Embed Size (px)

Citation preview

UNIT 5- MONEY, BANKING, FISCAL AND MONETARY POLICY

Chapters 9-11, 12 and 15Rev 7/11, © Robin Foster

CHAPTER 15THE FEDERAL RESERVE SYSTEM

THE FEDERAL RESERVEThe Federal Reserve (the Fed) was established

in 1913 as America’s central Bank.

It sets the nation’s monetary policy.

The actions of the fed affect everyone daily.

THE FEDERAL RESERVE ACT

Mandates of the Act:Stable prices

Moderate long term interest ratesMaximum employment

FED ACT-CON’T-DECENTRALIZED STRUCTURE

7 member Board of Governor’s in Washington, DC who are appointed by the President and confirmed by the Senate.

12 regional Reserve banks with a separate board of directors and a President

25 branch banks Financial Independence Congressional oversignt

THE FEDERAL RESERVE DISTRICTS

The country is divided into 12 districts. Washington, DC is the headquarters. Each district has a main bank located in a

major city. These cities were selected so they are no more than a 1 days train ride apart.

Houston is in the 11th district. Dallas is the main Bank San Antonio and El Paso have branch banks for

our region.

THE FEDERAL RESERVE DISTRICTS

ORGANIZATION OF THE FED.

The Fed is a corporation member banks own stock.

The Fed pays member banks a 6% annual dividend on Fed stocks.

Any profit by the Fed is returned to the US treasury. In 2009, this amount was $47.4 billion.

ORGANIZATION OF THE FED

FUNCTIONS OF THE FED

Approve bank mergers

Watch bank actions and lending

Currency supplier

Bank for U.S. Government accounts

Clear checks

Maintain Stability of the Financial System

Provide Financial Services

FUNCTIONS OF THE FED

Regulate foreign banks in the United States

Regulate U.S. banks overseas

Regulate military banks

Sets reserve requirement.

Buy/sell bonds to raise/lower interest rates.

Supervise and regulate banking industry

Conduct monetary policy

FUNCTIONS OF THE FED

Loans money to member banks.

Lender of Last Resort

THE FED IS A BANKER’S BANK

Check processing Electronic funds

transfer (EFT) Paid over $30 billion

in checks in 2006

Puts money in circulation

Distroy’s old money

By 2010 the Fed will have only 4 check clearinghouses-Atlanta, Dallas, Philadelphia and Cleveland

Payment SystemIssuer and distributor

of currency

FISCAL AGENT FOR THE US TREASURY

Maintain the treasury’s bank account.

Handle weekly actions of treasury securities.

Issue and redeem savings bonds

The bank for the US government

REGULATOR AND SUPERVISOR Examine banks to

foster a sound banking system

Ensure compliance with all consumer protection laws

Evaluate Community Investment performance

MONETARY POLICYMAKER Major function of all

central banks Monetary policy

actions influence availability and cost of money and credit

Focus on price stability

Promote savings and investment

Keep inflation and unemployment in check.

EXPANDED ROLE OF THE FED. The fed will have

expanded oversight of the banking and credit industry, including credit card interest rates.

DIFFERENCE BETWEEN FED AND TREASURY

The Federal Reserve System is the nations bank. Its primary purpose is to regulate the flow of money and credit in the country.

Janet Yellen

The Treasury is the department in government which is in charge of revenue, taxation and public finances. They are the financial operations for the government.

Jack Lew

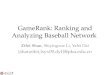

SECTION 2: TOOLS OF MONETARY POLICY

The Federal Open Market Committee (FOMC) meets 8 times a year in Washington, DC and announces any monetary action taken.

Actions of the FOMC

affect the country.

SECTION 2: TOOLS OF MONETARY POLICY

The Federal Open Market Committee (FOMC) meets 8 times a year in Washington, DC and announces any monetary action taken.

Actions of the FOMC

affect the country.

RESPONSIBILITIES OF THE FOMC

Assess National and regional economic and financial conditions using regional perspectives.

Determine credit and interest rates policies.

Target the Federal Funds rate. Direct open market operations

conducted by the New York Fed to achieve goals of price stability and sustainable economic growth.

SIX TOOLS OF MONETARY POLICY

Buy/sell government securities. This increases the money supply

Interest rate the Fed charges to member banks for loans.

Open Market Operations Discount rate

SIX TOOLS OF MONETARY POLICY

Increase or decrease required reserves held by banks.

Currently 10%

How much money is needed to purchase stocks.

Reserve Requirement Margin Requirements

SIX TOOLS OF MONETARY POLICY

Chairman of the Fed gives his opinion on the economy.

Selective, specific goals usually in wartime.

During WWII, no cars were produced.

Moral Suasion Selective Credit Controls

THE CHAIRMAN OF THE FED.

Ben Bernacke Reappointed by

President Obama for a 14 year term.

PART 3-MONETARY POLICY, BANKING AND THE

ECONOMY

Short run impact-of an increase or decrease in the money supply affects the price of borrowing.

The prime rate is the interest rate at commercial banks charge their best customers.

MONETARY POLICY, BANKING AND THE ECONOMY

Long run impact- of a change in the money supply affects the general level of prices or inflation.

The Quantity Theory of Money—example: the Continental Congress issued $250 million in currency causing 123% inflation.

EASY MONEY POLICY A group of actions to

increase the money supply, fight a “recession”—easy money.

Buy government securities

Lower discount rate Lower reserve

requirement

Interest rates fallSpending/borrowing

increasesMoney supply increases

TIGHT MONEY POLICY A group of actions

by the Fed to cut the money supply to fight inflation—”tight” money.

Sell government securities.

Raise discount rate Raise reserve

requirement

Interest rates riseSpending/borrowing

fallsMoney supply falls

THE FED AND THE PRESIDENT Interest rates are

political because Presidential elections are political.

The actions of the fed are political because the chair of the Fed is appointed by the President.

FEDERAL GOVERNMENT EXPENDITURES-OR THE BUDGET

The federal budget year is Oct. 1 to Sept 30 of each year.

The budget is prepared by the by the Office of Management and Budget.

The budget must be sent to Congress no later than Feb. of each year for Congressional approval.

TWO KINDS OF GOVERNMENT SPENDING

Spending authorized by law that continues without the need for government approval.

Examples: social security, medicare, debt payments

Programs that must receive annual authorization.

Examples: military and welfare

Mandatory SpendingDiscretionary Spending

ENTITLEMENT PROGRAMS

Entitlement is a guarantee of access to benefits because of rights or by agreement through law.

Social Security, Medicaid, Medicare are large entitlement programs that take.

These account for over $1 trillion of the federal budget.

CHAPTER 10-GOVERNEMENT SPENDING

IMPACT OF GOVERNMENT SPENDING

Easy? Recessions-push government spending

toward a deficit. Why?

Expansionary periods-push government spending toward a surplus Why?

TAX REVENUE VS EXPENSES

Gov’t revenue surplus

Gov’t spending

deficit

balanced budget.

KEYNES-GENERAL THEORY ON EMPLOYMENT, INTEREST AND MONEY

The level of employment needed is determined by the spending of Money.

Which means-persons working cost the government less money and government collects more money.

SECTION 4-DEFICITS, SURPLUSES AND THE NATIONAL DEBT.

DEFICITS, SURPLUSES AND NATIONAL DEBT

Deficit spending-is the amount by which a government, private company, or individual's spending exceeds income over a particular period of time, also called simply "deficit," or "budget deficit," the opposite of budget surplus.

Federal Debt or surplus-The annual government deficit or surplus refers to the cash difference between government receipts and spending.

Debt ceiling-limit on government spendingcurrently-$14.294 trillion by H.J.Res. 45 was signed into law on February 12, 2010

NATIONAL DEBT

National Debt

What happens when the USA reaches the debt ceiling? No more money can be borrowed to finance

government spending.

There is no constitutional requirement that the USA have an anually balanced budget

STATE OF TEXAS AND DEBT

The State of Texas is required by the Constitution to have an annually balanced budget. This means Texas cannot have a budget deficit.

What happens if they take in less money than they need to spend?

IMPACT OF THE NATIONAL DEBT Taxes and tax burden-increase taxes, less

money for consumers to spend.

Larger the debt, the larger the interest payments; and therefore the more taxes to pay them.

Increased taxes reduce incentive to work, save and invest.

PA

RT 1

-FU

NC

TIO

NS

AN

D C

HA

RA

CTER

ISTIC

S O

F M

ON

EY

Click icon to add picture What is money?

Money is any substance used to pay for goods or services.

Most people say they do not have enough money.

History of money

BARTER Barter is the trading of goods without money.

Yes, barter still happens today.

Pro’s of barter-no government, no taxes. Get what you need without money, if you have something to trade.

Con’s of barter-products/services may not divide evenly. Comparable values may not exist.

FUNCTIONS OF MONEYMedium of exchange-people must accept as

payment for goods.

Measure of value-measure of what a good is worth in dollars and cents.

Store of value-place holder of an amount.

EARLY MONEY

CHARACTERISTICS OF MONEYPortable-easy to carry and exchangeDurable-lasts over time, withstands

wear and tear.Divisible-divide into smaller units.*Stable in value-retains value over time.

But, can lose value due to inflation.Scarce-limited supply.Accepted-Government or an agency

must approve for use. You can’t just create your own money.

MONEY IN EARLY SOCIETIES Commodity money-money with an

alternative use. Wampum-sea shells used for money. Fiat money-money by government decree. Legal tender-currency that must be

accepted. Representative money-an be exchanged for

gold or silver. Specie-gold/silver coins from Europe.

IN THE COLONIESCommodity and fiat

money was used including:

tobaccoGunpowderCoinsColonial paper money

MONEY TODAYOur money today is:

Inconvertible Fiat Money

MONETARY UNIT

a standard unit of currency. Unique to each country

USA-dollar Mexico-Peso Japan-Yen France-Euro

GOLD STANDARD

Holds back economic growth.

Increased demand for gold lowers reserves.

Gold price must remain constant.

Advantages Disadvantages Trade money for

gold Trust in money Keeps government

from printing too much money.

GOLD STANDARD During the Depression the

government gave up on the gold standard.

People were encouraged to turn in their gold.

Many did not due to their loss of faith in paper money.

Having gold could result in fines, but people hid their gold.

GOLD STANDARD After leaving the gold

standard the US changed to inconvertible fiat money.

People cannot demand gold or silver in return for their money.

The government controls the money supply and issues a single currency.

BANKS An organization, usually a corporation,

chartered by a state or federal government, which does most or all of the following: receives demand deposits and time deposits, honors instruments drawn on them, and pays interest on them; discounts notes, makes loans, and invests in securities; collects checks, drafts, and notes; certifies depositor's checks; and issues drafts and cashier's checks.

SAVINGS AND LOANS Savings and Loan (S&L)- A federally or state

chartered financial institution that takes deposits from individuals, funds mortgages, and pays dividends.

CREDIT UNIONS A non-profit financial institution that is owned

and operated entirely by its members.

When a person deposits money in a credit union, he/she becomes a member of the union because the deposit is considered partial ownership in the credit union.

BANKS AND BANKING SERVICES

Since deregulation-banks do not charge the same fees for all services they provide.

Shop for the bank that is right for you.

TYPES OF DEPOSITS

Demand deposits-checking accounts Time deposits-savings accounts

Money Market Accounts-a checking account that is invested in the stock market and can earn interest and is charged a fee based on market fluctuations.

NOW account- Negotiable Order of Withdraw)--An interest-bearing checking account at a bank or savings and loan.

OTHER BANKING SERVICES Overdraft protection-A checking

account/debit card feature in which a person has a line of credit to write checks for more than the actual account balance.

BANKING SERVICES Electronic Funds Transfer

(EFT)- Any transfer of funds that is initiated by electronic means, such as an electronic terminal, telephone, computer, ATM or magnetic tape.

Automated Teller Machines (ATM)-a machine at a bank branch or other location which enables a customer to perform basic banking activities (checking one's balance, withdrawing or transferring funds) even when the bank is closed.

BANKING AND YOU

Debit card- A card which allows customers to access their funds immediately, electronically. Unlike a credit card, a debit card does not have any float.

Certificates of Deposit (CD’s)-CDs are low risk, low return investments, and are also known as "time deposits", because the account holder has agreed to keep the money in the account for a specified amount of time, anywhere from three months to six years

BANKING AND YOU Safe Deposit Box-a lock box in a bank that is

used to store valuable items and documents.

Electronic Banking-banking done on line. This can be used to pay bills, transfer funds, etc.

Service Charge-Bank fee charged for specific services or as a penalty for not meeting certain criteria

TRUTH IN LENDING LAWS Legislation passed in

some countries, such as the Home Mortgage Disclosure Act of 1968 and Consumer Credit Protection Act of 1969 in the US.

Under these laws a lender must, clearly and conspicuously, reveal all the key details of a home mortgage or consumer loan before the borrower signs the loan agreement.

Borrowers who mortgage their dwelling house as a collateral are generally allowed a cooling off period (usually three days) to rethink the implications of the loan agreement and to cancel it if they so decide.

MONEY TODAY

MONEY

Currency Paper money.

Coinsmetal money.

DENOMINATIONS OF MONEY Currency

$1, $2, $5, $10, $20, $50 and $100’s

Coins

$.01, $.05, $.10, $.25. $.50, $1.00

OUR MONEY:

BY THE NUMBERS Facts about on how much each denomination represents in the 9.12 billion currency notes the Bureau of Engraving and Printing will produce in the current budget year and the average life for each note:

$1 note: 45.5% of total note production; 21 months.

$5 note: 15.4%; 16 months. $10 note: 0.9%; 18 months. $20 note: 21.6%; 24 months. $50 note: 4.7%; 55 months. $100 note: 11.9%; 89 months.

COMPONENTS OF THE MONEY SUPPLY

M1 money-currency, coins and travelers checks. Money is more liquid.

M2 money-M1+checking and savings accounts +money market accounts and CD’s. Money is less liquid.

FT. KNOX KENTUCKY HOLDS THE US GOLD

FT. KNOX, KENTUCKY AND GOLD Not all currency is

backed by gold. There are 147.3

million ounces of gold.

The gold is held as an asset of the US Government at a book value of $42.22 per ounce.

A gold bar is 400 ounces or 27.5 pounds

MONEY IN CIRCULATION

Approximately $829 billion in circulation.

Most is held outside the USA.

COUNTERFEIT MONEY

Yes, printing your own money is a crime.

The Secret Service investigates counterfeit money.

SO YOU WANT TO OWN A BANK?

How banks operate:Banks make money by accepting deposits and

making loansLiabilities are the debt/obligations of the bank.Assets are the property/posessions of the bank.A balance sheet is a statement showing

assets/liabilities of a bank.The net worth is the excess of assets over

liabilities.

STARTING A BANK Organize, obtain a charter. Buy into the Fed (like buying insurance) Make loans

Excess reserves are deposits-reserves

Reaching maturity deposits=loans=economic growth

Loans=monetary growth---loans increase money for loans.

BANKS IN ACTION Equity-investment against bankruptcy Bank liabilities-obligations to others

Required reserves are the amount of money that a bank must set aside and not loan. The size of the reserve is set by the Fed. This is a fractional reserve system.

BANKS IN ACTION Most of the deposits are returned to the

community in the form of loans.

Banks invest in bonds: they are a safe investment and are easily converted to cash.

BANK BALANCE SHEETS

Assets LiabilitiesBonds Demand Deposits

Reserve requirement Time Deposits

Excess Reserves Capital Stock

Loans CD’s

Building/Equipment

Total: Total:

Assets and liabilities must always equalNotes page 16

BANK PROFIT For a bank to make a profit it must have a

spread between what is paid out in interest and what it takes in on interest on loans over 3%

BANKING A state bank is generally a financial

institution that is chartered by a state. It differs from a reserve bank in that it does not necessarily control monetary policy (indeed, the state in question may have no legal capacity to create monetary policy), but instead usually offers only retail and commercial services.

They oppose mandatory membership in the Fed.

BRANCH AND ELECTRONIC BANKING Until the 1990’s branch banking was illegal

(having more that one location of the same bank.)

Banks are facing increasing competition.

Electronic banks are putting pressure on brick and mortar banks due to lower costs.

DEPOSITORY INSTITUTION DEREGULATION AND MONETARY CONTROL ACT]

Passed in 1980, gave the Federal Reserve greater control over non-member

banks.

It forced all banks to abide by the Fed's rules.

It allowed banks to merge.

It removed the power of the Federal Reserve Board of Governors to set the

interest rates of savings accounts.

It raised the deposit insurance of US banks and credit unions from $40,000 to

$100,000.

It allowed credit unions and savings and loans to offer checkable deposits.

Allowed institutions to charge any interest rates they chose.

FDIC Since the start of FDIC insurance on January

1, 1934, no depositor has lost a single cent of insured funds as a result of a failure.

The FDIC receives no Congressional appropriations – it is funded by premiums that banks and thrift institutions pay for deposit insurance coverage and from earnings on investments in U.S. Treasury securities.

FDIC AND FSLIC

Your money is guaranteed by these groups. Look for the seal at your bank.

IS YOUR BANK INSURED?

WHY BANKS FAIL? Depositors lose money. Banks give bad loans Confidence is lost in banks

The FDIC/FSLIC can put a bank on a watch list; if things do not improve the bank will be declared insolvent.