Embed Size (px)

Citation preview

Managerial Accounting

Final Exam Review: Business Administration & Applied Accounting

Question Sheet

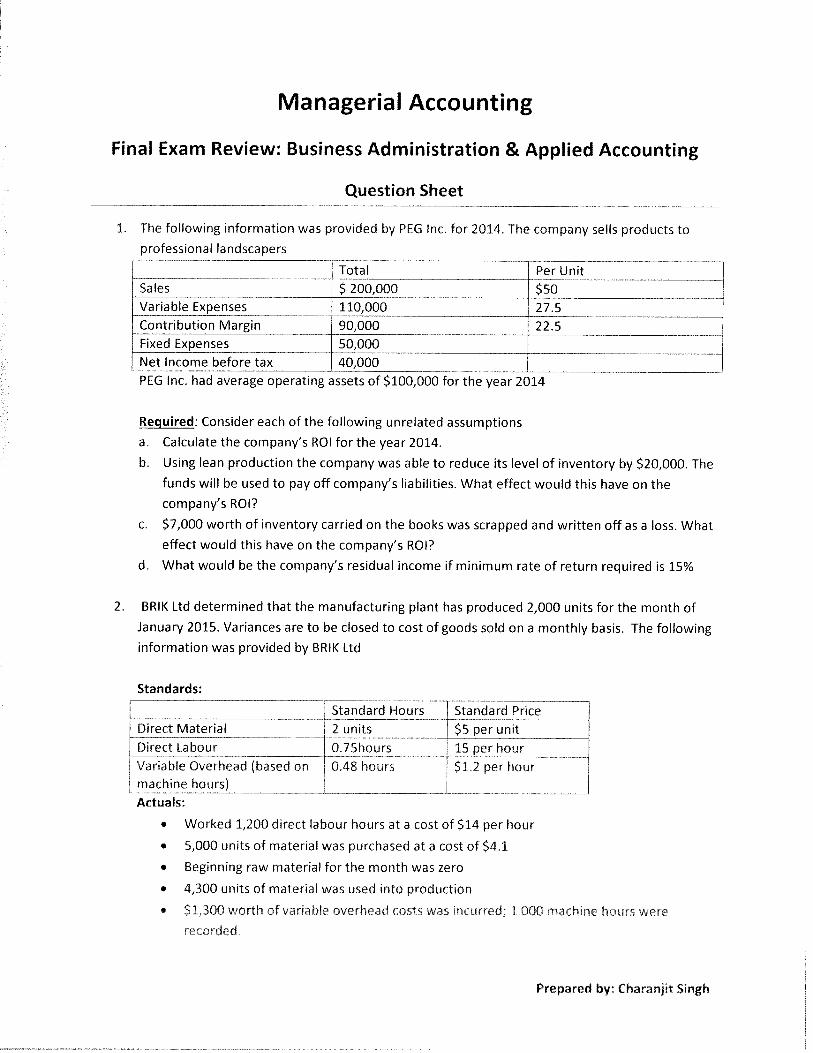

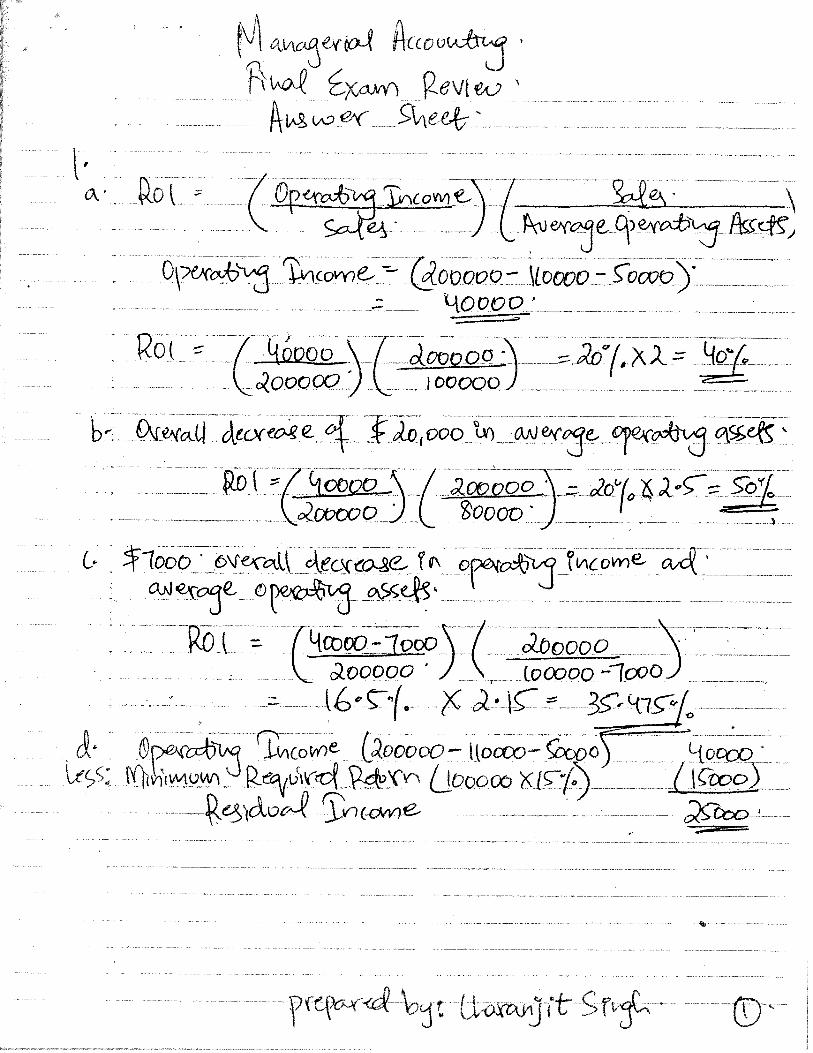

1. The following information was provided by PEG Inc. for 2014. The company sells products to

professional landscapers

__________

Total Per UnitSales $ 200,000 $50Variable Expenses 110,000 27.5Contribution Margin 90,000 22.5Fixed Expenses 50,000Net Income before tax 40,000PEG Inc. had average operating assets of $100,000 for the year 2014

çjed: Consider each of the following unrelated assumptions

a. Calculate the company’s ROl for the year 2014.

b. Using lean production the company was able to reduce its level of inventory by $20,000. The

funds will be used to pay off company’s liabilities. What effect would this have on the

company’s ROl?

c. $7,000 worth of inventory carried on the books was scrapped and written off as a loss. What

effect would this have on the company’s ROl?

d. What would be the company’s residual income if minimum rate of return required is 15%

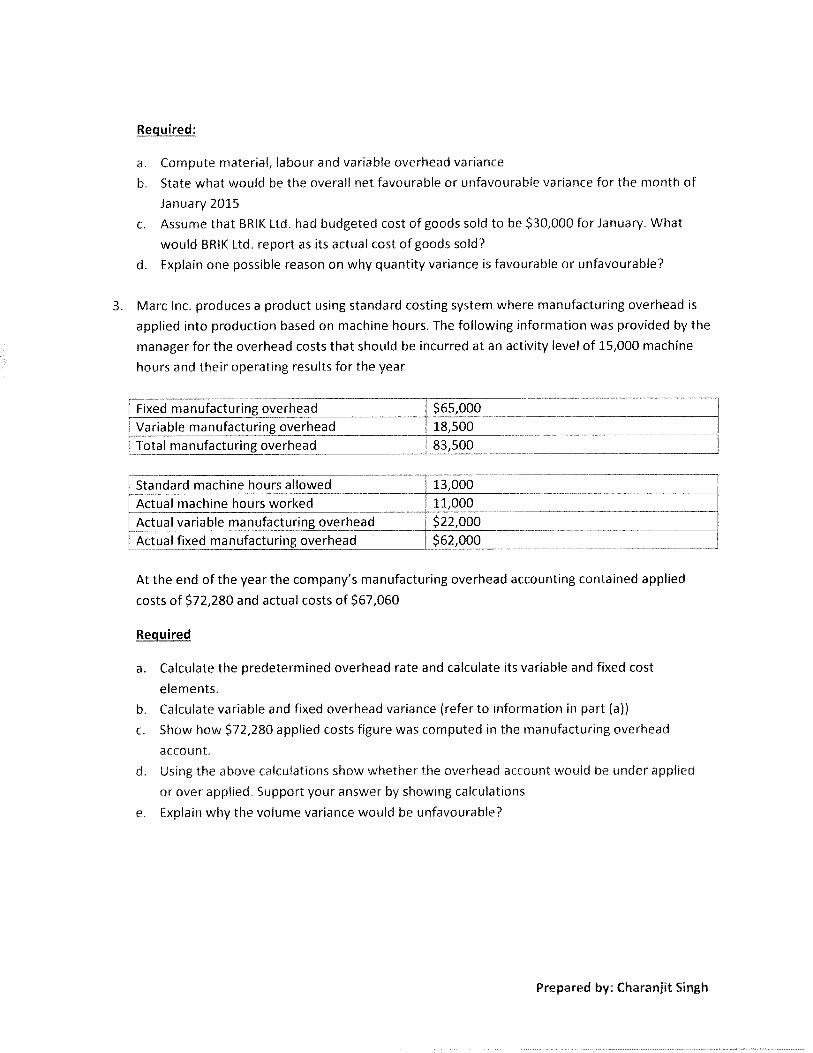

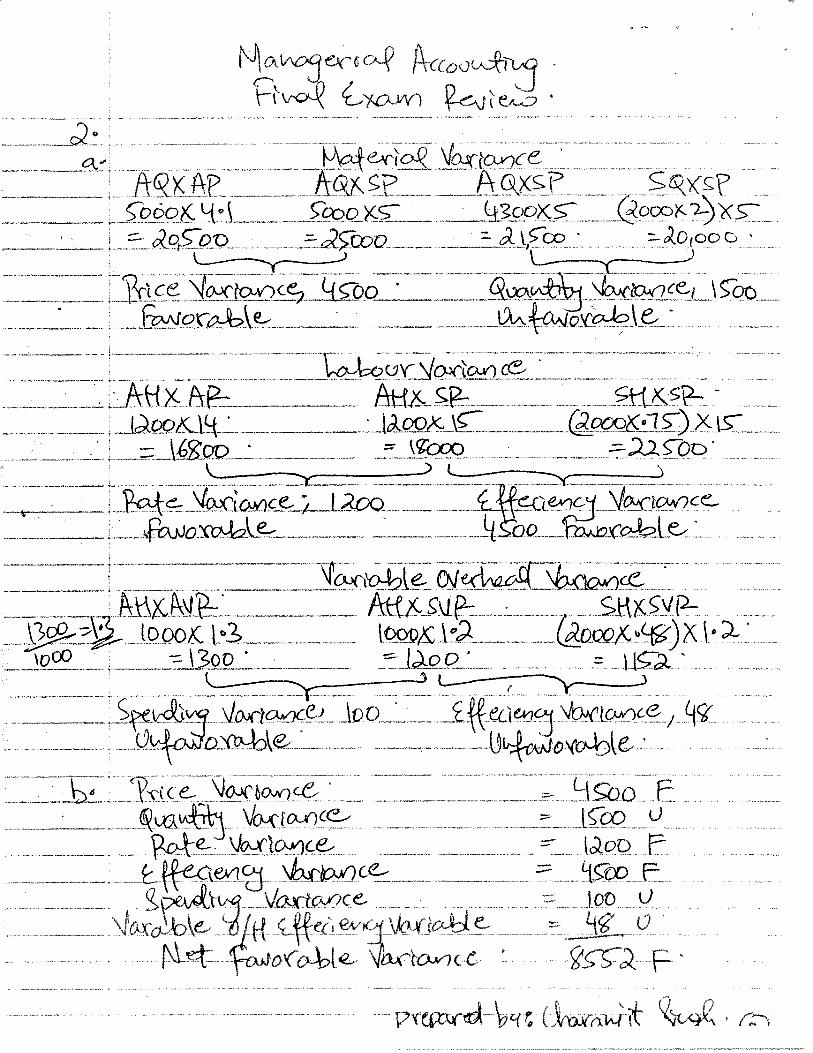

2. BRIK Ltd determined that the manufacturing plant has produced 2,000 units for the month of

January 2015. Variances are to be closed to cost of goods sold on a monthly basis. The following

information was provided by BRIK Ltd

Standards:

Standard Hours Standard PriceDirect Material 2 units $5 per unitDirect Labour 0.75hours 15 per hourVariable Overhead (based on 0.48 hours $1.2 per hourmachine hours) [Actuals:

• Worked 1,200 direct labour hours at a cost of $14 per hour

• 5,000 units of material was purchased at a cost of $4.1

• Beginning raw material for the month was zero

• 4,300 units of material was used into production

• $1,300 worth of variable overhead costs was incurred; 1,000 machine hours were

recorded.

Prepared by: Charanjit Singh

Required:

a. Compute material, labour and variable overhead variance

b. State what would be the overall net favourable or unfavourable variance for the month of

January 2015

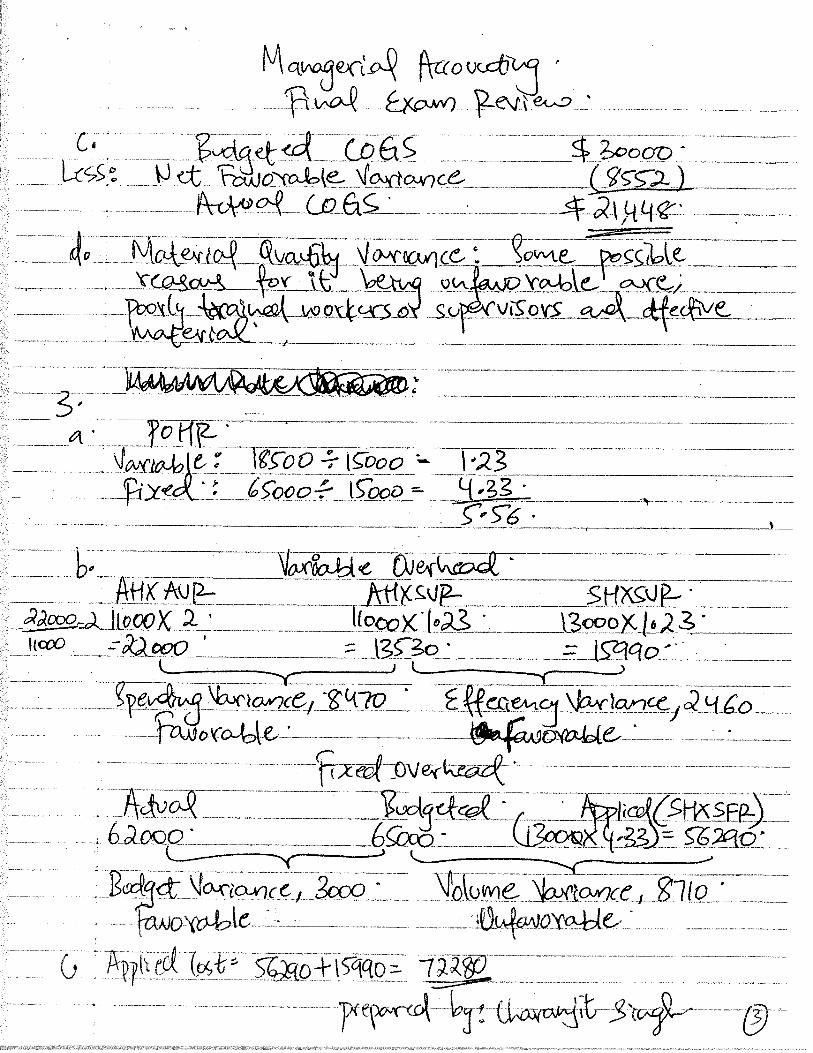

c. Assume that BRIK Ltd. had budgeted cost of goods sold to be $30,000 for January. What

would BRIK Ltd. report as its actual cost of goods sold?

d. Explain one possible reason on why quantity variance is favourable or unfavourable?

3. Marc Inc. produces a product using standard costing system where manufacturing overhead is

applied into production based on machine hours. The following information was provided by the

manager for the overhead costs that should be incurred at an activity level of 15,000 machine

hours and their operating results for the year

Fixed manufacturing overhead $65,000

Variable manufacturing overhead 18,500

Total manufacturing overhead 83,500

Standard machine hours allowed 13,000

Actual machine hours worked 11,000

Actual variable manufacturing overhead $22,000

Actual fixed manufacturing overhead $62,000

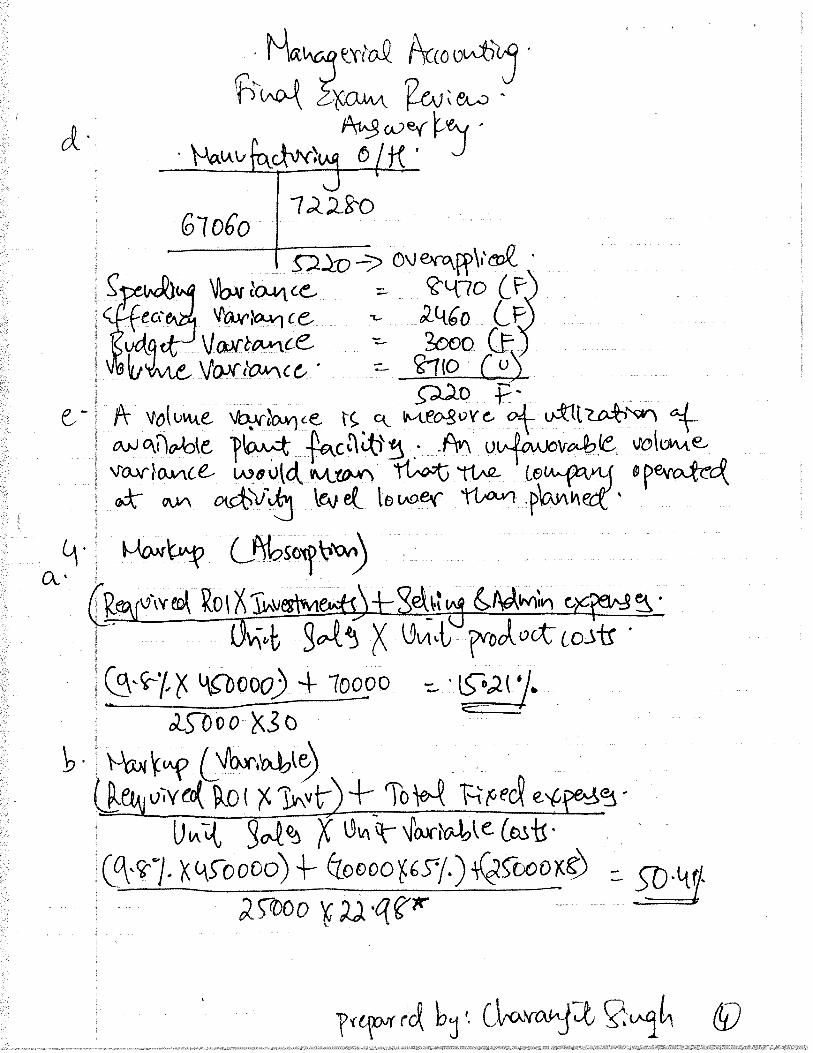

At the end of the year the company’s manufacturing overhead accounting contained applied

costs of $72,280 and actual costs of $67,060

Required

a. Calculate the predetermined overhead rate and calculate its variable and fixed cost

elements.

b. Calculate variable and fixed overhead variance (refer to information in part (a)>

c. Show how $72,280 applied costs figure was computed in the manufacturing overhead

account.

d. Using the above calculations show whether the overhead account would be under applied

or over applied. Support your answer by showing calculations

e. Explain why the volume variance would be unfavourable?

Prepared by: Charanjit Singh

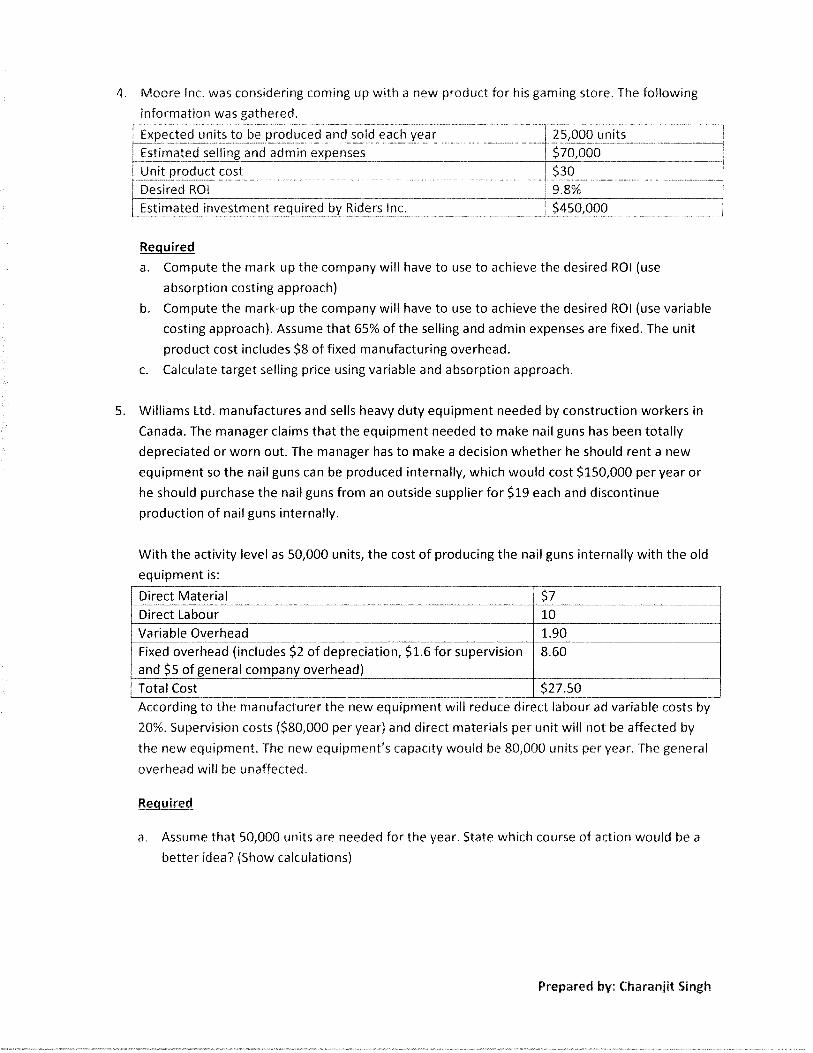

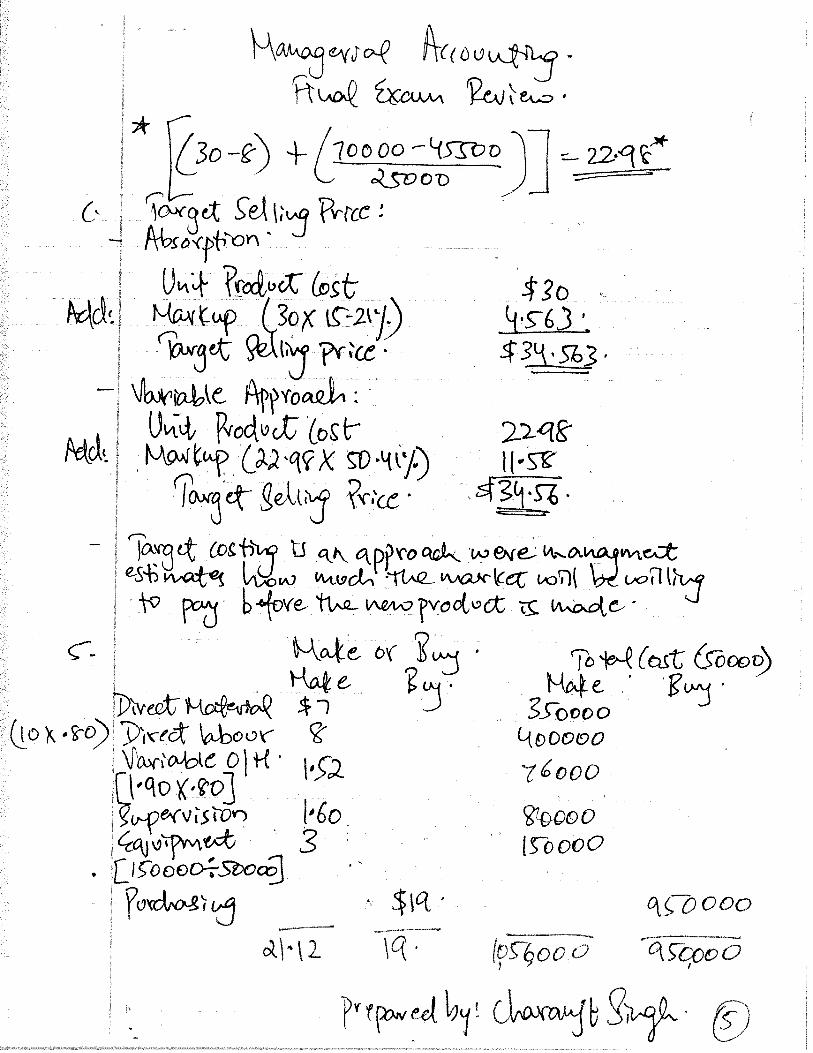

4. Moore Inc. was considering coming up with a new product for his gaming store. The following

information was gathered. -

Expected units to be produced and sold each year 25,000 units

Estimated selling and admin expenses $70,000Unit product cost j $30Desired ROt [ 9.8%

Estimated investment required by Riders Inc. [$450,000

Required

a. Compute the mark-up the company will have to use to achieve the desired ROl (use

absorption costing approach)

b. Compute the mark-up the company will have to use to achieve the desired ROl (use variable

costing approach). Assume that 65% of the selling and admin expenses are fixed. The unit

product cost includes $8 of fixed manufacturing overhead.

c. Calculate target selling price using variable and absorption approach.

5. Williams Ltd. manufactures and sells heavy duty equipment needed by construction workers in

Canada. The manager claims that the equipment needed to make nail guns has been totally

depreciated or worn out. The manager has to make a decision whether he should rent a new

equipment so the nail guns can be produced internally, which would cost $150,000 per year or

he should purchase the nail guns from an outside supplier for $19 each and discontinue

production of nail guns internally.

With the activity level as 50,000 units, the cost of producing the nail guns internally with the old

equipment is:

Direct Material $7

_____________

Direct Labour

_________________________________

10Variable Overhead 1.90Fixed overhead (includes $2 of depreciation, $1.6 for supervision 8.60and $5 of general company overhead)

_________

Total Cost $27.50

______________

According to the manufacturer the new equipment will reduce direct labour ad variable costs by

20% Supervision costs ($80,000 per year) and direct materials per unit will not be affected by

the new equipment The new eqwpment’s capacity would be 80,000 units per year. The general

overhead will be unaffected

red

a, Assume that 50,000 units are needed for the year. State which course of action would be a

better idea? (Show calculations)

Prepared by: Charanjit Singh

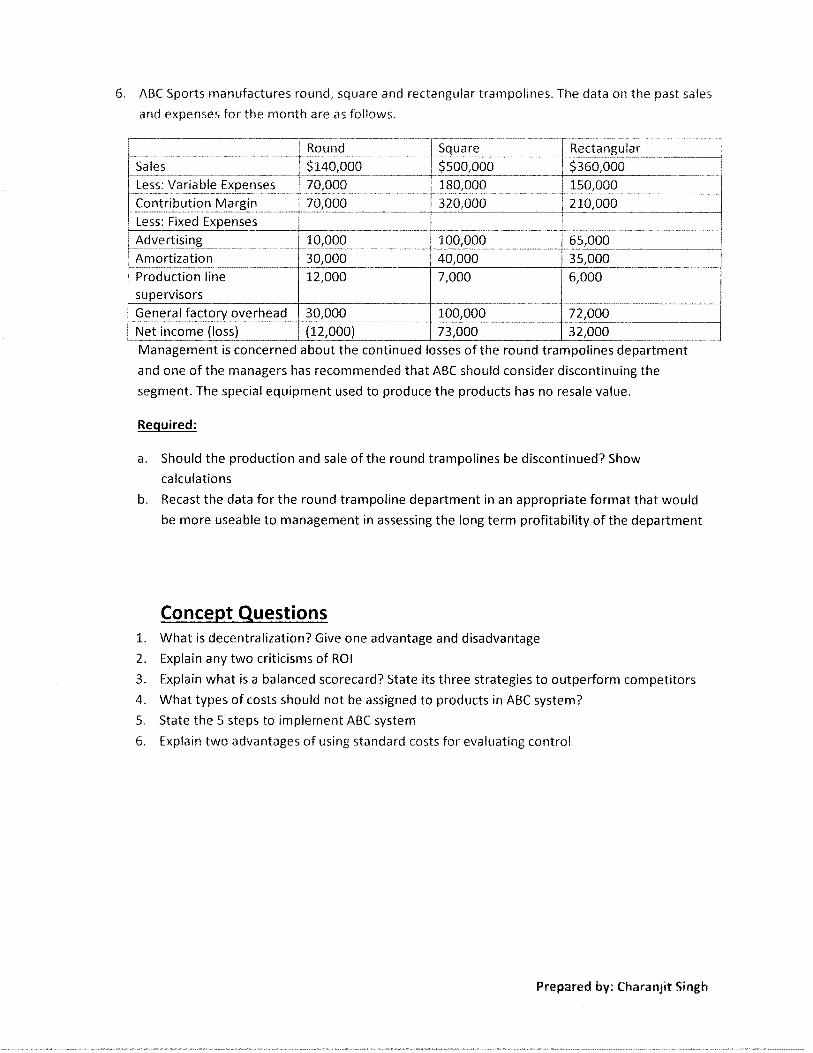

6. ABC Sports manufactures round, square and rectangular trampolines. The data on the past sales

and expenses for the month are as follows

Sales

Less: Variable Expenses

Contribution Margin

Less: Fixed Expenses

Advertising

Amortization

Production linesupervisors

General factory overhead

Rectangular

$360,000150,000

210,000

65,000

35,000

6,000

72,000

__________

32000

a. Should the production and sale of the round trampolines be discontinued? Show

calculations

b. Recast the data for the round trampoline department in an appropriate format that would

be more useable to management in assessing the long term profitability of the department

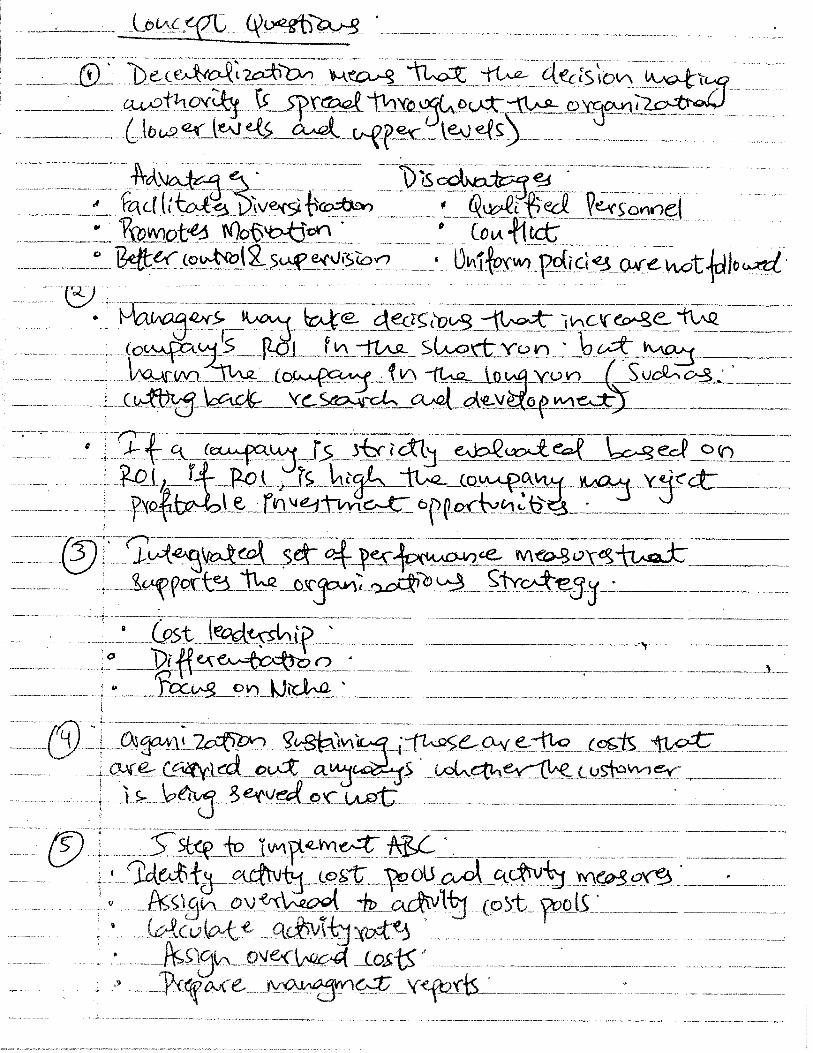

Concept Questions1. What is decentralization? Give one advantage and disadvantage

2. Explain any two criticisms of ROl

3. Explain what is a balanced scorecard? State its three strategies to outperform competitors

4. What types of costs should not be assigned to products in ABC system?

5 State the 5 steps to implement ABC system

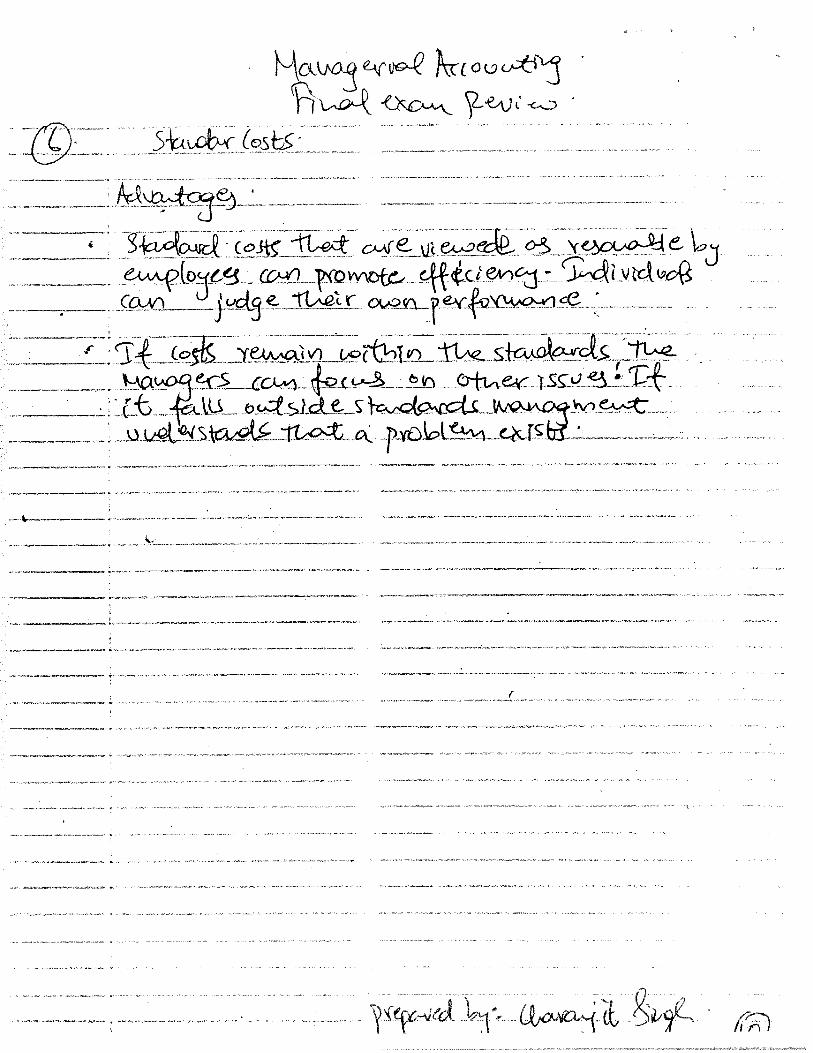

6 Explain two advantages of using standard costs for evaluating control

Round

$140,00070,000

70,000

10,000

30,000

12,000

_____Square

$500,000180,000

320,000

100,000

40,000

7,000

100,00030,000

Net income (loss) (12,000)

______

73,000

_______

Management is concerned about the continued losses of the

and one of the managers has recommended that ABC should

segment. The special equipment used to produce the products has no resale value.

Required:

round trampolines department

consider discontinuing the

Prepared by: Charanjit Smgh

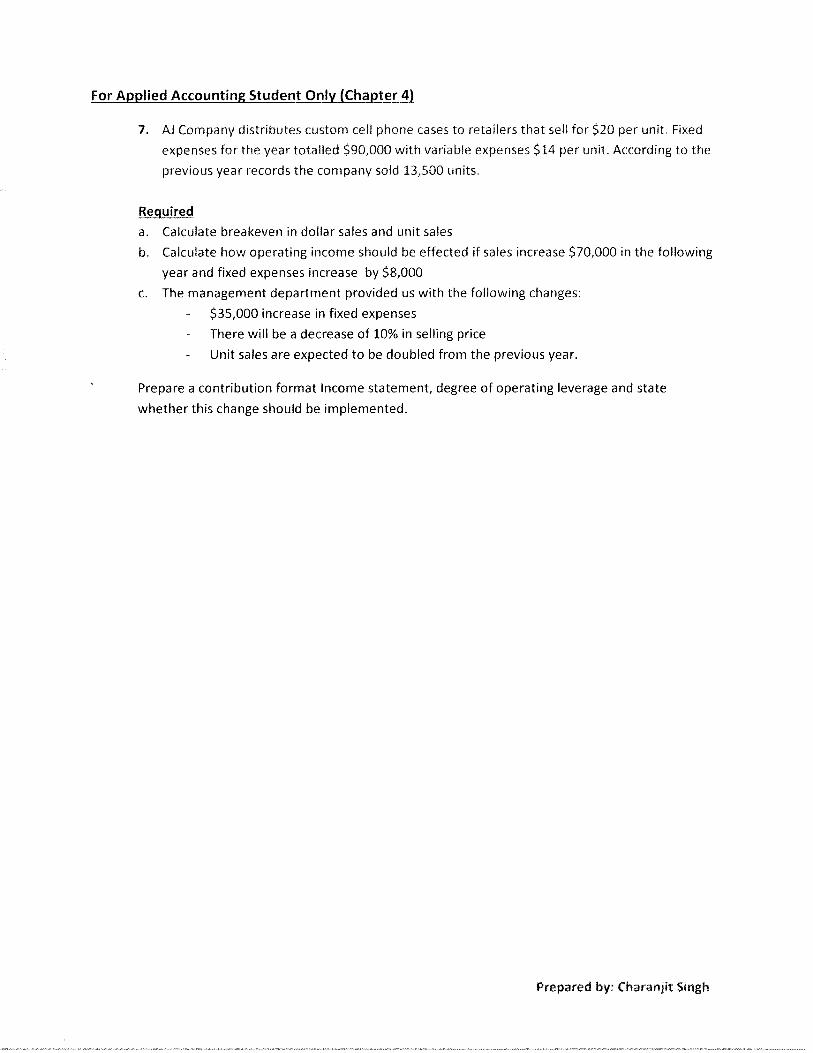

For Applied Accounting Student Only (Chapter 4)

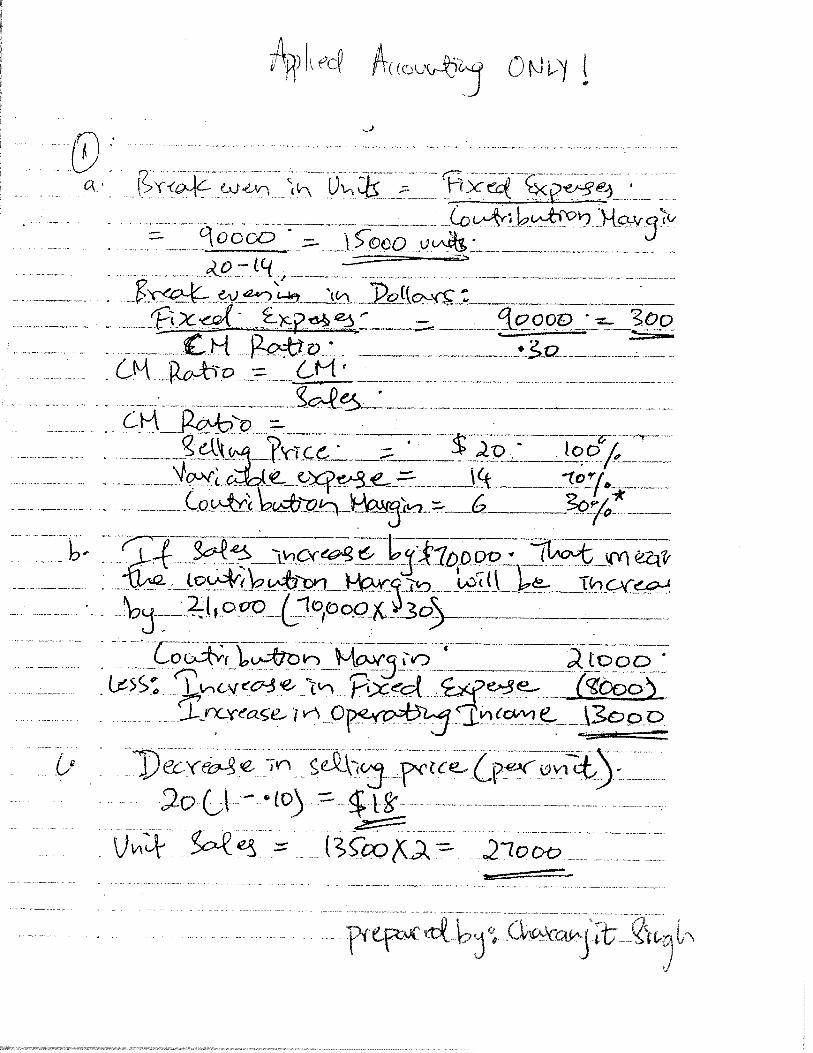

7. AJ Company distributes custom cell phone cases to retailers that sell for $20 per unit. Fixed

expenses for the year totalled $90,000 with variable expenses $14 per unit. According to the

previous year records the company sold 13,500 units.

Required

a. Calculate breakeven in dollar sales and unit sales

b. Calculate how operating income should be effected if sales increase $70,000 in the following

year and fixed expenses increase by $8,000

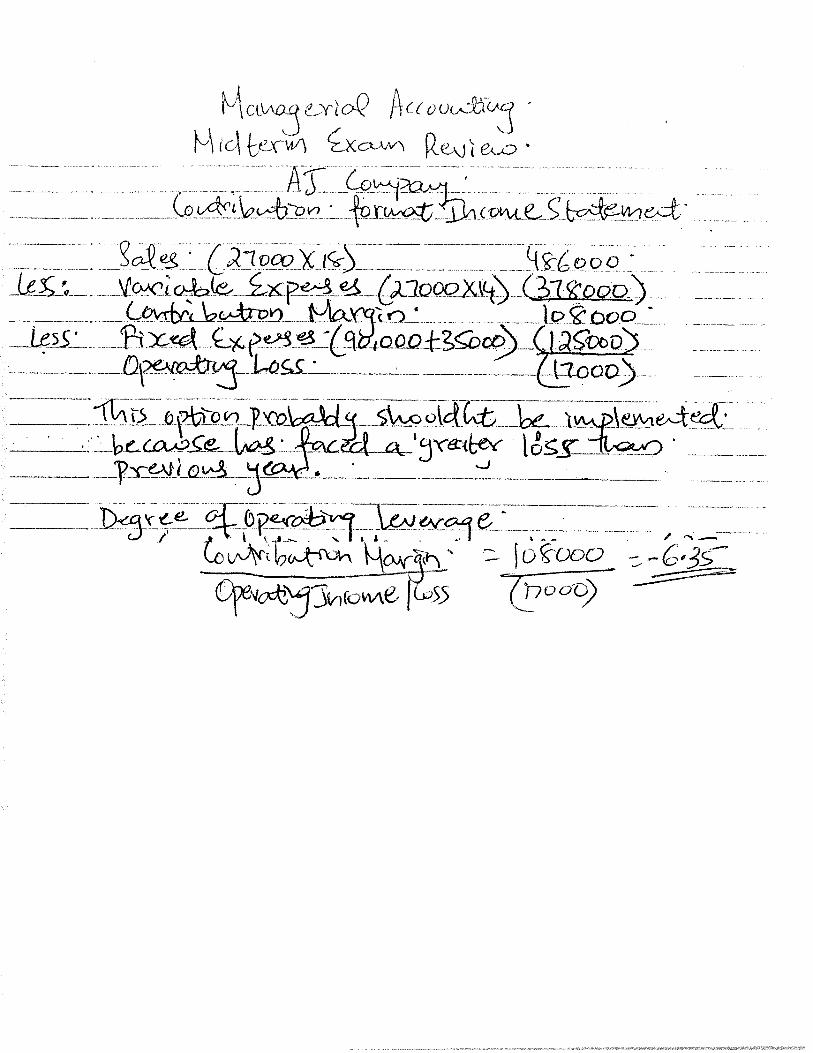

c. The management department provided us with the following changes:

- $35,000 increase in fixed expenses

- There will be a decrease of 10% in selling price

- Unit sales are expected to be doubled from the previous year.

Prepare a contribution format Income statement, degree of operating leverage and state

whether this change should be implemented.

Prepared by: Charanjit Singh

v-. o o

—2

r-

V\

_p,

-

t—.’

.——

..J

Hn

_1H

c3

Ici

H

1-iWrOç)rht\p)zi)zi

4

0--

001--

32•-.—.--

__

oo—:

-zI

z7z’jzzzzjzzzzzcJf 300tyoj

__

°or-.---—----—-

z1(sTyO3w.----——-1______-

-“-vzz:zzzzzzzzz

°

oor-ç

ooo’QO”dd

Mvec frocbj’

w) ee4D.: - -

ZccE z:zzi) _ccaj

•

___

Ci

__ _______-J ____

3,

__ _____ __ ____

zz JFWZZzzzz__

__ __

-____

J23__________

_____

LiSc LL

zz____

____ ______

iEccX2z____Jcc F_____

____tgQ_:_

EEmEE

__

•- -

•-—---•--•

-

-

o-kioc,:—

—

Aec. 0--cqo 7Z2• •- -- •-

----—--—:--

— —•—--- —— • •—-•

I

0 Qc

“il

l‘

r.\c

cçb

I

IQ

-t-

4—T

h>

<-

--

r

g (I

:)v

,-

L

•?

-p p

1t

‘

t

(acq54W

5..-QGGOl]

C*QJ5

[a’Yc]r5i.Q2P(J0J\

-c-:21-(1Z(o-8’Q1)

ci-cwJV1.1’boJ1’

.):L)

(/mosa’:vci°L°d‘‘n ‘(‘Oc

cIk7H.5Q)

fl

aoaQ

L00+

COQjc’J

oooO_5

o00Q1Q&0

oooy2.

ocooQb

°9’l

L44H1L

.as’11zZ

wr3QV

-

S2-

F

9

5

I

N

(1

0 oIo

C

I

T

€2ct tC- 4€c(S -?—. cA311oYcsOLockt

-

(ibLc

C

Z’WQt OO’-kJ

-— P4e ‘ 1)4cw, tØ()

• i

• i_I’_1L SL2ZQ-- jJY G.Z

___

-

• (cSt çct__ eçfr4C)

-__-.

cx °

__

— —-

-Lçecw e--1 cts tV

‘ Ccd cJ c cIs- ve’cu4oC

c )

4.OUGAC4J c•

__

cc,c1’ O\OQ( 4 c4.zwlt1 i)t xoiS’•, .

-• ‘‘- •-•• ‘.•• •% ‘,-•- I%.,

jc•_. -,

C(’Qc Costs - .-- --- -

j-)

11*

2

I‘I

II

4V

4V

48

V

4

44

44

:4

8j

II

•

H

C’ C,

II

iI

4

4.

_______

r,oci)

_

ooon-.2)

____

E

__

—__

o&jS

_____ __—

(QOOOO±)

--

0)

![*fiÊ 200,000 1 Okm 4 · 200,000 1 Okm 4 {51] . 200,000 10km ttaffiffi 6Èâ . Created Date: 3/14/2019 4:05:47 PM](https://img.pdfslide.us/doc/110x75/6052285d29bf7e47893e13e6/fi-200000-1-okm-4-200000-1-okm-4-51-200000-10km-ttaffiffi-6-created.jpg)