Embed Size (px)

Citation preview

Rossdale Group

August 3, 2016

12:00 pm to 1:30 pm EDT

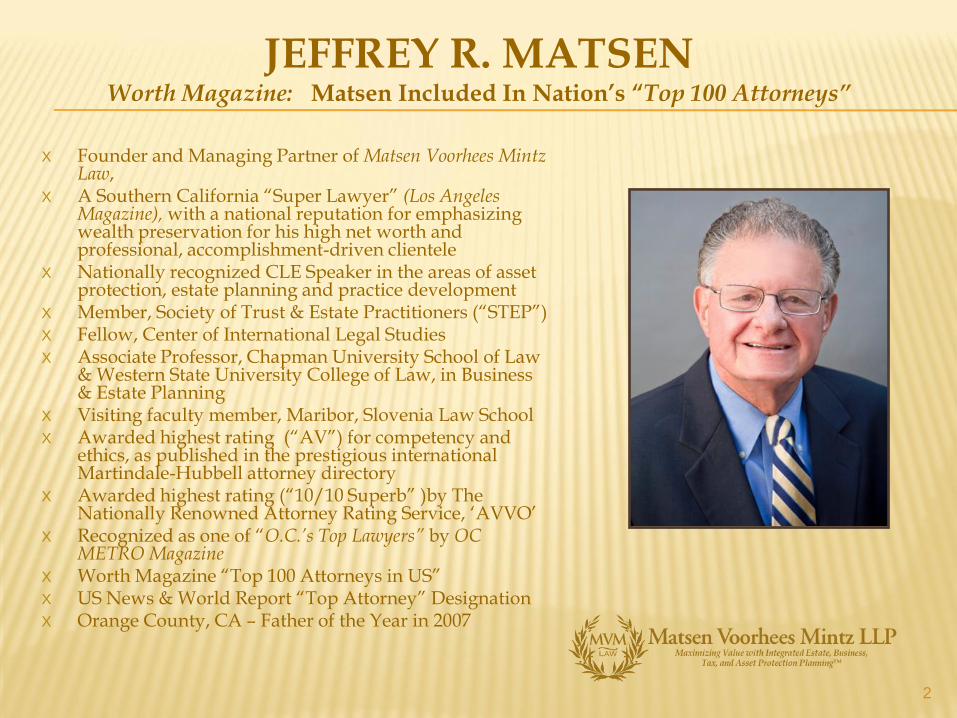

Jeffrey R. Matsen

1 ©August 2016Jeffrey R. Matsen

LLC FORMATION

695 Town Center Drive | 7th Floor | Costa Mesa, CA 92626

Phone: 714.384.6580 | Fax: 714.384.6551

www.JRMatsen.com | www.MVMLawyers.com

JEFFREY R. MATSEN Worth Magazine: Matsen Included In Nation’s “Top 100 Attorneys”

X Founder and Managing Partner of Matsen Voorhees Mintz Law,

X A Southern California “Super Lawyer” (Los Angeles Magazine), with a national reputation for emphasizing wealth preservation for his high net worth and professional, accomplishment-driven clientele

X Nationally recognized CLE Speaker in the areas of asset protection, estate planning and practice development

X Member, Society of Trust & Estate Practitioners (“STEP”) X Fellow, Center of International Legal Studies X Associate Professor, Chapman University School of Law

& Western State University College of Law, in Business & Estate Planning

X Visiting faculty member, Maribor, Slovenia Law School X Awarded highest rating (“AV”) for competency and

ethics, as published in the prestigious international Martindale-Hubbell attorney directory

X Awarded highest rating (“10/10 Superb” )by The Nationally Renowned Attorney Rating Service, ‘AVVO’

X Recognized as one of “O.C.’s Top Lawyers” by OC METRO Magazine

X Worth Magazine “Top 100 Attorneys in US” X US News & World Report “Top Attorney” Designation X Orange County, CA – Father of the Year in 2007

2

PRESENTER

Jeffrey R. Matsen is the founder and managing partner of Matsen Voorhees Mintz LLP (MVM Law). His practice encompasses business formation and transactional matters, estate planning, asset protection, probate, tax and real estate. Mr. Matsen has been an adjunct professor at Western State University College of Law, Golden Gate University and Chapman University School of Law. He has also lectured to various professional groups on areas related to his practice, including limited liability companies, business entity formation and selection, asset protection techniques, and other relevant topics. He wrote the award winning book, The Ladder of Success: An Asset Protection Planning Primer. Mr. Matsen is a member of the American Bar Association (Real Property and Trust Section), WealthCounsel and the Society of Trust and Estate Practitioners (STEP). He is a faculty member and fellow of the Center for International Legal Studies in Salzburg, Austria. Mr. Matsen earned his B.A. degree, cum laude, from Brigham Young University; and his J.D. degree, with honors, from the University of California at Los Angeles.

3

THE BASICS AND THE ORGANIZATION OF THE SINGLE MEMBER LLC

A History of the LLC:

x 1892: GmbH in Germany – limited liability but more restrictive than U.S. LLC laws

x Other Europeans and South Americans adopted GmbH model

x 1977: Wyoming LLC is First in U.S.

x 1982: Florida LLC

x 1988: IRS Rev Ruling that Wyoming style LLC would be taxed as a Partnership

x Remaining States jumped on the LLC bandwagon

x 1997: Hawaii is the last State to adopt the LLC

4

THE BASICS AND THE ORGANIZATION OF THE LLC

What is a LLC?:

x Separate Legal Entity

x Articles of Organization: State Charter

x Shield of Liability Protection

x Disregarded Entity For Tax Purposes

x Partnership if multi member

x Can Elect to be taxed as S Corp. or C Corp if circumstances warrant it

5

THE BASICS AND THE ORGANIZATION OF THE LLC

Organization:

x Filing of Articles of Organization

x Operating Agreement

x Federal Employer Identification Number (FEIN)

x Secretary of State Initial List

x LLC Post Organizational Memorandum

x LLC Bank Account

x Member Certificates

6

Management Structure

X Representative Management x (Corporate structure)

x (LLC with member election of manager/offices)

X Vested Management x (Limited partnership structure)

x (Manager managed LLC)

X Direct Management x (General partnership structure)

x (Member managed LLC)

7

x More like a Limited Partnership with General Partner and more passive limited partners.

Caveat: General Partner of a Limited Partnership is personally liable - Manager of LLC is not

x Manager Managed LLC may be better for Asset

Protection Planning-Manager can resign and appoint successor if Manager is personally sued.

8

MANAGER MANAGED LLC

Tax Issues

x Check-the-Box regulations allow unincorporated entities to be taxed as corporation, S corporation, partnership or as a disregarded entity (sole proprietor) x Flexibility

x Entity must otherwise qualify

x Unlikely for LLC to lose a partnership tax status while status is more problematic for S corporation (inadvertent S corp. termination under many circumstances)

9

x Flexibility in allocating income and/or distributions between the members.

x Availability of basis adjustments (IRC §754 election) upon sale or exchange of membership interests

x Ability to distribute property with no significant tax effects.

x Ability to liquidate with no significant tax effects.

x Ability to generate and distribute income not subject to self-employment tax

x Adjusted basis in the LLC for purposes of deducting losses includes all debt

x Allocated to the members under IRC §752.

10

PRINCIPAL TAX ADVANTAGES OF AN LLC TAXED AS A DISREGARDED ENTITY OR A PARTNERSHIP OVER AN S CORP.

x All “business” income is subject to self-employment tax.

x Sale of a membership interest may generate ordinary income or loss, depending on the assets of the LLC, under IRC §751. The balance is capital gains, although some may be at 25% or 28% federal rates.

x A pre-existing election under IRC §754 may cause a reduction in the basis of partnership assets.

11

PRINCIPAL DISADVANTAGES OF AN LLC TAXED AS A DISREGARDED ENTITY OR A PARTNERSHIP COMPARED TO AN S CORP.

x Sale of S Corp. stock is usually all capital gains.

x Provided “reasonable” salaries are paid, distributions of business profits are not subject to payroll taxes.

12

PRINCIPAL TAX ADVANTAGES OF AN S CORP. OVER AN LLC TAXED AS A DISREGARDED ENTITY

OR A PARTNERSHIP

x Lack of flexibility in allocating income and/or distributions

x Basis in S Corp. stock, for purposes of deducting losses, is increased only by direct loans from the shareholder to the S Corp.

x “Reasonable” compensation for services, subject to payroll taxes, must be paid regardless of the source or character of the income.

x Distributions of property to shareholders normally generate gain to the S Corp., either under IRC §311(b) or, in liquidation, IRC §336(a).

13

PRINCIPAL TAX DISADVANTAGES OF AN S CORP. COMPARED WITH AN LLC TAXED AS A DISREGARDED ENTITY OR A PARTNERSHIP

Which entity is the best for a taxpayer depends on the specific taxpayer. Because this determination is initially made before the taxpayer has begun the business, it is important to review not only the business plan but also the reasonableness of the assumptions on which the business plan is based.

14

ANSWER TO QUESTION: WHO WINS?

Type of Assets Owned

x Investment Assets better in a LLC or partnership because of step-up basis

x Operating Assets may be held by any, but consider owning in separate entity and leasing back to operating entity for asset protection

15

Funding The LLC

x Deeds for real property

x Assignments

x Changing title on bank and securities accounts

16

Investment Assets in LLC

x Client can transfer security accounts and other investments to LLC

x Affords more asset protection and also fits in to estate tax

planning structure

x High net worth clients like the protection and ease of

operation of LLCs for their investments

x Also, allows for both income and estate tax planning

17