Embed Size (px)

Citation preview

Understanding Business Tax Returns: A Case Study for Family Lawyers

www.aronsonllc.com/blogs

September 12, 2017

‹#› © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Agenda

• Introduction • Business Tax Return Basics • Case Study Part 1 – Fact Patterns & Tax

Filings • Case Study Part 2 – Comparisons &

Summaries • Conclusion

3 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Introduction

4 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

About Aronson LLC

Aronson LLC provides a comprehensive platform of assurance, tax, and consulting solutions to today’s most active industry sectors and successful individuals. For more than 50 years, we have purposefully expanded our service offerings and deepened our industry specialties to better serve the needs of our clients, people, and community. From startup to exit, we help our clients maximize opportunity, minimize risk, and unlock their full potential.

5 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Stuart A. Rosenberg, CPA, CVA, serves as a partner in Aronson LLC’s Financial Advisory Services group. He joined the firm in 1989 and has spent almost 30 years in the industry. Stuart’s clients include retail, wholesale, service, healthcare, hospitality, professional services, venture capital, construction and real estate businesses. Stuart specializes in litigation support services including valuations of closely-held businesses, preparation and documentation of lost profits, damages claims, evaluation of accounting and tax issues, financial analysis and investigations, general business issues and related expert testimony and forensic support services. As an expert in the field, Stuart has provided a variety of articles for publications such as Legal Time’s Commercial Litigation. He is a member of AICPA, VSCPA, and the National Association of Valuation Analysts. Stuart received his bachelor’s degree in business administration from American University in 1984, and he earned his certification as a valuation analyst from the National Association of Valuation Analysts in 1996.

Partner, Financial Advisory Services

301.231.6264

Stuart Rosenberg, CPA, CVA

6 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Sal is a Certified Public Accountant (CPA) with more than 25 years of assurance, tax, and financial advisory services experience. Sal has provided a broad range of services to closely-held businesses and the individual owners of those businesses. He has worked with clients in a variety of industries, including professional practices, retailers, manufacturers, software developers, and internet publishers. As a member of Aronson’s Financial Advisory Services practice, Sal specializes in litigation support services including, valuations of closely-held businesses, forensic accounting, tax matters, and financial analysis with an emphasis in family law engagements.

Senior Manager, Financial Advisory Services

301.231.6272

Sal Ambrosino, CPA, ABV

7 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Webinar Objectives

• Not mention a single IRS Code section • Distinguish between different types of business tax returns • Understand how the entity structure affects its tax reporting • Identify the “normal” owner compensation scenarios for different

entities • Identify other entity-specific differences • Develop more meaningful information requests

8 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Webinar Family Law Context

• Market Economy – Active business owners – Driven to maximize returns

• Return on capital investment • Compensation

• Divorce Motivations – Minimize income while maintaining returns – Minimize value of business interest while retaining control and cash

flows

9 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Business Tax Return Basics

10 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

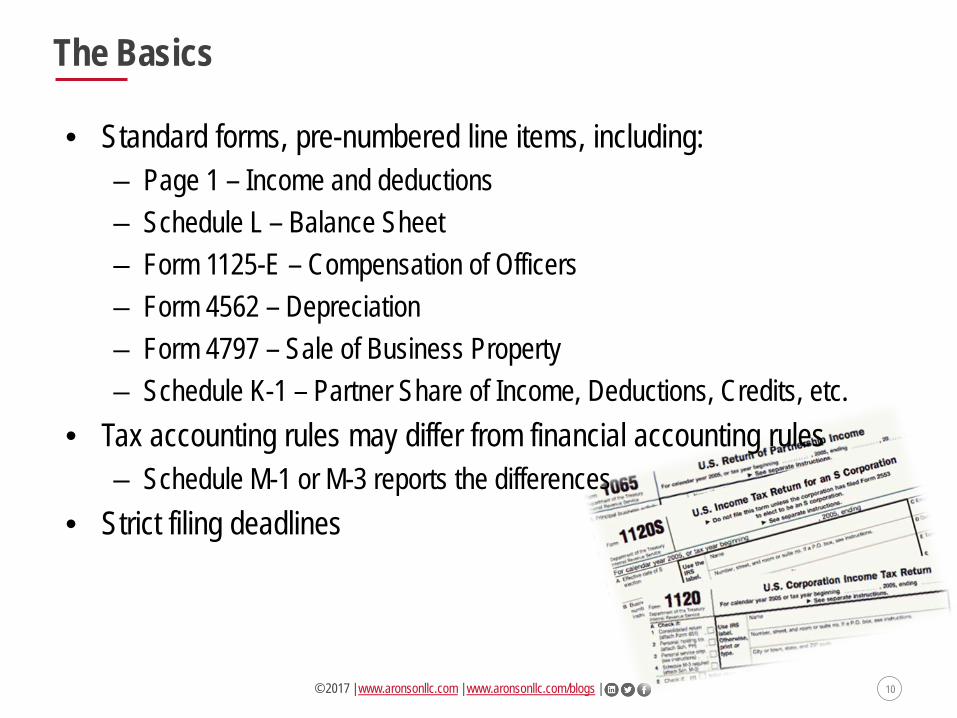

The Basics

• Standard forms, pre-numbered line items, including: – Page 1 – Income and deductions – Schedule L – Balance Sheet – Form 1125-E – Compensation of Officers – Form 4562 – Depreciation – Form 4797 – Sale of Business Property – Schedule K-1 – Partner Share of Income, Deductions, Credits, etc.

• Tax accounting rules may differ from financial accounting rules – Schedule M-1 or M-3 reports the differences

• Strict filing deadlines

11 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

The Basics

• Fines & penalties – For late filing – For incomplete or inaccurate reporting

• Basic non-financial information common to all business returns: – Name and address of business – Date business started – Method of accounting – Principal business activity – Other entities owned by the business – Principal officer – Tax preparer

12 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Different Forms for Different Entity Types

• Taxed first at the corporate level: – C Corporations / Form 1120

• Pass-Through Entities: – S Corporations / Form 1120S – Limited Liability Companies / Form 1065 – Partnerships / Form 1065

13 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Form 1120

• Used by C Corporations • Fiscal year permitted • Must use the accrual basis of accounting if over $5.0M in revenue • The C Corporation’s profits are tax at the corporate level separate

and apart from its owners • Distributions from a C Corporation to its stockholders (typically in the

form of dividends) are taxed again at the stockholder level • No ownership restrictions • May own interests in Partnerships and LLCs, may NOT own

interests in S Corporations

14 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Pass-Through Entities – In General

• In general, no income tax at the entity level • Profits are allocated to the owners and taxed on the owners’

separate tax returns • In general, owners taxed on allocated income, not on distributions • Entity will typically distribute at least enough to cover tax burden • There are different rules for different types of pass-through entities

15 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Form 1120S

• In general, ownership limited to individuals, estates and certain trusts • Number of stockholders limited to 100 or fewer • Limited to one class of stock – except voting rights • Must use a calendar year, unless special election made with annual filing and

special withholding tax paid • Use of cash basis permitted • Profits are reported on the owners’ tax returns • In general, distributions of profits to the stockholders are tax free • Distributions must be pro-rata to the stockholders • May own interests in C Corporations, partnerships, LLCs and certain S

Corporations

16 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

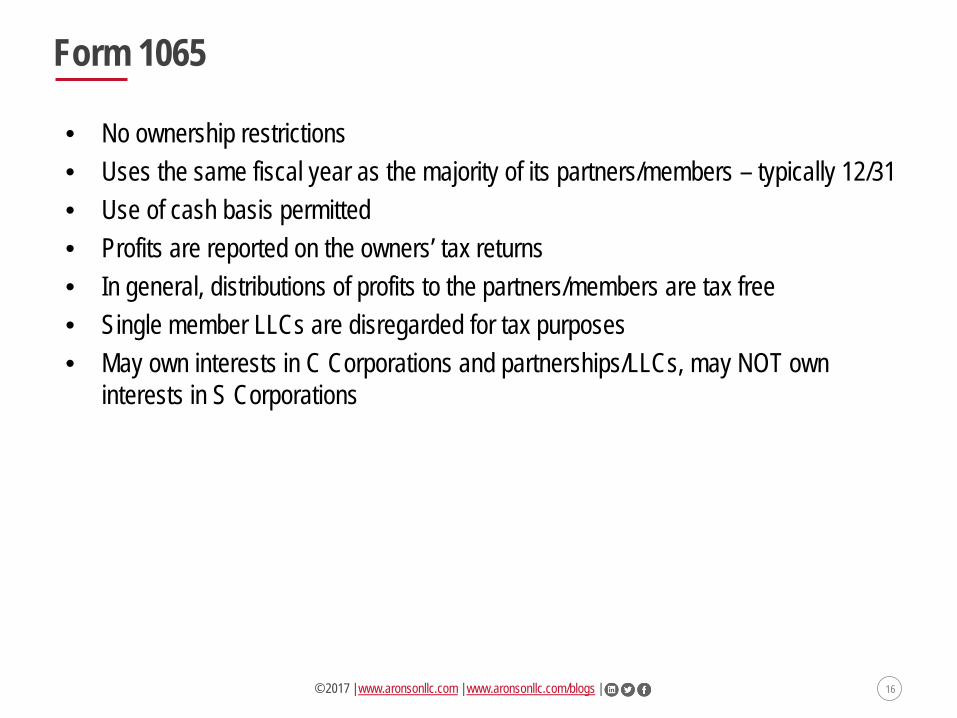

Form 1065

• No ownership restrictions • Uses the same fiscal year as the majority of its partners/members – typically 12/31 • Use of cash basis permitted • Profits are reported on the owners’ tax returns • In general, distributions of profits to the partners/members are tax free • Single member LLCs are disregarded for tax purposes • May own interests in C Corporations and partnerships/LLCs, may NOT own

interests in S Corporations

17 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Case Study Part 1 – Fact Patterns & Tax Filings

18 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Fact Patterns

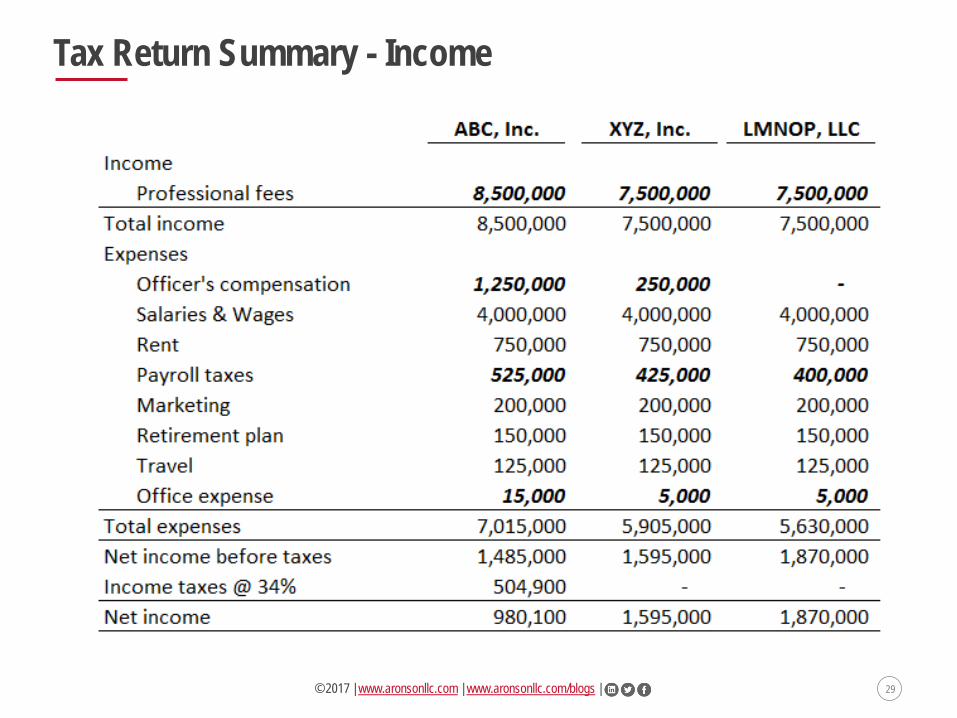

• ABC, Inc., XYZ, Inc., and LMNOP, LLC are small business which provide professional services in the Washington, D.C. Metropolitan Area.

• The companies are owned by triplets Pat (ABC), Alex (XYZ), and Jordan (LMNOP) who have shared everything equally since birth.

• Jordan and Ryan are divorcing. • The siblings have all told Ryan’s counsel that the businesses are

identical in all respects (except for their corporate structure) and generate equivalent amounts of income.

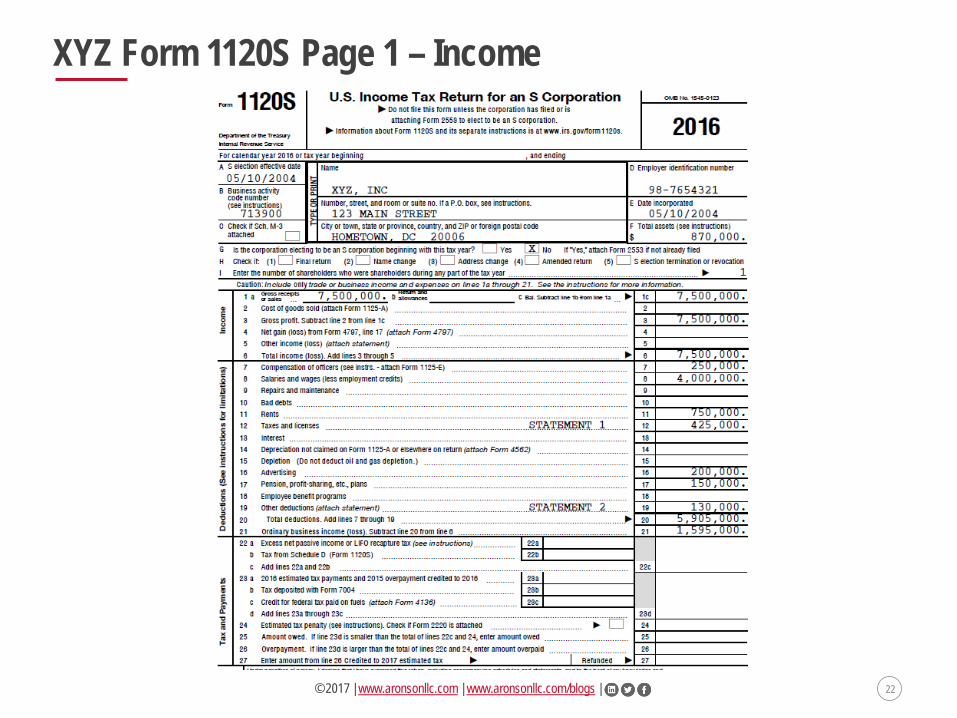

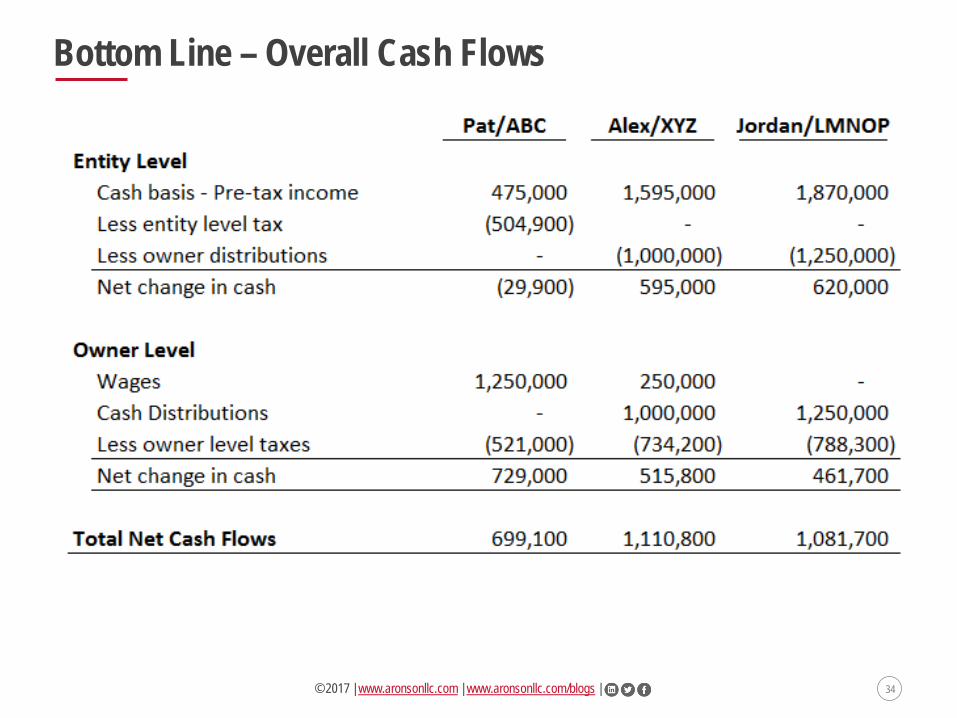

• However, Ryan knows for an absolute fact that the triplets’ salaries are $1,250,000 (Pat), $250,000 (Alex), and $0 (Jordan), and that the net income for the businesses are $973,500 (ABC), $1,595,000 (XYZ), and $1,870,000 (LMNOP).

19 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Fact Patterns

• Can the siblings possibly be telling the truth? • To get to the bottom of it, Ryan’s attorney requests, and Jordan’s

attorney provides, copies of the latest tax return for all three entities. • Is it possible to reconcile the significant differences between the

entities? • Will the tax returns demonstrate that each entity really generates the

same amount of income?

20 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

ABC Form 1120 Page 1 – Income

21 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

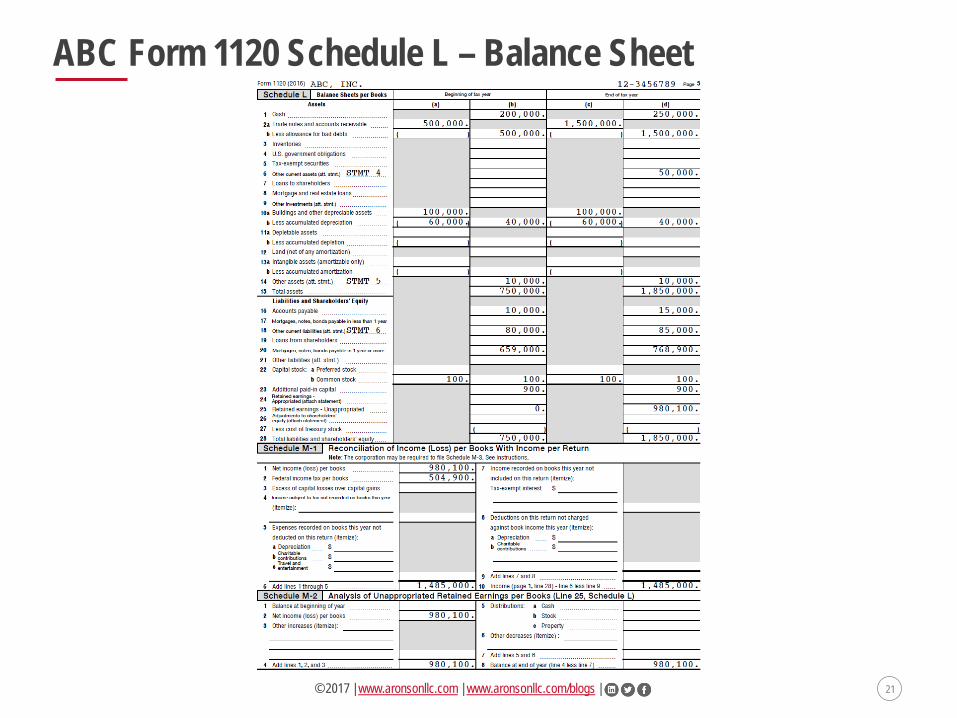

ABC Form 1120 Schedule L – Balance Sheet

22 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

XYZ Form 1120S Page 1 – Income

23 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

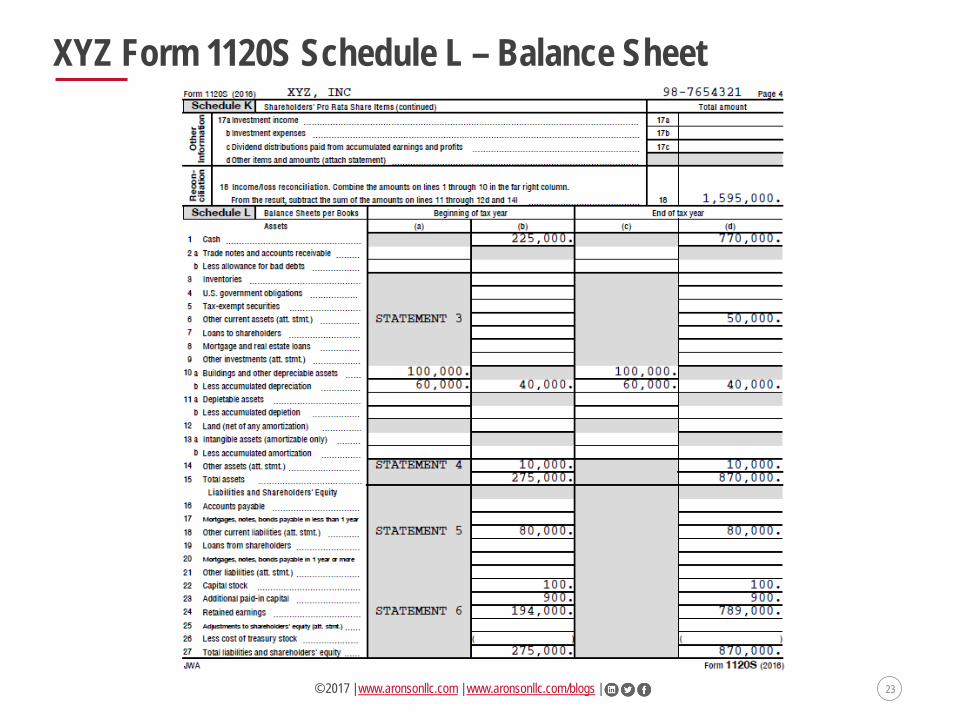

XYZ Form 1120S Schedule L – Balance Sheet

24 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

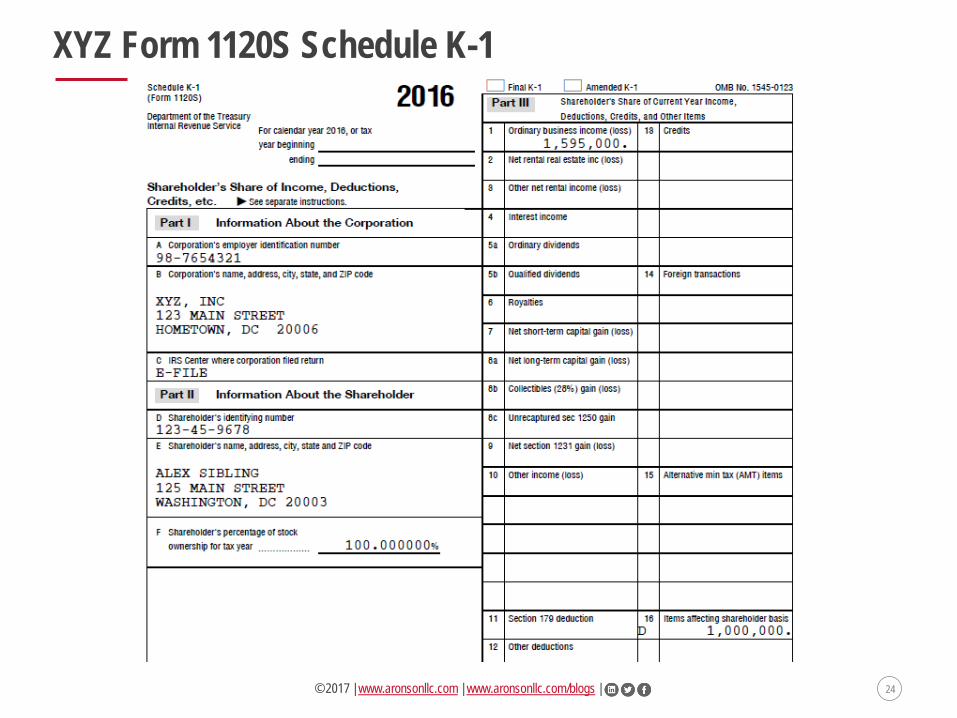

XYZ Form 1120S Schedule K-1

25 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

LMNOP Form 1065 Page 1 – Income

26 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

LMNOP Form 1065 Schedule L – Balance Sheet

27 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

LMNOP Form 1065 Schedule K-1

28 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Case Study Part 2 – Summaries & Comparisons

29 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Tax Return Summary - Income

30 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

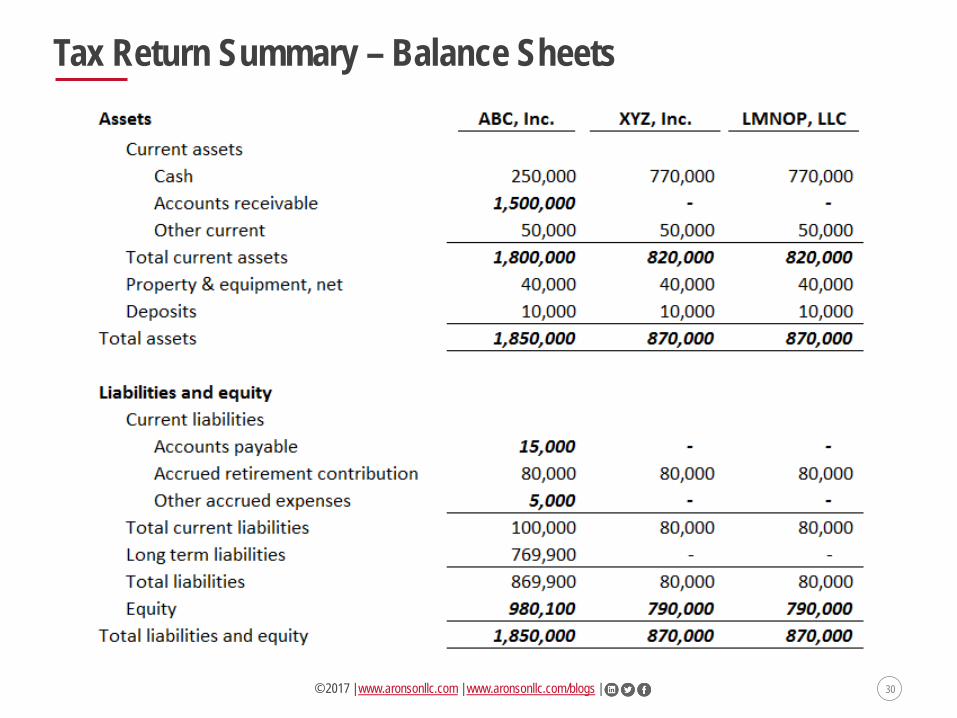

Tax Return Summary – Balance Sheets

31 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Income Statement Comparisons

32 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

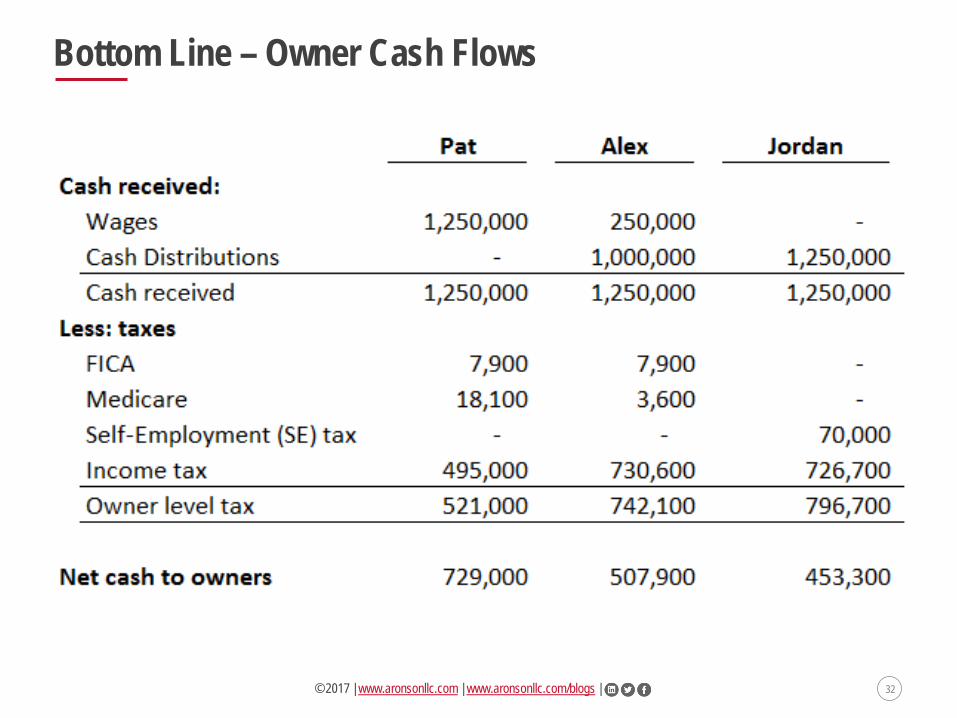

Bottom Line – Owner Cash Flows

33 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

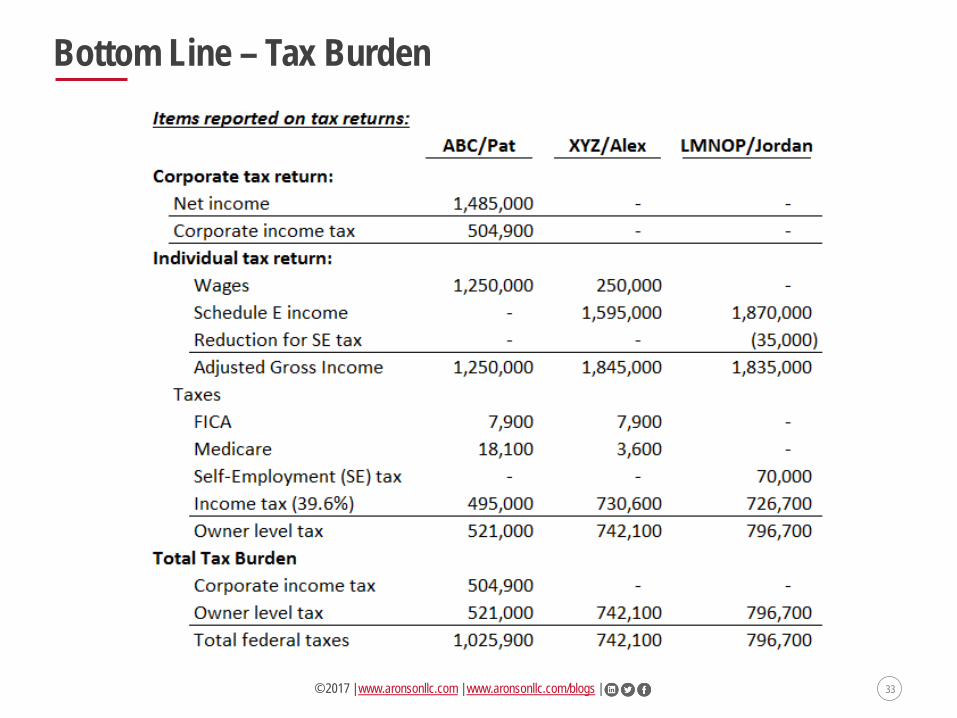

Bottom Line – Tax Burden

34 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Bottom Line – Overall Cash Flows

35 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Who Would You Rather Be?

• Pat ??? • Alex??? • Jordan???

36 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Conclusion

37 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Webinar Objectives

• Not mention a single IRS Code section • Distinguish between different types of business tax returns • Understand how the entity structure affects its tax reporting • Identify the “normal” owner compensation scenarios for different

entities • Identify other entity-specific differences • Develop more meaningful information requests

38 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Takeaways

• You don’t have to be a CPA to understand the basics of business tax returns

• Knowing the basics can help with case management • Identify financial and other issues up front by looking at your clients’

tax returns • Know when to engage specialists

39 © 2017 | www.aronsonllc.com | www.aronsonllc.com/blogs |

Q&A