Embed Size (px)

Citation preview

WANENO CHARLES OMONDI

B50/72456/08

15th Dec 20091

BBE 515: CONSTRUCTION INSURANCE

What is Insurance?

15th Dec 20092

Insurance is a risk transfer mechanism, whereby the individual or the business enterprise can shift some of the uncertainty of life on the shoulders of others; in return for a known premium, usually a small amount compared with the potential loss. The cost of the loss can be transferred to the insurer (Dickson, 1984).

History of Insurance

15th Dec 20093

King Hammurabi's CodeThe main concept of insurance - that of

spreading risk; has been around as long as human existence. Whether it was hunting the giant elk in a group to spread the risk of being the one gored to death or shipping cargo in several different caravans to avoid losing the whole shipment to a marauding tribe, people have always been wary of risk.

15th Dec 20094

The first written insurance policy appeared in ancient times on a Babylonian obelisk monument with the code of King Hammurabi carved into it. The "Hammurabi Code" was one of the first forms of written laws. These ancient laws were extreme in most respects, but it offered basic insurance in that a debtor didn't have to pay back his loans if some personal catastrophe made it impossible (disability, death, flooding, etc.).

Guild Coverage

15th Dec 20095

In the middle ages, most craftsmen were trained through the guild system. Apprentices spent their childhood working for masters for little or no pay. Once they became masters themselves, they paid dues to the guild and trained their own apprentices. The wealthier guilds had large coffers that acted as a type of insurance fund. If a master's practice burned down, a common occurrence in the wooden hovels of medieval Europe, the guild would rebuild it using money from its coffers. If a master were robbed, the guild would cover his obligations until money started to flow in again.

Dangerous Waters

15th Dec 20096

The earliest authenticated insurance contract (i.e. That which displays the characteristics of insurance in the sense of a transfer of risk of loss due to a fortuitous uncertain event in lieu of payment of consideration/ premium), is a marine insurance contract on a ship “The Santa Clara” dated 1347 in Genoa. The policy is in the Italian language and appears in the form a maritime loan to avoid the canon (church) prohibition against usury. The earliest insurers were merchants underwriting risks for fellow merchants, on a part time basis.

15th Dec 20097

The practice of underwriting emerged in the same London coffeehouses that operated as the unofficial stock exchange for the British Empire. In the late 1600s, shipping was just beginning between the New World and the old as colonies were being established and exotic goods were ferried back. A coffeehouse owned by Edward Lloyd, later of Lloyd's of London, was the primary meeting place for merchants, ship owners and others seeking insurance.

A basic system for funding voyages to the new world was established. In the first stage, merchants and companies would seek funding from venture capitalists. The venture capitalists would help find people who wanted to be colonists, usually those from the more desperate areas of London, and would purchase provisions for the voyage. In exchange, the venture capitalists would be guaranteed some of the returns from the goods the colonists would produce or find in the Americas.

15th Dec 20098

After the voyage was secured by venture capitalists, the merchants and ship owners would go to Lloyd's and hand over a copy of the ship's cargo to be read to the investors and underwriters who gathered there. The people interested in taking on the risk for a set premium would sign at the bottom of the manifest beneath the figure indicating what share of the cargo they were taking responsibility for (hence, underwriting). In this way, a single voyage would have multiple underwriters, who would try to spread their risk as well by taking shares in several different voyages.

Fire and Plague

15th Dec 20099

In 1666, the Great Fire of London destroyed around 14,000 buildings. London was still recovering from the plague had that ravaged it a year earlier, and many survivors found themselves without homes. As a response to the chaos and outrage that followed the burning of London, groups of underwriters who had dealt exclusively in marine insurance formed insurance companies that offered fire insurance. Armed with Pascal's triangle, these companies quickly expanded their range of business.

The Slow Exodus to America

15th Dec 200910

Insurance companies thrived in Europe, especially after the industrial revolution. In America, the story was very different. Colonists' lives were fraught with dangers that no insurance company would touch. As a result of lack food, wars with indigenous people and disease, almost three out of every four colonists died in the first 40 years of settlement. It took more than 100 years for insurance to establish itself in America. When it finally did, it brought the maturity in both practice and policies that developed during that same period of time in Europe.

History of Insurance in Kenya

15th Dec 200911

Modern insurance practices were introduced in Africa by colonial powers which sought to extend their operation of their home companies into the newly acquired territories.

Between the First and Second World Wars, local proprietors started setting up insurance companies in Kenya. In Kenya, offices were opened by Pioneer General Insurance in 1930, Jubilee Insurance in 1937 and Pan African Insurance in 1948.

Development of Insurance

15th Dec 200912

Basic Insurance Principles

15th Dec 200913

1. Utmost good faith The general rule of ‘caveat emptor’ (let the buyer

beware), which applies to ordinary trade contracts, does not apply to insurance contracts (Saleemi, 1992). Insurance contracts are contracts of utmost good faith or contracts of uberrimae fidei.

Accordingly, it is the inherent duty of both parties to a contract of insurance to make full and fair disclosure of all material facts relating to the subject matter of the proposed insurance. A material fact for this purpose is a fact which would affect the judgment of a prudent insurer in considering whether he would enter into a contract at all or enter into it at one premium rate or another.

15th Dec 200914

Although the duty of utmost good faith applies also to the insurer, for example he must not urge the proposer to affect the insurance which he knows is not legal, but this duty rests highly on the insured because he knows or is expected to know more about the subject matter. The proposer should disclose all material facts truly and fully. There should not be any false statement or half truth or silence on a material fact.

Failure to disclose a material fact could result in a claim being declined. In return, the insurance company must present the policyholder with a policy document and let him know all of the relevant terms, conditions and warranties.

Indemnity

15th Dec 200915

All contracts of insurance are contracts of indemnity except those of life and personal accident insurances where no money payment can indemnify for loss of life or bodily injury (Ibid).

The object of indemnity is to place the insured after a loss in the same position as he occupied immediately before the event. Under no circumstances is the insured allowed to benefit more than the loss suffered by him.

Insurable interest

15th Dec 200916

Insurable interest means some proprietary or pecuniary interest. The object of the insurance is to protect the pecuniary interest of the insured in the subject matter of the insurance and not the material property as such (Saleemi, 1992).

A person is said to have an insurable interest in the subject matter insured where he will derive pecuniary benefit from its existence or will suffer pecuniary loss from its destruction.

Insurable interest (cont’d)

15th Dec 200917

Insurable interest is thus a financial interest in the preservation of the subject matter. A purely sentimental or non-monetary benefit will not cause an insurable interest. In construction projects, the contractor, client as well as the consultants are some of the people who have an insurable interest in the project.

Causa proxima

15th Dec 200918

Under this principle, the insurer is only liable for the losses which have been proximately caused by the peril insured against. In order to make the insurer liable for a loss, the nearest or immediate or last cause is to be looked into, and if it is the peril insured against, the insured can recover.

Insurers are not liable for remote causes and remote consequences even if they belong to the category of insured perils.

Doctrine of Subrogation

15th Dec 200919

Given that insurance is a contract of indemnity, it would be unjust for a policy holder to receive compensation from his insurers for a loss and also compensation in terms of damages so awarded in a court if the fault was deemed to be the fault of a third party. The policy holder can make a claim either against the insurer or the wrongdoer.

According to the doctrine of subrogation, the insurer, after indemnifying the insured of his loss in full, steps into the shoes of the insured and is subrogated to all the alternative rights and remedies which the insured has against the third person, until he (the insurer) recoups the amount he has paid under the policy.

Points worth noting:

15th Dec 200920

The insured should provide all such facilities to the insurer which may be required by the insurer for enforcing his rights against third parties. Any action taken by the insurer is generally in the name of the insured, but the cost is to be borne by the insurer.

The insurer gets only such rights which are available to the insured. He gets no superior rights than the insured. As such, the insurer can recover under this doctrine, only which which the insured could himself have recovered.

This doctrine will not apply until the insured has recovered a full indemnity in respect of his loss from the insurer.

Doctrine of Contribution

15th Dec 200921

The doctrine of contribution states that ‘in case of double insurance, all insurers must share the burden of payment in proportion to the amount insured by each. If an insurer pays more than his rateable proportion to the loss, he has a right to recover the excess from his co-insurers, who have paid less than their rateable proportion.

15th Dec 200922

Essential requirement conditions for the application of the Doctrine of Contribution:

There must be double insurance i.e. there must be more than one policy from different insurers covering the same interest, the same subject matter and the same peril which has caused the loss.

There must be either over-insurance or only partial loss. If the amount of different policies is just equal to the value of the subject matter destroyed, the different insurers are liable to contribute towards the loss up to the full amount of their respective policies.

CATEGORIES OF INSURANCE

15th Dec 200923

Insurance policies in the construction industry fall into two categories:

Liability insurance policy: providing financial cover for legal liabilities owed to others.

Loss insurance policy: Providing cover for losses which fall directly on the insured parties.

Insurance provisions in Construction contracts

15th Dec 200924

Insurance provisions in construction contracts allocate risks of various kinds of loss or damage, which may arise in the course of the building work between the client and the contractor.

IndemnificationClause 13 of the Agreement and Conditions of

Contract for Building Works (JBC, 1999); places obligations upon contractors to indemnify Employers against the consequences of injury to persons and property.

Indemnification (cont’d)

15th Dec 200925

The contractor is to procure insurance before commencement of the works in the joint names of the Employer and the Contractor against loss and damage by fire, earthquake, lightning etc.

A contractor’s liability does not however extend to death or injury arising as a result of an act of neglect on the part of the Employer or persons for whom an Employer is responsible.

This insurance is to cover all the works executed. All unfixed materials and goods delivered to site but excluding temporary goods and equipment owned by the Contractor.

15th Dec 200926

It should be noted that all risks insurance must be maintained up to the date of issue of the practical completion certificate or the date of determination of the employment of the contractor, whichever is earlier.

15th Dec 200927

Damage to contract works in new buildingsIf there were no specific contractual provisions on

the matter, and assuming that there had been no negligence by either the employer or the contractor, the risk of damage to the contract works would lie on the contractor (Dickson, 1984).

Damage to contract works in existing buildingsIn this case, the Employer is required to arrange a

joint names policy in respect of the existing structure and its contents. The insurance must provide cover for the full cost of reinstatement, repair and replacement of loss or damage caused by the Specified Perils. This cover must be maintained until either the date of practical completion or determination of the contractor.

It is important to note that the employer is only required to insure against the ‘Specified Perils’, rather than against ‘All Risks’.

Other points to Consider:The Architect is contractually empowered

to suspend works if they are not insured.

15th Dec 200928

Classes of Insurance

Contractors’ All Risk Insurance Policies Contractor's All Risk Insurance offers comprehensive

and adequate protection against loss or damage in respect of contract works, construction plant and equipment and/ or construction machinery, as well as third party claims in respect of property damage or bodily injury arising in connection with the execution of a civil engineering project. This policy is extremely useful for consulting engineers, architects and financiers because it contributes to reducing the overall construction expenses and at the same time offers efficient financial protection for all parties concerned.

15th Dec 200929

Covered Risks:Contractor's All Risk provides 'all risk' cover

unless the hazard is specifically excluded. It covers the risk of fire, lightning, explosion, flood, inundation, rain, snow, earthquake, theft, burglary, bad workmanship, lack of skill, negligence, and human error.

Major Exclusions:This policy is subject to only a few

exclusions. Loss or damage to nuclear reaction, consequential loss, loss or damage due to faulty design, loss or damage due to war or war-like operation etc

15th Dec 200930

The Property insured

In commercial policies, the insured will require cover for buildings, machinery and plant, and stock. These are the three man headings under which property is insured and in some cases a list of such items can run to many pages, depending upon the size of the insured company.

New buildings under construction are usually covered by Contractors’ All Risks policy.

15th Dec 200931

Employers’ liability insurance

When an employer is held legally liable to pay damages to an injured employee or the representatives of someone fatally injured, he can claim against his employers’ liability policy which will provide him with exactly the same amount he himself has had to pay out.

In addition, the policy will also pay certain expenses by way of lawyer’s fees or doctor’s charges where an injured man has been medically examined. The intention is to ensure the does not suffer financially but is compensated for any money he may have to pay in respect of a claim. The policy is restricted to damages payable in respect of injury and does not apply where property of an employee is damaged.

15th Dec 200932

Motor insuranceThe minimum requirement by law is to provide

insurance in respect of legal liability to pay damages arising out of injury caused to any person (Ibid). A policy for this risk only is available and is termed as an ‘Act only’ policy. These policies are not common and are usually reserved for where the risk is exceptionally high.

A ‘third party only’ policy would satisfy the minimum legal requirements and in addition, would include cover for legal liability where damage was caused to some other person’s property. An addition to the form of cover is where damage to the car itself from fire or theft is included, a ‘third party, and fire and theft policy’.

15th Dec 200933

Salient features of an insurance contractThe insurance company will ask for information

relating to the risk and then will offer the person a quotation. If the quotation is accepted, then a contract will exist. The quotation should include amongst other things the following information:-

The premium that is payable The amount of taxation Any additional fees payable How long the quotation is valid for The name of the insurance company Key facts document outlining all the salient

information pertaining to the insurance

15th Dec 200934

BONDS AND GUARANTEES

A bond or guarantee is an arrangement under which the performance of a contractual duty owed by one person (A) to another (B) is backed up by a third party (C). What happens is that C promises to pay B a sum of money if A fails to fulfill the relevant duty.

In this context, A is commonly known as the principal debtor or the principal; B is called the beneficiary; and C is called the bondsman, surety or guarantor.

15th Dec 200935

Parent company guarantees

This is where the contractual performance of one company within a corporate group is underwritten by other members of the group. The importance of such guarantees derives from a combination of two factors:

Many companies operating within the construction industry are seriously undercapitalized (despite forming part of a financially stable corporate group).

English company law does not treat a parent company as responsible for the debts of its subsidiaries, unless such responsibility is expressly taken on.

15th Dec 200936

Bonds

These are normally provided (at a price) by a financial institution such as a bank or insurance company.

The principal will pay a premium (usually annually) in exchange for the bonding company's financial strength to extend surety credit. In the event of a claim, the surety will investigate it. If it turns out to be a valid claim, the surety will pay it and then turn to the principal for reimbursement of the amount paid on the claim and any legal fees incurred.

15th Dec 200937

Nature of Bonds

Payment: Examples include: the employer’s duty to

pay the contractor or the contractor’s duty to pay a subcontractor. A contractor may also provide a bond in favour of the employer, in return for an early release of retention money or, indeed, completely replacing the retention provisions. If defects are then found in the building, the employer can call on the bond, rather than the retention money to finance the necessary remedial work.

15th Dec 200938

Nature of Bonds (cont’d)In some contracts, there is an optional

requirement for advance payment bond, and another for payment for off-site materials or goods. These provide the employer with some recourse in the event that the contractor fails to fulfill obligations that have been paid for. In both cases, the bonds are ‘demand bonds’.

Specific obligations:This includes promises by contractors or

subcontractors not to withdraw a tender. This is of importance where the main contractor tenders on the basis of bids received from domestic subcontractors

15th Dec 200939

Nature of bonds (cont’d)If the subcontractor withdraws from a job

awarded to the main contractor, then the main contractor may pay a significantly higher price to another subcontractor for that part of the works.

These types of bonds are called bid bonds. They are aimed at preventing contractors from withdrawing their tenders until the contract is awarded.

15th Dec 200940

Nature of bonds (cont’d)Performance of the contract in

general:This is usually to guarantee the

performance of parties to a contract. The performance bond is usually taken out by the contractors and is usually equivalent to 10% of the contract sum.

The Agreement and Conditions of Contract for Building Works (JBC, 1999) also has a provision for an employer’s performance bond.

15th Dec 200941

It should be noted that the underlying purpose of a bond is to give financial protection where the principal debtor, whether it be the employer or the contractor, becomes insolvent.

15th Dec 200942

Professional indemnity insurance

The various professional members of a design and construction team, such as architects, specialist engineers and quantity surveyors, will each have their own insurance policy to indemnify them against liability for professional negligence.

Points worth noting:A contractor, at least one who does not specialize in

‘design and build’ work, may well not have insurance cover of this kind. As a result, the client may have less insurance protection in respect of a contractor’s design input than under a conventional set-up in which design is carried out by professional consultant.

15th Dec 200943

The cover provided by most professional indemnity insurance policies is subject to financial limits and, once those limits are exceeded, the professional’s own money is at stake and, of course, once that money is exhausted, the loss inevitably falls to the client.

Professional consultants are normally required by their institutions to take out and maintain a specified level of indemnity insurance. However, failure to do so would be a breach of the professional’s code of conduct; it would not usually be a breach of contract with the client (Murdoch & Hughes, 1992).

Notable exceptions are the standard RICS terms.

15th Dec 200944

It is worth noting that most professional indemnity policies are written on a ‘claims made’ basis. This means that they cover claims actually made against the professional person during the period of insurance, regardless of when the negligent act took place. As a result, it is essential that insurance cover is maintained, even after the retirement or death of the professional concerned, and this can usually be arranged on a single-premium ‘run off’ basis.

15th Dec 200945

INSURABLE RISKS

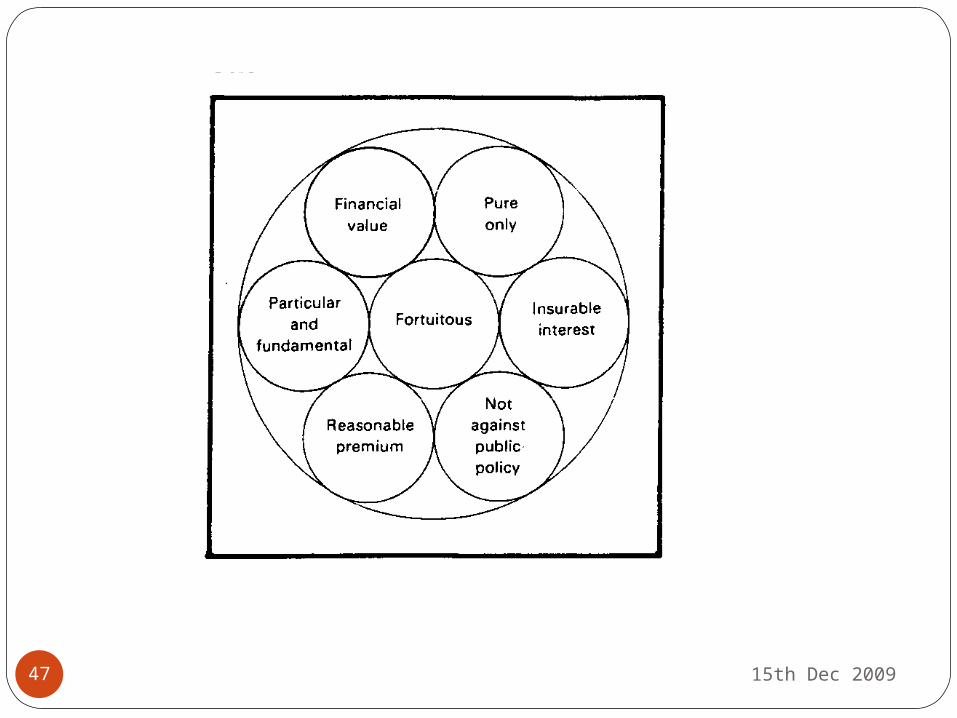

Rather than create a list of the kinds of events which can or cannot be insured, if such a list could ever be compiled, it is better to explore the characteristics of insurable risk. The common features of insurable risks are:

Financial valueThe risk must involve a loss that is of pecuniary/

financial measurement e.g. damage to property where the level of compensation can be equated to the cost of repairs. If one is injured in, say a motor accident, the court will decide how much the injured person should receive compensation.

15th Dec 200946

15th Dec 200947

Homogenous exposures There must be a large number of similar,

homogenous, risks before any one of that number is capable of being insured.

Reasons: The measurement of risk by probabilities

and statistics relies on there being reasonable experience and past events. Statistics have been compiled by insurance companies on most common risks such as fire, motor accidents etc. The minor exception to his criterion is subjective probabilities and insurance of certain unique and unusual occurrences.

15th Dec 200948

If there were only three or four exposures, then each one would have to contribute a very high amount if losses were to be met from these contributions. On the other hand, if there were thousands of similar exposures, then contributions could be comparatively small as only few would be unfortunate enough to suffer a loss and hence require it to be met from contributions. The insurance of household contents against fire is an example of homogenous exposures, whereas the insuring of a concert pianist’s fingers is not.

15th Dec 200949

Pure risks onlyInsurance is concerned with pure risks only;

speculative risks, where there is the possibility of some gain, cannot be insured. It is important to note that not all pure risks are insurable but speculative risks, on the whole, are not.

Particular and fundamental risksParticular risks are generally insurable

provided that they satisfy the other criteria for insurance. Fundamental risks do not however present such a straight forward approach. Insurers are very careful in selecting the fundamental risks which they wish to provide cover for.

15th Dec 200950

FortuitousThe loss must be entirely fortuitous as far

as the person seeking insurance is concerned. It is not possible to insure against an event that will occur with certainty as in such a case, there would be no risk, no uncertainty of loss. The frequency and severity of any risk must be completely beyond the control of the person insuring.

Insurable interestThe person insuring must stand to suffer

some financial loss if the risk materializes.

15th Dec 200951

Against public policyIt is a common principle in law that contracts must

not be contrary to what the society considers the right and moral thing to do. This also applies to insurance contracts. It is not possible to provide the insurance to pay the fine of some driver who is found guilty of some offence (Steele, 1984)

Reasonable premiumThe premium paid for the insurable risk must be

seen to be reasonable in relation to the likely financial loss. If the likelihood of an insured event is so high, or the cost of the event so large, that the resulting premium is large relative to the amount of protection offered, it is not likely that anyone will buy insurance, even if on offer.

15th Dec 200952

The effect of multiplicity of insurance requirements on the construction industryDouble InsuranceDouble insurance occurs when the same risk and

the same subject-matter is insured with more than one insurer. If two different policies are taken from one and the same insurer, it is not a case of double insurance and will be termed full insurance.

In the event of loss under double insurance, the insured may claim from the insurers in such order as he thinks fit, but he cannot recover more than the full amount of the actual loss, subject to the insured sum, as a contract of insurance is a contract of indemnity.

15th Dec 200953

When the amount, for which the property has been insured, is more than the real value of the property, it is called ‘over insurance’.

This double insurance causes construction participants to pay unnecessarily higher premiums than required.

15th Dec 200954

Importance of Insurance in the Construction industry

Risk transfer mechanism: an individual or a business enterprise can shift some of the uncertainties and risks to others through payment of premium.

Contractual requirement: Most of the standard contracts have an insurance clause requirement. They include: FIDIC, The Government of Kenya’s Standard Tender Document for Procurement of Works and the Agreement and Conditions of Contract for Building Works (JBC, 1999).

Stimulus to business enterprises:

15th Dec 200955

Security: insurance increases a firm’s confidence and enables it to concentrate on production and trading risks without the worry that their objectives may not be achieved through insurable risks.

Research and liaison: Insurers actively contribute to research in the prevention of loss and liaise with various public and private bodies in this connection.

15th Dec 200956

Problems / Controversies of InsuranceInsurance insulates too muchBy creating a "security blanket" for its insured, an

insurance company may inadvertently find that its insured may not be as risk-averse as they might otherwise be (since, by definition, the insured has transferred the risk to the insurer,) a concept known as moral hazard. To reduce their own financial exposure, insurance companies have contractual clauses that mitigate their obligation to provide coverage if the insured engages in behavior that grossly magnifies their risk of loss or liability.

For example, life insurance companies may require higher premiums or deny coverage altogether to people who work in hazardous occupations or engage in dangerous sports.

15th Dec 200957

Complexity of insurance policy contractsInsurance policies can be complex and some

policy holders may not understand all the fees and coverage included in a policy. As a result, people may buy policies on unfavorable terms. In response to these issues, many countries have enacted detailed statutory and regulatory regimes governing every aspect of the insurance business, including minimum standards for policies and the ways in which they may be advertised and sold.

For example, most insurance policies in the English language today have been carefully drafted in plain English; the industry learned the hard way that many courts will not enforce policies against insured when the judges themselves cannot understand what the policies are saying.

15th Dec 200958

RedliningRedlining is the practice of denying insurance

coverage in specific geographic areas, supposedly because of a high likelihood of loss, while the alleged motivation is unlawful discrimination. Racial profiling or redlining has a long history in the property insurance industry in the United States. From a review of industry underwriting and marketing materials, court documents, and research by government agencies, industry and community groups, and academics, it is clear that race has long affected and continues to affect the policies and practices of the insurance industry (Squires, 2003).

15th Dec 200959

The insurance industry and rent seekingCertain insurance products and practices

have been described as rent seeking by critics. That is, some insurance products or practices are useful primarily because of legal benefits, such as reducing taxes, as opposed to providing protection against risks of adverse events. Under United States tax law, for example, most owners of variable annuities and variable life insurance can invest their premium payments in the stock market and defer or eliminate paying any taxes on their investments until withdrawals are made. Sometimes this tax deferral is the only reason people use these products.

15th Dec 200960

PROJECT MANAGERS, ARE YOU COVERED?

15th Dec 200961

15th Dec 200962

THE END