Embed Size (px)

Citation preview

WO

CA

2015

–Pl

enar

y Se

ssio

n –

May

5th

Asia

n C

oal A

sh

Asso

ciat

ion

ITIB

MI

Coa

l Ash

Sol

utio

ns

IT

IB

MI

Institute

ofTechnical

InformationBuildingMaterials

In

du

st

ry

2015

Wo

rld

of

Co

al A

sh (

WO

CA

) C

on

fere

nce

in N

asvh

ille,

TN

- M

ay 5

-7, 2

015

htt

p:/

/ww

w.f

lyas

h.in

fo/

Cont

ents

Supp

ly &

D

eman

d vs

Geo

grap

hy

Inte

rnat

iona

l Tr

ade

•C

halle

nges

: •

Supp

ly/D

eman

d•

Logi

stic

s in

frast

ruct

ure

•Tr

ansp

ort c

osts

•Q

ualit

y•

Solu

tion:

•En

gage

men

t

Sum

mar

y

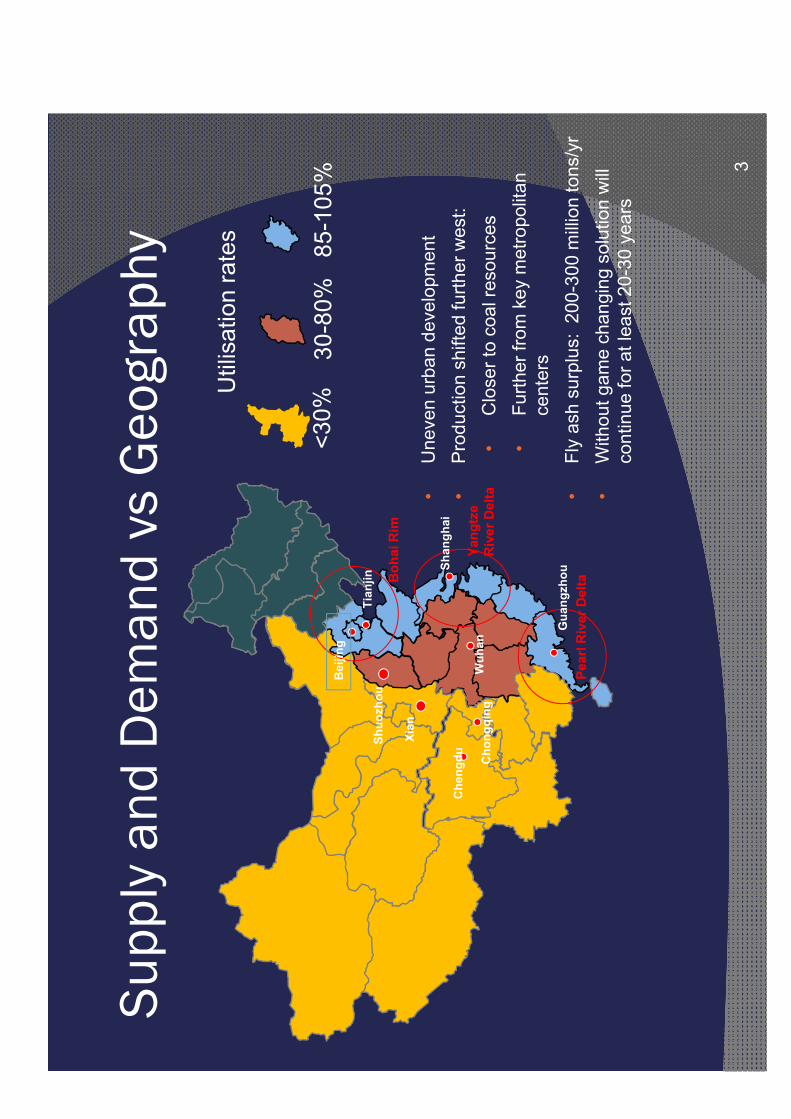

Supp

ly a

nd D

eman

d vs

Geo

grap

hy

•U

neve

n ur

ban

deve

lopm

ent

•Pr

oduc

tion

shift

ed fu

rther

wes

t:•

Clo

ser t

o co

al re

sour

ces

•Fu

rther

from

key

met

ropo

litan

ce

nter

s•

Fly

ash

surp

lus:

200

-300

milli

on to

ns/y

r•

With

out g

ame

chan

ging

sol

utio

n w

ill co

ntin

ue fo

r at l

east

20-

30 y

ears

3

Yang

tze

Riv

er D

elta

Pear

l Riv

er D

eltaB

ohai

Rim

Bei

jing

Tian

jin

Shan

ghai

Che

ngdu Cho

ngqi

ngW

uhan

Gua

ngzh

ou

Xian

Shuo

zhou

85-1

05%

30-8

0%<3

0%

Util

isat

ion

rate

s

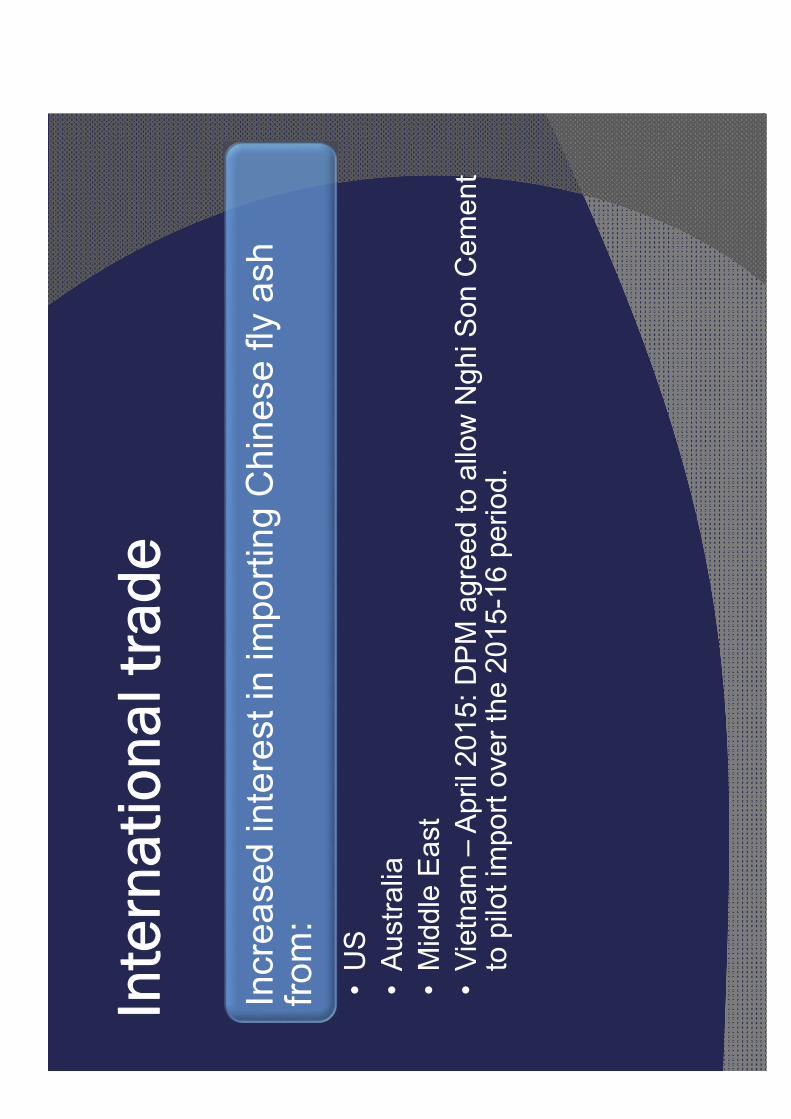

Inte

rnat

iona

l tra

de

Incr

ease

d in

tere

st in

impo

rting

Chi

nese

fly

ash

from

:•

US

•Au

stra

lia•

Mid

dle

East

•

Viet

nam

–Ap

ril 2

015:

DPM

agr

eed

to a

llow

Ngh

iSon

Cem

ent

to p

ilot i

mpo

rt ov

er th

e 20

15-1

6 pe

riod.

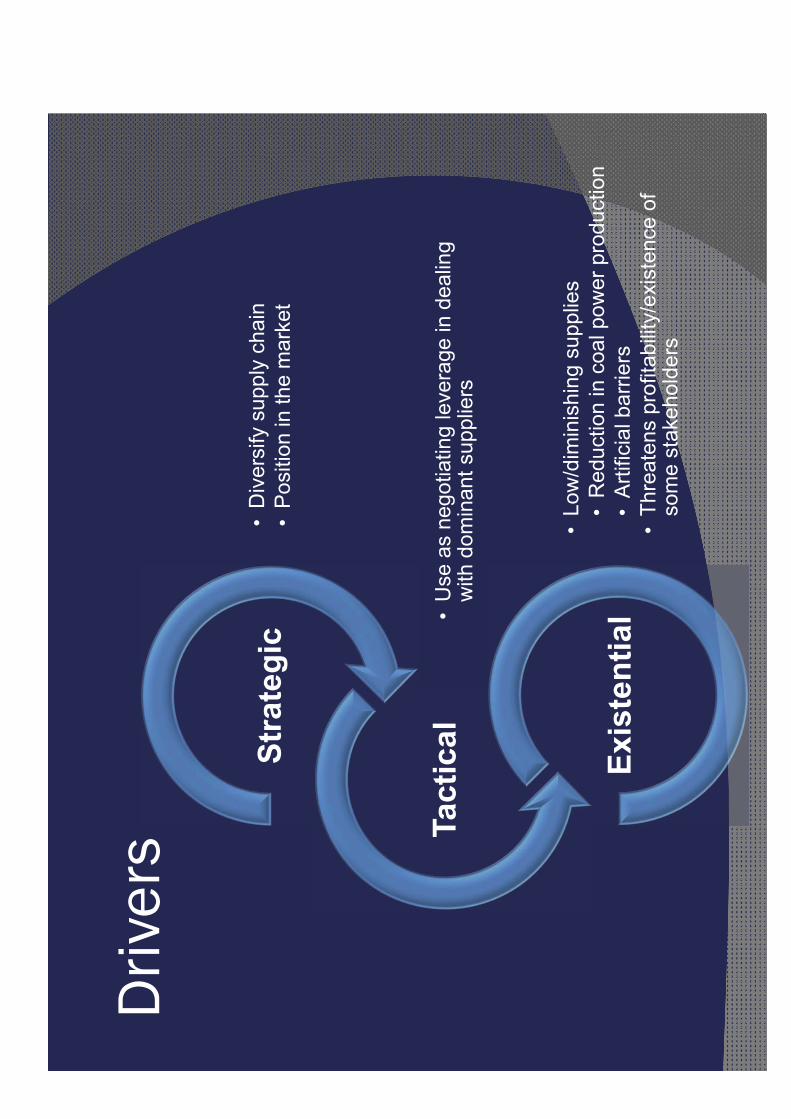

Driv

ers

•D

iver

sify

sup

ply

chai

n•

Posi

tion

in th

e m

arke

tSt

rate

gic

•U

se a

s ne

gotia

ting

leve

rage

in d

ealin

g w

ith d

omin

ant s

uppl

iers

Tact

ical

•Lo

w/d

imin

ishi

ng s

uppl

ies

•R

educ

tion

in c

oal p

ower

pro

duct

ion

•Ar

tific

ial b

arrie

rs•

Thre

aten

s pr

ofita

bilit

y/ex

iste

nce

of

som

e st

akeh

olde

rs

Exis

tent

ial

Res

earc

h

C

AS p

rimar

y re

sear

ch:

Fl

y as

h su

pplie

rs

Mat

eria

l cha

ract

eris

tics

Lo

gist

ics

Pr

ojec

ted

deliv

ered

cos

ts to

Aus

tralia

, USA

and

M

iddl

e Ea

st

Opp

ortu

nitie

s

A

num

ber o

f opp

ortu

nitie

s to

incr

ease

ex

ports

of c

emen

t gra

de fl

y as

h.

Supp

ort f

rom

pot

entia

l su

pplie

rs/g

over

nmen

ts

Lega

l and

ope

ratin

g en

viro

nmen

t gre

atly

im

prov

ed

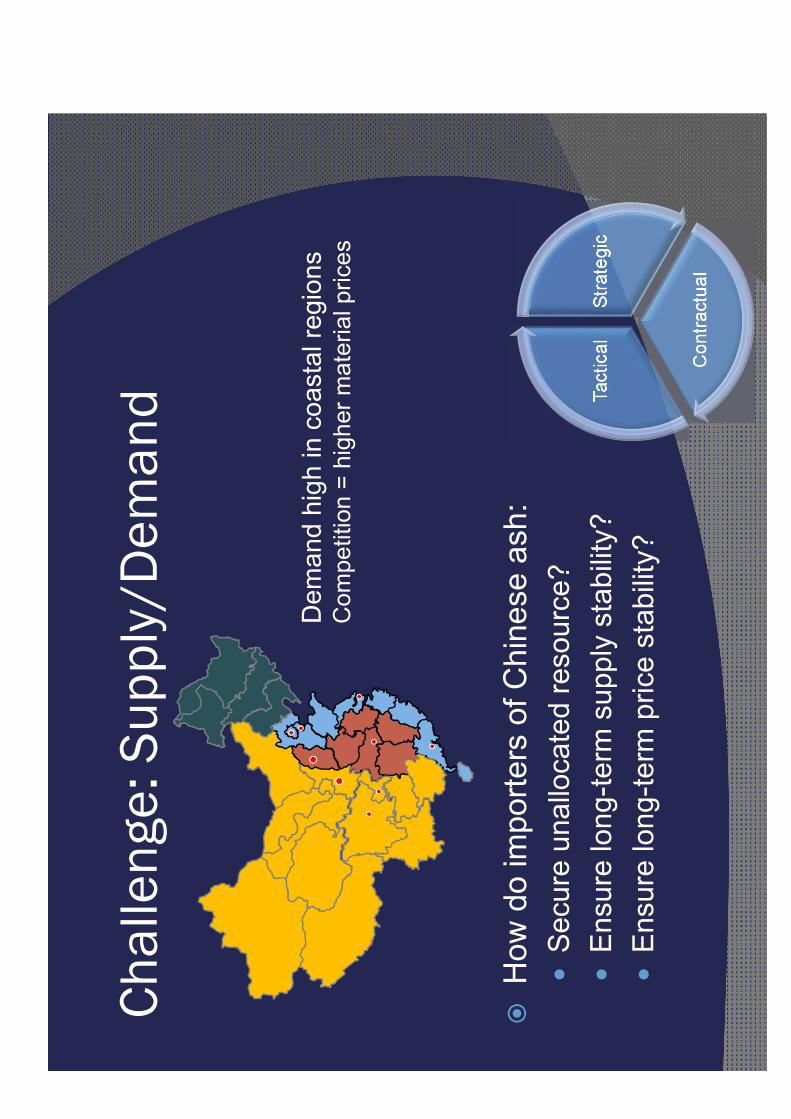

Chal

leng

e: S

uppl

y/D

eman

d

H

ow d

o im

porte

rs o

f Chi

nese

ash

:

Secu

re u

nallo

cate

d re

sour

ce?

En

sure

long

-term

sup

ply

stab

ility?

En

sure

long

-term

pric

e st

abilit

y?St

rate

gic

Con

tract

ual

Tact

ical

Dem

and

high

in c

oast

al re

gion

s C

ompe

titio

n =

high

er m

ater

ial p

rices

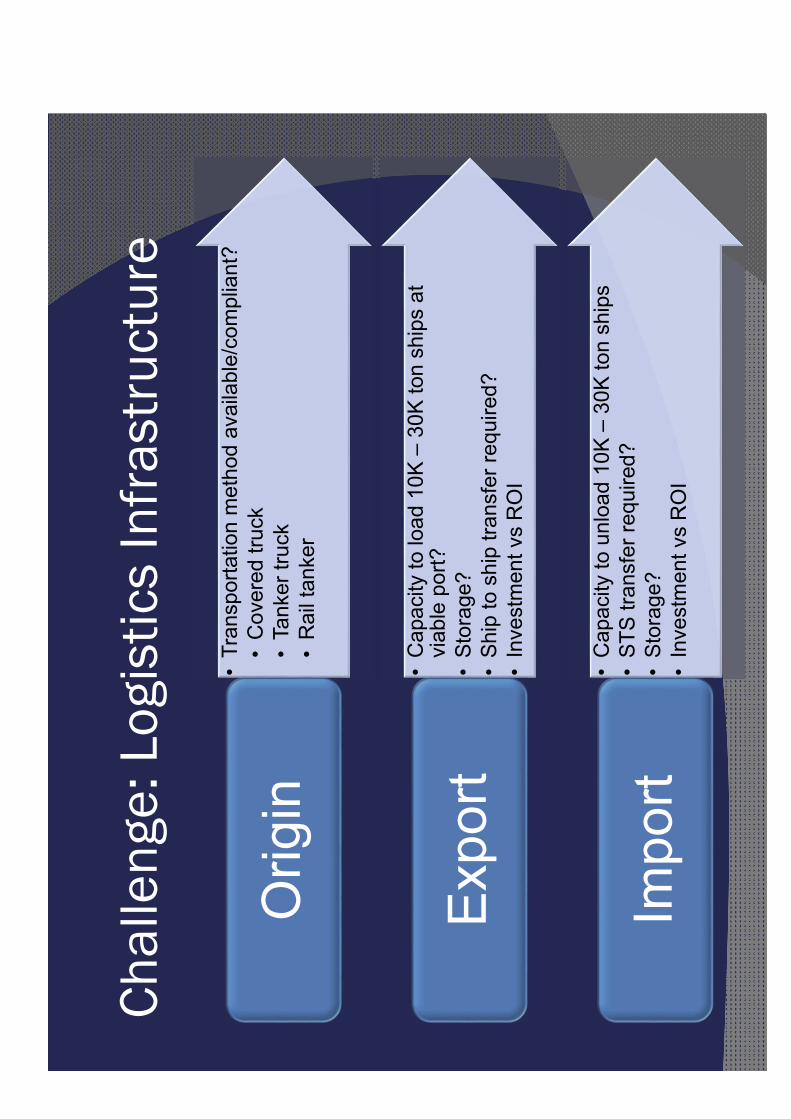

Chal

leng

e:Lo

gist

ics

Infr

astr

uctu

re

•Tr

ansp

orta

tion

met

hod

avai

labl

e/co

mpl

iant

?•

Cov

ered

truc

k•

Tank

er tr

uck

•R

ail t

anke

rO

rigin

•C

apac

ity to

load

10K

–30

K to

n sh

ips

at

viab

le p

ort?

•St

orag

e?•

Ship

to s

hip

trans

fer r

equi

red?

•

Inve

stm

ent v

sR

OI

Expo

rt

•C

apac

ity to

unl

oad

10K

–30

K to

n sh

ips

•ST

S tra

nsfe

r req

uire

d?•

Stor

age?

•

Inve

stm

ent v

sR

OI

Impo

rt

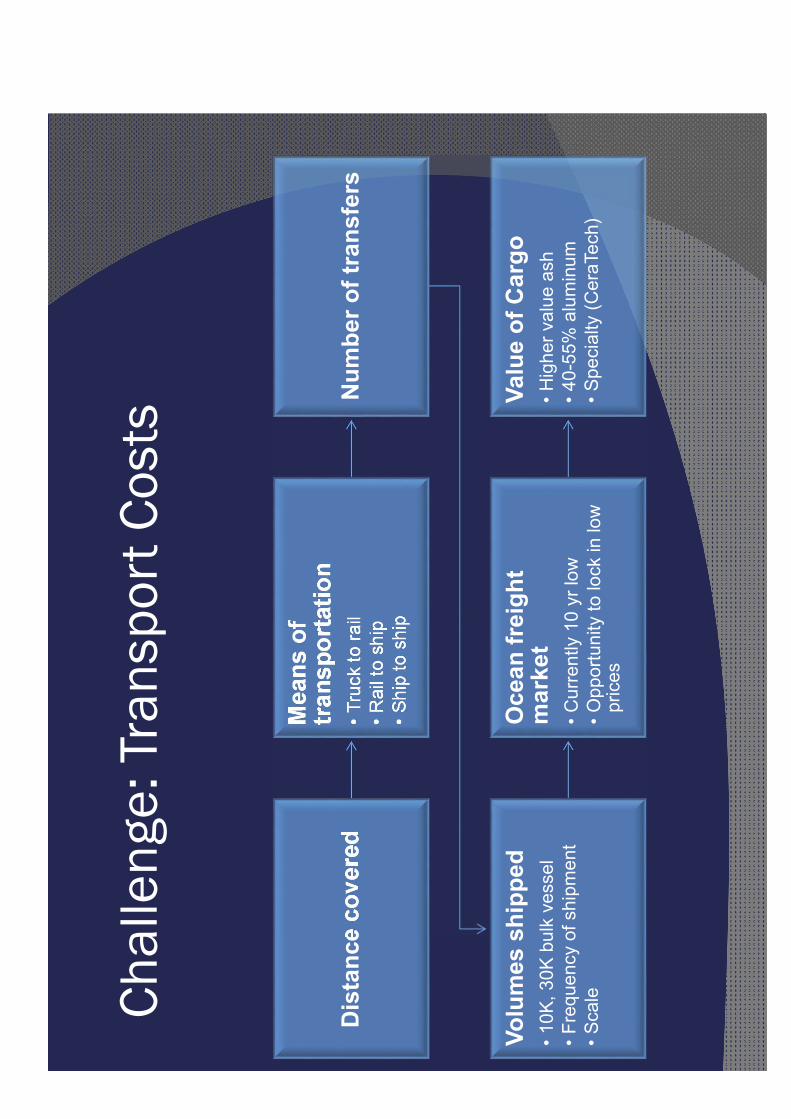

Chal

leng

e:Tr

ansp

ort C

osts

Dis

tanc

e co

vere

d

Mea

ns o

f tr

ansp

orta

tion

•Tru

ck to

rail

•Rai

l to

ship

•Shi

p to

shi

p

Num

ber o

f tra

nsfe

rs

Volu

mes

shi

pped

•10K

, 30K

bul

k ve

ssel

•Fre

quen

cy o

f shi

pmen

t•S

cale

Oce

an fr

eigh

t m

arke

t•C

urre

ntly

10

yrlo

w•O

ppor

tuni

ty to

lock

in lo

w

pric

es

Valu

e of

Car

go•H

ighe

r val

ue a

sh•4

0-55

% a

lum

inum

•Spe

cial

ty (C

eraT

ech)

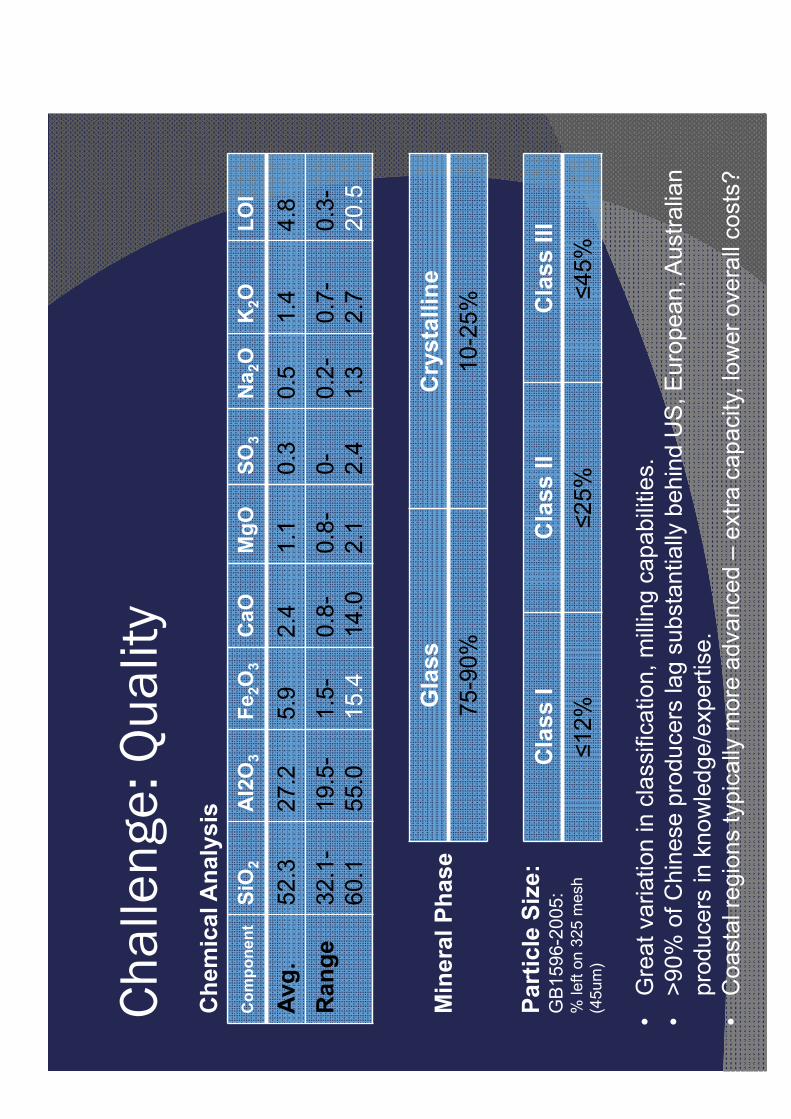

Chal

leng

e:Q

ualit

y

Com

pone

ntSi

O2

Al2

O3

Fe2O

3C

aOM

gOSO

3N

a 2O

K2O

LOI

Avg.

52.3

27.2

5.9

2.4

1.1

0.3

0.5

1.4

4.8

Ran

ge32

.1-

60.1

19.5

-55

.01.

5-15

.40.

8-14

.00.

8-2.

10- 2.

40.

2-1.

30.

7-2.

70.

3-20

.5

•G

reat

var

iatio

n in

cla

ssifi

catio

n, m

illing

cap

abilit

ies.

•>9

0% o

f Chi

nese

pro

duce

rs la

g su

bsta

ntia

lly b

ehin

d U

S, E

urop

ean,

Aus

tralia

n pr

oduc

ers

in k

now

ledg

e/ex

perti

se.

•C

oast

al re

gion

s ty

pica

lly m

ore

adva

nced

–ex

tra c

apac

ity, l

ower

ove

rall

cost

s?

Cla

ss I

Cla

ss II

Cla

ss II

I≤1

2%≤2

5%≤4

5%

Part

icle

Siz

e:

GB1

596-

2005

: %

left

on 3

25 m

esh

(45u

m)

Gla

ssC

ryst

allin

e 75

-90%

10-2

5%M

iner

al P

hase

Che

mic

al A

naly

sis

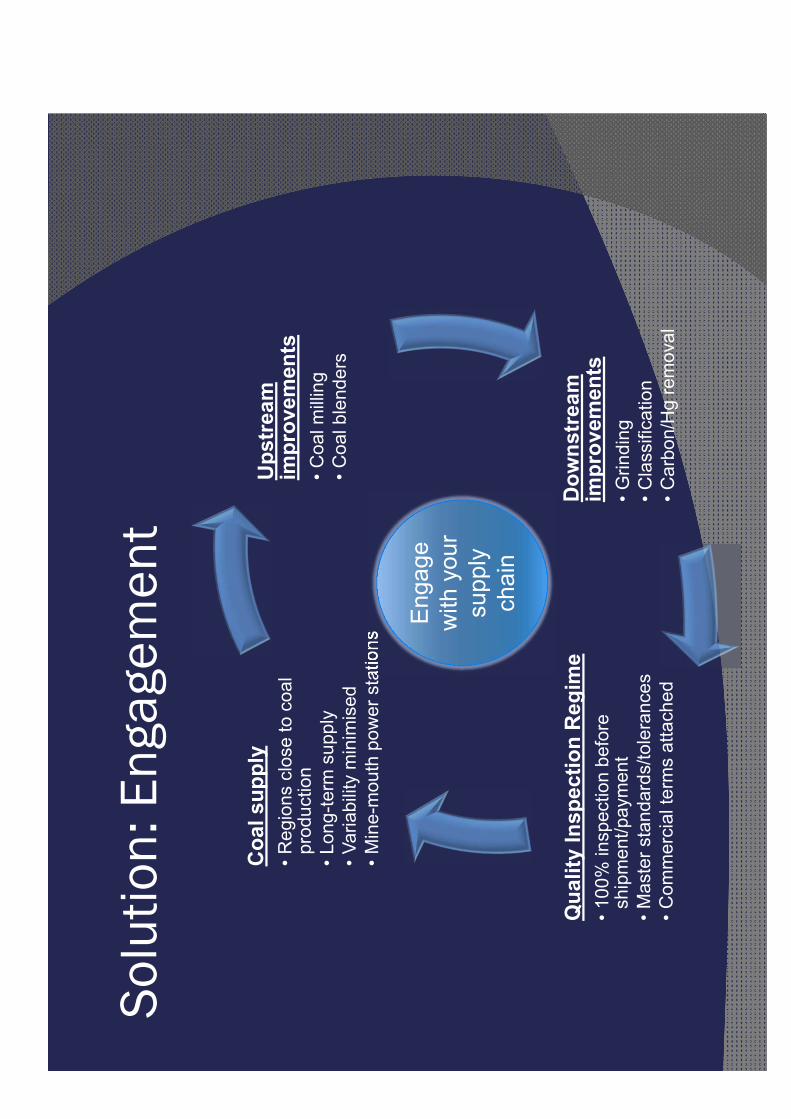

Solu

tion:

Enga

gem

ent

Ups

trea

m

impr

ovem

ents

•Coa

l milli

ng•C

oal b

lend

ers

Dow

nstr

eam

im

prov

emen

ts•G

rindi

ng•C

lass

ifica

tion

•Car

bon/

Hg

rem

oval

Qua

lity

Insp

ectio

n R

egim

e•1

00%

insp

ectio

n be

fore

sh

ipm

ent/p

aym

ent

•Mas

ter s

tand

ards

/tole

ranc

es•C

omm

erci

al te

rms

atta

ched

Coa

l sup

ply

•Reg

ions

clo

se to

coa

l pr

oduc

tion

•Lon

g-te

rm s

uppl

y•V

aria

bilit

y m

inim

ised

•Min

e-m

outh

pow

er s

tatio

ns

Enga

ge

with

you

r su

pply

ch

ain

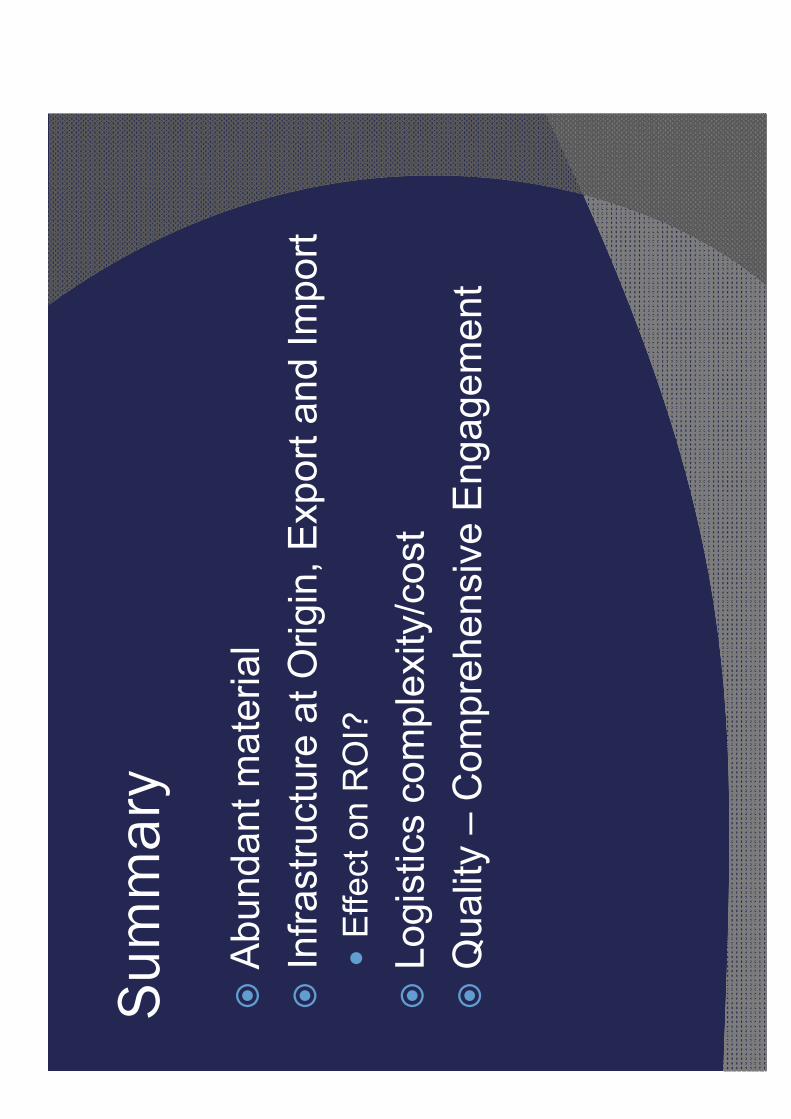

Sum

mar

y

Ab

unda

nt m

ater

ial

In

frast

ruct

ure

at O

rigin

, Exp

ort a

nd Im

port

Ef

fect

on

RO

I?

Logi

stic

s co

mpl

exity

/cos

t

Qua

lity

–C

ompr

ehen

sive

Eng

agem

ent

Than

k yo

u!

w

ww.

asia

ncoa

lash

.org

w

ww.

was

te-re

use.

com

w

ww.

coal

ashs

olut

ions

.com

Visi

t the

Coa

l Ash

Asi

a bo

oth

in th

e Ex

hibi

tion

Hal

l

Join

us

at C

oal A

sh A

sia!

Sept

embe

r 20-

24th

谢谢

!

Dav

id H

arris

d.ha

rris@

asia

ncoa

lash

.org

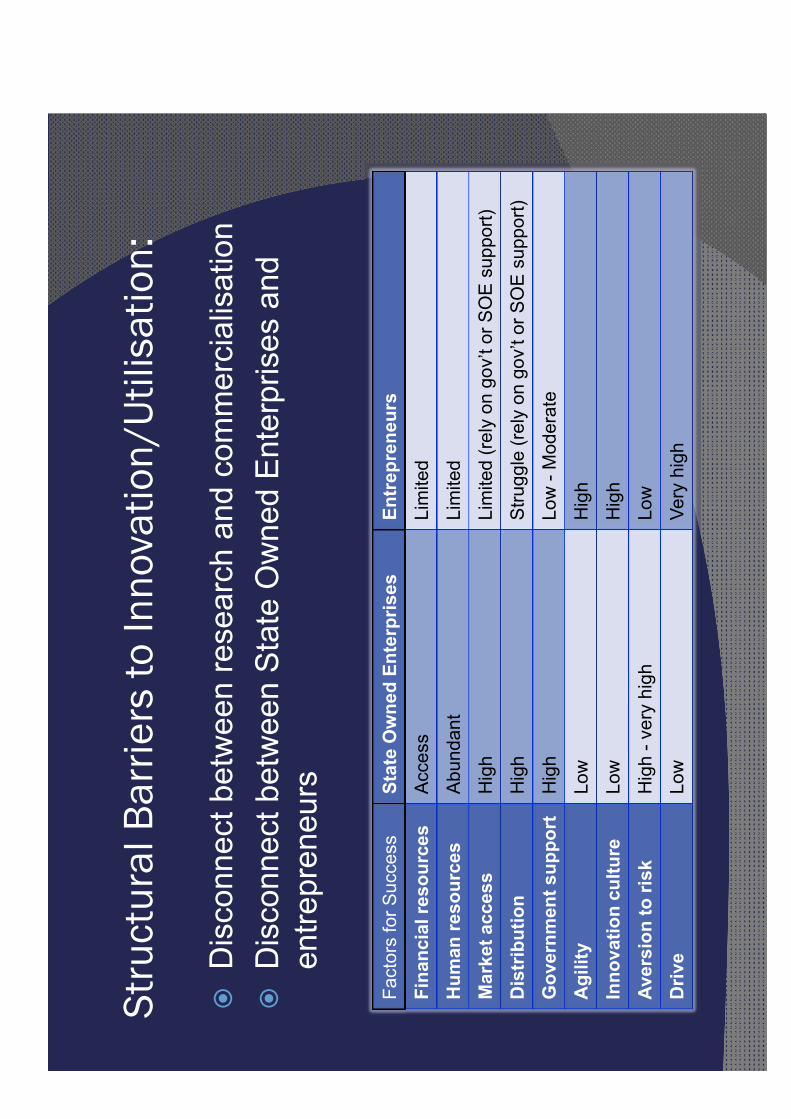

Stru

ctur

al B

arrie

rs to

Inno

vatio

n/U

tilis

atio

n:

D

isco

nnec

t bet

wee

n re

sear

ch a

nd c

omm

erci

alis

atio

n

Dis

conn

ect b

etw

een

Stat

e O

wne

d En

terp

rises

and

en

trepr

eneu

rs

Fact

ors

for S

ucce

ssSt

ate

Ow

ned

Ente

rpris

esEn

trep

rene

urs

Fina

ncia

l res

ourc

esAc

cess

Lim

ited

Hum

an re

sour

ces

Abun

dant

Lim

ited

Mar

ket a

cces

sH

igh

Lim

ited

(rely

on

gov’

t or S

OE

supp

ort)

Dis

trib

utio

nH

igh

Stru

ggle

(rel

y on

gov

’t or

SO

E su

ppor

t)

Gov

ernm

ent s

uppo

rtH

igh

Low

-M

oder

ate

Agi

lity

Low

Hig

h

Inno

vatio

n cu

lture

Low

Hig

h

Aver

sion

to ri

skH

igh

-ver

y hi

ghLo

w

Driv

eLo

wVe

ry h

igh

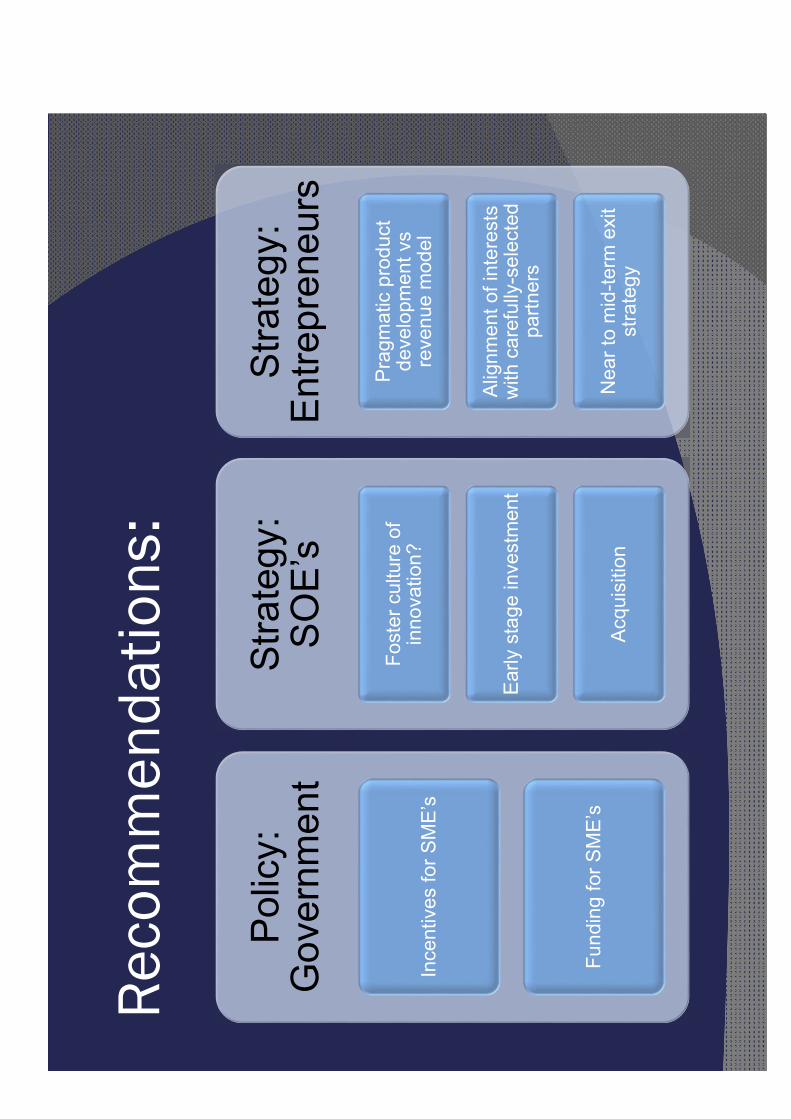

Rec

omm

enda

tions

:

Polic

y:

Gov

ernm

ent

Ince

ntiv

es fo

r SM

E’s

Fund

ing

for S

ME’

s

Stra

tegy

: SO

E’s

Fost

er c

ultu

re o

f in

nova

tion?

Early

sta

ge in

vest

men

t

Acqu

isiti

on

Stra

tegy

: En

trepr

eneu

rs

Prag

mat

ic p

rodu

ct

deve

lopm

ent v

s re

venu

e m

odel

Alig

nmen

t of i

nter

ests

w

ith c

aref

ully

-sel

ecte

d pa

rtner

s

Nea

r to

mid

-term

exi

t st

rate

gy