Embed Size (px)

Citation preview

BUSINESS

SCHOOL

Topic Seven: Risk and Return

Evelyn Lai

This lecture

› In this lecture, we will cover the following:

- Calculate realised and expected rates of return and risk for

individual assets

- Calculate the risk and return of portfolios

- Examine the components of total risk

›Readings: BMA Chapter 7

BUSINESS

SCHOOL

Risk and Return Calculations

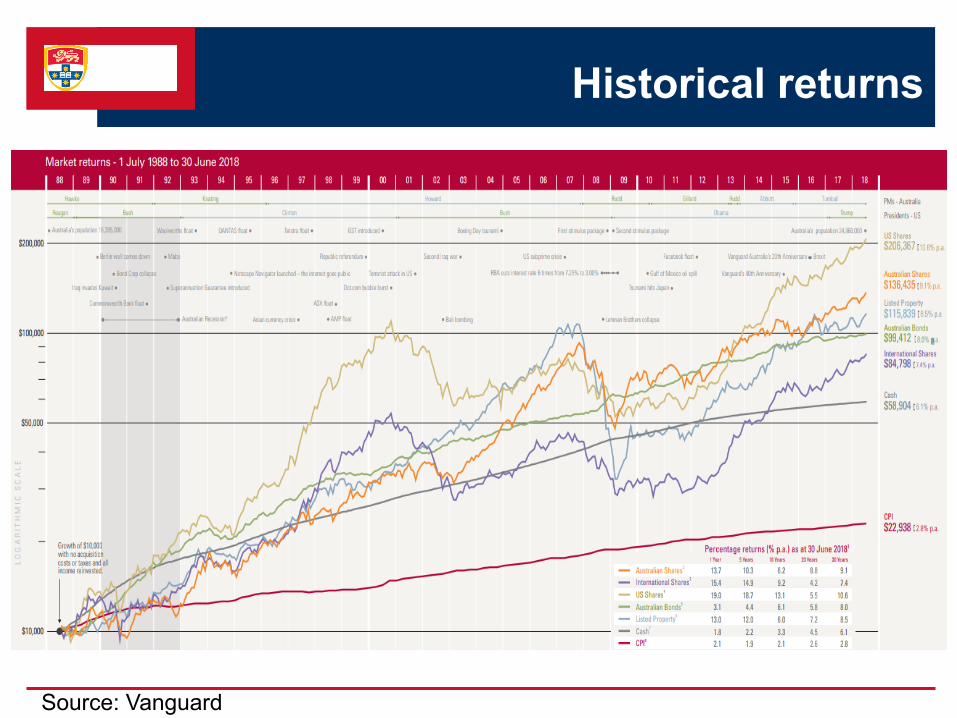

Historical returns

Source: Vanguard

Realised returns

› Realised return or cash return measures the gain or loss on

an investment.

11 )( ReturnCash

Stream IncomeGain CapitalReturnCash

ttt DivPP

Rate of return

› The rate of return is simply the cash return divided by the

beginning asset price.

t

ttt

t

tttt

P

DivP R

P

Div)P(P R

111

111

ln

Yield DividendYieldGain CapitalReturn of Rate

Price inningReturn/BegCash Return of Rate

Example

You invested in 1 share of Macquarie Group (MQG)

for $95 and sold a year later for $200. The company

did not pay any dividend during that period. What will

be the cash return on this investment? What is the

rate of return? How would these change if the

company paid a $10 dividend at the end of the

period?

_____________________________________________________

Rate of return

1. Expected return and risk – Historical time series

› Expected or mean return is what the investor expects to

earn from an investment in the future.

› The expected return is the arithmetic average of actual

returns over a specific period.

n

t

tn r

nn

rrrrrE

1

21 1)...()(

1. Expected return and risk – Historical time series

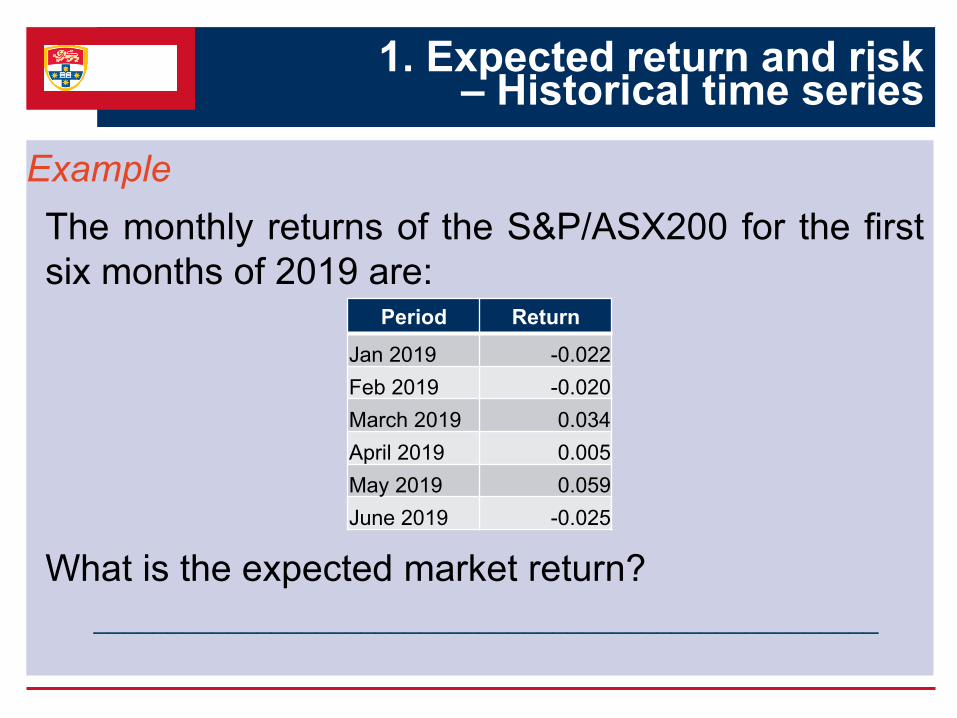

Example

The monthly returns of the S&P/ASX200 for the first

six months of 2019 are:

What is the expected market return?

_____________________________________________________

Period Return

Jan 2019 -0.022

Feb 2019 -0.020

March 2019 0.034

April 2019 0.005

May 2019 0.059

June 2019 -0.025

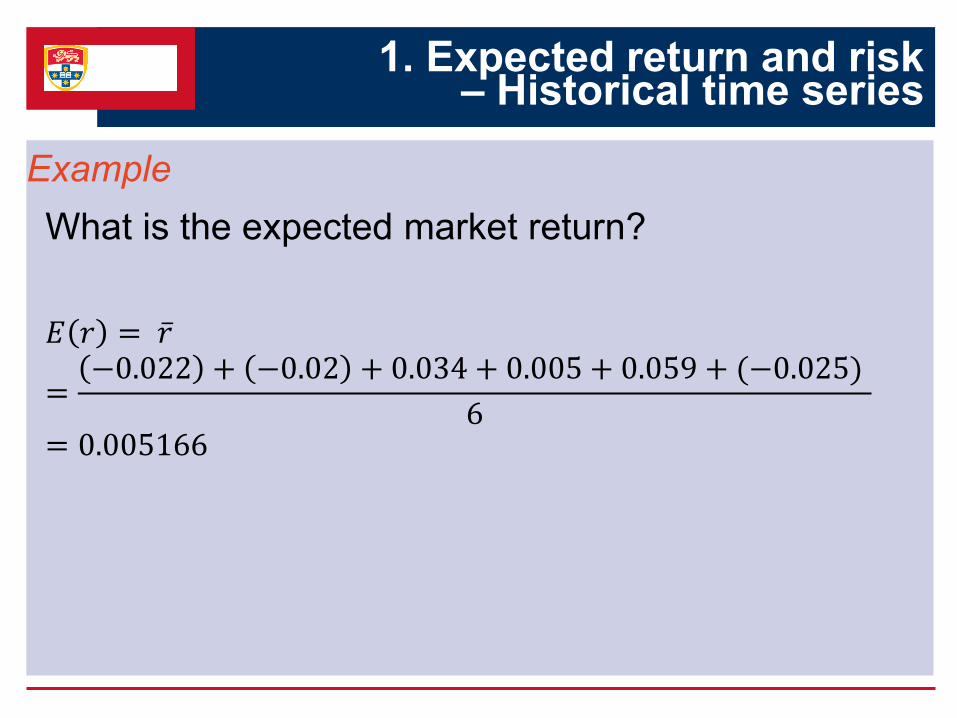

1. Expected return and risk – Historical time series

Example

What is the expected market return?

𝐸 𝑟 = 𝑟

=−0.022 + −0.02 + 0.034 + 0.005 + 0.059 + (−0.025)

6= 0.005166

Geometric vs arithmetic average rates of return

› The arithmetic average rate of return answers the question,

“What was the average of the rates of return per period?”

› The geometric or compound average rate of return answers

the question, “What was the growth rate of your investment?”

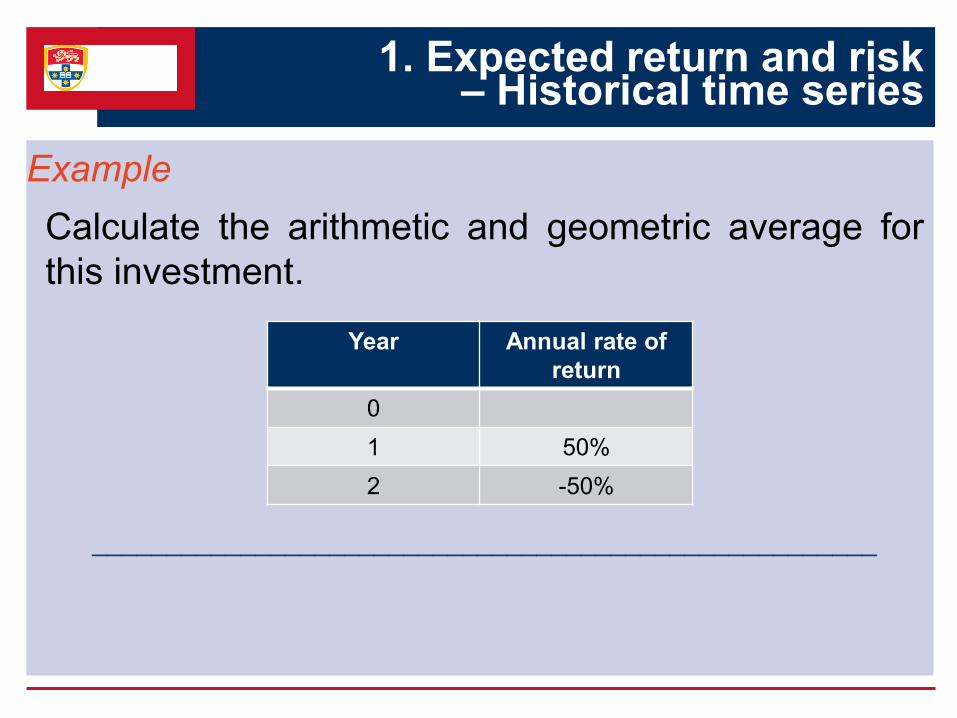

1. Expected return and risk – Historical time series

Example

Calculate the arithmetic and geometric average for

this investment.

_____________________________________________________

Year Annual rate of

return

0

1 50%

2 -50%

1. Expected return and risk – Historical time series

Example

I am considering investing in the S&P500 total returns index. I

would like to save $3 million over 30 years. How much would I

need to contribute each year to reach this goal? What

difference does arithmetic and geometric averages make?

_____________________________________________________2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

S&P500 Total Returns 28.7 10.9 4.9 15.8 5.5 -37 -9.2 15.1 2.1 15.8 32.4 13.7 1.4 -22.1 -11.9 26.5

-40

-30

-20

-10

0

10

20

30

40

Retu

rns (

%)

1. Expected return and risk – Historical time series

› Total risk is the extent to which payoffs on an asset are

expected to vary from their average or expected value.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

01-J

ul-9

2

01-F

eb

-93

01-S

ep

-93

01-A

pr-

94

01-N

ov-9

4

01-J

un-9

5

01-J

an-9

6

01-A

ug

-96

01-M

ar-

97

01-O

ct-

97

01-M

ay-9

8

01-D

ec-9

8

01-J

ul-9

9

01-F

eb

-00

01-S

ep

-00

01-A

pr-

01

01-N

ov-0

1

01-J

un-0

2

01-J

an-0

3

01-A

ug

-03

01-M

ar-

04

01-O

ct-

04

01-M

ay-0

5

01-D

ec-0

5

01-J

ul-0

6

01-F

eb

-07

01-S

ep

-07

01-A

pr-

08

01-N

ov-0

8

01-J

un-0

9

01-J

an-1

0

01-A

ug

-10

01-M

ar-

11

01-O

ct-

11

01-M

ay-1

2

01-D

ec-1

2

01-J

ul-1

3

01-F

eb

-14

01-S

ep

-14

01-A

pr-

15

01-N

ov-1

5

01-J

un-1

6

01-J

an-1

7

01-A

ug

-17

01-M

ar-

18

01-O

ct-

18

01-M

ay-1

9

Commonwealth Bank of Australia (CBA)

Monthly Returns Average Return (0.910%)

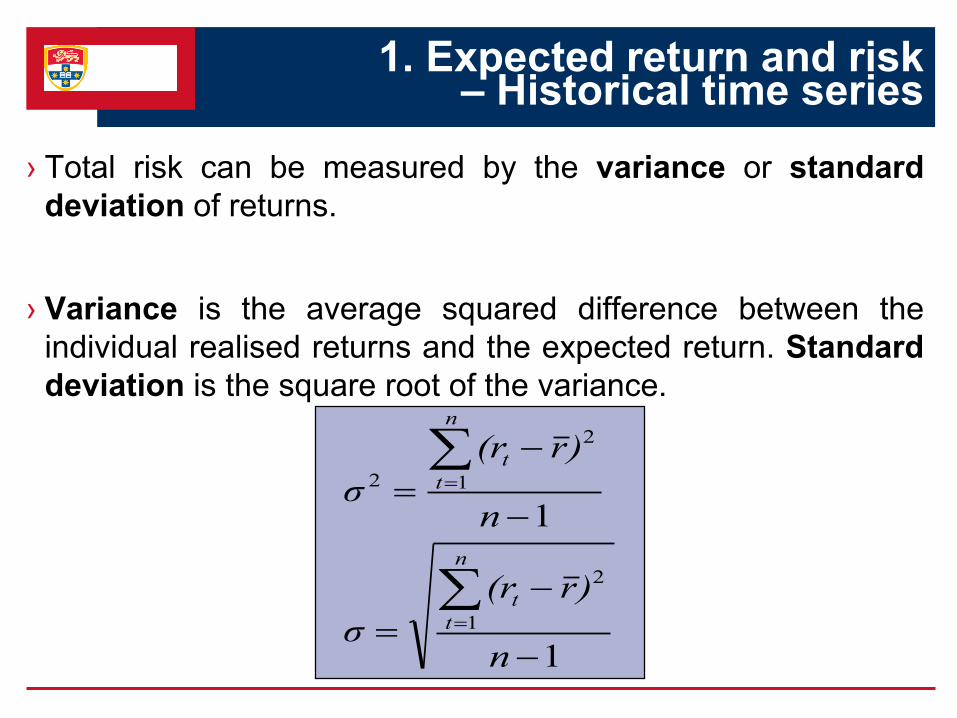

1. Expected return and risk – Historical time series

› Total risk can be measured by the variance or standard

deviation of returns.

› Variance is the average squared difference between the

individual realised returns and the expected return. Standard

deviation is the square root of the variance.

1

1

1

2

1

2

2

n

)r(r

σ

n

)r(r

σ

n

t

t

n

t

t

1. Expected return and risk – Historical time series

Example

The monthly returns of the S&P/ASX200 for the first

six months of 2019 are:

What is the risk of this market index?

_____________________________________________________

Period Return

Jan 2019 -0.022

Feb 2019 -0.020

March 2019 0.034

April 2019 0.005

May 2019 0.059

June 2019 -0.025

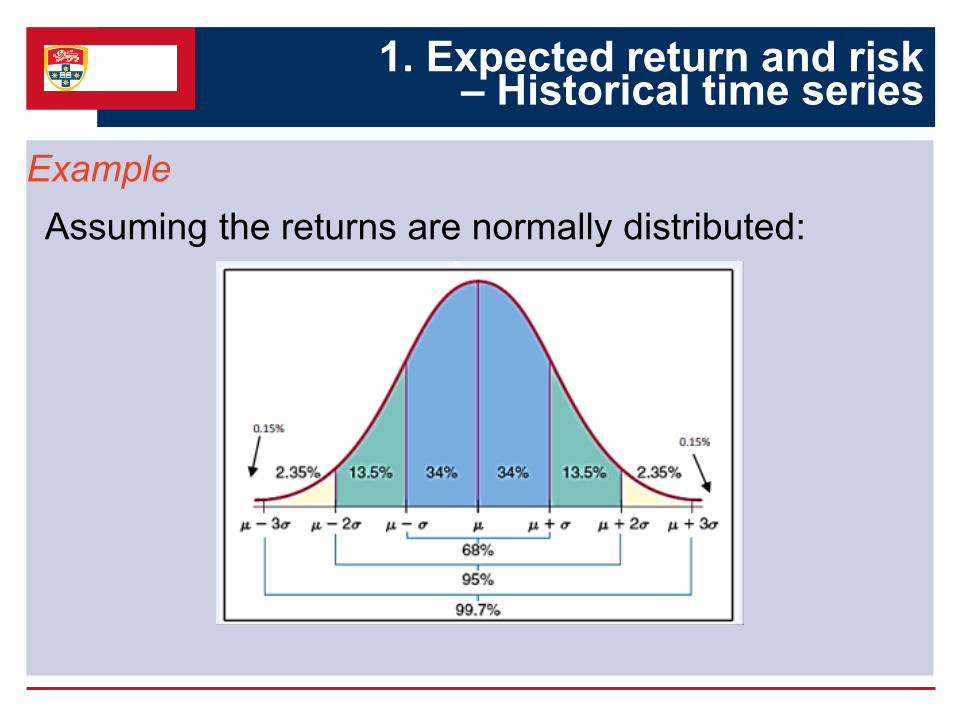

1. Expected return and risk – Historical time series

Example

Assuming the returns are normally distributed:

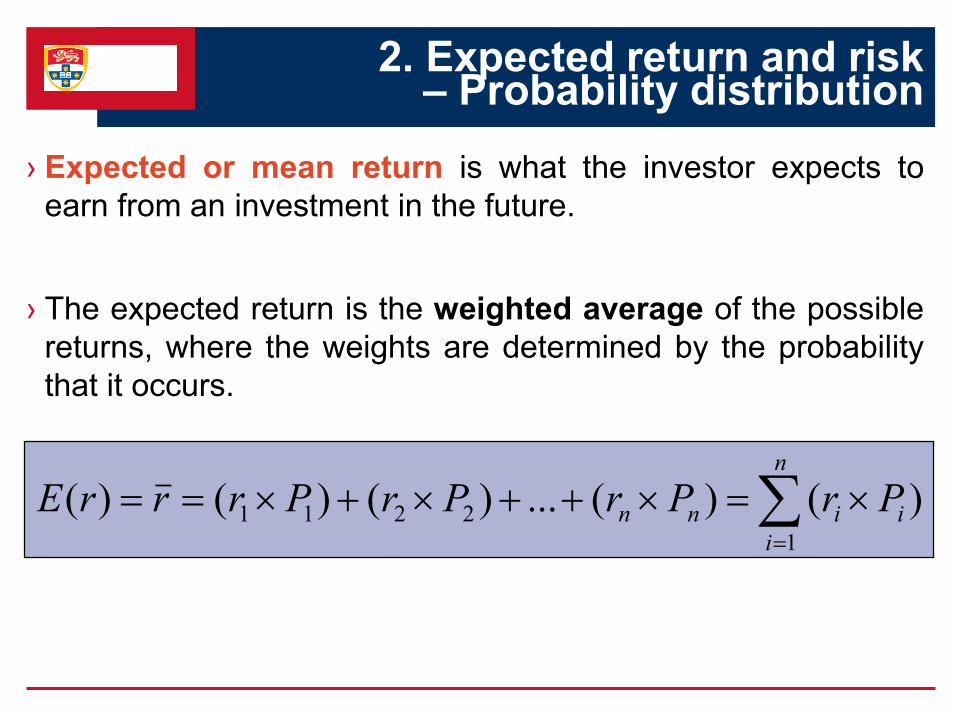

2. Expected return and risk – Probability distribution

› Expected or mean return is what the investor expects to

earn from an investment in the future.

› The expected return is the weighted average of the possible

returns, where the weights are determined by the probability

that it occurs.

n

i

iinn PrPrPrPrrrE1

2211 )()(...)()()(

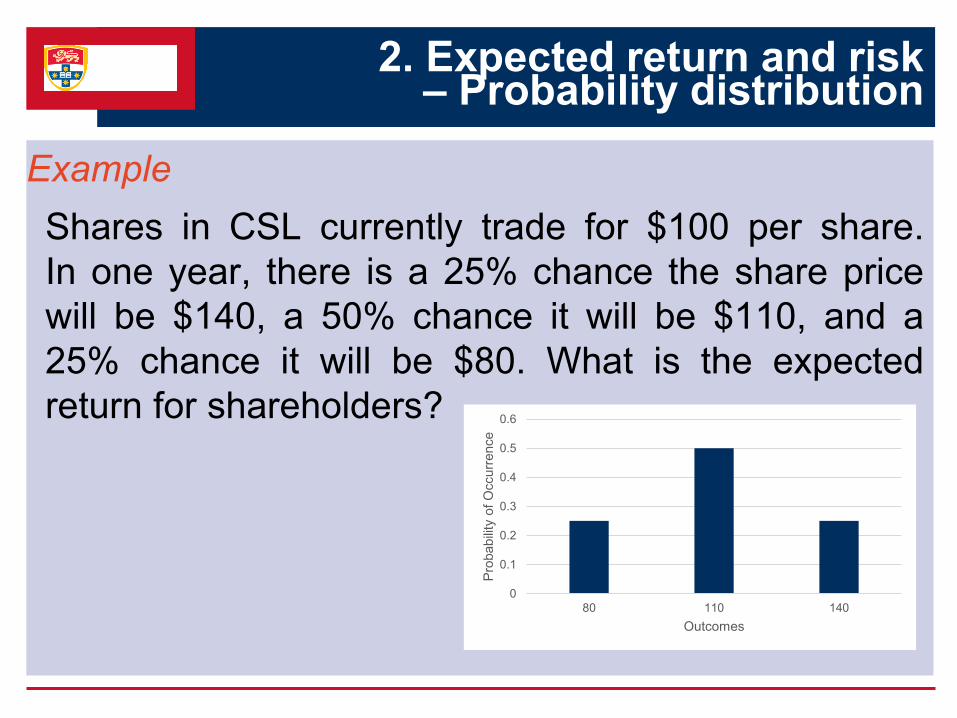

Example

Shares in CSL currently trade for $100 per share.

In one year, there is a 25% chance the share price

will be $140, a 50% chance it will be $110, and a

25% chance it will be $80. What is the expected

return for shareholders?

0

0.1

0.2

0.3

0.4

0.5

0.6

80 110 140

Pro

babili

ty o

f O

ccurr

ence

Outcomes

2. Expected return and risk – Probability distribution

2. Expected return and risk – Probability distribution

› When an investment is risky, there are different returns it may

earn. Each possible return has some likelihood of occurring.

This information is summarised with a probability distribution,

which assigns a probability that each possible return will

occur.

› The total risk is the weighted average of the possible returns,

where the weights are determined by the probability that it

occurs.

Pi

n

i

i rr 1

22

2. Expected return and risk – Probability distribution

› In finance, the standard deviation of a return is also referred

to as volatility. The standard deviation is easier to interpret

because it is in the same units as the returns themselves.

Pi

n

i

i rr 1

2

Example

Shares in CSL currently trade for $100 per share.

In one year, there is a 25% chance the share price

will be $140, a 50% chance it will be $110, and a

25% chance it will be $80. What is the variance of

returns?

0

0.1

0.2

0.3

0.4

0.5

0.6

80 110 140

Pro

babili

ty o

f O

ccurr

ence

Outcomes

2. Expected return and risk – Probability distribution

BUSINESS

SCHOOL

Risk and Return - Practical Application

A brief history of the financial markets

› Investors have historically earned higher rates of return on

riskier investments. However, having a higher expected rate of

return simply means that investors ‘expect’ to realise a higher

return. Higher return is not guaranteed.

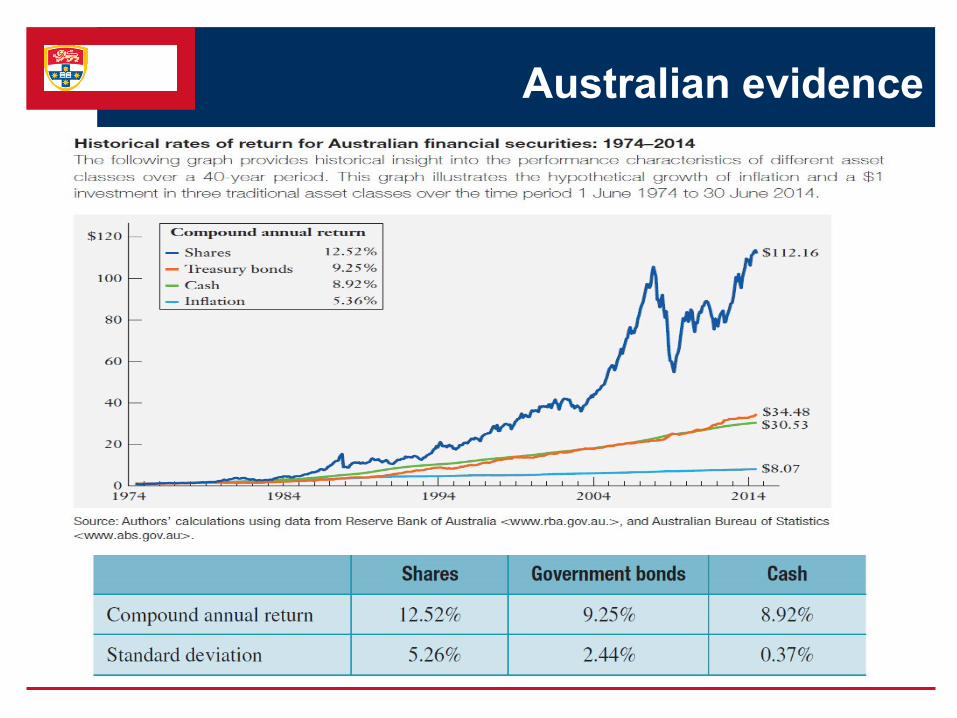

Australian evidence

US evidence

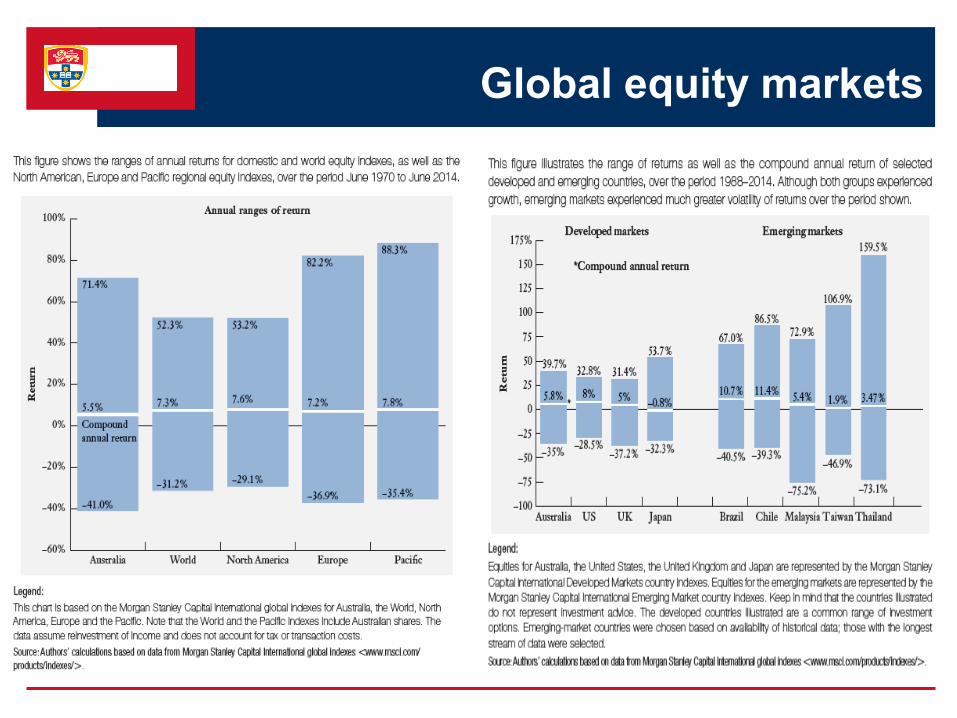

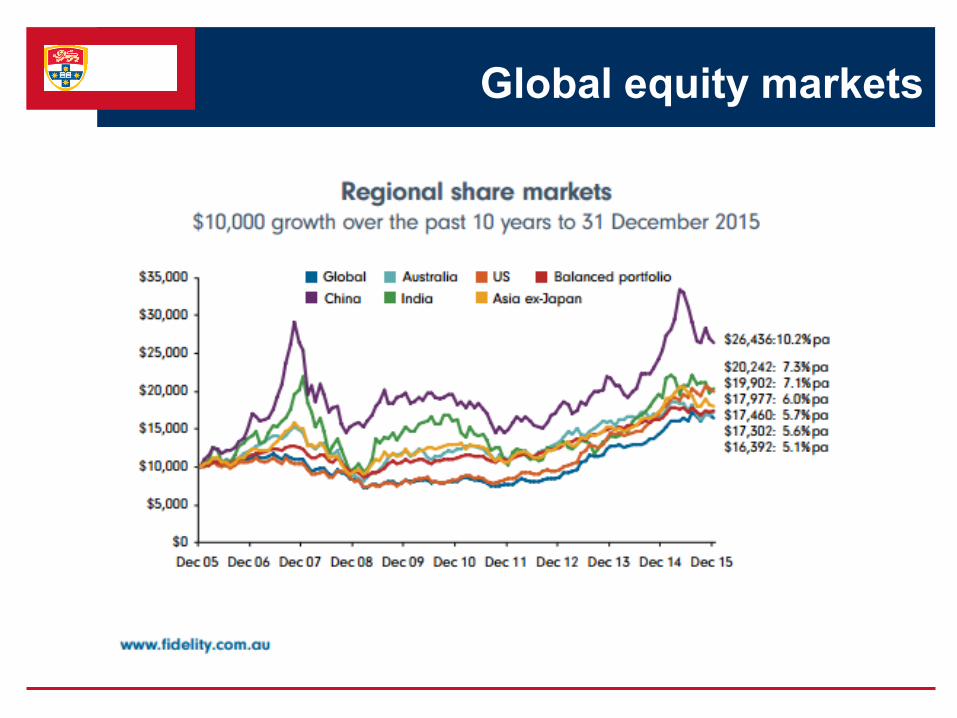

Global equity markets

Global equity markets

Global equity markets

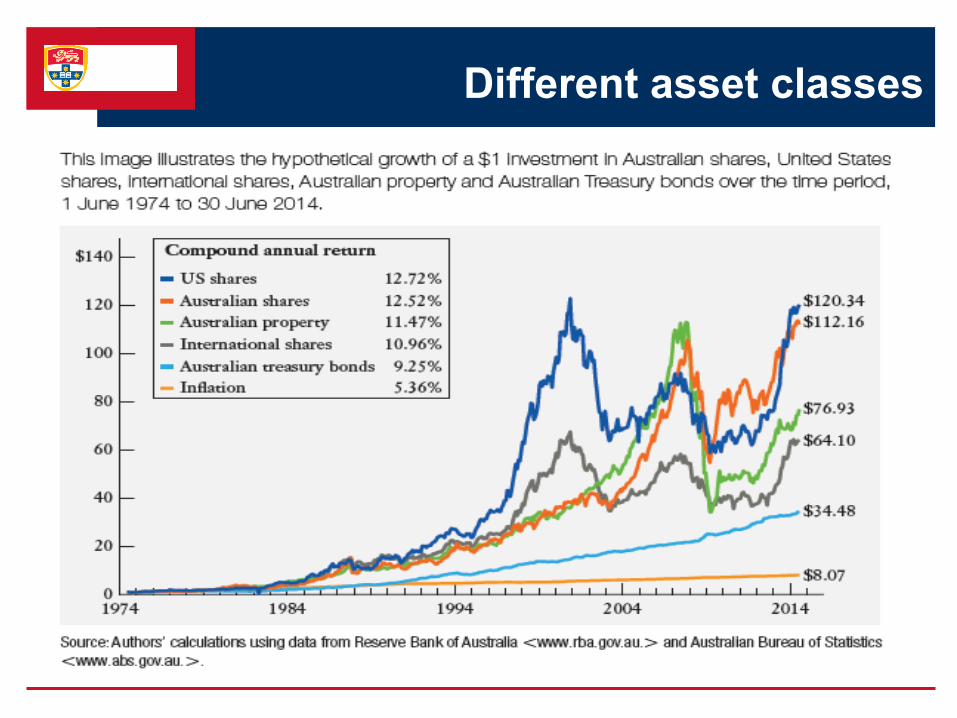

Different asset classes

BUSINESS

SCHOOL

Risk and Return of Portfolios

› A portfolio is a group of assets held by an investor.

› Holding a portfolio of assets reduces investment risk, but

often with no effect on overall returns, because:

- Within the portfolio, individual assets are more volatile than

the overall portfolio

- Poor returns on some assets could be offset by stronger

returns on others

- The overall portfolio return is “smoothed out”

Portfolios

› The portfolio expected return is a weighted average of the

expected returns on individual securities that make up the

portfolio, where weights correspond to the proportion of the

portfolio accounted by each of the respective component

assets.

𝐸 𝑟𝑝 = 𝑟𝑝 =

𝑖=1

𝑛

𝑤𝑖 𝐸(𝑟𝑖)

The return of portfolios

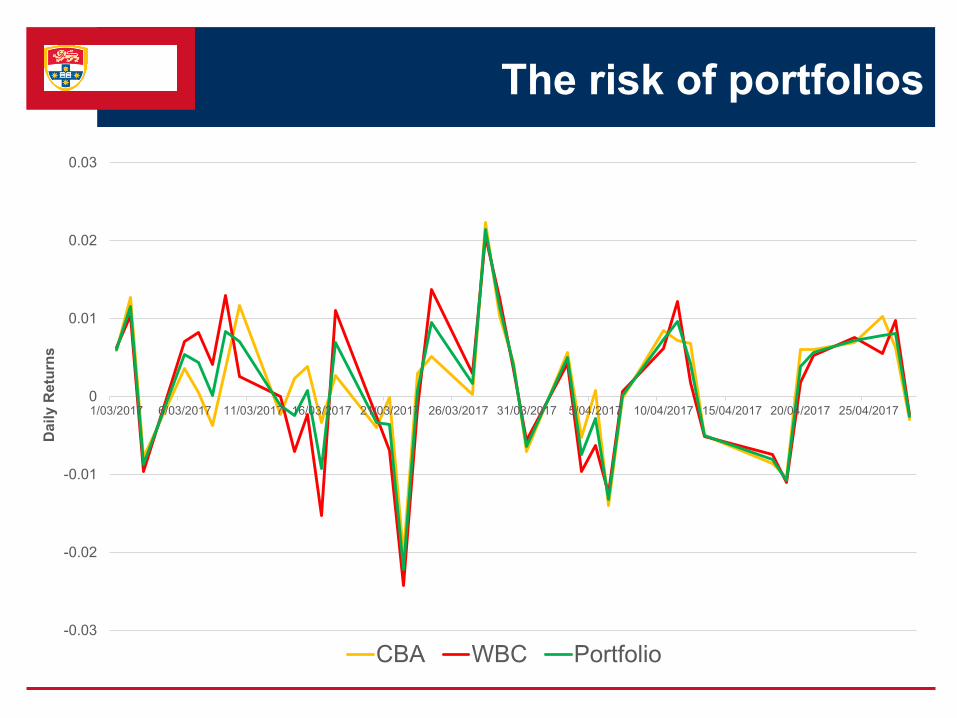

The risk of portfolios

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

1/03/2017 6/03/2017 11/03/2017 16/03/2017 21/03/2017 26/03/2017 31/03/2017 5/04/2017 10/04/2017 15/04/2017 20/04/2017 25/04/2017

Da

ily R

etu

rns

CBA WBC Portfolio

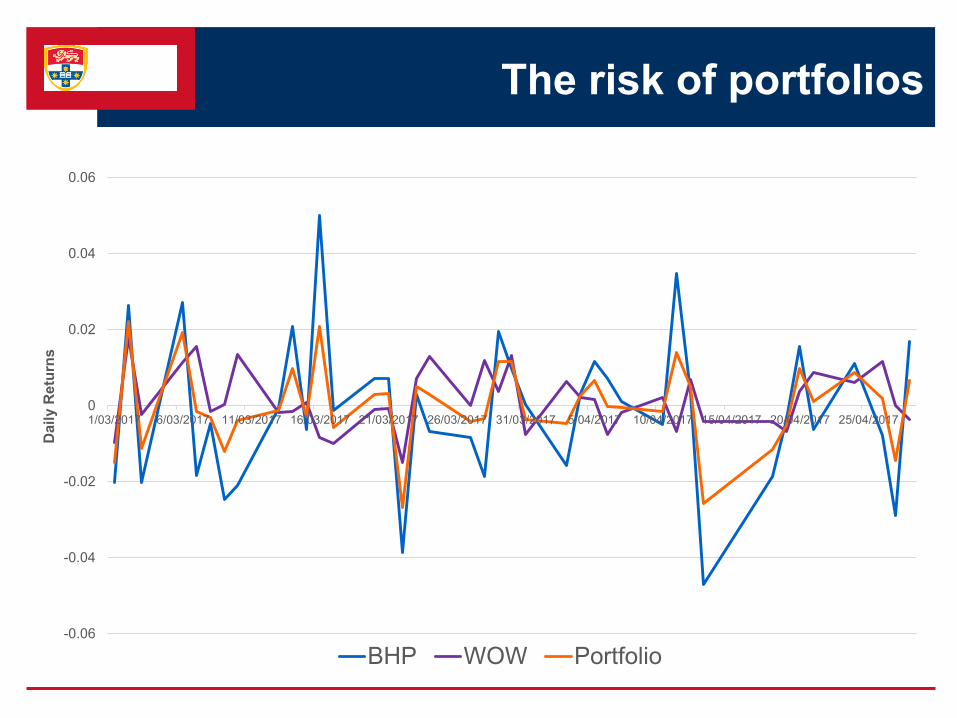

The risk of portfolios

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

1/03/2017 6/03/2017 11/03/2017 16/03/2017 21/03/2017 26/03/2017 31/03/2017 5/04/2017 10/04/2017 15/04/2017 20/04/2017 25/04/2017

Da

ily R

etu

rns

BHP WOW Portfolio

The risk of portfolios

› The risk of a portfolio is measured by the variability or

dispersion of the portfolio return around its mean or expected

value.

› Unlike the expected return of a portfolio, risk of a portfolio is

not a simple weighted average of the risk of individual

security returns.

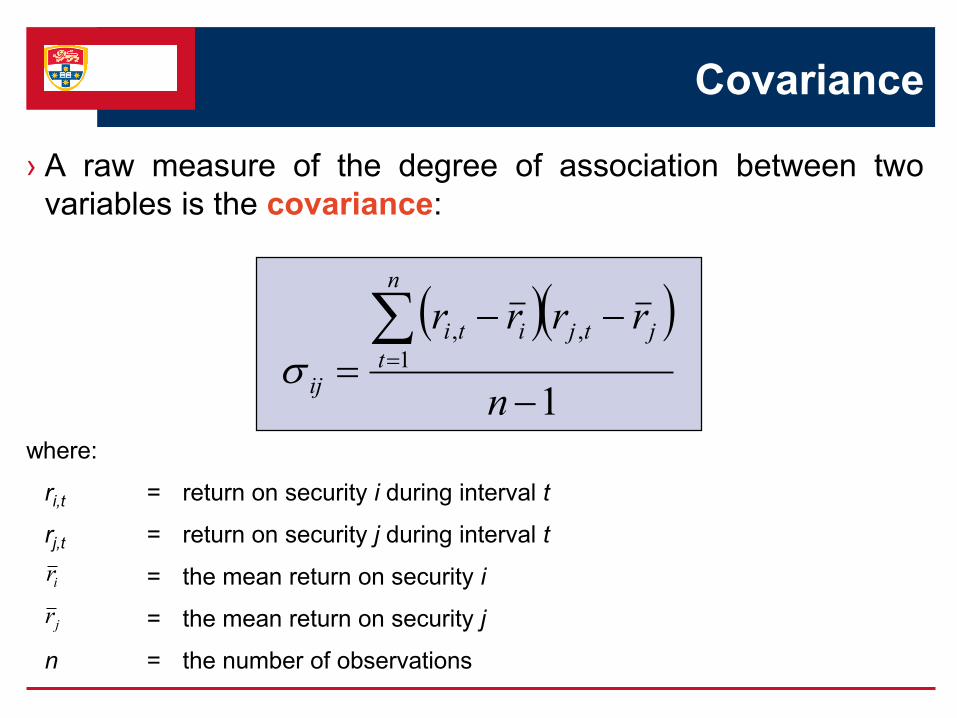

› A raw measure of the degree of association between two

variables is the covariance:

where:

ri,t = return on security i during interval t

rj,t = return on security j during interval t

= the mean return on security i

= the mean return on security j

n = the number of observations

1

1

,,

n

rrrrn

t

jtjiti

ij

jr

ir

Covariance

Covariance

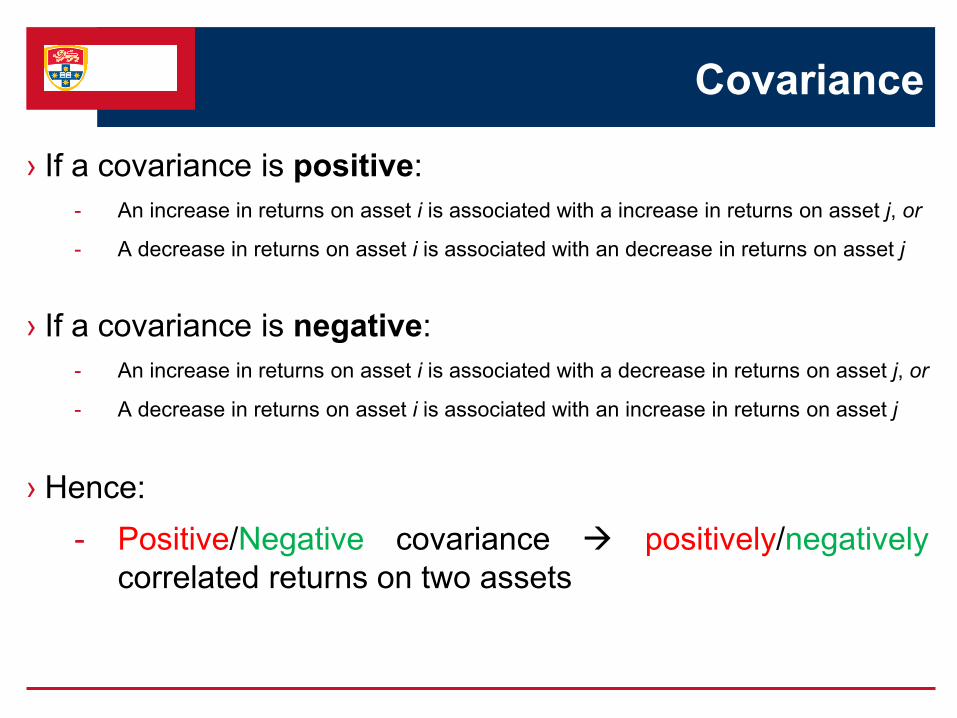

› If a covariance is positive:

- An increase in returns on asset i is associated with a increase in returns on asset j, or

- A decrease in returns on asset i is associated with an decrease in returns on asset j

› If a covariance is negative:

- An increase in returns on asset i is associated with a decrease in returns on asset j, or

- A decrease in returns on asset i is associated with an increase in returns on asset j

› Hence:

- Positive/Negative covariance positively/negatively

correlated returns on two assets

Covariance

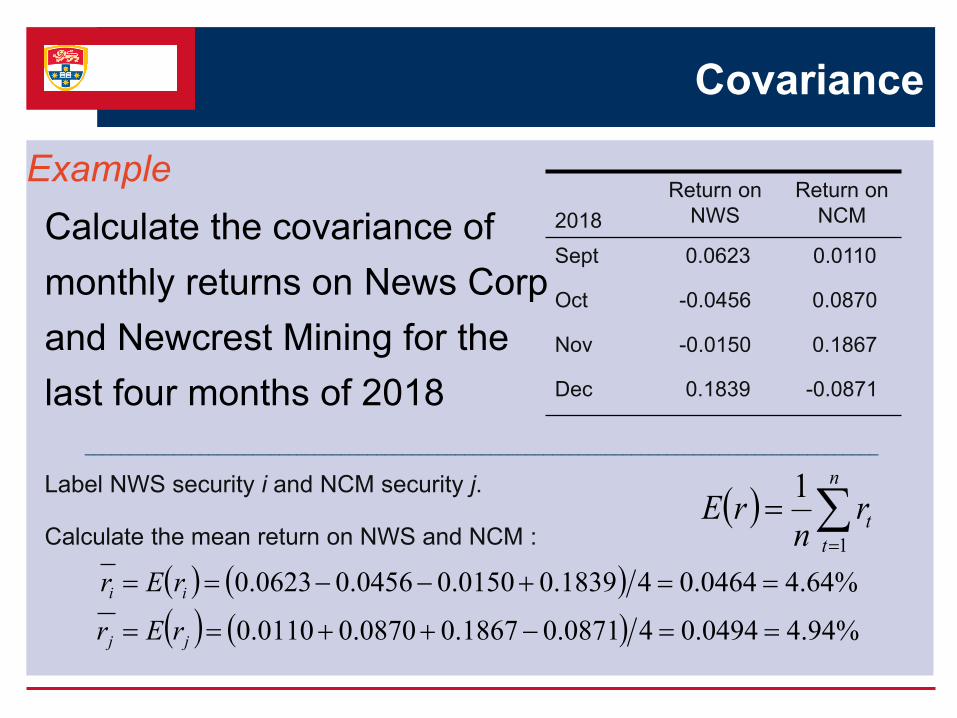

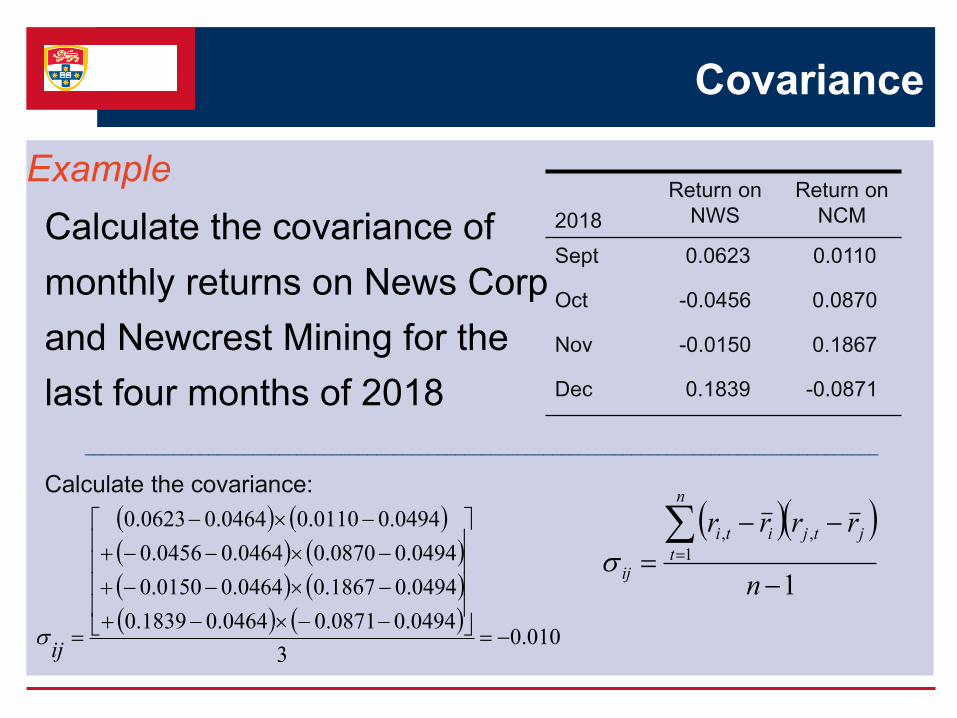

Example

Calculate the covariance of

monthly returns on News Corp

and Newcrest Mining for the

last four months of 2018

__________________________________________________________________________________________

Label NWS security i and NCM security j.

Calculate the mean return on NWS and NCM :

2018

Return on

NWS

Return on

NCM

Sept 0.0623 0.0110

Oct -0.0456 0.0870

Nov -0.0150 0.1867

Dec 0.1839 -0.0871

n

t

trn

rE1

1

%94.40494.040871.01867.00870.00110.0

%64.40464.041839.00150.00456.00623.0

jj

ii

rEr

rEr

Covariance

Example

Calculate the covariance of

monthly returns on News Corp

and Newcrest Mining for the

last four months of 2018

__________________________________________________________________________________________

Calculate the covariance:

2018

Return on

NWS

Return on

NCM

Sept 0.0623 0.0110

Oct -0.0456 0.0870

Nov -0.0150 0.1867

Dec 0.1839 -0.0871

010.0

3

0494.00871.00464.01839.0

0494.01867.00464.00150.0

0494.00870.00464.00456.0

0494.00110.00464.00623.0

ij

1

1

,,

n

rrrrn

t

jtjiti

ij

Correlation coefficient

› An alternative, and closely related, measure of the degree of

association between two securities is the correlation

coefficient:

where:

σij = covariance between returns on securities i and j

σi = standard deviation of security i

σj = standard deviation of security j

ij ij

i j

Correlation coefficient

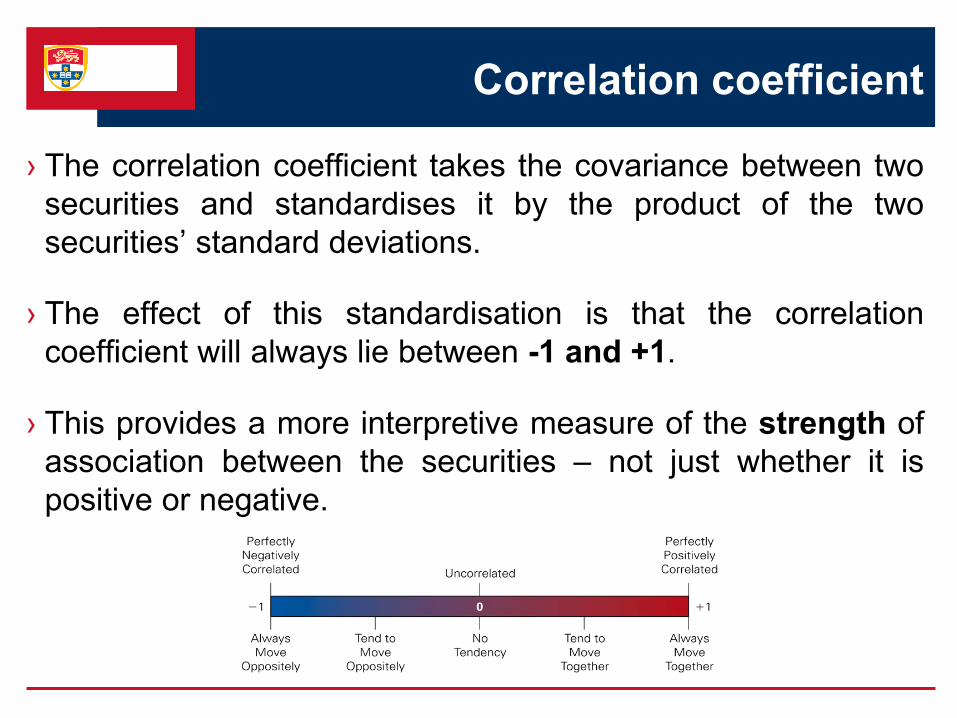

› The correlation coefficient takes the covariance between two

securities and standardises it by the product of the two

securities’ standard deviations.

› The effect of this standardisation is that the correlation

coefficient will always lie between -1 and +1.

› This provides a more interpretive measure of the strength of

association between the securities – not just whether it is

positive or negative.

Correlation coefficient

Example

Calculate the correlation coefficient for News Corp

and Newcrest Mining, given that the standard

deviation of returns on the two stocks were 7.73%

and 11.59% and the covariance is –0.000656.

__________________________________________________

› 073.01159.00773.0

000656.0

ji

ij

ij

The risk of portfolios

› The risk of a portfolio is related to the riskiness of the

stocks and the degree of covariance or correlation.

› The variance of returns on a portfolio is calculated as follows:

where:

σi, σj = the standard deviation of returns on asset i or j

wi, wj = proportion of the portfolio invested in asset i or j

σij = the covariance between assets i and j

ρij = the correlation coefficient between assets i and j

jiijjijjiip

ijjijjiip

wwww

wwww

2

2

22222

22222

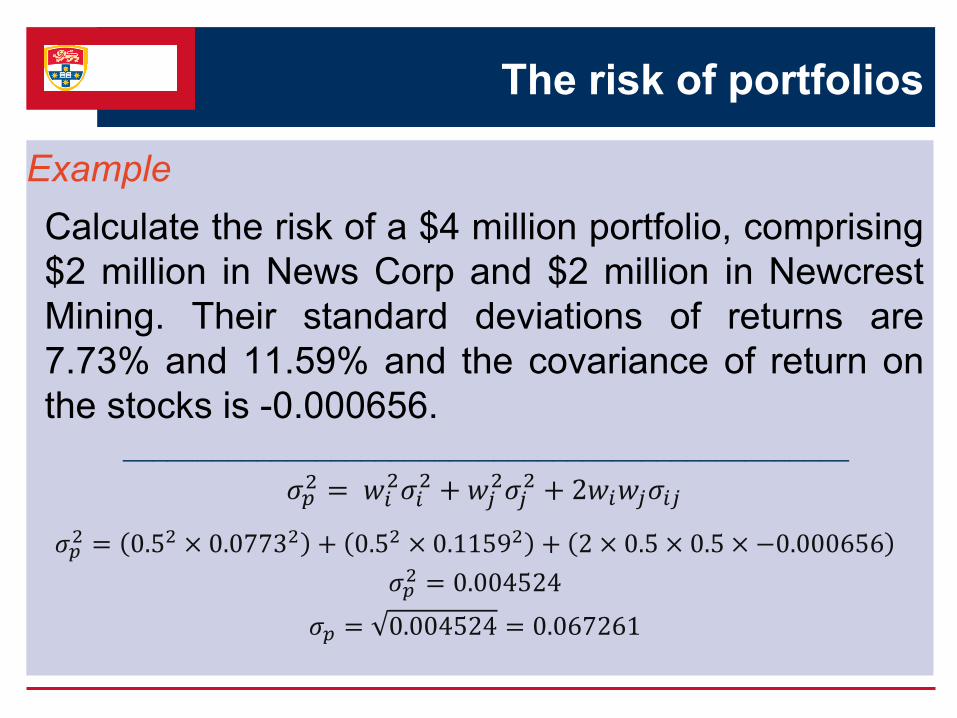

The risk of portfolios

Example

Calculate the risk of a $4 million portfolio, comprising

$2 million in News Corp and $2 million in Newcrest

Mining. Their standard deviations of returns are

7.73% and 11.59% and the covariance of return on

the stocks is -0.000656._________________________________________________

𝜎𝑝2 = 𝑤𝑖

2𝜎𝑖2 +𝑤𝑗

2𝜎𝑗2 + 2𝑤𝑖𝑤𝑗𝜎𝑖𝑗

𝜎𝑝2 = 0.52 × 0.07732 + 0.52 × 0.11592 + 2 × 0.5 × 0.5 × −0.000656

𝜎𝑝2 = 0.004524

𝜎𝑝 = 0.004524 = 0.067261

The risk of portfolios

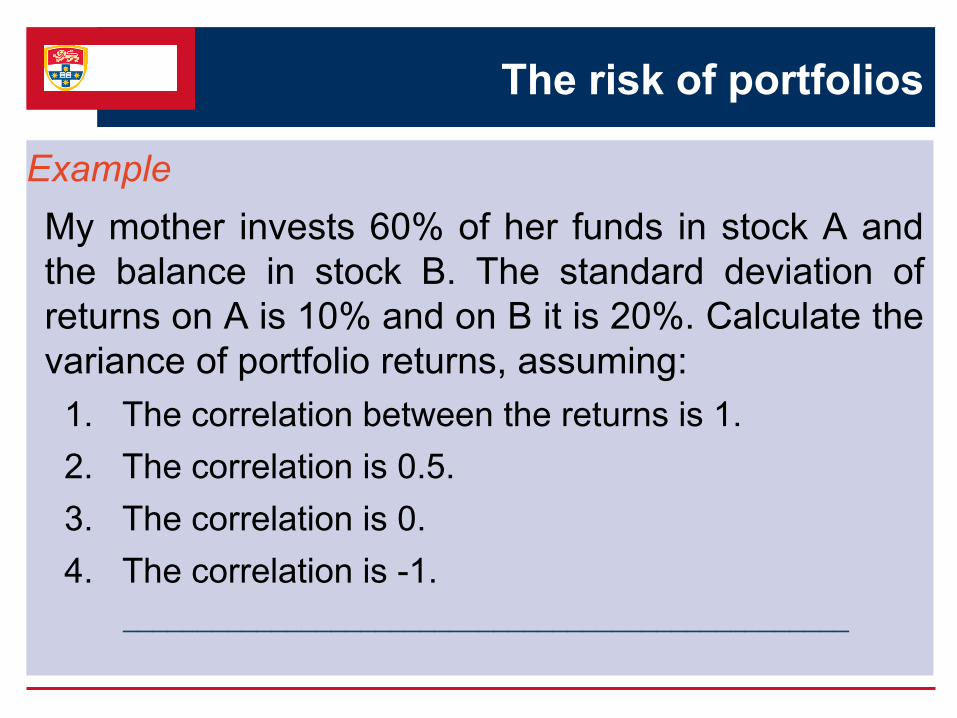

Example

My mother invests 60% of her funds in stock A and

the balance in stock B. The standard deviation of

returns on A is 10% and on B it is 20%. Calculate the

variance of portfolio returns, assuming:

1. The correlation between the returns is 1.

2. The correlation is 0.5.

3. The correlation is 0.

4. The correlation is -1.

_________________________________________________

The risk of portfolios

The risk of portfolios

› The variance of returns on a three-asset portfolio is calculated

as follows:

› This can be extended to an n-asset case:

jkkjikkiijjikkjjiip wwwwwwwww 2222222222

ij

n

i

n

j

jip ww

1 1

2

Components of risk

› The risk of investing in a single security can be reduced by

combining the security with others in a portfolio due to

diversification.

› However, this does not mean that all risk can be eliminated.

› This is because there are two components of total risk:

1. Non-systematic (or diversifiable) risk

2. Systematic (or non-diversifiable) risk

› Non-systematic risk relates to price movements that are

caused by an event that influences a single company alone.

› It is also known as diversifiable risk because it can be

diversified away.

› Systematic risk relates to macroeconomic events that affect

the prices of all securities and are reflected in broad market

movements.

› It is referred to as ‘non-diversifiable’ as it is common to all

securities and cannot be diversified away.

Components of risk

Components of risk

0

5 10 15

Po

rtfo

lio

ris

k

Number of Securities

Market risk

Unique

risk

› Diversification eliminates the non-systematic risk of a

portfolio.

› A well-diversified portfolio faces market risk alone and the

level of market risk will depend on the market risk of individual

assets included in the portfolio.

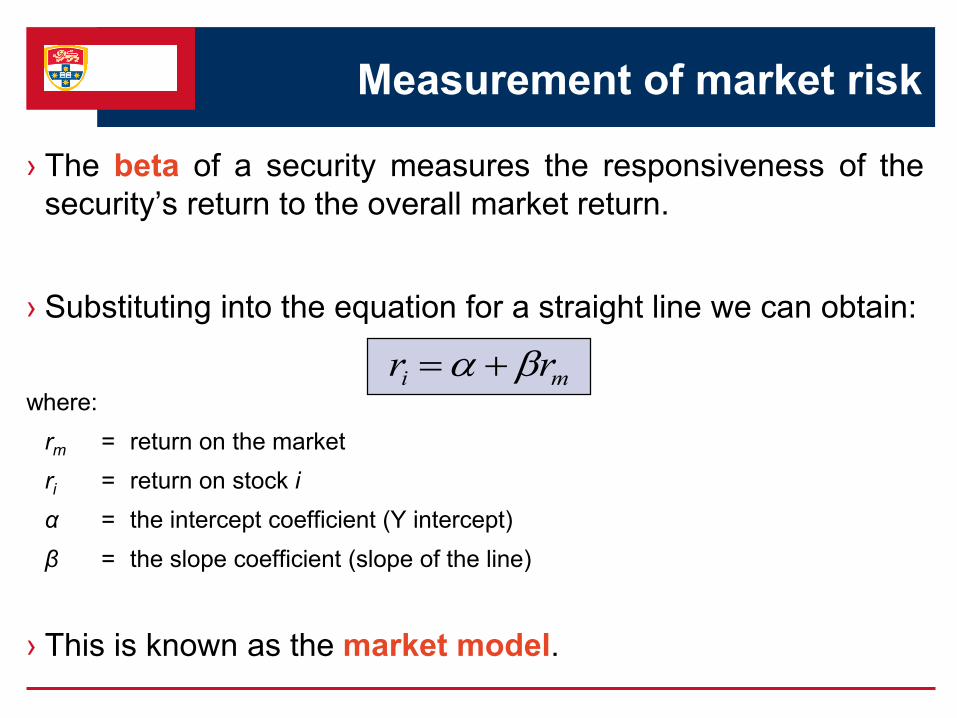

Measurement of market risk

› The beta of a security measures the responsiveness of the

security’s return to the overall market return.

› Substituting into the equation for a straight line we can obtain:

where:

rm = return on the market

ri = return on stock i

α = the intercept coefficient (Y intercept)

β = the slope coefficient (slope of the line)

› This is known as the market model.

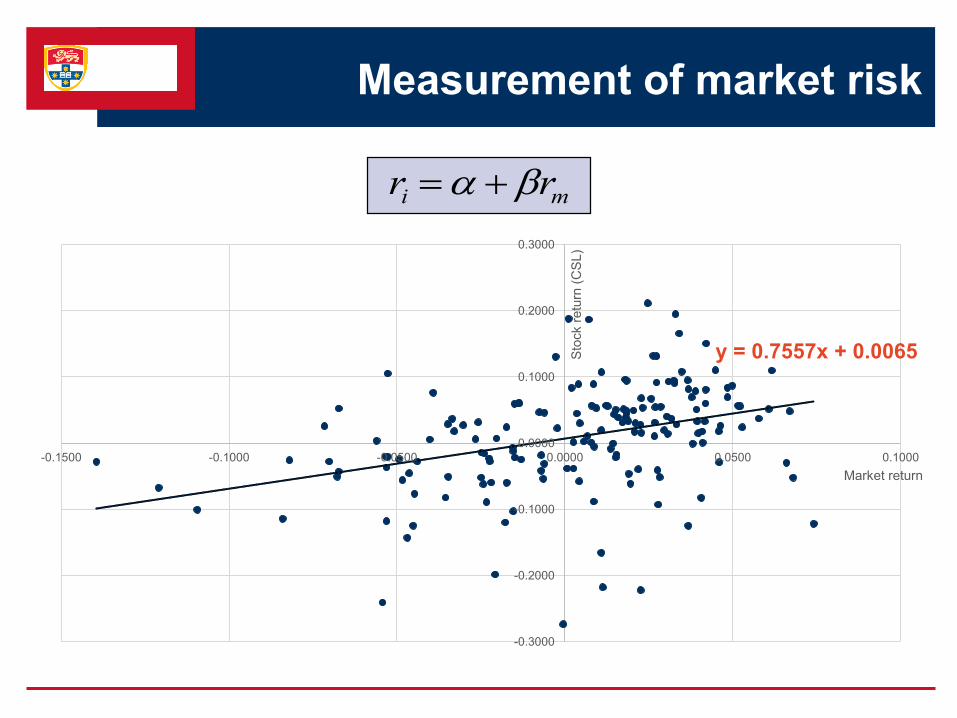

ri rm

Measurement of market risk

ri rm

y = 0.7557x + 0.0065

-0.3000

-0.2000

-0.1000

0.0000

0.1000

0.2000

0.3000

-0.1500 -0.1000 -0.0500 0.0000 0.0500 0.1000

Sto

ck r

etu

rn (

CS

L)

Market return

Measurement of market risk

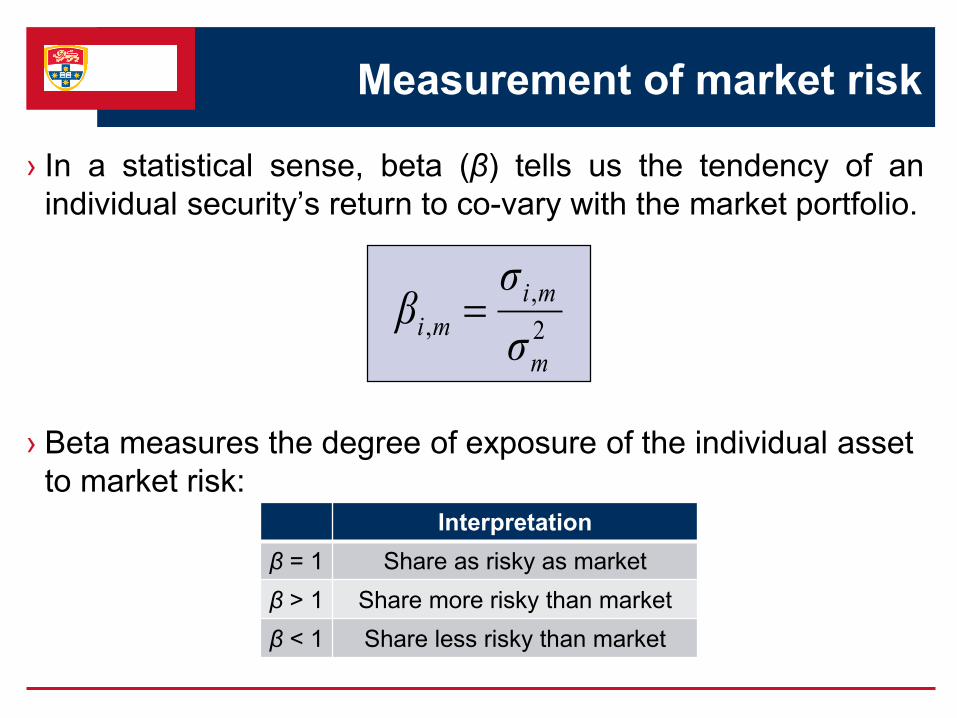

› In a statistical sense, beta (β) tells us the tendency of an

individual security’s return to co-vary with the market portfolio.

› Beta measures the degree of exposure of the individual asset

to market risk:

Interpretation

β = 1 Share as risky as market

β > 1 Share more risky than market

β < 1 Share less risky than market

2

,

,

m

mi

miσ

σβ

Conclusion

› Calculation of realised returns.

› Calculation of expected returns.

1. Returns from a time series

2. Returns from a probability distribution

› Calculation of risk.

1. Returns from a time series

2. Returns from a probability distribution

› The risk and return of portfolios.

› The components of total risk (non-systematic and systematic).

›Next lecture: CAPM

BUSINESS

SCHOOL

The End