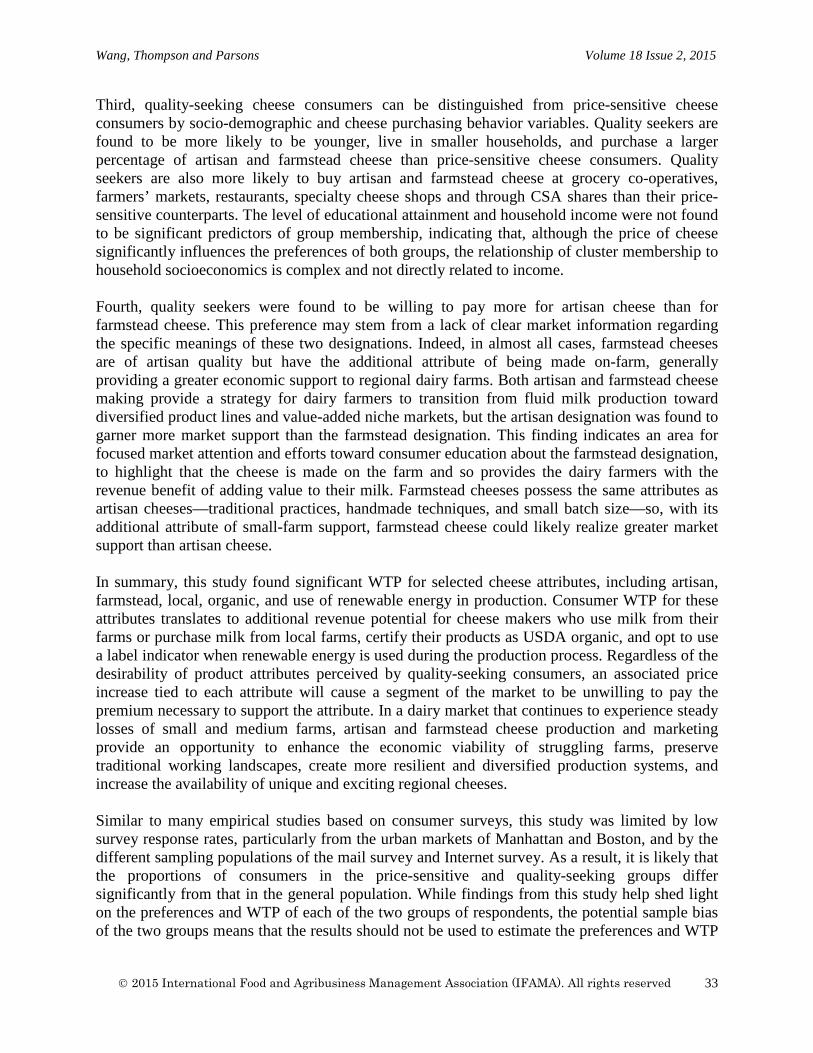

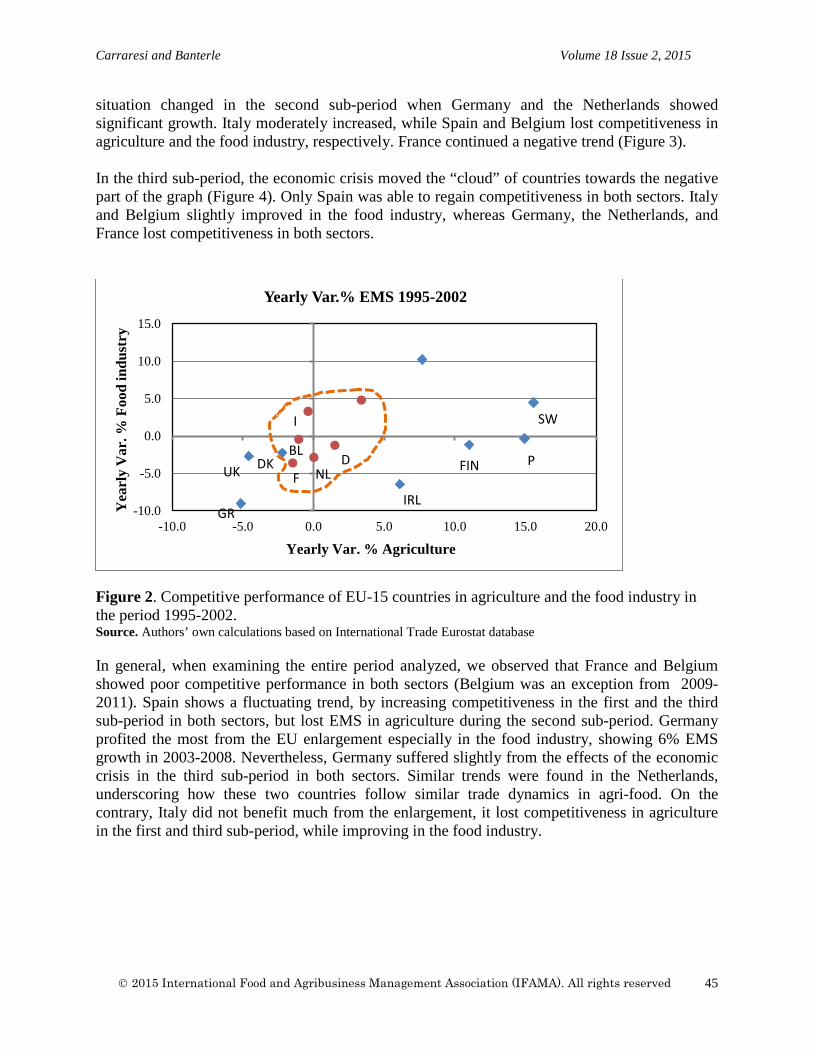

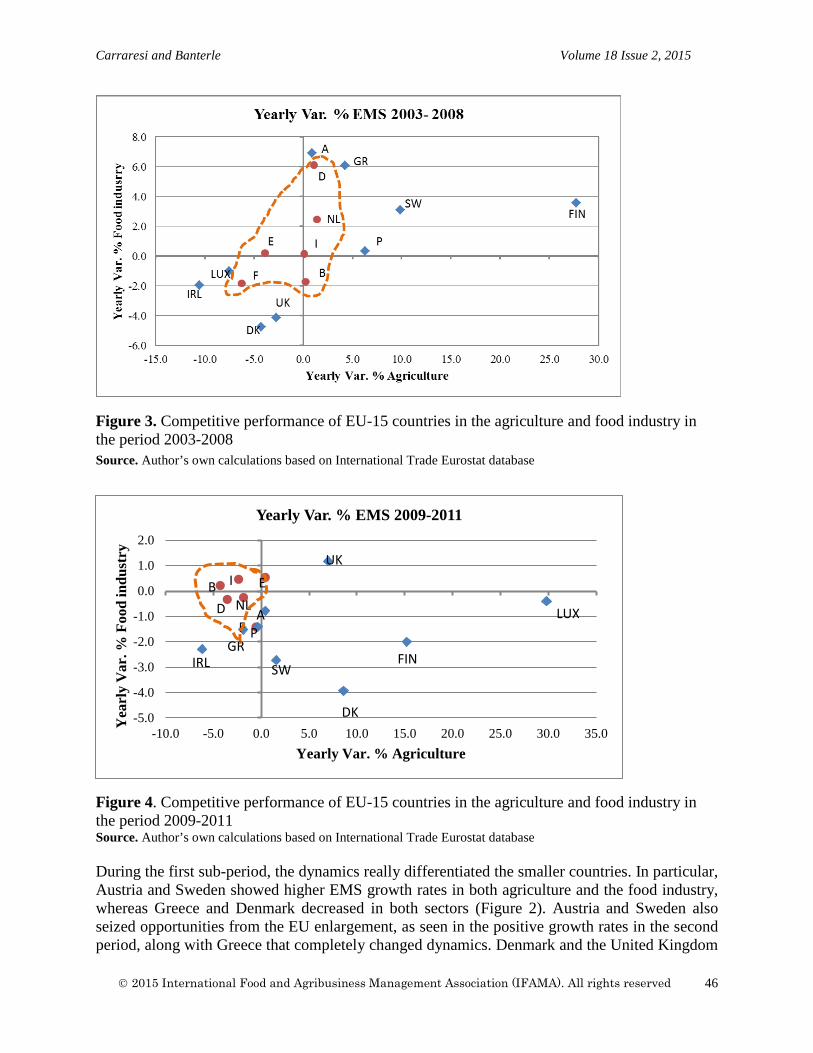

Embed Size (px)

DESCRIPTION

The International Food and Agribusiness Management Review is published quarterly by IFAMA. Learn more by visiting www.ifama.org

Citation preview

International Food and Agribusiness Management Review

Official Journal of the InternationalFood and Agribusiness Management Association

Volume 18 Issue 22015

International Food and Agribusiness Management Review

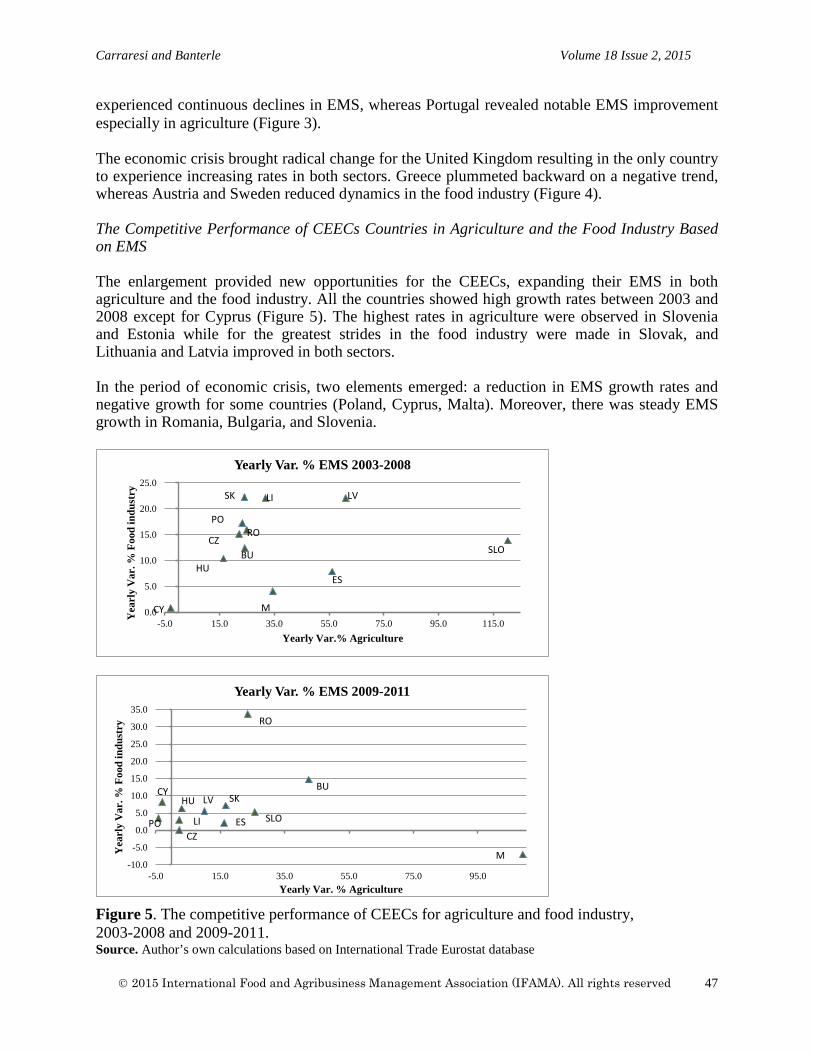

Editorial StaffExecutive Editor

Peter Goldsmith, University of Illinois, USA

Regional Managing EditorsAsia, Australia, and New Zealand

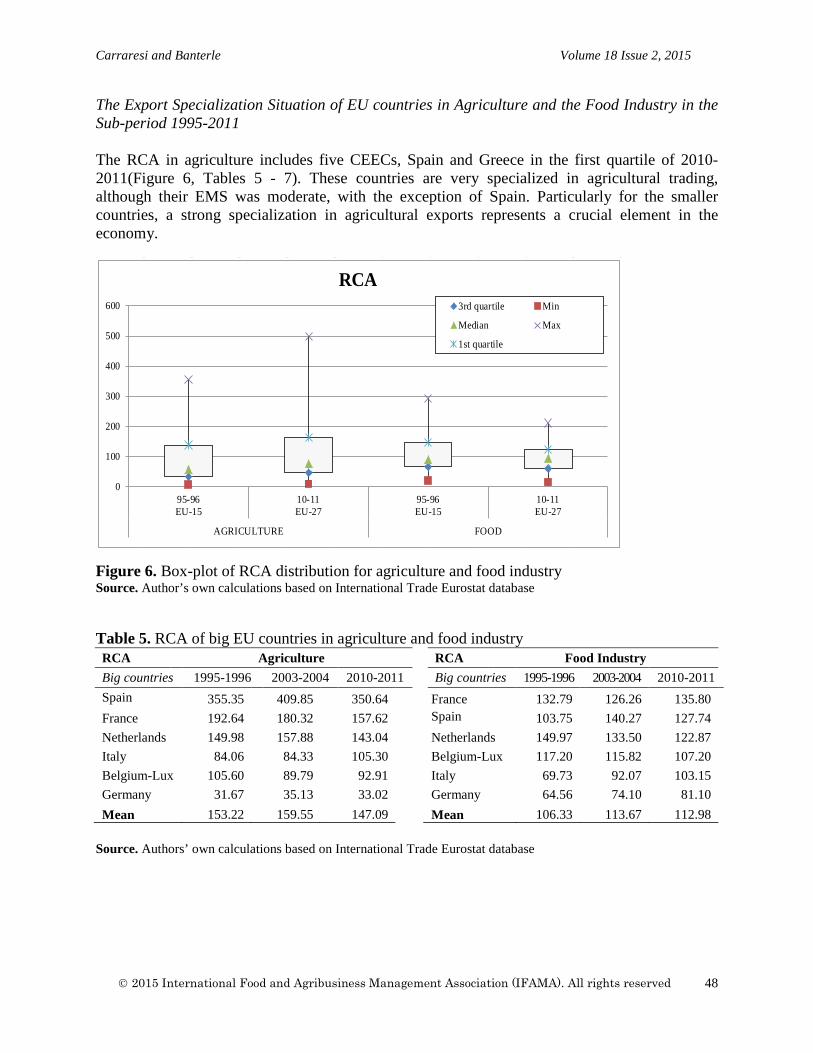

Murray McGregor, University of South Australia, AustraliaNicola M. Shadbolt, Massey University, New Zealand

EuropeJacques Trienekens, Wageningen University, The Netherlands

Vera Bitsch, Technical University of Munich, GermanyAlessio Cavicchi, University of Macerata, Italy

Diogo Souza Monteiro, University of Kent, United KingdomYuliya Bolotova, Clemson University, USA (Russia)

North AmericaRam Acharya, New Mexico State University, USA

Corinne Alexander, Purdue University, USAMichael Gunderson, Purdue University, USA

Vincent R. Amanor-Boadu, Kansas State University, USAMark Hansen, Brigham Young University, USADavid Van Fleet, Arizona State University, USA

David Sparling, The University of Western Ontario, CanadaR. Brent Ross, Michigan State University, USA

Cheryl Wachenheim, North Dakota State University, USA

South AmericaJoao Martines-Filho, Universidade de São Paulo, Brazil

AfricaAjuruchukwu Obi, University of Fort Hare, South Africa

Filippo Arfini, Universita’ di Parma, ItalyStefano Boccaletti, Universita’ Cattolica, ItalyMichael Boehlje, Purdue University, USAFabio Chaddad, University of Missouri, USADennis Conley, University of Nebraska - Lincoln, USAFrancis Declerck, ESSEC Business School, FranceHamish Gow, Massey University, New ZealandJukka Kola, University of Helsinki, FinlandJay Lillywhite, New Mexico State University, USA

Woody Maijers, INHOLLAND University, The NetherlandsMarcos Fava Neves, FEA / USP / PENSA, BrazilOnno Omta, Wageningen University, The NetherlandsHernán Palau, Buenos Aires University, ArgentinaChristopher Peterson, Michigan State University, USAThomas Reardon, Michigan State University, USAMary Shelman, Harvard Business School, USAJohan van Rooyen, University of Stellenbosch, South Africa

The IFAMR (ISSN #: 1559-2448) is published quarterly and is available at http://www.ifama.org. For copyright and publishing information, please contact: Kathryn White, Administrative Editor. IFAMA Business Office • 1010 Vermont Avenue, Suite 201, Washington, DC 20005 • USA • Tel: 1 (202) 429-1610 • Fax: 1 (202) 628.9044 • E-mail: [email protected] • Web: http://www.ifama.org

International Food and Agribusiness Management Review

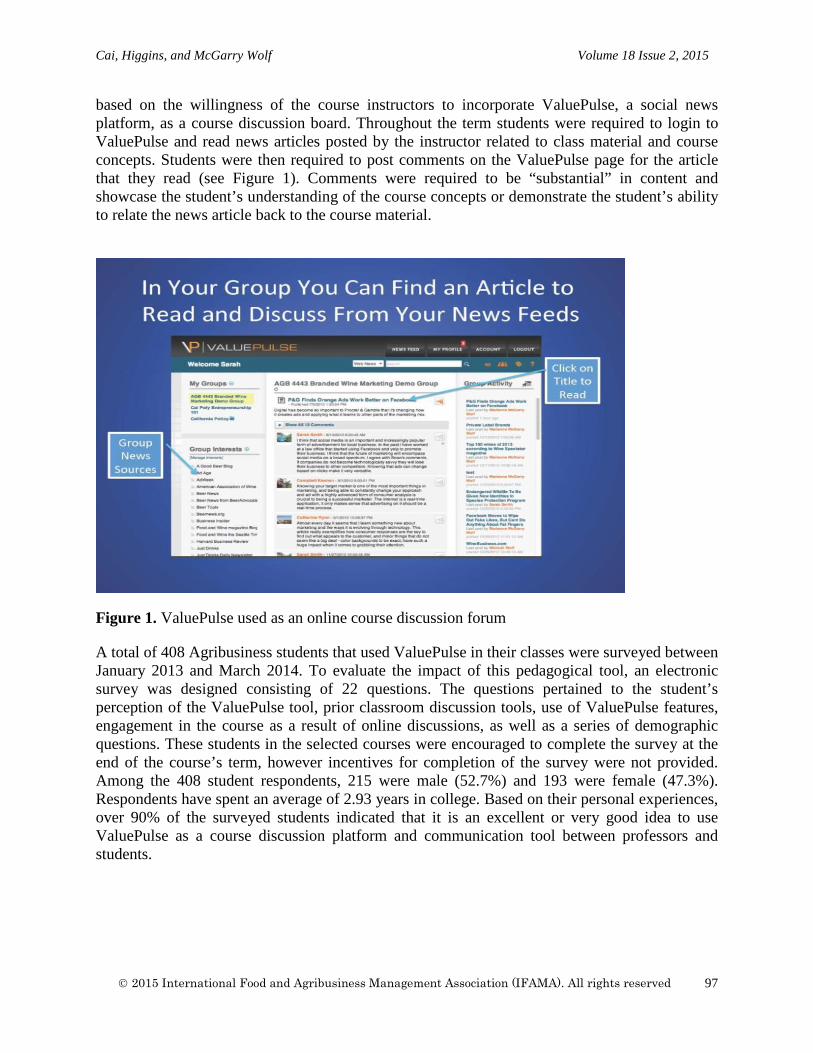

STUDY AGRICOMMERCE

AT MASSEY

WORLD LEADING IN AGRIFOOD

MASSEY.AC.NZ0800 MASSEY

The IFAMR Open Access Project is supported in part through contributions from these institutions. Scholars, practitioners, students, and policymakers may now read and download the most current and archival content from the IFAMR website. The Board of Directors of the International Food and Agribusiness Management Association feel that open and immediate access to IFAMR’s articles and case studies dramatically elevates the quality of scientific inquiry and instruction around the world in the field of agribusiness. If you would like to support this effort please contact: Kathryn White, Email: [email protected].

Food and Agribusiness Management

University of Fort HareTogether in Excellence

Strong Roots - Bright Future

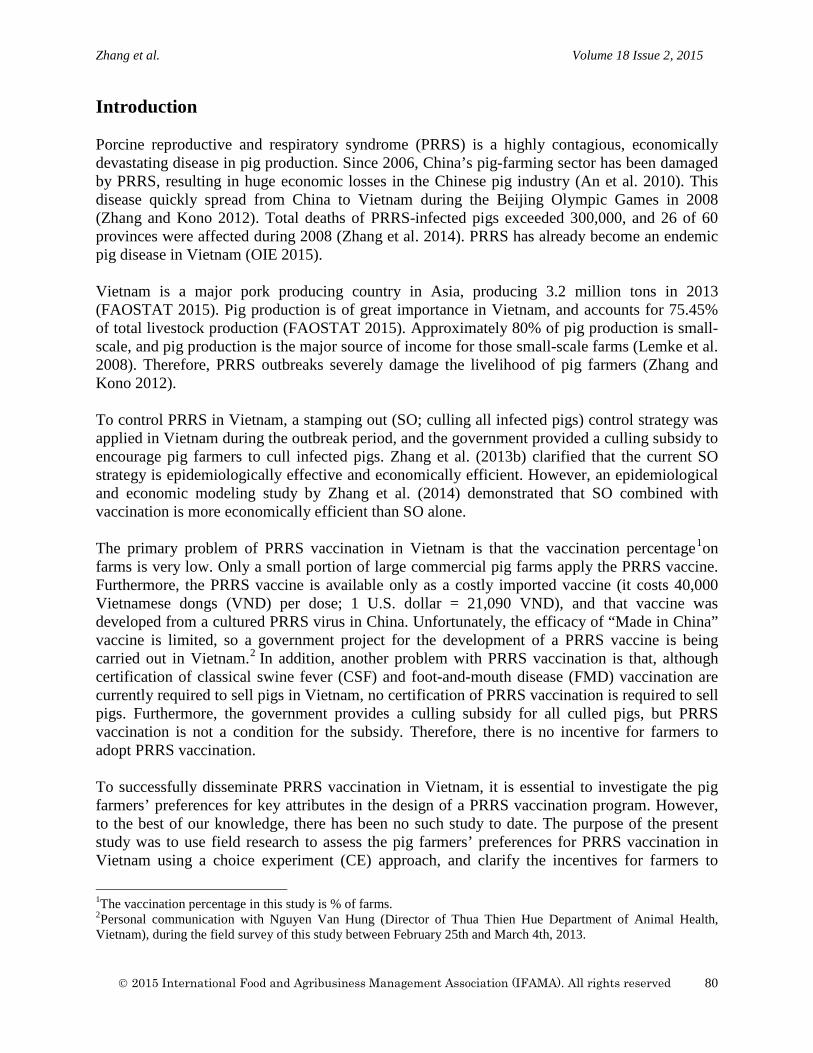

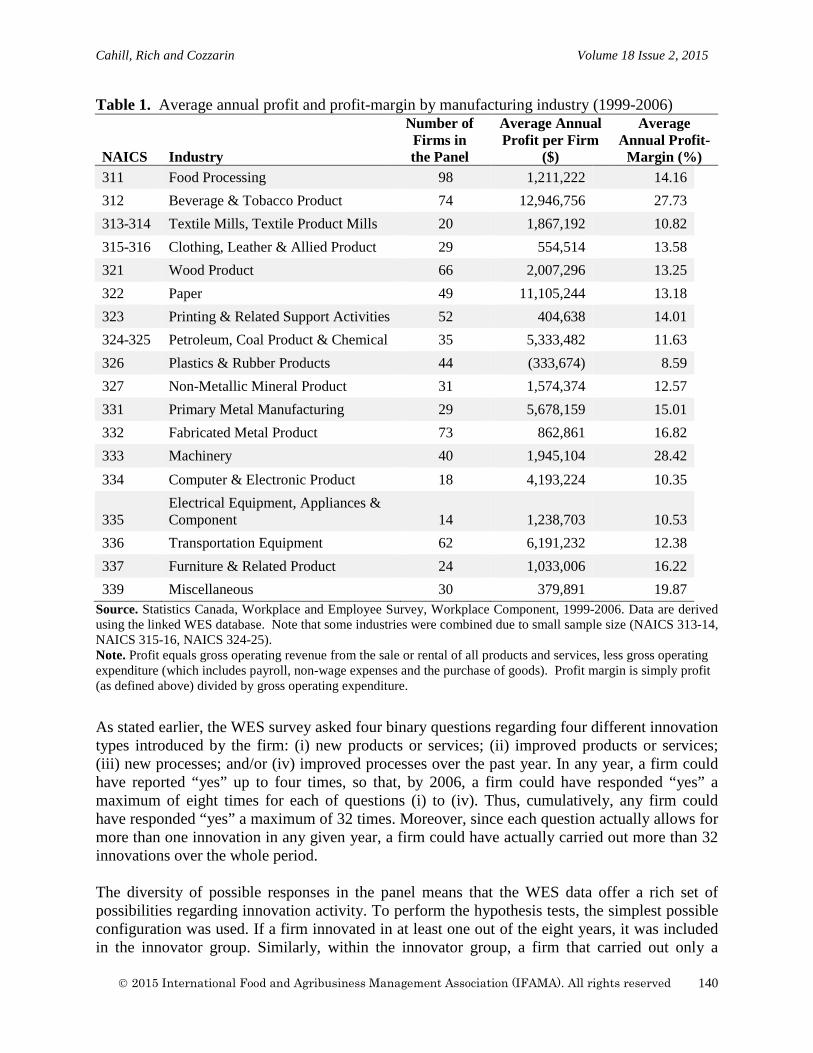

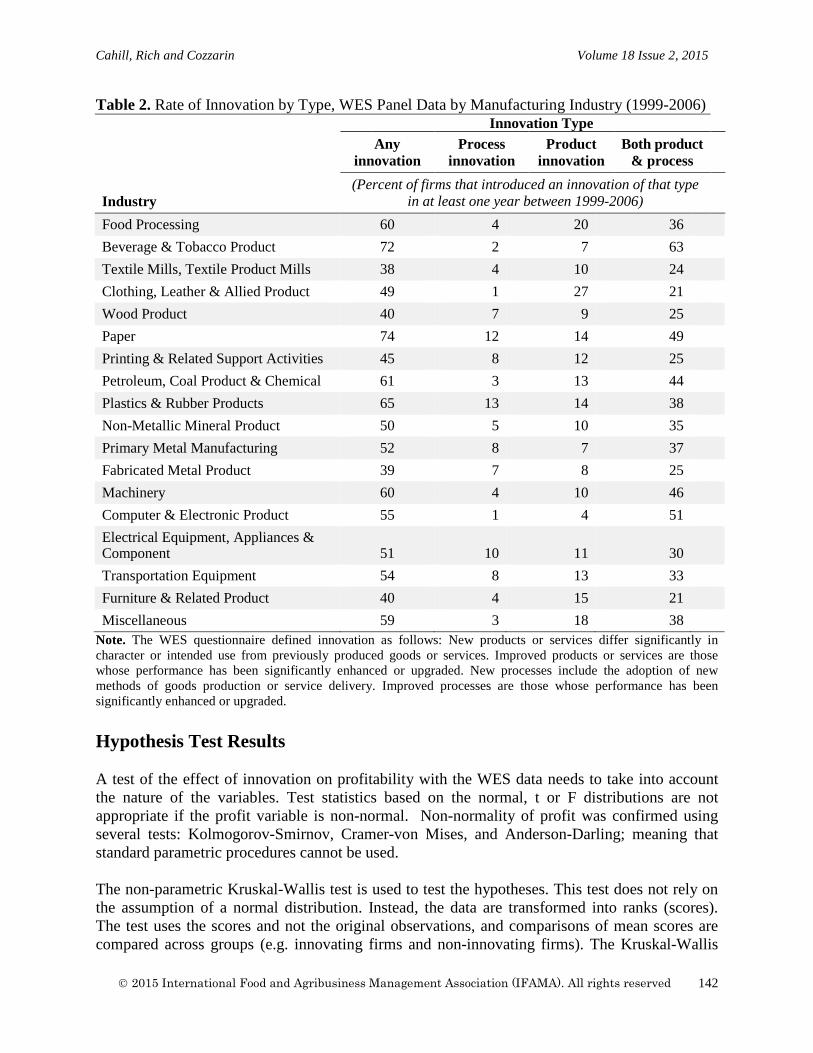

International Food and Agribusiness Management Review Volume 18 Issue 2, 2015

TABLE OF CONTENTS

Research

1. Grocery Shopping via T-Commerce in Korea: New Shopping Channel Adoption Behavior Based on Prior E-Commerce Experience Dongmin Lee, Haeyoung Jeong, Jongpyo Cho, Jaeseok Jeong, and Junghoon Moon .........................................................................................................

p. 1

2. Preferences for Farmstead, Artisan, and Other Cheese Attributes: Evidence from a Conjoint Study in the Northeast United States Qingbin Wang, Ethan Thompson, and Robert Parsons...............................................

p. 17

3. Agri-Food Competitive Performance in EU Countries: A Fifteen-Year Retrospective Laura Carraresi and Alessandro Banterle..........................

p. 37

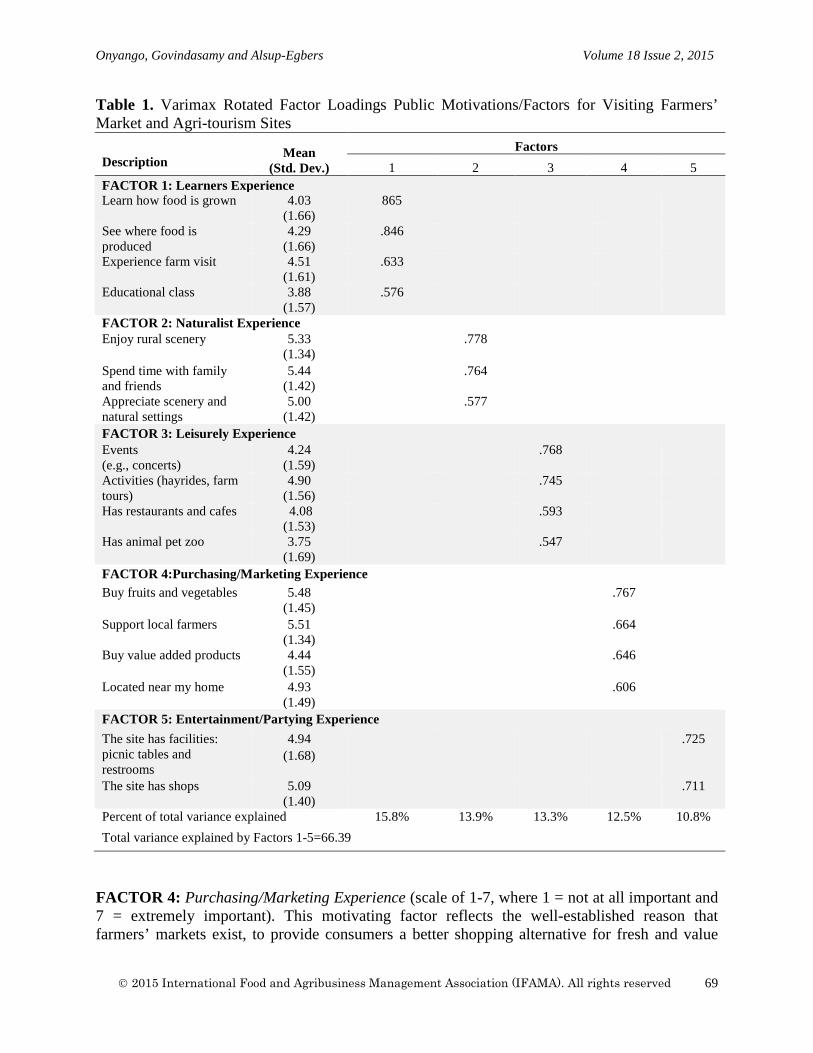

4. Uncovering Success Attributes for Direct Farmers’ Markets and Agri-Tourism in the Mid-Atlantic Region of the United States Benjamin Onyango, Ramu Govindasamy, and Clydette Michelle Alsup-Egbers........

p. 63

5. Farmers’ Willingness to Pay for a Porcine Reproductive and Respiratory Syndrome (PRRS) Vaccine in Thua Thien Hue Province, Vietnam Haifeng Zhang, Hiroichi Kono, Satoko Kubota and Jun Wang .....................................................................................................................

p. 79

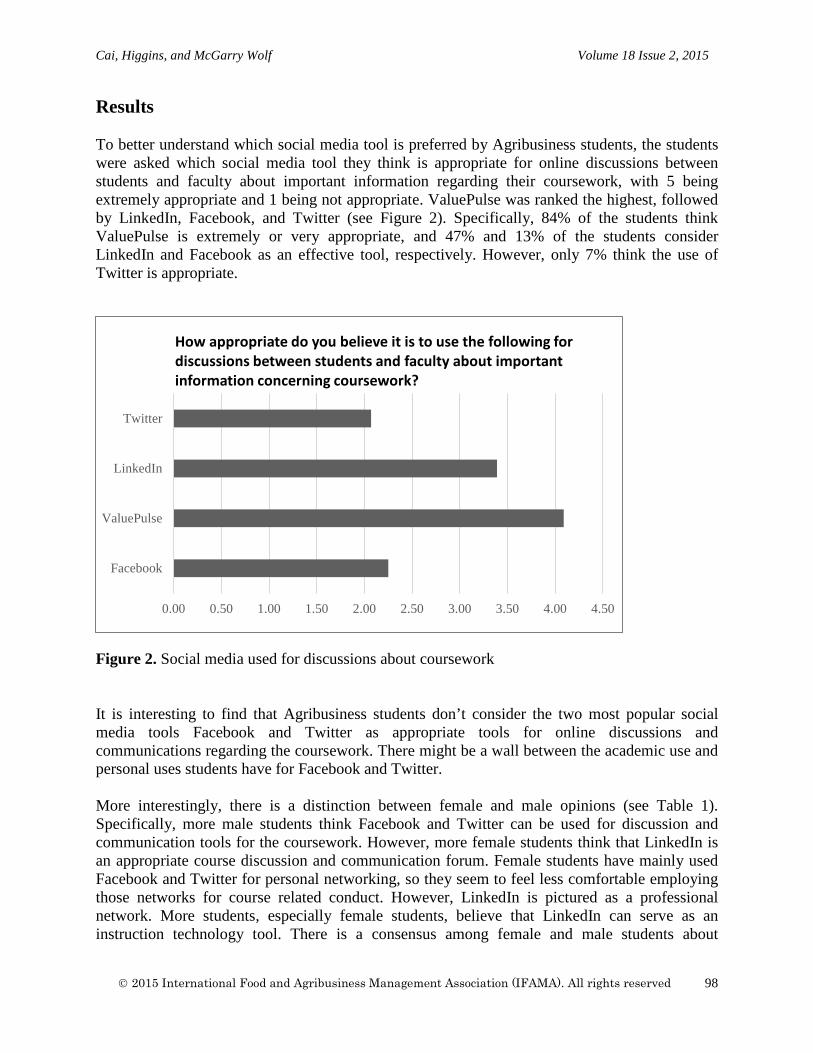

6. Millennials Leaning In: Can Women in Agribusiness Benefit from Technology and Social Collaboration in Higher Education? Xiaowei Cai, Lindsey Higgins, and Marianne McGarry Wolf.............

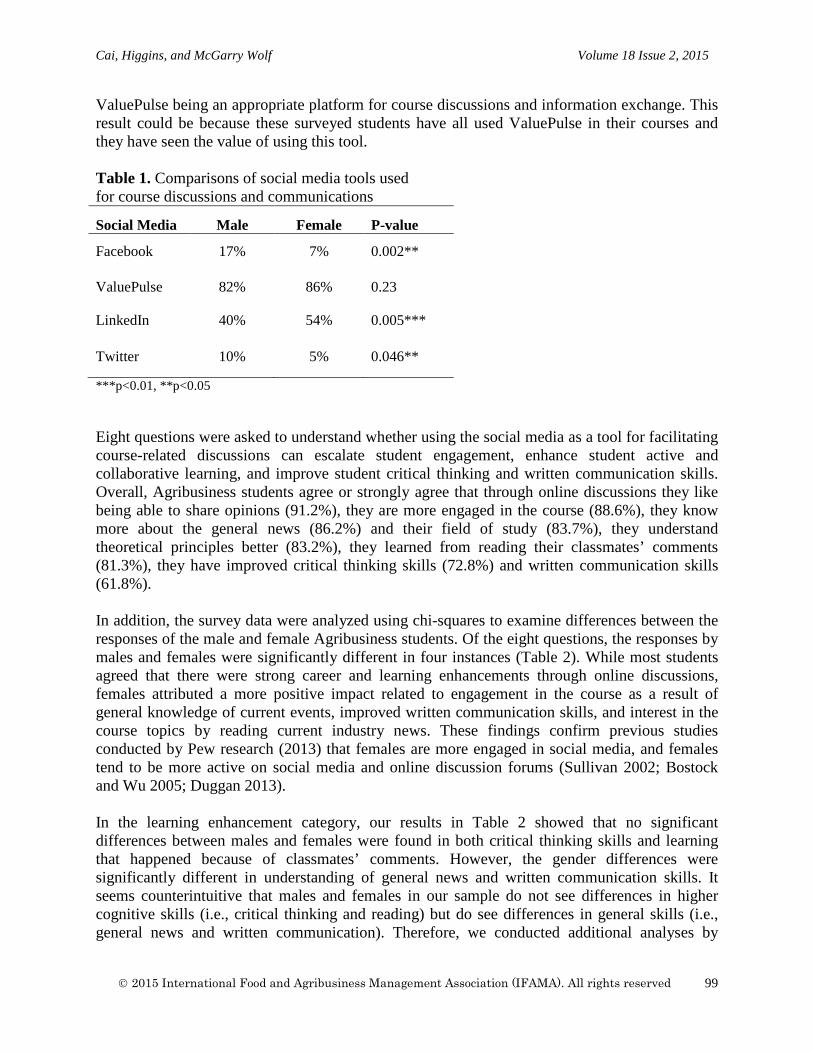

p. 93

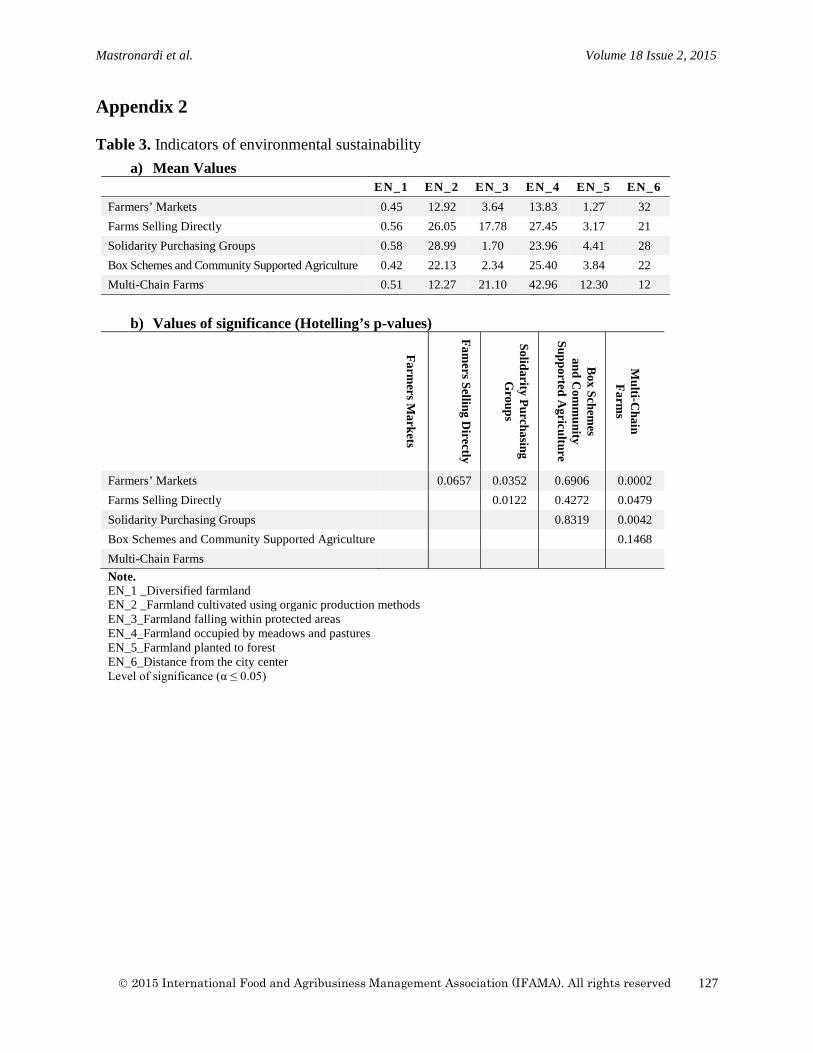

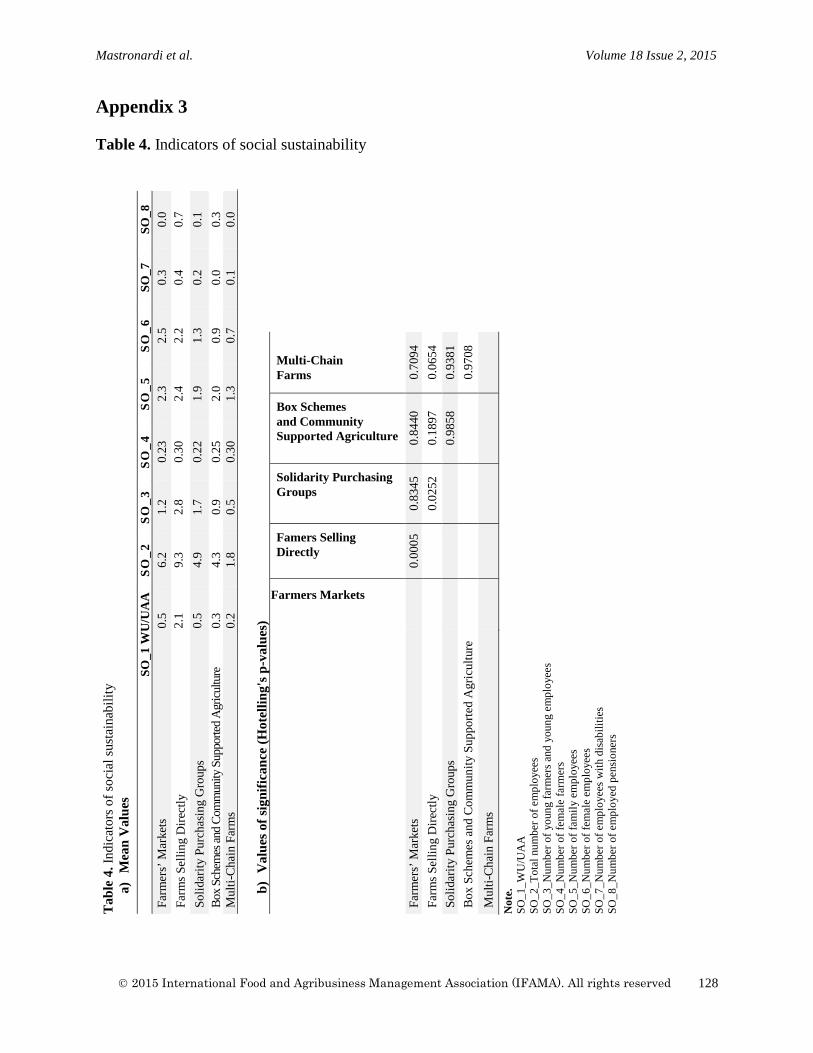

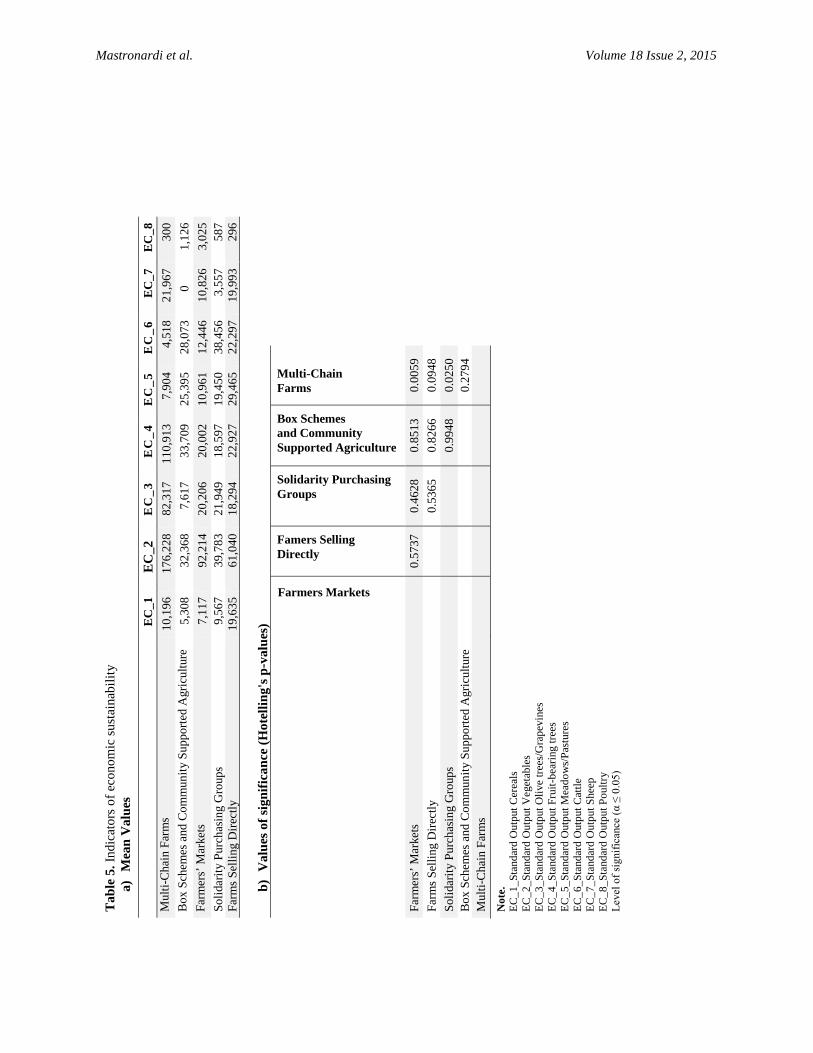

7. Exploring the Role of Farmers in Short Food Supply Chains: The Case of Italy Luigi Mastronardi, Davide Marino, Aurora Cavallo, and Agostino Giannelli.......................................................................................................

p. 109

8. Innovation in the Canadian Food Processing Industry: Evidence from the Workplace and Employee Survey Sean Cahill, Tabitha Rich, and Brian Cozzarin......................................................................................................

p. 131

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved. i

International Food and Agribusiness Management Review Volume 18 Issue 2, 2015

Case Study

9.

The Integrated Management of Food Processing Waste: The Use of the Full Cost Method for Planning and Pricing Mediterranean Citrus By-Products Daniele Vergamini, David Cuming, and Davide Viaggi.....

p. 153

10.

Syngenta: Changing a Global Company Elizabeth A Yeager, W. Scott Downey, and David A Widmar....................................................................................

p. 173

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved. ii

International Food and Agribusiness Management Review Volume 18 Issue 2, 2015

EDITOR’S NOTE Dear Colleagues, Enclosed is our second issue of the year. It is important to stop and thank the editorial team at the IFAMR for publishing its 26th straight quarterly issue on time. It is another full issue with ten articles, nine research manuscripts and one case study. Well done team. We continue to support scholars’ ambitions who seek to publish special issues on a topic of their choice. Forthcoming in June will be a special issue on the Global Poultry Industry, edited by staff at the USDA-ERS. We will issue calls at the annual meeting next month for two new special issues; one on big data and agribusiness edited by an industry-academic team put together by Conservis, LLC of Minneapolis; and a second special issue by a USDA-ERS team on the future of the global dairy complex. Look for the calls so you can get your work published. There are a number of very nice pieces in this issue. Let me draw your attention to a couple of highlights. First is a teaching case study on Syngenta that has students exploring the critical area of relationship marketing and customer intimacy. The work is poignant as firms explore news ways to connect with customers who increasingly have alternatives ways to increase profitability. We bring to the IFAMR readership two articles from Asian authors sharing perspectives on new high growth markets in the global food system. There are three articles from Italian authors. Thanks in no small part to our managing editor, Alessio Cavicchi at the University of Macerata, we have seen a dramatic increase in submissions from Italy. Finally, consistent with the IFAMA strategy supporting; students looking for jobs and firms seeking high quality talent, we published an interesting paper from the United States on gender balance among food and agribusiness applicants. Peter Goldsmith, Executive Editor, IFAMR

© 2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved. iii

International Food and Agribusiness Management Review Volume 18 Issue 1, 2015

© 2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved. iv

International Food and Agribusiness Management Review Volume 18 Issue 2, 2015

Grocery Shopping via T-Commerce in Korea:

New Shopping Channel Adoption Behavior Based on Prior E-Commerce Experience

Dongmin Leea, Haeyoung Jeongb, Jongpyo Choc, Jaeseok Jeong d, and Junghoon Moone

aResearcher , Food Business Lab., Program in Regional Information, Seoul National University 1, Gwanak-ro, Gwanak-gu, Seoul, 151-742, Republic of Korea

b Researcher, International Market Research Division, Gallup Korea

70, Sajik-ro, Chongro-gu, Seoul, 110-054, Republic of Korea

c Researcher, Food Business Lab., Program in Regional Information, Seoul National University 1, Gwanak-ro, Gwanak-gu, Seoul, 151-742, Republic of Korea

d Associate professor, Graduate School of Pan-Pacific International Studies, Kyung Hee University

1732, Deogyeong-daero, Giheung-gu, Yongin, 446-701, Republic of Korea

e Associate professor, Food Business Lab., Program in Regional Information, Seoul National University 1, Gwanak-ro, Gwanak-gu, Seoul, 151-742, Republic of Korea

Abstract The main goal of this study is to investigate the willingness to adopt t-commerce for grocery shopping in South Korea. This study endeavors to recognize existing differences among consumer behaviors based on e-commerce experience. The sample was divided into two groups: one group with online grocery shopping experience and one group without online grocery shopping experience. The groups were compared to identify differences in willingness to adopt t-commerce as a new shopping medium. The two groups showed different motivations for t-commerce-based grocery shopping based on their previous shopping experience. Keywords: t-commerce, online grocery shopping, Internet Protocol Television, compatibility

Corresponding author: Tel: + 82.2.880.4722

Email: D. Lee: [email protected] H. Jeong: [email protected] J. Cho: [email protected] J. Jeong: [email protected] J. Moon: [email protected]

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

1

Lee et al. Volume 18 Issue 2, 2015

Introduction As part of a direct agricultural market policy, the Korean government informatized agriculture by developing electronic commerce (e-commerce) in the late 1990s for local farmers (Moon et al. 2012). E-commerce has been associated with policies that shortened the supply chain by minimizing the role of a middleman, and thus provide consumers fresher product at lower prices along with higher profits for farmers. This has contributed to continuously expanding the e-commerce market for agricultural products; the market has increased from 182 million USD in 2001 to 3,847 million USD in 2012 (Statistics Korea 2013). The retail formats of grocery shopping have diversified into e-commerce and other non-store formats. Following the success of e-commerce as a medium for the direct agricultural market, TV commerce (t-commerce) based on Internet Protocol TV (IPTV) has received attention as an innovative transaction channel for increased competitiveness of the agricultural sector. T-commerce is an electronically mediated form of commerce that uses television as an interactive tool (Yu et al. 2005). T-commerce is also a non-store transaction format, similar to TV home shopping and e-commerce. This tool, like that of previous e-commerce activities, is expected to shorten the previous supply chain and thus enhance the welfare of farmers and consumers. Although the number of IPTV subscribers in South Korea has been increasing, and exceeded 7 million in 2013, the current t-commerce market is still in initial stages relative to other non-store transaction formats (Korea On-Line Shopping & Association 2013). Moreover, only a few empirical and theoretical studies address t-commerce in academia. Only a few studies (e.g., Yu et al. 2005, Brown et al. 2006, Park 2008, Jung 2011, Kim et al. 2011) focused on finding the factors that affect users’ adoption of t-commerce. This study is the first to compare customers’ attitudes toward adopting t-commerce by focusing on consumers’ previous online grocery shopping experience. The main goals of this study are as follows:

(1) to examine the relationship between prior online grocery shopping experience and preference for other retail formats (Study 1) and;

(2) to investigate the differences in attitudes toward adopting t-commerce for grocery shopping, based on prior online grocery shopping experience (Study 2).

T-Commerce and IPTV in Korea T-commerce refers to ‘all kinds of commercial services that occur through a digital set top box of either a cable TV or an IPTV’ (Lee 2013). As an electronically mediated business, t-commerce uses interactive television that combines video, voice, and transactional functions (Yu et al. 2005). It is one of various non-store shopping formats, such as TV home shopping and e-commerce (Dholakia et al. 2002). Oh (2010) classified t-commerce as ‘exclusive t-commerce’ and ‘subsidiary t-commerce’. Exclusive t-commerce provides t-commerce services only via an exclusive television channel. Subsidiary t-commerce, however, synchronizes with an existing television channel such as cable

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

2

Lee et al. Volume 18 Issue 2, 2015

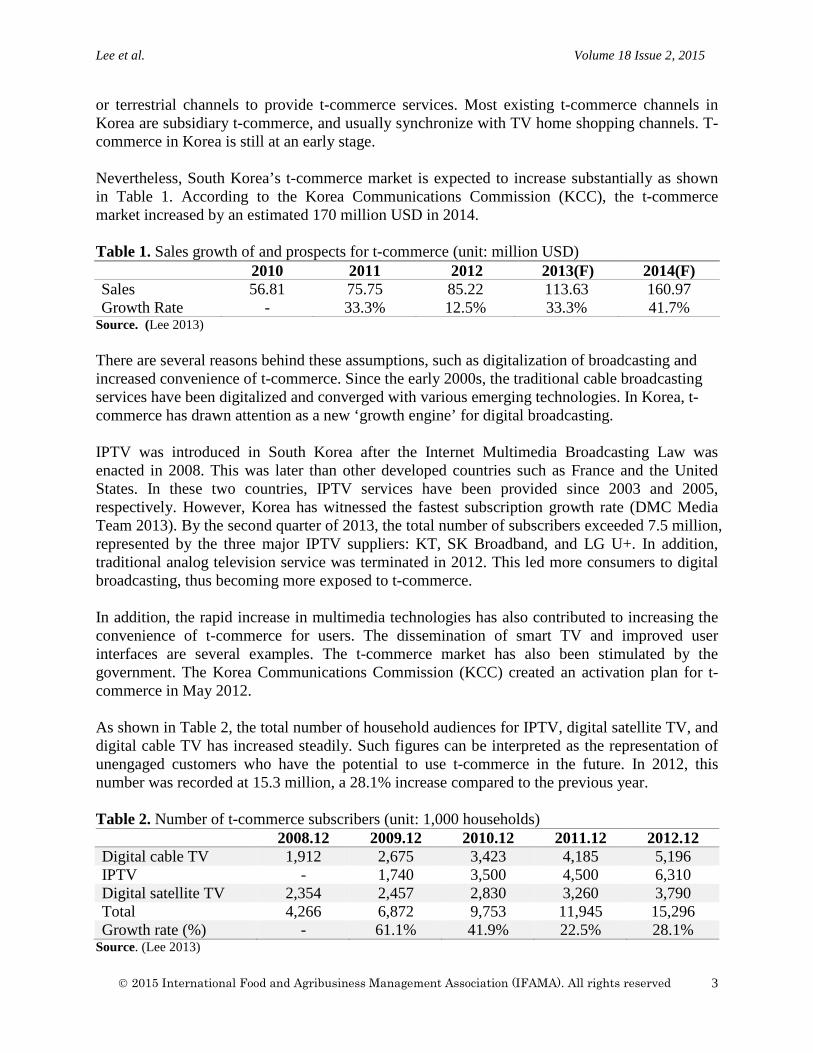

or terrestrial channels to provide t-commerce services. Most existing t-commerce channels in Korea are subsidiary t-commerce, and usually synchronize with TV home shopping channels. T-commerce in Korea is still at an early stage. Nevertheless, South Korea’s t-commerce market is expected to increase substantially as shown in Table 1. According to the Korea Communications Commission (KCC), the t-commerce market increased by an estimated 170 million USD in 2014. Table 1. Sales growth of and prospects for t-commerce (unit: million USD)

2010 2011 2012 2013(F) 2014(F) Sales 56.81 75.75 85.22 113.63 160.97 Growth Rate - 33.3% 12.5% 33.3% 41.7%

Source. (Lee 2013) There are several reasons behind these assumptions, such as digitalization of broadcasting and increased convenience of t-commerce. Since the early 2000s, the traditional cable broadcasting services have been digitalized and converged with various emerging technologies. In Korea, t-commerce has drawn attention as a new ‘growth engine’ for digital broadcasting. IPTV was introduced in South Korea after the Internet Multimedia Broadcasting Law was enacted in 2008. This was later than other developed countries such as France and the United States. In these two countries, IPTV services have been provided since 2003 and 2005, respectively. However, Korea has witnessed the fastest subscription growth rate (DMC Media Team 2013). By the second quarter of 2013, the total number of subscribers exceeded 7.5 million, represented by the three major IPTV suppliers: KT, SK Broadband, and LG U+. In addition, traditional analog television service was terminated in 2012. This led more consumers to digital broadcasting, thus becoming more exposed to t-commerce. In addition, the rapid increase in multimedia technologies has also contributed to increasing the convenience of t-commerce for users. The dissemination of smart TV and improved user interfaces are several examples. The t-commerce market has also been stimulated by the government. The Korea Communications Commission (KCC) created an activation plan for t-commerce in May 2012. As shown in Table 2, the total number of household audiences for IPTV, digital satellite TV, and digital cable TV has increased steadily. Such figures can be interpreted as the representation of unengaged customers who have the potential to use t-commerce in the future. In 2012, this number was recorded at 15.3 million, a 28.1% increase compared to the previous year. Table 2. Number of t-commerce subscribers (unit: 1,000 households)

2008.12 2009.12 2010.12 2011.12 2012.12 Digital cable TV 1,912 2,675 3,423 4,185 5,196 IPTV - 1,740 3,500 4,500 6,310 Digital satellite TV 2,354 2,457 2,830 3,260 3,790 Total 4,266 6,872 9,753 11,945 15,296 Growth rate (%) - 61.1% 41.9% 22.5% 28.1%

Source. (Lee 2013)

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

3

Lee et al. Volume 18 Issue 2, 2015

Although all channels listed in Table 2 are eligible to provide t-commerce services, IPTV holds the biggest market share and expected growth (Kim et al. 2006). Therefore, in this study, the scope of defining t-commerce is limited to IPTV.

Despite the increase in t-commerce, only a few empirical and theoretical studies address t-commerce in academia. Some studies (e.g., Park 2008, Kim et al. 2011) addressed consumers’ prior experience in other non-store media as an important factor that explains the current extension of t-commerce technology. Park (2008) investigated factors that influence willingness to adopt t-commerce. The results showed that the maximum willingness to pay for t-commerce tends to increase along with an increase in the average frequency of non-store transactions per month. Kim et al. (2011) also referred to compatibility in explaining the adoption of t-commerce, which they called ‘media substitutability’. The positive effect of the perceived substitutability of t-commerce for e-commerce on user intention to adopt t-commerce was investigated. Here, t-commerce is assumed to have similar functions to support e-commerce transactions; therefore, t-commerce is compatible with e-commerce. Although prior studies have attempted to draw out a relationship between a consumer’s experience and t-commerce, such studies were focused on ‘perceived’ media substitutability (Kim et al. 2011). Instead of examining the effect of ‘perceived’ substitutability, the present study endeavors to recognize the existing differences among the behaviors of t-commerce adoption, based on e-commerce experience by asking directly about the frequency of and preference for each retail format. Moreover, various retail formats (i.e., physical store, TV home shopping, e-commerce) were addressed to investigate the change within existing formats used when a new retail format is adopted. Park (2008) only examined within non-store retail formats.

Theoretical Background Kemp et al. (1998) argued that new technology or advanced technology is not easily accepted and adapted by society. There is not just one barrier to the introduction of alternative or new technologies; various factors hinder the introduction and diffusion. Numerous conditions and methods are required to fit the new technology into the world. Rodger’s (1995) innovation diffusion theory explains the barriers to new technology and the adoption process of information technologies in many studies. According to Rodger (1995), the technology adoption rate is affected by five innovation attributes: relative compatibility, relative advantage, complexity, trialability, and observability. In the same study, Rodger (1995) defined compatibility as ‘the degree to which an innovation is perceived as consistent with the existing values, past experiences, and needs of potential adopters’ (p. 224). Rodger stated that people are more likely to adopt an innovation they feel comfortable with, due to previous experience using a technology with similar functions. Wu et al. (2005) found that compatibility had the most significant influence on perceived usefulness and users’ behavioral intent to use. The researchers empirically tested the integrated model of innovation diffusion theory and the technology acceptance model (TAM). Other scholars agreed that people are more likely to adopt new information technologies compatible with those used previously (Joo et al. 2006, LaRose et al. 1992, Sarrina Li 2004). For

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

4

Lee et al. Volume 18 Issue 2, 2015

instance, according to Joo et al. (2006) individual intimateness, habit, and functional similarity positively influence the adoption intention when consumers adopt new technology, such as interactive TV. LaRose et al. (1992) investigated the adoption of phone-delivered information services, and Sarrina Li (2004) showed the effect of previous usage experience of similar technology in the adoption of interactive cable television. The effect of technology compatibility has also been explored in the field of retail formats choice. For instance, Eastin (2002) assessed the effect the experience formed through telephone and Internet usage on the adoption of four e-commerce activities (online shopping, online banking, online investing, and electronic payment for Internet services). According to the results, the experience built from previous use of telephone and the Internet positively affected the adoption of all four e-commerce activities. Hypothesis Development Study 1. Relationship between online grocery shopping experience and other grocery shopping channels experience

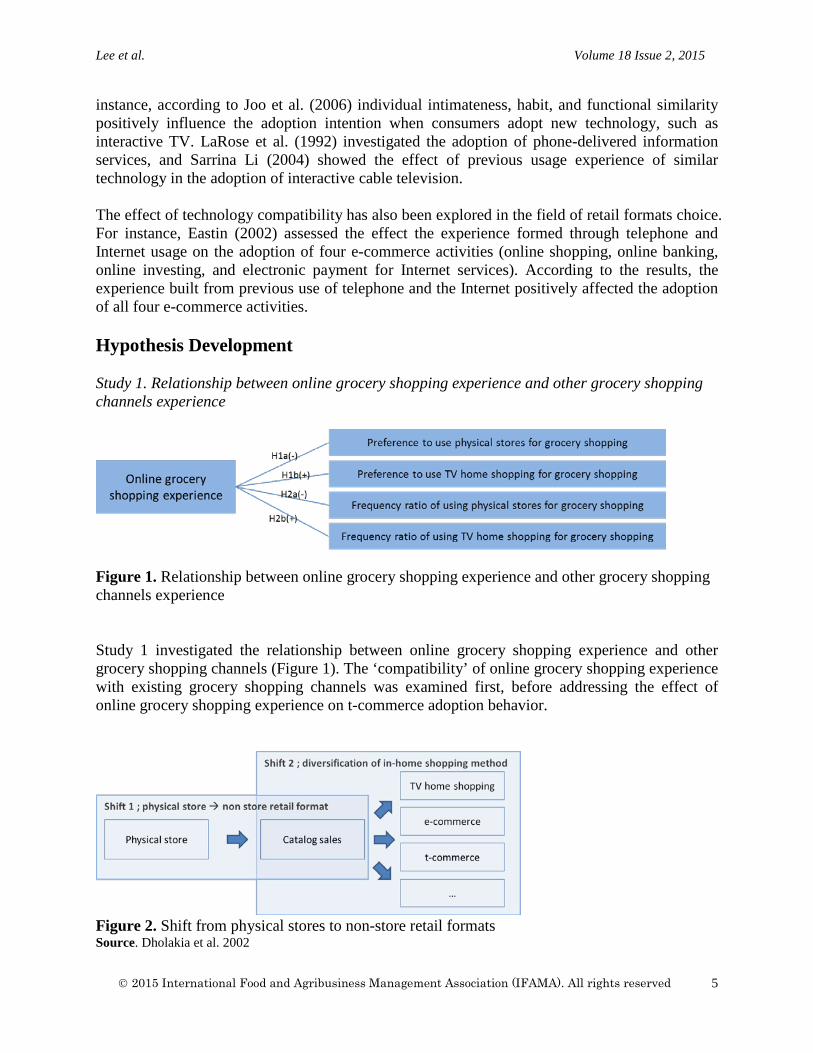

Figure 1. Relationship between online grocery shopping experience and other grocery shopping channels experience

Study 1 investigated the relationship between online grocery shopping experience and other grocery shopping channels (Figure 1). The ‘compatibility’ of online grocery shopping experience with existing grocery shopping channels was examined first, before addressing the effect of online grocery shopping experience on t-commerce adoption behavior.

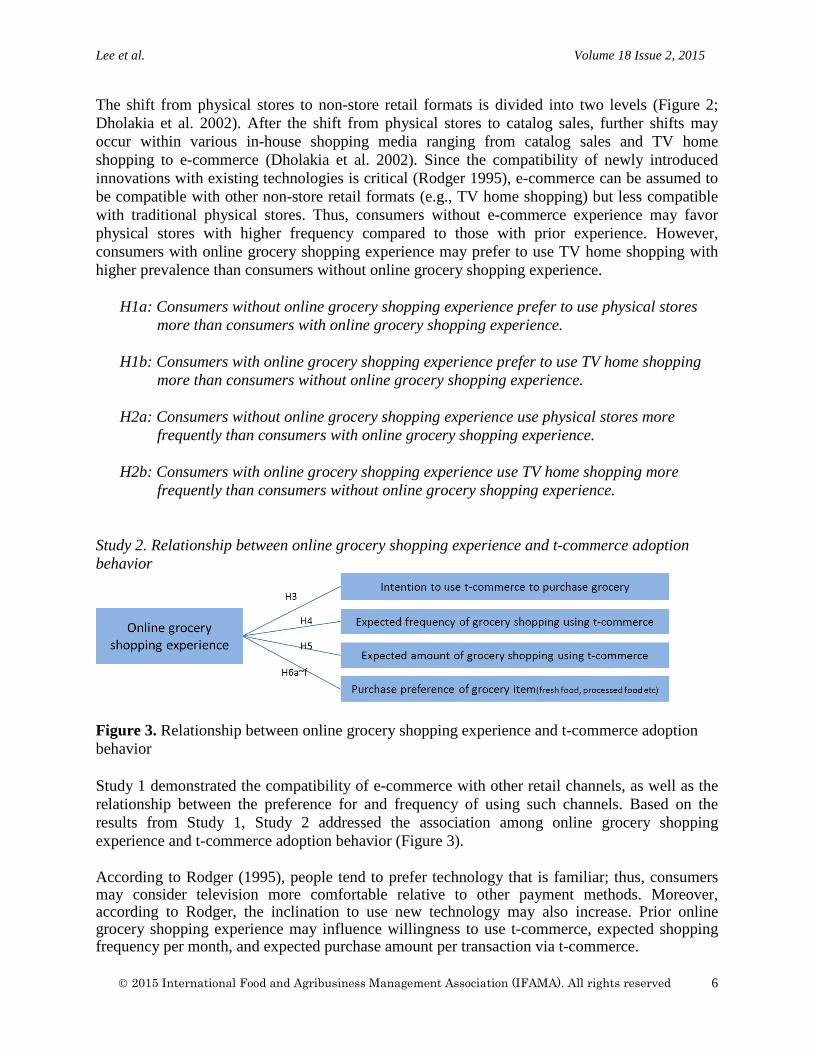

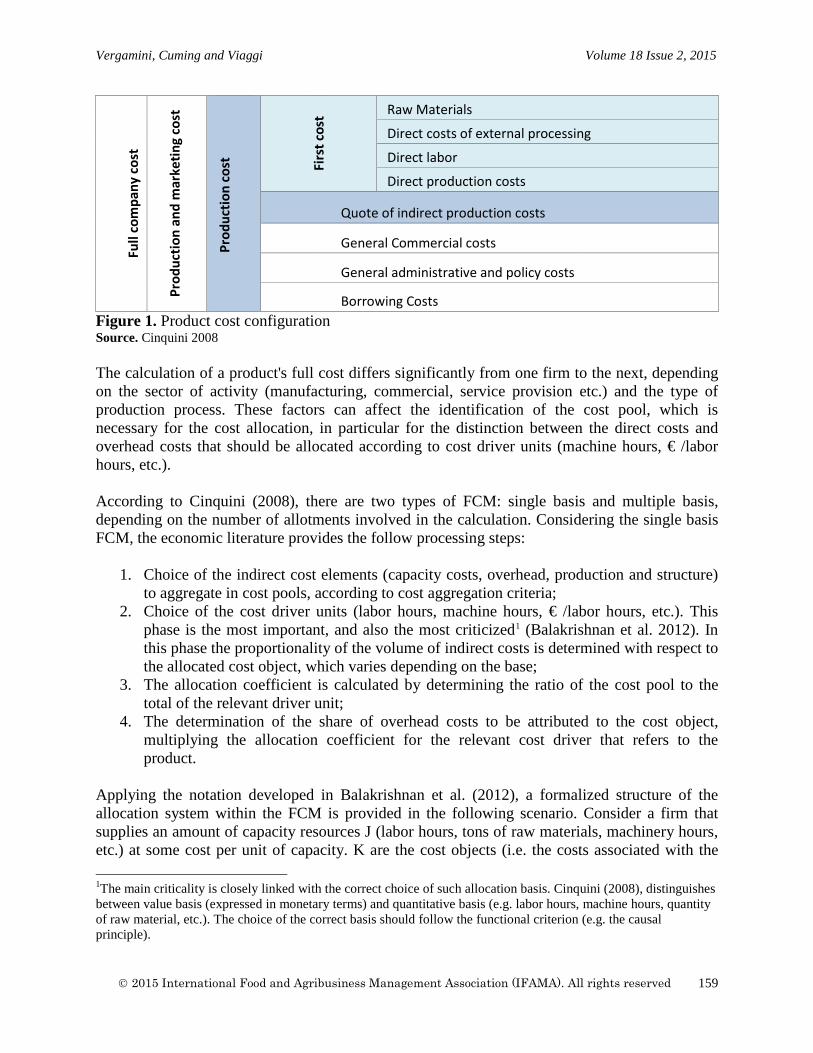

Figure 2. Shift from physical stores to non-store retail formats Source. Dholakia et al. 2002

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

5

Lee et al. Volume 18 Issue 2, 2015

The shift from physical stores to non-store retail formats is divided into two levels (Figure 2; Dholakia et al. 2002). After the shift from physical stores to catalog sales, further shifts may occur within various in-house shopping media ranging from catalog sales and TV home shopping to e-commerce (Dholakia et al. 2002). Since the compatibility of newly introduced innovations with existing technologies is critical (Rodger 1995), e-commerce can be assumed to be compatible with other non-store retail formats (e.g., TV home shopping) but less compatible with traditional physical stores. Thus, consumers without e-commerce experience may favor physical stores with higher frequency compared to those with prior experience. However, consumers with online grocery shopping experience may prefer to use TV home shopping with higher prevalence than consumers without online grocery shopping experience.

H1a: Consumers without online grocery shopping experience prefer to use physical stores more than consumers with online grocery shopping experience.

H1b: Consumers with online grocery shopping experience prefer to use TV home shopping more than consumers without online grocery shopping experience.

H2a: Consumers without online grocery shopping experience use physical stores more frequently than consumers with online grocery shopping experience.

H2b: Consumers with online grocery shopping experience use TV home shopping more frequently than consumers without online grocery shopping experience.

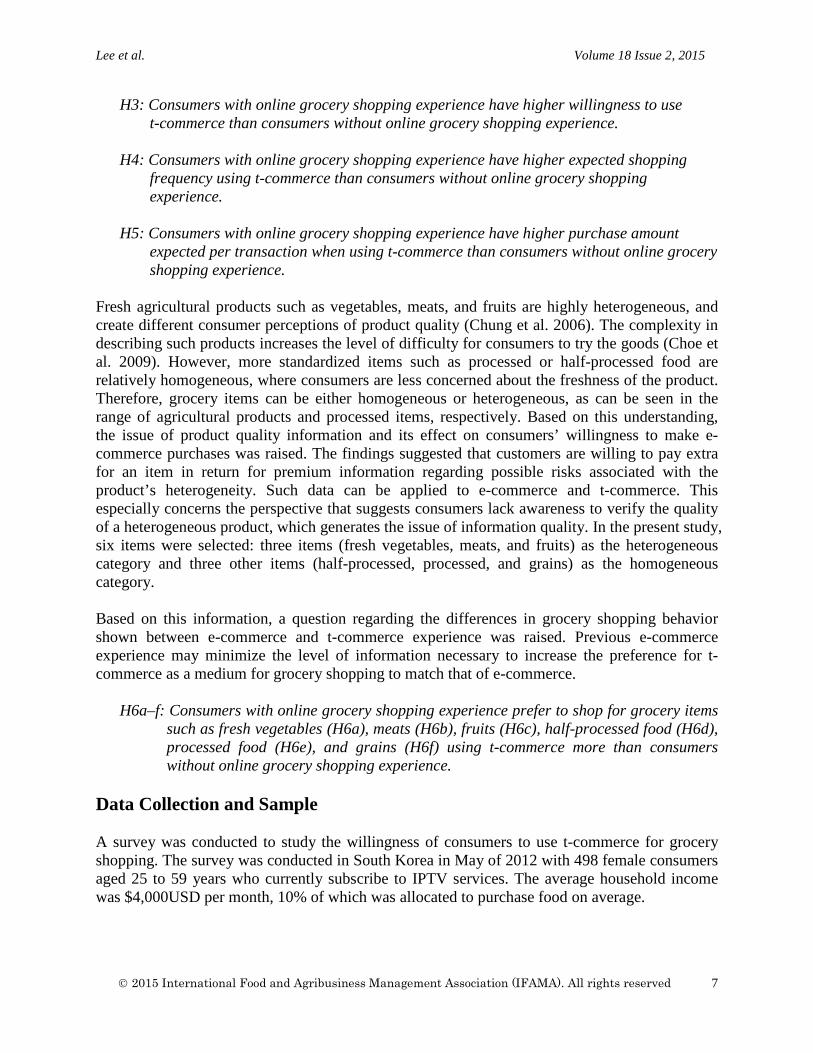

Study 2. Relationship between online grocery shopping experience and t-commerce adoption behavior

Figure 3. Relationship between online grocery shopping experience and t-commerce adoption behavior Study 1 demonstrated the compatibility of e-commerce with other retail channels, as well as the relationship between the preference for and frequency of using such channels. Based on the results from Study 1, Study 2 addressed the association among online grocery shopping experience and t-commerce adoption behavior (Figure 3). According to Rodger (1995), people tend to prefer technology that is familiar; thus, consumers may consider television more comfortable relative to other payment methods. Moreover, according to Rodger, the inclination to use new technology may also increase. Prior online grocery shopping experience may influence willingness to use t-commerce, expected shopping frequency per month, and expected purchase amount per transaction via t-commerce.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

6

Lee et al. Volume 18 Issue 2, 2015

H3: Consumers with online grocery shopping experience have higher willingness to use t-commerce than consumers without online grocery shopping experience.

H4: Consumers with online grocery shopping experience have higher expected shopping frequency using t-commerce than consumers without online grocery shopping experience.

H5: Consumers with online grocery shopping experience have higher purchase amount expected per transaction when using t-commerce than consumers without online grocery shopping experience.

Fresh agricultural products such as vegetables, meats, and fruits are highly heterogeneous, and create different consumer perceptions of product quality (Chung et al. 2006). The complexity in describing such products increases the level of difficulty for consumers to try the goods (Choe et al. 2009). However, more standardized items such as processed or half-processed food are relatively homogeneous, where consumers are less concerned about the freshness of the product. Therefore, grocery items can be either homogeneous or heterogeneous, as can be seen in the range of agricultural products and processed items, respectively. Based on this understanding, the issue of product quality information and its effect on consumers’ willingness to make e-commerce purchases was raised. The findings suggested that customers are willing to pay extra for an item in return for premium information regarding possible risks associated with the product’s heterogeneity. Such data can be applied to e-commerce and t-commerce. This especially concerns the perspective that suggests consumers lack awareness to verify the quality of a heterogeneous product, which generates the issue of information quality. In the present study, six items were selected: three items (fresh vegetables, meats, and fruits) as the heterogeneous category and three other items (half-processed, processed, and grains) as the homogeneous category. Based on this information, a question regarding the differences in grocery shopping behavior shown between e-commerce and t-commerce experience was raised. Previous e-commerce experience may minimize the level of information necessary to increase the preference for t-commerce as a medium for grocery shopping to match that of e-commerce.

H6a–f: Consumers with online grocery shopping experience prefer to shop for grocery items

such as fresh vegetables (H6a), meats (H6b), fruits (H6c), half-processed food (H6d), processed food (H6e), and grains (H6f) using t-commerce more than consumers without online grocery shopping experience.

Data Collection and Sample

A survey was conducted to study the willingness of consumers to use t-commerce for grocery shopping. The survey was conducted in South Korea in May of 2012 with 498 female consumers aged 25 to 59 years who currently subscribe to IPTV services. The average household income was $4,000USD per month, 10% of which was allocated to purchase food on average.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

7

Lee et al. Volume 18 Issue 2, 2015

Questionnaires were developed to explore the relationship between online grocery shopping experience and other grocery shopping channels (see Appendix). The respondents were asked to indicate their preference for each grocery shopping channel, such as physical store, TV home shopping, and e-commerce, using a seven-point Likert scale. There was also an open question that asked about the usage frequency per month of each channel. From this, the relationship between online grocery shopping experience and t-commerce adoption behavior was investigated. After brief instructions were provided about how to use t-commerce for grocery shopping, participants were asked to indicate their willingness to use the channel with a seven-point scale. Expected frequency and expected purchase rate using t-commerce were asked about as open questions. Last, when t-commerce is used, the preferences for each item for grocery shopping were asked with the same seven-point scale. Data Collection and Sample

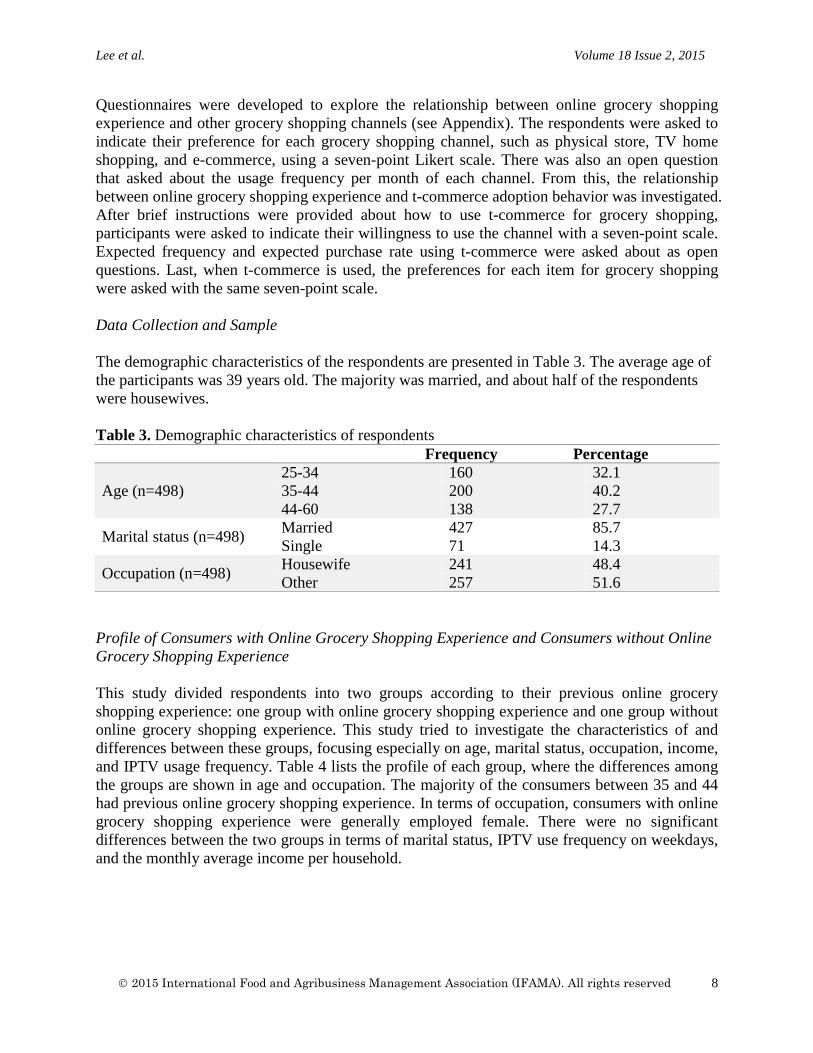

The demographic characteristics of the respondents are presented in Table 3. The average age of the participants was 39 years old. The majority was married, and about half of the respondents were housewives. Table 3. Demographic characteristics of respondents Frequency Percentage

Age (n=498) 25-34 160 32.1 35-44 200 40.2 44-60 138 27.7

Marital status (n=498) Married 427 85.7 Single 71 14.3

Occupation (n=498) Housewife 241 48.4 Other 257 51.6

Profile of Consumers with Online Grocery Shopping Experience and Consumers without Online Grocery Shopping Experience

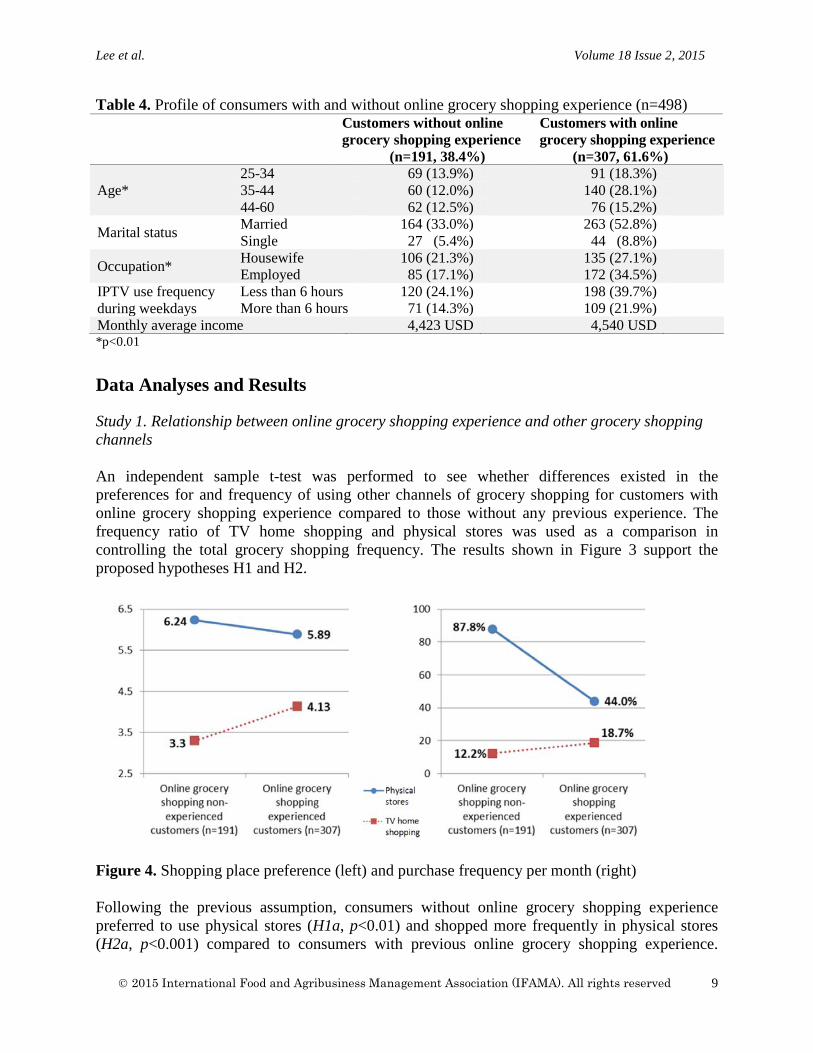

This study divided respondents into two groups according to their previous online grocery shopping experience: one group with online grocery shopping experience and one group without online grocery shopping experience. This study tried to investigate the characteristics of and differences between these groups, focusing especially on age, marital status, occupation, income, and IPTV usage frequency. Table 4 lists the profile of each group, where the differences among the groups are shown in age and occupation. The majority of the consumers between 35 and 44 had previous online grocery shopping experience. In terms of occupation, consumers with online grocery shopping experience were generally employed female. There were no significant differences between the two groups in terms of marital status, IPTV use frequency on weekdays, and the monthly average income per household.

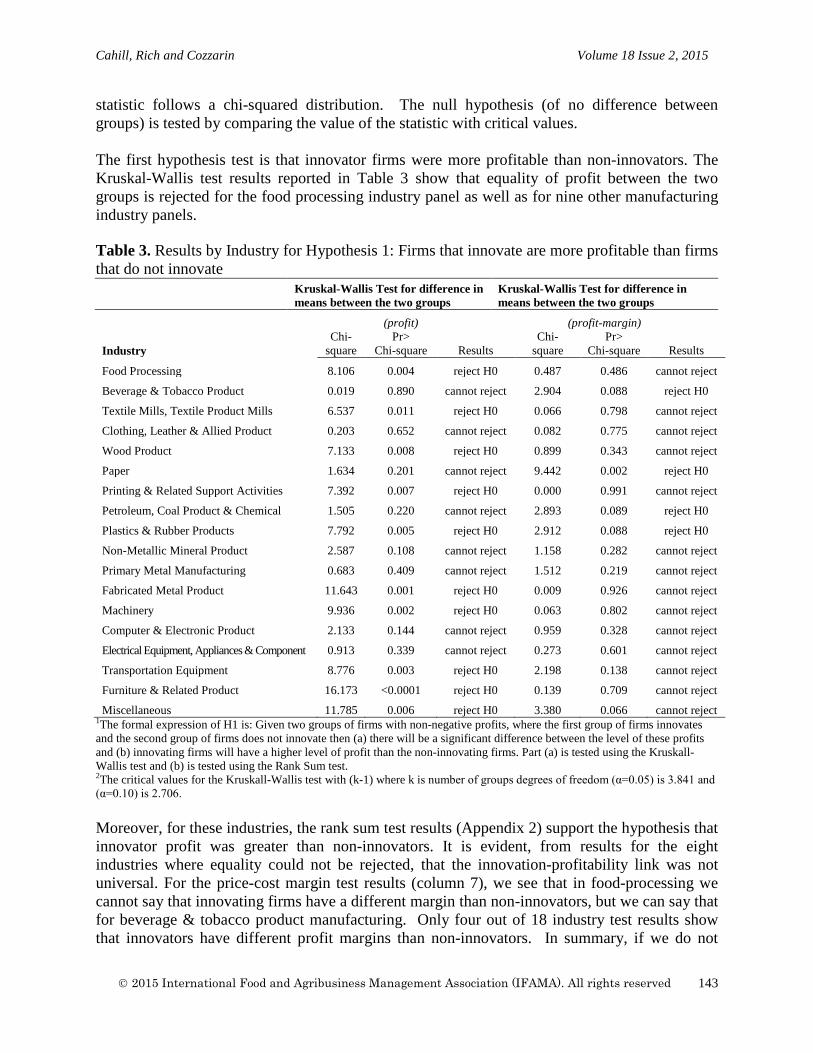

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

8

Lee et al. Volume 18 Issue 2, 2015

Table 4. Profile of consumers with and without online grocery shopping experience (n=498)

Customers without online grocery shopping experience (n=191, 38.4%)

Customers with online grocery shopping experience (n=307, 61.6%)

Age* 25-34 69 (13.9%) 91 (18.3%) 35-44 60 (12.0%) 140 (28.1%) 44-60 62 (12.5%) 76 (15.2%)

Marital status Married 164 (33.0%) 263 (52.8%) Single 27 (5.4%) 44 (8.8%)

Occupation* Housewife 106 (21.3%) 135 (27.1%) Employed 85 (17.1%) 172 (34.5%)

IPTV use frequency during weekdays

Less than 6 hours 120 (24.1%) 198 (39.7%) More than 6 hours 71 (14.3%) 109 (21.9%)

Monthly average income 4,423 USD 4,540 USD *p<0.01

Data Analyses and Results Study 1. Relationship between online grocery shopping experience and other grocery shopping channels

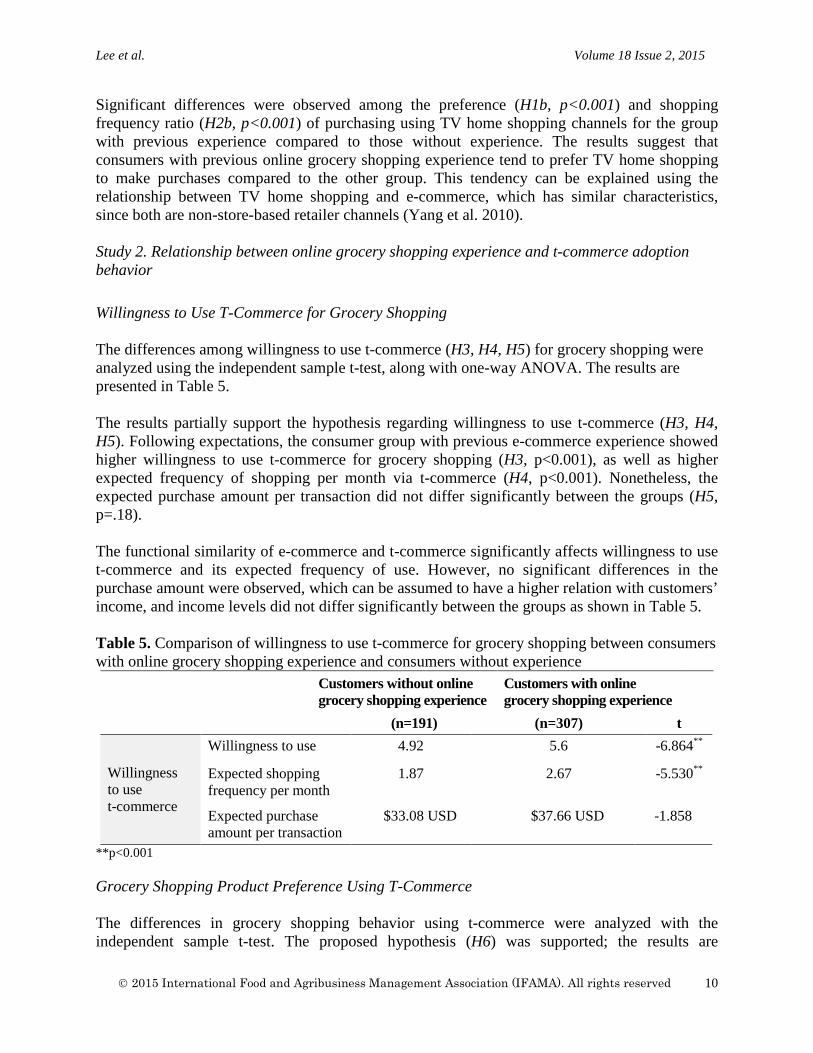

An independent sample t-test was performed to see whether differences existed in the preferences for and frequency of using other channels of grocery shopping for customers with online grocery shopping experience compared to those without any previous experience. The frequency ratio of TV home shopping and physical stores was used as a comparison in controlling the total grocery shopping frequency. The results shown in Figure 3 support the proposed hypotheses H1 and H2.

Figure 4. Shopping place preference (left) and purchase frequency per month (right)

Following the previous assumption, consumers without online grocery shopping experience preferred to use physical stores (H1a, p<0.01) and shopped more frequently in physical stores (H2a, p<0.001) compared to consumers with previous online grocery shopping experience.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

9

Lee et al. Volume 18 Issue 2, 2015

Significant differences were observed among the preference (H1b, p<0.001) and shopping frequency ratio (H2b, p<0.001) of purchasing using TV home shopping channels for the group with previous experience compared to those without experience. The results suggest that consumers with previous online grocery shopping experience tend to prefer TV home shopping to make purchases compared to the other group. This tendency can be explained using the relationship between TV home shopping and e-commerce, which has similar characteristics, since both are non-store-based retailer channels (Yang et al. 2010). Study 2. Relationship between online grocery shopping experience and t-commerce adoption behavior

Willingness to Use T-Commerce for Grocery Shopping

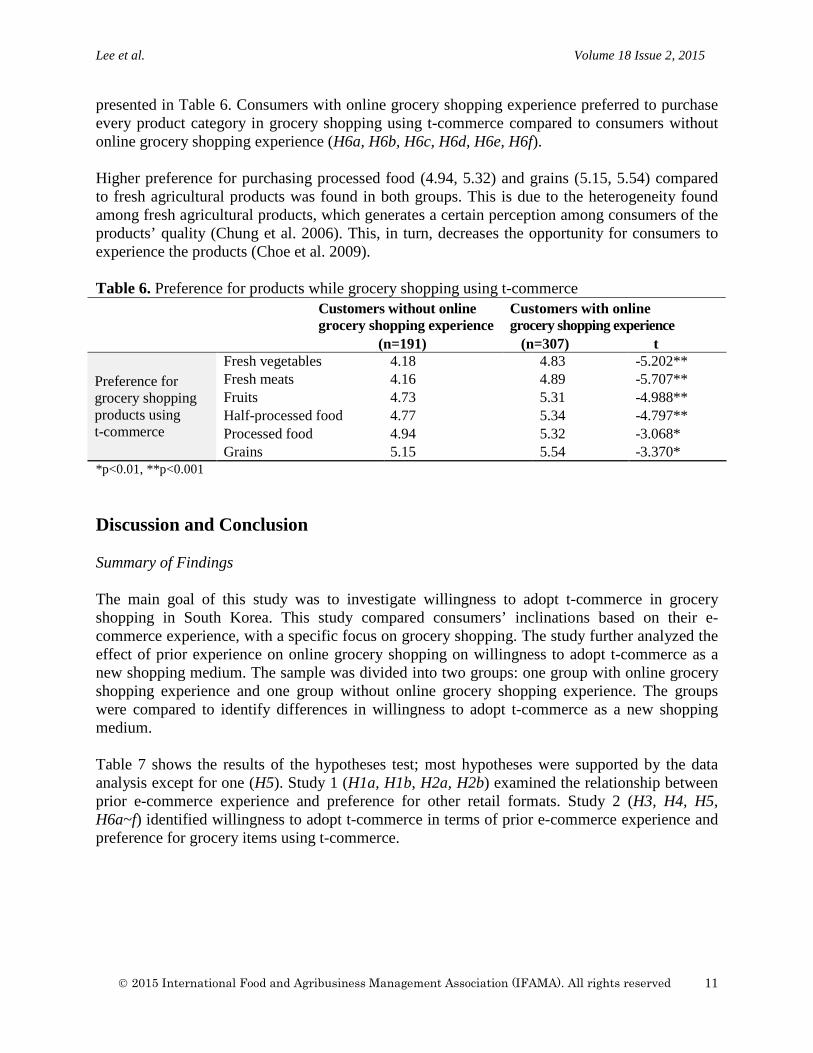

The differences among willingness to use t-commerce (H3, H4, H5) for grocery shopping were analyzed using the independent sample t-test, along with one-way ANOVA. The results are presented in Table 5. The results partially support the hypothesis regarding willingness to use t-commerce (H3, H4, H5). Following expectations, the consumer group with previous e-commerce experience showed higher willingness to use t-commerce for grocery shopping (H3, p<0.001), as well as higher expected frequency of shopping per month via t-commerce (H4, p<0.001). Nonetheless, the expected purchase amount per transaction did not differ significantly between the groups (H5, p=.18). The functional similarity of e-commerce and t-commerce significantly affects willingness to use t-commerce and its expected frequency of use. However, no significant differences in the purchase amount were observed, which can be assumed to have a higher relation with customers’ income, and income levels did not differ significantly between the groups as shown in Table 5. Table 5. Comparison of willingness to use t-commerce for grocery shopping between consumers with online grocery shopping experience and consumers without experience

Customers without online grocery shopping experience

Customers with online grocery shopping experience

(n=191) (n=307) t

Willingness to use t-commerce

Willingness to use 4.92 5.6 -6.864**

Expected shopping frequency per month

1.87 2.67 -5.530**

Expected purchase amount per transaction

$33.08 USD $37.66 USD -1.858

**p<0.001 Grocery Shopping Product Preference Using T-Commerce

The differences in grocery shopping behavior using t-commerce were analyzed with the independent sample t-test. The proposed hypothesis (H6) was supported; the results are

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

10

Lee et al. Volume 18 Issue 2, 2015

presented in Table 6. Consumers with online grocery shopping experience preferred to purchase every product category in grocery shopping using t-commerce compared to consumers without online grocery shopping experience (H6a, H6b, H6c, H6d, H6e, H6f). Higher preference for purchasing processed food (4.94, 5.32) and grains (5.15, 5.54) compared to fresh agricultural products was found in both groups. This is due to the heterogeneity found among fresh agricultural products, which generates a certain perception among consumers of the products’ quality (Chung et al. 2006). This, in turn, decreases the opportunity for consumers to experience the products (Choe et al. 2009). Table 6. Preference for products while grocery shopping using t-commerce

Customers without online grocery shopping experience

Customers with online grocery shopping experience

(n=191) (n=307) t

Preference for grocery shopping products using t-commerce

Fresh vegetables 4.18 4.83 -5.202** Fresh meats 4.16 4.89 -5.707** Fruits 4.73 5.31 -4.988** Half-processed food 4.77 5.34 -4.797** Processed food 4.94 5.32 -3.068* Grains 5.15 5.54 -3.370*

*p<0.01, **p<0.001 Discussion and Conclusion

Summary of Findings The main goal of this study was to investigate willingness to adopt t-commerce in grocery shopping in South Korea. This study compared consumers’ inclinations based on their e-commerce experience, with a specific focus on grocery shopping. The study further analyzed the effect of prior experience on online grocery shopping on willingness to adopt t-commerce as a new shopping medium. The sample was divided into two groups: one group with online grocery shopping experience and one group without online grocery shopping experience. The groups were compared to identify differences in willingness to adopt t-commerce as a new shopping medium. Table 7 shows the results of the hypotheses test; most hypotheses were supported by the data analysis except for one (H5). Study 1 (H1a, H1b, H2a, H2b) examined the relationship between prior e-commerce experience and preference for other retail formats. Study 2 (H3, H4, H5, H6a~f) identified willingness to adopt t-commerce in terms of prior e-commerce experience and preference for grocery items using t-commerce.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

11

Lee et al. Volume 18 Issue 2, 2015

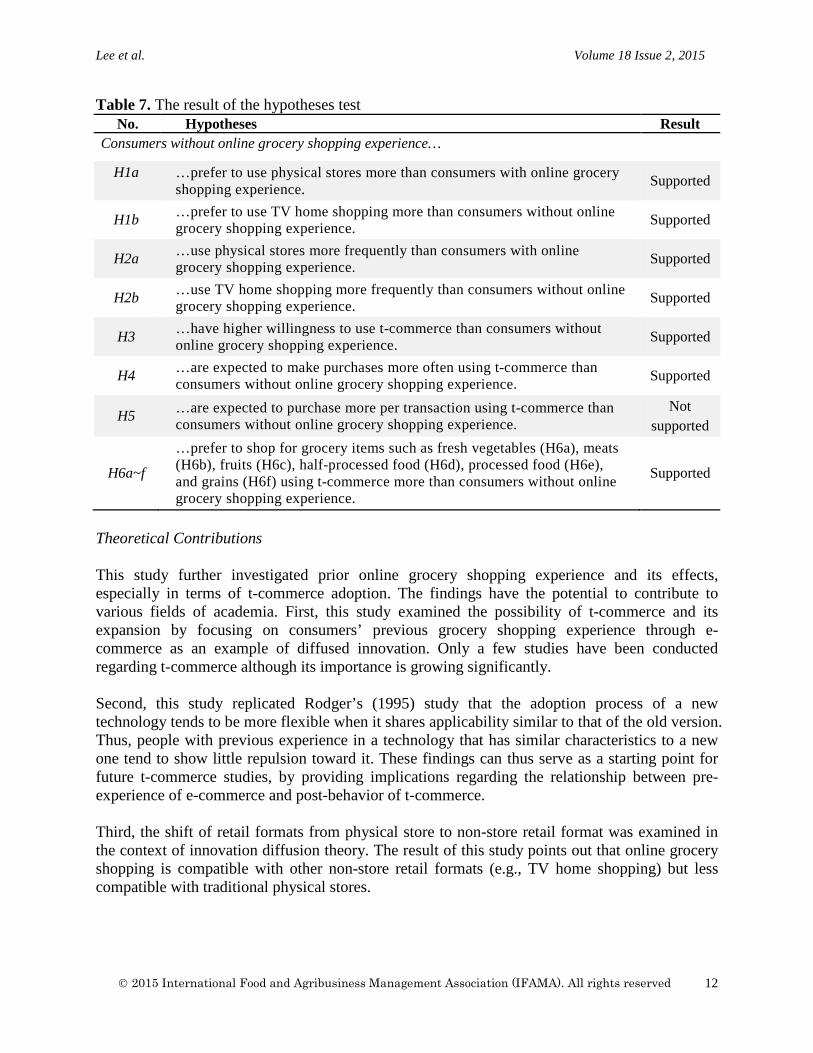

Table 7. The result of the hypotheses test No. Hypotheses Result

Consumers without online grocery shopping experience…

H1a …prefer to use physical stores more than consumers with online grocery shopping experience. Supported

H1b …prefer to use TV home shopping more than consumers without online grocery shopping experience. Supported

H2a …use physical stores more frequently than consumers with online grocery shopping experience. Supported

H2b …use TV home shopping more frequently than consumers without online grocery shopping experience. Supported

H3 …have higher willingness to use t-commerce than consumers without online grocery shopping experience. Supported

H4 …are expected to make purchases more often using t-commerce than consumers without online grocery shopping experience. Supported

H5 …are expected to purchase more per transaction using t-commerce than consumers without online grocery shopping experience.

Not supported

H6a~f

…prefer to shop for grocery items such as fresh vegetables (H6a), meats (H6b), fruits (H6c), half-processed food (H6d), processed food (H6e), and grains (H6f) using t-commerce more than consumers without online grocery shopping experience.

Supported

Theoretical Contributions This study further investigated prior online grocery shopping experience and its effects, especially in terms of t-commerce adoption. The findings have the potential to contribute to various fields of academia. First, this study examined the possibility of t-commerce and its expansion by focusing on consumers’ previous grocery shopping experience through e-commerce as an example of diffused innovation. Only a few studies have been conducted regarding t-commerce although its importance is growing significantly. Second, this study replicated Rodger’s (1995) study that the adoption process of a new technology tends to be more flexible when it shares applicability similar to that of the old version. Thus, people with previous experience in a technology that has similar characteristics to a new one tend to show little repulsion toward it. These findings can thus serve as a starting point for future t-commerce studies, by providing implications regarding the relationship between pre-experience of e-commerce and post-behavior of t-commerce. Third, the shift of retail formats from physical store to non-store retail format was examined in the context of innovation diffusion theory. The result of this study points out that online grocery shopping is compatible with other non-store retail formats (e.g., TV home shopping) but less compatible with traditional physical stores.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

12

Lee et al. Volume 18 Issue 2, 2015

Management Implications for Agribusiness Managers For agribusiness managers, the appropriate market segmentation is necessary to increase customers’ positive attitudes toward adopting t-commerce. In this sense, consumers with low inclination to adopt a new technology should be targeted to increase the overall adaptability. However, the findings of this study show that practitioners should target consumers with previous online grocery shopping experience to obtain t-commerce market growth. For instance, advertising a t-commerce-related product (i.e., IPTV) on t-commerce-related media (i.e., Internet shopping mall) is a good example of generating consumers’ first t-commerce experience and transaction. This then contributes to repeated purchases, which are now easier due to experience. Therefore, the findings imply that an advertising strategy that encourages the expansion of the t-commerce market through effective segmentation of target customers is needed. For example, strategies that encourage adoption of t-commerce through more lenient TV advertisement could be effective for expanding the t-commerce market at the initial stage. Since t-commerce is a promising industry, this study can serve as the foundation to spread the technology further. Moreover, this study can be applied to future studies regarding detailed investigations of a specific product category in relation to t-commerce. This is for the insight it offers for the differences in t-commerce adoption for grocery shopping, and its characteristics in terms of the homogeneity (e.g., processed food) and heterogeneity (e.g., fresh vegetables, fresh meats) of a product. In priori, processed food or grains should be promoted to sell through non-store retail format including t-commerce. After several experiences, consumers have higher tendencies to consume more heterogeneous products such as fresh agricultural products via non-store retail format.

Limitations and Future Research Directions Although this study has several findings, there are also some limitations. The study focused solely on grocery products. Thus, in terms of future studies regarding adoption of new technology, the subject should be generalized. Moreover, throughout the study, efforts were made to control factors during the process of making comparisons. The degree of willingness to adopt between consumers with and without e-commerce experience using t-test analysis, in terms of age and occupation, is one, though there were significant differences between the two groups. Thus, in future studies, all factors that influence the results should be removed. Acknowledgements

This research was supported by the MSIP(Ministry of Science, ICT and Future Planning), Korea,under the CITRC(Convergence Information Technology Research Center) support program (NIPA-2014-H0401-14-1008) supervised by the NIPA(National IT Industry Promotion Agency).

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

13

Lee et al. Volume 18 Issue 2, 2015

References Brown, I., K. De Rijk, K. Patel, Y. Twum-ampofo, and J. Van. 2006. T-Commerce: An

Investigation of Non-Adoption in South Africa. Proceedings of Conference on Information Science, Technology and Management (CISTM 2006), Chandigarh, India, July 16-18.

Choe, Y.C., J. Park, M. Chung, and J. Moon. 2009. Effect of the Food Traceability System for

Building Trust: Price Premium and Buying Behavior. Information Systems Frontiers 11(2):167-179.

Chung, M., J. Moon, B. Yoo, and Y.C. Choe. 2006. Paradox of Information Quality: Do

Consumers Pay More for Premium Product Information on E-Commerce Sites? Proceedings of Association for Information Systems (AMCIS) 2006 p57.

Dholakia, R.R., and U. Outi. 2002. Switching to electronic stores: consumer characteristics and

the perception of shopping benefits. International Journal of Retail & Distribution Management 30(10):459-469.

DMCMediaTeam. 2013. Evolution of TV and Change of Advertising Market. DMC Report p9. Eastin, M.S. 2002. Diffusion of E-Commerce: An Analysis of the Adoption of Four E-

Commerce Activities. Telematics and Informatics 19(3):251-267. Joo, J.M., and B.K. Park. 2006. A Study on Factors in Adopting the Interactive TV from the

Perspective of Technology Acceptance Model. Korean Journal of Journalism & Communication Studies 50(1):332-354.

Jung, K.S. 2011. Factors of on-Line Retail Purchase Action in T-Commerce. The e-Business

Studies 12(2):229-254. Kemp, R., J. Schot, and R. Hoogma. 1998. Regime shifts to sustainability through processes of

niche formation: the approach of strategic niche management. Technology Analysis & Strategic Management 10(2):175-198.

Kim, E., and S. Ko. 2011. Investigating User Adoption of T-Commerce. Computers. Networks,

Systems and Industrial Engineering (CNSI), 2011 First ACIS/JNU International Conference on: IEEE pp95-99.

Kim, M., Y. Park, and S. Go. 2006. A Study on the Trend and Forecast of IPTV Service.

Electronics and Telecommunication Trends 21(2):53-65. LaRose, R., and D. Atkin. 1992. Audiotext and the Re-Invention of the Telephone as a Mass

Medium. Journalism & Mass Communication Quarterly 69(2):413-421. Lee, K. 2013. Understanding and forecasting online shopping market. KOLSA Report 46-62.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

14

Lee et al. Volume 18 Issue 2, 2015

Moon, J., M.D. Hossain, H.G. Kang, and J. Shin. 2012. An Analysis of Agricultural Informatization in Korea: The Government’s Role in Bridging the Digital Gap. Information Development 28(2):102-116.

Oh, J. S. 2010. Current T-Commerce in Korea: As a retail distribution channel. Broadcasting

and Communications Policy 22(7):1-17. Park, S.Y. 2008. Consumer's Demands for the T-Commerce by the Technology Adoption Types.

Journal of Broadcast Engineering 13(3):319-327. Rodger, E. 1995. Diffusion of Innovations. New York: Free Press. Sarrina Li, S.C. 2004. Exploring the Factors Influencing the Adoption of Interactive Cable

Television Services in Taiwan. Journal of Broadcasting & Electronic Media 48(3):466-483.

Wu, J.H., and S.C. Wang. 2005. What drives mobile commerce? An empirical evaluation of the

revised technology acceptance model. Information & Management 42(5):719-729. Yang, L., and Y. Duan. 2010. Research on Culture-Based Model of TV Home Shopping

Development. Information Technology Journal 9(4):698-703. Yu, J., I. Ha, M. Choi, and J. Rho. 2005. Extending the Tam for a T-Commerce. Information &

Management 42(7):965-976.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

15

Lee et al. Volume 18 Issue 2, 2015

Appendix Place preference for grocery shopping Physical stores

1. How many times do you purchase groceries at physical stores on average per week?

_____times

TV home shopping

2. How many times do you purchase groceries from TV home shopping channels on average per month? _____times

Online shopping mall

3. How many times do you purchase groceries through online shopping malls on average per month? _____times

Willingness to use t-commerce for grocery shopping

1. If a t-commerce service that you can get related information and buy groceries is provided, are you willing to use the service?

(Likert-type scale: 1 = Definitely will not use and 7 = Definitely will use) 2. Expected shopping frequency per month

If you use the service, how many times are you willing to use per month? _____times

3. Expected purchase amount per one transaction

If you use the service, how much are you willing to spend on average per purchase? KRW _____

Preference in grocery shopping products using t-commerce

Please indicate your preference for each item as products the t-commerce service sells. (Likert-type scale: 1= No preference at all and 7= Very much prefer)

- Fresh meat - Fruits - Fresh vegetables

- Grains - Half-processed food - Processed food

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

16

International Food and Agribusiness Management Review Volume 18 Issue 2, 2015

Preferences for Farmstead, Artisan, and Other Cheese Attributes:

Evidence from a Conjoint Study in the Northeast United States

Qingbin Wanga, Ethan Thompsonb, and Robert Parsonsc

a Professor, Department of Community Development and Applied Economics, 205C Morrill Hall, The University of Vermont, Burlington, Vermont, 05405, U.S.A.

b Research Associate, Department of Community Development and Applied Economics,

The University of Vermont, Burlington, Vermont, 05405, U.S.A.

c Extension Professor, Department of Community Development and Applied Economics, The University of Vermont, Burlington, Vermont, 05405, U.S.A.

Abstract While many small American dairy farms are struggling to stay in business due to fluctuating milk prices and rising production costs, value-added products such as cheese may help to boost revenue and diversify production practices. This study assesses consumer preferences and willingness to pay (WTP) for selected cheese attributes (farmstead, artisan, organic, local, and use of renewable energy in cheese production) through a conjoint survey conducted in Vermont, Manhattan, and Boston. Survey participants were found to segment into two groups: a quality-seeking group that displays strong preferences and a significant WTP of 15% to 25% more for each of the quality attributes, and a price-sensitive group with preference ratings highly determined by price. This research provides useful information to managers and marketers involved in farmstead and artisan dairy production and marketing. Keywords: farmstead cheese, artisan cheese, conjoint analysis, willingness to pay, Northeast United States

Corresponding author: Tel: + 1 802.656.4564 Email: Q. Wang: [email protected]

E. Thompson: [email protected] R. Parsons: [email protected]

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

17

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

Introduction While on-farm production of value-added dairy products such as cheese, yogurt, butter, and ice cream may provide small dairy farms a means to increase revenue, escape the cyclical boom and bust pattern of fluid milk prices, and improve economic stability, the potential opportunities and benefits to dairy farms depend heavily on consumer preferences and willingness to pay (WTP) for such products. This study is motivated by the growing interest in on-farm production of value-added dairy products and by the lack of information on the market potentials for such products. The economic pressure placed on dairy farms by highly variable milk prices is the primary factor in small dairy farm business cessation in the United States (Gierzynski et al. 2010). National trends have moved toward fewer but significantly larger dairy farms, as large farms have been more likely to find efficiencies in production and to survive when the fluid milk price is low (MacDonald et al. 2007). For example, in Vermont, a traditional dairy shed of the Northeast United States, the annual statewide milk production increased from 1.49 billion pounds in 1947 to 2.61 billion pounds in 2013 but, over the same period, the number of dairy farms dropped from 11,206 to fewer than 900 (Gierzynski et al. 2010; Gould 2015; Vermont Agency of Agriculture, Food & Markets 2015). Most dairy farm business cessations in Vermont and across the United States have occurred in operations with 200 or fewer milking cows while the number of large farms with more than 500 cows has increased significantly. As a result, the percentage of milk produced by large farms has increased dramatically. In Vermont, the contribution to total state milk production from farms with more than 500 head rose from 9% in 1997 to 37% in 2007 (Gould 2010). As per capita fluid milk consumption in the United States has decreased significantly in the past three decades, the per capita consumption of cheese has increased year after year—reaching a record high of 33.51 pounds in 2012 (International Dairy Foods Association 2014). To meet the increasing demand for cheese and capture the benefits of economies of scale, modern cheese production has abandoned many traditional practices and embraced industrial-scale production models. The majority of this cheese is produced at factories that rely heavily on mechanization and automation. This cheese, often referred to as industrial, factory, or commodity cheese, is produced in very large batches intended to meet uniform standards, for trading in commodity markets. This process has led to very large increases in the quantities of cheese available in the market, bringing cheese to the diets of many people, but has also favored an agricultural system that relies on efficiency and large-scale production over traditional techniques and skills. Traditional cheeses, often referred to as artisan cheeses, are produced primarily by hand, in small batches, and with particular attention to the tradition and art of cheese making (American Cheese Society 2010). Further designating a cheese as farmstead indicates that the cheese was made on-farm and that the milk used in the cheese-making process came from only the farm where the cheese was made. Artisan and farmstead cheeses typically reflect the traditional flavors and characteristics of the particular region in which the cheese is made (a characteristic known as terroir), support small-scale milk producers, and benefit local economies in multiple ways, including through milk production and cheese-making cooperatives.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

18

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

Industrialized food production and distribution systems have raised public concerns about food safety and the disconnection between consumers and producers and, as a result, there is growing demand for traditional food products with attributes such as organic, local, and artisan. The major purposes of this study are to examine consumer preferences and WTP for artisan and other attributes of cheese and to provide market information to dairy farmers who are interested in producing and marketing cheese as a value-added product. Specifically, a conjoint survey was conducted in Vermont, Manhattan, and Boston to collect primary data, and the data were then used to analyze the relative importance of selected cheese attributes, assess WTP for artisan and other quality attributes, and derive marketing information and recommendations. The rest of this paper describes the research method and procedures, presents the empirical results, and summarizes the major findings and conclusions. Data and Methods Conjoint analysis was used to collect primary data and quantify consumer preferences and WTP for selected attributes of cheese in this study. Conjoint analysis has been widely used in marketing research and provides a means of empirically estimating consumer preferences and WTP for attributes of a specific product (Wittink and Cattin 1989). Although conjoint analysis may not eliminate the potential difference between the estimated WTP and true WTP in a marketplace, it has been considered to be more reliable than some other methods, such as contingent valuation (Wang, Shi, and Chan-Halbrendt 2004; Caruso, Rahnev, and Banaji 2009). Conjoint analysis is a decompositional method that assesses consumer preferences through the rating or ranking of a set of product profiles with varying attribute levels (Green and Srinivasan 1990). First introduced by Luce and Tukey (1964), conjoint analysis was shortly afterward developed into a practical method of measuring the joint effects of product or service attributes on consumer preferences for the product or service. In conjoint analysis, regression is generally used to estimate the contributions of selected attributes to the overall preference rating or ranking, and the estimated regression coefficients can then be used to calculate the relative importance of each attribute as well as the trade-offs between price and other attribute levels (Green and Srinivasan 1978; Wang, Shi, and Chan-Halbrendt 2004). In a conjoint survey, respondents are placed in a hypothetical situation that is as similar as possible to a purchase decision-making situation in which they have to consider the trade-offs between attributes, especially between price and other attributes. This ability to quantify trade-offs is one of the major reasons that conjoint analysis has been widely used in marketing research for product modification or new product development. This conjoint study of cheese is completed via the procedures detailed in the following sections. Selection of Attributes and Their Levels The most frequently used means of attribute selection are expert judgment and group interviews (Wittink and Cattin 1989). In this study, the attributes and their levels were selected on the basis of the objectives of the study, findings from reviews of relevant literature, input from focus groups of cheese consumers, and feedback from cheese industry professionals. The attributes and levels selected for this study are listed in Table 1. Note that the variable type to be used in the regression analysis in a later section is also included in Table 1.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

19

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

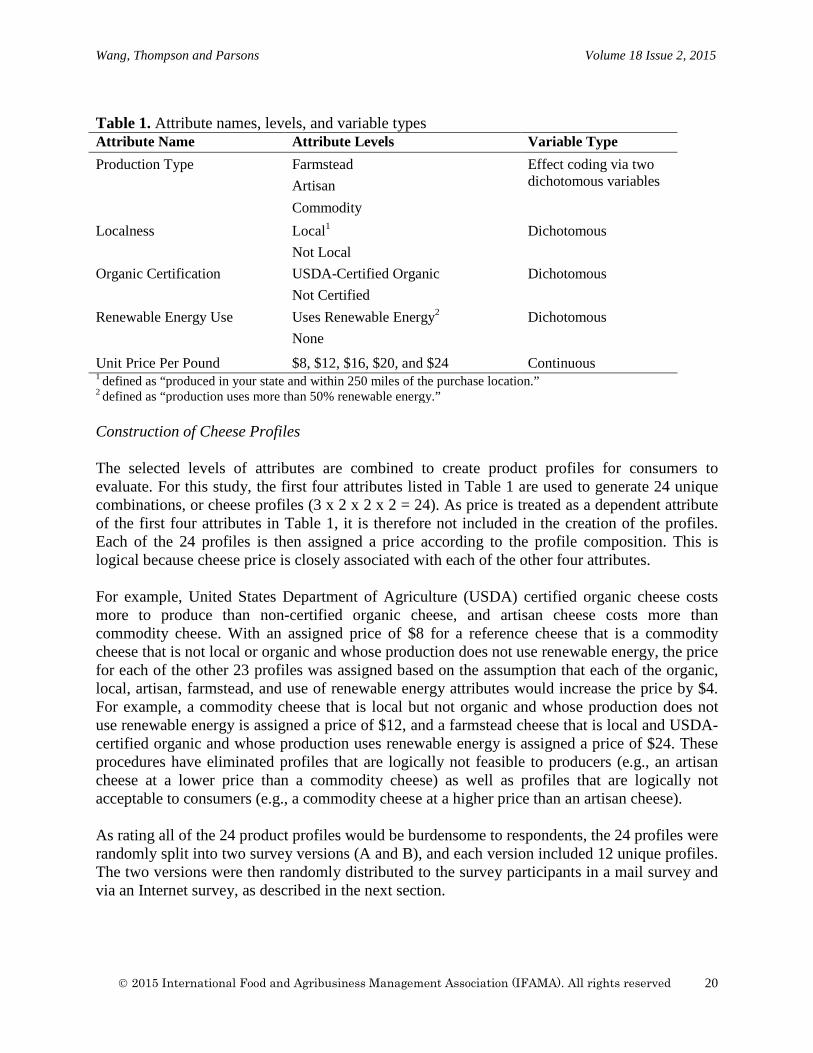

Table 1. Attribute names, levels, and variable types Attribute Name Attribute Levels Variable Type Production Type Farmstead Effect coding via two

dichotomous variables Artisan Commodity Localness Local1 Dichotomous Not Local Organic Certification USDA-Certified Organic Dichotomous Not Certified Renewable Energy Use Uses Renewable Energy2 Dichotomous None

Unit Price Per Pound $8, $12, $16, $20, and $24 Continuous 1 defined as “produced in your state and within 250 miles of the purchase location.” 2 defined as “production uses more than 50% renewable energy.” Construction of Cheese Profiles The selected levels of attributes are combined to create product profiles for consumers to evaluate. For this study, the first four attributes listed in Table 1 are used to generate 24 unique combinations, or cheese profiles (3 x 2 x 2 x 2 = 24). As price is treated as a dependent attribute of the first four attributes in Table 1, it is therefore not included in the creation of the profiles. Each of the 24 profiles is then assigned a price according to the profile composition. This is logical because cheese price is closely associated with each of the other four attributes. For example, United States Department of Agriculture (USDA) certified organic cheese costs more to produce than non-certified organic cheese, and artisan cheese costs more than commodity cheese. With an assigned price of $8 for a reference cheese that is a commodity cheese that is not local or organic and whose production does not use renewable energy, the price for each of the other 23 profiles was assigned based on the assumption that each of the organic, local, artisan, farmstead, and use of renewable energy attributes would increase the price by $4. For example, a commodity cheese that is local but not organic and whose production does not use renewable energy is assigned a price of $12, and a farmstead cheese that is local and USDA-certified organic and whose production uses renewable energy is assigned a price of $24. These procedures have eliminated profiles that are logically not feasible to producers (e.g., an artisan cheese at a lower price than a commodity cheese) as well as profiles that are logically not acceptable to consumers (e.g., a commodity cheese at a higher price than an artisan cheese). As rating all of the 24 product profiles would be burdensome to respondents, the 24 profiles were randomly split into two survey versions (A and B), and each version included 12 unique profiles. The two versions were then randomly distributed to the survey participants in a mail survey and via an Internet survey, as described in the next section.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

20

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

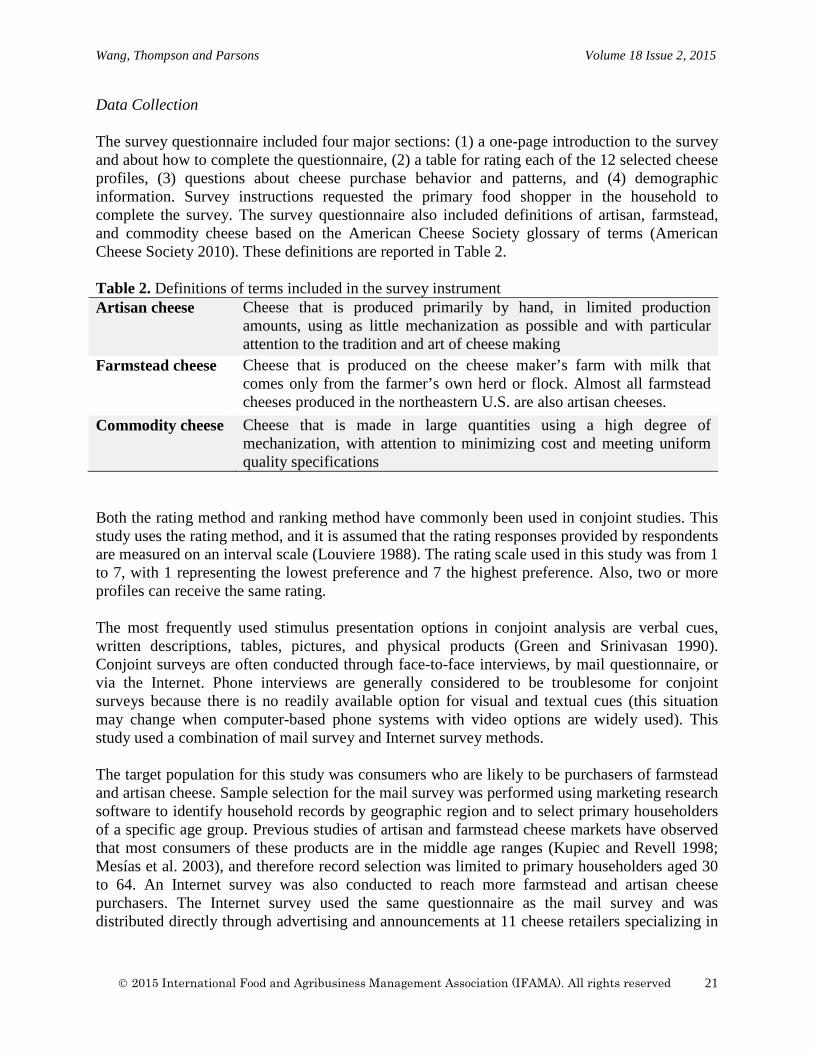

Data Collection The survey questionnaire included four major sections: (1) a one-page introduction to the survey and about how to complete the questionnaire, (2) a table for rating each of the 12 selected cheese profiles, (3) questions about cheese purchase behavior and patterns, and (4) demographic information. Survey instructions requested the primary food shopper in the household to complete the survey. The survey questionnaire also included definitions of artisan, farmstead, and commodity cheese based on the American Cheese Society glossary of terms (American Cheese Society 2010). These definitions are reported in Table 2. Table 2. Definitions of terms included in the survey instrument Artisan cheese Cheese that is produced primarily by hand, in limited production

amounts, using as little mechanization as possible and with particular attention to the tradition and art of cheese making

Farmstead cheese Cheese that is produced on the cheese maker’s farm with milk that comes only from the farmer’s own herd or flock. Almost all farmstead cheeses produced in the northeastern U.S. are also artisan cheeses.

Commodity cheese Cheese that is made in large quantities using a high degree of mechanization, with attention to minimizing cost and meeting uniform quality specifications

Both the rating method and ranking method have commonly been used in conjoint studies. This study uses the rating method, and it is assumed that the rating responses provided by respondents are measured on an interval scale (Louviere 1988). The rating scale used in this study was from 1 to 7, with 1 representing the lowest preference and 7 the highest preference. Also, two or more profiles can receive the same rating. The most frequently used stimulus presentation options in conjoint analysis are verbal cues, written descriptions, tables, pictures, and physical products (Green and Srinivasan 1990). Conjoint surveys are often conducted through face-to-face interviews, by mail questionnaire, or via the Internet. Phone interviews are generally considered to be troublesome for conjoint surveys because there is no readily available option for visual and textual cues (this situation may change when computer-based phone systems with video options are widely used). This study used a combination of mail survey and Internet survey methods. The target population for this study was consumers who are likely to be purchasers of farmstead and artisan cheese. Sample selection for the mail survey was performed using marketing research software to identify household records by geographic region and to select primary householders of a specific age group. Previous studies of artisan and farmstead cheese markets have observed that most consumers of these products are in the middle age ranges (Kupiec and Revell 1998; Mesías et al. 2003), and therefore record selection was limited to primary householders aged 30 to 64. An Internet survey was also conducted to reach more farmstead and artisan cheese purchasers. The Internet survey used the same questionnaire as the mail survey and was distributed directly through advertising and announcements at 11 cheese retailers specializing in

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

21

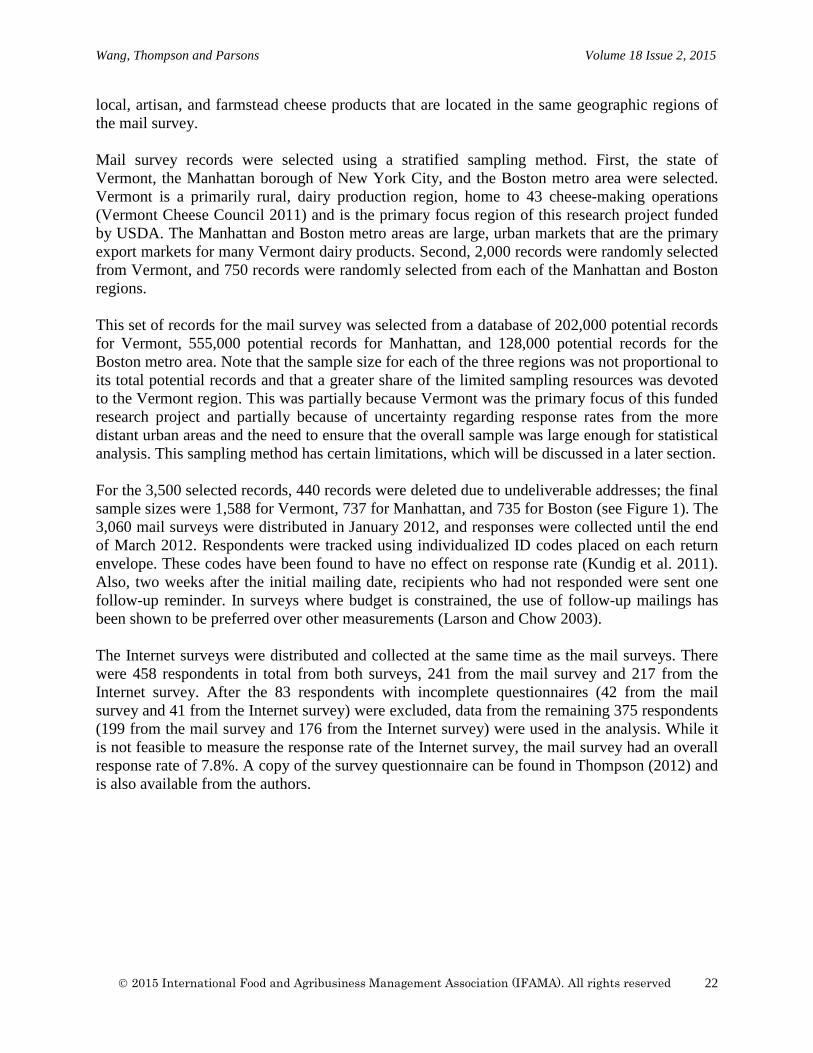

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

local, artisan, and farmstead cheese products that are located in the same geographic regions of the mail survey. Mail survey records were selected using a stratified sampling method. First, the state of Vermont, the Manhattan borough of New York City, and the Boston metro area were selected. Vermont is a primarily rural, dairy production region, home to 43 cheese-making operations (Vermont Cheese Council 2011) and is the primary focus region of this research project funded by USDA. The Manhattan and Boston metro areas are large, urban markets that are the primary export markets for many Vermont dairy products. Second, 2,000 records were randomly selected from Vermont, and 750 records were randomly selected from each of the Manhattan and Boston regions. This set of records for the mail survey was selected from a database of 202,000 potential records for Vermont, 555,000 potential records for Manhattan, and 128,000 potential records for the Boston metro area. Note that the sample size for each of the three regions was not proportional to its total potential records and that a greater share of the limited sampling resources was devoted to the Vermont region. This was partially because Vermont was the primary focus of this funded research project and partially because of uncertainty regarding response rates from the more distant urban areas and the need to ensure that the overall sample was large enough for statistical analysis. This sampling method has certain limitations, which will be discussed in a later section. For the 3,500 selected records, 440 records were deleted due to undeliverable addresses; the final sample sizes were 1,588 for Vermont, 737 for Manhattan, and 735 for Boston (see Figure 1). The 3,060 mail surveys were distributed in January 2012, and responses were collected until the end of March 2012. Respondents were tracked using individualized ID codes placed on each return envelope. These codes have been found to have no effect on response rate (Kundig et al. 2011). Also, two weeks after the initial mailing date, recipients who had not responded were sent one follow-up reminder. In surveys where budget is constrained, the use of follow-up mailings has been shown to be preferred over other measurements (Larson and Chow 2003). The Internet surveys were distributed and collected at the same time as the mail surveys. There were 458 respondents in total from both surveys, 241 from the mail survey and 217 from the Internet survey. After the 83 respondents with incomplete questionnaires (42 from the mail survey and 41 from the Internet survey) were excluded, data from the remaining 375 respondents (199 from the mail survey and 176 from the Internet survey) were used in the analysis. While it is not feasible to measure the response rate of the Internet survey, the mail survey had an overall response rate of 7.8%. A copy of the survey questionnaire can be found in Thompson (2012) and is also available from the authors.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

22

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

Figure 1. Study regions and sample size Survey response rates in the United States have been declining for several decades (Dey 1997). In addition to the common factors cited by many individuals who refuse to participate in mail or phone surveys, such as busy schedule and lack of compensation for their time, one potential factor for the low response rate for this survey is that some individuals may not be cheese consumers and therefore did not want to participate in this survey about cheese. This confirms the commonly observed trend that respondents who are interested in a survey are more likely to respond than those who are not interested (Schiltz 1988). Vermont provided 69.6% of the valid survey responses, while Manhattan and Boston generated 14.7% and 6.7%, respectively; the remainder were internet survey responses that originated from other areas in the Northeast. Because of the relatively low response rates in general and the small numbers of respondents from Manhattan and Boston, there are potential non-response bias issues in interpreting and applying the empirical results. The results of this study enhance our understanding of consumer preferences and WTP for artisan and other cheese attributes in the study regions, but these findings should be interpreted with caution and may not be used to estimate the preferences and WTP at the market level. More extensive studies with larger samples are needed to accurately estimate the market demand, especially in urban markets like Manhattan and Boston. Because each respondent provided rating responses for 12 cheese profiles, the 375 valid survey responses provided a total of 4,500 observations for use in the subsequent quantitative analysis. This is considered to be a major advantage of conjoint analysis as compared to other marketing research methods that provide only one observation from each respondent (Halbrendt et al. 1995). Efforts were also made to identify potential measurement errors or rating inconsistencies, which were then incorporated into the regression analysis through weighted least squares (WLS), discussed later. Specification of the Preference Model Conjoint analysis assumes that consumer preference ratings or rankings of a particular product or service are determined by the product’s attributes including price. In this study, consumer rating of the cheese profiles is assumed to be a function of the five selected cheese attributes:

Vermont: 1,588 Manhattan: 737 Boston: 735

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

23

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

(1) R = f (P, LO, OC, RE, PR) where R is the preference rating for each profile, P represents the production type, LO is localness, OC is the presence of USDA organic certification, RE is the use of renewable energy in cheese production, and PR is the price. In an empirical analysis, the above function needs to be presented in a specific functional form. Following the discussion about alternative preference model specifications by Green and Srinivasan (1978), this study uses a linear function to estimate the impacts of selected cheese attributes on the preference rating:

(2) 𝑅𝑅𝑖𝑖𝑖𝑖 = 𝑎𝑎0 + 𝑎𝑎1𝑃𝑃1𝑖𝑖 + 𝑎𝑎2𝑃𝑃2𝑖𝑖 + 𝑎𝑎3𝐿𝐿𝐿𝐿𝑖𝑖 + 𝑎𝑎4𝐿𝐿𝑂𝑂𝑖𝑖 + 𝑎𝑎5𝑅𝑅𝑅𝑅𝑖𝑖 + 𝑎𝑎6𝑃𝑃𝑅𝑅𝑖𝑖 + 𝑒𝑒𝑖𝑖𝑖𝑖 where Rij is the preference rating of the ith respondent for the jth profile; P1j and P2j are two dichotomous variables to represent production type through effect coding; LOj, OCj, and REj are dichotomous variables for localness, organic certification, and renewable energy use, respectively; PRj is a continuous variable for price; a0 is the intercept; a1–a6 are the coefficients to be estimated; and eii is the error term. As identified in Table 1, the production type is coded using effect coding through two dichotomous variables (P1 and P2). Specifically, P1 equals 1 for farmstead, 0 for artisan, and –1 for commodity, while P2 equals 0 for farmstead, 1 for artisan, and –1 for commodity cheese. Results and Discussion

This section presents the empirical results of the conjoint analysis and discusses the major findings. Market Segmentation

Preliminary analysis of the 4,500 observations in the dataset indicated a very limited association between the preference rating and the five cheese attributes. This finding was quite different from our research hypothesis, which was based on the consumer preference theory and findings from previous studies. One possible reason for this lack of close association for the whole sample was that the respondents might be from different groups or clusters defined by certain characteristics or preferences. Cluster analysis confirmed that the respondents were likely from two groups: one group with strong preferences for quality attributes and the other group with a strong preference for a low price.

The analysis of consumer preferences through a survey relies on a representative sample of the study population. However, when the sample is not from a homogenous population, the analysis based on the sample data can be subject to many problems. For example, in a study of consumer preference for cars, if the sample includes one group or segment that prefers large cars and another group or segment that prefers small cars, the aggregate analysis based on the sample data may suggest a preference for medium cars, which does not accurately represent the views of the individuals in the sample (Stoker 1993). In such a situation, cluster analysis should be used to

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

24

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

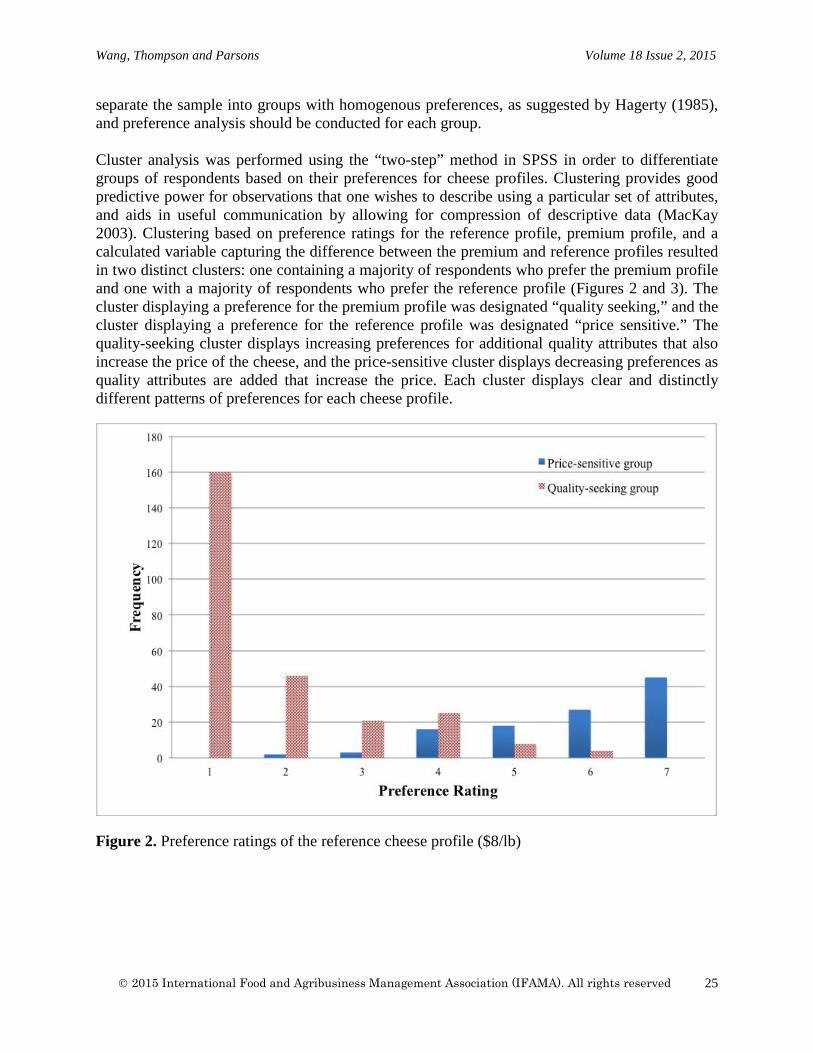

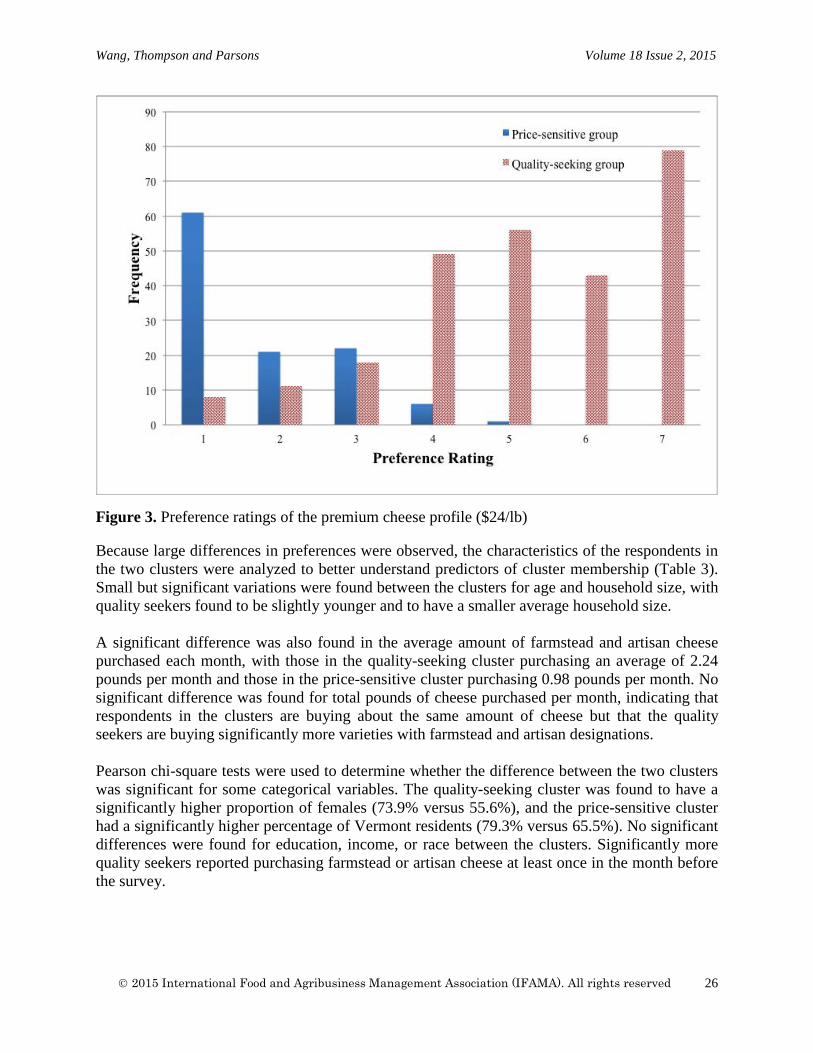

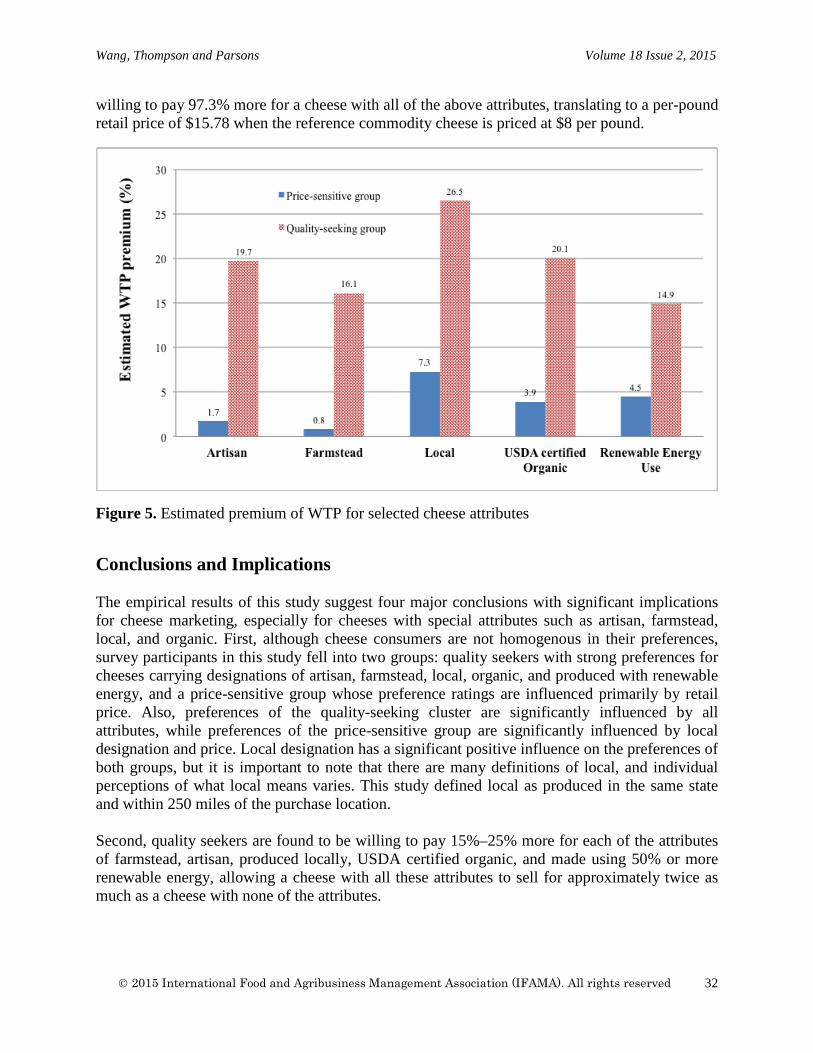

separate the sample into groups with homogenous preferences, as suggested by Hagerty (1985), and preference analysis should be conducted for each group. Cluster analysis was performed using the “two-step” method in SPSS in order to differentiate groups of respondents based on their preferences for cheese profiles. Clustering provides good predictive power for observations that one wishes to describe using a particular set of attributes, and aids in useful communication by allowing for compression of descriptive data (MacKay 2003). Clustering based on preference ratings for the reference profile, premium profile, and a calculated variable capturing the difference between the premium and reference profiles resulted in two distinct clusters: one containing a majority of respondents who prefer the premium profile and one with a majority of respondents who prefer the reference profile (Figures 2 and 3). The cluster displaying a preference for the premium profile was designated “quality seeking,” and the cluster displaying a preference for the reference profile was designated “price sensitive.” The quality-seeking cluster displays increasing preferences for additional quality attributes that also increase the price of the cheese, and the price-sensitive cluster displays decreasing preferences as quality attributes are added that increase the price. Each cluster displays clear and distinctly different patterns of preferences for each cheese profile.

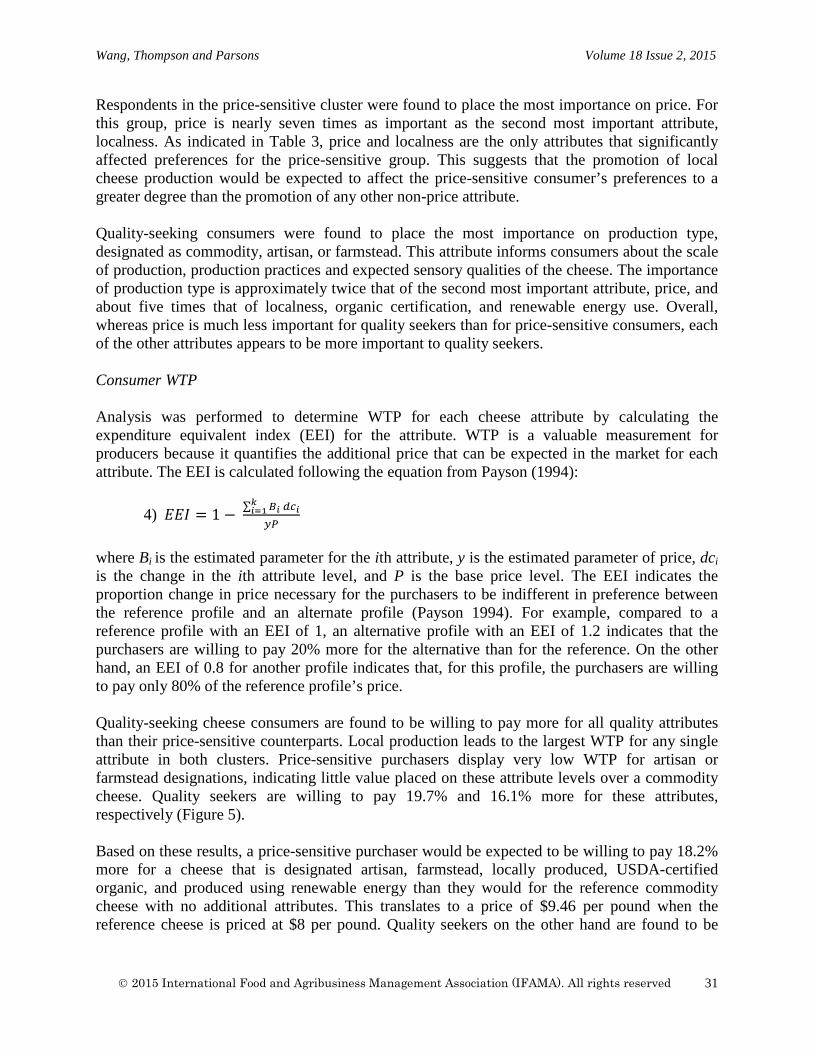

Figure 2. Preference ratings of the reference cheese profile ($8/lb)

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

25

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

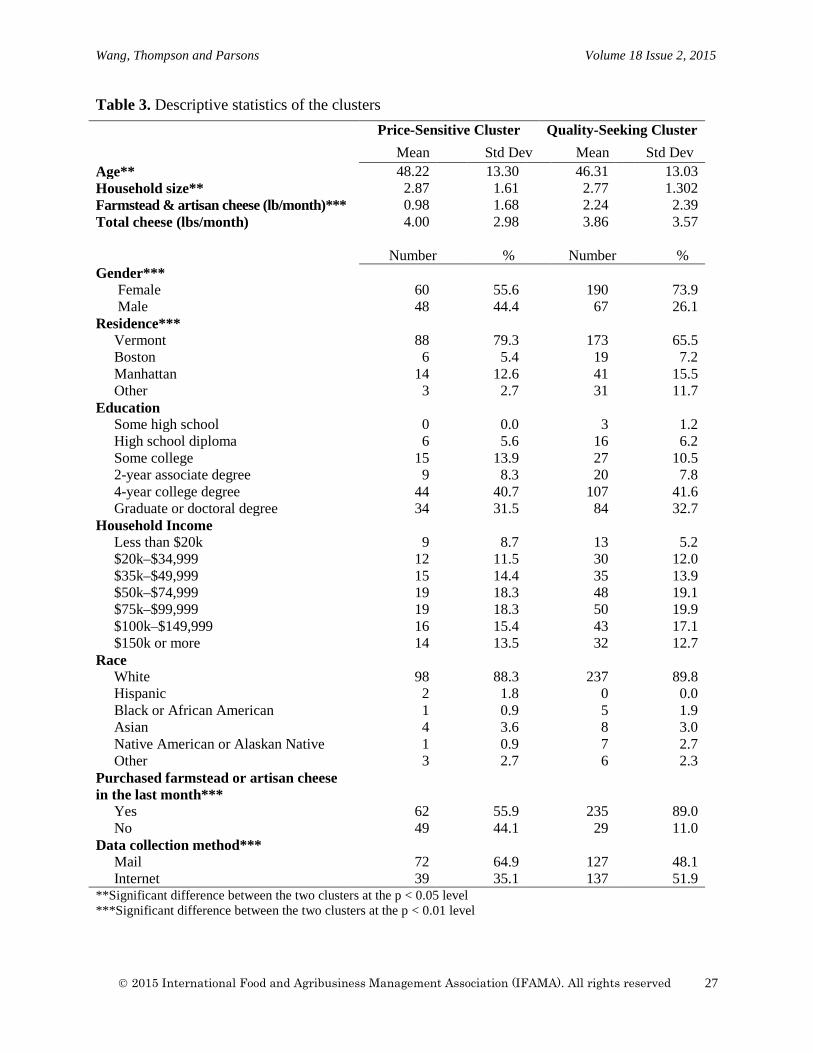

Figure 3. Preference ratings of the premium cheese profile ($24/lb) Because large differences in preferences were observed, the characteristics of the respondents in the two clusters were analyzed to better understand predictors of cluster membership (Table 3). Small but significant variations were found between the clusters for age and household size, with quality seekers found to be slightly younger and to have a smaller average household size.

A significant difference was also found in the average amount of farmstead and artisan cheese purchased each month, with those in the quality-seeking cluster purchasing an average of 2.24 pounds per month and those in the price-sensitive cluster purchasing 0.98 pounds per month. No significant difference was found for total pounds of cheese purchased per month, indicating that respondents in the clusters are buying about the same amount of cheese but that the quality seekers are buying significantly more varieties with farmstead and artisan designations.

Pearson chi-square tests were used to determine whether the difference between the two clusters was significant for some categorical variables. The quality-seeking cluster was found to have a significantly higher proportion of females (73.9% versus 55.6%), and the price-sensitive cluster had a significantly higher percentage of Vermont residents (79.3% versus 65.5%). No significant differences were found for education, income, or race between the clusters. Significantly more quality seekers reported purchasing farmstead or artisan cheese at least once in the month before the survey.

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

26

Wang, Thompson and Parsons Volume 18 Issue 2, 2015

Table 3. Descriptive statistics of the clusters

Price-Sensitive Cluster Quality-Seeking Cluster Mean Std Dev Mean Std Dev Age** 48.22 13.30 46.31 13.03 Household size** 2.87 1.61 2.77 1.302 Farmstead & artisan cheese (lb/month)*** 0.98 1.68 2.24 2.39 Total cheese (lbs/month) 4.00 2.98 3.86 3.57 Number % Number % Gender*** Female 60 55.6 190 73.9 Male 48 44.4 67 26.1 Residence*** Vermont 88 79.3 173 65.5

Boston 6 5.4 19 7.2

Manhattan 14 12.6 41 15.5

Other 3 2.7 31 11.7 Education Some high school 0 0.0 3 1.2 High school diploma 6 5.6 16 6.2 Some college 15 13.9 27 10.5 2-year associate degree 9 8.3 20 7.8 4-year college degree 44 40.7 107 41.6 Graduate or doctoral degree 34 31.5 84 32.7 Household Income Less than $20k 9 8.7 13 5.2 $20k–$34,999 12 11.5 30 12.0 $35k–$49,999 15 14.4 35 13.9 $50k–$74,999 19 18.3 48 19.1 $75k–$99,999 19 18.3 50 19.9 $100k–$149,999 16 15.4 43 17.1 $150k or more 14 13.5 32 12.7 Race White 98 88.3 237 89.8 Hispanic 2 1.8 0 0.0 Black or African American 1 0.9 5 1.9 Asian 4 3.6 8 3.0 Native American or Alaskan Native 1 0.9 7 2.7 Other 3 2.7 6 2.3 Purchased farmstead or artisan cheese in the last month***

Yes 62 55.9 235 89.0 No 49 44.1 29 11.0 Data collection method*** Mail 72 64.9 127 48.1 Internet 39 35.1 137 51.9 **Significant difference between the two clusters at the p < 0.05 level ***Significant difference between the two clusters at the p < 0.01 level

2015 International Food and Agribusiness Management Association (IFAMA). All rights reserved

27

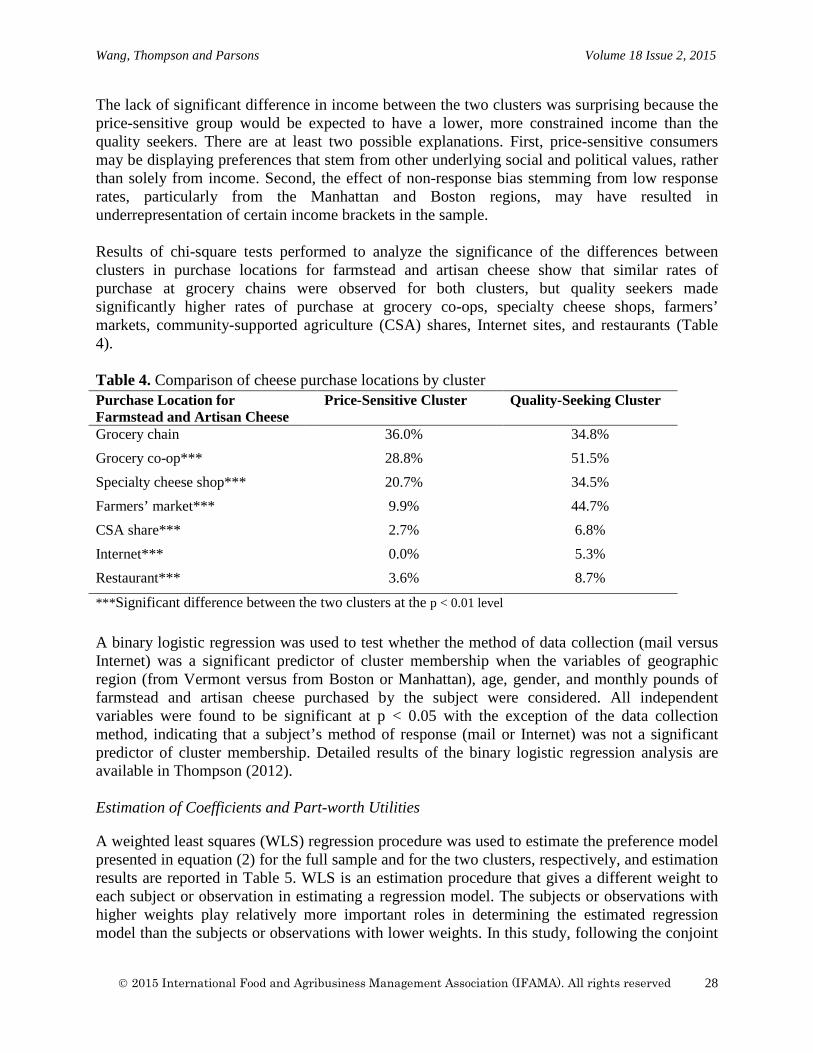

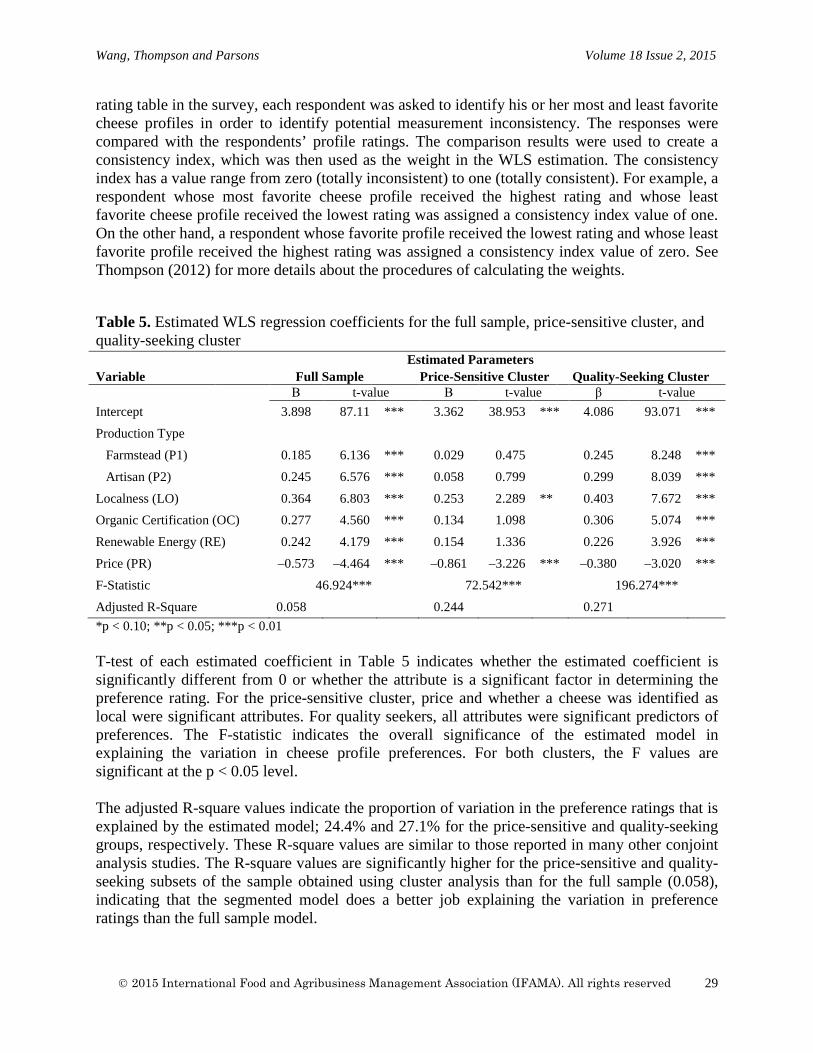

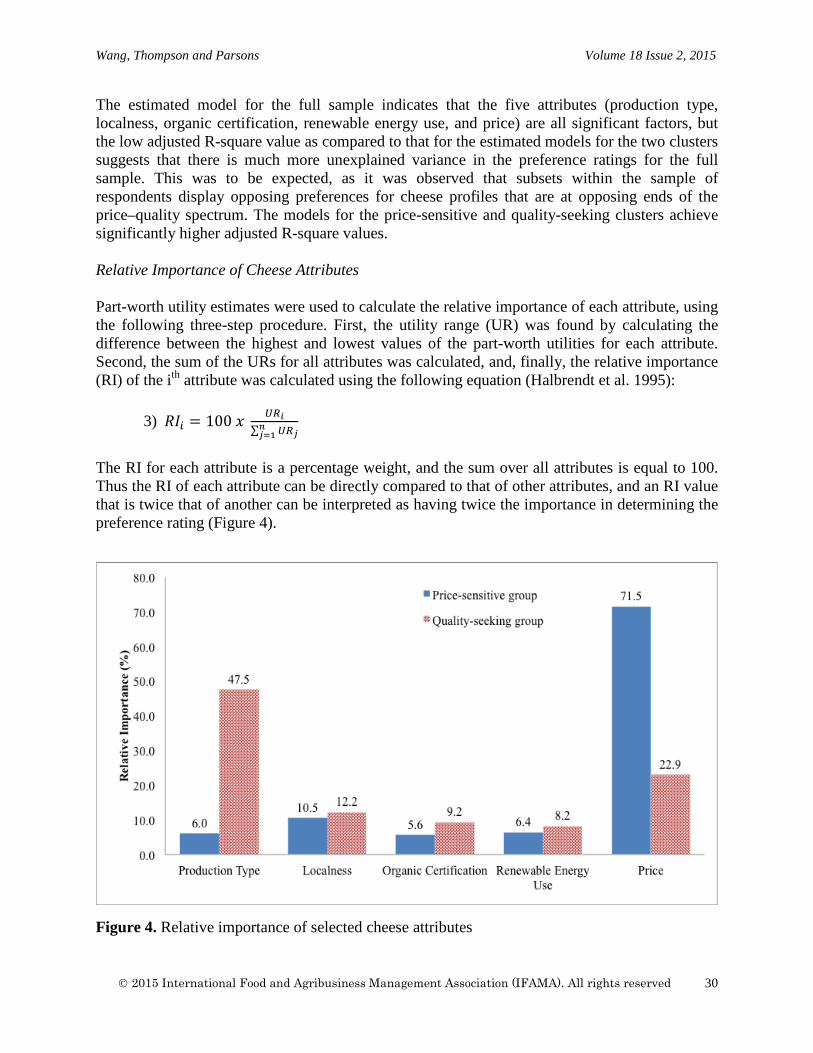

Wang, Thompson and Parsons Volume 18 Issue 2, 2015