Embed Size (px)

Citation preview

TRANSNET PRESENTATION TO PORTFOLIO COMMITTEE OF PUBLIC

ENTERPRISES

BRIEFING BY STATE OWNED ENTERPRISES ON

BUDGETS AND STRATEGIC PLANS 2009/10 Mr Chris Wells

Acting Group Chief Executive

17 June 2009

Mr Chris Wells

Acting Group Chief Executive

17 June 2009

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities 2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities 2009/10

2

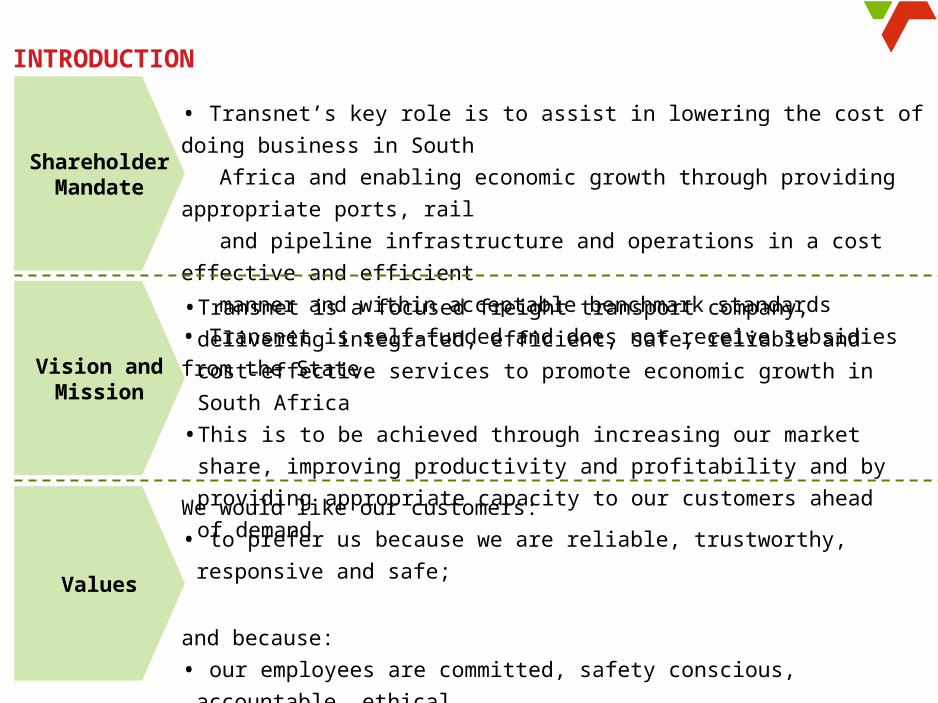

INTRODUCTION

• Transnet is a focused freight transport company, delivering integrated,

efficient, safe, reliable and cost-effective services to promote economic

growth in South Africa

• This is to be achieved through increasing our market share, improving

productivity and profitability and by providing appropriate capacity to our

customers ahead of demand

Vision and Mission

Shareholder Mandate

• Transnet’s key role is to assist in lowering the cost of doing business

in South

Africa and enabling economic growth through providing appropriate

ports, rail

and pipeline infrastructure and operations in a cost effective and

efficient

manner and within acceptable benchmark standards

• Transnet is self-funded and does not receive subsidies from the

State.

Values

We would like our customers:

• to prefer us because we are reliable, trustworthy, responsive and

safe;

and because:

• our employees are committed, safety conscious, accountable,

ethical,

disciplined and results orientated

3

TRANSNET STRUCTURE

*• Luxrail• arivia.kom

4

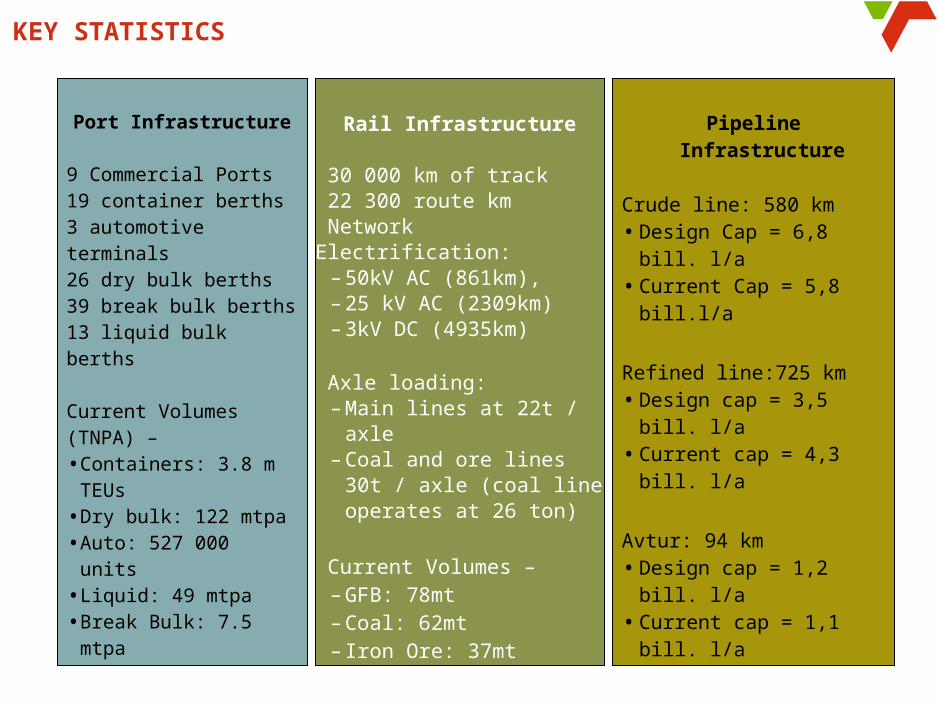

Rail Infrastructure

30 000 km of track 22 300 route km Network Electrification:

– 50kV AC (861km), – 25 kV AC (2309km) – 3kV DC (4935km)

Axle loading:– Main lines at 22t / axle– Coal and ore lines 30t /

axle (coal line operates at 26 ton)

Current Volumes – – GFB: 78mt– Coal: 62mt– Iron Ore: 37mt

Port Infrastructure

9 Commercial Ports19 container berths3 automotive terminals26 dry bulk berths39 break bulk berths13 liquid bulk berths

Current Volumes (TNPA) – • Containers: 3.8 m

TEUs• Dry bulk: 122 mtpa• Auto: 527 000 units• Liquid: 49 mtpa• Break Bulk: 7.5 mtpa

Pipeline Infrastructure

Crude line: 580 km• Design Cap = 6,8 bill. l/a• Current Cap = 5,8 bill.l/a

Refined line:725 km• Design cap = 3,5 bill. l/a• Current cap = 4,3 bill. l/a

Avtur: 94 km• Design cap = 1,2 bill. l/a• Current cap = 1,1 bill. l/a

KEY STATISTICS

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

6

RevenueRevenue

• Continuous increase in revenue showing results of

initiatives to grow the business, with revenue

increasing from R25.3bn in 2004/05 to R30.1bn in

2007/08 (19.0% increase) – 2008/09 in process of

being finalised

EBITDAEBITDA

• Improvements through:

Operational efficiency improvements, effective cost cutting initiatives mainly due to reengineering projects

Sale of discontinuing non-core businesses

• Improvement from R7.3bn in 2004/05 to R12.8bn in 2007/08 (75.3% improvement)

R billionR billion

Gearing (%)Gearing (%)

•Balance sheet restructuring and cost effective debt structures yielding positive results with consistent below target gearing from 61% in 2004/05 to 30% in 2007/08 (50.8% improvement)

•This enables Transnet to fund capital investments more cost effectively and without government guarantees

TRANSNET HAS EFFECTED A SUCCESSFUL FINANCIAL TURNAROUND OVER THE PAST FIVE YEARS

33.630.1

26.926.025.3

+7%

08/09

07/08

06/07

05/06

04/05

12.012.811.110.37.3

07/08

06/07

05/06

04/05

+13%

08/09

-11%

08/09

39%

07/08

30%

06/07

39%

05/06

46%

04/05

61%

CAGR

Budge

tB

udge

tB

ud

get

50%Max

7

Rail

Ports

Pipe-

lines

Key Performance Indicators

Moves per Crane Hour(No. of moves)

SIGNIFICANT IMPROVEMENT IN OPERATIONAL EFFICIENCIES

Containers per Berth (No.)

Weighted Loco Availability

(GFB, Coal and Ore - %)

* Net ton kilometer excluding the weight of the wagon

Net Ton Kilometre per Loco(GFB ‘000)

27

23

08/0904/05

+15% 88%

08/0904/05

82%

+7%

Net Ton Kilometre per Wagon

(GFB ‘000)637

620

04/05 08/09

+3%Improvement in asset utilization releasing the pressure on rolling stock requirements.

1817

18

2221

23

CTCTDCT PE

189,989

08/0904/05

150,261

+26%Sweating the Port assets to create additional capacity and alleviate pressure on investment

Capacity Utilisation(%)

88.5% 83.0%71.7%

87.1%76.5%

104.2%

AvturCrudeRefined

Production Interruptions (Internal & External - Hours)

06/07

965

755

08/09

-22%

Operational improvements and introduction of Drag Reducing Agents allow TPL to exceed design capacities for Refined products

04/05 08/09 04/05 08/09 04/05 08/09

04/05 08/09 04/05 08/09 04/05 08/09

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

9

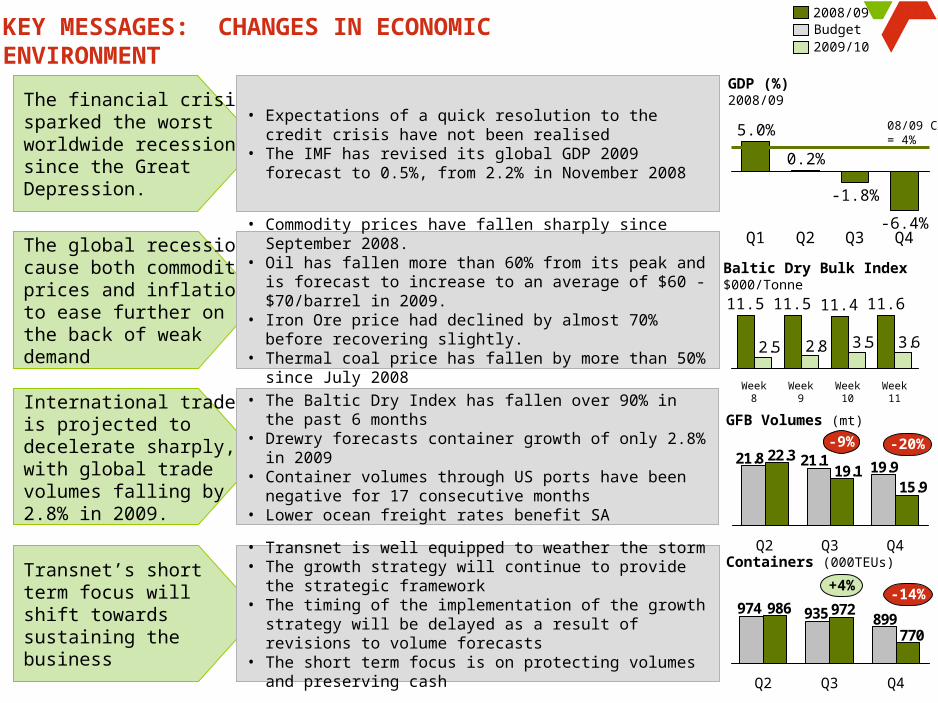

KEY MESSAGES: CHANGES IN ECONOMIC ENVIRONMENT

The global recession cause both commodity prices and inflation to ease further on the back of weak demand

International trade is projected to decelerate sharply, with global trade volumes falling by 2.8% in 2009.

• Commodity prices have fallen sharply since September 2008.

• Oil has fallen more than 60% from its peak and is forecast to increase to an average of $60 -$70/barrel in 2009.

• Iron Ore price had declined by almost 70% before recovering slightly.

• Thermal coal price has fallen by more than 50% since July 2008

• The Baltic Dry Index has fallen over 90% in the past 6 months

• Drewry forecasts container growth of only 2.8% in 2009

• Container volumes through US ports have been negative for 17 consecutive months

• Lower ocean freight rates benefit SA

The financial crisis sparked the worst worldwide recession since the Great Depression.

• Expectations of a quick resolution to the credit crisis have not been realised

• The IMF has revised its global GDP 2009 forecast to 0.5%, from 2.2% in November 2008

Transnet’s short term focus will shift towards sustaining the business

• Transnet is well equipped to weather the storm• The growth strategy will continue to provide the

strategic framework• The timing of the implementation of the growth

strategy will be delayed as a result of revisions to volume forecasts

• The short term focus is on protecting volumes and preserving cash

10

-6.4%

-1.8%

0.2%

5.0%

GDP (%) 2008/09

08/09 CP = 4%

Baltic Dry Bulk Index $000/Tonne

3.63.52.82.5

Week 9

11.5

Week 8

11.5

Week 11

11.6

Week 10

11.4

GFB Volumes (mt)

Containers (000TEUs)

Q4Q3Q2Q1

19.921.121.8

15.919.1

22.3

Q3Q2 Q4

-9% -20%

899935974

770

972986

Q4Q3Q2

+4%-14%

2008/09Budget2009/10

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

11

GROWTH STRATEGY: THE NEXT HORIZON OF THE TRANSFORMATION PROCESS

Individual programme focus:

• Getting the basics right

• Stabilising operations

Interactions:

• Leveraging benefits of an intermodal business

• Effective commercial management of the network business

• Operational and functional teams jointly optimise their interaction areas

Integration:

• Accelerated rollout of operational improvements

• Integrated business model

– End-to-end corridor view

– Integrated customer view

• Achieve world class performance

Stabilise

Optimise

Grow

2010

Three turnaround horizons

2005Four-point turnaround strategy Four-point growth strategy

1

4 3

2Reengi-neering – integration, productivity and efficiency

Capital optimisa-tion and financial manage-ment

Safety, risk and effective governance

Human capital execution

Growth through :Corporate governance and risk

Redirect and re-engineer

Balance sheet restructuring

Human capital development

2007/2008

Transformation horizon

Positioning the Company for growth in the future12

• Focusing on 5 key corridors, providing end-to-end logistics services to customers

• Focus on key commodities

• Productivity and efficiency improvements

Client orientated planning and execution through integrated commercial management

• Financial strength and sustainability

• Enterprise wide performance management linked to benchmarked operating KPIs

• Risk and safety management

• Transnet culture charter

Governance and performance management

• Replacement and expansion of existing infrastructure to support growth

• Integrated investments of R80bn across rail, ports and pipelines

• Maintenance of core asset base

• Disposal of non-core properties (e.g. hostels/houses)

Investment plans

Re-engineering, integration, productivity and efficiency

Capital optimisation and financial management

Safety, risk and effective governance

Human capital execution

Growth through

TRANSNET’S GROWTH STRATEGY

13

GOVERNANCE – MEDIA REPORTS

14

• Article attempted to conflate two different issues both apparently the subject of leaks from employees with their own agendas

• Succession • Totally incorrect and without foundation• Capital Projects Report has neither served at Board or provoked discussion at

prior Board meetings therefore has of course no bearing on succession discussion

• Acting CEO, Chris Wells informed Board in January 2009 that he was not available to be appointed as CEO. This also is in Public Domain.

• Board united on process.

• Capital Project Internal Audit Report• Alleged evidence of financial mismanagement• Transnet Internal Audit outsourced to Ernst & young• Strong control environment in line with best international practice• Audit report in question was the result of a normal audit and evidence of

proactive and very thorough governance processes• Senior Ernst & Young partner responsible issued press release saying that

issues are “not material” and are part of normal process. • Normal forensics in place to find source of leaks as this was a breach of

Transnet’s ethics and employment contract and sought to bring harm to Transnet

• Other• Transnet has an independent tip-offs line for any anonymous reports of

alleged corruption or malpractice.

Benefits of corridor approach

• Transnet as a network business needs to operate in an integrated manner throughout the logistics corridor

• Provide a common transformation and long-term planning backbone

• Maximise growth opportunities across all operating divisions (rail, port, pipeline)

• Capture operational and functional synergies across operating divisions through integrated solutions

• Improve efficiency and effectiveness of logistics supply chain

• Providing an end-to-end logistics service to customers

• Provide optimal capital base for network infrastructure evolution

• Focus on key commodities and aligning capital investment to high-growth potential corridors

Functions

NOC

Projects

Maintenance

Yards

Procurement

Network

Touwsrivier

Mid Ilovo

Plaston

Kelso

Eshowe

Utrecht

Hawerklip

Naboomspruit

Middelwit

Vierfontein

Sishen

Saldanha

Cape Town

East London

Port Elizabeth

Mosselbaai

Bredasdorp

ProtemStrandSimonstad

StellenboschFranschhoek

Bitterfontein

Porterville

Atlantis

Prins Alfred Hamlet

Riversdale

Knysna

Calitzdorp

George

Ladysmith

AvontuurPatensie

Klipplaat

Oudtshoorn

Rosmead

Kirkwood

AlexandriaPort Alfred

CookhouseSomerset East

Noupoort

De Aar

Prieska

Upington

Kakamas

Naroegas

Worcester

Sakrivier

CalviniaHutchinson

Kootjieskolk

Beaufort West

Belmont

Douglas

Hotazel

Warrenton

Pudimoe Makwassie

Mafikeng

Ottosdal

Vermaas

Schweizer-RenekeKlerksdorp

Orkney

Coligny

Bultfontein

Whites

Westleigh

Bloemfontein

Aliwal North

Sannaspos

Dreunberg

Springfontein

Koffiefontein

HofmeyerSchoombee

JamestownBarkley East

Maclear

Tarkastad QamataQueenstown

Blaney

Bethulie

Seymour

Umtata

FortBeaufort

Amabele

Maseru

Marquard

Ladybrand

Bethlehem

Wolwehoek

Lichtenburg

Warden

Harrismith

Bergville

Kokstad

Matatiele

HardingPort Shepstone

Durban

Kranskop

RichmondUnderberg

Stanger

NkwaliniRichards Bay

VryheidHlobane

Moorleigh

Ladysmith

Roossenekal

SteelpoortGraskop

MachadodorpBelfast

Lothair

Komatipoort

Baberton

Phalaborwa

Messina

Louis Trichardt

Soekmekaar

ZebedielaVaalwater

Nylstroom

J’burg

Pretoria

O/fontein

Ellisras

Northam

CharlestownVrede

Potchestroom

Empangeni

Donnybrook

Greytown

Franklin

Kimberley

Marble Hall

Standerton

BethalB/plaas

Simuma

Mandonela

Winburg

Theunisen

ChroomvalleiDrummondlea

VirginiaGlen H

HiltonCopperton

Cullinan

Rayton

Uitenhage

Klawer

Thabazimbi

Pietersburg

Beit Bridge

Howick

Nakop

Postmasburg

ErtsManganore

Palingpan

Rustenburg

Hoedspruit

Glencoe

Newcastle

Arlington

Witbank

Ogies

Breyten

Krugersdorp

WelverdiendSentrarand

Welgedag

Kroonstad

Golela

Ancona

Sentrarand

DCT

PortNewcastle

Durban

Yard

Depot

Danskraal

Kaserne

Corridors

Ex

am

ple

STRATEGY IMPLEMENTATION THROUGH CORRIDOR APPROACH

15

Growth Strategy

Key Focus Areas

Financial Value Creation

KEY OPERATIONAL AND FINANCIAL STRATEGIC INITIATIVES

Revenue optimisation-

Deliver on committed volumes for export coal and

iron ore Domestic coal Containers on rail

Targeted cost reduction including introducing shared

services & procurement

review

Improve key productivities and

operational efficiencies

Implement funding plan at cost effective

rates

Optimise Capex on value creating

growth and sustainability

R80,5 billion Capex spend over five years on key

corridors

Target coal (74mt) and iron ore (60mt)

volumes by 2013/14

Maintain operating cost increases below revenue

increases over the 5 year plan

Drive KPI’s to benchmark levels

Proactive cash management

Gearing to remain <47% and cash interest cover >3 times over

5 year plan

Growth throughReengineering integration, productivity and efficiency

Reengineering integration, productivity and efficiency

Capital optimi-sation and financial management

Capital optimi-sation and financial management

Safety, risk and effective governance

Safety, risk and effective governance

Human capital executionHuman capital execution

16

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

17

REGULATORY ENVIRONMENT

The following Acts impact on the operations of the business

• National Port Act (2005) – Transnet National Ports Authority responsible for

ensuring safety efficient and effective functioning of the ports. Setting of

tariffs.

Ports regulatory body appointed

• Petroleum Pipelines Act (2003) – to licence petroleum pipelines and storage

facilities and to set tariffs

Nersa as regulated body

Port directives/regulations not finalised as yet which makes it difficult to manage

and plan future revenues

Pipeline regulations /directives issued but principles inconsistently applied

between years

• Significant uncertainty on future revenues do not allow for alternative funding

options

• No policy on funding for capital work in progress

Regulation in its current form and application is not conducive for investment

in major infrastructure projects.

CONTENT OF THE PRESENTATION

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

• Introduction

• Overview – Achievements

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities

2009/10

19

SALIENT FEATURES: TRANSNET CORPORATE PLAN 2009/10(as submitted to Shareholder)

Economic recession put Transnet volumes under pressure (-4.7%

average growth against 2008/09) and lower volumes specifically in:

General Freight

Containers

Export volumes (excluding iron ore and coal)

Revenue growth 8.8% y-o-y

Cost containment to keep cost increases to 8.4%, notwithstanding

sharp increases in input costs such as electricity, fuel and other input

costs.

Profitability (EBITDA) of the Group increases by 9.6% y-o-y

The 5 year capital investment program remains on a R80bn level and

approximately R21bn to be invested in 2009/10

Cash from operations will remain a healthy R10.6bn in 2009/10

Gearing and cash interest cover remain within set limits over the 5

years

20

KEY COMMODITY VOLUMES AND TARIFF INCREASES: 5 YEAR PLAN

Containers(000 TEUs)

ExportIron Ore

(mtpa)

ExportCoal

(mtpa)

GFB(mtpa)

11/12

4,059

10/11

3,666

09/10

3,315

08/09

3,710

47.644.443.0

36.8

11/12

10/11

09/10

08/09

72.071.069.061.9

08/09

11/12

10/11

09/10

76.271.6

68.0

78.4

11/12

10/11

09/10

08/09

Commodity Volumes Average Tariff increases

09/10-13/14

5.9%

09/10-13/14

7.4%

09/10-13/14

9.7%

Avera

ge

09/10-13/14

6.3%

• Average tariff increase impacted by underlying product mix (Containers & GFB)

• Including negotiated contract tariffs (export coal and iron ore) to:

• Increase infrastructure capacity to meet customer demand, and

• Service requirements of clients

• Average tariff increase impacted by underlying product mix (Containers & GFB)

• Including negotiated contract tariffs (export coal and iron ore) to:

• Increase infrastructure capacity to meet customer demand, and

• Service requirements of clients

All numbers reflected as per Corporate Plan

21

Avera

ge

Avera

ge

Avera

ge

INCOME STATEMENT – CORPORATE PLAN 2009/10

Critical to maintain profitability to be able

to fund major component of capex

plans through internal funding sources

All numbers as per Corporate Plan

22

33 615

(21 569)

12 046

(5 329)

6 717

Budget

2 682

(2 477)

205

(921)

(716)

8.0

(11.5)

1.7

(17.3)

(10.7)

13/14

20,8

12/13

19,7

11/12

17,1

10/11

15,0

09/10

16,5

Operating Profit Margin (%)

EXTERNAL REVENUE CONTRIBUTION BY DIVISION – 5 YEAR VIEW

18%

TPT 14%

TPL

6%TRE

8%

TNPA

TFR53%

1%

Specialist Units

All numbers as per Corporate Plan

23

Budget

33.6

OPERATING COST CONTRIBUTION – 5 YEAR VIEW

• Labour cost increase over 5 year period on average 6% (reduction in numbers 3%)• Electricity cost increases by 158% from 2008/09 to 2013/14

8%

30%

Electricity6%

Fuel

Personnel56%

Materials &

Other

All numbers as per Corporate Plan

24

Budget

21.6

BALANCE SHEET

50

13/14

39,3

12/13

44,6

11/12

46,8

10/11

46,4

09/10

43,1

Gearing (%)Must maintain headroom to be

able to withstand unforeseen economic

circumstances

All numbers as per Corporate Plan

25

Budget

109 421

8 454

54 216

12 661

41 555

41 98813 217

109 421

100 967

CASH FLOW : CORPORATE PLAN 2009/10

Estimate Budget2008/09 2009/10 2010/11 2011/12 2012/13 2013/14R million R million R million R million R million R million

Cash flow from operating activities 7 747 10 557 11 577 13 156 14 440 16 840

Cash flow from investing activities (19 451) (23 438) (21 137) (18 765) (14 140) (10 151)

Capital expenditure (19 373) (21 913) (19 442) (16 337) (13 330) (9 480)Capitalised borrowing costs ( 682) (1 849) (1 854) (2 213) ( 663) ( 488)Other investing activities 604 324 158 ( 215) ( 147) ( 183)

Net cash surplus / (shortfall) (11 704) *(12 880) (9 560) (5 609) 300 6 689

Projections

* Excluding the redemption of current loans

Cash Interest Cover (times)

11/12

12/13

4,4

13/14

3,63,5

3,1

10/11

3,3

09/10

3,6

Critical ratio for investors to

ensure sufficient cash to service and repay loans

All numbers as per Corporate Plan

26

SALIENT FEATURES OF FIVE YEAR CAPITAL INVESTMENT PLAN

The 5 year capital investment plan approved in the 2008/09 Corporate Plan amounts

to R80.5bn

Latest approved 5-Year Investment Plan amounts to R80.5bn.

• Projects in plan have been reviewed and re-prioritised as well as rescheduling of

cash flows over 5 years to

- Remain within the financial parameters

- Ensuring that revised customer demands are still met

- Capacity is created on time to meet future volume demands

Of the planned Capital Investment of R80.5bn spending will be as follows:

• 32% in rolling stock (R25.8bn)

• 59% in Infrastructure related projects (R47.5bn)

• 9% in Acquisition of machinery & equipment and floating craft (R7.2bn)

The capital expenditure over the next three years of R57.7bn will be funded by

borrowings of R28.4bn and cash from operations of R29.3bn.

27

TRANSNET 5 YEAR CAPITAL HISTORICAL SPEND AND INVESTMENT PLAN

11.7

15.8

19.4

21.9

19.4

16.3

13.3

9.5

46.9

80.5

2006/07 5 yr plan2009/10 2010/11Cumulative 3 yr Actual

2011/122007/08 2013/142008/09 2012/13

R billion Average investment per annum 2000/01 – 2004/05

Invested cumulatively the last 4 years more than the previous 15 years

28

CAPITAL INVESTMENT: 5-YEAR PLAN R80.5bn

9,071

12,841

21,912

09/10

8,121

11,321

19,442

10/11

7,180

9,156

16,336

11/12

9,439

3,892

13,331

12/13

7,718

1,762

9,480

13/14

Annual Capex (Rbn)Annual Capex (Rbn) Sustaining vs Expansion (3 year view)

Sustaining vs Expansion (3 year view)

58%

42%

Capital spending will be closely monitored during year to ensure that financial metrics

are maintained

Sustaining

Expansion

54%TFR

R43.5bn

3%TRE

R2.1bn

20%TNPA

R16.3bn

8%

TPT

R6.3bn14%

TPL

R11.1bn

1%

Other

R1.2bn

Capex per DivisionCapex per Division

CAPITAL INVESTMENT: PLANNED SPENDING PER CORRIDOR

Capex spread over the Country

All numbers as per Corporate Plan

30

MAJOR EXISTING PROJECTTNPA: DURBAN HARBOUR ENTRANCE CHANNEL WIDENING

Investment Criteria

Cost Time Quality Local Content

Safety Risk

OverviewThe Durban Harbour Entrance Channel Widening and Deepening project is essential in enabling the Port of Durban to accommodate larger vessels through its entrance and to improve the safety of navigation. The widening of the entrance to 330m will enable the super post panamax container vessels to enter the port without any constraining factors.

Current StatusExcavation of the North revetment continues and is progressing well. Armouring of the new north grove and the south breakwater is making good progress. Design of the sand bypass system at A-berth is nearing completion while commissioning of the temporary bypass system is scheduled for June 2009. The project has reached a 60% stage of completion.

Spending (Rm)

Latest Estimated Total Cost (ETC)

2008/09 Spending

Spending since inception Actual

3 756 1 942 1 176

31

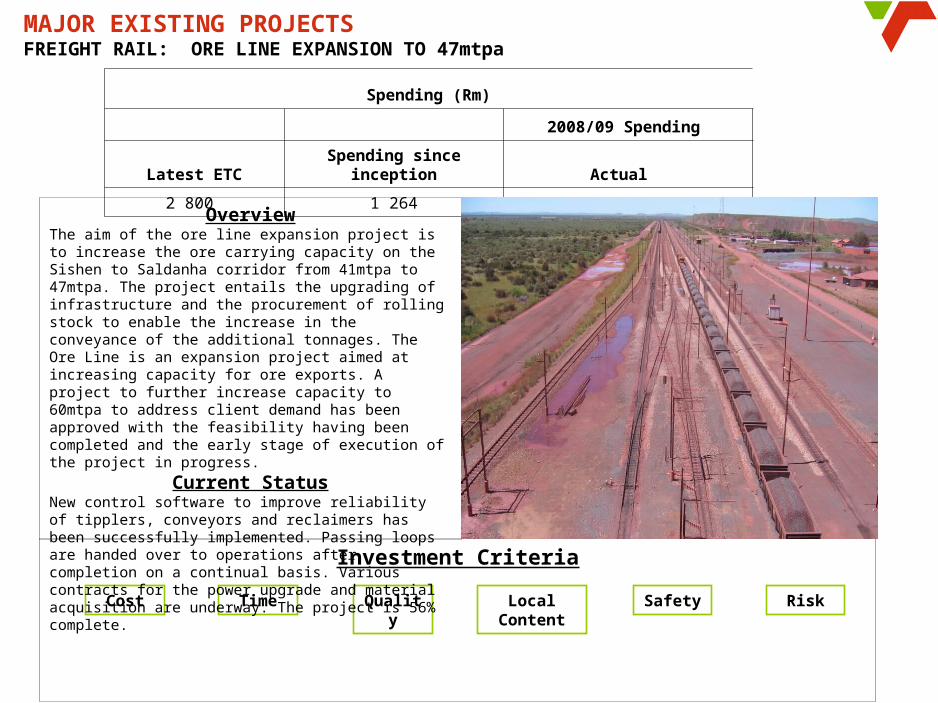

MAJOR EXISTING PROJECTSFREIGHT RAIL: ORE LINE EXPANSION TO 47mtpa

Investment Criteria

Cost Time Quality Local Content

Safety Risk

OverviewThe aim of the ore line expansion project is to increase the ore carrying capacity on the Sishen to Saldanha corridor from 41mtpa to 47mtpa. The project entails the upgrading of infrastructure and the procurement of rolling stock to enable the increase in the conveyance of the additional tonnages. The Ore Line is an expansion project aimed at increasing capacity for ore exports. A project to further increase capacity to 60mtpa to address client demand has been approved with the feasibility having been completed and the early stage of execution of the project in progress.

Current StatusNew control software to improve reliability of tipplers, conveyors and reclaimers has been successfully implemented. Passing loops are handed over to operations after completion on a continual basis. Various contracts for the power upgrade and material acquisition are underway. The project is 56% complete.

Spending (Rm)

2008/09 Spending

Latest ETC Spending since inception Actual

2 800 1 264 516

32

Investment Criteria

Cost Time Quality Local Content

Safety Risk

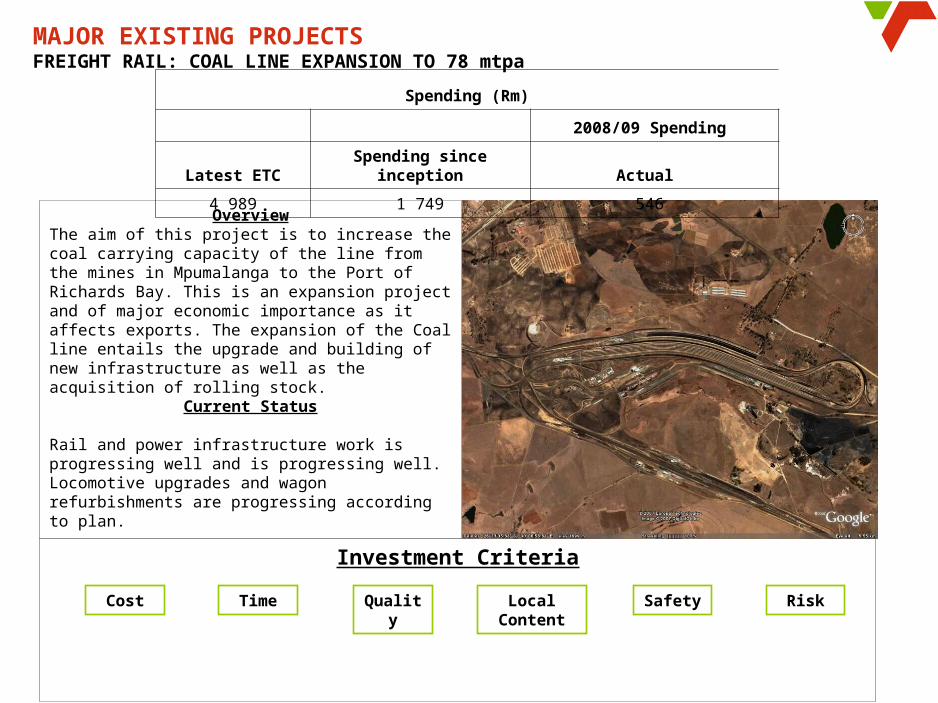

OverviewThe aim of this project is to increase the coal carrying capacity of the line from the mines in Mpumalanga to the Port of Richards Bay. This is an expansion project and of major economic importance as it affects exports. The expansion of the Coal line entails the upgrade and building of new infrastructure as well as the acquisition of rolling stock.

Current Status

Rail and power infrastructure work is progressing well and is progressing well. Locomotive upgrades and wagon refurbishments are progressing according to plan.

Spending (Rm)

2008/09 Spending

Latest ETC Spending since inception Actual

4 989 1 749 546

MAJOR EXISTING PROJECTSFREIGHT RAIL: COAL LINE EXPANSION TO 78 mtpa

33

Investment Criteria

Cost Time Quality Local Content

Safety Risk

OverviewNgqura Container Terminal is a Greenfield project with the objective of providing a full service container terminal together with rail links to the port. The scope is to develop a 4 berth container terminal and further extending the port infrastructure for a small craft basin, tugs, buildings and other landside infrastructure for the functioning of a container terminal. The project will provide 700 000 TEUs/a capacity when complete.

Current Status30 hectares of paving have been completed behind the first 2 berths while work on the trailer park and admin buildings is progressing well. The terminal handled its first two vessels in September 2008. Transformers for Eskom and cargo handling equipment for Port Terminals were offloaded from these vessels.

Spending (Rm)

2008/09 Spending

Latest ETC Spending since inception Actual

4 142 1 372 1 009

MAJOR EXISTING PROJECTSTNPA: NGQURA CONTAINER TERMINAL

34

Investment Criteria

Cost Time Quality Local Content

Safety Risk

OverviewThe aim of this project is to build a 550 km new trunk line from Durban to Jameson Park (Gauteng), 24 inch in diameter, addressing the increased demand for fuel in Gauteng and surrounding areas. The trunk line will connect an inland and coastal terminal with significant storage capacity. The existing pipeline is 40 years old and needs replacing. With the front-end engineering design phase completed, Transnet was granted licence to construct the NMPP by NERSA. It also entails the replacement of two northern network pipelines that have outlived their sustainable life. Given the energy problem facing South Africa, the Board has granted unconditional approval to commence construction in February 2008. This project is considered a strategic project for the Company, and is of national importance. Current StatusIn May 2008 a R3.3 Billion contract was awarded to Spiecapag Group 5, a South African French Consortium for the construction of the NMPP. Favorable Environmental Approvals for the project scope has also been received. Manufacturing for the 16” pipe commenced in April 2008 and all 105 000 tons of steel for the main 24” pipe has arrived in South Africa. As at end March 2009, the first 6 out of a total of 170 km of 16” pipe had been laid in the Kendall/Waltloo area. It is expected that the last phase of this project will be completed at the end of 2011.

Spending (Rm)

2008/09 Spending

Latest ETC Spending since inception Actual

12 600 3 278 2 565

MAJOR EXISTING PROJECTSTPL: NEW MULTI-PRODUCT PIPELINE

0

INDIANINDIANOCEANOCEAN

DURBANDURBAN

HOWICK

LADYSMITHLADYSMITH

BETHLEHEM

VOLKSRUST

NEWCASTLEKROONSTAD

KLERKSDORP

POTCHEFSTROOM

WITBANK

WALTLOOWALTLOOPRETORIA WEST

SECUNDA

STANDERTON

ALRODEALRODE

COALBROOKSASOLBURG

SCHEEPERSNEK

MAHLABATINI

HILLCREST

TARLTON

LESOTHO

NATAL

FREE

STATE

GAUTENG

ø457,2

ø406,4ø323,8

QUAGGA

N

RUSTENBURG

MAGDALA

NORTH - WESTMPUMALANGA

KWAZULU /

AIRPORT

VRYHEID

RICHARDS BAY

PPT-0231-/L

( 18" )

( 16" )( 12" )

ø457,2(18")

ø406,4( 16" )

BHT

MEYERTON

MNGENI

VAN REENEN

DUZI

INGOGO

WILGE

LANGLAAGTELANGLAAGTE

FORT MISTAKE

EMPANGENI

VREDE

MOOIRIVER

“T”

1

6

10

2

NMPP System Configuration in 2010

JAMESON PARKJAMESON PARK

KENDAL

36

COMPETITIVE SUPPLIER DEVELOPMENT PROGRAMME (CSDP)• The aim of the Transnet Competitive Supplier Development Programme (CSDP) is to localise Transnet supply chain

to a reasonable level and to promote South Africa as an off-shore source of goods and services for Original Equipment Manufacturers (OEM’s).

• This will secure source of supply, provide industrialisation opportunities for national businesses and reduce lead times

• Initially, the programme is being piloted over three years with rolling stock and port equipment purchases as its focus. The following is the progress to date:

• The aim of the Transnet Competitive Supplier Development Programme (CSDP) is to localise Transnet supply chain to a reasonable level and to promote South Africa as an off-shore source of goods and services for Original Equipment Manufacturers (OEM’s).

• This will secure source of supply, provide industrialisation opportunities for national businesses and reduce lead times

• Initially, the programme is being piloted over three years with rolling stock and port equipment purchases as its focus. The following is the progress to date:

Company & Investment Programme

Kalmar - R350 million port equipment and maintenance

• Kalmar has a previous NIPP obligation. They are first building a Cargotec (port handling equipment and freight solutions) training school. Their initial obligation for CSDP will be for free training hours and a discount rate per R10 million purchased

• Working with Kalmar on skills transfer to local organisations in respect of motor and engine maintenance

EMD - R800 million :5 year parts deal • EMD has already committed to the transfer of Intellectual Property to TRE in building a world class traction motor assembly line (EMD’s estimate of $15 million value)

EMD - R800m contract “50 Like New” Locomotives

• Local assembly and engineering done by TRE and with transfer of skills, TRE now able to do substantially more of the total Loco’s build.

Mitsui (VENUS /MARS) - Extension of the 19E contract - electric locomotive - by 35 vehicles – R600 million

• Original contract has NIPP obligations – Significant portion of assembly & engineering done locally.

• Mitsui will build a training facility to satisfy their NIPP obligations. We have also negotiated free training for TRE maintenance practitioners

Current 100 Locomotive tender (first time CSDP was used in a tender) -

• Both companies are proposing approximately a R1 billion investment over several years

• Adjudication process currently underway. Locomotive steering Committee set up to ensure adequate governance

5-YEAR FUNDING REQUIREMENT PER 2009/10 CORPORATE PLAN

* Excluding the redemption of current loans

More than 50% of the funding requirements for the 2009/10 financial year has already been raised to date on the strength of Transnet’s

balance sheet.

All numbers reflected as per Corporate Plan

37

Budget Projections

2009/10R million

2010/11R million

2011/12R million

2012/13R million

2013/14R million

Cash flow from operating activities 10 572 11 696 13 169 14 474 16 941

Cash flow from investing activities (23 438) (21 137) (18 765) (14 140) (10 151)

Capital investment (21 912) (19 442) (16 336) (13 331) (9 480)

Capitalised borrowing cost (1 850) (1 854) (2 212) (663) (489)

Other investing activities 324 159 (217) (146) (182)

Net cash surplus / (shortfall)* (12 866) (9 441) (5 596) 334 6 790

TRANSNET FUNDING SOURCES TO TAP INTO

The following funding sources have been initiated. The amounts are indicative & subject to market conditions

• Domestic bonds (TN17, TN23 and T27 Bonds)(±R6 bn)Currently tapping R1 bn per month and plan to launch at least 1 new bond & increase the size as liquidity increases

• ECA Supported Funding (R2 bn)1st transaction with Finvera to be concluded by early April 2009.

• Development Finance Institutions (R4bn) – JBIC loan agreement signed 26 March –first drawdown mid April 2009 approximately R2 bn and balance (R2bn) in

line with project payment dates– AfDB at due diligence stage expected to conclude end May 2009

• Domestic Loans (R7 bn)Rand Bilateral loans from banks(8) and other financial institutions(2)

• International Bond (±R5 bn)Close to concluding documentation & update with year-end financials, if not implemented will replace with domestic bonds

• Other International InitiativesAFLAC Loan (±R1.5 bn) – legal documentation finalized - still negotiating pricing levels

• Commercial Paper Bi-weekly issues of CP varying between R500m and R750m – plan to replace maturities with bonds.

• Pipeline FinancingConsidering a ring-fenced financing structure to align with regulatory environment.

Transnet has committed banking facilities in excess of R4 billion that can be utilised when required

CONTENT OF THE PRESENTATION

• Introduction

• Overview – 2008/09 Preliminary Results

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Strategic Priorities 2009/10

• Conclusion

• Introduction

• Overview – 2008/09 Preliminary Results

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Strategic Priorities 2009/10

• Conclusion

39

E

D

C

B

A

7 6 5 4 3 2 1

3

1

26

587

49

Consequence Rating

Lik

elih

ood

Rati

ng

Revenue/Volume Growth

Non compliance with Safety and Standard Operating Procedures (SOPs)

Economic Regulation (Ports Regulator and National Energy Regulator of South Africa)

Funding/Liquidity Risk

Delivery of capital projects on time and within budgets and affordability thereof

Asset Performance and Maintenance Regime

Human Resources Capability to deliver on growth strategy

Environmental Risks

Input costs including: Energy (electricity), Fuel, Steel, Pricing & Supply

Commodity & Concentration Risks (Third Party Supplier Risks)

GROUP’S KEY RISKS(as at May 2009)

Strategic residual risks heat map

10

Priority I risk – Transnet Group CE and Board levelPriority II risk - Operating Divisions’ CEOs LevelPriority III risk -General Managers’ levelPriority IV risk – Managers’ levelPriority V risk –Employees’ level

3

1

2

6

5

8

7

4

9

10

Mitigating plans are in place to manage the key risks

Mitigating plans are in place to manage the key risks

40

IMPLEMENTED A DYNAMIC MANAGEMENT FRAMEWORK WITHIN EPM OPERATING MODEL

Performance interactions

Performance Assessmentand Rewards

Strategyand

Targets

Track andmonitoring

Creating RealisticBudgets

and plans

EPM

Dynamic Management Framework to actively assess performance and plan/reallocate resources to achieve goals

Weekly Activity Reporting

Monthly Performance Assessment

Quarterly Performance Assessment

Focus on weekly trends volume trends, year end

estimates and impact analysis on Group Revenue

Monthly assessment of performance, success of cost cutting and capex initiatives

and updated year end estimates

Quarterly workshop (Ext. Exco) on year-to-date results,

year-end estimates and effectiveness of initiatives

Dynamic Process

Where we are?(measurement)Where we are?(measurement)

Where we planned to be?

(evaluation)

Where we planned to be?

(evaluation)

Corrective measures(action)

Corrective measures(action)

41

80%

90%

95%

100%

105%

Corporate Plan

2009/10EXECUTIVE SUMMARYWEEKLY ACTIVITY REPORTINGWeek 11 Results – Key Commodities

1,41

GFB (mt)

1,354,1% 66,644

Containers

(TPT)

61,102+9%

1,24

Export Coal

(mt)

1,37-9,5%

0.69

Export Iron Ore

(mt)

0.83 -17%

June 2009 Estimate

5.95

GFB

(mt)

5.897.39

1.0%

Analysis of Volume and Revenue Variance - Year end Estimate (2009/10)

Current EstimateBudget

268

Containers

(000 TEUs)

271

251

-1,0%3.72

Export Iron Ore

(mt)

3.68

2.50

1.1%

Revenue contribution to Group

Comments

5,8

Export Coal

(mt)

6,15,1

-3,6%

BudgetActual

Previous year

• The Transnet weighted volume variance estimate for 2009/10 is negative 1.4% (estimated 2.5% negative for June 2009).

• Group revenue (all commodities) is estimated to be 4.7% below budget for the 2009/10 year, mainly due to limitation on petroleum tariff increases, container volumes and negative price mix, export coal volumes and other bulk commodities.

• The Group revenue variance for 2009/10 would only be 2.0% below budget if the impact of TPL’s tariff increases are excluded.

447

Liquid Bulk (TNPA)

872 -49%

109,400

Break Bulk (TPT)

166,613 -34%358,376

Other Bulk (TPT)

369,753 -3%

% V

olu

me

Var

ian

ce

% Revenue Variance

Size

-22%

-20%

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

-8% -6%-42% -4% -2%-10% 6%4%2%0%

Gas

Petroleum

Other Bulk

Liquid Bulk

Automotives

Containers

Iron Ore (TPT)

Coal (TNPA)

Iron Ore (TNPA)

Coal (TFR)

Iron Ore (TFR)

GFB

56.15 56.15 59.2 60.6

115.75 122.95133.5 129.15

8 9 10 11

Spot Price $/Tonne Coal

Spot Price $/Tonne Iron Ore

Baltic Dry Bulk Index $/Tonne

Current YearPrior Year

2544 2786 3494 3646

11,459 11,465 11440 11612

8 9 10 11

67 69 76.567.5

177.5 181.5 181.5 172.5

8 9 10 10

Global Bulk Indicators

TRANSNET STATUS

Level 1 Negative 2% revenue

variance, excluding TPL tariffs

Negative 4.7% revenue variance, including TPL tariffs

Extract of Week 11 Report

42

CONTENT OF THE PRESENTATION

• Introduction

• Overview – 2008/09 Preliminary Results

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities 2009/10

• Introduction

• Overview – 2008/09 Preliminary Results

• Changes in Economic Environment

• Transnet Strategy

• Regulatory Environment

• 2009/10 Corporate Plan

• Risks and Mitigating Plans

• Conclusion - Strategic Priorities 2009/10

43

CONCLUSION - 2009/10 STRATEGIC PRIORITIES • Increasing export iron ore volumes by 11.6% above the budget to contractual levels (47.9mt

compared to budget of 43mt);• Increasing current throughput in domestic coal to at least achieve the budgeted volumes of

21.5mt;• Containers on rail to increase by 10% above the current budget of 544 460 TEUs to 600 000

TEUs;• To maintain at least the current trends in magnetite and cement volumes which are on

average 70% and 20% in excess of budgets respectively.

Volume and revenue

opportunities

Volume and revenue

opportunities

• Whilst most divisions have made good progress on committing to cost savings initiatives, we have only managed to obtain plans to substantiate R1bn savings compared to the R1.4bn (level 1) required.

• It is essential that the cost structures must be reduced through efficiency improvement and elimination of non-revenue related costs.

• The Group minimum requirement remains R1.4bn reduction in costs and operating divisions will be measured monthly against these targets going forward.

Cost savings

Cost savings

• Focusing on the execution of the capex plans with optimal phasing• Committed to investing R80.5bn over the next 5 years

Capital optimisatio

n

Capital optimisatio

n

• We will drive to achieve “a world-class” (otherwise known as best-in-breed) operational performance in each key area of operations, in the near future. Accordingly, the KPI project will be driven hard this year with the focus on at least achieving the KPIs set out in the Corporate Plan

Operational efficienciesOperational efficiencies

44

• The objective is to reduce the number of incidents and the cost of losses by 33% from 2009/08 actual levels (approximately R200m reduction at Group level).

• Environmental compliance has been elevated as a key priority in Transnet and we agreed to perform the following at all main areas of operations:

• Review of maintenance and implementation of proper and structured maintenance programmes

• Getting housekeeping up to standard and comply with all environmental requirements• To start with a compliance review/audit to identify areas of

non-compliance/unsatisfactory standards

Safety and environmen

t

Safety and environmen

t

THANK YOU

END OF PRESENTATIONEND OF PRESENTATION

![Transnet Port Terminal, a division of · Transnet Port Terminal, a division of TRANSNET SOC LTD Registration Number 1990/000900/30 [Hereinafter referred to as Transnet] REQUEST FOR](https://img.pdfslide.us/doc/110x75/5f5e4faa6b0e6821912b906b/transnet-port-terminal-a-division-of-transnet-port-terminal-a-division-of-transnet.jpg)

![TRANSNET PORT TERMINALS Notices... · TRANSNET PORT TERMINALS An Operating Division of TRANSNET SOC LTD [Hereinafter referred to as Transnet] Registration Number 1990/000900/30 REQUEST](https://img.pdfslide.us/doc/110x75/600560c52af56b6cdb7b80d6/transnet-port-notices-transnet-port-terminals-an-operating-division-of-transnet.jpg)

![Transnet]...TRANSNET FRAIGHT RAIL, a division of TRANSNET SOC LTD Registration Number 1990/000900/30 [thereinafter referred to as Transnet] REQUEST FOR QUOTATION …](https://img.pdfslide.us/doc/110x75/6050751b455b0f3d741c0d14/transnet-transnet-fraight-rail-a-division-of-transnet-soc-ltd-registration.jpg)