Embed Size (px)

Citation preview

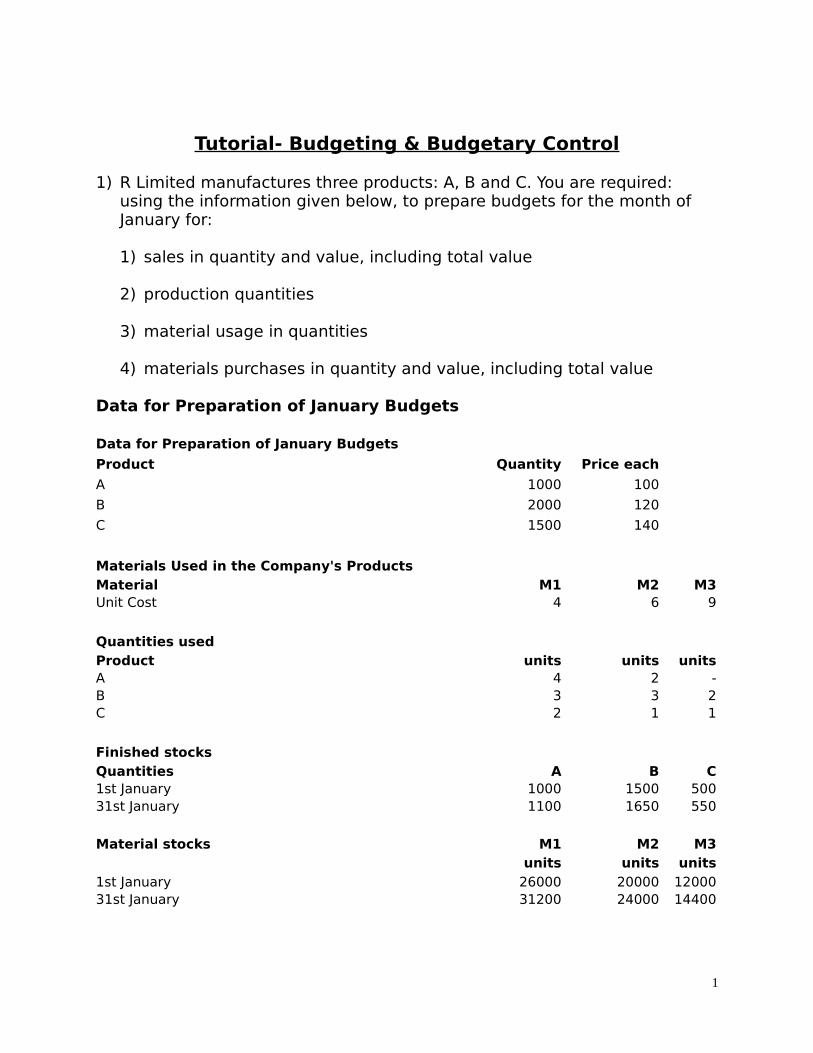

Tutorial- Budgeting & Budgetary Control

1) R Limited manufactures three products: A, B and C. You are required: using the information given below, to prepare budgets for the month of January for:

1) sales in quantity and value, including total value

2) production quantities

3) material usage in quantities

4) materials purchases in quantity and value, including total value

Data for Preparation of January Budgets

Data for Preparation of January Budgets

Product Quantity Price each

A 1000 100

B 2000 120

C 1500 140

Materials Used in the Company's ProductsMaterial M1 M2 M3Unit Cost 4 6 9

Quantities usedProduct units units unitsA 4 2 -B 3 3 2C 2 1 1

Finished stocksQuantities A B C1st January 1000 1500 50031st January 1100 1650 550 Material stocks M1 M2 M3

units units units1st January 26000 20000 1200031st January 31200 24000 14400

1

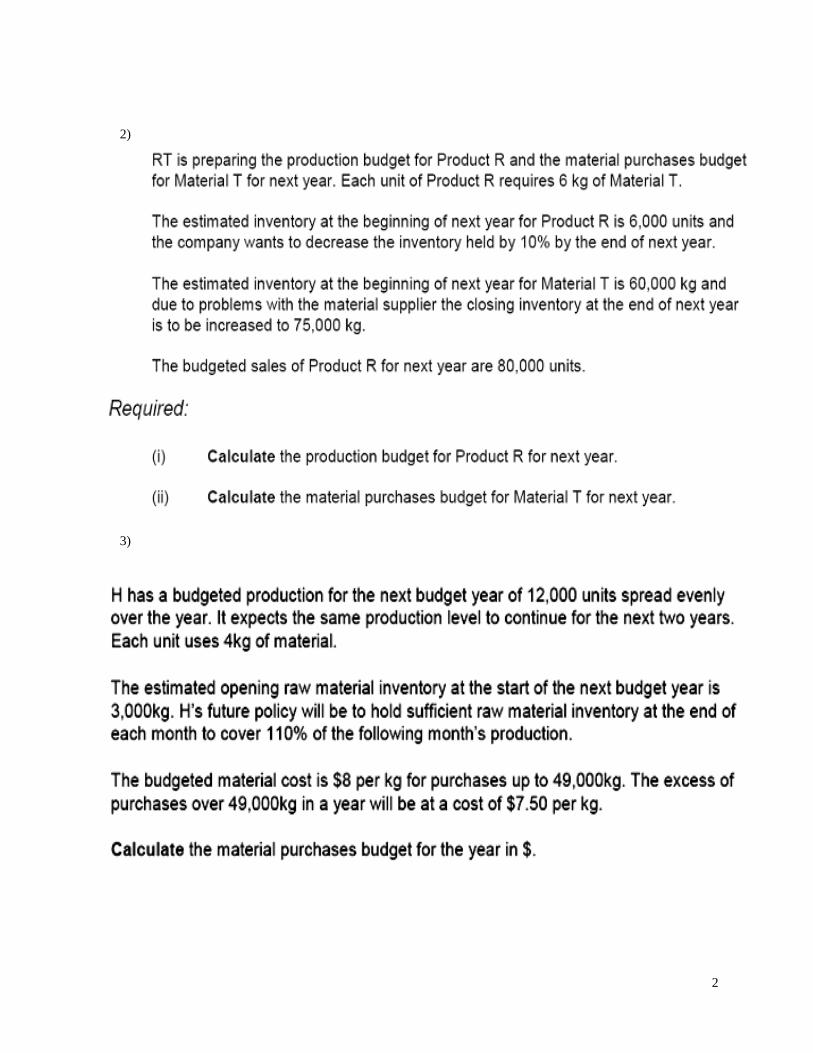

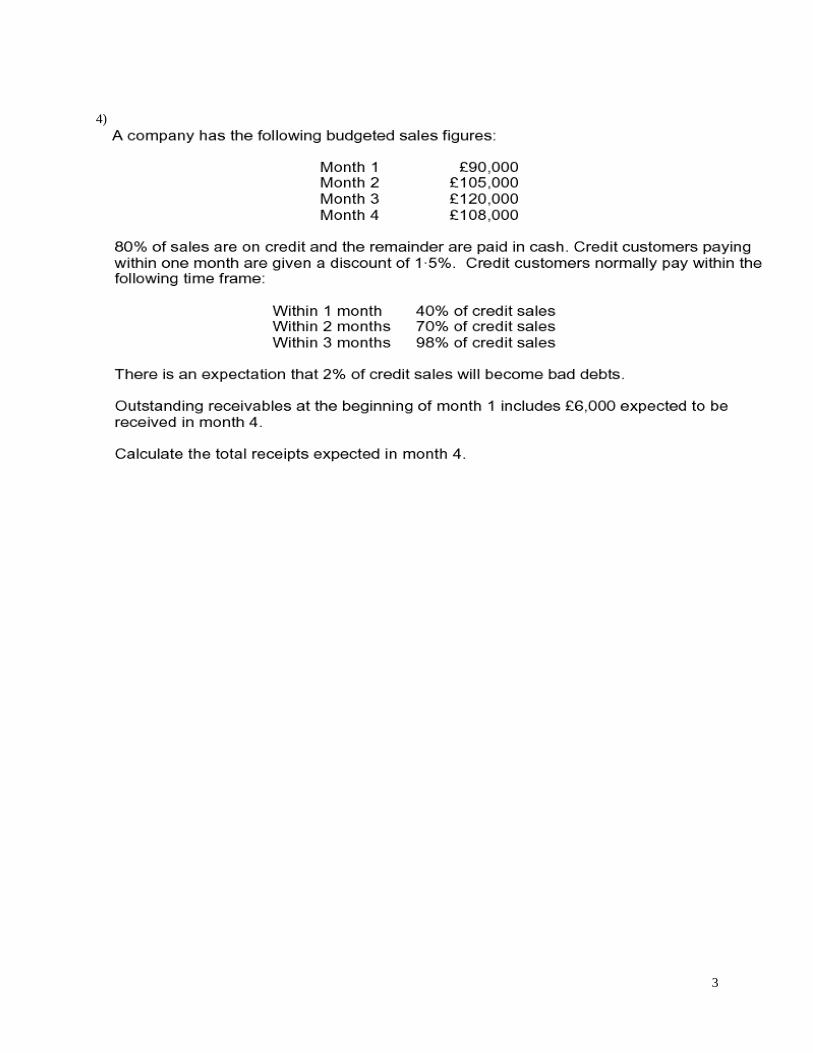

2)

3)

2

4)

3

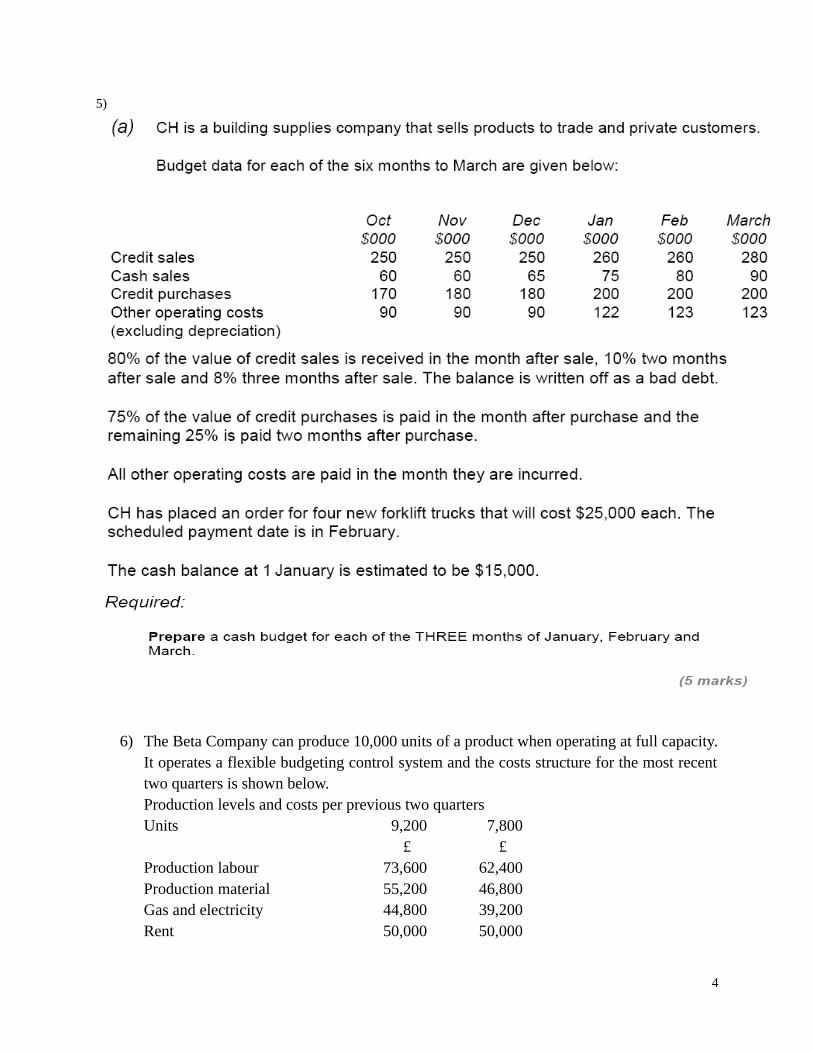

5)

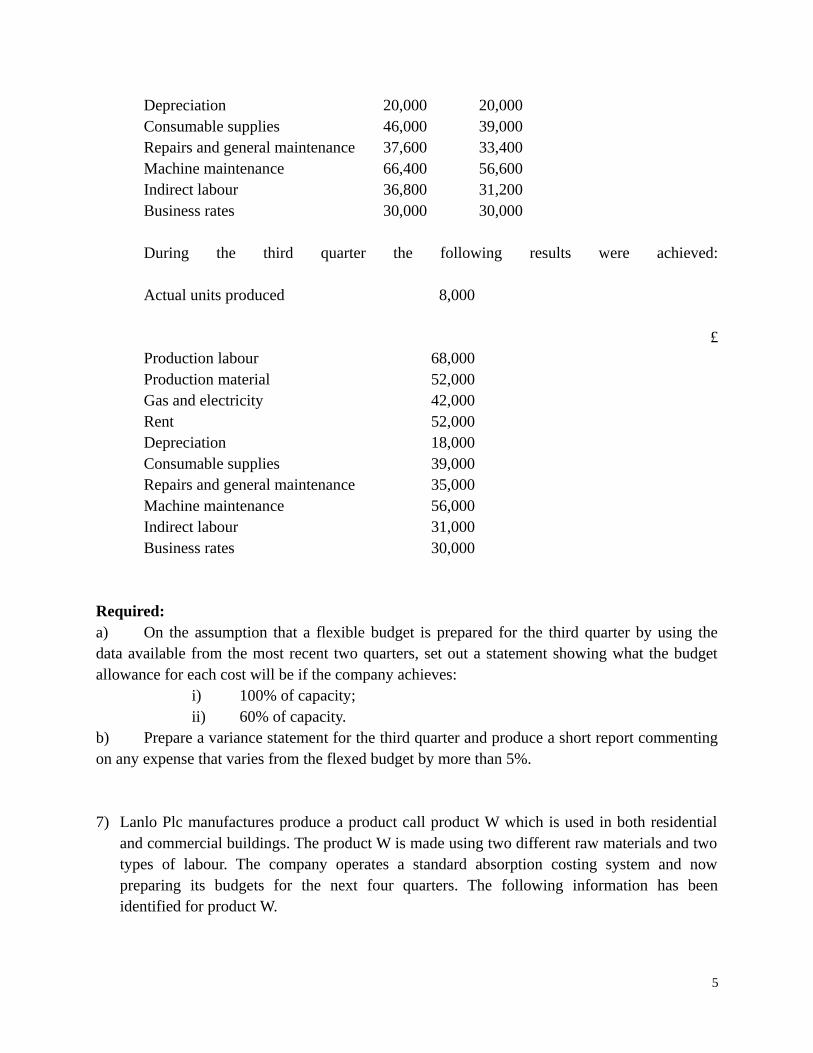

6) The Beta Company can produce 10,000 units of a product when operating at full capacity.It operates a flexible budgeting control system and the costs structure for the most recenttwo quarters is shown below.Production levels and costs per previous two quartersUnits 9,200 7,800

£ £Production labour 73,600 62,400Production material 55,200 46,800Gas and electricity 44,800 39,200Rent 50,000 50,000

4

Depreciation 20,000 20,000Consumable supplies 46,000 39,000Repairs and general maintenance 37,600 33,400Machine maintenance 66,400 56,600Indirect labour 36,800 31,200Business rates 30,000 30,000

During the third quarter the following results were achieved: Actual units produced 8,000

£Production labour 68,000Production material 52,000Gas and electricity 42,000Rent 52,000Depreciation 18,000Consumable supplies 39,000Repairs and general maintenance 35,000Machine maintenance 56,000Indirect labour 31,000Business rates 30,000

Required: a) On the assumption that a flexible budget is prepared for the third quarter by using thedata available from the most recent two quarters, set out a statement showing what the budgetallowance for each cost will be if the company achieves:

i) 100% of capacity; ii) 60% of capacity.

b) Prepare a variance statement for the third quarter and produce a short report commentingon any expense that varies from the flexed budget by more than 5%.

7) Lanlo Plc manufactures produce a product call product W which is used in both residentialand commercial buildings. The product W is made using two different raw materials and twotypes of labour. The company operates a standard absorption costing system and nowpreparing its budgets for the next four quarters. The following information has beenidentified for product W.

5

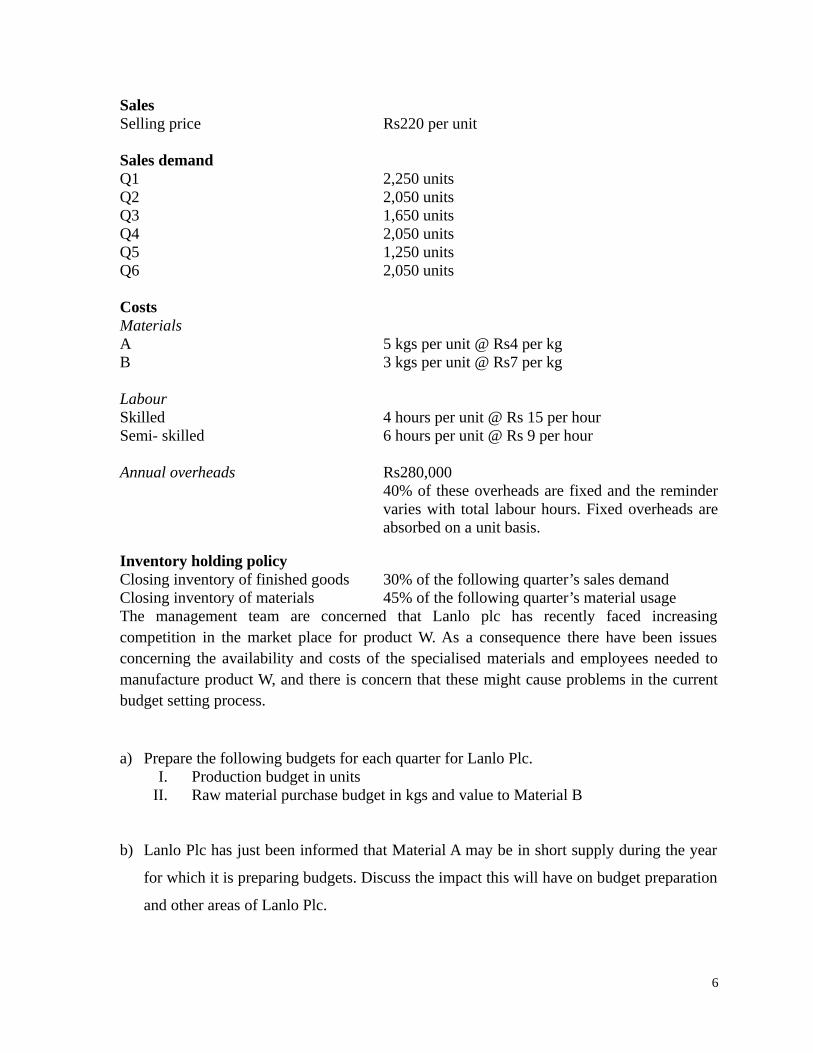

SalesSelling price Rs220 per unit

Sales demandQ1 2,250 unitsQ2 2,050 unitsQ3 1,650 unitsQ4 2,050 unitsQ5 1,250 unitsQ6 2,050 units

Costs MaterialsA 5 kgs per unit @ Rs4 per kgB 3 kgs per unit @ Rs7 per kg

LabourSkilled 4 hours per unit @ Rs 15 per hourSemi- skilled 6 hours per unit @ Rs 9 per hour

Annual overheads Rs280,00040% of these overheads are fixed and the remindervaries with total labour hours. Fixed overheads areabsorbed on a unit basis.

Inventory holding policyClosing inventory of finished goods 30% of the following quarter’s sales demandClosing inventory of materials 45% of the following quarter’s material usageThe management team are concerned that Lanlo plc has recently faced increasingcompetition in the market place for product W. As a consequence there have been issuesconcerning the availability and costs of the specialised materials and employees needed tomanufacture product W, and there is concern that these might cause problems in the currentbudget setting process.

a) Prepare the following budgets for each quarter for Lanlo Plc.I. Production budget in units

II. Raw material purchase budget in kgs and value to Material B

b) Lanlo Plc has just been informed that Material A may be in short supply during the year

for which it is preparing budgets. Discuss the impact this will have on budget preparation

and other areas of Lanlo Plc.

6

c) Assuming that the budgeted production of product W was 7,700 units and that the

following actual results were incurred for labour and overheads in the year:

Actual production 7,250 unitsActual overheads Variable Rs 185,000 Fixed Rs 105,000Actual labour costs Skilled- Rs16.25 per hour Rs 568,750 Semi-skilled – Rs8 per hour Rs 332,400

Prepare a flexible budget statement for Lanlo Plc showing the total variances that have

occurred for the above four costs only.

d) Lalo Plc currently uses incremental budgeting. Explain how Zero Based Budgeting could

overcome the problems that might be faced as a result of the continued use of the current

system.

8) D Ltd is preparing its annual budgets for the year to 31 December 2010. It manufacturesand sells one product, which has a selling price of Rs 150. The marketing directorbelieves that the price can be increased to Rs 160 with effect from 1 July 2010 and that atthis price the sales volume for each quarter of 2010 will be as follows.

Sales volume unitsQuarter 1 40,000Quarter 2 50,000Quarter 3 30,000Quarter 4 40,000

Each unit of the finished product that is manufactured requires four units of componentsR and three units of Component T, together with a body shell S. these items arepurchased from an outside supplier. Currently price at;

Component R Rs 8.00 eachComponent T Rs 5.00 eachShell S Rs 30.00 each

The components are expected to increase in price by 10% with effect from 1 April 2010,no change is expected in the price of the shell.

Stocks on 31 December 2009 are expected to be as follows:Units

7

Finished units 9,000Component R 3,000Component T 5,500Shell S 500

Closing stocks at the end of each quarter are to be as follows:Finished units 10% of next quarter’s salesComponent R 20% of next quarters production requirementsComponent T 15% of next quarters production requirementsShell S 10% of next quarters production requirements

Required :

Prepare the following budgets for D Ltd for the year ending 31 December 2010, showingvalues for each quarter and the year in total:

a) Sales budget ( in Rs and units)

b) Production budget ( in units)

c) Material usage budget (in units)

d) Material purchase budget (in units and in Rs)

8