Embed Size (px)

DESCRIPTION

good

Citation preview

SNURAZANI/PB303/JUN 2012

DEFINITION

Under the Banking and Financial Institutions Act (BAFIA) 1989, a

“bank’ is defined as “a person which carries on banking business”

SNURAZANI/PB303/JUN 2012

DEFINITION

“Banking business” in turn is defined as:

“ the business of:

(i) receiving deposits on current account, deposit account, savings account or other similar account;

(ii) paying or collecting cheques drawn by or paid in by customers; and

(iii) provision of finance; or

such other business as the Central Bank, with the approval from the Minister of Finance, may prescribe”

SNURAZANI/PB303/JUN 2012

DEFINITION

The “provision of finance” under BAFIA includes:

• the lending of money

• leasing business

• factoring business

• the purchase of bills of exchange, promissory notes, certificates of deposits, debentures or other negotiable instruments and

• the acceptance of any liability, obligation or duty of any person.

SNURAZANI/PB303/JUN 2012

ROLES AND RESPONSIBILITIES

SNURAZANI/PB303/JUN 2012

To actively promote and inculcate the saving habits, especially among the younger generation. It is also an important strategy to fight unnecessary inflationary pressures on the economy of the country. Commercial banks should also make their interest rates reasonable enough to make it worthwhile for the average people to save for the financial well-being of the populace in the country. Services and facilities that have been offered by the commercial banks should be readily available at reasonable costs.

ROLES AND RESPONSIBILITIES

SNURAZANI/PB303/JUN 2012

Banks should educate the users on making the most out of the services and facilities by giving simple pep talks and publishing pamphlets and brochures, clarifying on the procedure and advantages of the various types of services and facilities available. As the financial intermediaries between the depositors and borrowers, banks have to ensure that such funds lent out are for productive and economically viable purposes and activities for the betterment of the country as a whole.

FUNCTION OF COMMERCIAL BANK

Retail banking services such as acceptance of deposits, granting of loans and advances and financial guarantees

Trade financing facilities such as letters of credit, discounting of trade bills, shipping guarantees, trust receipt and Banker’s Acceptances (BA)

Treasury services such as foreign exchanges business, money market, investment and etc.

Cross border payment services such as money transfer service, international payment facilities

Custody services such as safe deposits and share custody

SNURAZANI/PB303/JUN 2012

Commercial banks are also authorized to deal in foreign exchange i.e. to buy,

sell, borrow and lend in foreign currencies and are also the only

financial institutions allowed to provide current account facilities.

SNURAZANI/PB303/JUN 2012

Sources and Uses of Fund

Sources •Capital and reserves •Debentures and notes •Deposits of which: NIDs issued Repos •Amount due to financial institutions and BNM •Bankers acceptances

Uses •Cash1 and reserves with BNM •Amount due from financial institutions and BNM •Placement with discount houses •Marketable securities of which: Treasury bills MGS NIDs held Cagamas bonds •Investments •Loans2 of which: Trade bills

SNURAZANI/PB303/JUN 2012

CREDIT DIRECTION

Manufacturing Real estate Construction Purchase of residential properties and building Consumption credit Purchase of transport vehicle Purchase of securities

General commerce Wholesale Retail Hotel & restaurants Finance, insurance & business services Agriculture, hunting, forestry & fishing Mining & quarrying Electricity, gas & water Transport, storage & communications Trade Bill

SNURAZANI/PB303/JUN 2012

STATUTORY REQUIREMENTS AND BANK’S LIQUIDITY

The statutory reserve and liquid asset ratios are two major tools for monetary management in Malaysia. These instruments have enabled the Central Bank to control the volume of liquidity

in the banking system and, hence, credit creation in the economy.

SNURAZANI/PB303/JUN 2012

STATUTORY REQUIREMENTS AND BANK’S LIQUIDITY

•DECREASE in SRR would raise the volume of resources available to the commercial banks for granting new credit. •INCREASE in SRR will make resources available reduce and directly limit the lending capacity of commercial banks.

•INCREASING the MLR ratio will: √ reduce the level of reserves available to the banking institutions. √ decrease the lending ability of the banking institutions

•DECREASING the MLR ratio will: √ increase the level of reserves available to the banking institutions. √ increase the lending ability of the banking institutions.

SNURAZANI/PB303/JUN 2012

Local Commercial

Banks

Affin Bank Berhad

Public Bank

Berhad

Alliance Bank

Malaysia Berhad

Malayan Banking Berhad AmBank

(M) Berhad

RHB Bank Berhad

CIMB Bank

Berhad

Hong Leong Bank

Berhad

SNURAZANI/PB303/JUN 2012

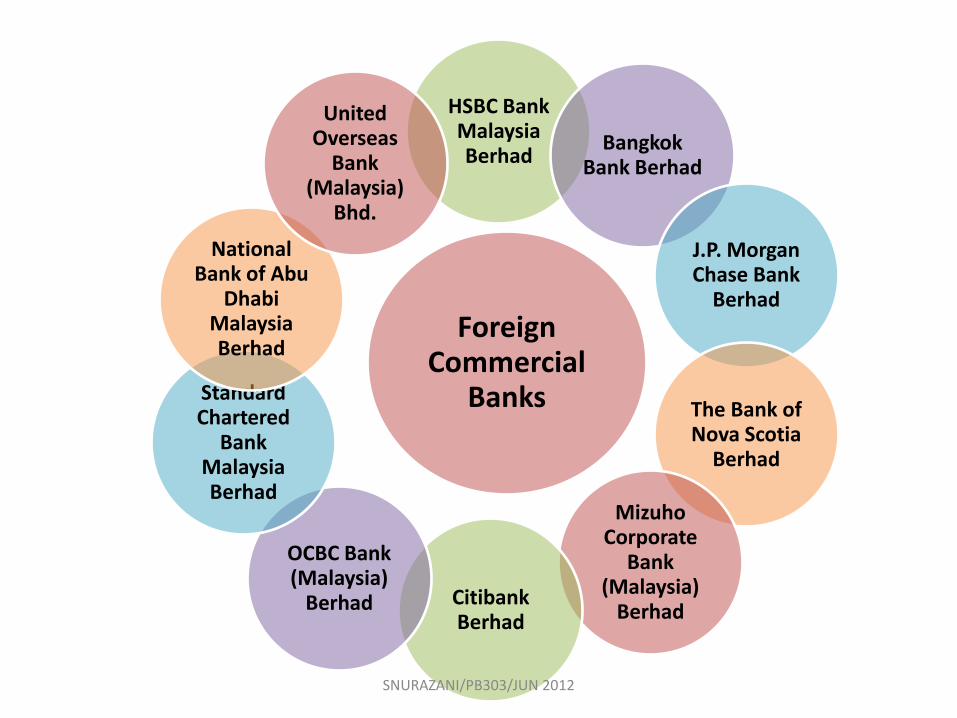

Foreign Commercial

Banks

HSBC Bank Malaysia Berhad

Bangkok Bank Berhad

J.P. Morgan Chase Bank

Berhad

The Bank of Nova Scotia

Berhad

Mizuho Corporate

Bank (Malaysia)

Berhad Citibank Berhad

OCBC Bank (Malaysia)

Berhad

Standard Chartered

Bank Malaysia Berhad

National Bank of Abu

Dhabi Malaysia Berhad

United Overseas

Bank (Malaysia)

Bhd.

SNURAZANI/PB303/JUN 2012

STATUS

REMITTANCE

LOANS & ADVANCE

DEPOSITS

FINANCIAL SERVICES

MODERN BANKING SERVICES

SNURAZANI/PB303/JUN 2012

DEPOSITS:

a. Current account

b. Savings account

c. Fixed account deposit

MONEY REMITTANCES:

a. Demand draft

b. Telegraphic transfer

c. Mail transfer

d. Standing instructions.

ADVANCE AND LOANS:

a. Overdraft

b. External cheque purchase

c. Fixed and term loans

STATUS:

a. Credit cards

b. Banker’s guarantee

c. Trust receipts

d. Enquiry status

e. Travellers’ cheques

OTHER SERVICES:

a. Share trading

b. Insurance

c. Unit trust

d. Will writing

SNURAZANI/PB303/JUN 2012

CONTINUE

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

Saving

Current

Fixed

Negotiable Certificates of Deposit (NCDs)

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

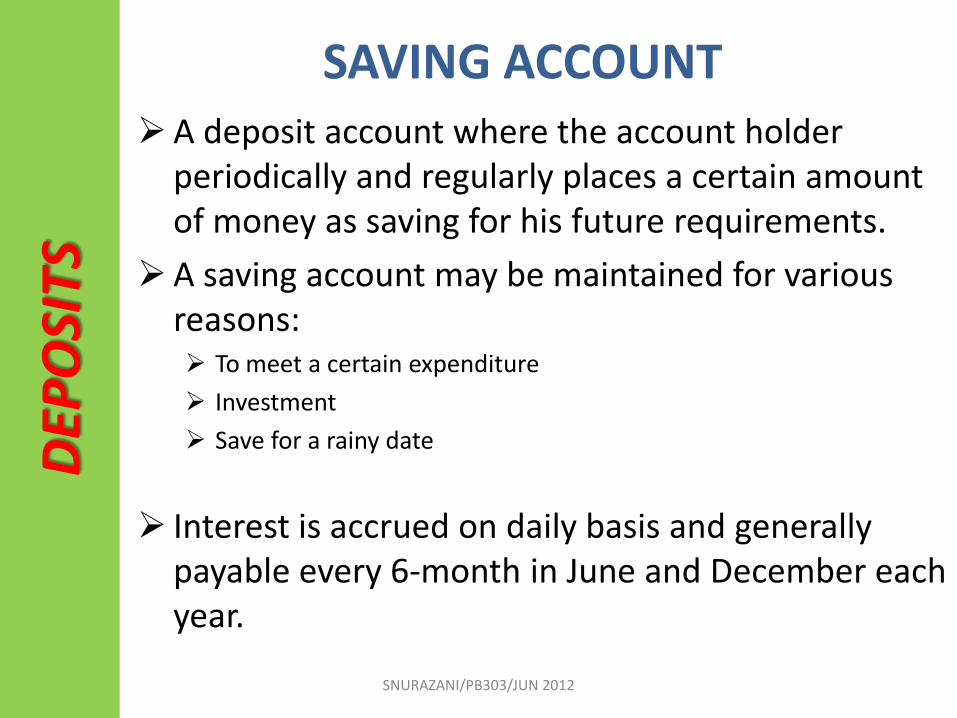

A deposit account where the account holder periodically and regularly places a certain amount of money as saving for his future requirements.

A saving account may be maintained for various reasons: To meet a certain expenditure

Investment

Save for a rainy date

Interest is accrued on daily basis and generally payable every 6-month in June and December each year.

SAVING ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

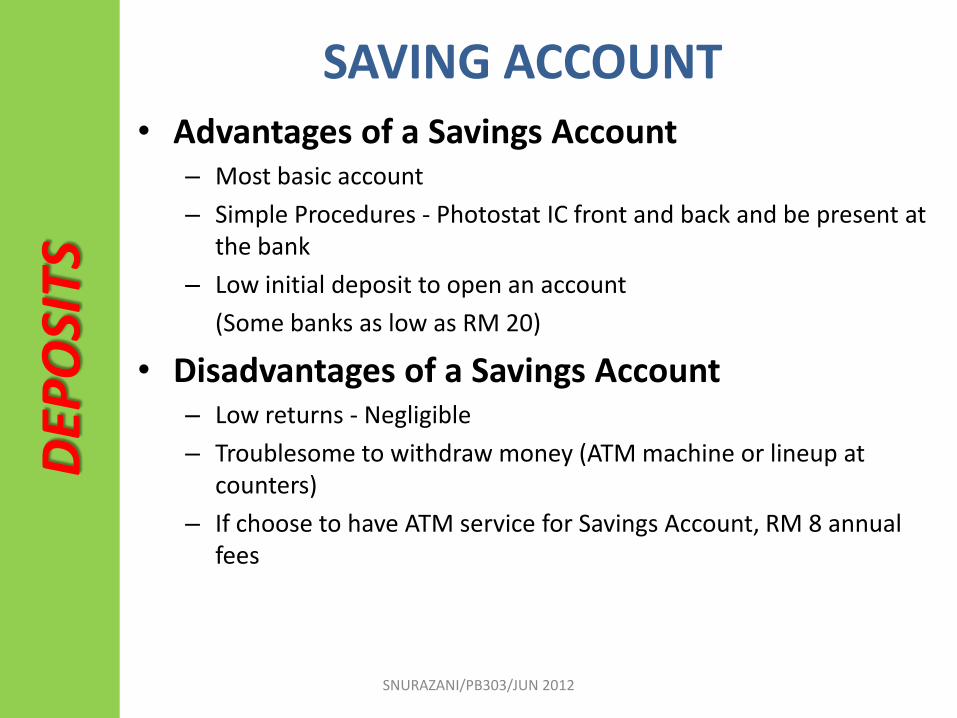

• Advantages of a Savings Account – Most basic account

– Simple Procedures - Photostat IC front and back and be present at the bank

– Low initial deposit to open an account

(Some banks as low as RM 20)

• Disadvantages of a Savings Account – Low returns - Negligible

– Troublesome to withdraw money (ATM machine or lineup at counters)

– If choose to have ATM service for Savings Account, RM 8 annual fees

SAVING ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• Example: CIMB

– Eligibility:

• Individuals aged 18 years and above who are either residents or non-residents.

• Joint account is allowed.

– Requirements:

• Minimum opening deposit of RM20.NRIC or passport.

• A copy of utility bill for verification of address.

SAVING ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

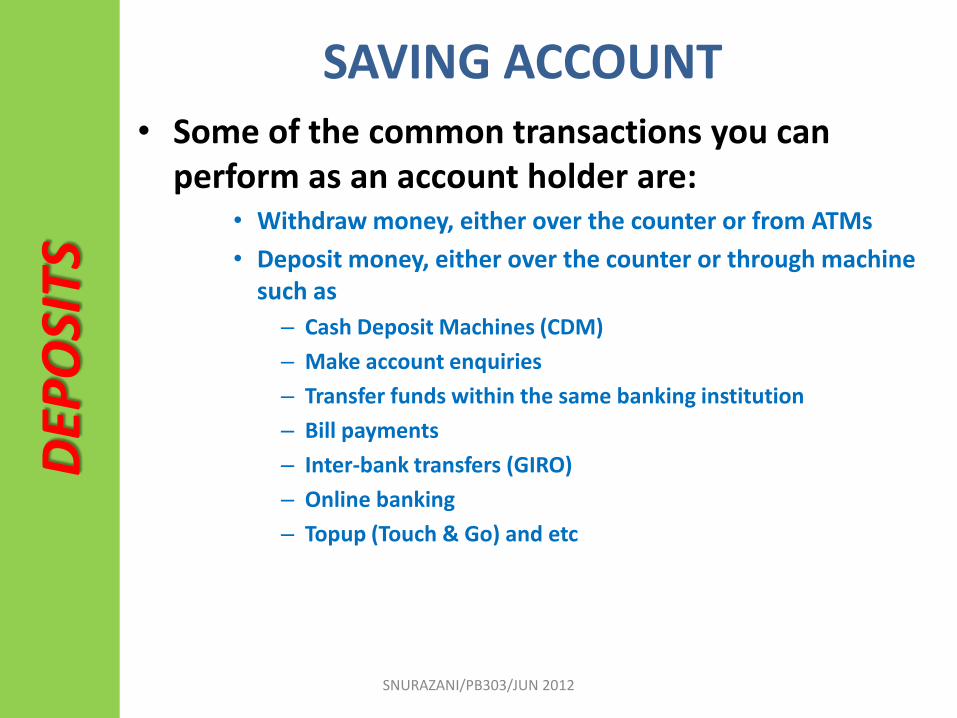

• Some of the common transactions you can perform as an account holder are:

• Withdraw money, either over the counter or from ATMs

• Deposit money, either over the counter or through machine such as

– Cash Deposit Machines (CDM)

– Make account enquiries

– Transfer funds within the same banking institution

– Bill payments

– Inter-bank transfers (GIRO)

– Online banking

– Topup (Touch & Go) and etc

SAVING ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• A form of working account and is operated through the used of cheques.

• When a current account is opened, the customer is regularly issued with a cheuqe book, containing a certain amount of cheque leaves. – If you have high payment volumes every month, an account that

comes with a chequebook will make things a lot easier.

– Just write a cheque for each transaction you need to make and send them off. Some current accounts even pay interest or hibah (profit) if you maintain a balance, so they are as good as savings accounts.

– This means you only need one account instead of multiple ones. An overdraft facility can also be added to your current account if you need additional funds.

CURRENT ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• Different banks have different criteria for opening a current account. Generally, banks would only consider the application if the applicant is:

– 18 years old or above

– not a bankrupt

– of sound mind and has the mental and physical capacity to operate the account properly

• For business owners and professional entities, they must ensure that they are properly registered with the relevant authorities.

• However, a bank has the discretion to accept or decline an application to open the account.

CURRENT ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• A cheque is an instrument in writing issued by the customer to his banker to pay out a certain sum of money against the available balance standing to the credit of his account.

– If balance insufficient, the banker may return the cheque with the answer REFER TO DRAWER.

– Banker may offer the customer to do overdraft.

• In the case of stop payment, customer may writing to the banker to not to pay the cheque and then the cheque will be return with the answer PAYMENT STOPPED or PAYMENT COUNTERMANDED.

CURRENT ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• Is the form of investment or deposit account where a certain sum of money is placed with a bank for a fixed period of time to earn interest.

• The interest rate is higher compare to saving accounts.

• Interest is normally paid on the maturity date.

• Protected from interest rate fluctuations

• An amount may be placed on fixed deposit for 1, 3, 6, 9, 12, 15, 18, 24, 36, 48 and 60 months to earn interest at a fixed rate.

• In the case of fixed deposits for various periods from 1 month to 12 months, banks may quote appropriate interest rates. The respective interest rates quoted by an individual bank however, are required to be prominently displayed in a special display board within bank premises.

FIXED ACCOUNT

SNURAZANI/PB303/JUN 2012

DEP

OSI

TS

• The rates for fixed deposits for periods exceeding 12 months are negotiable.

• Banks are not required to display, publish or announce the interest rates on deposits for more than 12 months.

• - As compared to a savings account, generally the interest rate payable on a fixed deposit account is higher.

• According to the Rules of the Association of Banks in Malaysia (ABM) – no interest will be paid on one month fixed deposit which is

uplifted before maturity.

FIXED ACCOUNT

SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E Demand Draft

Telegraphic Transfer

Mail Transfer

Standing Instruction

SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E DEMAND DRAFT

•It is a payment order in writing issued by an issuing bank to a payee bank to pay on demand the sum stated in the draft and to the order of the person specified on the draft.

•A local draft in Malaysia is drawn in Malaysian Ringgit.

•A foreign draft is usually drawn in a foreign currency on an overseas branch or foreign correspondent bank.

•Example: You are based in Johor, your son is studying in KL. You need to remit him of RM2000. You may purchase demand draft from your bank and remit it to your son. Your son should be able to receive the payment from the drawee bank upon the presentation of demand draft.

SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E DEMAND DRAFT

A Demand Draft or bank draft is a cheque drawn by a bank on its Head Office, on a branch or on another bank for payment outside the local area, either domestically or abroad. Features and Benefits: •Transferring funds within and outside the country. •If funds are to be sent abroad, the draft is drawn on a bank in a foreign country in the appropriate currency. •Demand Draft is paid for by the customer at the time of issue. The customer sends the draft to the payee who presents it at the drawee bank for payment. •Types of Demand Draft:- Local Demand Draft (RM). •Foreign Demand Draft (foreign currency). SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E TELEGRAPHIC TRANSFER

•Wire your money in a safe and quick mode of transfer to anyone and anywhere around the world.

•Also known as “telephonic transfer”

•Where the beneficiary requires the money urgently, it is possible to request the bank to effect the payment by using this instrument.

•The remitting bank will instruct its correspondent bank (branch) to make the payment.

•It make the couple of days to be transferred. •Based in overseas: within 5 days •Based on local: within same day SNURAZANI/PB303/JUN 2012

REMITER IN MALAYSIA REMITTING BANK IN MALAYSIA

BENEFICIARY IN SYDNEY BRANCH/CORRESPONDEN

T BANK IN SYDNEY

STEP 1

STEP 2

STEP 4

STEP 3

Completes application to

request his bank to remit the required

payment

Instruct by telex, telephone or SWIFT to settle payment

Notifies beneficiary of the remittance and

to collect payment

Notifies beneficiary of the remittance

SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E

• Similar to TT, but transaction is done by mail.

• When you are too busy, you may request the bank to remit the payment on your behalf. – You have to fill in the full name, address and telephone

number of the beneficiary.

– The bank will write to its correspondent bank/ branch to make the payment

MAIL TRANSFER

SNURAZANI/PB303/JUN 2012

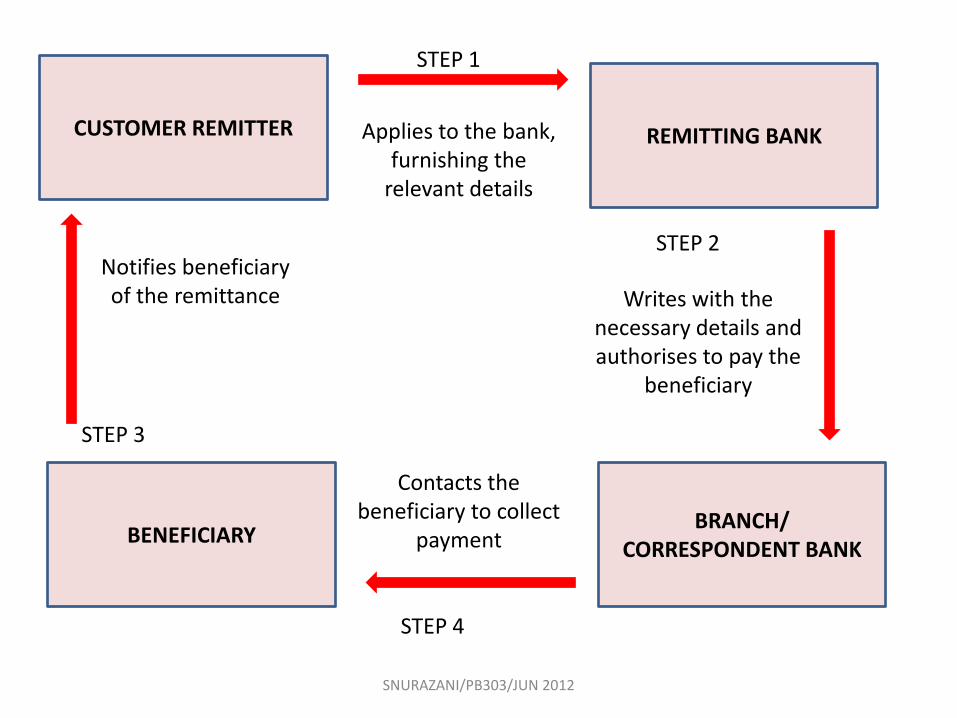

CUSTOMER REMITTER REMITTING BANK

BENEFICIARY BRANCH/

CORRESPONDENT BANK

STEP 1

STEP 2

STEP 4

STEP 3

Applies to the bank, furnishing the

relevant details

Writes with the necessary details and authorises to pay the

beneficiary

Contacts the beneficiary to collect

payment

Notifies beneficiary of the remittance

SNURAZANI/PB303/JUN 2012

REM

ITTA

NC

E • Also known as Standing Order

• Appropriate when a person has to make periodic payment i.e insurance premium, monthly installment of car/house and so on.

• It is possible for the periodically payment to be made by the issuing standing order from the bank .

STANDING INSTRUCTION

SNURAZANI/PB303/JUN 2012

STA

TUS

Credit Cards

Bankers Guarantee

Trust Receipt

Status Enquiry

Travellers’ Cheques

SNURAZANI/PB303/JUN 2012

STA

TUS

Master and Visa are two key players for credit cards. Most credit cards are issued by commercial banks. Credit cards are issued after an account has been approved by the credit provider.

If the cardholder uses the credit card for purchases goods or services from merchant, the transaction process overview is illustrated as follows:

i) The merchant will submit the ticket electronically to the

bank for payment, via the clearing and settlement systems;

ii) The bank credits the merchant for deposits;

iii) The bank issues bills to the cardholder; and

iv) The cardholder repays the bank for the goods or services originally purchased from the merchant.

Apart from the above, the cardholder can also take cash advance from the car.

CREDIT CARDS

SNURAZANI/PB303/JUN 2012

STA

TUS

A credit card enables its holder to buy goods and services with a credit

line given by credit card issuer and the amount will be settled at a later date.

Cardholders are billed on a monthly basis and cardholders would have to bear finance charges (interest) on the outstanding amount if full payment is not made by the due date. For a hefty fee, a credit card can also be used for cash advances at Automated Teller Machines (ATMs) and at respective credit card issuers' counters.

The government is imposing a service tax of RM 50 for each principal credit card and RM 25 for each supplementary card. ans.

CREDIT CARDS

SNURAZANI/PB303/JUN 2012

STA

TUS

A banker’s acceptance (commonly referred to as BA) is a usance bill of exchange drawn by the customer in Ringgit to finance an underlying genuine trade transaction that is accepted by his banker and payable on a specified future date.

BA can be used for domestic trade i.e. financing the buyer or seller of goods or import and export businesses. In its basic form, BA financing involves three basic steps:

a. The customer draws a bill of exchange on a bank

b. The bank accepts the bill of exchange.

c. The bank, at the request of the customer, discounts the accepted bill, thereby

advancing the discounted proceeds to the customer.

BANKER GUARANTEE

SNURAZANI/PB303/JUN 2012

STA

TUS

SALIENT FEATURES OF BA’S

The following are the salient features of BAs:

a. It is payable in Ringgit to the order of the drawer;

b. The tenor is at least 30 days but not later than 200 days from the date of

acceptance;

c. The minimum amount is RM30,000.00;

d. The facility is available for the purpose of financing a genuine commercial or

trade and certain service transactions;

e. In order to facilitate financing of smaller trade transactions, the grouping of

two or more trade transactions is permissible, i.e. bunching is allowed;

f. Extending or creating a new BA to retire an old BA is prohibited;

g. It is payable at the head office of a bank or investment bank in Kuala Lumpur

h. It is enfaced with a statement that is drawn to finance the purchase/sales of

goods, import as well as export of goods. BNM issued a BA guidelines to

describe the detailed procedure on financing under BA.

For more details, check www.bnm.gov.my.

BANKER GUARANTEE

SNURAZANI/PB303/JUN 2012

STA

TUS

Trust receipts (commonly referred to as TRs) are granted by a bank to finance domestic trade or the import of goods on behalf of the customer.

A trust receipt is a document executed by a customer, whereby he undertakes to: a. Take possession of the goods and hold it in trust for the bank,

b. Account for the goods at all times, and

c. Sell the goods and apply the proceeds thereof to settle the TR

outstanding amount plus interest to the bank, normally within a

specified period, e.g. 60, 90 or 120 days.

TRUST RECEIPT

SNURAZANI/PB303/JUN 2012

STA

TUS

Is the request for a banker's opinion or report, particularly regarding the financial standing of customers.

Its provided by banks to their customers

STATUS ENQUIRY

SNURAZANI/PB303/JUN 2012

STA

TUS

Traveler’s cheques are cheque issued by financial institutions such as American Express, Thomas Cook, Barclay Bank etc. to facilitate travel arrangements.

They are issued in various currencies, likes US dollars, sterling pound, Japanese Yen, Hong Kong dollars, Singapore dollars and in various denominations.

Traveler’s cheque has no life span i.e. it is not subjected to unclaimed moneys Act 1965 of Malaysia as in the case of current, fixed deposits and remittances.

Traveler’s cheques are easily obtainable from the Malaysian banks by anyone who wishes to travel abroad.

The issuer guarantees replacement if the traveler’s cheques are reported lost or stolen.

They are convenient & safer means as a traveler does not have to bother carrying large sums of foreign currencies each time he/she has to travel abroad either for pleasure or for business.

TRAVELER”S CHEQUEU

SNURAZANI/PB303/JUN 2012

LOA

NS

& A

DV

AN

CE

Overdraft

External Cheques Purchase

Term & Fixed Loan

SNURAZANI/PB303/JUN 2012

LOA

NS

& A

DV

AN

CE • An advance or facility granted under a current account

whereby the customer is authorised to draw on the account up to an approved limit.

• Overdraft facility is normally extended to customers to finance working capital or short terms transactions.

• Interest is charged only on the utilised portion of the overdraft limit. However, a commitment fee is levied on unutilised overdraft facilities.

OVERDRAFT

SNURAZANI/PB303/JUN 2012

LOA

NS

& A

DV

AN

CE • Are those which are drawn on banks outside the ‘clearing area’ of the

bank at which the cheques are deposited for clearing.

• Normally banks take a few days to clear outstation or outport cheques, depending on the locality of the drawee (paying) bank in relation to the collecting bank.

• However, the businessman needs to use the proceeds of the various cheques even before the said cheques are cleared in order to improve his cash flow or liquidity requirements.

EXTERNAL CHEQUE PURCHASE

SNURAZANI/PB303/JUN 2012

LOA

NS

& A

DV

AN

CE A facility amortized over a fixed period, with repayment

structured as repayable as monthly, quarterly, semi-annually or annually.

With this structure, each repayment consists of loan principal and interest.

The repayment can also be structured as balloon or bullet payment.

In this case, each repayment consists if only interest and principal to be repaid in one lump sum at the end of loan period.

A fixed loan is commonly usually used to finance CAPEX

Personal loan, housing loan, car loan.

TERM & FIXED LOAN

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

Units Trust

Share Trading

Insurance

Will Writing

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

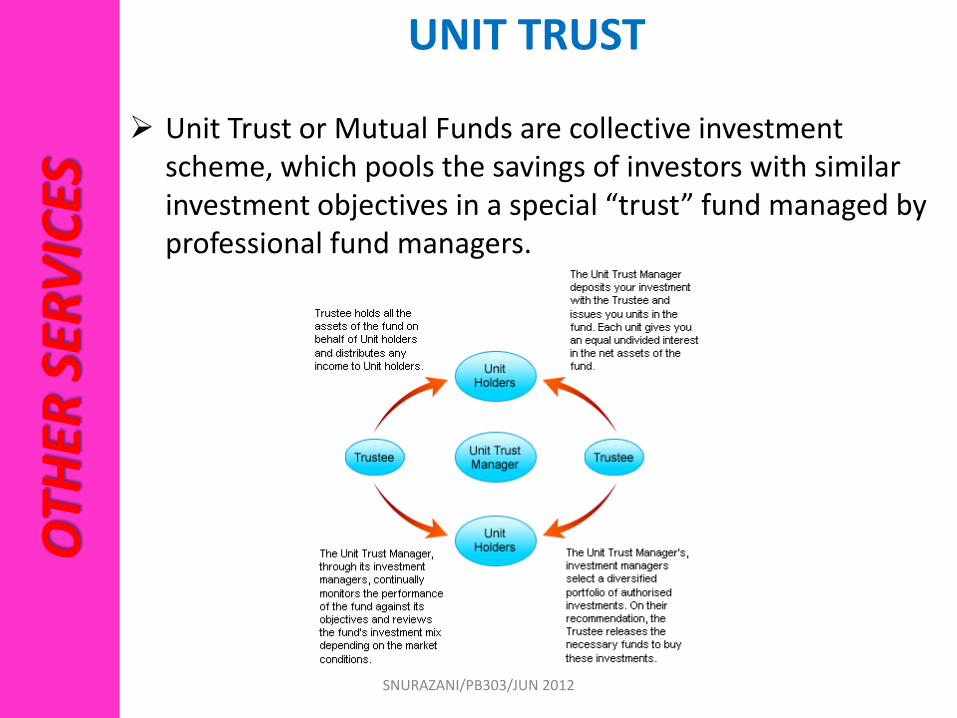

Unit Trust or Mutual Funds are collective investment scheme, which pools the savings of investors with similar investment objectives in a special “trust” fund managed by professional fund managers.

UNIT TRUST

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

The unit trust fund will invest in equities, fixed income securities and other assets authorised under the Guidelines.

Example: Am Mutual

Affin Fund

Public Mutual

Pacific Mutual

UNIT TRUST

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

• Will and Wasiat Writing Services are legally effective arrangements to ensure the disposition of assets in accordance to ones' personal wishes. It helps to smoothen the process of estate administration and distribution.

• Will/ Wasiat- A legally binding document by which an individual signifies his/her wishes as to the distribution of his/her estate upon death.

WILL WRITING

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

• Insurance is the equitable transfer of the risk of a loss, from one entity to another in exchange for payment. It is a form of risk management primarily used to hedge against the risk of a contingent, uncertain loss.

• An insurer, or insurance carrier, is a company selling the insurance; the insured, or policyholder, is the person or entity buying the insurance policy. The amount to be charged for a certain amount of insurance coverage is called the premium.

• Ex: Life Insurance, General Motor Insurance etc

INSURANCE

SNURAZANI/PB303/JUN 2012

OTH

ER S

ERV

ICES

• A share investing facility that allows you to purchase shares quoted on Bursa Malaysia using your own funds or via a Share Margin Financing scheme.

• Example:

Maybank Share Trading Minimum Financing Amount RM50,000.

SHARE TRADING

SNURAZANI/PB303/JUN 2012

CONGRATULATIONS!!!

You Have Completed Topic Commercial Bank

SNURAZANI/PB303/JUN 2012

![60053027 manual-del-instructor-tren-de-fuerza-tractores-130104175530-phpapp01[1] copy](https://img.pdfslide.us/doc/110x75/55b5251cbb61eb53188b466e/60053027-manual-del-instructor-tren-de-fuerza-tractores-130104175530-phpapp011-copy.jpg)