Embed Size (px)

Citation preview

SECTION 959 PREVIOUSLY TAXED INCOME OF A CFC John Robert Cohn, Partner Thompson & Knight LLP Dallas, Texas U.S. TAX PLANNING FOR CFCs UNDER SUBPART F

You’ve picked up a subpart F inclusion – now what do you do?

You receive a distribution –

am I taxed again?

/ / 3

OVERVIEW

• Section 959

General Operating Rules

Consequences of PTI Distributions

Successor Rules

• Proposed Regulations

• Section 986(c)

SECTION 959

/ / 5

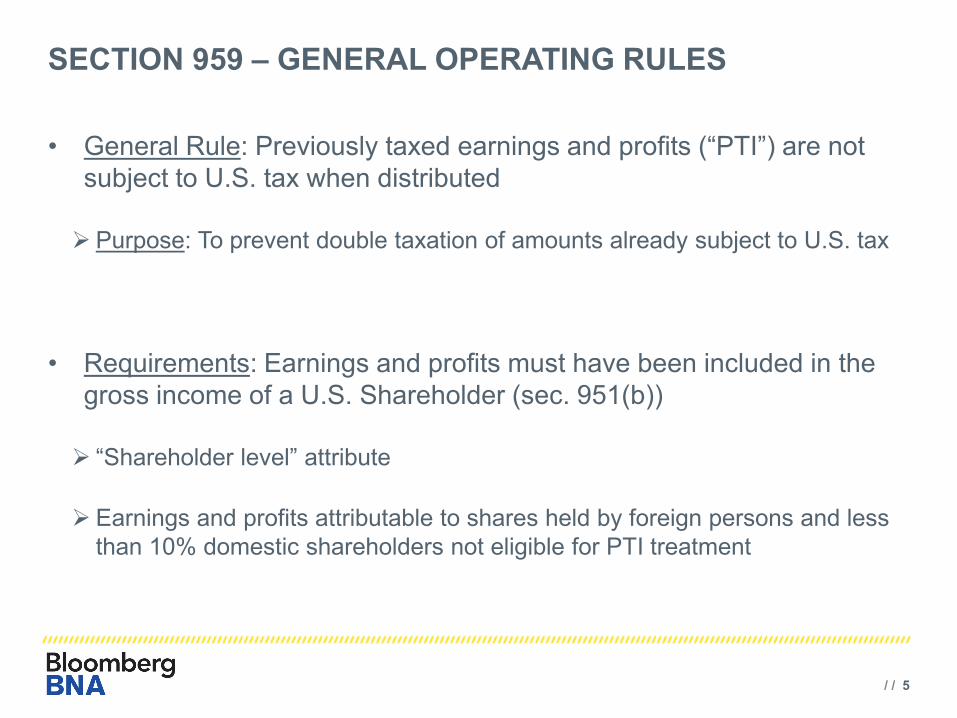

SECTION 959 – GENERAL OPERATING RULES

• General Rule: Previously taxed earnings and profits (“PTI”) are not subject to U.S. tax when distributed

Purpose: To prevent double taxation of amounts already subject to U.S. tax

• Requirements: Earnings and profits must have been included in the gross income of a U.S. Shareholder (sec. 951(b))

“Shareholder level” attribute

Earnings and profits attributable to shares held by foreign persons and less than 10% domestic shareholders not eligible for PTI treatment

/ / 6

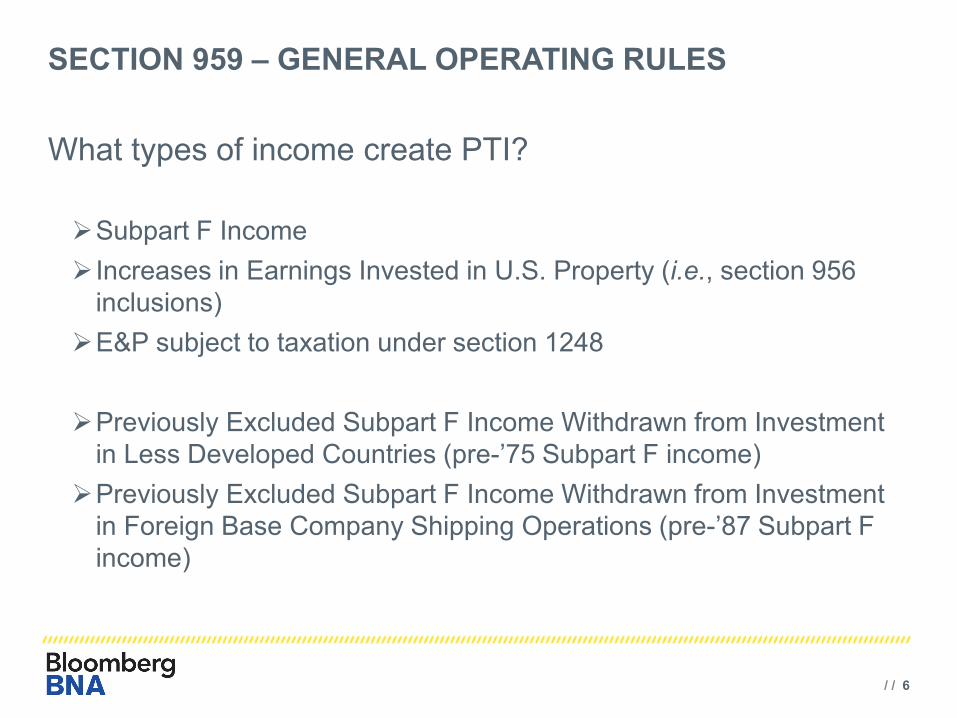

SECTION 959 – GENERAL OPERATING RULES

What types of income create PTI? Subpart F Income Increases in Earnings Invested in U.S. Property (i.e., section 956

inclusions) E&P subject to taxation under section 1248

Previously Excluded Subpart F Income Withdrawn from Investment

in Less Developed Countries (pre-’75 Subpart F income) Previously Excluded Subpart F Income Withdrawn from Investment

in Foreign Base Company Shipping Operations (pre-’87 Subpart F income)

/ / 7

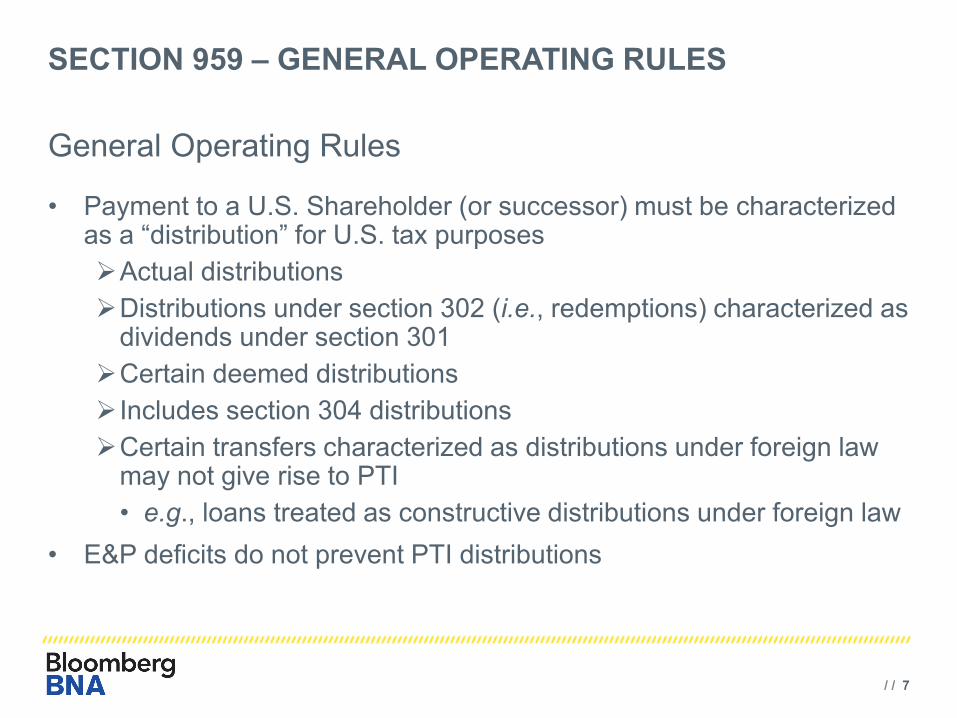

SECTION 959 – GENERAL OPERATING RULES

General Operating Rules • Payment to a U.S. Shareholder (or successor) must be characterized

as a “distribution” for U.S. tax purposes Actual distributions Distributions under section 302 (i.e., redemptions) characterized as

dividends under section 301 Certain deemed distributions Includes section 304 distributions Certain transfers characterized as distributions under foreign law

may not give rise to PTI • e.g., loans treated as constructive distributions under foreign law

• E&P deficits do not prevent PTI distributions

/ / 8

SECTION 959

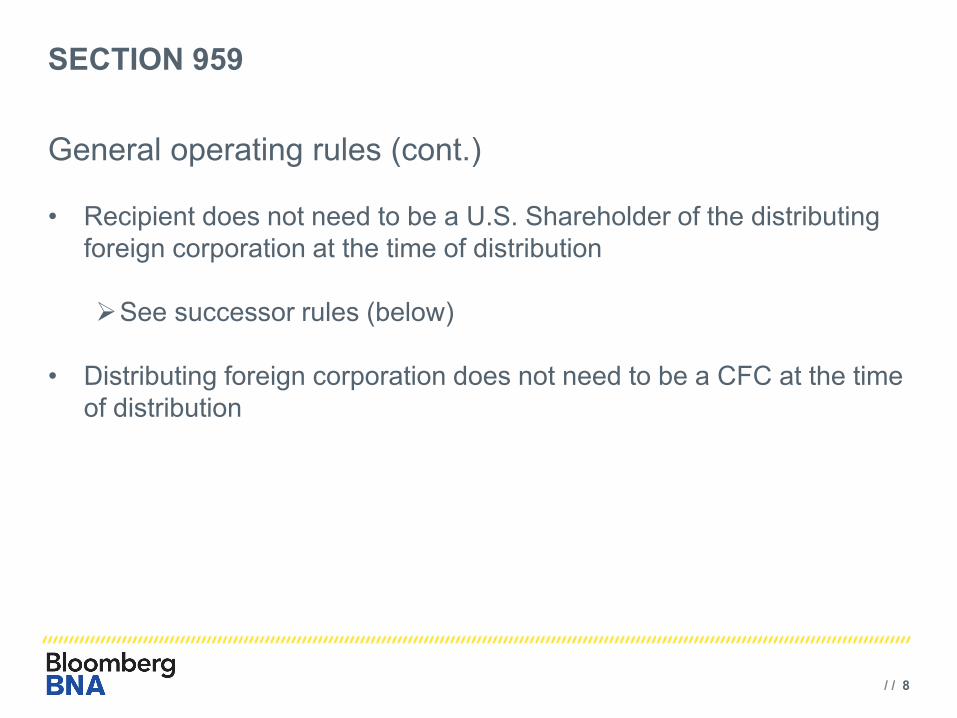

General operating rules (cont.)

• Recipient does not need to be a U.S. Shareholder of the distributing foreign corporation at the time of distribution

See successor rules (below)

• Distributing foreign corporation does not need to be a CFC at the time of distribution

/ / 9

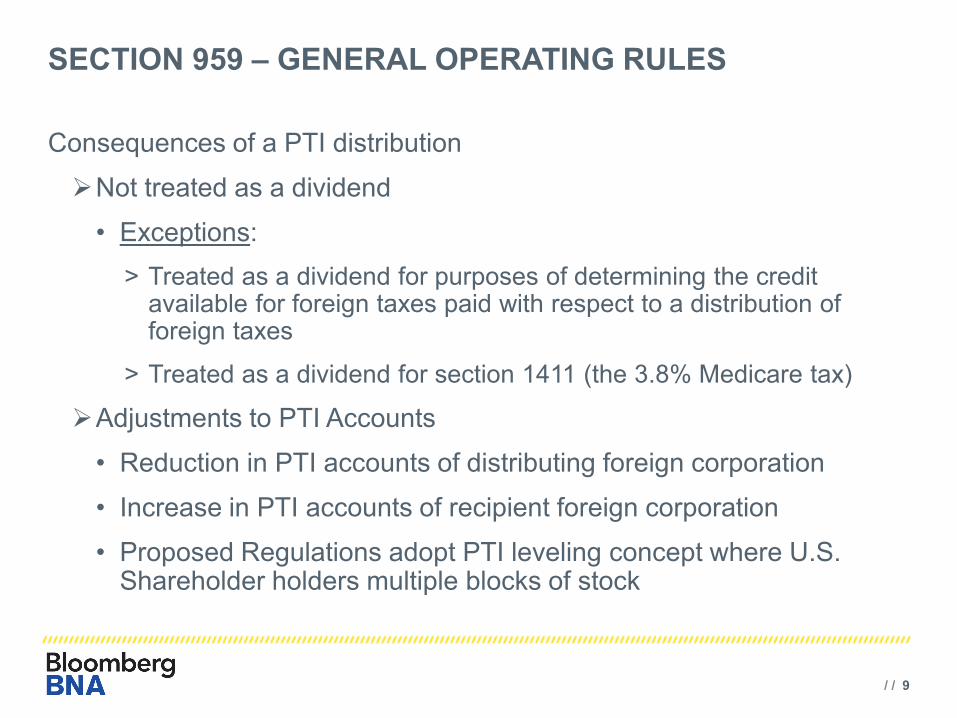

SECTION 959 – GENERAL OPERATING RULES

Consequences of a PTI distribution

Not treated as a dividend

• Exceptions: > Treated as a dividend for purposes of determining the credit

available for foreign taxes paid with respect to a distribution of foreign taxes

> Treated as a dividend for section 1411 (the 3.8% Medicare tax)

Adjustments to PTI Accounts

• Reduction in PTI accounts of distributing foreign corporation

• Increase in PTI accounts of recipient foreign corporation

• Proposed Regulations adopt PTI leveling concept where U.S. Shareholder holders multiple blocks of stock

/ / 10

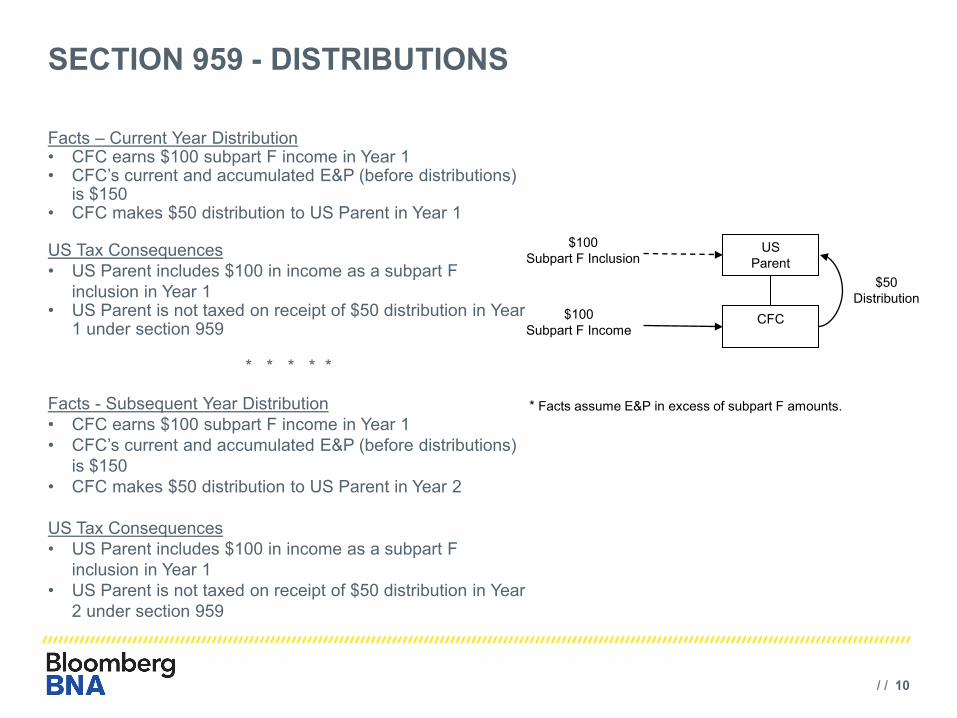

SECTION 959 - DISTRIBUTIONS

Facts – Current Year Distribution • CFC earns $100 subpart F income in Year 1 • CFC’s current and accumulated E&P (before distributions)

is $150 • CFC makes $50 distribution to US Parent in Year 1 US Tax Consequences • US Parent includes $100 in income as a subpart F

inclusion in Year 1 • US Parent is not taxed on receipt of $50 distribution in Year

1 under section 959

* * * * * Facts - Subsequent Year Distribution • CFC earns $100 subpart F income in Year 1 • CFC’s current and accumulated E&P (before distributions)

is $150 • CFC makes $50 distribution to US Parent in Year 2 US Tax Consequences • US Parent includes $100 in income as a subpart F

inclusion in Year 1 • US Parent is not taxed on receipt of $50 distribution in Year

2 under section 959

US Parent

CFC

$100 Subpart F Income

$100 Subpart F Inclusion

$50 Distribution

* Facts assume E&P in excess of subpart F amounts.

/ / 11

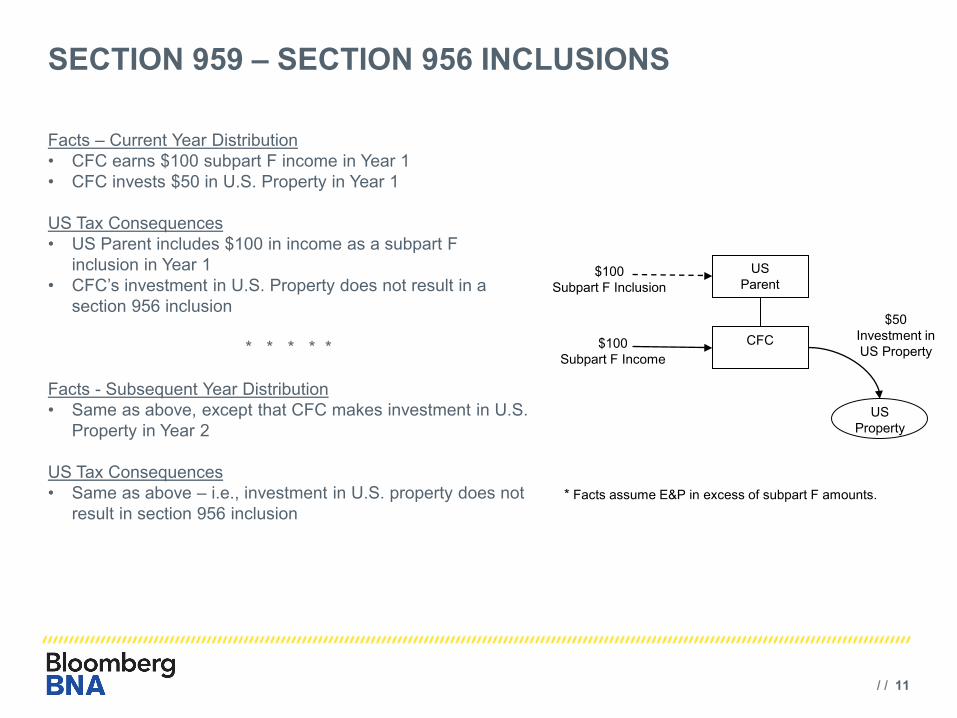

SECTION 959 – SECTION 956 INCLUSIONS

Facts – Current Year Distribution • CFC earns $100 subpart F income in Year 1 • CFC invests $50 in U.S. Property in Year 1 US Tax Consequences • US Parent includes $100 in income as a subpart F

inclusion in Year 1 • CFC’s investment in U.S. Property does not result in a

section 956 inclusion

* * * * * Facts - Subsequent Year Distribution • Same as above, except that CFC makes investment in U.S.

Property in Year 2 US Tax Consequences • Same as above – i.e., investment in U.S. property does not

result in section 956 inclusion

US Parent

CFC

$50 Investment in US Property

US Property

$100 Subpart F Inclusion

$100 Subpart F Income

* Facts assume E&P in excess of subpart F amounts.

/ / 12

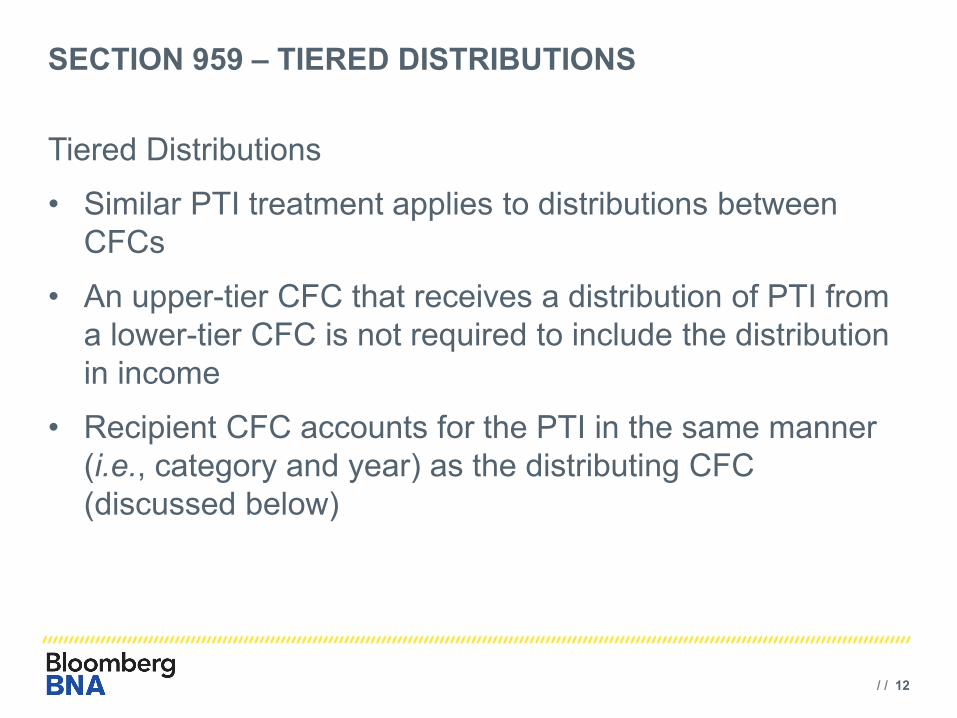

SECTION 959 – TIERED DISTRIBUTIONS

Tiered Distributions

• Similar PTI treatment applies to distributions between CFCs

• An upper-tier CFC that receives a distribution of PTI from a lower-tier CFC is not required to include the distribution in income

• Recipient CFC accounts for the PTI in the same manner (i.e., category and year) as the distributing CFC (discussed below)

/ / 13

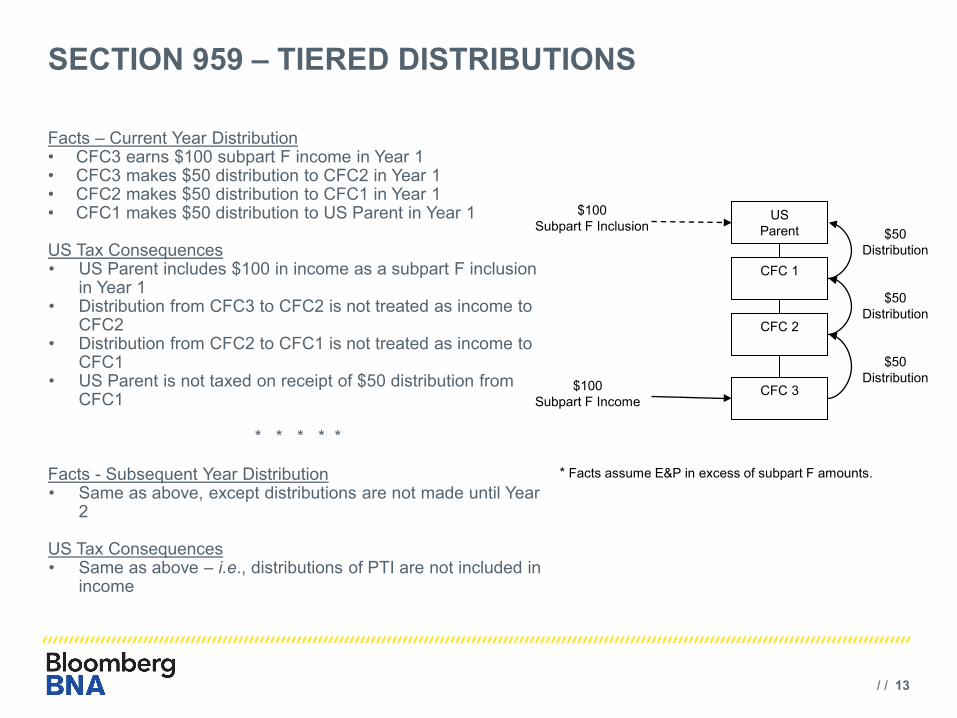

SECTION 959 – TIERED DISTRIBUTIONS

Facts – Current Year Distribution • CFC3 earns $100 subpart F income in Year 1 • CFC3 makes $50 distribution to CFC2 in Year 1 • CFC2 makes $50 distribution to CFC1 in Year 1 • CFC1 makes $50 distribution to US Parent in Year 1

US Tax Consequences • US Parent includes $100 in income as a subpart F inclusion

in Year 1 • Distribution from CFC3 to CFC2 is not treated as income to

CFC2 • Distribution from CFC2 to CFC1 is not treated as income to

CFC1 • US Parent is not taxed on receipt of $50 distribution from

CFC1

* * * * *

Facts - Subsequent Year Distribution • Same as above, except distributions are not made until Year

2

US Tax Consequences • Same as above – i.e., distributions of PTI are not included in

income

US Parent

CFC 3

CFC 2

CFC 1

$100 Subpart F Income

$100 Subpart F Inclusion $50

Distribution

$50 Distribution

$50 Distribution

* Facts assume E&P in excess of subpart F amounts.

/ / 14

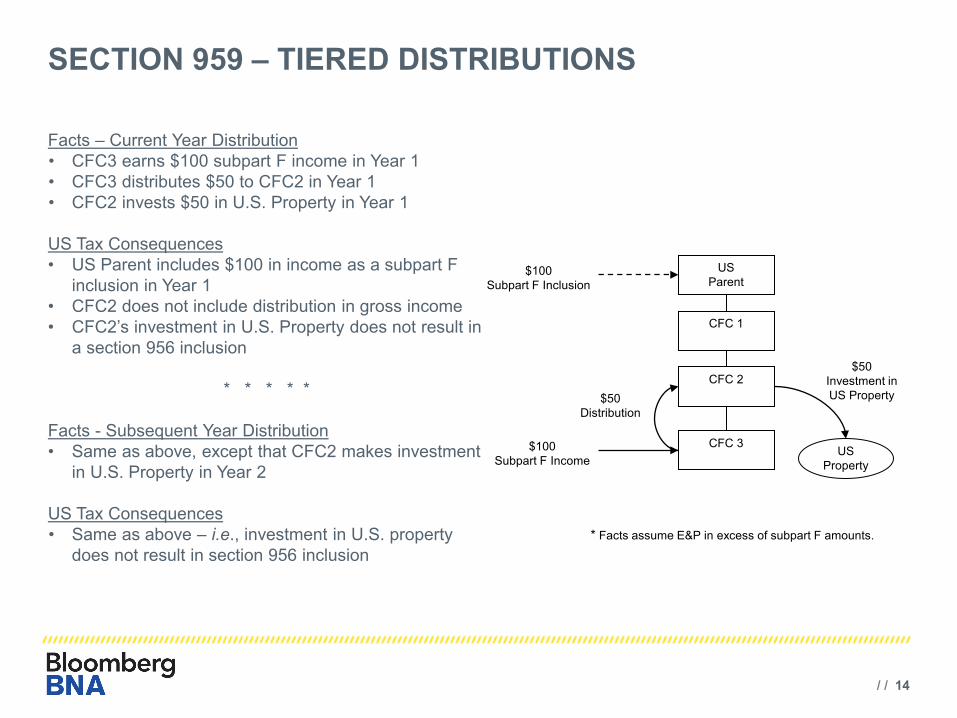

SECTION 959 – TIERED DISTRIBUTIONS

Facts – Current Year Distribution • CFC3 earns $100 subpart F income in Year 1 • CFC3 distributes $50 to CFC2 in Year 1 • CFC2 invests $50 in U.S. Property in Year 1 US Tax Consequences • US Parent includes $100 in income as a subpart F

inclusion in Year 1 • CFC2 does not include distribution in gross income • CFC2’s investment in U.S. Property does not result in

a section 956 inclusion

* * * * * Facts - Subsequent Year Distribution • Same as above, except that CFC2 makes investment

in U.S. Property in Year 2 US Tax Consequences • Same as above – i.e., investment in U.S. property

does not result in section 956 inclusion

US Parent

CFC 3

CFC 2

CFC 1

US Property

* Facts assume E&P in excess of subpart F amounts.

$100 Subpart F Inclusion

$100 Subpart F Income

$50 Distribution

$50 Investment in US Property

/ / 15

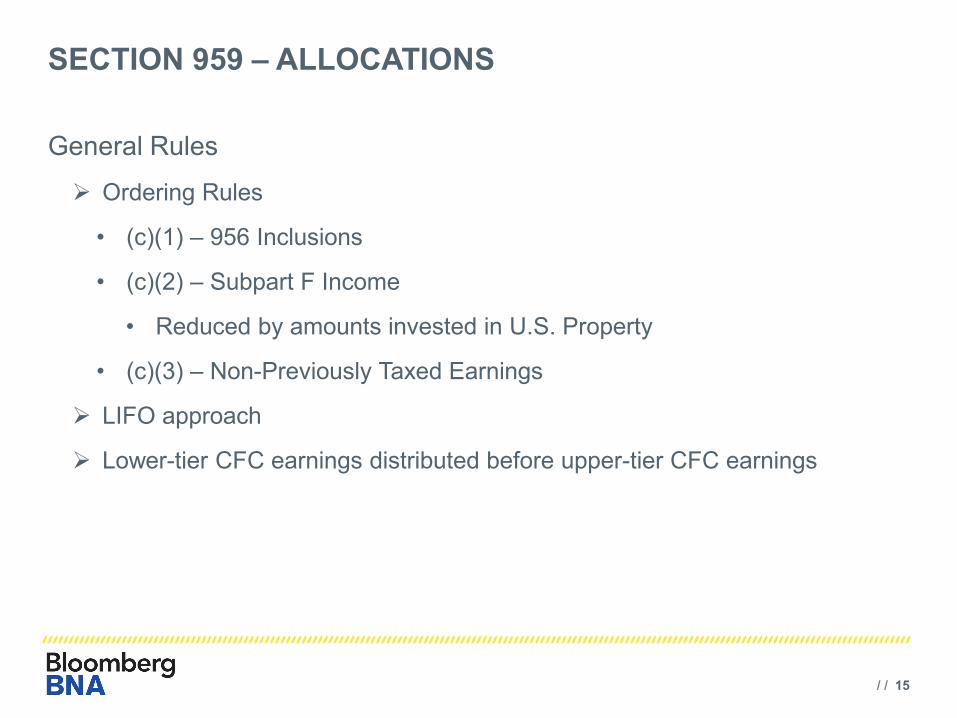

SECTION 959 – ALLOCATIONS

General Rules

Ordering Rules

• (c)(1) – 956 Inclusions

• (c)(2) – Subpart F Income

• Reduced by amounts invested in U.S. Property

• (c)(3) – Non-Previously Taxed Earnings

LIFO approach

Lower-tier CFC earnings distributed before upper-tier CFC earnings

/ / 16

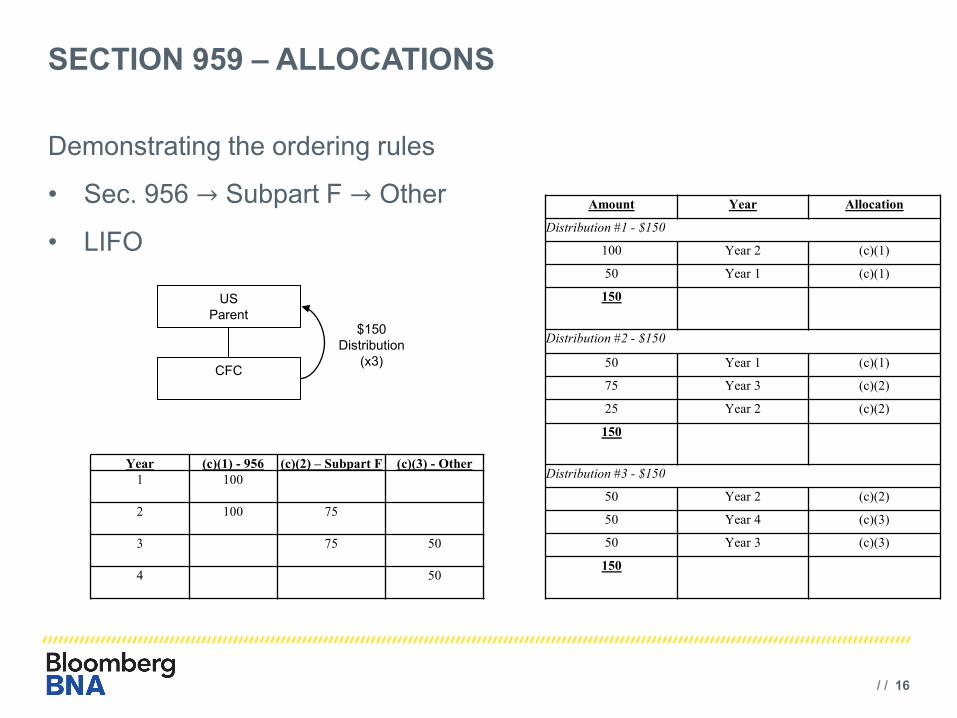

SECTION 959 – ALLOCATIONS

Year (c)(1) - 956 (c)(2) – Subpart F (c)(3) - Other 1 100

2 100 75

3 75 50

4 50

Amount Year Allocation

Distribution #1 - $150

100 Year 2 (c)(1)

50 Year 1 (c)(1)

150

Distribution #2 - $150

50 Year 1 (c)(1)

75 Year 3 (c)(2)

25 Year 2 (c)(2)

150

Distribution #3 - $150

50 Year 2 (c)(2)

50 Year 4 (c)(3)

50 Year 3 (c)(3)

150

US Parent

CFC

$150 Distribution

(x3)

Demonstrating the ordering rules

• Sec. 956 → Subpart F → Other

• LIFO

/ / 17

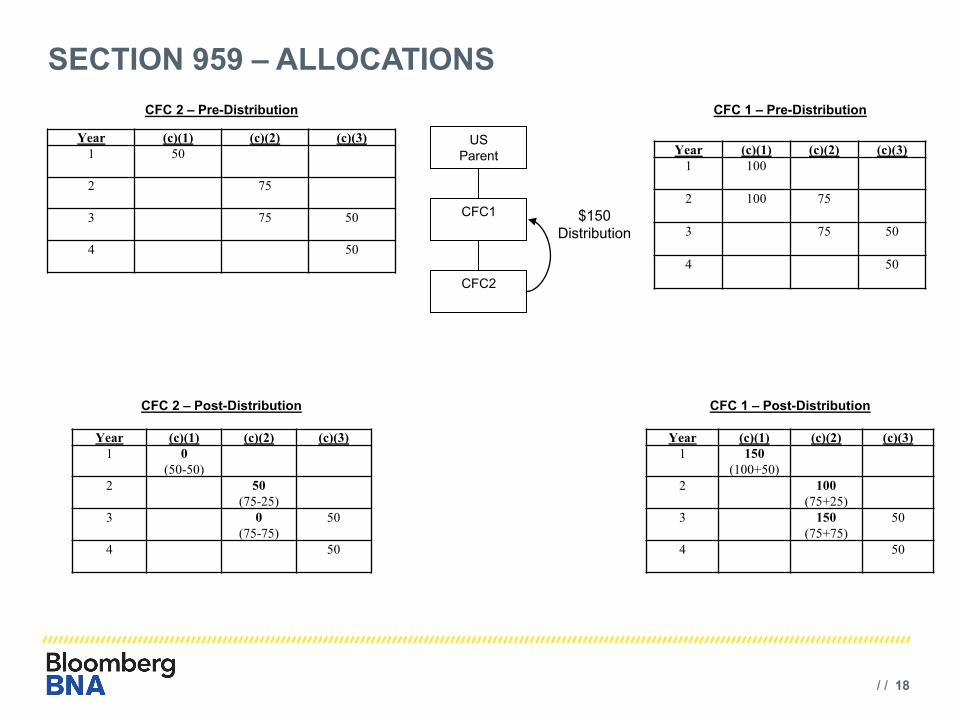

SECTION 959 – ALLOCATIONS

Distributions between CFCs

Allocated to the same category of the distributing CFC

Allocated to the same year in which incurred by the distributing CFC

/ / 18

SECTION 959 – ALLOCATIONS

Year (c)(1) (c)(2) (c)(3) 1 50

2 75

3 75 50

4 50

Year (c)(1) (c)(2) (c)(3) 1 100

2 100 75

3 75 50

4 50

Year (c)(1) (c)(2) (c)(3) 1 0

(50-50) 2 50

(75-25) 3 0

(75-75) 50

4 50

Year (c)(1) (c)(2) (c)(3) 1 150

(100+50) 2 100

(75+25) 3 150

(75+75) 50

4 50

US Parent

CFC1

$150 Distribution

CFC2

CFC 2 – Pre-Distribution CFC 1 – Pre-Distribution

CFC 2 – Post-Distribution CFC 1 – Post-Distribution

/ / 19

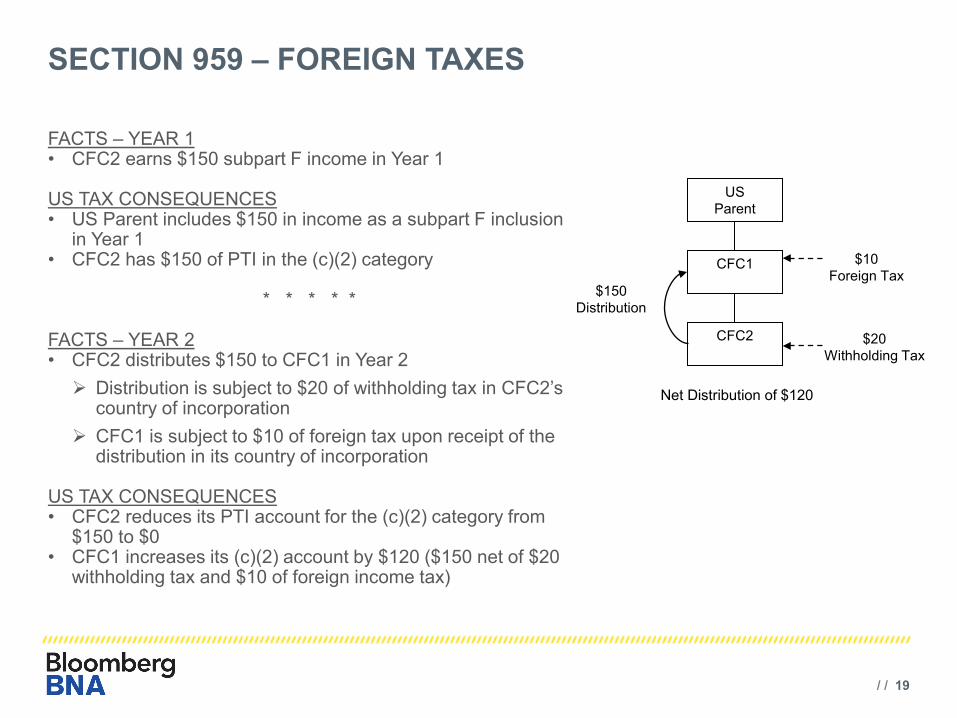

SECTION 959 – FOREIGN TAXES

FACTS – YEAR 1 • CFC2 earns $150 subpart F income in Year 1 US TAX CONSEQUENCES • US Parent includes $150 in income as a subpart F inclusion

in Year 1 • CFC2 has $150 of PTI in the (c)(2) category

* * * * * FACTS – YEAR 2 • CFC2 distributes $150 to CFC1 in Year 2 Distribution is subject to $20 of withholding tax in CFC2’s

country of incorporation CFC1 is subject to $10 of foreign tax upon receipt of the

distribution in its country of incorporation US TAX CONSEQUENCES • CFC2 reduces its PTI account for the (c)(2) category from

$150 to $0 • CFC1 increases its (c)(2) account by $120 ($150 net of $20

withholding tax and $10 of foreign income tax)

US Parent

CFC1

$150 Distribution

CFC2

$10 Foreign Tax

$20 Withholding Tax

Net Distribution of $120

/ / 20

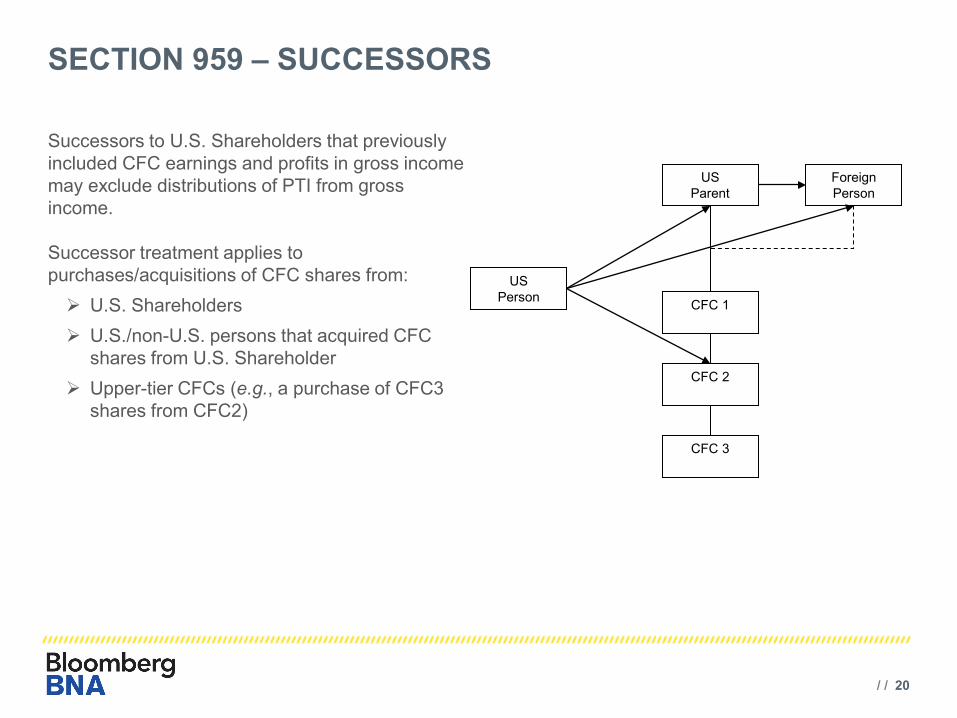

SECTION 959 – SUCCESSORS

Successors to U.S. Shareholders that previously included CFC earnings and profits in gross income may exclude distributions of PTI from gross income. Successor treatment applies to purchases/acquisitions of CFC shares from: U.S. Shareholders U.S./non-U.S. persons that acquired CFC

shares from U.S. Shareholder Upper-tier CFCs (e.g., a purchase of CFC3

shares from CFC2)

US Parent

CFC 1

CFC 2

CFC 3

Foreign Person

US Person

/ / 21

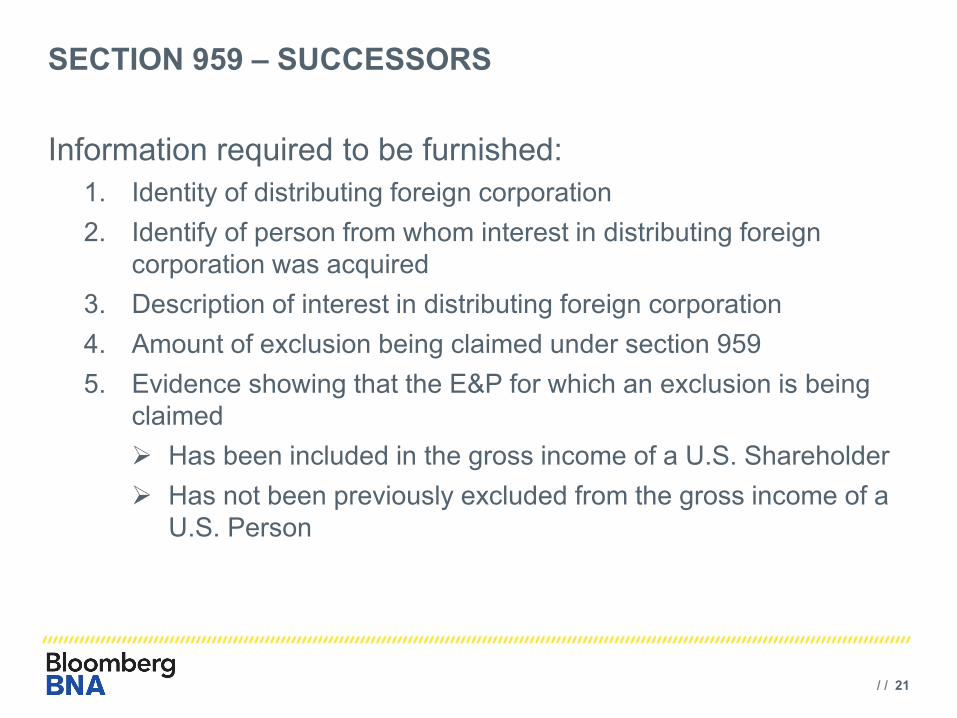

SECTION 959 – SUCCESSORS

Information required to be furnished: 1. Identity of distributing foreign corporation 2. Identify of person from whom interest in distributing foreign

corporation was acquired 3. Description of interest in distributing foreign corporation 4. Amount of exclusion being claimed under section 959 5. Evidence showing that the E&P for which an exclusion is being

claimed Has been included in the gross income of a U.S. Shareholder Has not been previously excluded from the gross income of a

U.S. Person

PROPOSED REGULATIONS (2006)

/ / 23

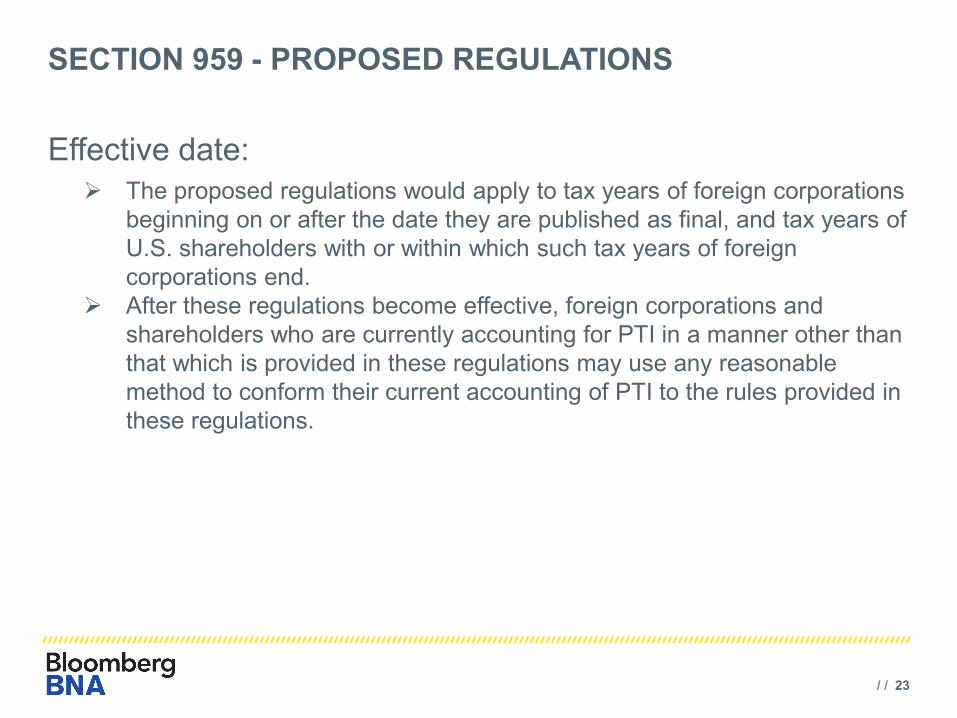

SECTION 959 - PROPOSED REGULATIONS

Effective date: The proposed regulations would apply to tax years of foreign corporations

beginning on or after the date they are published as final, and tax years of U.S. shareholders with or within which such tax years of foreign corporations end.

After these regulations become effective, foreign corporations and shareholders who are currently accounting for PTI in a manner other than that which is provided in these regulations may use any reasonable method to conform their current accounting of PTI to the rules provided in these regulations.

/ / 24

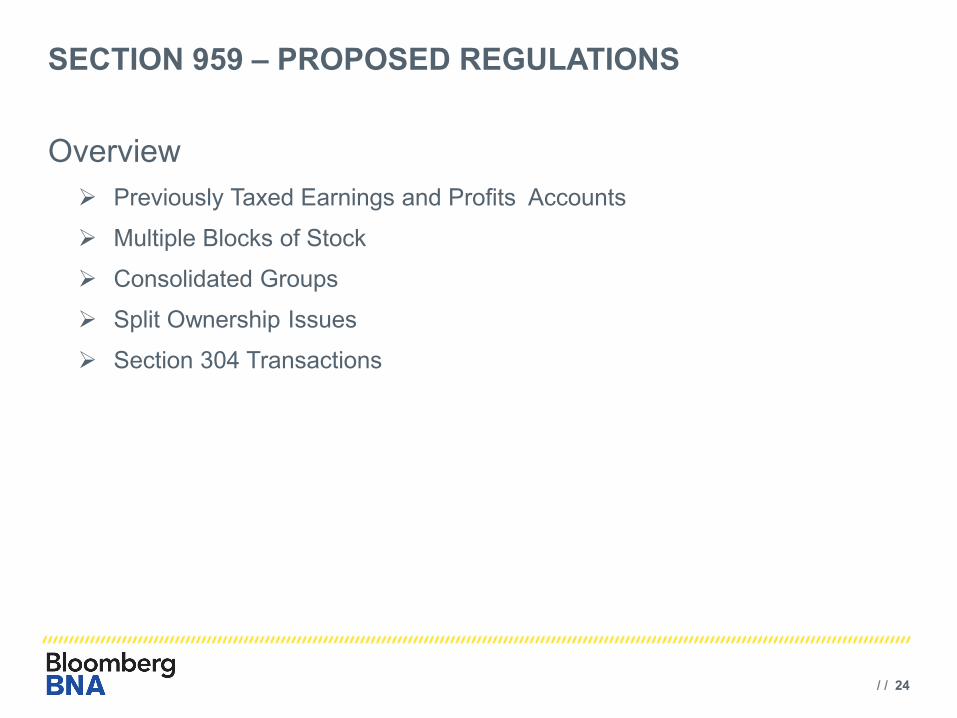

SECTION 959 – PROPOSED REGULATIONS

Overview Previously Taxed Earnings and Profits Accounts

Multiple Blocks of Stock

Consolidated Groups

Split Ownership Issues

Section 304 Transactions

/ / 25

SECTION 959 - PROPOSED REGULATIONS

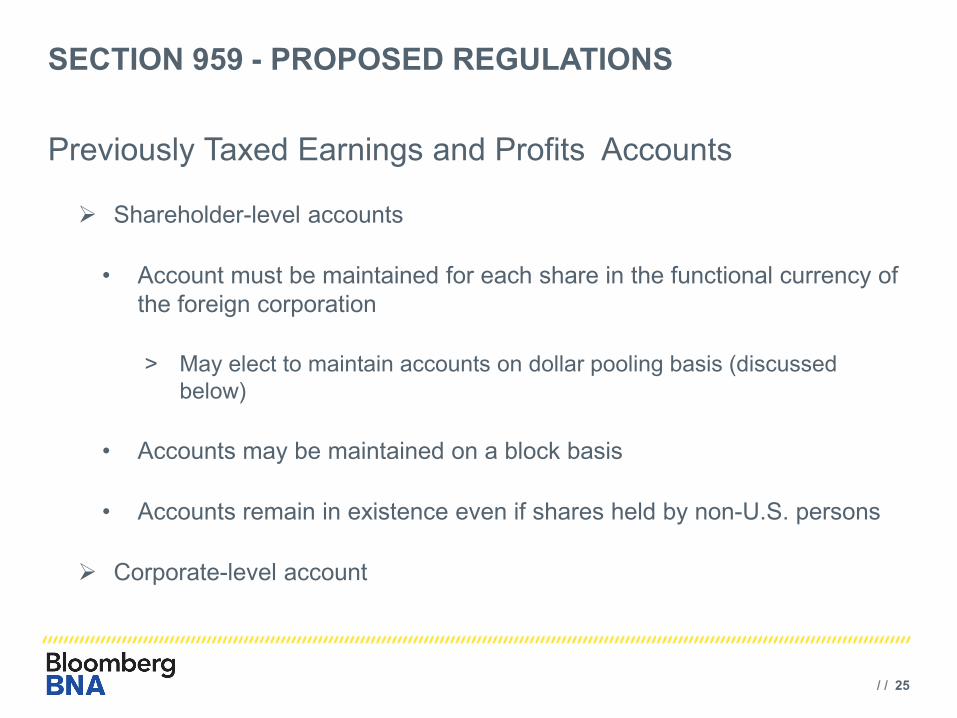

Previously Taxed Earnings and Profits Accounts

Shareholder-level accounts

• Account must be maintained for each share in the functional currency of the foreign corporation

> May elect to maintain accounts on dollar pooling basis (discussed below)

• Accounts may be maintained on a block basis

• Accounts remain in existence even if shares held by non-U.S. persons

Corporate-level account

/ / 26

SECTION 959 - PROPOSED REGULATIONS

Previously Taxed Earnings and Profits Accounts (cont.)

Foreign taxes paid with respect to distributions of PTI maintained in account separate from post-1986 foreign income taxes

• Foreign taxes deemed paid when PTI distributed

/ / 27

SECTION 959 - PROPOSED REGULATIONS

Multiple Blocks of Stock

• Premise:

A U.S. Shareholder holds multiple blocks of CFC stock with varying PTI account balances

CFC makes a distribution which exceeds the PTI balance for some shares (low-PTI shares), but not for others (high-PTI shares)

• Proposed Regulations

PTI from high-PTI shares reallocated to low-PTI shares

• Compare with Unified Loss Rules in consolidated return regulations (basis leveling)

/ / 28

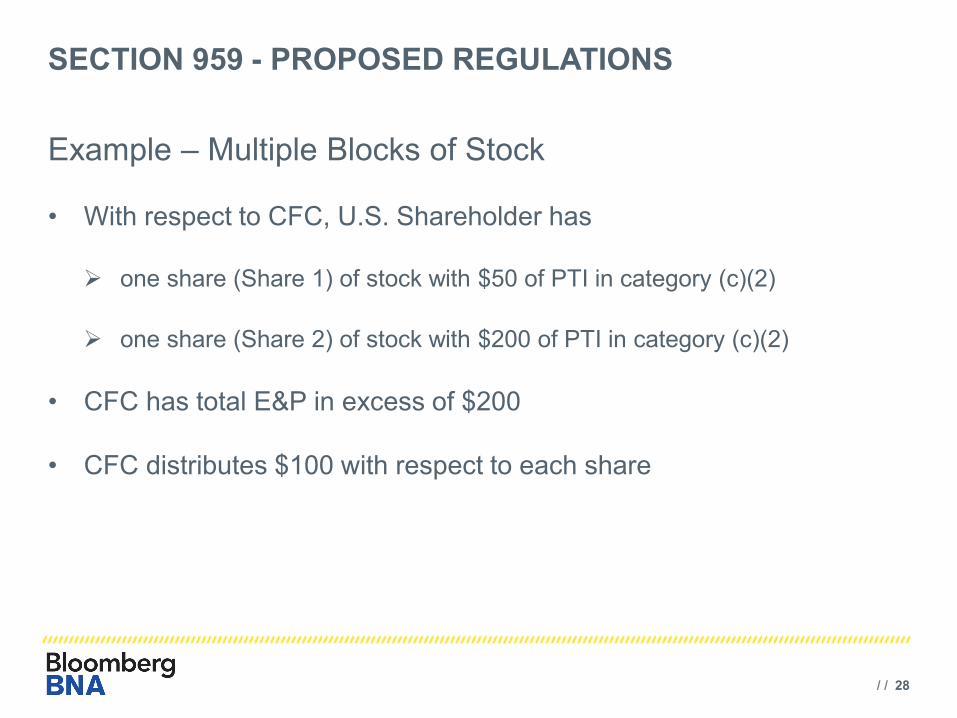

SECTION 959 - PROPOSED REGULATIONS

Example – Multiple Blocks of Stock

• With respect to CFC, U.S. Shareholder has

one share (Share 1) of stock with $50 of PTI in category (c)(2)

one share (Share 2) of stock with $200 of PTI in category (c)(2)

• CFC has total E&P in excess of $200

• CFC distributes $100 with respect to each share

/ / 29

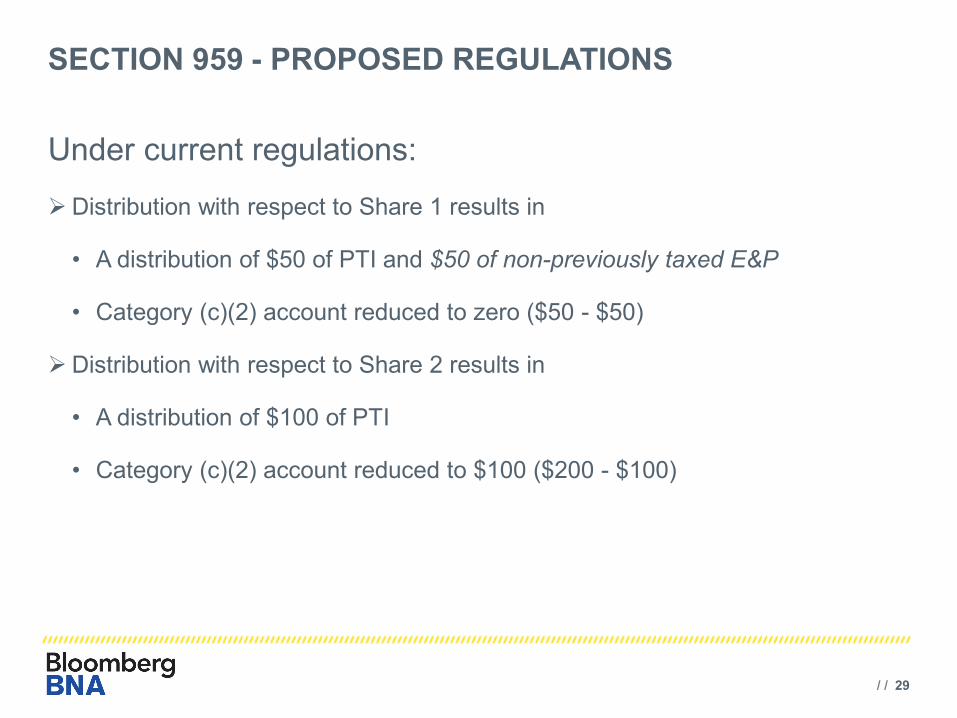

SECTION 959 - PROPOSED REGULATIONS

Under current regulations:

Distribution with respect to Share 1 results in

• A distribution of $50 of PTI and $50 of non-previously taxed E&P

• Category (c)(2) account reduced to zero ($50 - $50)

Distribution with respect to Share 2 results in

• A distribution of $100 of PTI

• Category (c)(2) account reduced to $100 ($200 - $100)

/ / 30

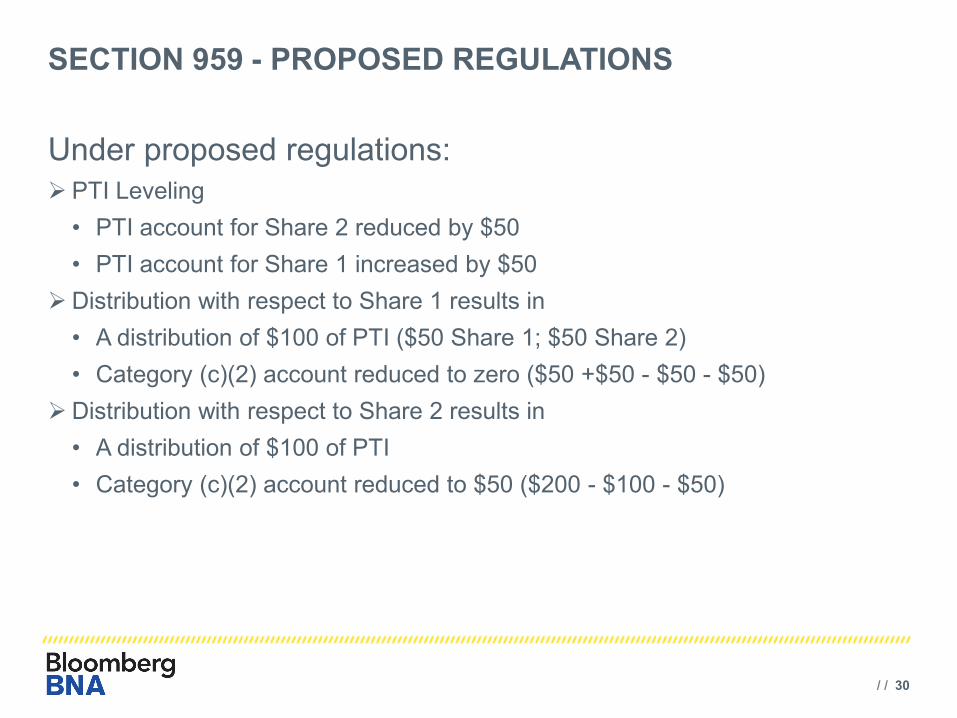

SECTION 959 - PROPOSED REGULATIONS

Under proposed regulations: PTI Leveling • PTI account for Share 2 reduced by $50 • PTI account for Share 1 increased by $50

Distribution with respect to Share 1 results in • A distribution of $100 of PTI ($50 Share 1; $50 Share 2) • Category (c)(2) account reduced to zero ($50 +$50 - $50 - $50)

Distribution with respect to Share 2 results in • A distribution of $100 of PTI • Category (c)(2) account reduced to $50 ($200 - $100 - $50)

/ / 31

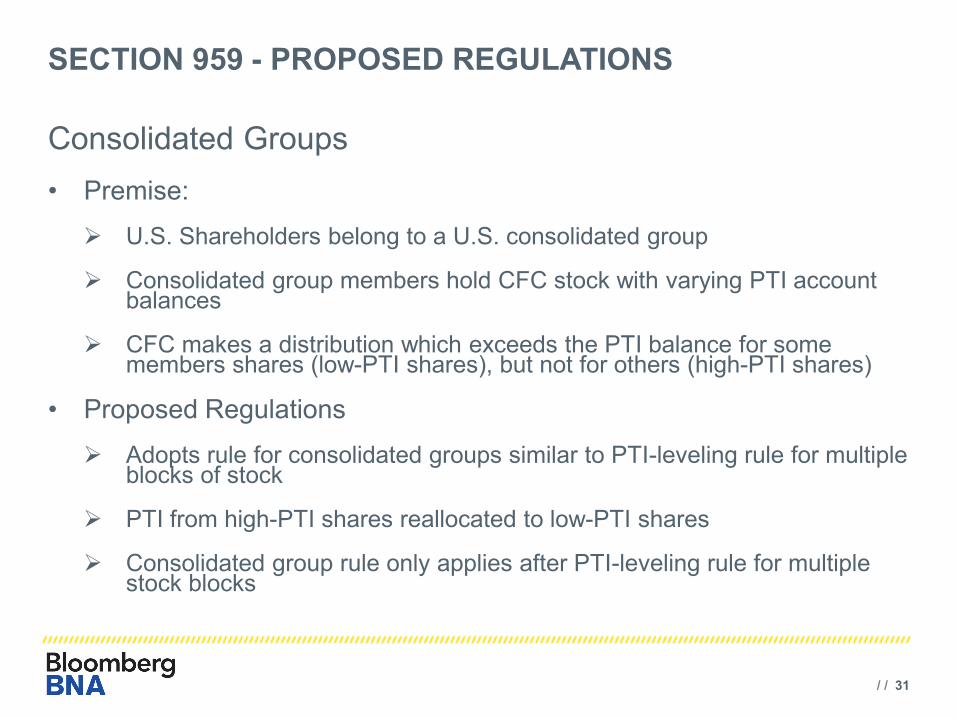

SECTION 959 - PROPOSED REGULATIONS

Consolidated Groups • Premise:

U.S. Shareholders belong to a U.S. consolidated group

Consolidated group members hold CFC stock with varying PTI account balances

CFC makes a distribution which exceeds the PTI balance for some members shares (low-PTI shares), but not for others (high-PTI shares)

• Proposed Regulations

Adopts rule for consolidated groups similar to PTI-leveling rule for multiple blocks of stock

PTI from high-PTI shares reallocated to low-PTI shares

Consolidated group rule only applies after PTI-leveling rule for multiple stock blocks

/ / 32

SECTION 959 - PROPOSED REGULATIONS

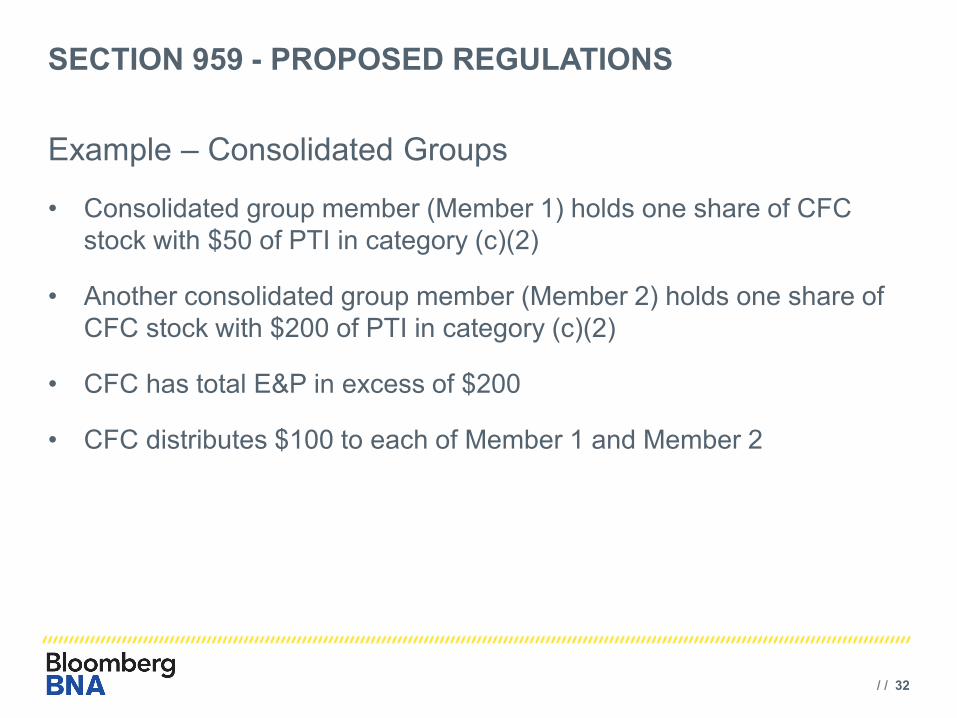

Example – Consolidated Groups

• Consolidated group member (Member 1) holds one share of CFC stock with $50 of PTI in category (c)(2)

• Another consolidated group member (Member 2) holds one share of CFC stock with $200 of PTI in category (c)(2)

• CFC has total E&P in excess of $200

• CFC distributes $100 to each of Member 1 and Member 2

/ / 33

SECTION 959 - PROPOSED REGULATIONS

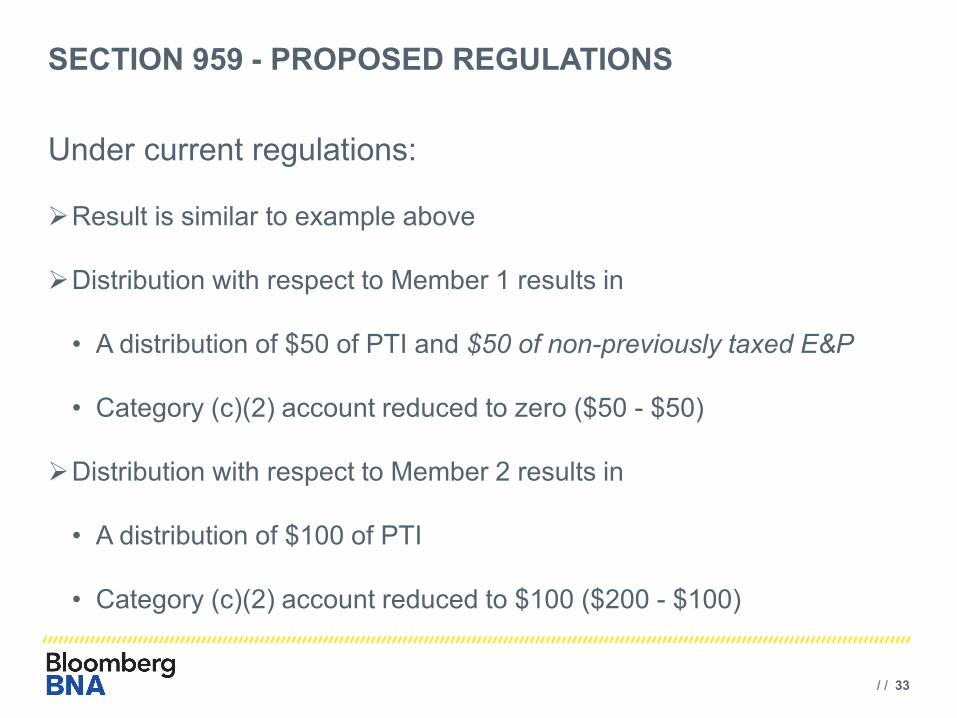

Under current regulations:

Result is similar to example above

Distribution with respect to Member 1 results in

• A distribution of $50 of PTI and $50 of non-previously taxed E&P

• Category (c)(2) account reduced to zero ($50 - $50)

Distribution with respect to Member 2 results in

• A distribution of $100 of PTI

• Category (c)(2) account reduced to $100 ($200 - $100)

/ / 34

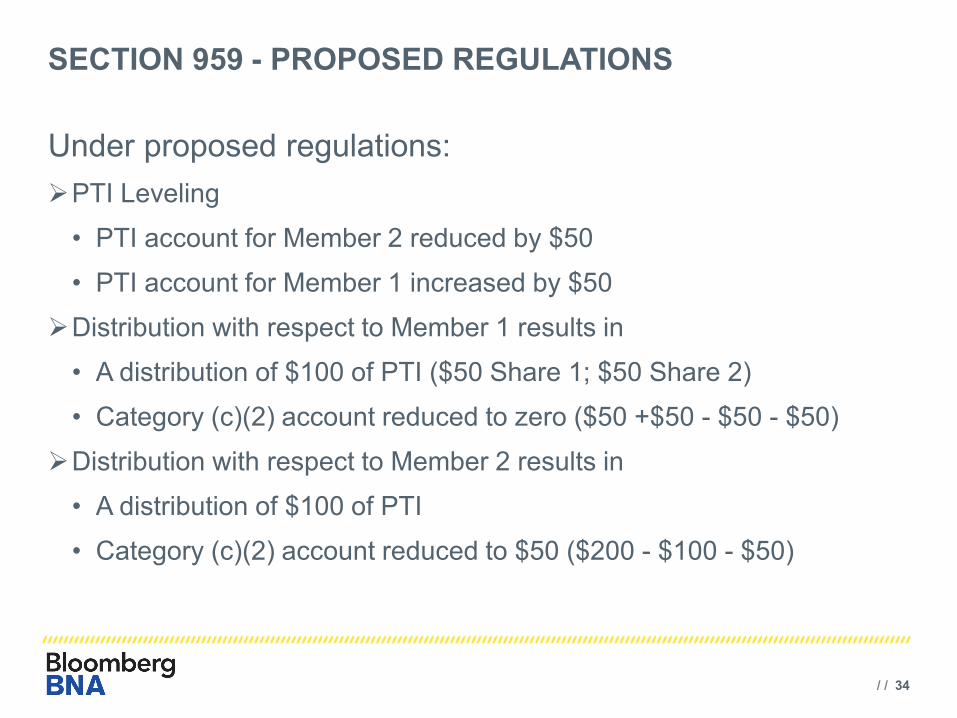

SECTION 959 - PROPOSED REGULATIONS

Under proposed regulations: PTI Leveling

• PTI account for Member 2 reduced by $50

• PTI account for Member 1 increased by $50

Distribution with respect to Member 1 results in

• A distribution of $100 of PTI ($50 Share 1; $50 Share 2)

• Category (c)(2) account reduced to zero ($50 +$50 - $50 - $50)

Distribution with respect to Member 2 results in

• A distribution of $100 of PTI

• Category (c)(2) account reduced to $50 ($200 - $100 - $50)

/ / 35

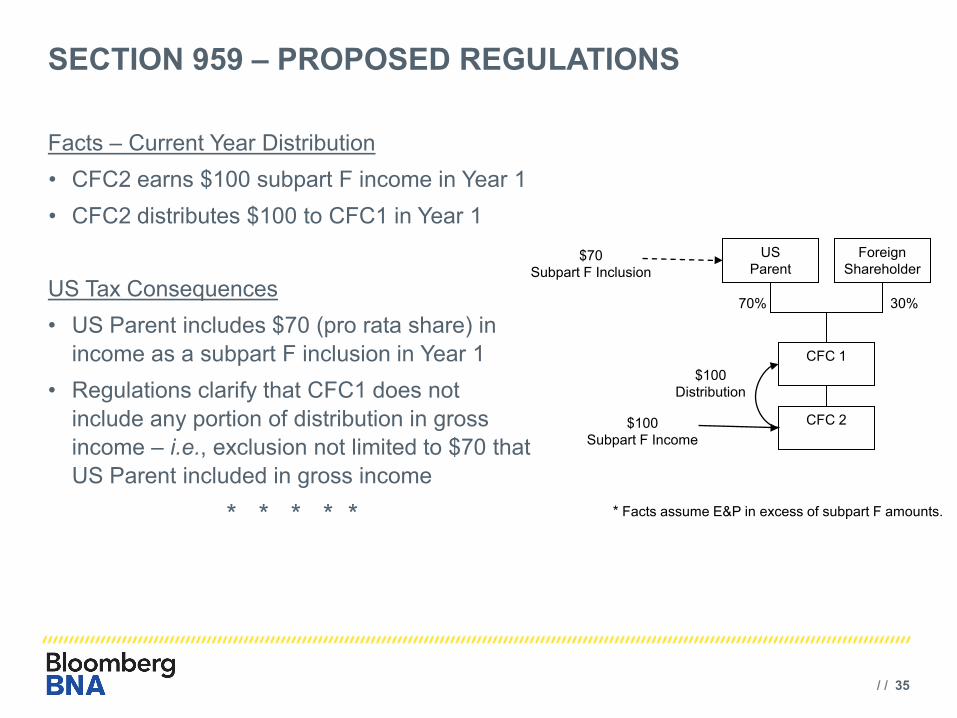

SECTION 959 – PROPOSED REGULATIONS

Facts – Current Year Distribution • CFC2 earns $100 subpart F income in Year 1 • CFC2 distributes $100 to CFC1 in Year 1 US Tax Consequences • US Parent includes $70 (pro rata share) in

income as a subpart F inclusion in Year 1 • Regulations clarify that CFC1 does not

include any portion of distribution in gross income – i.e., exclusion not limited to $70 that US Parent included in gross income

* * * * *

CFC 2

CFC 1

Foreign Shareholder

$100 Subpart F Income

$100 Distribution

US Parent

$70 Subpart F Inclusion

70% 30%

* Facts assume E&P in excess of subpart F amounts.

/ / 36

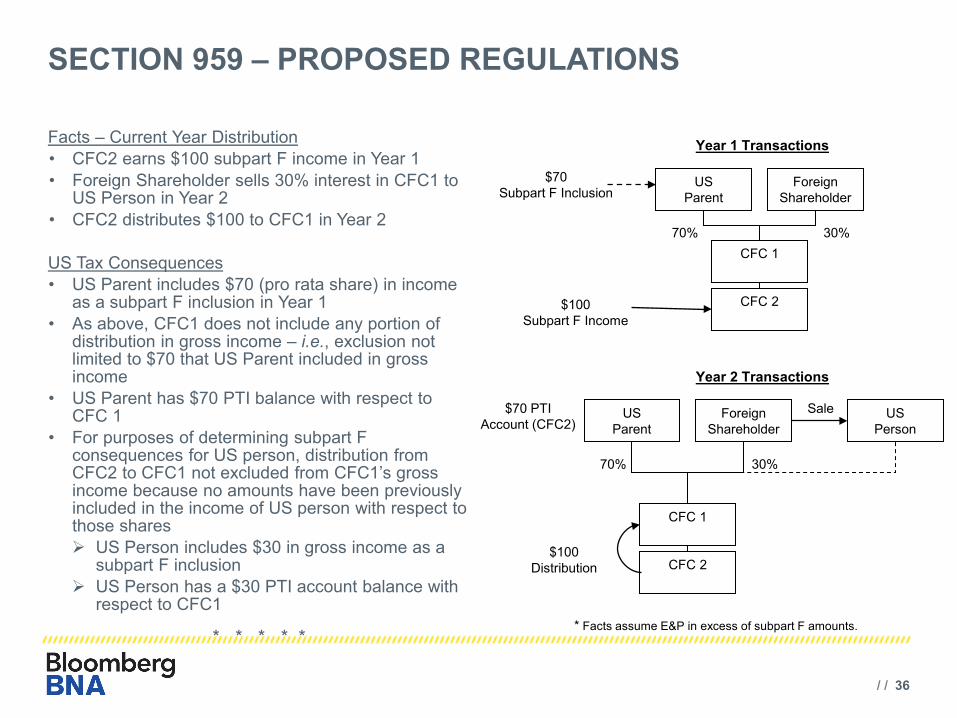

SECTION 959 – PROPOSED REGULATIONS

Facts – Current Year Distribution • CFC2 earns $100 subpart F income in Year 1 • Foreign Shareholder sells 30% interest in CFC1 to

US Person in Year 2 • CFC2 distributes $100 to CFC1 in Year 2

US Tax Consequences • US Parent includes $70 (pro rata share) in income

as a subpart F inclusion in Year 1 • As above, CFC1 does not include any portion of

distribution in gross income – i.e., exclusion not limited to $70 that US Parent included in gross income

• US Parent has $70 PTI balance with respect to CFC 1

• For purposes of determining subpart F consequences for US person, distribution from CFC2 to CFC1 not excluded from CFC1’s gross income because no amounts have been previously included in the income of US person with respect to those shares US Person includes $30 in gross income as a

subpart F inclusion US Person has a $30 PTI account balance with

respect to CFC1

* * * * *

CFC 2

CFC 1

Foreign Shareholder

$100 Subpart F Income

$100 Distribution

US Parent

$70 Subpart F Inclusion

70% 30%

Year 1 Transactions

CFC 2

CFC 1

Foreign Shareholder

US Parent

$70 PTI Account (CFC2)

70% 30%

Year 2 Transactions

US Person

Sale

* Facts assume E&P in excess of subpart F amounts.

/ / 37

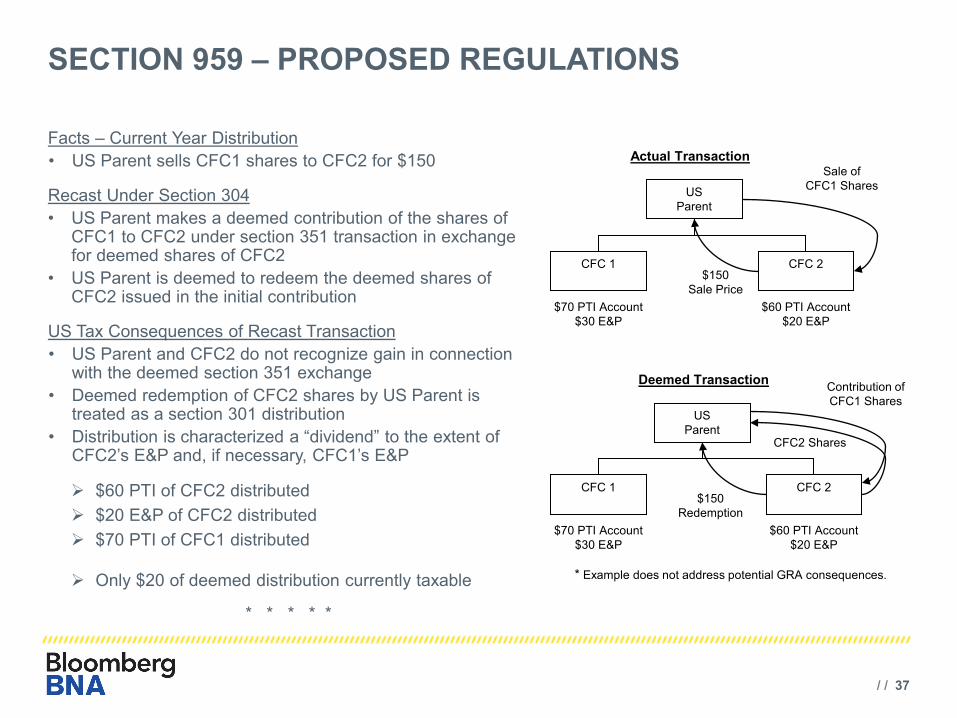

SECTION 959 – PROPOSED REGULATIONS

Facts – Current Year Distribution • US Parent sells CFC1 shares to CFC2 for $150

Recast Under Section 304 • US Parent makes a deemed contribution of the shares of

CFC1 to CFC2 under section 351 transaction in exchange for deemed shares of CFC2

• US Parent is deemed to redeem the deemed shares of CFC2 issued in the initial contribution

US Tax Consequences of Recast Transaction • US Parent and CFC2 do not recognize gain in connection

with the deemed section 351 exchange • Deemed redemption of CFC2 shares by US Parent is

treated as a section 301 distribution • Distribution is characterized a “dividend” to the extent of

CFC2’s E&P and, if necessary, CFC1’s E&P $60 PTI of CFC2 distributed $20 E&P of CFC2 distributed $70 PTI of CFC1 distributed

Only $20 of deemed distribution currently taxable

* * * * *

CFC 1 $150

Sale Price

Sale of CFC1 Shares US

Parent

CFC 2

$70 PTI Account $30 E&P

$60 PTI Account $20 E&P

Actual Transaction

CFC 1 $150

Redemption

Contribution of CFC1 Shares

US Parent

CFC 2

$70 PTI Account $30 E&P

$60 PTI Account $20 E&P

Deemed Transaction

CFC2 Shares

* Example does not address potential GRA consequences.

SECTION 986(c)

/ / 39

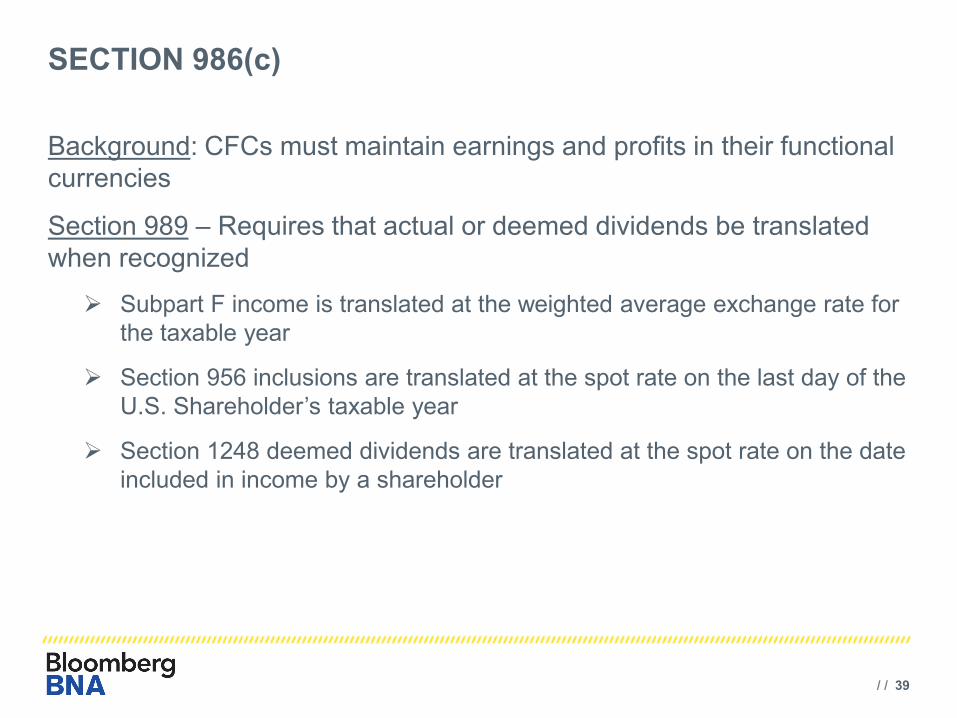

SECTION 986(c)

Background: CFCs must maintain earnings and profits in their functional currencies

Section 989 – Requires that actual or deemed dividends be translated when recognized

Subpart F income is translated at the weighted average exchange rate for the taxable year

Section 956 inclusions are translated at the spot rate on the last day of the U.S. Shareholder’s taxable year

Section 1248 deemed dividends are translated at the spot rate on the date included in income by a shareholder

/ / 40

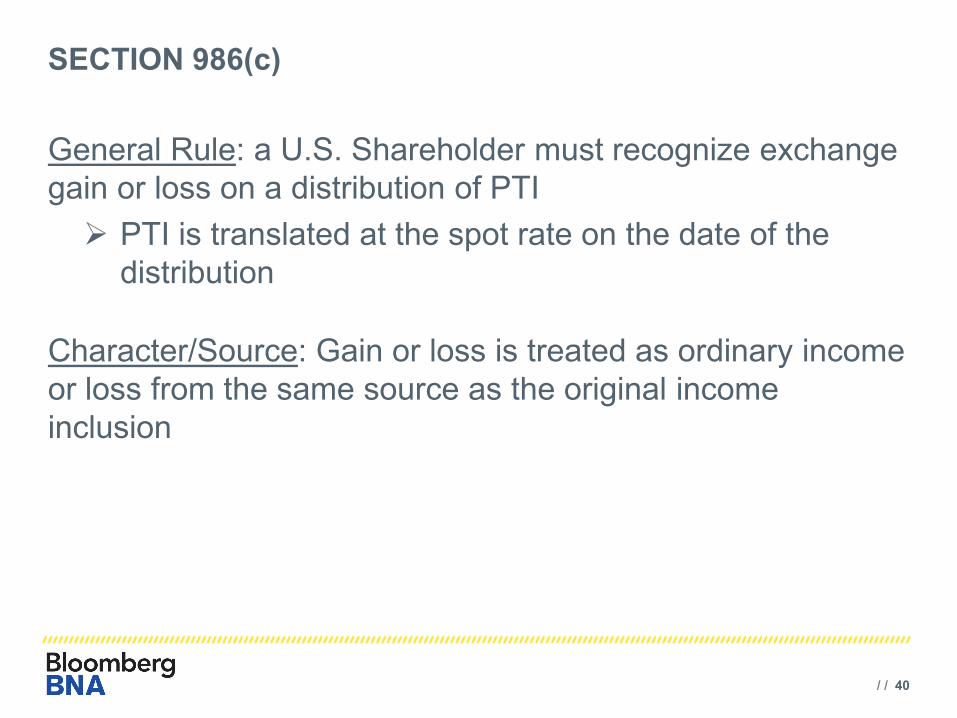

SECTION 986(c)

General Rule: a U.S. Shareholder must recognize exchange gain or loss on a distribution of PTI PTI is translated at the spot rate on the date of the

distribution Character/Source: Gain or loss is treated as ordinary income or loss from the same source as the original income inclusion

/ / 41

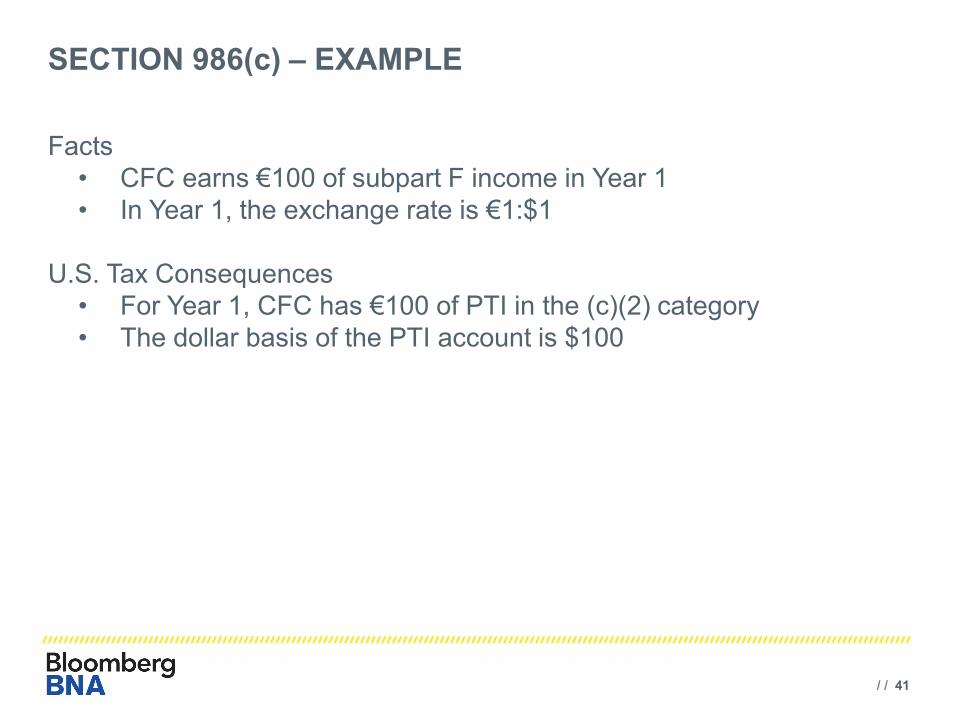

SECTION 986(c) – EXAMPLE

Facts • CFC earns €100 of subpart F income in Year 1 • In Year 1, the exchange rate is €1:$1

U.S. Tax Consequences • For Year 1, CFC has €100 of PTI in the (c)(2) category • The dollar basis of the PTI account is $100

/ / 42

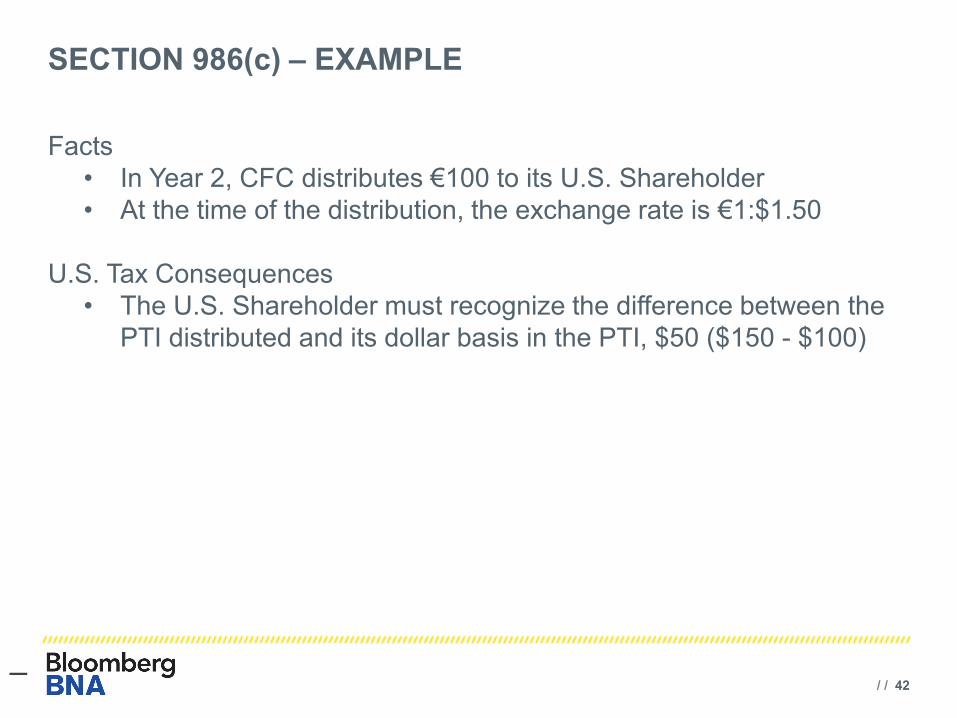

SECTION 986(c) – EXAMPLE

Facts • In Year 2, CFC distributes €100 to its U.S. Shareholder • At the time of the distribution, the exchange rate is €1:$1.50

U.S. Tax Consequences • The U.S. Shareholder must recognize the difference between the

PTI distributed and its dollar basis in the PTI, $50 ($150 - $100)

–

/ / 43

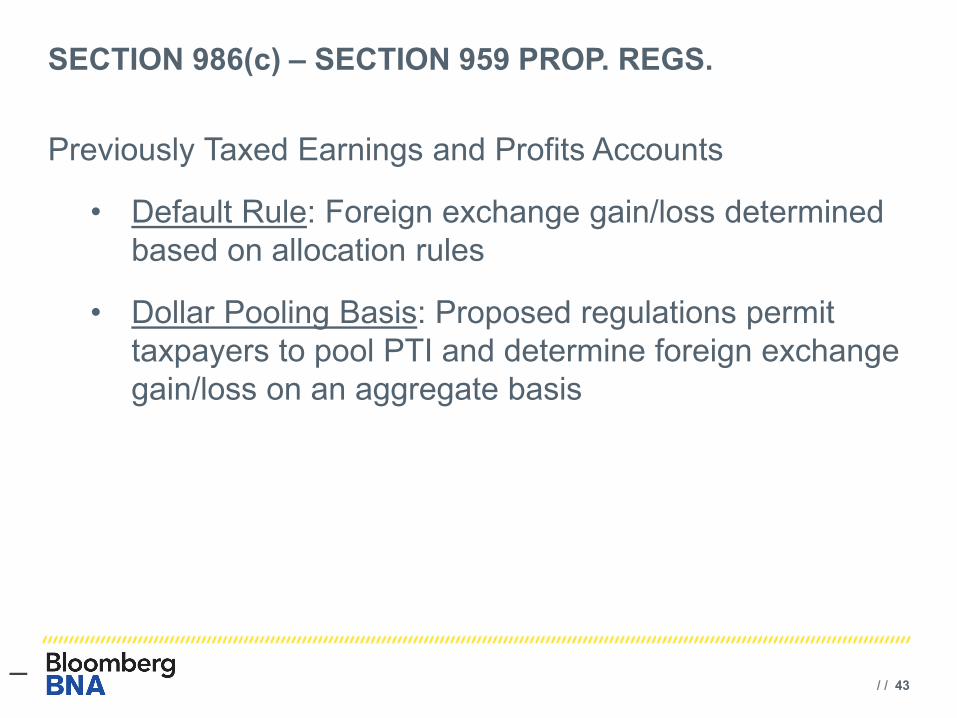

SECTION 986(c) – SECTION 959 PROP. REGS.

Previously Taxed Earnings and Profits Accounts

• Default Rule: Foreign exchange gain/loss determined based on allocation rules

• Dollar Pooling Basis: Proposed regulations permit taxpayers to pool PTI and determine foreign exchange gain/loss on an aggregate basis

–

/ / 44

SECTION 986(c) – EXAMPLE

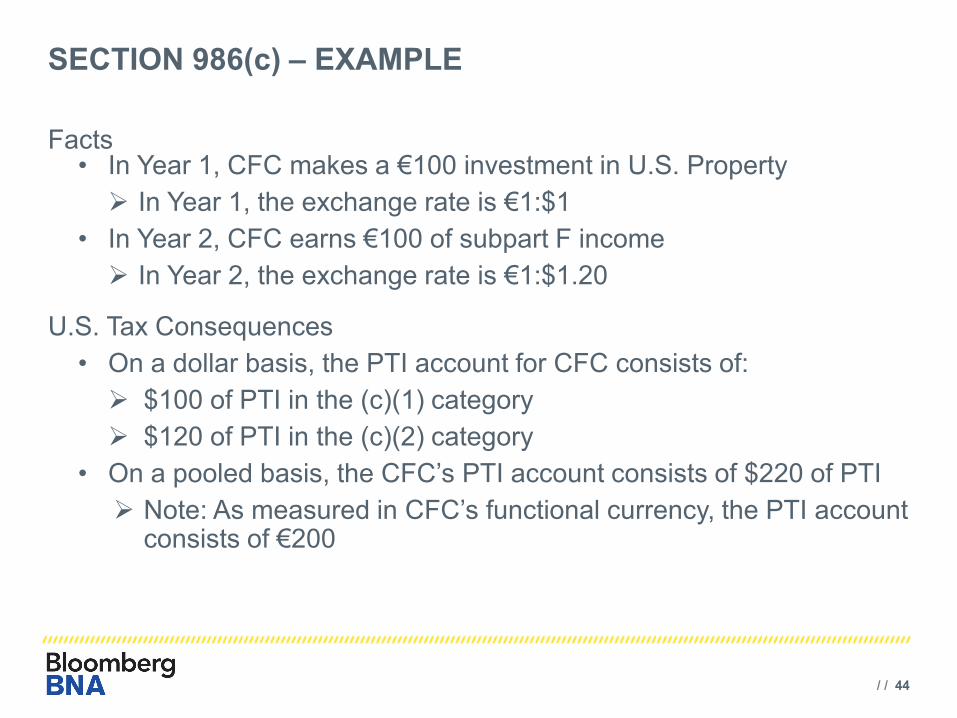

Facts • In Year 1, CFC makes a €100 investment in U.S. Property In Year 1, the exchange rate is €1:$1

• In Year 2, CFC earns €100 of subpart F income In Year 2, the exchange rate is €1:$1.20

U.S. Tax Consequences • On a dollar basis, the PTI account for CFC consists of: $100 of PTI in the (c)(1) category $120 of PTI in the (c)(2) category

• On a pooled basis, the CFC’s PTI account consists of $220 of PTI Note: As measured in CFC’s functional currency, the PTI account

consists of €200

/ / 45

SECTION 986(c) – EXAMPLE

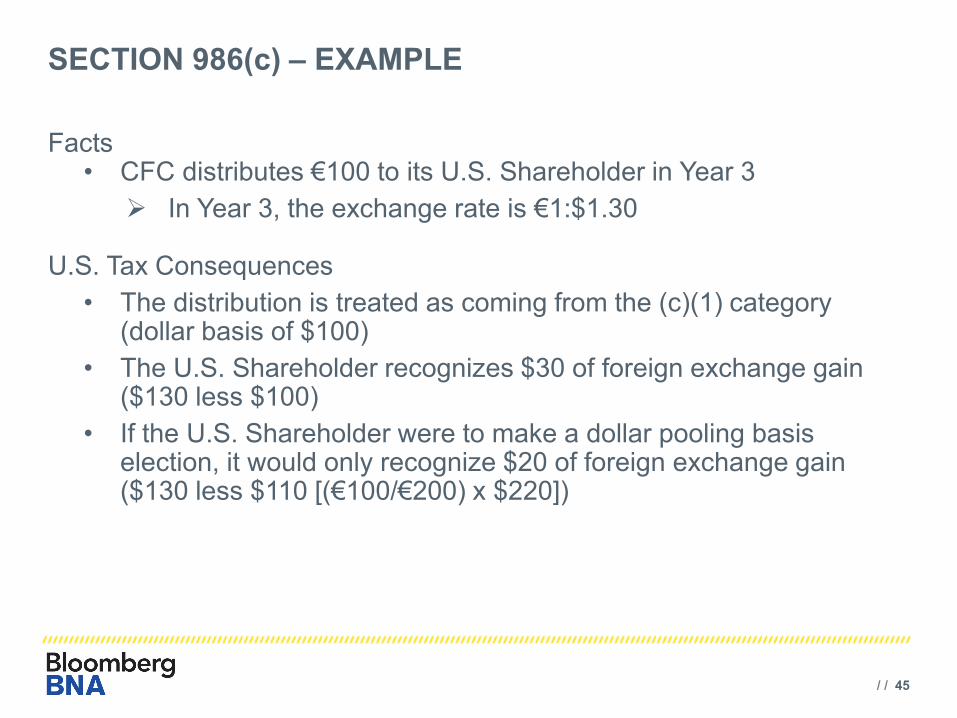

Facts • CFC distributes €100 to its U.S. Shareholder in Year 3 In Year 3, the exchange rate is €1:$1.30

U.S. Tax Consequences

• The distribution is treated as coming from the (c)(1) category (dollar basis of $100)

• The U.S. Shareholder recognizes $30 of foreign exchange gain ($130 less $100)

• If the U.S. Shareholder were to make a dollar pooling basis election, it would only recognize $20 of foreign exchange gain ($130 less $110 [(€100/€200) x $220])

THANK YOU