Embed Size (px)

Citation preview

© 2012 Cleary Gottlieb Steen & Hamilton LLP. All rights reserved.

Throughout this presentation, “Cleary Gottlieb” and the “firm” refer to Cleary Gottlieb Steen & Hamilton LLP and its affiliated entities in certain jurisdictions, and the term “offices”

includes offices of those affiliated entities.

Kenneth L. Bachman

Paul Marquardt

Understanding U.S. Sanctions May 15, 2012

The Office of Foreign Assets Control (OFAC)

and Sanctions Programs

The U.S. Treasury’s Office of Foreign Assets Control (“OFAC”) administers and

enforces certain U.S. sanctions imposed against targeted countries,

governments, persons and activities.

OFAC sanctions generally operate by restricting or prohibiting the activities of

“U.S. persons” – a defined term that includes both individuals and entities.

“U.S. persons” include:

• U.S. entities and their non-U.S. branches, but generally not their non-U.S. subsidiaries

(the Cuba sanctions are the exception);

• U.S. branches and U.S. subsidiaries of non-U.S. parent companies;

• U.S citizens or permanent residents (“green card” holders) – wherever located; and

• Non-U.S. directors, officers, and employees when present in the United States.

OFAC Jurisdiction

3

Non-U.S. companies who are acting outside the United States generally do not

face direct OFAC liability (except in the case of certain re-exports of U.S. goods

or technology).

However, OFAC has become increasingly aggressive in asserting jurisdiction

over non-U.S. companies through their U.S. contacts, because they “cause” or

“aid” a violation by a U.S. person, or because they “re-export” U.S. origin

services to sanctioned persons.

• A non-U.S. company may face direct liability for violating U.S. sanctions if any of the

following are involved in their dealings with sanctioned parties.

– U.S. dollars

– U.S. sources of funds or technical support

– “Hidden” U.S. persons (e.g., green card holders) working for the company

– Acts within the United States

– Assistance by a U.S. person

Primary OFAC Issues

4

U.S. Sanctions – Primary Issues

U.S. persons dealing with foreign companies will be primarily concerned

about the risk of “facilitating” (a very broad concept) indirect dealings with

sanctioned parties and will focus on:

• Whether the counterparty is a sanctioned entity

• Whether a significant portion of the counterparty’s business is with sanctioned

parties or in sanctioned countries

• Whether proceeds of any investment or financing will be used to support activities

with sanctioned parties or in sanctioned countries

5

U.S. Sanctions – Primary Issues (cont’d)

U.S. persons may seek contractual representations and covenants to

protect them from OFAC liability

• Counterparty is neither a sanctioned entity nor owned or controlled by sanctioned

entities

• Counterparty derives a de minimis portion of its operating income from dealings

with sanctions targets and has a de minimis proportion of its assets in sanctions

targets

• Proceeds of investments or financing will not be used for dealings with or in

sanctions targets

– Market standard, based on OFAC practice, is typically a 10% de minimis threshold. If the

threshold is exceeded, pressures on diligence and ringfencing of proceeds will increase, and

some U.S. parties may refuse to participate.

If the foreign company issues securities in the U.S., the SEC views an

issuer’s dealings with designated “state sponsors of terrorism” as material

information that should be disclosed

• Currently includes Iran, Sudan, Syria and Cuba

• Some U.S. institutional investors have policies prohibiting investment in companies

active in these countries, particularly Iran and Sudan

6

Increasing risk. Sanctions risk has increased sharply as U.S. regulators have

sought new tools for international enforcement, especially in anti-terrorism

efforts, and are increasingly aggressive in extraterritorial enforcement.

Increasing penalties. Penalties for most sanctions violations have also

increased sharply in recent years.

• For each transaction that is the basis of a violation, the civil fine for most sanctions

violations is now the greater of $250,000 or twice the transaction amount (there is no

cap).

• For most willful violations, a criminal fine of up to $1,000,000 may be imposed (and a

maximum jail sentence of 20 years for natural persons).

No defenses based on lack of knowledge or intent. OFAC sanctions are a

strict liability regime.

• OFAC is often unwilling to give clear comfort, other than on a case by case basis.

• However, penalties may be mitigated by a range of factors, including self-disclosure of

violations and good compliance programs.

The Importance of OFAC Sanctions

7

OFAC sanctions offer few bright-line principles dividing legal and illegal

behavior.

Instead, each person’s risks and requirements will depend on a number of

factors, including:

• What sanctions are encountered. The scope and severity of sanctions varies widely

depending on the activity, program, and persons involved.

• When sanctions are encountered. OFAC sanctions are a function of U.S. foreign

policy, and are generally subject to different interpretations depending on the

geopolitics of the moment.

• How sanctions are encountered. OFAC is a strict liability regime, but penalties are

assessed through a risk-based analysis and depend significantly on the policy impact

of behavior, the quality of compliance programs, and numerous additional factors.

The Office of Foreign Assets Control and Sanctions Programs

8

OFAC sanctions are principally authorized by Executive Orders under two

broad Congressional grants of authority.

• Trading with the Enemy Act (“TWEA”) (1917)

– Originally enacted for the President’s use of wartime economic powers.

– Expanded in 1933 to deal with peacetime national emergencies.

– Expansion clawed back by IEEPA, but existing TWEA-based program against Cuba

remains in place.

• International Emergency Economic Powers Act (“IEEPA”) (1977)

– Primary legal authority for virtually all existing OFAC sanctions.

– Supplemented occasionally by other legislation (e.g., the Anti-Terrorism and

Effective Death Penalty Act of 1996 and the Foreign Narcotics Kingpin Designation

Act of 1999).

Sources of OFAC Law: Statutes & Legal Authority

9

OFAC sanctions are generally implemented through regulations that OFAC

issues under broad directives set forth in Executive Orders.

• These regulations (31 C.F.R. ch. V) are the main source of law in assessing OFAC

risks.

• However, the regulations are often incomplete; many fact patterns will not be

addressed directly by a clear rule.

• Regulations can be effective immediately; ordinary notice and comment procedures

under the Administrative Procedure Act are inapplicable because a foreign affairs

function is involved.

Sources of OFAC Law: Implementing Regulations

10

The OFAC web site provides fairly complete summaries of (i) sanctions

programs and (ii) some risks for certain industries.

However, when there are ambiguities or nuances in the regulations or

summaries, other OFAC guidance is minimal.

• Published FAQs and industry guidance are often very general or oriented toward

operational, not legal, issues.

• OFAC often “mixes and matches” concepts from one sanctions program to interpret

another.

• Case law is minimal and often ill-suited for generalization.

• No analog to the SEC no-action process or FRB legal interpretation process exists.

OFAC only occasionally publishes interpretative rulings on individual inquiries it

receives (only 24 total to date).

• OFAC staff may be approached informally, but are often reluctant to opine on a fact

pattern without very specific and detailed information.

• Interpretative letters or licenses may be sought from OFAC with full written

documentation; the process often takes months and is rarely consistent with the timing

of transactions.

Sources of OFAC Law: Guidance

11

There are two general types of restrictions:

• Asset controls restrict a U.S. person from freely dealing in property in which a

sanctioned person has an interest. U.S. persons must usually freeze such property

when it comes into their possession or control.

– Under most programs, U.S. persons may not simply reject (return) the property.

– “Property” is defined very broadly and includes “any property, real, personal, or mixed, tangible

or intangible, or interest or interests therein, present, future or contingent.” Very indirect interests

are sufficient.

• Transaction controls restrict a U.S. person from freely dealing with sanctioned persons.

These restrictions range from a full embargo on all dealings between a U.S. person

and a sanctioned country to restrictions on particular types of transactions (e.g.,

transactions with specific persons or industries, or transfers of sensitive U.S. goods

and technology).

OFAC sanctions also generally prohibit U.S. persons from “approving” or

“facilitating” transactions by non-U.S. persons that would be unlawful if

conducted by a U.S. person.

Scope of OFAC Sanctions: Types of Restrictions

12

OFAC sanctions have increasingly targeted designated entities (“smart

sanctions”) and focused on terrorism.

• Older sanctions were rooted in TWEA and the historical practice of banning “trading

with the enemy” and applied comprehensive sanctions to entire countries (e.g., Cuba,

North Korea).

• Subsequent sanctions were narrower, principally using:

– Country-based programs that appear to sanction a smaller set of parties (e.g., Sudan, where the

government is sanctioned, but not all citizens) or activities (e.g., Burma, where exports to the

U.S. are prohibited, but most U.S. imports to Burma are not).

– Activity-based sanctions (e.g., terrorism, narcotics) that in practice tend to operate as sanctions

on named parties.

– Sanctions against Iran are the exception – the program is extremely broad.

• Most recent sanctions purport to be country programs but in practice apply only to

designated parties (e.g., Liberia, Zimbabwe, Belarus, Côte d’Ivoire, the Democratic

Republic of the Congo).

OFAC is using all of these sanctions most heavily in the service of the broad

U.S. anti-terrorism and anti-proliferation programs.

Scope of OFAC Sanctions: The Targeting Trend

13

Asset and transaction controls vary significantly depending on the

particular OFAC program involved. Very generally, OFAC programs may be

divided into four general categories:

• Comprehensive country programs. U.S. persons are prohibited from virtually all

dealings or transactions with a sanctioned country, with persons located, organized, or

resident in those countries, and in the case of Cuba, with all nationals wherever

located. Cuba, Iran, Sudan, and Syria are currently subject to comprehensive

programs.

• Non-comprehensive country programs. U.S. persons are prohibited from certain

specified activities with the sanctioned country, as well as dealings with certain

designated persons associated with the country or its government.

– Burma (Myanmar) and North Korea are currently subject to extensive programs.

– Restrictions are principally on some or all trade between U.S. persons and the

target country; many other transactions may be permissible.

Scope of OFAC Sanctions: Targets of Restrictions

14

• Regime-based country programs. U.S. persons are prohibited from dealing with

designated persons associated with a regime or activity in various countries.

– These programs include individuals from or related to activities in Belarus, Côte

d’Ivoire, the Democratic Republic of the Congo, Lebanon, Somalia and

Zimbabwe, as well as former regimes of Iraq, Liberia, Libya, and the Balkans.

– Restrictions extend only to dealings with the designated persons; there are no

general restrictions on dealings with associated countries or nationals.

• Activity-based programs. U.S. persons are prohibited from dealing with designated

persons associated with certain activities, such as terrorism, the proliferation of

weapons of mass destruction, narcotics trafficking, trading in conflict diamonds,

and activities of significant transnational criminal organizations. These programs

also include certain trade restrictions.

Scope of OFAC Sanctions: Targets of Restrictions (cont’d)

15

What are Specially Designated Nationals (“SDNs”)?

• SDNs are entities, groups or individuals specifically designated by OFAC as persons with

which U.S. persons are restricted from dealing (currently over 4,600 unique entities).

• SDNs are gathered on a single publicly available list, but may be designated by OFAC under

virtually any program. U.S. persons are therefore subject to different restrictions for different

SDNs.

• The SDN list is not exhaustive, and U.S. persons are prohibited from dealing with many

persons not specifically listed as SDNs, and sanctions diligence thus must go beyond name-

checking the SDN list.

– Example. U.S. person finances a French entity that donates 90% of its profits to Hizbullah but is

not listed as a SDN.

– Example. U.S. person enters into a service agreement with a Dubai entity that is controlled by a

Sudanese government agency but is not listed as a SDN.

– Example. U.S. person deals with Fidel Castro, who is not listed as a SDN.

• Any entity owned by an SDN or controlled by a sanctioned government is likely sanctioned.

While not all sanctioned parties are on the SDN list, many institutions use it as

an initial screen for potential sanctions target “hits” to safeguard against U.S.

persons within the organization engaging in clearly prohibited transactions.

Scope of OFAC Sanctions: Targets of Restrictions (cont’d)

16

All OFAC sanctions programs (even the comprehensive ones) allow certain

activities, either with a “specific license” from OFAC or without prior application

to OFAC (“general licenses”).

Specific licenses may be requested for virtually any transaction that would

ordinarily violate sanctions, but are typically denied without a compelling

rationale (e.g., humanitarian assistance).

General licenses vary depending on the program, but are usually confined to

purely informational or administrative activities. Examples of activities that may

be permissible for a U.S. person to conduct with a sanctions target include:

• Attending international conferences that include sanctions targets;

• Disseminating business information via a website; and

• Membership on worldwide or regional committees that (i) oversee transactions or other

dealings with a range of parties, including sanctions targets, or (ii) engage in global

business strategy and policy-making.

Permissible Activities & Licensing

17

This taxonomy and the SDN list must be treated with considerable caution.

Programs and designations change constantly.

• Example. Sanctions against Libya were terminated in September 2004. In response to the Qadhafi

regime’s actions in quelling a popular uprising, sanctions were reintroduced in February 2011, only

to be eased again in September 2011 after Qadhafi’s removal.

• Example. New designations of Iranian financial institutions, Mexican persons, and Syrian

corporations in just the last few weeks.

Categories and lists help, but are not sufficient.

• Avoiding governments is not enough. Sanctions may apply to virtually all persons related to a

specific country or activity.

• Avoiding certain countries is not enough. Sanctions may be unrelated to the geographic location or

nationality of a designated party.

• Avoiding SDNs is not enough. Sanctions may apply to entities that, while not themselves SDNs,

derive most of their operating income from sanctions targets or hold most of their assets in such

targets.

Scope of OFAC Sanctions: Footnotes and Caveats

18

OFAC Sanctions in Practice

Most common situations involve indirect dealings by a U.S. person with a

sanctions target (or approving or facilitating such dealings). For example:

• A U.S. company wants to make a minority investment in a Spanish company with

operations in Cuba.

• A London bank wants to underwrite a debt offering by a French company that has an

Iranian subsidiary and offer the debt to U.S. investors.

• A Dubai company with U.S. directors and managers wants to acquire a Sudanese

company.

• A German company with U.S. subsidiaries wants to acquire an Iranian company.

• A U.S. bank wants to clear U.S. dollars for a U.K. correspondent with Zimbabwean

clients.

Situations involving direct dealings are less common:

• A U.S. company may want to deal directly with a sanctions target, such as through use

of an OFAC license (e.g., export food to Cuba).

• New OFAC sanctions may directly affect the operations or business interests of a U.S.

or non-U.S. company.

Common OFAC Sanctions Issues

20

A London bank wants to underwrite a global offering of securities of a French company

that has investments and dealings in Iran.

• Issue. OFAC could see the purchase of securities by U.S. investors as a prohibited

facilitation or indirect dealing with Iran by the U.S. investors.

• Guidelines for facilitation. An informal “safe” harbor rule has been developed by the

sanctions bar after years of practice and consultation with OFAC to guide when a U.S.

person will be “facilitating” a transaction.

– U.S. persons can generally engage in transactions with a non-U.S. entity with bona fide business

activities that are unrelated to sanctions targets, provided that the non-U.S. entity derives less

than 10% of its operating income from dealings with sanctions targets and has less than 10% of

its assets in sanctions targets.

– Income or assets in excess of the 10% limits do not mean the U.S. bank would be ipso facto

prohibited from underwriting or purchasing the securities; however, further diligence and analysis

would be required.

– The 10% limit is informal, and market practice is currently unsettled, with some underwriters

seeking representations based on a 5% limit.

• But no indirect dealings whatsoever. Whatever the “safe” harbor levels, U.S. persons may

not be involved in any dealing with the French company that amounts to an indirect dealing

with Iran.

– For example, U.S. investors cannot purchase the securities where the proceeds are directed in

whole or in part to finance the company’s activities in Iran.

Practical Scenario #1: Underwriting or Financing in the U.S.

21

The underwriter can take several measures to protect itself:

• Diligence. Review the level of the issuer’s or seller’s involvement in activities in any

sanctioned country and ensure that the proceeds of the issuance or sale are not

directly linked to activities with sanctions targets.

• Contract terms. The underwriter should also obtain representations and covenants to

the effect that:

– The issue or sale of the securities do not and will not result in a violation of the U.S. sanctions

laws and regulations by any party; and

– The issuer or seller will not use the proceeds in a manner that will give rise to a violation of the

U.S. sanctions laws and regulations by any party.

• Disclosure. Ensure that any activities relating to sanctioned countries are disclosed to

U.S. investors.

These issues and concerns are present any time a U.S. person (e.g., private

equity fund, hedge fund, investment company) seeks to invest or otherwise

provide financing to a non-U.S. person that deals with sanctions targets.

Practical Scenario #1: Underwriting or Financing (cont’d)

22

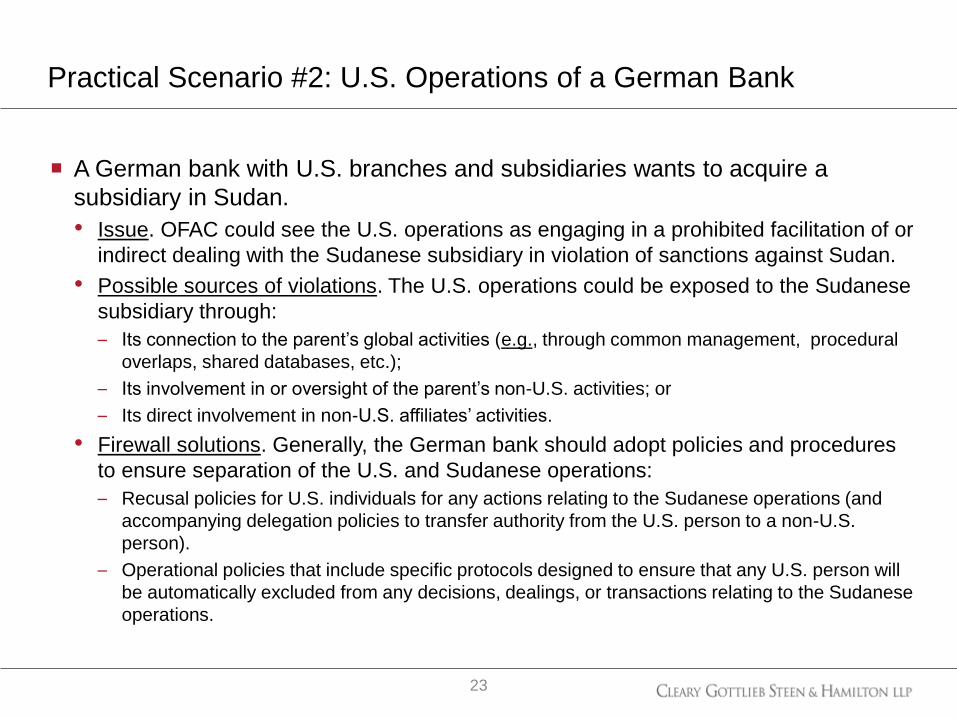

A German bank with U.S. branches and subsidiaries wants to acquire a

subsidiary in Sudan.

• Issue. OFAC could see the U.S. operations as engaging in a prohibited facilitation of or

indirect dealing with the Sudanese subsidiary in violation of sanctions against Sudan.

• Possible sources of violations. The U.S. operations could be exposed to the Sudanese

subsidiary through:

– Its connection to the parent’s global activities (e.g., through common management, procedural

overlaps, shared databases, etc.);

– Its involvement in or oversight of the parent’s non-U.S. activities; or

– Its direct involvement in non-U.S. affiliates’ activities.

• Firewall solutions. Generally, the German bank should adopt policies and procedures

to ensure separation of the U.S. and Sudanese operations:

– Recusal policies for U.S. individuals for any actions relating to the Sudanese operations (and

accompanying delegation policies to transfer authority from the U.S. person to a non-U.S.

person).

– Operational policies that include specific protocols designed to ensure that any U.S. person will

be automatically excluded from any decisions, dealings, or transactions relating to the Sudanese

operations.

Practical Scenario #2: U.S. Operations of a German Bank

23

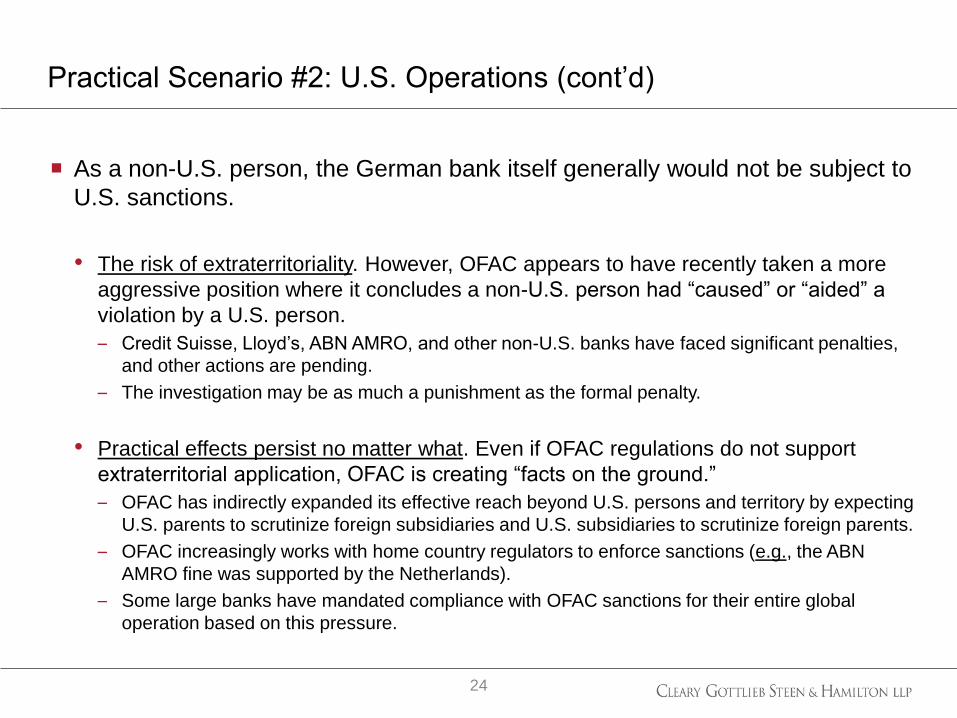

As a non-U.S. person, the German bank itself generally would not be subject to

U.S. sanctions.

• The risk of extraterritoriality. However, OFAC appears to have recently taken a more

aggressive position where it concludes a non-U.S. person had “caused” or “aided” a

violation by a U.S. person.

– Credit Suisse, Lloyd’s, ABN AMRO, and other non-U.S. banks have faced significant penalties,

and other actions are pending.

– The investigation may be as much a punishment as the formal penalty.

• Practical effects persist no matter what. Even if OFAC regulations do not support

extraterritorial application, OFAC is creating “facts on the ground.”

– OFAC has indirectly expanded its effective reach beyond U.S. persons and territory by expecting

U.S. parents to scrutinize foreign subsidiaries and U.S. subsidiaries to scrutinize foreign parents.

– OFAC increasingly works with home country regulators to enforce sanctions (e.g., the ABN

AMRO fine was supported by the Netherlands).

– Some large banks have mandated compliance with OFAC sanctions for their entire global

operation based on this pressure.

Practical Scenario #2: U.S. Operations (cont’d)

24

Recent OFAC Developments

Scrutiny of internationally active banks by OFAC is increasing, wherever they

are based.

• In recent years U.S. bank examiners and OFAC have been intensifying reviews of

letters of credit advising or confirming and U.S. dollar clearing for adequacy of

identifying information.

– A key issue is the use of “cover payments” (MT202s) that are used to clear U.S. dollar transfers

and do not disclose their origin or beneficiary.

– The Wolfsberg Group and The Clearing House Association have endorsed measures to enhance

the transparency of international wire transfers, including the development of more detailed

payment messages and the adoption of basic message transparency principles.

Dollar clearing is a key source of sanctions exposure; a U.S. bank (and

potentially a non-U.S. parent) may be liable for OFAC violations if it clears

dollars for sanctions targets, even indirectly (e.g., for a correspondent).

OFAC requires banks to implement risk-based policies and procedures

specifically for OFAC compliance (in addition to their anti-money laundering

policies).

Focus on Financial Institutions

26

The Iran sanctions involve some of the most complex, unintuitive provisions of

the OFAC regulations.

Regulators have focused on Iran owing to political pressure in the United

States and geopolitical developments.

• U.S. Treasury officials have visited CEOs of international banks and international

groups to urge that institutions cease doing business with Iran, particularly with its

financial sector, arguing that the risks to global peace (and the institutions) outweigh

the benefits.

• The U.S. has also globally supported targeted harsher actions, such as asset freezes,

against designated Iranian institutions and individuals connected to terrorism or to

nuclear proliferation.

• Many international banks have reduced or eliminated their dealings with Iran in recent

years, and the U.S. has publicized those actions.

Pending legislation would explicitly extend the Iranian sanctions to cover the

non-U.S. subsidiaries of U.S. persons.

Focus on Iran

27

Iran Sanctions

Iran Sanctions - Overview

In addition to OFAC sanctions, which apply to U.S. persons and activities, the

U.S. maintains indirect sanctions aimed at foreign companies dealing with

Iran.

Unlike OFAC, no connection between the United States and the sanctioned

activity needs to be shown.

These laws are not legally binding on foreign companies. However, if they

engage in the targeted activities with Iran, they themselves risk becoming the

subject of U.S. sanctions that will prohibit or restrict their access to the U.S.

market.

29

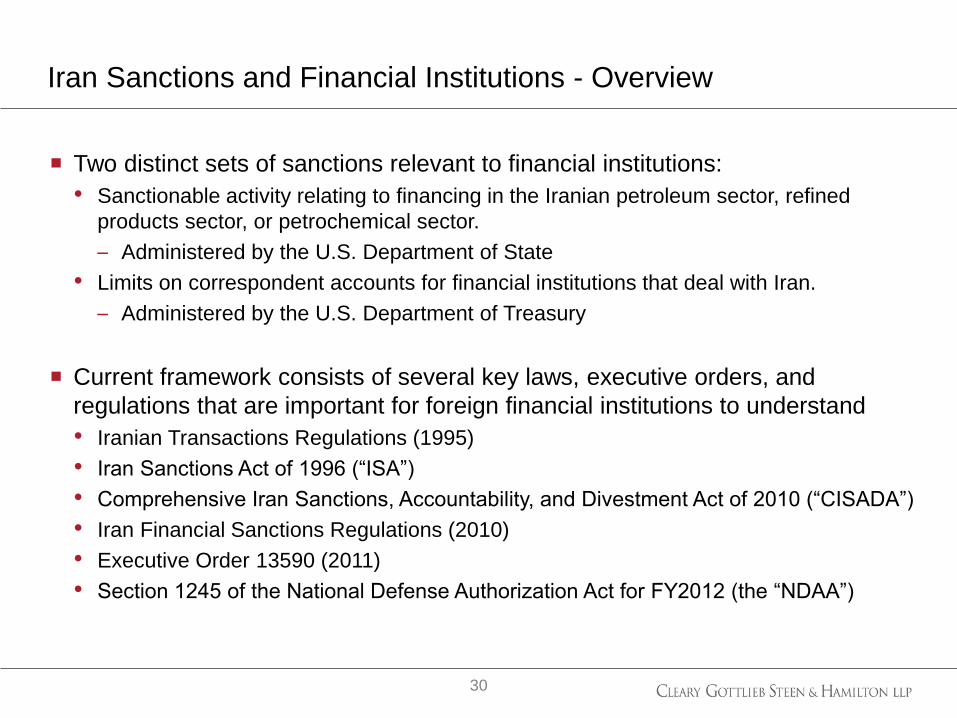

Two distinct sets of sanctions relevant to financial institutions:

• Sanctionable activity relating to financing in the Iranian petroleum sector, refined

products sector, or petrochemical sector.

– Administered by the U.S. Department of State

• Limits on correspondent accounts for financial institutions that deal with Iran.

– Administered by the U.S. Department of Treasury

Current framework consists of several key laws, executive orders, and

regulations that are important for foreign financial institutions to understand

• Iranian Transactions Regulations (1995)

• Iran Sanctions Act of 1996 (“ISA”)

• Comprehensive Iran Sanctions, Accountability, and Divestment Act of 2010 (“CISADA”)

• Iran Financial Sanctions Regulations (2010)

• Executive Order 13590 (2011)

• Section 1245 of the National Defense Authorization Act for FY2012 (the “NDAA”)

Iran Sanctions and Financial Institutions - Overview

30

Financing in the Iranian Petroleum

Production/Refined Products Sector

A financial institution could be sanctioned if it “knowingly” (includes “should

have known”):

• Finances a sale of refined petroleum products to Iran with a fair market value of

$1MM in a single transaction or $5MM over 12 months;

• Finances the provision of goods, services, technology, or support that could directly

and significantly contribute to the maintenance or enhancement of Iran's ability to

develop its oil and gas industry with a fair market value of $1MM in a single

transaction or $5MM over 12 months (including both upstream oil and gas production

and refined products);

• Finances the provision of goods, services, technology, or support that could directly

and significantly contribute to the maintenance or expansion of Iran's domestic

production of petrochemical products with a fair market value of $250K in a single

transaction or $1MM over 12 months.

• Itself provides any other service contributing to the activities listed above in excess of

the value limits.

Sanctionable Activity

32

Sanctions are not automatic.

• Investigation and then Presidential action required.

• Investigation, reporting and action on sanctionable activity are now “mandatory,” but no

mechanism other than political pressure exists to force the Administration to act.

• Investigation can be terminated if party being investigated agrees to stop activity.

• Includes mandatory investigation of past violations.

If a violation is found, the President is required to impose 3 of 9 available

sanctions from a menu. • Sanctions range from relatively mild to making the sanctioned party a Specially

Designated National (“SDN”) with whom U.S. persons may not deal.

Waivers of sanctionable activity possible.

State and local entities (e.g., public pension funds) are authorized to maintain

divestiture policies targeting companies doing business in Iran.

Enforcement

33

Limits on Correspondent Accounts for

Financial Institutions Dealing with Iran

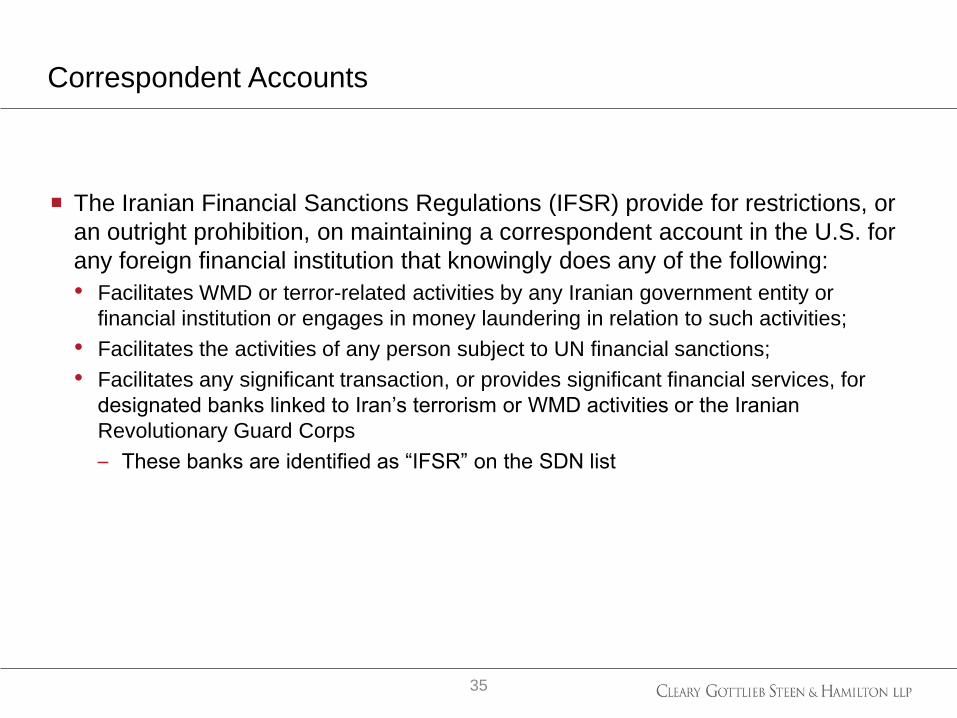

The Iranian Financial Sanctions Regulations (IFSR) provide for restrictions, or

an outright prohibition, on maintaining a correspondent account in the U.S. for

any foreign financial institution that knowingly does any of the following:

• Facilitates WMD or terror-related activities by any Iranian government entity or

financial institution or engages in money laundering in relation to such activities;

• Facilitates the activities of any person subject to UN financial sanctions;

• Facilitates any significant transaction, or provides significant financial services, for

designated banks linked to Iran’s terrorism or WMD activities or the Iranian

Revolutionary Guard Corps

– These banks are identified as “IFSR” on the SDN list

Correspondent Accounts

35

Correspondent Accounts (cont’d)

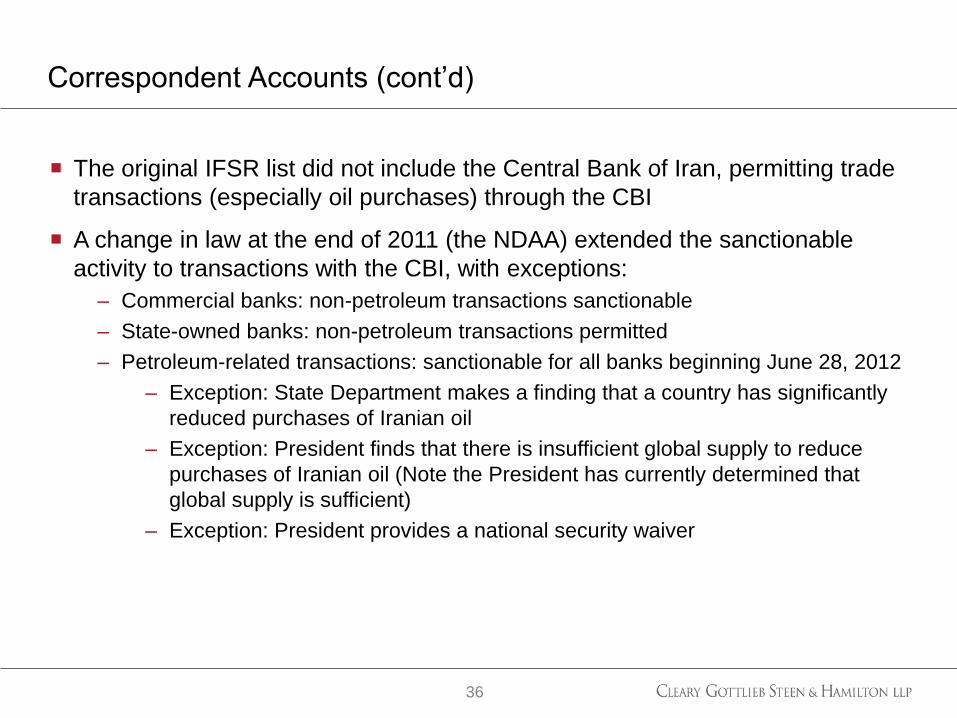

The original IFSR list did not include the Central Bank of Iran, permitting trade

transactions (especially oil purchases) through the CBI

A change in law at the end of 2011 (the NDAA) extended the sanctionable

activity to transactions with the CBI, with exceptions:

– Commercial banks: non-petroleum transactions sanctionable

– State-owned banks: non-petroleum transactions permitted

– Petroleum-related transactions: sanctionable for all banks beginning June 28, 2012

– Exception: State Department makes a finding that a country has significantly

reduced purchases of Iranian oil

– Exception: President finds that there is insufficient global supply to reduce

purchases of Iranian oil (Note the President has currently determined that

global supply is sufficient)

– Exception: President provides a national security waiver

36

Treasury may consider the totality of the facts and circumstances.

As a general matter, Treasury will look at the following:

• Size, number and frequency of transactions or financial services

• The nature of the transaction/financial service

• Level of awareness of personnel and whether the transactions are part of a pattern of

conduct

• The nexus between the financial institution and the blocked party

• The impact of the transaction or financial service on the objectives of the sanctions

against Iran

• Whether the transaction/financial service is part of deceptive practices

What is a Significant Transaction or Financial Service?

37

Treasury may impose the following sanctions on banks engaged in

sanctionable activity

• Complete ban on U.S. correspondent accounts;

• Prohibition of, or restrictions on, any trade financing through the correspondent

account;

• Restrictions on transactions processed through the account to certain types of

transactions, like personal remittances;

• Monetary limits on the transactions that may be processed through the correspondent

account;

• Requiring pre-approval from the U.S. financial institution for all transactions processed

through the account; or

• Prohibition of, or restrictions on, the processing of foreign exchange transactions

through the account (only with respect to sanctionable activities under the NDAA)

Limitations on Correspondent Accounts

38

Treasury has also adopted regulations requiring U.S. banks and branches to

make inquiries regarding their foreign correspondents upon request

• Applicable to US branches and agencies of foreign banks

Upon written request from the U.S. government regarding a specified foreign

financial institution for which a correspondent account is maintained, a financial

institution in the U.S. must request from the foreign financial institution

information about sanctionable activities with Iran that may have been recently

carried out by that foreign financial institution.

Regulatory Requests regarding Correspondent Accounts

39

Recent Executive Orders Targeting Iran and

Syria

Foreign Sanctions Evaders and Use of IT in Human Rights Abuses

Foreign Sanctions Evaders Executive Order

• Targets (1) facilitators of “deceptive transactions” for or on behalf of any sanctioned

person and (2) violators of U.S. sanctions not susceptible to prosecution as a practical

matter

• A “deceptive transaction” includes any transaction in any currency involving persons

sanctioned by the U.S. under the Iran or Syria sanctions in which the identity of the

sanctioned party is withheld from another participant in the transaction

“GHRAVITY” Executive Order

• Targets (1) operators of IT that facilitate “computer or network disruption, monitoring

or tracking” related to human rights abuses by the Government of Iran or Syria and

(2) suppliers of goods, services or technology “likely to be used to facilitate computer

or network disruption, monitoring or tracking” related to human rights abuses by the

Government of Iran or Syria

• Represents an expansion of U.S. sanctions to the IT and telecommunications sector

Both orders authorize the imposition of U.S. sanctions against targeted parties

• Consequences are not automatic; these orders are only authority to impose sanctions

41

Future Developments

Pending developments: Iran, Syria, and Burma

Additional proposed sanctions against Iran are likely to be adopted

• Expanded targeting of foreign companies doing business with Iran is likely

Strong political pressure for increased enforcement

• Proposals to require banks with correspondent accounts or listed securities in the

U.S. to publicly disclose all dealings with Iran

Syrian sanctions may follow Iran

• Possible that stronger measures will be taken to target companies doing business

with Syria

• FSE E.O. and GHRAVITY E.O. both treat Iran and Syria equally

Burma sanctions expected to be lifted at a slow pace

• Political developments have prompted EU and Canada to suspend most sanctions

against Burma, but initial steps by the U.S. have been modest

43

Other Sanctions Programs

OFAC coordinates with Commerce’s Bureau of Industry and Security (“BIS”)

and State’s Directorate of Defense Trade Controls (“DDTC”) in administering

U.S. export controls.

• Even if OFAC does not control trade with a particular country or for a particular good or

end-use, BIS or DDTC may.

BIS administers broad export and re-export controls generally focused on

“dual-use” goods and technology (e.g., encryption, optics, computers).

• However, certain BIS regulations may restrict virtually all exports to a particular country

(e.g., North Korea, Syria), regardless of “dual-use” classification.

• BIS controls are complex and require an item-by-item evaluation of several factors,

including the item being exported, the destination of the item, the end-use of the item,

and the identity of the end-user.

• “Exports” do not require sales (e.g., taking a laptop with Microsoft software to Iran).

DDTC administers export and re-export controls covering goods and

technology with military applications.

Export Controls

45

Helms-Burton Act (“HBA”). Targets any entity found to be “trafficking” in

property confiscated by the Cuban government.

• As with ISA, sanctions under HBA may be imposed on non-U.S. persons.

• Key provisions of HBA also have been effectively waived by the President, but certain

measures have been used (e.g., visa denials).

The potential extraterritorial application of U.S. sanctions has led Canada and

some E.U. countries to adopt “blocking legislation” designed to prohibit their

nationals from complying with such sanctions.

Independent Sanctions

46

The SEC has created the Office of Global Security Risk (the “OGSR”) in the

Division of Corporate Finance, which uses existing disclosure laws and

regulations to require registrants of securities in the United States to include

disclosure about any dealings with “state sponsors of terrorism” (e.g., Iran,

Syria).

• The SEC asserts that U.S. investors want to know about such activities and effectively

requires disclosure on the basis of qualitative materiality, even when the dealings are

not quantitatively material to the registrant.

After withdrawing an earlier system, the SEC is again considering adopting

mechanisms to facilitate investors’ access to these disclosures.

Significant divestment movements are also underway against Iran and Sudan,

with legislation pending to support both movements by publishing lists of

companies with certain interests in those countries. OGSR was also created in

part to facilitate such movements.

Securities Disclosure & Divestment

47

U.N. sanctions are adopted by Security Council resolution and generally are

not directly effective in the United States.

• U.S. sanctions programs are fundamentally unilateral and often exceed U.N. sanctions

in their scope (e.g., Iran) or are unconnected to U.N. programs (e.g., Cuba).

• The U.S. government’s general position is that no approval, authorization or

coordination with the United Nations is required in implementing its national sanctions

programs.

E.U. sanctions are adopted in common positions that are binding on member

states, their nationals, and their territory.

• Common positions typically implement U.N. Security Council resolutions.

• Similar to the SDN list, the E.U. maintains a “consolidated list” of persons, groups, and

entities subject to E.U. sanctions.

• Member states may adopt sanctions that exceed those set forth in a common position,

and may also need to adopt measures for the appropriate enforcement of common

positions (e.g., criminal penalties).

U.N. and E.U. Sanctions

48

www.clearygottlieb.com www.clearygottlieb.com

NEW YORK

WASHINGTON

PARIS

BRUSSELS

LONDON

MOSCOW

FRANKFURT

COLOGNE

ROME

MILAN

HONG KONG

BEIJING

BUENOS AIRES

SÃO PAULO