Embed Size (px)

Citation preview

GLOBAL BRAND DEVELOPMENT

INNOVATE. CONNECT WITH THE WORLD. AMAZE.

2

Trilogy Brands Group is a pioneer in the introduction of emerging,

fast growing, and star-performing American brands to the

Middle East and North Africa region.

3

GROWTH INSPIRED BY EXCITING NEW BRANDS

We build brand value through global partnerships via licensing, distribution, and joint venture programs to drive long term revenue potential and a cohesive brand presence with a footprint

across key international markets. We identify and develop infrastructure and partners that support existing and new business expansion plans worldwide.

4

THE BRAND BEHIND THE BRAND - WHO WE ARE

Revolutions can take all shapes and forms. Trilogy Brands Group (“Trilogy”) brings access to star performing, new and exciting American brands, accelerating business expansion brands into the Middle East and North Africa (“MENA”) region. Trilogy Brands operates as a growth engine driving new brand and enterprise development for mid to top tier US brands into the Middle East.

WE ARE A GLOBAL BRAND DEVELOPMENT AND STRATEGY CONSULTING FIRM PIONEERING A FASTER, BETTER WAY FOR BRANDS TO ACCESS HIGHLY COVETED INTERNATIONAL MARKETS.

Trilogy Brands is the brand behind the brands.

Global is the new local.

Trilogy Brands is focused on creating significant revenue by monetizing “idle brand value” in a very specific and unique region. A region that is ready to embrace the brands. This can quickly translate into sizeable economic value for both US and MENA partners alike. Trilogy will work closely with its American brand clients to achieve global growth by customizing services and solutions to assist clients in all phases of MENA business growth.

Trilogy Brands has built and maintains relationships with the premier fashion and lifestyle retail companies that own and operate the most prominent businesses in the MENA region. These businesses already operate a unique collection of hundreds of international brands across the entire region supported by solid management and considerable financial standing. Mall owners and operators in the MENA region are the largest owners of brand rights. This ensures that they bring the ultimate shopping experience to consumers and that they continue to attract foot traffic to their properties. Trilogy has also built a global ecosystem, a network to support your brand’s efforts in the region.

Trilogy Brands will negotiate and hold exclusive rights for the MENA region to a variety of brands today found throughout the US, predominantly those in metropolitan markets. These brand rights to representation will be presented by Trilogy to its local partners in the MENA region who will invest and develop the brands in the MENA region on a large scale. Trilogy Brands responsibilities include cultivating relationships, sourcing, establishing and maintaining new relationships with leading potential licensing partner groups. These groups are leading owners and operators of international brands in the region. Complementing this activity will be maintaining relationships in key growth markets with influencers such as sovereign wealth funds, prominent families, attorneys, bankers, professionals that know, have access to, and provide capital to these groups. MENA responsibilities also include organizing and conducting roadshows and presentations to showcase Trilogy-procured brands as well as related negotiation and execution of mutually beneficial terms for international brand licensing, revenue sharing, and franchising rights. Revenue split and/or license fee will be earned by the American brand owner and Trilogy, in exchange for its technical/management/infrastructure support.

5

Trilogy targets transactions with the following characteristics:

Size:

Retail brands originally developed in the US with 10 to 1,000+ units

US-based brands with current revenues generally under $500 Million

US-based brands that show continued growth and are ready to support international expansion

Industries:

Fashion

Accessories

Food and Beverage, Casual Dining

Entertainment

Sporting Goods

Action Sports

Supermarkets and Health Markets

Health, Fitness, Wellness, and Nutrition

Cosmeceuticals and Nutraceuticals

Multimedia and Electronics

E-Commerce and Mobile Applications

Home Furnishings

Education

Hotels and Leisure

Strategy:

Negotiate agreements with MENA regional partners to invest in and manage retail outlets throughout the region

Markets include GCC primary and secondary markets, including Levant, North Africa and CIS countries, predominantly

Focus on trendy brands and novel concepts that represent a draw for customers

Focus on brands established in major US metropolitan markets

Focus from fast casual dining to premium casual dining restaurants

Focus on mid-level price point brands preferred

Focus on brand quality and strong growth potential

Focus on scalable brands with franchise experience

6

WHY WORK WITH TRILOGY BRANDS?

Benefits for our clients and partners are that it is a highly lucrative, high growth model; that addresses a real problem and provides a high

competitive advantage, with a short timeframe to execute. We offer a real value solution to a real problem for US brands looking to attract

consumers and compete for profits. We provide immediate exposure and footprint for the brand translating into sizable economic value.

We build sustainable relationships, a “highway” for the introduction of American concepts into the Middle East. Business conducted in the

MENA region is based primarily on relationships and trust.

Unique relationships and business track record in the US and the Middle East, and a unique combination of expertise in finance, F&B,

fashion and retail. Knowledge, expertise, and customized approach a company needs to expand their brand into one of the hottest retail

markets in the world.

Harvard Business School-educated founder, combined with creative experience in the fashion trade and retail transaction history is an

“excellent” fit for the task at hand.

Managed a successful global investment banking firm while managing to be a notable member of numerous philanthropic causes globally.

The Founder was invited on three separate occasions to collaborate with the Office of His Highness Prince Charles on projects of global

significance, attended the World Economic Forum global symposium as a finance panelist by invitation of the organization, and was invited

to be a member of the International Economic Alliance conceived at Harvard and dedicated to global trade, development, investment, and

advancing business relations among nations.

Experienced deal maker, banker, and negotiator nationally and internationally for over 20 years, drawing from a decade long tenure of

doing business in the MENA region. Dealings in the region started when D’Amato arranged the financing of six large water production plants

in Iraq in 2006, followed by an in-depth analysis in order to commercialize product distribution and brand expansion into the MENA region,

and ultimately sourcing regional strategic and financial buyers culminating in the successful sale of the company to Pepsi in 2012.

Solid and credible partners in the region that can grow the brand aggressively, immediately unlocking and monetizing brand value which

makes for a compelling alliance with Trilogy with confidence of mutual success. Put financial capability aside (at over USD $1 billion cash on

balance sheet and access to international bond markets) these are well-run, strongly governed companies with high ethical standards and

thousands of employees managing hundreds of international brands. These are the most successful owners, developers, and operators of a

number of world-famous brands, engaged in sectors from shopping to entertainment, retail and property sectors, which makes for a

“compelling alliance” which Trilogy is confident of mutual success.

7

EXPANSION ANALYSIS

There is a strong need for American-based brands overseas. This is particularly true in the MENA region. Introduction of these brands by an experienced professional intermediary is the optimal way to connect with the strongest MENA operators. Trilogy has such expertise and therefore seeks formal engagements with American brand owners to represent their brands in the MENA region.

The world is brand-obsessed. Consumers want “American” products over all other products. You can look at the world’s 50 most innovative companies and find the answer: Apple, Google, Microsoft, Pixar, etc. Consumers want revolutionary, trendy, and experiential brands and they want them now.

Apple in China has officially surpassed the US as Apple’s biggest iPhone market. According to Warren Buffet, Coca Cola and Gillette, the two largest portfolio companies of Berkshire Hathaway, earn the vast majority of their profits abroad. Top US brands are participating in worldwide markets today and can still experience that early growth curve phenomenon. Marketshare is larger outside of the US for most top US brands because of the limited penetration of competing brands. American brands can thrive in other countries well after their US growth has stabilized. However, star and emerging American brands will rarely deploy in-house sales and licensing resources to the MENA region, choosing instead to allocate those resources to major markets such as China. This fact allows Trilogy a window to negotiate MENA brand representation today since the brand may be years or decades away from deploying a MENA expansion strategy.

The MENA region can be particularly attractive to American brands due to:

1. Young trend-oriented population 2. Rapid population growth 3. High spending power per capita 4. Favorable consumption habits 5. Regulated environment 6. Strong consumer protection 7. Emergence as a touristic destination 8. Inherent panache of “American” brand or product

The market for brand representation in MENA is untapped, with virtually no competition. The demographics of the MENA region are “extraordinary”. Dubai and Abu Dhabi lead the way in both real estate and hospitality demand and therefore continue to offer the highest returns.

8

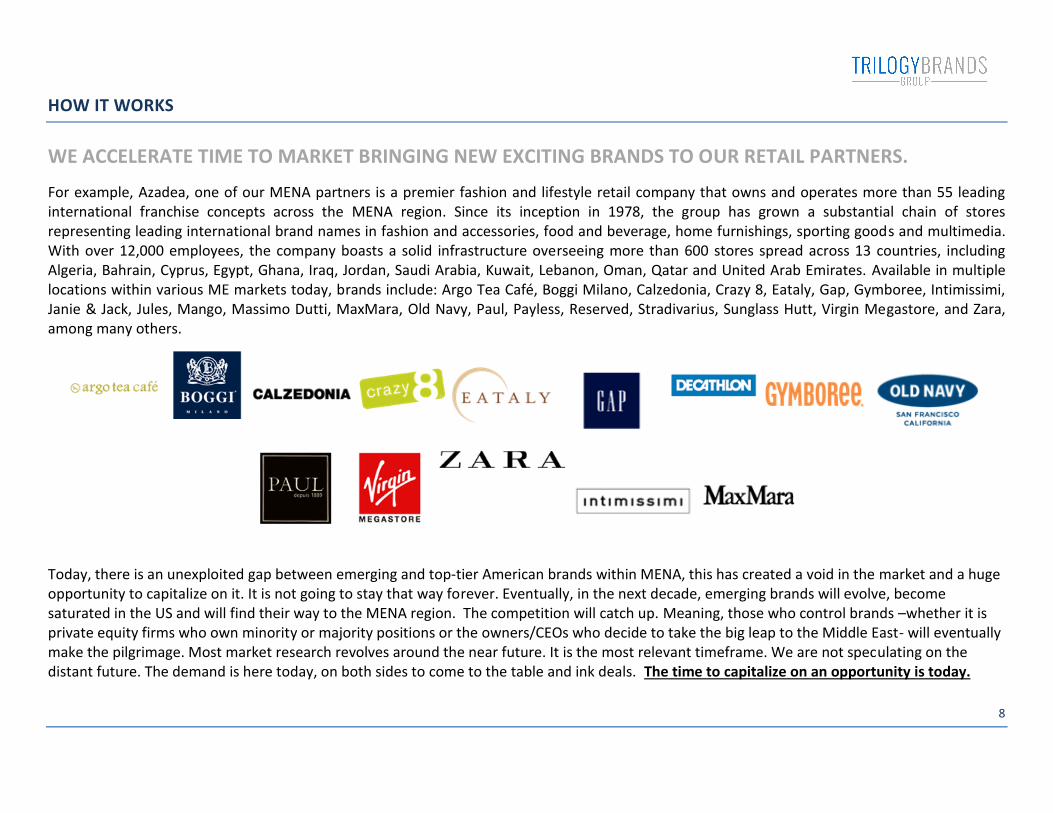

HOW IT WORKS

WE ACCELERATE TIME TO MARKET BRINGING NEW EXCITING BRANDS TO OUR RETAIL PARTNERS.

For example, Azadea, one of our MENA partners is a premier fashion and lifestyle retail company that owns and operates more than 55 leading international franchise concepts across the MENA region. Since its inception in 1978, the group has grown a substantial chain of stores representing leading international brand names in fashion and accessories, food and beverage, home furnishings, sporting goods and multimedia. With over 12,000 employees, the company boasts a solid infrastructure overseeing more than 600 stores spread across 13 countries, including Algeria, Bahrain, Cyprus, Egypt, Ghana, Iraq, Jordan, Saudi Arabia, Kuwait, Lebanon, Oman, Qatar and United Arab Emirates. Available in multiple locations within various ME markets today, brands include: Argo Tea Café, Boggi Milano, Calzedonia, Crazy 8, Eataly, Gap, Gymboree, Intimissimi, Janie & Jack, Jules, Mango, Massimo Dutti, MaxMara, Old Navy, Paul, Payless, Reserved, Stradivarius, Sunglass Hutt, Virgin Megastore, and Zara, among many others.

Today, there is an unexploited gap between emerging and top-tier American brands within MENA, this has created a void in the market and a huge opportunity to capitalize on it. It is not going to stay that way forever. Eventually, in the next decade, emerging brands will evolve, become saturated in the US and will find their way to the MENA region. The competition will catch up. Meaning, those who control brands –whether it is private equity firms who own minority or majority positions or the owners/CEOs who decide to take the big leap to the Middle East- will eventually make the pilgrimage. Most market research revolves around the near future. It is the most relevant timeframe. We are not speculating on the distant future. The demand is here today, on both sides to come to the table and ink deals. The time to capitalize on an opportunity is today.

9

REVENUE MODEL

Trilogy Brands will provide introductions and will negotiate on behalf of or in cooperation with the US client. In return, Trilogy will receive a percentage of the up-front fees and royalties, in the form of an annuity stream or a cash lump sum to be determined on a per transaction basis.

Typically, a MENA partner will pay up-front fees to the American brand owner anywhere from $100,000 per country to several million per territory depending on the strength of the brand, and a brand royalty 4-8% of revenues subject to a Master License Agreement (MLA), Master Franchise Agreement (MFA), or Area Development Agreement (ADA). Trilogy counsel has substantial expertise in the legal construction of these agreements subject to MENA legal jurisdiction.

Below are some examples of the many transactions –in F&B alone- which have recently entered the market:

10

California Pizza Kitchen expanded into the MENA region in the past few years with one of the largest franchise partners from the UAE. The new 5,500 SF store seated approx. 200 people, located in the Dubai Mall, and two other locations were set to open. The partners later on renegotiated the agreement to include growth of at least 19 stores throughout the region.

Denny’s, the world’s largest full service family dining chain, announced plans in 2014 to open 30 new restaurants in the MENA region. Denny’s signed a franchise agreement with a restaurant master franchise investor in the MENA region for the development of its restaurants in 9 countries over the next 10 years. The partner has the exclusive rights to open in the UAE, Saudi Arabia, Qatar, Bahrain, Kuwait, Egypt, Lebanon, Iraq, and Jordan. The first location opened in the UAE in 2015.

The Habit, in 2015, entered the MENA region with the same operator under a franchise agreement. This was the brand’s first international agreement for the development of 50 new restaurants across the region over the next 10 years. The Habit is a Southern California brand which owns over 100 restaurants in the US. This agreement represents an immediate 50% growth in size for the US brand and a major positioning ahead of competitors backed fully by one of the strongest players in the region.

Shake Shack is one of the most successful new brands in the MENA region. Originated in New York, the brand only had a handful of locations in the US. It wasn’t until 2000 when it gained recognition as a brand. They opened their first MENA location in Saudi Arabia in late 2013 and the Mall of the Emirates in the UAE in 2014. They flew the meat chilled (not frozen) from the US in order to maintain the consistent quality experienced in the US stores. In the US, Shake Shack was not a very strong brand, but it had great brand value “for the MENA region”. The model was scalable and replicable in international markets and not surprisingly did EXTREMELY well in the MENA region. The same ME partner brought The Cheesecake Factory, Texas Roadhouse, PF Chang’s and PizzaExpress to the region in 2014.

IHOP entered the MENA region in 2012 through a franchise agreement with a prominent Kuwaiti Group. The first IHOP opened in a prime location in the Mall of the Emirates, one of the largest malls in the Middle East drawing over 31 Million visitors a year. The restaurant featured the brand’s largest international design with 225 seated guests and opened 7 days a week including late night dining. This was a year after the news that IHOP had filed bankruptcy, and yet its brand value was significant in the MENA region.

Steak n Shake, a US burger restaurant company, signed in 2013 an exclusive deal with a Saudi Group to open 50 of its restaurants in Saudi Arabia, and an international development agreement with a second group in the UAE to open 40 restaurants in the country. The burger chain, owned by Biglari Holdings, said that this deal was part of its plan to further its global expansion to the Middle East and Europe. Steak n Shake was founded in 1934 and operates over 520 restaurants.

11

The same is true for brands outside of F&B, in Fashion and Retail predominantly. Abercrombie & Fitch Co., announced in 2013 a joint venture with a leading pioneer in the region, and only months later it opened a second store. Hollister, also part of the Abercrombie ‘s holding company, has also successfully launched in the region. Hollister launched in the UAE in Mall of the Emirates in early 2014 with the highest ever opening day sales for the US brand, and has since gone on to open 2 further stores in Yas Mall and Dubai Mall in the UAE. In 2015 the partners are in discussion of a new store openings as the brand is performing exceptionally well. Carrefour is an excellent example of the value creation and significant impact a ME partner can have on foreign brands. Carrefour, one of the largest French hypermarket chains in the world, is a great story for the region. They were introduced to the ME in 1995. The transaction was a 25% JV paying royalty to Carrefour France. As of 2005 revenues were reported at $1 Billion out of 13 stores. And in 2007, just 2 years later, revenues rose to $2.5 Billion together with aggressive regional growth. By 2015, the ME partner had bought out significant shares of the parent company to a 75% ownership for USD $750 million and recently extended the partnership for 10 more years to 2024 to expand their franchise to 40 countries throughout the Middle East (from 19), creating a significant first mover advantage for the foreign brand that has lasted over 2 decades and is going strong, meanwhile, providing an important exit strategy for the brand stepped out over time, together with a sizeable infusion of capital to the parent company. US restaurants and retailers are waking up, following the money to the MENA region. In the restaurant space alone, there has been an explosion of interest in the region. Friday’s, PF Chang’s, and Applebee’s owned by DineEquity are growing by putting new spins on their menu, while Smashburger and Darden Restaurants are just getting started having entered into international growth franchise agreements on some of their brands in the last few years.

For American brands, the time to act is now or they will be left behind in the most significant consumer markets in the world. It is a race against time to cut deals and cement growth capital with MENA partners who eventually can become viable exits for the brands. Competition for American brands in the MENA region is most prevalent from UK brands, especially those that build concepts as “knock-offs” of American brands, in order to fill in the void created by a lack of dialogue and familiarity of US businessmen with the MENA region.

12

BEST IN CLASS BUSINESS PARTNER

Trilogy Brands is partners with Hilco Global, a consumer-focused investor known for its international expertise with offices in North America, Europe, Asia-Pacific, Central and South America. Hilco is a strategic partner with management expertise in both opportunistic and distressed situations. Hilco acts as a principal and operator of strategic brands. Recent investments include some of the world’s most iconic brands such as: Halston, Haute Hippie, HMV, Polaroid, Altec Lansing + Nick Jonas, and more.

HILCO IS A PREEMINENT GLOBAL AUTHORITY ON DERIVING MAXIMUM VALUE SOLUTIONS FOR ASSETS WITH DEEP EXPERIENCE IN MAJOR APPAREL, RETAIL AND RESTAURANT INDUSTRIES, PARTICULARLY IN AREAS OF ASSET MONETIZATION, VALUATION, AND ADVISORY.

Hilco has the ability to act as advisor, agent, investor, and/or principal in every transaction. Hilco's Real Estate team focuses on innovative and strategic solutions for restaurants, including repositioning of leases, restructuring, asset protection, rent reduction, renewal, sublease, assignments, termination, and sale leasebacks, including property brokerage and principal acquisition services. Hilco has produced more than 1,500 real estate appraisals annually and more than 35,000 lease transactions resulting in over $4 Billion dollars of value for clients.

Over the last 30 years, Hilco has built one of the most successful retail practices in the global marketplace that focuses on servicing retailers from strategy to execution. Hilco's Retail Solutions team focuses on performance enhancement and cost optimization for retailers, as well as managing of store closings and inventory disposition. Hilco is the largest provider of retail inventory solutions in the world having monetized over $150 Billion dollars of retail inventory.

13

14

15

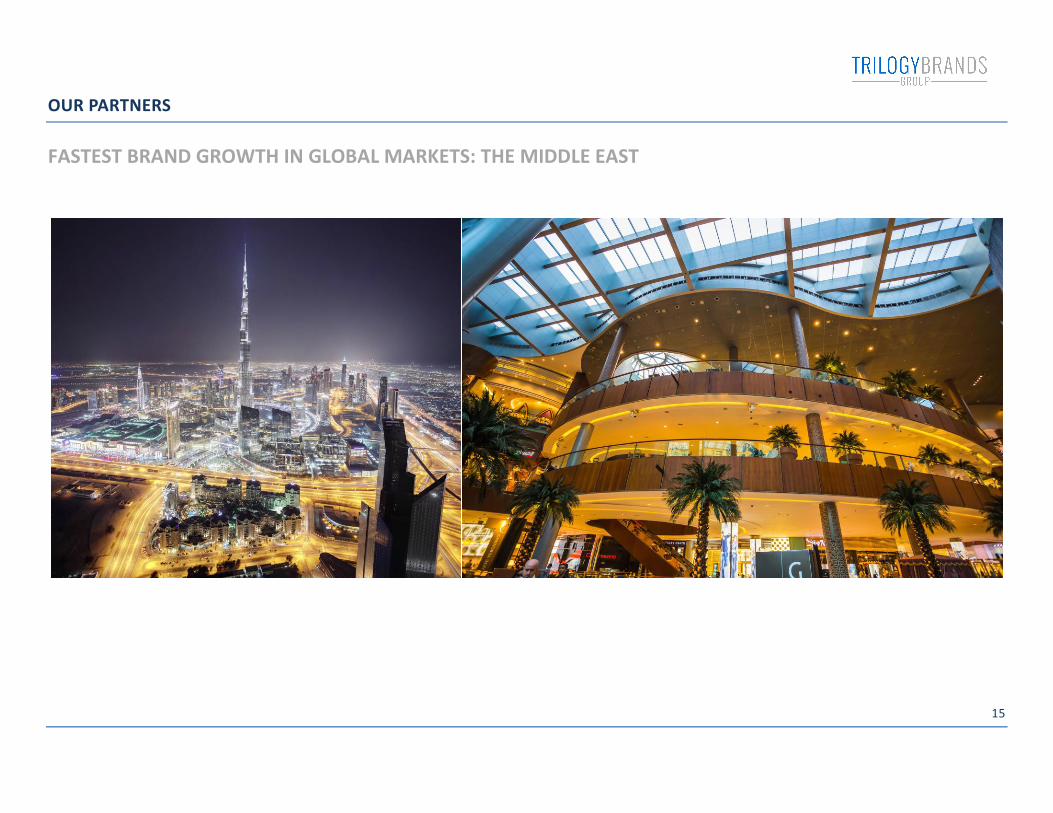

OUR PARTNERS

FASTEST BRAND GROWTH IN GLOBAL MARKETS: THE MIDDLE EAST

16

THE MIDDLE EAST TODAY

The UAE has long been the vanguard of major international retailers’ expansion strategies, with the GCC region comprised of 22 countries and at least 40 strong submarkets. Brands can grow much faster and more successfully under a franchised or licensed arrangement with a mega-regional partner rather than by operating as an independent. The sheer amount of retail space in Dubai alone –one square meter for every one of its 2.3 Million residents- coupled with extreme weather have made malls places to be, not just to shop. Jeddah and Riyadh offer unbeatable locations as the gateway to the economic capital of the largest economy in the MENA region, while Doha is gearing up for the World Cup bid in 2022. Markets like Egypt are increasingly relevant, while Kuwait, Oman and Bahrain offer strong underlying country fundamentals.

Dubai has ranked #1-5 in the world in tourism and hospitality consumer markets for the last decade; and is ranked #2-3 market in the world - -second only to London in terms of the world’s most popular retail city and the number of retail brands that are currently operating in the market. In recent announcements at Expo 2020, Dubai is set to become one of the leading F&B destinations in the world. Dubai and London are in the top retail city rankings followed only by the established markets of New York, Paris, Moscow, and Hong Kong, which clearly still hold considerable global pulling power. Dubai isn’t just the most important retail destination, but it has been ranked among the world’s top five “hot markets” attracting the most number of new retailers and tracking the most cross-border retail movement, with a commitment to doubling those numbers and number of visitors to the region by 2020.

The UAE is home to the world’s largest malls. The Dubai Mall alone –the largest mall in the world by total area- encompasses 13 Million square feet of space equivalent in size to more than 50 football fields. Retailers see it as a safe haven in an affluent region with abundant modern, well-trafficked malls. Its aggressive investment attitude and diversification across brands, countries and business lines, which includes multimedia, furniture outlets, restaurants and real estate, supported by rapid growth is what makes the region so active and vibrant. Sports and beaches are part of Dubai’s draw, but the key is inside the shopping malls. The UAE is typically the most profitable region for any brand that successfully positions itself in that market; while Saudi Arabia represents a much larger market with significant potential. For retailers seeking a wide swath of consumers, the Middle East is the most promising market in the world. Retailers and brands in the midrange, see a very aspirational component to the people living in the Middle East. There is nominal competition from local retailers. Salaries are very broad and so is the range of nationalities. Per capita GDP is the highest in the world, but more importantly, the UAE has the highest per capita spending in the world.

17

In 2015 malls in the Middle East earned $1,800 in average revenues per square foot annually compared to $666 in average revenues per square foot for malls in the US. Shopping centers such as Mall of the Emirates in Dubai have ranked over the past five years as the number 1 to number 7 shopping center in the world when measuring gross annual sales revenues. Today, the GCC’s total retail space exceeds 100 million square feet and it is estimated to grow 46% a year. The GCC retail market is set to reach $270 Billion USD in retail sales in 2016 (UAE $54 Billion) with sales densities per square foot per year consistently reaching $1,800 per square foot of gross leasable area (“GLA”).

In Dubai, Mall of the Emirates is 2.5 million sf of GLA and Dubai Mall is 3.77 million sf of GLA, and both are undergoing significant expansion to GLA. In Doha, Villagio, Mall of Qatar and Doha Festival Center are all super regional malls with areas of up to 2.9 million sf. Kuwait with Avenue and 360 Mall also boasts large scale shopping centers with areas of nearly 4 million sf of GLA.

In comparison with the US, Dubai offers 14,800 square feet of retail space per 1,000 people (highest in the world) whereas in the US the ratio is 11,000 for every 1,000 people. The US retail sector market size of $5 Trillion is however much larger than the GCC at $270 Billion.

Consumers in the UAE spend most of their income on housing with over 41% of total consumer spending. Food and beverage is the second most significant consumer spending category with a 14% share, followed by transport, communications, apparel and footwear each at under 10% of spending.

Infrastructure in the GCC overall is improving every year at an accelerated pace. Increased power and water generation capabilities enable the growth of large scale retail developments. New airports and efficient tourist visa handling procedures enable large numbers of people to travel easily and freely for leisure and shopping excursions. New brands are flocking to the region looking to increase their reach globally and to penetrate the lucrative GCC customer and tourist. Shoppers spend on average 5 hours of shopping sprees. Tourism remains a key driver for the GCC retail industry with tourist arrivals in the GCC expected to reach 44.4 million in 2016.

18

THE MIDDLE EAST TOMORROW

In the next few years, the Middle East will simply be unrecognizable.

The region is building dozens of mega malls, but is also building new artificial islands, new airport projects, mega green communities, infrastructure projects, aerospace projects, mega theme park projects, mega hotels and resorts, coupled with the latest in technological innovation.

Saudi Arabia for example has emerged as one of the fastest growing hospitality industries in the region as a result of religious tourism boosted by the expansion of the two Holy Mosques, which attract millions of Muslims every year. Colliers expects visitors to Makkah (Mecca) and Madinah to reach 25 million by 2025, from just over 17.5 million last year.

Mega Malls

The region is booming and building dozens of new mega malls –as well as massive extensions to existing high profile shopping destinations. Top 10 mega malls under construction today include:

Al Diriyah Festival City Mall, Riyadh, KSA Saudi Arabia: Built by Al Futtaim Group in Saudi’s capital city, Riyadh, the $1.6 Billion project involves construction of a mixed use development spread over an area of 250,000 sqm.

Mall of Egypt, Cairo, Egypt: Set to be complete in 2015 and with an area of 162,500 square meters (2 levels), Mall of Egypt will feature around 400 shops, including a range of international fashion and lifestyle retail brands, a ski park, a 17-screen cinema complex and a family entertainment center along with 50 food and beverage outlets. It is developed by UAE-based retailer Majid Al Futtaim (MAF) in Cairo.

19

Mall of the Emirates expansion, Dubai, UAE: Phase 2 of one of the UAE’s largest malls, dubbed ‘Evolution 2015’, will add 25,000 sqm in gross leasable area (GLA). Mall of the Emirates’ multi-stage redevelopment, worth more than $272 Million, includes a new 24 screen VOX Cinemas and further entertainment, dining and retail experiences with 12 new food and beverage options and parking space for more than 1,300 cars. The second phase of the expansion was completed in 2015.

Nakheel Mall, Dubai, UAE: Located on Dubai’s Palm Jumeirah, Nakheel Mall will feature 200 stores, including a Waitrose and two anchor department stores, 12 restaurants, six medical clinics and a nine-screen cinema. The project is worth $680 Million and is scheduled to be completed by 2016. The mall is being developed by Dubai firm Nakheel and will have a 50-story hotel alongside it.

Mall of the World, Dubai, UAE: Construction work on the Dubai-based, $6.8 billion project by Dubai Holding which began in 2015. Ibn Battuta Mall expansion, Dubai, UAE: Nakheel will build the new extension is in addition to Ibn Battuta Mall's phase 2 complex, currently

under construction and due to open in 2016, bringing the total size of Ibn Battuta to more than 650,321 sqm. The Pointe Mall, Dubai, UAE: Situated at the tip of Palm Jumeirah, the retail and entertainment complex is being developed by Dubai firm

Nakheel. The project is worth $217 Million and will be completed by end of 2016. Mall of Oman, Muscat, Oman: Mall of Oman is being developed by UAE retailer MAF in the Bauwsher district, will be the country’s largest

shopping and will feature a Carrefour outlet, VOX Cinemas and Magic Planet. It is scheduled for completion in 2017 and is worth $467 Million. Doha Festival City, Doha, Qatar: Owned and developed by Bawabat Al Shamal Real Estate Company (BASREC) and UAE-based Al Futtaim Real

Estate services, the project will feature the country’s only IKEA and will debut 550 new brands in Qatar. Mall of Qatar, Doha, Qatar: Adjacent to a World Cup stadium, the mall will be the country’s largest, phase 1 opened in 2015 and subsequent

phases will open in 2016-2017. It will feature 425 retail, dining and entertainment brands from all over the world as well as 50 luxury brands.

Mega Hotels

The region is building mega-resorts and hotels. In 2016, two key markets in the Middle East reported more than 20,000 rooms under construction: Makkah (Mecca) Saudi Arabia, reported the largest number of rooms under construction with 21,068 rooms in 13 new hotels, followed by Dubai, United Arab Emirates with 20,882 rooms in 67 new hotels under construction. Riyadh, Saudi Arabia reported 6,738 rooms in 30 new hotels; and Doha, Qatar 5,980 rooms in 26 new hotels. The busiest years for hotel openings will be 2017 and 2018 including the Paramount Hotel in Dubai and the Hard Rock Hotel in Abu Dhabi. There are 183 new hotel projects and 54,000 hotel rooms in the UAE pipeline alone. The majority of these hotels are expected to open by 2020.

Mega Theme Parks

New theme parks and leisure facilities that will boost tourism and attract visitors from around the world make this region one of the most exciting in the world. The world market for theme parks is forecast to exceed $31.8 Billion by 2017 and the Middle East, Asia Pacific and Latin America are set to lead that growth, according to Global Industry Analysts.

20

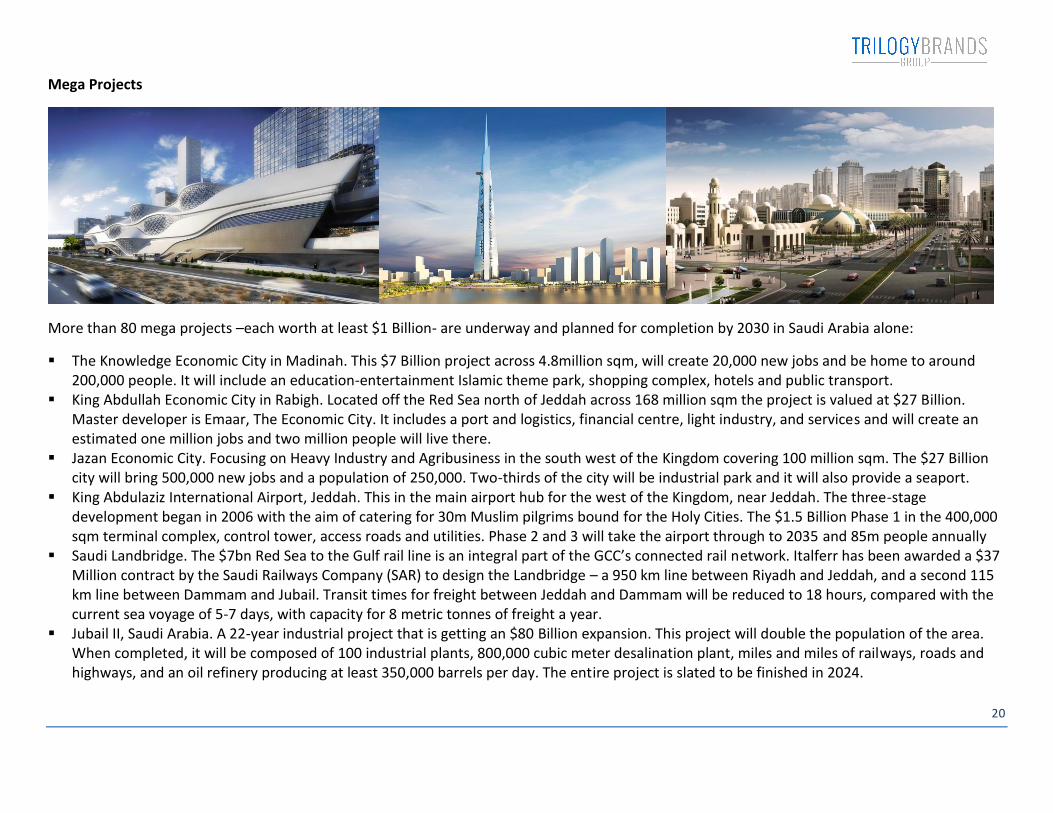

Mega Projects

More than 80 mega projects –each worth at least $1 Billion- are underway and planned for completion by 2030 in Saudi Arabia alone:

The Knowledge Economic City in Madinah. This $7 Billion project across 4.8million sqm, will create 20,000 new jobs and be home to around 200,000 people. It will include an education-entertainment Islamic theme park, shopping complex, hotels and public transport.

King Abdullah Economic City in Rabigh. Located off the Red Sea north of Jeddah across 168 million sqm the project is valued at $27 Billion. Master developer is Emaar, The Economic City. It includes a port and logistics, financial centre, light industry, and services and will create an estimated one million jobs and two million people will live there.

Jazan Economic City. Focusing on Heavy Industry and Agribusiness in the south west of the Kingdom covering 100 million sqm. The $27 Billion city will bring 500,000 new jobs and a population of 250,000. Two-thirds of the city will be industrial park and it will also provide a seaport.

King Abdulaziz International Airport, Jeddah. This in the main airport hub for the west of the Kingdom, near Jeddah. The three-stage development began in 2006 with the aim of catering for 30m Muslim pilgrims bound for the Holy Cities. The $1.5 Billion Phase 1 in the 400,000 sqm terminal complex, control tower, access roads and utilities. Phase 2 and 3 will take the airport through to 2035 and 85m people annually

Saudi Landbridge. The $7bn Red Sea to the Gulf rail line is an integral part of the GCC’s connected rail network. Italferr has been awarded a $37 Million contract by the Saudi Railways Company (SAR) to design the Landbridge – a 950 km line between Riyadh and Jeddah, and a second 115 km line between Dammam and Jubail. Transit times for freight between Jeddah and Dammam will be reduced to 18 hours, compared with the current sea voyage of 5-7 days, with capacity for 8 metric tonnes of freight a year.

Jubail II, Saudi Arabia. A 22-year industrial project that is getting an $80 Billion expansion. This project will double the population of the area. When completed, it will be composed of 100 industrial plants, 800,000 cubic meter desalination plant, miles and miles of railways, roads and highways, and an oil refinery producing at least 350,000 barrels per day. The entire project is slated to be finished in 2024.

21

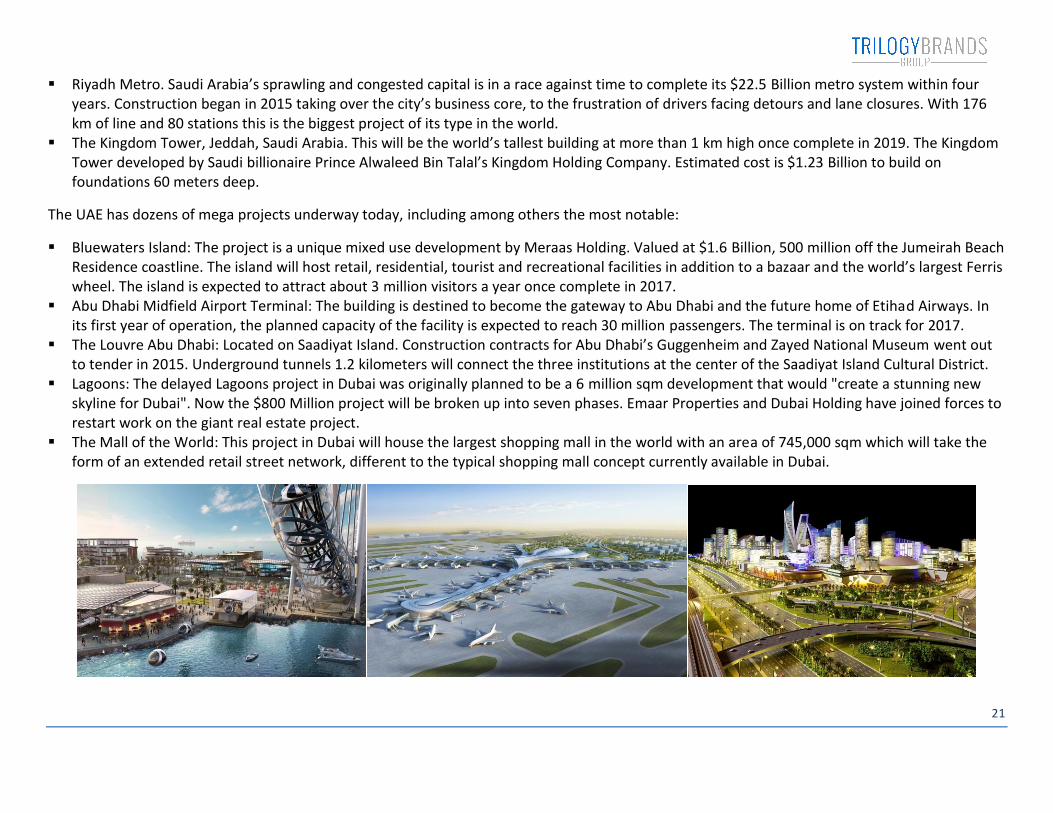

Riyadh Metro. Saudi Arabia’s sprawling and congested capital is in a race against time to complete its $22.5 Billion metro system within four years. Construction began in 2015 taking over the city’s business core, to the frustration of drivers facing detours and lane closures. With 176 km of line and 80 stations this is the biggest project of its type in the world.

The Kingdom Tower, Jeddah, Saudi Arabia. This will be the world’s tallest building at more than 1 km high once complete in 2019. The Kingdom Tower developed by Saudi billionaire Prince Alwaleed Bin Talal’s Kingdom Holding Company. Estimated cost is $1.23 Billion to build on foundations 60 meters deep.

The UAE has dozens of mega projects underway today, including among others the most notable:

Bluewaters Island: The project is a unique mixed use development by Meraas Holding. Valued at $1.6 Billion, 500 million off the Jumeirah Beach Residence coastline. The island will host retail, residential, tourist and recreational facilities in addition to a bazaar and the world’s largest Ferris wheel. The island is expected to attract about 3 million visitors a year once complete in 2017.

Abu Dhabi Midfield Airport Terminal: The building is destined to become the gateway to Abu Dhabi and the future home of Etihad Airways. In its first year of operation, the planned capacity of the facility is expected to reach 30 million passengers. The terminal is on track for 2017.

The Louvre Abu Dhabi: Located on Saadiyat Island. Construction contracts for Abu Dhabi’s Guggenheim and Zayed National Museum went out to tender in 2015. Underground tunnels 1.2 kilometers will connect the three institutions at the center of the Saadiyat Island Cultural District.

Lagoons: The delayed Lagoons project in Dubai was originally planned to be a 6 million sqm development that would "create a stunning new skyline for Dubai". Now the $800 Million project will be broken up into seven phases. Emaar Properties and Dubai Holding have joined forces to restart work on the giant real estate project.

The Mall of the World: This project in Dubai will house the largest shopping mall in the world with an area of 745,000 sqm which will take the form of an extended retail street network, different to the typical shopping mall concept currently available in Dubai.

22

Tourism and Hospitality: Deloitte predicts visitor growth of between 7% and 10% in the region, on target to achieve 20 million visitors per year by 2020

Dubai has ranked 5th in 2014 global destination cities with 12 million international overnight visitors up 7.5% from prior year

UAE could undertake Paris and Singapore within 5 years, to reach 3rd place behind London and Bangkok

Dubai International Airport surpassed London Heathrow as the busiest international airport in the world with 70 million passengers

Hospitality market in the region performed strong in the past few years. Dubai and Jeddah had the highest average occupancies at 80% and

experiencing 9% growth annually

Dubai also plans to become one of the leading medical tourism hubs globally with 500,000 tourists and $700 Billion in revenues by 2020

Economy: Fall in oil prices were predicted to have a limited impact on ME’s economy as most primary economies have reduced reliance on the oil

industry for over three decades, notably, sales of oil constitute only 6% of Dubai’s economy

Sizeable investments under way will further enhance the attractiveness of ME’s business environment for foreign companies and tourism

Population growth has the potential to drive continued demand for residential and retail assets

Real GDP growth in the UAE, for instance, averaged 4.8% in 2000-2015, above the global economic rate of 2.8%

UAE per capita GPD is $44K vs. the world’s per capital GDP $13K

The region boosts some of the fastest growing cities in the world and is recognized as a top 10 improver in the world

Retail: Demand for destination retail was strong driven by growth in resident spend, a relatively large demographic of young affluent adults,

increased tourist demand and visitors, increased disposable income, and growth in GDP

The Dubai Mall attracted a record 80 million visitors in 2015, equal to over 200,000 shoppers a day

Demand in the retail market will drive greater divergence between prime and secondary malls. Super prime and mega malls will continue to

experience growth in visitors, while residents will drive demand for convenience and non-mall retail

Social media in the Middle East is active with 64% of the population using Facebook and 71% using Twitter. Widespread access to internet

and the prevalence of smart phones, PCs and tablets, indicate that a gradual growth in e-commerce penetration will continue as internet

payment security improves, the number of retail websites increase, and retailers continue to establish logistics and supply chains

The impact of increased online retail will result in a growth in retail revenue, predominantly from electronic goods, which is unlikely to draw

revenue from malls as these will remain a key part of the lifestyle in the region for shopping, socializing, dining, and entertainment

Dubai’s status as a leading retail destination globally is predicted by Deloitte to continue to drive demand from world renowned retailers

23

Dubai Plan 2021

Dubai is a successful story that echoes in all corners of the globe. It is a convergence point of potentialities and opportunities, and a gateway to the

entire world. Dynamic Dubai is built on innovation, creativity, quality and commitment. These pillars have helped Dubai’s ambitious quest towards

sustaining excellence and stability across all sectors of the economy, which in turn has transformed the community lifestyle and ushered in a new

era of progress and prosperity. Over four decades, Dubai has emerged as the fulcrum between east and west, connecting the major trade routes of

Africa, Asia and Europe, and a magnet for global investors. Today, Dubai is a leader in many sectors and stands shoulder to shoulder with the

economic powerhouses of the world.

Dubai Plan 2021 aims to reinforce Dubai’s position as a global city, a leading tourist destination and the preferred business center of the Middle

East. In the past 7 years, the emirate has experienced a resurgence of ambitious initiatives, programs and projects. These include winning the right

to host the World Expo in 2020, the strategic plan to leverage Dubai’s culture and expertise to become the capital of the Islamic economy, and

comprehensive investments in the emirate’s tech infrastructure that have come full circle with the Dubai Smart City plan. According to the plan, by

2021, Dubai will be a smart and sustainable city that cultivates happy, creative, and empowered people, who are backed and supported by a

proactive and reliable smart government.

H.H. Sheikh Mohammed bin Rashid Al Maktoum

PRIME MINISTER OF THE UAE AND RULER OF DUBAI

24

NEXT STEPS

WE KNOW WHAT IT TAKES TO BUILD A PROFITABLE BUSINESS IN INTERNATIONAL MARKETS WHILE KEEPING YOUR BRAND CONSISTENT, AUTHENTIC, AND RELEVANT

ULTIMATELY LEADING TO STRONG BRAND EQUITY

Trilogy Brands Group is changing the old corporate model of global expansion and turning it on its head. We offer a real value solution to a real problem for US brands looking to attract consumers and compete for profits. Trilogy is at the forefront of the knowledge economy providing the business savvy needed to make better executive decisions, gain a better perspective on and an understanding of opportunities for growth in the MENA region.

TIME IS CRITICAL AND THE TIME TO ACT IS NOW. TRILOGY BRANDS OFFERS THE KNOWLEDGE AND EXPERTISE A COMPANY NEEDS TO EXPAND THEIR BRAND INTO ONE OF THE HOTTEST CONSUMER MARKETS IN THE WORLD.

Global is the new local. CEOs not currently targeting the region have nothing to lose and only upside by entering into a regional representation agreement with Trilogy. American brands are eager to engage in dialogue and will choose Trilogy Brands as a conduit to jump start their international presence, ahead of their competitors. That’s the name of the game.

It takes a highly differentiated skillset, global connections, resources, expertise in foreign markets, familiarity, unique entrepreneurship skills, and a “cultural understanding” that most American business professionals do not personally possess. Trilogy has a 10 year head start on any competition that might emerge. This is the Trilogy competitive edge and the value proposition that Trilogy Brands brings to the market.

Trilogy Brands also offers American brands the opportunity to immediately connect exceptional brands with solid global operators who today can grow a brand exponentially; and tomorrow, at the right time, potentially become an exit for these brands.

WELCOME TO THE RETAIL REVOLUTION. A REVOLUTION THAT IS ABOUT SPEED TO MARKET.

Consumers globally identify with a brand and want to experience that product today. Not 10 or 20 years from now when the brand is finally ready to enter new world markets. Trilogy’s MENA partners want to give their consumers what they want and have built fertile grounds for brands to thrive in their region. CEOs of American brands are now ready and are joining the retail revolution.

25

FOUNDER STORY

26

INFLUENCER AND CREATIVE CONSULTANT FOCUSING ON BRAND DEVELOPMENT AND GROWTH.

SOUGHT AFTER SPEAKER ON LEADERSHIP, FINANCE, AND ENTREPRENEURSHIP.

VISIONARY CHANGE AGENT FOR WOMEN AND YOUTH.

GLOBAL CATALYST.

AND NEXT GENERATION GLOBAL CITIZEN.

Quintessential deal-maker driving business growth for clients in the US and worldwide, with broad experience in all aspects of: Global Transaction Services, Growth Strategies, Capital Funding, Corporate Finance, M&A, Global Brand Development, Licensing and Franchising. Highly motivated to source, negotiate and execute on regional and cross-border transactions unlocking brand value. Unique expertise and status having managed a successful global investment banking firm while managing to be a notable member of philanthropic and humanitarian causes globally, having collaborated with the Office of HH The Crown Prince of Dubai and HRH The Prince of Wales on projects of global significance. Invited member of the International Economic Alliance dedicated to global trade, development, investment, advancing business relations among nations.

Finance Panelist and Speaker for the World Economic Forum, one of the most prestigious members-only world leaders’ organizations shaping the world today, comprised of 1,000 of the world’s top corporations. Invited as Innovation Forum Speaker at the Global Restaurant Leadership Conference representing over $2.7 Trillion in foodservice revenues. Honored at the Women in Business Awards by the OC Business Journal, recognizing outstanding professional women with significant contributions to organizations, professions, and community in Southern California. Lived and worked in United States, Europe, Middle East, Africa, and Latin America. Speaks multiple languages. Received a Post Graduate degree in Global Business Management from Harvard Business School, becoming alumni alongside some of the world’s most prominent leaders.

27

Trilogy Brands Group LLC Barbara D’Amato, CEO / Managing Partner

9701 Wilshire Blvd. Suite 1000 Beverly Hills, CA 90212 USA

US cell +1 949 922-2295 / UAE cell +971 50 929-3870 [email protected]

www.trilogybrandsgroup.com

DISCLAIMER: THIS DOCUMENT IS FURNISHED TO THE PARTIES WHO HAVE EXPRESSED AN INTEREST IN EVALUATING A BUSINESS OPPORTUNITY UNDER TRILOGY BRANDS GROUP LLC. THIS DOCUMENT IS DISCLOSED TO YOU

FOR INFORMATIONAL PURPOSES ONLY AND ITS CONTENTS SHALL REMAIN STRICTLY CONFIDENTIAL. THIS DOCUMENT DOES NOT CONSTITUTE AN OFFER TO SELL OR A SOLICITATION TO BUY UNITS OR STOCK IN ANY

COMPANY. THE DOCUMENT AND ITS CONTENTS ARE THE PROPERTY OF TRILOGY BRANDS GROUP LLC AND SHALL BE RETURNED WHEN REQUESTED. ALL DEVELOPMENT AND DESIGN OF CORPORATE MATERIALS CREATED

BY OR IN COLLABORATION WITH TRILOGY BRANDS GROUP INCLUDING, CONCEPT, MODEL, BRAND IDENTITY, DESIGN, AND AN OTHER DOCUMENTS OF THE COMPANY AND/OR ITS CLIENTS, SHALL REMAIN THE OWNERSHIP

OF TRILOGY BRANDS GROUP AS SOLE OWNER OF RESERVED RIGHTS AND COPYRIGHTS AVAILABLE UNDER THE LAW. RECIPIENT ACKNOWLEDGES THAT NO REMEDY OF LAW MAY BE ADEQUATE TO COMPENSATE TRILOGY

BRANDS GROUP FOR A VIOLATION OF THE ABOVE BY RECIPIENT; AND RECIPIENT HEREBY AGREES THAT IN ADDITION TO ANY LEGAL OR OTHER RIGHTS THAT MAY BE AVAILABLE IN THE EVENT OF A BREACH HEREUNDER,

TRILOGY BRANDS GROUP MAY SEEK EQUITABLE RELIEF TO ENFORCE THIS AGREEMENT.

LOS ANGELES NEW YORK DUBAI