Embed Size (px)

Citation preview

Trading in India

The Status Quo

Anshuman JaswalSenior Analyst, Celent

RoadmapRoadmap• Brief look at equity, bond and derivative

markets

• Level of electronic trading– DMA and Algorithmic trading

• Industry evolution

• Regulatory practices

Market OverviewMarket Overview

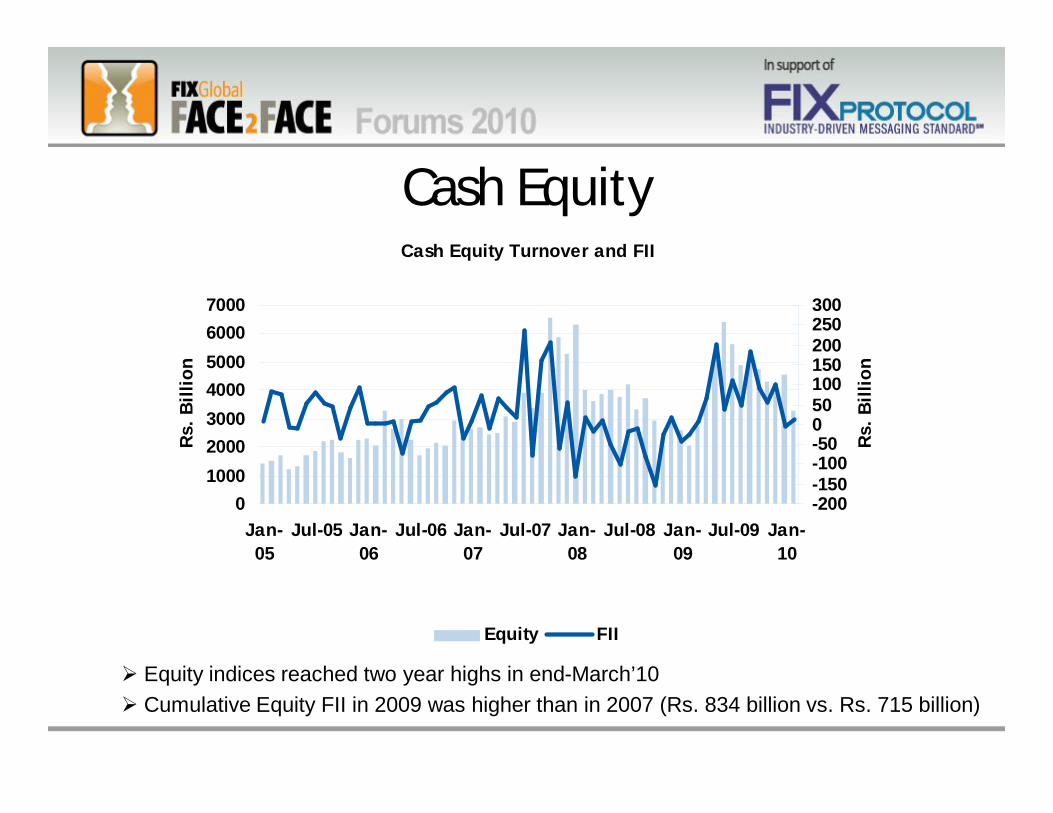

Cash Equity Turnover and FII

01000200030004000500060007000

Jan-05

Jul-05 Jan-06

Jul-06 Jan-07

Jul-07 Jan-08

Jul-08 Jan-09

Jul-09 Jan-10

Rs. B

illio

n

-200-150-100-50050100150200250300

Rs. B

illio

n

Equity FII

Equity indices reached two year highs in end-March’10 Cumulative Equity FII in 2009 was higher than in 2007 (Rs. 834 billion vs. Rs. 715 billion)

Cash Equity

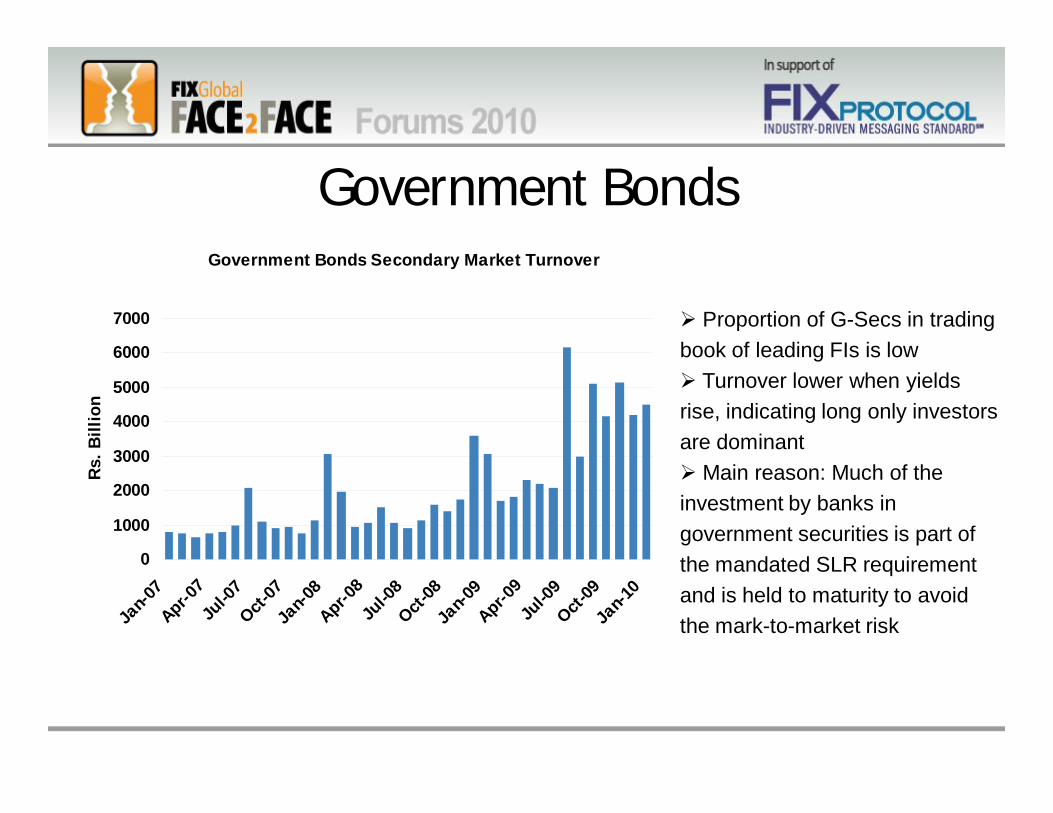

Government BondsGovernment Bonds Secondary Market Turnover

0

1000

2000

3000

4000

5000

6000

7000

Jan-0

7Apr-0

7Ju

l-07

Oct-07

Jan-0

8Apr-0

8Ju

l-08

Oct-08

Jan-0

9Apr-0

9Ju

l-09

Oct-09

Jan-1

0

Rs.

Bill

ion

Proportion of G-Secs in trading book of leading FIs is low Turnover lower when yields rise, indicating long only investors are dominant Main reason: Much of the investment by banks in government securities is part of the mandated SLR requirement and is held to maturity to avoid the mark-to-market risk

Corporate Bonds

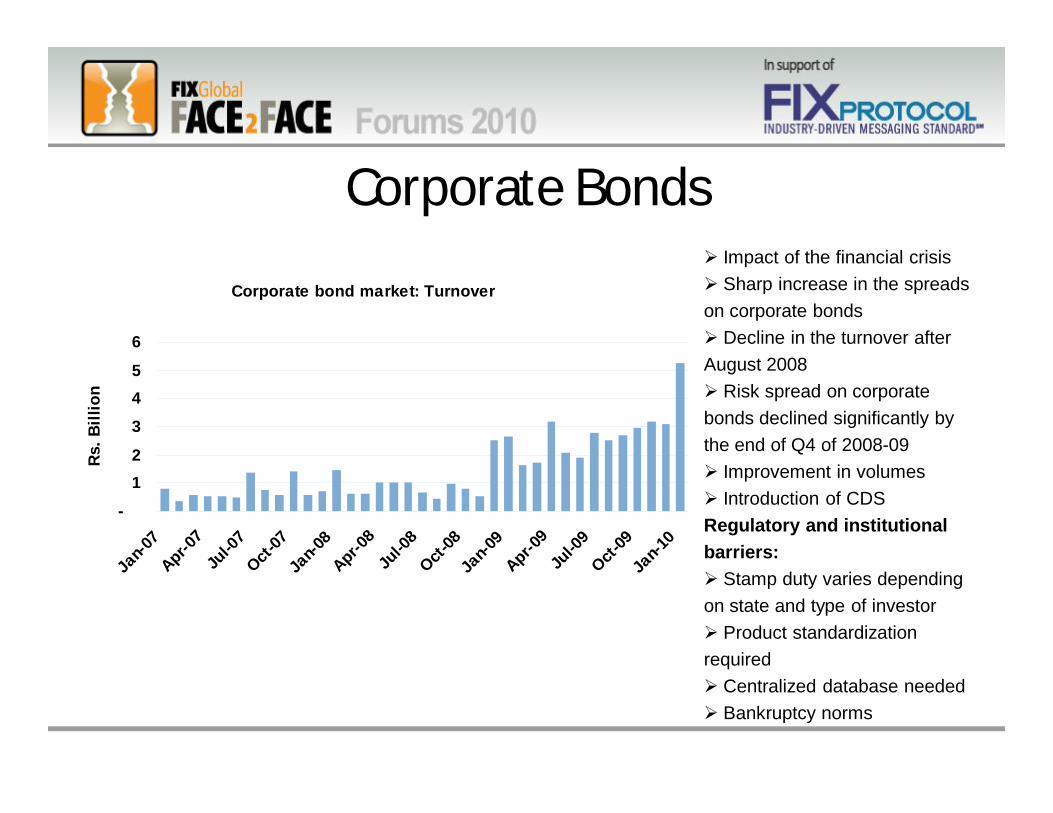

Corporate bond market: Turnover

-

12

3

45

6

Jan-0

7

Apr-07

Jul-0

7

Oct-07

Jan-0

8

Apr-08

Jul-0

8

Oct-08

Jan-0

9

Apr-09

Jul-0

9

Oct-09

Jan-1

0

Rs. B

illio

n

Impact of the financial crisis Sharp increase in the spreads on corporate bonds Decline in the turnover after August 2008 Risk spread on corporate bonds declined significantly by the end of Q4 of 2008-09 Improvement in volumes Introduction of CDSRegulatory and institutional barriers: Stamp duty varies depending on state and type of investor Product standardization required Centralized database needed Bankruptcy norms

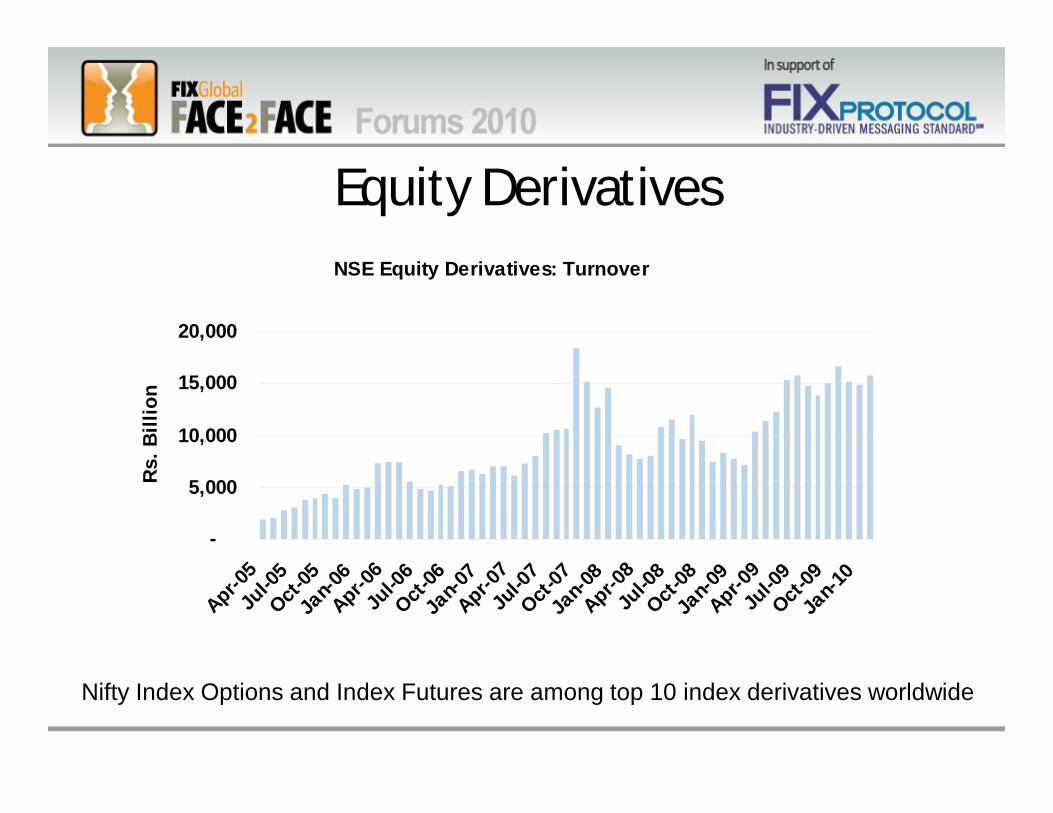

Equity DerivativesNSE Equity Derivatives: Turnover

-

5,000

10,000

15,000

20,000

Apr-05

Jul-0

5Oct-

05Ja

n-06

Apr-06

Jul-0

6Oct-

06Ja

n-07

Apr-07

Jul-0

7Oct-

07Ja

n-08

Apr-08

Jul-0

8Oct-

08Ja

n-09

Apr-09

Jul-0

9Oct-

09Ja

n-10

Rs.

Bill

ion

Nifty Index Options and Index Futures are among top 10 index derivatives worldwide

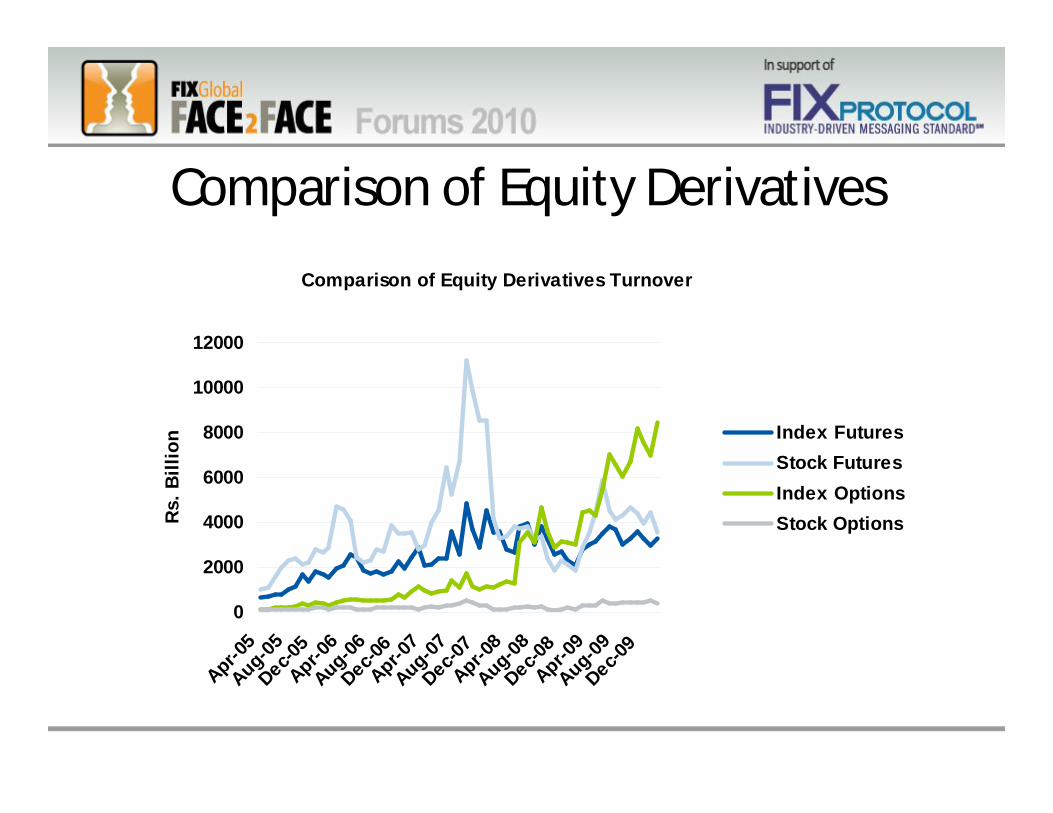

Comparison of Equity Derivatives

Comparison of Equity Derivatives Turnover

0

2000

4000

6000

8000

10000

12000

Apr-05

Aug-05Dec-0

5Apr-0

6Aug-06Dec-0

6Apr-0

7Aug-07Dec-0

7Apr-0

8Aug-08Dec-0

8Apr-0

9Aug-09Dec-0

9

Rs.

Bill

ion Index Futures

Stock FuturesIndex OptionsStock Options

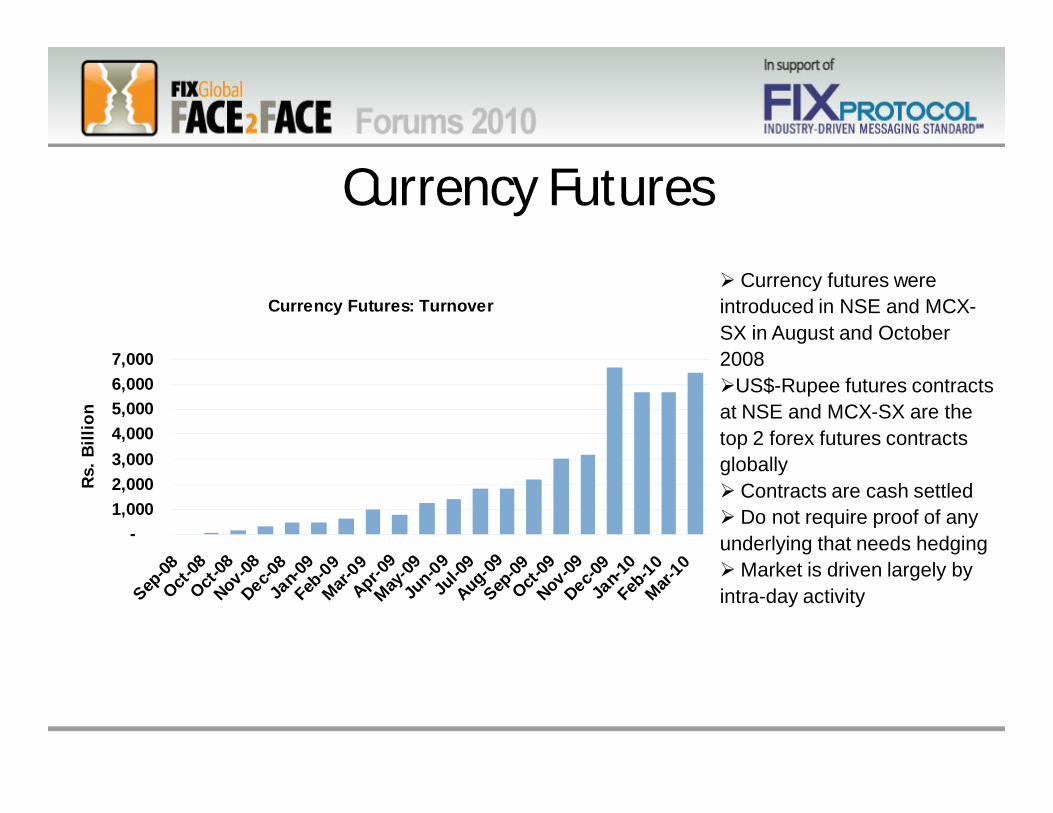

Currency Futures

Currency Futures: Turnover

-1,0002,0003,0004,0005,0006,0007,000

Sep-08

Oct-08

Oct-08

Nov-08

Dec-08

Jan-0

9

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-0

9

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-1

0

Feb-10

Mar-10

Rs.

Bill

ion

Currency futures were introduced in NSE and MCX-SX in August and October 2008 US$-Rupee futures contracts at NSE and MCX-SX are the top 2 forex futures contracts globally Contracts are cash settled Do not require proof of any underlying that needs hedgingMarket is driven largely by intra-day activity

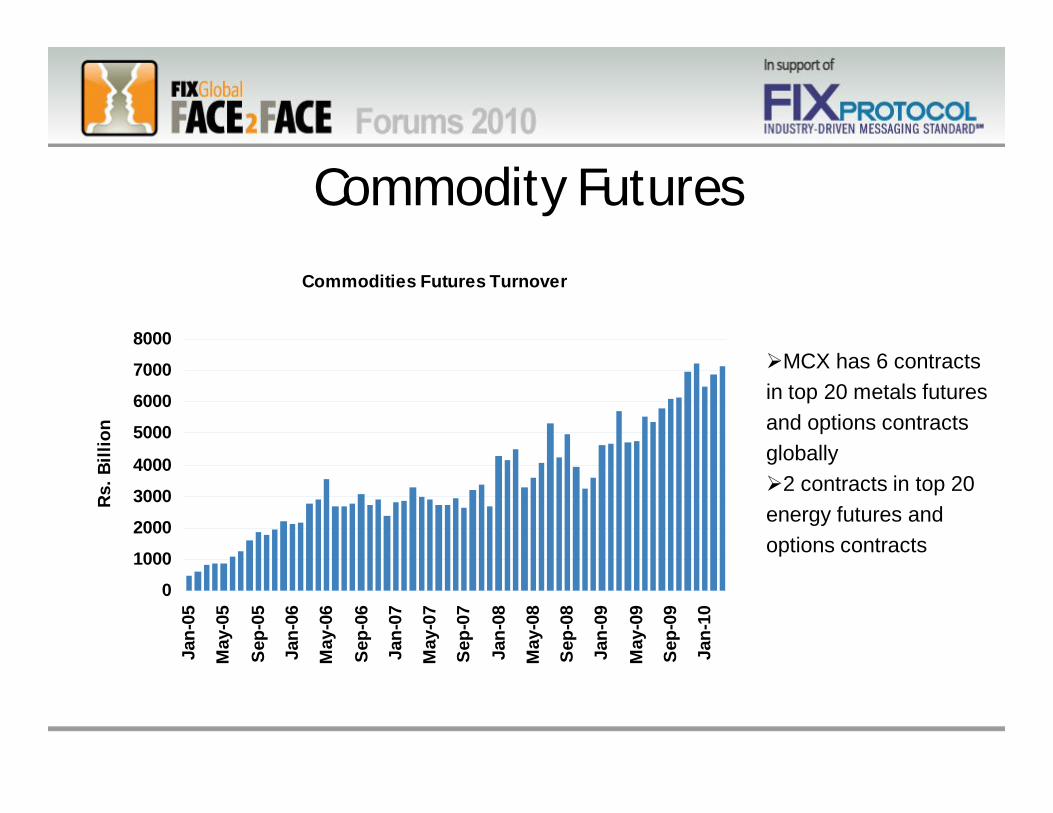

Commodity Futures

Commodities Futures Turnover

0

1000

2000

3000

4000

5000

6000

7000

8000

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

Rs.

Bill

ion

MCX has 6 contracts in top 20 metals futures and options contracts globally2 contracts in top 20 energy futures and options contracts

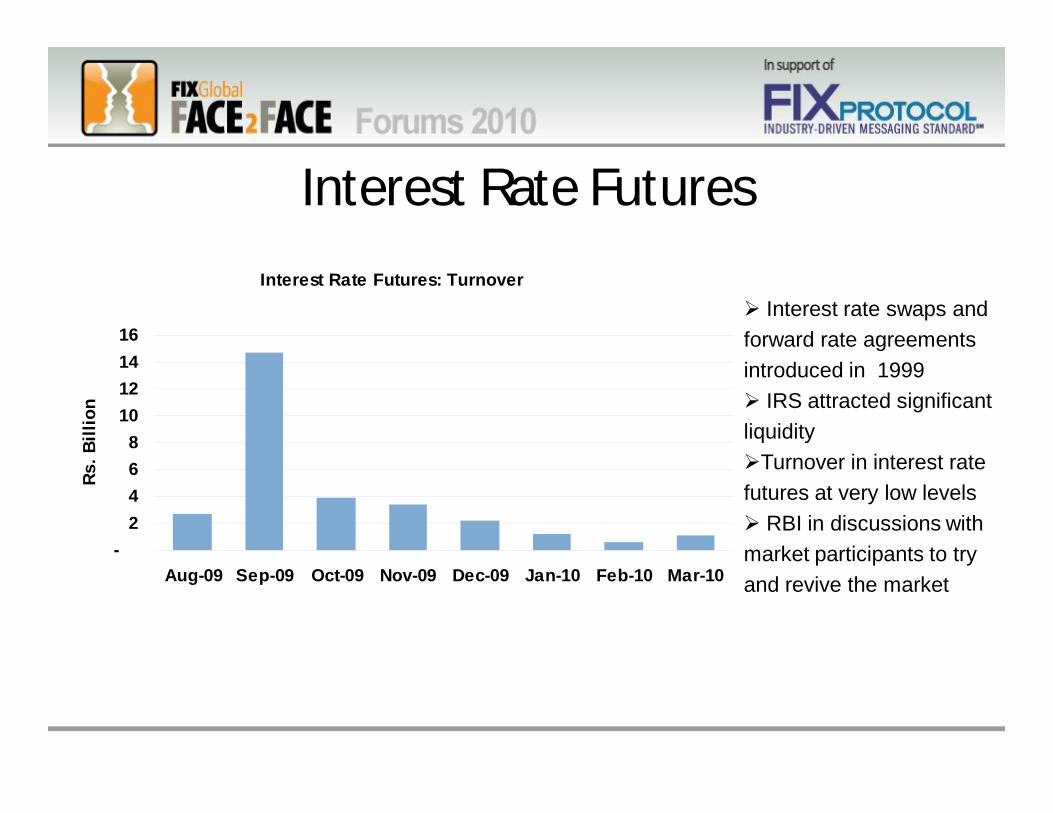

Interest Rate Futures

Interest Rate Futures: Turnover

-2468

10121416

Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10

Rs. B

illio

n

Interest rate swaps and forward rate agreements introduced in 1999 IRS attracted significant liquidityTurnover in interest rate futures at very low levels RBI in discussions with market participants to try and revive the market

Electronic TradingElectronic Trading

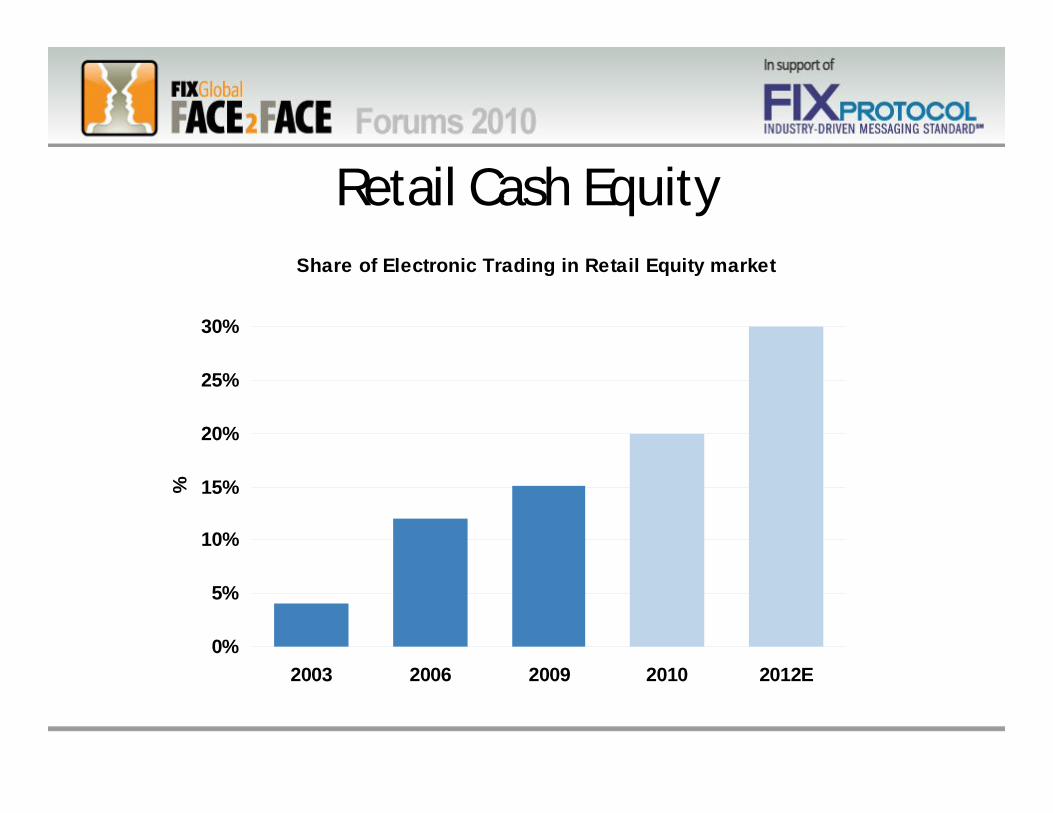

Retail Cash EquityShare of Electronic Trading in Retail Equity market

0%

5%

10%

15%

20%

25%

30%

2003 2006 2009 2010 2012E

%

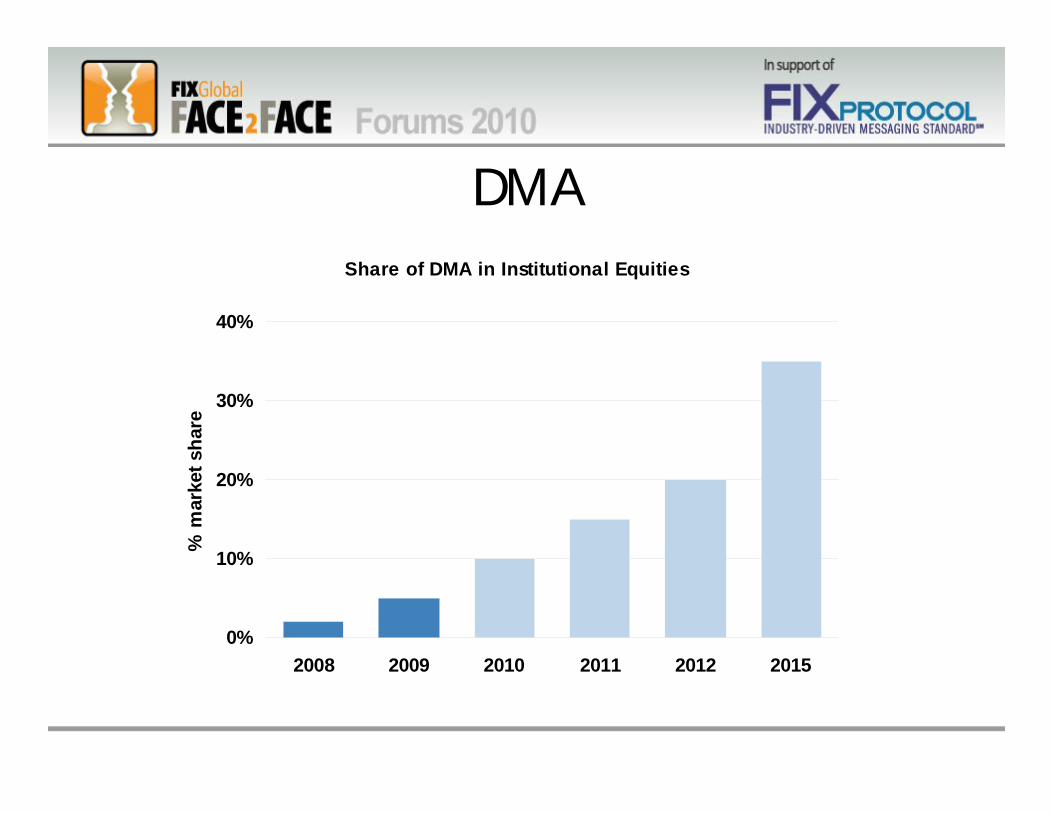

DMAShare of DMA in Institutional Equities

0%

10%

20%

30%

40%

2008 2009 2010 2011 2012 2015

% m

arke

t sha

re

Main IssuesMain Issues

Points of Discussion• DMA- more one touch than direct

• Physical infrastructure for algorithmic trading

• Co-location

• Higher compliance costs driving consolidation

• A volume game: automation and commissions

• Benefit of longer trading hours

• Standardization required

• Technology integrating front and back-office

DMA• FIIs driving change

• Greater acceptance among DIIs, especially top MFs

• Still mainly low-touch

• Restrictions on ‘direct’ DMA

• Even low-touch has improved level of automation Less manpower required

Costs of trading lowered

• Foreign and Tier I domestic brokerages geared up

• Tier II in process of adopting technology

Algorithmic Trading• Accepted as the future of institutional trading

• Infrastructure a barrier in short term Vital market data speed is improved

Latency reduced, matching engines faster

Low-touch DMA prevents algorithmic trading

Pre-order risk management also a factor - affects latency

• Regulation slowing adoption - only ‘white box’ for now Low incentive to foreign brokerages to bring developed algorithms to

India

Need to refine algorithms for local markets

• Local brokerages and vendors still developing capabilities

Cost of Trading

• By global comparison, Indian markets are: Costly in terms of exchange fees

Market data and clearing is much cheaper

• Automation beneficial to buy-sidePost-trade processing has improved

• Reducing revenues of sell-side: ‘volume’ game

Higher Compliance Costs

• SEBI and exchanges’ requirements tough on brokersSmaller brokers struggling to cope

Consolidation inevitable

• Need to take smaller brokers’ resources into accountProvide IT support

Standardization of procedures across exchanges required

Co-location

• International standard

• India late adopter

• Overall latency needs to be reduced for co-location to be meaningful

Longer Trading Hours

• Benefits still not conclusiveFurther extension expected

Greater pressure on post-trade processing

Smaller players will find it difficult to bear costs

Where does it end? Need for debate

Importance of Standardization

• Number of exchanges risingEach with own certification impacting costsStandardization required going forward

More cooperation between exchanges - finding common ground

Technology

• Front and back-office working together in real-timeAdvantageous for IT vendors which cater to both

front and back-office

• Global and local systems also closer

Clearing Houses• Clearing houses like ‘silos’Need to cover multiple assets across exchanges

Wider coverage will drive innovation and reduce costs

Block Deals• High market impact Operationally difficult to execute for institutional

investors

Dark pools beneficial but not probable

Regulator needs to address issue

Relationships Still Matter

• Domestic institutional brokerages recruited from foreign counterparts to increase market-share

• Reverse flow also seen

• Expected to continue as a factor despite automation

Regulatory Overlaps• Securities and Exchange Board of India is the main

capital market regulator• Overlap of its domain with:

– Insurance regulator, IRDA (e.g., unit linked insurance plans)– Central bank, RBI (e.g., FII limits, currency and interest rate futures,

investment banks)– Provident fund regulator, PFRDA (e.g., NSDL)– FMC (commodity markets)

• High Level Coordination Committee (HLCC) on capital markets not deemed successful

• Financial Stability and Development Council (FSDC)