Embed Size (px)

Citation preview

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 1

Unit – 2. Consignment Accounts:

Introduction – Meaning – Consignor – Consignee – Goods Invoiced at Cost Price –

Goods Invoiced at Selling Price – Normal Loss – Abnormal Loss – Valuation of Stock –

Stock Reserve – Journal Entries – Ledger Accounts in the books of Consignor and

Consignee.

Introduction: Business enterprises, apart from marketing their goods directly, also market them

through agents. When organizations do not have a reach for all markets or do not have

sufficient knowledge about certain markets, they appoint agents who have better

knowledge of the local markets, for marketing their products. Such arrangement of

sending goods to agents for further sale by them in the pre-defined market is called

Consignment. The agent will be compensated with commission for marketing the

goods on behalf of his principal, i.e., business enterprise (manufacturer or wholesaler or

dealer).

Meaning of Consignment: Consignment is an agreement under which a manufacturer or a wholesaler sends

goods to his agent for the purpose of sale on his behalf and at his own risk on

commission basis. The person sending the goods on consignment to another person is

called consignor (Principal). The person to whom the goods are sent on consignment is

called the consignee (Agent). The consignee sells the goods on behalf of the consignor

and may be allowed to incur expenses for this purpose. The expenses and losses

incurred by the consignee for selling the consigned goods will be reimbursed by the

consignor unless otherwise agreed.

Thus, Consignment refers to sending of goods by a principal to his agent, who

sells the goods on behalf of the principal in return for a commission.

Features of Consignment: 1. Goods are forwarded by the consignor to the consignee with an objective of sale

at a profit.

2. The person sending the goods on consignment is called the consignor and the

person to whom the goods are sent on consignment is called the consignee.

3. Under the consignment, goods are to be treated as the property of the consignor

and to be sold at his risk. The consignee does not buy the goods, he merely

undertakes to sell them on behalf of the consignor. He is not responsible for any

loss or even for any destructions or damages to the goods. But the consignee

should not show any negligence.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 2

4. The consignor does not sell the goods to the consignee. Therefore, he cannot

ask the consignee to pay the price of the goods unless they are sold and the sale

proceeds are actually realized.

5. The consignee agrees to sell the goods for an agreed rate of commission and is

allowed to deduct his commission due from the sale proceeds.

6. The relationship between the consignor and the consignee is that of principal and

agent.

7. The consignee is generally allowed to incur expenses to sell the goods

consigned which will be reimbursed by the consignor.

8. Any stock remaining unsold with the consignee belongs to the consignor.

9. As the consignee acts on behalf of the consignor, the profit or loss on sale of

goods sent on consignment belongs to the consignor.

10. When the goods are sent by the consignor he prepares a Proforma Invoice and

sends it to the consignee.

11. Sometimes before sending the goods, the consignor may require the consignee

to remit some money as advance.

12. The consignee sends periodically to the consignor a statement called Account

Sales giving details of goods sold, expenses incurred by him etc.

Differences between Sale and Consignment:

Sale Consignment 1. Ownership of goods sold transfers

from seller to buyer. 1. Ownership of goods sent remains with

the consignor. 2. Goods once sold cannot be returned

back by the buyer. (unless defective or not as per specification)

2. Goods sent to consignee and remaining unsold with him can be returned back to the consignor.

3. The relationship between buyer and seller will be that of a creditor and debtor.

3. The relationship between consignor and consignee is that of a Principal and Agent

4. Any risk relating to goods has to be borne by the buyer.

4. Any risk relating to goods has to be borne by the consignor.

5. Expenses incurred by the buyer are to be borne by the buyer himself after the delivery of goods.

5. Expenses incurred by the consignee to receive the goods and to keep it safely are to be borne by the consignor.

6. Stock of goods with the buyer is his own stock.

6. Goods unsold with the consignee are treated as stock in the books of the consignor.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 3

Advantages of Consignment:

1. It enables a business enterprise to reach its goods to every place in the country

and even outside, without the organization having its presence there.

2. It is most economical form of business expansion since without opening

branches, the market for goods can be increased and maximized.

3. It enables the business enterprise to capture better market share and be a

dominant player in the industry.

Important terms in Consignment:

The following are some of the commonly used terms in consignment –

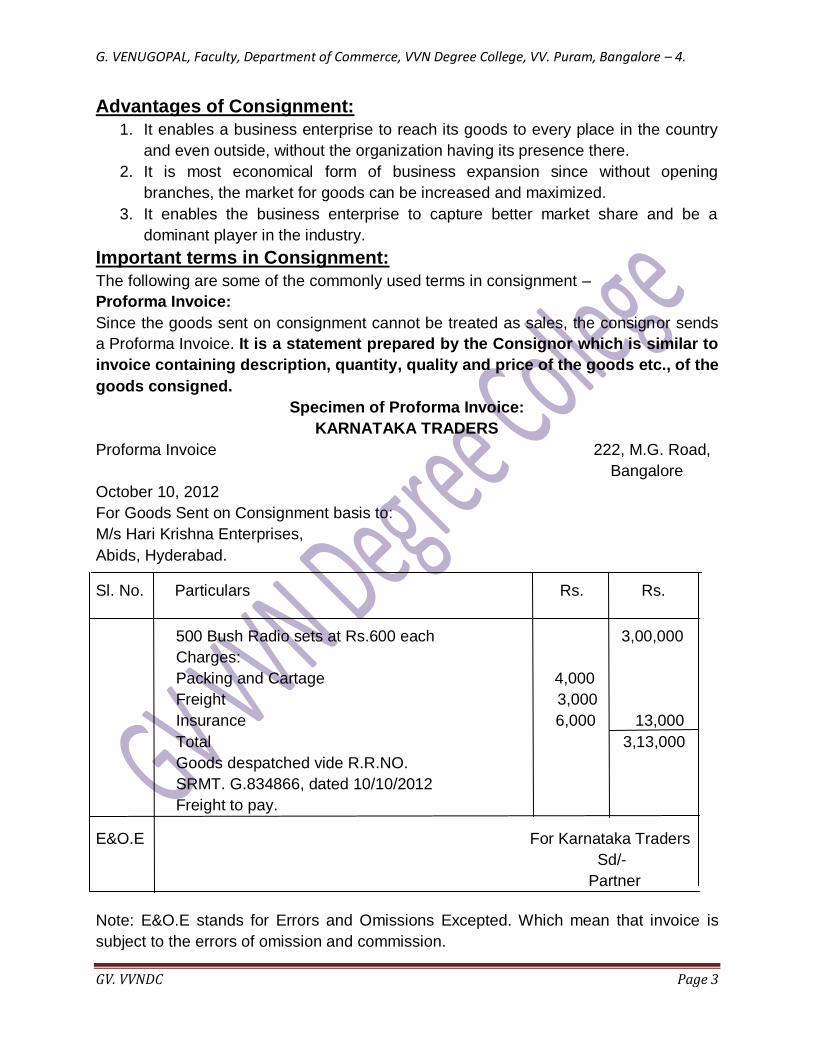

Proforma Invoice:

Since the goods sent on consignment cannot be treated as sales, the consignor sends

a Proforma Invoice. It is a statement prepared by the Consignor which is similar to

invoice containing description, quantity, quality and price of the goods etc., of the

goods consigned.

Specimen of Proforma Invoice:

KARNATAKA TRADERS

Proforma Invoice 222, M.G. Road,

Bangalore

October 10, 2012

For Goods Sent on Consignment basis to:

M/s Hari Krishna Enterprises,

Abids, Hyderabad.

Sl. No. Particulars Rs. Rs.

500 Bush Radio sets at Rs.600 each 3,00,000

Charges:

Packing and Cartage 4,000

Freight 3,000

Insurance 6,000 13,000

Total 3,13,000

Goods despatched vide R.R.NO.

SRMT. G.834866, dated 10/10/2012

Freight to pay.

E&O.E For Karnataka Traders

Sd/-

Partner

Note: E&O.E stands for Errors and Omissions Excepted. Which mean that invoice is

subject to the errors of omission and commission.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 4

Account Sales:

The consignee informs the consignor periodically about the volume and value of sales

affected and also the expenses incurred by him through a statement called ‘Account

Sales’. The account sales contains gross sale proceeds, the selling expenses

incurred by consignee and the commission payable to him and also the method

of settlement of balance due to the consignor.

Example:- On April 1, 2011, Alpha Radio Ltd., of Chennai consigned 200 radio sets to

Shanker Ltd., a radio dealer in Coimbatore. The cost of each set was Rs.250. On

receiving the consignment, Shanker Ltd., sent a bank draft for Rs.30,000 as an advance

to Alpha Radio Ltd. Shanker Ltd., paid Rs.500 as freight and Rs.1,000 for godown rent.

Shanker Ltd. submitted account sales on 1st June 2011, showing that all sets had been

sold at Rs.300 each. They were entitled to 5% commission on sales. Prepare Account

Sales.

Specimen of Account Sales:

Account Sales of 200 Radio sets received from and sold on account of

Alpha Radio Ltd., Chennai.

Particulars Amount Amount

Rs Rs

Sale Proceeds200 x 300 60,000

Less: Freight 500

Godown rent 1,000

Commission (5% on Rs.60,000) 3,000

----------------- 4,500

-----------------

55,500

Less: Advance (Bank Draft) 30,000

-----------------

Balance due (Bank Draft enclosed) 25,500

E&OE For Shanker Ltd.,

Dated Sd/-

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 5

Commission:

In consignment three types of commission are allowed to the consignee. They are

1. Commission on Sales or Ordinary Commission.

2. Del credere Commission.

3. Overriding Commission.

1. Commission on Sales or Ordinary Commission:

The consignee is entitled to remuneration by way of commission calculated at a

specified percentage on sales affected by him. This is known as Ordinary

Commission.

2. Del credere Commission:

The consignee may sell the goods either for cash or on credit. The consignee in

order to increase the commission may sell the goods on credit without any

responsibility for collection of debts. In order to check this tendency, the

consignor gives the consignee the Del credere commission. It is a commission

which is paid by the consignor to the consignee for taking additional risk of

recovery of debts due from customers to whom the goods have been sold

on credit.

3. Overriding Commission:

An extra commission over and above ordinary commission is given by the

consignor to the consignee for working hard to push a new line of product in the

market. Such commission is called Overriding Commission.

Expenses on Consignment:

Expenses relating to consignment of goods are divided into two categories. They are –

Non-recurring expenses and Recurring expenses.

1. Non-recurring Expenses:

All the expenses which are incurred for bringing goods to the godown of the

consignee are called non-recurring expenses. The consignor usually incurs

expenses on sending the goods to the consignee such as packing, carriage,

loading charges, freight, insurance etc. The consignee incurs expenses on

receiving the goods from the consignor such as dock dues, customs duty,

clearing charges, Carriage etc. These expenses are called as non-recurring

expenses.

2. Recurring Expenses:

These are incurred after the goods have reached the consignee’s place or

godown. The examples of recurring expenses incurred by the consignor are

advertising, travelling expenses of salesman, bank charges on bills discounted

etc. The examples of recurring expenses incurred by the consignee are godown

rent, insurance, salary, commission etc.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 6

Accounting Treatment:

A. It is necessary to ascertain the profit or loss made on each consignment

separately. Hence, a separate account for each consignment is opened.

B. For this purpose, the consignor prepares a consignment account to which all

expenses including the cost of goods consigned are debited and the sale

proceeds and the closing stock is credited. In addition, he also maintains

consignee’s account in order to calculate the amount due from him.

C. The consignee also maintains consignor’s account to which the amount remitted

to the consignor, expenses incurred by him and the commission due to him are

debited and the amount of sale proceeds is credited.

In the books of Consignor:-

The consignor prepares a consignment account relating to each consignment

separately. The following are the Journal entries to be passed in the books of the

Consignor When the goods are sent at Cost Price –

1. For Opening Stock with the Consignee:

Consignment a/c Dr

To Consignment Stock a/c

(Being the opening stock with the consignee)

2. For Goods dispatched to the Consignee:

Consignment a/c Dr

To Goods sent on Consignment a/c

(Being goods sent on consignment)

3. For Expenses incurred by the Consignor:

Consignment a/c Dr

To Cash/Bank a/c

(Being expenses incurred on consignment)

4. For Advance received from the Consignee:

Cash/Bank/Bills Receivable a/c Dr

To Consignee a/c

(Being the advance received)

5. For expenses incurred by the Consignee:

Consignment a/c Dr

To Consignee’s a/c

(Being the expenses incurred by the consignee)

6. For Sales affected by the Consignee:

Consignee’s a/c Dr

To Consignment a/c

(Being the gross sale proceeds as per account sales)

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 7

7. For Consignee’s Commission Payable:

Consignment a/c Dr

To Consignee’s a/c

(Being the commission payable on sale proceeds)

8. For Goods returned by the Consignee:

Goods sent on Consignment a/c Dr

To Consignment a/c

(Being goods returned by the consignee)

9. For Unsold Stock with the Consignee: *

Consignment Stock a/c Dr

To, Consignment a/c

(Being the value of closing stock on hand with the consignee)

10. For Profit or Loss on Consignment:

(i) If Profit:

Consignment a/c Dr

To Profit and Loss a/c

(Being profit on consignment transferred)

(ii) If Loss:

Profit and Loss a/c Dr

To Consignment a/c

(Being loss on consignment transferred)

11. For Settlement of Consignee’s Account:

Cash/Bank/Bills Receivable a/c Dr

To Consignee’s a/c

(Being the balance due from the consignee received)

12. For Closing Goods sent on Consignment Account:

Goods sent on Consignment a/c Dr

To Trading a/c / Purchases a/c

(Being the balance in goods sent on consignment a/c transferred)

*It is quite possible that all goods sent on consignment might not have been sold

by the consignee up to the date on which final accounts are prepared. It is

therefore, natural that stock on consignment should be properly valued and

credited to consignment account.

Unsold stock is valued at cost or market price whichever is less. While

calculating the cost of the stock, cost plus a proportionate share of non-

recurring expenses of consignor and consignee is considered. The stock on

consignment will be shown as an asset in the balance sheet of the consignor.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 8

Ledger Accounts:

The important Ledger Accounts to be prepared in the books of Consignor –

1. Consignment Account.

2. Consignee’s Account.

3. Goods sent on Consignment Account.

4. Consignment Stock Account.

Consignment Account:-

It is a nominal a/c prepared by the consignor to know the profit or loss on consignment.

The cost of goods consigned, expenses incurred by consignor and consignee,

commission due to the consignee are debited to this account. The sale proceeds, goods

returned by the consignee, closing stock with the consignee are credited to this account.

The difference between the debit and credit side totals of the consignment a/c is

transferred to the profit and loss a/c.

Proforma of Consignment Account:

Dr. Consignment Account Cr.

Date Particulars Amount Date Particulars Amount

Rs Rs

To Consignment Stock a/c xx By Goods sent on

To Goods sent on Consignment a/c xx

Consignment a/c xx (Returns)

To Bank a/c (Exp) xx By Consignee’s a/c xx

To Consignee’s a/c (Exp) xx (Sales)

To Consignee’s a/c xx By Consignment

(Commission) Stock a/c xx

To General P& L a/c --- By General P& L a/c ---

(Transferring profit) (Transferring loss)

------- -------

xx xx

------- ------

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 9

Consignee’s Account:-

It is a personal account prepared for ascertaining the amount due from the consignee.

Consignee’s account is debited with the total sales and credited with various expenses

incurred by the consignee, commission charged, advance remitted by him. This account

usually shows the debit balance indicating the amount due from the consignee.

Proforma of Consignee’s Account:

Dr Consignee’s A/c Cr

Date Particulars Amount Date Particulars Amount

Rs Rs

To balance b/d xx By Cash/Bank/BR a/c xx

To Consignment a/c xx By Consignment a/c xx

(Sales) (Expenses)

By Consignment a/c xx

(commission)

By Bank a/c xx

(final settlement)

-------- --------

xx xx

-------- --------

Goods sent on Consignment Account:-

It is a real account. The goods dispatched to the consignee will be credited to this

account and goods returned by the consignee are debited to this account. The balance

represents the cost of goods with the consignee for sale and is transferred to the

Trading account.

Proforma of Goods sent on Consignment Account:

Dr Goods sent on Consignment Account Cr

Date Particulars Amount Date Particulars Amount

Rs Rs

To Consignment a/c xx By, Consignment a/c xx

(Goods returned) (Goods consigned)

To Trading/Purchases a/c xx

(Balance transferred)

------- -------

xx xx ------- -------

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 10

In the Books of Consignee:-

The Consignee also prepares an account in the name of the consignor to find out what

is finally due to the consignor. The following journal entries are passed in the books of

consignee.

1. For Receipt of Goods by the Consignee: No entry

2. For Expenses incurred by the Consignee:

Consignor’s a/c Dr

To Cash/Bank a/c

(Being the expenses incurred)

3. For Advance payment to the Consignor:

Consignor’s a/c Dr

To Cash/Bank/Bills Payable a/c

(Being the advance payment)

4. For Sale of Goods by the Consignee:

Cash a/c / Bank a/c Dr (Cash Sales)

Debtor’s a/c Dr (Credit Sales)

To Consignor’s a/c

(Being goods sold on behalf of the consignor)

5. For Commission on Sales:

Consignor’s a/c Dr

To Commission a/c

(Being commission earned)

6. For Bad Debts incurred:

(i) If the consignee does not get Del credere commission, all the bad

debts have to be borne by the consignor himself. The entry is –

Consignor’s a/c Dr

To Debtor’s a/c

(Being bad debts debited to consignor’s a/c)

(ii) If the consignee gets Del credere commission, all the bad debts have

to be borne by the consignee. The entry will be –

Bad debts a/c Dr

To Debtor’s a/c

(Being bad debts incurred on consignment)

7. For Return of Goods to the Consignor: No entry

8. For Remittance made to the Consignor:

Consignor’s a/c Dr

To Cash/Bank/Bills Payable a/c

(Being consignor’s account settled)

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 11

Ledger Accounts in the books of Consignee:-

The Consignee prepares ‘Consignor’s Account’ which is a personal a/c and is

prepared for finding out the amount due to the Consignor. The amount received on sale

of goods is credited to this account. All expenses incurred by the consignee, in relation

to the consignment, the commission due to him, and the advance made to the

consignor will be debited to this account. The balance of this account indicates the

amount payable to the consignor.

Proforma of Consignor’s Account:

Dr Consignor’s Account Cr

Date Particulars Amount Date Particulars Amount

Rs Rs

To Cash/Bank a/c xx By Bank a/c xx

(Expenses) (Cash Sales)

To Bank/ Bills payable a/c xx By Debtors a/c xx

(Advance) (Credit Sales)

To Commission a/c xx

To Bank a/c xx

(Balance remitted)

----- ------

xx xx

------ ------

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 12

Problems on Consignment Accounts:

Problem – 1.

Mysore Sales Corporation of Mysore, invoices goods to its consignee Mr. Vishnu at

cost. On 1-4-06 it consigned Rs.2,00,000 worth of goods. They spent Rs.10,000

towards freight charges, Rs.5,000 towards insurance and other expenses. After

receiving the goods Mr. Vishnu spent Rs.12,000 towards rent, Rs.3,000 towards other

expenses. He was entitled to a commission of 10% on gross sale proceeds. He sold all

the goods for Rs.3,05,000. On 31-08-2006, he sent an Account sale with the above

details. He settled his account by a bank draft. Pass journal entries and prepare

consignment account.

Problem – 2.

Mr.Pandit sent on consignment to Mr.Purohit of Sringeri goods for Rs.1,50,000 on 1-5-

06. He incurred the following the expenses carriage Rs.6,000, insurance Rs.3,000,

sundries Rs.1,000. On 10-05-06 he received Rs.20,000 from Mr.Purohit. On 15-07-06

Purohit sends an Account sales showing that the goods were all sold for Rs.2,28,000.

He accepted a bill for the balance amount after deducting his expenses of Rs.10,000

towards rent, carriage and sundries and his commission at 12.5% on sales. Pass

journal entries and prepare consignment account.

Problem – 3.

Tarasu& Co. of Mandya sent on consignment to their agents Gundya& Co. Malavalli on

3-3-2010, 300 chairs costing Rs.200 each. The entire goods were sold on June 20,

2010 for Rs.90,000. The consignee, Gundya& Co. were entitled to receive a

commission of Rs.9,000. The amount due was settled by a Bank draft. Pass Journal

entries and show the consignment account in the books of Consignor.

Problem – 4.

M/s Jaipur & Co. of Delhi consigned on 15th March 2008, 45 cases of glassware (cost

price Rs.45,000) to Sinha & Co. of Agra for sale on commission @ 5% on gross sale

proceeds. The consignor paid freight and carriage amounting to Rs.500. The goods

were received at Agra on 20th March 2008, and Sinha & Co. paid clearing charges

Rs.300, Sundry charges Rs.50, Carriage Rs.150 and godown charges Rs.1,000. The

goods were sold by Sinha & Co. as under –

15 cases @ Rs.1,200 per case, 22 cases @ Rs.1,320 per case and the remainder for

Rs.10,000. On June 21, 2008 Sinha & Co. sent a draft for Rs.40,000 to M/s Jaipur &

Co. on account. On 1st July 2008, Sinha & Co. forwarded an Account Sale together with

a Bank draft for the balance.

Give Journal Entries and prepare the consignment account to record the

above transactions in the books of the Consignor.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 13

Problem – 5.

On 1st April, 2010 Mr. Amithab of Mumbai consigned to Mr. Vasco of Panaji 200 radio

sets at Rs.1,300 each. Mr. Amithab paid Rs.500 for insurance and Rs.1,000 for freight.

On 13th April Mr. Vasco received the consignment and had to pay Rs.300 as unloading

charges and Rs.150 as dock charges. On 4th October 2010, Mr. Vasco sent an account

sale to Mr. Amithab informing on 30th September 2010, that 180 sets were sold at

Rs.1,400 each and 20 sets at Rs.1,350 each. Mr. Vasco sent the balance by a demand

draft deducting his commission at 1% on sales.

Show necessary Journal Entries and relevant ledger accounts in the books of

Consignor.

Valuation of Closing Stock:

In Consignment accounts valuation of closing stock is one of the important aspect of

accounting as without proper valuation the profit or loss shown will be incomplete and

inaccurate.

The valuation of closing stock is done on similar lines as of ordinary stock i.e., it is

valued at cost or market price whichever is less.

It should be remembered that Cost price includes all those non recurring expenses

incurred by the consignor and the consignee. Expenses incurred after the goods are

brought to the godown are not to be considered.

*Cost of goods consigned + Non-recurring expenses

Closing Stock = -------------------------------------------------------------------- x Quantity of Closing Stock

*Quantity of goods consigned

Note:

1. * Cost of goods consigned means cost of goods consigned less cost of

goods returned by the consignee.

2. *Quantity of goods consigned means quantity of goods consigned less

quantity of goods returned by the consignee.

Problem – 6.

Mr.Rajkumar of Gajanur sent on consignment to Mr. NTR of Vizag costing Rs.44,250

and paid railway freight Rs.1,140, carriage Rs.350, insurance Rs.1,050. Half of the

goods were sold by NTR for Rs.26,250. He incurred storage expenses Rs.300 and

selling expenses Rs.525. He is entitled to a commission of Rs.1,310 and remitted the

balance by bank draft.

Pass journal entries and Prepare necessary ledger accounts in the books of

Mr.Rajkumar.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 14

Problem – 7.

Mr. Mahesh of Mandya consigned 100 boxes of CD’s to Arjun of Maddur. The cost of

each box was Rs.500. Mr. Mahesh paid insurance, freight charges of Rs.1,300. Mr.

Arjun sent an account sales for the sale of 80 boxes at Rs.650 per box after deducting

expenses of carriage Rs.200, establishment expenses Rs.130 and commission

Rs.2,400. He settled his account by accepting a bill for the balance amount.

Pass journal entries and Prepare necessary ledger accounts in the books of Mr.

Mahesh.

Problem – 8.

On 1-1-06 KMC consigned 180 cases of medicines at Rs.400 each to Vinayaka

medicals of Srinagar. KMC incurred Rs.1,800 towards carriage and Rs.3,600 towards

insurance and other charges.

The goods received on 6-1-06 and Rs.20,000 was advanced by bank draft to KMC.

Vinayaka medicals sent account sales with the following details.

Returns 20 cases.

Sales 150 cases at Rs.680 per case.

Clearing charges Rs.2,400 and carriage Rs.600.

Commission 10% of gross sales.

He accepted a bill for the balance amount.

Prepare necessary ledger accounts.

Accounting Treatment of Normal loss and Abnormal Loss:

Goods sent on consignment may be lost, damaged or destroyed either in transit or after

they reach the agent. Such loss may be a) Normal loss b) Abnormal loss.

1. Normal Loss:

When goods are lost or damaged due to normally expected but unavoidable causes

such as evaporation, leakage, breakage, dusting or weighment etc. Such loss is called

Normal Loss which is inherent and cannot be avoided and hence increases the cost of

goods.

Since normal loss forms a part of the cost, the cost of unsold goods increases

proportionately due to such loss. The formula to find out closing stock when there is

normal wastage –

Total cost of goods sent + Total non-recurring expenses ---------------------------------------------------------------------------- X Closing stock in units Total units of goods sent – Normal loss in units

2. Abnormal Loss:

Accidental loss or loss due to negligence is called abnormal loss. It is unexpected and

beyond the control of businessman. Loss of goods due to fire, flood, earthquake, theft

etc., is examples of abnormal loss.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 15

Abnormal loss should be transferred to general profit and loss account and it should not

affect any particular consignment. The following journal entries are to be passed to

record abnormal loss.

i. When loss is irrecoverable:-

a) For recording abnormal loss –

Abnormal loss a/c Dr

To Consignment a/c

(Being abnormal loss recorded)

b) For transferring abnormal loss to profit and loss account –

Profit and loss a/c Dr

To Abnormal loss a/c

(Being abnormal loss transferred)

ii. When the loss is fully recoverable from Insurance Company:-

a) For recording abnormal loss –

Abnormal loss a/c Dr

To Consignment a/c

(Being abnormal loss recorded)

b) For amount receivable from insurance company –

Insurance Co. a/c Dr

To Abnormal loss a/c

(Being amount receivable)

iii. When the loss is partly recoverable from Insurance Company:-

a) For recording abnormal loss –

Abnormal loss a/c Dr

To Consignment a/c

(Being abnormal loss recorded)

b) For amount partly recoverable from insurance company -

Insurance Co. a/c Dr

Profit and loss a/c Dr

To Abnormal loss a/c

(Being loss partly receivable and balance

transferred to Profit and loss a/c)

NOTE:

The valuation of abnormal loss is done in the same manner as that of valuation of

stock on consignment. Even if invoice price is given such loss should be valued

at cost plus proportionate non-recurring expenses.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 16

Problems on Normal Loss:

Problem – 9.

Mr. Nag consigned 2,000 kg of Gemini oil costing Rs.15,000. He paid freight and

insurance Rs.300 and Rs.200 respectively. Mr. Arjun the consignee received the

consignment and incurred Rs.300 towards unloading charges and carriage. He sold

1,800 kg of oil and reported the balance of stock at 150 kg. Find out the value of closing

stock.

Problem – 10.

Mr. Tarak sends 400 lb of Oil at Rs.2 per lb to his consignee at Bangalore. He spends

Rs.50 on cartage, insurance and freight. On the way due to leakage, 20 lb of Oil was

spoiled (normal loss). Consignee took delivery of the consignment and spent Rs.190 as

Octori, carriage and other non recurring expenses. He also paid Rs.200 as recurring

expenses. You are required to calculate stock at the end if the consignee sells away

300 lb of Oil.

Problem – 11.

Mr. Siva consigned 1,000 kg vegetables costing Rs.4,500. Expenses incurred were

Rs.600. If loss due to natural deterioration in quality is of 10 kg and 810 kg were sold,

calculate cost of stock at the end.

Problem – 12.

Mr. Robert of Delhi consigned 200 tons of coal at Rs.1,800 per ton to Mr. Rahim of

Galli. He paid Rs.15,000 as freight . Due to normal wastage 190 tons only were

received by Mr. Rahim. He paid Rs.5,000 as unloading charges. Goods sold were 130

tons. You are required to calculate the value of closing stock.

Problem – 13.

Mr. Ram consigned to Mr. Appu 1,000 kgs of Sunflower oil costing Rs.66,000. He spent

Rs.1,760 as forwarding charges. 12% of the consignment was lost in weighing and

handling. Mr. Appu sold 820 kgs of Sunflower oil at Rs.120 per kg and his selling

expenses were Rs.6,600 and commission at 5% on sales.

Prepare consignment account.

Problem – 14.

Sachin consigned 6,000 units of a product at Rs.150 per unit to Rahul of I. Nagar. He

paid Rs.60,000 as freight charges. 2.5% of the units sent were lost which was normal.

Rahul paid Rs.15,000 towards carriage and unloading charges. He sent account sales

informing that he had sold 4,200 units at Rs.340 per unit deducting his commission of

5% on sale proceeds. He accepted the bill for the amount due. Prepare Consignment

account.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 17

Problems on Abnormal Loss:

Problem – 15. (If abnormal loss is irrecoverable)

Bush Radio Co. sent on consignment 1,000 Radio sets to Singh and Co. of Delhi at a

cost price of Rs.320 each. Bush Co. paid freight charges of Rs.3,600.

While in transit 100 Radio sets have been totally damaged and became unsalable.

Nothing could be recovered from the Insurance Co. as the risk was not covered.

Singh and Co. took delivery of the remaining Radio sets and paid godown rent of

Rs.510, insurance of Rs.300. They sent an account sales showing that 600 Radio sets

were sold at Rs.420 each and the balance at Rs.400 each. Singh and Co. incurred

Rs.2,100 on sales promotion on behalf of Bush Radio Co. They were entitled to a

commission of 5% on sales.

Prepare consignment account.

Problem – 16. (If abnormal loss is fully recovered)

Tata ltd. sent on consignment 4,000 boxes of Assam Tea to MTR of Mavalli for

Rs.1,00,000. Out of these 200 boxes were totally destroyed by an accidental fire for

which the Insurance Co. agreed to pay the full amount. The expenses of consignment

before the loss are Rs.20,000 and after the loss are Rs.39,000 of which Rs.19,000 are

of non-recurring nature. The commission and selling expenses are Rs.60,000. An

account sale is received for 2,200 boxes showing gross sale proceeds of Rs.60 per box.

Show the consignment account.

Problem – 17. (If abnormal loss is partly recovered)

KMF Ltd., consigned 10,000 kgs of Ghee costing Rs.200 per kg to Balaji & Co. on 01-

01-05. KMF Ltd., paid Rs.5,00,000 as freight and insurance. 250 kgs of Ghee were

destroyed on 2-1-05 in transit. The insurance company claim was settled at Rs.45,000

and was paid directly to consignor’s.

Balaji & Co. took delivery of consignment on 10-01-05 and accepted a bill drawn upon

them by KMF Ltd., for Rs.10,00,000 for 3 months. On 31-3-05 Balaji & Co. reported as

follows –

i) 7,500 kgs were sold at Rs.400 per kg.

ii) Other expenses were –

Godown Rent Rs.20,000, Wages Rs.2,00,000, Printing and advertising

Rs.1,00,000

iii) 250 kgs were lost due to wastage in handling.

Balaji & Co. is entitled to a commission of 4% on the sales effected by them.

The consignee paid the amount due in respect of consignment on 31-03-05.

Show consignment account, consignee’s account and abnormal loss account.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 18

When goods are sent at Invoice Price:-

Many a time goods are consigned at a price higher than their cost price. The intention

behind the pricing the goods at higher price is to discourage the consignee from

resorting to dishonest practices. The real value of goods is not revealed to the agent so

that he should not be induced to buy the goods for himself and then make profit out of it.

Loading:

When goods are sent at invoice price which is higher than the cost price the difference

is known as Loading. Loading will have to be adjusted at the time of finding out the true

profit or loss made by the consignor on the consignment he sends. For this purpose,

along with other journal entries the following additional entries have to be passed.

a) For reserve on opening stock:

Stock reserve a/c Dr

To Consignment a/c

(Being load on opening stock adjusted)

b) For reserve on goods sent on consignment:

Goods sent on consignment a/c Dr

To Consignment a/c

(Being load on goods sent on consignment adjusted)

c) For reserve on goods returned by the consignee:

Consignment a/c Dr

To goods sent on consignment a/c

(Being load on goods returned by consignee adjusted)

d) For reserve on closing stock:

Consignment a/c Dr

To Stock reserve a/c

(Being load on closing stock adjusted)

Problem – 18.

Sri Krishna of Dwaraka consigned 100 articles to Sri Rama of Ayodhya. The cost of

each article was Rs.1,600 but the invoice price was Rs.2,000. Sri Krishna incurred

Rs.10,000 as freight and insurance. After receiving the articles Sri Rama sent a draft for

Rs.80,000 as advance. He incurred Rs.600 as rent and Rs.1,400 as selling expenses.

Sri Rama sent an account sales stating that he had sold 60 articles at a price of

Rs.2050 each for cash and 30 articles at Rs.2,300 on credit. He is entitled to an

ordinary commission of 4% on sales and 6% Del credere commission on credit sales.

Pass journal entries in the books of Sri Krishna.

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 19

Problem – 19.

Mr. Yeddy of Shimoga sent 150 machines on consignment to Mr. Reddy of Bellary. The

cost price of each machine was Rs.2,000 which was invoiced at 25% above the cost.

Mr. Yeddy spent Rs.6,000 towards freight. Mr. Reddy sold 100 machines at Rs.3,000

each for cash and 20 machines at Rs.3,200 each on credit. His selling expenses

amounted to Rs.3,000. He is entitled 6% selling commission and 2% del credere

commission. Pass journal entries and prepare necessary ledger accounts in the books

of Mr. Yeddy.

Problem – 20.

Hindustan Ltd. forwarded on 1st July, 2008, 100 bicycles to Bachan of Mumbai at an

invoice price of Rs.2,000, the cost of each bicycle being Rs.1,500. It paid Rs.10,000 for

freight and insurance. On receiving the consignment, Bachan accepted a draft for 3

months drawn by Hindustan Ltd for Rs.1,00,000. Bachan paid Rs.4,000 as rent and

Rs.2,500 as further expenses. By 31st December, 2008 Bachan has disposed of 80

bicycles at Rs.2,050 each. Bachan charged 6% as commission. Show the ledger

accounts in the books of Hindustan Ltd. Who closed the accounts on 31st December.

Problem – 21.

Manoj of Mysore sends a consignment of sewing machines to Rajesh of Raichur and

charges proforma invoice so as to show a profit of 25% on cost. The agent received

commission at 5% on all sales plus 3% del credere commission on credit sales made by

him. During the year ended 30th September, 2010, Manoj had the following transactions

with Rajesh.

a) Proforma invoice price of 200 sewing machines consigned to Rajesh Rs.50,000.

b) Freight and insurance on consignment paid by Manoj Rs.1,500

c) Advance received from Rajesh Rs.20,000.

d) Sales made by Rajesh:

i) 80 sewing machines for cash Rs.21,500.

ii) 100 sewing machines on credit Rs28,000.

e) Selling expenses met by the agent Rs.2,500.

f) Out of machines sold on credit, Rs.2,000 was irrecoverable and considered bad

by the agent.

g) The agent remitted the balance due by him by a bank draft.

Show the following ledger accounts to record the above transactions in the books of

Manoj. 1) Consignment A/c 2) Rajesh’s A/c and 3) Consignment stock A/c. and also

pass journal entries in the books of Rajesh and show the Consignor’s A/c.

Problem – 22.

On 1st January 2008, Rahul sends 30 LED’s costing Rs.30,000 each to Mr. Robert to be

sold on behalf of former at 5% commission on sales. Rahul paid Rs.3,000 as freight and

carriage for sending the LED’s. Mr. Robert sent the account sales on 31st March 2008

stating that:

G. VENUGOPAL, Faculty, Department of Commerce, VVN Degree College, VV. Puram, Bangalore – 4.

GV. VVNDC Page 20

1. 20 LED’s were sold for Rs.6,50,000

2. Expenses incurred on inward consignment were: Octroi Rs.500, Carriage

Rs.100, Godown rent Rs.4,200 and Advertisement and other selling expenses

Rs.3,000.

Prepare Consignment a/c, Consignee’s a/c and also calculate the value of consignment

stock on 31st March 2008. Pass journal entries in the books of Consignee and open

Consignor’s a/c.

Problem – 23.

Mr. Hero of Palghat sent 100 Hero cycles of Rs.1,200 each to Mr. Zero of Mangalore on

consignment basis. Mr. Hero paid freight Rs.5,000 and Rs.1,500 as insurance in transit.

Mr. Zero’s expenses at Mangalore to take the goods to his place were Rs.3,000. Mr.

Zero sold 80 Hero cycles at the rate of Rs.1,500 per cycle. Calculate the value of unsold

stock.

Problem – 24.

Mohini consigns to Kamini 160 cases of goods at a cost of Rs.500 per case and incurs

the following expenses: Carriage and freight Rs.1,200 and insurance Rs.2,800. On

arrival of the goods, Kamini spends unloading charges Rs.200, carriage Rs.200, Import

duties Rs.200, Octroi Rs.200. She also spends Rs.250 godown rent and Rs.150

godown keeper expenses. 120 cases were sold for Rs.90,000. She is entitled to a

commission of 10%. She sends Mohini an account sales and a bank draft for the

balance due. The market price at Kamini’s place falls to Rs.540 per case on the

accounting date.

Show the valuation of unsold stock and consignment account. Pass journal entries and

prepare consignor’s account in the books of consignee.

Problem – 25.

Mr. Manoj of Mandya consigned 300 bales of cloth at Rs.2,000 per bale to Mr. Narayan

of Nagapur paying freight Rs.4,000 and other expenses Rs.2,000. Mr. Narayan sold 250

bales at Rs.2,500 per bale on credit and 25 bales at Rs.2,200 per bale for cash. Mr.

Narayan spent for freight and octroi Rs.3,000 and other expenses Rs.1,000. Mr.

Narayan remitted the amount due to Mr. Manoj after deducting his commission at 5%

(normal), 2 ½% overriding and 1 ½% del credere commission is to be given on total

sales. Mr. Narayan found that one customer to whom credit of 40 days was allowed

paid only Rs.4,800 out of the total amount due from him of Rs.5,000 in full settlement of

account. Other customers paid the amount on due dates.

You are required to pass journal entries in the books of the consignor and consignee.

Also make ledger accounts in the books of both the parties.

![[PPT]Supplier Consignment Training - Supplier.intel.com · Web viewSM KM Consignment Model Supplier Consignment Training Agenda Overview of SM KM Consignment Model Current vs Consignment](https://img.pdfslide.us/doc/110x75/5b37de867f8b9a600a8cb065/pptsupplier-consignment-training-web-viewsm-km-consignment-model-supplier.jpg)