Embed Size (px)

Citation preview

University of PretoriaAnnual Financial Review

2011 Financial Review ii

Composition of the Council and Executive of the University of Pretoria as on 31 December 2011Council of the University of Pretoria

Members nominated by the MinisterMs B DibateDr PZ DubeMs NFT MpumlwanaDr B-A RibeiroMr AW Taylor

Members elected by the ConvocationMr AD BothaDr BP Botha (Deputy Chairperson)Dr EC BothaOne vacancy

Members elected by SenateProf I PikirayiProf RF SandenberghProf A Ströh

Members elected by the DonorsMr LL DippenaarProf DJ du Plessis

Members appointed by Council based on expertise/experienceDr SF BooysenProf RM LoubserMs D MagugumelaMs NT Mtoba (Chairperson)Mr IB SkosanaDr J van Zyl

Members appointed by the Tshwane local authorityMs PF Mashaba

Student representativesMr K MalatjiMr C Oberholzer

Employee representative (academic)Prof JH Potgieter

Employee representative (non-academic)Prof A van Aswegen

Principal and Vice-Principals (ex officio)Prof CM de la Rey (Vice-Chancellor and Principal)Prof RM Crewe (Vice-Principal)Prof SG Burton (Vice-Principal)Prof NA Ogude (Vice-Principal)Prof CR de Beer (Seconded as Administrator: University of Zululand as of 1 May 2011)

Executive of the University of Pretoria

Prof CM de la Rey (Vice-Chancellor and Principal)Prof RM Crewe (Vice-Principal)Prof SG Burton (Vice-Principal)Prof NA Ogude (Vice-Principal)Prof NJ Grové (Registrar)Prof AM de Klerk (Executive Director)Prof C Koornhof (Executive Director)Prof AP Melck (Executive Director)Prof CR de Beer (Seconded as Administrator: University of Zululand as of 1 May 2011)One vacancy

Addresses of the University

Physical addressUniversity of Pretoria Lynnwood Road Pretoria

Postal addressOffice of the RegistrarRoom 4-23Administration BuildingUniversity of Pretoria Pretoria0002

2011 Financial Review 1

ContentsScope of the summarised consolidated annual financial statements 2

Annual financial review for 2011 2

Report on internal administrative/operational structures and controls 5

Report on risk exposure assessment and the management thereof 6

Approval of the consolidated financial statements 6

Independent auditor’s report to the Council of the University of Pretoria 7

Summary of accounting policies 9

Consolidated statement of financial position 22

Consolidated income statement 24

Consolidated statement of comprehensive income 25

Consolidated statement of changes in equity 26

Consolidated statement of cash flows 27

Notes to the consolidated financial statements 28

2011 Financial Review 2

SCOPE OF THE SUMMARISED CONSOLIDATED ANNUAL FINANCIAL STATEMENTSThis report provides a financial profile of the University of Pretoria for the year ended 31 December 2011. The financial statements

includes revenues, expenses, assets and liabilities, as well as the transactions of all the operations and organisations under the

jurisdiction of the University.

ANNUAL FINANCIAL REVIEW FOR 2011INCOME AND EXPENDITURE

The University’s total income increased by R563 million to R4 811 million during the period under review.

The first main source of income remains the block grant received from the Department of Higher Education and Training, together

with earmarked grants to veterinary science, clinical training, foundation year programmes and teaching development initiatives.

The block grant of R1 476,26 million in 2011 represents an increase of 11,4% over 2010.

Tuition fees, the second main source of income, increased by 7%, despite an average increase of 8% in student fees raised for the

University’s programme offerings. The difference is primarily attributable to a decline in student numbers.

The following table provides a summary of the University’s sources of income:

Table 1: Total income of the University of Pretoria in 2011

Income2011 2010 Change

Rm Rm Rm %

Government grants 1 652 1 405 247 18

Tuition fees 1 000 931 69 7

Accommodation and meal fees 220 203 17 8

Investment income – profits on disposal 214 90 124 138

Interest / Dividend Income 197 229 (32) (14)

Expected return on plan assets 416 370 46 12

Income from contracts and other 475 489 (14) (2,9)

Service rendering 456 436 20 4,6

Donations and gifts 181 95 86 91

Total 4 811 4 248 563 13

Operating expenses were kept within the bounds of affordability by adopting measures to promote effectiveness and efficiency

and by maintaining stringent budget control. Operating expenses increased by 6,6% (2010: 13,7%) from R3 643 million in 2010

to R3 886 million in 2011.

2011 Financial Review 3

ASSETS AND LIABILITIES

The total assets increased by 8% (2010: 13%) to R8 878 million (2010: R8 191 million). The most significant categories of assets

are Property, Plant and Equipment, and Investments:

Property, Plant and Equipment

Property, Plant and Equipment increased from R2 200 million to R2 741 million, mainly due to the completion of the Engineering 3

Building and the Plant Sciences Building during the year. The University received infrastructure grants from the Department of

Higher Education and Training of R305,6 million for these and other infrastructure projects. The investment in these projects

supports the University’s objectives to increase the number of graduates in engineering and natural sciences.

Investments

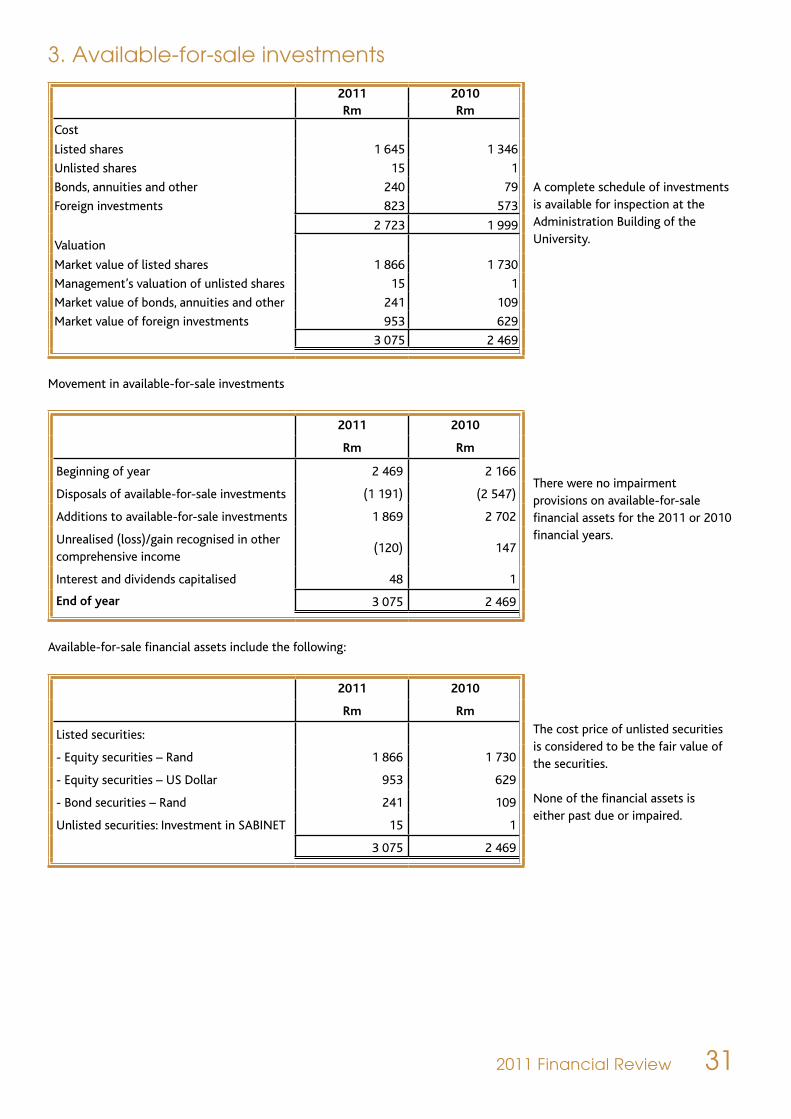

At 31 December 2011, the market value of the University’s investment portfolio was R3 075 million (2010: R2 469 million). The

major portion of investments is categorised under specifically funded activities that are either restricted or designated by Council.

The University’s investment funds serve the following purposes:

(1) Meet part of the short-term requirements of the University – these liabilities have a maximum term of 24 months. The risk

profile emphasises the need for capital protection over short periods and a high degree of liquidity.

(2) Meet some of the medium-term liabilities (two to five years) of the University – the risk appetite for these liabilities is a

combination of a moderate return relative to inflation (3,5% p.a.) plus capital protection over a period of three years.

(3) Meet the long-term liabilities (five years and more) of the University – the main requirement is a good return relative to

inflation (6% p.a.). The liquidity requirement is lower than for the other liabilities.

(4) A special class of the long-term liabilities is the University’s obligation to post-retirement medical aid benefits.

Portfolio Primary performance target Actual returns

Long-term capital portfolio 6% p.a. (net of fees) outperformance of consumer

price inflation over any rolling eight-year period.

6,4% p.a. real

Stable portfolio 3,5% p.a. (net of fees) outperformance of

consumer price inflation over any rolling three-

year period.

2,9% p.a. real

Money Market portfolio Performance in line with the STEFI (composite)

index

2,3% real

Continuation Medical Aid portfolio 6% p.a. (net of fees) outperformance of consumer

price inflation over any rolling eight-year period.

7,2% p.a. real

2011 Financial Review 4

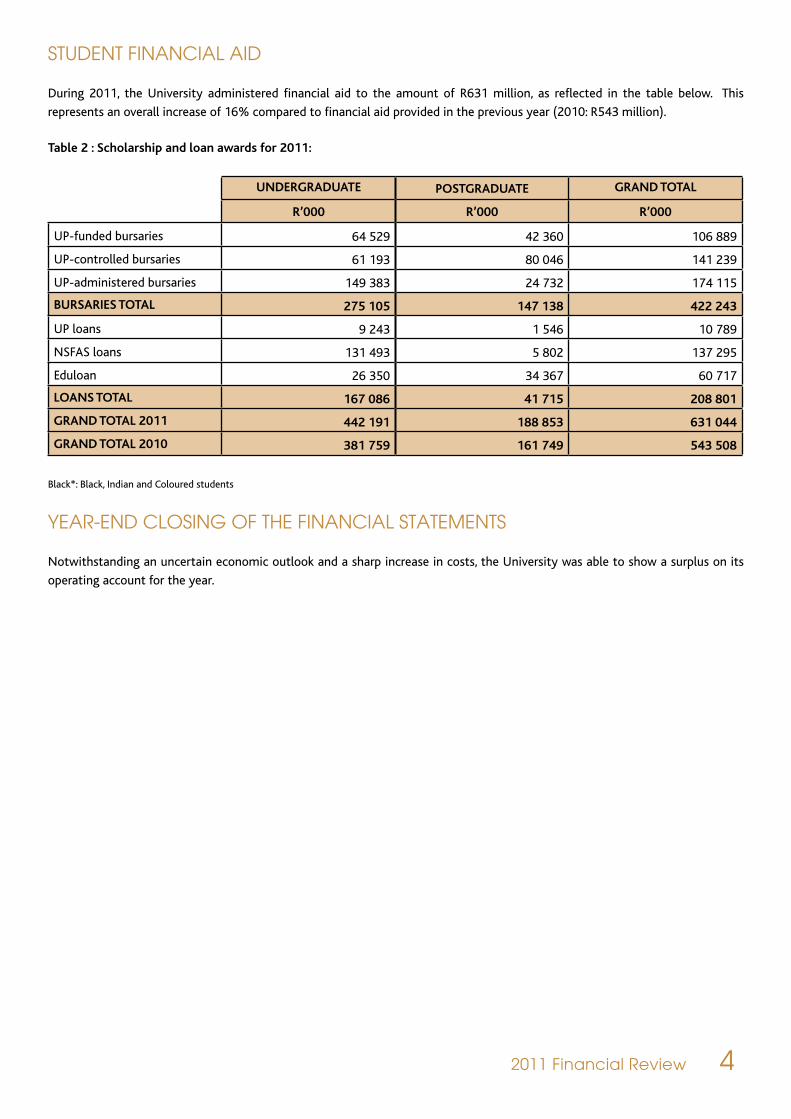

STUDENT FINANCIAL AID

During 2011, the University administered financial aid to the amount of R631 million, as reflected in the table below. This

represents an overall increase of 16% compared to financial aid provided in the previous year (2010: R543 million).

Table 2 : Scholarship and loan awards for 2011:

UNDERGRADUATE POSTGRADUATE GRAND TOTAL

R’000 R’000 R’000

UP-funded bursaries 64 529 42 360 106 889

UP-controlled bursaries 61 193 80 046 141 239

UP-administered bursaries 149 383 24 732 174 115

BURSARIES TOTAL 275 105 147 138 422 243

UP loans 9 243 1 546 10 789

NSFAS loans 131 493 5 802 137 295

Eduloan 26 350 34 367 60 717

LOANS TOTAL 167 086 41 715 208 801

GRAND TOTAL 2011 442 191 188 853 631 044

GRAND TOTAL 2010 381 759 161 749 543 508

Black*: Black, Indian and Coloured students

YEAR-END CLOSING OF THE FINANCIAL STATEMENTS

Notwithstanding an uncertain economic outlook and a sharp increase in costs, the University was able to show a surplus on its

operating account for the year.

2011 Financial Review 5

The University of Pretoria accepts that it has both an

obligation and a responsibility regarding the disclosure of

reliable financial information. To fulfil its responsibility in

this regard, the University maintains proper internal control

systems. These systems are designed to provide reasonable

assurance that the University’s assets are safeguarded

against unauthorised acquisition, use or disposal, and that the

accounting records provide a reliable basis for the preparation

of financial statements.

The internal control systems are based on an organisational

structure and the division of responsibilities. The University’s

established policies and procedures, including its Code of

Ethics, are communicated throughout the organisation to

foster a strong ethical climate. The University has also adopted

a Fraud Policy and Response Plan, as well as a Whistle Blowers

Policy to set the University’s stance on fraud and corruption

and to reinforce existing systems, policies and procedures

aimed at deterring, preventing, detecting, reacting to and

reducing the impact of fraud and corruption.

The University’s internal audit activities are performed by

the Department of Risk Management and Internal Audit,

while certain elements are co-sourced to an independent

firm of auditors. Internal control systems, in accordance with

the annual Internal Audit Plan, as approved by the Audit and

Risk Management Committee of Council, are appraised on a

continuous basis by either the Department of Risk Management

and Internal Audit, or the co-sourced independent internal

auditors. Such audit plan is largely based on the strategic risks

facing the University that emanated from the University’s risk

management process.

The internal audit function operates under the supervision

of the University Council. The Audit and Risk Management

Committee and the Standing Committee of Council exercise

the supervision on behalf of the Council. Weaknesses identified

in respect of the internal control systems are brought to the

attention of management and the Audit and Risk Management

Committee. Recommendations made to obviate weaknesses

are also submitted to management for appropriate action.

The effectiveness of any system of internal control is subject

to limitations. These limitations include the possibility

that human errors and the circumvention and overriding of

controls can occur. Effective internal control systems can only

provide reasonable assurance regarding the preparation of

financial statements and the safeguarding of assets. However,

the effectiveness of the systems can vary as circumstances

change.

REPORT ON INTERNAL ADMINISTRATIVE/ OPERATIONAL STRUCTURES AND CONTROLS

2011 Financial Review 6

REPORT ON RISK EXPOSURE ASSESSMENT AND THE MANAGEMENT THEREOF

The design, implementation and monitoring of the process of

risk management is the responsibility of the University. In this

regard, management is accountable to the University Council.

A Strategic Risk Management Committee, comprising members

of the Executive and a nominated Dean and Director, evaluates

and coordinates the management of identified strategic risks,

both financial and non-financial, faced by the University. Risk

management processes are reviewed regularly for continuing

relevance and effectiveness. The Strategic Risk Management

Committee reports to the Executive.

A report on the risk management process that is being

followed, as well as a summary of the risk register and

appropriate risk treatment plans, is presented to the Audit

and Risk Management Committee and to the Council of the

University on a regular basis.

APPROVAL OF THE CONSOLIDATED FINANCIAL STATEMENTS

The consolidated financial statements presented on pages

10 to 63 represent an extract of the full statements of

the University of Pretoria. These financial statements were

approved by the Council of the University of Pretoria at a

meeting held on 13 June 2012.

The full financial statements were prepared in accordance

with International Financial Reporting Standards and in the

manner required by the Minister of Higher Education and

Training in terms of section 41 of the Higher Education Act,

1997 (Act 101 of 1997), as amended.

The “going concern” approach has been adopted in the

preparing of the financial statements. Based on forecasts and

available cash resources, Council believes that the University

of Pretoria will remain a “going concern” for the foreseeable

future. The viability of the institution is borne out by the

content of the financial statements.

The financial statements have been audited by

PricewaterhouseCoopers Inc, who was given unrestricted access

to all financial records and related data, including the minutes

of meetings of Council and of all its committees. Council

believes that all representations made to the independent

auditors during their audit were valid and appropriate.

PROF CM DE LA REY PROF C KOORNHOFVice-Chancellor and Principal Executive Director

6 September 2012 6 September 2012

2011 Financial Review 7

INDEPENDENT AUDITOR’S REPORT TO THE COUNCIL OF THE UNIVERSITY OF PRETORIAREPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS

IntroductionWe have audited the consolidated financial statements of the University of Pretoria and its subsidiaries as set out on pages

10 to 63, which comprise the consolidated statement of financial position as at 31 December 2011, the consolidated income

statement and the consolidated statement of comprehensive income, statement of changes in equity and statement of cash

flows for the year then ended, and the notes, comprising a summary of significant accounting policies and other explanatory

information.

Council’s responsibility for the financial statementsCouncil is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with

International Financial Reporting Standards and the requirements of the Higher Education Act of South Africa, and for such

internal control as it determines is necessary to enable the preparation of consolidated financial statements that are free from

material misstatements, whether due to fraud or error.

Auditor’s responsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our

audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements,

and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free

from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated

financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of

material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments,

the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial

statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing

an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of

accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the

overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

PricewaterhouseCoopers Inc, 2 Eglin Road, Sunninghill 2157, Private Bag X36, Sunninghill 2157, South Africa

T: +27 (11) 797 4000, F: +27 (11) 797 5800, www.pwc.co.za

Executive: S P Kana (Chief Executive Officer) T P Blandin de Chalain D J Fölscher P J Mothibe S Subramoney F TonelliResident Director in Charge: E R MackeownThe company’s principal place of business is at 2 Eglin Road, Sunninghill where a list of directors’ names is available for inspection.Reg. no. 1998/012055/21, VAT reg.no. 4950174682

2011 Financial Review 8

OpinionIn our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the

University of Pretoria and its subsidiaries as at 31 December 2011, and their financial performance and cash flows for the year

then ended in accordance with International Financial Reporting Standards.

Other matterThe accompanying financial statements are not the statutory financial statements of the University and do not include all the

disclosures required by the Higher Education Act of South Africa. The statutory financial statements are available for inspection

at the Department of Higher Education and Training.

PricewaterhouseCoopers Inc.

Director: JFM Kotze

Registered Auditor

Johannesburg

6 September 2012

1 Summary of accounting policies

2011 Financial Review 9

2011 Financial Review 10

UNIVERSITY OF PRETORIA and its subsidiariesSUMMARY OF ACCOUNTING POLICIESFOR THE YEAR ENDED 31 DECEMBER 2011

1. General information

The consolidated financial statements were authorised for

issue by Council on 13 June 2012.

The University of Pretoria is a Higher Education Institution

governed by the Higher Education Act 101 of 1997 as amended

by Act 54 of 2000. The University of Pretoria is domiciled in

South Africa and the operations and principal activities of

the University relate to teaching, research and community

engagement. The presentation currency of the University of

Pretoria is South African Rands. All amounts are rounded to the

nearest thousand Rand.

2. Basis for preparation

The University prepared consolidated annual financial

statements in terms of International Financial Reporting

Standards (IFRS). The consolidated financial statements

are prepared in terms of the historical cost method and are

modified to accommodate the revaluation of available-for-

sale financial investments.

The preparation of financial statements in conformity with

IFRS requires the use of certain critical accounting estimates.

It also requires management to exercise its judgement in the

process of applying the University’s accounting policies. The

areas involving a higher degree of judgement or complexity,

or areas where assumptions and estimates are significant to

the University’s financial statements are disclosed in note 2.4.

The principal accounting policies adopted in the preparation

of these consolidated financial statements are set out below

and are consistent with those of the previous year, unless

otherwise stated.

2.1 Going concern

The University’s forecast and projections, taking account of

reasonably possible changes in operating circumstances, show

that the University should be able to operate within its current

financing. Council has a reasonable expectation that the

University has adequate resources to continue in operational

existence for the foreseeable future. The University therefore

continue to adopt the going concern basis in preparing its

annual financial statements.

2.2 New and amended standards adopted by the University

The accounting policies adopted are consistent with those of

the previous financial year, except for the following new or

amended standards and interpretations that were adopted

from the annual period beginning 1 January 2011:

• Amendment to IFRS 7, Financial Instruments: Disclosures –

This amendment clarifies certain of the disclosures relating

to credit risk.

• Amendment to IAS 1, Presentation of Financial Statements

– This amendment clarifies disclosures required for each

component of equity.

• Amendment to IAS 24, Related party disclosures – This

amendment clarifies and simplifies the definition of a

related party.

2.3 New standards, amendments and interpretations issued but not effective for the financial year beginning 1 January 2011 and not early adopted

IFRS 1 (Amendment): First-time Adoption of International

Financial Reporting Standards – Removal of Fixed Dates for

First-time Adopters (effective for financial periods beginning

on or after 1 July 2011). The amendment replaces references

2011 Financial Review 11

to a fixed date of ‘1 January 2004’ with ‘the date of transition

to IFRSs’, thus eliminating the need for companies adopting

IFRSs for the first time to restate derecognition transactions

that occurred before the date of transition to IFRSs.

IFRS 7 (Amendment): Financial Instruments: Disclosures –

Transfer of Financial Assets (effective for financial periods

beginning on or after 1 July 2011) – The amendment

will allow users of financial statements to improve their

understanding of transfer transactions of financial assets,

including understanding the possible effects of any risks that

may remain with the entity that transferred the assets. It

will also require additional disclosures if a disproportionate

amount of transfer transactions are undertaken around the

end of the reporting period.

IFRS 7 (Amendment): Financial instruments: Disclosures –

IFRS 9 Transitional Disclosures (effective for financial periods

beginning on or after 1 January 2015). The amendment

requires additional disclosures on the transition from IAS 39

to IFRS 9. This is only required where IFRS 9 is adopted for

financial periods beginning on or after 1 January 2013. If an

entity adopts IFRS 9 for financial period beginning on or after

1 January 2012 and before 1 January 2013, the entity can

either provide additional disclosure or restate prior periods.

IFRS 7 (Amendment): Financial instruments: Disclosures –

Offsetting of financial assets and financial liabilities (effective

for financial periods beginning on or after 1 January 2013). The

amended disclosures will require more extensive disclosures

than are currently required under IFRS. The disclosures focus

on quantitative information about recognised financial

instruments that are offset in the statement of financial

position as well as those recognised financial instruments

that are subject to master netting or similar arrangements

irrespective of whether they are offset.

IFRS 9, Financial instruments (effective for financial periods

beginning on or after 1 January 2015):

• IFRS 9 addresses classification and measurement of

financial assets. It uses a single approach to determine

whether a financial asset is measured at amortised

cost or at fair value;

• IFRS 9 was amended to incorporate financial

liabilities. The accounting and presentation for

financial liabilities and for derecognising financial

instruments has been relocated from IAS 39, ‘Financial

instruments: Recognition and measurement’,

without change, except for financial liabilities that

are designated at fair value through profit or loss.

The amendment introduces new requirements that

address the problem of volatility in profit or loss

(P&L) arising from an issuer choosing to measure its

own debt at fair value. With the new requirements,

an entity choosing to measure a liability at fair value

will present the portion of the change in its fair value

due to changes in the entity’s own credit risk in the

other comprehensive income (OCI) section of the

statement of comprehensive income, rather than

within P&L.

IFRS 10 Consolidated Financial Statements (effective for

financial periods beginning on or after 1 January 2013) – IFRS

10 establishes principles for the presentation and preparation

of consolidated financial statements when an entity controls

one or more other entities and supersedes IAS 27 Consolidated

and Separate Financial Statements. IFRS 10 changes the

definition of control so that the same criteria are applied to all

entities to determine control. The revised definition of control

focuses on the need to have both power and variable returns

before control is present. The standard provides additional

guidance to assist in determination of control where this is

difficult to assess.

IFRS 13 Fair Value Measurement (effective for financial periods

beginning on or after 1 January 2013) – IFRS 13 defines fair

value, sets out in a single IFRS a framework for measuring

fair value, and sets out disclosure requirements on fair value

measurements.

IAS 12 (Amendment): Income taxes – Deferred tax: Recovery

of underlying assets (effective for financial periods beginning

on or after 1 January 2012) – A limited scope amendment to

the recovery of underlying Basis of preparation continued

IAS 32 (Amendment): Financial instruments: Presentation

(effective for financial periods beginning on or after 1 February

2014) – Offsetting of financial assets and financial liabilities

has been amended to clarify that the right to offset must be

available today – that is it is not contingent on a future event.

It must also be legally enforceable for all counterparts in the

normal course of business, as well as in the event of default,

insolvency or bankruptcy. The amendments also clarify that

gross settlement mechanisms (such as through a clearing

house) with features that both (i) eliminate credit and liquidity

risk and (ii) process receivables and payables in a settlement

process are effectively equivalent to net settlement; they

would therefore satisfy the IAS 32 criterion in these instances.

2011 Financial Review 12

2.4 Critical accounting estimates and judgements

Some of the amounts included in the consolidated financial

statements involve the use of judgement and/or estimation.

These judgements and estimates are based on management’s

best knowledge of the relevant facts and circumstances,

having regard to prior experience, but actual results may

differ from the amounts included in the consolidated

financial statements. Information about such judgements and

estimations is contained in the accounting policies and/or the

notes to the consolidated financial statements, and the key

areas are summarised below.

Areas of judgement and key sources of estimation uncertainty

that have the most significant effect on the amounts

recognised in the consolidated financial statements are:

Impairment of receivables

The University tests whether trade receivables have suffered

any impairment in accordance with the accounting policy in

note 11. Assets that are individually significant are considered

separately for impairment. When these assets are impaired,

any impairment loss is recognised directly against the related

asset. Assets that are individually significant and that are not

impaired, and groups of smaller balances are considered for

impairment on a portfolio basis, based on similar credit risk.

Impairment losses are recognised in an “allowance account for

credit losses” until the impairment can be identified with an

individual asset, and, at that point, the allowance is written off

against the individual asset. Subsequent recoveries of amounts

previously written off are credited in the income statement.

Refer to note 7 for the carrying amount of receivables and the

impairment losses provided for in 2011.

Provisions

Provision for postretirement benefits has been recognised

in accordance with the accounting policy in note 20. The

cost of postemployment benefits is determined using

actuarial valuations. The actuarial valuation involves making

assumptions about discount rates, mortality rates and income

at retirement. Due to the long-term nature of these plans,

such estimates are subject to significant uncertainty. The main

assumptions and carrying amounts related to postretirement

benefits are summarised in note 10.

Deferred revenue

The University recognises private grants received, to

compensate for expenses incurred, as income. These grants are

subject to various requirements and therefore each grant is

recognised over a certain period (specific to each grant) under

the terms of the grant. In several instances, the contract’s

terms do not specifically determine that unspent amounts

are refundable but the nature of the grants and historic

experience necessitate the deferral of unspent amounts

to deferred income. Grants received are therefore limited

to the expenses incurred and the balance is recognised as

deferred income in the statement of financial position. Grants

obtained, to reimburse expenses incurred, are analysed on an

“individual contract” basis by grouping similar grants together.

The deferral of income therefore necessitates a degree of

judgement by management. Refer to note 14 for the carrying

amount of deferred income.

3. Reserve funds

3.1 Unrestricted operating fund

The unrestricted operating fund reflects the University’s

subsidised activities and also includes the tuition fees and

expenditure in respect of the formal courses of the Gordon

Institute of Business Science (GIBS). Additions to these funds

mainly comprise formula-subsidy, tuition fees and the sales

and services of educational activities (patient fees at the

Veterinary Academic Hospital) as well as transfers from other

funds to finance expenditure.

Expenditure mainly comprises direct expenses in academic

departments for teaching and learning, research and

community service as well as other support service expenses

such as academic administration, library facilities, bursaries

and loans. Institutional expenses, such as expenses incurred

for the Executive, student services, information technology

and operating costs regarding land and buildings, are also

recorded here.

3.2 Restricted funds

These funds may be used only for the purposes that have been

specified in legally binding terms by the provider of such funds

or by another legally empowered person.

3.3 Council designated funds

These funds fall under the absolute discretion/control of

Council, e.g. sales of goods and services; non-prescriptive

2011 Financial Review 13

donations and grants; income from investments that are

not held as cover for trust; specific purpose endowments or

administrated funds; etc.

3.4 Non-distributable reserves

These funds consist of the available-for-sale investment

revaluation reserve. Gains/losses on the fair value adjustments

of investments are recognised in a revaluation reserve until

such time as the investment is disposed, in which case the

gain/loss will be recognised in the income statement.

4. Revenue recognition

Revenue is generally recognised at the fair values of the

amounts of goods received or receivable. Revenue is shown

net of value-added tax, returns, rebates and discounts and

after eliminating sales within the group.

4.1 Government and other grants relating to income

Grants from the government are recognised at their fair value

where there is a reasonable assurance that the grant will be

received and the University will comply with all attached

conditions. The University follows the income approach

whereby the grant is taken to income (over one or more periods,

where relevant) and not the capital approach whereby the

grant is credited directly to shareholders’ interest. Government

grants relating to costs are deferred and recognised in the

income statement over the period necessary to match them

with the costs that they are intended to compensate. Private

gifts, grants and donations are recognised as income at the

fair value of the consideration received or receivable in the

period to which they relate. Any such income is recognised as

income in the financial period when the University is entitled

to use those funds. Therefore, funds that will not be used until

some specified future period or occurrence are recognised as

deferred income and released to the income statement as the

University becomes entitled to the funds. Grants received to

compensate for expenses to be incurred are often prescriptive

in nature and therefore it is recognised over a certain period

under the terms of the grant. Prescriptive grant income

is recognised with reference to the stage of completion

at the reporting date. If the stage of completion cannot be

measured reliably, the recognition of this income is limited to

the expenses incurred. The balance is recognised as deferred

income in the statement of financial position.

4.2 Government and other grants relating to assets

Government grants relating to property, plant and equipment

are included in non-current liabilities as deferred government

grants and are recognised in the income statement on a

straight-line basis over the expected lives of the related assets.

The portion of the grants that will be released to the income

statement during the next 12 months are included in current

liabilities.

4.3 Tuition fees and residence fees

Tuition fees and residence fees are recognised as income at

the fair value of the consideration received or receivable in

the period to which they relate. Revenue for tuition and

residence services is recognised with reference to the stage of

completion at the reporting date, based on services performed

to date as a percentage of total services to be performed.

Deposits provided by prospective students are treated as

current liabilities until the amount is billed as being due to the

University.

4.4 Restricted and earmarked funds

The University recognises grants received to compensate for

expenses incurred as income. These grants are often prescriptive

and therefore they are recognised over a certain period under

the terms of the grant. The recognition of this income is limited

to the expenses incurred. The balance is recognised as deferred

income in the statement of financial position.

4.5 Donations and gifts

Donations and gifts are recognised on receipt at fair value.

Donations in kind are recognised at the fair value thereof.

4.6 Investment income

Investment funds are pooled and the investment income is

apportioned to the various participating funds in proportion

to their balances.

2011 Financial Review 14

Interest income is recognised in profit or loss on a time-

proportion basis using the effective interest rate method.

Dividend income is recognised in profit or loss when the right

to receive payment is established.

When a receivable is impaired, the University and its

subsidiaries reduce the carrying amounts to its recoverable

amount, being the estimated future cash flow discounted

at the original effective interest rate of the instrument, and

continues unwinding discount as interest income. Interest

income on impaired loans is recognised using the original

effective interest rate.

4.7 Other income

Inter-departmental income and expenditure are eliminated.

Occasional sales and services are recognised in the period in

which they accrue.

5. Subsidiaries

Subsidiary entities are those entities over which the University

has the power, directly or indirectly, to exercise control.

Control is the power to govern the financial and operating

policies generally accompanying a shareholding of more than

one half of the voting rights. All subsidiaries are consolidated.

Subsidiaries are consolidated with effect from the date on

which effective control is transferred to the University and are

no longer consolidated with effect from the date of disposal

or when control ceases.

The acquisition method of accounting is used to account for

the acquisition of subsidiaries by the University. The cost of an

acquisition is measured as the fair value of the assets given,

equity instruments issued and liabilities incurred or assumed

at the date of exchange, plus costs directly attributable to

the acquisition. Identifiable assets acquired and liabilities and

contingent liabilities assumed in a business combination are

measured initially at their fair values at the acquisition date,

irrespective of the extent of any non-controlling interest.

The excess of the cost of acquisition over the fair value of

the University’s share of the identifiable net assets acquired

is recorded as goodwill. If the cost of acquisition is less than

the fair value of the net assets of the subsidiary acquired, the

difference is recognised directly in the income statement.

All inter-company transactions, balances as well as unrealised

gains and losses, are eliminated. Where it was found to be

necessary, accounting policies for subsidiary companies are

changed to ensure consistency with the policies adopted by

the University.

6. Non-controlling interest

The University and its subsidiaries apply a policy of treating

transactions with non-controlling interests as transactions

with parties external to the group. Disposals to non-controlling

interests result in gains and losses for the group and are

recorded in the income statement. Purchases from non-

controlling interests result in goodwill, being the difference

between any consideration paid and the relevant share

acquired of the carrying value of net assets of the subsidiary.

7. Associated companies

Associates are all entities over which the University and its

subsidiaries have significant influence but not control, generally

accompanying a shareholding of between 20% and 50% of

the voting rights. Investments in associates are accounted

for using the equity method of accounting and are initially

recognised at cost. The investment in associates includes

goodwill identified on acquisition, net of any accumulated

impairment loss.

The University and its subsidiaries’ share of its associates’

post-acquisition profits or losses is recognised in the income

statement, and its share of post-acquisition movements

in reserves is recognised in reserves. The cumulative post-

acquisition movements are adjusted against the carrying

amount of the investment. When the University and its

subsidiaries’ share of losses in an associate equals or exceeds

its interest in the associate, including any other unsecured

receivables, the University and its subsidiaries do not recognise

further losses, unless it has incurred obligations or made

payments on behalf of the associate.

2011 Financial Review 15

Unrealised gains on transactions between the University, its

subsidiaries and its associates are eliminated to the extent of

the group’s interest in the associates. Unrealised losses are

also eliminated unless the transaction provides evidence of

an impairment of the asset transferred. Accounting policies

of associates have been changed where necessary to ensure

consistency with the policies adopted by the University and

its subsidiaries.

Dilution gains and losses arising in investments in associates

are recognised in the income statement.

8. Foreign currencies

The consolidated annual financial statements are presented

in South African Rand, the functional and presentation

currency of the University. Foreign currency transactions are

accounted for at the exchange rates prevailing at the date

of the transactions. Monetary balances are translated at

the exchange rates prevailing at year end. Gains and losses

resulting from the settlement of such transactions and from

the translation of monetary assets and liabilities denominated

in foreign currencies are recognised in the income statement

in the year in which they arise.

9. Financial instruments

Financial instruments carried on the statement of financial

position include cash and bank balances, available-for-sale

investments, receivables, other receivables, trade payables and

borrowings. The particular recognition methods adopted are

disclosed in the individual policy statements associated with

each item.

The purchases and sale of financial assets that require delivery

are recognised on trade date, being the date on which the

University commits to purchase or sell the asset.

The University and subsidiary companies recognise a financial

asset or a financial liability on its statement of financial

position when, and only when, the group becomes a party to

the contractual provisions of the instrument.

Financial assets are derecognised when the rights to receive

cash flows from the financial asset have expired or have been

transferred and the group has transferred substantially all risks

and rewards of ownership. Financial liabilities (or a part of the

financial liability) is removed from the statement of financial

position when the obligation specified in the contract is

discharged or cancelled or expires.

10. Goodwill

Goodwill represents the excess of the cost of an acquisition

over the fair value of a subsidiary of the University’s share of

net assets of the acquired subsidiary undertaking at the date

of the acquisition. The carrying amount of goodwill is reviewed

annually and adjusted for impairment where it is considered

necessary.

11. Intangible assets

Computer software development costs

Costs incurred on development projects (relating to the design

and testing of new or improved products) are recognised as

intangible assets when the following criteria are fulfilled:

• it is technically feasible to complete the intangible

asset so that it will be available for use;

• management intends to complete the intangible

asset and use or sell it;

• there is an ability to use or sell the intangible asset;

• it can be demonstrated how the intangible asset will

generate probable future economic benefits;

• adequate technical, financial and other resources

to complete the development and to use or sell the

intangible asset are available; and

• the expenditure attributable to the intangible asset

during its development can be reliably measured.

Development costs include expenditure relating to the

implementation partner, additional staff employed specifically

for the Enterprise Resource Planning System, hardware and

software purchased specifically for the Enterprise Resource

Planning System. Capitalised development costs are amortised

from the point at which the asset is ready for use on a straight-

line basis over its estimated useful life of 10 years, however

the method of depreciation, useful live and residual value are

reviewed annually. Intangible assets are not revalued.

2011 Financial Review 16

Artwork

Artwork is recorded at cost or the estimated fair value at

the date of the donation. The fair value is deemed to be a

reasonable market value at the date of the donation or the

purchase price of the item. The market value at the date of the

donation is determined by an art appraiser. The useful life of

artwork is considered to be indefinite as artwork is not subject

to wear and tear. Intangible assets are not revalued. The

carrying amount is tested for impairment and whenever there

is an indication that the intangible asset may be impaired.

There was no indication that artwork should be impaired.

Vodacom league licence and franchise fee

Licences and franchise fees are shown at historical cost. Both

these categories have a definite useful life and are carried at

cost less accumulated amortisation. Amortisation is calculated

using the straight-line method to allocate cost of licences and

franchise fees over the estimated useful lives of 20 years for

licences and five years for franchise fees.

An intangible asset is regarded as having an indefinite useful life

when, based on all relevant factors, there is no foreseeable limit

to the period over which the asset is expected to generate net

cash inflows. Amortisation is not provided for these intangible

assets. For all other intangible assets amortisation is provided

on a straight line basis over their useful life. The amortisation

period and the amortisation method for intangible assets are

reviewed every period-end.

Reassessing the useful life of an intangible asset with a

definite useful life after it was classified as indefinite is an

indicator that the asset may be impaired. As a result the asset

is tested for impairment and the remaining carrying amount is

amortised over its useful life.

Internally generated brands, mastheads, publishing titles,

customer lists and items similar in substance are not

recognised as intangible assets.

12. Financial assets

Financial assets are classified in the following categories:

loans and receivables (student loans and loans to staff,

trade receivables) and available-for-sale financial assets.

The classifications depend on the purpose for which the

financial assets were acquired. Management determines the

classification of its investments at initial recognition.

All financial assets are accounted for at trade date.

Prepaid expenses comprise that portion of expenses that is

paid in the current year, but is applicable to the following

financial year. Prepaid expenses are not classified as a financial

asset and are included under non-financial assets.

12.1 Loans and receivables

Loans to students and staff are non-derivative financial assets

with fixed or determinable payments that are not quoted in

an active market. They are initially measured at fair value, plus

transaction costs and are included in current assets, except

for maturities greater than 12 months after the end of the

reporting period.

These are classified as non-current assets. The University’s

loans and receivables comprise “student and other loans”

and “cash and cash equivalents” in the statement of financial

position (notes 5, 7 & 8).

Subsequently, items included in this category are measured

at the amortised cost, calculated based on the effective

interest method, and interest income is included in profit or

loss for the period. Net gains or losses represent reversals of

impairment losses, impairment losses and gains and losses

on derecognition. Net gains or losses are included in “other

income” or “other expenses”.

Short-term receivables with no stated interest rate are

measured at the original invoice amount if the effect of

discounting is immaterial.

Trade receivables are non-derivative financial assets with fixed

or determined payments that are not quoted in an active

market. Financial assets classified as receivables are initially

recognised at fair value plus transaction costs. Subsequent to

recognition, receivables are carried at amortised cost using the

effective interest rate method, less provision for impairment.

Short term receivables which are due within 12 months, with

no stated interest are measured at the original invoice amount

if the effect of discounting is immaterial.

A provision for impairment for trade receivables is established

when there is objective evidence that the University will not

be able to collect all amounts due according to the original

terms of receivables. Significant financial difficulties of the

debtor and default or delinquency in payments are considered

indicators that the trade receivable is impaired. An impairment

loss is recognised in profit or loss when the carrying amount

of the asset exceeds its recoverable amount. The recoverable

amount is calculated as the present value of the estimated

2011 Financial Review 17

future cash flows discounted at the original effective interest

rate of the instrument.

Impairment losses are recognised on loans and receivables

when there is objective evidence of impairment. An impairment

loss is recognised in profit or loss when the carrying amount

of the asset exceeds its recoverable amount. The recoverable

amount is calculated as the present value of the estimated

future cash flows discounted at the original effective interest

rate of the instrument.

Assets that are individually significant are considered

separately for impairment. When these assets are impaired,

any impairment loss is recognised directly against the related

asset. Assets that are individually significant and that are not

impaired, and groups of small balances are considered for

impairment on a portfolio basis, based on similar credit risk.

Impairment losses are recognised in an “allowance account for

credit losses” until the impairment can be identified with an

individual asset, and, at that point, the allowance is written off

against the individual asset. Subsequent recoveries of amounts

previously written off are credited in the income statement.

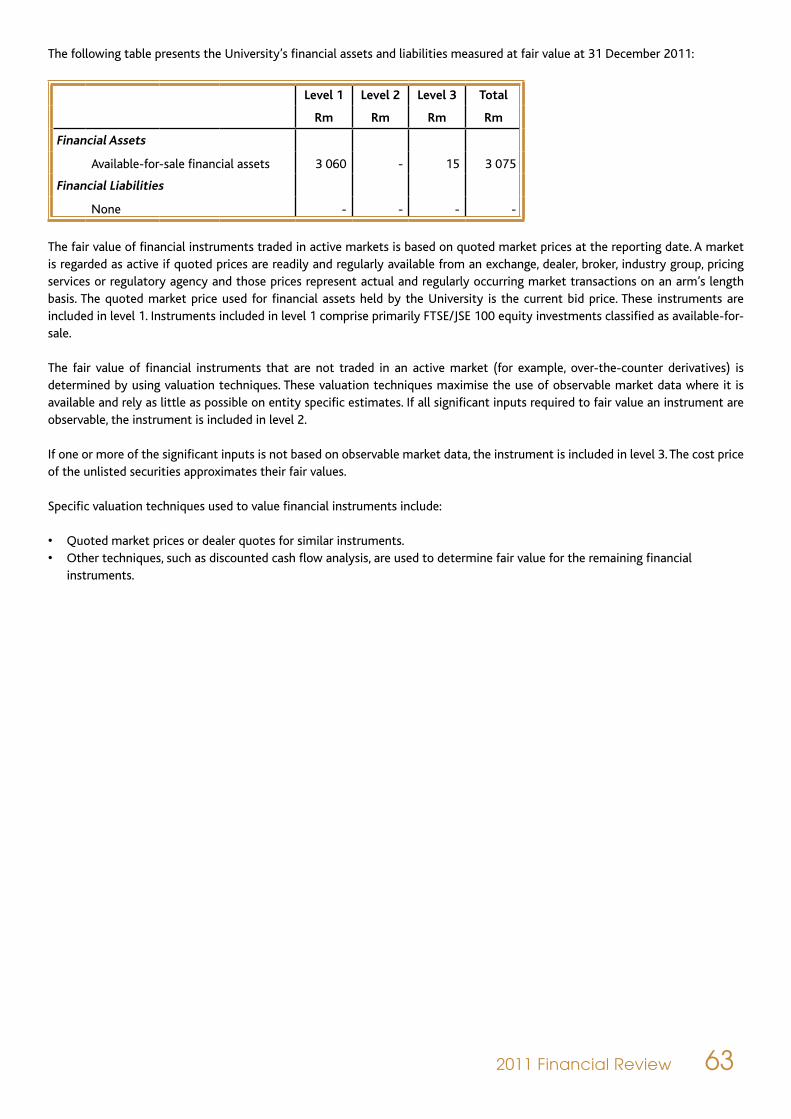

12.2 Available-for-sale financial assets

Financial assets classified as available-for-sale are initially

recognised at fair value plus transaction costs. Subsequent to

initial recognition, available-for-sale financial assets are carried

at fair value. The fair value of financial instruments traded in

active markets is based on quoted market prices at year end.

The quoted market price used for financial assets is the current

bid price as per the Johannesburg Stock Exchange. If the market

value of an investment cannot be determined, the investment is

measured using an acceptable valuation method.

Unrealised gains and losses arising from the change in fair

value are recognised directly in equity until the asset is

derecognised or impaired, at which time the cumulative gain

or loss previously recognised in equity is recognised in the

income statement. However, interest income on these items,

calculated using the effective interest method, is recognised

in profit or loss. Dividend income is recognised when the

University’s right to payment has been established and it is

included in “other income”. Net foreign exchange gains or

losses on monetary available-for-sale financial assets are

recorded directly in profit or loss as part of “other income”

or “other expenses”. Cumulative gains or losses accumulated

in equity are recognised in profit or loss upon disposal or

impairment of the financial asset, as part of net gains or losses,

and are included in “other income” or “other expenses”.

The University and its subsidiaries assess at each year end

whether there is objective evidence that a financial asset

or group of assets is impaired. A financial asset is impaired if

its carrying amount is greater than its estimated recoverable

amount. Available-for-sale financial assets will become impaired

when a significant or prolonged decline in the fair value of the

investment below its cost price or amortised cost is noted.

If any objective evidence of impairment exists for available-

for-sale financial assets, the cumulative loss, measured as the

difference between the acquisition cost and current fair value,

less any impairment loss on the financial asset previously

recognised in profit or loss, is removed from equity and

recognised in the income statement. If, in a subsequent period,

the fair value of a debt instrument classified as available-for-

sale increases and the increase can be objectively related to

an event occurring after the impairment loss was recognised

in profit or loss, the impairment loss is reversed through the

income statement.

Investments exclude entities of which the operating results

are included in the consolidated financial statements of the

University.

13. Property, plant and equipment

Land and buildings mainly consist of lecture halls, laboratories,

hostels and administrative buildings. All property, plant and

equipment are recorded at cost less accumulated depreciation.

Cost includes expenditure that is directly attributable to

the acquisition of the items. Property, plant and equipment

acquired by means of donations are recorded at fair value at

the date of the donation.

Depreciation is calculated as follows, using the straight-line

method to write off the cost of each asset to its residual

values over its estimated useful life:

• Buildings 15–50years

• Vehicles 5years

• Computerequipment(average) 3–5years

• Furnitureandequipmentandlaboratory

equipment 5–10 years

• Library items are depreciated in full in the year of

acquisition.

2011 Financial Review 18

• Landisnotdepreciatedasitisdeemedtohaveanindefinite

life.

• The methods of depreciation, useful lives and residual

values are reviewed annually where the specific assets

differs from the norm.

• Depreciationischargedtotheincomestatement.

Routine maintenance costs are charged to income as they are

incurred. The costs of major maintenance or overhaul of an

item of property, plant or equipment are recognised in the

carrying amount of the item of property, plant and equipment

if it is probable that future economic benefits associated with

the item will flow to the University and the cost of the item

can be measured reliably. Expenditure incurred to replace

a component of an item is capitalised to the cost of the

item. Any remaining carrying amount of the replaced part is

derecognised.

Property, plant and equipment are assessed at each reporting

date to determine whether there is an indication that the

carrying amount of the asset may be impaired. If such an

indication exists, the recoverable amount of the asset is

determined. The recoverable amount of an asset is the

higher of its fair value less costs to sell and its value in use. In

determining the value in use, the estimated future cash flows

of the asset is discounted to their present value based on pre-

tax discount rates that reflects current market assessments

of the time value of money and the risks that are specific to

the asset. If the value in use of an individual asset for which

there is an indication of impairment cannot be determined,

the recoverable amount of the cash-generating unit to which

the asset belongs is determined. An asset’s cash-generating

unit is the smallest group of identifiable assets that includes

the asset and that generates cash inflows from continuing use

that are largely independent from cash inflows from other

assets.

An impairment loss is recognised in profit or loss when the

carrying amount of an individual asset or of a cash-generating

unit exceeds its recoverable amount. Impairment losses

recognised on cash-generating units are firstly allocated to

goodwill and secondly, on a pro rata basis, to the other assets

in the cash-generating unit.

Impairment losses recognised on goodwill are not reversed.

With regard to other assets, impairment losses are reversed if

there has been a change in the estimates used to determine

the recoverable amount of the asset or cash-generating unit.

Reversals of impairment losses on cash-generating units are

allocated on a pro rata basis to the assets in the unit, excluding

goodwill. Impairment losses are reversed only to the extent

that the carrying amount of the asset does not exceed the

carrying amount that would have been determined if no

impairment loss had been recognised in the past. Reversals of

impairment losses are recognised directly in profit or loss.

Gains and losses on the disposal of property, plant and

equipment are determined by reference to their carrying

amounts and are taken into account in determining operating

profit.

14. Accounting for leases

14.1 Finance lease

Leases of property, plant and equipment in respect of which

the University assumes the benefits and risks of ownership are

classified as finance leases. Finance leases are capitalised at

the estimated fair value of the leased assets, or, if lower, at

the present value of the underlying lease payments. Each lease

payment is allocated to the liability and finance charges so as

to achieve a constant rate on the outstanding finance balance.

The corresponding rental obligations, net of finance charges,

are included in other long-term payables. The interest element

of the finance charge is charged to the income statement over

the lease period. The property, plant and equipment acquired

under finance leasing contracts are depreciated over the

shorter of the useful life of the asset and the lease term.

14.2 Operating lease

Leases of assets, in terms of which all the risks and benefits of

ownership are effectively retained by the lessor, are classified

as operating leases. Payments made in terms of operating

leases are charged to the income statement on a straight-line

basis over the period of the lease.

When an operating lease is terminated before the lease period

has expired, any payment required to be made to the lessor

by way of penalty is recognised as an expense in the period in

which termination takes place.

2011 Financial Review 19

15. Inventories

Inventories are initially measured at cost and subsequently

valued at the lower of cost and net realisable value. Any write-

down to net realisable value is recognised in profit or loss. Cost

is determined on the weighted average-cost basis and when

a perpetual inventory system is not present it is determined

at the most recent purchase price. Net realisable value is an

estimate of the selling price in the ordinary course of business,

excluding the cost of completion and selling expenses.

16. Cash and cash equivalents

Cash and cash equivalents are initially recognised at fair

value and subsequently measured at amortised cost. For

the purposes of the cash-flow statement, cash and cash

equivalents comprise cash in hand, deposits held at call with

banks and investments in money market instruments, net of

bank overdrafts. In the statement of financial position, bank

overdrafts are included in borrowings under current liabilities.

Cash equivalents are short term highly liquid investments that

are readily convertible to known amounts of cash and which

are subject to insignificant changes in value.

17. Trade payables

Trade payables are obligations to pay for goods or services that

have been acquired in the ordinary course of business from

suppliers. Accounts payable are classified as current liabilities

if payment is due within one year or less (or in the normal

operating cycle of the business if longer). If not, they are

presented as non-current liabilities.

Trade payables are recognised initially at fair value and

subsequently measured at amortised cost using the effective

interest method.

18. Provisions

Provisions are recognised when the University has a present

legal or constructive obligation as a result of past events, it is

probable that an outflow of resources embodying economic

benefits will be required to settle the obligation, and a reliable

estimate of the amount of the obligation can be made.

Provisions are measured based on the best estimate of the

expenditure required to settle the present obligation at the

reporting date. Where the effect of the time value of money is

material, the amount of the provision is discounted to present

value using a pretax rate that reflects current assessments of

the time value of money. The increase in the amount of the

provision as a result of the passage of time is recorded in profit

or loss for the year.

19. Borrowings

Borrowings are recognised initially at fair value, net of

transaction costs incurred. Borrowings are subsequently stated

at amortised cost; any difference between the proceeds (net

of transaction costs) and the redemption value is recognised in

the income statement over the period of the borrowings using

the effective interest method.

Borrowings are classified as current liabilities unless the

University has an unconditional right to defer settlement of

the liability for at least 12 months after the year end.

20. Current and deferred income tax

The tax expense for the period comprises current and deferred

tax. Tax is recognised in the income statement, except to the

extent that it relates to items recognised directly in equity. In

this case, the tax is also recognised in equity.

2011 Financial Review 20

The current income tax charge is calculated on the basis

of the tax laws enacted or substantively enacted at year

end in South Africa where the University’s subsidiaries and

associates operate and generate taxable income. Management

periodically evaluates positions taken in tax returns with

respect to situations in which applicable tax regulations is

subject to interpretation and establishes provisions where

appropriate on the basis of amounts expected to be paid to

the tax authorities.

Deferred income tax is provided in full, using the liability

method, on temporary differences arising between the tax

bases of assets and liabilities and their carrying amounts in

the consolidated financial statements. However, the deferred

income tax is not accounted for if it arises from initial

recognition of an asset or liability in a transaction other than

a business combination that at the time of the transaction

affects neither the accounting, nor taxable profit or loss.

Deferred income tax is determined using tax rates (and laws)

that have been enacted or substantially enacted by year end

and are expected to apply when the related deferred income

tax asset is realised or the deferred income tax liability is

settled.

Deferred income tax assets are recognised to the extent that it

is probable that future taxable profit will be available against

which the temporary differences can be utilised.

Deferred income tax is provided on temporary differences

arising on investments in subsidiaries and associates, except

where the timing of the reversal of the temporary difference is

controlled by the group and it is probable that the temporary

difference will not reverse in the foreseeable future.

21. Postemployment benefits

21.1 Pension and provident fund contributions

The University contributes towards two pension schemes

namely the AIPF and the UP Pension Fund as well as towards

one provident fund known as the UP Provident Fund. The

AIPF is registered and managed in terms of the Pension Funds

Act for Associated Institutions. The UP Pension Fund and

the UP Provident Fund are managed by Boards of Trustees

and are registered in terms of the provisions of the Pension

Funds Act. The schemes are funded through payments to

trustee-administered funds, determined by periodic actuarial

calculations.

A defined contribution plan is a pension plan under which

the entity pays fixed contributions into a separate entity. The

entity has no legal or constructive obligations to pay further

contributions if the fund does not hold sufficient assets to

pay all employees the benefits relating to employee service

in the current and prior periods. A defined benefit plan is a

pension plan that is not a defined contribution plan. Following

the above-mentioned definitions, the University therefore

contributes towards one defined contribution plan (the AIPF

Fund) and two defined benefit plans (the UP Pension Fund and

the UP Provident Fund). The UP Provident Fund is a “defined

contribution” plan with regards to members’ retirement

benefits. However, the disability and death benefits stipulated

in the rules of the Provident Fund represent a “defined benefit”

component. As a result of the defined benefit component, the

UP Provident Fund is classified as a defined benefit plan.

The asset recognised in the statement of financial position

in respect of defined benefit plan is measured at the lower

of (1) the fair value of the plan assets less the present value

of the defined benefit obligation at year end together with

adjustments for unrecognised actuarial gains or losses and

past service costs; and (2) the sum of the present value of any

economic benefits in the form of refunds from the plan or

reductions in future contributions to the plan and any balance

of unrecognised actuarial losses or unrecognised past service

costs. The defined benefit obligation is calculated annually

by independent actuaries using the projected unit credit

method. The present value of the defined benefit obligation is

determined by discounting the estimated future cash outflows

using interest rates of high-quality corporate bonds that are

denominated in the currency in which the benefits will be paid

and that have terms to maturity approximating to the terms

of the related pension liability.

For defined contribution plans, the University pays

contributions to privately administered pension insurance

plans on a mandatory, contractual or voluntary basis.

The University has no further payment obligations once

the contributions have been paid. The contributions are

recognised as employee benefit expense when they are due.

Prepaid contributions are recognised as an asset to the extent

that a cash refund or a reduction in the future payments is

available.

2011 Financial Review 21

Actuarial gains and losses are recognised immediately in the

year in which they occur. Actuarial gains and losses arising

from experience adjustments are charged or credited to the

statement of comprehensive income.

Past-service costs are recognised immediately in income,

unless the changes to the pension plan are conditional on the

employees remaining in service for a specified period of time

(the vesting period). In this case, the past-service costs are

amortised on a straight-line basis over the vesting period.

21.2 Medical aid fund contributions

In accordance with the existing personnel practice, the Council

has undertaken to make certain medical aid fund contributions

on behalf of retired staff and certain future retirees.

The expected costs of these benefits are accrued over the period

of employment using the same accounting methodology as

used for defined benefit pension plans. Actuarial gains and

losses arising from experience adjustments are charged or

credited to income. These obligations are valued annually by

independent qualified actuaries.

Actuarial gains and losses are recognised immediately in the

year in which they occur in the statement of comprehensive

income.

22. Agency funds

There are funds administered on behalf of beneficiaries of

deceased employees and other third parties. These funds are

recognised at the fair value thereof and subsequently carried

at amortised cost.

These funds are held in available-for-sale investments or cash

and cash equivalents until payments are requested by the

beneficiaries of these funds.

23. Leave accrual

Members of staff with leave with gratuity value to their

credit at the end of 2006 had a choice of either disbursing

the accumulated leave (as at 31 December 2006) to them

at the end of March 2007, or to retain such leave credits in

the system at the value as determined above. Leave credits

retained will be disbursed to the relative staff member upon

termination of service or on request at any time after March

2007, at the value as at 31 December 2006.

24. Research costs

Research costs are written off in the year in which they arise,

since both these types of costs are inherent in the normal

operations of a university. Research costs are not recorded or

disclosed separately.

25. Borrowing costs

Borrowing costs incurred for the construction of any qualifying

asset are capitalised during the period of time that is required

to complete and prepare the asset for its intended use. Other

borrowing costs are expensed.

2 Consolidated statement of financial position

2011 Financial Review 22

2011 Financial Review 23

UNIVERSITY OF PRETORIA and its subsidiariesSUMMARISED CONSOLIDATED STATEMENT OF FINANCIAL POSITION AT 31 DECEMBER 2011

Notes 2011 2010

Rm Rm

ASSETS

Non-current assets 6 623 5 411

Property, plant and equipment 1 2 741 2 200

Intangible assets 2 268 164

Available-for-sale investments 3 3 075 2 469

Investment in associate companies 23 2 2

Defined benefit assets 9 445 481

Non-current loans and receivables 4 92 95

Current assets 2 255 2 780

Inventories 5 10 10

Defined benefit assets 9 6 64

Receivables and prepayments 6 341 299

Cash and cash equivalents 7 1 898 2 407

Total assets 8 878 8 191

EQUITY AND LIABILITIES

Total funds 7 428 6 774

Non-distributable reserves

Available-for-sale investment revaluation 352 472

Reserve funds

Restricted funds 4 238 3 870

Council designated funds 2 838 2 432

Non-controlling interest (6) 2

Non-current liabilities 374 285

Borrowings 8 18 15

Deferred income 12 311 237

Agency funds 24 45 33

Current liabilities 1 082 1 130

Trade payables, accruals and other liabilities 11 470 577

Deferred income 12 400 390

Student deposits 211 162

Provisions 10 1 1

Total funds and liabilities 8 878 8 191

2011 Financial Review 24

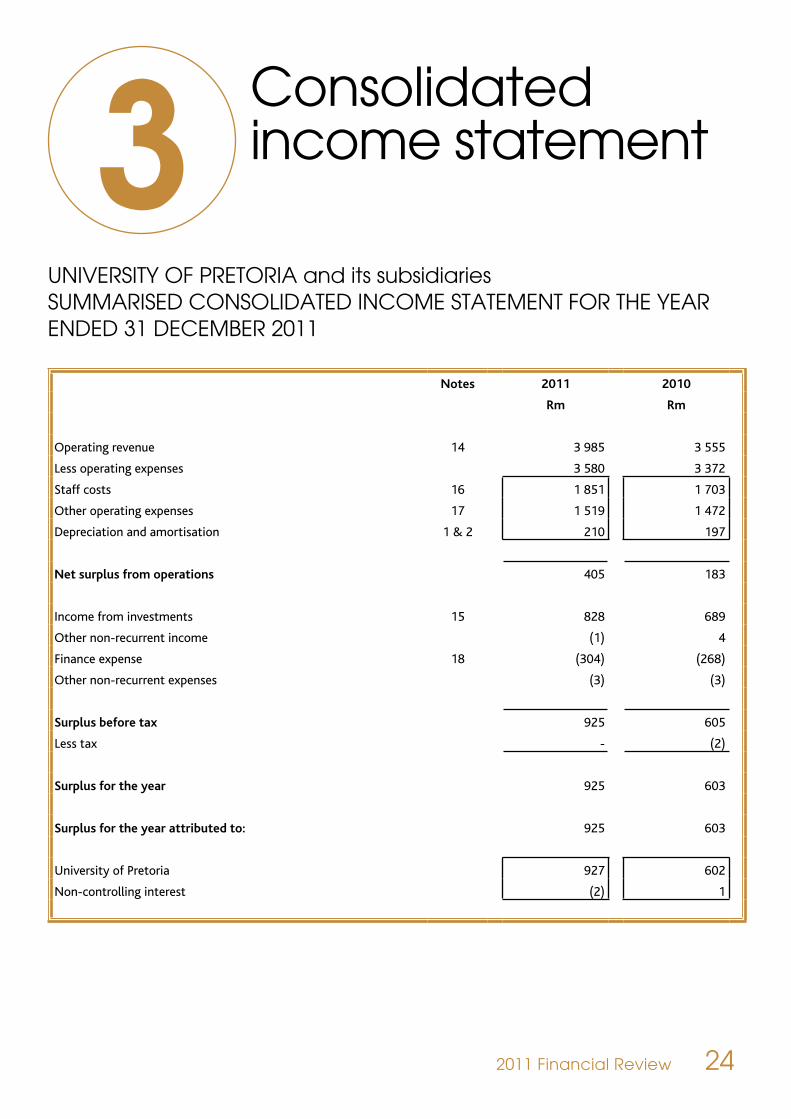

UNIVERSITY OF PRETORIA and its subsidiariesSUMMARISED CONSOLIDATED INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2011

Notes 2011 2010

Rm Rm

Operating revenue 14 3 985 3 555

Less operating expenses 3 580 3 372

Staff costs 16 1 851 1 703

Other operating expenses 17 1 519 1 472

Depreciation and amortisation 1 & 2 210 197

Net surplus from operations 405 183

Income from investments 15 828 689

Other non-recurrent income (1) 4

Finance expense 18 (304) (268)

Other non-recurrent expenses (3) (3)

Surplus before tax 925 605

Less tax - (2)

Surplus for the year 925 603

Surplus for the year attributed to: 925 603

University of Pretoria 927 602

Non-controlling interest (2) 1

3 Consolidated income statement

2011 Financial Review 25

UNIVERSITY OF PRETORIA and its subsidiariesSUMMARISED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2011

Notes 2011 2010

Rm Rm

Surplus for the year 925 603

Other comprehensive income for the year (273) 32

Actuarial gain/(loss) on defined benefit medical plan 9 (71) 23

Actuarial gain/(loss) on defined benefit pension plan 9 (60) (80)

Actuarial loss on defined benefit provident plan 9 (22) (58)

Fair value adjustment on available-for-sale investments 3 (120) 147

Total comprehensive income for the year 652 635

Total comprehensive income attributed to: 652 635

University of Pretoria 654 634

Non-controlling interest (2) 1

4 Consolidated statement of comprehensive income

2011 Financial Review 26

UNIVERSITY OF PRETORIA and its subsidiariesCONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2011

Unrestricted operating

fund

Council designated

and restricted funds – other

Council designated

and restricted property, plant and equipment

funds

Restricted student

accommodation fund

Total

Rm Rm Rm Rm Rm Balance at 31-12-2009: credit 72 3 053 2 998 17 6 140

Net (decrease)/increase in funds 53 271 300 10 634

Net income – surplus 226 264 51 61 602

Other comprehensive income - 32 - - 32

Net transfers (to)/from other funds (173) (25) 249 (51) -

Balance at 31-12-2010: credit 125 3 325 3 297 27 6 774

Non-distributable reserves - 472 - - 472

Council designated 125 1 938 369 - 2 432

Restricted – other - 915 2 928 27 3 870

Balance at 31-12-2010: credit 125 3 325 3 297 27 6 774

Net (decrease)/increase in funds (54) 225 510 (27) 654

Net income – surplus 288 550 57 32 927

Other comprehensive income - (273) - - (273)

Net transfers (to)/from other funds (342) (52) 453 (59) -

Balance at 31-12-2011: credit 71 3 550 3 807 - 7 428

Non-distributable reserves - 352 - - 352

Council designated 71 2 239 528 - 2 838

Restricted – other - 959 3 279 - 4 238

5 Consolidated statement of changes in equity

2011 Financial Review 27

UNIVERSITY OF PRETORIA and its subsidiariesCONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 2011

Note 2011 2010

Rm Rm

CASH FLOW FROM OPERATING ACTIVITIES 865 830

Cash generated from operations 21 668 605

Interest and dividend income 15 198 229

Taxation (paid)/received (1) (4)

CASH FLOW FROM INVESTING ACTIVITIES (1 377) (803)

Purchase of property, plant and equipment 1 (737) (675)

Purchase of intangible assets 2 (122) (63)

Increase in available-for-sale investments 3 (1 917) (2 703)

Proceeds on disposal of property, plant and equipment 1 2

Proceeds on disposal of investments 1 398 2 637

CASH FLOW FROM FINANCING ACTIVITIES 3 4

Increase in interest-bearing borrowings 3 4

INCREASE IN CASH AND CASH EQUIVALENTS FOR THE YEAR (509) 30

CASH AND CASH EQUIVALENTS AT THE BEGINNING OF YEAR 2 407 2 377

CASH AND CASH EQUIVALENTS AT THE END OF YEAR 7 1 898 2 407

6 Consolidated statement of cash flows

2011 Financial Review 28

7Notes to the consolidated financial statements

2011 Financial Review 29

UNIVERSITY OF PRETORIA and its subsidiaries NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2011

1. Property, plant and equipment

Land and Buildings

Furniture, equipment and

vehicles

Library books and journals

Computer equipment

Total

Rm Rm Rm Rm Rm

Year ended 31 December 2010

Opening net carrying amount 1 394 197 - 126 1 717

Additions 487 111 51 27 676

Disposals/write-offs - (3) - (3) (6)

Depreciation charge (37) (42) (51) (57) (187)

Closing net carrying amount 1 844 263 - 93 2 200

At 31 December 2010

Cost 2 113 712 525 426 3 776

Accumulated depreciation (269) (449) (525) (333) (1 576)

Net carrying amount 1 844 263 - 93 2 200

Year ended 31 December 2011

Opening net carrying amount 1 844 263 - 93 2 200

Additions 518 116 50 53 737