Embed Size (px)

Citation preview

“Trends and Vision”I. New Data Driven Business Models

Moderator: John CallanCo-Founder/Chairman

PostalVision 2020

The New Delivery RealityAaron JacksonManaging Director, Accenture Federal Services

Accenture

The Prime Membership EcosystemCooper SmithDirector of Research

L2

Copyright © 2017 Accenture All rights reserved. |

Achieving High Performance in

The Post and Parcel Industry

Copyright © 2017 Accenture All rights reserved. | 2

A DECADE OF RESEARCHACCENTURE POSTAL AND PARCEL RESEARCH

Copyright © 2017 Accenture All rights reserved. |Copyright © 2017 Accenture All rights reserved. | 3

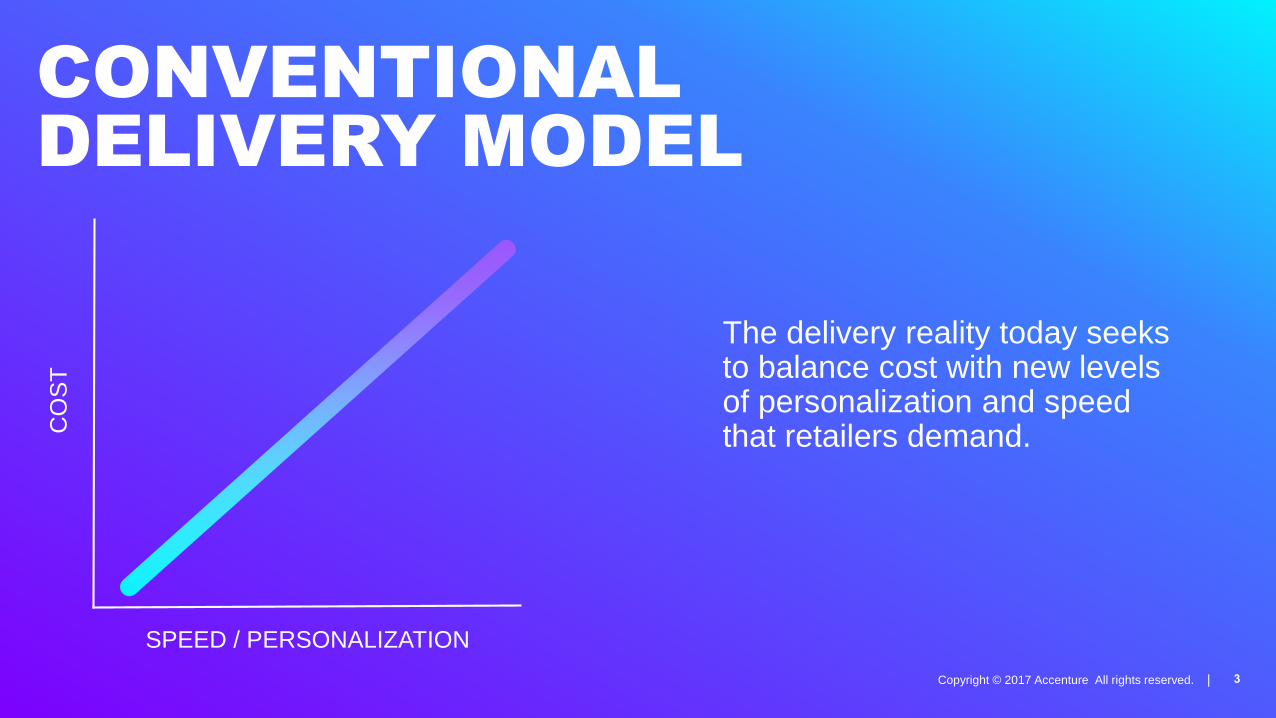

The delivery reality today seeks to balance cost with new levels of personalization and speed that retailers demand.

CONVENTIONAL

DELIVERY MODEL

SPEED / PERSONALIZATION

CO

ST

Copyright © 2017 Accenture All rights reserved. | 4

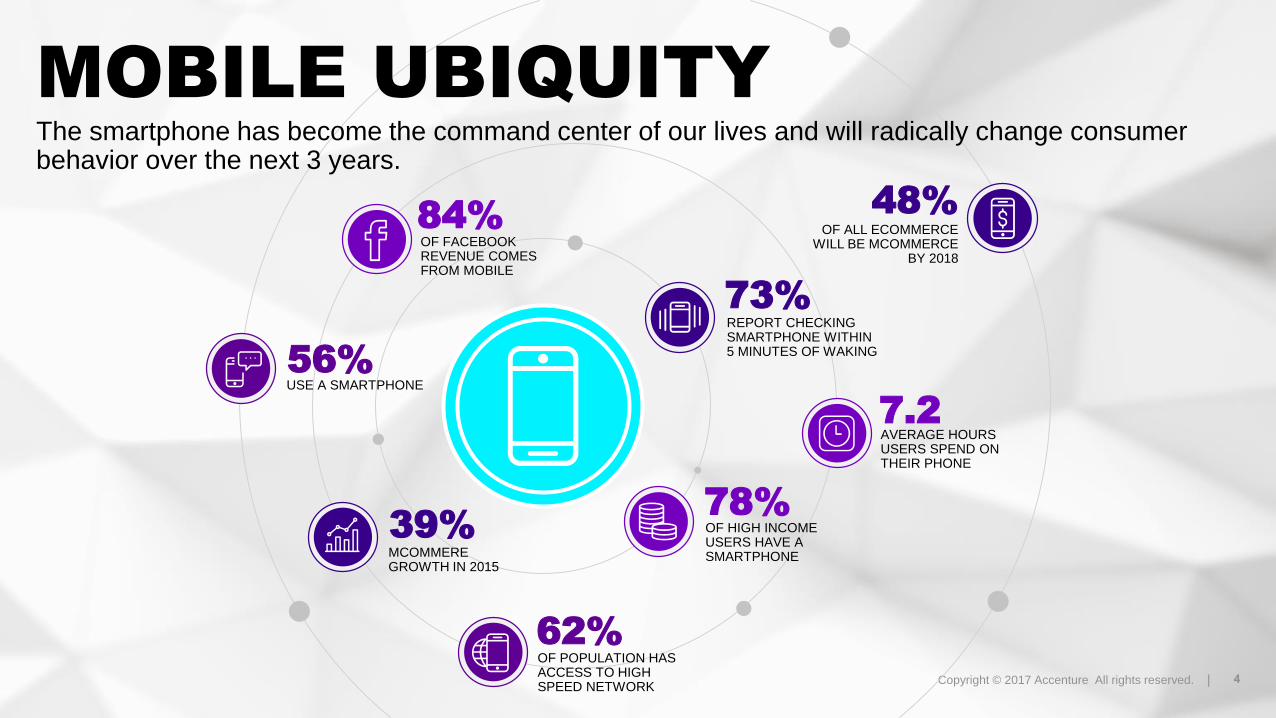

MOBILE UBIQUITYThe smartphone has become the command center of our lives and will radically change consumer behavior over the next 3 years.

56%

48%OF ALL ECOMMERCE

WILL BE MCOMMERCE BY 2018

73%

39%

84%

AVERAGE HOURS USERS SPEND ON THEIR PHONE

OF FACEBOOK REVENUE COMES FROM MOBILE

USE A SMARTPHONE

MCOMMERE GROWTH IN 2015

78%OF HIGH INCOME USERS HAVE A SMARTPHONE

REPORT CHECKING SMARTPHONE WITHIN5 MINUTES OF WAKING

7.2

62%OF POPULATION HAS ACCESS TO HIGH SPEED NETWORK

Copyright © 2017 Accenture All rights reserved. | 5

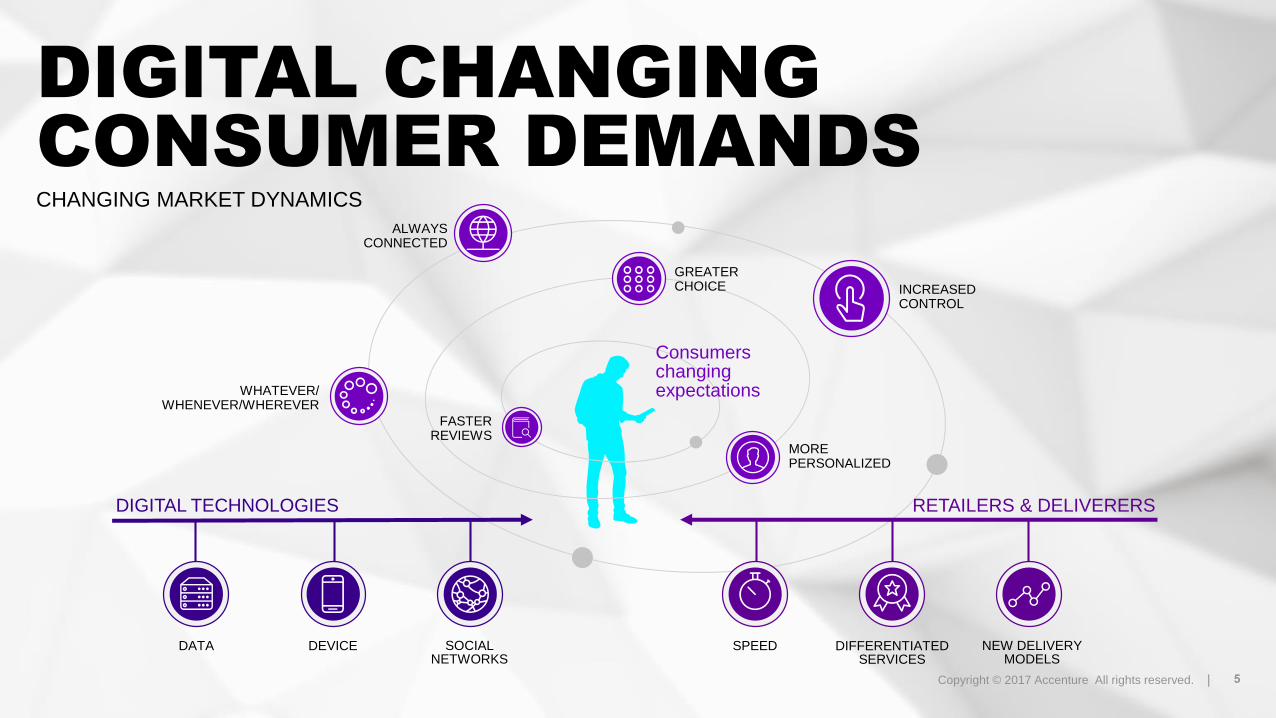

DIGITAL TECHNOLOGIES

DATA DEVICE SOCIAL NETWORKS

SPEED DIFFERENTIATED SERVICES

NEW DELIVERY MODELS

ALWAYS CONNECTED

INCREASED CONTROL

WHATEVER/WHENEVER/WHEREVER

MORE PERSONALIZED

GREATER CHOICE

FASTER REVIEWS

Consumers changing expectations

CHANGING MARKET DYNAMICS

DIGITAL CHANGING

CONSUMER DEMANDS

RETAILERS & DELIVERERS

Copyright © 2017 Accenture All rights reserved. | 6

RETAIL AND SHIPPING

CONVERGENCE

86%of consumers consider delivery to be part of their online shopping experience

70%of respondents overall would not or likely not shop with a retailer that has an inconvenient /costly return policy

33%of online shoppers have had a bad experience

Copyright © 2017 Accenture All rights reserved. | 7

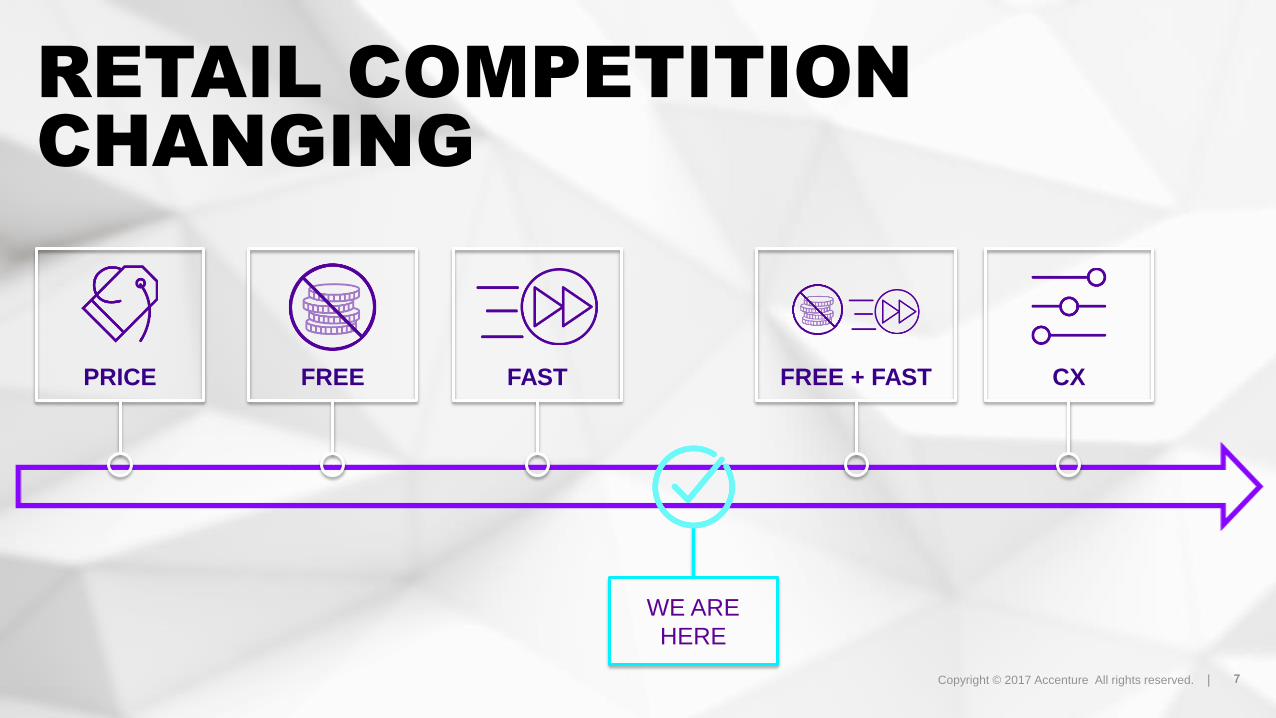

RETAIL COMPETITION

CHANGING

WE ARE

HERE

PRICE FREE FAST FREE + FAST CX

Copyright © 2017 Accenture All rights reserved. |

DIGITAL

TRANSFORMING RETAILTo address these new demands, retailers are investing in new capabilities that will change the landscape.

INVENTORY PROXIMITY

ALTERNATE DELIVERY OPTIONS

CONSUMER INTIMACY

BORDERLESS PRODUCT ACCESS

Copyright © 2017 Accenture All rights reserved. | 9

5

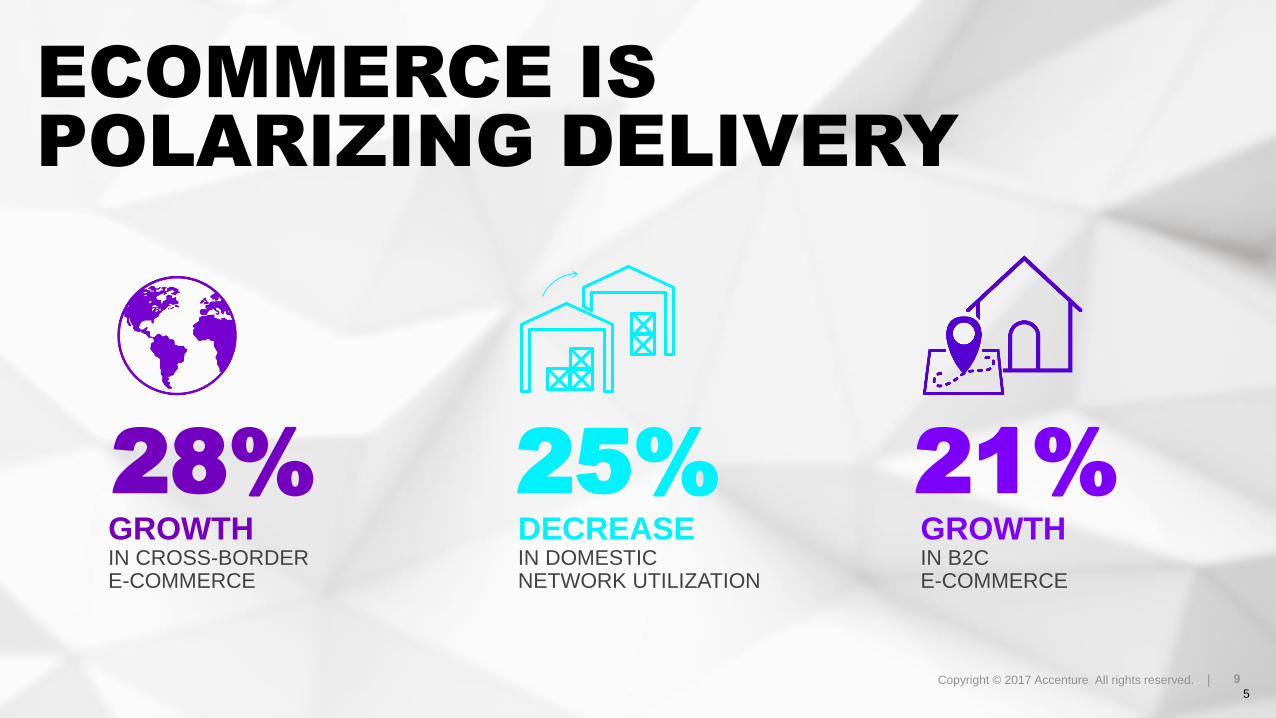

ECOMMERCE IS

POLARIZING DELIVERY

28%GROWTHIN CROSS-BORDER E-COMMERCE

21%GROWTHIN B2C E-COMMERCE

25%DECREASEIN DOMESTIC NETWORK UTILIZATION

Copyright © 2017 Accenture All rights reserved. | 10

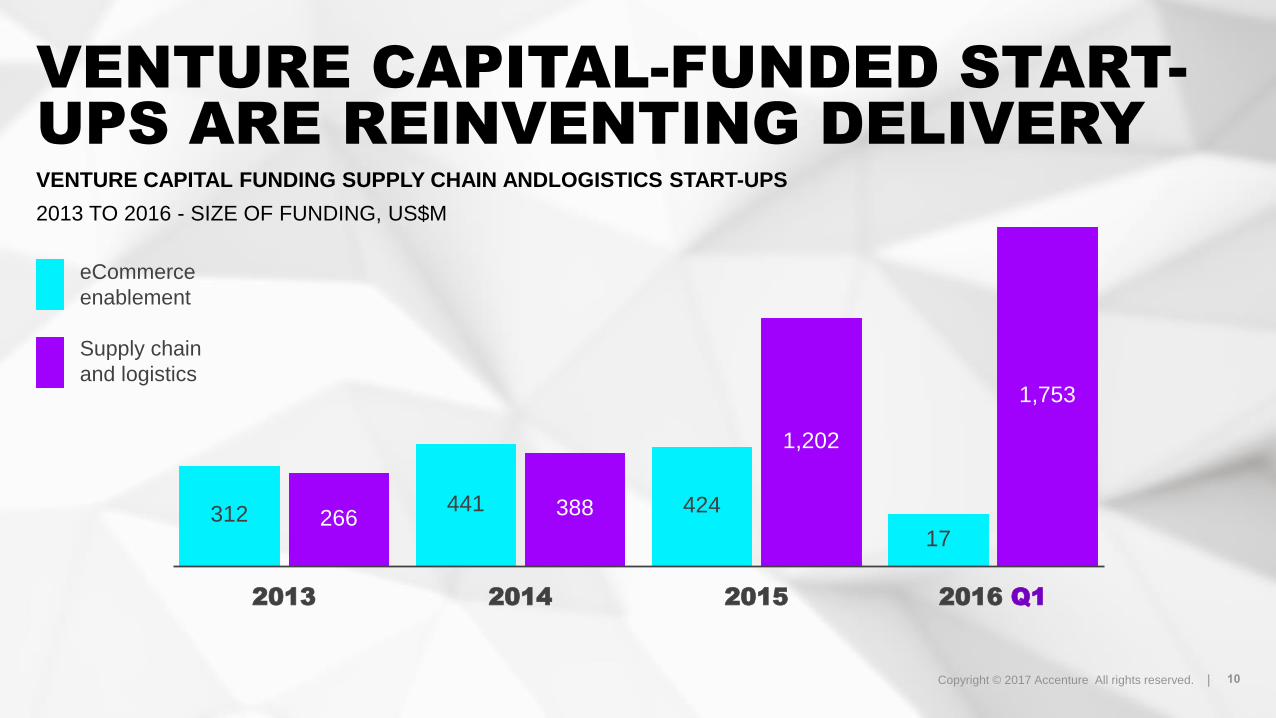

2013 2014 2015 2016 Q1

312 266441 388 424

1,202

1,753

17

eCommerce

enablement

Supply chain

and logistics

VENTURE CAPITAL-FUNDED START-

UPS ARE REINVENTING DELIVERY

VENTURE CAPITAL FUNDING SUPPLY CHAIN ANDLOGISTICS START-UPS

2013 TO 2016 - SIZE OF FUNDING, US$M

Copyright © 2017 Accenture All rights reserved. | 11

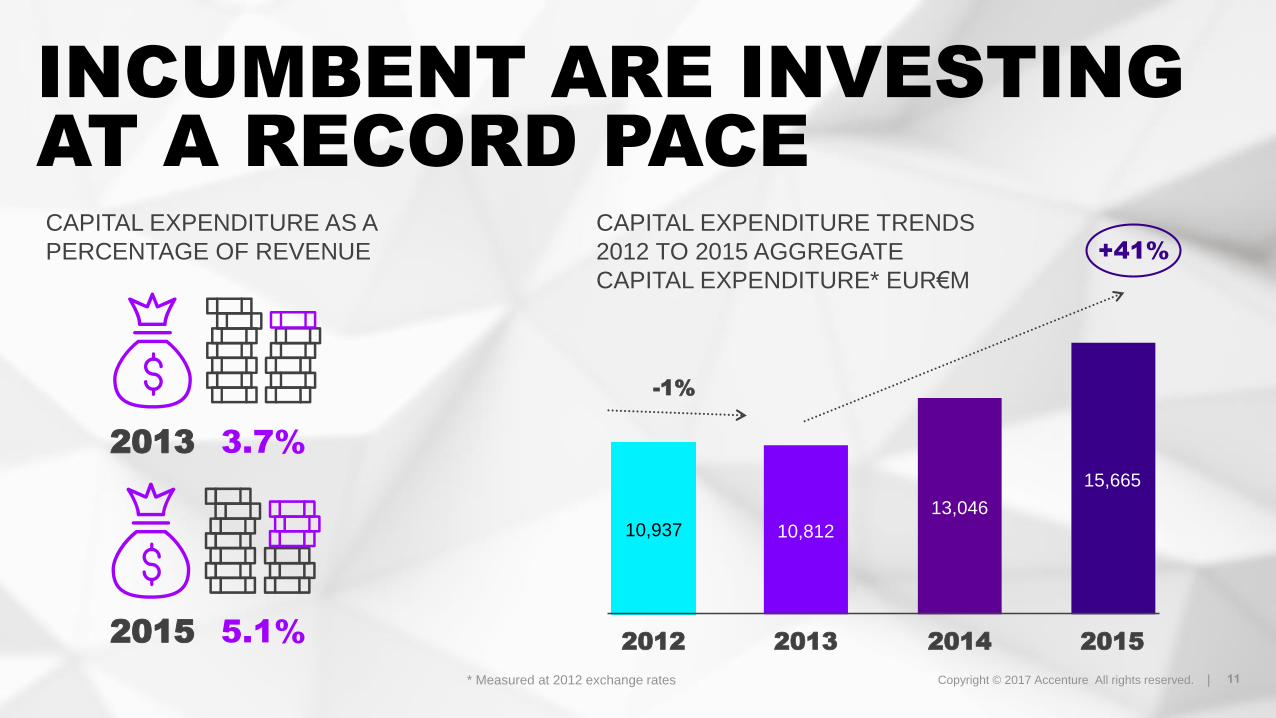

CAPITAL EXPENDITURE TRENDS

2012 TO 2015 AGGREGATE

CAPITAL EXPENDITURE* EUR€M

* Measured at 2012 exchange rates

2012 2013 2014 2015

+41%

-1%

15,665

13,046

10,81210,937

2013 3.7%

CAPITAL EXPENDITURE AS A

PERCENTAGE OF REVENUE

INCUMBENT ARE INVESTING

AT A RECORD PACE

2015 5.1%

Copyright © 2017 Accenture All rights reserved. | 12

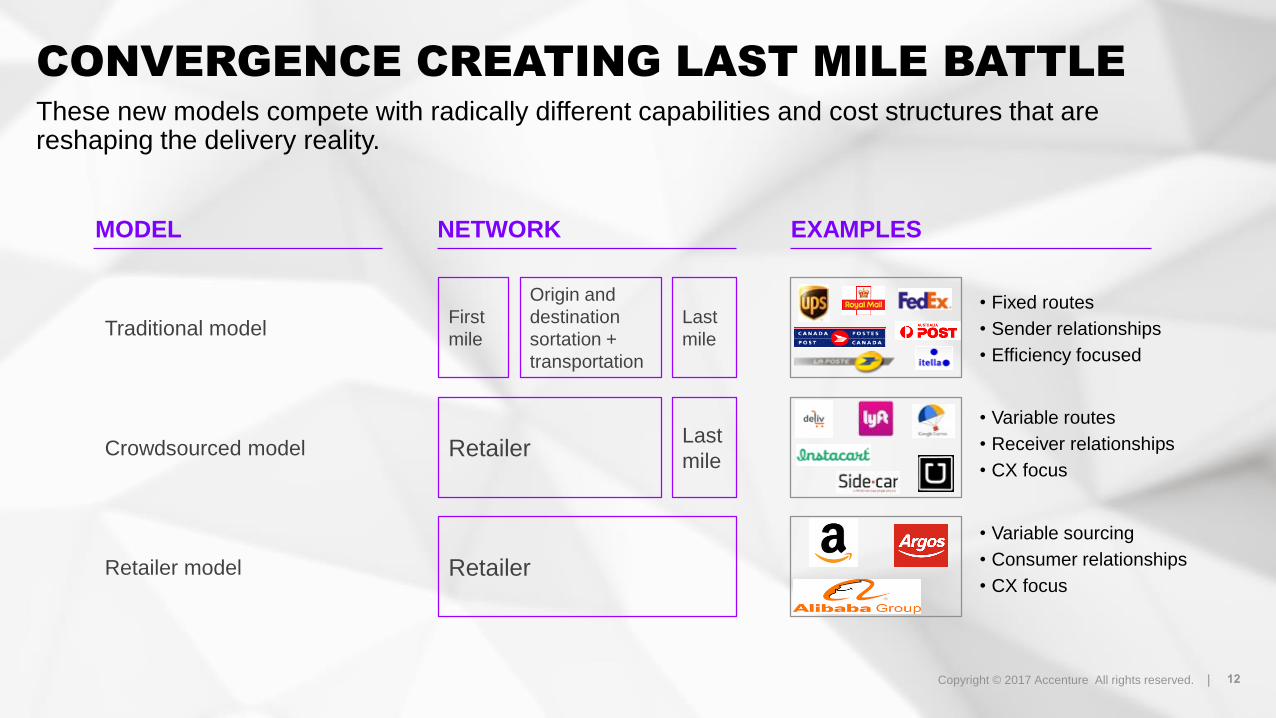

Traditional model

Retailer model

First

mile

Last

mile

Origin and

destination

sortation +

transportation

Retailer

MODEL NETWORK EXAMPLES

CONVERGENCE CREATING LAST MILE BATTLE

These new models compete with radically different capabilities and cost structures that are reshaping the delivery reality.

• Fixed routes

• Sender relationships

• Efficiency focused

• Variable routes

• Receiver relationships

• CX focus

• Variable sourcing

• Consumer relationships

• CX focus

Crowdsourced modelLast

mileRetailer

Copyright © 2017 Accenture All rights reserved. | 13

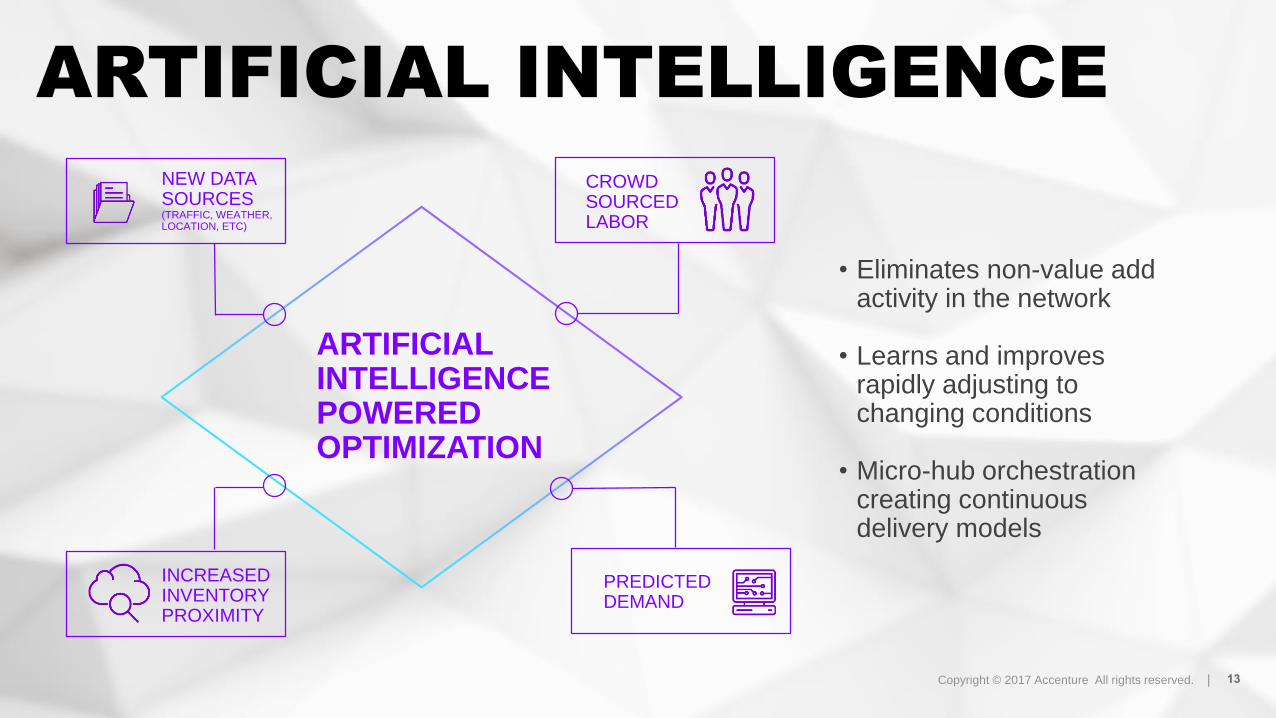

• Eliminates non-value add activity in the network

• Learns and improves rapidly adjusting to changing conditions

• Micro-hub orchestration creating continuous delivery models

ARTIFICIAL INTELLIGENCE

ARTIFICIAL INTELLIGENCE POWERED OPTIMIZATION

INCREASED INVENTORY PROXIMITY

NEW DATA SOURCES (TRAFFIC, WEATHER, LOCATION, ETC)

CROWDSOURCED LABOR

PREDICTED DEMAND

Copyright © 2017 Accenture All rights reserved. |Copyright © 2017 Accenture All rights reserved. | 14

These new capabilities significantly reduce the cost of new, advanced personalization and speed.

ARTIFICIAL

INTELLIGENCE

AI DRIVEN MICRO-NODE

New Reality

Old Reality

SPEED / PERSONALIZATION

CO

ST

Copyright © 2017 Accenture All rights reserved. | 15

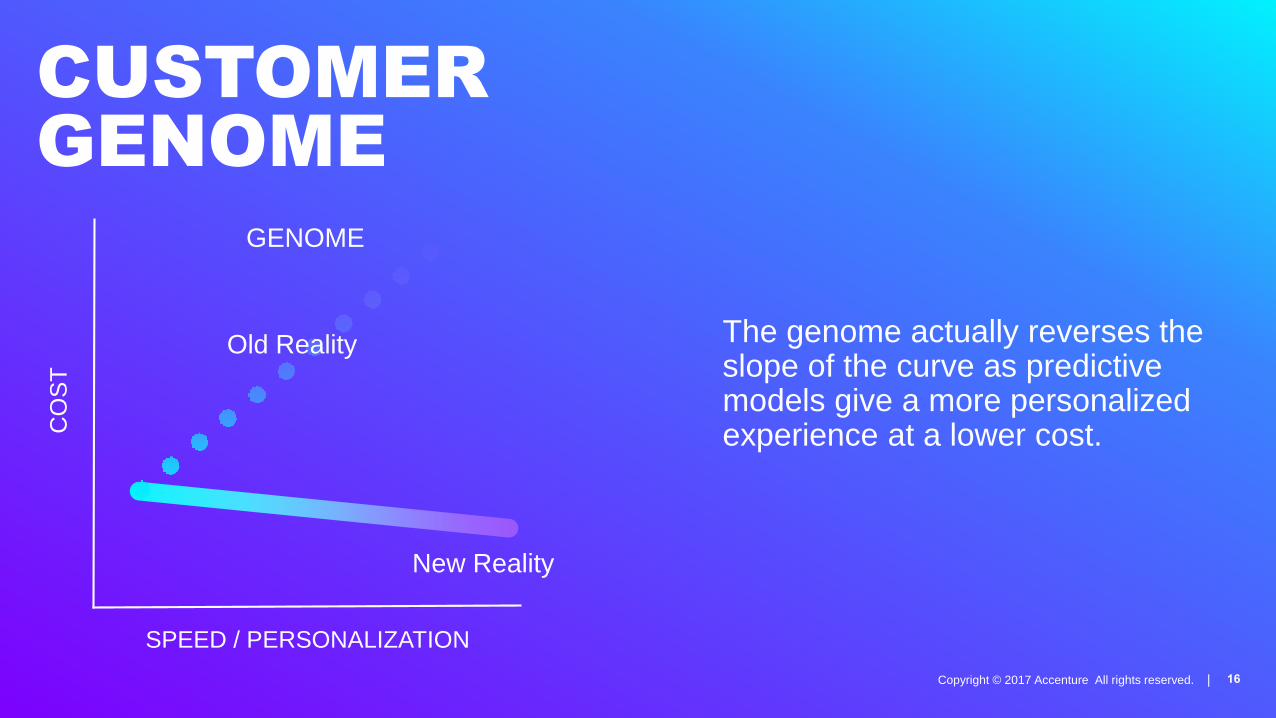

CUSTOMER DATA AS THE DIFFERENTIATOR

• Collecting preference and behavior data

• Turning insight into personalized actions

• Anticipatory delivery experiences

CUSTOMER

GENOME

Copyright © 2017 Accenture All rights reserved. |Copyright © 2017 Accenture All rights reserved. | 16

The genome actually reverses the slope of the curve as predictive models give a more personalized experience at a lower cost.

CUSTOMER

GENOME

SPEED / PERSONALIZATION

CO

ST

GENOME

New Reality

Old Reality

Copyright © 2017 Accenture All rights reserved. | 17

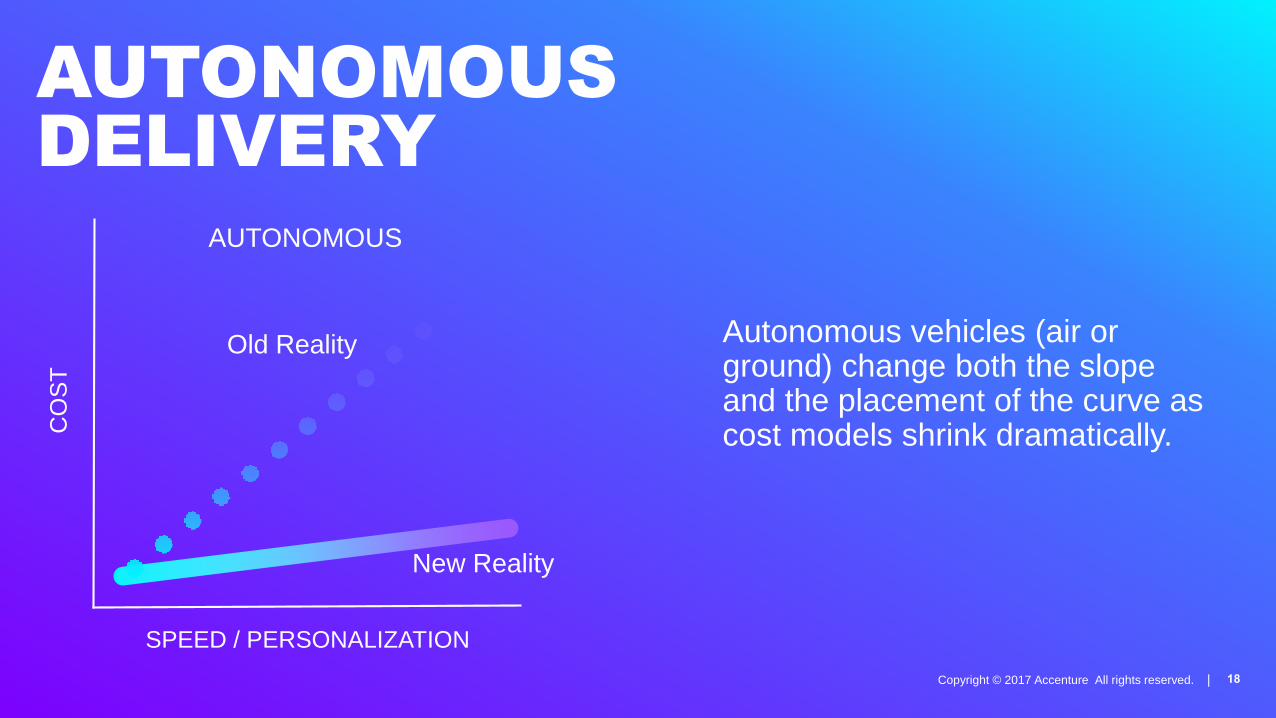

AUTONOMOUS

DELIVERY

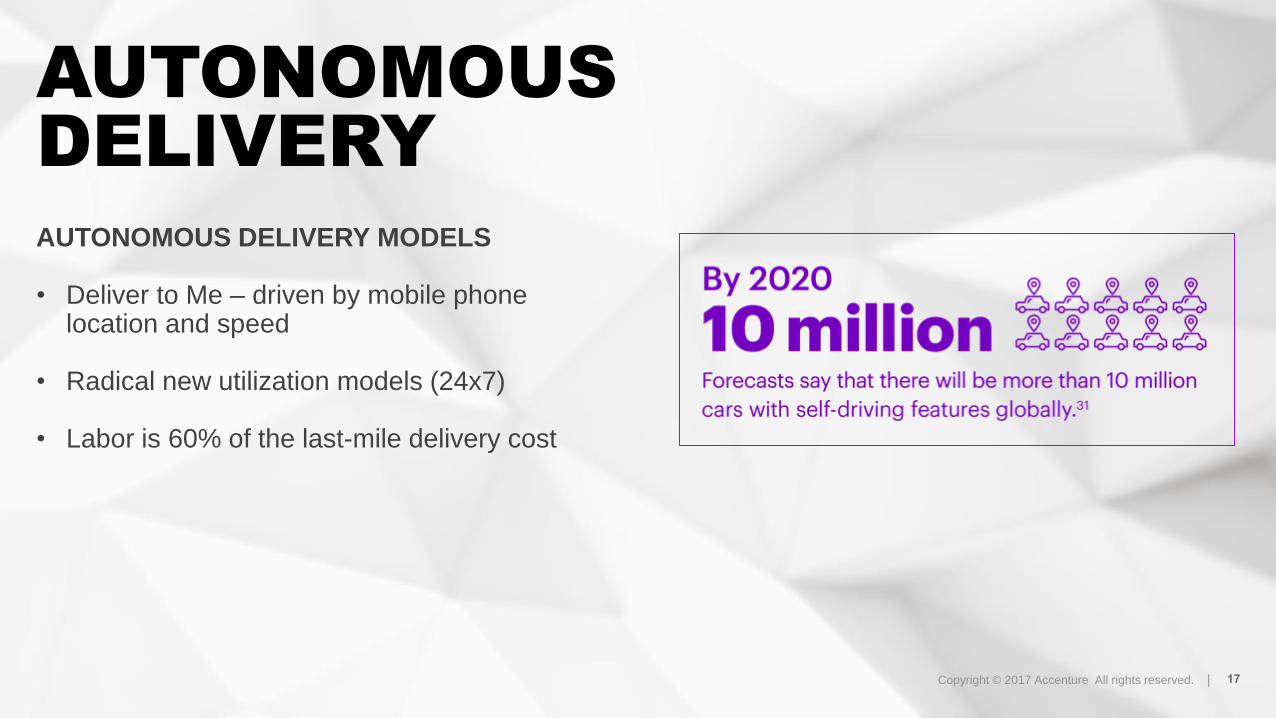

AUTONOMOUS DELIVERY MODELS

• Deliver to Me – driven by mobile phone location and speed

• Radical new utilization models (24x7)

• Labor is 60% of the last-mile delivery cost

Copyright © 2017 Accenture All rights reserved. |Copyright © 2017 Accenture All rights reserved. | 18

Autonomous vehicles (air or ground) change both the slope and the placement of the curve as cost models shrink dramatically.

AUTONOMOUS

DELIVERY

AUTONOMOUS

SPEED / PERSONALIZATION

CO

ST

New Reality

Old Reality

Copyright © 2017 Accenture All rights reserved. | 19

THE NEW DELIVERY

REALITY

New growth curves emerge as

transactions become frictionless

FRICTIONLESS TRANSACTIONS

Addressable market expands

as delivery becomes seamless

SEAMLESS DELIVERY

eCommerce transition accelerates

as delivery becomes ubiquitous

UBIQUITOUS DELIVERY

Copyright © 2017 Accenture All rights reserved. | 20

THANK YOU

Aaron

JacksonManaging DirectorAccenture Federal Services

Aaron Jackson

AMAZON

THE FOURTH HORSEMANCOOPER SMITH

AGENDA

1. AMAZON VS. RETAIL

2. UNDERSTANDING AMAZON

3. DEEP DIVE: APPAREL

AMAZON VS. RETAIL

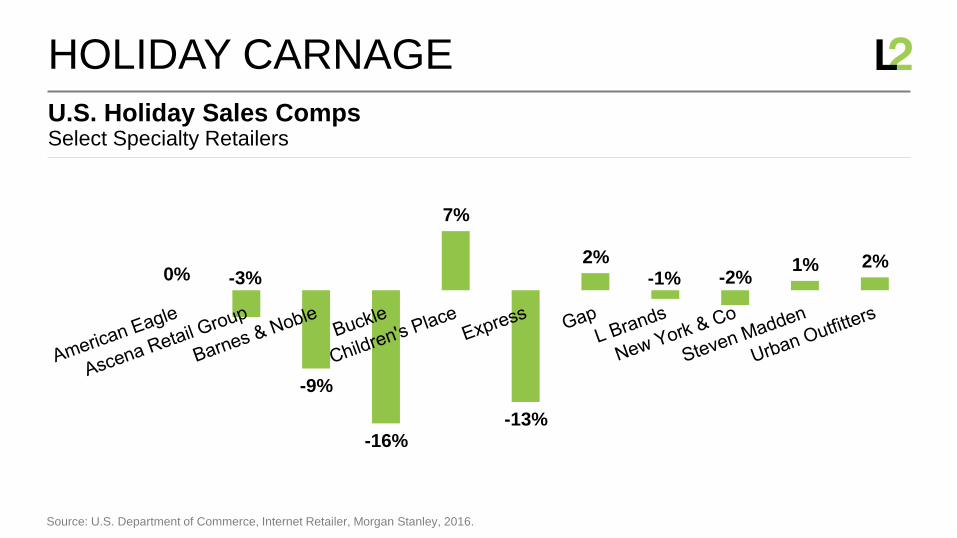

Select Specialty RetailersU.S. Holiday Sales Comps

HOLIDAY CARNAGE

Source: U.S. Department of Commerce, Internet Retailer, Morgan Stanley, 2016.

0% -3%

-9%

-16%

7%

-13%

2%-1% -2%

1% 2%

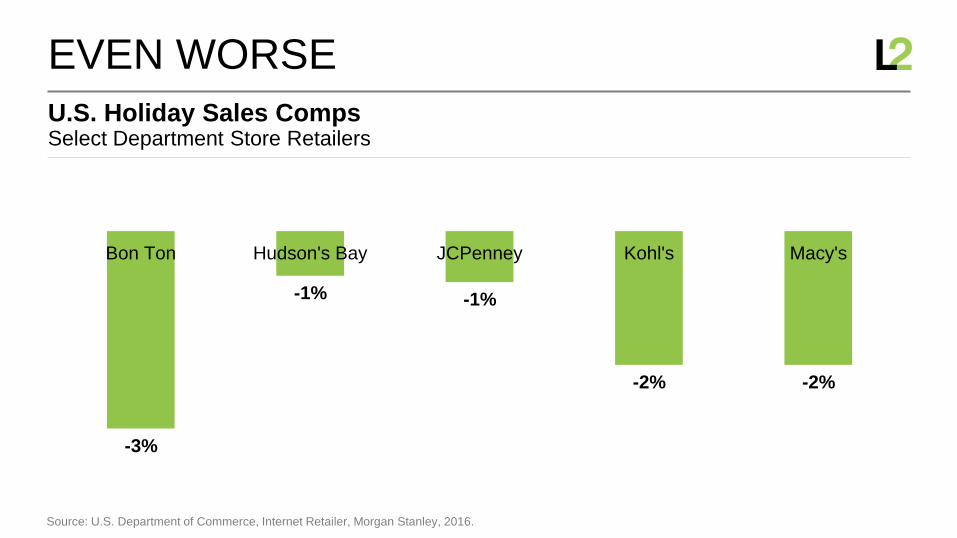

Select Department Store RetailersU.S. Holiday Sales Comps

EVEN WORSE

Source: U.S. Department of Commerce, Internet Retailer, Morgan Stanley, 2016.

-3%

-1% -1%

-2% -2%

Bon Ton Hudson's Bay JCPenney Kohl's Macy's

“We have had our best

holiday ever”

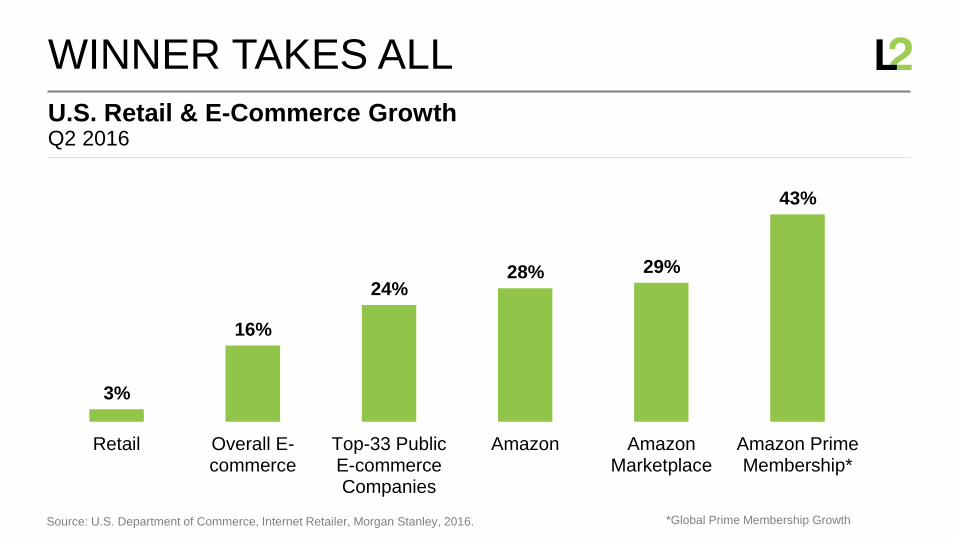

Q2 2016U.S. Retail & E-Commerce Growth

WINNER TAKES ALL

Source: U.S. Department of Commerce, Internet Retailer, Morgan Stanley, 2016. *Global Prime Membership Growth

3%

16%

24%28% 29%

43%

Retail Overall E-commerce

Top-33 PublicE-commerceCompanies

Amazon AmazonMarketplace

Amazon PrimeMembership*

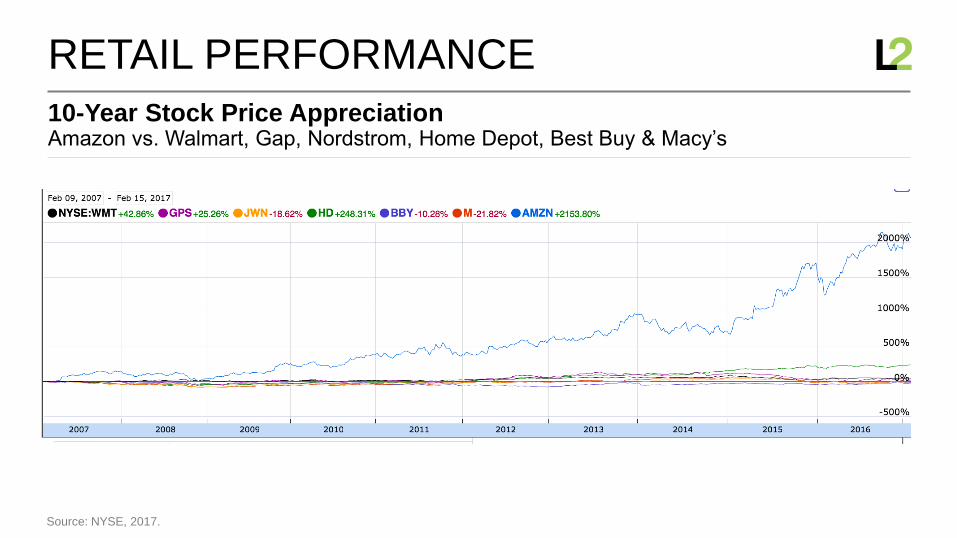

Amazon vs. Walmart, Gap, Nordstrom, Home Depot, Best Buy & Macy’s10-Year Stock Price Appreciation

RETAIL PERFORMANCE

Source: NYSE, 2017.

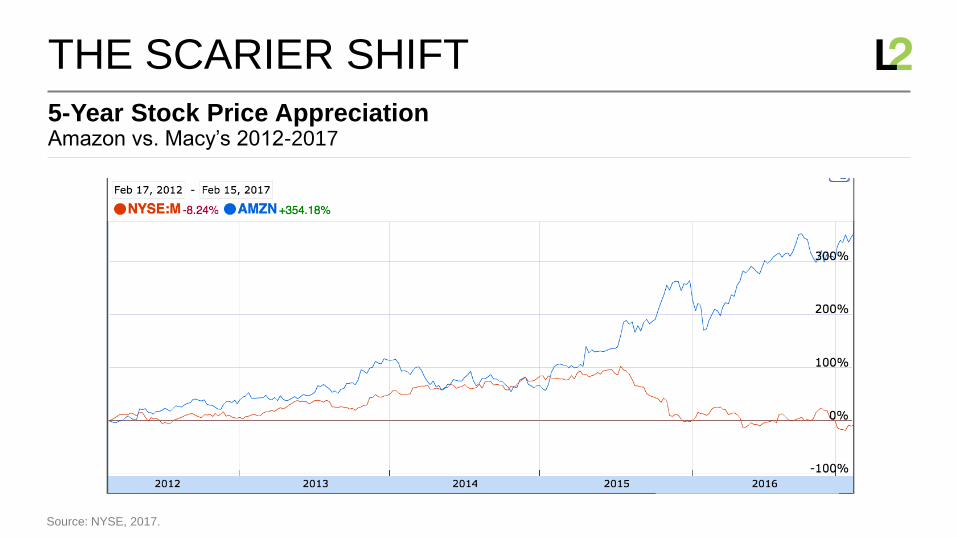

Amazon vs. Macy’s 2012-20175-Year Stock Price Appreciation

THE SCARIER SHIFT

Source: NYSE, 2017.

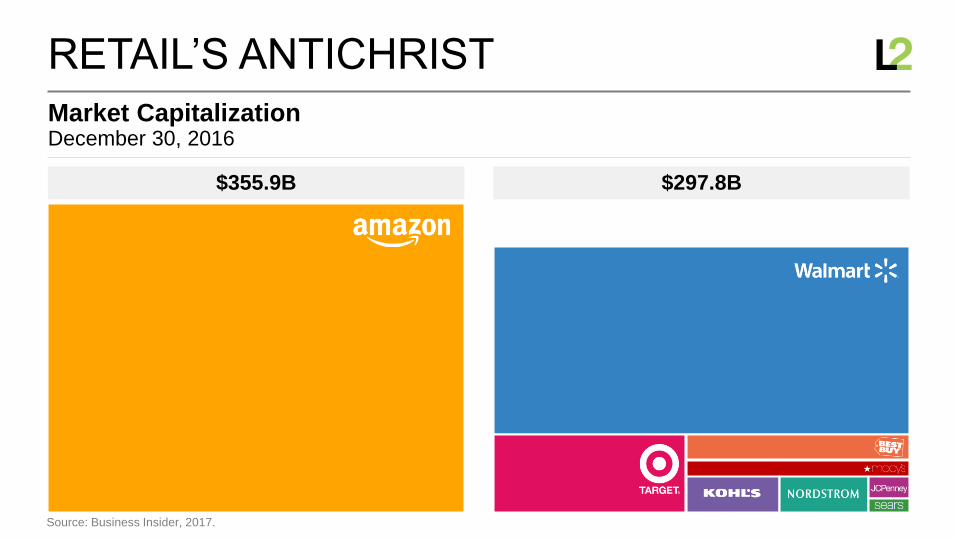

December 30, 2016 Market Capitalization

RETAIL’S ANTICHRIST

Source: Business Insider, 2017.

$355.9B $297.8B

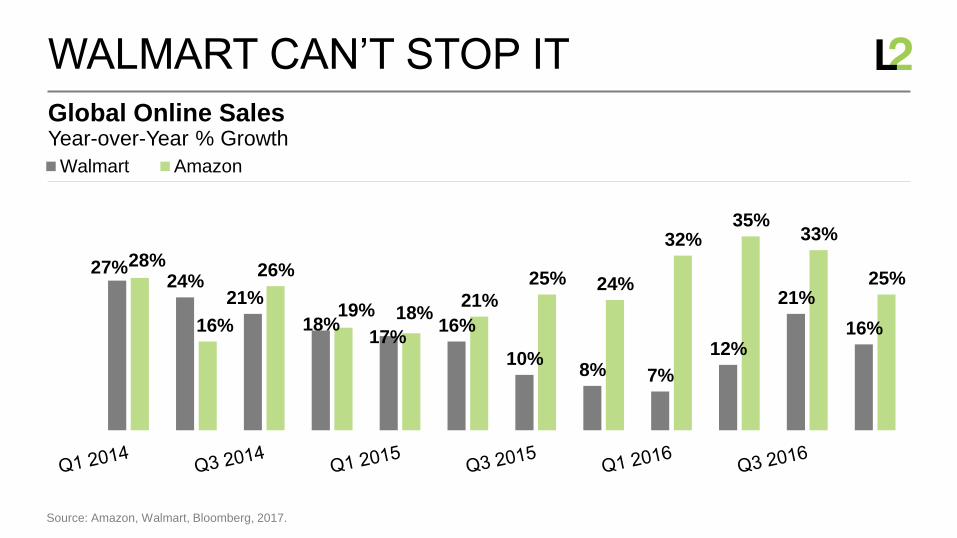

Year-over-Year % GrowthGlobal Online Sales

WALMART CAN’T STOP IT

Source: Amazon, Walmart, Bloomberg, 2017.

27%24%

21%

18%17%

16%

10%8% 7%

12%

21%

16%

28%

16%

26%

19% 18%21%

25% 24%

32%35%

33%

25%

Walmart Amazon

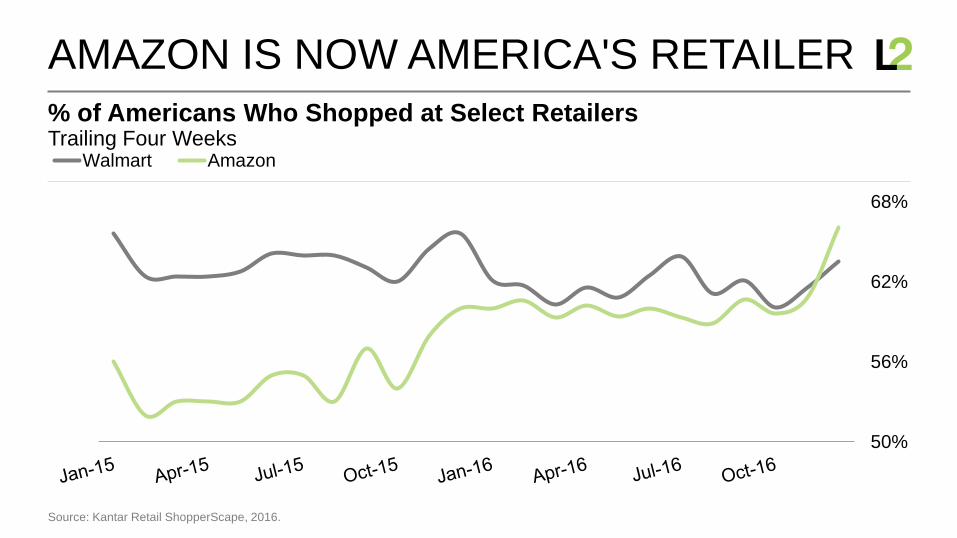

Trailing Four Weeks% of Americans Who Shopped at Select Retailers

AMAZON IS NOW AMERICA'S RETAILER

Source: Kantar Retail ShopperScape, 2016.

50%

56%

62%

68%

Walmart Amazon

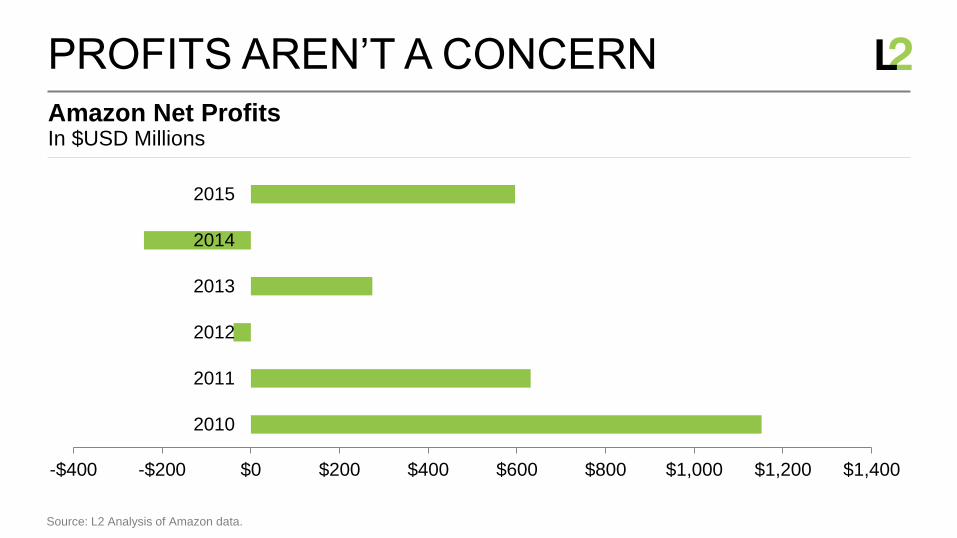

UNDERSTANDING AMAZON

In $USD MillionsAmazon Net Profits

PROFITS AREN’T A CONCERN

Source: L2 Analysis of Amazon data.

-$400 -$200 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400

2010

2011

2012

2013

2014

2015

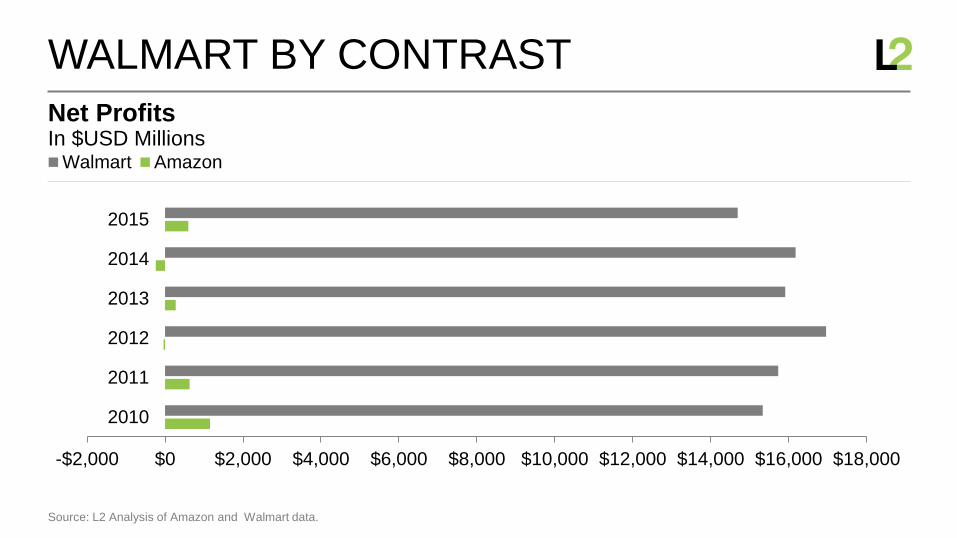

In $USD MillionsNet Profits

WALMART BY CONTRAST

Source: L2 Analysis of Amazon and Walmart data.

-$2,000 $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000

2010

2011

2012

2013

2014

2015

Walmart Amazon

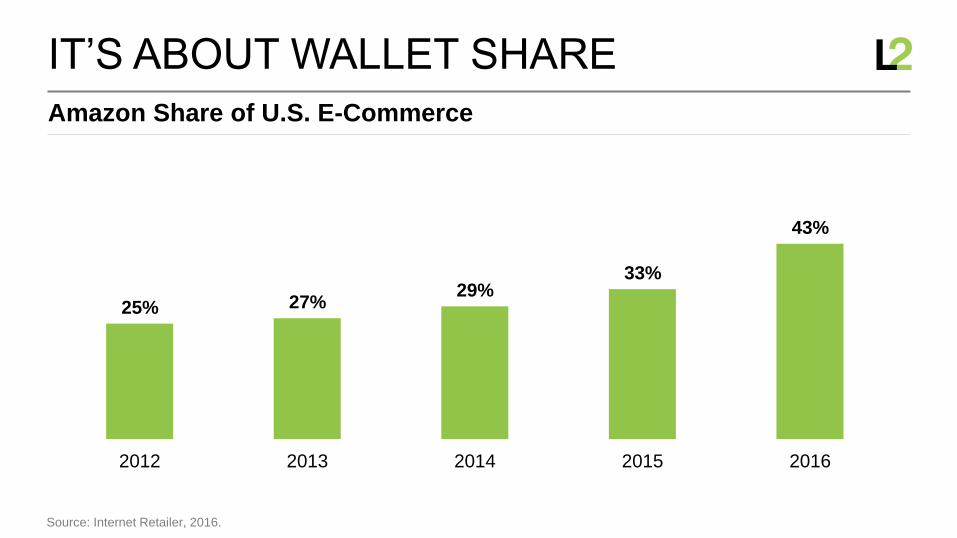

Amazon Share of U.S. E-Commerce

IT’S ABOUT WALLET SHARE

Source: Internet Retailer, 2016.

25% 27%29%

33%

43%

2012 2013 2014 2015 2016

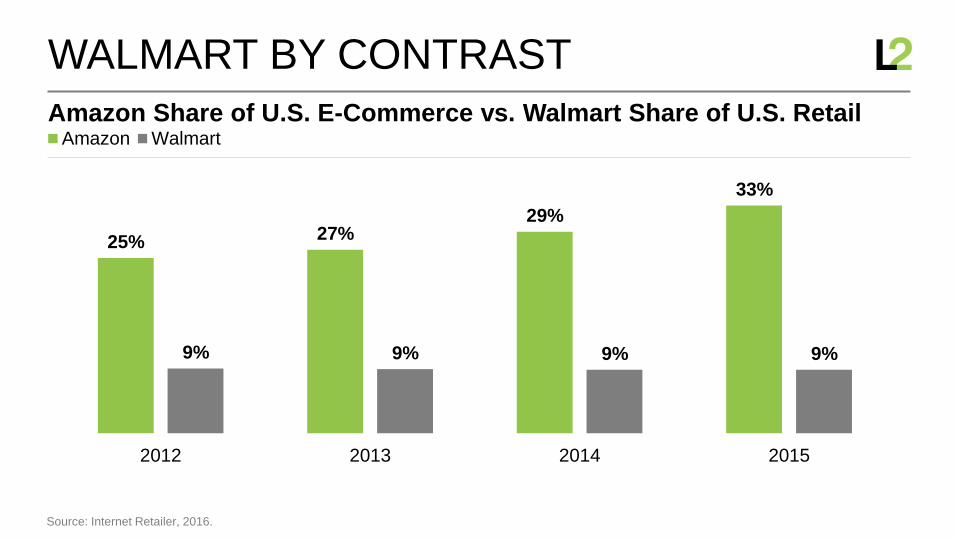

Amazon Share of U.S. E-Commerce vs. Walmart Share of U.S. Retail

WALMART BY CONTRAST

Source: Internet Retailer, 2016.

25% 27%29%

33%

9% 9% 9% 9%

2012 2013 2014 2015

Amazon Walmart

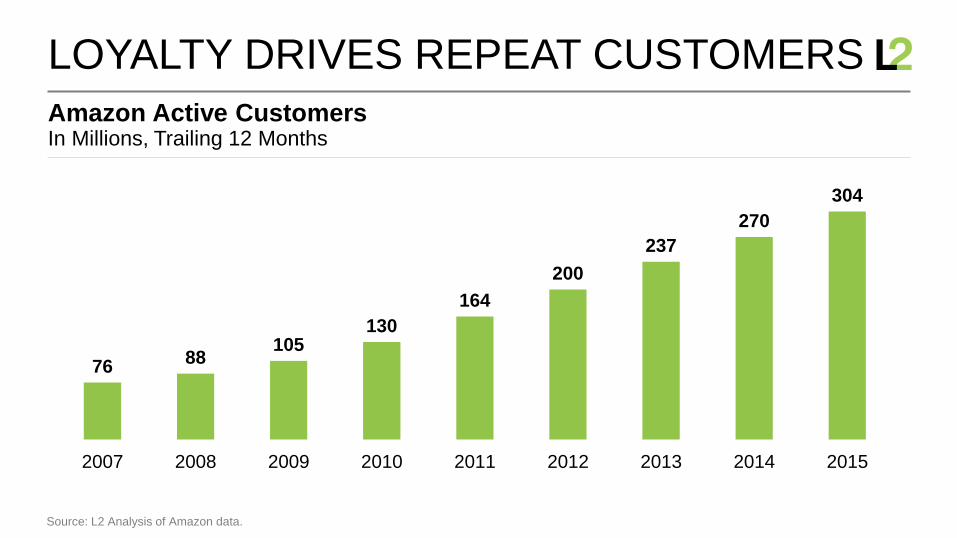

In Millions, Trailing 12 MonthsAmazon Active Customers

LOYALTY DRIVES REPEAT CUSTOMERS

Source: L2 Analysis of Amazon data.

7688

105130

164

200

237

270

304

2007 2008 2009 2010 2011 2012 2013 2014 2015

LOYALTY BY CONVENIENCE

LOYALTY BY PRICE

Source: Revionics, 2015.

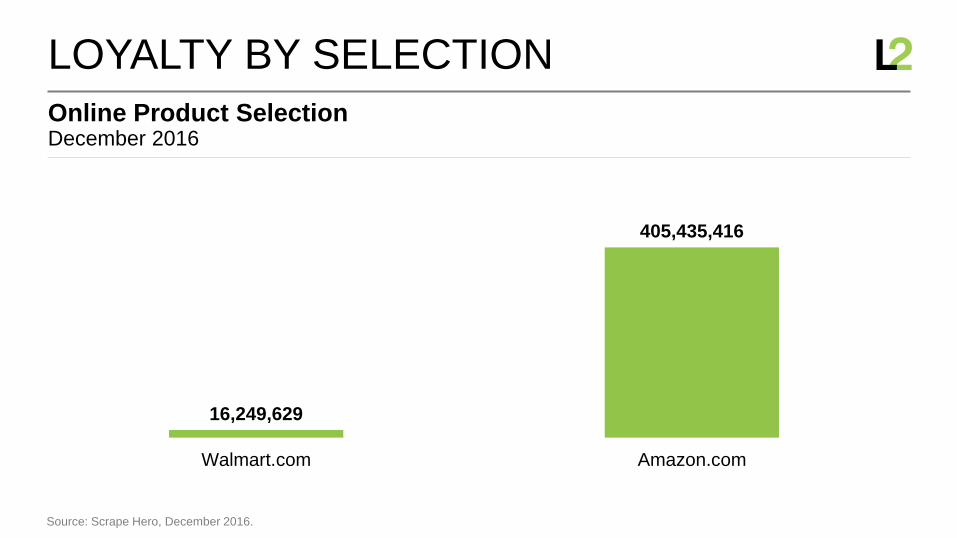

December 2016Online Product Selection

LOYALTY BY SELECTION

Source: Scrape Hero, December 2016.

16,249,629

405,435,416

Walmart.com Amazon.com

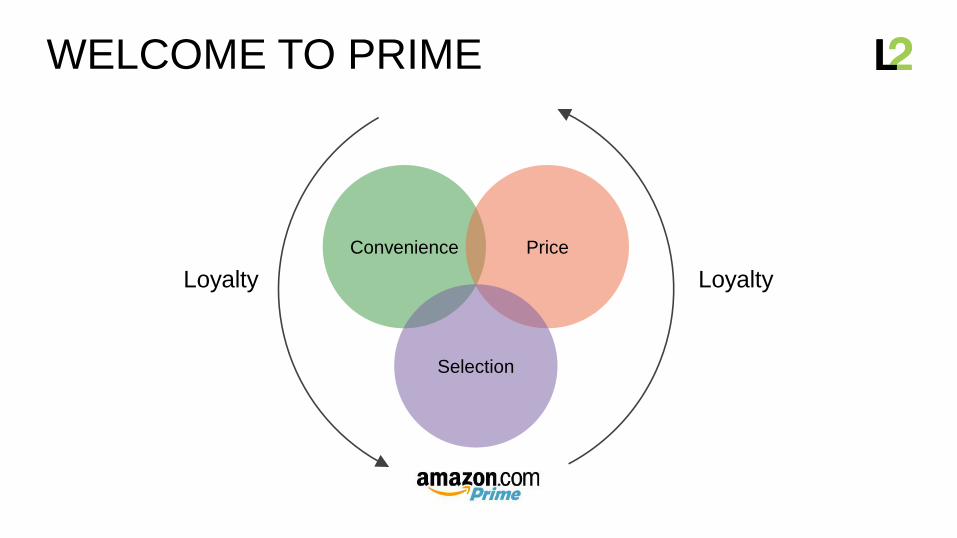

WELCOME TO PRIME

LoyaltyLoyalty

Convenience Price

Selection

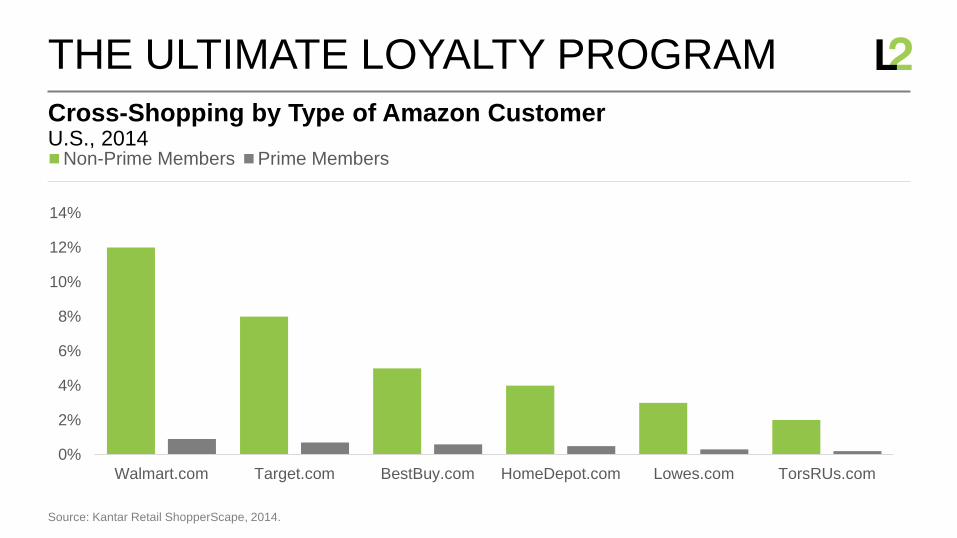

U.S., 2014Cross-Shopping by Type of Amazon Customer

THE ULTIMATE LOYALTY PROGRAM

Source: Kantar Retail ShopperScape, 2014.

0%

2%

4%

6%

8%

10%

12%

14%

Walmart.com Target.com BestBuy.com HomeDepot.com Lowes.com TorsRUs.com

Non-Prime Members Prime Members

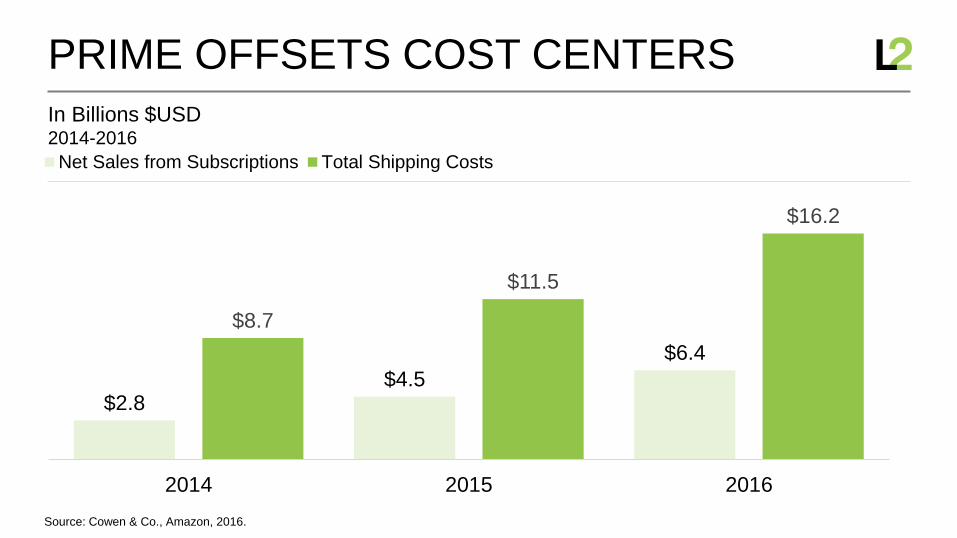

In MillionsPrime Members

THAT’S A LOT OF LOYAL SHOPPERS

Source: Cowen & Co., Amazon, 2016.

2528

4044

54

63 65

Dec-13 Jun-14 Dec-14 Jun-15 Dec-15 Jun-16 Sep-16

In Billions $USD

Source: Cowen & Co., Amazon, 2016.

PRIME OFFSETS COST CENTERS

2014-2016

$2.8$4.5

$6.4

$8.7

$11.5

$16.2

2014 2015 2016

Net Sales from Subscriptions Total Shipping Costs

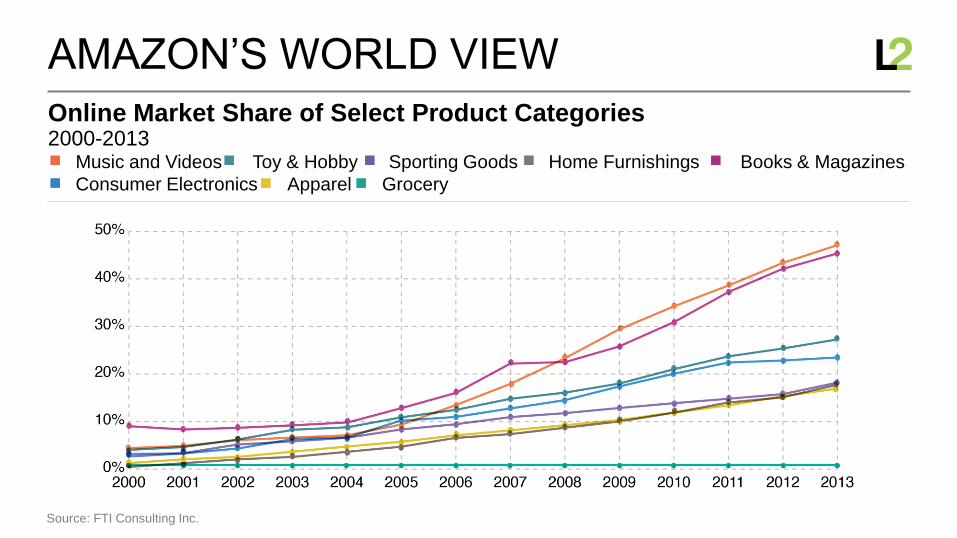

2000-2013Online Market Share of Select Product Categories

AMAZON’S WORLD VIEW

Source: FTI Consulting Inc.

Music and Videos Toy & Hobby Sporting Goods Home Furnishings Books & Magazines

Consumer Electronics Apparel Grocery

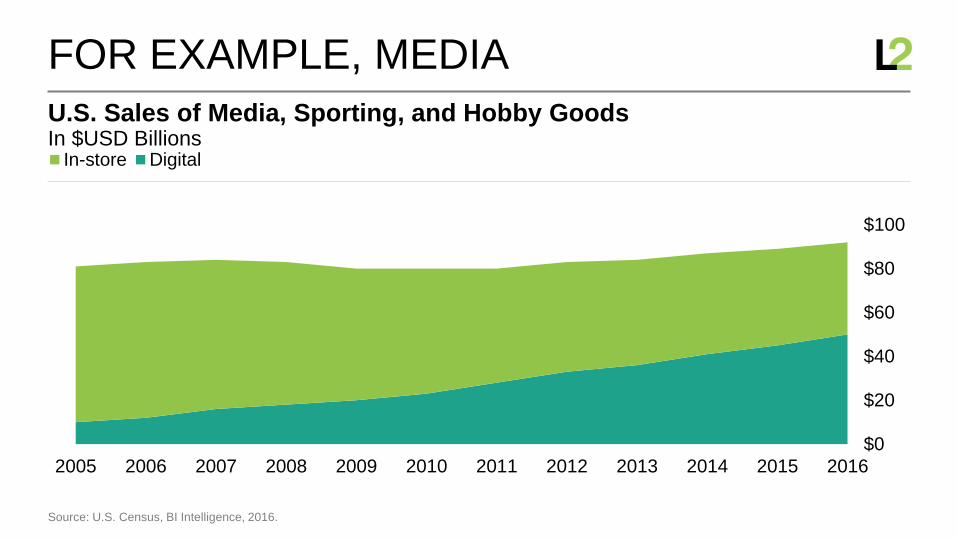

In $USD BillionsU.S. Sales of Media, Sporting, and Hobby Goods

FOR EXAMPLE, MEDIA

Source: U.S. Census, BI Intelligence, 2016.

$0

$20

$40

$60

$80

$100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

In-store Digital

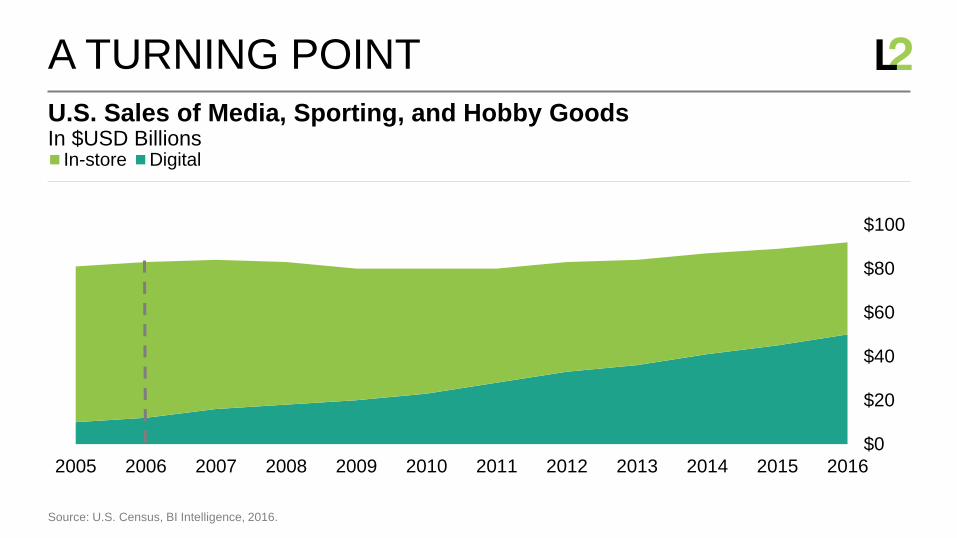

In $USD BillionsU.S. Sales of Media, Sporting, and Hobby Goods

A TURNING POINT

Source: U.S. Census, BI Intelligence, 2016.

$0

$20

$40

$60

$80

$100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

In-store Digital

Online Market Share of Select Product Categories

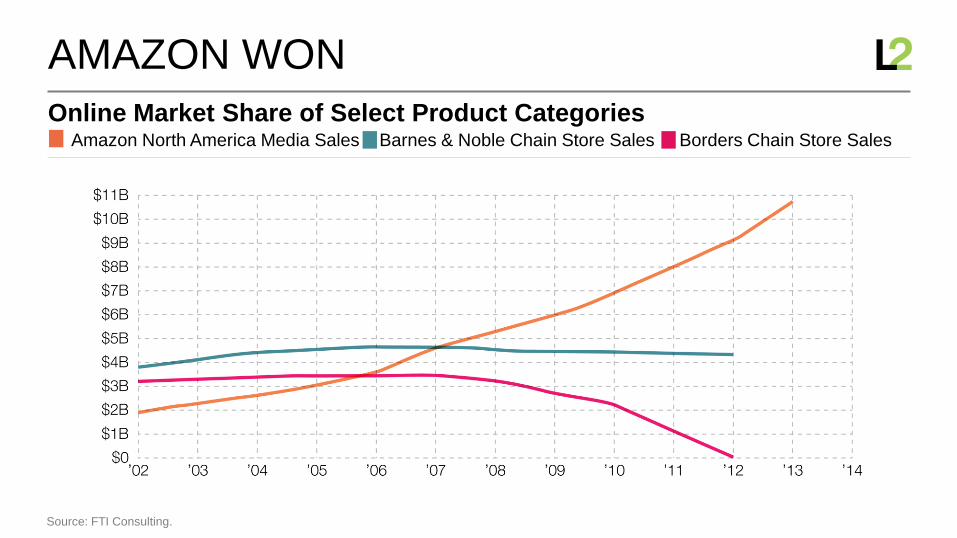

AMAZON WON

Source: FTI Consulting.

Amazon North America Media Sales Barnes & Noble Chain Store Sales Borders Chain Store Sales

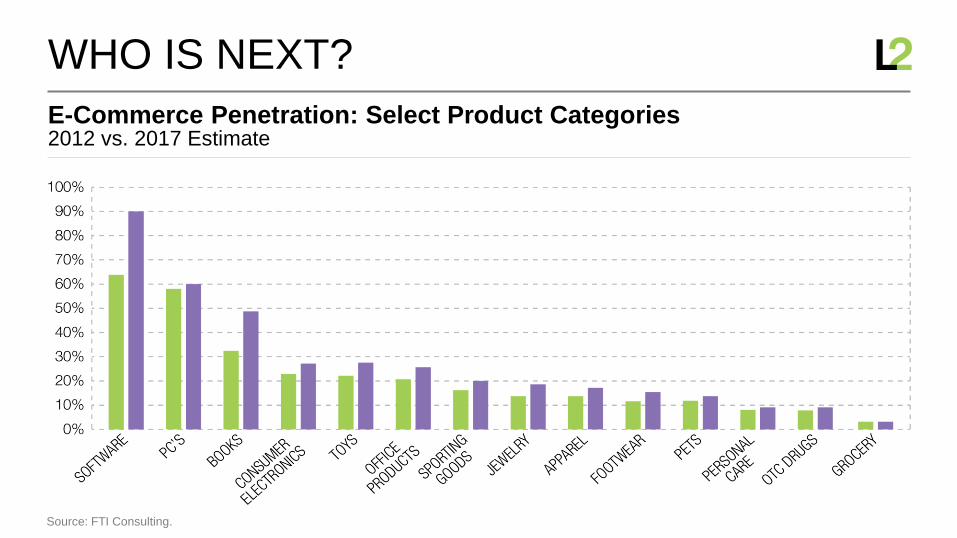

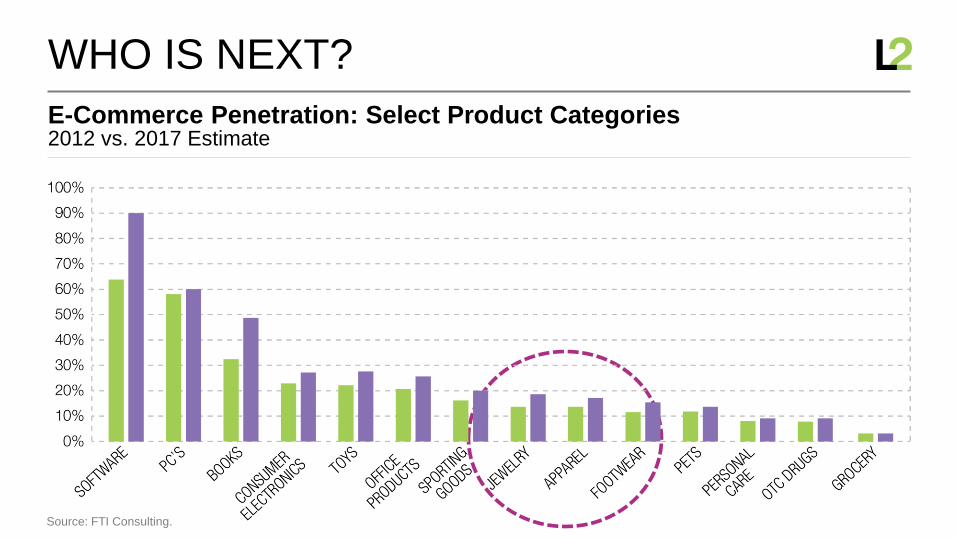

E-Commerce Penetration: Select Product Categories

WHO IS NEXT?

Source: FTI Consulting.

2012 vs. 2017 Estimate

E-Commerce Penetration: Select Product Categories

WHO IS NEXT?

Source: FTI Consulting.

2012 vs. 2017 Estimate

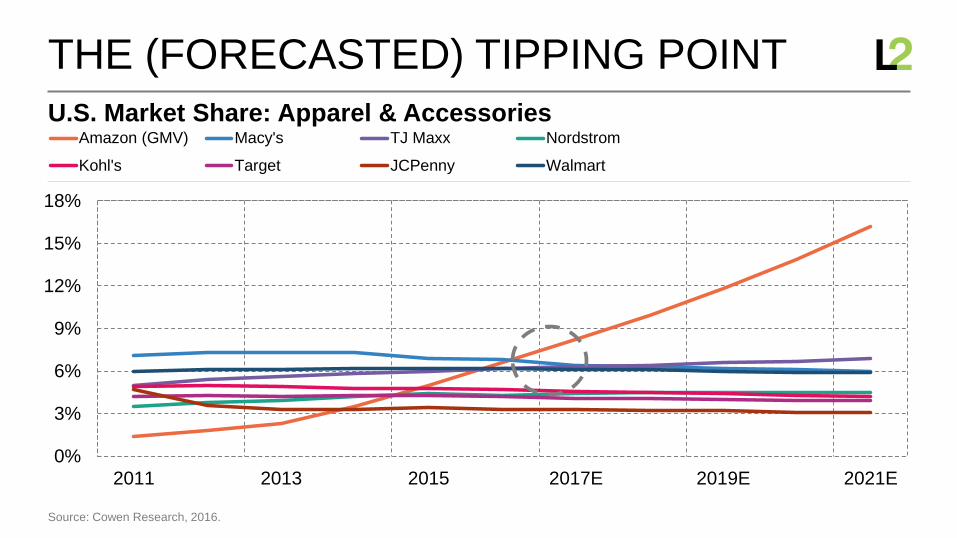

U.S. Market Share: Apparel & Accessories

THE (FORECASTED) TIPPING POINT

Source: Cowen Research, 2016.

0%

3%

6%

9%

12%

15%

18%

2011 2013 2015 2017E 2019E 2021E

Amazon (GMV) Macy's TJ Maxx Nordstrom

Kohl's Target JCPenny Walmart

DEEP DIVE: APPAREL

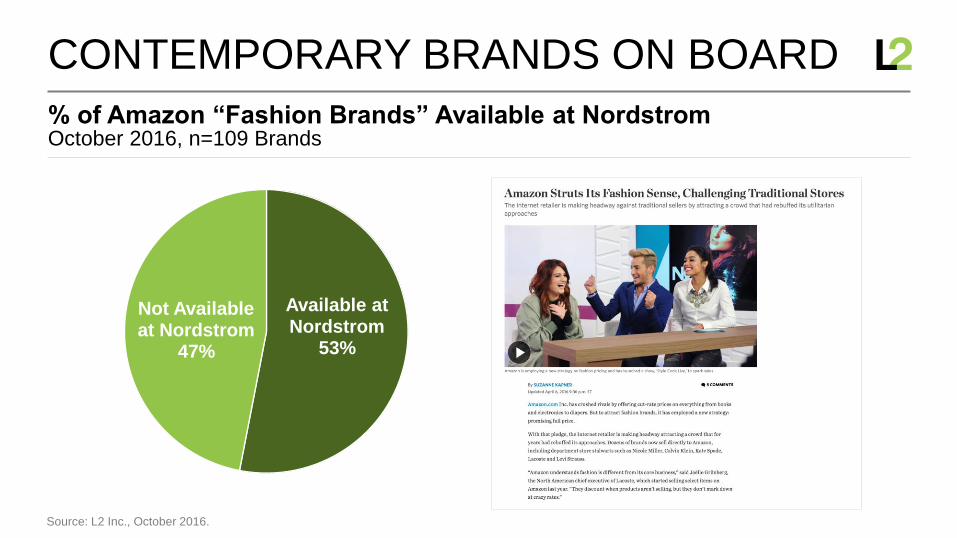

% of Amazon “Fashion Brands” Available at Nordstrom

CONTEMPORARY BRANDS ON BOARD

Source: L2 Inc., October 2016.

October 2016, n=109 Brands

Available at Nordstrom

53%

Not Available at Nordstrom

47%

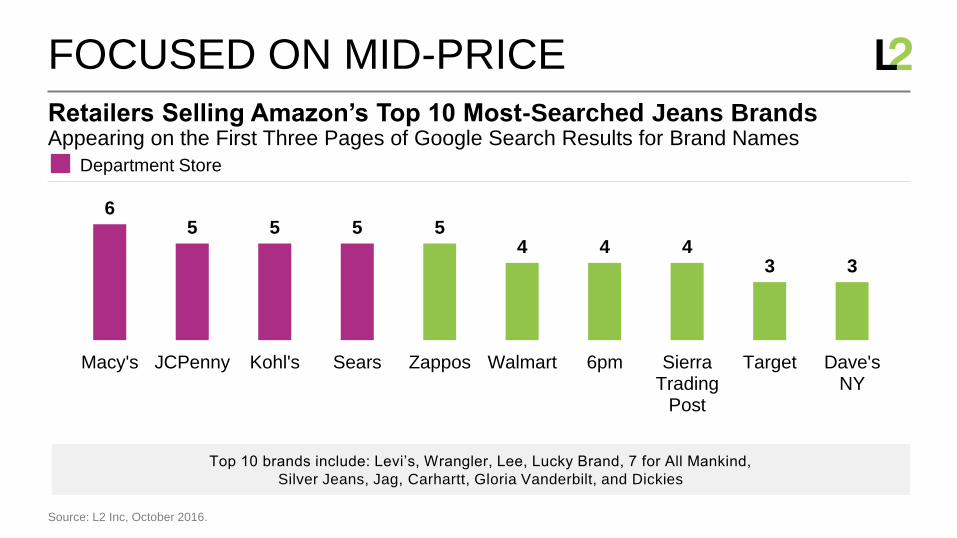

Appearing on the First Three Pages of Google Search Results for Brand NamesRetailers Selling Amazon’s Top 10 Most-Searched Jeans Brands

FOCUSED ON MID-PRICE

Source: L2 Inc, October 2016.

65 5 5 5

4 4 43 3

Macy's JCPenny Kohl's Sears Zappos Walmart 6pm SierraTrading

Post

Target Dave'sNY

Top 10 brands include: Levi’s, Wrangler, Lee, Lucky Brand, 7 for All Mankind,

Silver Jeans, Jag, Carhartt, Gloria Vanderbilt, and Dickies

Department Store

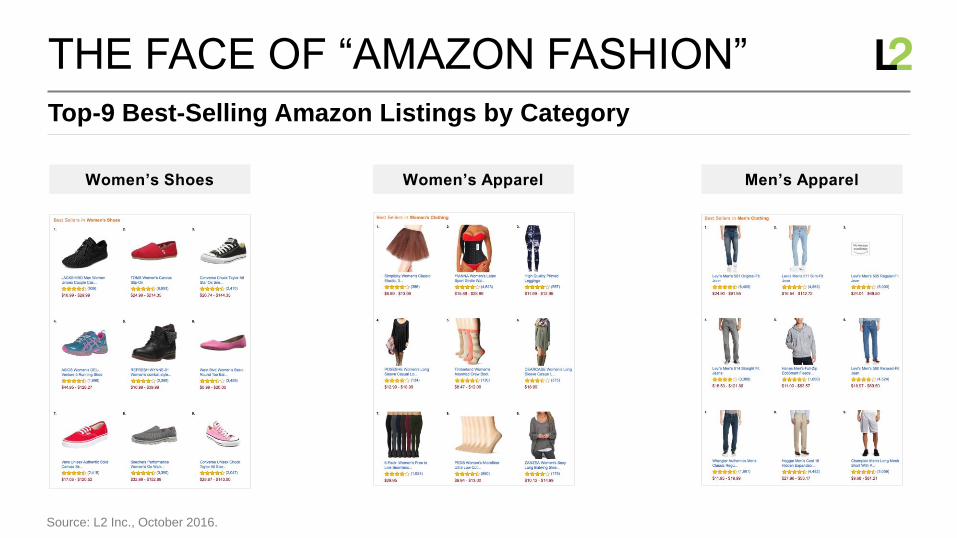

Top-9 Best-Selling Amazon Listings by Category

THE FACE OF “AMAZON FASHION”

Source: L2 Inc., October 2016.

Women’s Shoes Women’s Apparel Men’s Apparel

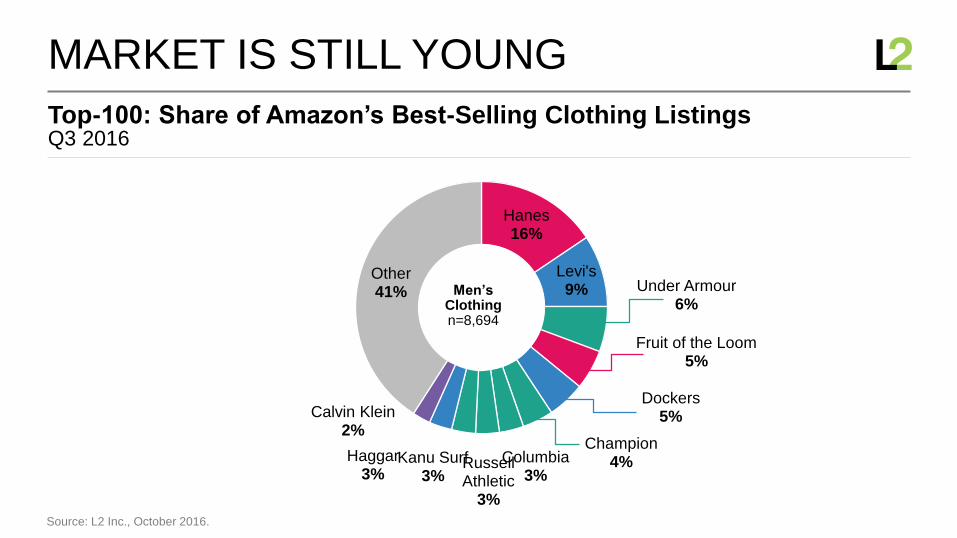

Top-100: Share of Amazon’s Best-Selling Clothing Listings

MARKET IS STILL YOUNG

Source: L2 Inc., October 2016.

Q3 2016

Hanes16%

Levi's9% Under Armour

6%

Fruit of the Loom5%

Dockers5%

Champion4%Columbia

3%Russell Athletic

3%

Kanu Surf3%

Haggar3%

Calvin Klein 2%

Other41% Men’s

Clothingn=8,694

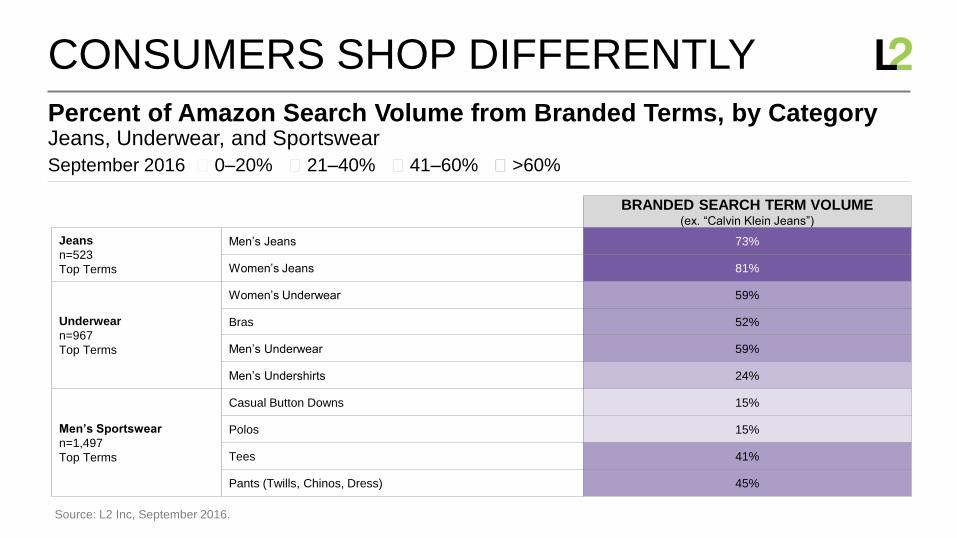

Jeans, Underwear, and SportswearPercent of Amazon Search Volume from Branded Terms, by Category

CONSUMERS SHOP DIFFERENTLY

Source: L2 Inc, September 2016.

BRANDED SEARCH TERM VOLUME(ex. “Calvin Klein Jeans”)

Jeans

n=523

Top Terms

Men’s Jeans 73%

Women’s Jeans 81%

Underwear

n=967

Top Terms

Women’s Underwear 59%

Bras 52%

Men’s Underwear 59%

Men’s Undershirts 24%

Men’s Sportswear

n=1,497

Top Terms

Casual Button Downs 15%

Polos 15%

Tees 41%

Pants (Twills, Chinos, Dress) 45%

September 2016 ◼ 0–20% ◼ 21–40% ◼ 41–60% ◼ >60%

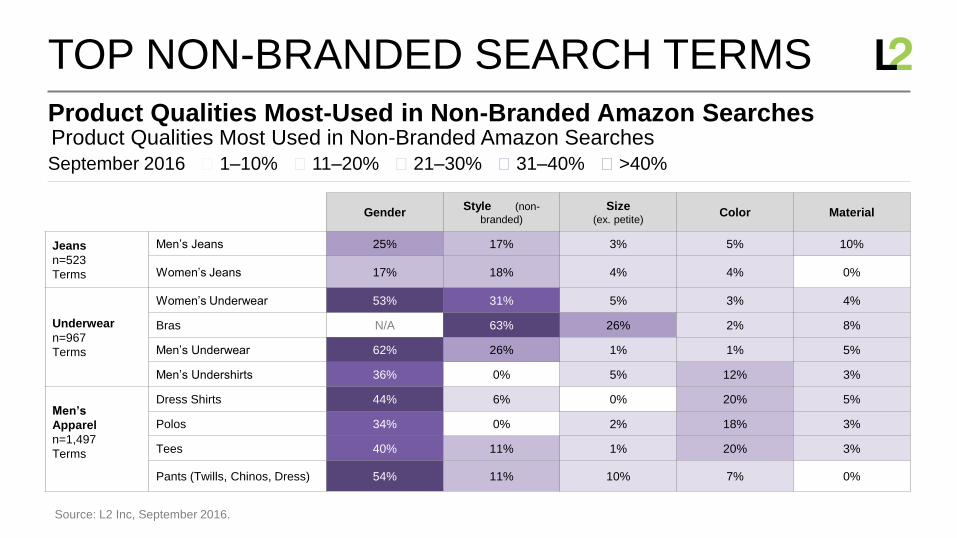

Product Qualities Most Used in Non-Branded Amazon SearchesProduct Qualities Most-Used in Non-Branded Amazon Searches

TOP NON-BRANDED SEARCH TERMS

Source: L2 Inc, September 2016.

GenderStyle (non-

branded)

Size (ex. petite)

Color Material

Jeans

n=523

Terms

Men’s Jeans 25% 17% 3% 5% 10%

Women’s Jeans 17% 18% 4% 4% 0%

Underwear

n=967

Terms

Women’s Underwear 53% 31% 5% 3% 4%

Bras N/A 63% 26% 2% 8%

Men’s Underwear 62% 26% 1% 1% 5%

Men’s Undershirts 36% 0% 5% 12% 3%

Men’s

Apparel

n=1,497

Terms

Dress Shirts 44% 6% 0% 20% 5%

Polos 34% 0% 2% 18% 3%

Tees 40% 11% 1% 20% 3%

Pants (Twills, Chinos, Dress) 54% 11% 10% 7% 0%

September 2016 ◼ 1–10% ◼ 11–20% ◼ 21–30% ◼ 31–40% ◼ >40%

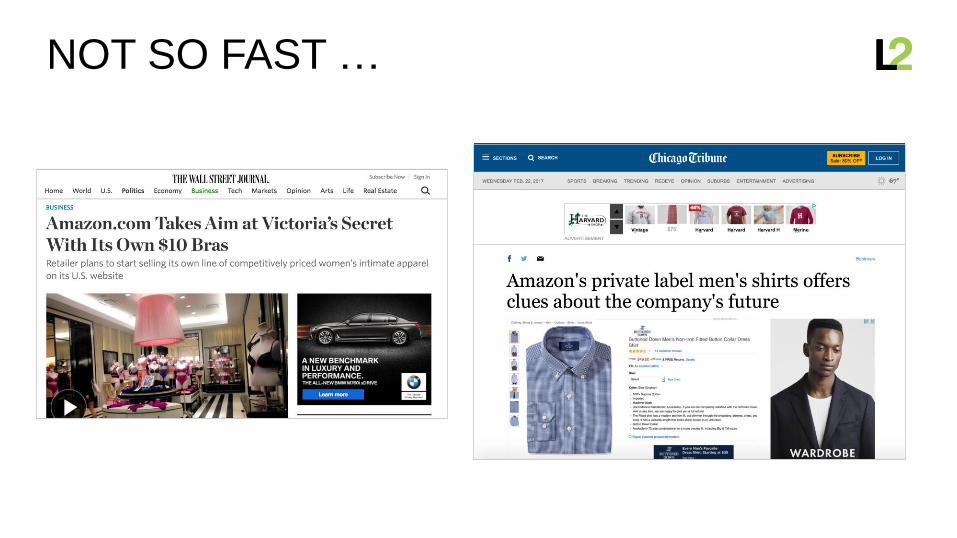

NOT SO FAST …

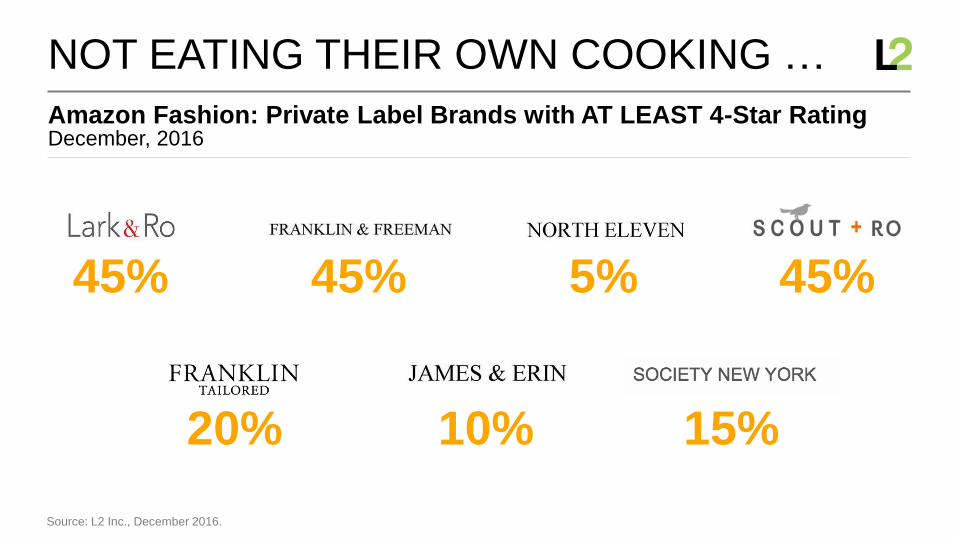

Amazon Fashion: Private Label Brands with AT LEAST 4-Star Rating

NOT EATING THEIR OWN COOKING …

Source: L2 Inc., December 2016.

December, 2016

45% 45% 5% 45%

20% 10% 15%

CONCLUSION

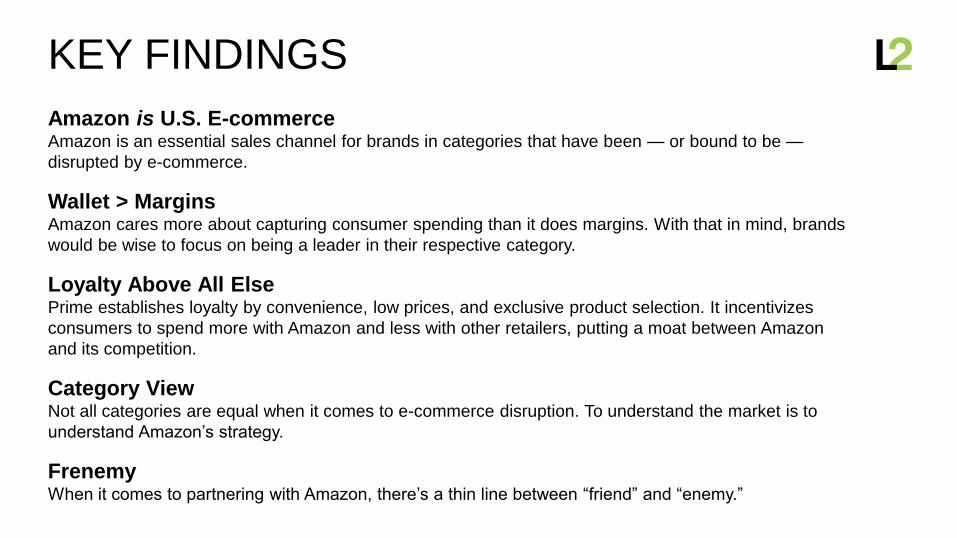

KEY FINDINGS

Amazon is U.S. E-commerceAmazon is an essential sales channel for brands in categories that have been — or bound to be —

disrupted by e-commerce.

Wallet > MarginsAmazon cares more about capturing consumer spending than it does margins. With that in mind, brands

would be wise to focus on being a leader in their respective category.

Loyalty Above All ElsePrime establishes loyalty by convenience, low prices, and exclusive product selection. It incentivizes

consumers to spend more with Amazon and less with other retailers, putting a moat between Amazon

and its competition.

Category ViewNot all categories are equal when it comes to e-commerce disruption. To understand the market is to

understand Amazon’s strategy.

FrenemyWhen it comes to partnering with Amazon, there’s a thin line between “friend” and “enemy.”

![Amazon’s ecommerce Empire_FINAL [Autosaved]](https://img.pdfslide.us/doc/110x75/587091c91a28ab412b8b59f3/amazons-ecommerce-empirefinal-autosaved.jpg)