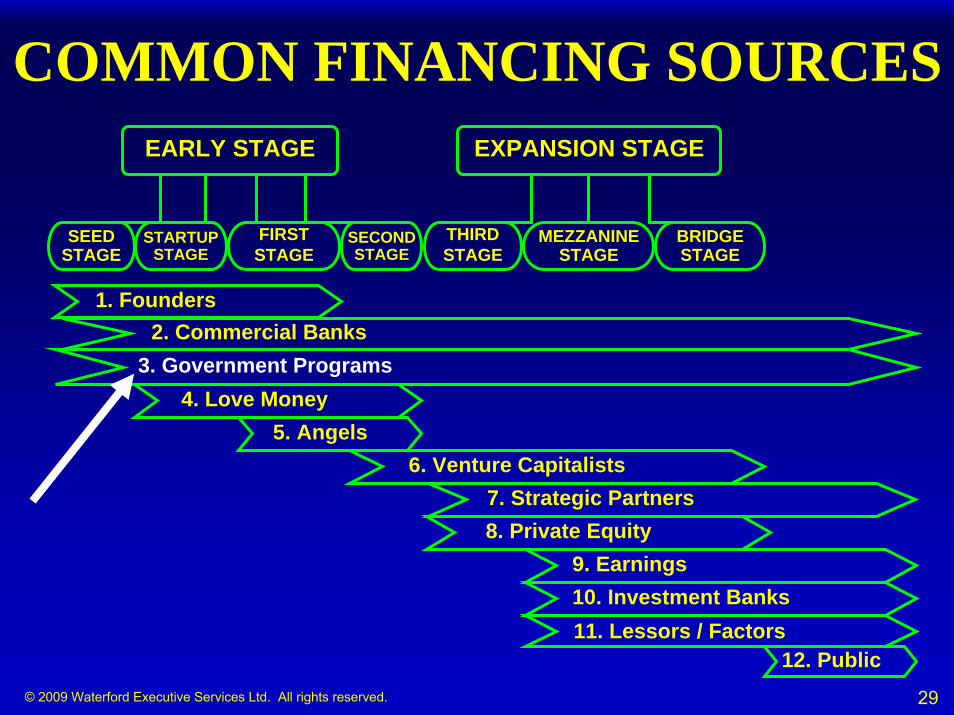

COMMON FINANCING SOURCESEARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity & Hedge Funds

© 2009 Waterford Executive Services Ltd. All rights reserved. 19

COMMON FINANCING SOURCESEARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity

© 2009 Waterford Executive Services Ltd. All rights reserved. 20

FOUNDER(S) OF LIFESTYLE BUSINESS

RECOMMENDATIONS:• Subscribe enough Seed Capital to boost Investors’

confidence in your commitment level

• The form of the Seed Capital can be Debt or Equity

• Do not issue so many Founders’ Shares that the Valuation at the first external Financing Round -likely to FF&BA - is forced unrealistically high

© 2009 Waterford Executive Services Ltd. All rights reserved. 21

FOUNDER(S) OF INVESTOR CENTRED BUSINESS

RECOMMENDATIONS:• Subscribe enough Seed Capital to boost Investors’

confidence in your commitment level

• The form of the Seed Capital must be Equity

• Do not issue so many Founders’ Shares that the Valuation at the first external Financing Round -likely to FF&BA - is forced unrealistically high

• Design a Vesting plan for the Founders’ Shares

© 2009 Waterford Executive Services Ltd. All rights reserved. 22

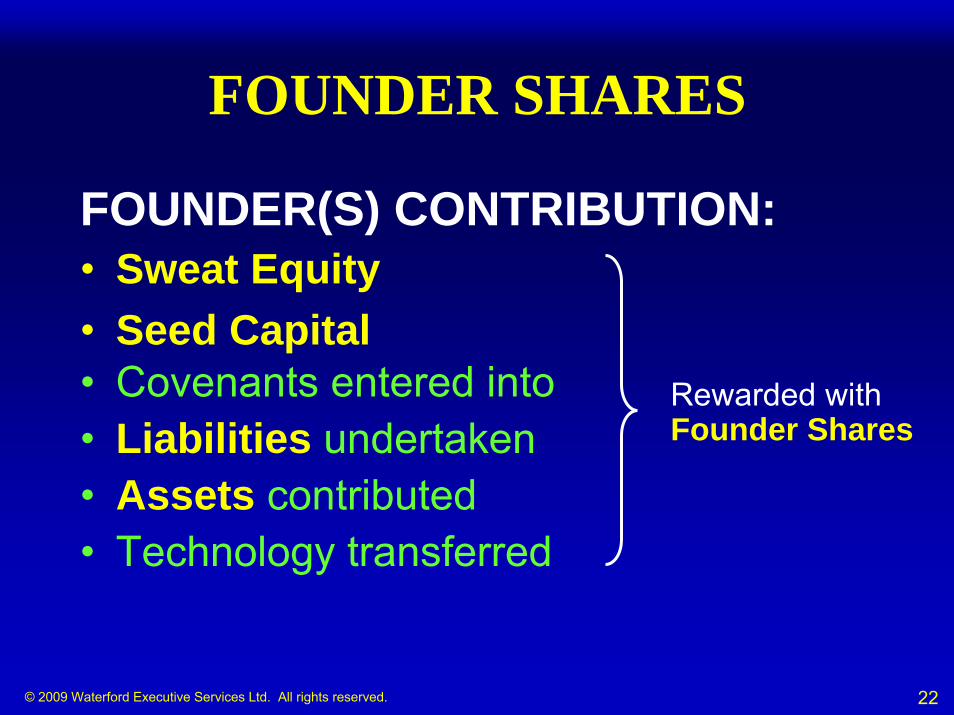

FOUNDER SHARES

FOUNDER(S) CONTRIBUTION:• Sweat Equity • Seed Capital• Covenants entered into• Liabilities undertaken• Assets contributed• Technology transferred

Rewarded withFounder Shares

© 2009 Waterford Executive Services Ltd. All rights reserved. 23

FOUNDER SHARESDEFINITION:Founder Shares are Common Shares that are available at anominal price to Founders only*

* May be provided to others via Founder’s Equity Trust

SUGGESTED ISSUANCE:• 1 Founder – 4m Common Shares• 2 Founders – 3m Common Shares each

• 3 Founders – 2.5m Common Shares each

• 4 Founders – 2m Common Shares each

• Issue price = $0.001 - $0.01 per Common Share i.e.,– Seed Capital of $4,000 - $40,000 if there is 1 Founder– Seed Capital of $3,000 - $30,000 if there are 2 Founders– Seed Capital of $2,500 - $25,000 from each of 3 Founders– Seed Capital of $2,000 - $20,000 from each of 4 Founders

© 2009 Waterford Executive Services Ltd. All rights reserved. 24

FOUNDER SHARE VESTING PLAN

SUGGESTED PLAN:• Initially place all the Founder Shares into Escrow• Use a linear Vesting approach to Vest 50% of these

Founder Shares at a rate of 1/1095 each day over 3 years (3 years = 1,095 days)

• The remaining 50% of these Founder Shares become Vested at the Liquidity Event

• Avoid Milestone based Vesting – it can give rise to disputes and hard feelings if the Milestones contain any subjective element e.g., complete Business Plan

© 2009 Waterford Executive Services Ltd. All rights reserved. 25

COMMON FINANCING SOURCESEARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity

© 2009 Waterford Executive Services Ltd. All rights reserved. 26

COMMERCIAL BANKSPRODUCTS:• Operating loan• Line of Credit• Term loan• Mortgage• Credit card• Cost:

– interest: ≈ prime + 2%– fees:

• loan application: ≈ 1%• transaction• loan management

often referred to as Senior Debt

© 2009 Waterford Executive Services Ltd. All rights reserved. 27

COMMERCIAL BANKS• Commercial Banks and Credit Unions

provide only money• Loan account managers have >100 account

caseloads• They are low risk lenders• They are low cost sources• They require Collateral, personal guarantees

and sometimes co-signers• They use loan acceptance factors

© 2009 Waterford Executive Services Ltd. All rights reserved. 28

LOAN ACCEPTANCE FACTORS• Ratio of Debt to Equity - 1:1 is OK; 3:1 is too high

• Debt service ratio - ratio of Earnings to principal + interest payments - 3:1 is OK; 2:1 is too low

• Collateral value to loan ratio: 2:1 is OK; 1:1 is too low• Current Ratio - 2:1 is OK; 1:1 is too low• Management capacity• Strength of personal guarantee• Age, size and track record of business• Credibility of projections

• Eligible for Canada Small Business Financing Program guarantee by federal government

© 2009 Waterford Executive Services Ltd. All rights reserved. 29

COMMON FINANCING SOURCESEARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity

© 2009 Waterford Executive Services Ltd. All rights reserved. 30

GOVERNMENT PROGRAMSADVANTAGES:• Low cost• Can finance substantive growth• Do not impair short-term Cash Flow• Minimize dilution• Increase credibility:

– partnership with Government of Canada– peer review

• Improve your Business Plan• No Collateral or guarantees required• Generous leverage

DISADVANTAGES:• Favour specific industries• Time-consuming to apply for and administer• Implications if your business is acquired by a foreign company

© 2009 Waterford Executive Services Ltd. All rights reserved. 31

BUSINESS FAILURE CAUSES

Failure by becoming a Government Program junkie: Do not twist your business into something that it isn’t just to qualify for a Government Program

© 2009 Waterford Executive Services Ltd. All rights reserved. 32

COMMON FINANCING SOURCESEARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity

© 2009 Waterford Executive Services Ltd. All rights reserved. 33

LOVE MONEY• FF&BA convert some personal financial

Assets into Venture Capital • FF&BA subscribe ≈ $5k - $25k each• Aggregate raised is ≈ $100k• FF&BA don’t know what they don’t know i.e.,

they are unconsciously incompetent• FF&BA like Founder Centred Businesses

and Investor Centred Businesses equally

Q What are the problems associated with Love Money?

© 2009 Waterford Executive Services Ltd. All rights reserved. 34

LOVE MONEY PROBLEMS• Awkward• Embarrassing• Guilt-ridden• Responsibility• Unwelcome advice• Interference

Due to the potential for a compromised personal relationship

© 2009 Waterford Executive Services Ltd. All rights reserved. 35

LOVE MONEY REVISITED

© 2009 Waterford Executive Services Ltd. All rights reserved. 36

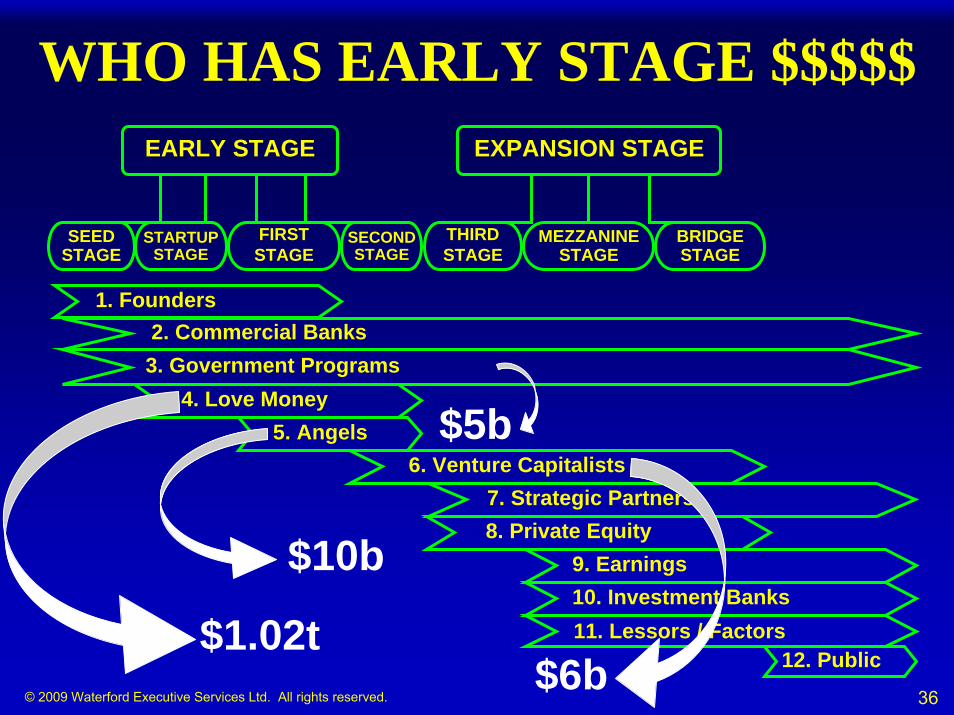

WHO HAS EARLY STAGE $$$$$EARLY STAGE EXPANSION STAGE

SEED STAGE

STARTUP STAGE

FIRSTSTAGE

SECOND STAGE

THIRDSTAGE

MEZZANINE STAGE

BRIDGE STAGE

10. Investment Banks11. Lessors / Factors

9. Earnings

7. Strategic Partners6. Venture Capitalists

5. Angels4. Love Money

3. Government Programs

1. Founders2. Commercial Banks

12. Public

8. Private Equity

$5b

$1.02t$6b

$10b

© 2009 Waterford Executive Services Ltd. All rights reserved. 37

CANADIANS’ PERSONAL FINANCIAL ASSETS

ASSET TYPE:Mutual funds $497b*

Deposits $203b Stocks $200bBonds $ 80bOthers $ 50b

$1.02t

About 50% is held inside RRSPs

* Investment Funds Institute of Canada, March 31, 2009

© 2009 Waterford Executive Services Ltd. All rights reserved. 38

RRSPs• 7.2m (≈ 25%) Canadians have RRSPs• > $60,000 average contents• 6m tax filers subscribe $33b annually• + $33b internal growth• = $63b annual growth• > $500b unused RRSP contribution room

growing by $25b annually• 100% eligible to invest in Qualified

Investments which include SBC Shares

© 2009 Waterford Executive Services Ltd. All rights reserved. 39

HOW MUCH IS $1.02 TRILLION

FIN. ASSETSPOPULATION*

Surrey

New Westminster

Vancouver $21,021,218,000587,891

$14,379,677,000

$6,314,650,400

402,150

176,599

Burnaby 205,477

AREA= $35,757 per Canadian man, woman & child

1,914,112 $68,442,901,300

$7,347,241,000

* 2006 BC government statistics

Richmond

Coquitlam

Delta

119,319

102,939

125,326

$4,890,341,800

$4,481,281,700

$4,266,489,400

Langley

North Vancouver

$3,680,789,800

$2,061,212,200

136,766

57,645

© 2009 Waterford Executive Services Ltd. All rights reserved. 40

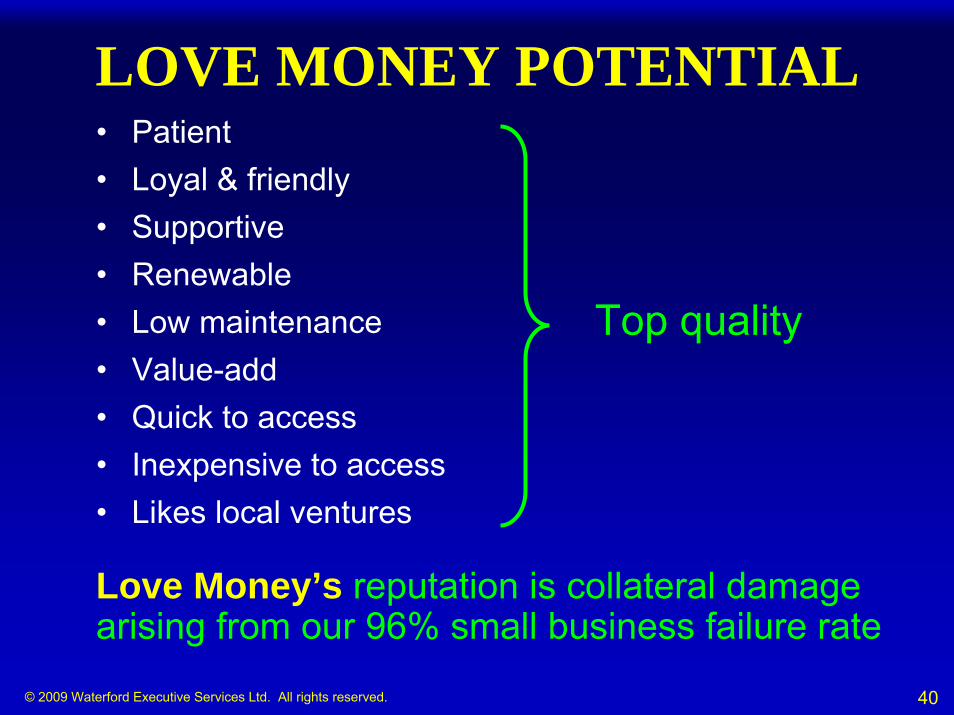

LOVE MONEY POTENTIAL• Patient• Loyal & friendly• Supportive• Renewable• Low maintenance• Value-add• Quick to access• Inexpensive to access• Likes local ventures

Top quality

Love Money’s reputation is collateral damage arising from our 96% small business failure rate

© 2009 Waterford Executive Services Ltd. All rights reserved. 41

$2,000,000

Q How do we raise up to $2,000,000 of top-quality Seed and Startup Capital?

A3 We prepare for our financing campaign

A1 We build an SME that is a worthy investment opportunity

A2 We target FF&BA

A4 We execute a new type of financing campaign

© 2009 Waterford Executive Services Ltd. All rights reserved. 42

The right valuation

The right offering

The right money

The right financing campaign

The right present-ation

The right investors

The right post startup

people

The right leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 43

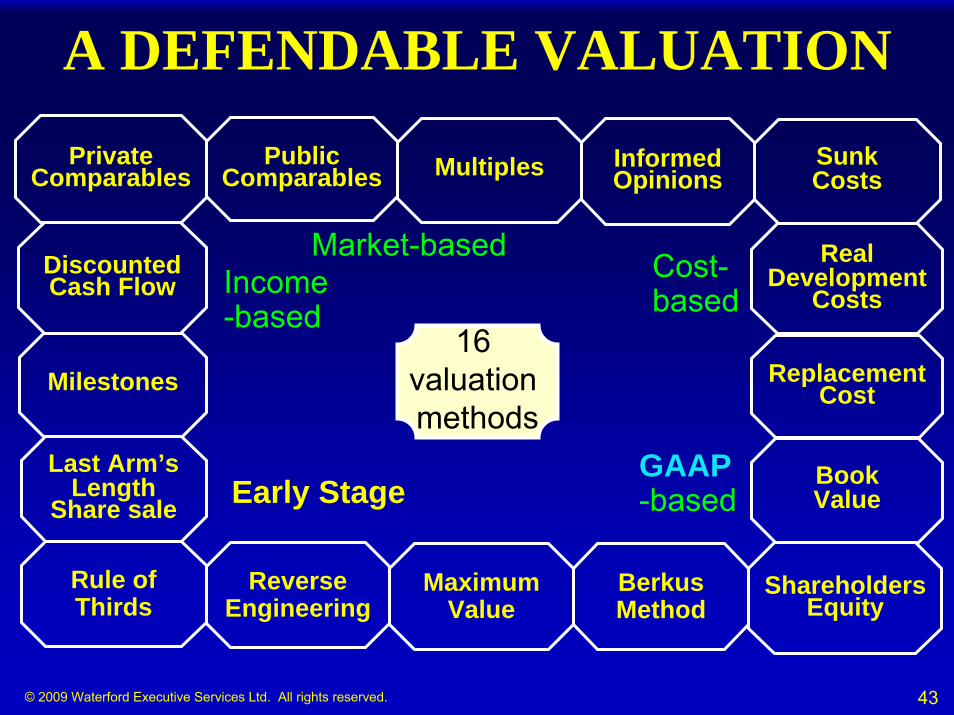

16 valuation methods

MultiplesPrivate Comparables

Public Comparables

Sunk Costs

Real Development

Costs

Replacement Cost

BookValue

Discounted Cash Flow

Informed Opinions

A DEFENDABLE VALUATION

Income -based

Cost-based

Market-based

Milestones

Last Arm’s Length

Share sale Early StageGAAP-based

Shareholders Equity

Reverse Engineering

Maximum Value

Rule of Thirds

BerkusMethod

© 2009 Waterford Executive Services Ltd. All rights reserved. 44

The right

offering

The right money

The right valuation

The right financing campaign

The right present-ation

The right investors

The right post startup

people

The right leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 45

THE RIGHT OFFERING1. Confidence Boosters2. No Confidence Killers3. Competitive returns4. Competitive liquidity5. Tax benefits6. Perks7. Full disclosure8. A monitoring mechanism

© 2009 Waterford Executive Services Ltd. All rights reserved. 46

The right present -ation

The right offering

The right valuation

The right financing campaign

The right money

The right investors

The right post startup

people

The right leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 47

THE RIGHT PRESENTATION

• Format• Structure• Content• Support tools• Delivery

© 2009 Waterford Executive Services Ltd. All rights reserved. 48

The right financing campaign

The right offering

The right valuation

The right money

The right present-ation

The right investors

The right post startup

people

The right leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 49

CONTACT FINANCING®

DEFINITION:Contact Financing® is a 12 step sequential System for attracting several Financing Rounds of Seed and Startup Capital by motivating Directors, Officers and Control People to introduce their Immediate Family Members, Close Personal Friends and Close Business Associates to the Company’s Early Stage Offerings

© 2009 Waterford Executive Services Ltd. All rights reserved. 50

ANALOGY• Think residential houses• For Sale by Owner Vs. Licensed Realtor

For Sale by Owner5% - 10%

• Compare sales success rates:Licensed Realtor

60% - 95%

© 2009 Waterford Executive Services Ltd. All rights reserved. 51

ANALOGY

Contact Financing® does for Early Stage business financing what a good licensed realtor does for residential house sales - it evokes results that are ≈ 10 times better

© 2009 Waterford Executive Services Ltd. All rights reserved. 52

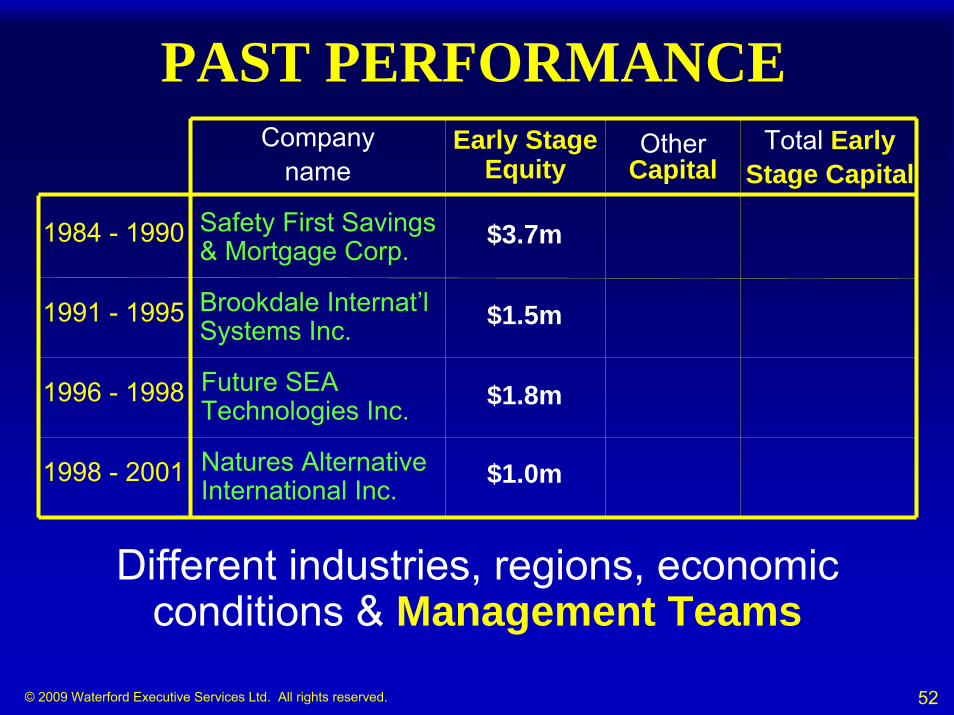

PAST PERFORMANCE

1991 - 1995

Company name

Total EarlyStage Capital

1996 - 1998

1984 - 1990 Safety First Savings & Mortgage Corp.

Brookdale Internat’l Systems Inc.

Future SEA Technologies Inc.

1998 - 2001 Natures Alternative International Inc.

$1.5m

Other Capital

Early StageEquity

$1.8m

$1.0m

$3.7m

Different industries, regions, economic conditions & Management Teams

© 2009 Waterford Executive Services Ltd. All rights reserved. 53

CONTACT FINANCING™

TWELVE STEP PROGRAM:1. Build a Positive Image locally2. Build a financing sales team3. Recruit a financing team leader4. Build a contact list5. Convert contacts into invitees6. Convert invitees into attendees7. Host a series of Long Seminars8. Cater to Investors varied circumstances9. Understand RRSPs10. Understand Trustees11. Follow up and enroll

12. Repeat x 3

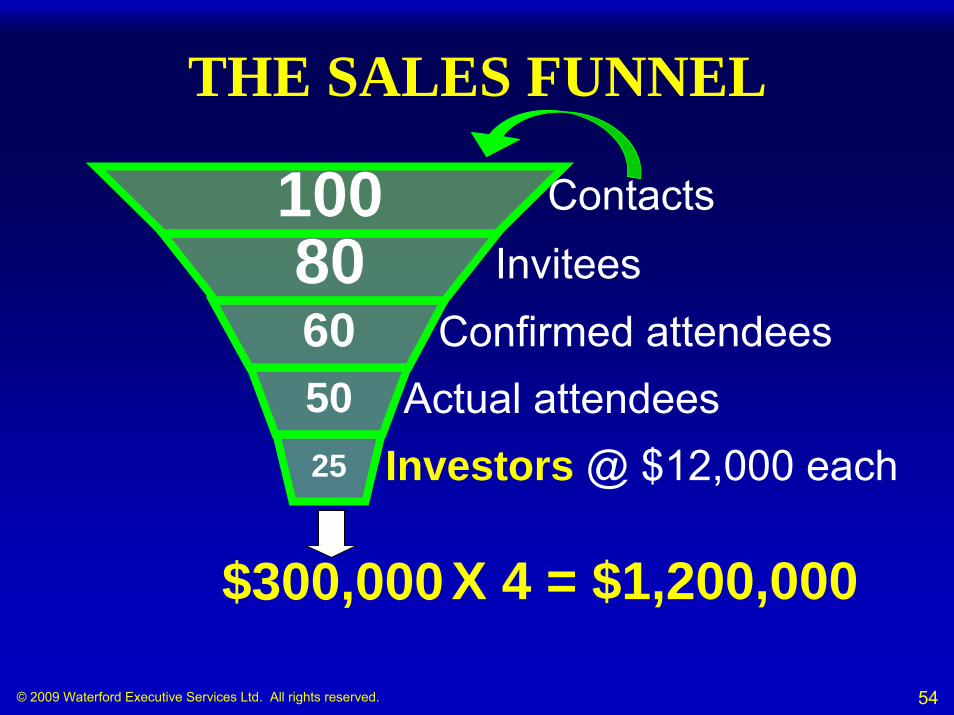

© 2009 Waterford Executive Services Ltd. All rights reserved. 54

THE SALES FUNNEL

10080605025

$300,000

ContactsInvitees

Confirmed attendeesActual attendees

Investors @ $12,000 each

X 4 = $1,200,000

© 2009 Waterford Executive Services Ltd. All rights reserved. 55

The right offering

The right valuation

The right financing campaign

The right present-ation

The right investors

The right post startup

people

The right money

The right

leverage

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 56

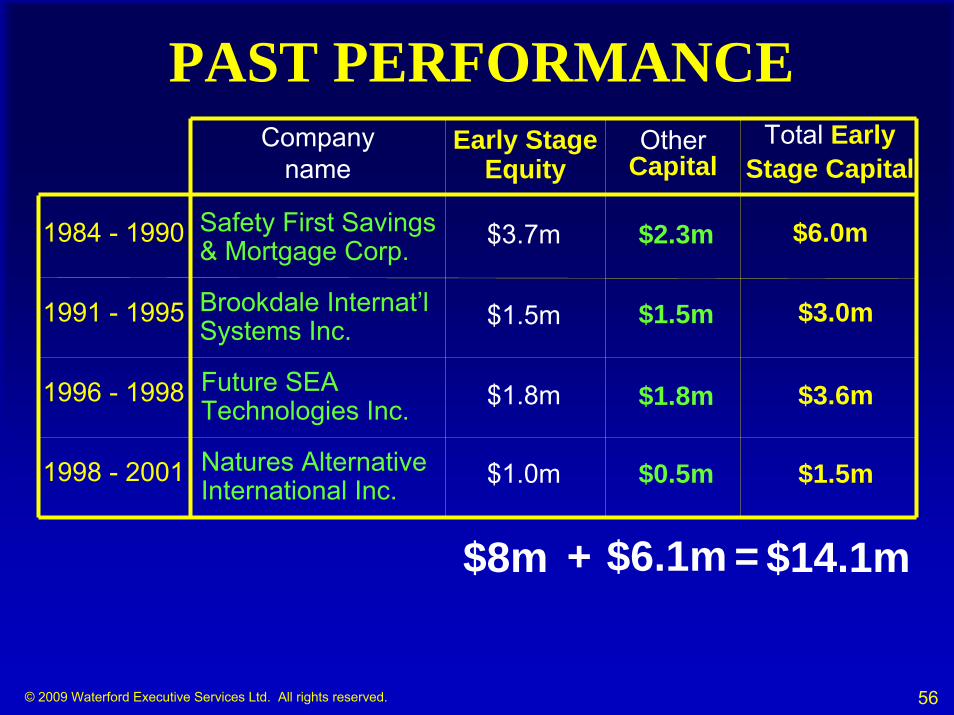

PAST PERFORMANCE

1991 - 1995

Companyname

Total Early Stage Capital

1996 - 1998

1984 - 1990 Safety First Savings & Mortgage Corp.

Brookdale Internat’l Systems Inc.

Future SEA Technologies Inc.

$6.0m

$3.0m

$3.6m

1998 - 2001 Natures Alternative International Inc. $1.5m

$1.5m

Other Capital

Early StageEquity

$1.8m

$1.0m

$3.7m $2.3m

$1.5m

$1.8m

$0.5m

$8m $6.1m $14.1m+ =

© 2009 Waterford Executive Services Ltd. All rights reserved. 57

ELIGIBLE COSTS• Government Programs are generally

tied to Eligible Costs• If Eligible Costs are incurred before

Government Program approval, the capital used to pay for them cannot be leveraged

• The sequence of incurring Eligible Costs is the key to optimally using Government Programs

© 2009 Waterford Executive Services Ltd. All rights reserved. 58

SEQUENCE FOR MAXIMUM LEVERAGE

Apply for Government Program fundingLaunch program to raiseEquity or Debt

Receive Government Program funding approval

Receive Equity orDebt

Month31 2 4

Incur Eligible Costs and apply for re-imbursement

5

© 2009 Waterford Executive Services Ltd. All rights reserved. 59

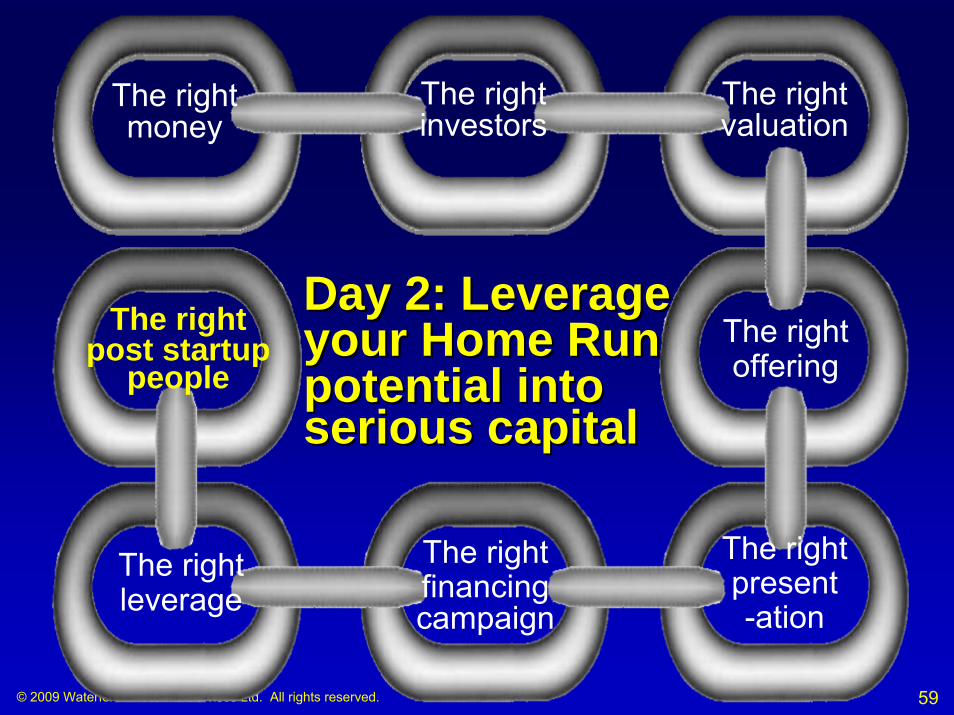

The right offering

The right valuation

The right financing campaign

The right present-ation

The right investors

The right money

The right leverage

The right post startup

people

Day 2: Leverage Day 2: Leverage your Home Run your Home Run potential into potential into serious capitalserious capital

© 2009 Waterford Executive Services Ltd. All rights reserved. 60

SME AT END OF Q4• Skilled Founder(s)• Strong market• Strong product• Defined Exit Strategy• Great people:

– Board– Advisory Councils– Professional Advisors– Management– Employees

• Robust Infrastructure• Serious $$$$$$ in bank• Attitude• Confidence• Discipline

© 2009 Waterford Executive Services Ltd. All rights reserved. 61

CONCLUSION

© 2009 Waterford Executive Services Ltd. All rights reserved. 62

SUCCESSSUCCESS IS A CHILD OF 2 PARENTS:• Knowing what to do• Doing what you know:

– if it is to be it is up to me– Entrepreneurs are doers, not dreamers

“Winners are simply willing to do what losers won’t” Slogan in the Hilary Swank, Clint Eastwood, Morgan Freeman movie ‘Million Dollar Baby’

© 2009 Waterford Executive Services Ltd. All rights reserved. 63

EntrepreneurInvestor