Embed Size (px)

Citation preview

UNDERWRITERS RATING BOARD

P.O. BOX 13-059 ALBANY, NEW YORK 12212

DWELLING PROGRAM BULLETIN # DWG-8 NOVEMBER 1, 1996

All rates, rules and forms promulgated by the Underwriters Rating Board are advisory in nature and their use is entirely dependent upon the specific decision of each Insurance Company. The manual changes are: Page Description of Change 1-18 Minor grammar changes have been made throughout including the removal of most ampersand

symbols and the substitution of the word and in their place. 1. Rule 1 has been changed to substitute the terms manufactured homes in place of the terms

mobile homes. 1. Item 1-b now refers to manufactured homes. 1. The list of endorsements was deleted. 2. The previous listing of perils was removed. 2. The mandatory forms list was augmented with references to FL-2B and 3B. Additionally, the

reference to URB-84 was linked to form FL-20, edition 11/79. 4. Item 3-f was reworded to improve readability. 6. Item 4-g, Upstate Cities, was added to the manual and items 4-h and 4-i were relettered. 8. Item 5-h(b) was reworded for improved readability. 9. Items 5-n through 5-p, Wind Deductibles, were added to the manual. 14. Added advisory rate structure for Upstate Cities. 18. Item 6-a refers to manufactured homes rather than mobile homes. 19-20. Items 5-n-1 through 5-p detail an advisory rate structure for the Coastal Properties Program.

Additional copies of this manual are available from the Underwriters Rating Board. UNDERWRITERS RATING BOARD James R. Lichtel, CPCU Manager

DWELLING PROGRAM 11/96

North Country Insurance Co. 7/05

DWELLING NCIC 11/96 7/05

INDEX

DESCRIPTION RULE NO. PAGES

Basic Policy Coverage and Limits 2 2 Eligibility 1 1 General Rules 3-a to 3-i 3-5 Mandatory Forms 2 2 Optional Coverages - Description 5-a to 5-p 7-8 Premium Section - Optional Coverages 4-c to 5-p 17 Premium Section - Special Premium 6-a to 6-b 17 Modifications Premium Tables --- 10-16 Rating 4 5 Rating-Descriptions of Classifications- 4-a to 4-i 5-6 Special Premium Modifications - 6-a to 6-b 9 Description

DWELLING NCIC 11/96 PAGE 1 5/05

DWELLING PROGRAM

Rule No. 1. ELIGIBILITY:

The Dwelling Manual contains rules, classifications and premiums for writing Fire & Allied Lines Insurance on Residences, Related Private Structures, Manufactured Homes and Personal Property in Residences and Apartments. Farm Residences are rated from this section of the manual. Refer to Farm Section for rating farm outbuildings.

1-a RESIDENCE - Shall mean a building occupied exclusively for dwelling purposes by not more than four families. Accommodations for up to 5 roomers or boarders are permitted: For one or two roomers or boarders - 1-2 family rates apply. For three to five roomers or boarders - 3-4 family rates apply.

1-b MANUFACTURED HOMES - Shall mean a portable unit, not self-propelled, constructed and used for residential purposes.

DWELLING NCIC 11/96 PAGE 2 5/08

2. BASIC POLICY COVERAGE AND LIMITS:

The basic policy provides coverage for the following: Coverage Description Limits A Residence Coverage included if shown on Declarations Page. * B Related Private Optional - 10% of Coverage A Structures C Personal Property Coverage included if shown on Declarations Page. * D Additional Living Optional - 10% of Coverage A Expense and Loss of Rent * 10% of the Coverage A Limit of Liability may be applied to Coverage B and D. Any payment under these options reduces the Coverage A Limit of Liability. MANDATORY FORMS - The following forms are mandatory for the Dwelling Program: Property Coverages - FL-20, (URB-84 with FL-20 (11/79)), PERILS SECTION (FL-1R, 2, 2B, 3 or 3B), FL-345 (may be removed at the insured’s request), NC FL-189 (may be removed at the insured’s request).

DWELLING NCIC 11/96 PAGE 3 5/05

3. GENERAL RULES:

3-a CANCELLATION -

If insurance is cancelled or reduced at the request of the company or the insured, the earned premium shall be computed on a pro-rata basis. NOTE: See Maximum and Minimum Charges for Annual Minimum Retained Premiums.

3-b INSURANCE BY MORE THAN ONE COMPANY - (FL-14) Coverage may be divided between two or more companies using the rates, rules, forms and endorsements of this manual.

3-c DEFERRED PREMIUM PAYMENT PLAN - It is permissible to write a policy for three years with the premium payable annually. If the premium is paid annually, the installment premium shall be determined as follows: The installment premium shall be the annual premium as shown in this manual.

3-d INTERPOLATION -

To determine the premium for an amount of insurance between two amounts shown in the premium table, add the pro-rata premium for the difference between the nearest amounts shown to the premium for the lower amount.

DWELLING NCIC 11/96 PAGE 4 5/05

3-e MAXIMUM AND MINIMUM CHARGES - ANNUAL No additional premium shall be charged and no return premium shall be allowed when such additional or return premium is less than $3.00. Annual Minimum Premium - $50.00 Annual Minimum Retained Premium - $20.00

3-f RATE REVISIONS After the Underwriters Rating Board announces a rate revision, each individual company choosing to adopt the revision, shall determine the effective date(s) for new and renewal policies.

3-g RESTRICTION OF INDIVIDUAL POLICIES - If a policy would not be issued because of unusual exposures, the applicant may request a restriction of the policy at no reduction in premium. The request, bearing the signature of the applicant, shall be referred to the Company.

3-h TERM INSURANCE - The fire policy may be written for a term up to three years. All premiums contained in this section are on an annual basis. Term factors are listed below: Term of Policy Term Factor 1 year 1.0 2 years 2.0 3 years 3.0

DWELLING NCIC 11/96 PAGE 5 5/05

3-i WHOLE DOLLAR PREMIUM - The premium for each exposure shall be rounded to the nearest whole dollar, separately for each coverage provided by the policy. A premium involving 50 cents or over shall be rounded to the next higher whole dollar.

4. RATING: All Premiums in this Manual are ANNUAL per $1,000. of Insurance. 1. Classify dwelling and/or contents by Construction and Protection. 2. Consult Rate Tables to obtain appropriate Annual Premium for Replacement Cost

or Actual Cash Value and the number of families. (see interpolation rule if premium for amount of insurance is not shown).

3. Add any special condition charges that apply. 4. Add premiums for optional coverages. 5. Apply deductible credits. 6. Add any other premiums that are written with the policy.

RATING - DESCRIPTION OF CLASSIFICATIONS: CONSTRUCTION -

4-a FRAME -

Shall mean a building with total exterior wall area of more than 33 1/3% Frame, Metal-sheathed or Stucco.

4-b MASONRY - Shall mean a building with more than 66 2/3% of the exterior wall area of Masonry or Masonry veneered construction.

4-c FIRE RESISTIVE - Shall mean a building with walls, floors and roof of masonry construction. Premiums are shown in the Premium Section of the manual.

DWELLING NCIC 11/96 PAGE 6 5/05

PROTECTION - 4-d PROTECTED -

Building is located within 1,000 feet of an approved fire hydrant and is within 5 road miles of a responding fire department.

4-e SEMI - PROTECTED Building is located more than 1,000 feet from an approved fire hydrant, but is within 5 road miles of a responding fire department.

4-f UNPROTECTED All Others.

4-g UPSTATE CITIES The cities listed below: Albany City Rochester City Binghamton City Schenectady City Buffalo City Syracuse City New Rochelle City Troy City Niagara Falls City Utica City Mount Vernon City Yonkers City

RESIDENCE REPLACEMENT COST / ACTUAL CASH VALUE PROVISIONS - 4-h REPLACEMENT COST -

The replacement cost value shall be determined by using the Replacement Cost Estimator. Replacement Cost premiums are to be used when the residence is insured for at least 80% of the Replacement Cost. Losses will be settled according to the provisions of the Replacement Cost Provision.

4-i ACTUAL CASH VALUE - The Actual Cash Value premiums are to be used when the residence is insured for less than 80% of the replacement cost. Losses will be settled on an actual cash value basis including deduction for depreciation.

DWELLING NCIC 11/96 PAGE 7 5/05

5. OPTIONAL COVERAGES:

5-a ADDITIONAL LIVING EXPENSE - Additional Living Expense in excess of the 10% included in the Agreement is available. Enter the total limit of insurance to be applied as Additional Living Expense on the Declarations Page. Premiums for the increased amount shall be the premiums shown "for each additional $1,000 add" at the bottom of the premium tables.

5-c BUILDINGS UNDER CONSTRUCTION - If a residence is insured from the start of construction until completion, the premium shall be 55% of the premium for the completed residence. Policy shall be written for 1 year only. Indicate "Builders Risk-Completed Value" on the Declarations Page. If a residence is not insured from the start of construction, the premium shall be the appropriate premium as shown. Indicate "Building Under Construction" on the Declarations Page.

5-d COVERAGES - OTHER PROGRAMS - It is permissible to attach any filed form offering supplemental coverage not included in this section. The appropriate rates are to be used.

5-e DEDUCTIBLES - Form used in conjunction with the premiums shown in this manual contemplate a $100 All Perils Loss Deductible Clause applying per occurrence. This deductible amount can be increased by entering the appropriate deductible amount on the Declarations Page and applying the appropriate deductible credit as shown in the Premium Section of the manual.

5-f EARTHQUAKE - (FL-12) Earthquake premiums are shown in the Premium Section of the manual.

DWELLING NCIC 11/96 PAGE 8 7/05

5-g EXTENDED COVERAGE -

Extended coverage perils may be included by charging premiums determined from the extended coverage premium tables. (Also see Miscellaneous Properties).

5-h IDENTITY FRAUD ENDORSEMENT – (NC FL-189)

Coverage will be added to all policies at the premium shown in the Premium Section of the manual. Coverage will be removed at the request of the insured.

5-j LOSS OF RENT -

Loss of Rent in excess of the 10% included in the Agreement is available. Enter the total limit of insurance to be applied as Loss of Rent on the Declarations Page. Premiums for the increased amount shall be the premiums shown "for each additional $1,000 Add" at the bottom of the premium tables.

5-k MECHANICAL, ELECTRICAL OR PRESSURE SYSTEMS BREAKDOWN – (FL-345)

Coverage for mechanical, electrical or pressure systems breakdown will be added to all policies at the premium shown in the Premium Section of the manual. Coverage can be removed at the request of the insured.

5-m RELATED PRIVATE STRUCTURES -

Related Private Structures may be insured as a separate item for a specific amount. The premium shall be 60% of the premium applicable.

5-n REPLACEMENT VALUE – PERSONAL PROPERTY – (NCFL-55) Personal property may be insured for replacement value at the charges shown in the Premium Section of the manual.

5-o TENANTS IMPROVEMENT AND BETTERMENTS - Coverage in excess of the 10% available in the Agreement for Tenants improvements & betterments may be provided. The premium is determined by using the appropriate contents rate, "for each additional $1,000. add" shown at the bottom of the premium tables.

5-p VANDALISM - Coverage may be included by charging premiums determined from the vandalism premium table. Vandalism premiums for miscellaneous properties are shown in the Premium Section of the manual. Vandalism premiums shall be charged in addition to Broad Form and Special Form additional premium.

DWELLING NCIC 11/96 PAGE 9 5/05

6. SPECIAL PREMIUM MODIFICATIONS:

6-a SPECIAL CONDITION CHARGES - Manufactured Homes - not on continuous masonry foundation - applicable additional premiums are shown in the Premium Section of the manual.

6-b HAZARDOUS CONDITIONS - Conflagration or substandard charges may be applied to residence and personal property where conditions exist as shown in the Premium Section of the manual.

7. AUTOMATIC COVERAGE ENDORSEMENTS:

7-a REFRIGERATED FOOD PRODUCTS – (ML-155 & NC-155) $500 Coverage Automatically Provided on policies with Farmers Comprehensive Personal Liability coverage. This policy is extended to provide coverage from loss or damage to food products contained in a freezer or refrigeration unit. No additional premium is charged for this coverage. No higher limits are available.

DWELLING NCIC 11/96 PAGE 10 5/05

FIRE PREMIUMS MASONRY OR FRAME TABLE NO. 1 PROTECTED DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV

1,000 22 32 4 27 36 5 13 2,000 25 36 6 31 41 7 17 3,000 28 39 8 33 44 9 22 4,000 31 43 10 37 49 11 27 5,000 34 47 11 40 54 13 32 6,000 36 50 13 43 58 15 37 7,000 39 54 15 47 62 17 41 8,000 41 58 17 49 66 19 47 9,000 44 62 19 53 71 21 51 10,000 47 66 21 56 75 23 56 11,000 49 69 22 59 79 24 61 12,000 52 73 24 63 84 26 65 13,000 55 77 26 66 88 28 70 14,000 57 80 27 69 92 30 74 15,000 60 84 29 72 97 32 79 16,000 62 88 31 75 100 34 84 17,000 65 92 32 79 105 36 89 18,000 68 96 34 82 110 38 93 19,000 71 99 36 85 113 39 98 20,000 74 103 38 88 118 41 102 25,000 83 117 46 100 133 51 126 30,000 93 130 55 111 149 61 150 35,000 102 144 64 123 164 70 174 40,000 112 157 73 134 179 80 197 45,000 122 170 82 146 195 90 221 50,000 131 184 90 158 210 100 245 55,000 146 205 101 175 234 111 272 60,000 161 225 110 193 258 121 299 65,000 176 246 120 211 281 133 326 70,000 190 267 131 229 305 144 353 75,000 205 288 141 246 329 155 381 80,000 220 308 150 264 352 166 407 85,000 235 329 161 282 376 177 434 90,000 250 350 171 300 400 188 462 95,000 264 370 181 317 423 199 488 100,000 279 391 191 335 447 210 515 FOR EACH ADDITIONAL $1,000 ADD 2 4 2 3 4 2 5

DWELLING NCIC 11/96 PAGE 11 5/05

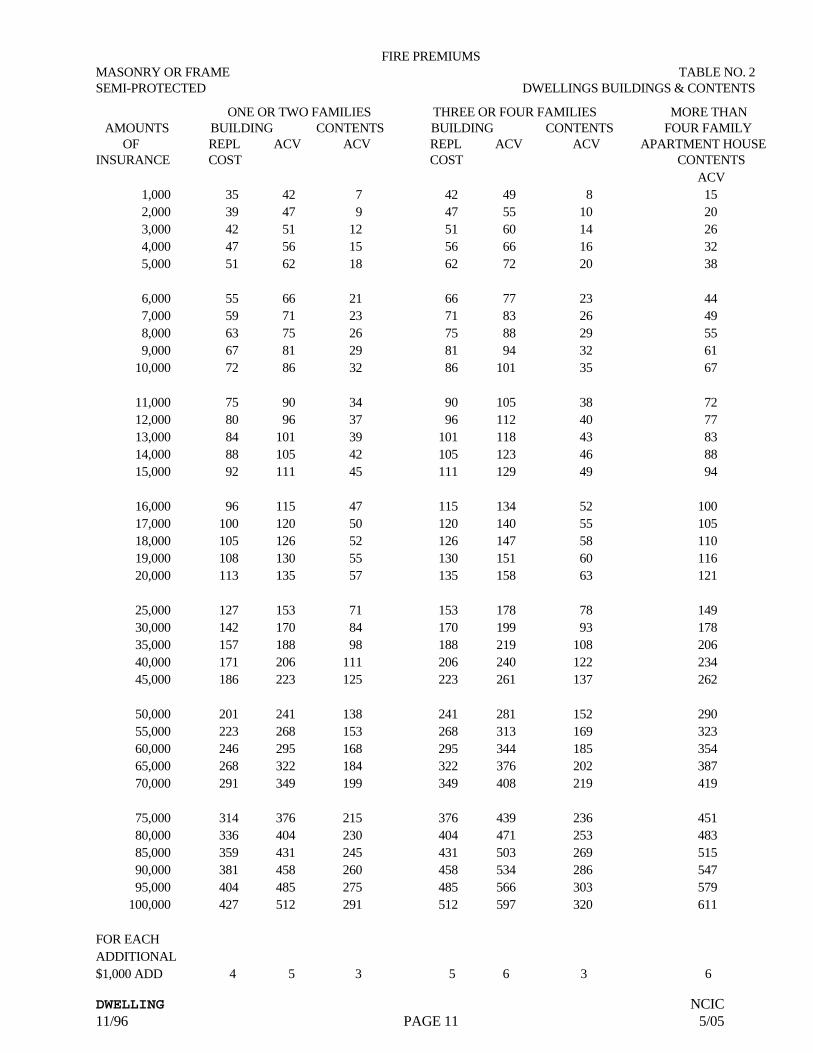

FIRE PREMIUMS MASONRY OR FRAME TABLE NO. 2 SEMI-PROTECTED DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV

1,000 35 42 7 42 49 8 15 2,000 39 47 9 47 55 10 20 3,000 42 51 12 51 60 14 26 4,000 47 56 15 56 66 16 32 5,000 51 62 18 62 72 20 38 6,000 55 66 21 66 77 23 44 7,000 59 71 23 71 83 26 49 8,000 63 75 26 75 88 29 55 9,000 67 81 29 81 94 32 61 10,000 72 86 32 86 101 35 67 11,000 75 90 34 90 105 38 72 12,000 80 96 37 96 112 40 77 13,000 84 101 39 101 118 43 83 14,000 88 105 42 105 123 46 88 15,000 92 111 45 111 129 49 94 16,000 96 115 47 115 134 52 100 17,000 100 120 50 120 140 55 105 18,000 105 126 52 126 147 58 110 19,000 108 130 55 130 151 60 116 20,000 113 135 57 135 158 63 121 25,000 127 153 71 153 178 78 149 30,000 142 170 84 170 199 93 178 35,000 157 188 98 188 219 108 206 40,000 171 206 111 206 240 122 234 45,000 186 223 125 223 261 137 262 50,000 201 241 138 241 281 152 290 55,000 223 268 153 268 313 169 323 60,000 246 295 168 295 344 185 354 65,000 268 322 184 322 376 202 387 70,000 291 349 199 349 408 219 419 75,000 314 376 215 376 439 236 451 80,000 336 404 230 404 471 253 483 85,000 359 431 245 431 503 269 515 90,000 381 458 260 458 534 286 547 95,000 404 485 275 485 566 303 579 100,000 427 512 291 512 597 320 611

FOR EACH ADDITIONAL $1,000 ADD 4 5 3 5 6 3 6

DWELLING NCIC 11/96 PAGE 12 5/05

FIRE PREMIUMS MASONRY OR FRAME TABLE NO. 3 UNPROTECTED DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV

1,000 44 52 11 52 61 12 18 2,000 49 59 14 59 69 16 24 3,000 53 64 19 64 75 21 31 4,000 59 71 23 71 83 25 38 5,000 65 78 27 78 91 30 45 6,000 69 83 31 83 97 34 52 7,000 75 90 35 90 105 39 58 8,000 79 95 39 95 111 43 65 9,000 85 102 43 102 119 48 72 10,000 90 109 48 109 127 52 79 11,000 95 114 51 114 133 57 85 12,000 100 120 55 120 141 61 91 13,000 106 127 59 127 149 65 98 14,000 110 132 63 132 155 69 104 15,000 116 139 67 139 163 74 111 16,000 120 144 71 144 168 78 118 17,000 126 151 75 151 176 82 124 18,000 132 158 79 158 184 87 130 19,000 136 163 83 163 190 91 137 20,000 142 170 86 170 198 95 143 25,000 160 192 107 192 224 117 176 30,000 178 214 127 214 250 139 209 35,000 197 236 147 236 276 162 243 40,000 215 259 167 259 302 184 276 45,000 234 281 187 281 328 206 309 50,000 252 303 207 303 353 228 342 55,000 281 337 230 337 393 253 380 60,000 309 371 253 371 433 278 418 65,000 337 405 276 405 473 304 456 70,000 366 439 299 439 512 329 494 75,000 394 473 322 473 552 354 532 80,000 423 507 345 507 592 379 569 85,000 451 541 368 541 632 404 607 90,000 479 575 391 575 671 430 645 95,000 508 610 413 610 711 455 682 100,000 536 644 436 644 751 480 720

FOR EACH ADDITIONAL $1,000 ADD 5 6 4 6 7 5 7

DWELLING NCIC 11/96 PAGE 13 5/05

FIRE PREMIUMS MASONRY OR FRAME TABLE NO. 4 UPSTATE CITIES DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV 1,000 25 35 5 30 40 5 14 2,000 28 39 7 34 45 7 19 3,000 30 43 9 37 49 10 24 4,000 34 47 11 41 54 12 29 5,000 37 52 13 44 59 14 35 6,000 39 55 15 47 63 16 40 7,000 43 60 17 51 69 18 45 8,000 45 63 19 54 72 20 51 9,000 48 68 20 58 78 23 56 10,000 52 72 23 62 83 25 62 11,000 54 76 24 65 87 27 67 12,000 57 80 26 69 92 29 72 13,000 61 85 28 73 97 31 77 14,000 63 88 30 76 101 33 81 15,000 66 93 32 80 106 35 87 16,000 69 96 34 83 110 37 92 17,000 72 101 36 86 115 39 97 18,000 75 105 37 90 121 41 102 19,000 78 109 39 93 125 43 107 20,000 81 113 41 97 130 45 112 25,000 91 128 51 110 147 56 138 30,000 102 143 60 123 164 67 164 35,000 113 158 70 135 181 77 190 40,000 123 173 80 148 197 88 216 45,000 134 188 89 161 214 98 242 50,000 144 202 99 173 231 109 268 55,000 161 225 110 193 257 121 298 60,000 177 248 121 212 283 133 327 65,000 193 271 132 232 309 145 357 70,000 210 294 143 252 336 157 387 75,000 226 316 154 271 362 170 417 80,000 242 339 165 291 388 181 446 85,000 258 362 176 310 414 194 476 90,000 275 385 187 330 440 206 506 95,000 291 407 198 349 466 218 535 100,000 307 430 209 369 492 230 565 FOR EACH ADDITIONAL $1,000 ADD 3 4 2 3 5 2 6

DWELLING NCIC 11/96 PAGE 14 5/05

FIRE PREMIUMS MASONRY TABLE NO. 5 NEW YORK CITY DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV 1,000 8 12 1 10 13 2 3 2,000 9 13 2 11 15 2 4 3,000 10 14 3 12 17 3 6 4,000 11 16 3 14 18 4 7 5,000 12 18 4 15 20 5 8 6,000 13 19 5 16 21 5 10 7,000 14 20 5 17 23 6 11 8,000 15 21 6 18 25 7 12 9,000 16 23 7 20 26 8 13 10,000 17 25 8 21 28 8 15 11,000 18 26 8 22 30 9 16 12,000 19 27 9 23 31 10 17 13,000 21 29 9 25 33 10 18 14,000 21 30 10 26 34 11 20 15,000 22 32 11 27 36 12 21 16,000 23 33 11 28 38 13 22 17,000 24 34 12 29 39 13 23 18,000 26 36 13 31 41 14 25 19,000 26 37 13 32 43 15 26 20,000 28 39 14 33 44 15 27 25,000 31 44 17 37 50 19 33 30,000 35 49 21 42 56 23 40 35,000 38 54 24 46 62 27 46 40,000 42 59 27 51 68 30 53 45,000 46 64 31 55 73 34 59 50,000 49 69 34 59 79 38 65 55,000 55 77 38 66 88 42 73 60,000 61 85 42 73 97 46 80 65,000 66 93 46 79 106 50 87 70,000 72 101 49 86 115 54 94 75,000 77 108 53 93 124 59 102 80,000 83 116 57 100 133 63 109 85,000 89 124 61 106 142 67 116 90,000 94 132 65 113 151 71 123 95,000 100 140 68 120 160 75 131 100,000 105 148 72 127 169 80 138 FOR EACH ADDITIONAL $1,000 ADD 1 1 1 1 1 1 2

DWELLING NCIC 11/96 PAGE 15 5/05

FIRE PREMIUMS FRAME TABLE NO. 6 NEW YORK CITY DWELLINGS BUILDINGS & CONTENTS

ONE OR TWO FAMILIES THREE OR FOUR FAMILIES MORE THAN AMOUNTS BUILDING CONTENTS BUILDING CONTENTS FOUR FAMILY

OF REPL ACV ACV REPL ACV ACV APARTMENT HOUSE INSURANCE COST COST CONTENTS ACV

1,000 22 30 5 26 35 5 3 2,000 24 34 7 29 39 7 4 3,000 26 37 9 32 43 10 6 4,000 29 41 11 35 47 12 7 5,000 32 45 13 39 52 14 9 6,000 34 48 15 41 55 16 10 7,000 37 52 17 45 60 18 11 8,000 39 55 19 47 63 20 13 9,000 42 59 20 51 68 23 14 10,000 45 63 23 54 72 25 16 11,000 47 66 24 57 76 27 17 12,000 50 70 26 60 80 29 18 13,000 53 74 28 63 85 31 19 14,000 55 77 30 66 88 33 21 15,000 58 81 32 69 93 35 22 16,000 60 84 34 72 96 37 23 17,000 63 88 36 75 101 39 25 18,000 66 92 37 79 105 41 26 19,000 68 95 39 81 109 43 27 20,000 71 99 41 85 113 45 29 25,000 80 112 51 96 128 56 35 30,000 89 125 60 107 143 67 42 35,000 98 138 70 118 157 77 49 40,000 107 151 80 129 172 88 56 45,000 117 164 89 140 187 98 62 50,000 126 176 99 151 202 109 69 55,000 140 196 110 168 224 121 77 60,000 154 216 121 185 247 133 85 65,000 168 236 132 202 270 145 92 70,000 183 256 143 219 293 157 100

75,000 197 276 154 236 315 170 108 80,000 211 296 165 253 338 181 115 85,000 225 316 176 270 361 194 123 90,000 239 335 187 287 383 206 131 95,000 254 355 198 305 406 218 138 100,000 268 375 209 322 429 230 146

FOR EACH ADDITIONAL $1,000 ADD 2 3 2 3 4 2 1

DWELLING NCIC 11/96 PAGE 16 5/05

PREMIUMS FOR E.C., VANDALISM, BROAD FORM & SPECIAL FORM MASONRY OR FRAME CONSTRUCTION ALL PROTECTION CLASSES

VAND + VAND + EXTENDED COVERAGE VANDALISM BROAD SPECIAL AMOUNT TABLE NO. 6 TABLE NO. 7 FORM FORM OF REPL TABLE TABLE

INSURANCE BUILDING CONTENTS COST ACV NO. 8 NO. 9 1,000 2.30 1.10 0.10 0.30 0.60 0.90 2,000 2.70 1.20 0.20 0.60 1.20 1.80 3,000 3.10 1.20 0.30 0.90 1.80 2.70 4,000 3.50 1.30 0.40 1.20 2.40 3.60 5,000 3.90 1.40 0.50 1.50 3.00 4.50 6,000 4.30 1.50 0.60 1.80 3.60 5.40 7,000 4.40 1.60 0.70 2.10 4.20 6.30 8,000 4.70 1.70 0.80 2.40 4.80 7.20 9,000 5.00 1.90 0.90 2.70 5.40 8.10 10,000 5.40 2.00 1.00 3.00 6.00 9.00 11,000 6.20 2.10 1.10 3.30 6.60 9.90 12,000 6.60 2.20 1.20 3.60 7.20 10.80 13,000 7.00 2.30 1.30 3.90 7.80 11.70 14,000 7.30 2.40 1.40 4.20 8.40 12.60 15,000 7.70 2.90 1.50 4.50 9.00 13.50 16,000 8.50 3.00 1.60 4.80 9.60 14.40 17,000 8.90 3.10 1.70 5.10 10.20 15.30 18,000 9.30 3.20 1.80 5.40 10.80 16.20 19,000 9.70 3.20 1.90 5.70 11.40 17.10 20,000 10.00 3.30 2.00 6.00 12.00 18.00

25,000 11.60 3.80 2.50 7.50 15.00 22.50 30,000 13.80 4.80 3.00 9.00 18.00 27.00 35,000 16.10 5.20 3.50 10.50 21.00 31.50 40,000 17.70 5.70 4.00 12.00 24.00 36.00 45,000 19.20 6.20 4.50 13.50 27.00 40.50

50,000 21.50 6.70 5.00 15.00 30.00 45.00 55,000 25.40 11.40 5.50 16.50 33.00 49.50 60,000 29.20 16.20 6.00 18.00 36.00 54.00 65,000 33.10 21.00 6.50 19.50 39.00 58.50 70,000 36.90 25.70 7.00 21.00 42.00 63.00

75,000 40.80 30.50 7.50 22.50 45.00 67.50 80,000 44.60 35.20 8.00 24.00 48.00 72.00 85,000 48.50 40.00 8.50 25.50 51.00 76.50 90,000 52.30 44.80 9.00 27.00 54.00 81.00 95,000 56.20 49.50 9.50 28.50 57.00 85.50 100,000 60.00 54.30 10.00 30.00 60.00 90.00

FOR EACH ADDITIONAL $1,000 ADD 1.00 1.00 0.10 0.30 0.60 0.90

DWELLING NCIC 11/96 PAGE 17 5/08

PREMIUM SECTION OPTIONAL COVERAGES

ANNUAL PREMIUMS Rule No. 4-c FIRE RESISTIVE - RESIDENCE -

Multiply Masonry Fire and EC Premiums by .50

5-e DEDUCTIBLES - Amount of Deductible Fire EC & Other Perils $ 100. --- --- 250. 8% 25% 500. 12% 30% 1,000. 16% 40% 2,500. 25% 55%

5-f EARTHQUAKE - (FL-12) Frame (excluding masonry veneer) .27 All other .41

5-h IDENTITY FRAUD ENDORSEMENT – (NC fl-189) $10 per policy 5-k MECHANICAL, ELECTRICAL OR PRESSURE SYSTEMS BREAKDOWN – (FL-345) $15 per policy 5-n REPLACEMENT VALUE- PERSONAL PROPERTY – (NCFL-55)

Charge an additional 20% of the contents premium. Minimum additional charge – 420.

5-p VANDALISM - Miscellaneous Properties - Rates per $1,000 Replacement Actual Cash Cost Value Seasonal - Unoccupied .60 1.00

6-a SPECIAL CONDITION CHARGES - Manufactured Home - not on continuous masonry foundation - Add $3.00 per $1,000 of insurance to the Fire Premium (bldg. & cnts.). Extended Coverage premium per $1,000 of insurance is: Actual Cash Value - $1.50

6-b HAZARDOUS CONDITIONS - Charge No. % of Increase Unoccupancy A 25% Vacancy B 50% Tenant Occupied C 15%

Burglary 12/96 Page 1 7/02

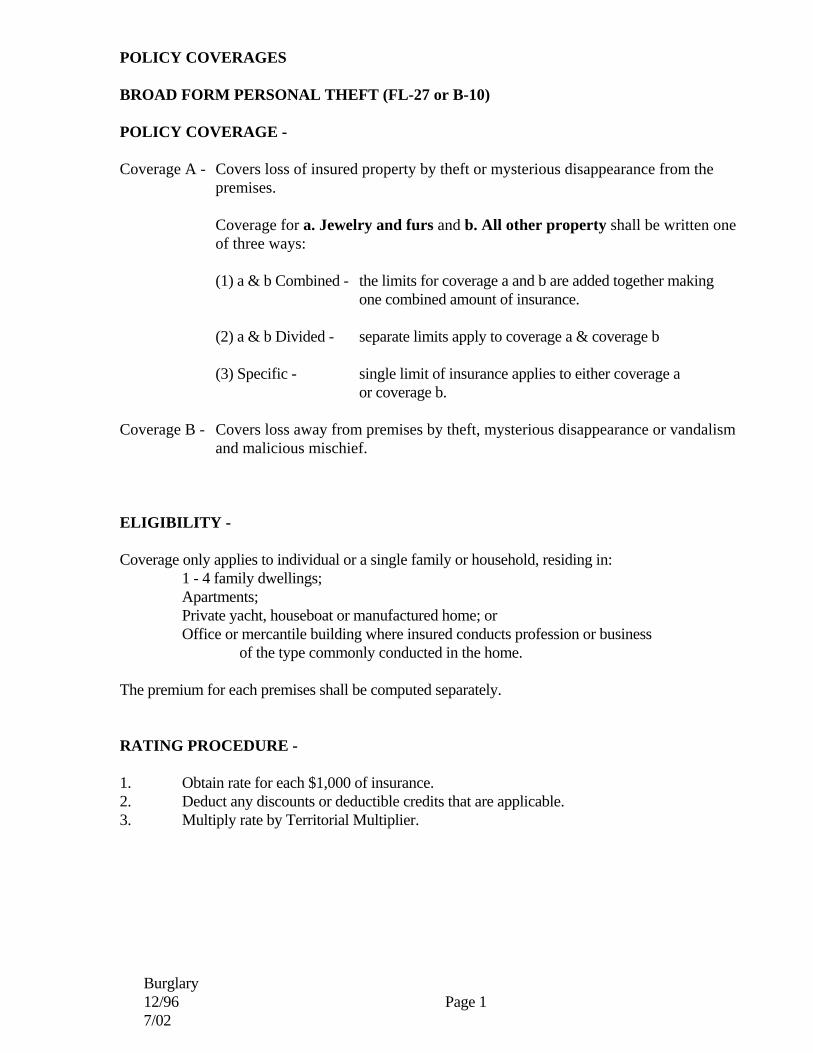

POLICY COVERAGES BROAD FORM PERSONAL THEFT (FL-27 or B-10)

POLICY COVERAGE -

Coverage A - Covers loss of insured property by theft or mysterious disappearance from the

premises.

Coverage for a. Jewelry and furs and b. All other property shall be written one of three ways:

(1) a & b Combined - the limits for coverage a and b are added together making

one combined amount of insurance. (2) a & b Divided - separate limits apply to coverage a & coverage b (3) Specific - single limit of insurance applies to either coverage a

or coverage b. Coverage B - Covers loss away from premises by theft, mysterious disappearance or vandalism

and malicious mischief. ELIGIBILITY - Coverage only applies to individual or a single family or household, residing in: 1 - 4 family dwellings; Apartments; Private yacht, houseboat or manufactured home; or Office or mercantile building where insured conducts profession or business of the type commonly conducted in the home. The premium for each premises shall be computed separately. RATING PROCEDURE - 1. Obtain rate for each $1,000 of insurance. 2. Deduct any discounts or deductible credits that are applicable. 3. Multiply rate by Territorial Multiplier.

Burglary 12/96 Page 2 7/02

RATES Coverage A - Loss From The Premises a. & b. a. & b. Each $1,000 of Insurance Combined Divided Specific 1st $45. $23. $11. 2nd 32. 14. 7. Each Additional 23. 11. 5.

Coverage B - Loss Away From The Premises

a. & b. Each $1,000 of Insurance Combined or Divided Specific 1st $65. $33. 2nd 42. 20. Each Additional 33. 7. Minimum Premium - The annual minimum premium is $25. OPTIONAL COVERAGES - LIMITATION TO BURGLARY ONLY - ( FL-28 or B-11) Coverage A - Coverage may be limited to burglary only. 20 % Credit DEDUCTIBLE CREDITS -

Deductible Amount Deductible Credit $100 15% $250 35% $500 60%

TERRITORIAL MULTIPLIER Remainder of State 1.00 New York 1.00 Bronx 1.00 Onondaga 1.00 Erie 1.00 Queens 1.00 Kings 1.00 Richmond 1.00 Monroe 1.00 Westchester 1.00 Nassau 1.00

Burglary 12/96 Page 3 7/02

PERSONAL THEFT COVERAGE (FL-26 or B-20) ELIGIBILITY - Coverage shall be written only for individual or a single family or household. Coverage shall be written to cover one to four family dwellings or individual units in apartments. RATING PROCEDURE - 1. Obtain rate for each $1,000 of insurance. 2. Deduct any discounts or deductible credits that are applicable. 3. Multiply rate by Territorial Multiplier. OPTIONAL COVERAGES - BURGLARY ALARM DISCOUNT - Coverage A - Central Station or Local Burglar Alarm 5% Credit DEDUCTIBLE CREDITS -

Deductible Amount Deductible Credit $100 15% $250 35% $500 60%

RATES Annual Rates Per Premises

Each $1,000 of Insurance a. & b. Divided Specific

1st $20. $10. 2nd 14. 6. Each Additional 10. 4.

TERRITORIAL MULTIPLIER

Remainder of State 1.00 New York 1.00 Bronx 1.00 Onondaga 1.00 Erie 1.00 Queens 1.00 Kings 1.00 Richmond 1.00 Monroe 1.00 Westchester 1.00 Nassau 1.00