Embed Size (px)

Citation preview

Counterparty exposure:sometimes simple is good enough

Risk Management Consultants

A commentary on the approaches tomeasuring counterparty risk and why all

institutions need not be leading edge

Introduction With so much emphasis placed on changes that the major banks have to

make in calculating their credit exposure and capital it is easy to forget that

most of the world’s banks are not systemically important nor derive a huge

amount of business from complex derivative products. Most financial

institutions are not banks at all - asset managers, insurance companies and

other institutions all need to have a methodology for measuring their credit

exposure, but they may not need to adopt the same level of sophistication

as the global banks. In this paper we explore the approaches that may be

appropriate for smaller and less sophisticated institutions.

Before focussing on the needs of smaller institutions we will briefly review where the “leading edge”

is. Recent years have seen huge innovations and regulatory developments in the field of credit risk

measurement. Major financial institutions have developed sophisticated Monte Carlo models to calculate

their credit exposure. Under the Basel II and III Internal Model Method Approach banks are allowed to

use these models to calculate their regulatory capital for counterparty risk. The importance of Credit

Valuation Adjustment (CVA) has risen, with the most sophisticated institutions setting up functions to

actively manage CVA and calculate the CVA risk capital charge under the advanced method under Basel III.

A significant proportion of OTC derivatives will soon be cleared via central counterparties (CCPs) and a

huge spend is underway to put in place the infrastructure to enable banks to deal through CCPs and

support clearing services for clients that will not themselves be members of CCPs.

At the other end of the spectrum are the simpler institutions which largely ignore counterparty risk.

If they take it into account at all, they look at it on a notional basis or perhaps apply the BIS 1 add-ons.

The financial crisis demonstrated that financial counterparties are not too big to fail and we would

recommend that no institution should ignore counterparty risk or consider it on a notional or highly

simplistic BIS1 basis. Each institution needs to find the approach that best meets its needs.

How and why is counterparty exposure measured?Counterparty exposure is the amount that a financial institution may lose if the counterparty with

whom it has derivative or FX exposure defaults. Institutions need to measure counterparty exposure

for a number of reasons:

• To compare their exposure to the credit limits they have set – all institutions should do this

• To calculate the amount of regulatory capital that needs to be held for counterparty risk –

most institutions need to do this but only under the more sophisticated Basel (and in due

course Solvency II) approaches is sophisticated modelling of counterparty risk required

• To calculate economic capital for internal capital allocation purposes or calculate the “price”

of credit in a transaction – many institutions do this but institutions for which counterparty

exposure is not particularly significant may not

…we would

recommend that no

institution should

ignore counterparty

risk or consider it on a

notional or highly

simplistic BIS1 basis.

Risk Management Consultants

2013 © InteDelta Limited 1

Risk Management Consultants

Counterparty exposure is difficult to measure because it is uncertain. If an institution places a money

market deposit with a counterparty the value that will be lost if the counterparty defaults will be known

with certainty. If an institution enters into a long dated FX transaction or derivative the amount that will

be lost if the counterparty defaults will depend on how FX rates, interest rates or equity prices behave

in the future, which cannot be determined with certainty. If the institution has many transactions with

a counterparty on different underlyings, some of which are subject to the legal ability to net and/or

collateral, the problem soon becomes very complex.

There are two basic measures of counterparty exposure: measures of peak exposure and measures of

expected exposure. Potential Future Exposure (PFE) is the most commonly used measure of peakexposure and seeks to quantify the “maximum” mark to market (MTM) of a portfolio of transactions

with a counterparty. The maximum is determined to a statistical confidence level, usually 95%, 97.5%

or 99%. If the statistics are correct the actual MTM of a portfolio of transactions over the remaining life

of the portfolio should only exceed the current PFE in 2.5% of cases (to a 97.5% confidence level). PFE

is typically used for exposure and limit management purposes. PFE is calculated and compared to limits

which are set on a risk adjusted (PFE) basis.

Measures of expected exposure are used as inputs into the calculation of metrics such as CVA, economic

capital and regulatory capital (under the Basel II and III Internal Model Method). The remainder of this

paper focuses on PFE, but the calculations for measures of expected exposure closely follow those for PFE.

The graph below shows a PFE exposure profile with the corresponding measures of expected exposure.

2013 © InteDelta Limited 2

Risk Management Consultants

2013 © InteDelta Limited 3

Methodologies for calculating PFEThe methodologies for the calculation of PFE lie on a spectrum of sophistication as shown below:

Quantifying counterparty exposure in notional terms is still practised by some institutions but bears

little resemblance to the risks faced.

The first real attempt to calculate PFE is by applying “BIS 1” or simple add-ons. PFE is quantified bymultiplying the notional of each transaction by the add-on and the total counterparty exposure is then

the sum of the individual transaction exposures. The BIS 1 add-ons are very simplistic factors stipulated

in the original Basel Accord for the calculation of regulatory capital for counterparty risk. Some institutions

still use these as a proxy for the calculation of PFE although this is not a practice we would recommend.

Rather than applying the BIS add-ons some institutions develop their own simple add-ons, for example

1% for interest rate swaps, 2% for FX etc. Such add-ons may have little or no quantitative underpinning

and are often very broad-brush – for example they may not take into account different underlyings

even though the volatilities of different FX rates, interest rates and equity prices can be very different.

As such, simple add-ons often represent a relatively crude representation of the risk of a transaction.

The next stage in the evolution of sophistication is the adoption of granular add-ons without portfolioeffects. Under this method quantitative models are developed to provide a more sophisticated

representation of the risk of each transaction often resulting in a granular set of add-ons tables which

differentiate between factors such as underlyings, maturity, direction of transaction (e.g. receiving or

paying fixed in an interest rate swap) and “in-the-moneyness”. The total PFE for that counterparty is then

calculated by summing the PFE for each transaction. Whilst this method can provide a good approximation

of risk at the transaction level, the total portfolio exposure may be significantly overstated because certain

transactions may offset one another (e.g. equal and opposite transactions with the same counterparty),

particularly with the ability to perform close-out netting which is permitted under ISDA. Counterparty

exposures may also be collateralised, in most cases under a Credit Support Annex (CSA), and the effect

of the collateral and the CSA parameters (e.g. Threshold and Minimum Transfer Amount) are not

incorporated into the PFE calculation.

�Methodologies for calculating PFE

> Notional > BIS/simple add-ons

> Granular add-ons without portfolio effects

> Granular add-ons with portfolio effects

> Monte Carlo simulation

Methodologies for

the calculation of PFE

lie on a spectrum of

sophistication.

Risk Management Consultants

2013 © InteDelta Limited 4

The above deficiencies are rectified under the granular add-ons with portfolio effects method.

This method represents the most sophisticated option that is possible under an add-on methodology

– a granular set of add-on tables with an algorithm that takes into account portfolio effects, close-out

netting and collateralisation. Nevertheless, such an advanced add-on approach may still suffer from a

number of deficiencies:

• Add-ons are determined by calculating PFE for generic proxy transactions. To the extent that actual

transactions differ from these proxies, the add-ons may not accurately reflect the true PFE

• The algorithms for taking into account portfolio effects usually work by assigning transactions to

groups which can be offset against one another. If these rules are too conservative the full extent

of portfolio benefits are not given. If the rules are not sufficiently conservative the true PFE may be

understated as two transactions may be assumed to perfectly offset when in reality they do not

These deficiencies are remedied by the application of the most sophisticated PFE methodology, MonteCarlo simulation. This is a general numerical technique used in a variety of scientific, engineering and

economic situations. It is particularly useful in dealing with mathematical situations which incorporate

randomness or uncertainty, and has found a home in solving the complex equations which exist in finance.

A detailed description of Monte Carlo simulation is beyond the scope of this paper but the diagram

below shows the stages in the calculation of PFE under Monte Carlo.

Stages in the calculation of PFE under Monte Carlo

> Evolution of risk factors on correlated basis

> Revaluation of all transactions in portfolio

> Apply effects of collateral and close-out netting

> Calculate distribution of MTMs

The evolution of risk factors on a correlated basis involves identifying each risk factor (i.e. FX rate,

equity price, interest rate etc) to which a counterparty portfolio is sensitive and evolving this over time.

Since risk factors evolve in a semi-random (stochastic) manner, these cannot be modelled with certainty,

but instead a range of possible paths is calculated. This is repeated several thousand times to build up

a distribution of possible outcomes for each risk factor. The correlation between risk factors is also

incorporated. The second stage is to revalue all transactions in the portfolio to determine the mark

to market for each transaction along each simulation path. Next the effects of collateral and close-out netting are applied to arrive at the total net credit exposure for each path. Finally, the distributionof mark to markets is assembled and the relevant percentile is calculated to arrive at the PFE.

Risk Management Consultants

2013 © InteDelta Limited 5

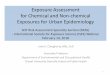

The graph below compares the PFE profile for a collateralised and uncollateralised portfolio under both

an advanced add-on approach (i.e. with portfolio effects) and Monte Carlo. It is striking that the Monte

Carlo profile is notably more granular and the exposures are much lower. This reflects the better

incorporation of diversification and the effect of offsetting transactions.

Add-ons - Uncollateralised.

Add-ons - Collateralised.

Monte Carlo - Uncollateralised.

Monte Carlo - Collateralised.

Which is the most appropriate methodology for an institution?Large, sophisticated banks will almost certainly adopt Monte Carlo simulation or at the very least an

advanced add-on methodology incorporating portfolio effects. For smaller institutions the decision

may be less clear cut. The primary considerations are:

• Significance of FX and derivative exposure – institutions for which exposure to FX and derivatives

accounts for a significant proportion of their exposure are more likely to invest in more sophisticated

risk measurement techniques for PFE to improve the overall accuracy of the institution’s risk exposures.

An institution whose credit exposure is primarily lending based and has only a small treasury and

limited derivative activities may opt for less sophisticated techniques

• Complexity of transactions – if an institution’s derivative transactions are non-vanilla more

sophisticated methodologies may be required to produce an accurate measure of PFE

• Credit pricing and regulatory capital – if an institution needs to produce a sophisticated measure

of CVA for credit pricing purposes or is using its own models for the calculation of regulatory capital

for counterparty risk (such as under the Basel II and III Internal Model Method) it will need to adopt

a more sophisticated measure of PFE, almost certainly Monte Carlo simulation

• Systems environment – it may be possible to accommodate an upgrade of PFE methodology

within the institution’s existing systems environment or a completely new system may need to be

implemented. Monte Carlo simulation is much more systems intensive than add-on techniques

• Expectations of regulators – regulators will often stipulate or encourage institutions of a certain

size to invest in more sophisticated risk measurement methodologies

Large, sophisticated

banks will almost

certainly adopt

Monte Carlo

simulation. For

smaller institutions

the decision is

less clear cut.

Risk Management Consultants

2013 © InteDelta Limited 6

• Cost/benefit – implementing a new counterparty methodology invariably involves a major systems

project. In general, the more sophisticated the methodology the more costly the initiative will be

both in terms of implementation and ongoing support. If the upgrade of methodology will result

in lower regulatory capital (for example by moving to the Internal Model Method) the benefit of

implementing the methodology will be transparent. More often, however, it will be less tangible:

- More efficient use of limits should enable more business under the same risk appetite

or the more efficient allocation of limits to business units

- Ability to more accurately price credit risk in transactions

- More accurate exposures should improve decision making and over the long term

reduce credit losses

- Regulators may be placated

• Availability of quantitative resources – more sophisticated methodologies require highly

quantitative staff with a background in risk management for traded products. Smaller institutions

may not have a ready pool of quantitative resource at their disposal and as a result may consider

the upgrade of counterparty methodology not worth hiring the required personnel.

How InteDelta can help

Methodology advice

Modeldevelopment

Implementation

Businessrequirementsand systemselection

InteDelta has advised many institutions on counterparty exposure methodology and more widely around

counterparty risk management. Taking advantage of the InteDelta Consulting Approach, our services

span the full lifecycle of a project ranging from initial strategic advice to the implementation of a

complete solution.

When institutions are in the early stages of considering an improvement to their counterparty risk

methodologies, systems and processes we are often engaged to provide methodology advice. Thisinvolves considering all of the aspects described in the section above to arrive at the most appropriate

methodology for that institution. The next stage in a typical engagement is to define the business

InteDelta has advised

many institutions on

counterparty exposure

methodology and

more widely around

counterparty risk

management.

Risk Management Consultants

2013 © InteDelta Limited 7

requirements for a new system. We are often involved in the decision of whether the institution

should develop in-house or select a vendor solution, and we have an established system selectionmethodology to provide an independent assessment of the solution that best meets the institution’s

requirements. We are very familiar with most of the major counterparty systems but are independent

of vendors and are vendor agnostic. During the implementation stage of a project we may undertake

model development to enhance the PFE methodologies and our implementation capability includes

programme and project management, business analysis, quantitative support and testing.

Case studies Asian Bank The bank is the largest player in its home market. It used a relatively simple add-on methodology for

the calculation of PFE and wished to make improvements to this methodology in minimum time and

at minimum cost. InteDelta was engaged to review its methodologies and made recommendations for

the changes it should make to its add-on approach without moving to Monte Carlo simulation. This

involved making improvements to the models used to calculate add-ons at the transaction level and the

development of a portfolio aggregation methodology to take account of close-out netting and collateral.

In the implementation phase InteDelta developed the models for the calculation of the revised add-ons

and wrote the methodology and business requirements for portfolio aggregation which was implemented

in the bank’s existing third party counterparty risk management system. InteDelta then worked with the

vendor of this system to deliver the methodology, providing full project management and testing support.

UK Insurance CompanyThe insurer used spreadsheets and very simplistic add-ons to calculate PFE. To meet the requirements

of Solvency II the insurer wished to upgrade its entire systems infrastructure for the management of

counterparty risk, including risk measurement. InteDelta was initially engaged to develop the business

requirements for the new solution and this included providing advice on the most appropriate PFE

methodology. The insurer subsequently took advantage of our system selection methodology to identify

a vendor that could meet its requirements.

Middle Eastern BankInteDelta was initially engaged to produce an analysis of the gaps in the bank’s approach to counterparty

risk, which identified deficiencies in the bank’s policies, methodologies and systems. InteDelta was then

subsequently engaged to develop a counterparty policy and methodology which could be tactically

implemented within the bank’s existing systems. The bank later decided to investigate a more strategic

approach and InteDelta advised on the different IT architecture options and the vendors that may be

able to meet its requirements for a new counterparty risk management system.

European BankThe bank is a medium sized European bank and used a relatively sophisticated add-on approach for

the measurement of PFE. The bank was considering making further upgrades to this methodology

or abandoning it in favour of Monte Carlo simulation. InteDelta was engaged to perform a detailed

analysis of the advantages and disadvantages of moving to Monte Carlo including a quantitative

analysis of the bank’s exposures under different methodologies. InteDelta also conducted a market

benchmarking study to establish the practices within the bank’s peer group.

InteDelta’s recommendation was for the bank to move to Monte Carlo simulation. This recommendation

was accepted and the bank subsequently selected a vendor solution and has now gained approval to

use its own models for the calculation of regulatory capital under the Internal Model Method.

Risk Management Consultants

2013 © InteDelta Limited 8

About InteDeltaInteDelta helps financial institutions better manage their risk. Through our range of consulting

and associated products we provide assistance in areas such as:

• Risk management policies and methodologies;

• Target operating model design;

• Technology selection and implementation;

• Market intelligence and benchmarking.

Our areas of expertise cover the major risk categories faced by financial institutions: credit, market,

liquidity and operational risk. We have advised a diverse portfolio of financial institutions located across

the world, at different levels of sophistication on counterparty risk methodology and more widely around

the systems, processes and policies required to manage counterparty risk. Our global client base includes

large US, European and Asian investment banks, asset servicing providers, regional banks, institutional

investors and hedge funds.

InteDelta applies subject matter expertise through our core consulting approach to deliver change

across all aspects of risk management.

Further InformationIf you would like to discuss any of the issues addressed in this White Paper, please contact:

Michael BryantManaging Director

Email: [email protected]

Tel: +44 (0)20 7153 1037

www.intedelta.com

Douglas WhiteBusiness Development and Marketing Manager

Email: [email protected]

Tel: +44 (0)20 7887 2205