Embed Size (px)

Citation preview

perspectives on the risks that will determine your company’s future

the oliver wyman

RISK jouRnalvolume 1

1RISK JOURNAL

Complex risks increasingly define the global

competitive landscape. Volatile commodity

prices, recent political unrest in the Middle

East and Japan’s earthquake all underscore how the pace, scale and impact of risks are increasing. In many

ways, rapidly changing risks put on hold by the financial crisis are returning with a vengeance, as reflected

in commodity prices that have rebounded back to the historical highs they first reached in 2008. While not

all of these prices may spike up much further, it’s clear their volatility will continue and possibly even

increase, creating new threats and opportunities for companies across the board. Companies can develop a

significant competitive advantage if senior executives make risk-adjusted decisions and anticipate how

these risks will reshape their industries. For this reason, it has never been more important for senior

executives to consider how they will respond to risks and their knock-on effects.

In recognition of this new reality, we are pleased to introduce our inaugural edition of the Oliver Wyman

Risk Journal. This publication is a collection of perspectives on what we consider to be key risks that will

determine many companies’ futures. Oliver Wyman’s Global Risk & Trading practice is launching this publi-

cation, which includes contributions from many different parts of the organization. It reflects our firm’s

broad expertise in risk management as well as the research we produce with the Oliver Wyman Global Risk

Center and top professional associations, non-governmental organizations and academic institutions on

issues that involve multiple industries and countries.

Many of the topics in this journal are intensely urgent. Our issue opens with a discussion of how volatile

commodity prices are rewriting the rules of industries ranging from airlines to food manufacturers by intro-

ducing unpredictability in their earnings. We then examine how commodity trading paradigms must

change—and swiftly—if trading organizations hope to benefit from the return of volatility to the markets.

Other stories explore how companies can better prepare for a number of other significant risks, such as

supply chain disruptions and information technology failures, or emerging risks that may initially appear

unrelated to a company’s business until an unanticipated event occurs. We also examine the difficult

trade-offs that countries and companies face when they pursue clean energy, the risks inherent in large

investment projects and a fundamental reason why banks still struggle to achieve their financial goals—

the data on which they base decisions is often faulty.

In each case, the authors offer practical advice on how to tackle trends that are increasingly redefining the

rules for business. Our goal is for these articles to inform as well as to provoke a reexamination of how your

organization conducts risk-adjusted decision making. I hope you will enjoy reading these perspectives and

that this publication will spark some interesting thoughts along these themes that we can discuss.

Roland O. Rechtsteiner

Managing Partner

Global Risk & Trading Practice

IntroductIon

2 RISK JOURNAL

VOlatile COmmOdity PRiCes

4 Volatile commodity prices should be on the CEO’s radar screen John drzik

8 Volatile agricultural prices are rewriting the rules for the food industry michael denton, mark Robson, alex Wittenberg

14 Airlines need a new game plan for hedging fuels – now Cantekin dincerler, mark Robson

Changing tRading PaRadigms

18 How to overcome implementation risks when setting up a new commodity trading business Cantekin dincerler, ernst Frankl, Roland Rechtsteiner

26 Why traders need more comprehensive risk and pricing frameworks in a fundamentally changed business environment michael denton, alexander Franke, Christian lins

34 Six lessons for commodity traders from the tragic events in Japan alexander Franke, Boris galonske, Christian lins

contents

3RISK JOURNAL

eneRgy sustainaBility

40 What country leads the world in providing stable, affordable and clean energy? The answer is that no one does. And that’s a problem John drzik

suPPly Chain disRuPtiOns

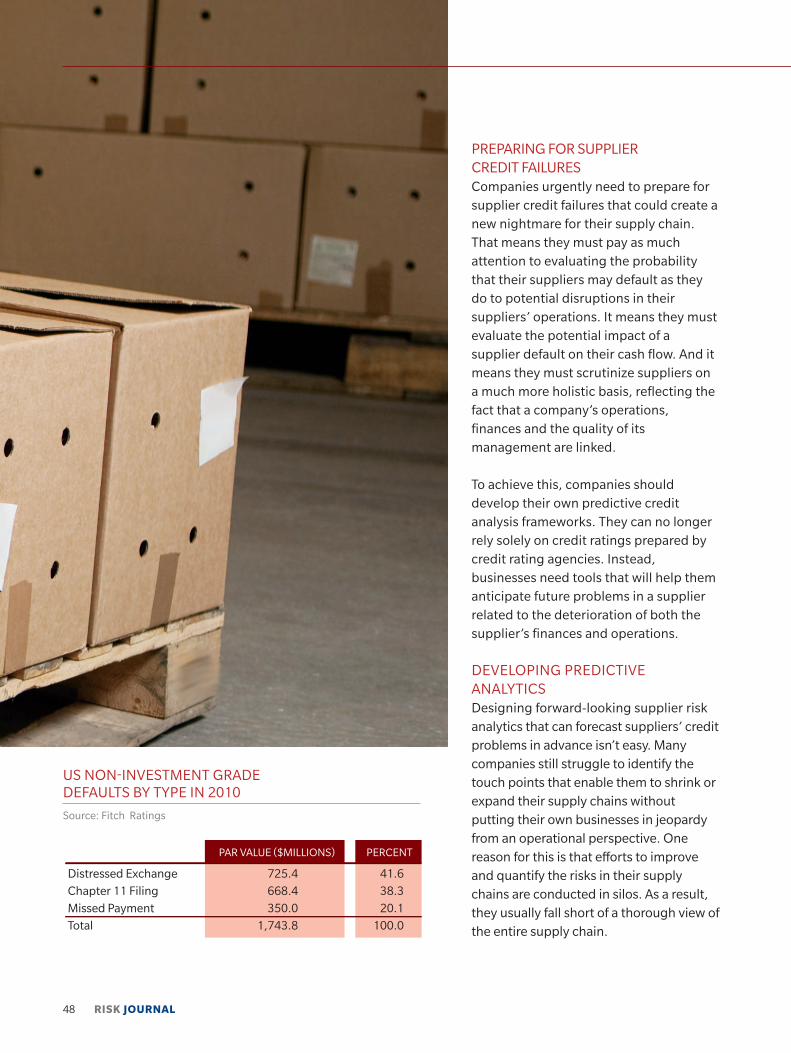

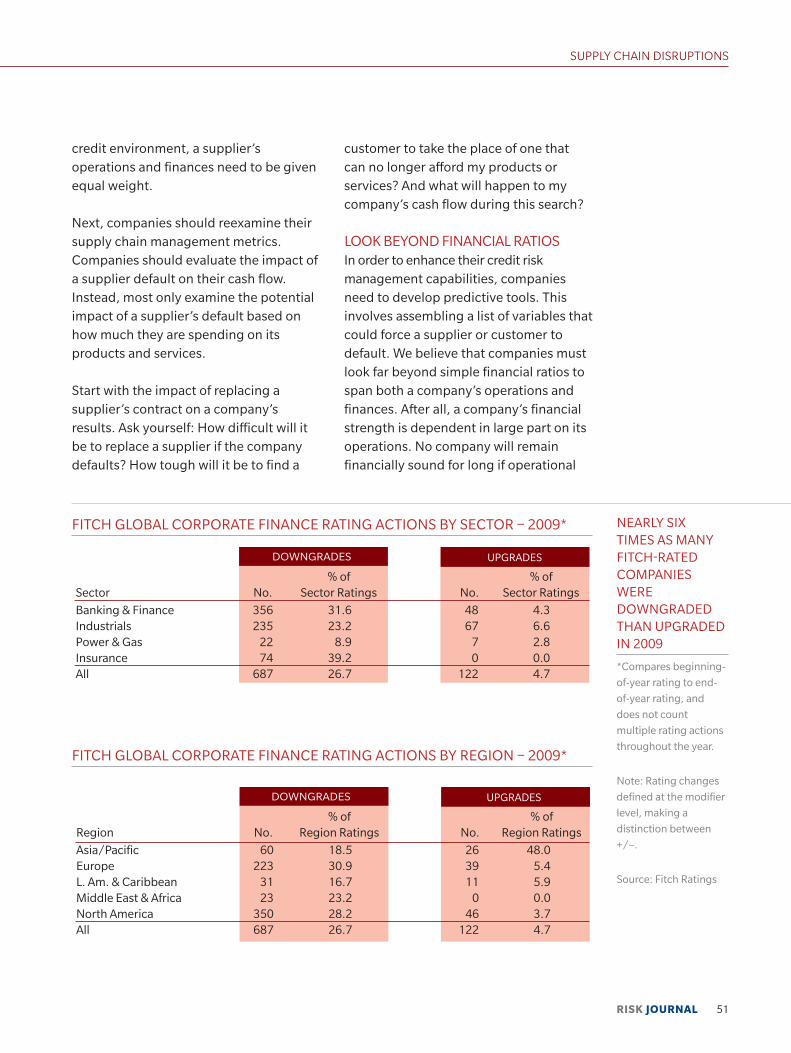

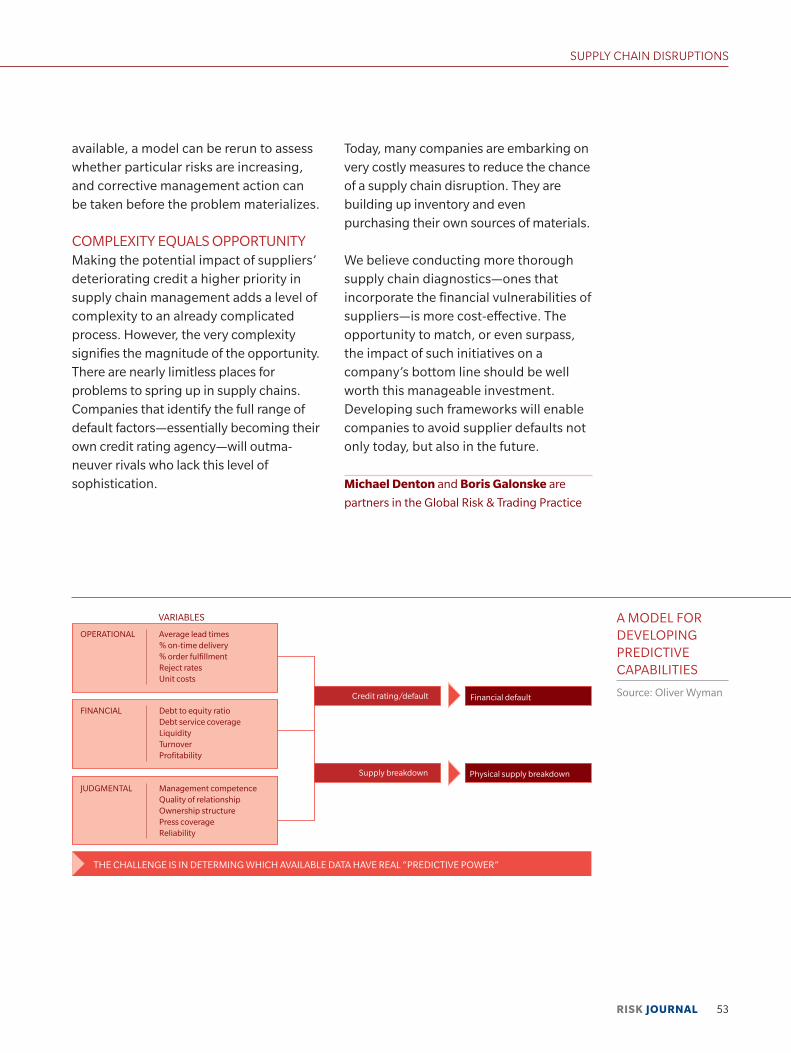

46 Why companies need to behave more like their own credit rating agencies michael denton, Boris galonske

emeRging Risks

54 Companies need to improve their ability to identify and prepare for emerging risks

alex Wittenberg

inFORmatiOn teChnOlOgy FailuRes

60 A new framework for boards of directors to manage IT risks Jonathan Cohn, mark Robson

mismanaged laRge PROJeCts

68 The “missing link” in infrastructure finance John larew, mark Robson

FinanCial Risks

74 Why do banks still struggle to achieve their financial goals? The data on which they base decisions is seriously flawed James mackintosh, Paul mee

4 Risk JOuRnal

COmmOdities Hot

John drzik

volatIle commodIty prIces sHould be on tHe

ceo’s radar screen

5Risk JOuRnal

Japan’s nuclear crisis and political unrest in the middle east have triggered price spikes and supply disruptions in everything from oil to wheat to gold. it might be tempting to view these recent price swings as a temporary phenomenon. they’re not. they are the new normal.

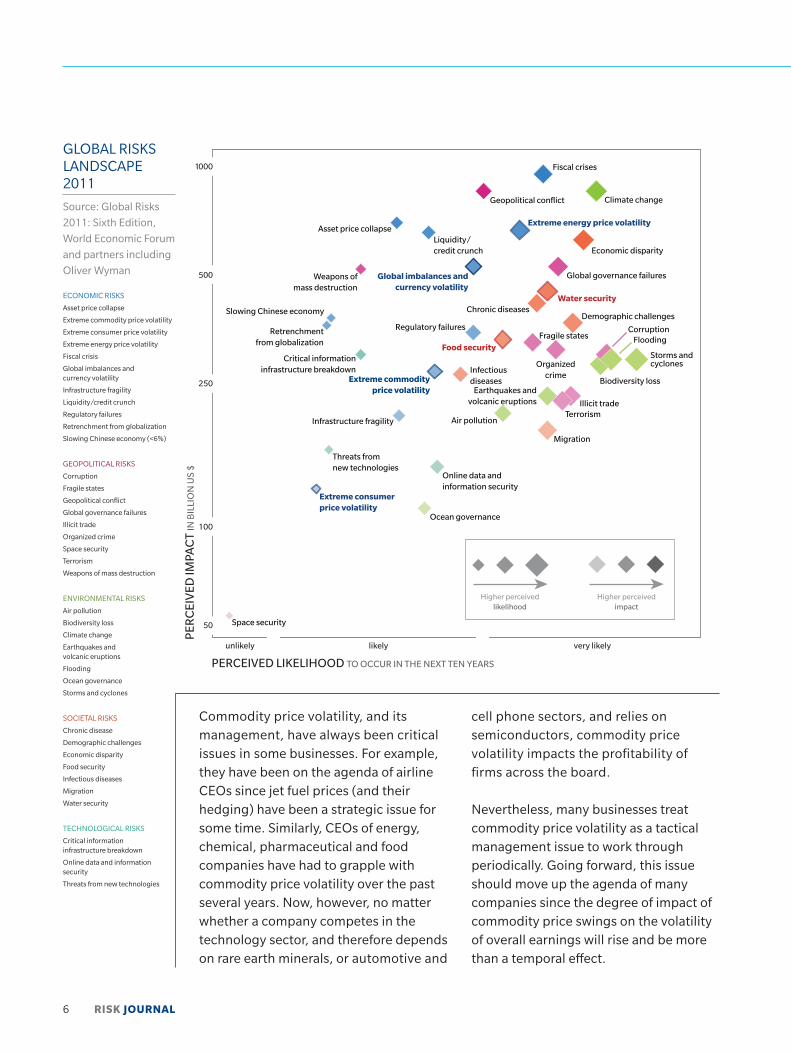

Changes in both supply and demand dynamics are likely to create a long period of sustained commodity price volatility, with significant downstream implications for many businesses. The recent Global Risks 2011 report published by the World Economic Forum with partners including Oliver Wyman revealed that 580 experts, business leaders and policy makers believe it is likely the world will experience extremely volatile energy prices, commodity prices and consumer prices in the next ten years.

There are a number of structural reasons for the sustained increase in commodity price volatility. Global demand for commodities such as food and energy will grow at a double-digit rate over the next decade due to population growth and increases in per capita usage driven by economic development. This rising demand will likely fuel investment in commodity extraction, encouraging players in these businesses to consider increasingly risky projects that will be more prone to disruption.

Supply disruptions will also be more frequent due to changing climate patterns and the increasing number and magnitude of extreme weather events that they will cause. Floods, droughts, hurricanes and many other types of extreme weather events are all projected to increase in the next decade. Shortages in some regions will likely be further exacerbated by a rising number of governments taking unilateral actions to cope with their scarcity of resources. In the last twelve months alone, Russia, Pakistan, India and Vietnam have all restricted exports of agricultural commodities ranging from grain to cotton to rice.

Further price swings might also be created by political choices related to the trade-offs inherent in addressing interconnected resource shortages. For example, the International Energy Agency predicts the globe will need 3.2 million barrels per day of biofuels to meet policy incentives related to reducing vehicle emissions. However, producing those fuels could amplify food shortages and put further pressure on water shortages as well. The range of geopolitical and environmental uncer-tainties surrounding commodity supply will also likely fuel financial speculation in commodities—amplifying price volatilities even further.

volatIle commodIty prIces

$1 trillionHow much more

companies and

consumers will

need to pay for

oil in 2011 if us

oil contracts

remain at $110

per barrel

6 RISK JOURNAL

PER

CEI

VED

IMPA

CT

IN B

ILLI

ON

US

$

PERCEIVED LIKELIHOOD TO OCCUR IN THE NEXT TEN YEARS

ECONOMIC RISKS

Asset price collapse

Extreme commodity price volatility

Extreme consumer price volatility

Extreme energy price volatility

Fiscal crisis

Global imbalances and currency volatility

Infrastructure fragility

Liquidity/credit crunch

Regulatory failures

Retrenchment from globalization

Slowing Chinese economy (<6%)

GEOPOLITICAL RISKS

Corruption

Fragile states

Geopolitical conflict

Global governance failures

Illicit trade

Organized crime

Space security

Terrorism

Weapons of mass destruction

ENVIRONMENTAL RISKS

Air pollution

Biodiversity loss

Climate change

Earthquakes and volcanic eruptions

Flooding

Ocean governance

Storms and cyclones

SOCIETAL RISKS

Chronic disease

Demographic challenges

Economic disparity

Food security

Infectious diseases

Migration

Water security

TECHNOLOGICAL RISKS

Critical informationinfrastructure breakdown

Online data and information security

Threats from new technologies

unlikely likely very likely

1000

500

250

100

50 Space security

Extreme consumerprice volatility

Threats from new technologies

Ocean governance

Online data andinformation security

Infrastructure fragility

Global governance failures

Economic disparity

Extreme energy price volatility

Climate changeGeopolitical conflict

Fiscal crises

Migration

Air pollution

Critical informationinfrastructure breakdown

Slowing Chinese economy

Weapons ofmass destruction

Regulatory failures

Food security

Retrenchmentfrom globalization

Extreme commodityprice volatility

Infectious diseases

Earthquakes andvolcanic eruptions

Storms andcyclones

Biodiversity loss

Flooding

TerrorismIllicit trade

Corruption

Organizedcrime

Fragile states

Demographic challengesChronic diseases

Water security

Global imbalances andcurrency volatility

Liquidity/ credit crunch

Asset price collapse

Higher perceivedlikelihood

Higher perceivedimpact

GlObAl RISkS lAndSCAPE 2011

Source: Global Risks

2011: Sixth Edition,

World Economic Forum

and partners including

Oliver Wyman

Commodity price volatility, and its management, have always been critical issues in some businesses. For example, they have been on the agenda of airline CEOs since jet fuel prices (and their hedging) have been a strategic issue for some time. Similarly, CEOs of energy, chemical, pharmaceutical and food companies have had to grapple with commodity price volatility over the past several years. now, however, no matter whether a company competes in the technology sector, and therefore depends on rare earth minerals, or automotive and

cell phone sectors, and relies on semiconductors, commodity price volatility impacts the profitability of firms across the board.

nevertheless, many businesses treat commodity price volatility as a tactical management issue to work through periodically. Going forward, this issue should move up the agenda of many companies since the degree of impact of commodity price swings on the volatility of overall earnings will rise and be more than a temporal effect.

7RISK JOURNAL

The stakes are rising. Consider: On April 7, US oil contracts exceeded $110 per barrel for the first time in two and a half years. If oil prices remain at that level, we estimate that companies and consumers will need to figure out a way to pay $1 trillion more for oil this year than they did in 2010. but that estimate just scratches the surface of the costs that companies and consumers will need to bear since there have been recent increases in the prices of many other commodities as well.

As a result, businesses ranging from manufacturers to retailers to bakers are all struggling to manage the volatility that raw material prices are introducing into their earnings. Some are discovering that the cost of their electricity supply, for example, is becoming a core driver of their earnings. Others are being forced to renegotiate contracts with their suppliers—if they don’t accept higher prices, their suppliers are at risk of going bankrupt as they are paying much higher prices for raw materials.

CEOs need to determine the degree to which taking commodity price risk fits with their risk appetite and shareholder expectations. It might be that their investors expect the company to have this risk, and fully expect to see the resulting increase in earnings volatility that stems from increasing commodity price swings. However, it might also be that the bet investors are making on the company lies in other factors, such as superior opera-tional management or customer distri-bution. In these businesses, CEOs will likely want to mitigate the effect of commodity price swings on earnings.

These companies need either to invest in the risk management capabilities necessary to manage through a long-term pattern of heightened commodity price volatility or to redefine their business models (for example, through supplier contract structures) so they are not directly exposed to the risk. Separately, all companies should consider investing in methods and technologies that ensure more effective and efficient usage of resources and commodities to reduce their overall exposure to volatile prices.

We are entering a new age of commodity price volatility, likely to extend for ten years or more. The impact on the earnings volatility of many companies is likely to be substantial and sustained—resulting in a meaningful effect on shareholder returns. These companies need to consider whether they change their business model or management approach or both to align their commodity risk exposure to their risk appetite. CEOs should have this issue on their radar screen and take the lead in arriving at an answer.

John drzik is the CEO of Oliver Wyman Group

It is likely the world will experience extremely volatile energy prices, commodity prices and consumer prices in the next ten years Global Risks 2011: Sixth Edition

volatIle commodIty prIces

sePaRating the Wheat

8 Risk JOuRnal

from tHe cHaff

9Risk JOuRnal

michael dentonmark robsonalex Wittenberg

volatIle agrIcultural prIces are reWrItIng tHe rules for

tHe food Industry

First, wildfires damaged wheat crops in Russia, prompting the government to ban exports. next, heavy rains reduced Canada’s wheat crop outlook to its lowest level since 2002. then, massive floods in Pakistan threatened to turn asia’s

third-largest wheat producer from a wheat exporter to a net importer.

Growing concerns about wheat shortages worldwide are sending prices soaring. So far, these price spikes are not as dramatic as those experienced in 2008, which triggered bread riots in Pakistan and Egypt. And some analysts have started to openly question the validity of current fears about a return of food price inflation.

Regardless of whether wheat prices correct, it is clear that agricultural prices have entered a new age of volatility. Food companies, ranging from processors to manufacturers to restaurants, need to better prepare for a new market reality in which ingredient prices will increasingly impact their earnings.

For much of the second half of the 20th century, agricultural prices declined fairly steadily. In more recent years, many have tripled and remained at a high level over several seasons. In 2010, wheat prices jumped roughly 50 percent. Volatility more than tripled to 62 percent in the third quarter of 2010.

We believe such sudden shifts in agricultural prices are here to stay for several reasons. First, the global demand for food is increasing. As populations grow and become more affluent, people are consuming more protein and processed food.

volatIle commodIty prIces

10 RISK JOURNAL

Second, the frequency of agricultural shocks has been rising as the number of extreme weather events has tripled since 1980, according to reinsurer Munich Re. devastating floods in Pakistan damaged an estimated $1 billion of crops and left millions of people without food, shelter and water.

Finally, fluctuating agricultural prices are attracting financial trading participants who are contributing to unpredictable price movements. For example, british financier Anthony Ward helped send cocoa prices to their highest level since 1977 in July of 2010 by holding 241,000 tons of cocoa, according to the Wall Street Journal.

The potential impact of sharp swings in ingredient prices on the food industry is significant. If wheat prices remain at the level they reached in the second half of 2010, food companies will have to absorb an additional $2 billion in costs on an annual basis or pass them on to

customers. Since the sluggish global recovery makes it difficult to pass on a large portion of this cost to consumers, higher wheat prices could put a significant strain on some food companies’ working capital and margins. They may also drive more consumers to less expensive substitutes like private label products.

A reversal in wheat prices could create a whole new set of problems. Many companies have been benefiting from systematically buying a fraction of their future grain consumption for 12 to 24 months in the future. by buying far ahead in a slowly rising market, their actual costs have tended to be lower than the alternative of buying a full month’s supply at today’s higher prices. but that strategy will no longer work when the markets correct.

Food companies need to develop more sophisticated cost and margin

nATURAl CATASTROPHES ARE InCREASInG

Updated value due to

reanalysis of March 31,

1973, thunderstorm

event in Georgia and

South Carolina. The

previous economic loss

value for the 1970-

1979 period was

US$ 52 billion.

Source: Munich RE

0

10

20

30

40

50

60

1950-1959 1960-1969 1970-1979 1980-1989 1990-1999 2000-20090

50

100

150

200

250

300

350

400

EVENTS

EVEN

TS

ECONOMIC LOSSES

ECO

NO

MIC

LO

SSES

($B

ILLI

ON

S)

11RISK JOURNAL

WHEAT PRICES ARE SOARInG

Source: bloomberg

volatIle commodIty prIces

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

2/8

/00

10

/8/0

0

6/8

/01

2/8

/02

10

/8/0

2

6/8

/03

2/8

/04

10

/8/0

4

6/8

/05

2/8

/06

10

/8/0

6

6/8

/07

2/8

/08

10

/8/0

8

6/8

/09

2/8

/10

10

/8/1

0

PRICE ($/BU)

ANNUALIZED VOLATILITY

management capabilities to cope with agricultural price swings over the long term. Here are five ways your company can gain a competitive edge by limiting the impact of volatile agricultural prices on your results:

1) REExAMInE yOUR RISk AnAlyTICS Wheat flour accounts for as much as 30 percent of the cost of producing baked products like bread and cereal. And yet, food companies devote substantially more resources to managing changes in consumer behavior than they do to price shifts in key ingredients.

Savvy food companies should take advantage of this disconnect by developing decision frameworks to help reduce the impact of one of the most significant causes of uncertainty in their results—volatile raw material prices. looked at another way, agricultural price fluctuations have become a key lever to

stabilize profits. Food companies should consistently trace and review how highly variable ingredient costs reduce, or increase, profit margins. A well-defined decision framework includes both a recommendation based on evolving global market conditions and a playbook that defines the conditions under which a decision will be revisited.

2) THInk MORE lIkE A TRAdER Many food companies passively hold call options that protect them from price spikes until maturity because they mistakenly believe they are behaving like speculators if they unwind a hedging instrument earlier. In fact, restructuring a trade is often the most prudent step a company can take to achieve its commodity price risk management goal. Studies show that 70 percent of options turn out to be worthless once they expire. Food companies should regularly reevaluate whether earlier hedging trans-actions are still reducing the risk created

12 RISK JOURNAL

4) SCRUTInIzE yOUR EnTIRE SUPPly CHAIn Companies need to constantly reevaluate the earnings impact of formerly uncor-related prices of crops moving in lockstep, or if an entirely different class of commodity—like oil or natural gas—suddenly decouples. As the wheat crisis illustrates, that calculation is becoming much more complicated. The price of oats has already become more correlated with wheat because they are both grown primarily in Russia and Canada. At the same time, wheat prices have decoupled from the prices of other crops that are usually correlated like corn and soybeans.

5) InClUdE THE IMPOSSIblE In yOUR STRESS TESTInG It has become more crucial than ever for food companies to analyze if their products will remain price competitive even under new and unfamiliar conditions, especially given the rise of extreme weather events. Food manufacturers need to examine how immediate and longer-term commodity price shifts will impact their margins in a wide range of scenarios on both a hedged and unhedged basis. They should also consider the potential impact of events that are both historical and hypothetical across a broad range of commodity classes. Equally important, they need to scrutinize how macroeconomic events and funda-mental changes in the food industry, such as the growing popularity of private label products, could alter their results.

by agricultural price volatility in the current market. If not, they need to re-balance their portfolios.

3) ExPlORE AlTERnATIVE WAyS TO STAbIlIzE THE COST OF kEy InGREdIEnTS As agricultural price shifts increasingly create uncertainty in food manufacturers’ earnings, companies need to consider adopting measures beyond financial hedging instruments to lessen their impact. For example, they should explore alternative ways of acquiring supplies at a stable cost, such as long-term purchase arrangements that use a combination of fixed and indexed prices. Some food manufacturers, like nestlé, are even training farmers to grow coffee and supplying them with coffee trees. To be effective, companies must simulta-neously establish regular communication across departments ranging from procurement to treasury so that senior managers can evaluate if the organiza-tion’s entire range of commodity price risk management practices fits with its corporate objectives.

$2 billionthe additional

amount of

money food

companies

may have to

absorb in

extra costs

13RISK JOURNAL

As has occurred in the markets for energy, metals and minerals, the agricultural markets have permanently and funda-mentally changed. large agricultural price swings could potentially hurt unprepared food companies’ earnings and force them to make difficult trade-offs. Instead, they should build up the risk management capabilities that will allow them to effec-tively manage sharp shifts in the prices of key agricultural commodities like wheat.

michael denton, mark Robson and alex

Wittenberg are partners in the Global Risk

& Trading Practice

volatIle commodIty prIces

It is more crucial than ever for food companies to analyze if their products will remain price competitive even under new and unfamiliar conditions

14 Risk JOuRnal

starIng Into tHe eye of the stORm

cantekin dincerler mark robson

aIrlInes need a neW game plan for

HedgIng fuels - noW

15Risk JOuRnal

It may seem like a distant memory, but major airlines lost an estimated $8 billion on their jet fuel hedges in 2009. as crude oil prices spiked, tumbled, and then doubled back to about $70 per barrel, we estimate such hedges soared to become more than half of top airlines’ total

losses. after a period of minimal volatility, large fuel price swings are once again returning. the only question is which airlines will emerge from the turbulence in the strongest position.

The main reason why airlines are once again experiencing larger fuel price fluctuations is that energy markets have fundamentally and permanently changed. Jet fuel prices will continue to be volatile in nature in part because demand for all refined petroleum products often outstrips supply. Oil drilling has become more problematic and politicized just when fast-growing countries like India and China use more fuel than ever.

Complicating matters, energy trading participants like investment banks and hedge funds who benefit from fuel price swings are contributing to their unpredictability. To curb trading activities, the US Congress has passed financial legislation that will limit the size of trades for anyone not hedging fuel with the intent of actually using it. but banks and hedge funds will remain significant players.

Given the speed at which fuel prices are shifting, airlines should not be tempted into thinking this new law will solve many of their fuel hedging problems. Consider: Traditionally, jet fuel prices have appreciated by about 5 percent annually. Today, they move by that much on a weekly basis.

Most airlines are poorly equipped to respond to such price swings. After being blindsided by fuel price spikes in the last couple of years, many have imple-mented rigid and programmatic hedging strategies determined on an annual basis. Some airlines have abandoned hedging jet fuel prices altogether.

There is a better approach. now is the perfect opportunity for airlines to invest in fuel hedging programs and capabilities that can mitigate the instability jet fuel prices introduce into their earnings. Jet fuel is one of the largest expenses for many airlines and now accounts for about 25 percent of airlines’ total costs. Carriers have already extensively managed to lower labor, maintenance and other operation costs. As a result, fuel is arguably one of their largest unresolved risks. The amount of margin—or collateral—that airlines must deposit with counter-parties to carry out fuel hedges can put a strain on working capital that otherwise could be used for other parts of their operations. yet airlines employ many more full-time employees to handle the risk of potential operational problems than they do to control risks created by volatile jet fuel prices.

volatIle commodIty prIces

16 RISK JOURNAL

recommended buying shares in Asian airlines in part because these airlines are expected to increase their fuel hedging positions with lower risk profiles.

The critical first step for an airline to steady its fuel hedge positions is for it to develop a set of analytics that make regularly evaluating fuel hedging recommendations manageable. Such tools rapidly process a wide range of data to truly capture the jet fuel market’s dynamics. Savvy airlines base hedging recommendations on fast-changing information available in jet fuel research like Jet Fuel Intelligence newsletters, ARGUS International papers and industry analyst reports. In addition, they examine thousands of potential scenarios involving risks like fuel price spikes that collapse immediately and the sudden decoupling of traditionally correlated currencies and energy prices.

Most software programs designed to calculate an energy portfolio’s total value at risk cannot currently take such a wide

Some airlines recognize that introducing more sophisticated fuel hedging capabilities will distinguish them from their competitors. One airline recently built up a substantial energy trading team and invested in its own jet fuel storage so that it can supply fuel to other airlines. by doing so, the airline not only gains better visibility into what its fuel will cost, but also can potentially reduce the total into-wing expense.

Other stakeholders are placing a greater value on airlines’ fuel hedging capabilities as well. In May of 2010, Morgan Stanley

now is the perfect opportunity for airlines to invest

in fuel hedging programs and capabilities that can mitigate

the instability jet fuel prices introduce into their earnings

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

4/2/90 10/3/93 4/5/97 10/6/00 4/8/04 10/10/07 4/12/11

DO

LLA

RS

PER

GA

LLO

N

lARGE FUEl PRICE SWInGS ARE RETURnInG

Source: U.S. Energy

Information

Administration

17RISK JOURNAL

variety of factors into account. They are also designed only to monitor risks—not to form a strategy based upon them. As a result, hedging strategies developed using these tools often provide protection in some scenarios but cause significant fuel hedging losses in many others. by examining a much broader spectrum of issues in 2008, Oliver Wyman was able to design a framework that allowed one airline to meet its fuel hedging objectives in a much wider range of potential scenarios. It also reduced the volatility in the airline’s energy portfolio in a cost-effective manner.

For these tools to be effective, airlines must also introduce the appropriate infra-structure to conduct deep reviews of hedging recommendations on at least a monthly basis. Following a hedging strategy set at one particular point in time will not fix a fuel hedging portfolio’s problems. In fact, that may create more difficulties.

Carriers need to determine what type of hedging transaction makes the most sense for their portfolio at any given moment. Instead of pursuing trans-actions without upfront fees, they may need to use more sophisticated hedging instruments with upfront costs to protect them against the potential downside in their earnings resulting from the cost of fuel or hedge settlements. One way airlines can gain some clarity around these benefits is simply by estab-lishing more regular communi-cation between their purchasing and treasury departments regarding their current fuel price assumptions.

At the same time, airlines require a clear reporting structure that enables them to make important fuel hedging decisions quickly based on changing market infor-mation. Responsibility for market analysis, potential hedging strategies and their execution must be appropriately segregated. A risk oversight committee with authority to approve hedge recommendations should also be formed.

Coping with volatile jet fuel prices will continue to be a challenge for the airline industry. In the long run, the price of air travel will adjust to reflect the cost of fuel. However, large fuel price swings could potentially force unprepared airlines to make difficult trade-offs in the short term. Significant fuel hedging losses could compel airlines to cut back growth plans, slash other costs or raise their prices more than their competitors.

Some airlines are already making a preemptive strike to gain control over how increasingly complex energy markets impact their earnings. Oliver Wyman has developed proven approaches and tools that ensure the benefits of airline jet fuel hedges will far outweigh potential losses.

Cantekin dincerler and mark Robson are

partners in the Global Risk & Trading Practice

volatIle commodIty prIces

25% the portion of

airlines’ total

costs that jet fuel

accounts for

18 Risk JOuRnal

veneratIng VOlatility

cantekin dincerler ernst franklroland rechtsteiner

HoW to overcome ImplementatIon rIsks WHen

settIng up a neW commodIty tradIng busIness

19Risk JOuRnal

Most companies curse the unpredictability that volatile commodity prices introduce into their earnings. But traders have a very different point of view. For them, volatile prices spell opportunity. Without them, many struggle to eke out

above-average earnings. indeed, our research shows that commodity traders earned 35 percent less in revenues in 2010 than they did in 2009 in large part because commodity prices remained relatively stable until the end of that year.

With volatility racing back to the markets in 2011 and the success of commodity traders such as Switzerland-based Glencore, which is currently preparing for an initial public offering estimated to be worth more than $55 billion, it is not surprising that organizations ranging from vertically integrated oil and gas players to independent commodity traders are now racing to ramp up new trading operations. Commodity producers who used to sit on the sidelines, letting other traders capture trading margin, are now setting up their own trading businesses. For example, Saudi Arabia’s Saudi Aramco, South korea’s kEPCO and Abu dhabi Resources have all announced plans to enter the commodity trading business in the past few months. They are betting that current commodity market conditions will continue due to factors ranging from increasing global supply- demand imbalances, to extreme weather, to political unrest.

but setting up new trading operations isn’t easy. As with any large project, it involves myriad details that need to be worked out diligently. Only then will a company be able to launch a new trading business on time, within budget and with an end result that is what was originally envisioned.

In our experience, mastering three key risks will determine whether a new commodity trading operation will be successful. Overcoming these three areas of implementation risk involve: articulating a future trading model clearly, aligning stakeholders and achieving excellence in execution. Trading organizations that focus on these critical success factors for setting up new trading operations in a timely manner will set themselves apart from their competitors.

VOlatility

cHangIng tradIng paradIgms

20 RISK JOURNAL

1318

24

12

7

7

8

4

5

8

8

5

10

12

10

9

4

5

5

5

1

2

1

1

10

20

30

40

50

60

2007 2008 2009 2010 2011e

OIL NA P&G EU P&G NICHE METALS INVESTOR

$39-42 BN

$51-53 BN

$54-57BN

$34-37BN

COMMOdITy TRAdERS EARnEd 35% lESS In REVEnUES In 2010 THAn THEy dId In 2009

Source: Oliver Wyman

ARTICUlATInG A TRAdInG bUSInESS MOdEl ClEARlyMost of the trading businesses now being launched are basing their business models on physical production from their parent company. In theory, this gives them the advantage of securing long-term supply positions from the very start. In practice, however, it is difficult to

reach a decision on what part of, and how much of, the physical supply should be transferred and at what price. That means a well-governed process needs to gain support from many stakeholders for this advantage to actually pan out.

To gain broad support, the amount of physical production that will be trans-ferred to the trading business, the new trading model, as well as the plans for building the new business, all need to be decided in detail. They also need to be communicated proactively in a clear and transparent way.

Moving from trading physical flows in order to optimize their value to proprietary trading for profit is a major shift in a business paradigm. Most vertically integrated oil companies are unfamiliar with the nature of proprietary trading. In fact, many have made a point of steering clear of buying and selling third party volumes for a profit or entering into positions that can not easily be offset by their own physical positions in the past.

Making matters more complicated, there is a high barrier to entry into trading. For

most vertically integrated oil companies are unfamiliar with the

nature of proprietary trading

21RISK JOURNAL

PRIMARY FOCUS OF ASSET TRADERS PRIMARY FOCUS OF

INDEPENDENTS AND BANKS

instance, for an oil trading company to be successful, it must build substantial operations. Consider: A world-class oil trader requires the equivalent of the amount of oil that Spain and France each use in a day, or 1.5 million – 2 million barrels of oil per day, to generate gross margins ranging from $400 million – $600 million. In our experience, a company will need to build an organization with 50 to 120 traders and approximately 150 to 400 support staff, to support handling that amount of physical product and the associated paper deals.

AlIGnInG STAkEHOldERSAnother key success factor is to engage key stakeholders continuously throughout the project from early on. For vertically

integrated oil and gas companies, the trading company will be a new entity within an organization that has tradi-tionally been made up of a strong upstream, midstream and downstream business. That means the establishment of a new trading company could have impli-cations for these other business units. It might even weaken their positions since a strong trading company can act as a central optimizer of all of the parent company’s commodity risks.

An effective and continuous communi-cation strategy must ensure that all of these key stakeholders are part of the design and implementation. Their voices should be heard and their contributions acknowledged.

dIfferent types of commodIty tradIng requIre dIfferent Business PaRadigms

PROPRIETARy TRAdInG

f Outright/ directional bets on market developments

f Arbitrage on cross-commodity, cross-location and inter-temporal pricing relationships

dEAl STRUCTURInG/ORIGInATIOn

f Selling of structured deals (e.g. writing options, selling virtual power plants) and collection of deal premium

f Gaining insight into market perspectives of other players

HEdGInG

f Reducing earnings volatility for physical business

f Management of risk exposures toward desired risk profile

ASSET OPTIMIzATIOn

f Monetizing flexibility in physical assets (e.g. adjusting product mix, scheduling and commodity delivery)

f Timing of buy/sell decisions for physical positions (e.g. Oil major - long crude)

MARkET MAkInG

f Enhanced insight into market development on the back of providing liquidity to other market participants by matching supply and demand

f Capitalizing on bid/offer spread

cHangIng tradIng paradIgms

Source: Oliver Wyman

22 Risk JOuRnal

six suggested WORk stReams for successfully buIldIng a neW commodIty tradIng operatIon

WORk STREAM kEy RESPOnSIbIlITIES

WORk STREAM 1 – Overall Project Management

f Create detailed plan

f Track and question the progress continuously and rigorously

f Identify potential delivery risks and support/conduct quality assurance of deliverables proactively

f Support communication between project and stakeholders and among work streams

WORk STREAM 2 – Chief Executive Officer

f Promote the business model and business

f Establish organizational design

f design and agree interface definitions/agreements (trading vs. exiting business)

f design HR/Compensation

f Create ‘day one plan’

WORk STREAM 3 – Chief Commercial Officer

f Provide clear vision on the future activity set

f Support recruiting efforts and talent selection

f design new front office processes

f Ensure sufficient link to established parent company front office processes

WORk STREAM 4 – Chief Risk Officer

f Create an independent and powerful CRO and control function that also supports the business

f Align risk appetite of key stakeholders and operationalize through risk limits

f Create and implement a set of comprehensive best-in-class risk policies and processes

f Ensure link to existing (parent company) risk management approach

WORk STREAM 5 – Chief Financial Officer

f Ensure access to financing and other banking services and develop financing strategy

f Create tax-optimized company set-up

f develop all back office processes and policies to support and control the business

f Ensure alignment with group finance functions and treasury

WORk STREAM 6 – Chief Information Technology Officer

f Establish system architecture to support business model and manage work stream requirements to a realistic level

f Ensure early selection and quick implementation of IT systems

f Manage multi-vendor/contractor environment

Source: Oliver Wyman

23RISK JOURNAL

The first step to achieving this is to have an influential project sponsor who can represent the project team at the same level of key stakeholders and steer the project team safely through the complex maze of corporate relationships. We recently observed a case where a project was executed very effectively in large part because a client made the company’s chief operating officer and a board member the project’s sponsor. As a result, he could represent and manage the new trading operation’s interests at the executive management and board level vis-à-vis other members.

ACHIEVInG ExCEllEnCE In ExECUTIOn Finally, a comprehensive plan for setting up a trading organization is crucial. With a well-structured and executed plan, a company can set up a new commodity trading organization in 12 months. Without one, there is a much higher risk that it will be executed poorly and take more than 18 months.

While many companies build work streams around the support functions needed for an individual trader, projects organized along the key responsibilities of the company’s top five senior executives—the chief executive officer, chief commercial officer, chief risk officer, chief financial officer and chief information technology officer—are much more effective. That’s in large part because the second approach clarifies the ownership of each of the required work streams.

Successful project management requires proactively coordinating people who can manage work stream interfaces and dependencies. The greatest challenge is

striking the right balance between the pace at which a project is being carried out and the pace at which it is gaining broad support. Stakeholders who are crucial to the success of a new trading business can easily lose interest if the project is moving forward too fast without sufficient communication. The project team leadership’s detailed knowledge of commodity trading can dramatically reduce delivery risk by continuously and rigorously tracking the project and asking key questions, while proactively identifying potential delivery risks.

TOP ExECUTIVE WORk STREAMSAt a higher level, the CEO should be handling many important initiatives. For example, the CEO needs to promote the business model and the business contin-uously internally and externally in a

coordinated manner. It’s also up to the CEO to make sure the commodity trading business is designed so that it will function well within its parent organi-zation, and yet have enough independence to meet a company’s desired financial targets.

As part of achieving that goal, the CEO should be intimately involved in recruiting the right people to lead the new business and define their reporting lines both within the trading business as well as in the broader organization. In our

projects organized along the key responsibilities of the company’s top five senior executives are much more effective

cHangIng tradIng paradIgms

24 RISK JOURNAL

experience, clients who have the foresight to recruit and appoint the top and middle management of a new trading organization early on benefit from these managers participating and contributing to the project almost from the start. Otherwise, a client may have to revisit the project team’s decisions every time a new manager is appointed since each new manager will have his or her own perspective on issues partic-ularly pertaining to his or her area of responsibility.

The CEO should also take charge of defining the tasks and responsibilities that need to be performed from the first day of trading, including defining what will need to be checked. Clients can potentially suffer significantly if the aspirations and requirements of the first day of a new trading operation are not well-articulated. In our experience, there’s a serious risk that the project team can become confused about what the endgame is, resulting in a potentially significant delay.

At the same time, the CCO should be working on a third work stream that involves developing and sharing the details of the future business. Unless this executive develops a clear and detailed vision of the trading business model, the scope of trading activities as well as the

interface requirements with other business units, stakeholders may draw different conclusions about how risks should be transferred from business units to the new trading operation. Indeed, without the right leadership, even with clearly defined principles, drafting commercial contracts that govern transfer mechanisms can take more than a year.

The CRO’s main responsibility is organizing an independent and powerful risk management function. Few trading businesses succeed unless a risk and controls culture is firmly established. One step to achieve this is for the CRO to develop the risk analytics capabilities necessary to support the trading business’ complex analysis. However, this can only be achieved if the CRO has a clear picture of the scope of trading and the risks that will need to be managed by the new trading operation. In complex situations that involve large and cross-commodity portfolios with many stakeholders, such clarity does not necessarily emerge quickly, preventing a CRO from properly building up his or her organization on time.

On a different front, the CFO needs to establish an organization capable of supporting a new trading business finan-cially. Since traders will need access to financing instruments as well as short and longer-term funding, the CFO should be solidifying a financing strategy and stable banking relationships. He or she also needs to make sure the tax regime that the trading business operates in is well-understood.

Finally, the CIO needs to be involved early on to evaluate the optimal information technology systems for the trading

clients can potentially suffer significantly if the aspirations and

requirements of the first day of a new trading operation are

not well-articulated

25RISK JOURNAL

operation from several perspectives. First, the CIO needs to asses to what degree the trading company has specific needs that necessitate its systems being run on a stand-alone basis. next, the CIO should select the trading business’ systems as early as possible so that enough input from the other work streams can be gathered to tailor the system to the business’ future needs. Then, the CIO must select and manage the appropriate vendors.

We have seen more than one case in which systems have been selected without taking into consideration how the business will evolve. This has resulted in multiple legacy systems on the trading floor that are not seamlessly inter-connected or connected to the risk management and back office systems. As a result, they become prohibitively expensive to maintain and possibly simply left idle.

SUMMARyHighly volatile commodity prices and changing market structures are creating huge potential opportunities for new trading businesses. but these new players are entering an increasingly competitive environment. Companies that place the responsibility for the success of a new trading business squarely on the agenda of their top executives early on will have a much greater chance of successfully estab-lishing new businesses on budget and on time. The firm foundations of these new trading businesses will also be a key differentiator of their performance over the long term.

Cantekin dincerler, partner, ernst Frankl,

senior associate, and Roland Rechtsteiner,

managing partner, are in the Global Risk &

Trading Practice

cHangIng tradIng paradIgms

1.5–2 million barrels the amount of oil a trader requires every

day to generate gross margins of at least

$400 million

WHy traders need more compreHensIve rIsk and prIcIng

frameWorks In a fundamentally cHanged busIness envIronment

michael dentonalexander frankechristian lins

26 Risk JOuRnal

maxImIzIng valuein VOlatile COmmOdity maRkets

27Risk JOuRnal

Political unrest in the middle east combined with the aftermath of Japan’s earthquake and tsunami have ushered in a new stage of volatile commodity prices. after remaining relatively stable last year, crude oil prices have spiked up by more than 20 percent in the

last several months to settle above $105 per barrel, while many fossil fuel prices have risen by more than 7 percent since Japan’s earthquake on march 11. Wheat, corn and milk prices all initially jumped up by at least 10 percent as well.

Anticipating greater commodity price volatility, commodity trading firms, major oil and gas players, as well as companies with significant exposure to fuels have all been rapidly expanding their trading capabilities everywhere from the United States to Europe to the Middle East. Indeed, at least a dozen new trading operations were registered or announced last year in Switzerland alone.

yet while many companies are increasing their trading capabilities, only a rare few are building out the risk and pricing resources needed for them to capture the optimal value from the higher risks they’re assuming in their expanded operations. As a result, they risk reducing the profitability of their structured products by up to 90 percent by potentially neglecting to take into account important factors such as market liquidity. To take advantage of volatile commodity markets, traders need to develop a single perspective on a wide range of different risks to evaluate the true aggregated impact on their organi-zation. doing so is critical to safeguard not only the profitability of traders’ day-to-day operations, but also their high performance over the long term.

There are several reasons why many firms are rushing to expand their commodity trading arms and to establish entirely new commodity trading operations. leading commodity trading firms are building out global networks of operations to gain direct access to commodities, including their storage, refining and blending. That way they can fully exploit physical product knowledge in their trading. Others are moving into alternative commodity markets to develop more diversified portfolios. large Asian and Russian oil and gas producers like PetroChina, Sinopec and Gazprom are branching out into the US, Europe and the Middle East to gain better insights into global pricing strategies.

At the same time, companies with significant exposure to energy like new york-based bunge, the world’s second-largest sugar trader, are expanding

90%How much traders

may reduce the

profitability of

structured

products if they

neglect to take

into account

market liquidity

cHangIng tradIng paradIgms

28 Risk JOuRnal

stumBling BlOCks In maxImIzIng value

gOal What’s WROng tOday hOW tO Fix it

extract optimal value from deal and portfolio

f Focus is purely on risk compliance f Focus on risk-adjusted value capture and capital efficiency paired with best-practice governance

f Employ a single methodological framework for deal valuation and risk quantification

maintain optimal amount of capital, processes and mitigation measures to withstand market stresses

f Only parametric and historical VaR used, rarely with adjustments for market illiquidity

f Asset optionality is ignored

f Use Monte Carlo simulation engine to incorporate empirical properties of commodities

f Apply Earnings at Risk framework to reflect available market liquidity in close-out scenario

f Incorporate physical characteristics of assets

Optimize capital, processes and mitigation measures to cope with counterparty credit risk

f Focus solely on current exposure and Credit VaR (if established) metrics computed on standalone basis

f Only ad hoc requests for third party credit information with limited predictive power – often too late to mitigate against counterparty default

f develop life cycle perspective on counterparty credit risk and link to market scenarios allowing for an integrated counterparty valuation approach

f Actively manage and trade credit risk at portfolio and deal level

allocate risk capital with optimal efficiency

f Risk is evaluated in silos with a limited amount of diversification considered between subportfolios

f lack of integrated view on market and credit risks

f Overall risk contributions of each branch of trading activity are not captured

f Quantify overall risk impact of a single deal and derive implications for valuation at the aggregated book, subportfolio and overall portfolio levels

f Consider cross-commodity and inter-temporal diversification as well as individual book or framework risk contributions

f Evaluate commonalities of risk drivers between market and credit risks

establish liquidity and contract management sufficient to support growth strategies

f Contract management solely focused on legal stipulations

f limited insight into mid to long-term liquidity needs

f Adopt contract management with rigid governance around securities employed

f Integrate working capital management as well as cash and net debt management with market and credit scenarios

f link different types of risk to increase the accuracy of liquidity planning

f Support structured trade finance initiatives in illiquid assets

their trading operations into physical oil in order to trade around their natural short position in fuel oil. by doing so, bunge can improve the margins in its shipping operation.

Many companies’ risk and pricing capabilities trail far behind their ambitious

expansions. Recent experiences from the financial crisis have highlighted weaknesses in risk quantification and valuation frameworks both in financial services companies as well as in commodity trading firms. Still, the common shortcomings have remained the same over the last couple of years as

Source: Oliver Wyman

29Risk JOuRnal

recent events have generally not led to structural improvements.

Worse, the recent ramping up of commodity trading operations is making the task of managing the risks embedded in them even more complex. Many companies are bringing together various trading operations with motley collections of risk management frameworks. Most need to be aligned for firms to capture the optimal value across their consolidated asset and customer portfolios.

Why then do so many commodity traders seem to ignore the need to evaluate their risks on a more comprehensive basis? Some don’t realize the magnitude of their risk exposure. Others don’t know that they are potentially forgoing opportunities for higher trading margins by inefficiently using their risk capital.

Adopting more comprehensive integrated risk and pricing approaches can resolve many of these issues. by developing deep insights into all of the fundamental value drivers in a trading portfolio, an integrated framework provides the radar for risk exposures across all trading activities. This enables risk managers to identify the tangible market and credit developments to which the firm’s financial performance and liquidity are particularly sensitive.

Profitability can be improved in a consistent way if the risk quantification methodologies used can capture the characteristics of the underlying asset base accurately. For example, a trading operation can understand the risks that it is facing and negotiate an appropriate margin for keeping the risk on its books. deals that reduce the overall portfolio risk can be

priced more aggressively than deals that increase risk, thereby creating an incentive for traders to develop an aggregated portfolio view on risks across all desks.

Indeed, price simulation engines that account for the key empirical properties of commodities paired with models capturing asset optionality are not only powerful tools in trading risk management, but also in strategic decision making as they help executives to understand the life cycle of a trading strategy.

This article highlights seven of the more common and onerous types of oversights that exist in commodity traders’ risk and pricing frameworks. We then suggest broad strategies for correcting these shortcomings and preventing new ones from springing up.

SEVEn blInd SPOTSThere are seven areas of risk that commodity traders often do not take into adequate account that can lead to dangerous underestimations of their true risk exposure:

1) Market liquidity – Many asset-backed traders hold positions that are more than 100 times their daily transacted volumes. As a result, the risk resulting from these long holding periods may be more than 10 times greater than what has been quantified with a standard VaR approach. One European energy trading company recently discovered this the hard way after it was hit with tens of millions of dollars of losses from a losing position even though its VaR was well within acceptable limits. The problem was that the firm had not accounted for the market liquidity associated with its losing

many asset-backed traders hold positions that are more than 100 times their daily transacted volumes

cHangIng tradIng paradIgms

30 RISK JOURNAL

position, which it suddenly could not close because other players were simultaneously trying to do the same thing. Oil and gas traders face a similar dilemma since they are often engaged in longer-term commitments that become costly to hedge in the absence of liquidity.

2) Methodology – Relying on insuf-ficient and inconsistent method-ologies can result in significant miscalculations of the value and the risk of a contract. A lack of

adequate modeling techniques can create a structural impediment to capturing higher trading margins by forcing a trader to forgo the benefits of advanced market analysis techniques. For example, the profitability of oil trading in 2010 was reduced significantly when compared to 2009 and 2008, in large part because only a few traders had considered the risk of the forward curve flattening. As a result, many found it difficult to recoup the premium paid on large amounts of contracted storage capacity.

3) diversification effects – If properly diversified, the market risk of a large commodity trading portfolio can be reduced by as much as 70 percent. However, many trading organizations lack the structural prerequisite for realizing such diversification benefits because they are unable to harmonize their risk quantifi-cation methodology across each of their trading books and risk types. As a result, they are missing out on potential savings: by increasing the scope of risks quantified and examining cross-commodity as well as inter-temporal correlations within a trading portfolio, Oliver Wyman recently

identified $700 million in potential savings in risk capital for a large commodity trading firm. Further benefits were achieved after measuring the extent of diversification of the portfolio’s market and credit risk.

4) Physical characteristics of real assets – The risks in structured deals and associated hedging activities are often incorrectly represented because traders rarely take into account the flexibility and optionality of assets like power plants, natural reserves, storage or transportation infrastructure. It is common practice to hedge out the portions of risk that are not well-understood or to disregard them in less sophisticated commodity trading operations. This often reduces the profit-ability of deals by more than half.

5) Credit risk – Few organizations quantify expected or unexpected credit losses when they measure credit exposure, and even fewer reflect this in profitability calculations on a deal level. yet taking credit losses into account can funda-mentally change the profitability of a trade, especially for asset-backed traders, who have the bulk of their credit exposure with non-financial services counterparties. For example, the fact that a rating migration from bbb to bb may quadruple the expected loss is often not considered adequately upon the inception of a deal.

6) liquidity and collateral management – At a time when the recently passed dodd-Frank Act will likely increase the volatility in exchange-traded and over-the-counter commodities, many large commodity trading operations still have difficulty quantifying their true liquidity needs for a limited number of days

70%How much the

risk in a large

commodity

trading portfolio

can be reduced

if it is properly

diversified

31RISK JOURNAL

ahead. This is in large part because they fail to examine all of their available sources of liquidity and commitments. In fact, many large operations have trouble assessing how much they are trading against open credit or third party guarantees. As a result, they have little understanding of the potential impact of collateral or margin calls on their liquidity.

7) Replacement cost – A combination of counterparty defaults and market turmoil may force a trader to source expensively at a spot price in order to compensate for physically missing forward volumes. nevertheless, few firms consider the replacement risk that can result from the potential inability of a counterparty to deliver contractually agreed physical volumes. The impact may not only be limited to an opportunity cost but also could become a material loss.

SIx RECOMMEndEd STEPS TO dEVElOP A MORE COMPREHEnSIVE RISk FRAMEWORkToday, most commodity traders can count on missing out on potential margins because they are inaccurately measuring risks or inefficiently using their risk capital. Fortunately, they can take steps to develop a more integrated perspective of their portfolio and its potential impact on their organization.

1) Treat risk management as a risk-adjusted value creator. The main purpose of a business enterprise is to capture rewards equivalent to the risks taken. And yet, many commodity trading organi-zations take a compliance-oriented view of risk management. As a result, they miss out on the potential benefits of developing a more comprehensive risk framework.

Trading and risk management teams need to raise top management’s awareness of the benefits of integrated risk and pricing frameworks. Maximum commercial leeway should be granted to traders under an effective governance framework that ensures that the targeted return is commen-surate with a level of risk that is in line with the entire organization’s risk appetite.

2) Establish adequate risk quantification methodologies. Commodity trading organi-zations need to develop processes to ensure that key risks such as the seven mentioned above are all considered and that their risk capital is quantified efficiently, taking into account the benefits of diversifi-cation for an organization’s entire portfolio. These methods need to be tailored to a company’s asset portfolio and risk governance principles so that the company can stay in control of them and understand the risks that have been quantified.

3) Enable consistent integration into a governance framework. A comprehensive governance framework is necessary to ensure that a broader set of risk infor-mation is used appropriately to steer a trading business. Risk-adjusted performance measures need to be linked to traders’ compensation in order to encourage them to use risk capital more efficiently and ultimately achieve greater profitability. Risk-adjusted financial planning for the holding company ensures that its strategic plan remains feasible and that any financial impact from trading operations in adverse conditions will be manageable. This way, the organization can be sure that it has sufficient cash liquidity to prevent being forced to pull out of positions prematurely.

most commodity traders can count on missing out on potential margins because they are inaccurately measuring risks or inefficiently using their risk capital

cHangIng tradIng paradIgms

32 Risk JOuRnal

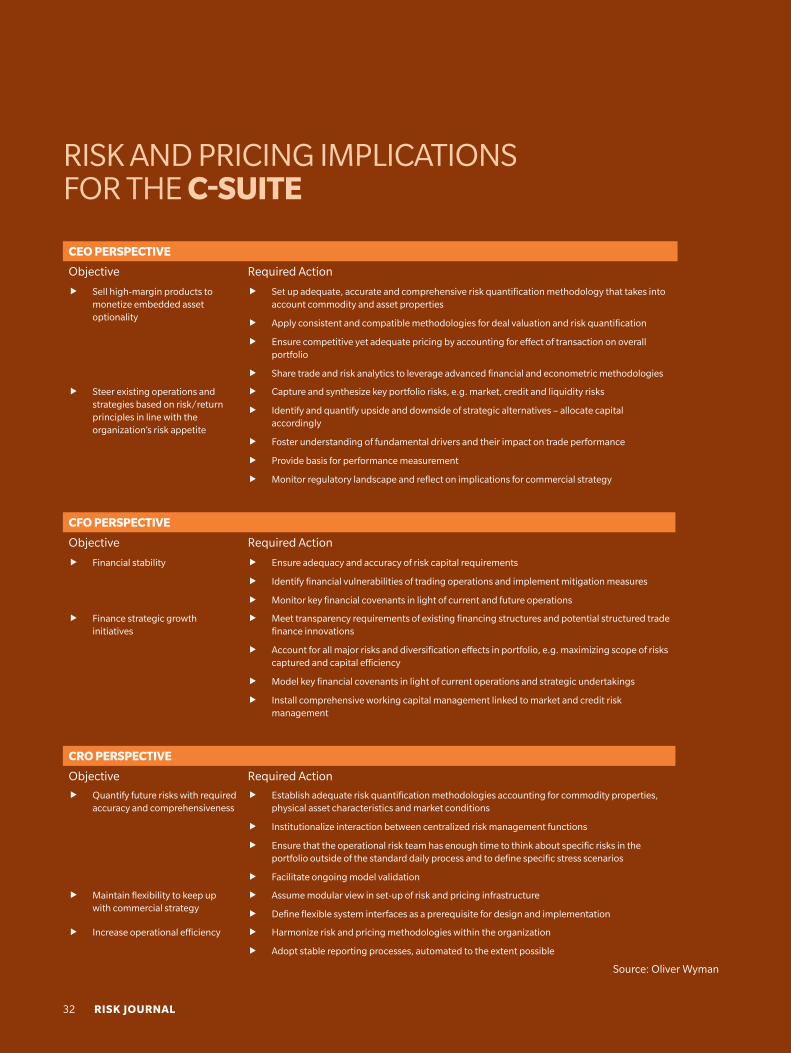

CeO PeRsPeCtiVe

Objective Required Action

f Sell high-margin products to monetize embedded asset optionality

f Set up adequate, accurate and comprehensive risk quantification methodology that takes into account commodity and asset properties

f Apply consistent and compatible methodologies for deal valuation and risk quantification

f Ensure competitive yet adequate pricing by accounting for effect of transaction on overall portfolio

f Share trade and risk analytics to leverage advanced financial and econometric methodologies

f Steer existing operations and strategies based on risk/return principles in line with the organization’s risk appetite

f Capture and synthesize key portfolio risks, e.g. market, credit and liquidity risks

f Identify and quantify upside and downside of strategic alternatives – allocate capital accordingly

f Foster understanding of fundamental drivers and their impact on trade performance

f Provide basis for performance measurement

f Monitor regulatory landscape and reflect on implications for commercial strategy

CFO PeRsPeCtiVe

Objective Required Action

f Financial stability f Ensure adequacy and accuracy of risk capital requirements

f Identify financial vulnerabilities of trading operations and implement mitigation measures

f Monitor key financial covenants in light of current and future operations

f Finance strategic growth initiatives

f Meet transparency requirements of existing financing structures and potential structured trade finance innovations

f Account for all major risks and diversification effects in portfolio, e.g. maximizing scope of risks captured and capital efficiency

f Model key financial covenants in light of current operations and strategic undertakings

f Install comprehensive working capital management linked to market and credit risk management

CRO PeRsPeCtiVe

Objective Required Action

f Quantify future risks with required accuracy and comprehensiveness

f Establish adequate risk quantification methodologies accounting for commodity properties, physical asset characteristics and market conditions

f Institutionalize interaction between centralized risk management functions

f Ensure that the operational risk team has enough time to think about specific risks in the portfolio outside of the standard daily process and to define specific stress scenarios

f Facilitate ongoing model validation

f Maintain flexibility to keep up with commercial strategy

f Assume modular view in set-up of risk and pricing infrastructure

f define flexible system interfaces as a prerequisite for design and implementation

f Increase operational efficiency f Harmonize risk and pricing methodologies within the organization

f Adopt stable reporting processes, automated to the extent possible

RISk And PRICInG IMPlICATIOnS FOR THE C-suite

Source: Oliver Wyman

4) Institutionalize interactions between centralized risk management functions in an integrated framework. Critical infor-mation must be shared effectively. This implies that market and credit views will be synthesized and adequately reflected in liquidity risk metrics. A liquidity and collateral management team needs to ensure that sufficient liquidity is available to support profitable trading strategies.

5) develop stable reporting processes. day-to-day trading operations must be supported with current risk information. data must be captured and stored centrally to ensure all information is simultaneously available across the whole trading portfolio. Processes need to be largely automated to reduce operational risks and to free up reporting teams’ time to investigate where specific risk exposures such as market, credit and liquidity risk reside in the trading portfolio.

6) Conduct ongoing model validation. An organization’s processes and compe-tencies to manage model risk are vital elements in ensuring that risk capital efficiency does not come at the cost of additional model risk. This can be achieved by supplementing risk quantification tools with independent testing. Models optimized for capital efficiency should be regularly scrutinized through back testing and standardized validation routines.

SUMMARyCommodity trading organizations that recognize an integrated risk and pricing framework contains tools for creating value will develop a significant competitive edge, particularly in highly volatile commodity markets. Custom tailored risk quantification methodologies that incorporate the

elements described above are crucial for revenue growth, profitability gains and financial stability.

Integrated risk and pricing practices will decrease operational risk dramatically. The combination of a centrally controlled methodology and an adequate governance framework reduces operational risk, partic-ularly when a trading organization has experienced significant inorganic growth or undergone a period of consolidation.

Management teams as well as shareholders will also have a better understanding of what capital buffer is required to realize strategic plans in a way that permits the trading organization’s cost of debt to be stabilized. Unlike using a standard VaR approach for determining the appropriate level of the capital buffer necessary, a more compre-hensive Earnings at Risk framework increases the accuracy of risk quantification, especially for positions that cannot be easily liquidated. It also has the potential to improve risk capital efficiency significantly when paired with adequate market price scenarios.

All of this will become increasingly important as commodity markets become more volatile in today’s fundamentally changed business environment.

michael denton, partner, alexander Franke,

associate partner, and Christian lins,

associate, are in the Global Risk & Trading

Practice

cHangIng tradIng paradIgms

33Risk JOuRnal

34 Risk JOuRnal

embracIng tHe

highlyimPROBaBle

alexander frankeboris galonskechristian lins

sIx lessons for commodIty traders from tHe tragIc

events In Japan

Risk JOuRnal 35

The tsunami-induced nuclear crisis in Japan reinforced a lesson that many organizations first learned from the financial crisis: Risks considered extremely unlikely can, and increasingly do, happen. many commodity trading organizations discovered

themselves on the wrong side of the market when power, natural gas, coal and carbon emission prices suddenly increased by double digits shortly after the events in Japan and government decisions to shut down nuclear plants in europe. this is likely to result in losses that will have a significant impact on their upcoming quarterly earnings results.

Agricultural commodity prices like corn, wheat, rice, sugar, soybeans and milk rebounded after dropping in reaction to fears of lower Japanese imports. Uranium also tumbled initially more than 20 percent as increasingly divided views about the future of the nuclear industry spread around the world. Some speculative market participants unloaded positions while plant operators and producers stepped in and bought the fuel raw material. Similarly, Australian coal fell more than 5 percent as Japan’s coal infrastructure and generation capacity declared force majeure and new buyers had to be sought for cargos.

The chain of incidents that led to Japan’s nuclear emergency highlights the structural deficits that many commodity trading organizations suffer from in their ability to cope with tail events. Well-established standard practices for preparing for highly improbable events such as nuclear conflicts in the Middle East and widespread power outages have existed for many years. And yet, many organizations do not embrace these practices with a sufficient sense of urgency under normal conditions.

cHangIng tradIng paradIgms

36 Risk JOuRnal

We believe the time has come for trading organizations to incorporate impossible events into their regular risk management routines. To this end, we suggest that every commodity trading organization should embrace the following six broad strategies:

f Supplement stress tests for risk reporting – Process a static set of stress scenarios consisting of extreme price movements; correlation coupling and decoupling; and liquidity decreases on a recurring basis. Make sure that the associated monitoring of stress test outcomes is a key element of the risk governance framework.

f Consider market liquidity – Regularly evaluate the market liquidity of each position. Asset-backed traders can hold positions that are more than 100 times the daily transacted volumes. As a result, any quantification of risk can be significantly distorted if the liquidity of a trading position’s market is not taken into account.

f Apply proven methods – Identify key historical incidents that had a detrimental impact on risk drivers and use them as inputs for standardized stress scenarios that are evaluated on a regular basis. This approach becomes especially relevant once full portfolio diversification benefits have been realized in favor of capital efficiency. Senior executives should also reevaluate whether they are using adequate stress testing tools. False security supported by insufficient models leads to severe financial consequences.

cHangIng tradIng paradIgms

37Risk JOuRnal

70%

80%

90%

100%

110%

120%

130%

10-Mar 14-Mar 16-Mar 18-Mar 22-Mar 24-Mar

IND

EXED

PR

ICES

POWER (GERMANY BASELOAD) EMISSIONS (CERTIFIED EMISSION REDUCTION)

COAL (API2, CIF NORTHWEST EUROPE) COAL (API6, FOB AUSTRALIA)

NATURAL GAS (DUTCH) URANIUM (NYMEX, OXIDE CONCENTRATE U3O8)

70%

80%

90%

100%

110%

120%

130%

10-Mar 14-Mar 16-Mar 18-Mar 22-Mar 24-Mar

IND

EXED

PR

ICES

RICE (CBOT)

CORN (CBOT)

WHEAT (CBOT)

MILK (CME, CLASS III)

SOYBEANS (CBOT)

SUGAR (NYMEX)

MARCH 10, 2011 = 100 %

MARCH 10, 2011 = 100 % AGRICUlTURAl PROdUCT PRICES

Initial concerns about

lower agricultural

product demand swiftly

disappeared.

Source: bloomberg

EnERGy And CARbOn EMISSIOnS PRICES

Concerns about nuclear

power affected the

prices of fossil fuels

and carbon emissions.

Source: bloomberg

COmmOdity PRiCe Changes tWo Weeks after tHe Japanese tragedy

38 RISK JOURNAL

f Conduct reverse stress tests – Examine the level of loss that would pose a significant threat to the trading organization. Such a critical loss could result from occurrences ranging from missing annual performance targets to traders’ reputations being damaged because they could suddenly trigger a need to hold a higher level of collateral, for example. A breach of a financial covenant requiring immediate refinancing of debt at a significantly higher margin or the failure to fulfill an obligation set forth by a contractual agreement could also jeopardize a trading organization’s survival in the mid to long term. developing stress scenario and associated thresholds of risk factors and their dependencies fosters a thorough understanding of the firm’s risk environment among all stakeholders. For senior management, reverse stress tests provide an excellent basis for prioritizing risk mitigation measures and allocating resources based on the vulnerabilities and dependencies of the firm’s businesses. Insightful reverse stress cases account for market, credit, liquidity, operational and legal implications as well as the specificities of the underlying physical asset base.

f define combined stresses for commodity price developments and correlations – Trading organizations increasingly need to develop stress tests and more sophisticated risk aggregation methodologies that take into account risks related to not only commodity price fluctuations, but also alterations in their correlations. Under extreme market conditions, commodities often become either much more positively or negatively correlated, increasing the basis risk in a hedge portfolio significantly. For instance, the observed change in the spread between South African coal delivered into Europe and coal shipped from Australia may become a standard example of a correlation suddenly decoupling. In terms of credit risk, the correlation between a potential counterparty default and the replacement value of a structured contract may also be suddenly, and dramatically, changed.

f Incorporate a checkpoint prior to stop-loss close-out procedures – Some commodities’ initial price shocks leveled off in the weeks following the initial tragic events in Japan. For instance, the 12 percent price increase of dutch natural gas in the first week shrank to less than half of that only a week later. Stop-loss limit procedures should be structured so that commodity traders must explain losses to senior management before hard limits are triggered. Furthermore, they should allow, in exceptional cases, a trader to leave a position open if a convincing case for the persisting fundamental rationale of the trade can be made.

the time has come for trading organizations to

incorporate impossible events into their regular

risk management routines

39RISK JOURNAL

cHangIng tradIng paradIgms