Embed Size (px)

Citation preview

Credit Report Summary

This segment summarizes the credit report by highlighting your Current Credit Exposure, Secured vs. Unsecured Loans and Current Credit Liability in an easy to understand graphical manner.

Apply for a Loan

This section has a range of pre-approved loan and credit card offers, based on your credit eligibility. You can compare offers made by different lenders and apply for a loan that best suits your needs.

Activity Report

A unique feature of the report is the credit activity tracker, which notifies you of the changes made to your report in the last 90 days. The following credit activites are reflected in this section: New Account Opened, Account Closed, Number of Enquiries, Late Payment and Account reported as ‘Written Off’.

myCIBIL is a platform that provides you access to all CIBIL services such as purchasing and/or renewing your Subscription, the ability to dispute inaccuracies in your credit report and getting pre-approved loan and credit card offers. It also provides you with a dashboard that has a snapshot of your credit profile.

DASHBOARD RAISE A DISPUTE DISPUTE STATUS UNDERSTAND YOUR REPORTVIEW REPORT

Consumer Dashboard

My Account

This section reflects your personal detailslike name, mailing address, permanent address, contact and income details. The edit feature allows you to modify or correct any information that you might find is incorrect or needs updation.

MY ACCOUNT HISTORY SUGGESTION LOGOUT

VIEW EDIT

PERSONAL DETAILS :Name Gopinath LLMRMailing Address Old No. L32, New No. L8, Ground Floor, 24th Street L Block, Anna Nagar EastState Tamilnadu City / District Chennai Pincode 600102

LOGIN PORTALCONSUMER DETAILS

Welcome, Member

Account Details

History

This section captures all your activities since the day you first login to myCIBIL. You can keep a track of events related to your account and e-mail or download your past credit reports. Your credit report is digitally signed for security reasons.

HISTORY SECTION

Welcome, Member

Date & Time of the Event Section Changes / Events

30.01.2014 - 07:10 Reports 1st Report Refreshed Email Download

30.01.2014 - 08:50 Reports Report Downloaded

MY ACCOUNT HISTORY SUGGESTION LOGOUT

Credit History

ACTIVITY REPORT

Note : Values as on dd-mm-yyyy.

Today 30 DaysJan 2015

60 DaysDec 2014

90 DaysNov 2014

New Account Opened Account Closed No. of Credit Application

Account reported as “Written off”

Late Payment

CREDIT REPORT SUMMARY

APPLY FOR A LOAN

Click Compare Apply

HomeLoan

Offer4

PersonalLoan

Offer1

Loan AgainstProperty

Offer3

CreditCard

Offers1

BusinessLoan

Offer0

GoldLoan

Offer1

AutoLoan

Offer1

RATEITRATEIT

View Report

You can access your latest CIBIL Score and Report by clicking on the ‘View Report’ tab on the Home page. For ease of understanding, the section is organized under 5 sub-sections i.e. Personal Information, Contact Information, Employment Information, Account Information and Enquiry Information as they would appear in your credit report.

DASHBOARD RAISE A DISPUTE DISPUTE STATUS UNDERSTAND YOUR REPORTVIEW REPORT

This is your 1st Report of Quaterly subscription.1st Report 2nd Report 3rd Report 4th Report

PersonalInformation

ContactInformation

EmploymentInformation

AccountInformation

EnquiryInformation

RefreshYour Report

ACCOUNT DETAILS Credit Limit - Rate of Interest -Sanctioned Amount 37,620 Eepayment Tenure -Current Balance 0 EMI Amount -Cash Limit - Payment Frequency -Amount Overdue - Actual Payment Amount -

BAJAJ FIN LTDMember Name

Consumer LoanAccount Type

4050CD07452404Account Number

INDIVIDUALOwnership

CIBIL Report

Raise a Dispute

This section gives you the ability to dispute inaccuracies, account ownership and duplication of information that may reflect in your Credit Report. You can initiate a dispute by entering the required value in the highlighted area for the respective field or checking the appropriate box.

Dispute Status

You can view the status of dispute in this section. You will also get an email notification from us informing the change status of the dispute request.

DASHBOARD RAISE A DISPUTE DISPUTE STATUS UNDERSTAND YOUR REPORTVIEW REPORT

INSTRUCTIONS :Click on the Dispute ID below, to check your dispute status.

Dispute ID Date Initiated Status of Dispute ID

DDMMYYYY000001 DD/MM/YYYY Open

3 of 3 records

Consumer Dispute Remarks are additional comments that you can add to your Credit Report. These remarks will be available on your report for a year and will be displayed whenever your report is accessed by credit institution/s or by you.

Consumer Dispute Remarks

DASHBOARD RAISE A DISPUTE DISPUTE STATUS UNDERSTAND YOUR REPORTVIEW REPORT

PersonalInformation

ContactInformation

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

NAME DATE OF BIRTH GENDERGopinath LLMR 30-08-1978 Male

SUBMIT RESET

Dispute ProcessNote : Values as on dd-mm-yyyy.

CURRENT CREDIT EXPOSURE SECURED VS UNSECURED CURRENT CREDIT LIABILITY

Open Account Closed Account Secured Unsecured Credit Card Auto LoanPersonal Loan

6

5

1 1

Understanding CIBIL

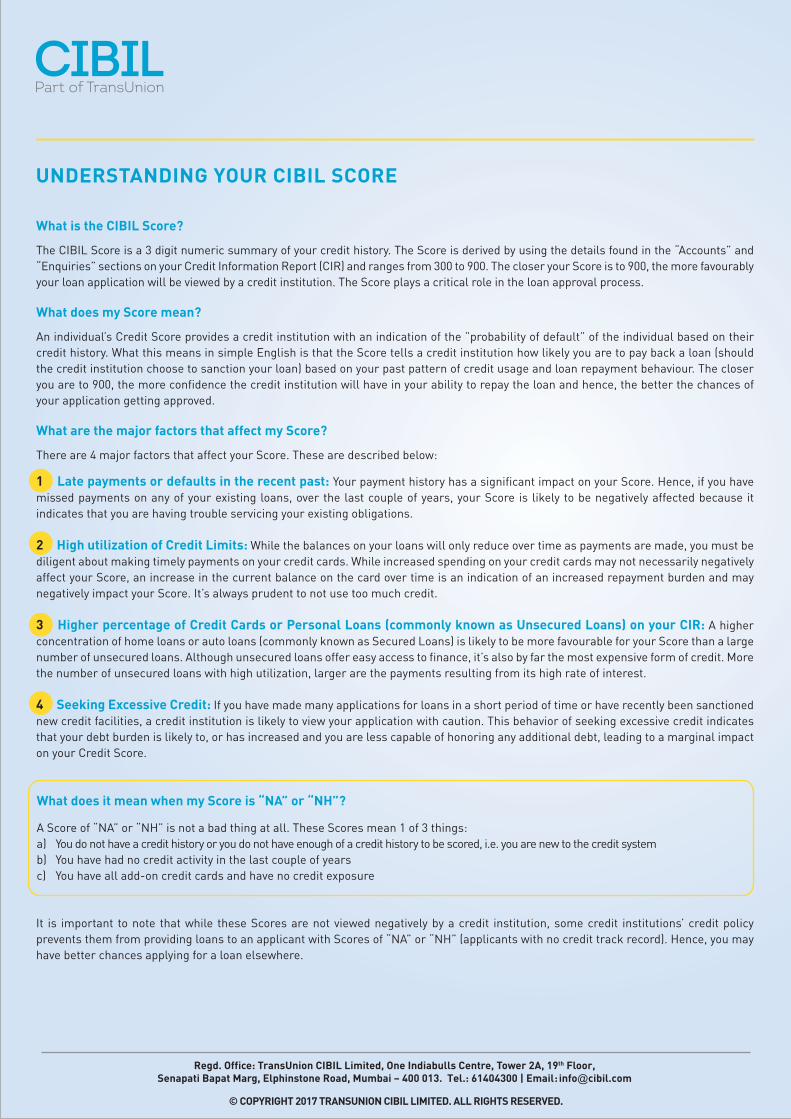

What is the CIBIL Score?

The CIBIL Score is a 3 digit numeric summary of your credit history. The Score is derived by using the details found in the “Accounts” and “Enquiries” sections on your Credit Information Report (CIR) and ranges from 300 to 900. The closer your Score is to 900, the more favourably your loan application will be viewed by a credit institution. The Score plays a critical role in the loan approval process.

What does my Score mean?

An individual’s Credit Score provides a credit institution with an indication of the ”probability of default” of the individual based on their credit history. What this means in simple English is that the Score tells a credit institution how likely you are to pay back a loan (should the credit institution choose to sanction your loan) based on your past pattern of credit usage and loan repayment behaviour. The closer you are to 900, the more confidence the credit institution will have in your ability to repay the loan and hence, the better the chances of your application getting approved.

What are the major factors that affect my Score?

There are 4 major factors that affect your Score. These are described below: 1 Late payments or defaults in the recent past: Your payment history has a significant impact on your Score. Hence, if you have missed payments on any of your existing loans, over the last couple of years, your Score is likely to be negatively affected because it indicates that you are having trouble servicing your existing obligations.

2 High utilization of Credit Limits: While the balances on your loans will only reduce over time as payments are made, you must be diligent about making timely payments on your credit cards. While increased spending on your credit cards may not necessarily negatively affect your Score, an increase in the current balance on the card over time is an indication of an increased repayment burden and may negatively impact your Score. It’s always prudent to not use too much credit.

3 Higher percentage of Credit Cards or Personal Loans (commonly known as Unsecured Loans) on your CIR: A higher concentration of home loans or auto loans (commonly known as Secured Loans) is likely to be more favourable for your Score than a large number of unsecured loans. Although unsecured loans offer easy access to finance, it’s also by far the most expensive form of credit. More the number of unsecured loans with high utilization, larger are the payments resulting from its high rate of interest.

4 Seeking Excessive Credit: If you have made many applications for loans in a short period of time or have recently been sanctioned new credit facilities, a credit institution is likely to view your application with caution. This behavior of seeking excessive credit indicates that your debt burden is likely to, or has increased and you are less capable of honoring any additional debt, leading to a marginal impact on your Credit Score.

It is important to note that while these Scores are not viewed negatively by a credit institution, some credit institutions’ credit policy prevents them from providing loans to an applicant with Scores of “NA” or “NH” (applicants with no credit track record). Hence, you may have better chances applying for a loan elsewhere.

What does it mean when my Score is “NA” or “NH”?

A Score of “NA” or “NH” is not a bad thing at all. These Scores mean 1 of 3 things:a) You do not have a credit history or you do not have enough of a credit history to be scored, i.e. you are new to the credit systemb) You have had no credit activity in the last couple of yearsc) You have all add-on credit cards and have no credit exposure

© COPYRIGHT 2017 TRANSUNION CIBIL LIMITED. ALL RIGHTS RESERVED.

UNDERSTANDING YOUR CIBIL SCORE

Regd. Office: TransUnion CIBIL Limited, One Indiabulls Centre, Tower 2A, 19th Floor, Senapati Bapat Marg, Elphinstone Road, Mumbai – 400 013. Tel.: 61404300 | Email: [email protected]

Your addresses, telephone, mobile numbers and email addresses as reported by lenders appear here.The address category explains whether the address is a residential address, official address, permanent address or temporary address as reported by the lender. Up to 4 addresses and email addresses are provided.

Contact Information: This section provides you with details regarding the enquiry made by the lender for your credit application such as name of the lender, date of application, the type of loan and its size.

Enquiry Information:

DASHBOARD RAISE A DISPUTE DISPUTE STATUS UNDERSTAND YOUR REPORTVIEW REPORT

This is your 1st Report of Quaterly subscription.1st Report 2nd Report 3rd Report 3th Report

PersonalInformation

ContactInformation

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

NAME DATE OF BIRTH GENDERGopinath LLMR 30-08-1978 Male

IDENTIFICATION TYPE NUMBER ISSUE DATE EXPIRATION DATEIncome Tax ID No. (PAN)(e) AGJPG3337R - -Passport No. F8783962 - -Driver’s License No. 10179/96 - -

ContactInformation

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

PersonalInformation

ADDRESS1 CATEGORY RESIDENCE CODE DATE REPORTEDOld No. L32, New No. L8 Not Categorized - 31-12-2008Ground Floor24th Street 'L' BlockAnna Nagar EastChennai, Tamilnadu-600102

ADDRESS2 CATEGORY RESIDENCE CODE DATE REPORTEDOld No. L32, New No. L8 Not Categorized - 31-12-2008Ground Floor24th Street 'L' BlockAnna Nagar EastChennai, Tamilnadu-600102

TELEPHONE TYPE TELEPHONE NO EXTENSIONNot Classified 080 41200103 -Office Phone 080 41085488 -Not Classified 08041085488 -Mobile Phone 919845884521 -

EMAIL CONTACTEmail Address1 [email protected] Address2 [email protected]

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

PersonalInformation

ContactInformation

ACCOUNT TYPE DATE REPORTED OCCUPATION Credit Card 20-05-2015 Salaried

INCOME FREQUENCY INCOME INDICATOR- - -

YOUR CIBIL SCORE IS

300 400 500 600 700 800 900750

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

PersonalInformation

ContactInformation

MEMBER NAME DATE OF ENQUIRY ENQUIRY PURPOSE ENQUIRY AMOUNT

Vaish Coop 25-10-2011 Personal Loan 50,000

IOB 23-10-2010 Personal Loan 1,00,000

HDFC Bank 09-10-2010 Personal Loan 5,00,000

FICCL 13-09-2010 Personal Loan 40,000

Barclays Finance 08-09-2010 Personal Loan 10,000

Dena Bank 10-08-2010 Auto Loan 15,00,000

Axis Bank 18-08-2007 Credit Card 1,00,00,000

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

PersonalInformation

ContactInformation

EmploymentInformation

AccountInformation

EnquiryInformation

ConsumerDispute Remarks

PersonalInformation

ContactInformation

CITI BANKMember Name

CREDIT CARDAccount Type

5546370220384934Account Number

INDIVIDUALOwnership

ACCOUNT DETAILSCredit Limit - Rate Of Interest 20.00Sanctioned Amount 3,36,000 Repayment Tenure 49Current Balance 0 RMI Amount 10,225Cash Limit - Payment Frequency MONTHLYAmount Overdue - Actual Payment Amount -

DATESDate Opened/disbursed 26-03-2008 Date Of Last Payment 17-05-2012Date Closed 17-05-2012 Date Reported And Certified 31-05-2012

PAYMENT HISTORY (UP TO 36 MONTHS)Payment Start Date 01-06-2009 PAYMENT END DATE 01-05-2012

DAYS PAST DUE (No. of Days) or ASSET CLASSIFICATION (STD, SMA, SUB, DBT, LSS)

MONTHYEAR

2014

2013

2012

DEC

000

000

000

NOV

000

000

000

OCT

000

000

000

SEP

000

000

000

AUG

000

000

000

JUL

000

000

000

JUN

000

000

000

MAY

000

000

000

APR

000

000

000

MAR

000

000

000

FEB

000

000

000

JAN

000

000

000

ACCOUNT INFORMATION UNDER DISPUTE

DISPUTE DATE: 31-10-2009CIBIL REMARKS: CIBIL remarks go here

COLLATERAL

VALUE Of Collateral Type Of Collateral

UN

DE

R D

ISP

UTE

How to read your CIBIL Report

CIBIL Score

This section reflects your credit score, which is widely used by loan providers to evaluate loan applications. An individual’s CIBIL Score ranges between 300-900, and is calculated basis the information in the “Accounts” and “Enquiry” section of the credit report. The closer the score to 900, the more confidence the loan provider will have in your ability to repay the loan and hence, the better the chances of your application getting approved.

This section has your Name, Date of Birth andGender as reported to CIBIL by the members.Identification lists your identification detailsas reported by the members. Your Income Tax ID (PAN), Passport, Drivers Licence and Voter ID, that have been reported by the lenders will appear in this section.

Personal Information

Data received through an Enquiry:

The symbol’(e)’ next to any of the details in your report indicates that the value is provided by lender when you applied for a credit facility.

Employment Information:

This section contains information on youroccupation and income (At the time of opening credit facility) as reported by the lender for a particular credit account.

Account Information:

The most important section of your CIR, this section contains the details of your loans and credit cards. It contains the name of the lender/s, the type of credit facilities (home loan, auto loan, credit card, etc), the account number/s, whether single or jointly held, when each account was opened, date of the last payment, loan amount, current balance, amount overdue (if any) and most importantly, a month on month record of up to 36 months of your payments.

A red band on the left of a report section indicates that the section is under dispute and will be removed when the dispute is closed. Upon closure, the disputed informa-tion may or may not be changed as per confirmation received from the lender.

Member Name & Account No. Remark Remarks Removal Date

Vaish Coop Your dispute will be initiated on submission 18-05-2015

HDFC Bank Your dispute will be initiated on submission 18-05-2015

Barclays Finance Your dispute will be initiated on submission 18-05-2015

Your CIBIL Credit Information Report (CIR) is a record of your credit payment history compiled from information received from banks and financial institutions. The purpose is to help loan providers make informed lending decisions basis your credit history, quickly and objectively. A healthy Credit Report can get your loan approved faster and often, at better terms.

Consumer Dispute Remarks:

Consumer Dispute Remarks are additional comments that you can add to your Credit Report. These remarks will be available on your report for a year and will be displayed whenever your report is accessed by credit institution/s or by you.