Embed Size (px)

Citation preview

CHAPTER – I

INTRODUCTION

INTRODUCTION1

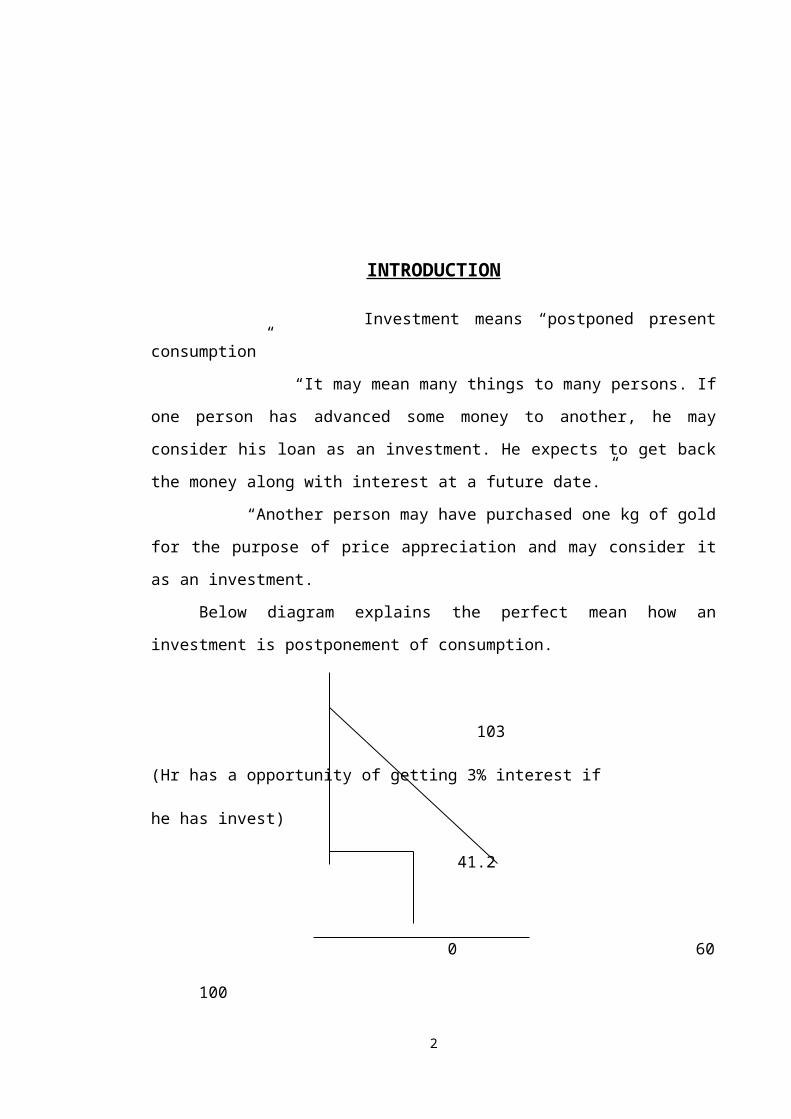

Investment means “postponed present consumption”

“It may mean many things to many persons. If one person has advanced some

money to another, he may consider his loan as an investment. He expects to get back the

money along with interest at a future date.”

“Another person may have purchased one kg of gold for the purpose of price

appreciation and may consider it as an investment.

Below diagram explains the perfect mean how an investment is postponement of

consumption.

103 (Hr has a opportunity of getting 3% interest if he has invest) 41.2

0 60 100

Co is the current year consumption axes he can consume high as 100 low as 0.

C1 is the next year consumption high as 103&low as 0

According to the diagram he consumed 60/- and he invested remaining 40/- he

got 41.2/- “so he got more

Avenues of investment

Corporate securities

Deposits in banks and non-banking companies

UTI and other mutual fund schemes

Post office deposits and certificates

Life insurance polices

Provident fund schemes

Government and semi-government securities

2

Driving forces of investment

Though there are many factors that influence the decision of investing in

assets, there are some main driving forces that cause investment in any society like

Retirement plan

Avoidance of taxation

Tempting high rates of interest

High inflation and resultant expectation of increase in the monetary return

Hike in income

Availability of a large number of investment avenues

Legal safeguards

Existence of financial institutions to encourage savings etc.,

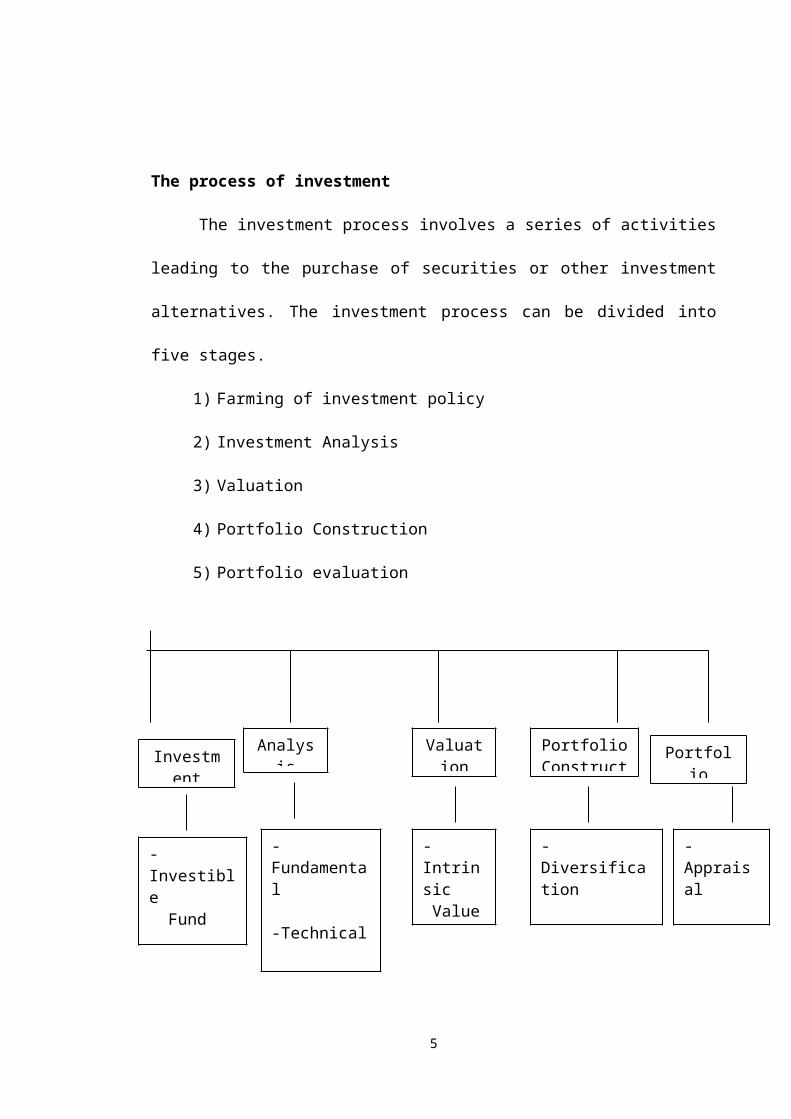

The process of investment

3

The investment process involves a series of activities leading to the purchase of

securities or other investment alternatives. The investment process can be divided into

five stages.

1) Farming of investment policy

2) Investment Analysis

3) Valuation

4) Portfolio Construction

5) Portfolio evaluation

Investment Policy4

Investment Policy

Analysis Valuation PortfolioConstruction

Portfolio Evaluation

-Investible Fund-Objectives-Knowledge

-Fundamental

-Technical

-Efficient Market Hypothesis

-Intrinsic Value-Future Value

-Diversification

-Selection & Allocation

-Appraisal

-Revision

The government or the investor before proceeding into investment formulates

the policy for the systematic functioning. The essential ingredients of the policy are the

Investible funds, objectives and the knowledge about the investment alternatives and

market.

Investible funds: The entire investment procedure revolves around the availability of

investible funds. The fund may be generated through savings or from borrowings. If the

funds are borrowed, the investor has to be extra careful in the selection of investment

alternatives. The return should be higher than the interest he pays. Mutual funds invest

their owner’s money in securities

.

Objectives: The objectives are framed on the premises of the required rate of return,

need for regularity of income, risk perception and the need for liquidity. The risk taker’s

objective is to earn high rate of return in the form of capital appreciation, whereas the

primary objective of the risk averse is the safety of the principle.

Knowledge: The knowledge about the investment alternatives and markets plays a key

role in the policy formulation, the investment alternatives range from security to real

estate, the risk and return associated with investment alternatives differ from each other.

Investment in equity is high yielding but has more risk than the fixed income securities.

The tax sheltered schemes offer tax benefits to the investors.

The investor should be aware of the stock market structure and the functions of

the brokers. The mode of operation varies among BSE, NSE, and OTCEI. Brokerage

charges are also different. The knowledge about the stock exchanges enables him to

trade the stock intelligently

Security Analysis

After formulating the investment policy, the securities to be bought have to be

scrutinized through either Fundamental analysis or Technical analysis or Efficient

Market Hypothesis theory.

Fundamental Analysis: Fundamental analysis is really a logical and systematic

approach to estimating the future dividends and share price. It is based on the basic

5

premise that share price is determined by a number of fundamental factors relating to

the economy, industry and company.

Technical Analysis: According to technical analysis the investors believe that share

prices are determined by the demand and supply forces operating in the market. These

demand and supply forces in turn are influenced by a number of fundamental factors as

well as certain psychological or emotional factors. Many of these factors cannot be

quantified. The technical analyst therefore concentrates on the movement of share

prices. He claims that by examining past share price movements future share prices can

be accurately predicted. Technical analysis is the name given to forecasting techniques

that utilize historical share price data.

The rationale behind technical analysis is that share price behavior repeats itself

over time and the analyst attempts to drive methods to predict this repetition.

Random Walk Theory:. There Stock prices are determined by a number of factors

such as fundamental factors, technical factors and psychological factors. The behavior

of stock prices is studied with the help of different methods such as fundamental

analysis and technical analysis. Fundamental analysis seeks to evaluate the intrinsic

value of securities by studying the fundamental factors affecting the performance of the

economy, industry and companies. Technical analysis believes that the past behavior of

stock prices gives an indication of the future behavior. It tries to study the patterns in

stock price behavior through charts and predict the future movement in pricesis a third

theory on stock price behavior, which questions the assumptions of technical analysis.

The basic assumption in technical analysis is that stock price movement is quite

orderly and not random. The new theory questions this assumption. From the results of

several empirical studies on stock price movements, the advocates of the new theory

assert that share price movements are random. The new theory came to be known as

Random Walk Theory because of its principal contention that share price movements

represent a random walk rather than an orderly movement.

Valuation

6

The valuation helps the investor to determine the return the return and risk

expected from an investment in the common stock. The intrinsic value of the share is

measured through the book value of the share and price earnings ratio. Simple

discounting models also can be adopted to value the shares. The stock market analysts

have developed many advanced models to value the shares. The real worth of the share

is compared with the market price and then the investment decisions and made.

Future value: Future value of the securities could be estimated by using a simple

statistical technique like rend analysis. The analysis of the historical behavior of the

price enables the investor to predict the future value.

Construction of a Portfolio

A portfolio is a combination of securities. The portfolio is constructed in such a

manner to meet the investor’s goals and objectives. The investor should decide how best

to reach the goals with the securities available. The investor tries to attain maximum

risk. Towards this end he diversifies his portfolio and allocates funds among the

securities.

Diversification: The main objective of diversification is the reduction of risk in the loss

of capital and income. A diversified portfolio is comparatively less risky than holding a

single portfolio. There are several ways to diversify the portfolio.

Debt and equity diversification Debt instruments provide assured return with

limited capital appreciation. Common stocks provide income and capital gain but with

the flavor of uncertainty. Both debt instruments and equity are combined to complement

each other.

Industry diversification Industries’ growth and their reaction to government

policies differ from each other. Banking industry shares may provide regular returns but

with limited capital appreciation. The information technology stock yields high return

and capital appreciation but their growth potential after the year2002 is not predictable.

Thus, industry diversification is needed and it reduces risk.

Company diversification Securities from different companies are purchased to

reduce risk. Technical analysts suggest the investors to buy securities based on the price

7

movement. Fundamental analysts suggest the selection of financially sound and investor

friendly companies

Selection: Based on the diversification level, industry and company analyses the

securities have to be selected. Funds are allocated for the selected securities. Selection

of securities and the allocation of funds and sales the construction of portfolio.

Evaluation

The portfolio has to be managed efficiently. The efficient management calls for

evaluation of the portfolio this process consists of portfolio appraisal and revision.

Appraisal: The return and risk performance of the security vary from time to time. The

variability in return of the securities is measured and compared. The developments in

the economy, industry and relevant companies from which the stocks are bought have

to0 be appraised. The appraisal warns the loss and steps cab be taken to avoid such

losses.

Revision: Depends on the results of the appraisal. The low yielding securities with high

risk are replaced with high yielding securities with low risk factor. To keep the return at

a particular level necessitates the investor to revise the components of the portfolio

periodically.

8

NEED OF THE STUDY

To overcome the rumors heard rather than by rational analysis, security analysis

and portfolio management has emerged as a separate discipline.

Portfolio management deals with the rational investment decision making

process.

Portfolio management deal with the analysis of individual securities as well as

with the theory and practice of optimally combining securities into portfolios.

Creation of portfolio helps to reduce risk without sacrificing returns.

SCOPE OF THE STUDY9

This scope of study is limited to few selected industries. Those are

Pharmaceutical, Information Technologies, Automobile, & Banking Industry.

In these industries, only some are selected. They are 6companies each from

pharmaceutical, I.T., Automobile industry and 12 companies from banking industry.

This study is analysis of previous twelve months (Jan-12 to Dec-12) data

relating to prices of shares in Bombay Stock Exchange only.

OBJECTIVES OF THE STUDY10

To ascertain the return both firm wise and industry wise as a whole

To know the risk factor in the firm and Industry as a whole

To know the fluctuations of the security prices of the selected firms.

To compare Industry index with BSE-200 Index in various aspects.

11

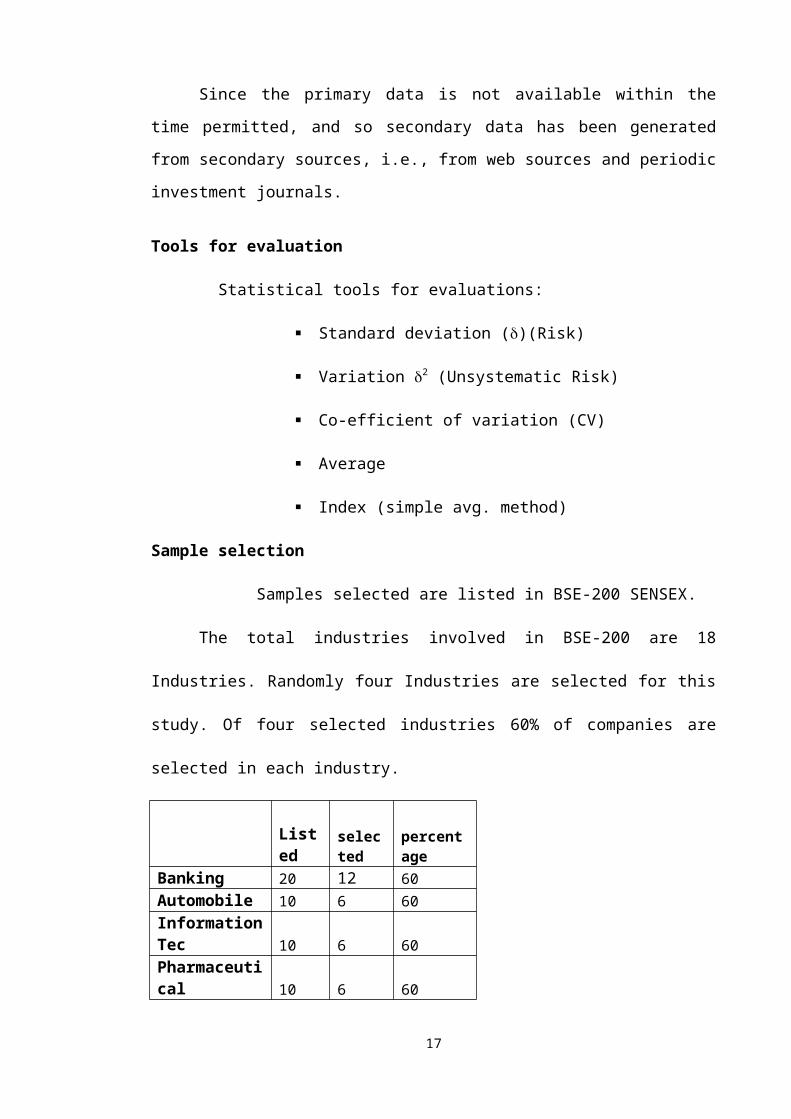

RESEARCH METHODOLOGY

Data Collection

Since the primary data is not available within the time permitted, and so

secondary data has been generated from secondary sources, i.e., from web sources and

periodic investment journals.

Tools for evaluation Statistical tools for evaluations:

Standard deviation ()(Risk)

Variation 2 (Unsystematic Risk)

Co-efficient of variation (CV)

Average

Index (simple avg. method)

Sample selection

Samples selected are listed in BSE-200 SENSEX.

The total industries involved in BSE-200 are 18 Industries. Randomly four

Industries are selected for this study. Of four selected industries 60% of companies are

selected in each industry.

Listed selected percentage

Banking 20 12 60Automobile 10 6 60Information Tec 10 6 60Pharmaceutical 10 6 60

12

CHAPTER - II

REVIEW OF LITERATURE

REVIEW OF LITERATURE

13

According to Adam. Y. C. Lei & Huihua.li (2012),

Motivated by an obvious gap between the widespread use of Bloomberg terminals in the

finance industry and the scant resources available to an instructor on how to incorporate

the available information through the terminal into a finance course, we illustrate our

experience using the terminal in an equity-focused security analysis and portfolio

management course. Our goal is to enable students inexperienced with the terminal to

prepare an analyst report. We identify the most significant challenges we face and

provide the corresponding solutions. Our results are also applicable to other finance

courses including financial analysis, investments, and student managed investment fund

According to Ali Asghary Karahroudy (2012),

Security Analysis and Framework of Cloud computing offers massive scalability,

immediate availability, and low cost services as major benefits, but as with most new

technologies, it introduces new risks and vulnerabilities too. Despite the fact that

different cloud structures and services are expanding, the cloud computing penetration

has not been as envisioned. Some specific concerns have stopped enterprises from

completely joining the cloud. One of the major disadvantages of using cloud computing

is its increased security risks. In this study I conduct an in depth analyses of

the different aspects of security issues in cloud computing and propose a file

distribution model as a possible solution to alleviate those security risks. It also shows

the effectiveness of the new security model as compared with those currently being

used. I present, a new file storage system with variable size chunks, distributed chunk

addressing, decentralized file allocation tables, spread deciphering key, randomly

selected file servers, and fault tolerant chunk system.\

According to Ran Canetti & IBM Research (2008),

Composable Formal Security Analysis, a security property of a protocol is composable

if it remains intact even when the protocol runs alongside other protocols in the same

system. We describe a method for asserting composable security properties, and

demonstrate its usefulness. In particular, we show how this method can be used to

provide security analysis that is formal, relatively simple, and still does not make un-

justified abstractions of the underlying cryptographic algorithms in use. It can also

greatly enhance the feasibility of automated security analysis of systems of realistic

size.

14

According to, Hari P. Sharma, Dinesh K. Sharma, Princess Anne Jana, (2008),,

The focus of this research paper is to develop a model for security analysis and

investment decisions using multi objective chance constrained programming (CCP).

Using relevant variables and constraints a deterministic nonlinear programming model

is derived using CCP technique. The model’s efficiency and effectiveness is also

evaluated as applied to a sample of stocks selected from the Dow Jones Industrial

Average compiled into a high yielding portfolio.

According to John T. Harvey, (2001),

Security analysis Psychological and Institutional Forces and the Determination

of Exchange Rates, Neoclassical economists, by their own admission, have had a

terrible time explaining foreign-currency prices. In large part, this is due to the fact that

they assume "economic" behavior to be independent of social and cultural influences.

But markets are social institutions. They "organize and guide human social behavior

through sanctions (formal and informal, negative and positive), mores, norms, status,

and shared worldviews". Consequently, explaining economic exchange requires an

understanding of the behavior associated with the subculture of those in question. The

purpose of this paper is to build a model of exchange rates that is based on the

assumption that Homo sapient behavior can only be understood in terms of its social

context. This will be accomplished in four steps. First, the participants in the market

will be identified. Second, their relative significance in the determination of prices will

be discussed. Third and most important, the psychological and institutional forces

molding the behavior of the most influential actors will be explained. Finally, the

implications for foreign exchange prices are outlined.

According to Stanis – aw – Gasik (2007),

Portfolio management, what is a project portfolio? May it contain a set of

investment project only? But in project-based organizations just commercial projects

and their sets are much more important than investment projects. Moreover, in such

organizations you may not easily strictly partition projects into investment and

commercial.Usually the first commercial project of given type delivered to a customer

is to some extent at the same time an investment project as the supplier develops new

techniques then. So even the full model of investment portfolios must cover commercial

project

15

According to keyser, leonid & jonathan W.Lewellen (2005),

The Capital Asset Pricing Model (CAPM), which relates the risk of an

individual security to its expected return, is frequently cited in investments textbooks

and the academic literature as a centerpiece of modem finance theory. The main

prediction of the CAPM is that investors are compensated in the form of expected return

only for bearing systematic or market risk, which is the portion of a security's risk that

cannot be diversified away. That investors demand reparation for and only for

systematic risk is a consequence from the pivotal assumption that all investors have

identical information for the entire universe of publicly traded securities. In actuality,

professional active money managers rarely invest in a portfolio broad enough to be

considered the market portfolio. Instead, the asset management industry has self-

organized over time according to a top-down investment process, where asset allocators

provide capital to security selectors who specialize in high-yield bonds, large-cap value

stocks, and the like. Any losses in diversification benefits resulting from this

theoretically suboptimal two-phase investment strategy are deemed an unavoidable cost

of obtaining accurate forecasts through specialization in security analysis and portfolio

management.

According to Alex Kane, Alan J. Marcus, and Robert R. Trippi (1999),

Active portfolio management is commonly partitioned into two types of

activities: market timing, which requires forecasts of broad-based market movements,

and security analysis, which requires the selection of individual stocks that are

perceived to be underpriced by the market. Robert Merton and others have provided an

insightful and easily implemented means to place a value on market timing and

fundamental analysis skills. While a normative theory of stock selection was outlined in

1973 by Jack Treynor and Fischer Black, no convenient means of valuing potential

selection ability has yet been devised. In this article the authors present a framework for

estimating the value of security analysis, be it by human or computer.

16

CHAPTER – III

INDUSTRY PROFILE&

COMPANY PROFILE

INDUSTRY PROFILE

Security market and Capital market

17

There are 22 stock exchanges in India, the first being the Bombay Stock

Exchange (BSE), which began formal trading in 1875, making it one of the oldest in Asia.

Over the last few years, there has been a rapid change in the Indian securities market,

especially in the secondary market. Advanced technology and online-based transactions

have modernized the stock exchanges. In terms of the number of companies listed and

total market capitalization, the Indian equity market is considered large relative to the

country’s stage of economic development. The number of listed companies increased

from 5,968 in March 1990 to about 10,000 by May 1998 and market capitalization has

grown almost 11 times during the same period.

Trading practices were not transparent, and there was a large amount of insider

trading. Recognizing the importance of increasing investor protection, several measures

were enacted to improve the fairness of the capital market. The Securities and Exchange

Board of The debt market, however, is almost nonexistent in India even though there has

been a large volume of Government bonds traded. Banks and financial institutions have

been holding a substantial part of these bonds as statutory liquidity requirement. The

portfolio restrictions on financial institutions’ statutory liquidity requirement are still in

place. A primary auction market for Government securities has been created and a

primary dealer system was introduced in 1995. There are six authorized primary dealers.

Currently, there are 31 mutual funds, out of which 21 are in the private sector. Mutual

funds were opened to the private sector in 1992. Earlier, in 1987, banks were allowed to

enter this business, breaking the monopoly of the Unit Trust of India (UTI), which

maintains a dominant position. Before 1992, many factors obstructed the expansion of

equity trading. Fresh capital issues were controlled through the Capital Issues Control

Act.

India (SEBI) was established in 1988. Despite the rules it set, problems continued

to exist, including those relating to disclosure criteria, lack of broker capital adequacy,

and poor regulation of merchant bankers and underwriters. There have been significant

reforms in the regulation of the securities market since 1992 in conjunction.

With overall economic and financial reforms. In 1992, the SEBI Act was enacted

giving SEBI statutory status as an apex regulatory body. And a series of reforms was

introduced to improve investor protection, automation of stock trading, integration of

national markets, and efficiency of market operations. India has seen a tremendous

change in the secondary market for equity. Its equity market will most likely be 18

comparable with the world’s most advanced secondary markets within a year or two. The

key ingredients that underlie market quality in India’s equity market are

• Exchanges based on open electronic limit order book;

• Nationwide integrated market with a large number of informed traders and

fluency of short or long positions; and

• No counterparty risk.

Among the processes that have already started and are soon to be fully

implemented are electronic settlement trade and exchange-traded derivatives. Before

1995, markets in India used open outcry, a trading process in which traders shouted and

hand signaled from within a pit. One major policy initiated by SEBI from 1993 involved

the shift of all exchanges to screen-based trading, motivated primarily by the need for

greater transparency. The first exchange to be based on an open electronic limit order

book was the National Stock Exchange (NSE), which started trading debt instruments in

June 1994 and equity in November 1994. In March 1995, BSE shifted from open outcry

to a limit order book market. Currently, 17 of India’s stock exchanges have adopted open

electronic limit order.

Before 1994, India’s stock markets were dominated by BSE. In other parts of the

country, the finding capital market: recent developments and policy issues 113 financial

industry did not have equal access to markets and was unable to participate in forming

prices, compared with market participants in Mumbai (Bombay). As a result, the prices in

markets outside Mumbai were often different from prices in Mumbai. These pricing errors

limited order flow to these markets. Explicit nationwide connectivity and implicit

movement toward one national market has changed this situation (Shah and Thomas,

1997). NSE has established satellite communications which give all trading members of

NSE equal access to the market. Similarly, BSE and the Delhi Stock Exchange are both

expanding the number of trading terminals located all over the country. The arbitrages are

eliminating pricing discrepancies between markets. Despite these big improvements in

microstructure, the Indian capital market has been in decline during the last three years.

The amount of capital issued has dropped from the level of its peak year, 1994/95, and so

have equity prices. In 1994/95, Rs276 billion was raised in the primary equity market.

This figure fell to Rs208 billion in 1995/96 and to Rs142 billion in 1996/97. The BSE-30

index or Sensex, the sensitivity index of equity prices, peaked at 4,361 in September 1994

19

and fell during the following years. A leading cause was that financial irregularities and

overvaluations of equity prices in the earlier years had eroded public confidence in

corporate shares. Also, there was a reduced inflow of foreign investment after the

Mexican and Asian financial crises. In a sense, the market is now undergoing a period of

adjustment. Thus, it is time for regulatory authorities to make greater efforts to recover

investors’ confidence and to further improve the efficiency and transparency of market

operations.

The Indian capital market still faces many challenges if it is to promote more

efficient allocation and mobilization of capital in the economy. First, market infrastructure

has to be improved as it hinders the efficient flow of information and effective corporate

governance. Accounting standards will have to adapt to internationally accepted

accounting practices. The court system and legal mechanism should be enhanced to better

protect small shareholders’ rights and their capacity to on it or corporate activities.

Second, the trading system has to be made more transparent.

Stock market primary market

Since 1991/92, the primary market has grown fast as a result of the removal of

investment restrictions in the overall economy and a repeal of the restrictions imposed

by the Capital Issues Control Act. In 1991/92, Rs62.15 billion was raised in the primary

market. This figure rose to Rs276.21 billion in 1994/95. Since 1995/1996, however,

smaller amounts have been raised due to the overall downtrend in the market and tighter

entry barriers introduced by SEBI for investor protection.

Equity price

For the past 12 years, equity prices have seen two extended periods of declining

prices and two periods of rising prices. Between April 1986 and March 1988, Sensex

decreased from 589 to 398, or by 32 percent. Prices also fell between March 1992, when

the monthly closing level of Sensex was 4,258, and April 1993, when the level was

2,122, a decline of 50.5 percent. Prices generally rose for extended periods from March

1988 to March 1992 and from May 1993 to August 1994. The monthly closing level of

Sensex climbed from 398 in March 1988 to 4,285 in March 1992, an increase of more

than 10 times. In the second period of extended rising equity prices, Sensex increased

20

1.16 times. Since 1995, it has fluctuated around the 3,000-4,000 mark In April 1998,

it hovered around 3,000. In the period of declining prices, from August 1994 to March

1998, the price-earnings (P/E) ratio fell more sharply than prices (Figure 1). In March

1998, the monthly average Sensex P/E ratio was 15.65 while the figure for October

1993 was 38.76.

Risk Management System

SEBI has taken several measures to improve the integrity of the secondary

market. Legislative and regulatory changes have facilitated the corporatization of

stockbrokers. Capital adequacy norms have been prescribed and are being enforced. A

mark-to-market margin and intraday trading limit have also been imposed. Further, the

stock exchanges have put in place circuit breakers, which are applied in times of

excessive volatility. The disclosure of short sales and long purchases is now required at

the end of the day to reduce price volatility and further enhance the integrity of the

secondary market.

Mark-to-market margin and intraday limit

Under the current clearing and settlement system, if an Indian investor buys and

subsequently sells the same number of shares of stock during a settlement period, or

sells and subsequently buys, it is not necessary to take or deliver the shares. The

difference between the selling and buying prices can be paid or received. In other

words, the squaring-off of the trading position during the same settlement period results

in non delivery of the shares that the. A short-term and speculative investment is thus

possible at a relatively low cost. FIIs and domestic institutional investors are, however,

not permitted to trade without delivery, since non delivery transactions are limited only

to individual investors. One of SEBI’s primary concerns is the risk of settlement chaos

that may be caused by an increasing number of non delivery transactions as the stock

market becomes excessively speculative. Accordingly, SEBI has introduced a daily

mark-to-market margin and intraday trading limit. The daily mark-to market margin is a

margin on a broker’s daily position. The intraday trading limit is the limit to a broker’s

intraday trading volume. Every broker is subject to these requirements. Each stock

exchange may take any other measures to ensure the safety of the market. BSE and NSE

impose on members a more stringent daily margin, including one based on

concentration of business. A daily mark-to-market margin is 100 percent of the notional

21

loss of the stockbroker for every stock, calculated as the difference between buying or

selling price and the closing price of that stock at the end of that day. However, there is

a threshold limit of 25 percent of the base minimum capital plus additional capital kept

with the stock exchange or Rs1 million, whichever is lower. Until the notional loss

exceeds the threshold limit, the margin is not payable. This margin is payable by a

stockbroker to the stock exchange in cash or as a bank guarantee from scheduled

commercial bank, on a net basis. It will be released on the pay-in day for the settlement

period. The margin money is held by the exchange for 6-12 days.This costs the broker

about 0.4-1.2 percent of the notional loss, assuming that the broker’s funding cost is

about 24-36 percent (Endo 1998). Thus, speculative trading without the delivery of

shares is no longer cost-free.

Each broker’s trading volume during a day is not allowed to exceed the intraday

trading limit. This limit is 33.3 times the base minimum capital deposited with the

exchange on a gross basis, i.e., purchase plus sale. In the event of brokers wishing to

exceed this limit, they have to deposit additional capital with the exchange and this

cannot be withdrawn for six months.

Circuit Breaker

SEBI has imposed price limits for stocks whose market prices are above Rs10

up to Rs20, a daily price change limit and weekly price change limit of 25 percent. BSE

imposes price limits as a circuit breaker system to maintain the orderly trading of shares

on the exchange. BSE’s computerized trading system rejects buy or sell orders of a

stock at prices outside the price limits. The daily price limit of a stock is measured from

the stock’s closing price in the previous trading session. The weekly price limit is based

on its closing price of the last trading in the previous week, usually its closing price on

the previous Friday.

Short sales and long purchases

SEBI regulates short selling in the stock market by requiring all stock exchanges to

enforce reporting by members of their net short sale and long purchase positions in each

stock at the end of each trading day.

22

Stock Lending

A scheme for regulating stock lending was introduced in February 1997,

following changes in tax regulations. Stock lending can take place through an

intermediary registered for this purpose with SEBI, and which has a minimum capital of

Rs500 million. Lenders and borrowers of securities have to enter into agreements with

the intermediary. Stock lending facilitates the timely settlement of transactions on the

stock exchanges, especially in an environment where physical delivery of certificates is

required for settlement

Stockbrokers

Most stockbrokers in India are still relatively small. They cannot afford to

directly cover every retail investor in a geographically vast country and in such a

complex society. Thus, they are permitted to transact with sub brokers as the latter play

an indispensable role in intermediating between investors and the stock market.

An applicant for a sub broker certificate must be affiliated with a stockbroker of

a recognized stock exchange. A sub broker application may take the form of sole

proprietorship, partnership, or corporation. There are two major issues concerning sub

broker sin the Indian capital market:

• Majority of sub brokers are not registered with SEBI;

• The function of the sub broker is not clearly defined. No sub broker is

supposed to buy, sell, or deal in securities, without a certificate granted by SEBI.

Nevertheless, there were only about 2,593 sub brokers registered with SEBI as of end-

June 1997, while the number of stock sub brokers in India was estimated in the range of

50,000 to 200,000 (Endo, 1998).The Indian law defines a sub broker as any person, not

being a member of a stock exchange, who acts on behalf of a stockbroker as an agent, or

otherwise, to assist the investors in buying, selling, or dealing securities through such a

stockbroker. Based on this definition, the sub broker is either a stockbroker’s agent or

an arranger for the investor. Thus, legally speaking, the stockbroker as a principal will

be responsible to the investor for a sub broker’s conduct if a sub broker acts as his or

her agent. However, the market practice is different from this legally defined

relationship. In reality, the stockbroker, in general, issues a contract note of a

transaction even to a registered sub broker, thus treating the latter as counterparty. This

implicitly denies the stockbroker’s privities with the investor. NSE does not officially

23

allow its members to transact with end-investors through a sub broker. This is probably

because NSE has liberal membership criteria

And its computerized trading network can easily provide geographically

scattered stockbrokers with direct access to trading on NSE. Nevertheless, many trading

members of NSE have been using registered and unregistered subbrokers. To sort out

this confusion, SEBI enforced the following measures in March 1997:

• Initiation of criminal actions on complaints received against unregistered sub-

brokers in suitable cases;

• Revival of the institution of “remises” under rules and by laws of the stock

exchanges;

• Prohibition of stockbrokers in dealing with unregistered sub brokers or

unregistered remise sifter 1 June 1997 (this deadline was later extended to 1 July

1997).In spite of these actions, the confusion has remained. There is a need to address

the basic issue of clarifying the role of the sub broker and to operationally define its

relationship with the stockbrokers.

Merchant Bankers

Under the old regulations, there were four categories of registered merchant

bankers with different minimum net worth requirements. Under the new regulations, the

categories were abolished. Among other provisions, a merchant banker applicant is

required to have a minimum net worth of Rs50 million. The new regulations have

drawn a clear-cut line between the merchant banker and the nonbanking finance

company (NBFC). Under the old regulations, a merchant banker is permitted to carry

out fund based activities such as deposit-taking, leasing, bill discounting and hire-

purchasing. The new regulations no longer allow a merchant banker to engage in these

fund-based activities except for those related exclusively to the capital market such as

underwriting. The merchant banker is required to cease such activities within two years.

Correspondingly, an existing NBFC performing merchant banking activities is required

to relinquish such activities after a certain period of time. The merchant banking

industry in India has many problems, the main ones being that there are too many

merchant bankers, and that they are considered to be relatively incompetent. Only 20

merchant bankers account for 60-85 per cent of the merchant banking business, while

148 of them are in business only on paper. In May 1997, a substantial number of

merchant bankers were found to be professionally imprudent or negligent (Endo 1998). 24

SEBI listed 134 merchant bankers of Categories I, II, and III who broke their

underwriting commitments for possible disciplinary actions. Of this number, 95 were in

Category I. Furthermore, there have been records of listing delay or rejection of initial

public offerings (IPOs) in the recent past.

Fragmentation of regulatory authorities

The present functions and powers of regulatory agencies for the securities

market seem to be fragmented. SEBI is the primary body responsible for regulation of

the securities market, deriving its powers of registration and enforcement primarily from

the SEBI Act. There was an existing regulatory framework for the securities market,

provided by the Securities Contract Regulation (SCR) Act and the Companies Act,

administered by the Ministry of Finance and the Department of Company Affairs

(DCA) of the Ministry of Law, respectively. SEBI has been delegated most of the

functions and powers under the SCR Act, and shares the rest with the Ministry of

Finance. It has also been delegated certain powers under the Companies Act. RBI also

has regulatory involvement in the capital market regarding foreign exchange control

liquidity support to market participants and debt management through primary dealers.

It is RBI and not SEBI that regulates primary dealers in the Government securities

market. However, securities transactions that involve a foreign exchange transaction

need the permission of RBI. So far, fragmentation of the regulatory authorities has not

been a major obstacle to effective regulation of the securities market. Rather, lack of

enforcement capacity by SEBI has been a more significant cause of poor regulation. But

since the Indian stock markets are rapidly being integrated, the authorities may follow

the global trend of consolidation of regulatory authorities or better coordination among

them.

Market Stock

Fragmented market

25

Of the 22 stock exchanges in the country, 17 have introduced screen-based

trading. With the expansion of trading networks of BSE and other stock exchanges

beyond their original jurisdictions, an increasing number of investors in different parts

of the country are within the reach of a national market system. This has raised

informational efficiency and helped rapid market integration. NSE, which provides a

screen-based order driven system, has already extended its network to more than 100

centers in the country that are connected to its central computer via its satellite network.

The Over-the-Counter Exchange of India (OTCEI)

Provides a nationwide electronic system for trading relatively smaller stocks.

BSE has introduced its own screen-based quote-driven trading system. However, the

market is still fragmented and needs further integration. The international trend is to

consolidate and merge existing stock exchanges rather than to set up new ones. In the

UK, there were about 20 stock exchanges

In the late 1960s, which were reduced to about half a dozen in 1972 and further

down to one, i.e., the London Stock Exchange, in 1986. NSE has already provided

connectivity to more than 100 cities, and other major stock exchanges are in the process

of extending their trading terminals outside their places of operation. Thus, it is

questionable whether India needs as many as 22 stock exchanges, even taking into

account the vastness of the country.

Transaction Costs in the Secondary Market

Screen-based trading introduces a greater degree of transparency and reduces

spreads. Market manipulation becomes more difficult with screen-based trading and

easier to investigate on account of the transparent audit trails that are established. As

estimated by Shah and Thomas (1997), the total transaction costs in India’s equity

market have been reduced by half, i.e., from 5 to 2.5 percent since the introduction of

screen-based trading (Table 8). But this is still high compared to advanced markets.

When depository, derivatives, and indexation are fully in place, the transaction costs of

the Indian equity market could be even lower than those of most advanced countries.

Debt Market

26

The debt market is not well developed in India. Even though the volume of

Government bonds outstanding is large, banks and other financial institutions hold a

substantial part of these bonds as liquidity requirement. The statutory liquidity

requirement (on top of cash requirement of 10 percent) has been reduced from 25 to 23

percent. But this is still high and should be further decreased to activate the private debt

market.

Mark-to-market

Banks tend to hold Government securities to maturity to avoid a capital loss on

the balance sheet. Until 1996, only 40 percent of the portfolio of Government securities

had to be marked-to-market. Starting fiscal year 1996/97, the requirement has been

raised to 50 percent for existing banks and 100 percent for the new private sector banks.

The pattern of ownership of Government securities is shown in Table 9. The biggest

holders of both central and state Government securities are commercial banks, with

more than two thirds of the total. Life insurance companies have also increased their

holdings of Government securities. Banks and life insurance companies are captive

markets for Government securities due to the portfolio restrictions imposed on them.

Meanwhile, the market for private companies’ debentures is not yet well developed.

COMPANY PROFILE27

India bulls are India’s leading Financial, Real Estate and Power Company with a

wide presence throughout India. They ensure convenience and reliability in all their

products and services. India bulls have over 640 branches all over India. The customers

of India bulls are more than 4,50,000 which covers from a wide range of financial

services and products from securities, derivatives trading, depositary services, research

& advisory services, consumer secured & unsecured credit, loan against shares and

mortgage & housing finance. The company employs around 4000 Relationship

managers who help the clients to satisfy their customized financial goals. India bulls

entered the Real Estate business in the year 2005 with its group of companies. Large

scale projects worth several hundred million dollars are evaluated by them.

India bulls financial services Ltd. is listed on the National Stock Exchange (NSE),

Bombay Stock Exchange (BSE) and Luxembourg Stock Exchange. The market

capitalization of India bulls is around USD 2500 million (29thDecember, 2006).

Consolidated net worth of the group is around USD 700 million. India bulls and its

group companies have attracted USD 500 million of equity capital in Foreign Direct

Investment (FDI) since March 2000. Some of the large shareholders of India bulls are

the largest financial institutions of the world such as Fidelity Funds, Goldman Sachs,

Merrill Lynch, Morgan Stanley and Farallon Capital.

Growth of India bulls

Year 2000-2001

One of India’s first trading platforms was set up by India bulls Financial Services Ltd.

with the development of an in-house team.

Year 2001-2003

The service offered by India bulls was increased to include Equity, F&O, Wholesale

Debt, Mutual fund, IPO Financing/Distribution and Equity Research.

Year 2003-2004

In this particular year India bulls ventured into Distribution and Commodities Trading

business.

Year 2004-2005

28

This was one of the most important years in the history of Indiabulls. In this

year:

India bulls came out with its initial public offer (IPO) in September 2004.

India bulls started its Consumer Finance business.

India bulls entered the Indian Real Estate market and became the first company

to bring FDI in Indian Real Estate.

India bulls won bids for landmark properties in Mumbai.

Year 2008-2009

Several developments across its group companies have propelled India bulls

forward and are expected to continue to power the rise of this conglomerate. India bulls

financial services limited has recently signed a joint venture agreement with sogecap,

the insurance arm of Society General (SocGen) for its upcoming life insurance venture.

At the same time it has also signed a Memorandum of understanding with

MMTC.

On the asset management front, the company has received formal approval from SEBI

and is expected to shortly launch its first NFO.

India bulls enter in to Public issue for his India bulls power Ltd.

Promoters for India bulls

Sameer Gehlaut, Rajiv Rattan and Saurabh Mittal are the promoters of India bulls

Financial Services Ltd. While Sameer Gehlaut will have a 23.0% stake in the company

post the IPO, Rajiv Rattan and Saurabh Mittal will have a post issue holding of 11.5%

and 10.1% respectively.

All the three promoters of the company are engineering graduates while Saurabh

Mittal is a management graduate as well.

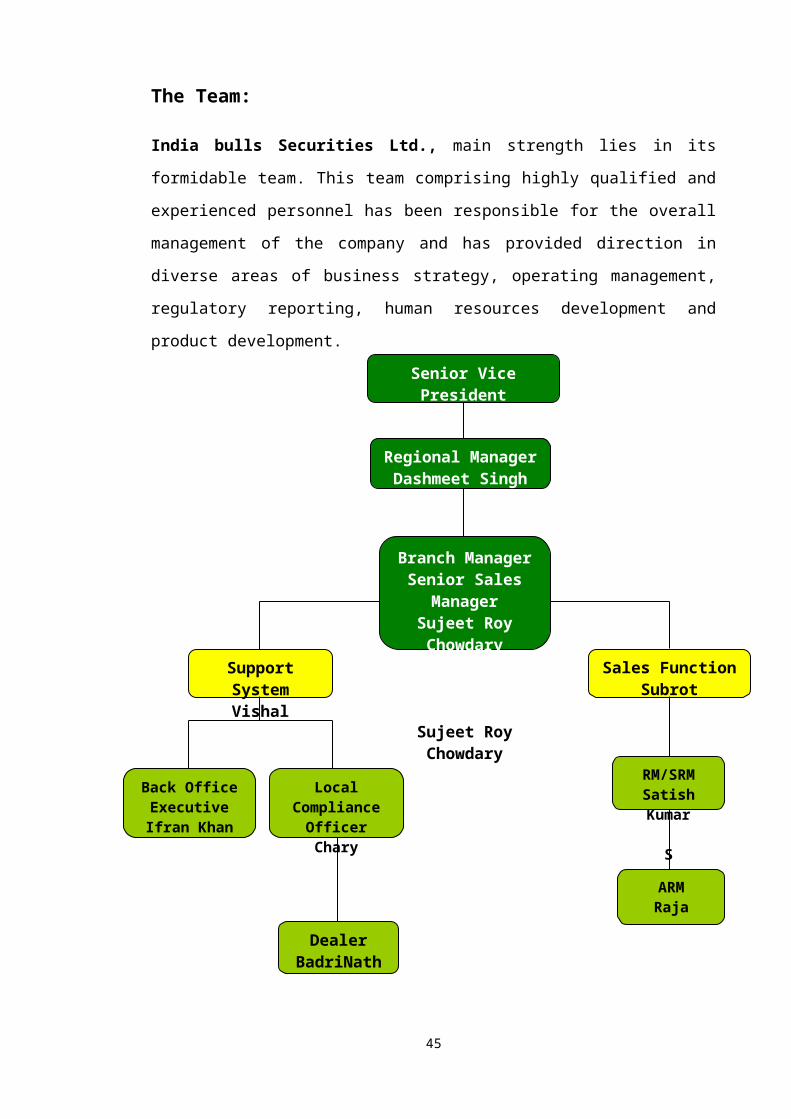

The Team:

29

Senior Vice PresidentYuv Raj Singh

Regional ManagerDashmeet Singh

Branch ManagerSenior Sales

ManagerSujeet Roy Chowdary

Sujeet Roy Chowdary

Support SystemVishal

Sales FunctionSubrot

RM/SRMSatish Kumar

S

ARMRaja

Local Compliance

OfficerChary

Back OfficeExecutive

Ifran Khan

DealerBadriNath

India bulls Securities Ltd., main strength lies in its formidable team. This team

comprising highly qualified and experienced personnel has been responsible for the

overall management of the company and has provided direction in diverse areas of

business strategy, operating management, regulatory reporting, human resources

development and product development.

30

Vision statement: To become the preferred long term financial partner to a wide base

of customers whilst optimizing stake holder’s value

Mission statement: To establish a base of 1 million satisfied customers by 2010. We

will create this by being a responsible and trustworthy partner

Corporate action: An Approach to Business that reflects Responsibility, Transparency

and Ethical Behavior. Respect for Employees, Clients & Stakeholder groups

India bulls Group entities in India

India bulls Capital Services Ltd.

India bulls Commodities Pvt. Ltd.

India bulls Credit Services Ltd.

India bulls Finance Co. Pvt. Ltd

India bulls Housing Finance Ltd.

India bulls Insurance Advisors Pvt. Ltd.

India bulls Resources Ltd.

India bulls Securities Ltd.

India bulls Power Ltd.31

Reasons to choose India bulls Securities Ltd:

The India bulls Financial Services stock is the best performing stock in the

MSCI Index – the global benchmark for equity investment person who bought India

bulls shares in the IPO at Rs. 19 (US$ 0.48) in September 2004 has been rewarded

almost 100 times in three and a half years – a feat unparalleled in the history of Indian

capital markets.

India bulls Real Estate Limited partnered Farallon Capital Management LLC of

the US to bring the first Foreign Direct Investment into real estate

Six Reasons why investing with India bulls Securities Limited is smarter

1) Customization: Formulates investment plans based on customer individual

requirements

2) Expertise: Brings within customer reach, about institutional expertise and companies

valuable understanding of the financial markets

3) One-stop shop: Caters to all customers’ investment needs under one roof.

4) Trust: Enjoys the pedigree of India bulls Securities Ltd and share its expertise in

financial services.

5) Personalized service: Helps customer through the entire investment process, step by

step, with innovative and efficient services.

6) Unbiased & Objective advice: We partner you in your investment process, with our

team of expert investment advisors

Products provided

Power India bulls

An online trading system designed for the high-volume trader. The platform provides

enhanced trade information and executes orders on an integrated software based trading

platform.

India bulls financial service offers:

32

SME finance

Mortgage loans

Commercial vehicle loans

Farm equipment loans

Commercial credit loans

Loan against shares and

Third part distribution of insurance products.

Broking: Equity, Derivatives, Commodities, Currency Derivatives.

Distribution: Mutual funds, IPO’s, Home loans, Insurance.

Divisions:

Investment Advisory and Broking? Division

Project Syndication Division?

Institutional Equity Broking? Division

Institutional Debt Broking? Division

Retail Offerings:

Wealth Management Services

Portfolio Management Services

Securities Broking-Equities and derivatives

Depository & Custodial Service & Distribution of financial Products.

Services:

India bulls securities provide a wide range of services that include:

33

Power India bulls: An online trading system designed for the high-volume trader. The

platform provides enhanced trade information and executes orders on an integrated

software based trading platform.

1) Equities,

2) Commodities,

3) Wholesale debts,

4) Futures and options,

5) Depository services,

6) Equity research services,

7) Post Trade – Custodian,

8) Depository Services,

9) Payment Gateway,

10) Other back office support,

Online Banks Tie-ups for trading:

Company having online transaction tie-ups with banks like,

HDFC BANK,

ICICI BANK,

IDBI BANK,

CITI BANK.

Company competitors

Kotak Securities Ltd,

ICICI Securities Ltd,

HDFC Securities Ltd,

Religare Securities Ltd,

34

Birla Money,

Indiainfoline Ltd

Company Achievements

The India bulls Group is one of the top fifteen conglomerates in the country with

businesses in several significant sectors.

The India bulls Financial Services stock is the best performing stock in the MSCI Index

– the global benchmark for equity investments.

India bulls Real Estate Limited partnered Farallon Capital Management LLC of the US

to bring the first Foreign Direct Investment into real estate.

India bulls Financial Services Limited was accorded the highest rating P1+ for

short term debt and the highest rating of AAA (SO) by CRISIL for loan receivables

securitization while India bulls Securities Limited is the only broker in India to be

assigned CRISIL’s highest broker quality grading of BQ1.

In December 2007, India bulls acquired Pyramid Retail including Piramyd

Megastores and Trumart, their chain of lifestyle and convenience outlets

The Board of Directors

Mr.SameerGehalaut Chairman & CEO

GaganBanga Executive Director

Rajiv Rattan CEO

Shamsher Singh Director

Aishwaryakatoch Director

Karan Singh Director

PremPrakashMird Director

Saurabh K Mittal Executive Director

Amith Jain Company Secretary

35

CHAPTER - IV36

DATA ANALYSISAND

PRESENTATION

DATA ANALYSIS & INTERPRETATION

Return

A major purpose of investment is to get a return or income on the funds

invested. On a bond an investor expects to receive interest. On a stock, dividends may

be anticipated. The investor may expect capital gains from some investments and rental

income from some investments and rental income from house property. Return may

take several forms.

Measurement of Return

The purpose of investment is to get a return or income on the funds invested in

different financial assets. The most important characteristics of financial assets are the

size and variability of their future returns. Since the return on years many methods were

adopted for quantifying returns.

In this study I considered only prices but not dividend in the calculation

return because the investor’s main motive to invest in shares is makes the profit from

37

changes in prices of shares. That’s why I calculated return from the prices of the shares

only.

Return = (P1 – P0)/P0

Where: P1 = Closing price of the share

P0 = Opening price of the share

In this Chapter I show the returns for each unit wise and industry wise

Returns for banking industry

Return = (P1 – P0)/P0

Where: P1 = Closing price of the share

P0 = Opening price of the share

In this Chapter I show the returns for each unit wise and industry wise

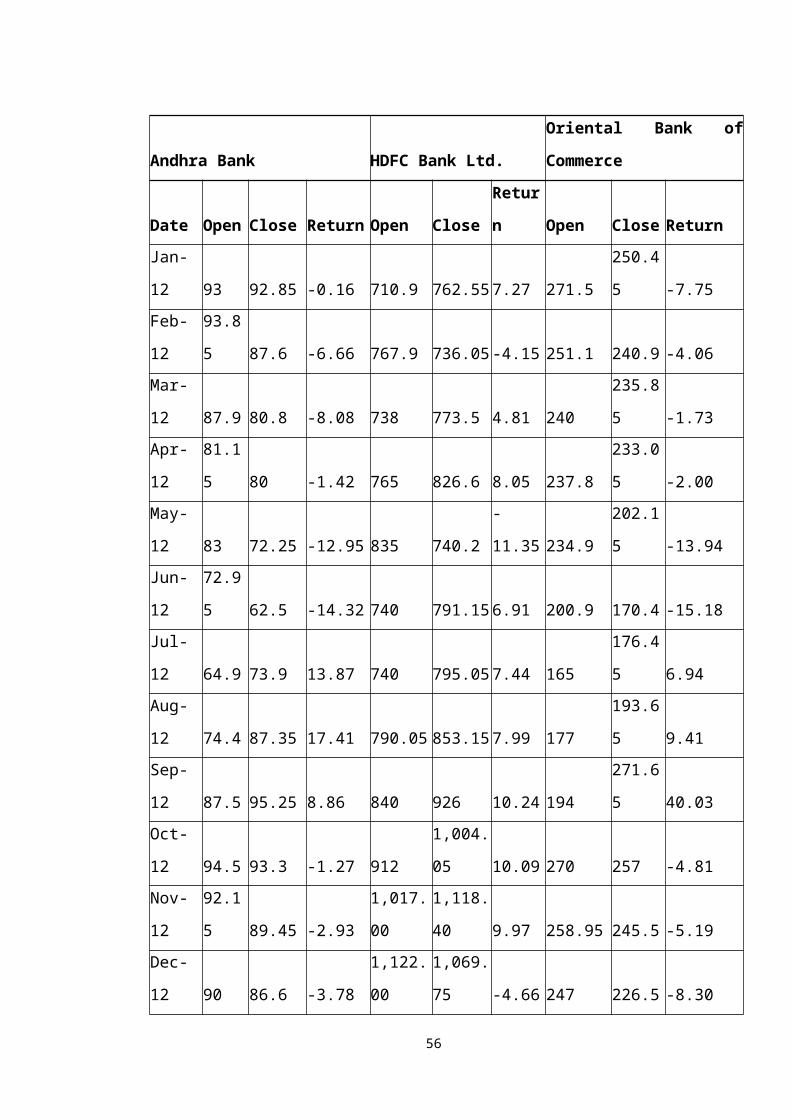

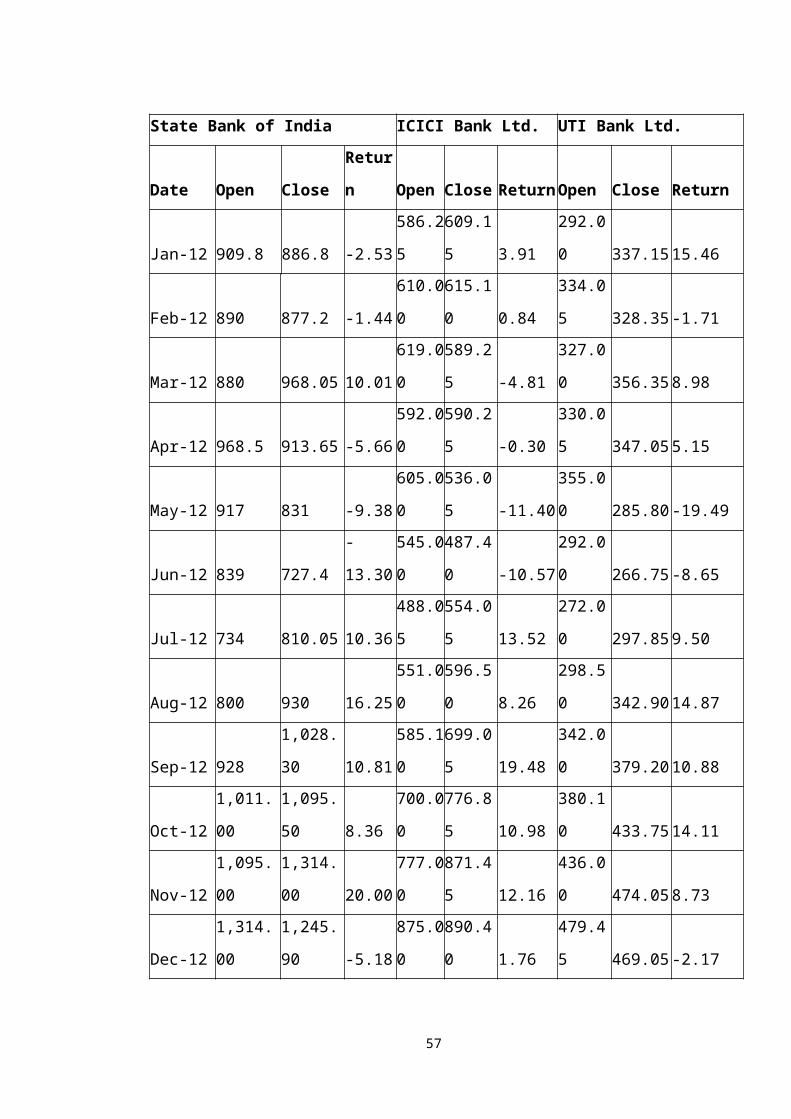

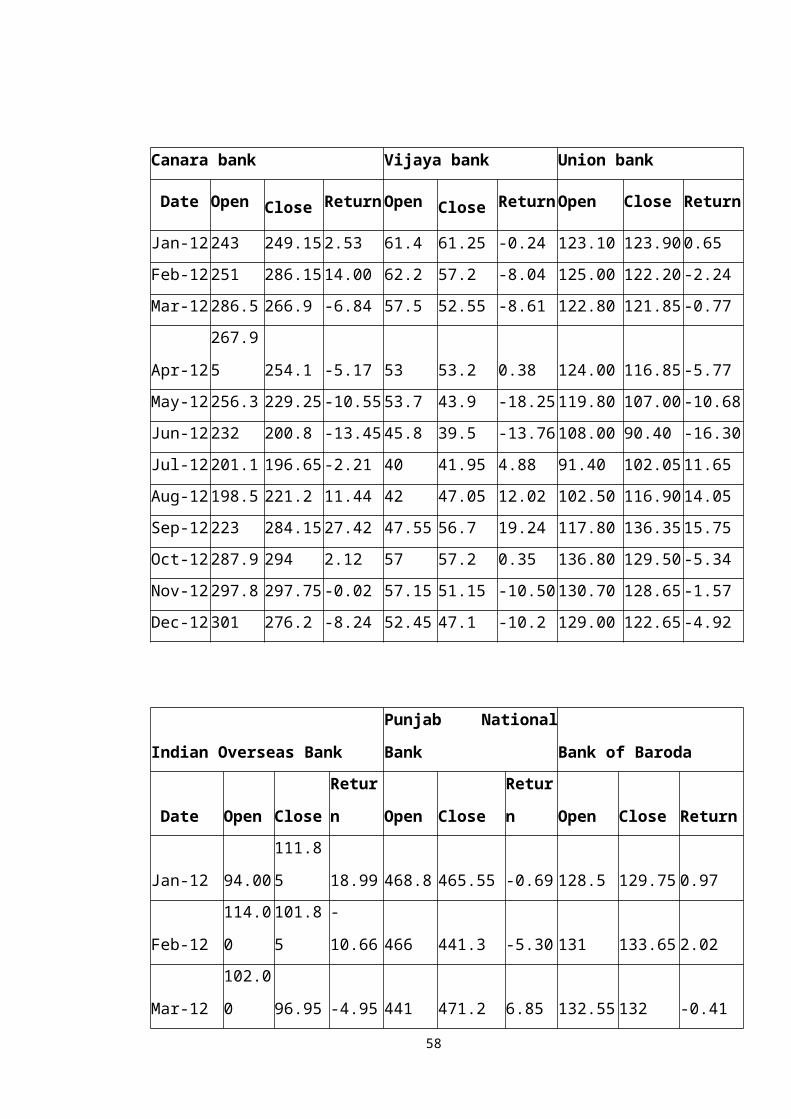

Table No. 1

Andhra Bank HDFC Bank Ltd. Oriental Bank of Commerce

Date Open Close Return Open Close Return Open Close Return

Jan-12 93 92.85 -0.16 710.9 762.55 7.27 271.5 250.45 -7.75

Feb-12 93.85 87.6 -6.66 767.9 736.05 -4.15 251.1 240.9 -4.06

Mar-12 87.9 80.8 -8.08 738 773.5 4.81 240 235.85 -1.73

Apr-12 81.15 80 -1.42 765 826.6 8.05 237.8 233.05 -2.00

May-12 83 72.25 -12.95 835 740.2 -11.35 234.9 202.15 -13.94

Jun-12 72.95 62.5 -14.32 740 791.15 6.91 200.9 170.4 -15.18

Jul-12 64.9 73.9 13.87 740 795.05 7.44 165 176.45 6.94

Aug-12 74.4 87.35 17.41 790.05 853.15 7.99 177 193.65 9.41

Sep-12 87.5 95.25 8.86 840 926 10.24 194 271.65 40.03

Oct-12 94.5 93.3 -1.27 912 1,004.05 10.09 270 257 -4.81

Nov-12 92.15 89.45 -2.93 1,017.00 1,118.40 9.97 258.95 245.5 -5.19

Dec-12 90 86.6 -3.78 1,122.00 1,069.75 -4.66 247 226.5 -8.3038

State Bank of India ICICI Bank Ltd. UTI Bank Ltd.

Date Open Close Return Open Close Return Open Close Return

Jan-12 909.8 886.8 -2.53 586.25 609.15 3.91 292.00 337.15 15.46

Feb-12 890 877.2 -1.44 610.00 615.10 0.84 334.05 328.35 -1.71

Mar-12 880 968.05 10.01 619.00 589.25 -4.81 327.00 356.35 8.98

Apr-12 968.5 913.65 -5.66 592.00 590.25 -0.30 330.05 347.05 5.15

May-12 917 831 -9.38 605.00 536.05 -11.40 355.00 285.80 -19.49

Jun-12 839 727.4 -13.30 545.00 487.40 -10.57 292.00 266.75 -8.65

Jul-12 734 810.05 10.36 488.05 554.05 13.52 272.00 297.85 9.50

Aug-12 800 930 16.25 551.00 596.50 8.26 298.50 342.90 14.87

Sep-12 928 1,028.30 10.81 585.10 699.05 19.48 342.00 379.20 10.88

Oct-12 1,011.00 1,095.50 8.36 700.00 776.85 10.98 380.10 433.75 14.11

Nov-12 1,095.00 1,314.00 20.00 777.00 871.45 12.16 436.00 474.05 8.73

Dec-12 1,314.00 1,245.90 -5.18 875.00 890.40 1.76 479.45 469.05 -2.17

Canara bank Vijaya bank Union bank

Date Open Close Return Open Close Return Open Close Return

Jan-12 243 249.15 2.53 61.4 61.25 -0.24 123.10 123.90 0.65

Feb-12 251 286.15 14.00 62.2 57.2 -8.04 125.00 122.20 -2.24

Mar-12 286.5 266.9 -6.84 57.5 52.55 -8.61 122.80 121.85 -0.77

Apr-12 267.95 254.1 -5.17 53 53.2 0.38 124.00 116.85 -5.77

May-12 256.3 229.25 -10.55 53.7 43.9 -18.25 119.80 107.00 -10.68

Jun-12 232 200.8 -13.45 45.8 39.5 -13.76 108.00 90.40 -16.30

Jul-12 201.1 196.65 -2.21 40 41.95 4.88 91.40 102.05 11.65

Aug-12 198.5 221.2 11.44 42 47.05 12.02 102.50 116.90 14.05

Sep-12 223 284.15 27.42 47.55 56.7 19.24 117.80 136.35 15.75

Oct-12 287.9 294 2.12 57 57.2 0.35 136.80 129.50 -5.34

Nov-12 297.8 297.75 -0.02 57.15 51.15 -10.50 130.70 128.65 -1.57

Dec-12 301 276.2 -8.24 52.45 47.1 -10.2 129.00 122.65 -4.92

39

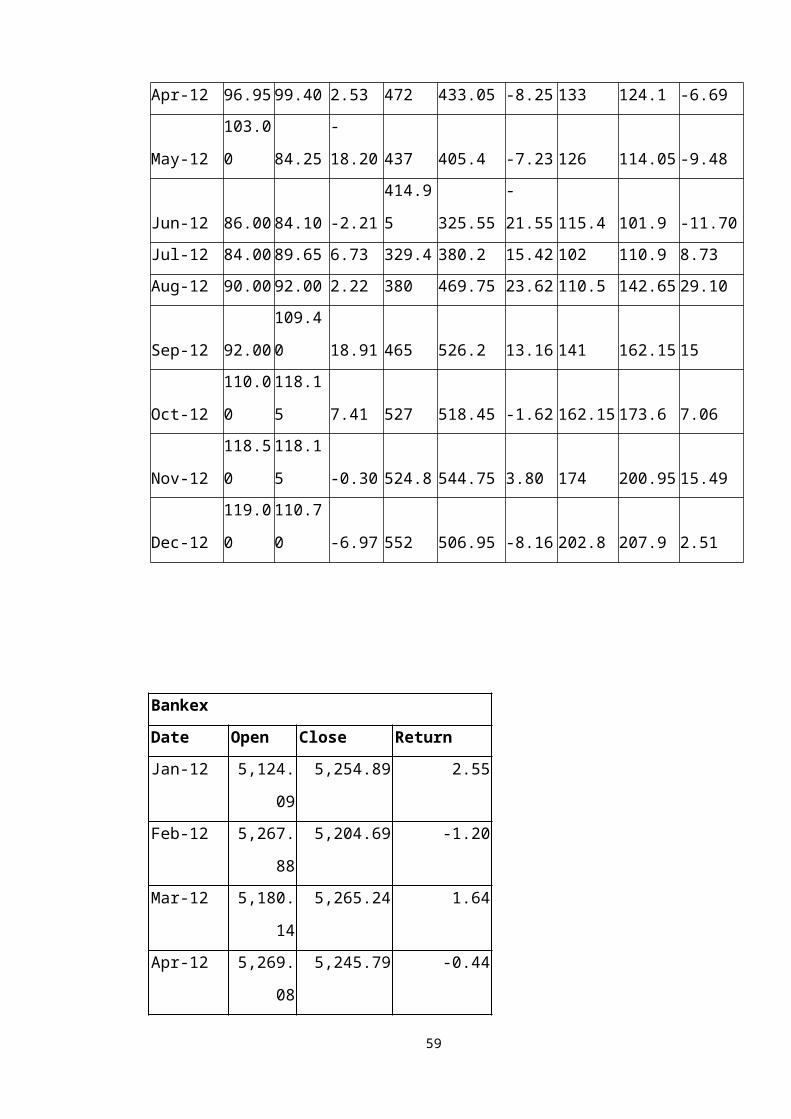

Indian Overseas Bank Punjab National Bank Bank of Baroda

Date Open Close Return Open Close Return Open Close Return

Jan-12 94.00 111.85 18.99 468.8 465.55 -0.69 128.5 129.75 0.97

Feb-12 114.00 101.85 -10.66 466 441.3 -5.30 131 133.65 2.02

Mar-12 102.00 96.95 -4.95 441 471.2 6.85 132.55 132 -0.41

Apr-12 96.95 99.40 2.53 472 433.05 -8.25 133 124.1 -6.69

May-12 103.00 84.25 -18.20 437 405.4 -7.23 126 114.05 -9.48

Jun-12 86.00 84.10 -2.21 414.95 325.55 -21.55 115.4 101.9 -11.70

Jul-12 84.00 89.65 6.73 329.4 380.2 15.42 102 110.9 8.73

Aug-12 90.00 92.00 2.22 380 469.75 23.62 110.5 142.65 29.10

Sep-12 92.00 109.40 18.91 465 526.2 13.16 141 162.15 15

Oct-12 110.00 118.15 7.41 527 518.45 -1.62 162.15 173.6 7.06

Nov-12 118.50 118.15 -0.30 524.8 544.75 3.80 174 200.95 15.49

Dec-12 119.00 110.70 -6.97 552 506.95 -8.16 202.8 207.9 2.51

Bankex

Date Open Close Return

Jan-12 5,124.09 5,254.89 2.55

Feb-12 5,267.88 5,204.69 -1.20

Mar-12 5,180.14 5,265.24 1.64

Apr-12 5,269.08 5,245.79 -0.44

May-12 5,252.40 4,769.87 -9.19

Jun-12 4,772.41 4,348.79 -8.88

Jul-12 4,311.56 4,781.14 10.89

Aug-12 4,772.39 5,308.01 11.22

Sep-12 5,301.98 6,038.87 13.90

Oct-12 6,044.05 6,484.06 7.28

Nov-12 6,486.64 7,179.71 10.68

Dec-12 7,183.78 7,085.73 -1.3640

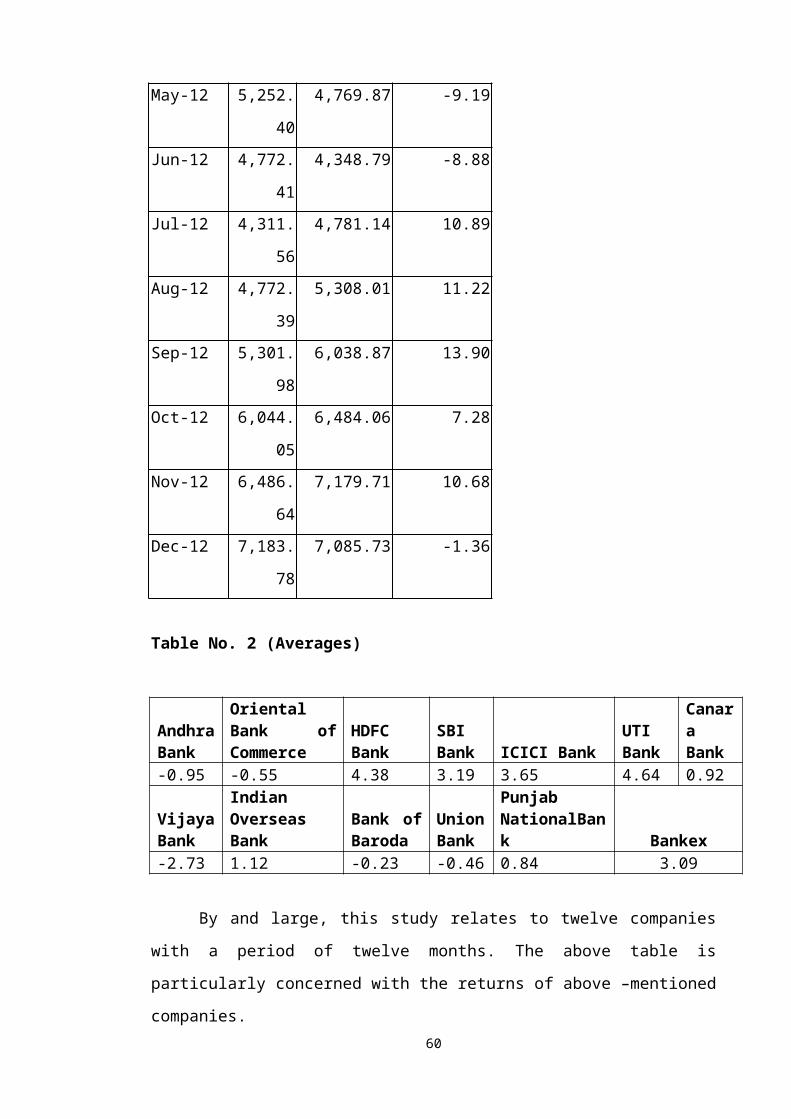

Table No. 2 (Averages)

Andhra Bank

Oriental Bank of Commerce

HDFC Bank

SBI Bank ICICI Bank

UTI Bank

Canara Bank

-0.95 -0.55 4.38 3.19 3.65 4.64 0.92Vijaya Bank

Indian Overseas Bank

Bank of Baroda

Union Bank

Punjab NationalBank Bankex

-2.73 1.12 -0.23 -0.46 0.84 3.09

By and large, this study relates to twelve companies with a period of twelve

months. The above table is particularly concerned with the returns of above –mentioned

companies.

In the course of the study it has been revealed that the highest return with respect

to Oriental Bank of Commerce took place in the month of September 2012 to the tune

of 40.02

In contrast to this the lowest return with respect of Punjab National Bank took

place in the month of June2012 to the tune of –21.55.

When overall performance i.e. average return is taken in to consideration UTI

Bank (4.64) reached the first position. When it comes to the lowest returns Vijaya Bank

(-2.73) remained in the forefront.

As per the BANKEX given by BSE, the returns remain highest in the month of

September 2012(13.90) and the lowest in the month of May 2012 (-9.19). The average

return of State Bank of India is closely related to the average return of BANKEX

average return. Totally eight banks are noted less average return than BANKEX and

remaining four banks are noted high average return than it

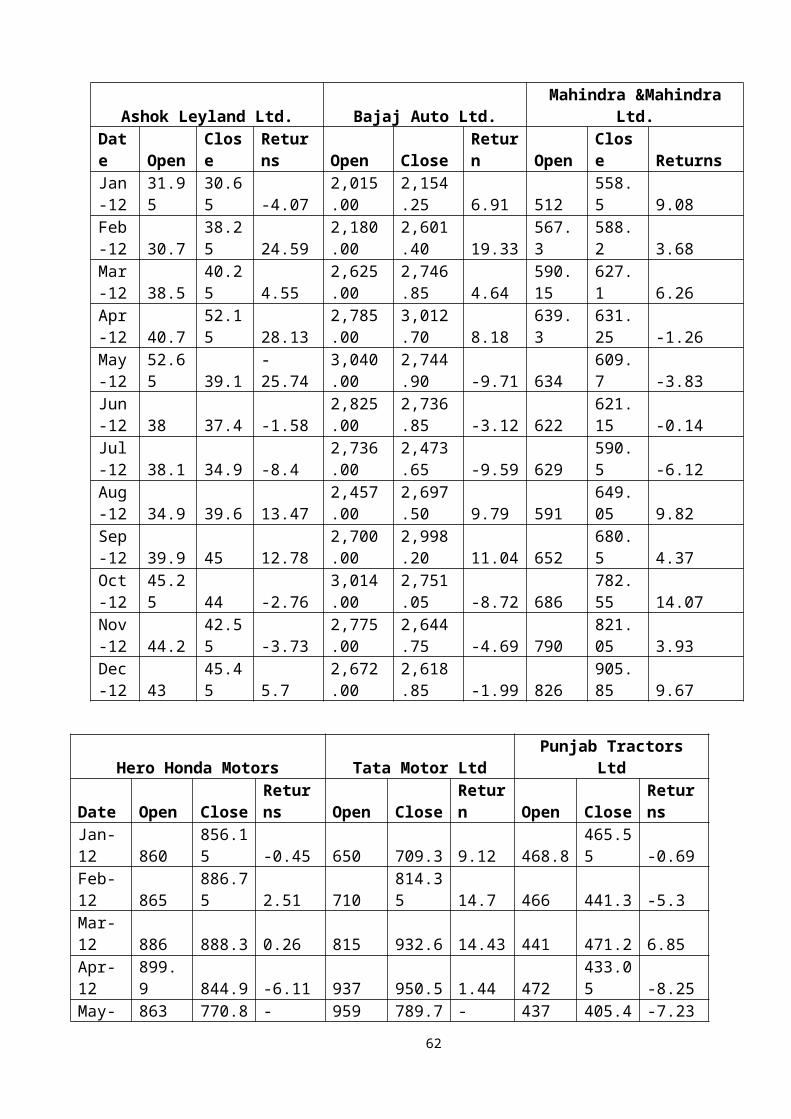

Returns for Automobile Industry

Return = (P1 – P0)/P0

Where: P1 = Closing price of the share

P0 = Opening price of the share

Table No. 3

41

Ashok Leyland Ltd. Bajaj Auto Ltd. Mahindra &Mahindra Ltd. Date Open Close Returns Open Close Return Open Close ReturnsJan-12 31.95 30.65 -4.07 2,015.00 2,154.25 6.91 512 558.5 9.08Feb-12 30.7 38.25 24.59 2,180.00 2,601.40 19.33 567.3 588.2 3.68Mar-12 38.5 40.25 4.55 2,625.00 2,746.85 4.64 590.15 627.1 6.26Apr-12 40.7 52.15 28.13 2,785.00 3,012.70 8.18 639.3 631.25 -1.26May-12 52.65 39.1 -25.74 3,040.00 2,744.90 -9.71 634 609.7 -3.83Jun-12 38 37.4 -1.58 2,825.00 2,736.85 -3.12 622 621.15 -0.14Jul-12 38.1 34.9 -8.4 2,736.00 2,473.65 -9.59 629 590.5 -6.12Aug-12 34.9 39.6 13.47 2,457.00 2,697.50 9.79 591 649.05 9.82Sep-12 39.9 45 12.78 2,700.00 2,998.20 11.04 652 680.5 4.37Oct-12 45.25 44 -2.76 3,014.00 2,751.05 -8.72 686 782.55 14.07Nov-12 44.2 42.55 -3.73 2,775.00 2,644.75 -4.69 790 821.05 3.93Dec-12 43 45.45 5.7 2,672.00 2,618.85 -1.99 826 905.85 9.67

Hero Honda Motors Tata Motor Ltd Punjab Tractors Ltd Date Open Close Returns Open Close Return Open Close ReturnsJan-12 860 856.15 -0.45 650 709.3 9.12 468.8 465.55 -0.69Feb-12 865 886.75 2.51 710 814.35 14.7 466 441.3 -5.3Mar-12 886 888.3 0.26 815 932.6 14.43 441 471.2 6.85Apr-12 899.9 844.9 -6.11 937 950.5 1.44 472 433.05 -8.25May-12 863 770.8 -10.68 959 789.7 -17.65 437 405.4 -7.23Jun-12 780 791.5 1.47 794.45 794.45 0 414.95 325.55 -21.55Jul-12 795 705.2 -11.3 801 739.75 -7.65 329.4 380.2 15.42Aug-12 709.7 720.3 1.49 737 845.15 14.67 380 469.75 23.62Sep-12 714.9 774.55 8.34 850 862.05 1.42 465 526.2 13.16Oct-12 778.5 756.15 -2.87 867.1 827.95 -4.52 527 518.45 -1.62Nov-12 762 742.65 -2.54 832 809.4 -2.72 524.8 544.75 3.8Dec-12 740 762.35 3.02 815 900.25 10.46 552 506.95 -8.16

42

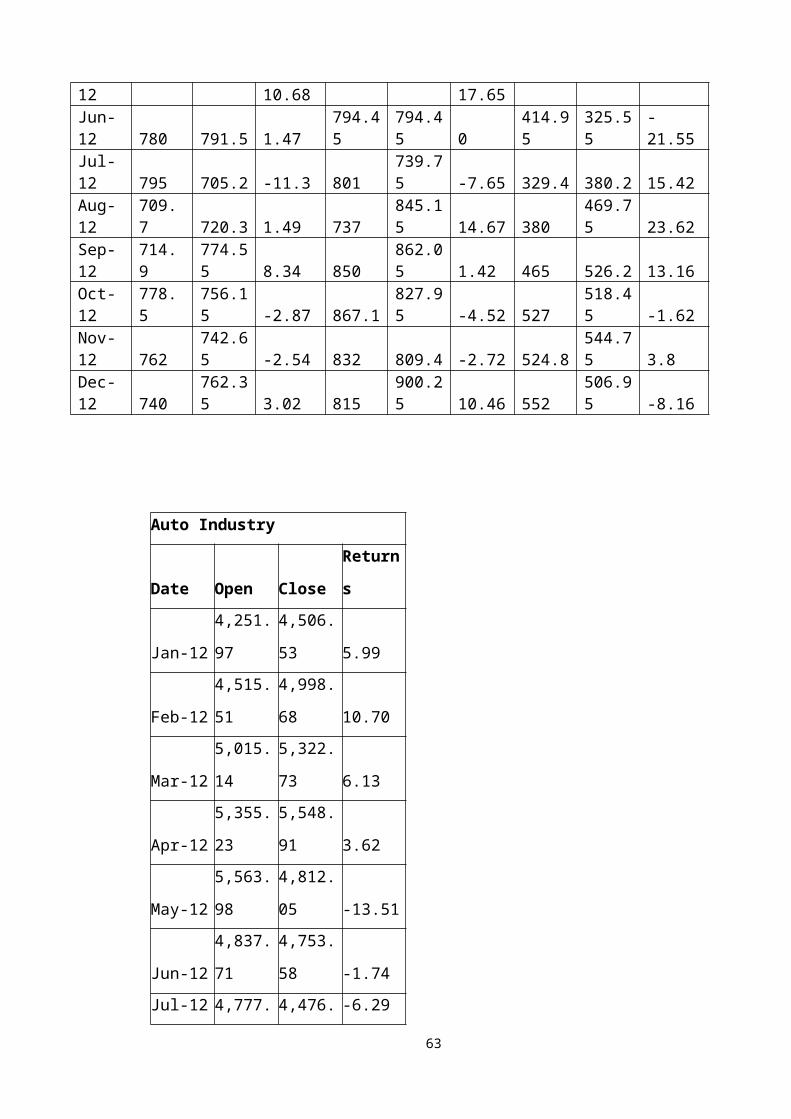

Auto Industry

Date Open Close Returns

Jan-12 4,251.97 4,506.53 5.99

Feb-12 4,515.51 4,998.68 10.70

Mar-12 5,015.14 5,322.73 6.13

Apr-12 5,355.23 5,548.91 3.62

May-12 5,563.98 4,812.05 -13.51

Jun-12 4,837.71 4,753.58 -1.74

Jul-12 4,777.54 4,476.87 -6.29

Aug-12 4,477.06 4,944.95 10.45

Sep-12 4,949.63 5,365.72 8.41

Oct-12 5,380.05 5,357.22 -0.42

Nov-12 5,371.03 5,321.85 -0.92

Dec-12 5,321.75 5,518.50 3.70

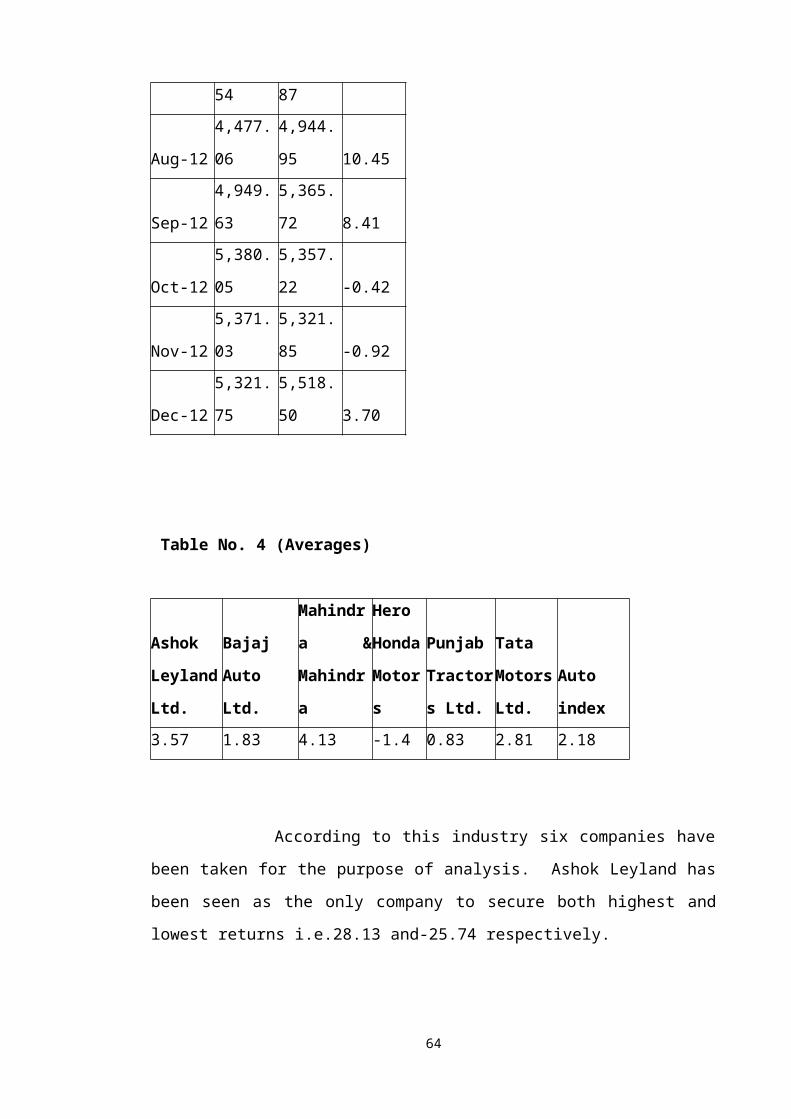

Table No. 4 (Averages)

Ashok

Leyland

Ltd.

Bajaj Auto

Ltd.

Mahindra

&

Mahindra

Hero

Honda

Motors

Punjab

Tractors

Ltd.

Tata

Motors

Ltd.

Auto

index

3.57 1.83 4.13 -1.4 0.83 2.81 2.18

According to this industry six companies have been taken for the purpose of

analysis. Ashok Leyland has been seen as the only company to secure both highest and

lowest returns i.e.28.13 and-25.74 respectively.

When it comes to the average performance i.e. average returns Mahindra &

Mahindra (4.13) has the highest return and Hero Honda Motors (-1.4) hold the lowest.

Highest return of this industry for the taken period was in the month of February

2012 (10.70) and the lowest return was in the month of May 2012 (-13.51).

43

(This Industry returns are calculated from the auto index, which is maintaining by the

BSE.)

In the above table show that Bajaj auto average return is closely related to the

average return of Auto industry. Overall three companies are noted less average return

and two are noted high average return than industry average return.

Returns for I.T. Industry

Return = (P1 – P0)/P0

Where: P1 = Closing price of the share

P0 = Opening price of the share

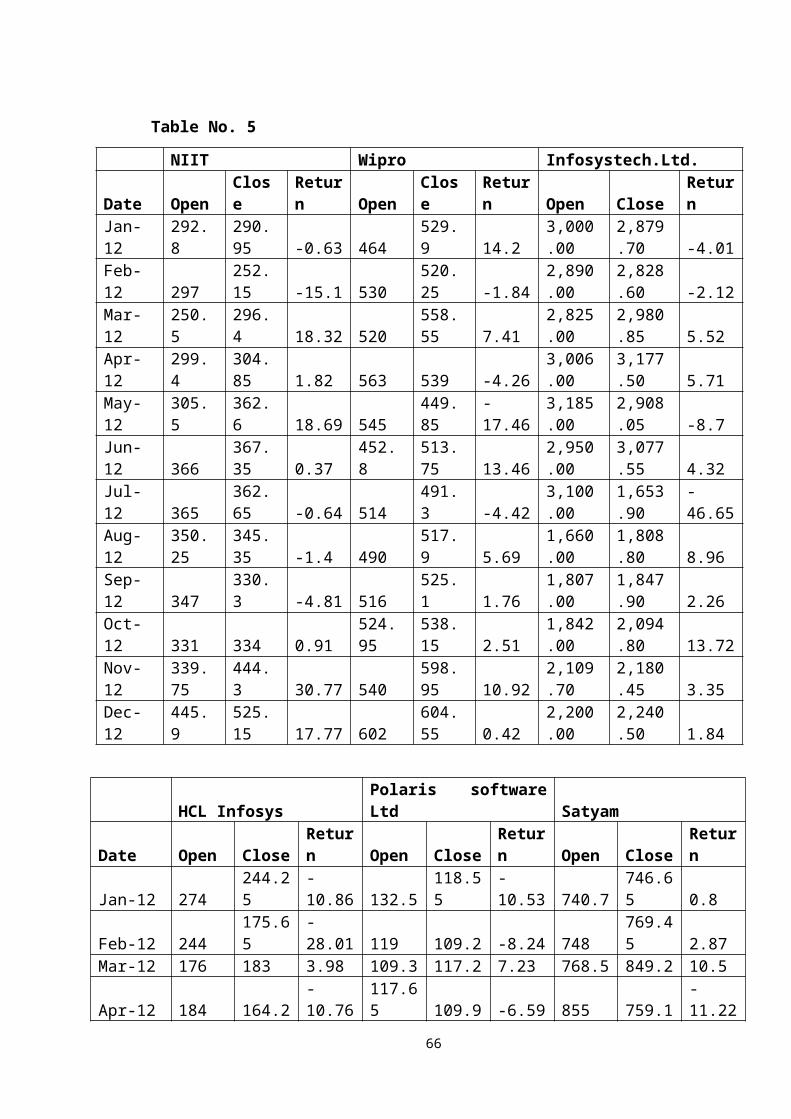

Table No. 5

NIIT Wipro Infosystech.Ltd.Date Open Close Return Open Close Return Open Close ReturnJan-12 292.8 290.95 -0.63 464 529.9 14.2 3,000.00 2,879.70 -4.01Feb-12 297 252.15 -15.1 530 520.25 -1.84 2,890.00 2,828.60 -2.12Mar-12 250.5 296.4 18.32 520 558.55 7.41 2,825.00 2,980.85 5.52Apr-12 299.4 304.85 1.82 563 539 -4.26 3,006.00 3,177.50 5.71May-12 305.5 362.6 18.69 545 449.85 -17.46 3,185.00 2,908.05 -8.7Jun-12 366 367.35 0.37 452.8 513.75 13.46 2,950.00 3,077.55 4.32Jul-12 365 362.65 -0.64 514 491.3 -4.42 3,100.00 1,653.90 -46.65Aug-12 350.25 345.35 -1.4 490 517.9 5.69 1,660.00 1,808.80 8.96Sep-12 347 330.3 -4.81 516 525.1 1.76 1,807.00 1,847.90 2.26Oct-12 331 334 0.91 524.95 538.15 2.51 1,842.00 2,094.80 13.72Nov-12 339.75 444.3 30.77 540 598.95 10.92 2,109.70 2,180.45 3.35Dec-12 445.9 525.15 17.77 602 604.55 0.42 2,200.00 2,240.50 1.84

HCL Infosys Polaris software Ltd SatyamDate Open Close Return Open Close Return Open Close Return

44

Jan-12 274 244.25 -10.86 132.5 118.55 -10.53 740.7 746.65 0.8Feb-12 244 175.65 -28.01 119 109.2 -8.24 748 769.45 2.87Mar-12 176 183 3.98 109.3 117.2 7.23 768.5 849.2 10.5Apr-12 184 164.2 -10.76 117.65 109.9 -6.59 855 759.1 -11.22May-12 164 155.5 -5.18 111 85.95 -22.57 762.9 691.15 -9.4Jun-12 158 130.6 -17.34 89.75 73.95 -17.6 700 711.4 1.63Jul-12 131 141.7 8.17 74.5 98.2 31.81 715 755.25 5.63Aug-12 140.55 163.5 16.33 98.5 112 13.71 753 808.2 7.33Sep-12 163.55 144.45 -11.68 112.3 117.5 4.63 810 818.55 1.06Oct-12 146 129.1 -11.56 118.5 130.75 10.34 826 440.55 -46.67Nov-12 129.2 164.45 27.28 132 121.55 -7.92 441 459.25 4.14Dec-12 164.45 159.2 -3.19 122.95 172.85 40.59 460 483.95 5.21

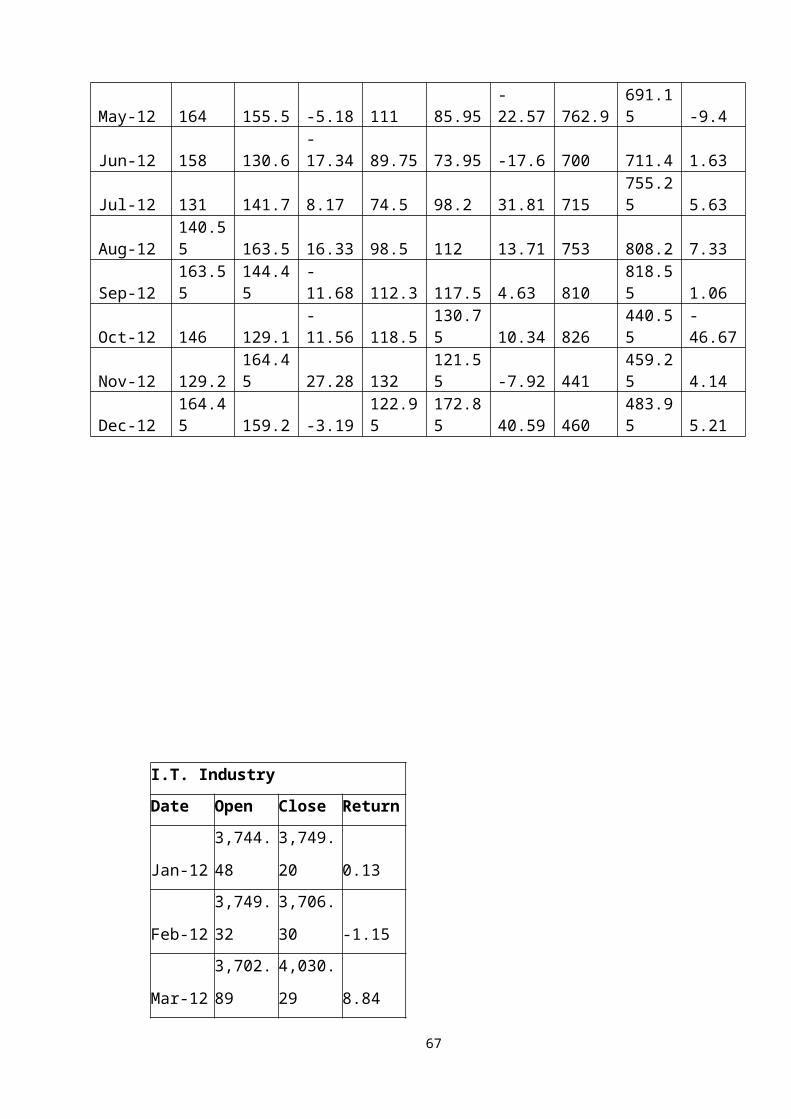

I.T. Industry

Date Open Close Return

Jan-12 3,744.48 3,749.20 0.13

Feb-12 3,749.32 3,706.30 -1.15

Mar-12 3,702.89 4,030.29 8.84

Apr-12 4,048.39 4,034.92 -0.33

May-12 4,046.60 3,642.67 -9.98

Jun-12 3,674.89 3,743.32 1.86

Jul-12 3,750.71 3,951.13 5.34

Aug-12 3,943.91 4,286.42 8.68

Sep-12 4,277.66 4,393.56 2.71

Oct-12 4,408.61 4,821.98 9.38

Nov-12 4,828.75 5,107.22 5.77

Dec-12 5,130.37 5,272.56 2.77

45

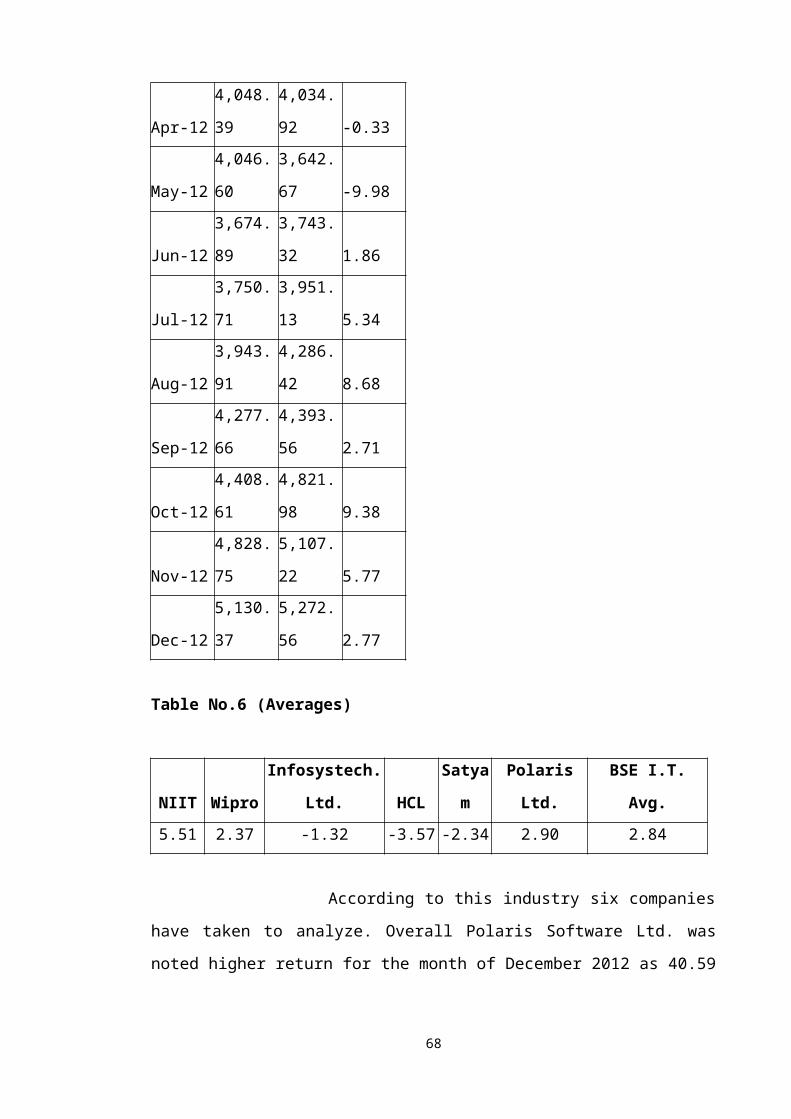

Table No.6 (Averages)

NIIT Wipro Infosystech. Ltd. HCL Satyam Polaris Ltd. BSE I.T. Avg.

5.51 2.37 -1.32 -3.57 -2.34 2.90 2.84

According to this industry six companies have taken to analyze. Overall

Polaris Software Ltd. was noted higher return for the month of December 2012 as 40.59

and Satyam was noted lower return for the month of October 2012 as –46.67.

Highest return of this industry for the taken period was in the month of

October 2012 (9.38) and the lowest return was in the month of May 2012 (-9.98).

(This Industry returns are calculated from the IT INDEX, which is maintaining by the

BSE)

According to the average return NIIT was noted highest return as 5.51 and HCL

Infosystech Ltd. was noted lowest return as –3.57.

In the above table No. 6 show that Polaris average return is closely related to the

average return of IT INDUSTRY. Over all only two companies are more than the

Industry average returns.

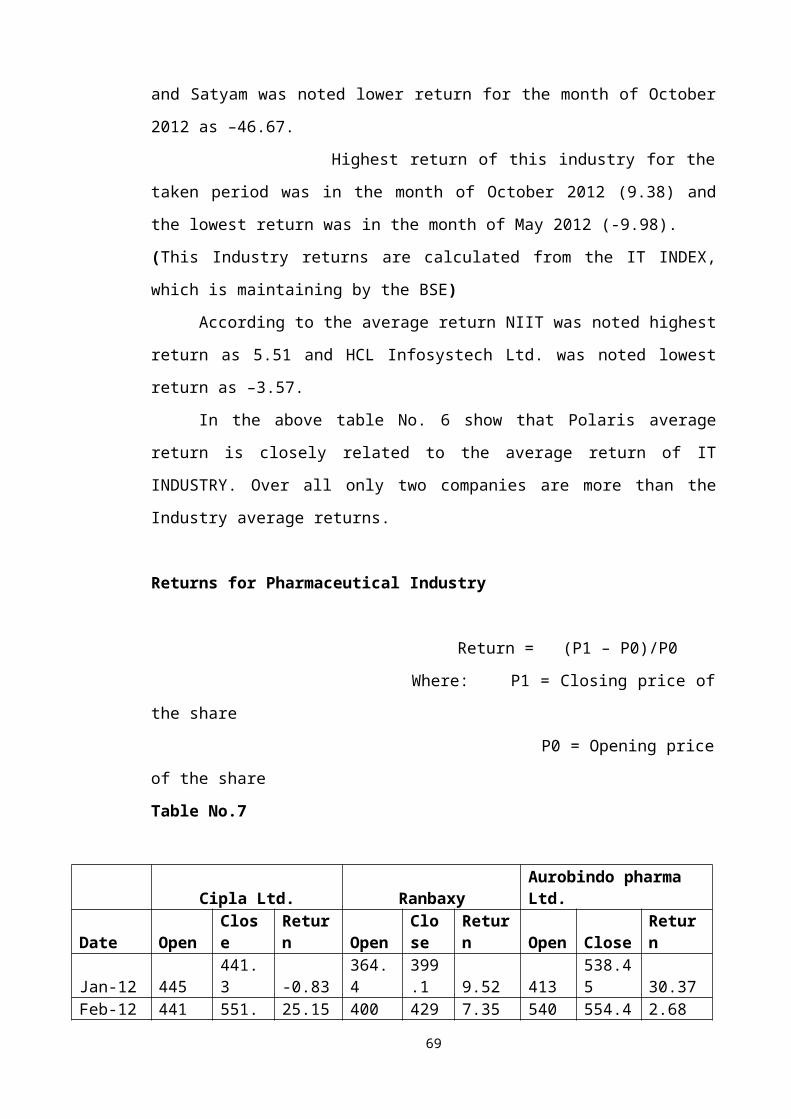

Returns for Pharmaceutical Industry

Return = (P1 – P0)/P0

Where: P1 = Closing price of the share

P0 = Opening price of the share

Table No.7

Cipla Ltd. Ranbaxy Aurobindo pharma Ltd.Date Open Close Return Open Close Return Open Close ReturnJan-12 445 441.3 -0.83 364.4 399.1 9.52 413 538.45 30.37Feb-12 441 551.9 25.15 400 429.4 7.35 540 554.45 2.68Mar-12 552 661.95 19.92 431 431.6 0.14 560 682.75 21.92Apr-12 665 260.8 -60.78 435.95 472.6 8.4 682.5 723.9 6.07May-12 263.9 229.5 -13.04 504 411.5 -18.36 734 581.35 -20.8Jun-12 233 215.8 -7.38 412.5 356.4 -13.6 592 582.25 -1.65Jul-12 216.3 236 9.11 360 373.9 3.85 586 617.65 5.4Aug-12 236 249.95 5.91 374 406.8 8.77 626 624.8 -0.19Sep-12 251 262.25 4.48 406 439.9 8.34 625 628.4 0.54Oct-12 261.9 262.05 0.06 435.7 399.7 -8.26 630 609 -3.33

46

Nov-12 264 253.85 -3.84 401.15 372.3 -7.19 614.7 619.9 0.85Dec-12 257.15 250.7 -2.51 372.9 391.9 5.08 626 705.15 12.64

Dr. Reddy's Laboratories

Ltd. Sterl Biotech Work hard Ltd.Date Open Close Return Open Close Return Open Close ReturnJan-12 986 1,119.60 13.55 123.95 125.3 1.09 445.1 483.45 8.62Feb-12 1,125.00 1,302.85 15.81 125.1 120.4 -3.8 490 513.85 4.87Mar-12 1,299.55 1,420.30 9.29 122.5 124.7 1.76 515 506.65 -1.62Apr-12 1,435.00 1,431.85 -0.22 126 120.6 -4.29 510.95 446.25 -12.66May-12 1,450.00 1,357.40 -6.37 121.95 119.2 -2.26 446 360.15 -19.25Jun-12 1,389.95 1,274.00 -8.34 120 105.9 -11.75 364.8 380.1 4.19Jul-12 1,273.50 1,396.95 9.69 106 102.6 -3.25 388 342.7 -11.68Aug-12 1,375.05 720.5 -47.6 104 110.8 6.54 342.7 364.55 6.38Sep-12 723 731.3 1.148 111.15 145.4 30.77 368.95 401.5 8.82Oct-12 731 748.05 2.33 145.5 122.2 -16.01 404.8 388.95 -3.92Nov-12 709 750.8 5.9 123.9 167.7 35.35 390 372.2 -4.56Dec-12 755 811.2 7.44 166 192.5 15.96 376.5 350.4 -6.93

Pharma Index

Date Open Close Returns

Jan-12 3,103.76 3,290.65 6.02

Feb-12 3,290.95 3,553.78 7.99

Mar-12 3,549.54 3,858.10 8.69

Apr-12 3,867.08 3,894.84 0.72

May-12 3,973.37 3,387.94 -14.73

Jun-12 3,416.41 3,132.42 -8.31

Jul-12 3,136.32 3,227.22 2.90

Aug-12 3,234.52 3,538.50 9.40

Sep-12 3,543.77 3,684.44 3.97

Oct-12 3,680.87 3,641.60 -1.07

Nov-12 3,630.59 3,720.61 2.48

Dec-12 3,720.14 3,792.05 1.93

Table No .8 (Averages)

47

Cipla Ranbaxy Aurobhindo Dr. Reddy's Sterl biotech Work hard Index

-1.98 0.34 4.54 0.22 4.18 -2.31 1.67

According to this industry six companies have taken to analyze. Overall

STERL. Was noted highest return for the month of November 2012 as 35.35 and the

Cipla Ltd. was noted lowest return for the month of February 2012 as –60.78.

Highest return of this industry for the taken period was in the month of August

2012 (9.40) and the lowest was in the month of May 2012 (-14.73).

According to the average return AUROBINDO Pharma Ltd. was noted

highest return as 4.54 and Wockhardt was noted lowest return

Fluctuations in the prices of the selected shares in respect to industries

Market indexes have always been of great importance in the world of

security analysis and portfolio management. People from different walks of life use and

are affected by market indicators. Investors, both individual and institutional, use the

market index as a benchmark against which they evaluate the performance of their own

or Institutional portfolio. The technicians or the chartists often base their decisions to

buy and sell on the patterns emerging out of the time series data of market indexes.

Even the economists and statisticians use stock market indexes to study the trend of

growth patterns in the economy, to analyses as well as forecast business cycles and to

correlate stock market indexes to economic activities.

The index is just an indicator of market and did nothing to the formation of

decision of selecting the investment or portfolio. So the investor should have the highest

degree in analyzing this index. They simply not only tell the movement of share prices

but also reflected by the weight of those shares. So, a high increase in share price of a

minor share with a small share holding will not affect the market.

48

In this study to analysis the fluctuations in the prices of shares for selected

companies in the selected industries index has prepared in the simple average method

with the selected companies for the period of thirteen months.

In general stock exchanges are using some methods to construct indexes. Those

are

Simple average method

Market capitalization Method

Free-float Capitalization Method

The construction of index in simple average met

= (Simple average on the day of cons. /simple average on base day)*100

Example: DJIA

Securities Day1 (Rs) Day2 (Rs) Day3 (Rs) Day4 (Rs)A 100 150 180 130B 110 105 200 90C 85 80 130 90D 180 220 270 150 Average 119 139 195 115Index Points 100 117 164 97

The prepared industry indexes are based on the selected companies for the

selected period. Below mentioned indexes are prepared in this study.

(i) Banking Industry Index (Bank ex)

(ii) Auto Industry Index

49

Construction of Index for Banking Industry

The Base period of Banking index Jan-2012.

The base points of banking industry index are 100.

The Banks involved in the bank industry index are thirteen randomly

selected banks from BSE200 index.

Banking Index

Table No. 9

DateAndhra Bank HDFC OBC SBI ICICI UTI Canara

Jan-12 92.925 736.725 260.975 898.3 597.7 314.575 246.075Feb-12 260.975 751.975 246 883.6 612.6 331.2 268.575Mar-12 84.35 755.75 237.925 924.025 604.1 341.675 276.7Apr-12 80.575 795.8 235.425 941.075 591.1 338.55 261.025May-12 77.625 787.6 218.525 874 570.5 320.4 242.775Jun-12 67.725 765.575 185.65 783.2 516.2 279.375 216.4Jul-12 69.4 767.525 170.725 772.025 521.1 284.925 198.875Aug-12 80.875 821.6 185.325 865 573.8 320.7 209.85Sep-12 91.375 883 232.825 978.15 642.1 360.6 253.575Oct-12 93.9 958.025 263.5 1053.25 738.4 406.925 290.95Nov-12 90.8 1067.7 252.225 1204.5 824.2 455.025 297.775Dec-12 88.3 1095.88 236.75 1279.95 882.7 474.25 288.6

DateVijaya Bank IOB PNB

Union Bank BOB Avg.

Index point

Jan-12 61.325 102.925 467.175 123.5 246.3 345.71 100Feb-12 59.7 107.925 453.65 123.6 237.1 361.4 109.83Mar-12 55.025 99.475 456.1 122.325 227.6 348.76 105.99

50

Apr-12 53.1 98.175 452.525 120.425 231.8 349.96 106.36May-12 48.8 93.625 421.2 113.4 230 333.21 101.26Jun-12 42.65 85.05 370.25 99.2 212.7 301.99 91.779Jul-12 40.975 86.825 354.8 96.725 211 297.9 90.536Aug-12 44.525 91 424.875 109.7 235.8 330.25 100.37Sep-12 52.125 100.7 495.6 127.075 269.6 373.89 113.63Oct-12 57.1 114.075 522.725 133.15 287.5 409.96 124.59Nov-12 54.15 118.325 534.775 129.675 271.1 441.69 134.23Dec-12 49.775 114.85 529.475 125.825 251.9 451.52 137.22

Figure No. 1

In the diagram shown above months are (Jan-12 to Dec-12) shown on the x-axis.

Index points are shown on the y-axis.

During the initial period of the study that is Jan-12 to May-12 the index

points moved from 100 to 109 points. However during the period of June-12 to July–12

there is a drastic decrease in the index points they reached the lowest level of 90.536

soon there is an upturn in the index points by rising to the level of 100.37 points. This

time there is a standard increase in the index points in the next coming periods. In the

month of December the index points reached to the level of 137.22.

Construction of Index for Automobile Industry

The Base period of Automobile Industry index Jan-2012

The Base points of Automobile Industry index are 100

The Companies involved in the Automobile industry index are six randomly

selected companies from BSE200 index.

Automobile Index

Table No. 10

Date Ashok Bajaj M&M Hero Tata Punjab Avg. Index 51

Leyland

Ltd. Ltd Ltd.

Honda

Motors.

Motor

Ltd.

Tractors

Ltd. Point

Jan-12 31.3 2084.6 535.25 858.08 467 679.65 776 100

Feb-12 34.48 2390.7 577.75 875.88 454 762.175 849 109.42

Mar-12 39.38 2685.9 608.625 887.15 456 873.8 925 119.22

Apr-12 46.43 2898.9 635.275 872.4 453 943.75 975 125.63

May-12 45.88 2892.5 621.85 816.9 421 874.35 945 121.83

Jun-12 37.7 2780.9 621.575 785.75 370 794.45 898 115.78

Jul-12 36.5 2604.8 609.75 750.1 355 770.375 854 110.10

Aug-12 37.25 2577.3 620.025 715 425 791.075 861 110.94

Sep-12 42.45 2849.1 666.25 744.73 496 856.025 942 121.44

Oct-12 44.63 2882.5 734.275 767.33 523 847.525 967 124.55

Nov-12 43.38 2709.9 805.525 752.33 535 820.7 944 121.70

Dec-12 44.23 2645.4 865.925 751.18 529 857.625 949 122.29

Figure No. 2

In the diagram shown above months are (Jan-12 to Dec-12) shown on the x-axis.

Index points are shown on the y-axis.

During the initial period of the study that is Jan-12 to Apr-12 the index points

moved in upward trend at the level of 125.63 points, though there is a slight change.

However during the period of May-12to July–12 there is a down ward trend decrease in

the index points they reached the lowest level of 110.10. Soon there is an upturn in the

index points by rising to the level of 110.94 points and that has been followed by the

next months.

52

Construction of Index for I.T. Industry

The Base period of I.T. Industry index Jan-2006

The Base points of I.T. Industry index are 100

The Companies involved in the I.T. industry index are six randomly

selected companies from BSE200 SENSEX.

I.T. Industry Index

Table No. 11

Date NIIT Wipro Infosys HCL Polaris Satyam Avg.

Index

Point

Jan-12 291.875 728.95 4439.85 396.125 1114.025 191.775 1193.8 100

Feb-12 423.075 790.125 4304.3 331.825 1132.725 173.6 1192.6 99.90

Mar-12 398.7 799.275 4315.425 267.5 1193.1 167.9 1190.3 99.81

Apr-12 451.825 832.5 4594.75 266.1 1234.55 172.6 1258.7 105.75

May-12 486.8 769.925 4639.025 241.75 1108.475 153.975 1233.3 97.98

Jun-12 549.675 709.675 4488.775 223.3 1055.7 126.725 1192.3 96.67

Jul-12 546.325 759.65 3926.95 201.85 1092.625 123.6 1108.5 92.97