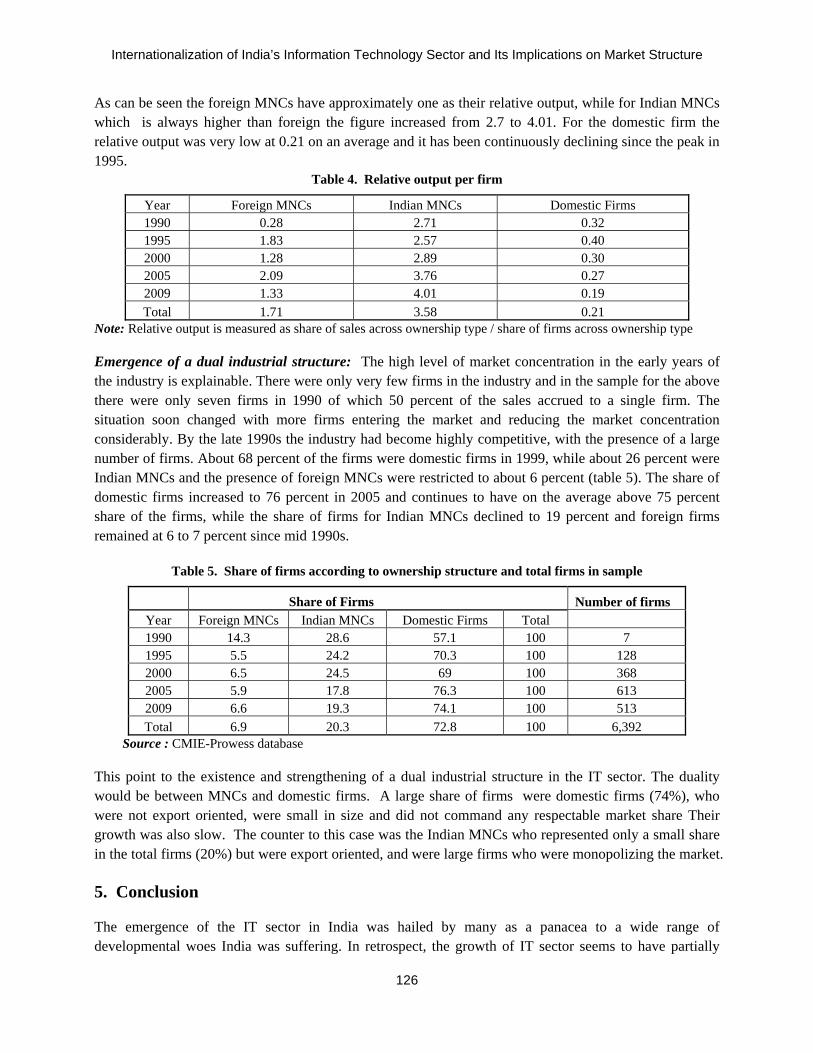

Embed Size (px)

Citation preview

Transnational Corporations Review:

• Published in English and Chinese

• Supported by international experts and partners

• Focuses on TNC, FDI, Innovation, and Development

• Provides opportunities to recent graduates and young professionals in the fields of policy and economics

It’s Easy to Ask for a Copy!

Just write to [email protected] and we will respond to you immediately

Visit the Website to Learn More!

To learn more about Transnational Corporations Review and relevant information, please visit the website at www.tnc-online.net

Ottawa International Students Entrepreneurship:

• Supported by the Ottawa United Learning Academy

• Managed by a group of senior students and professionals

• Assists students with their studies and career development

• Reduces the cost of education for international students

FOREIGN DIRECT INVESTMENT AND DEVELOPMENT IN INDIA

Guest Editor

Jaya Prakash Pradhan

Transnational Corporations Review

Ottawa United Learning Academy, Canada

June 2011

Transnational Corporations Review www.tnc-online.net [email protected] i-ii

i

Editorial Statement

Transnational Corporations Review (TNCR), published by the Ottawa United Learning Academy (OULA) and Denfar Transnational Development (Denfar), is a modern media journal dedicated to providing economic, policy, and business analysis of current issues related to transnational corporations (TNCs), foreign direct investment (FDI), institutional innovation, and international development. The journal puts emphasis on China's growing involvement in the global economy. FDI by TNCs is the most dominant and dynamic element of the world economy in terms of production value; TNCR fills the urgent need for a journal on the topic that is available in both English and Chinese. It is the only journal published in the West that addresses the topic from modern theoretical and practical including knowledge management perspectives. The journal particularly serves the needs of globally dispersed young professionals and senior graduate students majoring in Chinese business and international economics.

Special Advisors

Dr. Manfred Bienefeld, Carleton University, Canada Dr. Someshwar Rao, Industry Canada (Government of Canada)Dr. Anne Miroux, United Nations Conference on

Trade and Development (UNCTAD) Dr. Karl Sauvant, Vale Columbia Center on Sustainable

International Investment, Columbia University, USA Dr. Elinor Ostrom, Indiana University, USA Dr. Yongding Yu, Chinese Academy of Social Sciences, China Dr. Vincent Ostrom, Indiana University, USA Dr. Yanzhong Zhang, Aviation Industry Corporation of China

Editorial & Review Board

Dr. Connie Carter, School of Business, Royal Roads University, Canada Dr. Arthur Cheung, City University of Hong Kong Dr. Xinjian Cui, School of Business, Central University of Finance and Economics, China Dr. Michael Hansen, Copenhagen Business School, Denmark Dr. Manqing He, Research Center on Transnational Corporations, MOFCOM, P.R. China Dr. Hafiz Mirza, United Nations Conference on Trade and Development (UNCTAD), Geneva Dr. Val Samonis, The Web Professor of Global Management(SM), Lansbridge University, Canada Dr. Jianmin Tang, Productivity and Competitiveness Analysis Directorate, Industry Canada Dr. Theo Toonen, Delft University of Technology & Leiden University, The Netherlands Dr. Tim Wang, Chinese eBusiness Association of Canada (CeBA) Dr. Hong-Xing Wu, Public Health Agency of Canada (Government of Canada) Dr. Guomin Xian, Center for Transnationals’ Studies, Nankai University, China Dr. George Xue, School of Management, Fudan University, China Dr. Zhizhong Yao, Chinese Academy of Social Scienences, P.R. China Dr. Joe Zhao, School of Economics and Management, Northwest University, China

Development & Management

Hugh Dang, Managing Editor Denny Liao, Online Manager Someshwar Rao, Special Editor Karl Sauvant, Editor (Honorary)

Val Samonis, Special Editor (knowledge) Gloria Yuan, Communications Manager Helen Zhang, Consultant Editor Joe Zhao, Associate Editor (China)

Editorial Statement

ii

Copyright and Disclaimer

This journal retains copyright to all published documents in order to circulate as widely as possible the work of those authors selected for the publication. The opinions expressed in this publication are those of the authors and do not necessarily reflect the views of the publisher and relevant partners. While every effort has been made to ensure that the information is accurate, TNCR does not accept any liability for error of fact or opinion present.

Publisher’s Information

ISSN 1918-6444 (Print); 1925-2099 (Online)

Indexes ALJC, AMICUS, EBSCO, EconLit, SSCI/SCI (under review)

Production Printed on acid-free paper (required)

Printing Merriam Print Canada

Acknowledgements

For more information − Visit our Web sites:

www.tnc-online.net, www.tnc-online.org

− Contact us by mail: 58 Rideau Heights Dr. Ottawa, ON K2E 7A6 Canada

To submit an inquiry − Send us an e-mail at: [email protected]

To submit an article − Send us an e-mail at: [email protected]

To subscribe to TNCR (yearly)

− Print only: US$168; Electronic only: US$100 − Print and electronic: US$150

Transnational Corporations Review Volume 3, Number 2 June 2011 www.tnc-online.net [email protected]

TABLE OF CONTENTS

In This Issue ………………….…………….………………………………………….………….…….....I FDI in India

Non-Equity Operation of Multinational Enterprises in India: Focus on Outsourcing Jaya Prakash Pradhan…………………………………...………………………………...…..……….…..….1

DOI: 10.5148/tncr.2011.1110

Location of FDI in India: Some Less-Explored Aspects K.S. Chalapati Rao and M.R. Murthy…………………….…………………………....................................12

DOI: 10.5148/tncr.2011.1111

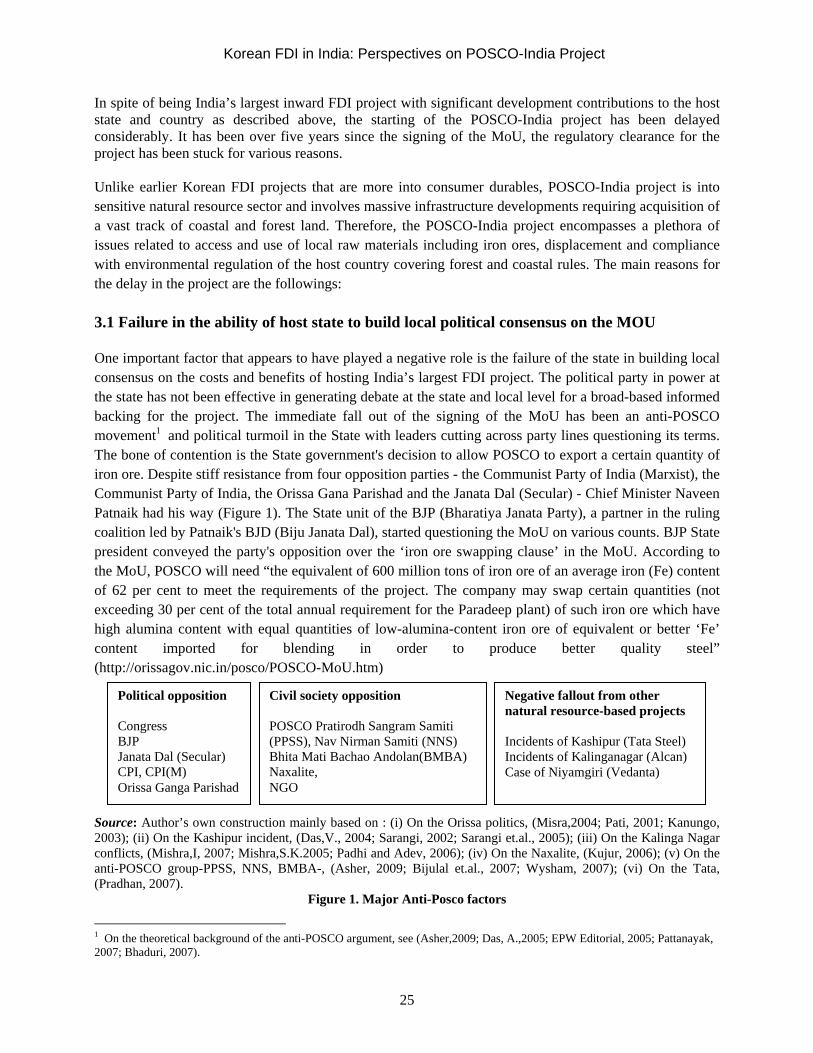

Korean FDI in India: Perspectives on POSCO-India ProjectJongsoo Park………………………………………………………………………..…….………………..……….22

DOI: 10.5148/tncr.2011.1112

FDI from India India’s Agriculture and Food Multinationals: a First Look

Premila Nazareth Satyanand……………………………………………………………………………..….31DOI: 10.5148/tncr.2011.1113

Technology Sourcing and Outward FDI: Comparison of Chemicals and Information Technology Industries in India

Savita Bhat and K. Narayanan………………………………………………………………………………50DOI: 10.5148/tncr.2011.1114

Outward FDI from India in the United StatesVinod K. Jain……………………………………………………………………….……………………..…...65

DOI: 10.5148/tncr.2011.1115

Economic Liberalisation and Financing Pattern of Indian Acquiring Firms Abroad P.L. Beena……………………………………………………………………………………………………..76

DOI: 10.5148/tncr.2011.1116

Issues in FDI and Internationalization Foreign Equity and Technological Capabilities: a Comparison of Joint-Venture and National Automotive Suppliers

Rajah Rasiah…………………………………………………………………………………………………..87DOI: 10.5148/tncr.2011.1117

Change of Subsidiary Mandates in Emerging Markets: the Case of Danish MNCs in India Michael W. Hansen, Bent Petersen and Peter Wad…………………………………………….……….104

DOI: 10.5148/tncr.2011.1118

Internationalization of India’s Information Technology Sector and its Implications on Market StructureVinoj Abraham…………………………………………….……………………………………………….....117

DOI: 10.5148/tncr.2011.1119

The Role of Networks in the Accelerated Internationalization of Indian FirmsSumati Varma…………………………………………….……………………………………………..…...128

DOI: 10.5148/tncr.2011.1120

Analysis of Cross-Border and Domestic M&A Deals in Technology Sector in India and China Arindam Das and Sheeba Kapil …………………………………………….…………………………..…...148

DOI: 10.5148/tncr.2011.1121 Book Review

How Human Psychology Drives the Economy and Why It Matters for Global Capitalism……..……......164 Call for Submissions Subscriptions

Transnational Corporations Review Volume 3, Number 2 June 2011 www.tnc-online.net, [email protected] I-VI

I

Guest Editorial

Foreign Direct Investment and Development in India

Jaya Prakash Pradhan

Central University of Karnataka & Sardar Patel Institute of Social and Economic Research

Abstract: This editorial introduction provides an overview of different issues and topics analyzed in the present TNCR special issue. Topics surrounding the rise of India as a host to FDI and a home for emerging Indian TNCs are discussed. The special issue makes a significant contribution to the current debate on internationalization of emerging economies like India. Keywords: Emerging economies, India, FDI, TNCs

JEL: O50, F23 1. Introduction The rise of relatively large emerging economies is leading to significant structural transformation of global industries, international institutions and global power arrangements (Pradhan and Lazaroiu, 2011). Accelerated internationalization involving foreign direct investment (FDI) is turning out to be an important medium of these economies’ expanding global influence. Being the sources of higher growth, they are the most sought after destination for global firms from developed countries looking for growth, opportunities and stability of performance. These emerging economies’ share in global FDI inflows has gone up sharply in the past decade with developing and transition economies receiving more than half of global FDI inflows in 2010 (UNCTAD, 2011). Besides, the growth of global firms based in emerging economies is making market competition ever more challenging across sectors and geographies. Outward FDI undertaken by emerging transnational corporations (TNCs) is growing faster as they are on a buying spree of assets and companies abroad. The share of developing and transition economies in global FDI outflows increased to 19 per cent in 2008 and further to 25 per cent in 2009 (UNCTAD, 2010). This changing importance of emerging economies as a host to and source of global FDI flows therefore raises important issues regarding the activities and role of established and emerging TNCs. Among relatively large emerging economies, India represents an interesting case of rapid growth and internationalization witnessed during the past two decades. It achieved the second highest real GDP growth (8.4 per cent) after China (10.1 per cent) during 2006−20101 and became the top ninth host to global FDI inflows in 2009 (UNCTAD, 2010). Although, India lagged behind China in terms of the scale of FDI inflows received (e.g. China received US$95 billion in 2009 as compared to US$34.6 billion of

1 This is among top 15 populated economies and based on the average growth rate obtained from the data on 'Real Historical Gross Domestic Product (GDP) and Growth Rates of GDP for Baseline Countries/Regions (in billions of 2005 dollars) 1969-2010’ available from www.ers.usda.gov.

Foreign Direct Investment and Development in India

II

India), the former outpaced the latter if the intensity of such investment is considered in relation to the gross fixed capital formation of the host country during 2005−2009 (this ratio is 5.9 per cent for China while it is 6.8 per cent for India). Clearly, India turns out to be an attractive emerging economy host for global TNCs seeking new sources of growth, efficiency and low-cost innovation. As the gravity of global growth shifts from developed to emerging markets, it appears that securing a successful presence in a growing emerging economy like India is a crucial strategy of TNCs to ensure their future growth. A stronger domestic demand, pursuance of a liberal policy regime for FDI and opening up of new domestic sectors to foreign operations in India since 1990s seem to have supported this intensifying involvement of global TNCs in India. The internationalization of Indian economy has also assumed even stronger sense with the transformation of a large number of Indian firms into TNCs. The outflows of FDI from India grew by a whopping 119 per cent on annual average during 2000−09 far exceeding that of China at 97 per cent. Similar to the case of inward FDI flows, India falls behind China substantially in terms of the scale of OFDI but outperform by OFDI intensity. In 2009 Chinese OFDI flows stood at US$48 billion as compared to US$15 billion of outflows from India. However, as a per cent of gross fixed capital formation such flows from China averaged 1.8 per cent during 2005−2008 which is nearly half of that relates to India (3.6 per cent). The emergence of Indian multinationals and their expanding profile in global markets through large sized acquisitions and green-field projects abroad may possess implications for a host country’s market structure, capital formation, productivity, technology, employment and trade performance. In the above context, understanding the role of global TNCs in India and Indian TNCs in global markets are clearly crucial issues worthy of analysis and learning. While there are voluminous studies about the Chinese experience, it is only fitting that the study of India should complement the literature on internationalization of emerging economies. The present special issue of the Transnational Corporations Review (TNCR) was imagined precisely to deals with the recent FDI experience of the emerging economy of India. The contributions in the special issue can be broadly grouped under three main headings: ‘FDI in India’, ‘FDI from India’ and ‘Issues in FDI and Internationalization’ each presenting state of the art knowledge, thoughts, assessments and research findings about the operation of TNCs in India and that of Indian TNCs. 2. FDI in India The first part of the special issue reviews some of the emerging subjects related to the operation of foreign firms in India. Special attention is given to the role of non-equity operation of TNCs, locational distribution of their investments, and challenges emanating for operationalizing natural resource-based FDI projects in India. TNC involvements in India is not just limited to equity modes like establishing joint ventures and wholly-owned subsidiaries recently but the same is assuming new forms of non-equity modes like outsourcing, strategic alliances and licensing. Pradhan’s essay is primarily concerned with the outsourcing as an important form of TNC operation in India. While India is well known as an attractiveness destination for outsourcing by global services TNCs, such outsourcing activities of global firms to India in manufacturing is less recognized. In addition to their captive sourcing of raw materials and inputs locally in India, a growing number of MNCs can be observed to have resorted to contract manufacturing from independent

Jaya Prakash Pradhan

III

suppliers in pharmaceuticals and automotive sectors. These emerging non-equity modes of TNC operations can have significant development implications for the host country. Rao and Murthy revisit the analysis of the location of FDI in India. They argue that existing studies on state-wise distribution of FDI in India are mostly based on aggregate flows data and could offer inadequate perspectives into the location choice of foreign firms. However, as the location of FDI is being deeply related to the specific characters of FDI projects such as modes of entry (greenfield vs. acquisitions; joint ventures vs. wholly-owned subsidiaries), nature of the foreign investor, sector of investment, etc. Incorporating these characteristics would yields more illuminating views of regional dimension of FDI distribution in India. Analysis of India shows that FDI inflows have been largely dominated by services and infrastructure projects, equity hikes by existing foreign firms, and takeover of existing companies/units and therefore, relating aggregate FDI flows with state level characteristics such as level of industrialisation, infrastructure development, growth trend, reform-orientation, corruption and quality of governance, is less appropriate. The paper by Park explores host country issues associated with the entry of natural resource-based FDI into India. His analysis of the experience of India’s biggest foreign direct investment (FDI) project, namely the proposed Posco integrated steel plant in Orissa, reveals a complex set of issues from regulatory clearances especially forest and environmental clearances and the socially and politically sensitive issue of land acquisition and displacement. This natural resource-based project has faced long drawn protests by local people against land acquisition and got entangled in environmental concerns and livelihood issues. The delay in the beginning of the project is a clear reflection on the failure of state and local administration in building local consensus about the benefits of it and in addressing effectively the compensation and livelihood issues of the local people being displaced. This would suggests that massive FDI in natural resource sector is required to be facilitated in an holistic environment of consensus building and assurance of new employment in the relocation zone for the displaced population. 3. FDI from India The second part of the special issue raises and discusses issues concerning the rise of Indian TNCs and their outward FDI (OFDI) activities. The study by Nazareth Satyanand provides preliminary account of Indian OFDI in the agriculture and food sector. India provides an interesting example of a rapidly internationalizing economy with a broad-based sectoral OFDI profile (Pradhan, 2011). However, when it comes to agriculture, the emergence of Indian TNCs is of more recent origin. With the consistently growing food prices and relaxation on restrictions on corporate involvement in agriculture during the last decade, a number of Indian firms turn translational. An upsurge of overseas acquisitions by Indian firms can be seen in beverages, tea, crop protection and floriculture. These acquisitions are driven by a multiplicity of firm-specific objectives like access to new technology, products, networks, raw materials, etc. Bhat and Narayanan focuses on the OFDI behaviour of Indian TNCs from chemicals and information technology (IT) sectors. Specifically they examined Indian TNCs investment in their existing affiliates abroad. Their analysis shows that Indian firms from both these sectors are more likely to undertake investment in their foreign affiliates if parent entities are engaged in in-house R&D. In the chemical industry, imports of capital goods and disembodied technologies also play a positive role. This would

Foreign Direct Investment and Development in India

IV

verify that acquisition of technology internally by firms or through external purchase may encourage their OFDI involvements. Firm’s spending on labour is found to be positively related to the OFDI probability and OFDI level of IT and chemical firms respectively. The United States has emerged as the third largest host to Indian OFDI flows during the period April 2000 to March 2009 (Pradhan, 2010). It attracted about US$6.2 billion of FDI accounting for 8.6 per cent of total FDI flows from India. In this context, Jain’s paper is a rich empirical account of the operation of Indian firms in the U.S. through greenfield investments and mergers and acquisitions (M&As). It presents a number of interesting characteristics of Indian FDI in the U.S. that are worth exploring further. Between greenfield investments and M&As, Indian TNCs are observed to prefer the latter while entering the U.S. market and even in M&As they tend to target high-technology, knowledge-intensive manufacturing industries and services, such as pharmaceuticals, automotive and IT. It appears that U.S. bound Indian FDI projects are motivated by the desire to acquire technology and brands and facilitated by the liberal U.S. business environment and opportunities to acquire valuable assets at low valuations. Are Indian acquisitions abroad simply a result of cash-rich Indian firms? Beena’s paper introduces the debate on whether recent foreign shopping of Indian firms is due to their internal resource base. The data presented in the paper pertaining to the period 1991–2009 shows that internal finances constitute about 40 per cent of total resource mobilization by Indian acquiring firms for their business operation. In comparison, the share of external finances reached 60 per cent. Borrowings and resources raised from capital markets played a key role in the financing patterns of these companies. The case studies of selected acquiring Indian TNCs further confirm that these firms have resorted to foreign borrowings and issues of Foreign Currency Convertible Bonds and Foreign Currency Exchangeable Bonds in order to acquire large sized foreign entities. 4. Issues in FDI and internationalization The third part of the special issue contains the remaining set of five papers each offering thoughtful analysis of emerging topics related to India’s experience with internationalization. The essay by Rasiah explores the contribution of joint ventures to the firm-level technological capability building in the rapidly evolving Indian automotive sector. This knowledge-based sector has been significantly liberalized since 1990s and restriction on foreign ownership has been removed. It is to be expected that enterprises with foreign ownership would go for higher local R&D activities given the large size of the host market, stiff competition, stringent quality and regulatory conditions and adequate supply of human capital. The findings on technological performance of a sample of firms from the greater Delhi region do seem to bode well for local innovation. Firm’s overall technological capabilities through human resource practices, process technology and R&D are found to be higher for joint-venture firms with over 10% foreign equity as compared to fully domestic owned firms. The superior performance of firms with foreign equity also hold true at the disaggregated level for human resources and process technology. The contribution by Hansen, Petersen and Wad analyzed the interesting issue of how subsidiary mandates changes with the shifting characteristics of a host emerging economy like India. Unlike the previous period, India has adopted a progressively outward-looking trade and investment regimes since 1990s and considerably liberalized its business environment. Rapid growth of Indian market, access to skilled labour, cost effective production, quality changes in local industry and growing capability of local suppliers have

Jaya Prakash Pradhan

V

positively affected the mandates of Danish subsidiaries in India. These subsidiaries have evolved being small assisting operations with relatively low standing in the global strategy of their parents in 2001, to be assigned with larger and more significant operations in 2008. The impression gathered in the survey suggests that Danish subsidiaries are preparing for increased activities related to after-sales services, R&D expansion and export mandate for regional markets. In his paper Abraham dealt with the changes in the competitive structure and composition of the Indian IT industry among three types of firms distinguished based on the perspective of internationalization. They are the Indian owned IT firms having overseas subsidiaries (Indian TNCs), those Indian firms without such affiliates (Indian domestic firms) and subsidiaries of foreign firms operating in the Indian IT sector (foreign TNCs). Statistics presented in the paper suggests that Indian TNCs, on an average, are larger than foreign TNCs and both these TNCs in turn are larger than domestic Indian IT firms. In addition, there is a secular decline in the share of both foreign TNCs and domestic firms in the industry sales since 2004. Domestic firms constituted about three-fourth of the total number of IT firms but were small in size, least export-oriented and claimed marginal market share. On the contrary, Indian TNCs represented only a small share in the total number of firms (20 per cent) but are export oriented and large sized entities that dominated the Indian IT industry. From this the author argues that there exists a dual industrial structure in the IT sector between Indian TNCs and domestic firms. To understand the internationalization of Indian firms, it is also important to explore the role of business networks that help firms to access critical resources and deal with environmental uncertainty. Varma devoted her attention to the theoretical underpinnings of networks affecting the rise of born global firms from India. Though her main hypotheses remained untested empirically, findings from another study tend to suggest that business ties are important for firm’s internationalization pattern. While dealing with the locational patterns of Indian overaseas M&As, business group (BG) affiliated Indian TNCs are found to be guided by a broader set of considerations than standalone Indian TNCs mainly due to BG’s derived resources and access to parental networks (Pradhan and Sing, 2011). Finally, the article by Das and Kapil delves into the characteristics of M&A transactions involving Indian and Chinese companies in the technology sector comprising of computer and electronic manufacturing, IT, telecommunication, media, and professional, scientific and technical services. Empirical results suggest that while outbound M&A deals from India and China are not significantly different, domestic and inbound deal types in these two countries are significantly different. It is found that in most cases Indian and Chinese TNCs opted for similar acquisition strategy, namely acquisition of controlling stake. 5. Concluding remarks In closing, it is our hope that this special issue of TNCR offers reader with new insights and perspectives for understanding the current and emerging trends in India’s FDI experience. The variety of issues discussed and analyzed for India may also be useful and relevant for other emerging economies.

Foreign Direct Investment and Development in India

VI

Reference Pradhan, J.P. (2010) ‘Emerging Multinationals from India and China: Origin, Impetus and Growth’ in H. Esho and P.

Xu (eds.) International Competitiveness, Globalization and Multinationalization of Firms: A Comparison of China and India, Institute of Comparative Economic Studies, Hosei University, Tokyo, Japan, pp. 95–135.

Pradhan, J.P. (2011) ‘Emerging Multinationals: A Comparison of Chinese and Indian Outward FDI’, International

Journal of Institutions and Economies, 3(1), pp.113–148. Available at http://ijie.um.edu.my/RePEc/umk/journl/v3i1/Fulltext6.pdf

Pradhan, J.P. and G. Lazaroiu (2011) ‘Rise of Emerging Economies: An Introduction’, Economics, Management,

and Financial Markets, 6(1), pp. 8–18. Pradhan, J.P. and N. Singh (2011) ‘Business Group Affiliation and Location of Indian Firms’ Foreign Acquisitions’,

Journal of International Commerce, Economics and Policy, 2(1), pp. 19–41. DOI: 10.1142/S1793993311000208, available at: http://www.worldscinet.com/jicep/02/0201/S1793993311000208.html

UNCTAD (2010), ‘World Investment Report 2010: Investing in a Low-Carbon Economy’, New York and Geneva:

United Nations. UNCTAD (2011), ‘Global and Regional FDI Trends in 2010’, UNCTAD Global Investment Trends Monitor 5, New

York and Geneva: United Nations. Acknowledgement I am highly thankful to Professor Hugh Deng for putting forward the idea of the TNCR special issue on India and kindly inviting me to be its special editor. The present shape of the special issue largely owes to his unstinting support and constant pursuance. I am also indebted to my distinguished colleagues―Vinoj Abraham, Aradhna Aggarwal, Amita Shah, P.L Beena, Nandita Dasgupta, Ranjan Kumar Dash, Elumalai Kannan, Santosh Kumar, Premila Nazareth Satyanand, S. Puttaswamaiah, Subhas Sasidharan, Sumati Varma, and Mohammad Zohair for accepting the role of anonymous referee and helping this special issue achieve the present scholarly standards.

Transnational Corporations Review Volume 3, Number 2 June 2011 www.tnc-online.net, [email protected], DOI:10.5148/tncr.2011.1110 1-11

1

Non-equity Operation of Multinational Enterprises in India Focus on Outsourcing

Jaya Prakash Pradhan1

Abstract: The development policy literature on multinational enterprises (MNEs) is yet to adequately analyze the emerging cross-border activities of MNEs through emerging modes of non-equity operation like international outsourcing. As a result of accelerating globalization process and growing trend of vertical disintegration of value-chains, MNEs and their foreign affiliates are increasingly sourcing raw materials, intermediates, parts and services from independent suppliers based in emerging and developing economies like India. It is, therefore, necessary that host countries like India should appreciate this non-equity operation of MNEs and formulate suitable policies for enhancing their development impacts. Keywords: MNEs, foreign affiliates, non-equity modes, outsourcing, India JEL classification: F23, L24, N65 1. Introduction Multinational enterprises (MNEs) are key players in the growth of global business and their role has only increased during the last two decades of globalization. They dominate the world markets by a network of affiliates located across different countries with inter-affiliates flows of investment, trade and technology and their non-affiliate business transactions. The growing trends of international outsourcing and offshoring in the global value chain of goods and services are clearly changing the operative functions of MNEs in the global business. MNEs involvements in a host country is assuming a complex combination of equity modes like establishing wholly-owned subsidiaries and joint ventures and various non-equity modes like international subcontracting, licensing, franchising, management contracts, etc. (UNCTAD, 2010). MNEs are outsourcing their business functions over the value chain hitherto done in-house to companies based overseas. In addition to the captive offshoring, such activities are increasingly being rendered by external suppliers in the host economy. It is not just the parent MNEs that are relying on overseas outsourcing but their affiliates operating in the host country are likely to depend on purchasing of local intermediate and raw materials for their operation. That means that the parent MNE and its network of foreign affiliates are adopting the tool of strategic outsourcing to reduce cost, improve quality and competitiveness. Their choice of outsourcing can be at any level like low-skilled labuor-intensive tasks, manufacturing of a product or a component, R&D and logistics depending upon the business environment and comparative advantages of a host country and capabilities of host local firms.

1 Acknowledgement: This paper has been prepared for the UNCTAD Expert Meeting on World Investment Report 2011, Geneva, February 15, 2011.

Non-equity Operation of Multinational Enterprises in India Focus on Outsourcing

2

In addition, MNEs are entering into strategic alliances with local companies for joint R&D or product development and marketing arrangements. Sometime they are sourcing technologies for niche products from local firms in a host country. For a host country promoting or facilitating such non-equity operation of MNEs can be critical for improving technological efforts of local firms and exports in the global value chain. Therefore issues of what determine MNEs outsourcing and other non-equity operation to a host country at macro, sectoral and firm-level is a critical policy issue. In this brief note, we document outsourcing to India by global MNEs for selected industries and explore on the key determinants of such process. Due to paucity of information at the economy level, we will also supplement the analysis by presenting data on the sourcing of local raw materials and intermediates by foreign affiliates operating in India. 2. Outsourcing and MNE: a theoretical view As outsourcing shifts outside some activities internal to the firm, it can be seen as a process of redrawing the boundary of it (Coombs and Battaglia, 1998). In the transaction cost theory, the boundary of a firm gets larger if the transaction costs of using markets for its activities are greater than the costs of performing in-house, reflecting greater levels of uncertainty, frequency and asset specificity (Williamson, 1985; Holmstrom and Roberts, 1998). Within the firm production by integration is more optimal in this situation and the firm will bypass the market. However, firms’ make or buy decision are not independent of the dynamics of the evolution of industries or value chain structures. The emergence of specialist departments representing different parts of the value chain within a single organization (i.e. intraorganizational boundaries) and the associated learning process ultimately pave the use of a market (Jacobides, 2005). According to Jacobides, the simplification and minimization of the coordination between the adjoining stages along a value chain and standardization of information and ease of their transfer finally led to the creation and growth of intermediate markets. Vertically specialized firms are driving the disintegrated industry structure with significant value creation in the form of gains from specialization and trade. The rise of the vertically disintegrated value chains can significantly alter the modes of global operation by an MNE. It allows MNEs to adopt new forms of interaction with their host countries in addition to establishing affiliated units like wholly owned subsidiaries and joint ventures. An MNE can source services and inputs from unaffiliated foreign suppliers or resort to procurement from their affiliated overseas ventures. When MNEs prefer offshore external sourcing of inputs due to existence of specialized suppliers they have little need to do FDI for sourcing abroad. Therefore, there is a trade-off between FDI to procure inputs in a host country and outsourcing (Grossman and Helpman, 2003) and given the standardization of information (Jacobides, 2005), MNEs are likely to opt for outsourcing from efficient local suppliers. Clearly, MNEs involvements in host input markets is likely to be more in the form of non-equity modes (i.e. outsourcing) than FDI. 3. MNE outsourcing in India In the last two decades, India has emerged as an attractive destination for global outsourcing in many areas of service and manufacturing sectors. India ranked the top attractive outsourcing destination in the A.T. Kearney Global Services Location Index (GSLI) throughout during 2004–2011 (Figure 1). The most important locational advantage that India enjoys over her competitors is on the category of

people skcumulativadvantageimprovemsector arecompanieIndian adv As per t(NASSCOcent in 20ITeS-BPO2010 (DeFortune 5century aInterestinggrowth inmode of MPhilippinecentres, co MNE outthe manufpharmaceincidents emerging

Source: B

2 Internation

February 43 NASSCOM

www.nass

kills and avaive business pe of English

ment in telecoe all contribues in moving vantage as a l

the informatOM), India’s 0092. About O (Informatiopartment of I00 were outs

and this propgly, this incrn sourcing frMNE operatioes, Indonesiaost advantage

sourcing in Ifacturing sectuticals and auof internationas important

Based on AT. K

nal Businesss Tim4. M (undated) ‘Indscom.in/downloa

ilability (Figurocess experilanguage (A

ommunicationuting to the

up the valuleader in serv

tion from thshare in the g25 per cent o

on TechnologInformation Tourcing their portion increreasing MNEom third-paron (Reuters, 2

a and Vietname and strategic

India is not cotor now coverutomotives tonal outsourcinform of MNE

Kearney global Figure 1.

mes (2011), ‘Ind

dian IT Industry–ad/IndianITIndu

Jaya Pra

ure 2). It repience and ski

A.T. Kearney,n infrastructur

global attracue chain whilvices outsourc

he National global outsouof the Indiangy Enabled STechnology, software req

eased to arouE outsourcingrty service pr2009). Moreom are catchinc government

onfined to thrs a wide rano low-technolng vary considE operation in

services locatiGlobal servic

dia's share in glo

– A Success Stoustry.doc; www.e

kash Pradha

presents Indiaills and a larg, 2004; Chanre and proactictiveness of le maintainincing.

Association urcing marketn software anServices- Bus

2010). Abouquirements to und two-thirg trend to Inroviders thanover, other emng up with It efforts.

he services senge of activitilogy productsderably amonn India.

ion index, varies location ind

obal outsourcing

ory’, accessible aescindia.com/htm

an

a’s first movge pool of ednda, 2008). Live governmeIndia. The a

ng their low-

of Softwart rose to 55 pd services exiness Process

ut one-third oIndia in the e

rds in the landia is assocn captives immerging econoIndia due to

ector alone. Gies from knows like apparelng different m

ous years dex, 2004–201

market rises to

at mlsite/AboutUs.

ver advantageducated manpLow cost of ent policies foattempt of Incost arbitrag

re & Servicer cent in 201

xports is conts Outsourcingf the global early half of tatter half of iated with re

mplying growiomies like Chmaturing of

Global firms’ wledge-based l and footwea

manufacturing

11

55 pct in 2010, s

aspx?Id=35

e in possessinpower with thskilled labouor the softwandian softwae is furtherin

es Companie10 from 51 ptributed by thg) segments firms from ththe twenty-firf the decadeelatively fasting non-equihina, Malaysif their service

outsourcing d industries likar. Though thg activities, it

says Nasscom’,

ng he ur, are re ng

es er he in he rst 3 .

ter ty ia, es

in ke he is

N

Source: Ba

Figure Pharmac Internationcompaniesterm comproducers manufactu(InternatioGood Manregulatorysuppliers clinical tri A large noutsourcinfrom RanbRanbaxy Chemical As per thSchwarz P The U.S. Mwith Lupinproducts t

4 India Info

(2003), ‘PIndia for c

5 Ranabxy (Release, Ju

6 Hindu Bus

Non-equity O

ased on AT. Ke 2. Category-w

ceuticals

nal contract ms in the 1990

mpetitiveness of active ph

uring capabilonal Organizanufacturing P

y bodies fromfor MNEs in

ials, data man

number of Mng deals can bbaxy in 1993to acquire tEntity RBx-2

he agreement Pharma.

MNE, DSM n Limited whto DSM und

oline (2000), ‘CPharma outsourccost managemen(2002) ‘Ranbaxyune 27.

siness Line (2005

Operation of

earney global swise average l

manufacturin0s (Pradhan, 2

and create eharmaceuticalities approveation for StanPractices), U.Sm other coun contract m

nagement and

MNEs have rbe elaborated. In June 200

the exclusive2258 for the tRanbaxy wo

Anti-Infectivhere the Indiaer the allianc

Contract Manufa

ing: The next bnt’, August 6. y and Schwarz P

5), ‘Lupin signs

Multinationa

services locatiolocational attr

ng emerged a2006). Pharmeconomic valal ingredients,ed by intern

ndardization) S. FDA’s (F

untries, Indianmanufacturingd laboratory se

resorted to cd here. The U.02, Schwarz Pe rights of dtreatment of B

ould manufac

ves, entered inn entity is to ce6. In the sa

acturing: Growthbig thing’, Augu

Pharma Sign a D

pact with DSM’

al Enterprise

4

on index, varioractiveness sco

as an importamaceutical MN

lues by outs, raw materinational qualicertificationsood and Drugn pharmaceu

g as well as ervices4.

contract man.S. MNE Eli Pharma AG odeveloping, mBenign Prost

cture and sup

nto a supply asupply the acame year, Lu

h Engine for Inst 25; India Bra

eal to Develop N

’, September 3.

es in India Fo

ous years. ore in services

ant growth mNEs realized tourcing fromials and bulkity and regu, WHO’s GMg Administrautical compacontract serv

nufacturing frLilly started

of Germany amarketing antate Hyperplapply finished

and marketingctive pharmacupin had ano

ndian Pharma Cand Equity Foun

New Drug to Tre

ocus on Out

s offshoring du

model for Indithat they can

m worlds’ onk drugs. Wi

ulatory standaMP (World He

tion) current anies turn ouvices like m

rom India busourcing Cefaannounced a lnd distributinsia in USA, Jformulations

g agreement iceutical ingredther marketin

ompanies?’, Aundation (2004), ‘

eat Benign Prost

tsourcing

uring 2004–20

ian pharmacen harness theirne of the cheith their lowards like theealth OrganizGMP (cGMP

ut to be attrmarketing, res

ut cases of afaclor intermelicensing deag Ranbaxy's Japan and Eus of the prod

in Septemberdient for a ranng agreement

ugust 16; Equity‘Pharma MNCs

tate Hyperplasia

011

eutical r long eapest

w cost e ISO zation-P) and ractive earch,

a few ediates al with

New urope5. duct to

r 2005 nge of t with

ymaster turn to

’, Press

Jaya Prakash Pradhan

5

GlaxoSmithKline (GSK) to manufacture and supply certain fixed dose combinations of tuberculosis drugs to GSK for marketing in the Philippines7. In December 2003, Nicholas Piramal got a five-year outsourcing deal from Advanced Medical Optics Inc. of the US. As per the deal, Nicholas Piramal will supply the opthalmic products to the American company for developed markets like the US, Europe and Japan. The Indian company expected additional annual revenue in the range of around $15–25 million from this contract manufacturing arrangement8. The year 2004 has seen Nicholas Piramal entered into two new custom manufacturing agreements with two US drug companies, which are expected to add $30 million revenues per annum9. One contract deal is from Allergan Inc of the US to whom Nicholas Piramal would supply two eye-related, anti-glaucoma active pharmaceutical ingredients, namely Levobunolol and Brimonidine. In November 2005, AstraZeneca AB, Sweden, signed a development and know-how agreement with Nicholas Piramal. As per this agreement, Nicholas Piramal is chosen as a partner in development of processes for the manufacture of intermediates, active ingredients or bulk drugs for supply to AstraZeneca10. In December 2005, a long-term contract manufacturing agreement between Pfizer International LLC and Nicholas Piramal was signed for animal health products11. Under this agreement, Nicholas Piramal will develop processes for Pfizer, provide scale-up batches for Phase trials and contract manufacture after the product is launched. In the first case of a patented molecule to be manufactured in India on a contract basis, Solvay Pharmaceuticals of Netherlands signed its contract manufacturing agreement with Dishman Pharmaceuticals in 2001 for production and supply of an active ingredient of an anti-hypertension drug, Teveten. The contract was for eight years with an estimated value of more than $10 million12. Since then Dishman is providing contract services to a growing number of global pharmaceutical firms including AstraZeneca, GlaxoSmithKline and Merck. In July 2005, Dishman entered into an agreement with NU SCAAN of the UK to develop and manufacture bulk actives for nutraceutical products of NU Scaan13. Shasun Chemicals and Drugs another Indian company chosen by MNEs for contract manufacturing, was found to derive nearly 12 per cent of its turnover from contract research and manufacturing business in the third quarter that ended on December 200514. The the US-based company, Austin Chemical, entered into a joint venture with Shasun in December 1999 for joint process development and custom manufacturing to serve multinational pharmaceutical companies operating in the regulated American market. In June 2004, Shasun achieved a strategic partnership with another US firm, Eastman Chemical, to collaborate on the development and manufacture of performance chemicals for the pharmaceutical industry15. In May 2005, US firm Codexis and Shasun entered into a manufacturing and supply agreement under which Shashun will manufacture the intermediate for a generic drug and Codexis will market the products worldwide to

7 Hindu Business Line (2005), ‘Lupin joins hands with GSK to market TB drugs in Philippines’, October 25. 8 Financial Express (2003), ‘NPIL In Outsourcing Deal With Advanced Medical Optics’, Wednesday, December 10. 9 Hindu Business Line (2004), ‘NPIL inks two custom mfg contracts’, November 04. 10 Express Pharma (2005), ‘AstraZeneca, Nicholas Piramal clinch R&D pact’, 16-30 November. 11 Hindu Business Line (2005), ‘NPIL-Pfizer deal on animal health products’, Dec 27. 12 Hindu Business Line (2001) ‘Dishman inks supply pact with Dutch co’, March 22. 13 Express Pharma (2005) ‘Dishman Pharma enters into an agreement with NU SCAAN, UK’, July 05. 14 Hindu Business Line (2006) ‘Shasun Chemicals net up 43 pc’, Saturday, Jan 21. 15 Hindu Business Line (2004) ‘Shasun, Eastman Chemical in tie-up — To make performance chemicals for pharma cos’,

Wednesday, Jun 16.

Non-equity Operation of Multinational Enterprises in India Focus on Outsourcing

6

the generic pharmaceutical industry16. Shasun also had other strategic partnerships for supplying ranitidine (anti-ulcer drug) and ibuprofen (anti-inflammatory pain reducer) to the US-based Apotex and for anti TB drugs with Eli Lilly. Automotives The Indian automotive industry is also turning out to be another centre for outsourcing by automotive MNEs. According to the online data released by the Automotive Component Manufacturers Association of India (ACMA), the auto component segment of the industry had grown nearly 19 per cent per annum in terms of production during 2000–09 and exports accounted for about 18 per cent of Indian auto component output in the same period17. Again in this industry, India offers MNEs the advantage of sourcing from low cost auto component suppliers possessing the globally preferred industry-specific quality standards. Singh (2010) noted that two-thirds of the ACMA members are ISO/TS-16949 accredited and some of them possessed more than one quality management system accredits. Most of the vehicle MNEs operating in India through local subsidiaries shows a strong preference for local component sourcing. Take for example the cases of Japanese MNEs like Maruti, Toyota, and Nissan and the U.S. MNEs like Ford Motor Company. The crucial role of Maruti (then a joint venture with Government of India) during the 1980s in establishing a chain of subcontracting for component manufacturing in India with a supportive vendor development programme is well documented in the literature (Suneja, 2000). For this Japanese MNE the use of local components account for as high as 90 per cent of the total components for manufacturing of its cars in India. Maruti has played a very important role in the technological developments of Indian auto component suppliers. The Indian subsidiary of Toyota Motor Corporation, Toyota Kirloskar Motor (TKM), currently sources components from some 67 domestic suppliers and is planning to expand its supplier base to 101 when the production of its model Etios starts in India18. Another Japanese MNE Nissan Motor Company sources auto components from India through its Indian subsidiary Nissan Motor (India) Limited for local production as well as its production units in China, Japan and Thailand. As per the company source, it has a target of sourcing components worth $25-30 million from India during 2010-1119. Similar to Maruti, Ford India’s model the Ikon has an indigenisation level close to 90 per cent. It had a supplier base of 100 in 2003. In addition to its own procurement of local components, in January 2003 Ford India Limited selected about 7 local suppliers to supply components to the parent’s subsidiaries elsewhere20 . The company also extended help to its Indian suppliers to earn Q1 quality certification so that the latter becomes eligible to supply to any of the Ford affiliates across the globe. As per the newspaper report, the Fiat Group Purchasing and General Motors are targeting sourcing of auto components worth $1 billion each from India and Ford is looking at Indian components purchase worth $500 million for its world-wide operations21.

16 Hindu (2005), ‘Shasun Chemicals pact with Codexis of U.S.’, Thursday, May 12. 17 Industry data is available here: http://www.acmainfo.com/#stat 18 Financial Express (2010), ‘Toyota to widen supplier base after Etios launch’, June 10. 19 Hindu Business Line (2010), ‘Nissan revises parts-sourcing target from India to $30 m’, December 12. 20 Hindu Business Line (2003), ‘India to become component sourcing base for Ford’, January 28. 21 Financial Express (2009), ‘Auto parts sourcing from India on a steady upswing’, October 17.

4. Trend As emphamotivatingbut their creation. strengthen However, MNEs is India. As affiliates osection, a purchase o The studyCentre forforeign mlatest year Figure 3 smanufactuhas been oand then rtotal manu2000–08. given that

ds and patt

asized before,g them to extforeign subsThe rise of

n the process

the data on not readily aa result, a n

operating in similar exerof local raw m

y has draws upr Monitoring

manufacturing r information

summarizes turing during on the rise in reached to $1ufacturing enNevertheless

t foreign affili

terns of loc

the fragmentternalize theisidiaries are cost efficienof local sourc

the exact extavailable for number of sta host countrrcise has beematerials has b

pon a sampleIndian Econoaffiliates couon the firm-l

the trends in 1991–2008. Tthe last two

12 billion in nterprise spens, this share oiates constitut

Jaya Pr

cal sourcing

tation of valur upstream analso adopting

nt and qualitycing by MNE

tent of total many host c

tudies have ary (Giroud an

en undertakenbeen presente

of 8369 Indiomy (CMIE).uld be identifievel foreign e

the size of loThe spendingdecades. It in2008. In the

nding on locaof foreign firmte about just 7

rakash Prad

7

g by MNE

ue chains has nd downstreag outsourciny intermedia

Es.

outsourcing (countries and analyzed the nd Mirza, 20n for India aned.

ian manufactu. Out of the tofied based onequity particip

ocal raw matg by foreign ncreased from1990s, foreig

al raw materiams in all firm7 per cent of t

han

affiliates i

changed the bam functions.g model for te suppliers

(i.e. captive aparticularly local inputs

006; Giroud, nd statistics

uring firms frotal number othe CMIE grpation.

erial sourcingmanufacturin

m $4.7 billiongn firms accoals; the ratio ms spending othe total of nu

n Indian m

boundary of t. It is not just

reaping the in a host co

and standalonso for emergsourcing beh

2007; De Beon the size o

rom the Prowof sample firmroup classifica

g by foreign ng firms on ln in 1991 to $ounted for abslightly fell ton local mateumber of firm

manufactur

the global firmt the parent Mbenefits of

ountry is like

ne outsourcinging countriehaviour of fo

eule, 2009). Iof MNE affil

wess database ms, a subset oation and ava

affiliates in Ilocal raw mat$7.4 billion inbout 15 per cto 13.5 per cerials is signi

ms in the samp

ring

ms by MNEs value

ely to

ng) by es like oreign In this liates’

of the of 566 ailable

Indian terials

n 2000 ent of

cent in ificant ple.

N

Source: BaF

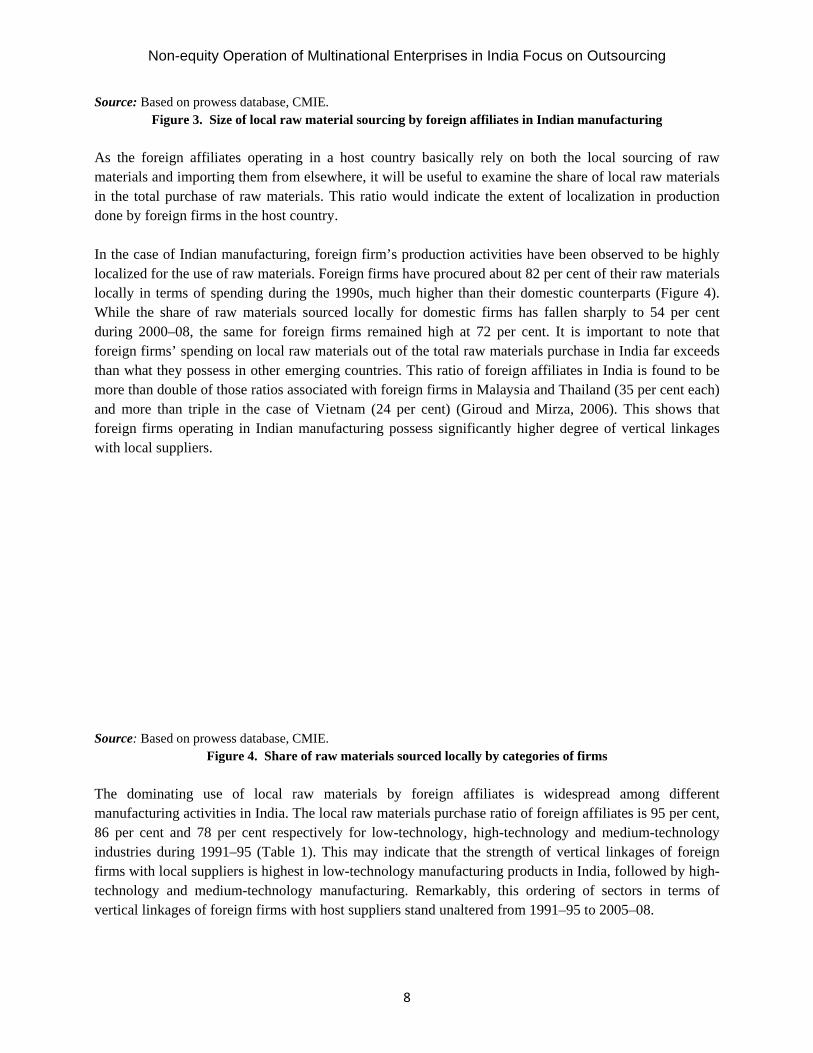

As the fomaterials in the totadone by fo In the caslocalized flocally in While theduring 20foreign firthan whatmore thanand more foreign firwith local

Source: Ba

The dommanufactu86 per ceindustries firms withtechnologvertical lin

Non-equity O

ased on prowesFigure 3. Size

oreign affiliatand importingal purchase ooreign firms i

e of Indian mfor the use ofterms of spe

e share of raw000–08, the srms’ spendingt they possessn double of th

than triple irms operatingl suppliers.

ased on prowesFigu

minating use uring activitient and 78 peduring 1991

h local suppliey and mediunkages of fore

Operation of

ss database, CMe of local raw

tes operating g them from

of raw materiin the host cou

manufacturingf raw materialending duringw materials ssame for foreg on local raws in other emeose ratios assin the case og in Indian m

ss database, CMure 4. Share o

of local rawes in India. Ther cent respec–95 (Table 1ers is highest um-technologeign firms wi

Multinationa

MIE. material sour

in a host coelsewhere, it als. This ratiountry.

g, foreign firmls. Foreign firg the 1990s, msourced localeign firms remw materials ouerging countrsociated with f Vietnam (2

manufacturing

MIE. of raw materia

w materials he local raw mctively for lo1). This may in low-techn

gy manufactuith host suppl

al Enterprise

8

rcing by foreig

ountry basicawill be usefuo would indi

m’s productiorms have procmuch higher lly for domesmained high ut of the totalries. This ratiforeign firms

24 per cent) g possess sign

als sourced loc

by foreign materials purcow-technology

indicate thatnology manufauring. Remarkiers stand una

es in India Fo

gn affiliates in

ally rely on bul to examine cate the exte

on activities hcured about 8than their dostic firms haat 72 per ce

l raw materiao of foreign a

s in Malaysia (Giroud and nificantly hig

cally by categ

affiliates ischase ratio ofy, high-technt the strengthfacturing prodkably, this oaltered from 1

ocus on Out

n Indian manu

both the locathe share of lnt of localiza

have been obs2 per cent of

omestic counts fallen sharp

ent. It is impals purchase inaffiliates in Inand ThailandMirza, 2006

gher degree o

ories of firms

s widespreadf foreign affilinology and mh of vertical lducts in India,ordering of se1991–95 to 20

tsourcing

ufacturing

al sourcing olocal raw matation in produ

served to be htheir raw matterparts (Figuply to 54 pe

portant to notn India far exndia is found

d (35 per cent 6). This showof vertical lin

d among difiates is 95 per

medium-technlinkages of fo, followed byectors in term005–08.

of raw terials uction

highly terials

ure 4). r cent te that xceeds d to be

each) ws that nkages

fferent r cent,

nology oreign

y high-ms of

Jaya Prakash Pradhan

9

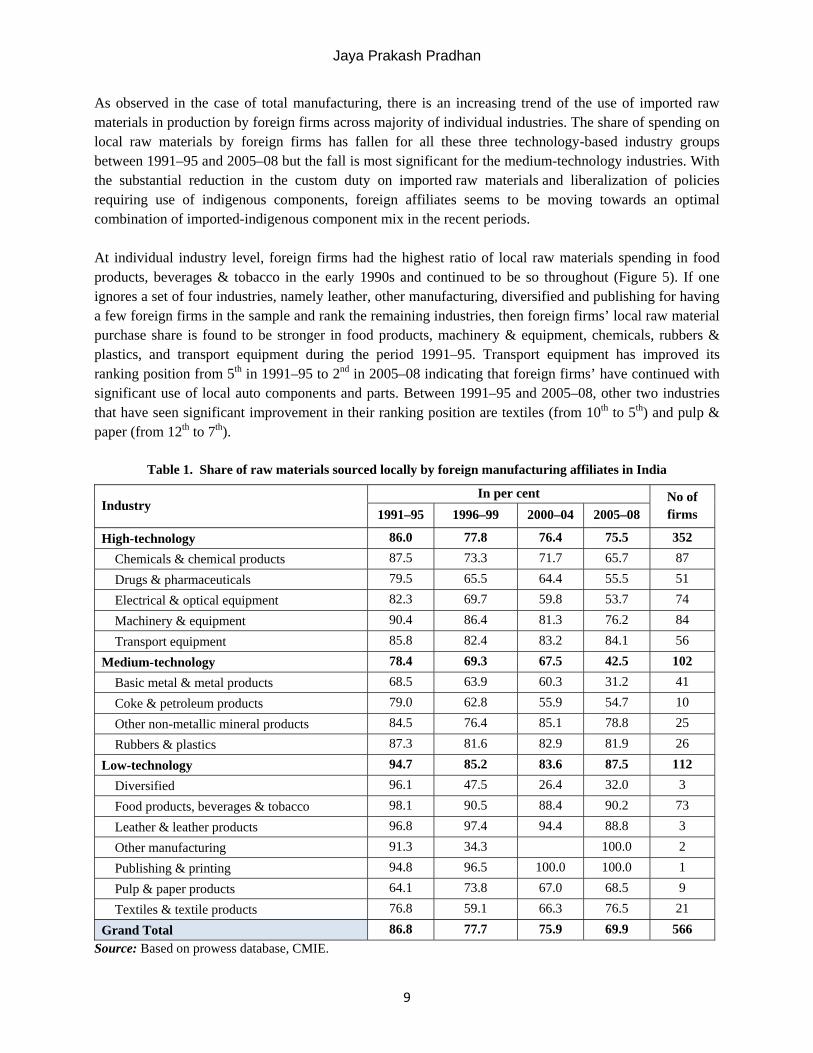

As observed in the case of total manufacturing, there is an increasing trend of the use of imported raw materials in production by foreign firms across majority of individual industries. The share of spending on local raw materials by foreign firms has fallen for all these three technology-based industry groups between 1991–95 and 2005–08 but the fall is most significant for the medium-technology industries. With the substantial reduction in the custom duty on imported raw materials and liberalization of policies requiring use of indigenous components, foreign affiliates seems to be moving towards an optimal combination of imported-indigenous component mix in the recent periods. At individual industry level, foreign firms had the highest ratio of local raw materials spending in food products, beverages & tobacco in the early 1990s and continued to be so throughout (Figure 5). If one ignores a set of four industries, namely leather, other manufacturing, diversified and publishing for having a few foreign firms in the sample and rank the remaining industries, then foreign firms’ local raw material purchase share is found to be stronger in food products, machinery & equipment, chemicals, rubbers & plastics, and transport equipment during the period 1991–95. Transport equipment has improved its ranking position from 5th in 1991–95 to 2nd in 2005–08 indicating that foreign firms’ have continued with significant use of local auto components and parts. Between 1991–95 and 2005–08, other two industries that have seen significant improvement in their ranking position are textiles (from 10th to 5th) and pulp & paper (from 12th to 7th).

Table 1. Share of raw materials sourced locally by foreign manufacturing affiliates in India

Industry In per cent No of

firms 1991–95 1996–99 2000–04 2005–08

High-technology 86.0 77.8 76.4 75.5 352 Chemicals & chemical products 87.5 73.3 71.7 65.7 87 Drugs & pharmaceuticals 79.5 65.5 64.4 55.5 51 Electrical & optical equipment 82.3 69.7 59.8 53.7 74 Machinery & equipment 90.4 86.4 81.3 76.2 84 Transport equipment 85.8 82.4 83.2 84.1 56

Medium-technology 78.4 69.3 67.5 42.5 102 Basic metal & metal products 68.5 63.9 60.3 31.2 41 Coke & petroleum products 79.0 62.8 55.9 54.7 10 Other non-metallic mineral products 84.5 76.4 85.1 78.8 25 Rubbers & plastics 87.3 81.6 82.9 81.9 26

Low-technology 94.7 85.2 83.6 87.5 112 Diversified 96.1 47.5 26.4 32.0 3 Food products, beverages & tobacco 98.1 90.5 88.4 90.2 73 Leather & leather products 96.8 97.4 94.4 88.8 3 Other manufacturing 91.3 34.3 100.0 2 Publishing & printing 94.8 96.5 100.0 100.0 1 Pulp & paper products 64.1 73.8 67.0 68.5 9 Textiles & textile products 76.8 59.1 66.3 76.5 21

Grand Total 86.8 77.7 75.9 69.9 566 Source: Based on prowess database, CMIE.

N

Note: Rankfirms in theSource: BaFigure 5. Iin India 5. Concl The role oover time are likelybusiness acontributiotechnologcrowding-investmen The case oMNEs as automotivinternation However, ability in infrastructto be havipolicy chaadjust to t

Non-equity O

king is done ee sample. ased on table 1Industry rank

luding rem

of non-equityas global ind

y to carry onand regulatoron to the devical capabilit-out possibilitnt and creates

of India demowell as their

ves as global nalization of f

sustaining anthe provisio

ture. For examing unclear panges, it is ahe changing q

Operation of

xcluding leath

. king based on t

marks

y mode of Mdustry evolven their outsoury environmevelopment prty building ty in a host clocal employ

onstrates that affiliates opecentres of ou

firms under a

nd improvingon of requirmple, in the c

policy, intelleclso very impquality requir

Multinationa

her, other manu

the share of lo

MNEs operatioes and value curcing from ents. This norocess of hosin local enteountry, MNE

yment.

a host countrrating in the hutsourcing w

a plethora of s

g the process ed regulatorycase of outsouctual propertyortant that lorements of MN

al Enterprise

10

ufacturing, div

ocal raw mate

on in host couchains get molocations tha

on-equity intest economies erprises. Un

Es sourcing of

ry may attracthost economy

was preceded strategic gove

of outsourciny regime, inurcing in bioly issues and pocal suppliersNEs.

es in India Fo

versified and pu

erial purchase

untries like oore and moreat provides ceraction of Mby enhancin

nlike horizonf inputs and s

t raw materiay. The rise ofby a phase o

ernment polic

ng would largnnovative suplogics manufproblem in qs be ready to

ocus on Out

ublishing for h

by foreign ma

outsourcing ise vertically dicost advantag

MNEs can mng their expontal FDI by services actua

l and service f Indian IT, phof local capabies.

gely depend upport-institutifacturing, Indiquality regulat move up the

tsourcing

having a few f

anufacturing

s continue to isintegrated. Mge and facili

make commenrts and faciliMNEs that

ally boost dom

sourcing by pharmaceuticability buildin

upon host couions and adeia is still perction. In addite value ladde

foreign

firms

grow MNEs itative ndable itating

have mestic

parent als and ng and

untry’s equate ceived tion to er and

Jaya Prakash Pradhan

11

Reference A.T. Kearney (2004), Making Offshore Decisions, Chicago: A.T. Kearney, Inc. Chanda, R. (2008), ‘India and Services Outsourcing in Asia’, Singapore Economic Review, 53(3), pp. 1–29. Coombs, R. and P. Battaglia (1998), ‘Outsourcing of Business Services and the Boundaries of the Firm’, CRIC

Working Paper, No. 5, Centre for Research on Innovation and Competition, Manchester: University of Manchester. De Beule, F. (2009), ‘Sourcing of multinational enterprises in China’, Paper presented at the Annual Research

Center for International Economics (RCIE) Conference 2009, University of International Business and Economics, Beijing, June 22–23.

Department of Information Technology (2010), Annual Report 2009–10, Ministry of Communications & Information Technology, New Delhi: Government of India.

Giroud, A. (2007), ‘MNEs vertical linkages: The experience of Vietnam after Malaysia’, International Business Review, 16(2), pp.159–176.

Giroud, A. and H. Mirza (2006), ‘Factors determining supply linkages between transnational corporations and local suppliers in ASEAN’, Transnational Corporations, 15(3), pp. 1-34.

Grossman, G.M., and E. Helpman, (2003), ‘Outsourcing versus FDI in Industry Equilibrium’, Journal of European Economic Association 1(2–3), pp. 317–327.

Holmstrom, B. and J. Roberts (1998), ‘The Boundaries of the Firm Revisited’, Journal of Economic Perspectives, 12(4), pp. 73–94.

Jacobides, M.G. (2005) ‘Industry Change through Vertical Disintegration: How and Why Markets Emerged In Mortgage Banking’, Academy of Management Journal, 48(3), 465–498.

Pradhan, J.P. (2006), ‘Global Competitiveness of Indian Pharmaceutical Industry: Trends and Strategies, ISID Working Paper, No.2006/05, New Delhi: Institute for Studies in Industrial Development.

Reuters (2009), ‘Captives in India: Is the honeymoon over?’, November 3, available at: http://in.reuters.com/article/2009/11/03/idINIndia-43637520091103.

Singh, N. (2010), ‘Adoption of industry-specific quality management system standards: determinants for auto component firms in India’, International Journal of Productivity and Quality Management, 5(1), pp. 88-107.

Suneja, J.S. (2000), ‘TNC-SME Co-operation: The Experience of India’, in UNCTAD (eds.) TNC-SME Linkages for Development: Issues-Experiences-Best Practices, pp. 85-97, New York and Geneva: United Nations.

UNCTAD (2010), World Investment Report 2010: Investing in a Low-carbon Economy, New York and Geneva: United Nations.

Williamson, O. (1985), The Economic Institutions of Capitalism. New York: The Free Press. About the Author

Jaya Prakash Pradhan, (PhD, Jawaharlal Nehru University) is an Associate Professor of Economics at the Central University of Karnataka, India. He has served on faculties of leading academic institutions in India including the Sardar Patel Institute of Economic & Social Research (Ahmedabad), Institute for Studies in Industrial Development (New Delhi), Gujarat Institute of Development Research (Ahmadabad), and worked as a consultant to the Research and Information System for Developing Countries (New Delhi). He is the authour of Indian Multinationals in the World Economy: Implications for Development (Bookwell Publisher, New Delhi, 2008); co-editor of The Rise of Indian Multinationals: Perspectives on Indian Outward Foreign Direct Investment (Palgrave

Macmillan, New York, 2010) and Industrialization, Economic Reforms and Regional Development: Essays in Honour of Professor Ashok Mathur (Shipra Publication, New Delhi, 2005); and co-authour of Transnationalization of Indian Pharmaceutical SMEs (Bookwell Publisher, New Delhi, 2008). He is also the co-editor of the special issue of International Journal of Emerging Markets on Emerging Multinationals (2010) and that of the special issue of Economics, Management, and Financial Markets on The Rise of Emerging Economies (2011).

Contact Information: Jaya Prakash Pradhan, Associate Professor, Department of Economic Studies & Planning, School of Business Studies, Central University of Karnataka, II Floor, Karya Soudha, Gulbarga University Campus, Gulbarga-585106, Karnataka, India. Telefax: 08472-272 066 (off.), [email protected] .

Transnational Corporations Review Volume 3, Number 2 June 2011 www.tnc-online.net, [email protected], DOI:10.5148/tncr.2011.1111 12-21

12

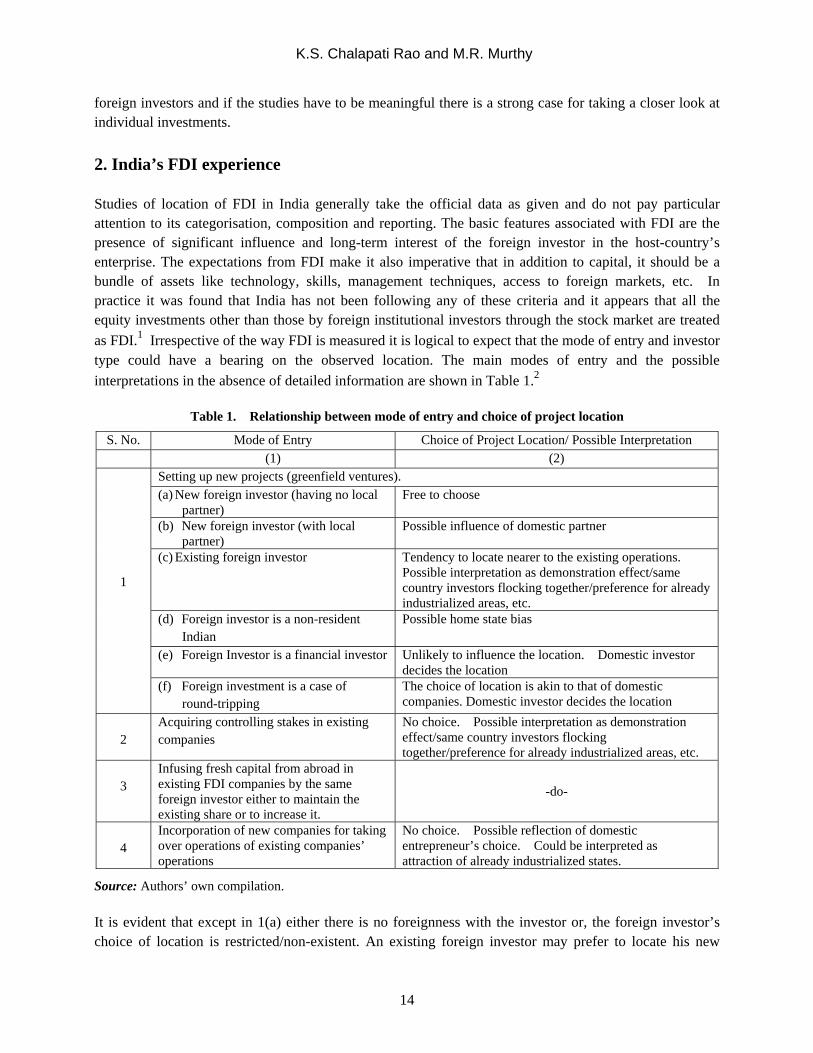

Location of FDI in India: Some Less-explored Aspects

K.S. Chalapati Rao and M.R. Murthy* Abstract: While there has been extensive research to identify the factors which influence FDI’s choice of host countries to invest in, considerable interest is also being attached to location of FDI establishments within specific countries. In India too, a few studies focused on the distribution of FDI in different states. Most of these were, however, based on aggregate FDI and that too of approvals only. Even those attempted at some level of disaggregation do not take note of specific characteristics of FDI like modes of entry, nature of the foreign investor, sector of investment, characteristics of local partner if any, etc. Since mid-2000s even this information is not available and it has become more difficult to identify FDI flows/establishments in different states. Based on India’s experience since 1991, this note seeks to underline the need for disaggregated analysis which takes into account investor/sectoral characteristics, mode of entry, size of investment, etc. Keywords: Foreign direct investment, location choice, India, investor characteristics, manufacturing 1. Introduction As in most developing countries, the perceived benefits of foreign direct investment (FDI) have led to heavy emphasis being placed on attracting large sums of FDI into India in the post-1991 period. Within the country, the same perception has led to different states to vie with each other for attracting major foreign direct investment projects which could be the nuclei for further industrialisation and generation of employment opportunities. Sub-national location of FDI has been a subject matter of research not only for developing countries but also the developed ones. Identification of influencing factors could in turn help attract FDI to the host country. The identified factors include agglomeration (Guimaraes, et. al., 2000; Crozet, et. al., 2004; Lee, et. al., 2008; Kim et. al., 2003; Dinh, 2008), imitation/demonstration (Barry, et. al., 2001; Araujo, 2009), governance (Du, et.al., 2007), already developed areas (Ögütçü, 2002), infrastructure (Chiang, 2010), labour quality (Gao, 2005; Liu, 2009), country affinity (Shannon et. al., 1999; Tan and Meyer, 2011), etc. Chadee, et. al. (2003) noted that for equity joint ventures (EJVs) in China level of foreign equity ownership, home country of the foreign partner, industry/sector, duration of the contract, and size and timing of investment influenced the location. Those investing in the service sector showed preference for major metropolitan cities. In a similar vein and in the context of India’s quest to attract large FDI inflows, a few studies examined the issue of location of FDI at the state level. The findings varied widely. Some have argued that the ability of a state to attract FDI depends on the policies of the individual state. For instance, based on the

* K.S. Chalapati Rao, Institute for Studies in Industrial Development, 4 Institutional Area, Vasant Kunj, New Delhi – 110070, India. Tel: 91 11 26761607, Fax: 91 11 26761631, E-mail: [email protected] M.R. Murthy, Institute for Studies in Industrial Development, 4 Institutional Area, Vasant Kunj, New Delhi – 110070, India. Tel: 91 11 26132791, Fax: 91 11 26761631, E-mail: [email protected]

Location of FDI in India: Some Less-explored Aspects

13

state-wise FDI approvals, Bajpai and Sachs (1999) noted that relatively fast moving reformers tended to attract larger investments, both from foreign and domestic investors. The ability to attract FDI was also associated with development of physical and human infrastructure. Similarly, based on an examination of state-wise aggregate approved FDI during 1991-2001, Singh and Srinivasan (2004) noted that variations in FDI across states could be influenced by specific policy initiatives and narrowly focused government investments in infrastructure. Sachs, Bajpai & Ramiah (2002) found that FDI was getting attracted to urban areas and natural resource deposits. It was, however, pointed out that despite being well-publicised as reform-oriented, Andhra Pradesh could attract only about 4.6 per cent of the total FDI approved till 2003 (Mahendra Dev, 2004). Padhi (2002), again based on state-wise approvals of FDI, noted that the initial level of manufacturing influences the location of FDI more than the infrastructure. Morris (2004), by analysing individual cases of approvals instead of state-wise aggregates, observed that leaving aside the cases of investment whose location is strictly related to availability of natural resources or those requiring nearness to markets, FDI tends to concentrate in the largest and best cities and attributed the modest FDI in Gujarat to its inability to develop cities like Bangalore and Hyderabad. Chakravorty (2002), based on a study of new projects that were implemented or were under implementation during 1992 to early 1998, noted that FDI preferred the coastal and metropolitan districts. He, however, noted that with a very small share in the overall, FDI projects were not significant in the total investment. Archana (2006) also based on state-level approval data, found infrastructure, quality of human capital and labour cost to be important factors for attracting FDI. Siddharthan (2008), based on an analysis of state-wise FDI approval data in case of India and inflows in case of China, noted that governance indicators played a crucial role in attracting FDI and domestic investment. It was therefore suggested that states instead of competing with each other in offering tax concessions should concentrate on good governance and in providing better infrastructure (both physical and human) facilities to attract investments. NCAER (2009) was based on Capitaline corporate database and a primary sample survey based on company level records provided by the government. It found that a significant proportion of FDI plants were located in Class-3 cities and that regions generally did not have an influence on FDI plants to locate in Class-3 cities. Based on a study of district-level data on individual FDI approvals during 1991-2005, Mukim & Nunnenkamp (2010) found that foreign investors have strong preference for locations where other foreign investors are. They are also attracted to industrially diverse locations and those with better infrastructure. Horna, et. al. (2010) noted that the involvement of Japanese automobile investors in four regions (New Delhi, Bangalore, Mumbai/Pune and Chennai) suggests that what constitutes an ‘agglomeration’ in emerging markets may involve a wider geographic area and more numerous business clusters than is typically the case for Japanese investment in other contexts. As seen above, studies on FDI inflows during the post-liberalisation period in India have generally dealt with aggregate level data and/or of approvals. In contrast to international studies, the disaggregation attempted in case of India was to a limited extent only. All these studies practically refer to the period till the early 2000s when the inflows were higher but the increase over the pre-1991 period was rather modest. In the absence of state-wise data on actual inflows, these had to work with approvals data. This was, however, often justified that approvals would reflect foreign investors’ intentions better than actual inflows. The criteria adopted by some studies to identify FDI companies in India and the data sources they relied upon were also open to question. The limited objective of this note is to underline that the Indian data on FDI approvals and inflows is not easily amenable to firm conclusions on the locational choices of

K.S. Chalapati Rao and M.R. Murthy

14

foreign investors and if the studies have to be meaningful there is a strong case for taking a closer look at individual investments. 2. India’s FDI experience Studies of location of FDI in India generally take the official data as given and do not pay particular attention to its categorisation, composition and reporting. The basic features associated with FDI are the presence of significant influence and long-term interest of the foreign investor in the host-country’s enterprise. The expectations from FDI make it also imperative that in addition to capital, it should be a bundle of assets like technology, skills, management techniques, access to foreign markets, etc. In practice it was found that India has not been following any of these criteria and it appears that all the equity investments other than those by foreign institutional investors through the stock market are treated as FDI.1 Irrespective of the way FDI is measured it is logical to expect that the mode of entry and investor type could have a bearing on the observed location. The main modes of entry and the possible interpretations in the absence of detailed information are shown in Table 1.2

Table 1. Relationship between mode of entry and choice of project location

S. No. Mode of Entry Choice of Project Location/ Possible Interpretation (1) (2)

1

Setting up new projects (greenfield ventures). (a) New foreign investor (having no local

partner) Free to choose

(b) New foreign investor (with local partner)

Possible influence of domestic partner

(c) Existing foreign investor Tendency to locate nearer to the existing operations. Possible interpretation as demonstration effect/same country investors flocking together/preference for already industrialized areas, etc.

(d) Foreign investor is a non-resident Indian

Possible home state bias

(e) Foreign Investor is a financial investor Unlikely to influence the location. Domestic investor decides the location

(f) Foreign investment is a case of round-tripping

The choice of location is akin to that of domestic companies. Domestic investor decides the location

2

Acquiring controlling stakes in existing companies

No choice. Possible interpretation as demonstration effect/same country investors flocking together/preference for already industrialized areas, etc.

3

Infusing fresh capital from abroad in existing FDI companies by the same foreign investor either to maintain the existing share or to increase it.

-do-

4

Incorporation of new companies for taking over operations of existing companies’ operations

No choice. Possible reflection of domestic entrepreneur’s choice. Could be interpreted as attraction of already industrialized states.

Source: Authors’ own compilation. It is evident that except in 1(a) either there is no foreignness with the investor or, the foreign investor’s choice of location is restricted/non-existent. An existing foreign investor may prefer to locate his new

Location of FDI in India: Some Less-explored Aspects

15