Embed Size (px)

Citation preview

Using Budgets

AS Business Studies

Aims & Objectives

Aim:• Understand variance analysisObjectives:• Define variance analysis• Explain the causes of variance• Analyse managerial reactions to variance analysis• Evaluate the usefulness of variance analysis

Starter

• Define a budget

• Give 2 advantages to the business of using budgets

• Give 2 disadvantages to the business of using budgets.

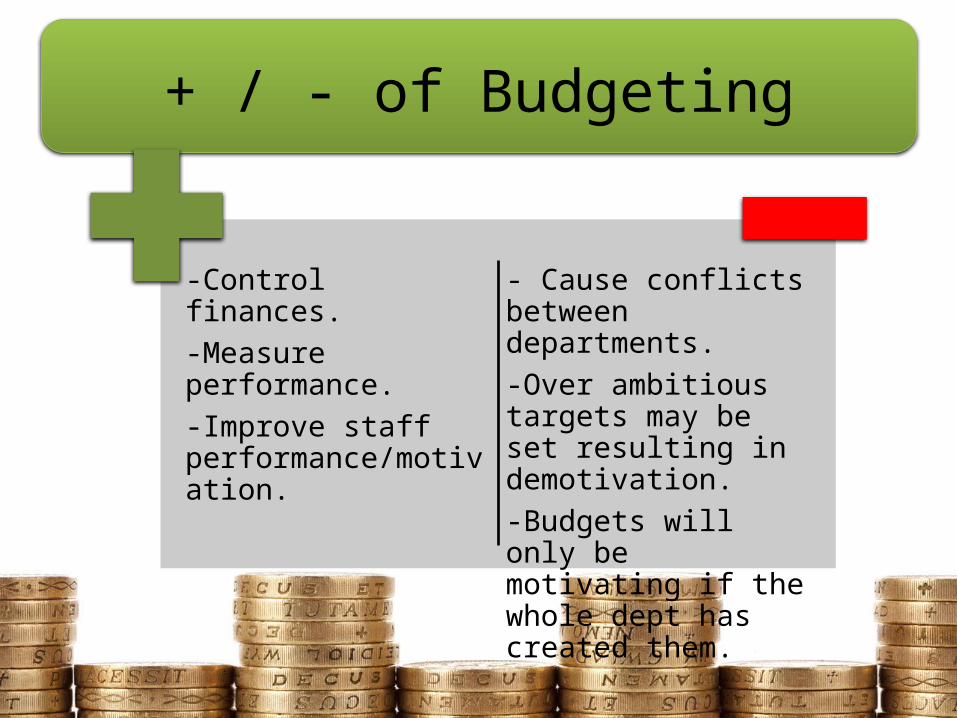

+ / - of Budgeting

-Control finances.-Measure performance.-Improve staff performance/motivation.

- Cause conflicts between departments.-Over ambitious targets may be set resulting in demotivation.-Budgets will only be motivating if the whole dept has created them.

Bob’s Beer Budget

• Bob• University Student• Budgeted his first week at

university• After his first month he

realised that his actual amount spent was different

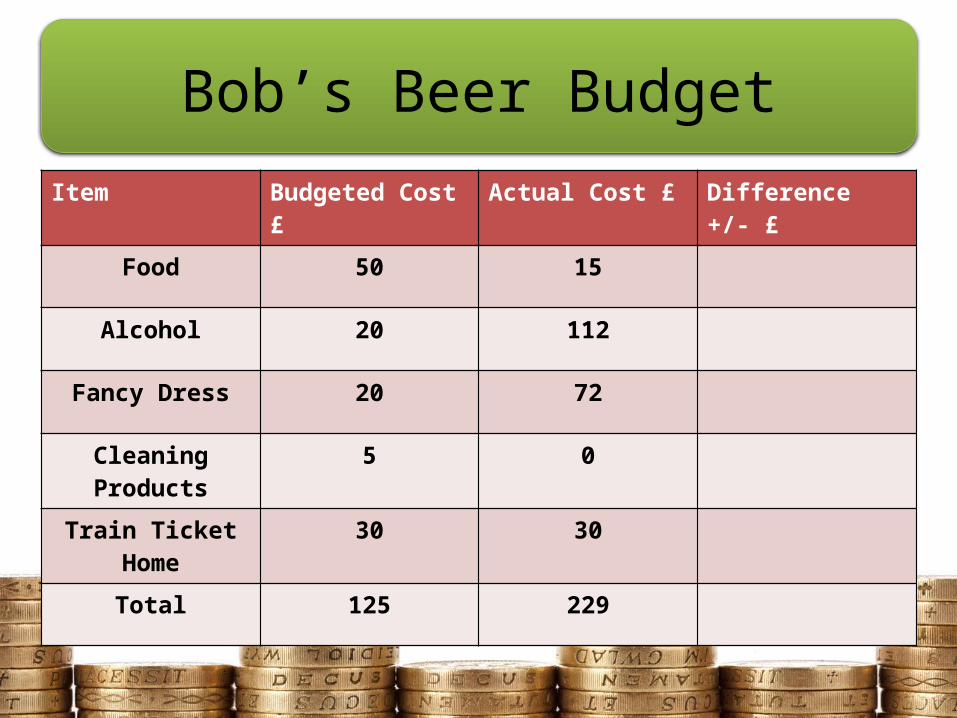

Bob’s Beer BudgetItem Budgeted Cost £ Actual Cost £ Difference +/- £

Food 50 15

Alcohol 20 112

Fancy Dress 20 72

Cleaning Products 5 0

Train Ticket Home 30 30

Total 125 229

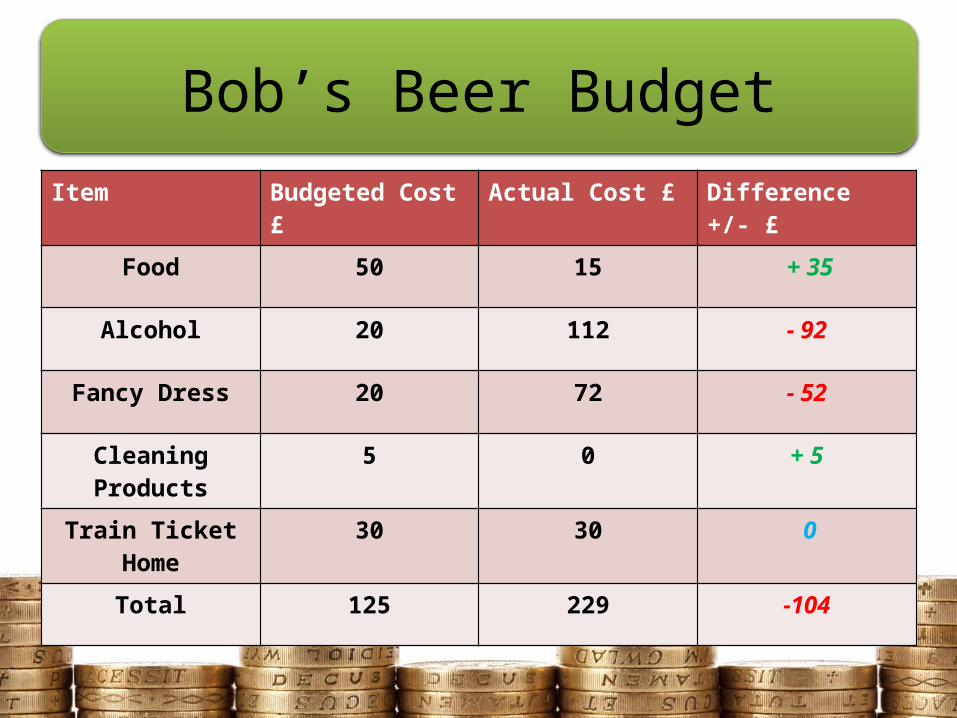

Bob’s Beer BudgetItem Budgeted Cost £ Actual Cost £ Difference +/- £

Food 50 15 + 35

Alcohol 20 112 - 92

Fancy Dress 20 72 - 52

Cleaning Products 5 0 + 5

Train Ticket Home 30 30 0

Total 125 229 -104

Bob’s Beer Budget

• Bob blew his budget in the first week!

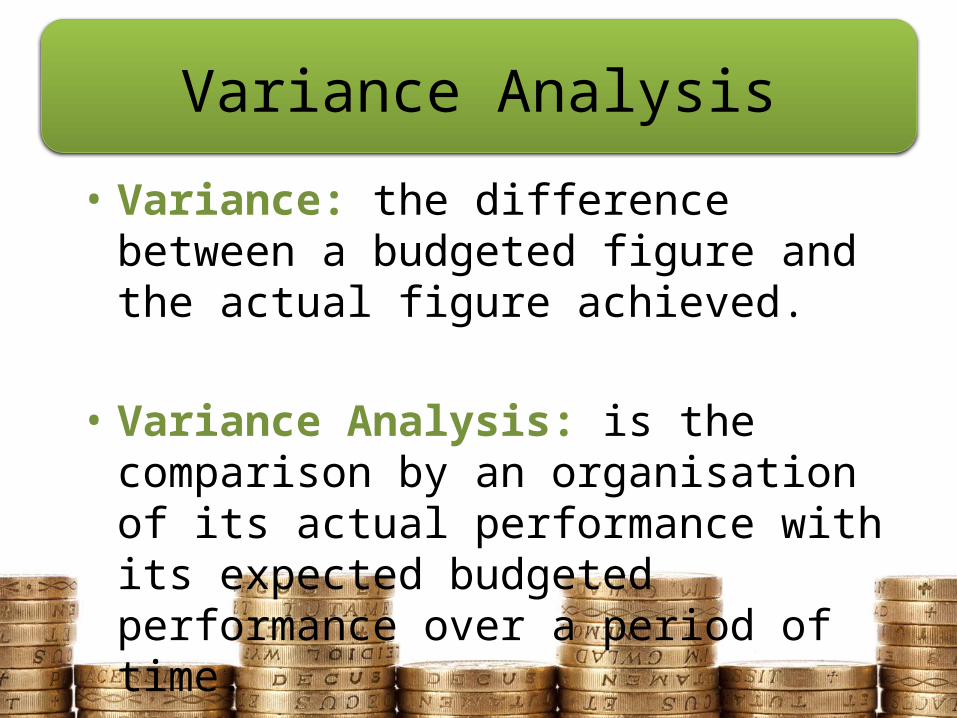

Variance Analysis

• Variance: the difference between a budgeted figure and the actual figure achieved.

• Variance Analysis: is the comparison by an organisation of its actual performance with its expected budgeted performance over a period of time.

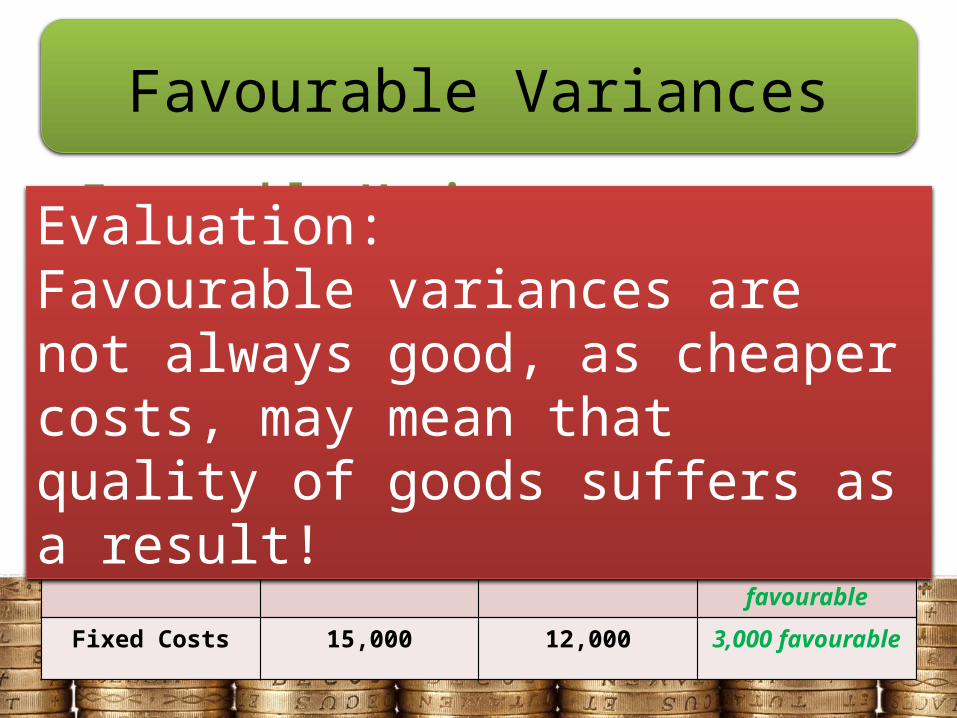

Favourable Variances

Favourable Variances: • A better result than expected• Budgeted figure is less (costs) or more

(revenue) than expected.• Leads to higher than expected profits

Item Budget £ Actual £ Variance £

Sales Revenue 50,000 60,000 10,000 favourable

Fixed Costs 15,000 12,000 3,000 favourable

Evaluation:Favourable variances are not always good, as cheaper costs, may mean that quality of goods suffers as a result!

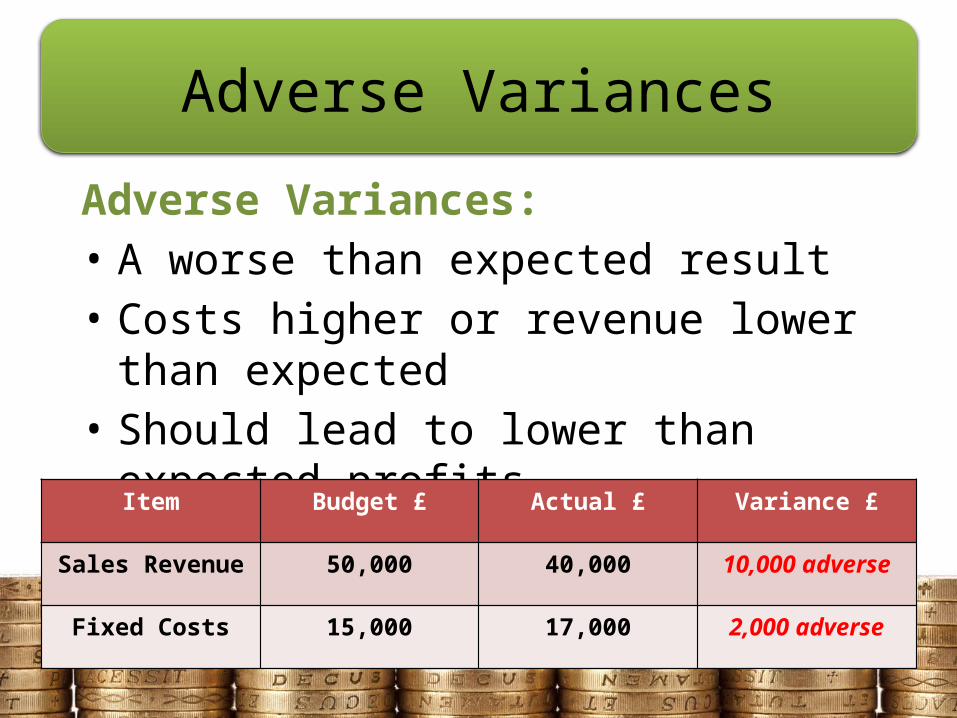

Adverse Variances

Adverse Variances:• A worse than expected result• Costs higher or revenue lower than expected• Should lead to lower than expected profits

Item Budget £ Actual £ Variance £

Sales Revenue 50,000 40,000 10,000 adverse

Fixed Costs 15,000 17,000 2,000 adverse

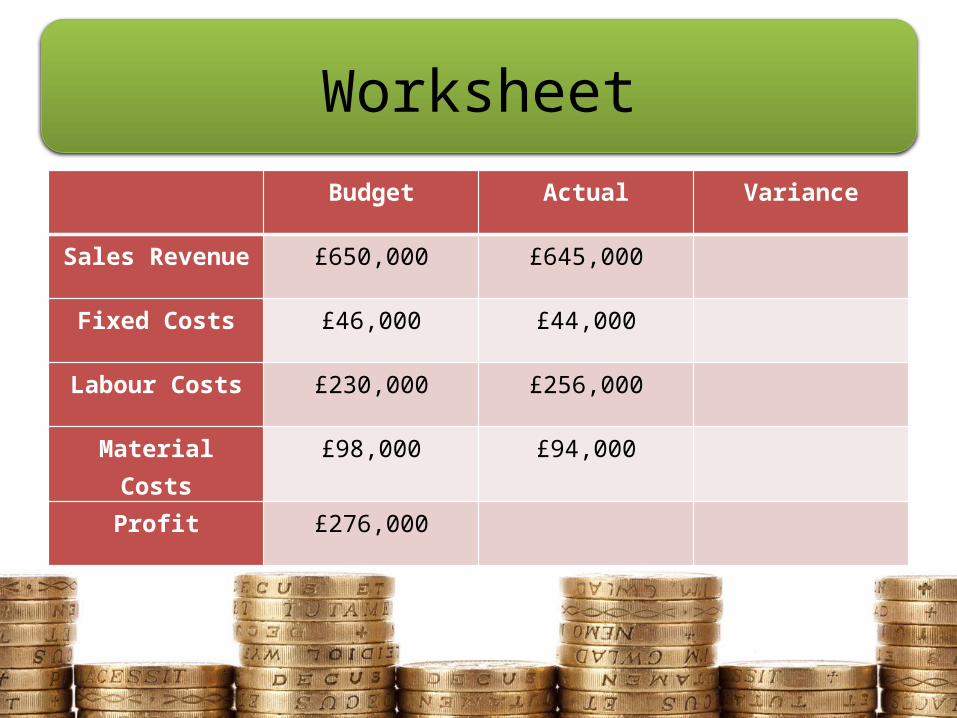

Worksheet Budget Actual Variance

Sales Revenue £650,000 £645,000

Fixed Costs £46,000 £44,000

Labour Costs £230,000 £256,000

Material Costs £98,000 £94,000

Profit £276,000

What causes variances?

• In groups discuss what the main causes of favourable and adverse variances may be?

Favourable Variance Causes

1• Bad publicity for competitors products leads to increased sales

2• Lower interest rates lead to increased sales

3• Consumers have more disposable income

4• Demand for good/service increases

Adverse Variance Causes

1• Competitors offer better price deals, lowering sales.

2• Labour productivity falls leading to higher costs per unit

3• Oil prices increase

4• Rent/rates/lighting increases

Decision Making

• Variances affect decision making by managers.

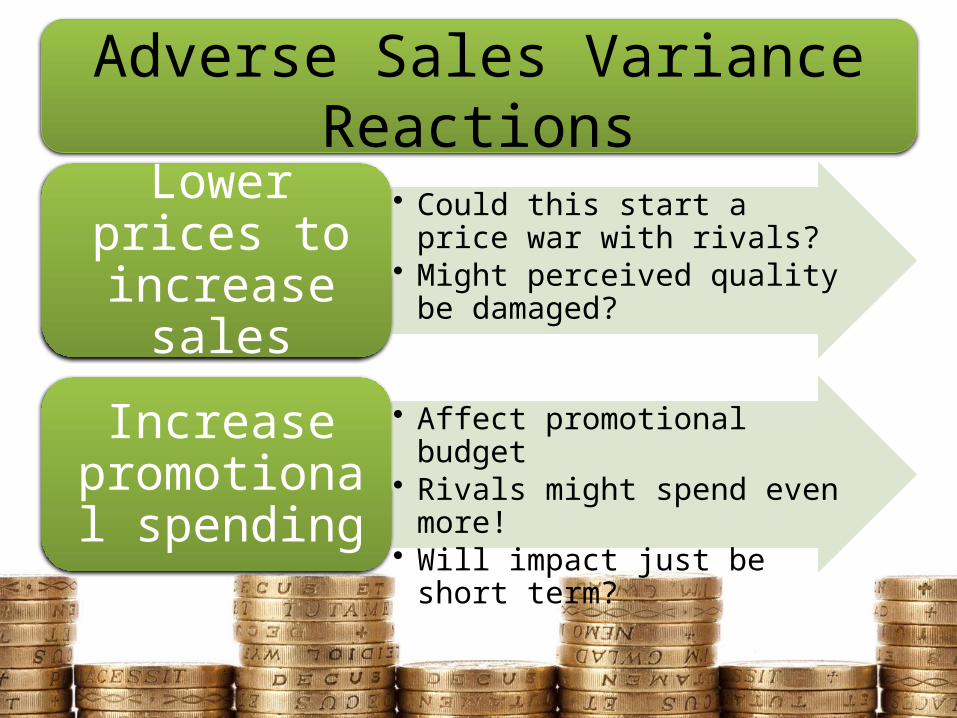

Task: Identify the potential drawbacks of the following management reactions to adverse sales variances.

Adverse Sales Variance Reactions

• Could this start a price war with rivals?

• Might perceived quality be damaged?

Lower prices to increase sales

• Affect promotional budget• Rivals might spend even more!• Will impact just be short term?

Increase promotional

spending

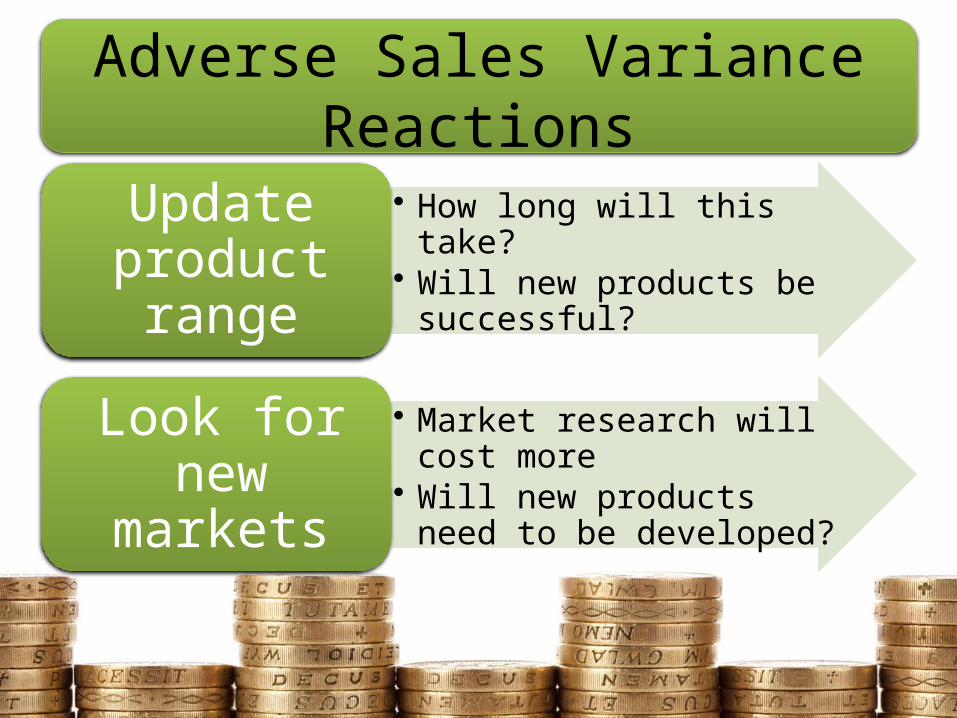

Adverse Sales Variance Reactions

• How long will this take?• Will new products be

successful?Update

product range

• Market research will cost more• Will new products need to be

developed?Look for new

markets

Adverse Cost Variance Reactions

Task: Identify the potential drawbacks of the following management reactions to adverse cost variances.

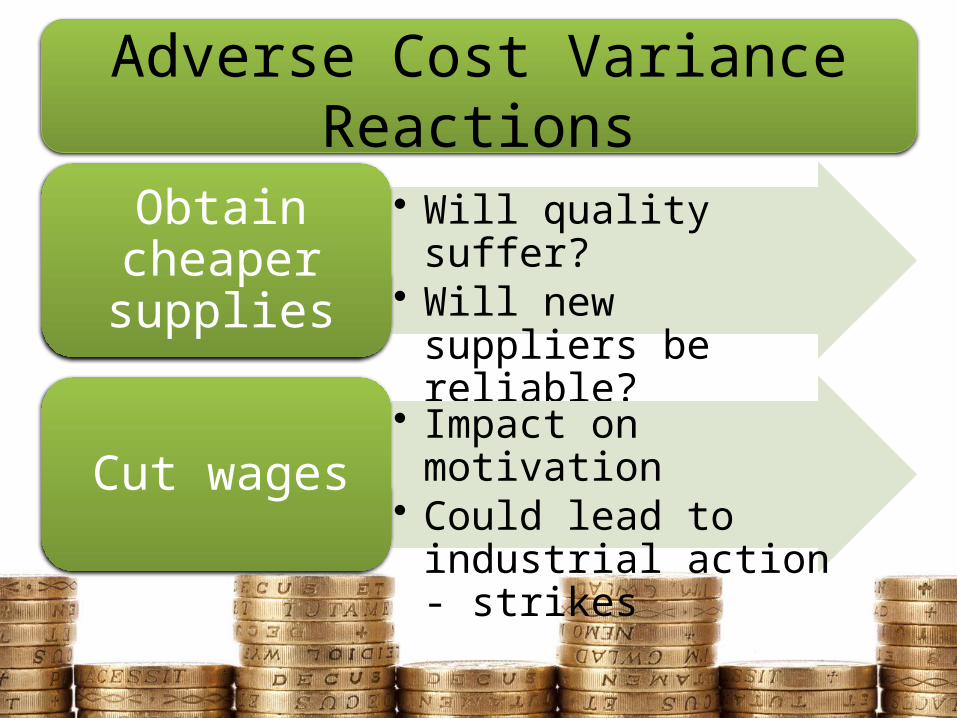

Adverse Cost Variance Reactions

• Will quality suffer?• Will new suppliers be

reliable?

Obtain cheaper supplies

• Impact on motivation • Could lead to industrial

action - strikesCut wages

Adverse Cost Variance Reactions

• May need new machinery, staff training, leading to higher costs in SR.

Increase Labour Productivity to

reduce labour cost per unit

• May need a change in working practices, short term benefits may be limited.

Reduce Waste Levels

Highcroft Hotels Case Study