-

7/28/2019 Weekly Strategic Plan 02132012

1/9

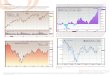

Liquidity Cycle

Greek version of Groundhog Day played out all week as an

agreement was near, agreed to, or not so much, near, done, not so

much, etc.

The US market nally had an off day after a steep steady incline

in January and early February. Frankly, a little setback was needed

to let

participants catch their breadth.

The individual charts of components of the indicator relative to

the SPY etf reveal pretty clearly the surging relative strength of

the lead growth

compared to a similar chart of the most defensive components

which are now losing ground. The early cycle group has had several

brief per

positive performance breakouts over the past year and is

somewhat unproven at this point. But the late cycle group has

outperformed for a si

period and has rather rigorously broken the previous trend,

lending conviction to the belief in prospects for a more lasting

period of positive ac

growth securities.

The ICM Liquidity Cycle Indicator experienced a very small

pullback Friday, yet is still pointing higher.

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

-

7/28/2019 Weekly Strategic Plan 02132012

2/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

ECRI Weekly Leading Index (black) did turn higher last week as

LCI hinted, this despite the continued recessionary stance at

ECRI.

(see video) I am am going to utilize some information from

Bespoke research here since their weekly review is chock full of

good information this week.

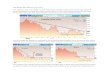

In the scope of the last few years, t he period of calm that we

have seen so far this year seems out of place and not the norm.

From a longer

term perspective, however, the 30 day stretch is anything but

rare. The chart below shows streaks where the S&P 500 went

without a decline

of 1% or more. As shown, there have been numerous periods where

the index went 30 days, or for that matter, much longer, without a

1% drop.

Since 1980 alone we have seen three separate stretches where the

index went more than 100 trading days without a 1% decline.

Taking an even longer term view, since 1928 there have been 135

streaks where the S&P 500 went without a 1% drop for more than

30 trading

days, and of those streaks, eleven lasted more than 100 trading

days.

Even though AAPL was not chosen to replace GM, it is always fun

to see what might have been. To that end, we have recalculated

the

performance of the DJIA to reect how it would have done if AAPL

was added to the DJIA instead of CSCO. The chart below shows the

current

DJIA (blue line) compared to the Apple DJIA (red line).

Currently, the DJIA is trading at a level of roughly 12,865, which

is about 12.1% off

its all-time high of 14,198.10 from October 2007. If AAPL was in

the DJIA, though, the index would not only be signicantly higher

(14%), but

it would also be trading at an all-time high of 14,636. Granted,

you cannot go back and change the past, but we wonder if investor

sentiment

would be more positive if the DJIA was trading at record

highs?

http://www.businesscycle.com/http://www.bespokepremium.com/http://www.bespokepremium.com/http://www.businesscycle.com/

-

7/28/2019 Weekly Strategic Plan 02132012

3/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

The next couple of pages have a table of a broad range of ETF

arranged by type and the daily closes on Friday. The overwhelming

color

red illustrates the breadth of downward price action. Green

quotes are pretty much limited to inverse and short funds, as well

as a few x

income securities.

SECTOR : The Bespoke Table reveals through the correlation

column the sectors driving the market this year.

ETF daily on Friday Feb 10

Sector charts covering 3 months:

-

7/28/2019 Weekly Strategic Plan 02132012

4/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Commodites: I have found some different tables on the Bloomberg

that I am using this week. I hope these are readable because

they have a lot of information that is useful in a fairly

concise grouping. These include the metals outright, and various

spread

indications as well as price, 5 day movement and seasonal

compared to normal. The Ags and Energy tables follow.

-

7/28/2019 Weekly Strategic Plan 02132012

5/9THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Ags Most outrights ag markets nished the week lower with

exceptions being Sugar, Lean Hogs, Palm oil, and lumber. Old crop

corn and wheat

both gained, though corn lost ground to wheat and beans on the

week. Also many ags are trading above seasonal norms, though wheat

and

cocoa are not.

Energies: The WTI-Brent spread probably got the most attention

as threats of embargo and possible strikes against Iran have

Brent

trading rm relative to both WTI and Dubai. WTI has its own

issues as large supplies from Canada the Bakken elds stress the

storage

capacity in Cushing Oklahoma.

-

7/28/2019 Weekly Strategic Plan 02132012

6/9

-

7/28/2019 Weekly Strategic Plan 02132012

7/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

In the meantime the meantime representing mere mortals I feel

the endgame is nearing for the falling 30 yr trend. One must expect

an

extraordinarily dismal economic picture globally to support a

long extension of the current trend lower. Though one should

remember

Japan has achieved even lower rates. Of course the Japanese lack

the zealous determination of our own currency debauchers. Japan

just does not have decient economists with degrees from the Ivy

League.

If one takes a look at the same long term period of rate

declines on a Bollinger band chart one can make the case that a

simple pull

back to the mean of the trend would still produce a signicant

price change. (Roughly a 15-point drop in 30 treasury futures.) I

submit

that while the trend may continue lower it will be grudging as

it approaches the zero bound and negative real yields. Therefore

the

chances of a large and rapid price move are now to the downside

and trades should reect that possibility. I will be looking to

sell

modest amounts of option premium above the market and /or being

long of the same to the downside. (I am talking price here now

yield) Tread lightly though; the street is littered with

premature bond bears.

Trend and Volatility Environment

-

7/28/2019 Weekly Strategic Plan 02132012

8/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

Supporting Information and Commentary Money, Money,

Everywhere

My desk is littered with analysts charts showing the explosion

of central bank assets over the past four years. As interest rates

have

dropped to just above the infamous zero bound while the global

banking system and t he developed economies have threatened to

collapse, the central banks have responded with new forms of

monetary stimulus to keep the nancial system alive and to push

their

economies toward growth. The acronyms might be different for the

methods used by the US Fed, ECB, Bank of England, Bank of

Japan, and Swiss National Bank, but these various techniques

have all served to expand the high-powered money available to

their

banking systems by at least a factor of three. These ve

countries all have ratios of central bank assets to GDP over 18%,

and in

Switzerland it is over 40%, a far cry from the old days. Add to

this the extension of swap lines between the Fed and other central

banks,

and liquidity is everywhere. Those of us in the nancial world

are surrounded by a sea of money, but just like the ditty of my

youth when

sailing on the ocean, water, water, everywhere, but not a drop

to drink, there seems to be nothing economically constructive

to

do with this money. If the idea was to keep the banking system

alive, it is obvious that this strategy will work. Clearly, giving

money

to banks at no cost or, at the worst, extremely low cost means

that they dont have to pay anything for their liabilities a perfect

match

for all of their bad-loan assets, which give them no revenue

either. This allows the banks to avoid: calling their bad loans,

causing

companies to go bankrupt or real estate to go on the auction

block, and admitting economic reality. To us, this seems to be

exactly the

strategy followed by the Bank of Japan for years, the one that

was so harshly criticized by Bernanke ten years ago.

Europe and the US now have their own zombie banks dead but they

keep on walking, not lending money or clearing out the bad

debts. If this massive infusion of liquidity was meant to help

main street, the operating economy, or the average worker, it has

been a

complete failure in each country, except Switzerland where this

was not its goal.

This gigantic ood of extremely inexpensive high-powered money

does have a major impact, not in the real economy, but in t he

liquid

investment markets. Free money sets a very low hurdle for a

short-term investment and as long as the transaction has decent

liquidity,

why not do the trade. As a result, almost every equity,

commodity, and credit market is moving higher. High beta currencies

are

moving higher as well, as risk is clearly on the front foot.

This positive mood began at the start of October, a bit more than a

week after

Bernanke announced the start of Operation Twist, a subtle way to

improve the prots of the banks and increase the risk of the Fed

without expanding its balance sheet. Global equity markets began

to climb. Bernanke then announced an expansion and cheapening

of

the US swap lines with Europe, which currently have $103 billion

outstanding, adding massively to Europe and Japans liquidity.

Mario

Draghis move into the ECB Presidency on November 1 was the next

harbinger of a new wave of liquidity, as he dropped the

renancing

rate a few days later and then announced the LTRO on December 8,

expanding the ECB balance sheet by over 4% of t he GDP in one

day later in the month. By the end of December things were

clearly moving up in all the traded markets, and Bernanke put the

cherry

on the top of the sundae not once, but several times in the last

few weeks. First, he announced that US rates would be extremely

low

into late 2014, then, a bit later, he emphasized the likelihood

of QE3 if there were any economic pause, and then Tuesday he told

theUS Senate that he was not happy with the way the economy was

growing more hopes for QE3. As the markets always respond to

monetary stimulus when the trend is already positive, prices

will be forced even higher. Although we cant be positive about

the

real economy, this expanding liquidity will keep us happy until

a political accident intervenes. Europe offers some candidates:

Greece in March, followed by France in April.

Avoiding EM economies is the biggest gamble of all

The world this year will continue to be divided into

deleveraging developed economies and emerging market economies

without

excessive debt. The US and Europe will continue to experience

sub-trend growth, with the main risk still a return to recession

or

depression. Many emerging economies will grow close to trend,

the main risks being country specic, not least ination. Developed

and

emerging economies will continue to experience broadly

synchronised intra-year inventory cycles due to the increasingly

globalised

nature of the manufacturing supply chain, but the underlying

growth stories and the demand side conditions will continue to

differ

markedly.

Emerging countries are highly heterogeneous and no longer share

the common feature of potential default should they be cut off

from

foreign capital for the simple reason that they are now often

the net creditors. All their main risk scenarios are either country

specic, or

emanate from the mess in the developed world. The former can be

avoided by a portfolio investor, the latter scenarios all pose

greater

risks for those invested in the developed than in the emerging

world.

Warren Buffett: Why stocks beat gold and bonds

Follow this link for the entire article which is worthwhile. I

am including one small portion of the article which makes and

important point:

Today the worlds gold stock is about 170,000 metric tons. If all

of this gold were melded together, it would form a cube of about 68

feet

per side. (Picture it tting comfortably within a baseball

ineld.) At $1,750 per ounce -- golds price as I write this -- its

value would be

about $9.6 trillion. Call this cube pile A.

Lets now create a pile B costing an equal amount. For that, we

could buy all U.S. cropland (400 million acres with output of about

$200

billion annually), plus 16 Exxon Mobils (the worlds most

protable company, one earning more than $40 billion annually).

After these

purchases, we would have about $1 trillion left over for

walking-around money (no sense feeling strapped after this buying

binge). Can

you imagine an investor with $9.6 trillion selecting pile A over

pile B?

Mr, Buffett wrote on this topic long ago very near the $800 peak

of gold in the early 1980s. He was criticized for his view then but

he

was dead right. I believe he is right now and yet I remain

bullish of gold and believe it should be a portion of long term

portfolios. Mr.

Buffett has great faith in the eventual future of the United

States and sanity of the countrys leadership. I am less sanguine.

The currentadministration and legislative leadership is a

kleptocracy made of greedy and self-serving blowhards lacking (as a

group) the moral ber

to address issues that threaten their re-election. I prefer a

bit of protection against the mendacity of this group.

growth of government made clear

This 3 minute 40 second video clip may be the most important

Clip you have ever watched ...

This is probably the most intelligent presentation of the

truth

You have seen in a long time ....

Please take the time to view this clip and then share it with

others

Now a Positive: Study of the Day: Gene Therapy Can Restore

Vision One Eye at a Time

Ten states join effort to buy natural gas vehicles

China tells banks to roll over loans

China has instructed its banks to embark on a mammoth roll-over

of loans to local governments, delaying the countrys reckoning

with

debts that have clouded its economic prospects.

Chinas stimulus response to the global nancial crisis saddled

its provinces and cities with Rmb10.7tn ($1.7tn) in debts about

a

quarter of the countrys output and more than half those loans

are scheduled to come due over the next three years.

From The Absolute Return Letter

The latest report from Instituto Nacional de Estadistica

suggests that the overall level of unemployment in Spain now stands

at 22.85%

(see here) and youth unemployment has risen to more than 50%.

Although a ourishing black economy in Spain ensures that not

all

these people are without work, the relentless rise in

unemployment is crippling the domestic economy.

This is a combustible and impatient demographic BBL

http://www.zerohedge.com/news/money-money-everywherehttp://finance.fortune.cnn.com/2012/02/09/warren-buffett-berkshire-shareholder-letter/?section=money_topstories&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+rss%2Fmoney_topstories+(Top+Stories)http://www.youtube.com/watch_popup?v=xOAgT8L_BqQ&feature=player_embeddedhttp://www.theatlantic.com/health/archive/2012/02/study-of-the-day-gene-therapy-can-restore-vision-1-eye-at-a-time/252655/http://www.stateline.org/live/details/story?contentId=630771http://www.stateline.org/live/details/story?contentId=630771http://www.theatlantic.com/health/archive/2012/02/study-of-the-day-gene-therapy-can-restore-vision-1-eye-at-a-time/252655/http://www.youtube.com/watch_popup?v=xOAgT8L_BqQ&feature=player_embeddedhttp://finance.fortune.cnn.com/2012/02/09/warren-buffett-berkshire-shareholder-letter/?section=money_topstories&utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+rss%2Fmoney_topstories+(Top+Stories)http://www.zerohedge.com/news/money-money-everywhere

-

7/28/2019 Weekly Strategic Plan 02132012

9/9

THIS COMMUNICATION IS INTENDED ONLY FOR THE USE OF INFINIUM

CAPITAL MANAGEMENT, LCC AND ITS EMPLOYEES TO WHICH IT IS ADDRESSED

AND CONTAINS OR MAY CONTAIN INFORMATION THAT IS PRIVILEGED,

CONFIDENTIAL OR EXEMPT FROM DISCLOSURE UNDER APPLICABLE LAW. If the

reader of this communicati on is not the intended recemployee or

agent responsible for delivering to the intended recipient), you

are hereby notied that any dissemination, distribution, or copying

of this communication is strictly prohibited. If you have received

this communication in error, please immediately inform Innium

Capital Management, LLC and then disregard and delete this

communication. Do nretain any copy of this communication.

The chart below resembles similar charts in the US when the Fed

rst began various rounds of liquidity injection into the US

banking

system. The result is likely to be similar. Very of little of

the liquidity gets into the economy but is absorbed into the

banking system

which is too busy trying to bail out old investments to bother

making new ones. Classic pushing on a string, so far, though this

does not

cover the period after the LTRO was initiated. This M3 series

needs to turn up.

I remain generally positive on US and Emerging market equity

markets as the staggering sums of central bank credit

expansion will leak into equity prices as the markets re state

the relative value of real assets to the declining value of

newly

printed at paper. Lean heavily to strong franchise, safe balance

sheets, and a history of reliable management. Diversify

across countries since none of them can be trusted.

Bruce Lawrence