Embed Size (px)

Citation preview

Forrester Research, Inc., 60 Acorn Park Drive, Cambridge, MA 02140 USA

Tel: +1 617.613.6000 | Fax: +1 617.613.5000 | www.forrester.com

Trends 2013: North American Insurance eBusiness And Channel Strategyby Ellen Carney, May 16, 2013

For: eBusiness & Channel Strategy Professionals

Key TaKeaways

six Forces are Driving Digital Insurance agendas In 2013Extreme weather, consumer embrace of mobile, a more buoyant economy, and regulatory shifts like the Affordable Care Act and access to medical marijuana are shaping digital insurance business strategies.

Consumers are Changing The RulesAll things digital are empowering consumers, who are shifting from being passive sideliners into playing new, more active roles like regulators and adjustors. And beware of not keeping up as insurers look to embrace consumer impatience and willingness to switch.

Four Overarching Trends are Disrupting Insurance Business ModelsFour trends are fomenting change in the insurance industry: the digital expectations of small business insurance shoppers; a renewed passion for agents; the ubiquity of mobile in informing consumer context; and the coming shopping bonanza for health plans with 2013 Affordable Care Act deadlines.

© 2013, Forrester Research, Inc. All rights reserved. Unauthorized reproduction is strictly prohibited. Information is based on best available resources. Opinions reflect judgment at the time and are subject to change. Forrester®, Technographics®, Forrester Wave, RoleView, TechRadar, and Total Economic Impact are trademarks of Forrester Research, Inc. All other trademarks are the property of their respective companies. To purchase reprints of this document, please email [email protected]. For additional information, go to www.forrester.com.

For eBusiness & Channel strategy ProFessionals

why ReaD ThIs RepORT

There’s one word that sums up what’s going on in the business of insurance right now: disruption. There are four drivers behind the state that the industry is in, all of which have implications across the industry: an improving economy driven by a turn in the housing market; activist consumers willing to both join forces with their insurers and regulate them through social media; converging physical and digital worlds that engage consumers through smart portable devices; and two maturing US regulatory reforms—access to healthcare and medical marijuana. Whether you think of the notion of disruption as provoking commotion, trouble, or tumultuous uproar, others, including new entrants, are embracing these as moments of opportunity in 2013.

table of Contents

Insurance eBusiness and Channel strategy Drivers To watch In 2013

Digital insurance teams reckon With six Forces in 2013

Consumers are Changing the rules of engagement

Digital Disruption Drives Four Key Trends In 2013

Falling in love again: Carriers rekindle the agent Flame

six Million small Businesses go shopping online For insurance

Mobile ubiquity and Context Change Customer Behavior and insurer strategy

health Plans Prep For the Crush of Consumer health Plan shopping

supplemental Material

notes & resources

Forrester regularly interviews north american insurance eBusiness and channel strategy executives. these interviews, along with our ongoing analysis of consumer data and technology evolution, form the basis of our analysis.

related research Documents

2013 Mobile trends For eBusiness ProfessionalsFebruary 13, 2013

the Future of insurance is Mobileseptember 28, 2012

trends 2012: north american insurance eBusiness and Channel strategyMarch 15, 2012

Trends 2013: North american Insurance eBusiness and Channel strategyDisruption Drives 12 trends in Digital insurance agendasby ellen Carneywith Benjamin ensor, Julie a. ask, and lily Varon

2

9

19

May 16, 2013

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 2

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

INsuRaNCe eBusINess aND ChaNNel sTRaTegy DRIveRs TO waTCh IN 2013

There’s one word that sums up what’s going on in the business of insurance right now: disruption. Prevailing forces — from the extreme impact of Superstorm Sandy, customer affection for and reliance on mobile and social, consumer behavior that’s challenging insurer notions of long-standing segmentation models, and an economy that’s sailing on freshening housing winds — are stirring up the insurance landscape and driving the decisions that insurance digital teams will make through the rest of 2013.

Digital Insurance Teams Reckon with six Forces In 2013

We expect the following factors to shape the landscape and determine the priorities for insurance eBusiness and channel strategy executives in 2013:

■ Addressing a reviving global economy that re-energizes insurance markets. In the US, there’s an energy boom rippling across the economy and trickling down to home and commercial construction markets. At the same time, home prices are rising in key markets, and the number of foreclosures is dropping. For insurer portfolios, the fears over the European debt crises are largely easing, while the US’s fiscal cliff can get kicked down the road once again. But the impact of the revival is uneven. There remains entrenched underemployment for 20- and even 30-somethings compounded by student loan debt that’s deferring the acquisitions that come with age, like cars and homes.

■ Addressing evolving societal changes with regulatory reforms. Regulatory reforms like the Affordable Care Act are changing how insurers sell from business-to-business to direct-to-the-consumer.1 Meanwhile, the medical marijuana gold rush means new business risks to protect, from new forms of crop and horticultural coverage to product liability insurance for dispensaries.2 Finally, legislators are weighing in on new laws that would pull insurance companies into the gun debate, by requiring that gun buyers buy liability insurance.3

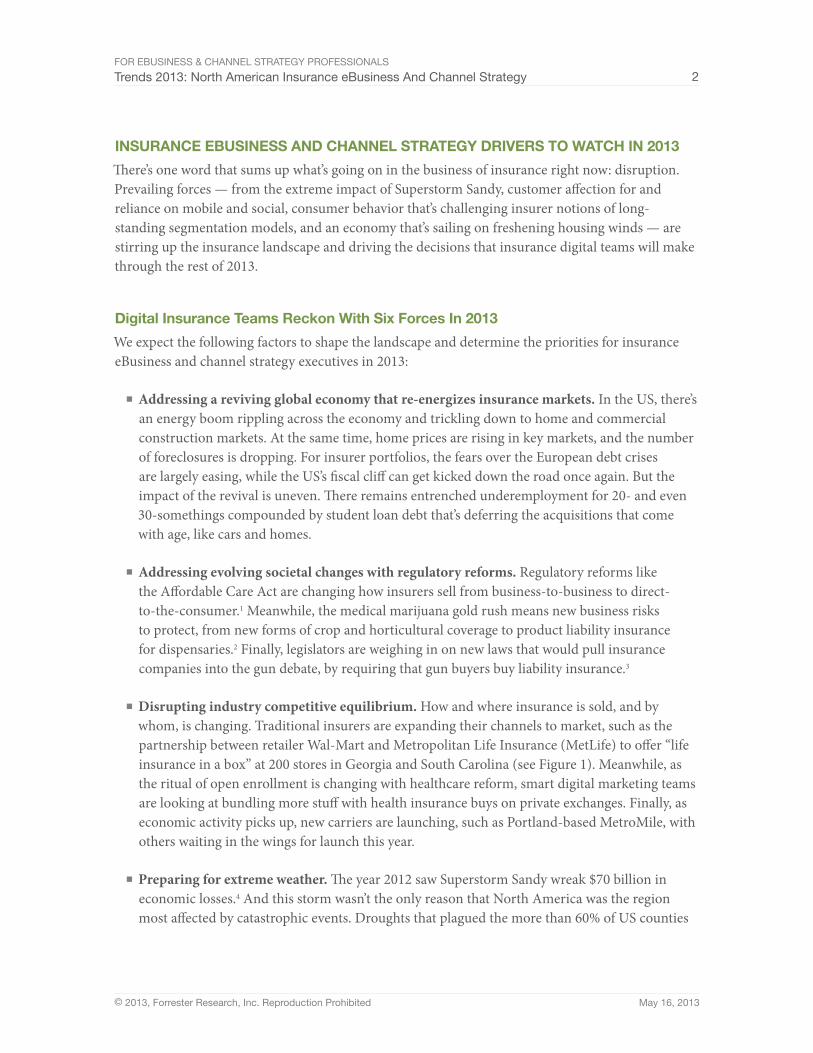

■ Disrupting industry competitive equilibrium. How and where insurance is sold, and by whom, is changing. Traditional insurers are expanding their channels to market, such as the partnership between retailer Wal-Mart and Metropolitan Life Insurance (MetLife) to offer “life insurance in a box” at 200 stores in Georgia and South Carolina (see Figure 1). Meanwhile, as the ritual of open enrollment is changing with healthcare reform, smart digital marketing teams are looking at bundling more stuff with health insurance buys on private exchanges. Finally, as economic activity picks up, new carriers are launching, such as Portland-based MetroMile, with others waiting in the wings for launch this year.

■ Preparing for extreme weather. The year 2012 saw Superstorm Sandy wreak $70 billion in economic losses.4 And this storm wasn’t the only reason that North America was the region most affected by catastrophic events. Droughts that plagued the more than 60% of US counties

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 3

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

represented $20 billion in crop insurance losses. But Sandy’s good-news/bad-news story is that the 250,000 cars totaled in the superstorm means 250,000 new cars to insure and presents a good reason for insurers to get homeowner underwriting and experience under control.5

■ Addressing changing customer behavior. In terms of Connected Seniors, Detached Millennials, and the rise of the small business customer, getting and serving these customers demands new thinking about how to segment the customer base. After decades of segmentation based on attitudes and averages, insurers are now equipped with the business intelligence needed to look at just how customers behave.6

■ Keeping up with changing technology. Mobile devices are everywhere, mobile apps are getting smarter, and busy consumers and agents are substituting mobiles and tablets for PCs. Digital insurance professionals are tapping into the power of mobile context to deliver the right information at the right time, empowering customers and agents. Add to that the fact that insurers are looking at the role that mobile is playing in lifestyle. Assurant’s Protect Your Bubble features a mobile app to cover mobile and home gadgets as well as user identities.7 Further out, but still catching the attention of insurers, are new mobile medical applications as well as surgical and other robotics, including drones.8

Figure 1 MetLife And Wal-Mart Partner To Offer Life Insurance In 200 Stores

Source: Forrester Research, Inc.94742

Source: YouTube website

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 4

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Consumers are Changing The Rules Of engagement

All things digital are driving long-term shifts in the way Americans and Canadians research and buy insurance. Overall, consumers are:

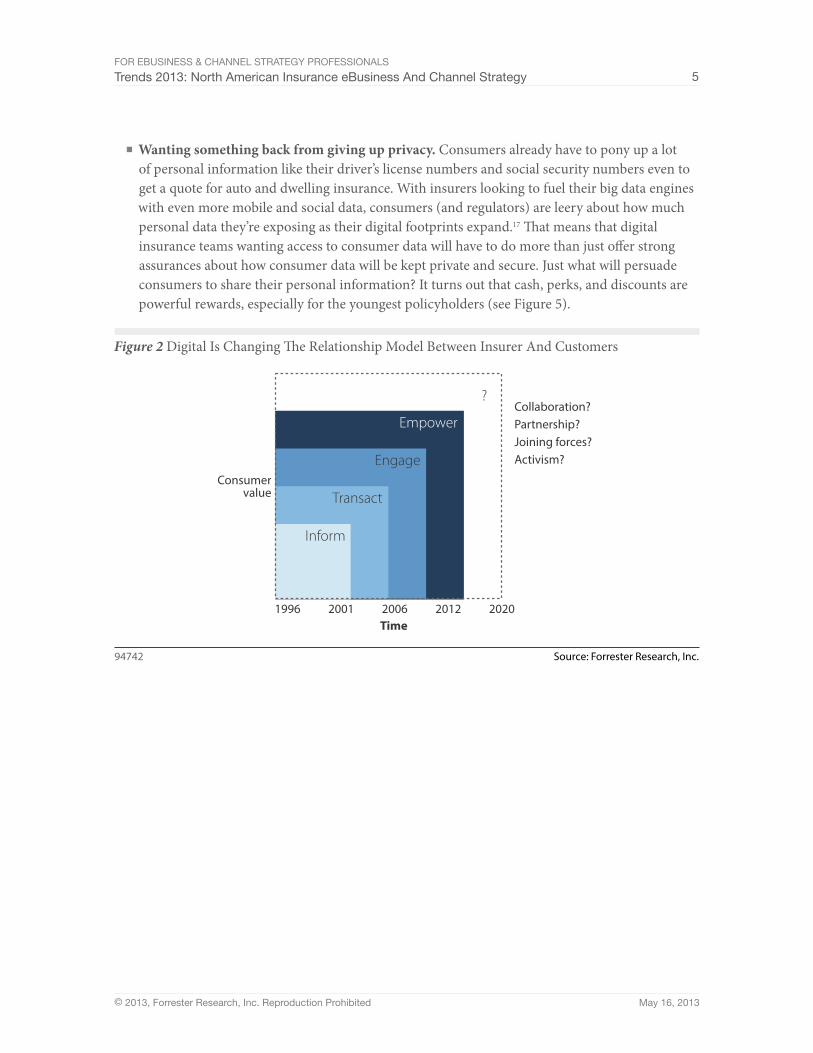

■ Empowered by mobile and social to expand their roles. The role that the Internet has in consumer lives has evolved from being a means to inform at its inception to being a way to engage with and empower customers (see Figure 2). It’s now moving from simply creating empowered customers to creating customer activists. This activism is taking on highly public forms that have resulted in business strategy changes, where the consumer has taken on the role of regulator.9 That activism is also taking less public forms such as Castlight Health’s employer-sponsored mobile healthcare and quality transparency app that could lead consumers to negotiate provider prices in the shift to high-deductible plans.10

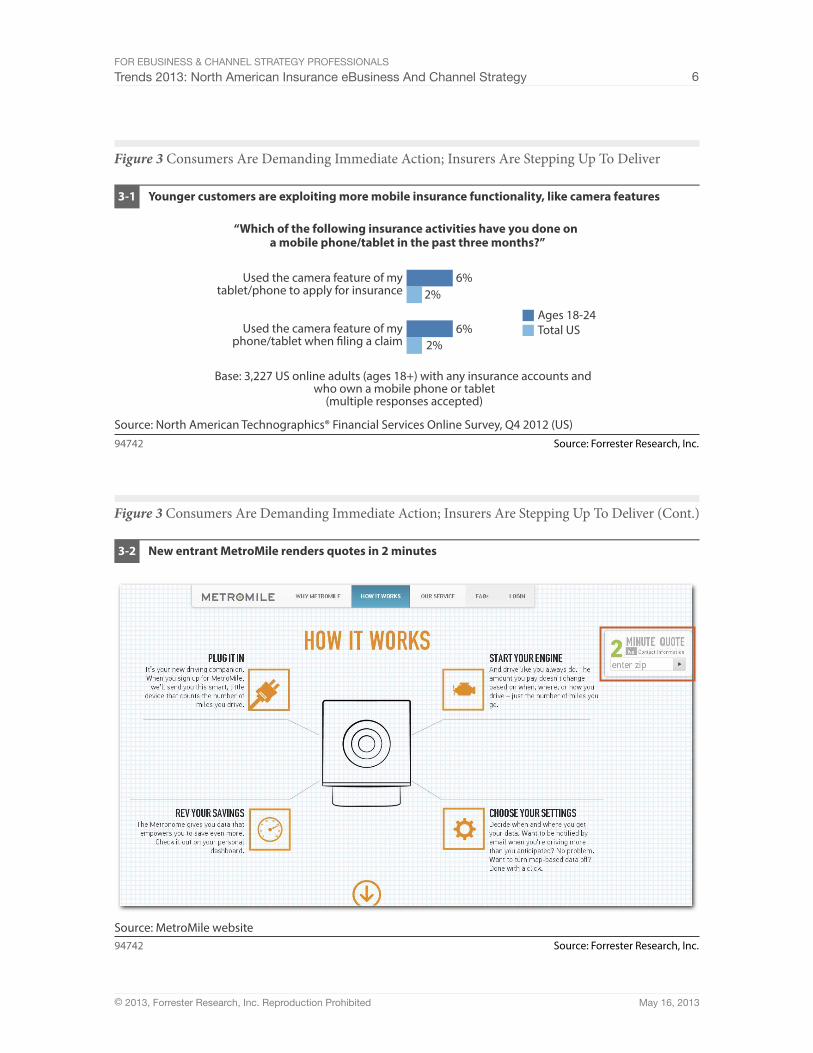

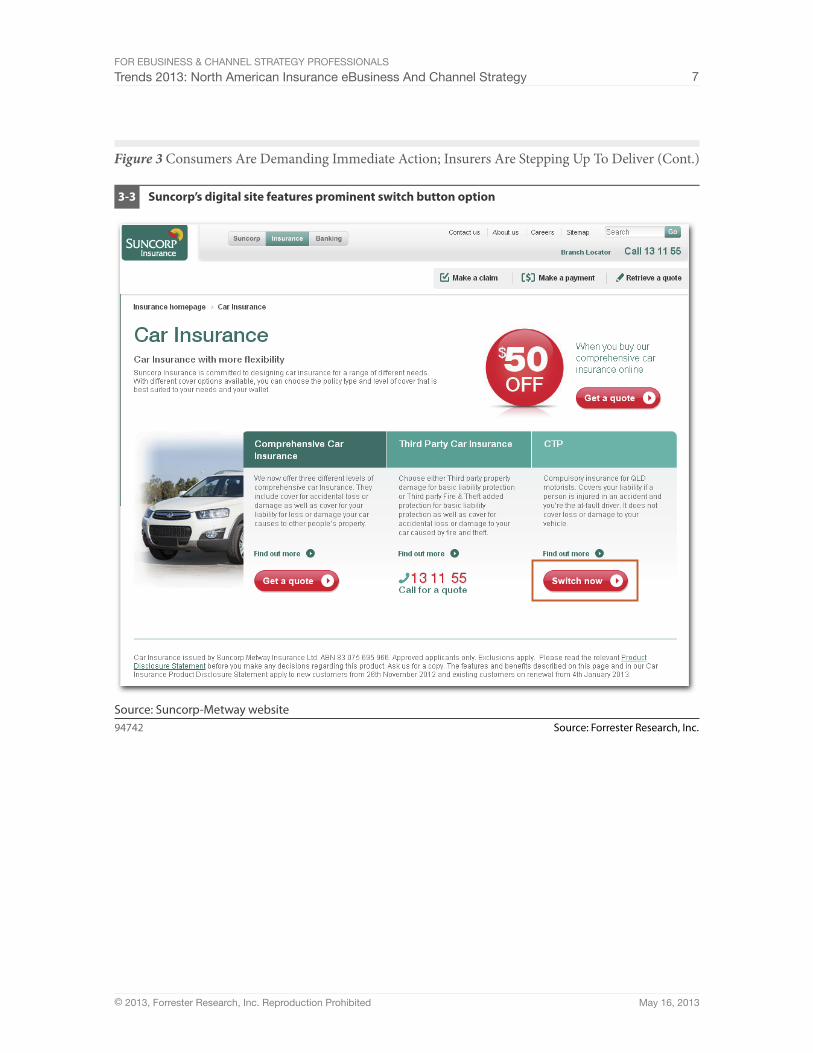

■ Expecting instant gratification. Patience is a long-gone virtue.11 Digital experiences are causing younger consumers to demand immediate results. For example, 6% of surveyed online adult policyholders between ages 18 and 24 have grabbed their phones or tablets and used their device’s photo image capture function when applying and claiming versus 2% of US online adults surveyed who admitted using that same functionality (see Figure 3-1). In another example, US pay-as-you-drive startup MetroMile is pitching a 2-minute insurance quote only to be one-upped by Australian insurer Suncorp’s smoking-fast 30-second quote promise (see Figure 3-2). And Suncorp is taking that instant gratification a step further, by positioning a big red “switch” button on its site to quickly draw in shoppers in the market to change carriers, an innovation that could be easily copied by Canadian and US insurers (see Figure 3-3).12

■ Demanding more personalized and tailored experiences. Customers now expect that experiences from insurers will emulate online retail — and member association — even for digital small business offerings. These expectations are driving new ways to sell complex insurance products. Online banker Movencorp uses a personality test to understand the consumer’s financial personality to target and tailor services to specific consumer behaviors.13 Allstate Insurance made a game attempt with its My Insurance Personality test, which only makes suggestions about relative insurance needs.14 More robust ones from a variety of insurers will be unveiled during 2013.

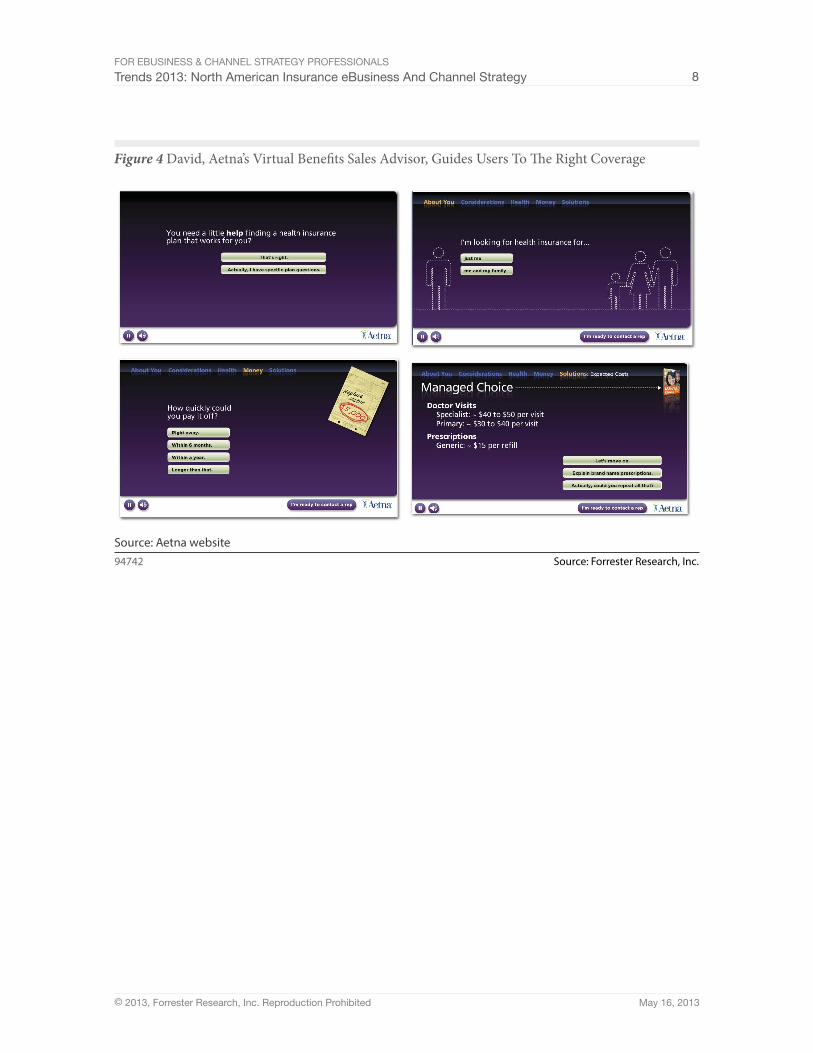

■ Looking for fun. Done right, gaming features can motivate people to complete tasks they might otherwise not do.15 That includes preparing for retirement and thinking about life insurance, challenges for 20-somethings who have a hard time projecting life 50 years out.16 Likewise, shopping for insurance online can be hard because consumers are confronted with terms they don’t understand, especially in big structural disruptions such as with consumer-directed health plans. Aetna tackles it with its conversational and engaging Virtual Benefits Advisor, David, essentially a guided selling tool that uses a very clever approach in helping customers understand their ability to pay deductibles (see Figure 4).

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 5

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

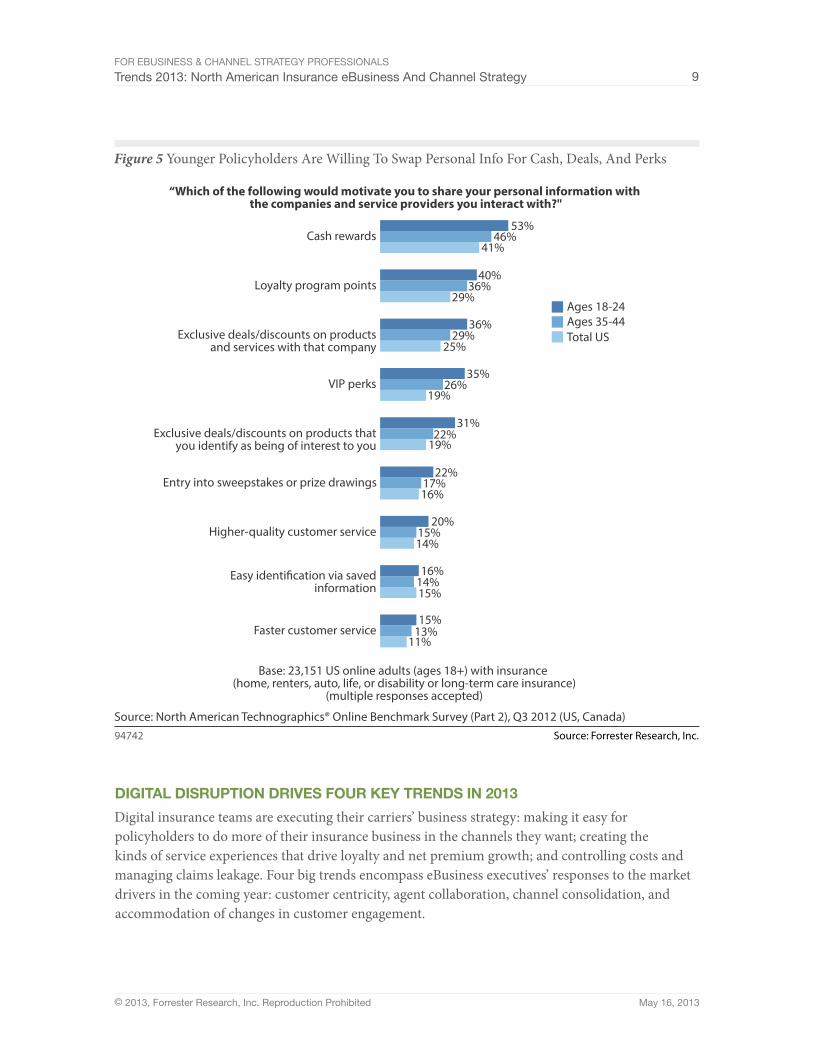

■ Wanting something back from giving up privacy. Consumers already have to pony up a lot of personal information like their driver’s license numbers and social security numbers even to get a quote for auto and dwelling insurance. With insurers looking to fuel their big data engines with even more mobile and social data, consumers (and regulators) are leery about how much personal data they’re exposing as their digital footprints expand.17 That means that digital insurance teams wanting access to consumer data will have to do more than just offer strong assurances about how consumer data will be kept private and secure. Just what will persuade consumers to share their personal information? It turns out that cash, perks, and discounts are powerful rewards, especially for the youngest policyholders (see Figure 5).

Figure 2 Digital Is Changing The Relationship Model Between Insurer And Customers

Source: Forrester Research, Inc.94742

Time

Consumervalue Transact

Inform

Engage

Empower

1996 2001 2006 2012 2020

?Collaboration?Partnership?Joining forces?Activism?

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 6

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 3 Consumers Are Demanding Immediate Action; Insurers Are Stepping Up To Deliver

Source: Forrester Research, Inc.94742

Source: North American Technographics® Financial Services Online Survey, Q4 2012 (US)

6%

6%

Used the camera feature of myphone/tablet when �ling a claim

Used the camera feature of mytablet/phone to apply for insurance

Ages 18-24Total US

Base: 3,227 US online adults (ages 18+) with any insurance accounts and who own a mobile phone or tablet

(multiple responses accepted)

2%

2%

“Which of the following insurance activities have you done on a mobile phone/tablet in the past three months?”

Younger customers are exploiting more mobile insurance functionality, like camera features3-1

Figure 3 Consumers Are Demanding Immediate Action; Insurers Are Stepping Up To Deliver (Cont.)

Source: Forrester Research, Inc.94742

Source: MetroMile website

New entrant MetroMile renders quotes in 2 minutes3-2

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 7

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 3 Consumers Are Demanding Immediate Action; Insurers Are Stepping Up To Deliver (Cont.)

Source: Forrester Research, Inc.94742

Source: Suncorp-Metway website

Suncorp’s digital site features prominent switch button option3-3

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 8

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 4 David, Aetna’s Virtual Benefits Sales Advisor, Guides Users To The Right Coverage

Source: Forrester Research, Inc.94742

Source: Aetna website

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 9

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 5 Younger Policyholders Are Willing To Swap Personal Info For Cash, Deals, And Perks

Source: Forrester Research, Inc.94742

Source: North American Technographics® Online Benchmark Survey (Part 2), Q3 2012 (US, Canada)

14%

16%

19%

19%

25%

29%

41%

15%

15%

13%11%

14%

17%

22%

26%

29%

36%

46%

15%

16%

20%

22%

31%

35%

36%

40%

53%

Faster customer service

Easy identi�cation via savedinformation

Higher-quality customer service

Entry into sweepstakes or prize drawings

Exclusive deals/discounts on products thatyou identify as being of interest to you

VIP perks

Exclusive deals/discounts on productsand services with that company

Loyalty program points

Cash rewards

Ages 18-24Ages 35-44Total US

Base: 23,151 US online adults (ages 18+) with insurance (home, renters, auto, life, or disability or long-term care insurance)

(multiple responses accepted)

“Which of the following would motivate you to share your personal information with the companies and service providers you interact with?"

DIgITal DIsRupTION DRIves FOuR Key TReNDs IN 2013

Digital insurance teams are executing their carriers’ business strategy: making it easy for policyholders to do more of their insurance business in the channels they want; creating the kinds of service experiences that drive loyalty and net premium growth; and controlling costs and managing claims leakage. Four big trends encompass eBusiness executives’ responses to the market drivers in the coming year: customer centricity, agent collaboration, channel consolidation, and accommodation of changes in customer engagement.

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 10

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Falling In love again: Carriers Rekindle The agent Flame

One standout trend in 2013 is the attention that carriers are again lavishing on their agents. Even with all of the ways that consumers can buy and get service for their insurance needs, the local agent who knows that customer and that market remains a top consumer choice. No surprise, understanding why that agent can promote a feeling of being protected among its customer base and what makes the independent agent tick in terms of writing business with one carrier over another are keen carrier interests. Just how is the re-found affection for the agent being manifested in insurers’ digital strategies?

■ Embedding more multichannel functionality. When shopping for insurance, many consumers go online for their research. But when it comes to the application and purchase, many of these online shoppers turn to human channels, like the local agent.18 Canadian auto and home insurer Intact Insurance cross-pollinates the processes of online research with the broker by featuring a clickable online auto quote button for each broker appearing in its locator, marrying its knowledge of consumer shopping behavior and the need to retain broker loyalty.19

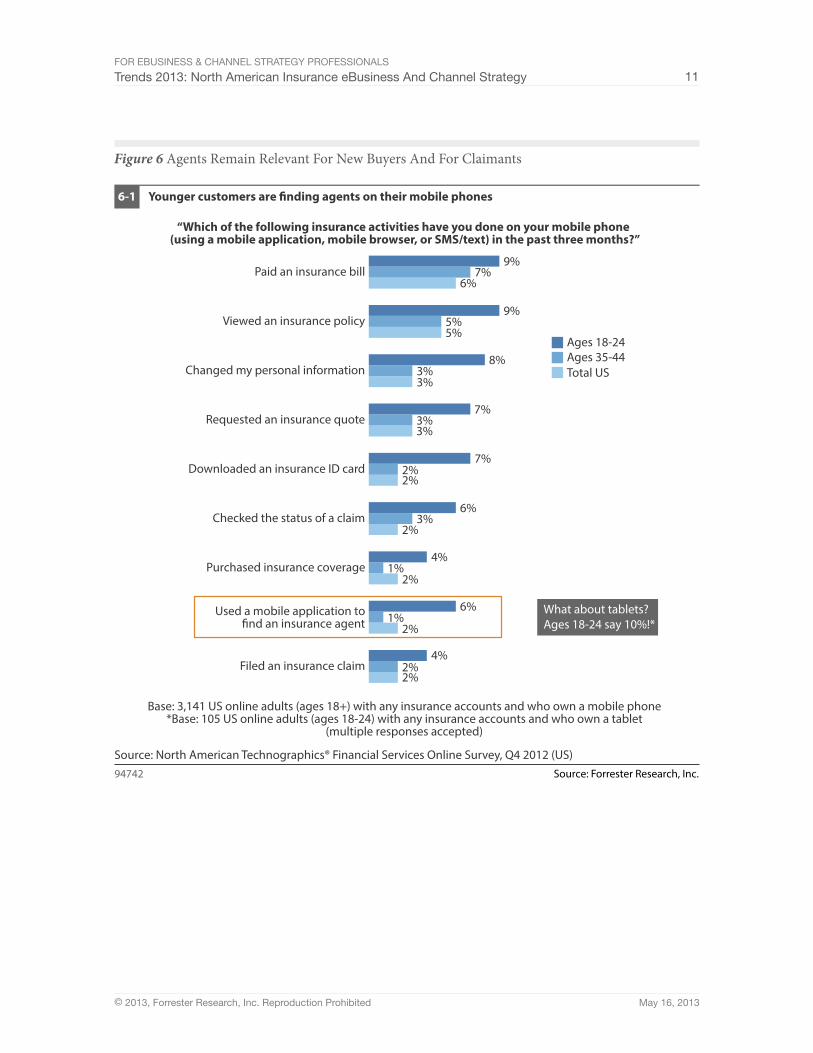

■ Mobilizing to support agent sales and boost productivity. Touchscreen-based smartphones and tablets are purpose-built for the needs of the insurance agents, brokers, and advisors.20 One of the most useful mobile features are agent locator tools that marry context — where the user is located — with a list of nearby agents, including contact information, maps and directions, as well as languages spoken. Just who’s using smartphones and tablets to put their finger on agent locator tools? In a surprising twist, it’s online mobile phone owners with insurance accounts between ages 18 and 24 who report the most frequent use of mobile agent locators, with 6% reporting having used a smartphone and 10% of them with a tablet having used a tablet to find a local agent in the past three months (see Figure 6-1).

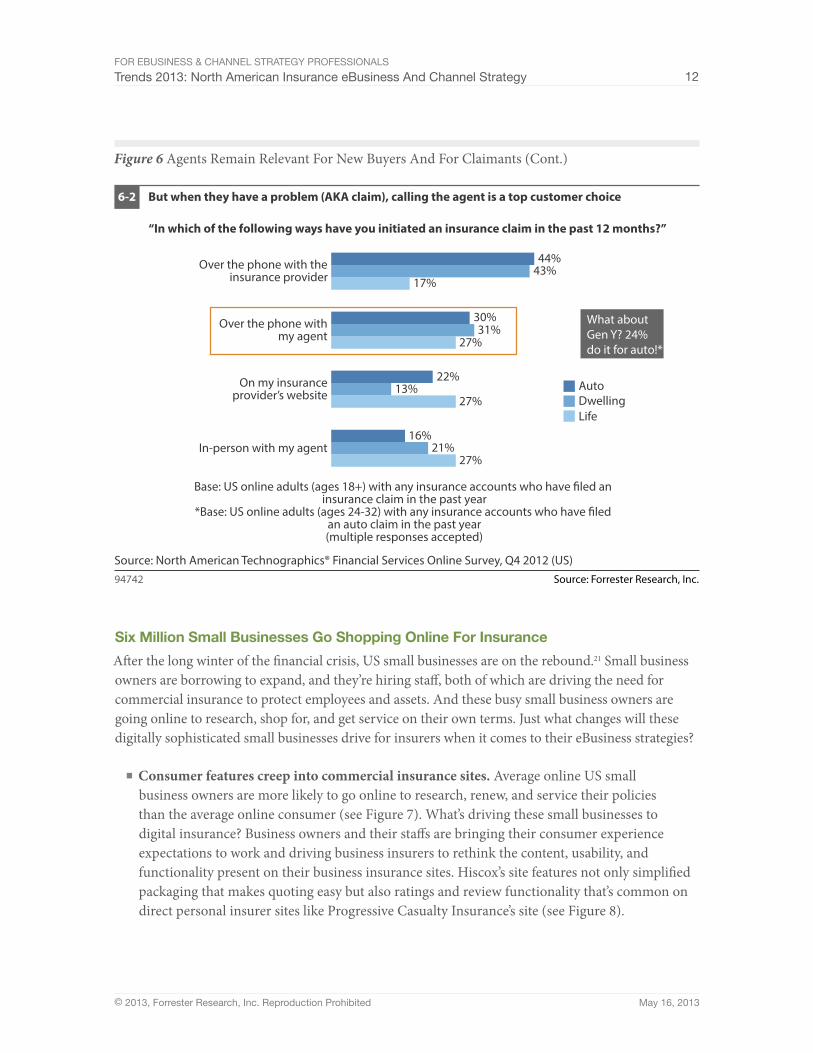

■ Streamlining agent portal access. When policyholders have a problem, like a claim, what are they most likely to do? More than 40% of US online insurance owners who have filed an auto or dwelling claim in the past year will pick up the phone to talk to their insurers, and at least 30% will call their agents (see Figure 6-2). But poor portal performance ends up being one more stone in the agent’s shoe when he or she is saving the carrier servicing costs and engendering that feeling of being protected just when that policyholder has a problem. Use scenario design methodologies to first learn which agents are using which portal functionality, what their goals are when they visit, and how they expect to accomplish their goals in the portal, and then understand the cost of difficult-to-navigate portals.

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 11

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 6 Agents Remain Relevant For New Buyers And For Claimants

Source: Forrester Research, Inc.94742

Source: North American Technographics® Financial Services Online Survey, Q4 2012 (US)

2%

2%

2%

3%

3%

5%

6%

1%

2%

2%2%

1%

3%

2%

3%

3%

5%

7%

4%

6%

4%

6%

7%

7%

8%

9%

9%

Filed an insurance claim

Used a mobile application to�nd an insurance agent

Purchased insurance coverage

Checked the status of a claim

Downloaded an insurance ID card

Requested an insurance quote

Changed my personal information

Viewed an insurance policy

Paid an insurance bill

Ages 18-24Ages 35-44Total US

What about tablets?Ages 18-24 say 10%!*

Base: 3,141 US online adults (ages 18+) with any insurance accounts and who own a mobile phone*Base: 105 US online adults (ages 18-24) with any insurance accounts and who own a tablet

(multiple responses accepted)

“Which of the following insurance activities have you done on your mobile phone (using a mobile application, mobile browser, or SMS/text) in the past three months?”

Younger customers are �nding agents on their mobile phones6-1

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 12

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 6 Agents Remain Relevant For New Buyers And For Claimants (Cont.)

Source: Forrester Research, Inc.94742

Source: North American Technographics® Financial Services Online Survey, Q4 2012 (US)

Base: US online adults (ages 18+) with any insurance accounts who have �led an insurance claim in the past year

*Base: US online adults (ages 24-32) with any insurance accounts who have �led an auto claim in the past year(multiple responses accepted)

But when they have a problem (AKA claim), calling the agent is a top customer choice6-2

27%

27%

27%

17%

21%

13%

31%

43%

16%

22%

30%

44%

In-person with my agent

On my insuranceprovider’s website

Over the phone withmy agent

Over the phone with theinsurance provider

“In which of the following ways have you initiated an insurance claim in the past 12 months?”

AutoDwellingLife

What aboutGen Y? 24% do it for auto!*

six Million small Businesses go shopping Online For Insurance

After the long winter of the financial crisis, US small businesses are on the rebound.21 Small business owners are borrowing to expand, and they’re hiring staff, both of which are driving the need for commercial insurance to protect employees and assets. And these busy small business owners are going online to research, shop for, and get service on their own terms. Just what changes will these digitally sophisticated small businesses drive for insurers when it comes to their eBusiness strategies?

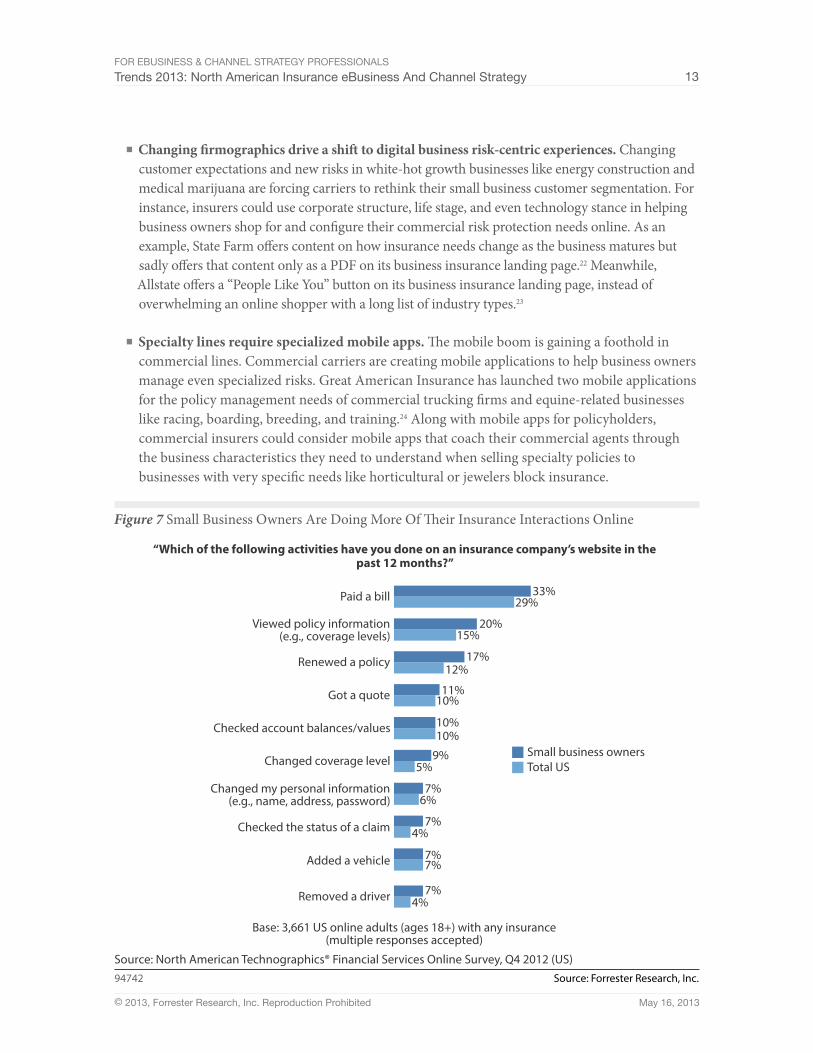

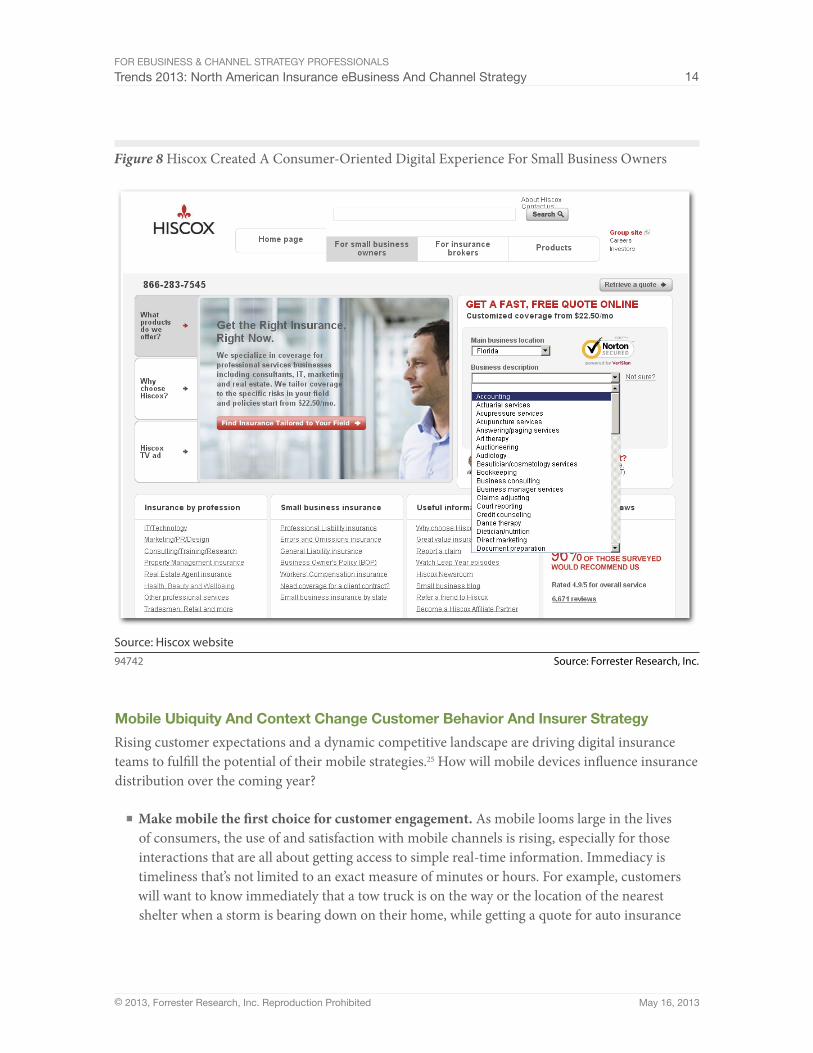

■ Consumer features creep into commercial insurance sites. Average online US small business owners are more likely to go online to research, renew, and service their policies than the average online consumer (see Figure 7). What’s driving these small businesses to digital insurance? Business owners and their staffs are bringing their consumer experience expectations to work and driving business insurers to rethink the content, usability, and functionality present on their business insurance sites. Hiscox’s site features not only simplified packaging that makes quoting easy but also ratings and review functionality that’s common on direct personal insurer sites like Progressive Casualty Insurance’s site (see Figure 8).

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 13

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

■ Changing firmographics drive a shift to digital business risk-centric experiences. Changing customer expectations and new risks in white-hot growth businesses like energy construction and medical marijuana are forcing carriers to rethink their small business customer segmentation. For instance, insurers could use corporate structure, life stage, and even technology stance in helping business owners shop for and configure their commercial risk protection needs online. As an example, State Farm offers content on how insurance needs change as the business matures but sadly offers that content only as a PDF on its business insurance landing page.22 Meanwhile, Allstate offers a “People Like You” button on its business insurance landing page, instead of overwhelming an online shopper with a long list of industry types.23

■ Specialty lines require specialized mobile apps. The mobile boom is gaining a foothold in commercial lines. Commercial carriers are creating mobile applications to help business owners manage even specialized risks. Great American Insurance has launched two mobile applications for the policy management needs of commercial trucking firms and equine-related businesses like racing, boarding, breeding, and training.24 Along with mobile apps for policyholders, commercial insurers could consider mobile apps that coach their commercial agents through the business characteristics they need to understand when selling specialty policies to businesses with very specific needs like horticultural or jewelers block insurance.

Figure 7 Small Business Owners Are Doing More Of Their Insurance Interactions Online

Source: Forrester Research, Inc.94742

Source: North American Technographics® Financial Services Online Survey, Q4 2012 (US)

Small business ownersTotal US

Base: 3,661 US online adults (ages 18+) with any insurance(multiple responses accepted)

“Which of the following activities have you done on an insurance company’s website in thepast 12 months?”

Changed my personal information(e.g., name, address, password)

Changed coverage level

Checked account balances/values

Got a quote

Checked the status of a claim

Removed a driver

Paid a bill

Viewed policy information(e.g., coverage levels)

Added a vehicle

Renewed a policy

33%

4%7%

7%7%

4%7%

6%7%

5%9%

10%10%

10%11%

12%17%

15%

29%

20%

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 14

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 8 Hiscox Created A Consumer-Oriented Digital Experience For Small Business Owners

Source: Forrester Research, Inc.94742

Source: Hiscox website

Mobile ubiquity and Context Change Customer Behavior and Insurer strategy

Rising customer expectations and a dynamic competitive landscape are driving digital insurance teams to fulfill the potential of their mobile strategies.25 How will mobile devices influence insurance distribution over the coming year?

■ Make mobile the first choice for customer engagement. As mobile looms large in the lives of consumers, the use of and satisfaction with mobile channels is rising, especially for those interactions that are all about getting access to simple real-time information. Immediacy is timeliness that’s not limited to an exact measure of minutes or hours. For example, customers will want to know immediately that a tow truck is on the way or the location of the nearest shelter when a storm is bearing down on their home, while getting a quote for auto insurance

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 15

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

has less urgency. The same goes for sharing information with the insurance provider. The mobile app Phrex lets users exchange documents with other Phrex users, which is ideal for all those trailing claim documents.26

■ Winnow down native apps to make room for new functionality and experiences. Mobile insurance apps are chock full of functions.27 But with spending on the rise to enable mobile services, supporting these portable connections is no longer cheap.28 Facing expensive development and maintenance costs for native apps, many digital professionals are choosing the Web over apps to support devices with smaller market shares. Expect to see digital insurance strip out functionality from native apps that experience (and analytics) proves no longer makes sense — like quoting — in favor of more valuable features to prepare themselves in case of an emergency, such as Security First Insurance’s embedded shelter locator for its hurricane-prone customer base, as well as to simplify and accelerate the claims settlement process, such as Symbility Solutions’ mobile “consumer as adjuster” functionality.

■ Focus on measuring mobile’s changing multichannel impact. Advanced analytics techniques for the mobile Web and apps are getting more attention from digital insurance business teams earlier in the development process. And they’re getting a hand from newer technologies like tag management systems. More eBusiness professionals are thinking about how to make the shift from mobile to physical touchpoints more fluid. Interactive Intelligence’s Interaction Mobilizer not only supplies contextual information to call center agents about mobile callers but also fuels insurers’ analytic engines.29

Health Plans prep For The Crush Of Consumer Health Plan ShoppingThe most frequent inquiries Forrester received from its US insurance clients in 2012 were questions from all manner of roles within health plans, as looming 2013 exchange deadlines neared.30 Just like retailers ramping up for key holiday shopping dates like Black Friday and Cyber Monday, health plans are readying their public exchange strategies in order to prepare for a crush of health plan shoppers on October 1, 2013. At the same time, consumers have heightened experience expectations as a result of their interactions with their online retailers, banks, and even auto insurers, driving plan attention on their private exchange strategies. Take into account these three business trends that highlight the needs of consumer-directed health plan buyers and what health plan digital strategists tell us are at the top of their agendas in 2013:

■ Change your thinking about reform from threat to opportunity for change. Even with the uncertainty of June 2012’s US Supreme Court decision and November 2012’s presidential election, digital strategists were turning lemons into lemonade, forging ahead and readying their digital strategy. What was propelling these digital teams forward? While attention in the media has primarily been on public exchange solutions, significant efforts are going into private exchange initiatives, largely because plans view their ability to meet the needs of direct-to-the-

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 16

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

consumer as the differentiator of the future. With multimillion-dollar exchange budgets, many are hiring expertise from digital direct-to-consumer industries to prepare them for this new and very different business-to-consumer model.

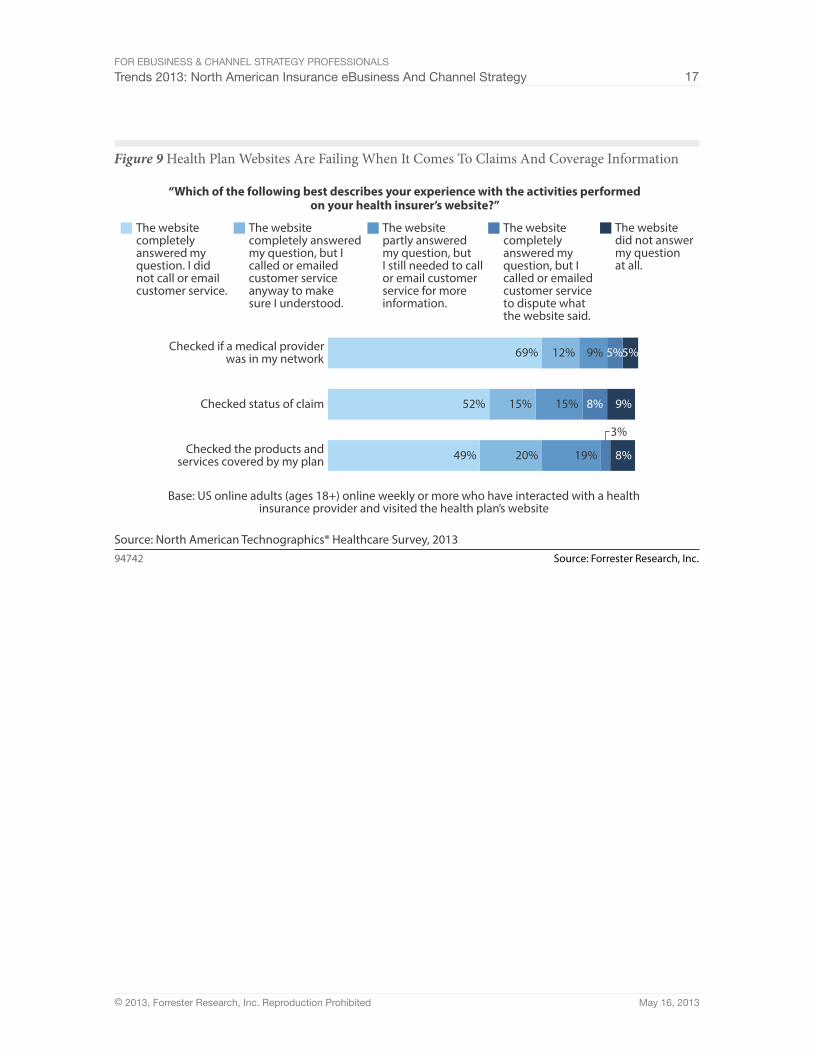

■ Prioritize attention on web sales and service functionality. With time running out to address all manner of exchanges and reorient websites from being business-to-business to business-to-consumer, digital business teams need to be concerned about their online presence. Why? Because consumers can’t find answers on health insurance websites about coverage, providers, and claims status. In Forrester’s North American Technographics® Healthcare Survey, 2013, just fewer than half of US online consumers who had visited a health insurance website in the past year felt that the website fully answered their question around what products and services their plans covered (see Figure 9). Worse, many plans are failing to provide even the basic product information, research tools, and application functionality that a consumer would be looking for to apply for coverage on plan websites.31

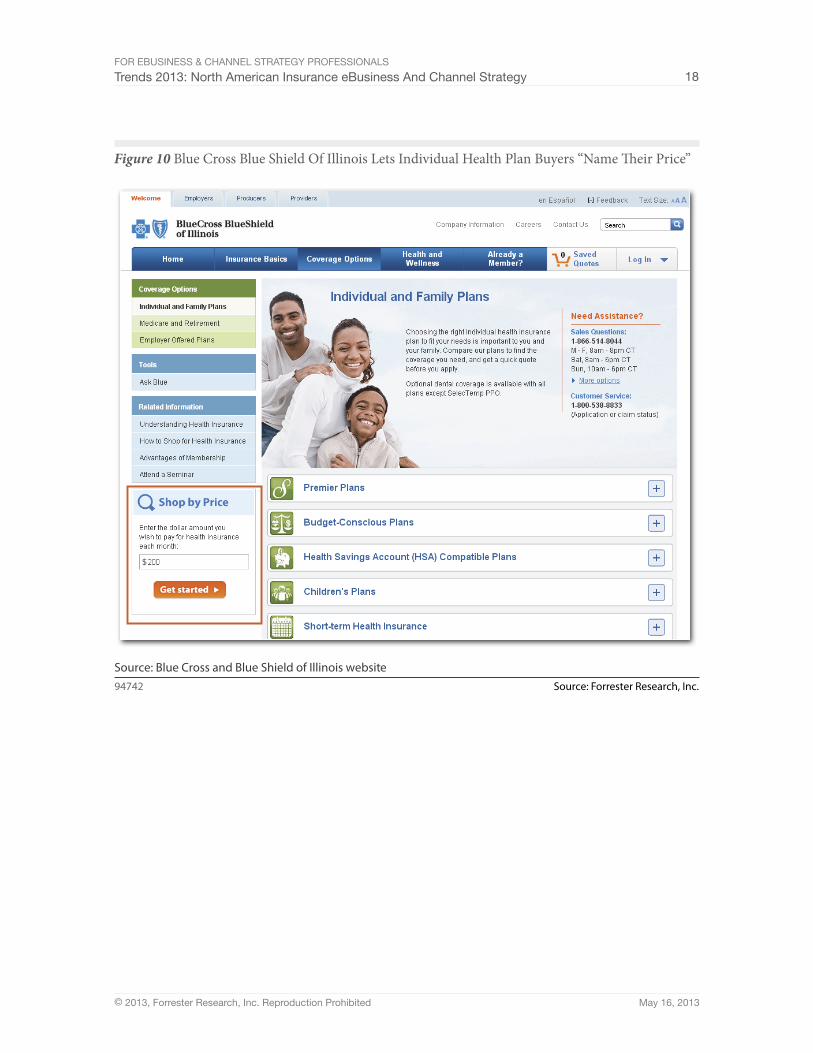

■ Turn to digital role models outside of healthcare. In our inquiries with the plans’ digital business teams, conversations often turned to digital best practices in industries outside of healthcare. Which digital experiences did health plans want to emulate? Top honors went to Progressive Casualty Insurance, Apple, and Amazon.com. Indeed, private health plans are going so far as to look at being distributors for the kinds of voluntary and group benefits that consumers were purchasing through employer payroll deductions. Still, others were looking at launching selling functionality like comparative raters and ratings and reviews. And plans aren’t waiting for reform deadlines to hit to launch new sales tools. For instance, Blue Cross and Blue Shield of Illinois rolled out shop-by-price functionality on its home page, a clear riff on Progressive Casualty Insurance’s Name Your Price tool (see Figure 10).

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 17

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 9 Health Plan Websites Are Failing When It Comes To Claims And Coverage Information

Source: Forrester Research, Inc.94742

Source: North American Technographics® Healthcare Survey, 2013

“Which of the following best describes your experience with the activities performedon your health insurer’s website?”

49%

52%

69%

20%

15%

12%

19%

15%

9%

3%

8%

5%

8%

9%

5%

Checked the products andservices covered by my plan

Checked status of claim

Checked if a medical providerwas in my network

The websitecompletelyanswered myquestion. I didnot call or emailcustomer service.

The websitecompletely answeredmy question, but Icalled or emailedcustomer serviceanyway to makesure I understood.

The websitepartly answeredmy question, butI still needed to callor email customerservice for moreinformation.

The websitecompletelyanswered myquestion, but Icalled or emailedcustomer serviceto dispute whatthe website said.

The websitedid not answermy questionat all.

Base: US online adults (ages 18+) online weekly or more who have interacted with a healthinsurance provider and visited the health plan’s website

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 18

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

Figure 10 Blue Cross Blue Shield Of Illinois Lets Individual Health Plan Buyers “Name Their Price”

Source: Forrester Research, Inc.94742

Source: Blue Cross and Blue Shield of Illinois website

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 19

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

suppleMeNTal MaTeRIal

survey Methodology

In its North American Technographics® Healthcare Survey, 2013, Forrester Research conducted an online survey fielded in February 2013 of 4,504 US individuals ages 18 to 88. For results based on a randomly chosen sample of this size (N = 4,504), there is 95% confidence that the results have a statistical precision of plus or minus 1.46% of what they would be if the entire population of US online individuals (defined as those online weekly or more often) ages 18 and older had been surveyed. Forrester weighted the data by age, gender, income, broadband adoption, and region to demographically represent the adult US online population. The survey sample size, when weighted, was 4,458. (Note: Weighted sample sizes can be different from the actual number of respondents to account for individuals generally underrepresented in online panels.)

In its North American Technographics Financial Services Online Survey, Q4 2012 (US), Forrester conducted an online survey fielded in November 2012 of 4,501 US individuals ages 18 to 88. For results based on a randomly chosen sample of this size (N = 4,501), there is 95% confidence that the results have a statistical precision of plus or minus 1.46% of what they would be if the entire population of US online individuals ages 18 and older had been surveyed. Forrester weighted the data by age, gender, income, broadband adoption, and region to demographically represent the adult US online population. The survey sample size, when weighted, was 4,458. (Note: Weighted sample sizes can be different from the actual number of respondents to account for individuals generally underrepresented in online panels.)

In its North American Technographics Financial Services Online Survey, Q4 2011 (US), Forrester conducted an online survey fielded in October 2011 of 4,505 US individuals ages 18 to 88. For results based on a randomly chosen sample of this size (N = 4,505), there is 95% confidence that the results have a statistical precision of plus or minus 1.46% of what they would be if the entire population of US online individuals ages 18 and older had been surveyed. Forrester weighted the data by age, gender, income, broadband adoption, and region to demographically represent the adult US online population. The survey sample size, when weighted, was 4,504. (Note: Weighted sample sizes can be different from the actual number of respondents to account for individuals generally underrepresented in online panels.)

Please note that all three surveys were online surveys. Respondents who participate in online surveys have in general more experience with the Internet and feel more comfortable transacting online. The data is weighted to be representative for the total online population on the weighting targets mentioned, but this sample bias may produce results that differ from Forrester’s offline benchmark survey. The samples were drawn from members of MarketTools’ online panel, and respondents were motivated by receiving points that could be redeemed for a reward. The samples provided by MarketTools are not random samples. While individuals have been randomly sampled from MarketTools’ panel for each of these surveys, they have previously chosen to take part in the MarketTools online panel.

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 20

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

eNDNOTes1 Source: Justin Stephani, “Actuaries Examine the Impact of Health Care Reform on P&C Insurers,” Insurance

Networking News, March 27, 2013 (http://www.insurancenetworking.com/news/actuaries-examine-impact-of-healthcare-reform-on-pc-insurers-32048-1.html).

2 Retail medical cannabis sales in the US could hit an estimated $1.3 billion to $1.5 billion in 2013 and are forecast to grow to $6 billion by 2018, according to a report released by MMJ Business Daily. Source: Chris Walsh, “Exclusive: US Medical Marijuana Sales to Hit $1.5B in 2013, Cannabis Revenues Could Quadruple by 2018,” MMJ Business Daily, March 21, 2013 (http://mmjbusinessdaily.com/2013/03/21/us-medical-marijuana-sales-estimated-at-1-5b-in-2013-cannabis-industry-could-quadruple-by-2018/).

3 In much the same way that car owners are required to buy auto insurance, gun owners could be required to buy a liability policy when purchasing firearms. The thinking (and hope) is that doing so would give a financial incentive for safe behavior, as people with less dangerous weapons or safety locks could qualify for lower rates. Source: Michael Cooper and Mary Williams Walsh, “Buying a Gun? States Consider Insurance Rule,” The New York Times, February 21, 2013 (http://www.nytimes.com/2013/02/22/us/in-gun-debate-a-bigger-role-seen-for-insurers.html?pagewanted=all&_r=0).

4 2012 was the third most expensive on record with respect to insured losses, based on a report by Swiss Re. The most expensive event last year was Superstorm Sandy, with Swiss Re estimating insured losses of $35 billion. In terms of economic loss, Swiss Re says Sandy is the second most expensive wind event on record at $70 billion. Hurricane Katrina in 2005 still tops the list at more than $100 billion. Source: “Natural catastrophes and man-made disasters in 2012,” Swiss Re, 2013 (http://media.swissre.com/documents/sigma2_2013_en.pdf).

5 Source: “Swiss Re cites US weather for big insurance losses,” TheHuffingtonPost.com, March 27, 2013 (http://www.huffingtonpost.com/huff-wires/20130327/eu-world-disasters-insured-losses/?utm_hp_ref=green&ir=green).

6 According to Forrester’s Forrsights Budgets And Priorities Tracker Survey, Q2 2012, the software category that commanded the highest number of respondents stating that their spend would increase by at least 5% was business intelligence and real-time analytics software.

7 A unit of Assurant, Protect Your Bubble covers the stuff in the consumers’ home from the technology they use daily — like smartphones, tablets, laptops, and TVs — to furry family members and everything in between. Source: “Get to know Protect Your Bubble,” Protect Your Bubble (http://us.protectyourbubble.com/about-protect-your-bubble/about-us.html).

8 Technology developments are also suggesting disruption in the broad healthcare market, just as in insurance, and have already disrupted other industries. Source: Jonathan Cohn, “The Robot Will See You Now,” The Atlantic Monthly, February 20, 2013 (http://www.theatlantic.com/magazine/archive/2013/03/the-robot-will-see-you-now/309216/).

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 21

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

9 Regulation is getting crowdsourced, according to writers Don Tapscott and Anthony Williams. Source: Don Tapscott and Anthony Williams, “Macrowikinomics: The Citizen Regulator: Increased Citizen Participation Adds Muscle to Traditional Regulatory Systems,” TheHuffingtonPost.com, January 4, 2011 (http://www.huffingtonpost.com/don-tapscott/macrowikinomics-the-citiz_b_804284.html).

10 Healthcare transparency is changing the way healthcare is consumed. Armed with information about both the cost and the quality of care, people can utilize less expensive care while achieving better outcomes. Founded in 2008, Castlight Health delivers the solution to enable employers and health plans to lower the cost of healthcare and provide individuals with unbiased pricing and quality information to make smart healthcare purchase decisions. Source: Castlight Health (http://www.castlighthealth.com/company/).

11 Teens and young adults brought up from childhood with a continuous connection to each other and to information will be nimble quick-acting multitaskers who count on the Internet as their external brain and who approach problems in a different way from their elders. But the experts also predict that this generation will exhibit a thirst for instant gratification and quick fixes, a loss of patience, and a lack of deep-thinking ability due to what one referred to as “fast-twitch wiring,” according to a Pew Internet & American Life Project survey. Source: Janna Anderson and Lee Rainie, “Millennials will benefit and suffer due to their hyperconnected lives,” Pew Internet & American Life Project, February 29, 2012 (http://pewinternet.org/Reports/2012/Hyperconnected-lives.aspx).

12 Indeed, one in five US online adults who are auto and dwelling insurance buyers either were planning on switching or were on the fence about their insurance carriers in 2012. See the February 23, 2012, “Gone Shopping: US Auto And Home Insurance Buyers Will Test eBusiness Strategies In 2012” report.

13 For additional information, check out Mowen’s website. Source: Mowen (https://www.moven.com/).

14 Check out the “My Personality Insurance” test on Allstate Insurance’s website. Source: Allstate Insurance (http://www.allstate.com/myinsurancepersonality.aspx).

15 By employing a suite of game mechanics — including challenges, progress bars, and alerts — Mint persuaded more than 75% of users to log in daily or more frequently. See the January 26, 2012, “Case Study: Mint.com Grows Its Business Using Game Mechanics” report.

16 Gen Yers are a big market, counting as one-third of workforces, and that will grow. Insurers have to take a fresh approach to creating experiences for this segment. Four elements need to be considered: Understand the decision process; engage emotions; plan for mobile at the outset; and think of your audience as a channel. See the July 27, 2011, “Case Study: MassMutual Helps Gen Yers See Into Their Futures” report.

17 Consumers are leaving an exponentially growing digital footprint across channels and media, and they are awakening to the fact that marketers use this data for financial gain. As a result, consumers are demanding a change to the ecosystem. See the September 30, 2011, “Personal Identity Management” report.

18 When it comes to the shift from research to buying, the insurance shopping journey becomes more complicated, making it essential for digital insurance business teams to understand the choices a customer makes when he or she decides to move from researching to applying. See the November 24, 2009, “The US Auto Insurance Buyer’s Journey” report.

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 22

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

19 Using Intact’s broker locator tool and indicating postal code or city and province, online shoppers are presented with a list of nearby agents, each with an “Online Auto Quote” button under the agency name, contact information, and distance. Check out the tool on Intact Insurance’s website. Source: Intact Insurance (https://www.intactinsurance.com/maps-ontario.html?form=locator_search&addressline=Montreal%20QC&returnURL=https%3A//apps.intactinsurance.com/wep/WEP/newQuote.do%3Forigin%3DINTACT%26province%3DON%26language%3Den&AUTOQUOTE=Y®ion=ontario).

20 Insurance shoppers and policyholders expect to interact with insurance companies via the touchpoints of their choice, and digital insurers are aligning their distribution mix to their customers’ preferences. Smartphones, and especially tablets, matter in two important insurance scenarios: customers seeking information on their own and agents looking for greater efficiency. See the November 15, 2012, “Digital Insurance Teams Need A Tablet Strategy” report.

21 According to ADP Research Institute’s National Employment Report, US small businesses that employed 49 or fewer added 196,000 jobs in the first two months of 2013. Source: Automatic Data Processing (http://www.adpemploymentreport.com/).

22 State Farm looks at four stages of the business life cycle: startup, growth, maturity, and transfer. Source: State Farm Mutual Automobile Insurance (http://www.statefarm.com/_pdf/business-life-cycle.pdf).

23 Allstate’s “People Like You” link provides a high-level overview of insurance needs by industry, services, and home-based business. Source: Allstate Insurance (http://www.allstate.com/business-insurance/industries.aspx).

24 Additional information on these apps is available on iTunes. Source: Apple (https://itunes.apple.com/us/app/equine-division/id412469222?mt=8); Apple (https://itunes.apple.com/us/app/gaig-trucking/id580150746?mt=8).

25 Mobile will be the catalyst for changes that will ripple across the insurance industry and ecosystem. Products, payments, distribution, underwriting, operations, and even what constitutes intellectual property will look very different in 2020 because of the native capabilities of mobile devices. See the September 28, 2012, “The Future Of Insurance Is Mobile” report.

26 Phrex is a free mobile document exchange application developed by IBromed. Source: Apple (https://itunes.apple.com/in/app/phrex/id561605223?mt=8).

27 Forrester looked at the mobile apps of more than 30 insurance companies worldwide, assessing the presence of a number of functions. See the January 22, 2013, “The State Of Mobile Insurance In 2013” report.

28 Designing smart mobile services requires new skills and expertise — ranging from design to app development via data scientists and analytics specialists. See the February 13, 2013, “2013 Mobile Trends For eBusiness Professionals” report.

For eBusiness & Channel strategy ProFessionals

trends 2013: north american insurance eBusiness and Channel strategy 23

© 2013, Forrester Research, Inc. Reproduction Prohibited May 16, 2013

29 Source: Interactive Intelligence (http://www.inin.com/solutions/Pages/Mobile-Customer-Service.aspx).

30 When the Affordable Care Act was enacted in March 2010, a number of milestones were spelled out. While many deadlines under the act have passed, two key ones are ahead of US health insurers: the beginning of open enrollment in the health insurance marketplaces on October 1, 2013; and the requirement for all US individuals to have health insurance coverage by January 1, 2014. Check out the timeline of the Affordable Care Act at HealthCare.gov. Source: US Department of Health & Human Services (http://www.healthcare.gov/law/timeline/).

31 In Forrester’s review of the usability of seven health plan websites in 2011, none of the plan websites evaluated was able to muster a passing score in the four dimensions evaluated: value, navigation, presentation, and trust. See the May 19, 2011, “Best And Worst Of Website User Experience, 2011: Health Insurers” report.

Forrester Research, Inc. (Nasdaq: FORR) is an independent research company that provides pragmatic and forward-thinking advice to global leaders in business and technology. Forrester works with professionals in 13 key roles at major companies providing proprietary research, customer insight, consulting, events, and peer-to-peer executive programs. For more than 29 years, Forrester has been making IT, marketing, and technology industry leaders successful every day. For more information, visit www.forrester.com. 94742

«

Forrester Focuses On eBusiness & Channel Strategy Professionals responsible for building a multichannel sales and service strategy,

you must optimize how people, processes, and technology adapt

across a rapidly evolving set of customer touchpoints. Forrester

helps you create forward-thinking strategies to justify decisions and

optimize your individual, team, and corporate performance.

ERIC CHANG, client persona representing eBusiness & Channel Strategy Professionals

About Forresterglobal marketing and strategy leaders turn to Forrester to help

them make the tough decisions necessary to capitalize on shifts

in marketing, technology, and consumer behavior. We ensure your

success by providing:

nData-driven insight to understand the impact of changing consumer behavior.

nForward-looking research and analysis to guide your decisions.

nobjective advice on tools and technologies to connect you with customers.

nBest practices for marketing and cross-channel strategy.

foR moRE INfoRmAtIoN

To find out how Forrester Research can help you be successful every day, please contact the office nearest you, or visit us at www.forrester.com. For a complete list of worldwide locations, visit www.forrester.com/about.

ClIENt suppoRt

For information on hard-copy or electronic reprints, please contact Client Support at +1 866.367.7378, +1 617.613.5730, or [email protected]. We offer quantity discounts and special pricing for academic and nonprofit institutions.