-

7/28/2019 Weekly Strategic Plan 11192012

1/11

Liquidity Cycle

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

The second week following the re-election of President Obama

ended the same way as the rst, with markets lower. The media

removed their self-

imposed blinders and gags and discovered the scal cliff. This

pending disaster and source of potential calamity which had been

studiously ignored

, overshadowed by the horrifying image of a successful business

man being elected to the highest ofce in the land. No one in the

media has asked

why there is a scal cliff. Why all these important decisions and

tax hikes were scheduled at the same time. (Hint, Jan 1 2013 is

after an important

election.) We have president who has not passed a budget in his

entire time in ofce, even when he had control of both the House and

the Senate. I

know I am lled with condence that the demonstrated incompetent,

of both parties, will suddenly develop the wisdom and integrity to

deal the scal

problems of the United States. Is it really surprising that

investors are showing some reluctance to invest?

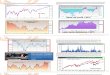

This chart is the SPX hourly since July. With the prole overlay

we can see the market stair stepping higher right up to QEnity was

announce

September 14, where upon the market attened and began to

pullback. Then following a rally as Obama secured the election the

market promptly

walked off of its own cliff. All of this involves a rational

response by investors facing a doubling of capital gains taxes.

The next charts show the SPX Index and the Liquidity Cycle Index

together with a ratio of the two. The following chart shows the NDX

Index also with

the Liquidity Cycle Index and a ratio. The charts are similar

but the NDX version shows a very clear change in behavior as the

NDX which had beenleading turned aggressively lower. The magnitude

of these pullbacks is still not very large and may well provide a

very good entry point for what has

been a bull market. Agreements that avoid the scal cliff would

likely give some optimism and produce a bounce. But, only if the

agreements dont

result in policy prescriptions of a staunchly anti-business

avor.

The next chart is a similar one to the two previous charts. This

time we have the MSCI World Index with Innium Global Growth

ExpectationsThe recent drop in the World index is more severe than

the growth proxy. We want to track this to see if some divergence

develops which wo

probably come from stronger relative behavior in Asian markets.

Those markets and currencies have underperformed but will pick up

sharply

China appears to be improving.

Here is Apple just for a long view of the stock that more than

any other has dened the bull market and is also leading the

correction. This is a

scale chart and that little pullback almost a 30% drop from the

highs. That was one of Peter Lynchs ten baggers just since early

2009.

-

7/28/2019 Weekly Strategic Plan 11192012

2/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

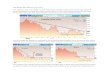

The xed income market is still being held hostage by the Fed but

the recent anxiety that has hurt the equity market has left its

footsteps in the rate

markets too. This chart has the generic ten year and 30 year

treasury yield indices overlaid. Clearly the rates have dropped

back toward their lower

levels on fears of slowing economic action, or risk off as the

current slang describes market pessimism.

SECTORS

Consumer Staples is the best performing sector since the

election and even it is down 3.1%.

Bespoke Investments had the following comment in their weekly

review Saturday:

The S&P 500 is down 7.9% from its closing high on September

14th, but the decline has been especially painful due to the way it

has gotten there.

What weve seen during this pullback is a lot of head fakes

higher at the open and then a steady move lower throughout the

trading day. Any buy in

the morning has quickly turned into a loss as the day goes on.

In the chart below, we highlight the average hourly change (%) of

the S&P 500 since

the September 14th high. As shown, the index has actually

averaged a small gain in the rst half hour of trading (0.03%), but

then it has averaged

declines during every hour from 10 AM through the close.

-

7/28/2019 Weekly Strategic Plan 11192012

3/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

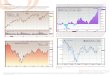

We (Bespoke) have made numerous mentions of the fact that unlike

prior pullbacks where Europe led US markets lower, the current

pullback has been

US-centric. For most of 2012 up until the last week or so,

investors in the US took solace in the fact that we were much

better off t han Europe. Any

time the market declined, it was blame Europe time. That is no

longer the case.

As shown below, the S&P 500 is now up just slightly more

than Europes stock market in 2012. Now its European investors that

are blaming the US for

market declines, and if we do go over the Fiscal Cliff, they

will be the ones saying at least were better off than the US.

Ironic isnt it.

The role reversal between the US and rest of the world is

evident in Q4 performance numbers of international markets. So far

this quarter, the S&P

500 is down 3.67%, which ranks dead last in QTD performance of

just the G7 countries. France is up the most of the G7 countries

this quarter witha gain of 2.30%. Italy and the UK are the only

other G7 countries in the black this quarter, while Germany,

Canada, Japan and the US are in the red.

Bespoke Inv.

Credit spreads in Europe improved very slightly this week after

deteriorating last week. This seemed to result from rumors of some

debt relief for

Greece. No tangible announcements have been forthcoming so

far.

-

7/28/2019 Weekly Strategic Plan 11192012

4/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Volatility Environment

Bullish trends in place in xed income markets but everything

else is bearish or neutral. Quiet and neutral vol readings except

in Indices, gas oil,

heating oil, and Yen.

The next few pages will have the volatility tables with 30 day

implied, implied to realized, and skew readings for the indices,

commodities, and

currencies.

-

7/28/2019 Weekly Strategic Plan 11192012

5/11THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Commodities Currency

-

7/28/2019 Weekly Strategic Plan 11192012

6/11THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Commodity Futures 5 day % price changes as of Friday

-

7/28/2019 Weekly Strategic Plan 11192012

7/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

-

7/28/2019 Weekly Strategic Plan 11192012

8/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Articles & Commentary

Niall Ferguson On Chinas Gold And The Tremendous Flux In

International Order

This is a time of tremendous ux in the international order is

how Harvards Niall Ferguson describes the world in which we live as

he opines

expertly on the change in China, Europes pending lost decade,

and the Middle Easts post-Arab Spring disestablishment of the 1970s

ord

with GoldMoneys Alasdair Macleod. From Chinas need to begin

privatizing SOEs and globalizing the RMB (with an interesting focus

on

introduction of reliable property rights to enable the middle

class) to concerns about its large dollar holdings (and the

top-down and bottom-u

diversication into gold that continues); Ferguson notes that the

ongoing attempt to diversify its wealth and revenues (stock and ow)

is relativ

limited by the ability to secure hard assets but adds that as

the worlds trade center of gravity shifts east at a very fast pace

so gold will ow

the West to the rest as Western power declines and the Asia bloc

rises. A fascinating macro-economic and geo-political discussion

tha

concludes with a shift t hrough Russias energy quagmire, Japans

debt problems, and the faulty design of the European Union.

VIDEO Link

Kyle Bass: Fallacies Such As MMT Are Leading The Sheep To

Slaughter And We Believe War Is Inevitable

Below are some of the key highlights from Kyle Bass latest, and

as usual, must read letter:

On central banks and t he nal round of global monetary

debasement:

Central bankers are feverishly attempting to create their own

new world: a utopia in which debts are never restructured, and

there are no

consequences for scal proigacy, i.e. no atonement for prior

sins. They have created Potemkin villages on a Jurassic scale. The

sum total of

the volatility they are attempting to suppress will be less than

the eventual volatility encountered when their schemes stop

working. Most refer

comments like this as heresy against the orthodoxy of economic

thought. We have a hard t ime understanding how the current

situation ends a

way other than a massive loss of wealth and purchasing power

through default, ination or both.

In the Keynesian bible (The General Theory of Employment,

Interest and Money), there is a very interesting tidbit of Keynes

conscience in th

chapter titled Concluding Notes from page 376:

[I]t would mean the euthanasia of the rentier, and,

consequently, the euthanasia of the cumulative oppressive power of

the capitalis

exploit the scarcity value of capital. Interest today rewards no

genuine sacrice, any more than does the rent of land. The owner of

capital

obtain interest because capital is scarce, just as the owner of

land can obtain rent because land is scarce. But whilst there may

be intrinsic refor the scarcity of land, there are no intrinsic

reasons for the scarcity of capital.

Thus we might aim in practice (there being nothing in this which

is unattainable) at an increase in capital until it ceases to be

scarc

that the functionless investor will no longer receive a bonus[.]

(emphasis added)

This is nothing more than a chilling prescription for the

destruction of wealth through the dilution of capital by monetary

authorities.

Central banks have become the great enablers of scal proigacy.

They have removed the proverbial policemen from the bond market

highw

If central banks purchase the entirety of incremental bond

issuance used to nance scal decits, the checks and balances of

normal marke

interest rates are obscured or even eliminated altogether. This

market phenomenon does nothing to encourage the body politic to

take their fo

off the spending accelerator. It is both our primary fear and

unfortunately our prediction that this quixotic path of spending

and printing will con

ad innitum until real cost-push ination manifests itself. We

wont get into the MV=PQ argument here as the reality of the

situation is the fact

the V is the solve for variable, which is at best a concurrent

or lagging indicator. Given the enormity of the existing government

debt stock, it

not be possible to control the very ination that the market is

currently hoping for. As each 100 basis points in cost of capital

costs the US fede

government over $150 billion, the US simply cannot afford for

another Paul Volcker to raise rates and contain ination once it

begins.

Hayek was, of course, right:

The current modus operandi by central banks and sovereign

governments threatens to take us down Friedrich von Hayeks Road to

Serfdom

Published in 1944, its message, that all forms of socialism and

economic planning lead inescapably to tyranny, might prove to have

been pres

In the 1970s, when Keynesianism was brought to crisis,

politicians were vociferously declaring that attempting to maintain

employment throug

inationary means would inevitably destroy the market economy and

replace it with a communist or some other totalitarian system which

is th

perilous road to be avoided at any price. The genius in the book

was the argument that serfdom would not be brought about by

evil

like Stalin or Hitler, but by the cumulative effect of the

wishes and actions of good men and women, each of whose

interventions co

easily justied by immediate needs. We advocate social

liberalism, but we also need to get there through scal

responsibility. Pushing for in

at this moment in time will wreak havoc on those countries whose

cumulative debt stocks represent multiples of central government

tax reven

http://www.youtube.com/watch?feature=player_embedded&v=arCgWVZD3jA#t=0shttp://www.youtube.com/watch?feature=player_embedded&v=arCgWVZD3jA#t=0shttp://www.zerohedge.com/news/2012-11-17/kyle-bass-falacies-such-mmt-are-leading-sheep-slaughter-and-we-believe-war-inevitablhttp://www.zerohedge.com/news/2012-11-17/kyle-bass-falacies-such-mmt-are-leading-sheep-slaughter-and-we-believe-war-inevitablhttp://www.youtube.com/watch?feature=player_embedded&v=arCgWVZD3jA#t=0shttp://www.youtube.com/watch?feature=player_embedded&v=arCgWVZD3jA#t=0s

-

7/28/2019 Weekly Strategic Plan 11192012

9/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Trillions of dollars of debts will be restructured and millions

of nancially prudent savers will lose large percentages of their

real purchasing po

exactly the wrong time in their lives. Again, the world will not

end, but the social fabric of the proigate nations will be

stretched and in some ca

torn. Sadly, looking back through economic history, all too

often war is the manifestation of simple economic entropy played to

its logica

conclusion. We believe that war is an inevitable consequence of

the current global economic situation .

All this and much more, including the usual detailed summary

depicting the Japanese ultra slow-motion trainwreck (which is

picking up speed

none other than Seiji Maehara, state minister for economic and

scal policy, admitted yesterday when he said that [The Japan

economy] is

dire state) in the full letter below:

Link to the full letter at Scribd.com

The non-linearity of expenses versus revenues is what will bring

them down.

Pavlovs Party is ending, and when it does, it will happen so

fast no reaction will be possible:

Through travel and meetings around the world, it has become

clear to us that most investors possess a heavily anchored bias

that has been

engrained in their belief systems mostly through inductive

reasoning. Using one of the Nobel Laureate Daniel Khanemans

theories, participants fall

under an availability heuristic whereby they are able to process

information using only variables that are products of recent data

sets or events. Lets

face it the brevity of nancial memory is shorter than the

half-life of a Japanese nance minister.

Humans are optimistic by nature. Peoples lives are driven by

hopes and dreams which are all second derivatives of t heir innate

optimism. Humans

also suffer from optimistic biases driven by the rst inalienable

right of human nature, which is self-preservation. It is this reex

mechanism in our

cognitive pathways that makes difcult situations hard to reect

and opine on. These biases are extended to economic choices and

events. The

fact that developed nation sovereign defaults dont advance

anyones self-interest makes the logical outcome so difcult to

accept. The inherent

negativity associated with sovereign defaults brings us to such

difcult (but logical) conclusions that it is widely thought that

the powers that be

cannot and will not allow it to happen. The primary difculty

with this train of thought is the bias that most investors have for

the baseline facts: they

tend to believe that the central bankers, politicians, and other

governmental agencies are omnipotent due to their success in

averting a nancial

meltdown in 2009.

The overarching belief is that there will always be someone or

something there to act as the safety net. The safety nets worked so

well recently that

investors now trust they will be underneath them adinnitum.

Markets and economists alike now believe that quantitative easing

(QE) will always

work by ooding the market with relatively costless capital. When

the only tool a central bank possesses is a hammer, everything

looks like a nail.

In our opinion, QE just doesnt stimulate private credit demand

and consumption in an economy where total credit market debt to GDP

already

exceeds 300%. The UK is the poster child for the abject failure

of QE. The Bank of England has purchased over 27% of gross

government debt (vs.

12% in the US). UK bond yields have all but gone negative and

are now negative in real terms by at least ?1%. Unlimited QE and

the zero lower

bound (ZLB) are likely to bankrupt pension funds whose expected

returns happen to be a good 600 basis points (or more) higher than

the 10?year

risk-free rate. The ZLB has many unintended consequences that

are impossible to ignore.

Despite reading through Keynes works, we didnt nd a single index

referencing the ZLB or any similar concept. In his General Theory,

there are 64

entries in the index under Interest but no entry for the ZLB,

zero rates, or even really low rates.

Our belief is that markets will eventually take these matters

out of the hands of the central bankers. These events will happen

with such rapidity that

policy makers wont be able to react fast enough.

On the lunacy of such modern economic theories as MMT (which may

or may not stand for Magic Money Trees)

The fallacy of the belief that countries that print their own

currency are immune to sovereign crisis will be disproven in the

coming

months and years. Those that treat this belief as axiomatic will

most likely be the biggest losers. A handful of investors and asset

managers have

recently discussed an emerging school of thought, which

postulates that countries, as the sole manufacturer of their

currency, can never become

insolvent, and in this sense, governments are not dependent on

credit markets to remain scally operational. It is precisely this

line of thinking

which will ultimately lead the sheep to slaughter.

The inevitable end of that supremely awed monetarist experiment

- the Eurozone:

Each subsequent save of the European debt crisis has been

devised by the Eurocrats coming up with some new amalgamation of an

entity that is

more complex than its predecessor that is designed to project

size, strength, and condence to investors that the problem has been

solved. Raoul,

a friend of mine who resides in Spain, put it best:

Lets just clear this up again. The ECB is going to buy bonds of

bankrupt banks just so the banks can buy more bonds from bankrupt

governments.

Meanwhile, just to prop this up the ESM will borrow money from

bankrupt governments to buy the very bonds of those bankrupt

governments.

The EFSF, the IMF, the ESM, and the OMT (and who knows what

other vehicles they will dream up next) have all been developed to

serve as anoptical backstop for investors globally. The Eurocrats

are sticking with the Merkelavellian playbook of hiding behind the

complexity of these various

schemes. All one has to do is review the required contributions

to said vehicles from bankrupt nations to realize that the circular

references are

already beginning to show in broad daylight. Does anyone stop to

consider that the two largest contributors to the IMF are the two

largest debtor

nations in the world? Are t hings beginning to make sense

now?

In the end, the EMU wont look the same, if i t exists at

all.

And nally, a less than rosy outlook for the entire developed

world.

Intended and Unintended Consequences: The Darden Approach to

Obamacare

One of the few bright spots for job creation over the preceding

year or two was the hospitality segment. This includes restaurants,

hotels, bars

Most of the work comes with low base pay. Tip income makes up a

majority of the employees total compensation.

Managements were happy to add workers as business conditions

permitted. Obamas reelection cemented the fate of his new

healthcare

monstrosity. It now will be implemented and thats very, very bad

news for the restaurant industry.

Why is that? Many fast food and casual dining chains generate

decent revenues but low net prot margins. Some, like McDonalds

(MCD), ha

been offering employees low-priced but relatively bare-bones

health care policies on a voluntary sign-up basis. That was

affordable both for lo

wage employees and MCD.

Obamacare takes away that option. Minimum coverage requirements

under the ACA [Affordable Care Act] mean that (post-January 1,

2014) th

limited coverage plans can no longer be offered.

So much for that infamous claim, If you like your present health

plan and want to keep it you can.

The ACA requires that full-time employees must be enrolled in an

approved healthcare plan or the employer will be subject to a

$2,000 per he

penalty (now called a tax by the Supreme Court). Worse still,

the denition of full-time has been dialed back to just 30 hours a

week.

At Novembers Restaurant Finance & Business Development

Conference Darden Restaurants (DRI) test plan was much discussed.

They are

reducing hours of employees to below 30 to limit the number of

employees who would be eligible for coverage.

Darden is the parent of Olive Garden, Red Lobster, Longhorn

Steakhouse, Bahama Breeze and other chains. They employee about

185,000

people.

Can employers simply wait until 2014 to make adjustments to

their employee hours? No. The ACA has a look-back period to keep

businesses

doing exactly that. Determining if a worker meets that 30-hour

threshold will be done using their 2013 hours worked.

The cost of providing an approved policy will likely be well

above t he $2,000 tax imposed. Employers have a huge incentive to

purge their

businesses of scheduled workers with 30+ hour schedules. That

means many people will be getting hours cut back now, in 2012, in

orde

avoid being classied as full-time in 2014.

Instead of helping waiters, greeters, kitchen staff and busboys

become more prosperous ObamaCare may well curtail their ability to

work as m

hours as they would prefer.

It might also deprive business owners of the chance at rewarding

their best workers with maximum earnings power. The cost

differential betwe

part-time and full-time might be the swing factor separating

protability and bankruptcy.

Brad Richmond, Dardens CFO, was asked whether reducing hours

will allow the restaurant to maintain customer engagement and

employeesatisfaction. I think its going to be very hard, he said.

They work 30 35 hours for a reason.

Another potential strategy discussed at the conference? Dont

provide health insurance at all. From a strictly economic viewpoint

paying the

$2,000-per-year, per-employee tax penalty for not providing

coverage might well be the best choice.

Alexis Becker, of accounting rm SS&G, noted that most

scenarios nd paying the penalty will be cheaper for employers than

providing cover

The ACA only covers employers with 50 or more workers. Franchise

owners will be loath to exceed, or even approach this potentially

busines

lethal number.

http://www.scribd.com/doc/113621307/Kyle-Basshttp://www.marketshadows.com/2012/11/17/intended-and-unintended-consequences-the-darden-approach-to-obamacare/http://www.marketshadows.com/2012/11/17/intended-and-unintended-consequences-the-darden-approach-to-obamacare/http://www.scribd.com/doc/113621307/Kyle-Bass

-

7/28/2019 Weekly Strategic Plan 11192012

10/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

That could mean cutting back on overall operating hours or

running with much leaner stafng levels. It also makes opening new

units much less

attractive. All three of those trends are bad news for workers

and jobs.

Most franchiser owners keep each unit as a separate legal entity

in order to avoid triggering the 50-employee rule. Rumors have been

oating

around about new government regulations that would lump multiple

units back together for ACA purposes.

That would be an absolute dagger to the heart of owners of t

hese multiple units with segregated legal ownership.

Hasnt our president been saying since 2008Job creation is my #1

priority? Obamacare is a job killer.

Actions speak louder than words.

No matter how this ultimately plays out it will be a huge

headwind for the protability of this industry. Avoid stocks in this

group until they start pricing

in the future bottom line hits.

Ray Dalio

Here is a link to a paper by Ray Dalio of Bridgewater, the

largest hedge fund in the world. The paper is too long to include

but I found it to be very

interesting and clear.

How the Economic Machine Works

Ray Dalio | October 2008 (Updated March 2012): The economy is

like a machine. At the most fundamental level it is a relatively

simple machine, yet

it is not well understood. I wrote t his paper to describe how I

believe it works.

Goodbye Japan, Hello Korea

As the government and Bank of Japan constantly survey the

marketplace for speculation while intervening en masse with

ever-decreasing levels of

effectiveness, we thought the following charts would highlight

the impact of the relative strength of the JPY. Of course, in the

past, at least the trade

surplus (thanks to these legacy companies) used to provide

incremental capital into the country but now even t hat is gone

[5]. As Credit Suisse

notes, the TWI of the JPY has appreciated by more than 40% post

crisis even more than the CHF!But it is the relative strength

versus the KRW

that is really hurting Japanese rms. The Won plummeted sharply

post crisis and has recovered nowhere near pre-crisis levels. Some

of this shift

in relative competitiveness may be reected in the market cap of

Samsung versus that of major Japanese tech rms. Samsung is more

than three

times the size of Japans top technology rms.

Since the crisis, Samsung has overwhelmed the largest 5 Japanese

Tech rms...

Why is this a concern? Because whereas in the past Japans

economy at least had a source of endogenous capital courtesy of its

trade surplu

offset all the other drains of domestic capital, this is no

longer the case as we showed recently [5].

http://www.bwater.com/Uploads/FileManager/research/how-the-economic-machine-works/How-the-Economic-Machine%20Works--A-Template-for-Understanding-What-is-Happening-Now-Ray-Dalio-Bridgewater.pdfhttp://www.bwater.com/Uploads/FileManager/research/how-the-economic-machine-works/How-the-Economic-Machine%20Works--A-Template-for-Understanding-What-is-Happening-Now-Ray-Dalio-Bridgewater.pdf

-

7/28/2019 Weekly Strategic Plan 11192012

11/11

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

This means that the government is now effectively the only

source of capital to offset all other Current Account outows. This

also means that Japan

will be forced to monetize more and more, issue more and more

debt, even as its population gets older and older and is forced to

withdraw ever

more savings, shrink the nancial system, and sell ever more

securities, thus nally accelerating the collapse of the Japanese

monetary neutron

stars 30+ year implosion into what, inevitably, becomes a black

hole.

This is Thanksgiving week and I hope each of you has a wonderful

Thanksgiving with family and friends. I also hope you have t he

chance to reect

on events and conditions in the world and in your life focusing

on the good things you have and the good things to come. Personally

I do not think

there has ever been a better time to be alive, or a time with

more progress ahead. Sure there are huge problems, but that has

always been true.

Never have we had so many tools with which to attack problems

nor so many educated minds around the globe searching for

solutions.

Bruce Lawrence November 19, 2012