Embed Size (px)

Citation preview

TRENDS AND DEVELOPMENTS IN

LNG MARKETS & MARKETING: Adjusting Contracts to Fit a Shifting Market

Daniel R. Rogers Partner

King & Spalding LLP Houston

© King & Spalding 2017

2

© King & Spalding 2017

Agenda

• Today’s LNG market

• What do today’s LNG Buyers want?

• Trends in LNG marketing & impacts on contracting

• The changing LNG SPA

4

© King & Spalding 2017

Recent LNG market headlines

5

© King & Spalding 2017

Recent LNG market headlines (cont’d)

6

© King & Spalding 2017

Recent LNG market headlines (cont’d)

7

© King & Spalding 2017

Shifting tides?

• While today’s buyer’s market condition is a product of the present “supply overhang”, many analysts project that LNG supply and demand will come back into balance sometime between 2021-2023

• In the meantime, pricing shifts in the relevant oil and natural gas market price indexes may begin to change the market dynamic somewhat on a bit earlier timeline

8

© King & Spalding 2017

Historical U.S. natural gas pricing

9

© King & Spalding 2017

Historical U.S. shale gas production

10

© King & Spalding 2017

Near-term gas price forecasts (EIA)

11

© King & Spalding 2017

Source: Market Realist

Long-term gas price forecasts

12

© King & Spalding 2017

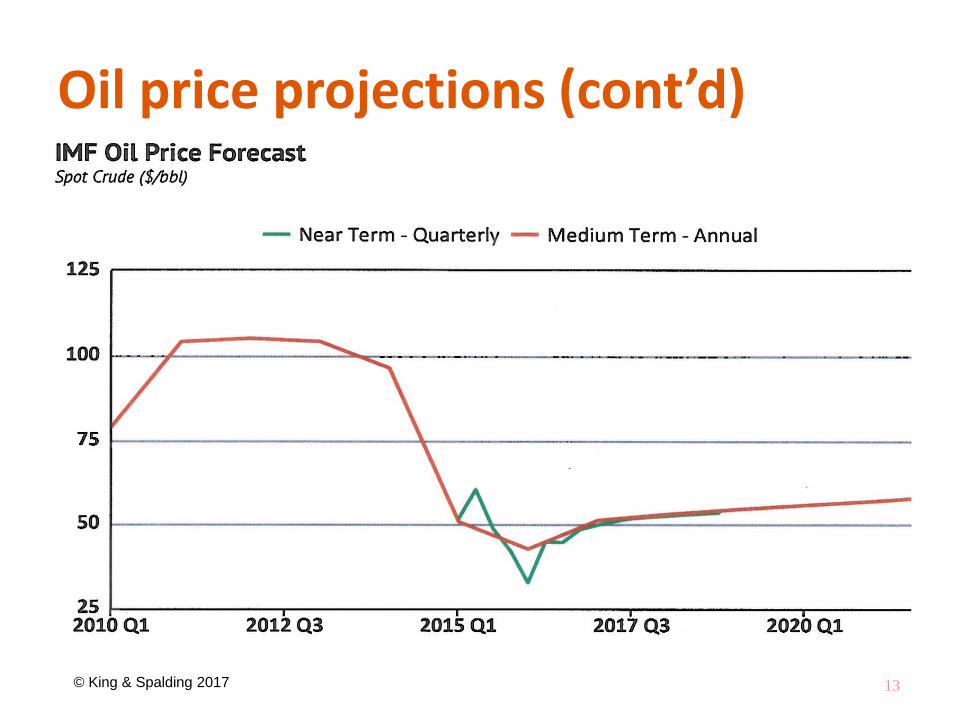

Oil price projections (cont’d)

13

© King & Spalding 2017

Oil price projections (cont’d)

14

© King & Spalding 2017

Oil price projections

15

© King & Spalding 2017

Market impact conclusions • Regardless of whether oil prices remain flat or gradually

escalate from US$55/bbl to US$80/bbl over the next 10+ years,

– it seems plausible that U.S. Henry Hub pricing is likely to continue to rise, and

– a US$4.00-5.00/mmBtu HH pricing level is possible in the near-term

• Higher HH prices will begin to erode some of the “pricing advantage” that theoretical U.S.-origin LNG supplies would have enjoyed over the past few years

– Asian buyers that were dead-set on moving to HH pricing 5 years ago will continue to re-think their pricing strategies

16

© King & Spalding 2017

Market impact conclusions (cont’d)

• Even though we may be moving toward more global LNG supply-demand balance over the next 5 years (with corresponding LNG price increases), many North American export projects still may not be seen as being as competitive as they were viewed 3-4 years ago

• U.S. HH feed gas cost increases may offset or even exceed the significant liquefaction cost improvements that we may see with some of the new liquefaction technologies and improved construction methods

• The “next wave” of North American LNG producers will need to significantly bring down the cost of liquefaction in order to maintain a competitive foothold in the global marketplace

17

© King & Spalding 2017

What do today’s LNG Buyers want from Sellers?

© King & Spalding 2017

1. Many buyers want shorter-term contracts

• Recent McKinsey & Company survey of LNG buyers & industry experts:

– Significant shift towards shorter term sales contracts

• Average length of a term contract signed in 2015 was just 8 years, compared to 15 years in 2008.

– Trend is likely to continue

• McKinsey survey suggests that more than half of LNG buyers expect their next LNG term contract to be a 5-9 year deal

19

© King & Spalding 2017

2. Many buyers are not interested in contract renewals

– McKinsey survey also found a reduced likelihood that buyers will renew their existing term contracts

• 2/3 of buyers with existing contracts reported that the chances of renewing those contracts were either ‘somewhat unlikely’ or just ‘possible’.

• The most significant reason for this was that the supplier was not felt to be price competitive (38 out of a possible 100 points)

• Supplier under-performance and inability to guarantee future volumes were also important, (accounting for nearly 27 out of a possible 100 points.)

20

© King & Spalding 2017

Source: McKinsey & Company (Energy Insights, January 2017)

3. Long-term buyers want very low pricing

• Today’s spot LNG prices are lower than many Buyers’ long-term contract prices – Some Buyers seem to be happy buying additional quantities on the spot

market rather than committing to longer-term contracts

• Buyers now have actual “gas-on-gas” pricing competition with the introduction of significant US HH-indexed supplies

• With oil prices in the US$50+/bbl range (Brent), traditional oil-linked Asian contract prices are very competitive with present US HH-linked supply pricing

• Some Buyers are now pushing down “slopes” in oil-linked pricing formulas

• Today’s low LNG and gas prices and gas-on-gas competition may further open the door to new emerging market Buyers

21

© King & Spalding 2017

Oil-indexed LNG Pricing

• Typical Asian market LNG contract price formula:

CP (in US$/mmBtu) = [0.1485 x JCC (in US$/bbl)] + ß

22

© King & Spalding 2017

JCC / Brent oil price slope

@ oil = US$50 / bbl

@ oil = US$100 / bbl

0.1485 x JCC [Traditional Asian oil-indexed pricing slope]

US$ 7.425 / mmBtu

US$ 14.85 / mmBtu

0.1335 x Brent [QatarGas – Pakistan State Oil Company Limited slope]

US$ 6.675 / mmBtu

US$ 13.35 / mmBtu

0.1267 x Brent [RasGas – Petronet LNG Limited slope]

US$ 6.335 / mmBtu

US$ 12.67 / mmBtu

Further downward pressure on oil price index slopes

• Latest 15 year term Pakistan supply tender:

– Eni – 12.29% x Brent

– Shell – 12.599% x Brent

– Gunvor – 12.7% x Brent

– Petronas – 12.9% x Brent

– Trafigura – 13.3699% x Brent

• Latest 5 year term Pakistan supply tender: – Gunvor – 11.6247% x Brent

– Eni – 12.29% x Brent

– Shell – 12.3% x Brent

– Engie - 12.39% x Brent

– Gazprom - 12.4700% x Brent

– Trafigura - 12.4874% x Brent

– CNOOC - 12.8280% x Brent

– Petronas - 12.900% x Brent

– Gas Natural – 13.29% x Brent

– Glencore – 14.4865% x Brent

23

© King & Spalding 2017

U.S. HH-indexed LNG pricing

• Representative U.S. Gulf Coast (FOB) pricing :

–Brownfield (conversion) facility:

• 115% x HH + US$2.25-3.00

–Greenfield facility:

• 115% x HH + US$3.50

• At today’s HH price of US$3.26/mmBtu, this equates to an FOB LNG price of US$6.00-6.75 per mmBtu

24

Detailed oil-indexed pricing analysis

25

© King & Spalding 2017

Detailed HH-indexed pricing analysis

26

© King & Spalding 2017

4. Buyers want more quantity flexibility

• Upward Quantity Tolerance (UQT)

– Typical limits

– Timing of exercise

• Downward Quantity Tolerance (DQT)

– Typical limits

– Timing of exercise

• Cargo cancellation rights

• Back-end “ramp-down” rights

• Call option structure

27

© King & Spalding 2017

Composite quantity flexibility

28

© King & Spalding 2017

5. Buyers want more cargo destination flexibility

• Destination restrictions

– Historical rationale for destination restrictions

– European Commission competition laws

– Easing of destination restrictions

• Today’s market:

– Destination flexibility in DAT deals – geographic area limits, “same or shorter distance” limits or unlimited range?

– Vessel-terminal compatibility issues (in DAT deals)

– Incremental shipping costs (in DAT deals)

– Which party may request (in DAT deals)?

– Economic “upside” sharing (in both FOB and DAT deals)

– Timing for request (in both FOB and DAT deals)

29

© King & Spalding 2017

6. Some buyers want seasonal delivery schedules

• Typical contract language:

– LNG to be made available for delivery from Seller to Buyer “shall be at rates and intervals and in quantities reasonably equal and ratable throughout each Contract Year . . .” (emphasis added)

• Today’s market:

– Requests for a disproportionate quantity of the AACQ to be delivered in a defined 3-5 month season (typically winter)

– Issue: since a Seller-producer will produce LNG on a reasonably ratable basis throughout the year, seasonal deliveries put significant strains on its ability to market all of its production on a long-term basis

30

© King & Spalding 2017

7. Buyers want more expansive FM protection

• Many traditional LNG SPAs do not explicitly extend FM protection to the Buyer for facilities and customers downstream of the LNG receiving terminal

• Today’s market: some Buyers are pressing for explicit FM coverage for various downstream pipeline, power generation and industrial facilities in the Buyer’s end-market

• Issue: this exposes the Seller to risks that are well outside its ability to understand or mitigate

31

© King & Spalding 2017

Trends in LNG marketing and contracting: Emergence and impact of portfolio marketing and LNG commodities trading

© King & Spalding 2017

Portfolio Marketers • Who are they?

– LNG trading companies linked to their upstream LNG producing affiliates

– Shell Marketing & Trading, BP Gas Marketing Ltd., Total Gas Marketing, Cheniere Marketing, Petronas LNG Limited, etc.

• What do they do?

– Take/purchase equity LNG from one or more upstream LNG producer affiliates

– Will also buy LNG from other producers

• Spot and term

• Typically FOB (loading port) delivery terms

– On-sell LNG to third-party buyers on a spot & long-term basis, typically on DAT delivery terms

33

© King & Spalding 2017

Commodities traders • Who are they?

– Pure commodities trading entities: no affiliated upstream LNG production

– Gunvor, Trafigura, Vitol, Glencore, Mercuria, etc.

• What do they do?

– Purchase LNG supplies from multiple non-affiliated LNG producers/sellers

• Spot and term

• Typically purchased on FOB (loading port) delivery terms

– On-sell LNG to third-party buyers on a spot & long-term basis, typically on DAT delivery terms

34

© King & Spalding 2017

Portfolio marketers & commodities traders

• What is the impact on the LNG SPA?

– No fixed upstream facilities or dedicated reserves for supply

– Buyer must focus on financial credit & experience of Seller • No dedicated plant facility & reserves supporting contract

• Seller typically has a large number of customer relationships to manage

• ADP will typically identify plant and vessels, but may vary from cargo to cargo

– Better ability of Seller to mitigate supply interruptions

– Seller might better accommodate Buyer’s seasonality requests

– Need for closer monitoring of credit & performance risks

35

© King & Spalding 2017

Portfolio marketers & commodities traders

• What is the impact on the LNG SPA? (continued)

– Cargo-by-cargo seller shortfall / buyer deficiency regime

• Differs significantly from traditional take-or-pay (TOP)

• Parties’ delivery & receipt obligations are measured on a “real-time” basis

– Buyer’s and Seller’s performance failures are settled as and when they occur, instead of accumulating into year-end TOP invoice or Seller Shortfall invoice

– Buyer typically pays in full for missed cargo and receives a credit from Seller’s re-sale proceeds

» increased focus on Seller’s mitigation re-sale obligations & transparency of re-sale pricing

– Potentially lower payment security needed from Buyer

36

© King & Spalding 2017

Portfolio marketers & commodities traders

• What is the impact on the LNG SPA? (continued)

– FM risks and handling are very different

• Typically a more cargo-by-cargo approach, with main focus on loading terminal and ship named in the ADP/90 Day Schedule

• Issue re whether events affecting upstream gas reserves or delivery pipelines should be covered

• Complicated issues flowing from allocation / spreading of FM risks across multiple supply sources in any single Contract Year

37

© King & Spalding 2017

Portfolio marketers & commodities traders

• What is the impact on the LNG SPA? (continued)

– Greater shipping & cargo size flexibility

• Need to address potential for Seller’s “out of fleet” supply and delivery opportunities

• Puts more pressure on Buyer’s inventory management

– Potentially greater scheduling flexibility

• Potential for Buyer cargo diversions and cancellations within the 90 Day Schedule

– Potentially broader GHV specification range from multiple supply sources

38

© King & Spalding 2017

QUESTIONS?

© King & Spalding 2017

Chambers Quotes on K&S LNG Team: • “They have a very specialised knowledge that most firms don't have, particularly on LNG

projects.” Chambers Global 2016

• “They are very creative and willing to chat through unique and challenging circumstances without preconceived notions of how to solve issues.” Chambers USA 2016

• “Considering the many millions of dollars that we save our company with their help, their value far exceeds the money that we pay for them.” Chambers USA 2015

• “Very hands-on and incredibly responsive, they assign the right people at the right value level for what needs to be done. They are fast and give the right advice.” Chambers USA 2015

• “Respected project finance group that focuses on advising sponsor clients on the development and financing of oil and gas infrastructure.” Chambers USA 2015

• “Exceptional expertise in LNG matters and frequently sought out to play a leading role on some of the largest mandates worldwide.” Chambers Global 2015

• “They are very strong in LNG.” Chambers Global 2015

40

© King & Spalding 2017

41

© King & Spalding 2017